Embed Size (px)

Citation preview

The Retirement ChallengeDilemmas and Decisions Through Every Decade

Contents

How Women in All of Life’s Stages Can Prepare for a Secure Retirement 3

In Her Twenties 4

In Her Thirties 5

In Her Forties 6

In Her Fifties 7

In Her Sixties 8

In Her Seventies and Beyond 9

The Retirement Challenge: Dilemmas and Decisions Through Every Decade 33

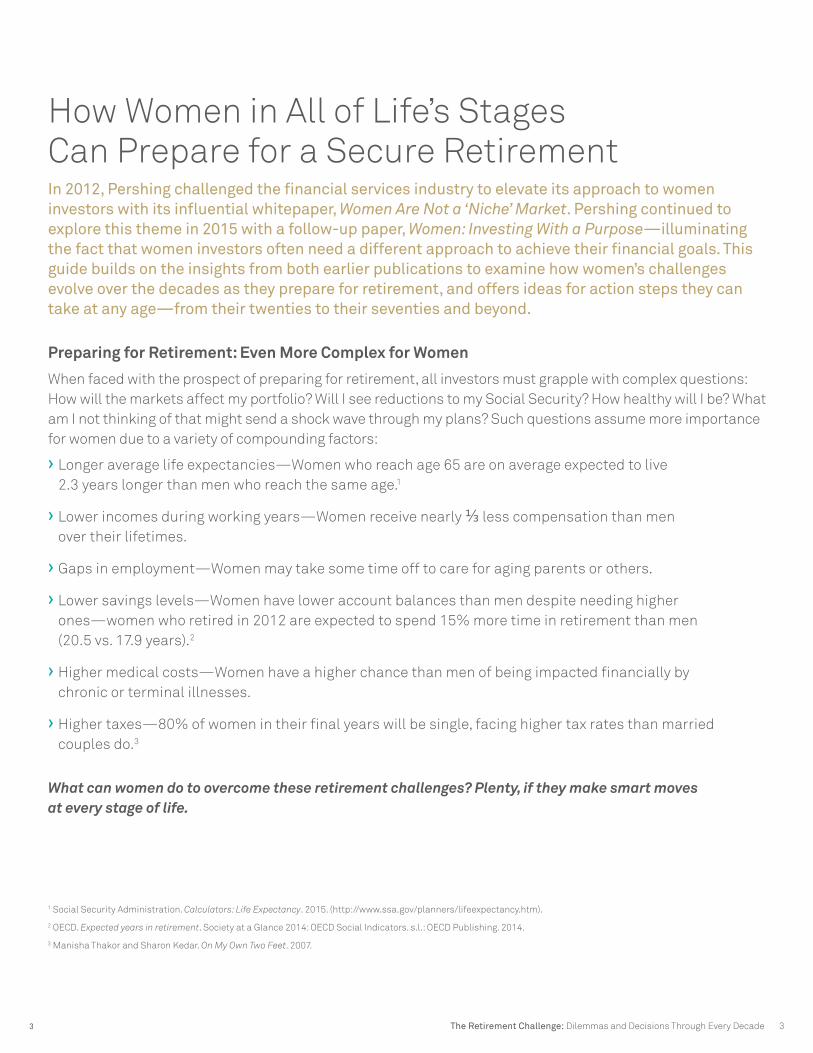

How Women in All of Life’s Stages Can Prepare for a Secure RetirementIn 2012, Pershing challenged the financial services industry to elevate its approach to women investors with its influential whitepaper, Women Are Not a ‘Niche’ Market. Pershing continued to explore this theme in 2015 with a follow-up paper, Women: Investing With a Purpose—illuminating the fact that women investors often need a different approach to achieve their financial goals. This guide builds on the insights from both earlier publications to examine how women’s challenges evolve over the decades as they prepare for retirement, and offers ideas for action steps they can take at any age—from their twenties to their seventies and beyond.

