Embed Size (px)

Citation preview

The Quaide Milleth College For Men

Department of Corporate Secretaryship

VI Sem. Model Examination. March 2015.

Income Tax Law Practice (BYA5C)

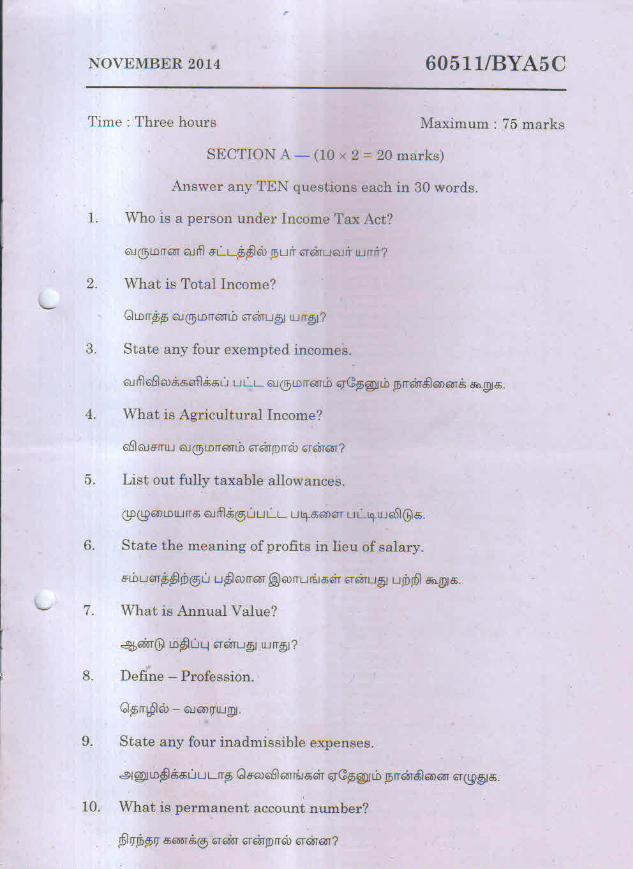

SECTION A – (10 x 2 = 20 marks)

Answer any TEN questions each in 30 words.

1. Who is a person under Income Tax Act?

2. What is Total Income?

3. State any four exempted incomes.

4. What is Agricultural Income?

5. List out fully taxable allowances.

6. State the meaning of profits in lieu of salary.

7. What is Annual Value?

8. Define – Profession.

9. State any four inadmissible expenses.

10. What is permanent account number?

11. Write a note on voluntary filing of return of income.

12. What is self assessment?

SECTION B – (5 x 5 = 25 marks)

Answer any FIVE questions each in 200 words.

13. How to determine residential status of an individual?

14. State the powers of income tax officers.

15. Mr. X went to Germany for diploma course on 5th August 2013 and

returned to India on 25th February 2014. His family (wife and children)

remained in India. He had never been out of India before. What is his

residential status for the previous year 2013-14?

16. Following are the incomes of Mr. X for the year 2013-14.

Rs.

a. Interest on savings bank deposit in Delhi 1,200

b. Income from agriculture in Africa invested in Nepal 10,000

c. Dividend received in UK from an American company 10, 000

d. Pensions received in Japan for services rendered in India, compute gross

total income if he is resident, not ordinarily resident and non-resident.

20, 000

17. From the following details, calculate taxable house rent allowance of Mr.

X, who is living in Chennai. Basic salary Rs. 78,000, Dearness allowance

forming part of salary Rs. 7,800, House rent allowance Rs. 11,700, Rent

paid Rs. 13,200.

18. Calculate net annual value from the following:

Municipal rental value Rs. 28,000, Fair rental value Rs. 34,000, Standard

rent Rs. 35,000, Actual rent Rs. 36,000, Municipal tax paid by the owner

Rs. 1,500.

