Embed Size (px)

Citation preview

The Rise of SASAC: Asset Management,Ownership Concentration, and Firm Performancein China’s Capital Markets

Junmin Wang,1 Doug Guthrie,2 and Zhixing Xiao3

1University of Memphis, USA, 2George Washington University, USA, and 3China European

International Business School, China

ABSTRACT Since the mid 1990s the State-Owned Assets Supervision andAdministration Commission (SASAC) has emerged as a key institution governing firmownership in China, but its impact on firm performance is understudied. Through ananalysis of Chinese firms listed on the Shanghai and Shenzhen stock exchanges from1994–2003, we examine how the changing ownership patterns following the rise ofSASAC influenced firm performance. We have three findings. First, contrary to thepopular view that state ownership in China’s listed firms has declined, we find thatthe state shares have been moved from the original state offices to the SASAC in theformat of ‘state institutional shares’. Second, compared with the old state shares, theSASAC institutions affect firm performance more positively. Third, after controllingfor state and SASAC ownership, ownership concentration is a strong positive factor infirm performance. Our findings fit squarely within a long tradition of agency theoristswho argue that ownership concentration helps solve the free-rider problem and thushas positive effects on firm performance. However, we focus on the ways in whichownership concentration allows firm owners to monitor and stabilize firm behaviour,which has more important implications for emerging economies such as China’sdomestic capital markets.

KEYWORDS China’s capital markets, Chinese SOEs, firm performance, gradualism,ownership concentration

INTRODUCTION

The second half of the 1990s saw the proliferation of a new type of institutiongoverning firm ownership in China’s transition economy – Asset ManagementCompanies (AMCs). These companies were initially set in place by the fourstate-owned banks as a way to move bad loans off the books. However, they quicklybecame institutions that spread throughout the economy as a way for state offices

Management and Organization Reviewdoi: 10.1111/j.1740-8784.2011.00236.x

© 2011 The International Association for Chinese Management Research

to appear to be divesting their ownership stakes in publicly-traded firms. TheAMCs were pushed to act like institutional investors – managing the companies intheir portfolios and thinking about issues like operational efficiency, return oninvestment, etc. This new institutional form eventually reached the highest levels ofgovernment with the founding of the State-Owned Assets Supervision and Admin-istration Commission (SASAC), a central government agency that directly super-vises 121 of the largest centrally-owned companies (zhongyang qiye ) as ofMay, 2011 (SASAC, 2011). When SASAC was founded in 1999, it was initiallyestablished to manage about 6.9 trillion yuan in assets (about US$866 billion), withseveral high-profile initial public offerings (IPOs) on the books – including Petro-China’s recent IPO, which (briefly) gave it a market capitalization of over US$1trillion; the value of SASAC’s assets is likely over several trillion dollars. Theemergence of the AMCs and SASAC is a crucial step in China’s gradualist modelof economic reform process, yet surprisingly little has been written about this keyinstitution.

To examine this issue in greater depth, we begin with two related questions:How have ownership patterns of China’s large state-owned firms changed in thelast decade of the reforms? And how have these changing ownership patternsinfluenced firm performance? Through an analysis of ownership data of the firmslisted from 1994–2003, we show three specific findings: first, contrary to thepopular view that the Chinese state has steadily divested its interest in thesefirms, we show this not to be the case. While it is true that state ownership hasofficially declined over this period, there is a hidden reality behind this decline:local state owners have moved their shares from the ‘state shares’ to the ‘stateinstitutional shares’ category, placing those shares in the State-Owned AssetManagement Companies (SOAMCs); and under the control of SASAC, organi-zations that are usually owned by the same state office that originally held theshares. Second, there is some evidence that these institutions have a more posi-tive impact on firm performance than the state offices that originally held them.Third, the most consistent significant impact on firm performance has to do withownership concentration: controlling state and state institutional ownership,ownership concentration is also a strong positive factor in firm performanceacross these categories. Following a long tradition of agency theorists who haveexamined the positive relationship between ownership concentration and firmperformance in a variety of contexts, we argue that ownership concentration inChina is a governance issue, whereby concentrated owners are better able toguide their firms through economic reforms. Where most agency theorists havefocused on the free-rider problems that accompany dispersed ownership – andthus the ways in which ownership concentration helps solve the free-riderproblem – we focus on the ways in which ownership concentration allows firmowners to monitor and stabilize firm behaviour in the emerging markets of thetransition economy.

2 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

THEORETICAL BACKGROUND AND HYPOTHESES

China’s Gradualist Reform

During the 1980s and 1990s, economists and institutional advisors from the Westadvocated that the ‘big bang’ or ‘shock therapy’ approach – rapid privatization –was the only sure path for the transition from communist economies to marketeconomies (Barro & Sala-i-Martin, 1995; Blanchard, Boycko, Dabrowski, Dorn-busch, Layard, & Shleifer, 1993; Cao, Fan, & Woo, 1997; Fischer, 1992; Fischer &Gelb, 1991; Kornai, 1980, 1990; Sachs, 1992, 1993, 1995a,b; Sachs & Woo,1994a,b, 1997; Woo, 1997, 1999; Woo, Parker, & Sachs, 1997). The argumenthere was that private property is the cornerstone of economic efficiency and, byextension, profitability. Thus, only through privatization could communist societ-ies successfully make the transition to a healthy, functioning market economy(Kornai, 1990; Sachs, 1992, 1993). However, in opposition to this Western advice,China took a reform approach of ‘gradualism’ during its market-oriented transi-tion, putting the state at center stage in the process of long-term institutionalchange while at the same time taking the time to experiment with new institutionsand to implement them incrementally within the context of existing institutionalarrangements (Chen, Wang, Zheng, Jefferson, & Rawski, 1988; Naughton, 1995;Nee, 1992; Rawski, 1994, 1995, 1999).

In the 1980s, instead of rapidly removing the state from control over the economy,China decentralized and localized the managerial control over enterprises toprovincial-, municipal-, township-, and village-level governments while at the sametime allowing for the emergence of a private economy that would compete with thestate-owned economy. In his study of township and village enterprises (TVEs),Walder (1995) found that lower-level governments were able to run efficient andproductive public firms due to the institutional conditions that increased economicautonomy in localities and the ‘hardening’ of fiscal constraints on the enterprisesowned by lower-level local governments. Oi (1989, 1992, 1995) made a similarargument based upon the parts of the rural economy she examined, calling thephenomenon ‘local state corporatism’. Thus, the localization of state control overthe economy contributed to a dynamic rural industrial economy in the first decadeof economic reform. China’s decentralization reform measures also resulted incompetition among local areas over a variety of scarce resources, from attractingforeign direct investment (FDI) to attracting the central government’s investments(Che & Qian, 1998; Qian & Roland, 1998). In the 1990s, China embarked on a newset of projects tied to the gradual reform. Among these were the aggressive creationof a rule-of-law infrastructure and the creation of the Shanghai and Shenzhen stockexchanges. It appears that the stock exchanges became the primary vehicle forprivatizing the large state-owned enterprises (SOEs), but as we show below, evenamong Chinese publicly-traded companies, the privatization process has been muchmore complex and gradual than previous studies have shown.

Ownership Concentration in Chinese SOEs 3

© 2011 The International Association for Chinese Management Research

In light of the distinct reform practices of post-communist countries since the late1980s, and especially China’s remarkable economic success, the scholarship oftransitional economy has reached a conclusion that gradualism is a workablemodel of economic reform (Guthrie, 2006; Naughton, 1995). The success ofgradualism can be attributed to two main factors. First, in the midst of theturbulence that inevitably accompanies the transition from plan to market, thegradualist reform approach allows the state to retain its role as a stabilizing force(Naughton, 1995). Gradual control allowed the Chinese central government tomaintain synchronization between the political and economic arenas during thecountry’s economic transition, a regime Lin (2011) names a ‘centrally managedcapitalism’. Moreover, the Chinese government was given time to strategicallyadjust the firms’ ownership structure and restructure its industries in order tocultivate national champions that were expected to better cope with global com-petition (Wang, 2009). Second, through decentralization instead of privatization,the central government has gradually pushed ownership-like control down thegovernment administrative hierarchy to the localities. Local officials were givenfree rein to generate income. The intertwining between the bureaucratic systemand the transformed economic organizations also motivated governmental juris-dictions to ‘teach’ successful market behaviour to the firms under their control(Guthrie, 2005). In a sense, pushing economic responsibilities onto local adminis-trators created an incentive structure much like those experienced by managers oflarge industrial firms (Walder, 1995). SOEs were slower to see true reform thantheir counterparts in the TVE sector, but the push for these changes would comein the 1990s. Since then, substantial restructuring of the state-owned industry hasbeen central to the reform agenda. Although the transition away from the plannedeconomy was a gradual process, managers in many Chinese SOEs were increas-ingly handed the main responsibilities associated with the management of a busi-ness organization: although they did not possess the right to transfer assets, theyincreasingly had the rights to residual income flows, and the power and responsi-bility of managerial control (Guthrie & Wang, 2007).[1]

Layers of State Ownership in China’s Nascent Stock Market

In 1990 and 1991 respectively, the Shanghai and Shenzhen Stock Exchanges werefounded. China’s nascent stock market has since grown tremendously, and by theend of 2008 the number of domestically listed companies in China had risen to1,625 with a total market capitalization of US$1,733.8 billion (China SecuritiesRegulatory Commission, 2009). As one of the key market mechanisms, China’sstock market was introduced in order to restructure SOEs through corporatizationand simultaneously to attract private and foreign capitals to finance the SOEsin transition. Thus, building a stock market was not out of step with the broaderlogic of China’s gradual reform. Following the gradualist model, the Chinese

4 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

government’s construction of the institutions that govern public ownership hasbeen spread across the period. The 1994 Company Law pushed enterprises tostandardize governance structures by codifying the process of converting SOEsinto corporations and of limiting political intervention. During the 1990s, the legalbasis for the standardized operation of listed companies in the stock market wasgradually developed, and a series of regulations and laws such as ‘The Opinions onStandardizing the Joint Stock Limited Companies’, ‘The Provisional Regulationson the Administration of Issuing and Trading of Stocks’, and the Securities Law of the

People’s Republic of China were instituted.As China has been systematically constructing the institutions of a publicly-

traded economy, it has been widely reported that the government has significantlydecreased its stake in the state-owned firms that have been listed on the Shanghaiand Shenzhen Stock Exchanges, and these companies are becoming ‘privatized’ insome ways. Woo (1999) saw the 15th Congress of the Chinese Communist Party(CCP) in September 1997 as a watershed moment, as the state passed key resolu-tions to accelerate privatization of the state sector. And as scholars have watchedthis process unfold over the decade following the 15th Congress, many have cometo the conclusion that the state has indeed proceeded in the process of privatizingthe state sector, particularly those firms listed in domestic and international stockexchanges. As Beamish and Delios describe the trend: ‘Along with . . . growth inthe number of listed companies has come a change in ownership, in which formerlystate-owned companies have had their shares transferred into the hands of privateinterests. . . . ’ (2005: 310).

