Embed Size (px)

Citation preview

THE RELATIONSHIP BETWEEN REAL EFFECTIVE

FINANCIAL EXCHANGE RATE (REFER) AND

CAPITAL FLOWS: IN THE CASE OF THAILAND

BY

MS. THIPSUDA SUKDAM

ANINDEPENDENT STUDYSUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR

THE DEGREE OF MASTER OF SCIENCE

PROGRAM IN FINANCE (INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2014

COPYRIGHT OF THAMMASAT UNIVERSITY

THE RELATIONSHIP BETWEEN REAL EFFECTIVE

FINANCIAL EXCHANGE RATE (REFER) AND

CAPITAL FLOWS: IN THE CASE OF THAILAND

BY

MS. THIPSUDA SUKDAM

ANINDEPENDENT STUDYSUBMITTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR

THE DEGREE OF MASTER OF SCIENCE

PROGRAM IN FINANCE (INTERNATIONAL PROGRAM)

FACULTY OF COMMERCE AND ACCOUNTANCY

THAMMASAT UNIVERSITY

ACADEMIC YEAR 2014

COPYRIGHT OF THAMMASAT UNIVERSITY

(1)

Independent Study Title THE RELATIONSHIP BETWEEN REAL

EFFECTIVE FINANCIAL EXCHANGE RATE

(REFER) AND CAPITAL FLOWS: IN THE

CASE OF THAILAND

Author Ms. Thipsuda Sukdam

Degree Master of Science (Finance)

Major Field/Faculty/University Master of Science Program in Finance

(International Program)

Faculty of Commerce and Accountancy

Thammasat University

Independent Study Advisor Assistant Professor Suluck Pattarathammas, DBA.

Academic Years 2014

ABSTRACT

A real exchange rate, being an indicator of monetary policy transmission,

is used measure to country’s international competitiveness. Due to the rapid growth in

international financial transactions, financial market transmission of exchange rate

movement are in interests. Real effective financial exchange rate (REFER) index is

introduced as an indicator of price competitiveness of country’s assets. This research

proposes the REFER index in the case of Thailand and concentrates exchange rate

movement through the valuation channel. Thailand’s REFER index movements are

heterogeneous from REER which is trade-weight real exchange rate index.

Moreover, this paper investigates the relationship between real exchange rate and

international capital flows. The main finding shows the different impact size of any

kind of capital flows on REER and REFER. However, both of real exchange rate

indexes, REER and REFER, benefit policy makers as an intermediate target for

monetary policy operations.

Keywords: Real effective financial exchange rate, Capital flows, Valuation channel

(2)

ACKNOWLEDGEMENTS

I have completed this paper under the best supporting from many

important people. Firstly, I would like to special acknowledge my advisor, Assistant

Professor Suluck Pattarathammas, who always gives me the valuable guidance,

advices and suggestions. I also appreciate my committee, Associate Professor

Kulpatra Sirodom, who help to enhance the analysis framework and improve the

research quality. Moreover, I am so grateful for my parents, all MIF instructors,

administrative staffs and friends who are the background of my successful.

Ms. Thipsuda Sukdam

(3)

TABLE OF CONTENTS

Page

ABSTRACT (1)

ACKNOWLEDGEMENTS (2)

LIST OF TABLES (5)

LIST OF FIGURES (6)

CHAPTER 1 INTRODUCTION 1

CHAPTER 2 STRUCTURE OF THAILAND’S BALANCE OF PAYMENTS 3

CHAPTER 3 REVIEW OF LITERATURE 5

CHAPTER 4 THEORETICAL FRAMEWORK 7

4.1 Real effective exchange rate 7

4.2 Real effective financial exchange rate 8

4.3 Exchange Rate Impacts: Valuation Channel 10

CHAPTER 5 RESEARCH METHODOLOGY 12

5.1 Real effective financial exchange rate 12

5.2 The relationship between real effective financial exchange rate 14

and capital inflows

CHAPTER 6 DATA 17

(4)

CHAPTER 7 RESULTS AND DISCUSSION 21

7.1 Thailand Real Effective Financial Exchange Rate (REFER) 21

7.2 The empirical results of the relationship between real exchange rate 25

and capital flows.

CHAPTER 8 CONCLUSIONS AND RECOMMENDATIONS 30

REFERENCES 32

BIOGRAPHY 34

(5)

LIST OF TABLES

Tables Page

2.1 Thailand balance of payments component from 2005-2014 4

5.1 Thailand’s top trading partner and financial partner countries 13

7.1 The REER and REFER determination model of private capital inflows 26

(6)

LIST OF FIGURES

Figures Page

2.1 Thailand’s balance of payments 3

7.1 The comparison between NEER and NEFER movements 21

7.2 Volatility of REFER and REER 23

7.3 Return of MSCI Thailand versus MSCI Financial Partners Countries 23

7.4 Thailand REER and REFER index 24

(7)

1

CHAPTER 1

INTRODUCTION

Although the world economy continues to recover from the global

financial crisis in 2008, uncertainties from financial risks remain such as capital flows

reversal. Looking ahead, the divergence in monetary policy in G-3 countries due to

the divergent recovery path in each country is also the new challenge to global

financial markets. As a result, global capital markets would likely to be more volatile

in the periods ahead.

Thailand’s financial market, which is a part of global financial

integration, would inevitably face international capital mobility. Thai currency

exchange market would be pressured from international capital reversal and/or capital

inflows due to the high correlation between foreign capital flows and exchange rate.

Thus, it needs to understand the relationship between exchange rate and capital

inflows in case of Thailand.

In Thailand, capital flows are a major share of cross-border transaction

which play an important role to determine the movement in exchange rate under

diminishing current account conditions. The Foreign Direct Investment (FDI) is the

majority of capital flows into Thailand for long time. However, after the global

financial crisis in 2008 there are large portfolio flows from core markets into

emerging markets including Thailand. Therefore, portfolio inflows are one of

exchange rate determinants and becoming more powerful whereas the size of FDI

inflows and trade balance of Thailand tend to slow down. In conformity with the

studies of Lartey (2007) and Combes et al. (2011), portfolio investment has the

highest appreciation effect followed by FDI and loans because FDI and loans are

potentially related to an increase in productive capacity.

Numerous economic research papers studied the relationship between

capital inflows and real effective exchange rate (REER) to describe behavior of the

country trading competitive indices affected by international fund flows. However,

recent researches emphasize that exchange rate movements operate through the

valuation channel, in addition to traditional impact on real variables such as trade

2

balance, in line with the rapid growth in the scale of cross-border financial holding

(Lane and Shambaugh, 2010). Because trade weighted exchange rate index or REER

is insufficient to fully understand the financial impact of currency movement, Gelman

et al. (2013) propose the new integrated approach to investigate the interaction

between asset prices, exchange rate and capital flows. Real Effective Financial

Exchange Rate (REFER), being financial weighted exchange rate index, is introduced

as an indicator of the price competitiveness of country’s assets. Lane and Shambaugh

(2010) show that the trade-weighted exchange rate index and financial-weighted

exchange rate index are heterogeneity. In addition, Gelman et al.’s (2013) study

suggests a better performance of the new financial-weighted index than traditional

real effective exchange rate.

The new approach motivates this paper to construct the REFER in case of

Thailand in order to understand the relationship between exchange rate, capital

inflows and asset prices under global financial market integration. Meanwhile, the

main purpose of this paper is to investigate the relationship between REFER and

different forms of capital flows (FDI, portfolio investment and loans) which are the

main pressure on the exchange rate. This paper also aims to compare the REER and

REFER movements in case of Thailand and then describe the differences among two

indices.

