Embed Size (px)

Citation preview

Journal of Intellectual Disability Research

pp

–

©

Blackwell Publishing Ltd

210

Blackwell Science, LtdOxford, UKJIRJournal of Intellectual Disability Research

-

Blackwell Publishing Ltd,

3210217

Original Article

Factors affecting financial decision-making abilitiesW. M. I. Suto

et al.

Correspondence: Dr Irenka Suto, Department of Psychiatry (Section of Developmental Psychiatry), University of Cambridge, Douglas House,

b Trumpington Road, Cambridge, CB

AH, UK (e-mail: wmis

@cam.ac.uk).

The relationships among three factors affecting the financial decision-making abilities of adults with mild intellectual disabilities

W. M. I. Suto,

1

I. C. H. Clare,

1

A. J. Holland

1

& P. C. Watson

2

1

Department of Psychiatry (Section of Developmental Psychiatry), University of Cambridge, UK

2

MRC Cognition and Brain Sciences Unit, Cambridge, UK

Abstract

Background

Among adults with intellectual disabil-ities (IDs), there is a need not only to assess financial decision-making capacity, but also to understand how it can be maximized. Although increased finan-cial independence is a goal for many people, it is essential that individuals’ decision-making abilities are sufficient, and many factors may affect the devel-opment of such abilities.

Method

As part of a wider project on financial decision-making, we analysed previous data from a group of

adults with mild IDs, identifying corre-lations among four variables: (i) financial decision-making abilities; (ii) intellectual ability; (iii) under-standing of some basic concepts relevant to finance; and (iv) decision-making opportunities in everyday life.

Results

The analysis indicated a direct relationship between ID and basic financial understanding. Strong relationships of a potentially reciprocal nature

were identified between basic financial understanding and everyday decision-making opportunities, and between such opportunities and financial decision-making abilities.

Conclusions

The findings suggest that the role of intellectual ability in determining financial decision-making abilities is only indirect, and that access to both basic skills education and everyday decision-making opportunities is crucial for maximizing capacity. The implications of this are discussed.

Keywords

capacity, choice, decision-making, financial affairs

Introduction

Issues surrounding self-determination are salient at present (Ashbaugh

; McComb

) and include those relating to the capacity of adults with intellectual disabilities (IDs) to manage their own finances. However, while the definition and assess-ment of capacity have received much attention [e.g. Law Commission (England & Wales)

;

Adults with Incapacity (Scotland) Act

; Suto

et al.

; Department for Constitutional Affairs

,

; Grisso

; British Medical Association & The Law

Journal of Intellectual Disability Research

W. M. I. Suto

et al

. •

Factors affecting financial decision-making abilities211

©

Blackwell Publishing Ltd,

Journal of Intellectual Disability Research

,

–

Society

], much less consideration has been given to finding ways in which capacity might be maximized. The widely accepted ‘functional’ approach to assessing capacity entails establishing the extent to which an individual’s financial decision-making abilities meet the demands of his or her per-sonal financial circumstances (Wong

et al.

; Brit-ish Medical Association & The Law Society

). It follows that capacity may be increased either through reducing situational demands, or through enhancing decision-making abilities (Grisso & Appelbaum

; Murphy & Clare

). In this paper, the second of these possibilities is considered, in an investigation of the relationships among three factors that contribute to the acquisition of financial decision-making abilities.

The factor analysis reported here forms part of a wider project about financial decision-making among adults with mild IDs (Suto

). It brings together the findings of earlier stages of the project, in which financial decision-making abilities were assessed among

individuals, in addition to the following three factors: (i) intellectual ability; (ii) decision-making opportunities in everyday life; and (iii) under-standing of some basic concepts relevant to finance. Table

summarizes the measures used to assess these four variables.

All three of the factors measured were found to correlate reasonably well with financial decision-making abilities (Suto

; Suto

et al.

,

). The broadness of these correlations allows for sev-eral hypotheses about interactions among the fac-

tors to be explored. Frameworks of ‘social disablement’ similar to Wing’s (

) conceptualiza-tion of the nature of difficulties experienced by peo-ple with a ‘mental illness’, may be applied to adults with mild learning disabilities (Murphy & Clare

). Wing’s (

) framework comprises three interacting components: primary impairments, social disadvantages, and adverse self-attitude. Using such a framework, it can be hypothesized that primary impairments in intellectual ability contrib-ute to weak understanding of basic financial con-cepts; the limited learning, memory, reasoning, attention, language development and communica-tion skills that are associated with such impairments (Murphy & Clare

) could directly constrain the acquisition of such understanding in everyday life. Furthermore, an individual’s levels of these skills, and of the social functioning to which they contrib-ute, could also determine the types of formal educa-tion received, through which such understanding may develop.

