Embed Size (px)

Citation preview

The

Political Ecology

of

the

Japanese Paper Industry

Ian William Penna

Submitted in total fulfilment of the requirements of the degree of Doctor of Philosophy

School of Anthropology, Geography and Environmental Studies

The University of Melbourne

November 2002

ii

Dedication

This dissertation is dedicated to

the memory

of

Peter Rawlinson

and

Gordon Robinson

iii

iv

Declaration This is to certify that this dissertation: • comprises only my original work; • contains no material that has been used for the award of any other degree to

myself from any university or institution and no material that has been previously published or written by any other person except where acknowledgment is given in the text; and

• is less than 100,000 words in length, exclusive of appendices, bibliographies, figures and tables.

Ian William Penna

v

vi

Abstract The Japanese paper and paperboard industry has grown to be one of the largest in the

world. It manufactures a range of products for sale primarily within Japan, and

consumes organic fibre for these products from dispersed domestic and foreign

forests, plantations and cities.

This dissertation examines the links between the development and structure of

the industry and its use of papermaking fibre. It takes a political ecology perspective

and uses an industrial structure/consumption-production chain approach to show how

the industry’s development and structure continue to depend on company control

over fibre flows and the restructuring of products, product distribution and

manufacture, the fibre supply chain and fibre resources.

As with the modern global paper/board industry, the recent growth of the

Japanese industry has been characterised by cycles of capacity expansion, market

collapse, excess capacity and low prices and profits. Manufacturers and general

trading companies involved in the industry have tried to support growth in the use of

paper/board and counter these cycles by restructuring production, distribution,

ownership and fibre supply. This restructuring helps protect the flow of fibre

through the industry and concentrated it in particular companies.

Obtaining increasing quantities of suitably-priced fibre has been at the base of

the industry’s development. Control by manufacturers and general trading

companies over prices and fibre supply chains has been central to the exploitation of

different fibre resources. Much of the industry’s growth has depended on increasing

the use of native forests and waste paper/board. It is now expanding its use of

plantation wood.

The transnational flow of fibre through the Japanese paper industry links

dispersed economies and environments. The dissertation emphasises the importance

of all the dimensions of the characteristics of the resources – physical, political,

economic, ecological – in determining how fibre is exploited and the interactions

between these economies, environments and communities. It argues that the

expanding and diversified fibre supply integral to the industry’s growth has relied on

significant restructuring of social and natural environments to suit the interests of

pulp and paper capital. The rapid restructuring of forests to supply large volumes of

vii

pulpwood has been at the expense of many non-wood values. Increasing the supply

of recovered fibre involved restructuring Japan’s waste paper/board collection sector

to shift costs out of the fibre supply chain. Similar restructurings are occurring with

the establishment and use of plantation wood. Case studies explain the processes

involved.

The industry’s fibre sourcing strategies are directed by ‘shallow’ environmental

philosophies that are concerned primarily with maintaining fibre supplies. This is

reflected in the ‘environmental charters’ of paper manufacturers and general trading

companies. Environmental benefits resulting from these strategies are primarily

produced by the pursuit of economic objectives. The ability and desire of these

companies to develop and implement more environmentally-benign strategies are

limited by the political economies in which they operate and the priorities and

philosophies that dominate within the industry.

viii

Acknowledgements The preparation of this dissertation taught me many lessons about things other than

Japan’s paper industry. In particular, it showed me how, even though the task of

preparing a PhD dissertation is very personal and can consume much of one’s life, it

is ultimately a cooperative effort and depends on the goodwill, knowledge and skills

of many other people.

First, I want to express my gratitude and loving thanks to my parents and brother

for their love and support, not only through the years it took in preparing the

dissertation, but also through the life that led me to it. I hope they find satisfaction

and relief in seeing the dissertation finally completed.

Also, I am most grateful to Professor Michael Webber, my supervisor, who

welcomed me into the University of Melbourne, supported my decision to write this

dissertation and gave me invaluable assistance over the years I took to complete it.

Mark Wang, Peter Christoff and Geoff Missen also provided advice and

encouragement, personally and through my progress review committee. All other

staff of the School of Anthropology, Geography and Environmental Studies were

generous in their help.

During 1997, I was an Invited Guest Researcher at Kokugakuin University,

Tokyo. The financial and organisational support of Kokugakuin University allowed

me to gather much information and make important contacts. Staff were always

most helpful. Special thanks go to Furusawa Koyu for his personal support of my

research and Shimoyama Nobukatsu and other staff of the University’s International

Exchange Center for their kind assistance while I was living there.

