Embed Size (px)

Citation preview

THE PROBLEM OF NEWSPRINT AND OTHER PRINTING PAPER

by the Intelligence Unit, “THE ECONOMIST”, London.

U N E S C O P A R I S 1 9 4 9

PRESS, FILM AND RADIO IN THE WORLD TODAY. Series of studies published by Unesco.

Publication No 594 of the United Nations Educational, Scientific and Cultural Organization.

Printed in France b y M. Blondin. Copyright b y Unesco, Paris.

F O R E W O R D

In sponsoring this series of studies on specific problems of mass communications, Unesco is complying at once with its constitutional obligation to “further b y all possible means the use of the instruments of mass communications in the work o/ advancing the mutual knowledge and understanding of peoples”, and with the repeatedly expressed desire of experts that Unesco should promote and sponser the publication of technical and sociological works dealing with mass com- munications questions. Surveys of the press, film and radio in the world have shown

that side b y side with purely material needs, which are linked up with the economic and technical development of each coun- try or region, there exists a wide need for knowledge of the use that can be made, and the abuses that must be avoided, of these powerful means of reaching the mind, of influencing the opinions and the way of life, of modern man. The series covers a wide ground, ranging from the profes-

sional training of those who work in press, film and radio to ‘ the organisation of educational radio skrvices, the equipment and operation of mobile cinemas, and €he production, consumption and demand for paper for reading material. But. all -these studies have this in common, that their aim is to provide practical information and, in some cases, advice for all whose interests or whose work lie in the field of mass communications, and thus to spread knowledge of the highest standards that are being attained and the new techniques that are being evolved. To prepare these studies, Unesco has called upon specialists

throughout the world. It is recognised that some of the subjects mag be controversial, but the authors have been left completely free to express their own opinions and to speak with the full

5

outhority of their personal experience., Even should they provoke disagreement, it is felt that only beneficial results can stem from the stimulation of thought and the casting of new light upon these different subjects. Among the dangers which can beset the press, the film and the radio, one of the greatest perhaps is that of routine and stagnation.

* **

Paper for printing books, magazines and newspapers is a material essential to the development of education, science and culture and to the effective enjoyment of freedom of informa- tion both within and between countries. It is for this reason that Unesco has, since its establishment, concerned itself with the problem of the production and distribution of paper, and especially newsprint, in quantities adequate to meet not only present demands but also the growing needs of the world. Shortages in supply and unequal distribution of paper impede the progress of that human welfare and understanding between peoples which are essential to peace.

It is from this point of view that Unesco has approached the problem at sessions of its General Conference, at meetings of its Commission on technical facilities and needs for the press and at conferences organised b y the Economic Commis- sions of the United Nations and b y the Food and Agriculture Organization. In a message to the Preparatory Conference on World Pulp Problems, Montreal, organized b y the Food and Agriculture Organization in association with the Canadian Government, the Director-General of Unesco said:

“It is not for Unesco to suggest here remedies for this situa- tion. But it is Unesco’s duty to appeal on each occasion to the goodwill of all in order to correct as far as possible such inequality in the distribution of a product so essential for the intellectual and social progress of humanity.” The object of this study is to present in as non-technical

fashion as possible as many of the facts as possible and to indicate the nature and size of the problem both for today and tomorrow. The study, in this present form, has been prepared for Unesco b y the Intelligence Unit of the London Economist; this Unit had at its disposal all the information available from Unesco and from the Food and Agriculture Orzanization’s Forestry Division with which Unesco works closely in its endeavours to promote effective and appropriate action in fhin field.

R

C O N T E N T S

e w e CHAPTER I PAPERMAKING .............................. 9 CHAPTER 11 PULPWOOD AND WOOD PULP. ................. 17 .

Pulpwood W o o d pulp General Europe North America Other regions International trade

CHAPTER III PRINTING PAPER .......................... 27 - Characteristics Importance of printing paper Location and structure of the paper industry

Production Capacity Producers output

Consumption Growth In equality

CHAPTER IV NEWSPRINT ................................. 37 Characteristics of the newsprint industry Production

Distribution of capacity Meaning of capacity The production problem output

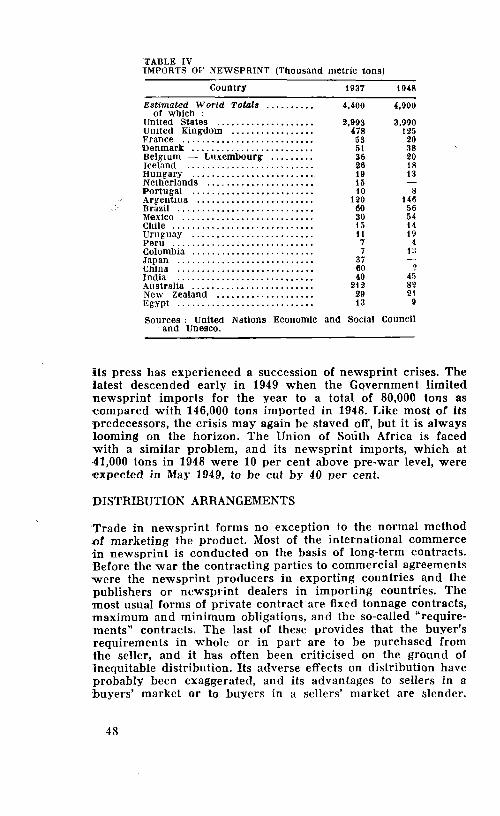

Distribution of exports and imports Distribution arrangements

International trade

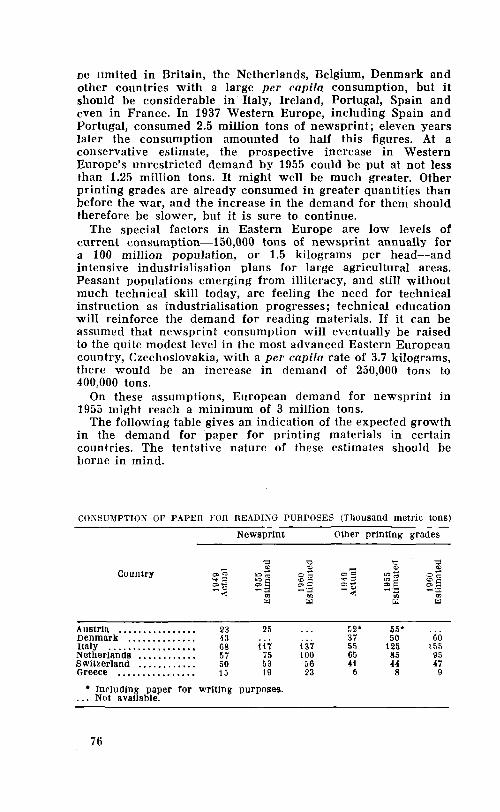

Consumption Growth Inequality Restrictions on consumption The newsprint balance

CHAPTER V DBMAND TRENDS ............................ 63 North America Consumption of printing paper and industrial activity Post-war boom Saturation United States demand and Canadian production

A rising pre-war trend Post-war economic revival Rising demand for paper resumed?

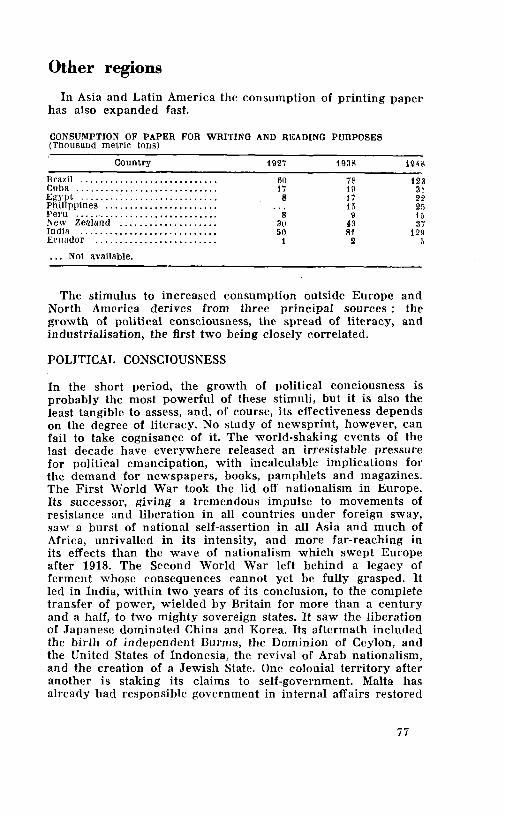

Other regions Political consciousness Literacy Industrialisation Expanding demand for paper for reading materials