This view, however, lacks a nuanced understanding of the complexities ofenterprise–state relations, as the government’s receding from control over publicly-listed companies has, like every other institutional change in China’s economicreform, been a gradual process. In this study we argue that because the statemaintains a controlling interest in these publicly-traded firms in a variety of ways,state-ownership of publicly-traded firms has declined only by degrees. First, overthe course of the IPO process, the state office overseeing a large group company(jituan gongsi )[2] usually has a heavy hand in deciding which part of thegroup will be spun off for the IPO. Most often the strongest performing factory orgroup of factories goes public. The state maintains the basic state–firm relationshipwith the remaining part of the group company – it remains on as the advisoryadministrative office, playing a significant role in the strategic decisions the firm orgroup makes as well as maintaining a hand as the partial residual claimant on firmprofits (Guthrie, Xiao, & Wang, 2009). In some cases in which firms are not partof a group, the entire factory may go public; however, IPO processes more ofteninvolve a spin-off situation. In the initial stages of the IPO, the state administrativeoffice and the group company maintain control of between 20 percent and 60percent of the shares, though in the early years of the stock exchanges thesenumbers were closer to 70 percent. The remainder of the shares is divided between

Ownership Concentration in Chinese SOEs 5

© 2011 The International Association for Chinese Management Research

various types of institutional and free-floating shares. A typical ownership trans-formation for a state-owned enterprise would allow the state to retain between40 percent and 50 percent of the company’s shares; between 20 percent and 30percent of the shares are designated for institutional shares; the remaining 30percent of shares are designated for public consumption as free floating shares(Guthrie et al., 2009).

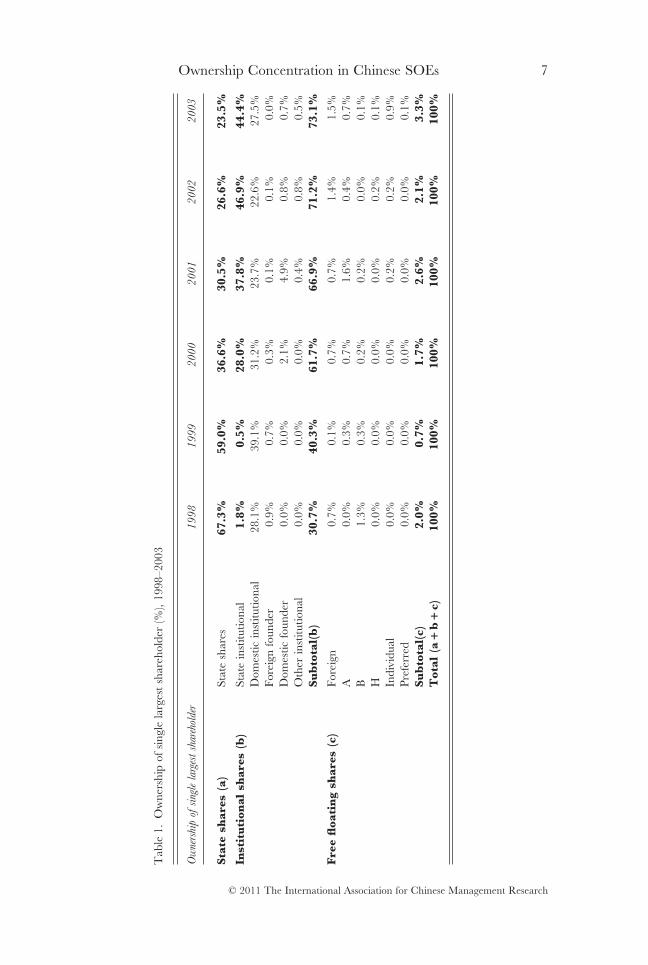

More importantly, the above-mentioned popular view that former SOEs havehad their shares ‘privatized’ neglects the roles that the newly-built SOAMCs in themid 1990s have played in masking continued state ownership over publicly-listedfirms. Table 1 shows the ownership trends of the largest shareholders of all publiccompanies from 1998–2003.[3] As the state shares of the largest shareholdersdeclined from 67.3 percent to 23.5 percent (a decline of 43.8 percent), stateinstitutional shares rose from 1.8 percent to 44.4 percent (an increase of 42.6percent). However, to the extent that state ownership (guojia gu ) declined,those ownership shares were placed in state institutional shares (guoyou faren gu

). Note that virtually no other categories of ownership changed overthis time period. In other words, to the extent that the state offices have divestedthemselves from ownership of publicly-traded firms, nearly 100 percent of thosedivested shares have been moved directly into SOAMCs. Just as the state banksmoved bad loans off their books into AMCs that they owned, state offices shiftedtheir ownership shares into SOAMCs that they also owned.

These SOAMCs can be treated as ‘institutional investors’ as they are organiza-tions set up (at least in theory) to manage a portfolio of assets. Through the creationof SOAMCs, the state appeared to demonstrate a commitment to a decliningpresence in these publicly-listed firms. However, it should be clear at this earlystage, in practical terms, little changed for these offices – they still employed thesame people and they still maintained the same relationships with the firms undertheir jurisdictions in terms of managerial and ownership control. In the mid 1990s,the largest and most famous of these were the AMCs connected to each of the fourmain Central Government banks (initially set up to help these banks move badloans off their books). As with the AMCs owned by the banks, these smaller AMCswere usually owned by a local government administrative office. Today, there areliterally hundreds of organizations in the Chinese economy that used to be gov-ernment administrative offices and are now owned by state offices or that now callthemselves asset management companies. The largest and most powerful of theasset management institutions is SASAC, the Central Government commissioncharged with transforming the largest and most powerful of the firms in the stateeconomy.

The diffusion of SOAMCs is important because it has allowed the state toappear to be divesting its ownership stake in SOEs, though these shares have beenmoved into another state-owned category. We are not arguing that the rise of thesenew organizational structures is inconsequential for organizational performance.

6 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

Tab

le1.

Ow

ners

hip

ofsi

ngle

larg

est

shar

ehol

der

(%),

1998

–200

3

Ow

ners

hip

ofsi

ngle

larg

est

shar

ehol

der

19

98

19

99

20

00

20

01

20

02

20

03

Stat

esh

ares

(a)

Stat

esh

ares

67.3

%59

.0%

36.6

%30

.5%

26.6

%23

.5%

Inst

itu

tion

alsh

ares

(b)

Stat

ein

stitu

tiona

l1.

8%0.

5%28

.0%

37.8

%46

.9%

44.4

%D

omes

ticin

stitu

tiona

l28

.1%

39.1

%31

.2%

23.7

%22

.6%

27.5

%Fo

reig

nfo

unde

r0.

9%0.

7%0.

3%0.

1%0.

1%0.

0%D

omes

ticfo

unde

r0.

0%0.

0%2.

1%4.

9%0.

8%0.

7%O

ther

inst

itutio

nal

0.0%

0.0%

0.0%

0.4%

0.8%

0.5%

Sub

tota

l(b

)30

.7%

40.3

%61

.7%

66.9

%71

.2%

73.1

%

Fre

efl

oati

ng

shar

es(c

)Fo

reig

n0.

7%0.

1%0.

7%0.

7%1.

4%1.

5%A

0.0%

0.3%

0.7%

1.6%

0.4%

0.7%

B1.

3%0.

3%0.

2%0.

2%0.

0%0.

1%H

0.0%

0.0%

0.0%

0.0%

0.2%

0.1%

Indi

vidu

al0.

0%0.

0%0.

0%0.

2%0.

2%0.

9%Pr

efer

red

0.0%

0.0%

0.0%

0.0%

0.0%

0.1%

Sub

tota

l(c)

2.0%

0.7%

1.7%

2.6%

2.1%

3.3%

Tot

al(a

+b

+c)

100%

100%

100%

100%

100%

100%

Ownership Concentration in Chinese SOEs 7

© 2011 The International Association for Chinese Management Research

Rather, our main thesis is to show that it is naïve to view the state as simply havingdivested itself from ownership of the state sector. Virtually all of the figures thatscholars and the popular press have picked up as evidence of the declining role ofthe state relates to the decline in state shares but ignores the rise in state institu-tional shares. In this study, we examine the extent to which the emergence of thesenew institutions has influenced the governance of SOEs in recent years.

Hypotheses

It is relevant to ask whether and how the changes described above matter for theperformance of Chinese firms. Economists such as Kornai (1980, 1990) andSachs (1992, 1993, 1995a,b) have argued that state ownership is anathema to awell-functioning market economy. State involvement leads inevitably to rent-seeking, graft, and other forms of corruption, while the discipline of the marketis the most effective (and parsimonious) path to efficient market behaviour. Someeconomists have countered this view by arguing that gradualism allows forexperimentation and stability within the market and, therefore, creates the con-ditions for firms to navigate the complexities of market reform (Naughton, 1995;Rawski, 1994, 1995, 1999). Other scholars have taken an even stronger positionon the role of state involvement in China’s reform, arguing that state involve-ment in the economy can actually lead to positive outcomes for transformingstate-owned firms (Guthrie, 2005; Oi, 1992, 1995; Walder, 1995; Wang, 2009).The basic argument among these scholars is that gradual reform meant that thebureaucratic sector slowly pushed economic responsibilities on the shoulders oflocal officials and individual managers. Local-level actors were able to experi-ment with new ways of participating in the global economy. They also experi-enced a sense of stability in the process, as state owners helped to gradually weanthem off their dependence on budgetary allocations from the state while learningthe rules of effective market behaviour. Guthrie (1997, 1999) argues that thenumber of firms over which state offices have control is inversely related to firmperformance in the reform era. As the jurisdiction increases in size, and theadministrative burdens of state jurisdictions grow, officials’ monitoring capacity isweakened, and accordingly, firms experience greater uncertainty and conse-quently do worse. In a recent study of transformed SOEs between 2000 and2005, Li, Xia, Long, and Tan (forthcoming) argue that compared to the firms’ownership type – one variable often used in most current studies – the firms’actual control mode after transformation plays a more critical role in determin-ing firm performance. They find that among state-owned firms those with dis-persed or private control structures outperform the firms with actual statecontrol. These studies suggest the issue of poorly performing SOEs is less aboutownership type and more about the actual control structures of the firms and theadministrative capacity of state offices.

