Embed Size (px)

Citation preview

Papula-Nevinpat IP Seminar

THE RELATION BETWEEN IP VALUATION AND COMPANY VALUATION IN M&A

TRANSACTIONS

8 November 2016

Eng. Andrea Tiburzi

1 © 2016 - Barzanò & Zanardo

Agenda

• Who am I?

• Introduction

• The main message

• Strategy analysis

• Value extraction

• Examples from real life

© 2016 - Barzanò & Zanardo2

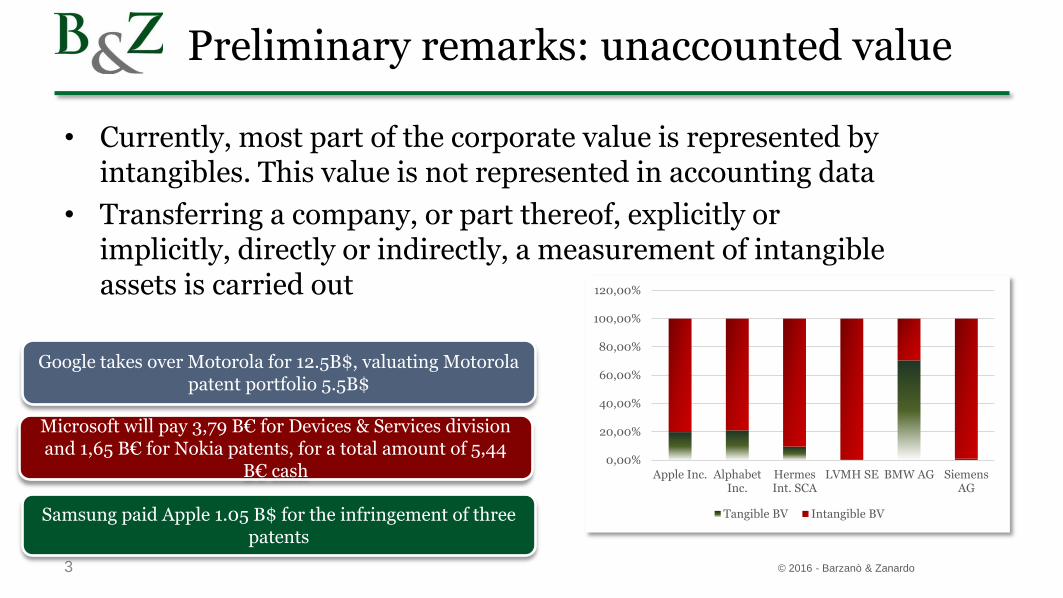

Preliminary remarks: unaccounted value

© 2016 - Barzanò & Zanardo3

Google takes over Motorola for 12.5B$, valuating Motorola patent portfolio 5.5B$

Microsoft will pay 3,79 B€ for Devices & Services division and 1,65 B€ for Nokia patents, for a total amount of 5,44

B€ cash

Samsung paid Apple 1.05 B$ for the infringement of three patents

• Currently, most part of the corporate value is represented by intangibles. This value is not represented in accounting data

• Transferring a company, or part thereof, explicitly or implicitly, directly or indirectly, a measurement of intangible assets is carried out

0,00%

20,00%

40,00%

60,00%

80,00%

100,00%

120,00%

Apple Inc. AlphabetInc.

HermesInt. SCA

LVMH SE BMW AG SiemensAG

Tangible BV Intangible BV

Preliminary remarks: problem

© 2016 - Barzanò & Zanardo

What is the driver for a CEO or a consultant in tackling or analyzing IP rights valuation in M&A transactions