A further hypothesis is that, in turn, weak financial understanding could limit an individual’s decision-making opportunities in everyday life. Health and social care professionals and other carers may be very protective of adults with IDs, associating weak under-standing with vulnerability to abuse and exploitation. Within a ‘social disablement’ framework (Wing

; Murphy & Clare

), a lifestyle limited in this way can be regarded as a social disadvantage of having IDs, because decision-making opportunities have come to be regarded as an essential component of

Table 1

Measures used in the project on financial decision-making among adults with intellectual disabilities

Variable Measure used

Financial decision-making abilities

Novel methodology comprising five vignettes, each portraying a fictitious financial decision.The five decisions increase in complexity, ranging from choosing between items in a supermarket,

to deciding whether to sell some shares. Each vignette is followed by a semi-structured interview, in which five decision-making abilities are considered: identification, understanding, reasoning, appreciation, and communication (for further details, see Suto

et al.

2005).Intellectual ability Wechsler Abbreviated Scale of Intelligence (WASI, The Psychological Corporation 1999)Decision-making

opportunities in everyday life

Choice Questionnaire: self-report version (Stancliffe & Parmenter 1999)

Understanding of basic financial concepts: quantity, numbers and money

Novel methodology involving spotted and numbered cards, money, and a scale of ‘more and less’.Participants are required to order sets of items along the scale, as well as recognize and recall their

values.

Journal of Intellectual Disability Research

W. M. I. Suto

et al

. •

Factors affecting financial decision-making abilities212

©

Blackwell Publishing Ltd,

Journal of Intellectual Disability Research

,

–

‘quality of life’ models and constructs (Hughes

et al.

; Wehmeyer

).Because learning and practice effects are well

established throughout most areas of psychology (Eysenck & Keane

), it may be further hypoth-esized that the relationship between these two factors may be reciprocal, with decision-making opportuni-ties also impacting positively upon the acquisition of financial understanding. Indeed, there is empirical evidence to suggest that this occurs among typically developing children (Berti & Bombi

; Nunes

et al.

). Similarly it seems reasonable to hypoth-esize a potentially reciprocal relationship between decision-making opportunities and financial decision-making abilities.

Because the data collected in the present project are not of a longitudinal nature, the causal directions of any relationships existing among the four mea-sured variables cannot be confirmed here through statistical analysis. However, by examining the rela-tive strengths of the correlations among the variables, the major direct relationships can be identified and compared with those hypothesized using a ‘social dis-ablement’ model. These were the aims of the follow-ing statistical analysis.

Method

Participants

The data analysed here were collected from

paid participants with IDs. This group comprised

men and

women (mean age

=

.

years; SD

=

.

years) who were recruited through the local service providing specialist health and/or social care for people with IDs; the group had a mean FSIQ of

.

(SD

=

.

). A number of further selection criteria were used: all participants were aged

–

, had the expressive language ability to answer simply phrased questions, were native English speak-ers, and did not have dementia or an active ‘mental illness’.

Statistical techniques and data

The data were analysed using SPSS for Windows Version

.

(SPSS Version

.

for Windows

) statistical software. For each of the four variables assessed, the measure used (see Table

) gave rise to ordinal data. Each measure comprised several differ-

ent sections and subtests, all of which gave rise to numerical scores for participants. These scores were summed together to give an overall score on each measure for each participant. It is these overall scores that were used in the present analysis. As most of the data were not normally distributed, only nonpara-metric statistical techniques were used. All correla-tions were calculated using the Kendall

T

, because (unlike with the Spearman

r

s

) first order partial cor-relation coefficients can be derived from standard bivariate correlation coefficients (Siegel & Castellan

). There are no established methods of calculat-ing higher order partial correlation coefficients for nonparametric data.