The rest of this paper is organized as follows: Section II shows the

structure of Thailand’s Balance of Payments. Related literatures are reviewed in

section III. Section IV describes the theoretical framework of this study especially the

concept of financial-weighted real exchange rate index under portfolio balance

approach. Section V explains (i) REFER construction procedure and (ii) the

methodology of investigation the relationship between real exchange rate (both REER

and REFER) and capital inflows. Section VI shows the empirical results (i) Thailand

REFER index and the comparison between the movements of REFER and REER (ii)

the relationship between real exchange rate and capital flows. Finally, the conclusion

and implication of overall subsequent is in the section VII.

3

-20,000

-10,000

0

10,000

20,000

30,000

40,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Mn USD Figure 2.1: Thailand's balance of payments

Current Account Financial Account

CHAPTER 2

STRUCTURE OF THAILAND’S BALANCE OF PAYMENTS

The foreign capital flows into Thailand come from two channels, namely,

the current account and financial account. These two accounts cause exchange rate

movements. The first channel, current account (CA), is the sum of trade balance and

net service incomes and transfers. The CA is composed of high proportion of trade

balance (Export - Import). The second channel, financial account (FA), represents

non-resident claim on transactions in financial instruments. Main components in FA

are composed of direct investment, portfolio investment, loans and others. Changes in

either direction or magnitude of capital flows can influence exchange rate movements.

From the figure 2.1, after the global financial crisis, the current account

tends to decline owing to lower growth in export of goods. Then, financial

transactions such as foreign direct investment (FDI), portfolio investment and loans

become the main source of international capital inflows and affect exchange rate

movements.

Source: Bank of Thailand

4

Table2.1: Thailand Balance of Payment’s component development from 2005-2014

Year 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Current Account -7,642 2,315 15,682 2,157 21,896 10,024 8,902 -1,499 -3,881 13,129

Trade Balance 3,402 13,670 26,640 17,348 32,620 29,751 16,989 6,670 6,661 24,582

Net Services Incomes

and Transfers -11,044 -11,354 -10,959 -15,191 -10,724 -19,727 -8,087 -8,169 -10,542 -11,453

Financial Account 6,974 8,106 -1,649 12,633 -2,601 24,809 -8,269 12,790 -4,163 -14,564

Direct Investments 7,545 8,487 8,314 4,449 701 4,495 -4,702 -1,362 2,140 4,869

Portfolio Investments 5,510 4,232 -6,723 -2,080 -5,530 9,828 6,163 3,398 -4,766 -12,072

Financial Derivatives -529 353 -314 -677 1,113 -102 -610 539 -341 308

Other Investments -5,553 -4,966 -2,926 10,941 1,116 10,588 -9,120 10,214 -1,195 -7,668

Net Errors and Omissions 6,090 2,320 3,070 9,902 4,764 -3,753 622 -6,261 2,713 124

Balance of Payments 5,422 12,742 17,102 24,693 24,127 31,324 1,214 5,265 -5,049 -1,210

Note: Thailand’s balance of payment is compiled based on IMF balance of payment edition 6th (BPM6)

Source: Bank of Thailand

5

CHAPTER 3

REVIEW OF LITERATURE

There are various studies about the relationship between exchange rate

and capital flows. The previous study of Zanello and Desruelle (1 9 9 7 ) shows the

cointegration between capital inflows and real exchange rate. At the same time, Fund

inflows have dual effects to host country that is a dilemma for policymakers to

manage capital policy. The pick-up in capital inflows possibly lead to a loss in trade

competitiveness due to host country REER appreciation. Bakardzhieva et al. (2 0 1 0 )

also find that net capital flows have a positive impact on REER, implying that capital

flows could be a factor which leads to REER appreciation and distort country trade

competitiveness. On the contrary, capital inflows could benefit host country due to the

improvement in investment and a current account deficit financing. Moreover, the

impacts of each type of inflows on REER are different. In term of financial markets,

asset price competitiveness and the construction of the real effective financial

exchange rate are concentrated. Net foreign asset position and REFER are

cointegrated and have the long-run relationship (Gelman et al., 2 0 1 3) (Kubelec and

Sa, 2012).

In the case of Thailand, foreign capital inflows and net foreign equity

purchases are found to be the cause of real effective exchange rate movements

according Gyntelberg et al. (2 0 0 9 ) and Chai-Anant et al. (2 0 0 8 ) . Furthermore,

Ananchotikul and Sitthikul (2008) find that an increase in capital flows into Thailand

benefits the country to upgrade macroeconomic fundamentals.

The previous analysis about the correlation of real exchange rate and

international capital flows mostly focuses on traditional impacts on real variables such as

trade balance. Nonetheless, the new wave of financial research proposes another side of

exchange rate movement effect through valuation channel in addition to traditional

impact. The valuation channel refers to capital gains and losses on the international

balance sheet from cross-border financial holding. To understand the financial impact of

change in exchange rate, Land and Shambaugh (2 01 0 ) construct net financial exchange

rate indices that is the combination of asset- and liability-weighted exchange rate indices.

6

Moreover, the proposition of real effective exchange rate that is not only financially

weighted but also deflated by financial asset price is used to emphasize causes and

consequences of exchange rate movement in international capital market transaction.

The net financial index captures the exposure of a country’s international

balance sheet to exchange rate movements. The comparison result of Lane and

Shambaugh (2 0 1 0 ) shows tremendous heterogeneity in the co-movement between

conventional trade-weight exchange rate index and net financial index. Moreover,

they observe that the trade-weighted rate indices are insufficient to provide a full

understand about financial impacts of currency movements. Their analysis also shows

that many developing countries have a negative position in foreign currencies such

that depreciation in domestic currency leads to negative wealth effects due to funding

foreign liability in foreign currencies. In addition, they find that the wealth effects

associated with exchange rate are substantial and can explain a sizable share of the

overall valuation shocks that hit the net foreign asset position.

The previous empirical study of Lane and Shambaugh (2 0 1 0 ) , Tille

(2003) and Lane and Milesi-Ferretti (2007) find that the financial weighted indices for

United States are quite different from trade weighted indices.

Recently, Gelman et. al. (2 0 1 3 ) propose new index of exchange rate

adjusted by cross-country asset price ratio which is interpreted as a real effective

financial exchange rate (REFER) based on the standard international capital asset

pricing model. They study a new integrated approach of interaction between asset

price, exchange rates and capital flows. The analysis result shows that country’s real

financial exchange rate cointegrates with international investor’s net foreign asset

holding. The most interest of this paper is the empirical results suggesting a better

performance of the REFER than REER which is applied in many literatures.

7

𝑊𝑖𝑗 = 𝛼𝑖 𝑀 𝑊𝑖𝑗 𝑀 + 𝛼𝑖 𝑃 𝑊𝑖𝑗 𝑃 + 𝛼𝑖 𝑇 𝑊𝑖𝑗 (𝑇)

CHAPTER 4

THEORETICAL FRAMEWORK

4.1 Real Effective Exchange Rate (REER)

Real Effective Exchange Rate (REER) is an indicator used to measure

country’s international trade competitiveness. The index comes from nominal

exchange rate movements adjusted by goods prices ratio of the country to trading

partner’s countries.

The REER index is geometrically weighted average of bilateral exchange

rates. As represented by Loretan (2005), the nominal exchange rate index at time t (𝑰𝒕)

is equal to;

(1)

where 𝐼𝑡−1 is value of index at time t-1, 𝑒𝑗,𝑡 and 𝑒𝑗,𝑡−1 are the price of currency i in

term of currency j at time t and t-1 respectively, 𝑤𝑗,𝑡 is weight of currency j in the

index and N is the number of currencies in the index.