4

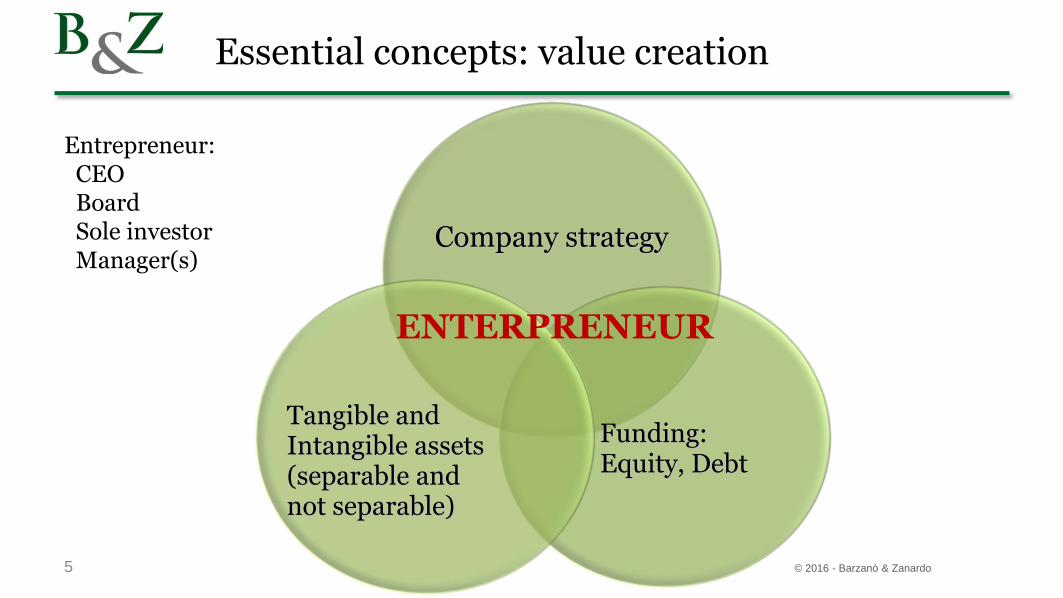

Essential concepts: value creation

5 © 2016 - Barzanò & Zanardo

Company strategy

Funding:Equity, Debt

Tangible and Intangible assets (separable and not separable)

ENTERPRENEUR

Entrepreneur:CEOBoardSole investorManager(s)

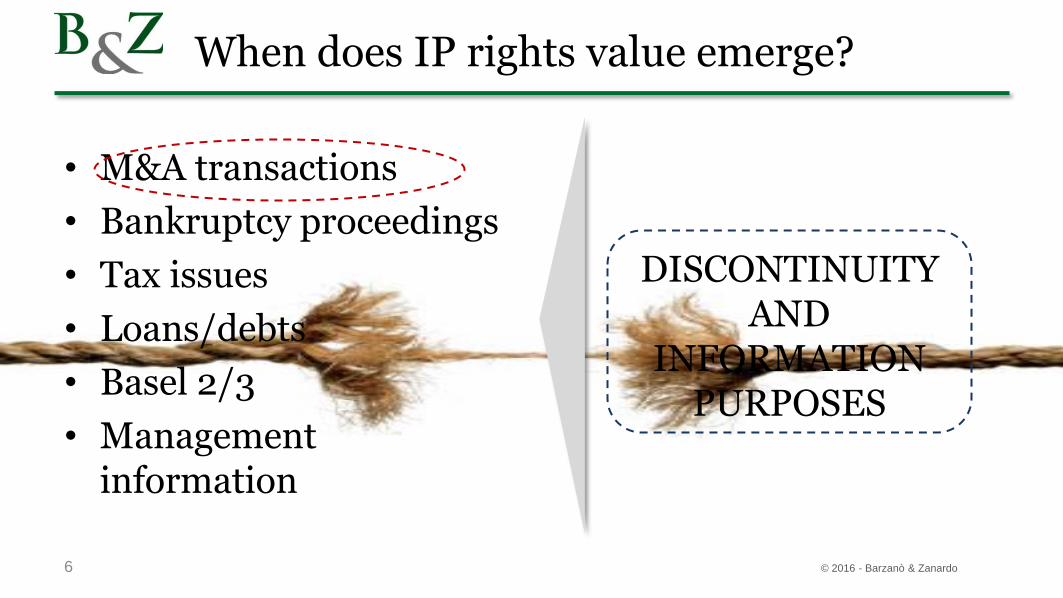

When does IP rights value emerge?