Europe

Prices and costs

CHAPTER VI BASIC FACTORS AFFECTING THE SUPPLY IN THE FUTURE .......................... 91

R a w materials Softwood origin Newly developed raw materials

Capital and equipment Currency

............................................ CONCLUSION s 109

8

C H A P T E R I

Papermaking

An ancient product

Paper is an age-old product, and its manufacture is a simple process, although nowadays it is mainly carried on by highly complex machinery. The fundamental principles of paper- making have changed little since its inception in China nearly two thousand years ago, although the basic raw materials are different. Fibres in the form of pulp and obtained from wood or other fibrous substances are inter-mixed with water and then passed over a screen through whose openings the water is drained off until a thin layer of inter-twined, moist fibre is formed on its flat surface. The thin layer which remains is paper. Paper has been defined as a substance made in the form of

thin sheets or leaves from disintegrated fibre derived from rags, straw, bark, wood or other fibrous material. True paper must necessarily be made from fibre which has been treated untir each individual filament is a separate unit. Papyrus, which was used centuries before paper, is not made from disintegrate& fibre. The product is obtained by slicing the stalks of the papyrus plant, and it is simply a laminated material. Like other writing materials of ancient origin such as parchment, papyrus is not classed as true paper. The conventional date normally given for the invention of paper

by the Chinese is A.D.105. For five hundred years the Chinese succeeded in keeping the art of making paper a well guarded secret. Thereafter it spread into Central Asia, Persia and South- ern Russia. In the early Middle Ages paper found its way into Arabia, Egypt and Morocco and thence, after another lengthy interval, into the Western Mediterranean. It was only in the thirteenth century that it was introduced into Northern Europe. Well over a thousand years thus elapsed before the invention completed its travels from East to West. It took many more years until it was firmly established as a handicraft in Europe, where at first it met with little favour. The early paper of Europe was more expensive and less resistant than parchment, which was used for book-making, and its uses were limited for a: long time. Moreover, its Moslem origin rendered the new art suspect to Christendom.

In quest for raw materials

The first milestone in the history of paper outside the Orient was the invention of the printing press. Although the design .of the early printing presses was strongly influenced by, and necessarily adapted to, the grades of paper then available, the growing use of the new invention created a permanently larger and expanding outlet for paper. The technique of making paper was steadily improved and the craft was eventually adopted in one European country after another. Until the second half ‘of the eighteenth century, however, all paper made in the West was fabricated exclusively from linen or cotten rags. While paper made from these materials was of high quality, its production became less and less able to satisfy requirements. The eighteenth century was an era of great intellectual ferment and saw a wide diffusion of popular knowledge, accompanied ’by a growing clamour for more books, newspapers and peri- odicals. Numerous books for general readership were published and many fresh newspapers, periodicals and popular magazines were established. The rise in the use of paper which ensued was unprecedented and caused a severe shortage of the product. Appeals for increased collection of rags were made throughout Europe and Norih America, but produced no tangible results. So keenly was the paper shortage felt that intensive researches

were conducted into the suitability of additional fibrous materials. There was no thought then of replacing scarce cotton and linen rags altogether. To supplement thc traditional materials, however, alternative fibres had to be not only more abundant, but also more economic to process and convert into paper. Evidently the need for the printed word in response to .a rising demand for reading matter had shifted the demand for paper from considerations of quality to quantity and cheap- ness. The quest for new papermaking materials yielded its Arst fruits in 1801. In that year an English papermaker was granted a patent for the manufacture of paper from straw, hay, thistles, waste and refuse of hemp and flax, and other kinds of vegetable fibres. Straw thus preceded the use of wood. The patentee founded a company and set up in London a paper mill, the Arst of its kind in the West, for the extensive utilisation on a commercial scale of vegetable fibres other than those of cotton and linen rags. The enterprise proved a costly financial failure and had to be abandoned after three years. Nevertheless, this venture in new raw materials was destined to be the precursor of the modern wood based paper industry, and it is rightly regarded as another milestone in the history of papermaking.

10

The papermaking machine

The third milestone was the invention of the papermaking machine. Until the beginning of the nineteenth century all paper was made by hand. The tool employed was a sieve-like mould which~was dipped into a vat filled with macerated fibres floating on water. When the mould was lifted it was covered with a thin layer of matted fibres, that is, a sheet of paper. The size of the sheet was limited by the size of the mould which hand labour could conveniently handle. Paper, therefore, was dear and scarce as well as small in its dimensions. The urgent need for more and cheaper paper stimulated the search for cheaper papermaking materials, no less than for more effective and cheaper methods of paper production. In an age of rapid industrial change a mechanical device naturally suggested itself as the most appropriate method to raise productive efficiency. Foremost among the pioneers endeavouring to produce paner uy machine was a Frenchman, Nicholas-Louis Robert. This ingenious inventor was the first in the field to construct a machine designed to supplant the old and laborious hand processes. After several unsuccessful efforts his first workable model appeared in 1798, followed by various improvements in the next few years. Robert’s model was based upon the ancient practice of papermaking, and all future modifications of the paper machine, by himself and his successors, embodied the principles of his original model. But Robert’s device did not perform all stages of paper-

making by mechanical means. Although the moist sheets which it turned out were much cheaper as well as far greater in width and length than those made by hand, they still had to be taken from the machine by hand labour to be hung up to dry. Simul- taneous drying followed close on the invention of Robert’s machine, but the large-scale production of paper in the form of reels, instead of single sheets, belonged to a later age. This stage of manufacture was perfected towards the middle of the nineteenth century, coinciding with the advent of the rotary printing press. The rotary press, which nowadays print all newspapers with a large circulation, must, of course, be fed from paper delivered in reels. Moreover, operating at high speed, this type of press necessitates the use of paper grades able to meet more exacting specifications. Earlier printing presses, including flatbed presses, modernised versions of which are still in use for the publication of newspapers with small circulations, operated at much lower speeds, and the paper used for them needed neither the tensile strength nor the uniformity of quality required for high speed printing on the rotary press. One interesting fact about the paper industry is that its evolution is a record of constantly interacting inven- tions and improvements both in papermaking and printing.

11

A place of prominence among the men who contributed to the perfection of the machine process is due to the Fourdrinier brothers, who were contemporaries of Robert. To this day the papermaking machine is named after them. The function of the Fourdrinier machine is to convert the mass of macerated fibres mixed with water and chemical solutions into a thin web of dry paper which is either cut in sheets, or as in the case of newsprint, wound off the machine into large reels containing as much as four miles of paper up to twenty-five feet wide. The important thing about the Fourdrinier machine is its continuity. From the forming of the mixture over an endless moving screen and the subsequent emergence of a moist sheet, through a variety of drying processes, to the final touches at the winding or cutting stage, this machine performs the whole process of paper manufacture in a series of continuous operations. Every Fourdrinier machine works on this principle, irrespective of the capacity, the price, and the grades of paper which it produces. Indeed the modern Fourdrinier machine is adapted to the production of any grade of paper. It speaks for the ingenuity of the inventors that the succession of refinements and improvements which engineers have added to the machine since it made its first appearance one hundred and forty years ago has left its basic structure unchanged. The width and opera- tional speed of the machine have immensely increased, its drying mechanisms have been steadily improved, the range of its prod- ucts has become more and more diversified; yet its early design has stood the tests of time. The Fourdrinier machine made the modern paper industry, and the efficient application of the principle of continuity was its outstanding merit.

Harnessing wood and water

Before the industry could develop as a large-scale and low cost enterprise it had to surmount yet one more obstacle: the shortage of raw materials. So long as papermaking materials were scarce and dear, the applications of the Fourdrinier machine were inevitably few and confined to a small number of industrialised countries. To be economic this expensive machine has to be run as near as possible to capacity. But the dearth of raw materials prior to the use of wood severely limited the scope for production as well as the extent of the producers’ market. The very existence of the papermaking machine, however, made it imperative to search for new papermaking materials, Success w a s not long in coming. It was provided by the epoch-making discovery that paper could be made from wood, which was cheap and in apparently unlimited supp1y.l This discovery finally swept away all remaining ,obstacles to the paper

i. The discovery alone was not siimcient, since a way had to be found to extract the wood fibres by a grinding process.

12

industry’s expansion. But it did more than that. The introduction of the new material linked the future of paper production to’ a set of entirely new industries which spring up all over the vast forest areas of the Northern Hemisphere. It allowed the papermaking machine to come into its own once raw materials were abundant and cheap. It made possible a steep increase in output at fast decreasing costs precisely at the time when paper was becoming daily more essential for industrial and domestic uses alike. Wood pulp revolutionised paper making: its coming w a s the fourth milestone in the history of paper. Thereafter nothing could arrest the rise of the modern paper industry. The use of wood pulp reinforced the importance of water to

the paper industry. Papermaking in the wood pulp age requires water for three purposes: as a means of transportation, as an agent in manufacturing and as a source of power. Pulpwood is bulky and costly to transport overland, and in densely forested Scandinavia and Canada, with their wealth of waterways, rivers are normally used to float the logs down to the mills. Most of the early mills were, in fact, erected on the banks of streams. Secondly, water of fine quality is an essential ingredient in the manufacture of both pulp and paper. As a papermaker once declared: “the manufacture of paper consists of putting water into wood and taking it out again.” Chemical treatment has diminished the importance of water, but has by no means dispensed with its use. Thirdly, pulp and paper mills are enormous users of energy, and water is by far the cheapest source of power. In Canada, for example, the pulp and paper industry consumes more than one-third of all the electric energy generated. Without ample and advantageously located resources of hydro-electric power the paper industry could never have developed as a low cost producer.