Path analysis

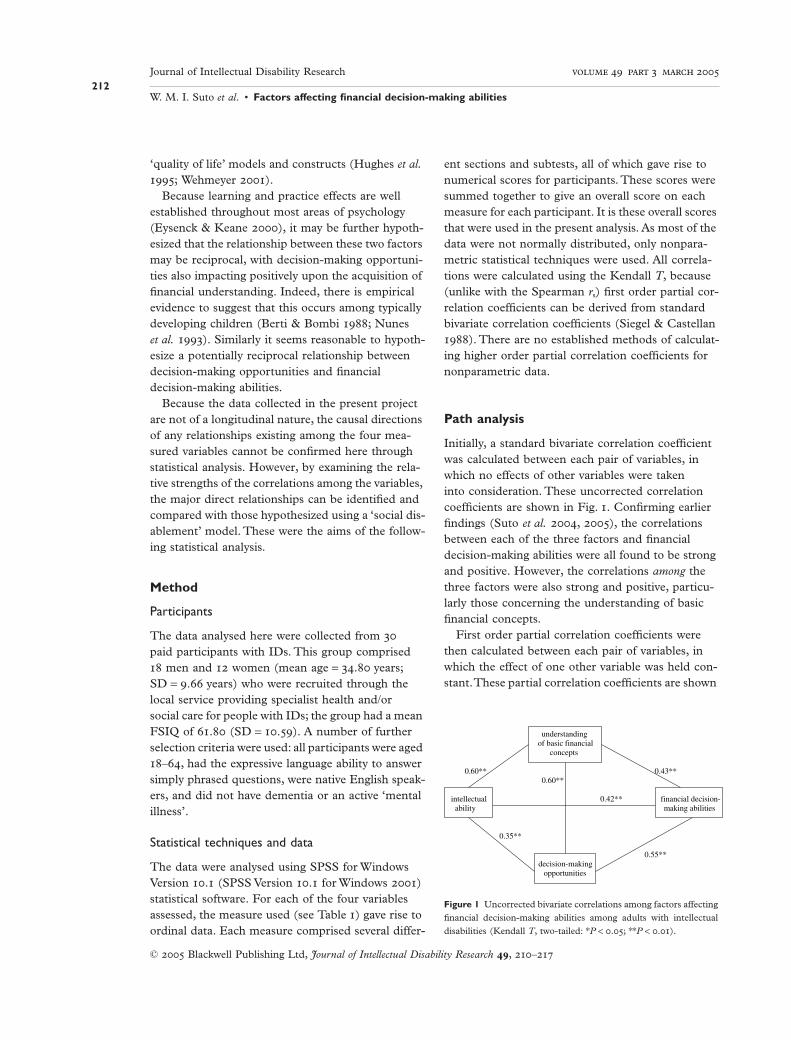

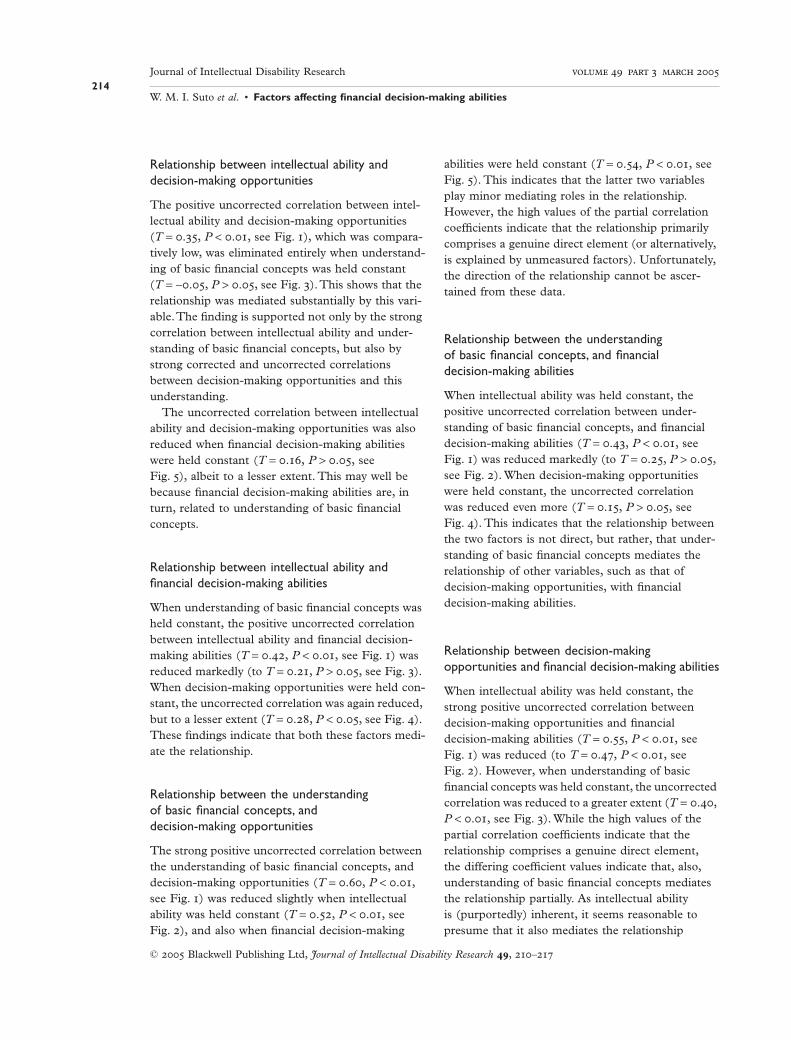

Initially, a standard bivariate correlation coefficient was calculated between each pair of variables, in which no effects of other variables were taken into consideration. These uncorrected correlation coefficients are shown in Fig.