• M&A transactions

• Bankruptcy proceedings

• Tax issues

• Loans/debts

• Basel 2/3

• Management information

© 2016 - Barzanò & Zanardo

DISCONTINUITY AND

INFORMATION PURPOSES

6

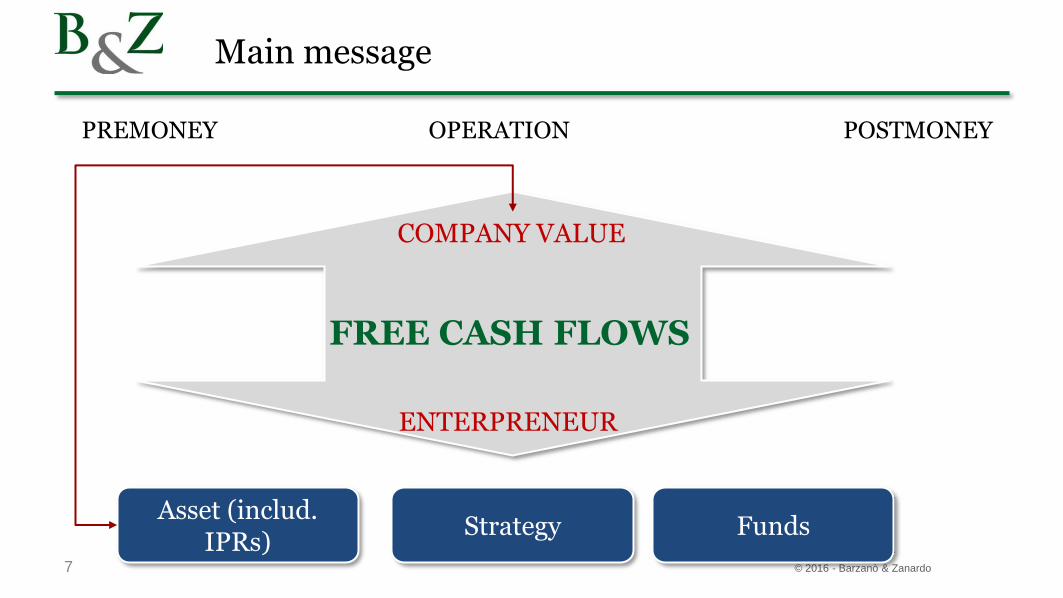

Main message

7 © 2016 - Barzanò & Zanardo

StrategyAsset (includ.