The International Monetary Fund’s Information Notice System (INS) uses the

trade competitiveness weighting scheme and consumption price deflators for the

computation of REER index. The weights are based on trade in manufactures, primary

commodities and tourism services and are derived from;

(2)

where 𝑊𝑖𝑗 𝑀 ,𝑊𝑖𝑗 𝑃 , 𝑊𝑖𝑗 𝑇 are weight for trade in manufactures, primary

commodities, and tourism services respectively (Zanello and Desruelle, 1997).

Moreover, the currency weights designed in the study of Loretan (2005) show that the

weights for each country reflect the importance of respective economies for trade

competition. Competition in traded goods occurs in both domestic and foreign

markets so that weights of currency indices are linear combination of three

components which consist of (1) merchandise imports from country j to country i

(2) merchandise exports from country i to country j (3) fraction of economy k’s

,which is third market, merchandise import from country j.

𝐼𝑡 = 𝐼𝑡−1 ∗ (𝑒𝑗 ,𝑡

𝑒𝑗 ,𝑡−1

)𝑤𝑗 ,𝑡

𝑁

𝑗=1

8

𝑊𝑡𝑖 =

𝑃𝑗 ,𝑡 ∗ 𝐹𝑗 ,𝑡𝑖

𝑆𝑖𝑗 ,𝑡

, j = 1, … , i, … , N

𝑁

𝑗=1

4.2 Real Effective Financial Exchange Rate (REFER)

The concept of REER focuses only on international trade patterns.

Meanwhile, Gelman et al. (2013) and Lane and Shambaugh (2010) consider that

REER is insufficient to investigate the international financial transactions. In order to

capture impacts of real exchange rate movements caused by cross-border financial

transactions, the financial effective exchange rate ( REFER) is generated from

standard portfolio balance approach. REFER follows an exchange rate theory that

represents a function of relative supplies of domestic and foreign bonds (Husted and

Melvin, 2009). The exchange rate movements are determined by investors’ decision

to allocate their portfolio either to domestic or foreign assets which based on expected

returns.

According to REFER concept from Gelman et al. (2013), the model of

REFER explicitly concentrates on short-run portfolio dynamics allocation and assume

constant in real supply in domestic and foreign assets. There are N investors, one

investor for each country, allocating their wealth into the financial assets of N

countries. The nominal wealth of the country i investor in term of domestic currency

(𝑊𝑡𝑖 is;

(3)

where 𝑃𝑗,𝑡 is foreign currency price of foreign assets, 𝐹𝑗,𝑡𝑖 is N-1 real foreign assets in

terms of foreign currency and 𝑆𝑖𝑗,𝑡 is the spot exchange rate that can be defined as the

price of domestic currency in units of foreign currency.

Moreover, there is more assumed that investor i can buy foreign assets by

selling domestic assets for short-run and they hold these positions of portfolio for one

period. At the end of the period, investor i will totally unwind their foreign assets and

the investor then holds only domestic assets. This transaction influences the exchange

rate to realize.

Total nominal stock of country’s i asset in terms of domestic currency will

be 𝑃𝑖,𝑡 ∗ 𝐹𝑖 where 𝐹𝑖 is country i assets and 𝑃𝑖,𝑡 is the domestic currency price of the

domestic assets.

9

Because assets 𝐹𝑖 are either obtained by domestic investor i or the foreign

investors, nominal stock of country’s i asset then follows as

𝑃𝑖,𝑡 ∗ 𝐹𝑖 = ∑ 𝑃𝑖,𝑡 ∗ 𝐹𝑖,𝑡

𝑗𝑁𝑖=1 , j = 1, … , i, … , N (4)

Under the condition that investors can take foreign assets by selling domestic assets,

the domestic assets that are hold by foreign investors equate the foreign assets that are

hold by domestic investors.

∑ 𝑃𝑖,𝑡 ∗ 𝐹𝑖,𝑡𝑗

= ∑𝑃𝑗,𝑡∗𝐹𝑗,𝑡

𝑖

𝑆𝑖𝑗,𝑡

𝑁𝑗=1

𝑁𝑖=1 ,∀𝑗 ≠ 𝑖 (5)

Then, the equilibrium condition form will be

𝑃𝑗,𝑡∗𝐹𝑗,𝑡

𝑖

𝑆𝑖𝑗,𝑡= 𝜔𝑗,𝑡

𝑖 𝑊𝑡𝑖 , ∀𝑖, 𝑗 (6)

Where 𝜔𝑗,𝑡𝑖 is the efficient share of country j’s asset in investor i’s portfolio and

∑ 𝜔𝑗,𝑡𝑖𝑁

𝑗=1 = 1 , ∀𝑖

From eq.6 it can be rewritten into

𝑃𝑗,𝑡

𝑆𝑖𝑗,𝑡=

𝜔𝑗,𝑡𝑖 𝑊𝑡

𝑖

𝐹𝑗,𝑡𝑖 , ∀𝑖, 𝑗(7)

According to 𝑆𝑖𝑗,𝑡 =1

𝑆𝑗𝑖,𝑡 and N-1 ratios of cross-countries holding denominated in

country j currency for each portfolio, the equilibrium of investment is

𝑃𝑖,𝑡∗𝑆𝑖𝑗,𝑡

𝑃𝑗,𝑡=

{𝜔𝑖,𝑡𝑗

𝑊𝑡𝑗𝑆𝑗𝑖,𝑡}/𝐹𝑖,𝑡

𝑗

{𝜔𝑗,𝑡𝑖 𝑊𝑡

𝑖}/𝐹𝑗,𝑡𝑖

(8)

In the equilibrium, the asset price ratio in terms of country-j currency is

equal to the ratio of nominal demand per a unit of real assets. The left-hand side term

in eq. 8 can be approximated to currency i’s real bilateral exchange rate relative to

currency j. When this term goes up, it means that real exchange rate of country i

appreciates. The asset price ratio will be interpreted as currency i’s real bilateral

exchange rate versus currency j. Hence, the formula of currency i’s real effective

financial exchange rate is following;

∏ 𝑃𝑖,𝑡𝑆𝑖𝑗,𝑡

𝑃𝑗,𝑡 𝜃𝑗

𝑖𝑁𝐽=1 = ∏

{𝜔𝑖,𝑡𝑗

𝑊𝑡𝑗𝑆𝑗𝑖,𝑡}/𝐹𝑖,𝑡

𝑗

{𝜔𝑗,𝑡𝑖 𝑊𝑡

𝑖}/𝐹𝑗,𝑡𝑖

𝜃𝑗𝑖

𝑁𝐽=1 ,∀𝑗 ≠ 𝑖 (9)

10

where 𝜃𝑗𝑖 are constant weights derived from the cross-country holding of investor i

and j (both assets and liabilities side) so that ∑ 𝜃𝑗𝑖𝑁

𝑖=1 = 1 , ∀𝑖.

From the equilibrium equation in eq.(9), the left-hand side term will be

interpreted as REFER or real exchange rate of currency i against currency j while the

right-hand side term represents the weighted average of net foreign holdings i’s assets

in the portfolios of foreign investors. In other words, it shows the importance of

market capitalization in the domestic market as well as in the foreign market. When

investors change the proportion in their portfolio by increasing share of domestic asset

and decreasing foreign investment position, foreign asset price should be lower and

REFER will appreciate.