. Confirming earlier findings (Suto

et al.

,

), the correlations between each of the three factors and financial decision-making abilities were all found to be strong and positive. However, the correlations

among

the three factors were also strong and positive, particu-larly those concerning the understanding of basic financial concepts.

First order partial correlation coefficients were then calculated between each pair of variables, in which the effect of one other variable was held con-stant. These partial correlation coefficients are shown

Figure 1

Uncorrected bivariate correlations among factors affectingfinancial decision-making abilities among adults with intellectualdisabilities (Kendall

T

, two-tailed:

*

P

<

.

;

**

P

<

.).

understanding of basic financial

concepts

0.60** 0.43** 0.60**

intellectual 0.42** financial decision- ability making abilities

0.35**

0.55**decision-making

opportunities

Journal of Intellectual Disability Research

W. M. I. Suto et al. • Factors affecting financial decision-making abilities213

© Blackwell Publishing Ltd, Journal of Intellectual Disability Research , –

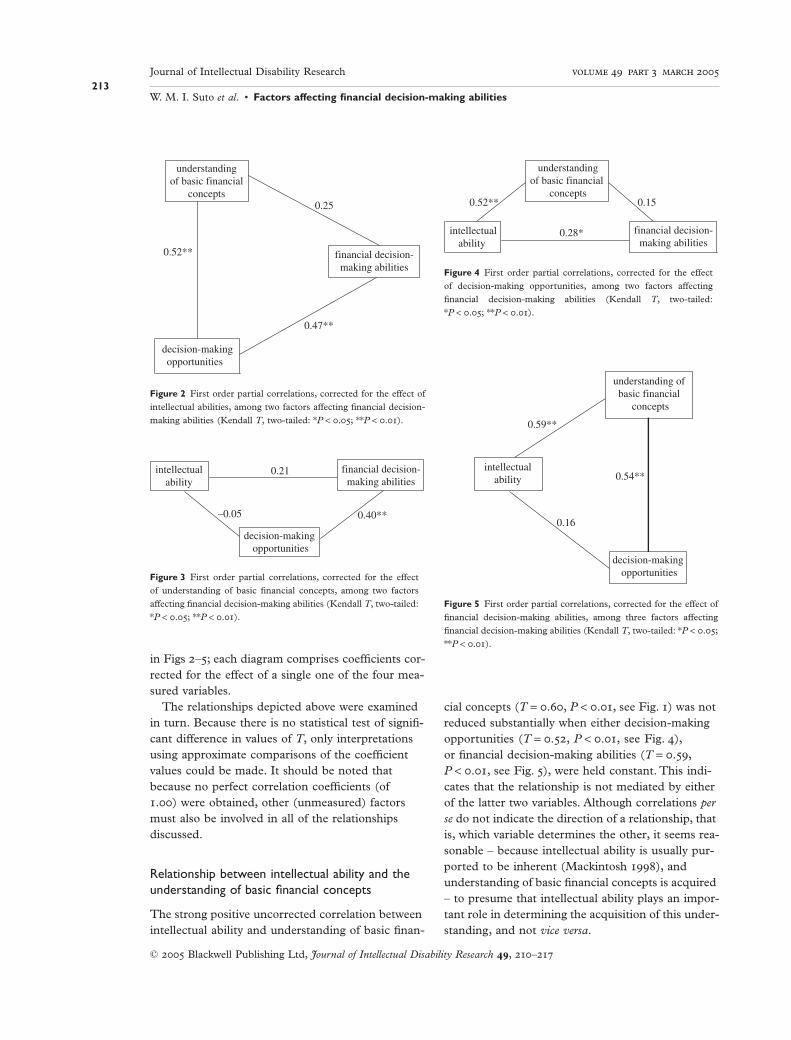

in Figs –; each diagram comprises coefficients cor-rected for the effect of a single one of the four mea-sured variables.

The relationships depicted above were examined in turn. Because there is no statistical test of signifi-cant difference in values of T, only interpretations using approximate comparisons of the coefficient values could be made. It should be noted that because no perfect correlation coefficients (of .) were obtained, other (unmeasured) factors must also be involved in all of the relationships discussed.