IPRs)Funds

ENTERPRENEUR

FREE CASH FLOWS

COMPANY VALUE

PREMONEY POSTMONEYOPERATION

Main message

© 2016 - Barzanò & Zanardo

IP rights do not have an ACTIVE market

Any financial valuation isPOTENTIAL

IP rights value is related to the (company/strategy) context

8

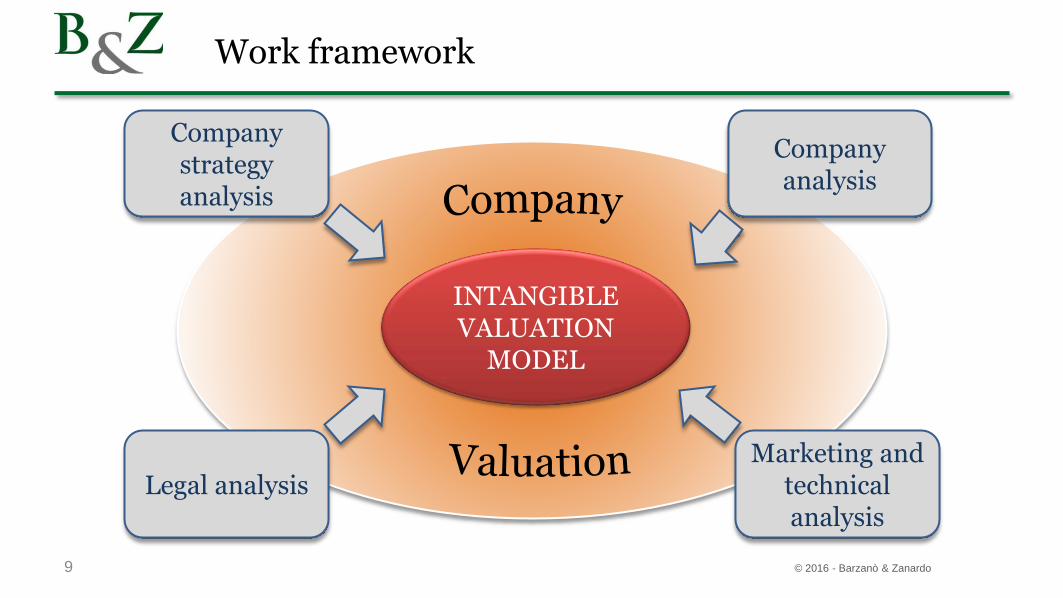

Work framework

9 © 2016 - Barzanò & Zanardo

INTANGIBLE VALUATION

MODEL

Company strategy analysis

Company analysis

Marketing and technical analysis

Legal analysis

Strategy

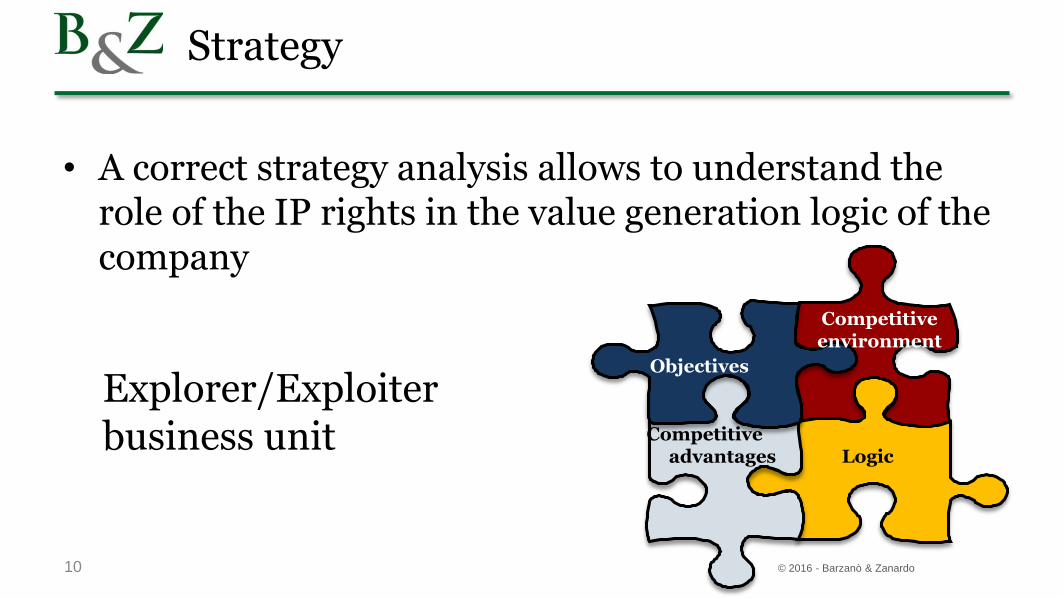

• A correct strategy analysis allows to understand the role of the IP rights in the value generation logic of the company

© 2016 - Barzanò & Zanardo10

Objectives

Competitiveenvironment

Competitive advantages Logic

Explorer/Exploiter business unit

Wall street well known proverb

© 2016 - Barzanò & Zanardo11

Revenue is vanity, profit is sanity,but cash is reality

M&A valuation methods: DCF

Discounted Cash Flows models are based on discounting future cash flows at an appropriate