4.3 Exchange Rate Impacts: Valuation Channel

Impacts of exchange rate movements on international balance sheet

through valuation channel can be expressed in following framework. The change in

the net foreign asset position (NFA) coming from current account surplus and net

capital gain can be written as

𝑁𝐹𝐴𝑡 − 𝑁𝐹𝐴𝑡−1 = 𝐶𝐴𝑡 + 𝑉𝐴𝐿𝑡 (10)

where 𝐶𝐴𝑡 is the current account surplus and 𝑉𝐴𝐿𝑡 is net capital gain on existing

holding foreign assets and liabilities. Under currency denomination of foreign assets

and liabilities conservation, the net foreign asset position can be replaced with

𝑁𝐹𝐴𝑡 − 𝑁𝐹𝐴𝑡−1 = 𝑇𝐵𝑡 + 𝐹𝐶𝑡 = 𝑇𝐵𝑡 + 𝑁𝐸𝑇𝐼𝑁𝑉𝐼𝑁𝐶𝑡 + 𝑉𝐴𝐿𝑡𝑀𝑉 + 𝑉𝐴𝐿𝑡

𝑋𝑅 (11)

where 𝑇𝐵𝑡 is the trade balance and 𝐹𝐶𝑡 is the aggregate net financial return on

external investment position. The financial return on external investment position is

sum of investment incomes 𝑁𝐸𝑇𝐼𝑁𝑉𝐼𝑁𝐶𝑡), net capital gains from shifting in local-

currency asset prices (𝑉𝐴𝐿𝑡𝑀𝑉) and net capital gains from currency movement

(𝑉𝐴𝐿𝑡𝑋𝑅). According to the financial-weight exchange rate concept, international

investors allocate their portfolios by considering the net capital gain from investment.

The REFER would operates through the valuation channel, while the trade-weighted

index influences net exports.

11

There are generally evidences suggesting that currency movements do

matter for investor-currency returns (Lane and Milesi-Ferretti, 2005). The local

country’s currency depreciation causes improvement in export value and could

increase the local currency returns on holding equity (both form of portfolio

investment in equity and foreign direct investment) of export-oriented firms. In the

other way, the currency depreciation may be caused by weak economy. It would be

negative effects to the local currency returns on domestically-oriented firms. Then,

the relationship between exchange rate movements and local currency returns on

foreign portfolio investment in equity and FDI could be weak correlation. Meanwhile,

loans and deposits have no price valuation effects.

The valuation effects depend on the net foreign position of the country.

The country receives valuation gains if net financial-weighted effective exchange rate

index (REFER) increases. On the contrary, the country gets valuation loss if financial-

weighted effective exchange rate index falls. The results of Lane and Milesi-Ferretti

(2005) show that many developing countries have negative net position in foreign

currencies and depreciations in domestic currency generate negative wealth effects.

However, many countries could balance their foreign position by increasing net

foreign asset position to absorb wealth shocks from currency movements.

12

CHAPTER 5

RESEARCH METHODOLOGY

5.1 Real Effective Financial Exchange rate

From equation (9),

∏ (𝑃𝑖,𝑡𝑆𝑖𝑗,𝑡

𝑃𝑗,𝑡)𝜃𝑗𝑖

𝑁𝐽=1 = ∏

(

{𝜔𝑖,𝑡𝑗

𝑊𝑡𝑗𝑆𝑗𝑖,𝑡}

𝐹𝑖,𝑡𝑗

{𝜔𝑗,𝑡𝑖 𝑊𝑡

𝑖 }

𝐹𝑗,𝑡𝑖

)

𝜃𝑗𝑖

𝑁𝐽=1 for∀𝑗 ≠ 𝑖

The currency i’s real bilateral exchange rate versus currency j can be calculated from

geometric financial-weighted aggregate exchange rate under financial asset price

deflator. The left hand side term is REFER.

There are three steps to compute REFER. Firstly, the financial market

weight (𝜃𝑗𝑖) is derived from the cross-country holdings of investors i and j that

incorporate both asset-side and liability-side position. These weights indicate the

direction of the valuation impact of a movement in currency j against currency i. In

this study, the author uses the Bank of Thailand International Investment Position

(IIP) dataset that is the balance sheet of the country vis-à-vis the rest of the world and

comprising of financial claims on nonresidents and liabilities to nonresidents

provides. The IIP dataset provides direct investment and portfolio investment of

Thailand classified by country in both asset and liabilities side. Furthermore, the

dataset shows financial transactions between residents and nonresidents, reflecting

changes of ownership over financial assets and liabilities, which may be categorized

as direct investment, portfolio investment, financial derivatives, and other investment.

According to the annually financial weight from IIP, the author assumes that these

weights are constant over 12 months in each year, and the weights will change every

year following the latest foreign assets position survey.

Weight of REFER would be different from REER due to distinction of

partner countries between trading transitions and financial transactions. The

13

following table shows the share of Thailand Top 10 trading partner and financial

partner countries in 2014.

Table5.1: Thailand’s Top trading partner and financial partner countries

Rank

Trading partners Financial partners

Country % Share to trade volume Country % Share to International

Investment Position

1 China 13.6 Japan 17.6

2 Japan 13.2 United Kingdom 13.3

3 USA 7.8 Singapore 12.0

4 Malaysia 5.5 USA 11.4

5 UAE 4.3 HongKong 5.9

6 Singapore 4.1 Netherland 3.4

7 Indonesia 4.0 Cayman Islands 3.4

8 Australia 3.3 Belgium 3.3

9 Hong Kong 3.1 Mauritius 2.2

10 Korea 2.9 British virgin 2.1

Source: Bank of Thailand and calculated by author.

The second step is to collect the daily bilateral exchange rate data in form

of closing rate from Reuter’s database. Then, the daily exchange rate data is

transformed to monthly dataset by using average method. After that, the nominal

financial market bilateral exchange rates are constructed by geometric aggregating the

bilateral exchange rate of financial partner countries with financial-weighted in the

first step.

Third, the nominal financial market bilateral exchange rates are deflated

by the ratio of Thailand’s financial asset prices to foreign financial asset prices. The

14

author uses MSCI Thailand stock market index and financial partner’s weighted

average MSCI stock market index to be proxies of financial asset prices. MSCI stock

market indices are constructed by MSCI Global Investable Market Indices (GIMI)

method which is representative of foreign asset price.

5.2 The relationship between real effective financial exchange rate and capital

inflows

A number of studies look at the impact of capital flows on Real Effective

Exchange Rate (REER). The REER determination model of private capital inflows

are given as:

𝑅𝐸𝐸𝑅𝑡 = 𝛼0 + 𝛼1𝑇𝑂𝑇𝑡 + 𝛼2𝑇𝑂𝑇𝑡−1 + 𝛼3𝐶𝐴𝑡 + 𝛼4𝐶𝐴𝑡−1 + 𝛼5𝐹𝐷𝐼𝑡 + 𝛼6𝐹𝐷𝐼𝑡−1 +

𝛼7𝑃𝑜𝑟𝑡𝑡 + 𝛼8𝑃𝑜𝑟𝑡𝑡−1 + 𝛼9𝐿𝑜𝑎𝑛𝑡 + 𝛼10𝐿𝑜𝑎𝑛𝑡−1 + 𝜀𝑡

(12)

where 𝑅𝐸𝐸𝑅𝑡 is the real effective exchange rate; 𝑇𝑂𝑇𝑡 is the term of trade; 𝐶𝐴𝑡 is

the ratio of current account balance to GDP which shows the value of trade balance of

goods, net service incomes and transfers; 𝐹𝐷𝐼𝑡 is the ratio of net foreign direct

investment inflows to GDP; 𝑃𝑜𝑟𝑡𝑡 is the ratio of net foreign portfolio investment

inflows, both in bond market and equity market, to GDP; 𝐿𝑜𝑎𝑛𝑡 is the ratio of net

foreign loan inflows to GDP.

To understand the relationship between REFER and capital inflows, the

author thus follows the determination model to investigate the relationship between

real effective financial exchange rate and macroeconomic fundamentals.