Wood pulp The commercial use of wood pulp in papermaking began in the eighteen-fifties, following a century of pioneer attempts and vain experiments. At first the change-over from rag to all wood paper was slow and uneven. For many years wood pulp was mixed with pulp made from straw, rags and other fibrous materials. The transitional period was spread over several *

decades. But the use of wood pulp was destined to expand until it achieved a virtual monopoly among papermaking materials. By 1870 cotton and linen rags had already ceased to be the principal soiirce of supplies. To-day wood pulp accounts for more than 90 per cent of the virgin pulp fibre consumed by the world‘s paper and board industries and is the chief, or sole, constituent of the principal paper products, including newsprint. Cotton and linen rags are now used only for the finest papers,

13

and even these may contain up to 50 per cent wood pulp. The . other raw materials, including esparto 'grass, which is grown mainly in North Africa, and straw are only of minor impor- tance. Periodic attempts to utilise straw whose production- though, unfortunately, not its transportation-is gratuitous, have never been very successful. Small quantities of straw go into certain grades of ordinary paper other than printing paper and newsprint, but the chief product is straw board. Wood is the most versatile and least homogeneous of raw

materials. It has easily the widest range of applications running into tens of thousands, and timber exists in uncounted varieties, of which about three thousand are in commercial use. But all woods can be divided in two main groups; hardwoods and soft- woods. Hardwoods are an immense group which comprises beech, oak, ash, maple and other species of the temperate zone, and various tropical woods including teak and mahogany. Hard- woods possess great strength, toughness and durability, and are eminently suited for the manufacture of furniture and for heavy constructional work. Softwoods comprise the less numer- ous species of the conifer family whose principal members are the spruce, fir, larch and cedar. Softwoods are, as the name implies, easy to work, and are used in light manufacturing processes and building. Wood pulp is at present made mainly from softwood species, and in particular from spruce. But experiments, before the war in Germany and the United States, and more recently in Sweden, Australia and French West Africa, have suggested the possibility of utilizing more hard- wood which at one time was widely held to be quite unsuit- able for pulping. A new and important source of pulp which was unused before the nineteen-thirties is the Southern pine.1 For several years Kraft wrapping paper and fibre boards have already been made successfully from the pulp of the southern pine, and the production of newsprint from this material is now emerging from the experimental stage. Pulp production is a comparatively small user of timber and absorbs rather less than 10 per cent of world timber supplies. Even in Canada, the world's largest producer of paper, papermaking has never accounted in any one year for a large proportion of the tqtal lumber felled. Wood pulp is processed chemically or mechanically from

pulpwood for use in the manufacture of paper, rayon or other cellulose products. Pulpwood is the name given to woods suit- able for the manufacture of pulp; it is unprocessed material stripped of the bark and is usually supplied in the form of logs. Pulp obtained by the mechanical process is merely ground wood reduced to fibre by revolving grinders under cold or hot treatment and with the application of quantities of water. Mechanical pulp, or groundwood as it is sometimes called, is

1. So called because it was nrst used for pulp manufacture in the Southern States of the U. S.

14

made from the softer woods, contains a fairly high percentage of impurities and lacks permanence. Paper manufactured from mechanical pulp is liable to deterioration after exposure to light and air; on the other hand it is cheap and possesses great absorbency. Mechanical pulp is used extensively in the manufact- ure of newsprint, book paper and other printing grades. Chemical pulp is produced by cooking pulpwood cut into small chips with a chemical agent which readily dissolves most of the impurities binding the fibres. Several cooking processes have been devised, but the two most usual ones are the sulphite and the sulphate processes. Chemical treatment is more expen- sive than grinding and produces higher grade pulps more or less free from impurities, the top grades approaching cellulose in a purified state. Chemical pulps vary considerably in their physical properties and their uses vary accordingly, from writing papers which require softness and smoothness to Wrap- ping and industrial papers which require strength and durabil- ity. A few printing papers are made wholly from chemical pulp, and many contain admixtures in varying degrees. The best grade of chemical pulp is used in the manufacture of rayon, plastics, cellophane and photographic films. When used for theses purposes it is known as dissolving pulp or simplv cellulose.

Printing paper Printing grades and newsprint are often put into a category apart from the rest of the paper products. Newsprint has been defined as the grade of paper used in ,the regular editions of daily and weekly newspapers. It is normally composed of 75 per cent to 85 per cent of mechanical pulp and 25 to 15 per cent of unbleached chemical pulp made by the sulphite process. Book paper and certain other printing grades frequently contain a higher proportion of chemical to mechanical pulp. High quality book paper is made from bleached suplhite pulp.' The properties peculiar to newsprint are light weight and

rapid ink absorbing power combined with great tensile strength to enable the product to withstand the strain of running on fast newspaper presses. Where newspapers are printed on rotary presses, as most of them are, newsprint must be supplied in reels. Other printing grades are also made in reels but are often cut up by the makers and delivered to the printers in sheets adapted to flatbed presses on which all books, most magazines and some periodicals are printed. Modern flatbed

i. AS a result of the many different grades of printing paper as opposed to newsprint it 1s often dflflcult to obtain complete or accurate information upon them. Most nations consume about three times as much newsprint as all other types or printing paper.

15

presses are often used to print newspapers and can be fed from reels at great speed. Newsprint is a mass product and the largest and fastest paper

machines are employed in its manufacture. The largest news- print machines ever constructed have a capacity of 50,000 tons a year and turn out newsprint at the rate of 2,000 feet per minute.

,

16

C H A P T E R I 1

Pulpwood and wood pulp

Pulpwood Pulpwood is usually the by-product of forest use, and the proportion of pulpwood within the total annual cut varies great- ly, according to forest management. Good forest management means heavy thinnings and yields a lot more pulpwood than if indifferent forest management simply allows a tree to grow without much care. An increasing amount of the raw material needs for pulp is being supplied from logging, sawmill, and other industrial waste. As a result it follows that production is somewhat elastic. The vast bulk of the world’s principal raw material for pulp

and paper manufacture is produced and processed in North America, Europe and the Soviet Union. In 1937 these three regions accounted for 48 per cent, 41 per cent and 7 per cent respectively of a total pulpwood output of nearly 100 million cubic metres (Table I). Canada alone supplied 40 per cent of world exports, followed by the Soviet Union with 30 per cent, Finland 16 per cent, Austria 5 per cent, ‘Czechoslovakia 4 per cent and Poland 3 per cent. All but about 2 per cent of Canada’s exports was taken by the United States, while most of the Soviet Union’s large exportable surplus, constituting 42 per cent of the annual supply, was available to meet Europe’s equally large deficiency. World output has appreciably expanded since 1937. It

amounted to 111 million cubic metres in 1947 including the Soviet Union, and to an estimated 120 million cubic metres in 1949. To this figure should be added an amount around 10 million cubic metres for the Soviet Union, for which no accurate statistics are available. Owing to a great many factors, including the war, North America has become the centre of production. But in 1949 Europe’s output was substantially below the 1937 level and its share of the world total was only one-third, whereas North America’s output was almost double the 1937 level and constituted roughly two-thirds of the world total. Pre-war levels were regained in Sweden, Europe’s largest producer of pulpwood but remained distant in such countries

’

17

TABLE I PULPWOOD (Thousand cubic metres solid volume)

1 9 3 7 * I 9 4 9 - Provisional

Country

~

Estimated World Totals ....... Europe ........................ of which: Sweden ....................... Finland ....................... Norwag ....................... Germany ...................... Czechoslovakia ................ Austria ....................... Poland ........................ Italy .......................... France ........................ United Kingdom ................ Belgium ...................... Switzerland ................... u.s.s.1i. .................... North America ................ United States .................. Canada ** .................... Latin America ................. Asia .......................... nf which: Japan *** ..................... Oceania ....................... of which: Australia ......................