discount rate

12 © 2016 - Barzanò & Zanardo

Financial valuation methods: DCF

© 2016 - Barzanò & Zanardo13

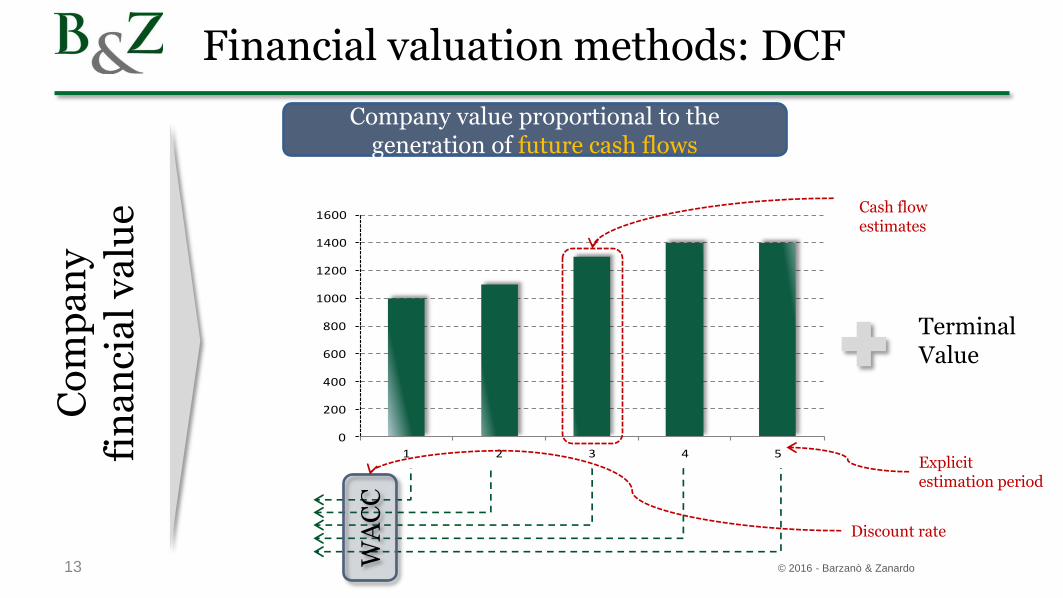

Company value proportional to the generation of future cash flows

Co

mp

an

y

fin

an

cia

l v

alu

e

WA

CC

0

200

400

600

800

1000

1200

1400

1600

1 2 3 4 5Explicit estimation period

Discount rate

TerminalValue

Cash flow estimates

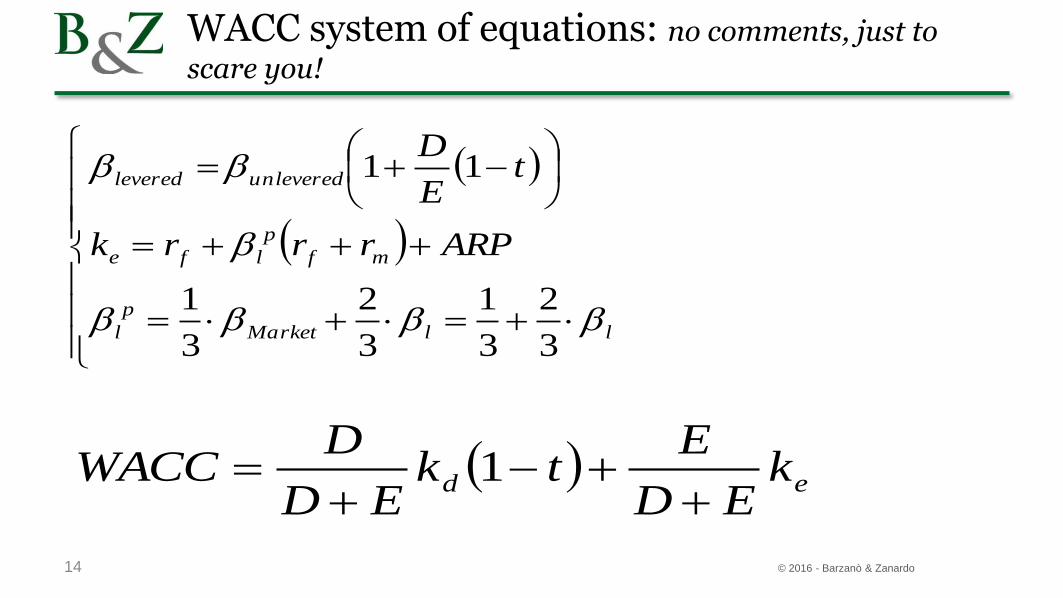

WACC system of equations: no comments, just to

scare you!