I interviewed many employees of Japanese paper and trading companies as well

as people employed in, or close to, the paper and wood products industry in Japan

and elsewhere. Many of these people preferred to remain anonymous, so I do not

directly acknowledge them by name. They know who they are, and here I extend my

grateful thanks for allowing me to meet with them. However, I would particularly

like to thank Nakano Shogo and staff of Daishowa Paper Manufacturing Co. in Japan

and its associated companies in North America and Australia who made time

available in their busy schedules to meet me and respond to my requests.

ix

Kondo Tadahiro and other staff of the Japan Paper Association provided me

with introductions, interviews and copies of regular publications that supplied much

statistical data and policy information on the Japanese paper industry. Oe Reizaburo,

Emeritus Professor at Tokyo University of Agriculture and Technology, and the staff

of the Paper Recycling Promotion Center, particularly Ono Mikio, helped me gain

information on recycling of used paper/board in Japan. Iida Kiyoaki of Japan TAPPI

also directed me to useful information on a variety of issues related to paper

production in Japan.

Robert Johnston of the Australian Pulp and Paper Institute and Morita Tsuneyuki

of Japan’s National Institute for Environmental Studies kindly provided references

for the questionnaire that I sent to Japanese paper/board manufacturers and general

trading companies. Allan Jamieson of AOK Innovations and Noel Clark of CSIRO

unfailingly responded to all my requests for assistance, and provided valuable

support and advice that improved my understanding of the paper industry. Sugimura

Ken, Ryukoh Hiroto, Sawanobori Yoshihide and Narita Masami answered my

various questions, and the comments and information they provided were extremely

important in helping me understand the forestry scene in Japan.

The interpreting and translating skills of my friends Takeguchi Ryu, Ikeda

Mariko and Watanabe Masako were crucial for my interviews in Japan. Also, the

help of Matsuoka Tomohiro, Yamane Akiko and Hashimoto Yoji with translations in

Australia was very important. Michelle Hall in the University of Melbourne’s library

tracked down Japanese references for me, and Justin Wejak translated letters into

Indonesian.

My travels through North America were facilitated by the welcomes and

continuing support of old and new friends - thanks to Susan Grigsby, Sabrina Huang,

Denny Haldeman, Cielo Sand, and Ian and Theresa Urquhart who provided

accommodation, transport, introductions and good times during this period. Harriett

Swift, Keith Hughes, Peter Morgan and Judy Clark provided support, information

and ideas during the research process in Australia. My thanks and appreciation also

go to all other people listed in Appendix 4.1 whom I met or helped me in some way.

My apologies to any that I have inadvertently omitted.

The friendships I made with other students while studying at the University of

Melbourne are not only valuable to me in their own right, but helped me handle the

x

frustration and angst that accompany the PhD task. In particular, my thanks go to

Terri Chala, Jenny Newton, Lesley Rigg, David Goldblum, Christina Jarvis, Ben

Miller, Paul Reich and all occupants of Rooms 414 and 415 during my stay. The

encouragement of friends around the Pacific helped me persevere – thanks to Gail

James, Susan Grigsby, Morita Tsuneyuki, Allan Jamieson, Maureen Smith, Claire

Day, Moriyama Tae, Bob and Reiko Gavey, Jonathan Holliman, Kanazawa

Mutsumi, Stephen McKay, Michael Bjorn and Randy Helton. ‘Sabah’, ‘Nigah’ and

the platypus family in the Moorabool River provided great companionship too.

The real beginnings of a task like a PhD can be found well before the formal

process starts, so there are many people in my past who may not appreciate their

contribution. They include the staff and post-graduate students of the Institute of

Agriculture and Forestry in the University of Tsukuba from 1993 to 1995, especially

Kumazaki Minoru who was my supervisor while I was a research student there.

The Australian Securities & Intelligence Commission provided annual financial

statements and reports of Harris-Daishowa (Australia) Pty. Ltd. for the years 1990-

1998 at a concessional rate. However, AS&IC is not responsible for the reliability of

any such information supplied to it, or for the way that information was used in this

dissertation. Timber Mart-South kindly provided data on the prices of pulpwood in

south eastern USA.