99,500 47,960 -3.600

18.200 - 170 10.400 +1,540 5,300 - 560 5,700 -3,140

1,900 + 500 1.200 + 340 800 - 600 - 800 - 330 - 180

240 - 120 6,700 +2,820 40,800 + 230 20,800 -3,820 20.000 +4,050

200 - 3,800 - 3,500 -

2.300 + 370

- -

- -

120,285 120,680 42,115 41,685 + 4ii 17.000 8,000 3,950 6,020 1.800 1,050 800 850 910 90 175 450

17,200 7,500 4,000 4.870 1,240 1,400 800 850

1,960 210 190 450

200 500 50

,150 5 60 I50 - - ,050 120 15 -

... ... 76,530 76,610 - -86 45,645 50,490 -4,845 30,885 26,120 +4.565

1,645 1,700 - 53 340 340 - 311 311 -

* Consumption flgures by countries are not available. World consumption is estimated at 98,000,000 ciibic metres solid volume.

** Includlng Newfoundland. *** Jauan Drouer. ... Not aviilgble. Source: Report of the Prwaratory Conference on World Pulu Problems. 1949.

as Finland, Norway, Czechoslovakia and Poland. The recent increase in the output of pulpwood in Germany was deter- mined by the temporary overcutting of German forests. In the near future Germany as a whole will produce substantially less pulpwood than before the war. By comparison, production in Canada was up by about one-half and showed a twofold increase in the United States. United States consumption, how- ever, has expanded faster than has domestic production, and the resultant deficit is larger, therefore, than it was in 1937. In 1939 it equalled the whole of the Canadian surplus. The same trend incidentally, is also visible in woodpulp and news- print. The decline in European pulpwood consumption in the post-

war period has been aggravated by the virtual disappearance of Russian exports, and it has been accompanied by a con- traction of the intra-European pulpwood trade. In 1949 Europe consumed less than one-third of the world's pulpwood

18

production, against an estimated one-half in 1937. Post-war figures for Russian output are not available, but it is known that the rehabilitation of devasted areas and the development of a domestic pulp industry absorb large quantities of avail- able timber resources. In consequence, the pulpwood supplies of the rest of Europe are now to a greater extent dependent on the size of the current output, although diversions to relieve shortages of coal, pitprops and timber as well as for reconstruc- tion purposes, are now smaller than during the immediate post- war era. The interruption of German pulpwood imports has reduced

the impact of suspended Russian exports on European con- sumption. Germany has in fact exchanged its pre-war r61e as Europe’s largest pulpwood importer against that of Europe’s largest exporter, the French zone contributing a very large proportion to total European exports. Exports from Czecho- slovakia have improved and are considerably larger than in 1937. On the other hand, exports from Finland have sharply declined, and the large pre-war surpluses available for export from a number of European countries have been transformed into deficits. None of the other regions produces at present much pulp-

wood. Before the war Japan had a sizeable output, but in the early post-war period, when all Japanese industry was in eclipse pulpwood output fell to a fraction of the pre-war level, although it has made some recovery since. In Oceania the first pulp and newsprint mills were erected during the war and pulpwood production from hardwood species was undertaken simultaneously. Australia already accounts for 3 per cent of world output of pulpwood. Vast forest areas are located in Africa, but they are virtually undeveloped, except in parts of the Union of South Africa, and are almost wholly covered by hardwood species. Latin America’s forests are vaster still, but the pulp industry of this continent is so undeveloped that few local outlets for pulpwood production exist at present. The current share of this region of the world is only 4 per cent. The n’ear East and North Africa are almost bare of forested areas.

Wood pulp GENERAL

The location of a pulp industry is primarily determined by consumer needs and has caused in turn the development of the pulpwood resources. It is marked by the preponderance of North America and Europe. Pulp consumption is largest in industrialised countries with a high national income and shows a similar regional distribution. With the outstanding exception of the United Kingdom, which imports 90 per cent of its pulp

19

requirements, and the Netherlands, many of the important consuming countries are themselves substantial pulp producers, For wood pulp, like pulpwood, the effects of the war have

caused a profound regional redistribution resulting in the emergence of North America as the world’s largest producing and by far the largest consuming region.

~~

Production Consumption Per cent of Per cent or world total world total

1937 1940* 1937 1949’

Europe .......................... 49 31 42 29 North America .................. 46 65 51 65

* Provisional.

In terms of tonnages the setback was less severe for Europe.

Production Consumption

Europe .......................... 11.6 8.7 -32 9.8 8.1 --2I North America .................. 11.0 18.4 4-67 12.1 18.9 -+56

* Provisional.

The rest of the world has a current output of about 2 million tons, of which one half is produced in the Soviet Union, and it consumes about half a million tons more. At 28 million tons in 1948, world production (Table 11) was

well above the 1947 quantity and slightly in excess of world consumption (Table III), while both achieved all-time records. By comparison, production and consumption in 1937, the best pre-war year, balanced each other. A further increase in production has been reported for 1949,

but despite this new record some 3 million tons of pulp producing capacity are at present surplus to requirements as measured by effective demand. At the same time many countries outside North America are unable to obtain enough pulp to allow their paper industries to operate at capacity. This paradox is explained by physical shortages of pulpwood limiting pulp production in Europe combined with shortages of currency required for the import of raw materials.

20

TABLE I1 CAPACITY - PRODUCTION OF WOODPULP (Thousand metric tons)

1 9 3 7 1 0 4 8

Chemical Mechanical W ~ ~ ~ ~ t l p

Estimated WOTld total 14480 10,000 24 480 19 720 18 650 1 1 800 9 580 31 520 28.230

Europe ...... 7i360 4,320 11:680 61140 5:020 3:830 2;580 9:970 7,600 of which :

Sweden ..... 2,790 734 3,524 2.Y46 2,224 800 625 3.546 2,849 Finlan& ..... 1.481 820 2,301 1,466 1,040 1,060 400 2,526 1.440 Norway ..... 552 543 1.095 621 386 695 400 1,316 786 Germany .... 1,349 f,l34 2.483 . . . . . . . . . . . . . . . . . . France ...... 105 251 356 194 171 350 291 544 462 Czecho- slovakia ... 270 73 343 319 241 inn 74 419 315 .....

Italy ........ 37 150 187 64 54 150 140 214 194 Netherlands . 50 71 121 60 25 70 15 130 40 Austria ...... 304 110 414 294 145 110 70 404 215 llnltcrl Kingdom ..

Switzerland . . Poland ...... Belgium ..... U. S. S. R. .. North Ame7tca United States . Canada ...... Newroundland. Latin America.

or which : Brazil ....... Mexico ...... Near East and North Africa

Africa ....... South and East A s h .. of which :

Japan ....... Oceania ..... of which :

Australia ....

18 55 93 - 435

6,150 4,502 1,594

53

530

526 -

183 201 15 5 2&0 35 90 75 75 60 81 174 . . . . . . . . .

66 32 28 45

4,800 10,950 12,3iO 12.7iO 6,GO 1461 5 963 9 414 9 703 2 468 31071 41665 2:785 21940 4:128 268 321 136 98 322 25 25 120 75 135

53 25 87 5 5 64 47 30

5 5 15 5 5 15 15 -

460 990 425 140 455

375 901 426 141 454 60 60 50

60 60 36

- 405 840

_ _ - -

- - _ _

52 225 57 60 135 135

45 77 73 . . . . . . . . .

6 3 0 19,iGo ia.iii 1,974 11,882 11.67'1 3,951 6,913 6,891 299 458 397 115 255 190

80 140 105 I8 94 65

5 20 10 - 15 15

200 880 340

191 880 332 45 110 105

34 96 94

... Not available. Source : Report of the Preparatory Conference on World Pulp Problems, 1040.

EUROPE

The decline in output has been sharpest among some of the countries in Europe with the largest pulp industries: Germany, Norway and Finland, for example. One immediate cause, has been the shortage of raw materials, reflecting equally the decline in imports and the depletion of local forests, and, to a smaller degree, the use of pulpwood as a fuel and constructional material. But the Scandinavian industries were also hampered

21

TABLE 111 CONSUMPTION OF WooUPuLP (l'houssnd metric tons)

1 9 3 7 1 9 4 8

9,995 24,470 18,800 9,200 28,000 4,040 9,775 4,400 2,600 7.000

Estiniated World Totals. Europe ................ United Kingdom ....... Germany ...............

of which :

France ................. Sweden ................ Finland ................ Norway ................ Italy ................... Netherlands ............ Czechoslovakia ......... Belgium ................ Aufitria ................. Poland ................. Switzerland ............ i3.S.S.R ............. North Amerlca ......... United States .......... Canada ................. Newfoundland .......... Latin Amerlca .......... Brazil .................. Mexico ................. Argentina .............. Wear East arid North Africa ................

Africa .................. South and South East Asia ..................

Japan .................. China .................. India ................... Oceania ................ Australia ............... N e w Zealand ...........

of which :

of which :

14,475 5,735

...

... 603 600 302 221 ... ... ... ... 144 ... ...

7,180

6,192 986

185

32

-

...

- ... ... ... ... ... ... ... ... ...

...

... 409 382

237 538

...

...

...

... 88 ... ...

4,875

1.650 2,907

60 - ... 14 - ... ... ... ... ... ... ... ... ...