𝑅𝐸𝐹𝐸𝑅𝑡 = 𝛽0 + 𝛽1𝑇𝑂𝑇𝑡 + 𝛽2𝑇𝑂𝑇𝑡−1 + 𝛽3𝐶𝐴𝑡 + 𝛽4𝐶𝐴𝑡−1 + 𝛽5𝐹𝐷𝐼𝑡 + 𝛽6𝐹𝐷𝐼𝑡−1 +

𝛽7𝑃𝑜𝑟𝑡𝑡 + 𝛽8𝑃𝑜𝑟𝑡𝑡−1 + 𝛽9𝐿𝑜𝑎𝑛𝑡 + 𝛽10𝐿𝑜𝑎𝑛𝑡−1 + 𝜀𝑡

(13)

where 𝑅𝐸𝐹𝐸𝑅𝑡 is real effective financial exchange rate which uses financial-weighted

regime and asset price deflators.

Terms of trade (TOT) use to measure the country’s international trading

gain. A rise in terms of trade is expected to cause the real exchange rate appreciation

15

through income effects rather than substitution effects. Better terms of trade can also

improve trade balance and the country will receive more income from exports.

Current account balance (CA) is the summation of net income from

exporting goods and services to foreign countries and foreign investment incomes.

Higher country’s competitiveness in global market generates more income to the

country and real exchange rate should be appreciated. However, demand of foreign

goods and services would increase from wealth effects and lead to high degree of

import value. The real exchange rate equilibrium is adjusted following trade activities.

Capital flows affect real exchange rate in different results depending on

the composition of capital flows. Foreign direct investment (FDI) moves into target

countries for market expansion, resource seeking and risk diversification objectives.

The large amount of capital flows is the nature of FDI which pressure on real

exchange rate. However, FDI flows could be related to investment in imported

machinery and equipments, and FDI may improve local productivity through

knowledge transfers. Hence, the pressure of FDI on real exchange rate would be

reduced. Foreign portfolio investment (PORT) is another kind of international fund

flows. PORT is relatively liquid due to short term investment position of foreign

investors. The investors want to take a position in profitability of firms and have no

management authority. Furthermore, foreign loan is a loan issued by non-resident

lenders. The foreign loan inflows are uncertain depending on the demand for loan of

local firms. Appreciation in real exchange rate due to portfolio investments and loans

inflows are more volatile. These flows do not necessarily improve productivity

capacity.

The Ordinary Least Square (OLS) is applied to estimate the relationship

between real exchange rate indices, both REER and REFER, and capital inflows. The

time-series variables used in all regression models in this paper are quarterly data

from 1st quarter of2006 to 4th quarter of2014. Before choosing an appropriate model,

the author tests a unit root by employing the Augmented Dicky –Fuller test whether

a unit root is presented in an autoregressive model.

∆𝑅𝐸𝐹𝐸𝑅𝑡 = 𝜇 + 𝛾𝑅𝐸𝐹𝐸𝑅𝑡−1 + ∑ ∅𝑖∆𝑅𝐸𝐹𝐸𝑅𝑡−1 + 𝜀𝑖𝑝𝑖=2 (14)

16

where ∆ is the first difference operator. This model can be estimated and test for a

unit root under null hypothesis of 𝛾 = 0. The optimal number of lags (p) is justified

by using Schwarz’s Bayesian information criterion (SBIC). The test-statistic is

compared to Dickey–Fuller table.

One of assumptions underlying ordinary least square (OLS) estimation is

that the errors are uncorrelated. This assumption can easily be violated for time series

data. Durbin-Watson test is highly parametric test for autocorrelation. It is assumed

that there are no autocorrelation:

𝐻0: 𝜀𝑖 ∽ 𝑁 0, 𝜎2 𝑓𝑜𝑟 𝑎𝑙𝑙 𝑖 𝑎𝑛𝑑 𝑐𝑜𝑟𝑟(𝜀𝑖, 𝜀𝑗) = 0 𝑓𝑜𝑟 𝑖 ≠ 𝑗

The Durbin-Watson test is simply

DW = ∑ εi − εi−1

2ni=1

∑ εi2n

i=1

where 𝜀𝑖 is the 𝑖𝑡ℎ residual. Small values of DW indicate of positive autocorrelation,

while large values indicate negative autocorrelation.

The cointegration test for real exchange rate model is also important

because it is usually believed to near-cointegrated or cointegrated time series.

Spurious regression problem would occur when the variables are cointegrated. Thus,

Johansen’s maximum eigenvalue and trace tests are used to determine the number of

cointergrating vectors in the system.

17

CHAPTER 6

DATA

Throughout this paper, the author focuses on foreign assets and liabilities

of Thailand that are classified based on IMF Balance of Payments and International

Investment Position manual 6th edition. Balance of Payments is a summary of

economic transactions between residents and nonresidents that occurs at specific time

period. Balance of payments consists of three accounts, namely, current account,

capital account and financial account. Bank of Thailand is complier and publisher

Thailand Balance of payments.

The definition of nonresident investors1 consists of (1) cooperation,

institutions, funds, financial institutions or juristic person located outside Thailand;

(2) entities of foreign governments located outside Thailand (3) branches and agents

of domestic juristic persons located outside Thailand; and (5) natural person not of

Thai nationalities who do not have alien identity or residence permits.

According to the study of foreign assets and liabilities position of

Thailand, the author focuses on financial transaction between resident and non-

resident in financial account which reflect the change of ownership over financial

assets and liabilities. The assets and liabilities are categorized as direct investment,

portfolio investment, financial derivatives, and other investment.

- Direct Investment2refers to the claims on resident assets of non-

resident. A direct investor may invest in firm’s equity of capital,

lending to branch enterprise, reinvested earnings, buying debt

securities and giving trade credit to business affiliates. Investment of

nonresident in equity is indicated as a direct investment when the direct

investors have own claim equal and over than 10 percent of the

ordinary shares for an entity.

- Portfolio Investment refers to the activities among resident and

nonresidents that involves buying and selling of equity securities, debt

securities in terms of bonds, notes, money market instruments which

1 The definition from Bank of Thailand based on BPM manual edition 6. 2 Source: Bank of Thailand Meta data.

18

are not include the securities classified as direct investment and reserve

assets. The values of investments are recorded in market price basis.

- Financial Derivatives refers to the financial transactions in financial

derivatives. The financial derivative value is recorded only realized

gains and losses.

- Other Investment refers to the transaction between resident and non-

residents that includes loans, trade credits, deposits, other account

receivables and account payables.

This study provides the new approach index “Real effective financial

exchange rate (REFER)”. The index creation uses the geometric method to aggregate

bilateral exchange rate with financial weight. Aggregated weights from assets and

liabilities position in any countries are used to identify the important of these

countries to Thailand. Monthly REFER index of Thailand is presented from January

2006toDecember 2014.

However, financial weights rely on Thailand international position in

direct investments and portfolio investments and foreign investors’ investment

position in Thailand. The data of Thailand International Investment Position (IIP) are

surveyed by Bank of Thailand. Annually data are available from 2006 to 2014. The

related reports of data are following:

(1) Report EC_XT_063 represents foreign direct investment outstanding

classified by country.

(2) Report EC_XT_064 represents Thai direct investment abroad

outstanding classified by country.

(3) Report EC_XT_065 represents foreign portfolio investment

outstanding classified by country.

(4) Report EC_XT_066 represents Thai portfolio investment abroad

outstanding classified by country.

The weights of REFER vary in each year from international investment

position rebalancing and are assumed to be a constant in every month.

19

The daily closing rate of bilateral exchanges are collected from Reuter’s

database, then author averages into monthly time series data to aggregating the

nominal financial-weighted exchange rate by geometric method. The nominal rates

are deflated by Thailand financial asset prices relative to global financial asset prices.