llMarket

p

l

mf

p

lfe

unleveredlevered

ARPrrrk

tE

D

3

2

3

1

3

2

3

1

11

14 © 2016 - Barzanò & Zanardo

ed kED

Etk

ED

DWACC

1

Company valuation and IP valuation

15 © 2016 - Barzanò & Zanardo

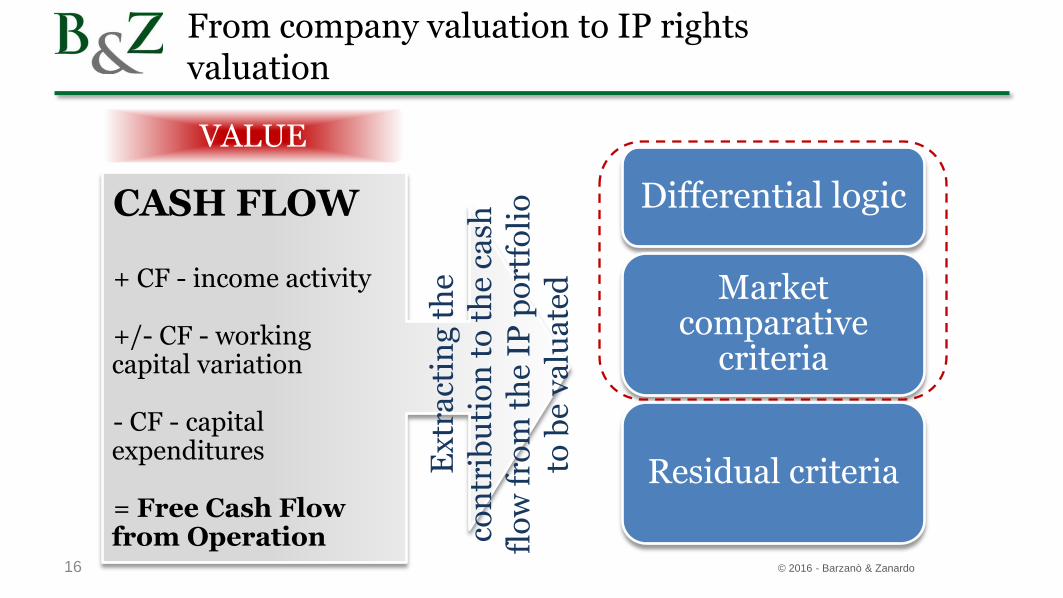

CASH FLOW

+ CF - income activity

+/- CF - working capital variation

- CF - capital expenditures

= Free Cash Flow from Operation

From company valuation to IP rights valuation

Ex

tra

ctin

g t

he

con

trib

uti

on

to

th

e ca

sh

flo

w f

rom

th

e IP

po

rtfo

lio

to

be

va

lua

ted

Differential logic

Market comparative

criteria

Residual criteria

VALUE

16 © 2016 - Barzanò & Zanardo

Scholars

• Differential logic: differential cash flows, differential income (ROS, EBITDA, EBIT),

differential margin (EBITDA indices / Sales, EV/EBITDA), premium price, cost savings,

multiples method (EBITDA/Sales, EBIT/Sales), cost losses, estimates of the damage that

the company undergoes losing the availability of IPRs

• Comparative criteria: comparable transactions, relief from royalty approach,

multiples implicit in the negotiations

• Residual approach: it estimates intangible differential profit as the residual profit after

subtracting to the normalized company profit the tangible and financial asset profits