8 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

Thus, the logic of the arguments about the positive impact of state involvementin the economy hinges on the nature of that involvement. State involvement cancome in a variety of forms, and under the right institutional conditions it canproduce a constellation of incentives and capacity for a given state office toeffectively guide the firm(s) under its jurisdiction through the reforms. Accord-ingly, for this population of firms, we expect that the impact of state involvementin firm governance is going to depend on the nature of state involvement. Spe-cifically, we expect that the firms with continued state ownership under thehighest level offices will perform worse than those controlled by lower level gov-ernmental offices as the latter are faced with hardening budget constraints andreceive closer monitoring and more hands-on attention and guidance from localofficials. In line with this argument, the vast majority of state-controlled shares(guojia gu ) lie in the hands of very high-level administrative offices and areexpected to produce the poorest performance. Accordingly, over the course of thelast decade the emergence of SOAMCs may constitute a critical institutionalchange in the Chinese industrial economy. These organizations represent agradual progression away from the direct state ownership of the early parts of thereform area. We conjecture that SOAMCs that retain state institutional shares(guoyou farengu ) of the firms will have a more positive effect on firmperformance, for SOAMCs bring benefits of state involvement, yet they are orga-nizations solely committed to firm performance in ways that the administrativeoffices above them are not.

Hypothesis 1a: The proportion of state institutional ownership of a firm will have a net

positive impact on the firm’s overall profitability. That is: the greater the percentage of shares that

lie in the category of state institutional ownership, the better a firm’s profitability.

Hypothesis 1b: The proportion of state institutional ownership of a firm will have a net

positive impact on the firm’s efficiency. That is: the greater the percentage of shares that lie in the

category of state institutional ownership, the better a firm’s operating margins.

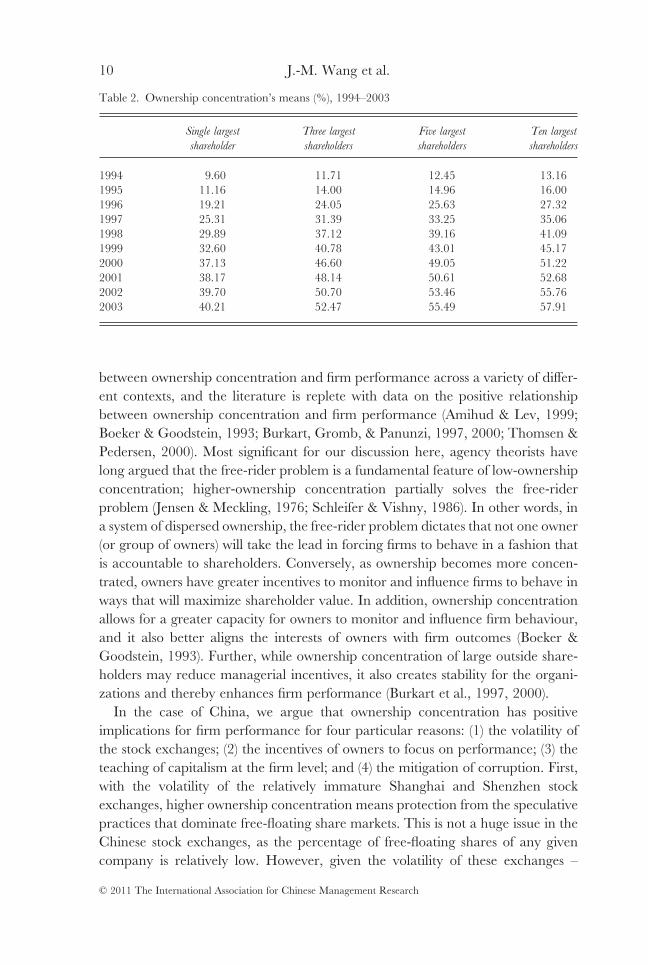

Following our analysis on how ownership patterns of the state sector havechanged over the course of economic reforms and how these changes have affectedfirm performance, we look at the concentration of ownership among the largestshareholders of each publicly-traded company. Related to the emergence ofSOAMCs, we have seen an increase in ownership concentration over the course ofthe life of the stock exchanges. Whereas the average ownership concentration fora given firm in 1994 was between 9 percent and 13 percent, that figure rose tobetween the range of 40 percent and 57 percent in 2003. Table 2 shows theincreasing ownership concentration over the course of the last decade.

Ownership concentration is likely to be an important factor in the governance ofChinese publicly-traded firms. Many scholars have examined the relationship

Ownership Concentration in Chinese SOEs 9

© 2011 The International Association for Chinese Management Research

between ownership concentration and firm performance across a variety of differ-ent contexts, and the literature is replete with data on the positive relationshipbetween ownership concentration and firm performance (Amihud & Lev, 1999;Boeker & Goodstein, 1993; Burkart, Gromb, & Panunzi, 1997, 2000; Thomsen &Pedersen, 2000). Most significant for our discussion here, agency theorists havelong argued that the free-rider problem is a fundamental feature of low-ownershipconcentration; higher-ownership concentration partially solves the free-riderproblem (Jensen & Meckling, 1976; Schleifer & Vishny, 1986). In other words, ina system of dispersed ownership, the free-rider problem dictates that not one owner(or group of owners) will take the lead in forcing firms to behave in a fashion thatis accountable to shareholders. Conversely, as ownership becomes more concen-trated, owners have greater incentives to monitor and influence firms to behave inways that will maximize shareholder value. In addition, ownership concentrationallows for a greater capacity for owners to monitor and influence firm behaviour,and it also better aligns the interests of owners with firm outcomes (Boeker &Goodstein, 1993). Further, while ownership concentration of large outside share-holders may reduce managerial incentives, it also creates stability for the organi-zations and thereby enhances firm performance (Burkart et al., 1997, 2000).

In the case of China, we argue that ownership concentration has positiveimplications for firm performance for four particular reasons: (1) the volatility ofthe stock exchanges; (2) the incentives of owners to focus on performance; (3) theteaching of capitalism at the firm level; and (4) the mitigation of corruption. First,with the volatility of the relatively immature Shanghai and Shenzhen stockexchanges, higher ownership concentration means protection from the speculativepractices that dominate free-floating share markets. This is not a huge issue in theChinese stock exchanges, as the percentage of free-floating shares of any givencompany is relatively low. However, given the volatility of these exchanges –

Table 2. Ownership concentration’s means (%), 1994–2003

Single largest

shareholder

Three largest

shareholders

Five largest

shareholders

Ten largest

shareholders

1994 9.60 11.71 12.45 13.161995 11.16 14.00 14.96 16.001996 19.21 24.05 25.63 27.321997 25.31 31.39 33.25 35.061998 29.89 37.12 39.16 41.091999 32.60 40.78 43.01 45.172000 37.13 46.60 49.05 51.222001 38.17 48.14 50.61 52.682002 39.70 50.70 53.46 55.762003 40.21 52.47 55.49 57.91

10 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

fuelled by rampant speculative activity over the course of their first decade –ownership concentration does help mitigate this effect. Second, ownership concen-tration means a greater amount of focused attention to the economic performanceof firms – as a management issue, firm performance is tied to the incentives of a fewowners who are able to focus attention on how to make the firm most profitable. Asone of our interviewees, the founder of one of Shanghai’s first institutional investingcompanies, put it, ‘What we look for is good management. We don’t care if theyare state-owned or privately-owned. All we care about is whether they are gettinggood advice. There are bad owners on both the state and private side. We are justfocused on governance and performance’.[4] Third, in the turbulent markets of atransition economy, having ownership shares concentrated in the hands of a fewpowerful owners allows for greater stability as managers learn the practices of theemerging market economy. One of the key factors allowing firms to succeed understate control, as argued above, lies in the capacity of administrative offices tomonitor the firms under their jurisdictions. This monitoring capacity dependsheavily on how concentrated their ownership stake in a given firm is. Finally, it islikely that ownership concentration helps mitigate the corruption of local officialsand firm managers. While a number of scholars have argued that corruption is aninevitable outcome of continued state ownership (Kornai, 1980, 1990; Sachs,1992, 1995b), this assumption depends upon the ability of firm managers to actwithout being monitored by bodies that have the ability to influence their actions– an assumption that does not necessarily fit with reality in China’s transition.Under certain conditions, owners will have incentives to monitor firms and therebyshift the behaviours of corrupt officials. This was the case with concentratedownership in the Chinese rural economy in the 1980s (Walder, 1995), and it is thecase with large-scale industrial enterprises that have been recently listed on thedomestic stock exchanges. Thus, we assume that firms with higher ownershipconcentration will perform better in China’s transitional economy:

Hypothesis 2a: Controlling for other factors, as ownership concentration increases, so will

a firm’s profitability.

Hypothesis 2b: Controlling for other factors, as ownership concentration increases, so will

a firm’s efficiency.

METHOD

Two primary modes of study have dominated the field of research on the impactof privatization in transition economies. One of these examines the effectiveness ofprivatization by comparing the performance of privatized firms with those that arestill governed by the state (e.g., Boardman & Vining, 1989; Frydman, Gray, Hessel,& Rapaczynski, 1999; Pohl, Robert, Stijn, & Djankov, 1997). A second compares

Ownership Concentration in Chinese SOEs 11

© 2011 The International Association for Chinese Management Research

the performance of firms over time, as they make the transition from state-ownedto private (Megginson, Nash, & Randenborgh, 1994). We take a different approachto this question, focusing on the degree and type of state ownership in China’sdomestic publicly-traded firms. We analyze the impact of continued state owner-ship in the firms that have been listed on the Shanghai and Shenzhen stockexchanges from 1994–2003. We also explore the impact of ownership concentra-tion, arguing that ownership concentration is a key additional variable in thequestion of the firm’s success in the reform era.