19. To what extent following are allowed as deductions in computing the

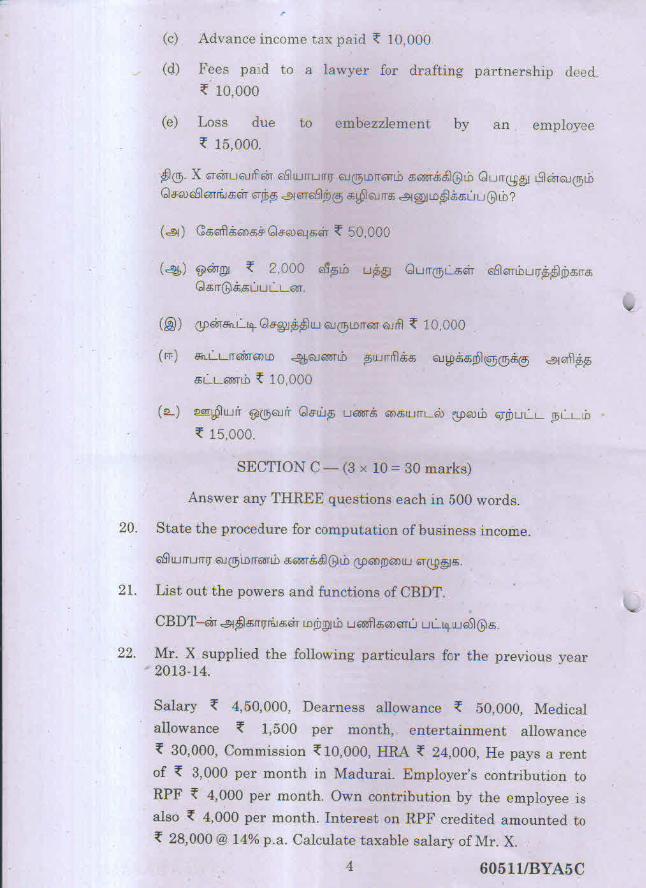

income of business of Mr. X.

a) Entertainment expenditure Rs. 50,000

b) Ten items were presented on advertisement each costing Rs.

2,000.

c) Advance income tax paid Rs. 10,000

d) Fees paid to a lawyer for drafting partnership deed Rs. 10,000

e) Loss due to embezzlement by an employee Rs. 15,000

SECTION C – (3 x 10 = 30 marks)

Answer any THREE questions each in 500 words.

20. State the procedure for computation of business income.

21. List out the powers and functions of CBDT.

22. Mr. X supplied the following particulars for the previous year 2013-14.

Salary Rs. 4,50,000, Dearness allowance Rs. 50,000, Medical allowance

Rs. 1,500 per month, entertainment allowance Rs. 30,000, Commission

Rs. 10,000, HRA Rs. 24,000, He pays a rent of Rs. 3,000 per month in

Madurai. Employer’s contribution to RPF Rs. 4,000 per month. Own

contribution by the employee is also Rs. 4,000 per month. Interest on

RPF credited amounted to Rs. 28,000 @ 14% p.a. Calculate taxable

salary of Mr. X.