• Others: real option, scenario analysis

17 © 2016 - Barzanò & Zanardo

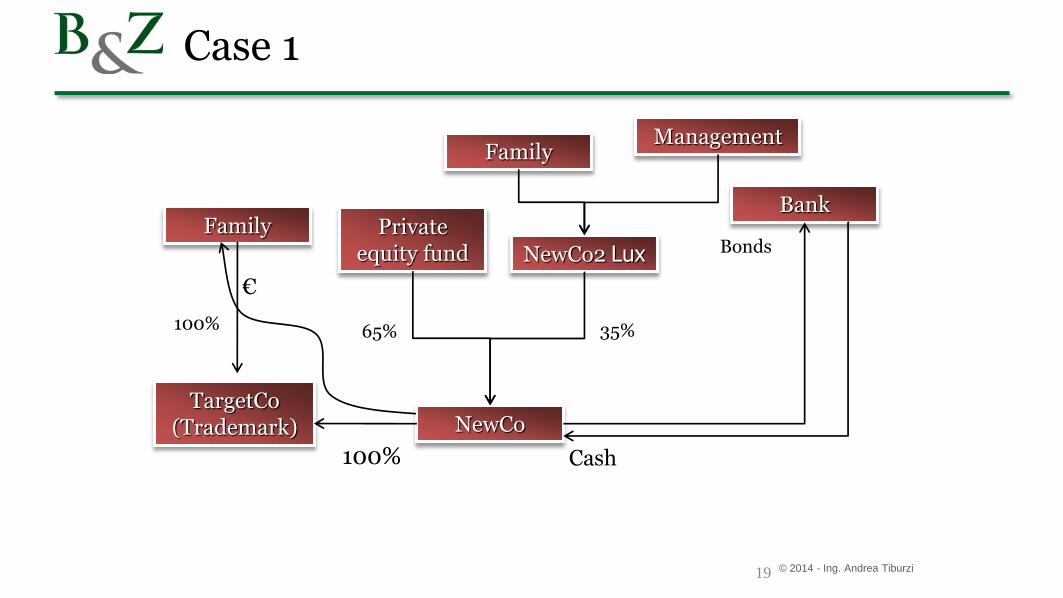

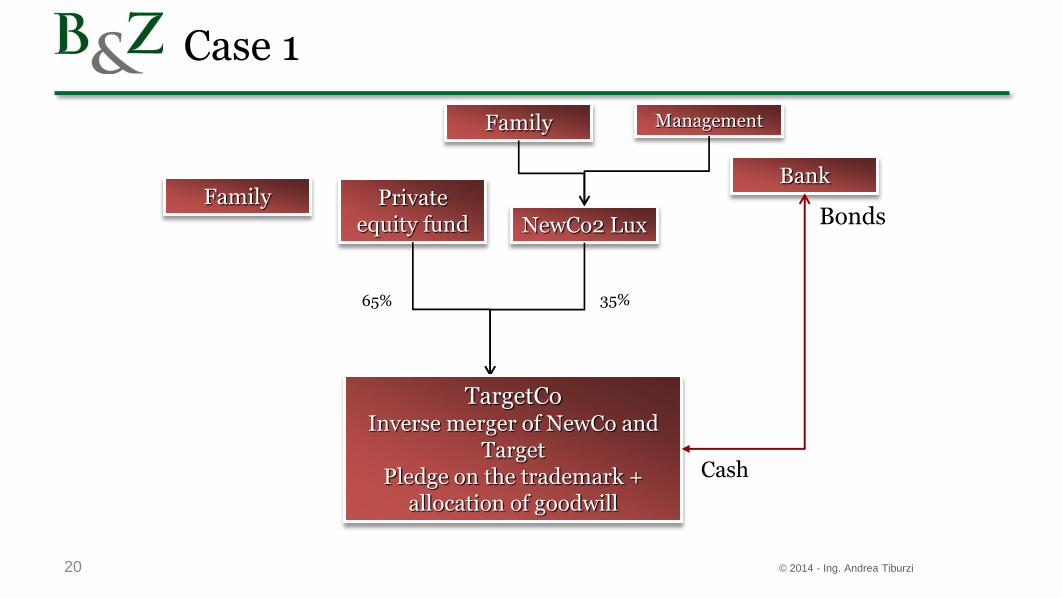

Case 1

• Leveraged buyout by a US private equity fund

• Italian target company active in the food

• Very strong and popular brand

18 © 2014 - Ing. Andrea Tiburzi

19

Bank

Cash

BondsFamily Private

equity fund

TargetCo (Trademark)