This population and time period are important for several reasons. First, thisperiod coincides with two important institutional changes in China’s emergingmarket economy: the creation of the domestic market for publicly-traded firms andthe renewed resolve by the central government that SOEs would be pushedthrough the final phase of reform to privatization or, if necessary, liquidation.Second, while these are not the blue-chip firms that are listed on internationalexchanges (including Hong Kong), this population of firms comprises a group ofthe largest SOEs that the reforms of the late 1990s were set to target. These dataallow us to show hidden details about the enduring structure of state–firm relationsamong this population of firms, specifically a much closer set of ties betweenpublicly-traded SOEs and their former state owners. These ties are mitigated bygovernance and control by SOAMCs and SASAC.

Sample

Our starting point for data on Chinese listed companies was the WindDB data-base, which reports all of the financial data for publicly-listed firms in China’sdomestic economy. In 1994, there were a total of 338 stocks listed in China. By2003, there were 1,371. From the database, we obtained the information ofshareholders who held 5 percent or more in each of these listed companies. Withthe goal of uncovering who actually owned shares in each company in a given year– as opposed to the listed shareholder – we also traced the owners of each listedshareholding entity through supplementary information including company’sannual reports, announcements, website information, stock market research bystock analysts, and so forth. In some cases, we uncovered up to six identifiablelayers of ownership ‘shells’. We coded each real shareholder (the ultimate owner,as opposed to the shell) and discovered that among the top 10 owners of eachcompany, the real owners of most listed companies fell into three categories: (1)state shares (guojia gu ), which includes central government, provincialgovernments, municipal governments of five cities (that report directly to thecentral government in the planning system: Dalian, Ningbo, Qingdao, Shenzhenand Xiamen) and SOEs; (2) institutional investors ( faren gu ), which includeSOAMCS, non-state, domestic, foreign, founders, and private investors; and (3)free-floating shares. Owing to missing data and differential reports among some

12 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

shares/companies, the final available data for our study came from 328 companiesin 1994 and 1,305 companies in 2003. These numbers differ from the numberslisted above (particularly in the case of 1,371 versus 1,305) because in a number ofcases, A and B shares are listed as different companies, when in fact they are listingsof the same company. Once we corrected for this factor, the actual number of casesomitted due to missing data was 15 cases, or less than 1 percent of the populationin 2003.

There are important potential biases to consider with respect to these data. It iscrucial to note here that in no case on the domestic exchanges from 1994–2003 dida firm, once it was listed, drop out of the sample. Thus, we do not have a problemhere of censorship due to non-random dropping out of the sample. A largerconcern, however, has to do with selection bias in the listing of a company.Companies are selected by their governing administrative office (zhuguan bumen

) to be listed on the stock exchanges. They are usually part of a largergroup or cluster of factories. As such, there is an obvious selection bias in the waysin which companies are chosen for their listing on the Shanghai and Shenzhenexchanges – state offices choose the best performing firms under their jurisdictionsto be listed. And since we are examining firm performance, the selection processitself is correlated with the dependent variables. However, we view this bias as lessproblematic than it might initially seem. The main reason for this is that we aredealing with a specific population of firms, and our comparisons are within thispopulation. In other words, all firms suffer from the same selection bias, so there isa systematic bias that makes these firms comparable to each other. Thus, we areless concerned with the question of whether our firms are a representative sampleof state-owned organizations in China – they are not. In this sense, we are moreconcerned with size, direction, and robustness of the effects we are analyzing. Butthe firms that we analyzed are a population that was overwhelmingly selectedthrough the same process and is therefore comparable within the sample. Becausewe are basically dealing with the entire population of firms, we are not concernedwith the issue of sampling from within this population.

Measures

In our analysis, we take up the challenge laid out by Frydman et al. (1999) to findnew ways to examine the effectiveness of privatization versus continuing stateownership. We look at the degree of state ownership in publicly-traded firms.Conceiving of state ownership as a continuous variable of the percentage of sharesowned by a given state office, we look at the impact that ownership percentage hason various performance outcomes. Because this variable is continuous, it is notframed as a binary comparison of state-owned or not; rather the notion of thedegree of state ownership allows us to examine the question of whether an increasein state ownership has positive, negative, or neutral effects on a firm’s performance.

Ownership Concentration in Chinese SOEs 13

© 2011 The International Association for Chinese Management Research

However, despite the fact that this is not a binary comparison, there is an implicitcomparison in the analysis because as state ownership declines, the stake controlledby other shareholders increases. Second, we look at the degree of state institutionalownership to test the same sets of questions regarding the proportion of sharescontrolled by the AMCs. Third, we also look at the extent to which ownership isconcentrated in the hands of a few shareholders. Even with publicly-traded firms,there is significant variation in the area of ownership concentration. Understand-ing the impact of ownership concentration is crucial for understanding the perfor-mance of these firms, as it leads to a separate set of issues about governance andshareholder influence.

From these three areas of inquiry, we generate three key independent variablesfor our analyses below: (1) percentage of a firm’s shares that fall into the categoryof state shares in a given year; (2) percentage of a firm’s shares that fall into thecategory of state institutional shares, which are essentially shares owned bySOAMCs and ultimately under the jurisdiction of SASAC; and (3) percentage ofshares owned by the top controlling owners for a firm in a given year.[5] In ourmodels, we also control for the sales of the firm in a given year (a proxy for size),the year, and the sector of the firm (in the models we present below; however, thetime invariant sector controls fall out because we employ the more rigorousfixed-effects models). Following Holz (2002) our dependent variables include netprofits, cash operating profits (EBIT), and the operating margins of the firm. EBITprofits are simply earnings before deducting interest, taxes, depreciation, amorti-zation, and other non-operating items. Net profits are calculated as gross profitsminus indirect costs (i.e., costs not directly attributable to production that werealready removed from sales revenues to arrive at the gross profit figure). Perfor-mance or operating margins are calculated as profits divided by revenues.

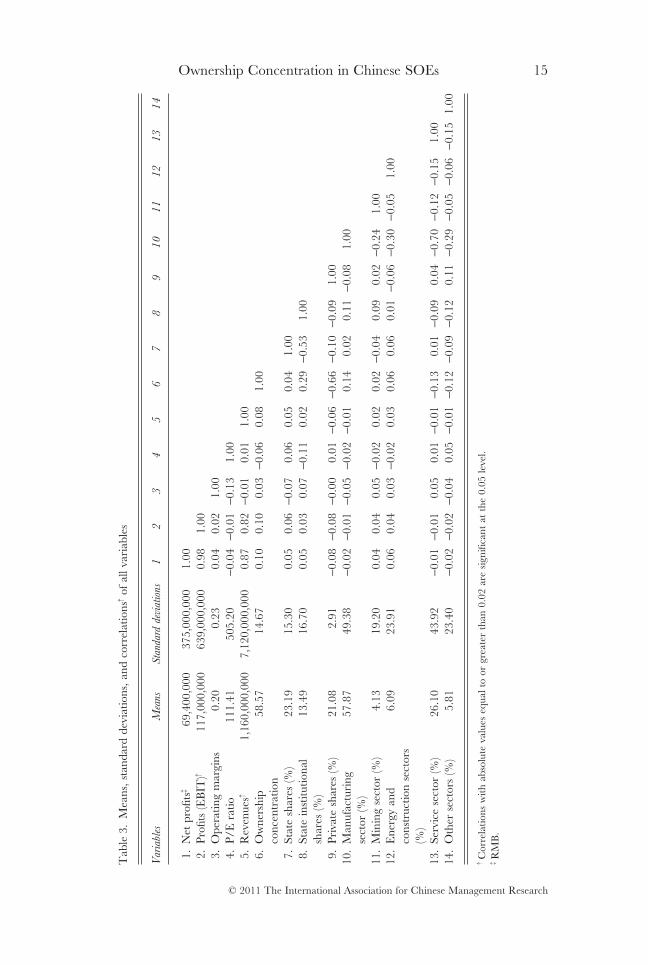

As Table 3 shows, over the course of the first decade of publicly-traded firms inChina, these organizations had revenues of 1.16 billion yuan (~$143 million). Theaverage net profit of these firms over the last decade was 69 million yuan (~$8.6million), and cash operating profits averaged 117 million yuan (~$14 million). Theaverage operating margin was 21 percent, and the average price-to-equity ratiowas an astounding 111. These firms had an average of 23 percent of state sharesand an average of 13 percent of state institutional shares. Finally, the averagepercentage of shares held by the top five shareholders for these firms that measuresfirms’ ownership concentration was nearly 60 percent. Table 3 also presents thecorrelations for all the variables included in the statistical analysis.

Analyses

The general model shown by Equation (1) that we use to analyze the associationsamong these variables takes the form of a fixed effects model for the determinantsof firm profitability and efficiency for the firms in our data:

14 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

Tab

le3.

Mea

ns,s

tand

ard

devi

atio

ns,a

ndco

rrel

atio

ns†

ofal

lvar

iabl

es

Var

iabl

esM

eans

Sta

ndar

dde

viat

ions

12

34

56

78

91

01

11

21

31

4

1.N

etpr

ofits

‡69

,400

,000

375,

000,

000

1.00

2.Pr

ofits

(EB

IT)†

117,

000,

000

639,

000,

000

0.98

1.00

3.O

pera

ting

mar

gins

0.20

0.23

0.04

0.02

1.00

4.P/

Era

tio11

1.41

505.

20-0

.04

-0.0

1-0

.13

1.00

5.R

even

ues†

1,16

0,00

0,00

07,

120,

000,

000

0.87

0.82

-0.0

10.

011.

006.

Ow

ners

hip

conc

entr

atio

n58

.57

14.6

70.

100.

100.

03-0

.06

0.08

1.00

7.St

ate

shar

es(%

)23

.19

15.3

00.

050.

06-0

.07

0.06

0.05

0.04

1.00

8.St

ate

inst

itutio

nal

shar

es(%

)13

.49

16.7

00.

050.

030.

07-0

.11

0.02

0.29

-0.5

31.

00

9.Pr

ivat

esh

ares

(%)

21.0

82.

91-0

.08

-0.0

8-0

.00

0.01

-0.0

6-0

.66

-0.1

0-0

.09

1.00

10.

Man

ufac

turi

ngse

ctor

(%)

57.8

749

.38

-0.0

2-0

.01

-0.0

5-0

.02

-0.0

10.