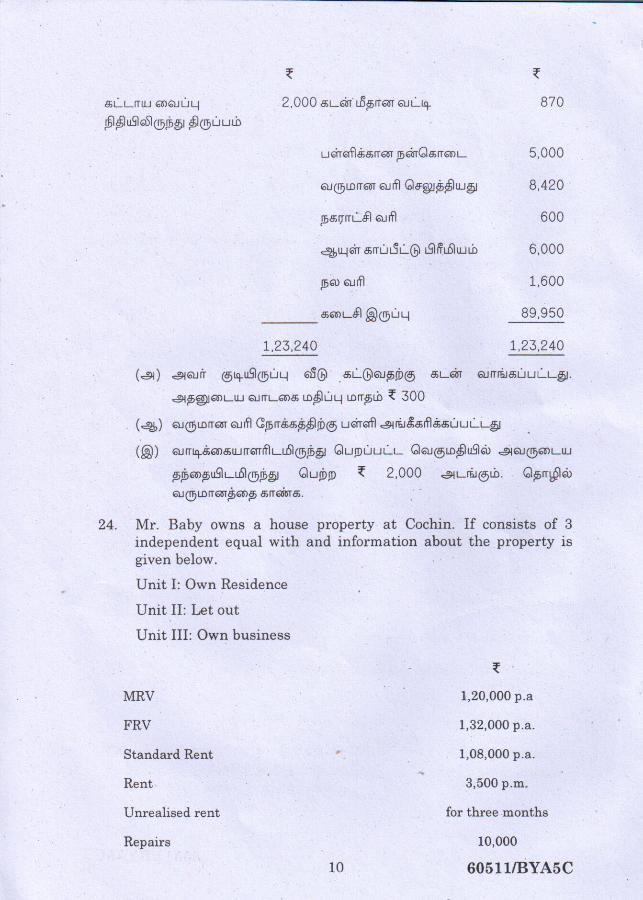

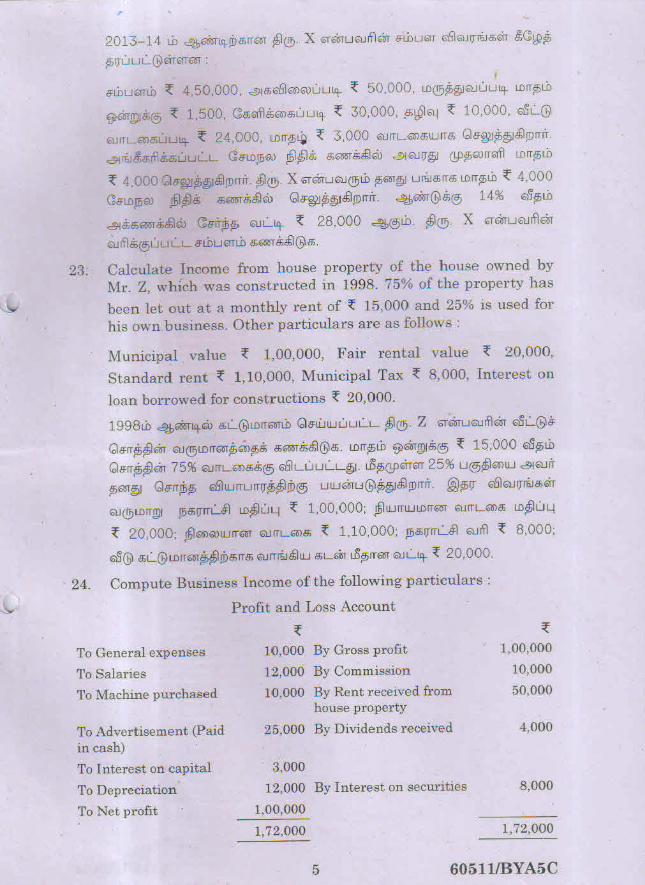

23. Calculate Income from house property of the house owned by Mr. Z,

which was constructed in 1998. 75% of the property has been le out at a

monthly rent of Rs. 15,000 and 25% is used for his own business. Other

particulars are as follows:

Municipal value Rs 1,00,000, Fair rental value Rs. 20,000, Standard rent

Rs. 1,10,000, Municipal Tax Rs. 8,000, Interest on loan borrowed for

constructions Rs. 20,000.

24. Compute Business Income of the following particulars:

Profit and Loss Account

Rs. Rs.

To General expenses 10,000 By Gross profit 1, 00,000

To Salaries 12,000 By commission 10,000

To Machine purchased 10,000 By Rent received from 50,000

house property

To Advertisement 25,000 By Dividends received 4,000

(paid in cash)

To Interest on capital 3,000

To Depreciation 12,000 By Interest on securities 8,000

To Net profit 1, 00,000

_________ _________

1 ,72, 000 1, 72, 000

_________ _________

THE QUAIE MILLETH COLLEGE FOR MEN, MEDAVAKKAM, CHENNAI

DEPARTMENT OF CORPORATE SECTRETARYSHIP

QUESTION BANK AND KEY ANSWERS

INCOME TAX LAW AND PRACTICE I (BYA5C)

BASIC CONCEPTS

Short Answers:

1. Define ‘Assessee’.

2. Who is representative assessee?

3. Who is assessee in default?

4. Write short note on a. Total income, b. Assessee.

5. Define ‘Previous Year’.

6. What is ‘Assessment Year’?

7. What is “income” u/s 2 of the Income Tax Act?

8. Who is a ‘Person’ under the Income Tax Act?

9. What are ‘Gross Total Income’ and ‘Total Income’?

Long Answers:

1. Explain the concept of ‘Income’ and give its features.

2. Distinguish between ‘Assessment Year’ and ‘Previous Year’.

3. Under what circumstances income of a person can be assessed in the same year in which it is

earned?

4.

RESIDENTIAL STATUS:

Short Answers;

1. What is Residential Status?

2. Who is a Resident?

3. Who is not ordinarily resident?

4. Who is nonresident?

5. Explain two basic conditions to determine the Residential status of an individual.

6. What are the incomes deemed to have received in India?

Long Answers:

1. What are different categories of Assessees according to their Residential status? How is this

status determined?

2. Explain the terms: a. Resident, b. Non-resident, c. Not ordinarily resident

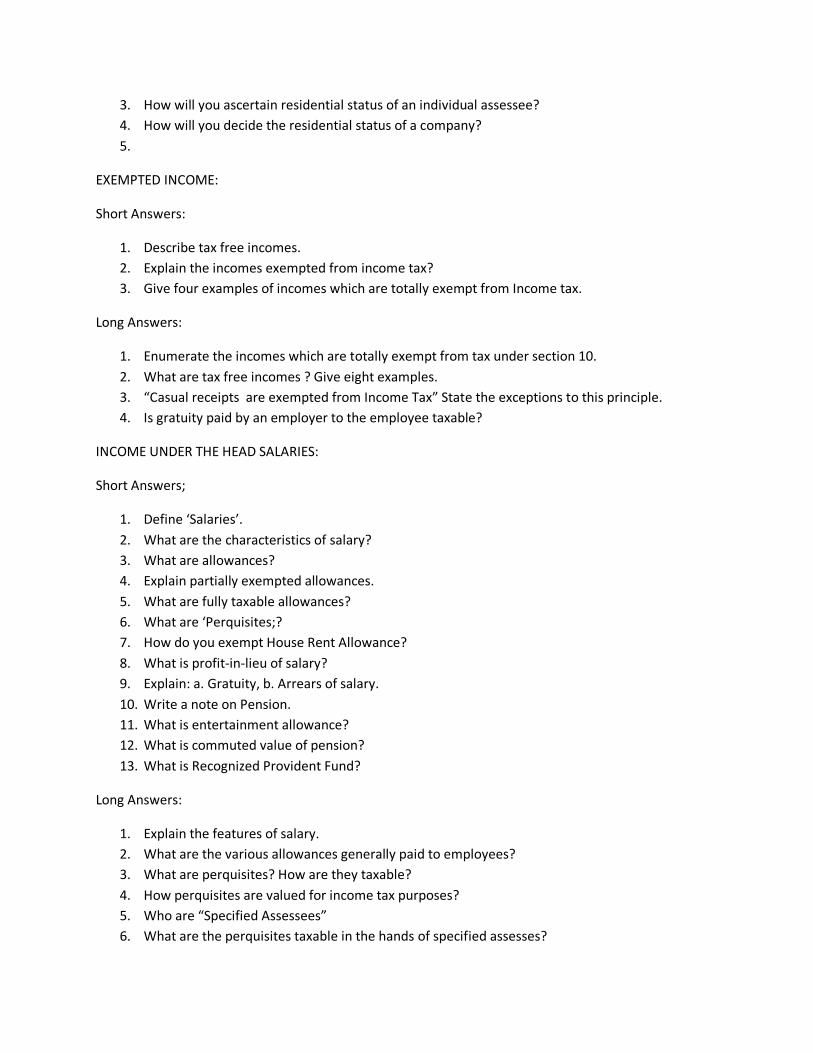

3. How will you ascertain residential status of an individual assessee?

4. How will you decide the residential status of a company?

5.