Relationship between intellectual ability and the understanding of basic financial concepts

The strong positive uncorrected correlation between intellectual ability and understanding of basic finan-

cial concepts (T = ., P < ., see Fig. ) was not reduced substantially when either decision-making opportunities (T = ., P < ., see Fig. ), or financial decision-making abilities (T = ., P < ., see Fig. ), were held constant. This indi-cates that the relationship is not mediated by either of the latter two variables. Although correlations per se do not indicate the direction of a relationship, that is, which variable determines the other, it seems rea-sonable – because intellectual ability is usually pur-ported to be inherent (Mackintosh ), and understanding of basic financial concepts is acquired – to presume that intellectual ability plays an impor-tant role in determining the acquisition of this under-standing, and not vice versa.

Figure 2 First order partial correlations, corrected for the effect ofintellectual abilities, among two factors affecting financial decision-making abilities (Kendall T, two-tailed: *P < .; **P < .).

understandingof basic financial

concepts 0.25

0.52** financial decision-making abilities

0.47**

decision-makingopportunities

Figure 3 First order partial correlations, corrected for the effectof understanding of basic financial concepts, among two factorsaffecting financial decision-making abilities (Kendall T, two-tailed:*P < .; **P < .).

intellectual ability

0.21 financial decision-making abilities

–0.05 0.40**

decision-making opportunities

Figure 4 First order partial correlations, corrected for the effectof decision-making opportunities, among two factors affectingfinancial decision-making abilities (Kendall T, two-tailed:*P < .; **P < .).

understandingof basic financial

concepts0.52** 0.15

intellectualability

0.28* financial decision-making abilities

Figure 5 First order partial correlations, corrected for the effect offinancial decision-making abilities, among three factors affectingfinancial decision-making abilities (Kendall T, two-tailed: *P < .;**P < .).

understanding of basic financial

concepts

0.59**

intellectual ability 0.54**

0.16

decision-making opportunities

Journal of Intellectual Disability Research

W. M. I. Suto et al. • Factors affecting financial decision-making abilities214

© Blackwell Publishing Ltd, Journal of Intellectual Disability Research , –

Relationship between intellectual ability and decision-making opportunities

The positive uncorrected correlation between intel-lectual ability and decision-making opportunities (T = ., P < ., see Fig. ), which was compara-tively low, was eliminated entirely when understand-ing of basic financial concepts was held constant (T = -., P > ., see Fig. ). This shows that the relationship was mediated substantially by this vari-able. The finding is supported not only by the strong correlation between intellectual ability and under-standing of basic financial concepts, but also by strong corrected and uncorrected correlations between decision-making opportunities and this understanding.

The uncorrected correlation between intellectual ability and decision-making opportunities was also reduced when financial decision-making abilities were held constant (T = ., P > ., see Fig. ), albeit to a lesser extent. This may well be because financial decision-making abilities are, in turn, related to understanding of basic financial concepts.

Relationship between intellectual ability and financial decision-making abilities

When understanding of basic financial concepts was held constant, the positive uncorrected correlation between intellectual ability and financial decision-making abilities (T = ., P < ., see Fig. ) was reduced markedly (to T = ., P > ., see Fig. ). When decision-making opportunities were held con-stant, the uncorrected correlation was again reduced, but to a lesser extent (T = ., P < ., see Fig. ). These findings indicate that both these factors medi-ate the relationship.

Relationship between the understanding of basic financial concepts, and decision-making opportunities

The strong positive uncorrected correlation between the understanding of basic financial concepts, and decision-making opportunities (T = ., P < ., see Fig. ) was reduced slightly when intellectual ability was held constant (T = ., P < ., see Fig. ), and also when financial decision-making

abilities were held constant (T = ., P < ., see Fig. ). This indicates that the latter two variables play minor mediating roles in the relationship. However, the high values of the partial correlation coefficients indicate that the relationship primarily comprises a genuine direct element (or alternatively, is explained by unmeasured factors). Unfortunately, the direction of the relationship cannot be ascer-tained from these data.

Relationship between the understandingof basic financial concepts, and financial decision-making abilities

When intellectual ability was held constant, the positive uncorrected correlation between under-standing of basic financial concepts, and financial decision-making abilities (T = ., P < ., see Fig. ) was reduced markedly (to T = ., P > ., see Fig. ). When decision-making opportunities were held constant, the uncorrected correlation was reduced even more (T = ., P > ., see Fig. ). This indicates that the relationship between the two factors is not direct, but rather, that under-standing of basic financial concepts mediates the relationship of other variables, such as that of decision-making opportunities, with financial decision-making abilities.