140.

020.

11-0

.08

1.00

11.

Min

ing

sect

or(%

)4.

1319

.20

0.04

0.04

0.05

-0.0

20.

020.

02-0

.04

0.09

0.02

-0.2

41.

0012

.E

nerg

yan

dco

nstr

uctio

nse

ctor

s(%

)

6.09

23.9

10.

060.

040.

03-0

.02

0.03

0.06

0.06

0.01

-0.0

6-0

.30

-0.0

51.

00

13.

Serv

ice

sect

or(%

)26

.10

43.9

2-0

.01

-0.0

10.

050.

01-0

.01

-0.1

30.

01-0

.09

0.04

-0.7

0-0

.12

-0.1

51.

0014

.O

ther

sect

ors

(%)

5.81

23.4

0-0

.02

-0.0

2-0

.04

0.05

-0.0

1-0

.12

-0.0

9-0

.12

0.11

-0.2

9- 0

.05

-0.0

6-0

.15

1.00

†C

orre

latio

nsw

ithab

solu

teva

lues

equa

lto

orgr

eate

rth

an0.

02ar

esi

gnifi

cant

atth

e0.

05le

vel.

‡R

MB

.

Ownership Concentration in Chinese SOEs 15

© 2011 The International Association for Chinese Management Research

Y Zit it i t it= + + + +α γ δ λ ε . (1)

In the model described above, Yit represents the outcome for firm i at time t, a isan intercept, Zit is a vector of measurable firm-level variables for firm i at time t, gis a vector of regression coefficients corresponding to the variables in vector Z, di

represents yearly firm-level heterogeneity, lt represents unobserved time-basedheterogeneity (year effects), and eit is a time-varying error term. The firm-level fixedeffects, di, allow us to control for unobservable firm-level differences. On a theo-retical level, we believe that the fixed effects models are actually the appropriatemodels for our analysis (i.e., more appropriate than random effects models), asthere are several identifiable firm-level variables for which we do not have data(e.g., organizational size, board composition, the role of the Party committee in thefirm) that are likely to influence both ownership concentration and firm perfor-mance.[6] However, to be sure of this view, in previous analyses we tested bothrandom and fixed-effects models, assessing the differences between the randomand fixed effects models through the Hausman Specification Test (HST)(Hausman, 1978), where significance of difference between the two models suggeststhe better fit of the fixed effects model. In most cases, HST indicated the presenceof firm-level heterogeneity, so, for the results we present here, we err on the side ofconservatism and present the results of the models that include firm-level fixedeffects.

As a final point, we should note that, while conventional approaches tomodels such as these would typically log the dependent variables – particularlyin the cases of the two profitability variables – our models do not take thisapproach for two reasons. First, there are a significant number of cases thatyield negative values on these outcomes, making the natural log of the outcomevariables undefined in some cases. In order to test the importance of thisissue, in addition to all of the models presented below, we also ran all of themodels based upon the following transformation for the Net Profits and EBITProfits:

Y * Y Ci i= + +( )[ ]ln ,1 (2)

where Yi represents either the dependent variables Net Profits or EBIT Profitsand C is equal to the largest value of Yi. In none of these models were theresubstantive differences in the magnitude or significance of the effects, so, for thesake of simplicity and interpretability of the results, we present results based onthe untransformed variables. Second, the distributions of the outcome variablesare not in the least skewed, with the exception of one outlier. We also ran alluntransformed models omitting this sole outlier and found no substantive differ-ences from the results we present here.

16 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

RESULTS

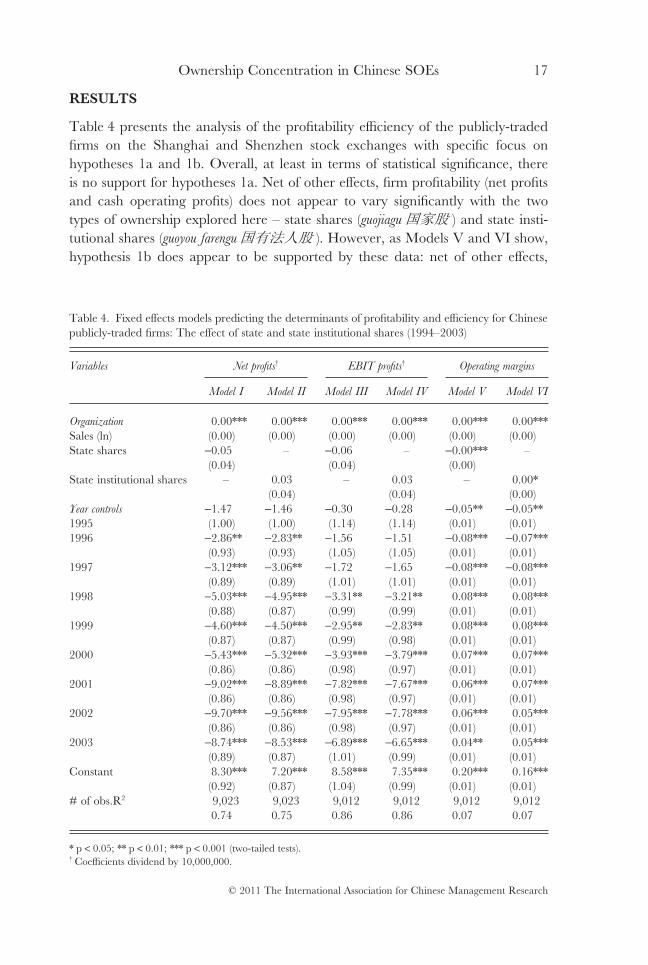

Table 4 presents the analysis of the profitability efficiency of the publicly-tradedfirms on the Shanghai and Shenzhen stock exchanges with specific focus onhypotheses 1a and 1b. Overall, at least in terms of statistical significance, thereis no support for hypotheses 1a. Net of other effects, firm profitability (net profitsand cash operating profits) does not appear to vary significantly with the twotypes of ownership explored here – state shares (guojiagu ) and state insti-tutional shares (guoyou farengu ). However, as Models V and VI show,hypothesis 1b does appear to be supported by these data: net of other effects,

Table 4. Fixed effects models predicting the determinants of profitability and efficiency for Chinesepublicly-traded firms: The effect of state and state institutional shares (1994–2003)

Variables Net profits† EBIT profits† Operating margins

Model I Model II Model III Model IV Model V Model VI

Organization 0.00*** 0.00*** 0.00*** 0.00*** 0.00*** 0.00***Sales (ln) (0.00) (0.00) (0.00) (0.00) (0.00) (0.00)State shares -0.05 – -0.06 – -0.00*** –

(0.04) (0.04) (0.00)State institutional shares – 0.03 – 0.03 – 0.00*

(0.04) (0.04) (0.00)Year controls

1995-1.47 -1.46 -0.30 -0.28 -0.05** -0.05**(1.00) (1.00) (1.14) (1.14) (0.01) (0.01)

1996 -2.86** -2.83** -1.56 -1.51 -0.08*** -0.07***(0.93) (0.93) (1.05) (1.05) (0.01) (0.01)

1997 -3.12*** -3.06** -1.72 -1.65 -0.08*** -0.08***(0.89) (0.89) (1.01) (1.01) (0.01) (0.01)

1998 -5.03*** -4.95*** -3.31** -3.21** 0.08*** 0.08***(0.88) (0.87) (0.99) (0.99) (0.01) (0.01)

1999 -4.60*** -4.50*** -2.95** -2.83** 0.08*** 0.08***(0.87) (0.87) (0.99) (0.98) (0.01) (0.01)

2000 -5.43*** -5.32*** -3.93*** -3.79*** 0.07*** 0.07***(0.86) (0.86) (0.98) (0.97) (0.01) (0.01)

2001 -9.02*** -8.89*** -7.82*** -7.67*** 0.06*** 0.07***(0.86) (0.86) (0.98) (0.97) (0.01) (0.01)

2002 -9.70*** -9.56*** -7.95*** -7.78*** 0.06*** 0.05***(0.86) (0.86) (0.98) (0.97) (0.01) (0.01)

2003 -8.74*** -8.53*** -6.89*** -6.65*** 0.04** 0.05***(0.89) (0.87) (1.01) (0.99) (0.01) (0.01)

Constant 8.30*** 7.20*** 8.58*** 7.35*** 0.20*** 0.16***(0.92) (0.87) (1.04) (0.99) (0.01) (0.01)

# of obs.R2 9,023 9,023 9,012 9,012 9,012 9,0120.74 0.75 0.86 0.86 0.07 0.07

* p < 0.05; ** p < 0.01; *** p < 0.001 (two-tailed tests).† Coefficients dividend by 10,000,000.

Ownership Concentration in Chinese SOEs 17

© 2011 The International Association for Chinese Management Research

the greater the level of state ownership the worse a firm does in the efficiencyrealm and the greater the level of state institutional ownership the more effi-ciently a firm performs. This is an important finding, because, at first glance, itappears that firms with higher levels of concentration in the hands of SOAMCsare going to do better in firm performance – measured by efficiency – than thosewhose ownership is concentrated in the hands of state or private owners.However, we still need to test these results against the issue of ownership con-centration.