Permission to reproduce maps was provided by Dana Ltd. (Figures 8.6, 8.7 and

8.8), Southeast Alaska Conservation Council (Figure 8.15), Alberta Sustainable

Resource Development (Figure 8.16), Daishowa-Marubeni International (Figure

9.11), Friends of the Lubicon (Figure 9.12), State Forests of New South Wales

(Figure 9.13) and the Japan Paper Association (Appendix 1.1). Jo Sasse authorised

reproduction of the map of Japan’s forest zones in Figure 6.1, the original source of

which is the Japan Forest Technical Association. Permission to reproduce

photographs was provided by Sugimura Ken (Figure 6.16) and Nihon Consumer

News (Figure 7.7).

The frontispiece comes from the packaging for a CD Rom in the computer game

‘Riven’. I am grateful to Cyan Worlds, Inc for giving permission to use this image.

All Myst, Riven and D'ni images and text © Cyan Worlds, Inc. All rights reserved Myst ®, Riven ® and D'ni ® Cyan Worlds, Inc.

xi

xii

Contents Frontispiece....................................................................................................................i Dedication................................................................................................................... iii Declaration....................................................................................................................v Abstract...................................................................................................................... vii Acknowledgements......................................................................................................ix Contents .................................................................................................................... xiii Figures ..................................................................................................................... xvii Tables.........................................................................................................................xxi Abbreviations and special terms ............................................................................. xxiii Chapter 1: Introduction................................................................................................1

1.1 International fibre resource links ......................................................................1 1.2 Japan’s paper use and the Japanese paper industry...........................................2 1.3 The research importance of Japan’s paper industry..........................................6

1.3.1 Research issues and Japan’s paper industry................................................6 1.3.2 Industrial structure and natural resources....................................................7 1.3.3 The application of environmental policies ..................................................8 1.3.4 Japan and Japanese companies as resource consumers...............................9

1.4 Research questions..........................................................................................11 1.5 Structure of the dissertation ............................................................................12

Chapter 2: ‘Political ecology’, industrial structure and resource exploitation ...........15

2.1 Introduction.....................................................................................................15 2.2 The political economy of resource exploitation..............................................15 2.3 Political ecology..............................................................................................18 2.4 The political ecology of resource-based industries.........................................20

2.4.1 An approach for analysing resource-based industries...............................20 2.4.2 The influence of resource characteristics ..................................................20 2.4.3 Global economic structures and ‘shadow ecologies’ ................................23

2.5 Political ecology, industrial structure and resource use..................................26 2.5.1 Industrial structure and the environment...................................................26 2.5.2 Industrial transformation and environmental change................................27 2.5.3 Industrial structures and ‘consumption-production chains’ ......................29

2.6 Industrial structure and socio-environmental consequences...........................34 2.6.1 Introduction ...............................................................................................34 2.6.2 The Japanese aluminium industry .............................................................34 2.6.3 Agriculture and the food industry .............................................................35 2.6.4 Forest exploitation and wood industries....................................................37 2.6.5 Application to the dissertation...................................................................38

2.7 Industrial structure and environmental protection ..........................................38 2.8 Conclusions.....................................................................................................43

Chapter 3: Papermaking and the role of fibre............................................................45

3.1 Introduction.....................................................................................................45 3.2. Fibre characteristics and properties and the papermaking process ................46

3.2.1 ‘True’ paper and fibre characteristics........................................................46 3.2.2 The papermaking process..........................................................................48 3.2.3 Characteristics and properties of papermaking fibres ...............................50

3.3 The economics of modern paper production and fibre supply........................54 3.3.1 Pulpmill operation and economics ............................................................54

xiii

3.3.2 Fibre supply and pulp/papermill economics .............................................57 3.3.3 Wood fibre supply and pulp/paper production .........................................58 3.3.4 Recovered fibre supply and paper/paperboard production .......................59 3.3.5 Non-wood fibres .......................................................................................61

3.4 Fibre and the political economy of papermaking ...........................................62 3.4.1 The development of ‘true paper’ and the shift to wood............................62 3.4.2 The expanding use of wood and restructuring supply ..............................64 3.4.3 Industrial attitudes to fibre resources ........................................................70 3.4.4 Restructuring manufacturing and distribution ..........................................74

3.5 Conclusions.....................................................................................................76 Chapter 4: The research method................................................................................81

4.1 Introduction.....................................................................................................81 4.2 The research paradigm and approach .............................................................81 4.3 The research agenda........................................................................................83

4.3.1 Research process, topics and sources........................................................83 4.3.2 Initial information collection ....................................................................83 4.3.3 Overseas fieldwork ...................................................................................85 4.3.4 Further information collection ..................................................................87

4.4 Methodological issues.....................................................................................87 4.5 Information presentation.................................................................................91

Chapter 5: Restructuring the consumption, manufacture and distribution of Japan’s paper and paperboard ...........................................................................93