Relationship between decision-making opportunities and financial decision-making abilities

When intellectual ability was held constant, the strong positive uncorrected correlation between decision-making opportunities and financial decision-making abilities (T = ., P < ., see Fig. ) was reduced (to T = ., P < ., see Fig. ). However, when understanding of basic financial concepts was held constant, the uncorrected correlation was reduced to a greater extent (T = ., P < ., see Fig. ). While the high values of the partial correlation coefficients indicate that the relationship comprises a genuine direct element, the differing coefficient values indicate that, also, understanding of basic financial concepts mediates the relationship partially. As intellectual ability is (purportedly) inherent, it seems reasonable to presume that it also mediates the relationship

Journal of Intellectual Disability Research

W. M. I. Suto et al. • Factors affecting financial decision-making abilities215

© Blackwell Publishing Ltd, Journal of Intellectual Disability Research , –

because, in turn, it determines the acquisition of such understanding.

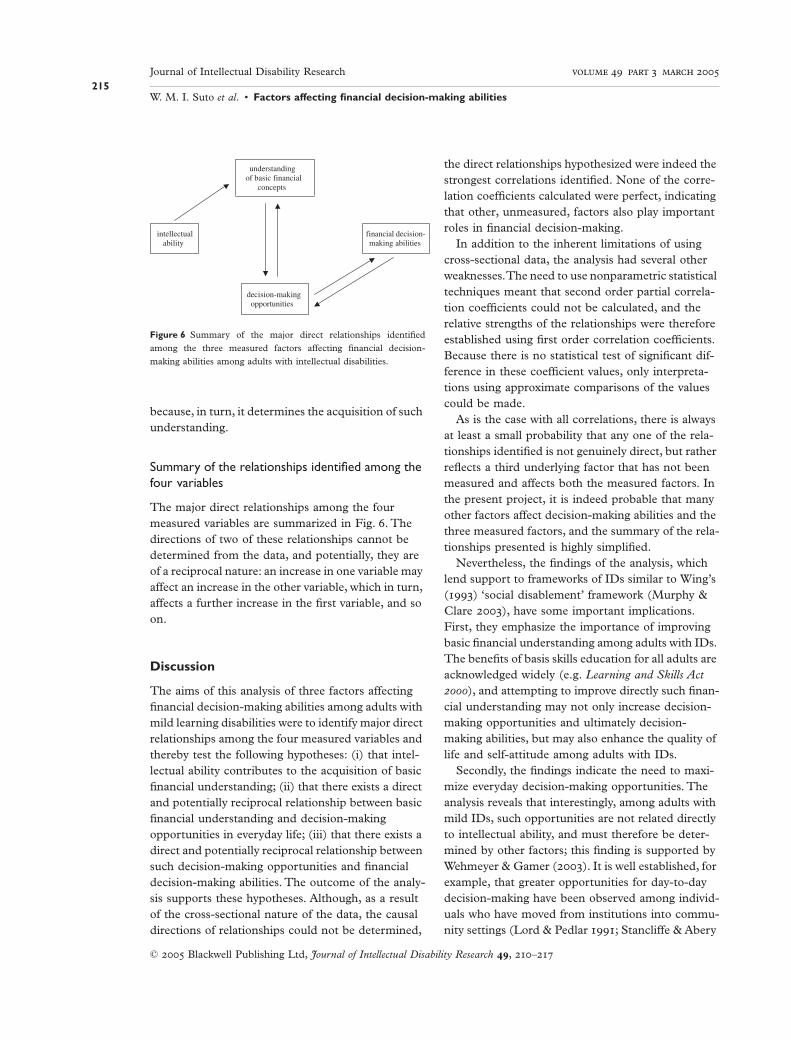

Summary of the relationships identified among the four variables

The major direct relationships among the four measured variables are summarized in Fig. . The directions of two of these relationships cannot be determined from the data, and potentially, they are of a reciprocal nature: an increase in one variable may affect an increase in the other variable, which in turn, affects a further increase in the first variable, and so on.

Discussion

The aims of this analysis of three factors affecting financial decision-making abilities among adults with mild learning disabilities were to identify major direct relationships among the four measured variables and thereby test the following hypotheses: (i) that intel-lectual ability contributes to the acquisition of basic financial understanding; (ii) that there exists a direct and potentially reciprocal relationship between basic financial understanding and decision-making opportunities in everyday life; (iii) that there exists a direct and potentially reciprocal relationship between such decision-making opportunities and financial decision-making abilities. The outcome of the analy-sis supports these hypotheses. Although, as a result of the cross-sectional nature of the data, the causal directions of relationships could not be determined,

the direct relationships hypothesized were indeed the strongest correlations identified. None of the corre-lation coefficients calculated were perfect, indicating that other, unmeasured, factors also play important roles in financial decision-making.