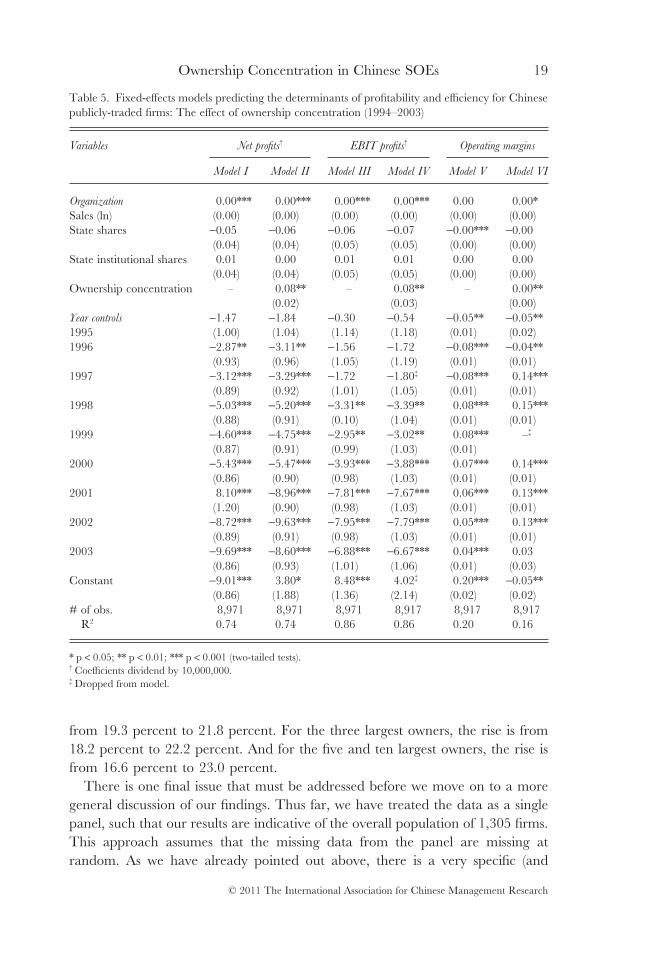

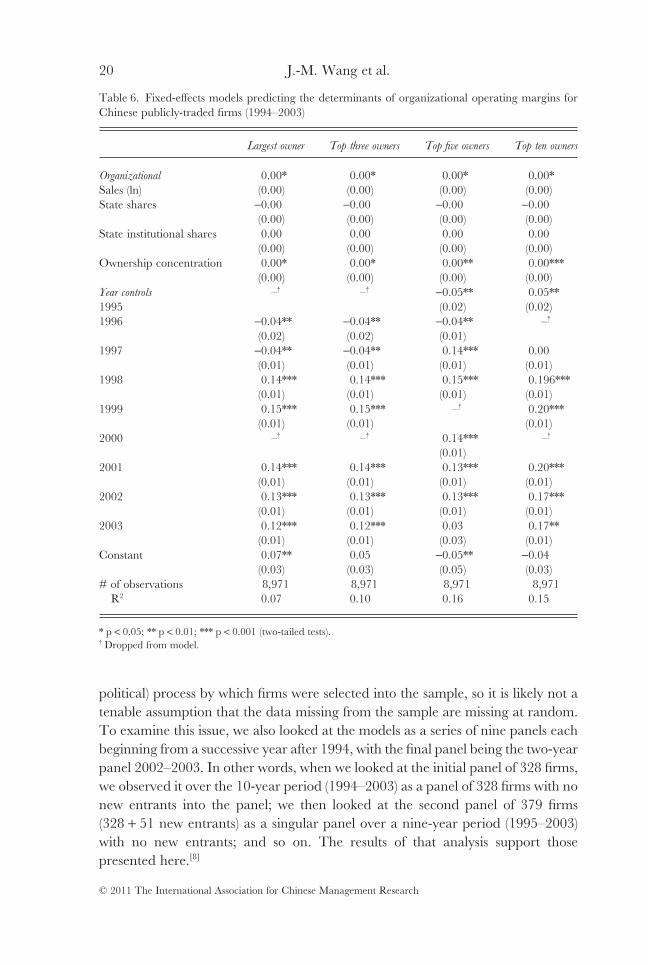

Table 5 presents the results from analyses that include ownership concentration.First, with respect to hypothesis 1b, the results we presented above disappear whenwe control for ownership concentration (Model VI), a fact that must temper ourview that there is much difference between state and state institutional ownership.The results of the tests of hypotheses 2a and 2b are the strongest and mostconsistent in our analyses. In Table 5, we report the effects for ownership concen-tration amongst the top five owners and find that ownership concentration has astrong, consistent, and statistically significant positive association with firm profit-ability (both measures) and with firm performance. As ownership concentrationincreases among the top five largest owners of a given firm, net profits and cashoperating profits also increase: for each percentage increase in the shares that areheld by the five largest owners, we find an increase in profits of nearly 8 millionyuan. For cash operating profits, we find a similar set of effects, yielding 8.1 millionyuan for each percentage increase in ownership among the top five owners. Asnoted above, we also find a statistically significant effect of ownership concentra-tion on the operating margins of the firm. In Table 6, we show the effects ofownership concentration measured by the top one, three, five, and ten controllingshareholders on firm efficiency. As ownership concentration increases across all ofthe categories of ownership we collected data on, so do the operating margins ofthese firms.

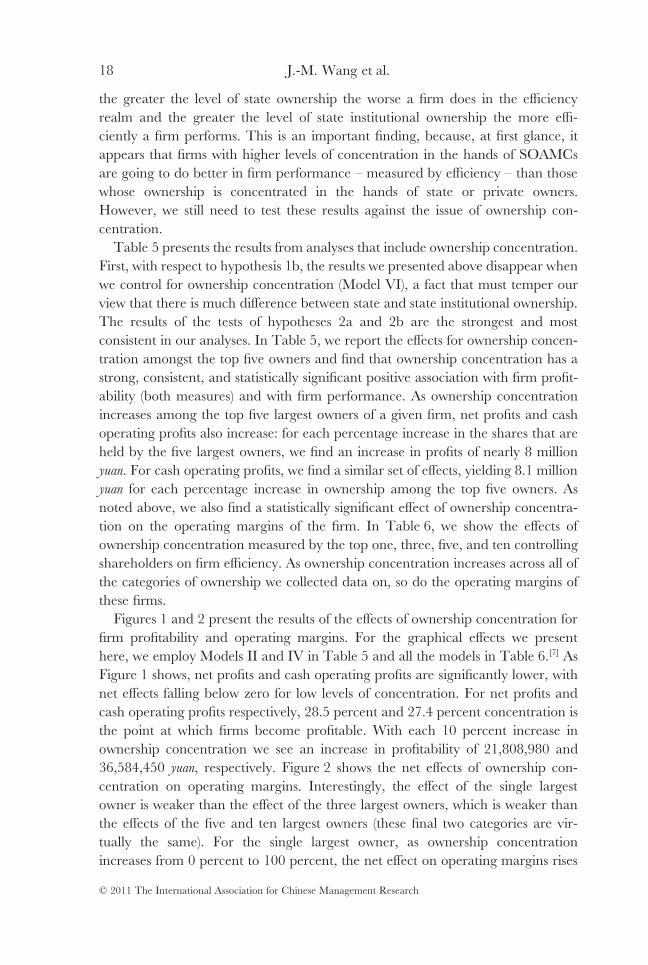

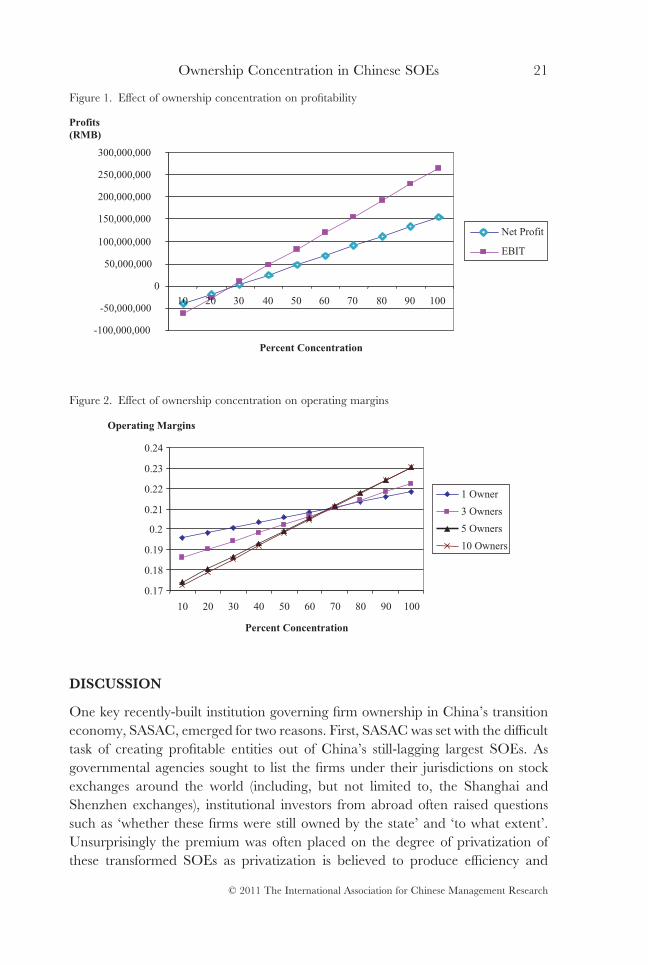

Figures 1 and 2 present the results of the effects of ownership concentration forfirm profitability and operating margins. For the graphical effects we presenthere, we employ Models II and IV in Table 5 and all the models in Table 6.[7] AsFigure 1 shows, net profits and cash operating profits are significantly lower, withnet effects falling below zero for low levels of concentration. For net profits andcash operating profits respectively, 28.5 percent and 27.4 percent concentration isthe point at which firms become profitable. With each 10 percent increase inownership concentration we see an increase in profitability of 21,808,980 and36,584,450 yuan, respectively. Figure 2 shows the net effects of ownership con-centration on operating margins. Interestingly, the effect of the single largestowner is weaker than the effect of the three largest owners, which is weaker thanthe effects of the five and ten largest owners (these final two categories are vir-tually the same). For the single largest owner, as ownership concentrationincreases from 0 percent to 100 percent, the net effect on operating margins rises

18 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

from 19.3 percent to 21.8 percent. For the three largest owners, the rise is from18.2 percent to 22.2 percent. And for the five and ten largest owners, the rise isfrom 16.6 percent to 23.0 percent.