100%

NewCo

65%

NewCo2 Lux

35%

FamilyManagement

€

© 2014 - Ing. Andrea Tiburzi

100%

Case 1

Bank

Cash

BondsFamily Private

equity fund

65%

NewCo2 Lux

35%

Family Management

TargetCoInverse merger of NewCo and

TargetPledge on the trademark +

allocation of goodwill

20

Case 1

© 2014 - Ing. Andrea Tiburzi

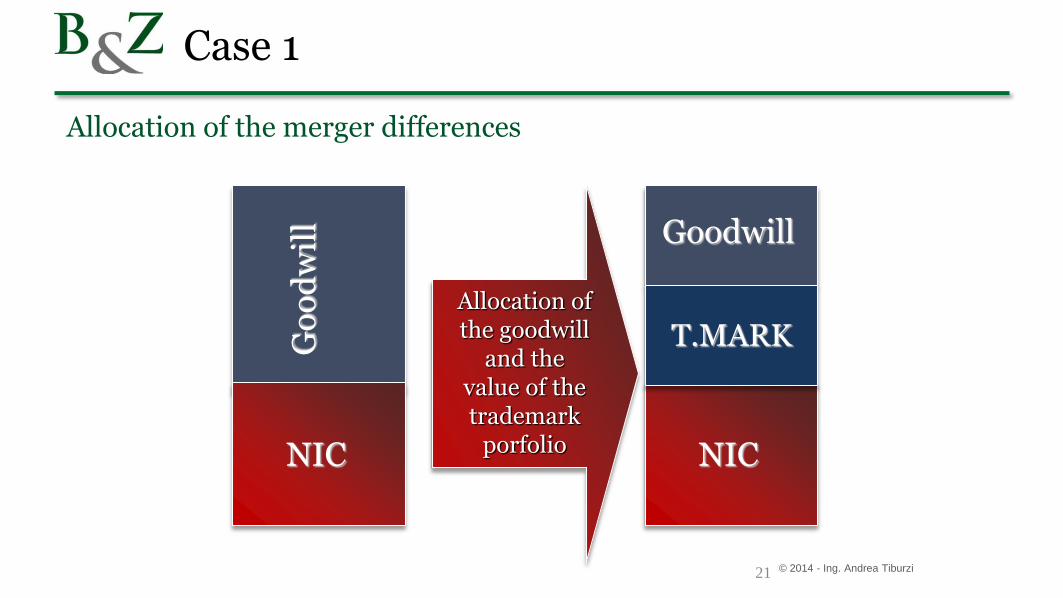

21

NIC

Go

od

wil

l

NIC

Goodwill

T.MARKAllocation of the goodwill

and the value of the trademark

porfolio

© 2014 - Ing. Andrea Tiburzi

Allocation of the merger differences

Case 1

Case 2

• Parties:

– Company active in the chemical process industry (ChemCo) with technologies for the production of biodegradable plastics. High profit margins but production saturation problems

– Oil company (OilCo) also active in the production of industrial chemicals, with a large production site in a structural loss due to low-margin products

22 © 2014 - Ing. Andrea Tiburzi

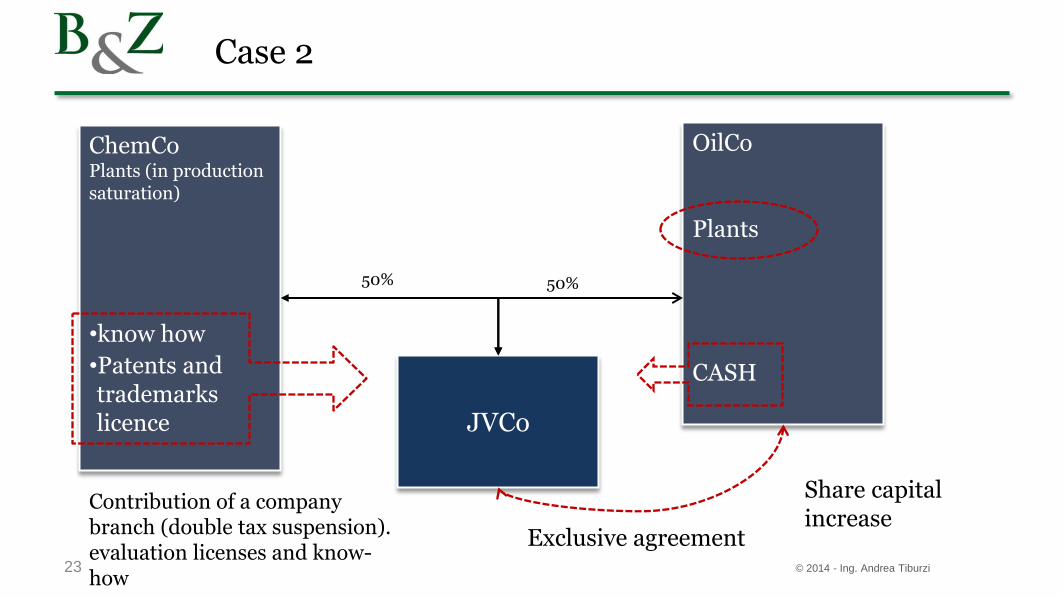

Case 2

23 © 2014 - Ing. Andrea Tiburzi

JVCo

ChemCoPlants (in production saturation)

•know how

OilCo

Plants

CASH

50% 50%

Contribution of a company branch (double tax suspension). evaluation licenses and know-how

Share capitalincrease

Exclusive agreement

•Patents and trademarks licence

“It is money that generates the brightestideas”

F. Fellini

24 © 2016 - Barzanò & Zanardo

And if it was just the opposite ...?

Thank you

Eng. Andrea Tiburzi

Rome Office

Tel.: 06421771

© 2016 - Barzanò & Zanardo25