In addition to the inherent limitations of using cross-sectional data, the analysis had several other weaknesses. The need to use nonparametric statistical techniques meant that second order partial correla-tion coefficients could not be calculated, and the relative strengths of the relationships were therefore established using first order correlation coefficients. Because there is no statistical test of significant dif-ference in these coefficient values, only interpreta-tions using approximate comparisons of the values could be made.

As is the case with all correlations, there is always at least a small probability that any one of the rela-tionships identified is not genuinely direct, but rather reflects a third underlying factor that has not been measured and affects both the measured factors. In the present project, it is indeed probable that many other factors affect decision-making abilities and the three measured factors, and the summary of the rela-tionships presented is highly simplified.

Nevertheless, the findings of the analysis, which lend support to frameworks of IDs similar to Wing’s () ‘social disablement’ framework (Murphy & Clare ), have some important implications. First, they emphasize the importance of improving basic financial understanding among adults with IDs. The benefits of basis skills education for all adults are acknowledged widely (e.g. Learning and Skills Act ), and attempting to improve directly such finan-cial understanding may not only increase decision-making opportunities and ultimately decision-making abilities, but may also enhance the quality of life and self-attitude among adults with IDs.

Secondly, the findings indicate the need to maxi-mize everyday decision-making opportunities. The analysis reveals that interestingly, among adults with mild IDs, such opportunities are not related directly to intellectual ability, and must therefore be deter-mined by other factors; this finding is supported by Wehmeyer & Gamer (). It is well established, for example, that greater opportunities for day-to-day decision-making have been observed among individ-uals who have moved from institutions into commu-nity settings (Lord & Pedlar ; Stancliffe & Abery

Figure 6 Summary of the major direct relationships identifiedamong the three measured factors affecting financial decision-making abilities among adults with intellectual disabilities.

understanding of basic financial

concepts

intellectual financial decision- ability making abilities

decision-making opportunities

Journal of Intellectual Disability Research

W. M. I. Suto et al. • Factors affecting financial decision-making abilities216

© Blackwell Publishing Ltd, Journal of Intellectual Disability Research , –

; Apgar et al. ), and in particular, into smaller and more individualized residences (Emerson & Hatton ; Stancliffe , ; Wehmeyer & Bolding ; Stancliffe et al. ). According to Stalker & Harris (), service-providers, at all lev-els, play a crucial role in facilitating or inhibiting the exercise of choice. Arguably, they therefore play a similarly crucial role in the development of financial decision-making abilities and, ultimately, in enhanc-ing capacity.

At the highest of these levels of service-providers, the UK Government has set out some proposals for improving the lives of people with IDs and their fam-ilies and carers in England in its White Paper Valuing People (Department of Health ), and many of these proposals are centred about the principles of choice and independence. In this White Paper, the Government has expressed a commitment to increas-ing some decision-making opportunities among adults with IDs.

In addition to these developments in social policy and practice, there is a need for further research into financial decision-making among adults with learning disabilities. The three factors considered here are likely to interact with many others, and in particular, there may be a danger of overlooking the effects of social and emotional factors on both the development of decision-making abilities and the demands of decision-making situations. There are many ways of maximizing capacity and thereby improving the autonomy of adults with IDs, and all should be given serious consideration.

Acknowledgements

The study reported in this paper was carried out by Dr Irenka Suto as part of a project on the manage-ment of financial affairs by people with IDs, and funded initially by a Postgraduate Scholarship from the Nightingale Trust of Trinity Hall, Cambridge. Further development of the project was funded by the Nuffield Foundation and then by the Health Foundation. We are grateful to the Nightingale Trust, the Nuffield Foundation, and the Health Foundation for their generous support. We would also like to thank all the men and women who participated and without whose support the study would not have been possible.

References

Adults with Incapacity (Scotland) Act () The Stationery Office, London.

Apgar D. H., Cook S. & Lerman P. () Life after Johnstone: Impacts on Consumer Competencies, Behaviors, and Quality of Life. New Jersey Institute of Technology, Developmental Disabilities Planning Institute, Newark, NJ.

Ashbaugh J. W. () Down the garden path of self-deter-mination. Mental Retardation , –.

Berti A. E. & Bombi A. S. () The Child’s Construction of Economics. Cambridge University Press, Cambridge.

British Medical Association & The Law Society () Assessment of Mental Capacity: Guidance for Doctors and Lawyers, nd edn. British Medical Association, London.

Department for Constitutional Affairs () Draft Mental Incapacity Bill. HMSO, London.

Department for Constitutional Affairs () Draft Mental Capacity Bill. The Stationery Office, London.