The MSCI Thailand Index is representative of Thailand financial asset price. This

index is designed to measure the performance of the large and mid capital segments of

the Thailand market with 32 components that can cover about 85% of the Thailand

equity market. Thailand MSCI would compare to the weighted average MSCI of

financial partners which captures large and mid capital segments in any financial

markets. Finally, the index REFER is created in monthly data from January 2006 -

December 2014.

In second session of this paper, the author would investigate the

relationship between real effective financial exchange rate (REFER) and the capital

flows which be separated into Foreign Direct Investment, Portfolio Investment and

Loans. Because of scaling problem avoidance, all private capital flows value was

transformed into the ratio of capital flow to GDP. REFER was also transformed to

quarterly data by arithmetic mean in order to estimation the relationship with the

different types of capital flows to GDP.

Moreover, the author examines the relationship of traditional real

exchange rate or REER in the same model to compare the results. The quarterly data

of net capital flows are provided by Bank of Thailand. Report EC_XT_051 represents

the component of capital flows in financial account classified by sectors and

instruments from 1st quarter of 2006 to the 4th quarter of 2014.

Thai Baht Real Effective Exchange Rate (REER) is represented in

report table EC_EI_007: Nominal Effective Exchange Rate (NEER) and Real

Effective Exchange Rate (REER) by Bank of Thailand.

Current account balance (CA) which is net export of goods and

services of Thailand is quarterly data from Bank of Thailand. Its value is sum of trade

balance, net service incomes and transfers. Table EC_XT_049 shows all components

of Balance of Payments.

20

Terms of Trade are the ratio of average export prices to import prices.

Bureau of Trade and Economic Indices (BTEI), Ministry of Commerce (MOC) is the

provider and they publish the data every month since January 2000.

21

CHAPTER 7

RESULTS AND DISCUSSION

7.1 Thailand Real Effective Financial Exchange Rate (REFER)

Thailand’s REFER index represents Thai Baht currency (THB) movement

against the currencies movement of financial/investment partners which are both

outward and inward fund flow. The index is deflated by domestic financial asset

prices relative to financial asset prices in financial-partner countries. The

interpretation of REFER movements is similar to the trade-weight real exchange rate,

REER, that is higher REFER reflects more appreciated THB than financial partner

currencies. REFER appreciation could be a cause of loosing financial asset prices

competitiveness in foreign investor perspectives. On the contrary, a fall in REFER

means that THB is more depreciated than financial partners which could improve

financial asset prices competitiveness. Thus, the benefit of tracking REFER is to help

evaluate the asset price competition and the impact of international fund flow through

exchange rate channel.

Figure 7.1: The comparison between NEER and NEFER movements

Source: Bank of Thailand and the author calculation

80

85

90

95

100

105

110

115

120

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4index

2012 = 100

The NEER and NEFER

NEER NEFER

22

Figure 7.1 shows the comparison between the movements of trade-

weighted exchange rate index, called nominal effective exchange rate (NEER), and

financial-weighted scheme index which is called nominal effective financial exchange

rate (NEFER). The graph represents highly correlation of both weighed scheme

indices movements. The co-movement between NEER and NEFER implicates that

weighted bilateral exchange rate of trading partners and financial partners are not the

main cause of divergence between REER and REFER. However, there are conflicts in

some periods such as January 2009 and January - April 2012.

In January 2009, NEFER was more appreciated than NEER because of

sharp depreciations in Euro (EUR) and Singapore dollar (SGD) which are major

financial partners of Thailand. At the same time, Japanese Yen (JPY) India Rupee

(INR) and Chinese Renminbi (CNY), turned appreciate against Thai baht due to their

strong economic fundamental. The fact that Japan and India are the main trading

partners of Thailand; therefore it was the main factor to support NEER more

depreciated than NEFER.

In the first half of 2012, NEER suddenly shrank resulted from the

appreciation of Malaysian Ringgit (MYR), Indian Rupee (INR) and Philippine Peso

(PHP), which are minor countries in term of financial corporation.

Recently, Thai baht tends to continuously appreciate against both financial

and trading partners since the second half of 2014. As a result NEER and NEFER

move together in appreciation trend.

23

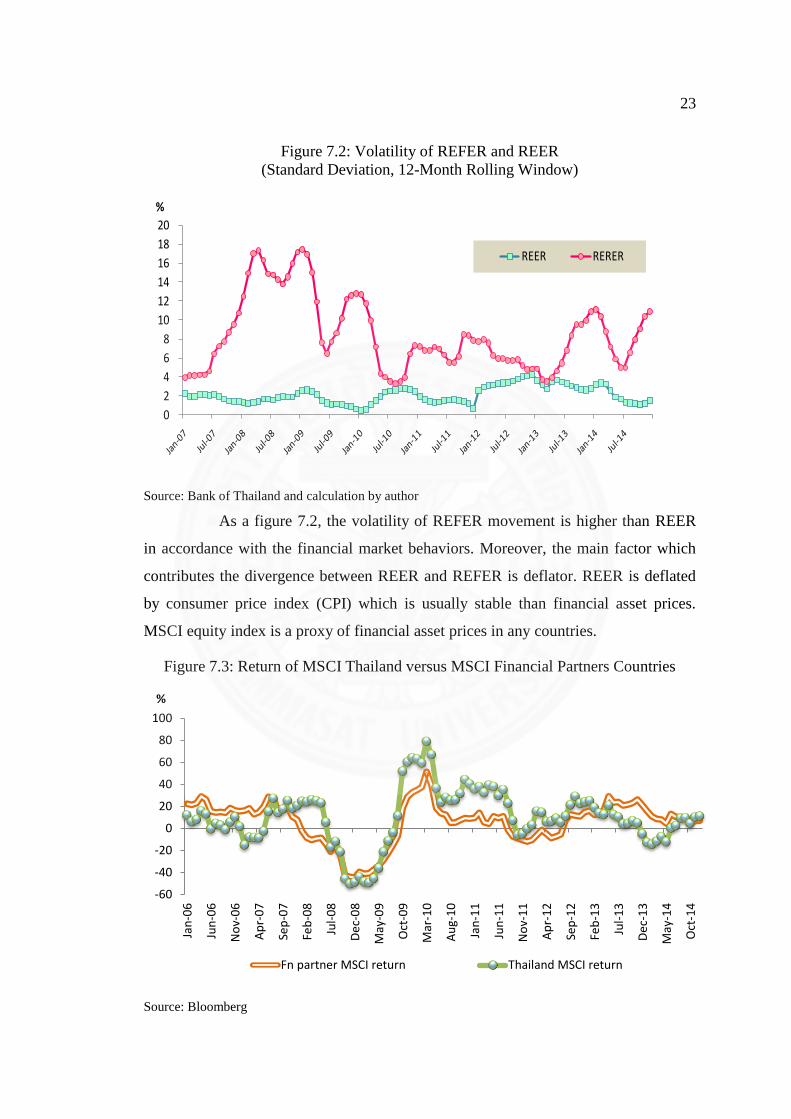

Figure 7.2: Volatility of REFER and REER

(Standard Deviation, 12-Month Rolling Window)

Source: Bank of Thailand and calculation by author

As a figure 7.2, the volatility of REFER movement is higher than REER

in accordance with the financial market behaviors. Moreover, the main factor which

contributes the divergence between REER and REFER is deflator. REER is deflated

by consumer price index (CPI) which is usually stable than financial asset prices.

MSCI equity index is a proxy of financial asset prices in any countries.