2,018 2,501 1,012 982 831 458 437 231 216 216 232 195 104 840

12,055

7,842 3.893 318 245

100 46 55

15 ...

1;495 1,375

96 21 50 46 4

585

370 717 300 263 222 127 183 147 110

145

...

...

12,ii.o

11,345 1,374

51 340

133 91 58

io 15

165 152 10 3

i10 97 13

272 857

347 717 ... ...

399 1,116 300 600 175 438 141 363 59 186 73 256 86 233 69 17Y ... ... 63 208

6,190 18.i66

2,230 13,575 3,664 5.038 298 349 120 460

85 218 18 109 6 64

5 15 15

...

- 200 365 191 343 6 16

3 45 155 34 131 1 1 24

-

... Not available. Source : Report of the Preparatory Conference on World Pulp Problems, 1949.

indirectly by currency shortages in their European markets, and to a certain extent the dislocation of their economy. In Finland there have been territorial losses, in Norway reduced forest yields in the north and the competition from sawmill industries in addition have been major factors.1 Moreover, Scandinavia produces relatively more pulp for rayon and less for paper than before the war. German pulp output has inev- itably declined with political and industrial disruptions. The United Kingdom also produces much less pulp than before the 1. This situation was particularly true for the years 1945-48, and has much improved during 1949.

22

war. France, the Netherlands, Switzerland and Belgium, on the other hand, have improved upon their pre-war output. In Europe as a whole pulp producing capacity to the extent of 2.5 million tons is at present unused. The decline in pulp consumption has been greatest in the

United Kingdom and Germany, which were before the war Europe’s largest consumers. Current British pulp consumption is running at only 60 per cent of the 1937 level. In Finland, France, Italy and the Netherlands consumption has also fallen. In Switzerland, Belgium, Czechoslovakia and Sweden - Europe’s largest pulp exporter - consumption has exceeded the pre-war level, and in the first it has more than doubled.

NORTH AMERICA

A number of new mills have increased the pulp capacity of North America within the last ten years. Compared with 1937, production in 1948 had risen by about two-thirds, and the increase in consumption was equally striking But 1948 was a peak year, and 1949 saw the first signs of

contraction. In the United States, the business recession took its toll of the pulp producing and consuming industries, and the demand for pulp fell off slightly, to recover more recently. The Canadian pulp industry was affected not so much by reduced United States import requirements as by the trading policies adopted by European countries. Owing to the dollar shortage, certain European governments were constrained to impose further restrictions on pulp imports from Canada, while others endeavoured to foster pulp exports to the United States. The situation on North American pulp markets was, however, stabi- lised during the last half of the year.

OTHER REGIONS

Outside Europe and North America only the Soviet Union and Japan possess large pulp industries. The Soviet Union produced 840,000 tons in 1937, and its current output is be- lieved to be over l million tons a year.i Consumption closely approximates to these figures. Japanese pulp production was reduced from 900,000 tons in

1937 to 340,000 tons in 1948, and consumption by over two- thirds. Unused capacity amounted to about 450,000 tons in 1948. The only other Asiatic countries producing and consum- ing wood pulp are China and India, but the tonnages are negligible. Production and consumption in Africa and the Near East

is a matter of about 30,000 tons annually. Latin America with n population of 150 million, about the same as that of North

i Various sources give double this flgure for the present production estimate.

23

America, consumes little pulp - just under half a million at present-and produces less. Yet the pulp and paper industries of this region have made great strides since 1937, consumption having risen twofold and production tenfold. Development in Oceania has also been quite fast, following the establishment of the first local pulp mills during the war, and current pro- duction is around 100,000 tons a year.

INTERNATIONAL TRADE

Pulp exports come from three regions: Europe, North America and the Soviet Union. Of these, Europe is much the most important, for it is the only one with a large net balance available for exports (Table VI). North America imports consid- erably more pulp than it exports. Russia’s surplus over domestic requirements is small and is mainly sold to Eastern European countries, so that little Russian pulp enters world trade. Most of the pulp trade of North America is carried on with-

in the boundaries of this continent, and only a minute propor- tion of North American pulp exports finds its w a y at present to countries outside North America. But more than a third of European exports go overseas. The pulp imports of the rest of the world, amounting to about 400,000 tons in terms of effective demand, are thus covered to a very large extent by exports from Europe, especially from Scandinavia.

Scandinavia and Canada between them account for 90 per cent of world exports (Table IV). The other net exporters are

TABLE IV EXPORTS OF WOODPULP (Thousand metric tons)

Country 1937 1947 IQ48

Estamated World Totals .......... 6,480 4,550 4.618 Europe .......................... 5,390 2,830 ...

Sweden .......................... 2,553 1,797 1,681 Finland .......................... 1,470 731 800 Norway .......................... 656 241 346 Germany 166 - ... Austria .......................... 186 9 39 Czechoslovakia ................... 136 44 24 Belgium 24 ... U . S . S . R . ...................... ... 20 ... North America .................. 1.090 1,700 1,710

Canada ........................... 793 1.581 1,633 United States ................... 2Y 3 118 75

... Not available. Source : Report of the Preparatory Conference on World Pulp Problems, 1949.

Austria, Germany and Czechoslovakia. The bulk of Canada’s exports is taken by the United States, while Scandinavian ship- ments are widely dispersed all over the world. Prominent among importing countries are the United States and the United Kingdom (Table V). These two countries absorb at least 60 per

of which :

.........................

......................... -

of which :

24

TABLE V IMPORTS OF WOODPULP (Thousand metric tons)

country 1937 1947 19118

Estimated World Totals .......... 6,450 4,620 .... 3,490 2,020 ... 1,824 876 1.16f 662 361 244 251 182 Q@

........................ 175 207 , 130 ................. 112 135 151 ............... _. 184 ................. 50 m SF

Hungary ......................... 42 - f 36 32 .’. $1 6t 70

Greece ........................... 24 7 10: 22 ... ...

................... 24 15 ...

................. -. 6 19 1Q.i 13 .... Portugal -

U . S . S . R . ......... 5 120 ... North America ................... 2,190 2,140 2.005

United States .................... 2;172’ 2.1 15 1,974: Latin America - 21 0, 270

Brazil ........................... 100 104 .... Argentina ........................ 43 64 .... Mexico ........................... 36 39 ... Chile ............................ 15 24 ....

99 -

....................... -.

of which :

of which : ................... ...

...

. ..-

...

IO. 5

500

Cuba ........................... Near East and North Africa ...... South and East Asia .............

Japan ............................ of which :

China .......................... I-

India and Pakistan .............. Oceania ..........................

Australia ......................... N e w Zealand ......................

of which :

474% 16 1 1 59

46 1.

15 5 20

6 8 5

45

34 10

* Bizone only. ... No1 available. Source : Report or the Preparatory Confierence on. World, Pulp Problems,

...

...

...

...

...

1940:

cent of world exports. Next in importance come France, Bel- gium, the Netherlands, Italy, Brazil, Argentina, and before the- war Japan. The Latin American countries are becoming increas- ingly important importers. World exports in 1948 totalled 4.6 million tons, or 1.9 million

tons less than in 1937, and world imports suffered a similar- decline. Scandinavia’s expaft fell from 4.6 to 2.8 million tons, whereas Canada’s exports increased from 790,000 tons to 1.6 million tons. United States impo-rts were reduced by only 10 per- cent to 2 million tons, but imports by the rest of the world dropped by nearly 40 per cmt from 4.3 million tons to 2.6 mil- lion tons. The principal short-term victims of this drastic decline are Britain, France and Japan, although its effects are even more serious in minor importing countries with new paper industries. Indeed, compared with 1937, imports into Asia, Latin Smerica and Africa show a decrease of about 30 per cent. The,

25

TABLE VI W O R L D PULP BALANCE (Thousand Metric Tons) ~ ~ ~~

1 9 3 7 I 9 4 9 (Provisional)

Estimated World total . 23,665* 23,840' + 635 28.345* 28.265' - 80 Europe ................ 9,790 11,670 +1.880 8,150 8.900 + 750 U.S.S.R. ............... ... + 195 - + 50 North America ........ 12,055 13.950 -1,105 18,& 16,485 - 445 Latin America ......... 245 25 - 220 540 295 - 248 Near East 15 5 - 10 20 15

15 15 Africa - - - Asia ................. 1,525 1,190 - 335 630 545 - 85 Oceania .............. 50 - - 50 160 110 - 50

- .............. - ...............