Preparing for Retirement: Even More Complex for Women

When faced with the prospect of preparing for retirement, all investors must grapple with complex questions: How will the markets affect my portfolio? Will I see reductions to my Social Security? How healthy will I be? What am I not thinking of that might send a shock wave through my plans? Such questions assume more importance for women due to a variety of compounding factors:

› Longer average life expectancies—Women who reach age 65 are on average expected to live 2.3 years longer than men who reach the same age.1

› Lower incomes during working years—Women receive nearly 1/3 less compensation than men over their lifetimes.

› Gaps in employment—Women may take some time off to care for aging parents or others.

› Lower savings levels—Women have lower account balances than men despite needing higher ones—women who retired in 2012 are expected to spend 15% more time in retirement than men (20.5 vs. 17.9 years).2

› Higher medical costs—Women have a higher chance than men of being impacted financially by chronic or terminal illnesses.

› Higher taxes—80% of women in their final years will be single, facing higher tax rates than married couples do.3

What can women do to overcome these retirement challenges? Plenty, if they make smart moves at every stage of life.

1 Social Security Administration. Calculators: Life Expectancy. 2015. (http://www.ssa.gov/planners/lifeexpectancy.htm).

2 OECD. Expected years in retirement. Society at a Glance 2014: OECD Social Indicators. s.l.: OECD Publishing. 2014.

3 Manisha Thakor and Sharon Kedar. On My Own Two Feet. 2007.

4

$0

$150,000

$100,000

$50,000

$200,000

$250,000

$300,000

$350,000

$450,000

$400,000

When You Start Saving Outweighs How Much You Save: Saving at 25 vs. 35

Emily

Age

Dave

25 30 35 40 45 50 55 60 65

Sav

ings

Source: “These 3 Charts Show The Amazing Power Of Compound Interest,” Business Insider, http://www.businessinsider.com/amazing-power-of-compound-interest-2014-7

In Her TwentiesLimitless possibilities. Countless uncertainties.For many women in their twenties, life may present more questions than answers. They may still be considering whether marriage or children are right for them. Their career options are often broad and earnings potential very hazy. They may not even be thinking about retirement, as they are focused on meeting current financial demands such as rent, college loan payments and transportation costs.

What’s on her mind?What are her overriding

financial considerations?What might she do to make

retirement a priority?

› Getting a good job

› Relationships and/or marriage

› Children—soon, later or never?

› Balancing career responsibilities with enjoying life

› Preparing a budget

› Making college loan payments

› Saving or paying for a home, car or wedding

› Trying to save money—simply for peace of mind

› Sketch out a clear plan for: paying current expenses, paying down debt through loan repayments, and saving for major purchases such as a wedding, home or car

› Start small—save a little every week in an interest-bearing account, for emergencies such as a lost job or surprising expense

› Take advantage of her company’s retirement plan, including any dollar match; if such a plan is not available, open an IRA and contribute to it monthly