EXEMPTED INCOME:

Short Answers:

1. Describe tax free incomes.

2. Explain the incomes exempted from income tax?

3. Give four examples of incomes which are totally exempt from Income tax.

Long Answers:

1. Enumerate the incomes which are totally exempt from tax under section 10.

2. What are tax free incomes ? Give eight examples.

3. “Casual receipts are exempted from Income Tax” State the exceptions to this principle.

4. Is gratuity paid by an employer to the employee taxable?

INCOME UNDER THE HEAD SALARIES:

Short Answers;

1. Define ‘Salaries’.

2. What are the characteristics of salary?

3. What are allowances?

4. Explain partially exempted allowances.

5. What are fully taxable allowances?

6. What are ‘Perquisites;?

7. How do you exempt House Rent Allowance?

8. What is profit-in-lieu of salary?

9. Explain: a. Gratuity, b. Arrears of salary.

10. Write a note on Pension.

11. What is entertainment allowance?

12. What is commuted value of pension?

13. What is Recognized Provident Fund?

Long Answers:

1. Explain the features of salary.

2. What are the various allowances generally paid to employees?

3. What are perquisites? How are they taxable?

4. How perquisites are valued for income tax purposes?

5. Who are “Specified Assessees”

6. What are the perquisites taxable in the hands of specified assesses?

7. Explain various types of Provident Funds.

8. Distinguish between Recognized and Unrecognized Provident Funds.

INCOME FROM HOUSE PROPERTY

Short Answers:

1. Define Annual Value

2. Define Gross Annual Value. How do you determine Annual value of House properties?

3. How Annual value of a let out house; is determined?

4. How the “Net Annual Value” of a house is determined?

5. Write a note on self-occupied property.

6. Write short notes on: a. unrealized rent b. vacancy allowance

7. Long Answers:

8. What are the circumstances under which a person becomes “Deemed Owner” of a house

property?

9. What deductions are allowed from the Annual value in computing taxable income from House

property?

10. How will you compute income from let out house property?

Profits and Gains from Business or Profession:

Short Answers:

1. What is “Business”?

2. What is “Profession”?

3. What do mean by self-generated assets?

4. What are the provisions relating to Preliminary expenses?

5. Write a note on expenditure on scientific research.

6. What is depreciation?

7. Define ‘Block of Assets’ and ‘Written Down Value’

Long Answers:

1. What are the incomes chargeable to tax under the head ‘Profits and Gains of business or

profession’?

2. Explain the method of computing income from business.

3. Discuss the various expenses that are expressly disallowed in the assessment of Business

Income.

4. Describe some of the admissible and inadmissible deductions while computing the income from

business.

5. Discuss the provisions regarding expenditure on know-how.

6. What are deemed profits? And how are they charged to tax?

INCOME TAX AUTHORITIES

Short Answers:

1. Who are Income tax Authorities?

2. Describe the role of Central Board of Direct Taxes.

3. What are the powers of the Chief Commissioner of Income Tax?

4. Explain lthe powers of Assessing Officer.

5. Mention any three powers of Income Tax Officer.

6. Who is Inspector of Income Tax?

7. What is permanent Account Number?

8. Describe the’ Assessment Procedure’.

9. What is due date of filing return?

10. List out due date of filing of return.

11. What is revised return?

12. What is ‘belated return’?

13. What is ‘Self Assessment’?

14. What is ‘Best Judgment Assessment’?

Long Answers:

1. Mention the various Income Tax Authorities.

2. Describe the powers and function of Central Board of Direct taxes.

3. Describe the procedure for search and seizure by the Income tax authorities.

4. What is defective return? How can it be rectified?

5. What are the different types of Assessments under Income tax law? Explain the procedure of

Regular Assessment.

6. What is Best Judgment Assessment? What are the consequences? What are the remedies

available to the assessee?

7. Under what circumstances can an assessing officer make Ex-Parte Assessment?

8. Describe the procedure for appeal against an assessment?