* Excludin U.S.S.R. ... NO^ amifable. Source : Report of the Preparatory Conference on world Pulp Problems, 1949.

ability of importers in these regions to cover their pulp require- ments in Europe is evidently prejudiced by Europe's dollar drive, which seeks to direct a larger share of a smaller volume of pulp exports to dollar countries. Until recently, European pulp found a ready market in the United States, and not un- naturally, European exporting countries were unwilling to divert a dollar earning export to markets where no hard currency can be earned. Whether the recent devaluation of Scandinav- ian currencies against the dollar will have the effect of reviving a flagging United States demand for European pulp, is to be seen. The shrinking of the world's trade in wood pulp has been

associated with the virtual elimination of a free world pulp market. Private enterprise in the pulp trade has frequently been superseded by the operations of public authorities whose prime consideration more often than not, is the availability of currency. Currency fluctuations and artificial exchange rates have added their influence to that of bulk buying under long- term contract and monetary restrictions in distorting the inter- national pattern of pulp distribution.

:26

C H A P T E R I 1 1

Printing paper Characteristics

IMPORTANCE OF PRINTING PAPER

This chapter is devoted to book paper, magazine paper and other printing grades excluding newsprint. It differs appreciably in treatment and length from the next chapter which deals exclusively with newsprint. Greater emphasis on newsprint does not, of course, imply that other printing grades merit less consideration. In fact, printing grades other than newsprint are, in a sense, even more important to the problems posed in this report, which discusses both the world’s growing demands for paper for reading purposes and the producer’s ability to meet these demands. The newspaper is the largest single out- let for printing paper, but it is not always the most suitable medium for imparting knowledge and information in print. Books are more fundamental to education than newspapers and education is fundamental to literacy, without which there can be no demand for newsprint. Unesco’s special obligations lie in the field of education,

and it would have been desirable, therefore, to present a comprehensive picture of the demand for, and the supply of, book paper and similar printing grades. That other printing paper should receive less consideration than newsprint in this report is unfortunate but unavoidable. Newsprint is a well organized and articulate industry. It consists, in the main, of large units producing a much publicised commodity and it easily overshadows the other sections of the paper industry. Data about newsprint exist in abundance. Not so with other printing papers. These comprise a wide variety of grades for books, magazines and periodicals, rarely standardised and frequently made with glossy, de luxe and other special finish. They are produced by a great many manufacturers, large and small, who are less organised and less practised in making statistical returns than are the newsprint manufacturers. More- over, returns often include writing paper, tissue paper, other fine paper, and similar items, and it is impossible to split the totals. In sharp contrast, newsprint is in a distinct category and can be readily separated from other paper products, much the same as wrapping paper and cardboard. The products of the paper industry fall into four main groups,

newsprint, other printing and writing paper, wrapping and

27

industrial paper, and cardboard, the first accounting for about 40 per cent and the other three for about 20 per cent each. Printing and writing paper, though different products, are frequently given as one total, but the share of writing paper is small and probably amounts to less than 5 per cent of total paper output.

LOCATION AND STRUCTURE OF THE PAPER INDUSTRY

The world's paper industries do not quite conform to the pattern which characterises the pulp industries, either in respect of their geographical distribution or their structure. Pulp production is based mainly on local resources of wood and water, and the world's pulp industries are accordingly located close to their sources of raw materials, that is in the vast forest areas of the Northern Hemisphere. Moreover, in pulp produc- tion, the large unit predominates. For papermaking, however, such considerations as the availability of skilled labour and fuel-where cheap hydro-electric power cannot be obtained the degree of industrial technique and the extent of the domestic market may be as important as the proximity of raw materials in determining the location of the mills. Some of the world's largest paper industries, indeed, rely in large measure on imported raw materials. The British paper industry is almost entirely dependent on imports for its pulp requirements, and the Netherlands, traditionally an important producer of pulp and paper, produces no pulpwood. Geographically, then, papermaking is much more widespread than pulp production and, indeed, common in all but a few newly-developed countries with little secondary production. Paper mills exist in practically every European country, and in several Latin American and Asiatic countries, although only few are able to operate up-to-date machinery, and fewer still can satisfy all the needs of their domestic markets. It should be noted however, that while paper for books and magazines is often made in comparatively small mills, it is evident that nations with a small consumption cannot manufacture their o w n sup- plies of newsprint, simply because the machinery would be idle for a large part of the year. The structure of the paper industry exhibits equally

distinctive features. Large-scale methods are not essential, though perhaps desirable, in the manufacture of paper other than industrial paper and newsprint. Capital requirements vary considerably with the type of product, but for many types of printing paper they are not heavy-again in contrast with newsprint. Paper mills, therefore, are numerous and widely scattered. They range in size from old-fashioned establishments with less than 50 workers, and for many decades in family ownership to giant companies equipped with Fourdrinier machines. It significant that both extremes of industrial enter-

28

prise exist peacefully side by side within the industry except the newsprint section. Dwarfed by the highly capitalised modern mill and enormously surpassed by it in operating emciency, the small family establishment has somehow managed to survive, confining itself to the production of high quality, special grades and relying on a long tradition of craftsmanship which can neither be copied nor readily utilised for mass produced lines. In a limited way, it has successfully held its own against the onslaught of price competition. Nevertheless, the small unit has not entirely resisted the

advance of modern industry. Even in the manufacture of print- ing paper there is a perceptible trend towards concentration, which is leaving its mark on both the geographical distribution and the structure of the paper industry. Evidently the existence of numerous small mills divorced from their raw materials is not conducive to high productivity and low costs. To realise in full the benefits of continuous-flow operations there must be a degree of integration between pulp production and paper- making, and such integration requires large-scale manufacture of paper. The need for vertical integration also underlies the trend towards greater concentration of papermaking in pulp producing countries. As is well known, pulp producers have attempted, in recent years, to develop the manufacture of news- print, paperboard and a few other mass produced articles, and to augment their export trade in finished or semi-finished goods rather than of pulp. As a result, the pulp producing countries are becoming pre-eminent also as manufacturers and converters of paper.

Production

CAPACITY

It would be interesting to give capacity estimates and compare them With those shown in the next chapter for newsprint. But capacity figures by countries have never been published, and the preceding section partly explains why they cannot be determined with any accuracy. All capacity totals are in varying degrees conjectural, even for a mass product like newsprint. Other printing papers are still more dimcult to deal with, for two reasons. First, the printing paper section of the industry is not a

homogeneous entity. It is composed of a large number of mills, many of them very small, which make all sorts of paper, in addition to printing paper. The combined total capacities of such mills have never been assessed for more than a handful of countries and these, with some exceptions, are usually minor producers. The exceptions include the United States and Canada, both of which are discussed below in this chapter. Secondly,

29

calculations of capacity are complicated by grade-switching. Alternative use of plant is common to all sections of the paper industry, including newsprint manufacture. Newsprint, how- ever, is normally produced by the Fourdrinier machine, and although this machine can be used in the manufacture of many grades of paper, there is no insuperable difficulty in ascertain- ing what portion of it is devoted to newsprint and other mass produced lines. But many manufacturers of printing paper operate on a small scale and cannot afford to use this vast and expensive machine. Their plant can, and frequently is, turned over to other uses, depending on the demands of the market and the relative profitability of the various products. It is impossible, therefore, to estimate the percentage of machine capacity used at any one time for printing paper or alternative products such as writing paper and tissue paper.

PRODUCERS

The largest printing paper industries are found in the principal pulp producing countries: the United States, Canada, Scandinav- ia and Germany. Other important producers are Britain, France, Belgium, the Netherlands, Austria and several non-European countries, including the Soviet Union, Brazil, Mexico, India and Australia. New capacity is being set up in Pakistan, Turkey, Argentina and other Latin American countries, while consider- able extensions are planned in Eastern Europe, New Zealand and the Union of South Africa. Paper for reading and other pur- poses is foremost amongst the products benefiting from the diversification and spread of manufacturing industry through- out the world. The dispersion of the industry is thus considerable. This is

another characteristic in which printing paper differs from newsprint. Whereas four countries, Canada, the United States, Britain and Finland, represent between them some two-thirds of world newsprint capacity, there is no similar concentration for the rest of the paper industry. Again, a very large pmportion of newsprint output enters international trade. More than four- fifths of the Canadian and Scandinavian newsprint industries cater exclusively for export markets, and even some of the smaller newsprint producers, for example Austria, export a large proportion of their output. By the same token, many consuming countries, including major consumers, like the United States, and a host of minor ones, import thc bulk, or the whole, of their newsprint requirements. But printing paper is produced, in the first place, for the needs of the domestic market, and the balance absorbed by world trade is very much smaller, both relatively and absolutely, than for newsprint. For printing paper there is a degree of self-sumciency in many countries. Thus India imports all its newsprint but only one-half of all the other grades which it consumes, and Argentina has a size-

30

able output of printing paper, although it produces at present very little newsprint. It is very nearly accurate to say that no country which

produces newsprint is without corresponding mills for the production of other grades of printing paper. But in addition many nations which import all their newsprint supplies have mills producing paper for periodicals and books. This is true for Greece and Denmark, as well as for the Union of South Africa, Peru and Mexico, as some instances outside Europe.