The Retirement Challenge: Dilemmas and Decisions Through Every Decade 5

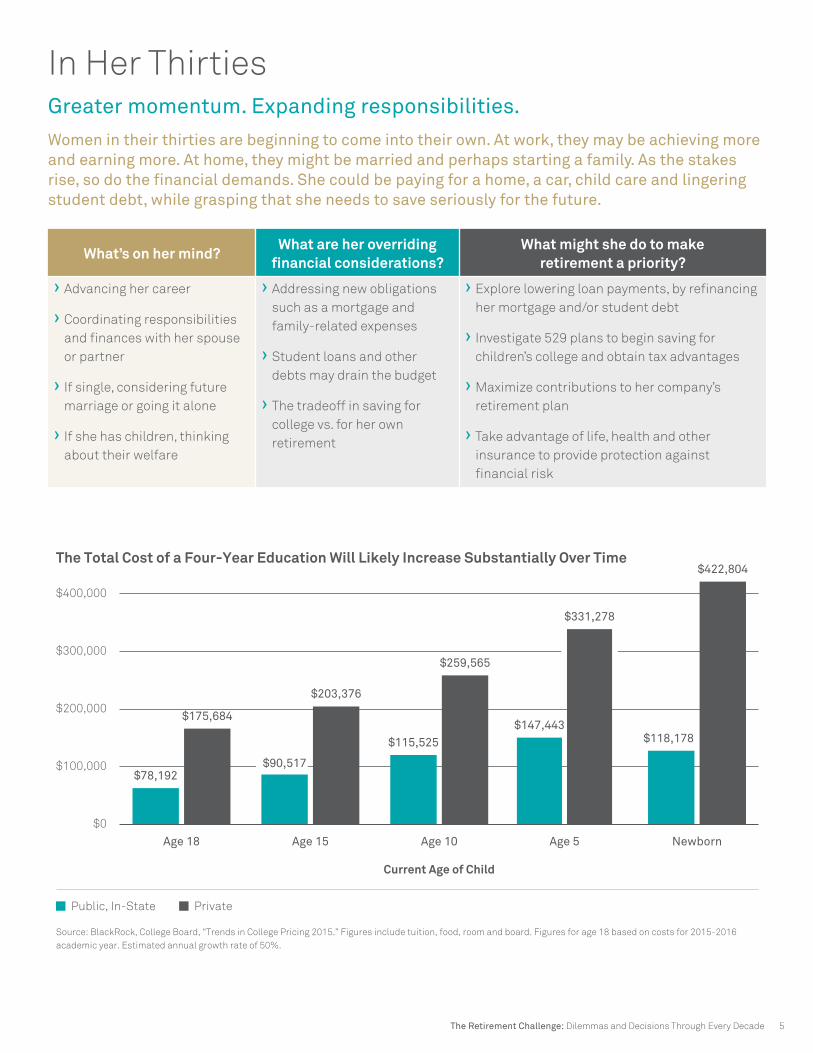

In Her ThirtiesGreater momentum. Expanding responsibilities.Women in their thirties are beginning to come into their own. At work, they may be achieving more and earning more. At home, they might be married and perhaps starting a family. As the stakes rise, so do the financial demands. She could be paying for a home, a car, child care and lingering student debt, while grasping that she needs to save seriously for the future.

What’s on her mind?What are her overriding

financial considerations?What might she do to make

retirement a priority?

› Advancing her career

› Coordinating responsibilities and finances with her spouse or partner

› If single, considering future marriage or going it alone

› If she has children, thinking about their welfare

› Addressing new obligations such as a mortgage and family-related expenses

› Student loans and other debts may drain the budget

› The tradeoff in saving for college vs. for her own retirement

› Explore lowering loan payments, by refinancing her mortgage and/or student debt

› Investigate 529 plans to begin saving for children’s college and obtain tax advantages

› Maximize contributions to her company’s retirement plan

› Take advantage of life, health and other insurance to provide protection against financial risk

$0

$200,000

$100,000

$300,000

$400,000

The Total Cost of a Four-Year Education Will Likely Increase Substantially Over Time

Current Age of Child

Age 18 Age 15 Age 10 Age 5 Newborn

Public, In-State Private

$78,192

$175,684

$115,525

$259,565

$147,443

$331,278

$118,178

$422,804

$90,517

Source: BlackRock, College Board, “Trends in College Pricing 2015.” Figures include tuition, food, room and board. Figures for age 18 based on costs for 2015-2016 academic year. Estimated annual growth rate of 50%.

$203,376

6

In Her FortiesBolder steps. Bigger challenges.By their forties, women typically have committed to specific life paths, whether pursuing a traditional career, starting a business, getting married or having children. They also may face big challenges: loss of career momentum by taking time off to raise children, divorce or taking care of elderly parents. They wonder how to meet near-term financial demands while carving out a measure of security in the future.

What’s on her mind?What are her overriding

financial considerations?What might she do to make

retirement a priority?