Department of Health () Valuing People: A New Strategy for Learning Disability for the st Century. Department of Health, London.

Emerson E. & Hatton C. () Deinstitutionalization in the UK and Ireland: outcomes for service users. Journal of Intellectual and Developmental Disabilities , –.

Eysenck M. W. & Keane M. T. () Cognitive Psychology: A Student’s Handbook, th edn. Psychology Press, Phila-delphia, PA.

Grisso T. () Evaluating Competencies: Forensic Assess-ments and Instruments, nd edn. Plenum Publishers, New York.

Grisso T. & Appelbaum P. S. () Assessing Competence to Consent to Treatment: A Guide for Physicians and Other Health Professionals. Oxford University Press, Oxford.

Hughes C., Hwang B., Kim J., Eisenman L. T. & Killian D. J. () Quality of life in applied research: a review and analysis of empirical measures. American Journal on Mental Retardation , –.

Law Commission () Mental Incapacity. Law Commis-sion Report no. , HMSO, London.

Learning and Skills Act () The Stationery Office, London.

Lord J. & Pedlar A. () Life in the community: four years after the closure of an institution. Mental Retardation , –.

Mackintosh N. J. () IQ and Human Intelligence. Oxford University Press, Oxford.

McComb D. () If not self-determination, then what? Mental Retardation , –.

Murphy G. H. & Clare I. C. H. () Adults’ capacity to make legal decisions. In: Handbook of Psychology in Legal

Journal of Intellectual Disability Research

W. M. I. Suto et al. • Factors affecting financial decision-making abilities217

© Blackwell Publishing Ltd, Journal of Intellectual Disability Research , –

Contexts (eds D. C. Carson & R. H. C. Bull), nd edn, pp. –. John Wiley & Sons, Chichester.

Nunes T., Schliemann A. D. & Carraher D. W. () Street Mathematics and School Mathematics. Cambridge University Press, Cambridge.

Siegel S. & Castellan N. J. () Nonparametric Statistics for the Behavioral Sciences, nd edn. McGraw-Hill Co, New York.

SPSS Version . for Windows () SPSS Inc., Chicago.

Stalker K. & Harris P. () The exercise of choice by adults with intellectual disabilities: a literature review. Journal of Applied Research in Intellectual Disabilities , –.

Stancliffe R. () Community living-unit size, staff pres-ence, and residents’ choice-making. Mental Retardation , –.

Stancliffe R. () Living with support in the community: predictors of choice and self-determination. Mental Retar-dation and Developmental Disabilities Research Reviews , –.

Stancliffe R. J. & Abery B. () Longitudinal study of deinstitutionalization and exercise of choice. Mental Retardation , –.

Stancliffe R. J., Abery B. & Smith J. () Personal control and the ecology of community living settings: beyond living-unit size and type. American Journal on Mental Retardation , –.

Stancliffe R. J. & Parmenter T. R. () The ‘Choice Questionnaire’: a scale to assess choices exercised by adults with intellectual disability. Journal of Intellectual and Developmental Disability , –.

Suto W. M. I. () Psychological constructs of financial decision-making capacity: Implications for adults with learning disabilities. PhD Thesis, University of Cambridge.

Suto W. M. I., Clare I. C. H. & Holland A. J. () Substitute decision-making in England and Wales: a study of the Court of Protection. Journal of Social Welfare and Family Law , –.

Suto W. M. I., Clare I. C. H. & Holland A. J. () Managing money: the path to independent choice-making. Living WELL.

Suto W. M. I., Clare I. C. H., Holland A. J. & Watson P. C. () Capacity to make financial decisions among people with mild intellectual disabilities. Journal of Intel-lectual Disability Research , –.

The Psychological Corporation () Wechsler Abbreviated Scale of Intelligence. The Psychological Corporation, San Antonio.

Wehmeyer M. W. () Self-determination and mental retardation. International Review of Research in Mental Retardation , –.

Wehmeyer M. W. & Bolding N. () Self-determination across living and working environments: a matched-samples study of adults with mental retardation. Mental Retardation , –.

Wehmeyer M. W. & Gamer N. L. () The impact of personal characteristics of people with intellectual and developmental disability on self-determination and autonomous functioning. Journal of Applied Research in Intellectual Disabilities , –.

Wing J. () Social consequences of severe and persistent psychiatric disorders. In: Principles of Social Psychiatry (eds D. Bhugra & J. Leff), pp. –. Blackwell Scien-tific Publications, Oxford.

Wong J. G., Clare I. C. H., Gunn M. J. & Holland A. J. () Capacity to make health care decisions: its impor-tance in clinical practice. Psychological Medicine , –.

Accepted May