Figure 7.3: Return of MSCI Thailand versus MSCI Financial Partners Countries

Source: Bloomberg

0

2

4

6

8

10

12

14

16

18

20

% 12-Month Rolling Window of REER and REFER Standard Deviation

REER RERER

-60

-40

-20

0

20

40

60

80

100

Jan

-06

Jun

-06

No

v-0

6

Ap

r-0

7

Sep

-07

Feb

-08

Jul-

08

De

c-0

8

May

-09

Oct

-09

Mar

-10

Au

g-1

0

Jan

-11

Jun

-11

No

v-1

1

Ap

r-1

2

Sep

-12

Feb

-13

Jul-

13

De

c-1

3

May

-14

Oct

-14

% MSCI Thailand vs MSCI Financial Partners Return

Fn partner MSCI return Thailand MSCI return

24

The REER and REFER indices are heterogeneity. The financial asset

prices competitiveness index, REFER, is quite volatile more than the index measuring

trade competiveness or REER due to the flexibility of investment fund flows and

financial asset prices volatility. The figure 7.3 shows the development of MSCI stock

index return from 2006 – 2014. Though Thailand’s equity return moves together with

the financial partner markets for a long time, there are the divergent points due to the

different domestic economy environments. The equity returns difference between

Thailand and financial partner countries are the cause of REFER movement

fluctuation.

Figure 7.4: Thailand REER and REFER index

Source: Bank of Thailand and the author calculation

The figure 7.4 shows the comparison movements of REER compare to

REFER index. An increase in REFER means an appreciation of Thailand securities

relative to financial partner countries. Before the global financial crisis (GFC), Thai

REFER continued to appreciate as global financial market boom and international

funds flow into Thailand as a resulted of economy flourish. In 2008, Thailand’s

financial securities unavoidably depreciated because of global financial market

crunch. Since March 2009, REFER turned to be an upward trend reflecting increased

financial asset prices as a result of strong economic fundamental in Thailand.

Subsequently, Thai financial markets are become an attractive investment destination.

70

75

80

85

90

95

100

105

110

115

50

60

70

80

90

100

110

120

130

index REERindex REFER

The REER and REFER index

REFER REER

25

However, the return of Thailand financial market is slightly decreased from January

2013 - January 2014 because of geopolitical problem and economic slowdown. In

other words, negative impacts from domestic problem contribute to the drop in

REFER on this time. The lower REFER reflecting better asset price competitiveness

is an impulsive factor to foreign investors turn to allocate their funds into Thai

financial market after geopolitical problem relaxation. Recently, REFER is sharply

appreciation caused by strong value of Thai baht relative to core financial partners,

which make Thailand would lose financial asset prices competitiveness.

7.2 The empirical results of the relationship between real exchange rate and

capital flows.

The relationship between the real exchange rate, both measured by trade-

weighted and financial-weighted regime, and external sector indicators is estimated

by OLS method in the period ofQ1 2006 – Q4 2014. The explanatory variables of real

exchange rate consist of both international merchandise and capital flow variables.

For the first step, Augmented Dicky-fuller unit root testis applied to the level of all

variables. The test finds that REER, REFER and term of trade (TOT) are I(1),

meaning that these variables are non-stationary at level but become stationary in first-

difference form. Meanwhile, other explanatory variables, including current account to

GDP ratio (CA), foreign direct investment to GDP ratio (FDI), foreign portfolio

investment to GDP ratio (PORT) and foreign loans to GDP ratio (LOANS),

are stationary at level form or I(0). Moreover, this study considers the reverse

causality bias of the relationship between real exchange rate and capital flows.

However, according to Gyntelberg et al. (2012), the Thai baht movement was not a

driver of non-resident investors’ equity investment on stock exchange of Thailand

(SET). Thus, the OLS estimation could be an appropriate method. Moreover, the

model does not face the autocorrelation problem as reflected from Durbin-Watson

values which are close to 2. The estimation result of the relationship between REER

and private capital flows is shown in table 3.

26

Table 7.1: The REER and REFER determination model of private capital inflows

Estimation method: OLS

Determinant variables: DLOG(REER) DLOG(REFER)

C -0.006007

(-0.7845)

-0.043346

(-0.9923)

DLOG(TOT) 0.616653**

(2.5954)

-0.845284

(-0.5561)

CA -0.001059

(-1.2185)

0.003376

(0.8833)

FDI 0.001730**

(1.9176)

0.009295

(0.9082)

PORT 0.001350

(0.8420)

0.015049**

(2.6441)

PORT(-1) 0.004822***

(3.0207)

0.012122***

(3.9228)

LOAN -0.001126

(-1.0849)

-0.002361

(-0.3895)

LOAN(-1) 0.001276

(0.6544)

-0.010543**

(-2.1760)

R2 0.4202 0.4372

Adj. R2 0.2698 0.2913

Note: ***, ** and * denote level of significance at 1%, 5% and 10%, respectively.

Value in parenthesis is t-statistics.

The regression results show that REER adjustments were associated with

changes in term of trade (TOT), foreign direct investment (FDI)and lagged of foreign

portfolio investments (PORT(-1)). Term of trade is the main determinant of REER

movement with direct variation. An increase in export prices which relative to import

prices represents the better international trade competitiveness and encourage the

REER move to appreciation. An increase in term of trade by 1% leads to an

appreciation of the REER by 0.62%. Price competitiveness of goods is the important

factor of Thailand’s exports. The higher export prices lead to export revenue increase

that is income effects. On the contrary, higher export prices could destroy the price

competitiveness because of low-technology and low-value added goods and this

situation is called substitution effect. As the empirical result shows that better term of

trade benefits to Thai economy from larger income effects than substitution effect.

27

Private capital inflows in terms of FDI and lagged foreign portfolio

investment (PORT(-1)) significantly influence on current REER appreciation. Along

the time, FDI continued to flow into Thailand especially manufacturing sectors thanks

to the strong economic fundamental and supportive resources such as low wages.

Recently, FDI has remained flow not only into Thailand’s manufacturing sectors but

also financial service sectors as a result of financial market development and regional

integration from ASEAN Economics Community (AEC).Changes in foreign direct

investment (FDI) inflows suddenly contribute to the REER appreciation. An increase

in FDI to GDP ratio by 1% makes the REER appreciate by 0.002%. Impacts of FDI

on REER are smaller than TOT because FDI inflows are more stable. Add up with,

FDI inflows could be related to investment through imports of machinery and

equipments, and also FDI may improve local productivity through knowledge

transfers. Hence, the pressure on real exchange rate from FDI would be reduced.

Another determinant factor of REER is the lagged foreign portfolio

investment. Changes in lagged PORT significantly influence on current REER

movements. An increase of foreign portfolio investment to GDP ratio by 1% leads to

an appreciation of REER by only 0.004% in the next quarter. The capital inflows in

terms of portfolio investment area source of funding of listed companies that

encourage the REER appreciation. However, the lag of PORT has the lower effect on

REER appreciation due to the high capital mobility.

In the case of REFER, the OLS regression is employed to estimate as

same as the REER model. The result of the relationship between REFER and private

capital flows is also presented in table 3.

Since REFER is measured Thailand’s financial asset prices

competitiveness against financial partner countries, the capital flows related with

foreign portfolio investments (PORT) and foreign loans (LOAN) are the significant

determinant of REFER movements. The foreign portfolio investments, which are net

foreign purchases in financial assets, have highly impacts on REFER. An increase of

portfolio investment to GDP ratio by 1% suddenly influence the REFER appreciate by

0.015%. Add up with, 1% of lagged PORT cause the REFER appreciate by 0.012%.

28

When non-resident investors move their funds into Thailand’s financial markets,

which are generally traded in terms of Thai baht, the REFER would be appreciated.