› Preserving career momentum, especially if she has taken time off to care for children or elders

› If married, finding ways to share financial responsibilities with her spouse

› If single or divorced, achieving security without feeling boxed in

› Determining what college costs she can afford as children grow up

› Managing credit card debt

› Whether to refinance her home or other loans

› Getting the best financial aid package for children’s college

› Whether her company retirement plan is the only savings strategy she should be focusing on

› Imagining how her financial picture would change if her marriage ended by divorce or premature death

› Aggressively pay off high-interest debt

› Calculate how lowering interest rates on mortgages and other loans might free up cash today and/or reduce interest costs

› Learn about the financial aid process and execute strategies that mitigate family contribution expectations

› Maximize retirement plan contributions and save more, if necessary

› Calculate personal net worth and income needs—independent of spouse’s financial contribution

› Revisit insurance needs for financial protection

The Retirement Challenge: Dilemmas and Decisions Through Every Decade 7

In Her FiftiesMaximizing income. Multiplying demands.Women in their fifties don’t have all the answers yet, but they know their own minds and how to make informed decisions—at home and at work. In or approaching their peak earning years, they may still feel a squeeze: assisting aging relatives or supporting recently graduated children who can’t find adequate jobs. With retirement quickly approaching, these women may feel that their savings aren’t building up nearly as much as they’d envisioned.

What’s on her mind?What are her overriding

financial considerations?What might she do to make

retirement a priority?

› Staying alert to workplace changes that could disrupt her employment situation

› If married, managing the time conflicts present if both spouses have careers

› If single or divorced, considering proactive career moves to avoid dead-end jobs or layoffs

› Emerging health complications may surface now for parents entering their later years

› Mounting credit card debt

› Uncertainty about being on track with retirement savings

› Worry that unforeseen health issues may force early retirement

› Weighing and prioritizing debt payoff options (mortgage, etc.)

› Concern that parents are not financially prepared for health and long term care costs

› Systematically pay off debt with highest interest rates

› Meet with financial advisor to clarify retirement scenarios: what she has, what she’ll need, and a path forward

› Determine if investment allocation needs to change if nearing retirement or withdrawing funds for other needs

› Get quotes on long-term care insurance, or life insurance with riders that can offset health care costs

› Evaluate the benefits of accelerating mortgage payments

› Continue to maximize retirement plan contributions

8

In Her SixtiesLife-changing decisions. Breathtaking opportunities.For many women, the sixties represent a decade of transformation. They may trade their careers for adventures ranging from travel, to charitable work, to launching long-imagined businesses. Parents may have passed away, and children may have married. The pace of change is brisk, and the financial decisions they must make are complex and highly important.

What’s on her mind?What are her overriding

financial considerations?What might she do to make

retirement a priority?

› Whether to retire or keep working

› If married, coming to agreement about plans, priorities and timing for retirement

› If single, widowed or divorced, how to protect against potential health issues or financial setbacks

› Whether to downsize locally, move closer to children (if she has them), or pursue an entirely new retirement living arrangement

› Not retiring so early that life-long income is uncertain, but also not so late that health problems limit her ability to enjoy retirement

› Social Security rule changes may reduce her anticipated benefit

› The specter of severe illness or burdensome long term care costs

› A desire to leave something behind—to children or charity

› Sign up for my Social Security account access (http://ssa.gov) to find out how much she can expect and determine when she should begin to receive her benefits

› Work with a financial advisor to discuss the pros and cons of retiring soon versus waiting until her late sixties or early seventies

› Purchase a long term care policy to address those potential costs

› Investigate new living options that might reduce monthly expenses

› Identify specific goals for a legacy, and consider gifts of real estate or valuables, or using investment assets to fund a trust

$0

$600

$300

$900

$1,500

$1,200

This example assumes a benefit of $1,000 at a full retirement age of 66

Monthly Benefit Amounts Differ Based on the Age You Decide toStart Receiving Benefits

Age You Choose to Start Receiving Benefits

Mon

thly

Ben

efit A

mou

nt

62 63 64 65 66 67 68 69 70

$750 $800$866 $933

$1,000

$1,160 $1,240$1,320

$1,080

Source: “When to Start Receiving Retirement Benefits,” Social Security Administration, August 2015. https://www.ssa.gov/pubs/EN-05-10147.pdf

The Retirement Challenge: Dilemmas and Decisions Through Every Decade 9

In Her Seventies and BeyondGreater momentum. Expanding responsibilities.By age 70, most—but certainly not all—women have retired from their careers. Those who continue working often do so to bolster retirement savings, or simply to stay engaged with people and the community. They may encounter a range of challenges—moving to a new home, losing a spouse, or dealing with health problems. But, the seventies and beyond are also a time of deep family involvement, personal exploration and thoughts of legacy.