There is one final issue that must be addressed before we move on to a moregeneral discussion of our findings. Thus far, we have treated the data as a singlepanel, such that our results are indicative of the overall population of 1,305 firms.This approach assumes that the missing data from the panel are missing atrandom. As we have already pointed out above, there is a very specific (and

Table 5. Fixed-effects models predicting the determinants of profitability and efficiency for Chinesepublicly-traded firms: The effect of ownership concentration (1994–2003)

Variables Net profits† EBIT profits† Operating margins

Model I Model II Model III Model IV Model V Model VI

Organization

Sales (ln)0.00*** 0.00*** 0.00*** 0.00*** 0.00 0.00*(0.00) (0.00) (0.00) (0.00) (0.00) (0.00)

State shares -0.05 -0.06 -0.06 -0.07 -0.00*** -0.00(0.04) (0.04) (0.05) (0.05) (0.00) (0.00)

State institutional shares 0.01 0.00 0.01 0.01 0.00 0.00(0.04) (0.04) (0.05) (0.05) (0.00) (0.00)

Ownership concentration – 0.08** – 0.08** – 0.00**(0.02) (0.03) (0.00)

Year controls

1995-1.47 -1.84 -0.30 -0.54 -0.05** -0.05**(1.00) (1.04) (1.14) (1.18) (0.01) (0.02)

1996 -2.87** -3.11** -1.56 -1.72 -0.08*** -0.04**(0.93) (0.96) (1.05) (1.19) (0.01) (0.01)

1997 -3.12*** -3.29*** -1.72 -1.80‡ -0.08*** 0.14***(0.89) (0.92) (1.01) (1.05) (0.01) (0.01)

1998 -5.03*** -5.20*** -3.31** -3.39** 0.08*** 0.15***(0.88) (0.91) (0.10) (1.04) (0.01) (0.01)

1999 -4.60*** -4.75*** -2.95** -3.02** 0.08*** –‡

(0.87) (0.91) (0.99) (1.03) (0.01)2000 -5.43*** -5.47*** -3.93*** -3.88*** 0.07*** 0.14***

(0.86) (0.90) (0.98) (1.03) (0.01) (0.01)2001 8.10*** -8.96*** -7.81*** -7.67*** 0.06*** 0.13***

(1.20) (0.90) (0.98) (1.03) (0.01) (0.01)2002 -8.72*** -9.63*** -7.95*** -7.79*** 0.05*** 0.13***

(0.89) (0.91) (0.98) (1.03) (0.01) (0.01)2003 -9.69*** -8.60*** -6.88*** -6.67*** 0.04*** 0.03

(0.86) (0.93) (1.01) (1.06) (0.01) (0.03)Constant -9.01*** 3.80* 8.48*** 4.02‡ 0.20*** -0.05**

(0.86) (1.88) (1.36) (2.14) (0.02) (0.02)# of obs.

R28,971 8,971 8,971 8,917 8,917 8,9170.74 0.74 0.86 0.86 0.20 0.16

* p < 0.05; ** p < 0.01; *** p < 0.001 (two-tailed tests).† Coefficients dividend by 10,000,000.‡ Dropped from model.

Ownership Concentration in Chinese SOEs 19

© 2011 The International Association for Chinese Management Research

political) process by which firms were selected into the sample, so it is likely not atenable assumption that the data missing from the sample are missing at random.To examine this issue, we also looked at the models as a series of nine panels eachbeginning from a successive year after 1994, with the final panel being the two-yearpanel 2002–2003. In other words, when we looked at the initial panel of 328 firms,we observed it over the 10-year period (1994–2003) as a panel of 328 firms with nonew entrants into the panel; we then looked at the second panel of 379 firms(328 + 51 new entrants) as a singular panel over a nine-year period (1995–2003)with no new entrants; and so on. The results of that analysis support thosepresented here.[8]

Table 6. Fixed-effects models predicting the determinants of organizational operating margins forChinese publicly-traded firms (1994–2003)

Largest owner Top three owners Top five owners Top ten owners

Organizational

Sales (ln)0.00* 0.00* 0.00* 0.00*(0.00) (0.00) (0.00) (0.00)

State shares -0.00 -0.00 -0.00 -0.00(0.00) (0.00) (0.00) (0.00)

State institutional shares 0.00 0.00 0.00 0.00(0.00) (0.00) (0.00) (0.00)

Ownership concentration 0.00* 0.00* 0.00** 0.00***(0.00) (0.00) (0.00) (0.00)

Year controls

1995–† –† -0.05** 0.05**

(0.02) (0.02)1996 -0.04** -0.04** -0.04** –†

(0.02) (0.02) (0.01)1997 -0.04** -0.04** 0.14*** 0.00

(0.01) (0.01) (0.01) (0.01)1998 0.14*** 0.14*** 0.15*** 0.196***

(0.01) (0.01) (0.01) (0.01)1999 0.15*** 0.15*** –† 0.20***

(0.01) (0.01) (0.01)2000 –† –† 0.14*** –†

(0.01)2001 0.14*** 0.14*** 0.13*** 0.20***

(0.01) (0.01) (0.01) (0.01)2002 0.13*** 0.13*** 0.13*** 0.17***

(0.01) (0.01) (0.01) (0.01)2003 0.12*** 0.12*** 0.03 0.17**

(0.01) (0.01) (0.03) (0.01)Constant 0.07** 0.05 -0.05** -0.04

(0.03) (0.03) (0.05) (0.03)# of observations

R28,971 8,971 8,971 8,9710.07 0.10 0.16 0.15

* p < 0.05; ** p < 0.01; *** p < 0.001 (two-tailed tests).† Dropped from model.

20 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

DISCUSSION

One key recently-built institution governing firm ownership in China’s transitioneconomy, SASAC, emerged for two reasons. First, SASAC was set with the difficulttask of creating profitable entities out of China’s still-lagging largest SOEs. Asgovernmental agencies sought to list the firms under their jurisdictions on stockexchanges around the world (including, but not limited to, the Shanghai andShenzhen exchanges), institutional investors from abroad often raised questionssuch as ‘whether these firms were still owned by the state’ and ‘to what extent’.Unsurprisingly the premium was often placed on the degree of privatization ofthese transformed SOEs as privatization is believed to produce efficiency and

Figure 1. Effect of ownership concentration on profitability

-100,000,000

-50,000,000

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

10 20 30 40 50 60 70 80 90 100

Percent Concentration

Profits (RMB)

Net Profit

EBIT

Figure 2. Effect of ownership concentration on operating margins

0.17

0.18

0.19

0.2

0.21

0.22

0.23

0.24

10 20 30 40 50 60 70 80 90 100

Percent Concentration

Operating Margins

1 Owner

3 Owners

5 Owners

10 Owners

Ownership Concentration in Chinese SOEs 21

© 2011 The International Association for Chinese Management Research

profitability. However, it is increasingly acknowledged that the term ‘privatization’is in fact misleading in depicting Chinese transformed SOEs and developmentaltrajectory (Fligstein & Zhang, 2011; Lin, 2011; Meyer, 2011; Walder, 2011). Ourstudy shows that the state’s approach to transforming listed SOEs was to formSOAMCs and move the ownership accounts of these organizations over to theSOAMCs. The catch was that, unbeknownst to many investors, the same stateagencies that previously owned the SOEs also owned the SOAMCs. The divest-ment of their ownership stake in publicly-traded SOEs was part of an accountingmove by the government agencies to make these firms more attractive for institu-tional investors from abroad.

While this account might be taken as a cynical view of the state’s effort tomaintain property rights and governance over the firms under their jurisdictions,there is a second force at work. The logic of what the Chinese government hasdone with the transfer of ownership to SOAMCs is not out of step with the broaderlogic of gradual reform, which is fundamentally about experimenting with newinstitutional forms that allow for stability and connection with past institutionalforms while at the same time encouraging new management models. TheSOAMCs can be seen in this light, though it may simply be too early to see thepositive effects on firm performance. Under the logic of gradual reform, SOAMCsare organizations that may be an interim model of corporate ownership andgovernance – it is likely the case that these organizations will act more and moreindependently from the state agencies to which they report and, eventually, actfully independent of their influence. These state organizations devoted to theperformance of the firms under their jurisdictions helped buffer transformingSOEs from the shock of the market reforms, stabilizing the firms under theircontrol and offering administrative resources and advice where needed. The realquestion for SOAMCs is not whether they are still ultimately owned by the state,but, rather, whether they manage and govern firms differently than the govern-ment agencies that were formerly the direct owners. Our findings are in perfect linewith Li et al.’s (forthcoming) argument that the actual control modes determinefirm performance, and transformed SOEs with less state control outperform tra-ditional SOEs with more state control. Our data analyses also offer some evidenceof differences in the effects of classical state ownership and state institutionalownership.

Most importantly, we looked at the relationship between firm performance andownership concentration. Over the last decade of the stock exchange’s existence,ownership has been slowly but increasingly concentrated in fewer and fewer hands.However, it should be noted here that, while ownership concentration might seemintuitively like a negative factor in firm governance (at least in cases in whichultimate owners are the state), the concentration of ownership in the Chineseeconomy is not so different from that found in advanced industrialized capitalisteconomies like the U.S.,[9] and there is a growing mass of evidence that ownership

22 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

concentration is positively correlated with firm performance. The case of China isno different. In our study, ownership concentration appears to have the mostconsistent positive effects on the performance of Chinese firms measured by prof-itability and efficiency. Many scholars have argued that ownership concentrationhelps solve the free-rider problem that agency theorists have associated withdispersed ownership, and we believe those arguments apply here as well.

Moreover, there are important issues about ownership concentration that arespecific for China. First, higher ownership concentration means greater controland therefore greater monitoring capacity and stability for the firms under theirowners’ jurisdictions. As owners have greater control over the firms under theirjurisdictions, they are able to guide them to a more stable outcome as they navigatetheir way through the turbulent markets of China’s transforming economy.Second, learning the rules of the game in an emerging market economy is a difficultprocess, and concentrated ownership forces a small number of investors withstrong interests in the success of the firm to help these firms navigate the complexi-ties of the transition economy. Third, although concerns over corruption havebeen fundamental to the analysis of state control in a gradually transformingeconomy (e.g., Kornai, 1990), it is also likely that having a concentrated group ofowners with incentives that are aligned with generating capital is likely to helpmitigate corruption.

There are two interesting caveats in the effect of ownership concentration,however. First, although our study shows that across the board, the higher theconcentration of ownership the better a firm performs, we think that a balance isrequired in China’s context: ownership concentration has a positive effect on firmperformance, but if ownership is too highly concentrated (for example, in the handsof a single-owner), the effect on firm performance is more modest than whenownership is concentrated in the hands of five to ten owners. The reason for this,we believe, is that the free-rider problem can be mitigated with a relatively smallnumber of owners who can pressure each other to be attentive to the firms in whichthey have a controlling interest. However, there are also advantages to a largernumber of owners: SOAMCs, for example, which have controlling stakes in anumber of different firms, can share information. Knowledge diffuses across thesegroups of owners, so that best practices for the firms under their jurisdictions candraw upon the multiplicity of firms that each institutional investor (or other type ofgovernmental agency) owns. Thus, the key issue here is that, while solving thefree-rider problem is important, it is also crucial to have a group of owners withwhich to share knowledge and best practices. Beyond the sharing of knowledge, itis also important to have a variety of sources to draw upon for the monitoring andstability we have discussed above.