On the other hand, net selling-off in Thai securities of foreign investors leads to

REFER depreciation due to lower demand for Thai baht. This result is in line with the

study of Gyntellberg et al. (2012) which empirically study about systematic links

between capital flows and exchange rate. They find that net capital flow into Thai

equity market has a positive correlation with Thai baht appreciation. Moreover, higher

dollar-denominated SET returns relative to S&P equity market returns contribute to

foreign investors’ sell-off in Thai equity. Therefore, the result of Gyntellberg et al.

supports the positive relationship between REFER and PORT that is found in this

study. It also confirms that the financial asset prices competitiveness would decline

when REFER is appreciated from non-resident investors’ portfolio rebalancing.

Lagged foreign loan (LOAN(-1)) is another significant REFER

determinant with negative correlation. Because the foreign loan is a source of funding

for Thai businesses, the net foreign loan inflows can occur when Thai businesses

perform badly and need the extra working capital. Subsequently, Thai financial asset

values would decrease and REFER would be lower. Additionally, international loans

are used to be foreign asset-liabilities position management of commercial bank under

the central banks’ regulations to limit their foreign exchange exposure. Exporters,

importers and investors would hedge their foreign exchange rate risks through the

financial derivative products such as forwards, swaps and options with commercial

banks. Based on the regulation, commercial banks are limited their foreign exchange

position, and then they must manage their foreign assets and liabilities in accordance

with the customer transactions. The foreign loan repayments of commercial banks

would occur when the Thai investors invest less in foreign securities and allocate their

portfolio more into Thai securities. The net foreign loan repayments improve the

value of Thai securities by portfolio rebalancing of Thai investors, thus REFER is

higher in the same time with loan outflows. However, the variables related to

international merchandise, including TOT and CA, and FDI have no impact on

REFER adjustments.

29

The result from REER determination model is quite different from

REFER. These results confirm the hypothesis that the trade-weighted exchange rate

index, REER, and financial-weighted exchange rate index, REFER, are heterogeneity.

The REFER is another real effective exchange rate index that helps to capture the

impact of international financial fund flow through the exchange rate channel in

financial markets.

30

CHAPTER 8

CONCLUSIONS AND IMPLICATIONS

Real exchange rate indexes are constructed for many purposes; (1) to

measure country’s international competitiveness (2) to access the financial conditions

indexes and (3) to be an indicator of monetary policy transmission and financial

stability. Therefore, real exchange rate indexes are important for policy makers and

market participants. Although the REER index is widely used to measure the

country’s international competitiveness and monitor exchange rate stability, it only

concentrates on international merchandise transactions which ignore the international

relationships in terms of financial transactions. As a result, REFER index is proposed

to explain the impact of exchange rate movements on international balance sheet

through valuation channel.

This paper introduces the real effective financial exchange rate (REFER)

which measure the country’s financial asset price competitiveness in the case of

Thailand. The REFER is generated based on the standard portfolio balance approach.

The comparison between REER, which is traditional real exchange rate index, and

REFER movements shows that they are heterogeneity. Thailand’s financial-weight

real exchange rate, REFER, is more volatile than REER because of the flexibility of

financial asset price differential among the financial partners. In the case of Thailand,

REFER was largely appreciated before the global financial crisis (GFC) in 2008.

Although REFER suddenly depreciated due to the global turmoil in the GFC period,

REFER turned to improve quickly since the second half of 2009. Since January 2014,

the steep REFER movement has shown stronger Thai baht than other financial partner

countries which could be a cause of loss in financial asset prices competitiveness.

This paper also investigates the relationship between real exchange rate,

both REER and REFER, and the ratio of capital flows to GDP. The estimation results

show the different impact size of capital flows on REER and REFER. The REER

appreciation due to term of trade improvement is statistically higher than capital

inflows. Moreover, FDI inflows have a positive relationship with REER appreciation,

influencing more than portfolio investment inflows. Meanwhile, the foreign loan also

has impacts on the REFER movement in opposite direction. In the case of REFER,

31

the portfolio investment and foreign loans are the main contribution of REFER

appreciation. Meanwhile, the variables related to international merchandise, including

TOT and CA, and FDI have no impact on REFER adjustments.

In the case of Thailand, this research finds that the REER and REFER

indexes are heterogeneity due to discrepancy of theoretical concepts. The REFER

movements are more sensitive to financial asset return changes because of wealth

effects. Because of international investment expansion, the REER index is not enough

to indicate the impacts of exchange rate movements to economy. The policy makers,

who monitor the external stability through exchange rate channel, should also concern

the financial impacts. Therefore, both of real exchange rate indexes, REER and

REFER, should be used together as a measure of country’s competitiveness, an

intermediate target for monetary policy or exchange rate intervention.

32

REFERENCES

1. Ananchotikul and Sitthikul, 2008, Capital flows in Thailand: Trends,

Determinants, and Implications for Central Bank Policies, Bank of Thailand

Discussion Paper, April, 3-41.

2. Arteta, C., Eichengreen, B. and Wyplosz, C., 2003, When Does Capital

Account Liberalization Help More than it Hurts?, Economic Policy in the

International Economy,177–206.

3. Bakardzhieva, Ben Naceur, and Kamar, 2010, The Impact of Capital and

Foreign Exchange Flows on the Competitiveness of Developing Countries, IMF

Working Paper, WP 06/266.

4. Balakrishnan, Nowak, Panth and Wu, 2012, Surging Capital Flows to

Emerging Asia: Facts, Impacts, and Responses, IMF Working Paper, WP 12/130.

5. Bonizzi, 2013, Capital Flows to Emerging Markets: An alternative Theoretical

Framework, SOAS Department of Economics Working Paper Series, No. 186, The

School of Oriental and African Studies.

6. Chai-Anant and Ho, 2008, Understanding Asian Equity Flows, Market

Returns and Exchange Rates, Bank for International Settlements, Paper No. 245.

7. Devereux and Saito, 2006, A Portfolio Theory of International Capital Flows,

IIIS Discussion Paper, No.124.

8. Gelman, Jochem, Reitz and taylor, 2013, Real Financial Market Exchange

Rates and Capital Flows, QBER Discussion Paper, No.3.

9. Gyntelberg, Loretan, and Subhanij (2012), “Private Information, Capital

Flows, and Exchange Rates,” IMF Working Paper WP/12/213.

10. Husted and Melvin, 2010, Exchange rate theories, International Economics,

451-468.

11. Jongwanich, 2010, Capital Flows and Real Exchange Rates in Emerging Asian

Countries, ADB Economic Working Paper Series, No.210.

12. Kubelec, C., and F. Sa, 2012, The Geographical Composition of National

External Balance Sheets: 1980–2005, International Journal of Central Banking 8:

143–189.

33

13. Lane and Milesi-Ferretti, 2007, The external wealth of nations mark II:

Revised and extended estimates of foreign assets and liabilities 1997-2004, Journal of

International Economics, 73.

14. Lane and Shaugh, 2010, Financial exchange rates and International Currency

Exposures, American Economic Review, 100(1).

15. Louis Combes, Kinda, and Plane, 2011, Capital Flows, Exchange Rate

Flexibility, and the Real Exchange Rate, IMF Working paper, WP/11/9.

16. Zanello, Alessandro, and Dominique Desruelle, 1997, A Primer on the IMF’s

Information Notice System, IMF Working paper, WP97/71.

34

BIOGRAPHY

Name Ms.Thipsuda Sukdam

Date of Birth July 2, 1987

Educational Attainment

2014: Master in Finance (MIF) Program,

Thammasart University

2010: Bachelor of Art (Economics) with first class

honours, Thammasart University

Work Position Senior Economist

Bank of Thailand

Work Experiences 2010-2013: Economist

Bank of Thailand