What’s on her mind?What are her overriding

financial considerations?What might she do to make

retirement more secure?

› Spending her time involved in meaningful endeavors

› If married, concerned that she may outlive her spouse for many years

› If single, thinking about how to preserve her financial independence

› If she has children and grandchildren, wondering how to have the greatest impact on their lives

› Preserving her health and ability to go places

› Outliving her savings

› Rising costs of medical care and inflation taking a toll on her buying power

› Whether to devote any time to generating income, to provide an extra measure of security

› Deciding if leaving a legacy is important and, if so, taking the right steps

› Continue to keep part of her investment portfolio exposed to equities, to pursue growth and potentially offset inflation, or to leave to a legacy

› Determine whether her investments provide a consistent income stream and peace of mind

› If it makes sense to remain in her home, ensure that she can afford it and make appropriate financial decisions to maintain the property and meet other expenses

› If she is hoping to leave a legacy, establish the right vehicles and investments, such as trusts, charitable accounts or other options

65 76

Longer Life Expectancies and Rising Expenses

Male Life Expectancy1

1 Source: National Center for Health Statistics, National Vital Statistics Reports. Web:www.cdc.gov/nchs.2 Source: National Center for Health Statistics. Health, United States, 20133 Source: Statista Inc., 2015

1960 2010

71 81

Female Life Expectancy1

1960 2010

66 64

Average Retirement Age2

1960 2010

$147 $8,417

Health CareExpenditures per Capita3

1960 2010

10

Notes

The Retirement Challenge: Dilemmas and Decisions Through Every Decade 11

Notes

WE ARE PERSHING. WE ARE BNY MELLON.

Pershing, a BNY Mellon company, and its affiliates provide global financial business solutions to advisors, asset managers, broker-dealers, family offices, fund managers, registered investment advisor firms and wealth managers. A financial services market leader located in 23 offices worldwide, we are uniquely positioned to provide advisors and firms global insights into industry trends, regulatory changes and best practices, as well as shifts in investor sentiment and expectations. Pershing provides solutions—including innovative programs and business consulting—that help create a competitive advantage for our clients. Pershing LLC, member FINRA, NYSE, SIPC.

Important Legal Information

Please read these terms and conditions carefully. By continuing any further, you agree to be bound by the terms and conditions described below.

• This paper has been designed for informational purposes only. The services and information referenced are for investment professional use only and not intended for personal individual use. Pershing and its affiliates do not intend to provide investment advice through this guidebook and do not represent that the services discussed are suitable for any particular purpose. Pershing and its affiliates do not, and the information contained herein does not, intend to render tax or legal advice.

Warranty and limitation of liability

• The accuracy, completeness and timeliness of the information contained herein cannot be guaranteed. Pershing and its affiliates do not warranty, guarantee or make any representations, or make any implied or express warranty or assume any liability with regard to the use of the information contained herein.

• Pershing and its affiliates have no duty, responsibility or obligation to update or correct any information contained herein.

Copyrights and Trademarks

• Except as may be expressly authorized, all information contained in this guidebook may not be reproduced, transmitted, displayed, distributed, published or otherwise commercially exploited without the written consent of Pershing LLC.

©2016 Pershing LLC. Pershing LLC, member FINRA, NYSE, SIPC, is a wholly owned subsidiary of The Bank of New York Mellon Corporation (BNY Mellon).

Trademark(s) belong to their respective owners. For professional use only. Not for distribution to the public.

One Pershing Plaza, Jersey City, NJ 07399GB-PER-IWD-2-16

pershing.com