OUTPUT

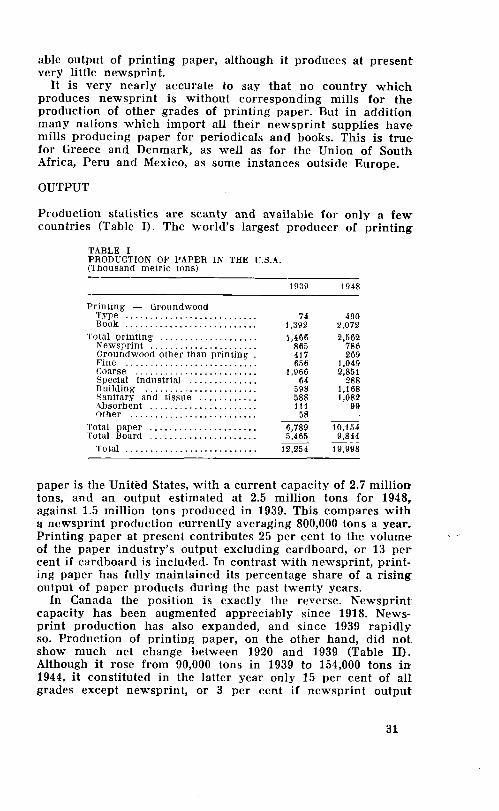

Production statistics are scanty and available for only a few countries (Table I). The world's largest producer of printing

TABLE I PRODUCTION OF PAPER IN THE U.S.A. (Thousand metric tons) --

1939 1948

Printing - Groundwood Type ........................... 74 490 Rook ........................... 1,392 2.072

Total printing .................... 1,466 2,562 Newsprint ...................... 865 186 Groundwood other than urintinr . 41 7 269 Fine 656 1,049 ........................... Coarse ......................... 1,966 2,851 Special industrial .............. 64 288 Building 598 i,i68 Sanitary and tissue ............ 588 1,082 Absorbent ...................... i l i 99

.......................... 58 other Total paper ...................... 6.Y89 10,154 -rota1 Board ...................... 5,465 9,844 'rota1 ........................... 12,254 19,998

.......................

- _ _ ~

-~

paper is the United States, with a current capacity of 2.7 million tons, and an output estimated at 2.5 million tons for 1948, against 1.5 million tons produced in 1939. This compares with a newsprint production currently averaging 800,000 tons a year. Printing paper at present contributes 25 per cent to the volume of the paper industry's output excluding cardboard, or 13 per cent if cardboard is included. In contrast with newsprint, print- ing paper has fully maintained its percentage share of a rising output of paper products during the past twenty years. In Canada the position is exactly the reverse. Newsprint

capacity has been augmented appreciably since 1918. News- print production has also expanded, and since 1939 rapidly so. Production of printing paper, on the other hand, did not show much net change between 1920 and 1939 (Table 11). Although it rose from 90,000 tons in 1939 to 154,000 tons in 1944, it constituted in the latter year only 15 per cent of all grades except newsprint, or 3 per cent if newsprint output

-

31

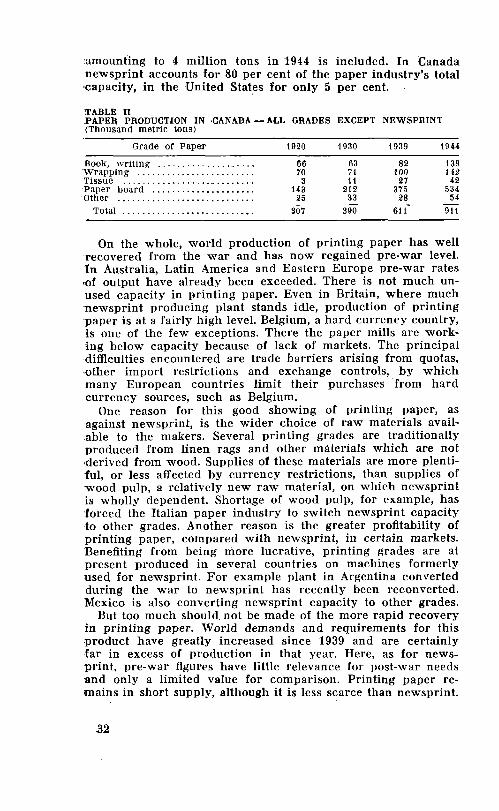

amounting to 4 million tons in 1944 is included. In Canada newsprint accounts for 80 per cent of the paper industry's total capacity, in the United States €or only 5 per cent.

TABLE I1

(Thousand metric tons) PAPER PRODUCTION IN CANADA - ALL ORADES EXCEPT NEWSPRINT

Grade of Paper 1920 1930 1939 1944

Book, writing ................... 66 63 82 139 Wrapping ........................ 70 71 too 142 Tissue ........................... 3 11 27 42 Paper board ..................... 143 212 375 534 Other ............................ 25 33 28 54 - - - - Total ........................... 307 390 61 1 911

On the whole, world production of printing paper has well recovered from the war and has now regained pre-war level. In Australia, Latin America and Eastern Europe pre-war rates .of output have already been exceeded. There is not much un- used capacity in printing paper. Even in Britain, where much newsprint producing plant stands idle, production of printing paper is at a fairly high level. Belgium, a hard currency country, is one of the few exceptions. There the paper mills are work- ing below capacity because of lack of markets. The principal dimculties encountered are trade barriers arising from quotas, other import restrictions and exchange controls, by which many European countries limit their purchases from hard currency sources, such as Belgium. One reason for this good showing of printing paper, as

against newsprint, is the wider choice of raw materials avail- able to the makers. Several printing grades are traditionally produced from linen rags and other materials which are not 'derived from wood. Supplies of these materials are more plenti- ful, or less affected by currency restrictions, than supplies of wood pulp, a relatively new raw material, on which newsprint is wholly dependent. Shortage of wood pulp, for example, has forced the Italian paper industry to switch newsprint capacity to other grades. Another reason is the greater profltability of printing paper, compared with newsprint, in certain markets. Benefiting from being more lucrative, printing grades are at present produced in several countries on machines formerly used for newsprint. For example plant in Argentina converted during the war to newsprint has recently been reconverted. Mexico is also converting newsprint capacity to other grades. But too much should not be made of the more rapid recovery

in printing paper. World demands and requirements for this product have greatly increased since 1939 and are certainly far in excess of production in that year. Here, as for news- print, pre-war figures have little relevance for post-war needs and only a limited value €or comparison. Printing paper re- mains in short supply, although it is less scarce than newsprint.

32

Consumption

GROWTH Tables 111 and IV give an indication of the growth in con- sumption since 1927 for certain countries, in so far as figures are obtainable. Consumption of printing paper of all descrip- tions has followed the trends of wood pulp, newsprint and other grades of paper, and has expanded appreciably over a period. But the pace of expansion has been slower as well as more steady. Printing paper is not as dependent on economic conditions as is newsprint, the demand for which is strongly influenced by the volume of advertising. Consumption of print- ing paper, therefore, fluctuates less sharply. In fact the demand for printing paper other than newsprint is normally stable, showing a steady increase. In the Netherlands, a country suf- ficiently representative of Western Europe to be quoted, con- sumption of printing paper increased in nine of the thirteen years before the war and contracted only in 1938. In 1939, Netherlands consumption had almost doubled compared with 1927. In Latin America and Asia the growth in demand w a s sharply accelerated in the second half of the .nineteen-thirties. Costa Rica’s consumption expanded more than twofold between 1935 and 1939. Between 1927 and 1948 consumption had doubled in N e w

Zealand and Colombia, and was more than twice as large for the same years in the United States, Switzerland and Norway. The amount of printing paper used in India has risen by 150 per cent since 1925. Two new states, Pakistan and Israel es- timate that printing paper consumption, exclusive of newsprint, will quadruple within the next five years.

It is only in the United States, whose flexible economy is prone to abrupt alternations of boom and slump, that printing paper has reproduced the fluctuations which mark the con- sumption of newsprint. In that country per capita consumption of printing paper fell off heavily in each depression period between the wars, and during the Great Depression from 1930 to 1932 it w a s halved (Table IV). Recovery was slow, with the result that per capita consumption w a s no higher in 1939 than in 1927 and not significantly above 1920. But from 1945 on- wards United States consumption of printing paper went up by leaps and bounds, and to-day it is 50 per cent above pre-war level. As will be seen later the trend in newsprint, during the past twenty-five years, is almost in exact replica of the trend in printing paper.

INEQUALITY Although the selection of countries for which per capita con- sumption figures are shown in Table V is by no means complete,

33

a 0 a 0

4 E E a a E

C

c

E F. m b

......................

......................

......................

......................

......................