Second, it is important to note that these issues, while apparently important inthe early years of China’s domestic exchanges, have declined in importance overtime. We believe this has to do with the maturity of China’s markets. The mid

Ownership Concentration in Chinese SOEs 23

© 2011 The International Association for Chinese Management Research

1990s was still a fairly uncertain time for firms in China’s transforming state sector,particularly those firms at the upper levels of China’s command economy – thevery firms that are today listed on China’s domestic stock exchanges. Furthermore,the exchanges themselves in the early years were extremely volatile institutions. Insuch uncertain circumstances, ownership concentration is all the more important,as it allows interested owners to have significant influence over the firms undertheir jurisdictions. However, as the markets have matured in China, this type ofcontrol has become less of a necessity, and the importance of ownership concen-tration for firm performance is expected to drop off.

Limitations

This study has several limitations. First, the differences in the effects of classicalstate ownership and state institutional ownership on firm performance areevident in our data analyses, but some important issues are worthy of furtherexamination including, but not limited to, the different incentives facingSOAMCs and traditional state offices, the transformed and new institutionalmechanisms that ensure SOAMCs’ involvement to produce positive outcomes,and the institutional arrangements that shield SOAMCs from interference fromhigher state offices. Second, in this paper we have studied the ownership struc-ture of Chinese listed firms from 1994–2003, the first decade of China’s stockmarkets. Although this particular period offers us important evidence that helpsunderstand the success of these firms, future research must track down the mostrecent institutional and organizational changes to Chinese transformed SOEs.Specifically, the future will tell whether the gap between classical state ownershipand state institutional ownership will grow and in what ways. Finally, we realizethat how ownership concentration serves as a mechanism positively affecting firmperformance and governance is a complex issue. Although we have robust andconsistent results showing the positive effects of ownership concentration on firmperformance in China’s stock markets, our data do not allow an empirical test ofhow the mechanisms functioning in the Chinese context are different from thosein advanced economies where the conventional agency theory has been devel-oped. In-depth case studies may be necessary to disclose how ownership con-centration works in practice in different ownership types of firms, and perhapscomparative research will help reveal whether these institutional mechanismsfunctioning in the Chinese context are similar to or different from other worldregions.

Future Research Implications

Since the early 1990s, Chinese SOEs have been pushed to restructure their opera-tions in fundamental ways and changes in the ownership and control of these firmshave accelerated in the recent decade. Although it seems clear that China’s

24 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

corporate organizations have been experiencing a ‘managerial revolution’(Walder, 2011), some important issues remain unexplained and call for morecomprehensive and intensive research. The studies, including our own, haveoffered evidence indicating the dominant role of the state in China’s corporatesector, although the state’s ownership and control has changed in explicit andsometimes subtle ways (Guthrie, 2005; Li et al., forthcoming; Walder, 1995, 2011;Young, Peng, Ahlstrom, Bruton, & Jiang, 2008). Future research must look morecarefully at how much autonomy transformed state offices such as SOAMCs willenjoy and how extensively the state’s traditional ownership and its actual control offirms may wither away. Such research may enrich our knowledge of what patternsof ownership and control will come to characterize the Chinese corporate economyat the organizational level and contribute to our understanding of the nature ofChinese capitalism at a broader level (Fligstein & Zhang, 2011; Lin, 2011; Meyer,2011).

CONCLUSION

In this study, we have looked closely at the ownership of those state-owned firmsthat have been listed on the Shanghai and Shenzhen stock exchanges from 1994–2003. We find that while state-held shares of these Chinese firms have decreased,the real story concerns the emergence of SOAMCs, and what these organizationsmean for firm governance and, ultimately, for firm performance. We also find thepositive effects of ownership concentration in determining firm performanceduring the evolution of state ownership. We hope that this study contributes to thethriving literature on China’s corporate governance by calling for more compre-hensive and intensive research on the new patterns of ownership and control oftransformed SOEs.

NOTES

This paper has benefited from helpful comments and advice from many individuals. In addition tothe research seminars at Cambridge University, the Center for Advanced Study of the Social andBehavioral Sciences, INSEAD, Haas, Harvard Business School, the Hong Kong University ofScience and Technology, and the International Association of Chinese Management Research, wewould like to thank Bruce Kogut, David Greenberg, Neil Fligstein, Woody Powell, and MichaelSobel for comments on earlier drafts. In particular, we are grateful to Anne Tsui, Editor-in-Chief, andYanjie Bian, Senior Editor of Management and Organization Review, and three anonymous reviewers fortheir constructive comments and suggestions on earlier versions.

[1] There are obvious and famous exceptions here – SOEs like Baoshan Steel were still closelymonitored and supported by the state (Steinfeld, 1998). While important to the economy, thelargest SOEs are not representative of the economy as a whole. Thus, while many scholars viewthese SOEs as measures of the progress of China’s reforms, they are more accurately theexceptions that prove the rule.

[2] Under the planned economy, large state-owned factories generally reported directly to theministries [bu] (central government), provincial bureaus [ting], or municipal bureaus [ju] that

Ownership Concentration in Chinese SOEs 25

© 2011 The International Association for Chinese Management Research

govern a given sector (Guthrie, 1999). Over the course of the economic reforms, as the central,provincial, and municipal governments began to recede from direct control over factories in theirjurisdictions, factories in some sectors were placed into group companies, and coordinatedeconomic decision making as a coalition of organizations (Keister, 1998, 2000).

[3] For this table we start with 1998, because this is the first year that significant numbers ofSOAMCs became players in the economy. From 1994–1997, the percentage of shares held bySOMACs is basically zero.

[4] Interview with second author (Shanghai, 2005).[5] We have run the analyses by looking at the largest, third-, fifth-, and tenth-largest owners. For the

sake of parsimony, we simply report the results for the ownership concentration among the fivelargest owners, as the effects are the same across all of these groups – the results for models runwith the largest, third-, and tenth-largest owners are very similar to these, with some differencesin the magnitude of the effects but no differences in statistical significance.

[6] The difference between fixed and random effects models in these cases are that the fixed effectsmodels assume that there is an unknown constant differing across organizations and the esti-mators are transformed such that dependent variables, independent variables, and error termsequal the observed values minus the average values of the panel and are estimated within anOLS framework; random effects models assume that the unobserved effects are uncorrelatedwith Zi and ei and are estimated in a GLS framework (Hausman, 1978). In general, we assumethat there are unobservable firm-level effects – such as party involvement and level of owner-ship (Guthrie, 2005; Walder, 1995) – and because these effects are unobservable, our baselineassumption is that the fixed-effects models are the better models. The Hausman SpecificationTest (Hausman, 1978) supports this view. All of these results are available upon request fromthe first author.

[7] In Figure 1 we use the ownership concentration of the five largest shareholders from Table 4.However, the results look much the same across the models, albeit with gentler slopes for theconcentration of the largest and three largest owners. For Figure 2, we show the effects of alllevels of ownership concentration. All figures are based on full models. All other variables areconstrained at the means.

[8] An additional problem with our analysis is the potential issue of endogeneity. It could be thatcase ownership concentration has maintained strong associations with performance becausesuccessful SOAMCs have aggressively purchased shares of the best performing firms. The bestway to attempt to control for this is by lagging the independent variables, though the inter-pretation of these outcomes becomes complicated given the combination of the fixed effectswith variable lags. In any case, we did run the models with lagged independent variables andfound exactly the same results. Results are available upon request.

[9] Our analysis of the interlocking ownership of Chinese SOEs has shown that the small-worldstatistics (Kogut & Walker, 2001) of ownership of publicly-traded Chinese organizations aresimilar in magnitude to those found in the U.S.

REFERENCES

Amihud, Y., & Lev, B. 1999. Does corporate ownership structure affect its strategy towards diversi-fication? Strategic Management Journal, 20(11): 1063–1069.

Barro, R. J., & Sala-i-Martin, X. 1995. Economic growth. Cambridge, MA: MIT Press.Beamish, P. W., & Delios, A. 2005. Selling China: Looking back and looking forward. Management

and Organization Review, 1(2): 309–313.Blanchard, O., Boycko, M., Dabrowski, M., Dornbusch, R., Layard, R., & Shleifer, A.

1993. Postcommunist reform: Pain and progress. Cambridge, MA; London: MITPress.

Boardman, A. E., & Vining, A. R. 1989. Ownership and performance in competitive environments:A comparison of the performance of private, mixed, and state-owned enterprises. Journal ofLaw and Economics, 32: 1–33.

Boeker, W., & Goodstein, J. 1993. Performance and successor choice: The moderating effects ofgovernance and ownership. The Academy of Management Journal, 36(1): 172–186.

Burkart, M., Gromb, D., & Panunzi, F. 1997. Large shareholders, monitoring, and the value of thefirm. The Quarterly Journal of Economics, 112(3): 693–728.

26 J.-M. Wang et al.

© 2011 The International Association for Chinese Management Research

Burkart, M., Gromb, D., & Panunzi, F. 2000. Agency conflicts in public and negotiated transfers ofcorporate control. The Journal of Finance, 55(2): 647–677.

Cao, Y. Z., Fan, G., & Woo, W. T. 1997. Chinese economic reforms: Past successes and futurechallenges. In WT Woo, S Parker & J Sachs (Eds.), Economies in transition: ComparingAsia and Eastern Europe: 19–40. Cambridge, MA: MIT Press.

Che, J., & Qian, Y. 1998. Insecure property rights and government ownership of firms. TheQuarterly Journal of Economics, 113(2): 467–496.

Chen, K., Wang, H., Zheng, Y., Jefferson, G. H., & Rawski, T. G. 1988. Productivity change inChinese industry: 1953–1985. Journal of Comparative Economics, 12: 570–591.

China Securities Regulatory Commission. 2009. China securities and futures statistical year-book. Shanghai: Xuelin Publisher.

Fischer, S. 1992. Privatization in Eastern European transformation. In C. Clague & G. C. Rausser(Eds.), The emergence of market economies in Eastern Europe: 227–243. Cambridge,MA: Blackwell.

Fischer, S., & Gelb, A. 1991. The process of socialist economic transformation. Journal of Eco-nomic Perspectives, 4: 91–106.