...................... ~

~~

m~

w0

mm

0~

00

~l

-0

a0

rm

m~

---cc

-- damm

nmmm

.....mmwwdmmmw0t-wm00. t-

.....

.....

......

m-mm w.3wr*r*v~.~mrn0

......

......

-mi r- oz. w m U-. m

- w G w m 0) m U-. a

CD w r-

N N w N m 01 N

N m m .3 m

m D U .3 w

01 w m m

............

............

............

............

............

............

............

............

............

....

....

..I.

....

....

....

....

....

.... ..

..

..

-.

..

..

..

..

TABLE IV PER CAPITA CONSUMPTION OF BOOK PAPER IN THE U.S.A. * (kg. per head)

1900 ........................ 4 .................... 9 1910 ........................ 6 1936 ................... 10

........................ 8

............. ...... 10

........................ 10

........................ 11

........................ 10

........................ 6

................

....... 1934 .......

1920 1927 1928 1029 1930 1931 1932 1933

1937 ........................ 1938 ........................ 1939 ........................ 1940 ........................ I945 ........................ 1446 ........................ 1047 ........................ 1948 .......................

It 9

IO I1 10 12 14 14

* Excluding certain prlnting grades.

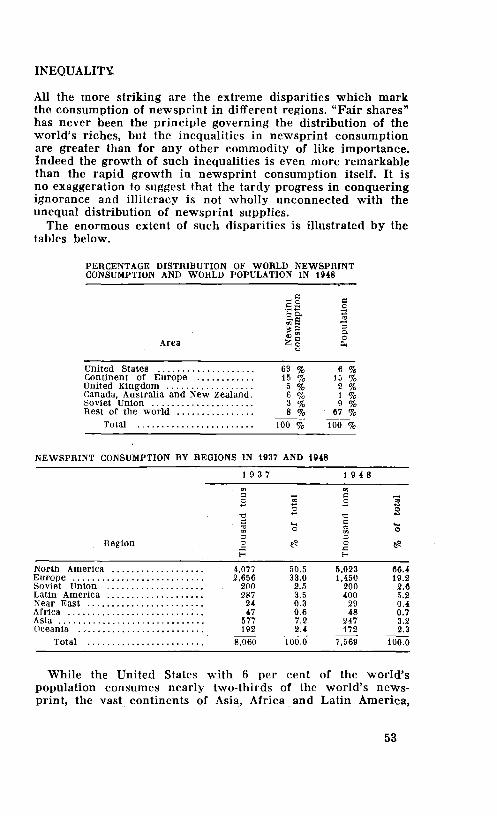

it is evident that the distribution of supplies is very unequal. Heading the group of countries covered, the United States annually consumes at present 26.4 kg. of both printing and writing paper per head. Scandinavian countries, the Nether- lands, France and New Zealand average each 7 to 10 kgs. Austria has a consumption of 7.3 kgs per head of printing paper. But per capita consumption in Italy is only 1.2 kg. and outside Europe, North America and Australia it rarely exceeds 1 kg. Thus Peruvians consume only 0.4 kg. a year, in spite of domestic production of printing paper, and per capita consumption in Ecuador, Turkey and the Philippines is as low as 0.2 kg. The figures for Burma, China and Pakistan are even lower. Immense as such inequalities are, they are greater still for newsprint, per capita consumption of this commodity in the United States being five hundredfold above that in India, China, Indonesia and most of Africa. The disparities in consumption have widened since 1945.

The few countries which have emerged from the war with strengthened economies, e.g. the United States and Switzerland, have enlarged their share of an unchanged volume of world supplies, while many other countries, especially those directly affected by military operations, have not yet fully retrieved the war-time decline in consumption. In consequence, con- sumption in regions other than North America and Australia is now somewhat lower than it was in 1939. But the 1939 level is an inadequate criticism to apply to consumption needs in 1949. The world's demand for book paper has materially ex- panded with the post-war drive for education throughout vast and largely illiterate continents, and the current supply position in those regions must be seen in the light of their current needs. Judged by this criterion, requirements are far in excess of

consumption levels in many of the countries where modern educational methods are only now taking root. Indonesia today consumes about the same quantities of printing paper as in 1939. Yet the demand has since multiplied, and meanwhile Indonesia lacks the paper to print the school books upon which

35

TABLE V PRINTING A N D WRITING PAPER ESTIMATED PER CAPITA CONSUMPTION IN 1948 (EXCLUDES NEWSPRINT) (kg. per head)

kg. per head Country kE. per head country

0.6 0.9 1.1

........... 0.i Austria .............. 7.3 Honduras Bolivia .............. 0.4 India ................ 0.2 Brazil ................ 1 .o Ireland .............. 8: 3 Bulgaria . . 0.; Italy ................ 1 .2 Burma .... 0.1 Japan ............... 4.1 Colombia ............ Lebanon ............. 0.6 Costa Rlca .......... New Zealand ........ 8.0 Cuba ................ Norway .............. 10.4 Czechoslovakia ....... Pakistan 0.1 Denmark Peru ................ 0.4 Ecuador ............. Philippines .......... 0.2 Egypt ............... Switzerland 8.9 Federation 01 Malaya Turkey .............. 0.2 and Singapore .... Union of South Africa 3.8

Prance .............. United States ........ 26.4

............. ............

..........

5.8 8.i 0.2 0.3

0.4 7.5

Greece 0.7 ..............

its post-war programme of education depends. Even in France or Czechoslovakia and other countries with a relatively large per capita consumption there has been a considerable expansion in the demand for book paper in the past ten years. Paper supplies, however, have not matched the increase in demand, and the publication of books for educational and other pur- poses is accordingly hampered. Such deficiencies could, of course, be relieved if countries were free to compete for supplies in the world market. But those countries which are short of paper are usually also short of foreign currency and are forced to confine their purchases to soft currency sources, where sup- plies are limited.

It is pertinent to note that a mope equitable distribution of printing paper is, to some extent, hindered by high import tariffs. Newsprint and other grades of paper are also liable to customs duties, but the incidence of such restraints affects particularly the importation of printing paper. Many countries are importers as well as producers of printing paper and afford their paper industries enough protection to safeguard their domestic markets from foreign competition. But much of the newsprint consumed cannot be produced economically by domestic paper manufacturers and must be imported. The import duties on newsprint are thus lower than for printing paper, and many countries admit newsprint duty free.

3F

C H A P T E R I V

Newsprint

Characteristics of the newsprint industry For none of the diverse products of papermaking are the ad- vantages of mass production as manifest as for newsprint. In volume, newsprint is far and away the most important single pulp product. In a normal year it constitutes approximately 45 per cent of total paper output and absorbs a very large quantity of the pulp consumed in papermaking. Then newsprint is destined for some specific use, which requires less variety of grade, quality and size than most other kinds of paper. Light weight newsprint for carriage by air is at present very ex- pensive and is the exception rather than the rule. Newspapers, moreover, have a very short life, and to achieve a wide circula- tion they must be printed as economically as possible on cheap, mass produced material. Newsprint is therefore eminently suited for mass production by high-speed machinery. Such machinery is extremely costly, and it is only economic at a large and continuous throughput. To some extent, investment risks are reduced by the adaptability of certain types of newsprint machinery to the production of other grades of paper. Older machines can be readily converted, although most machines for newsprint manufacture constructed within the last twenty years are not capable of producing other grades. Grade-shifting tends to spread investment risks over a range of products, but it also tends to make production of particular products, especially newsprint, highly sensitive to profit yields. A further characteristic is the length of the business cycle.

Some forty years of planned forest growth are necessary before the trees are mature for cutting; yet mill stocks must be con- tinually replenished to keep the plant running at an economic level of capacity. Growth is not entirely a natural process. It has to be planned years in advance in areas suitable for cutting and transportation. Provision must be made for housing labour near the cutting areas, roads may have to be driven through miles of thick forest and the transportation of men and materials has to be organised. To sustain an efficient cycle of operations the mills have to ensure a smooth flow of raw materials all the year round. The problem of forest conserva- tion is indeed vital to the paper industry and consequently to readers everywhere. Forestry officials in many parts of the world have warned of the dangers of over-cutting, and only

37

recently a prominent Canadian forester predicted that “unless new growth was established, Canadian supplies of marketable timber will disappear in less than sixty years.” The structure and organization of the newsprint industry

have been vitally affected by the magnitude of the capital requirements and the need to programme production many years ahead of requirements. First, the rise of the large unit has been favoured. The smaller type of establishment is not lacking but it is gencrally tending to be eliminated or absorbed by the larger onc. The long-term trend is definitely towards greater concentration of newsprint production in a diminish- ing number of growing concerns. Secondly, the processes of production have become increasingly integrated. Newsprint mills have expanded in varying degrees towards the sources of their raw materials. Several British mills have a stake in pulp production in Scandinavia and North America, and some own or control pulp mills in these countries. Thirdly, an elaborate system of long-term contracts has