5.1 Introduction.....................................................................................................93 5.2 Paper/board use in Japan since World War 2 .................................................96

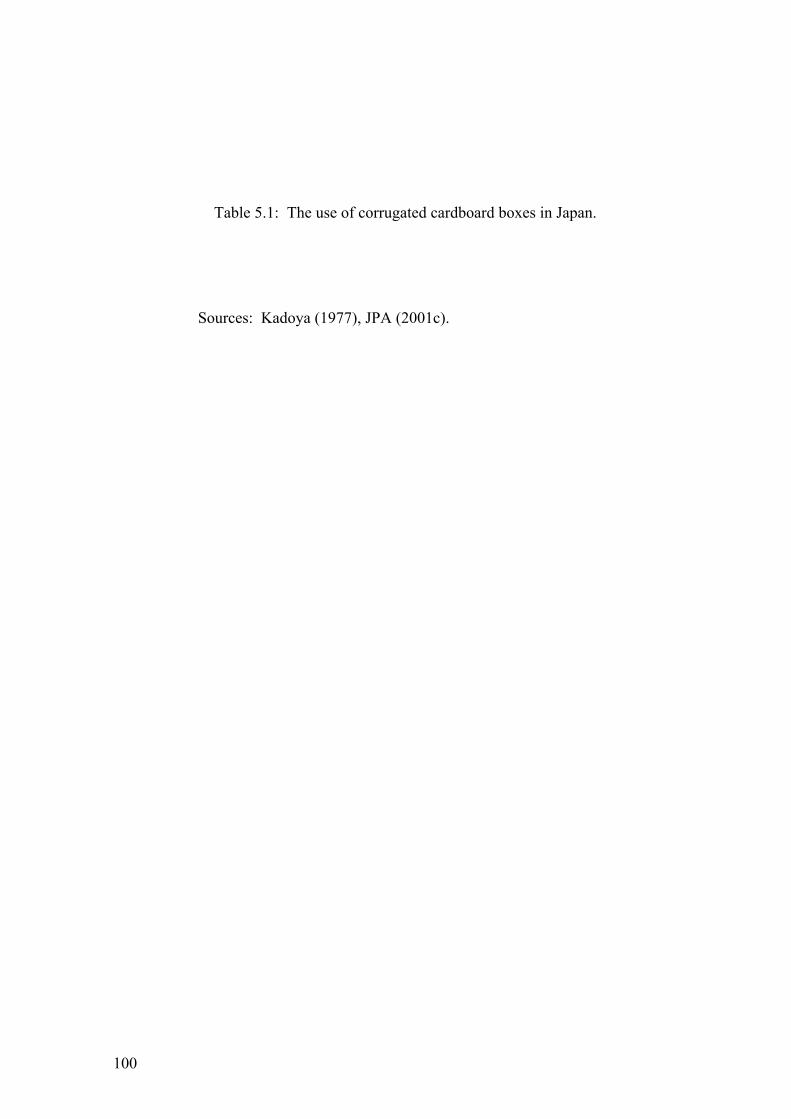

5.2.1 Post-war trends in domestic production....................................................96 5.2.2 Restructuring paper and paperboard use...................................................96 5.2.3 Overview.................................................................................................114

5.3 Restructuring pulp, paper and paperboard production..................................115 5.3.1 Trends, causes and consequences ...........................................................115 5.3.2 Industrial structure, competition, profitability and market share............116 5.3.2 Restructuring industry ownership ...........................................................119 5.3.3 Restructuring production facilities..........................................................122 5.3.4 MITI and industry policy ........................................................................129

5.4 Restructuring paper/board distribution .........................................................131 5.5 Conclusions...................................................................................................135

Chapter 6 - Restructuring domestic supplies of new fibre .......................................137

6.1 Introduction...................................................................................................137 6.2 Fibre supply to World War 2 ........................................................................140

6.2.1 Establishment of machine-made paper production.................................140 6.2.2 Exploiting resources in the ‘periphery’...................................................142 6.2.3 Impacts on forests ...................................................................................144

6.3 Growth after World War 2............................................................................145 6.3.1 Pulpwood resources and exploitative pressures......................................145 6.3.2 Restructuring pulpwood procurement - ‘keiretsu’ control......................164 6.3.3 Pulpwood logging, resource management and environmental impact ...168

6.4 Conclusions...................................................................................................175

xiv

Chapter 7: Restructuring the supply of used fibre – ‘logging Japan’s urban forests’...................................................................................................179

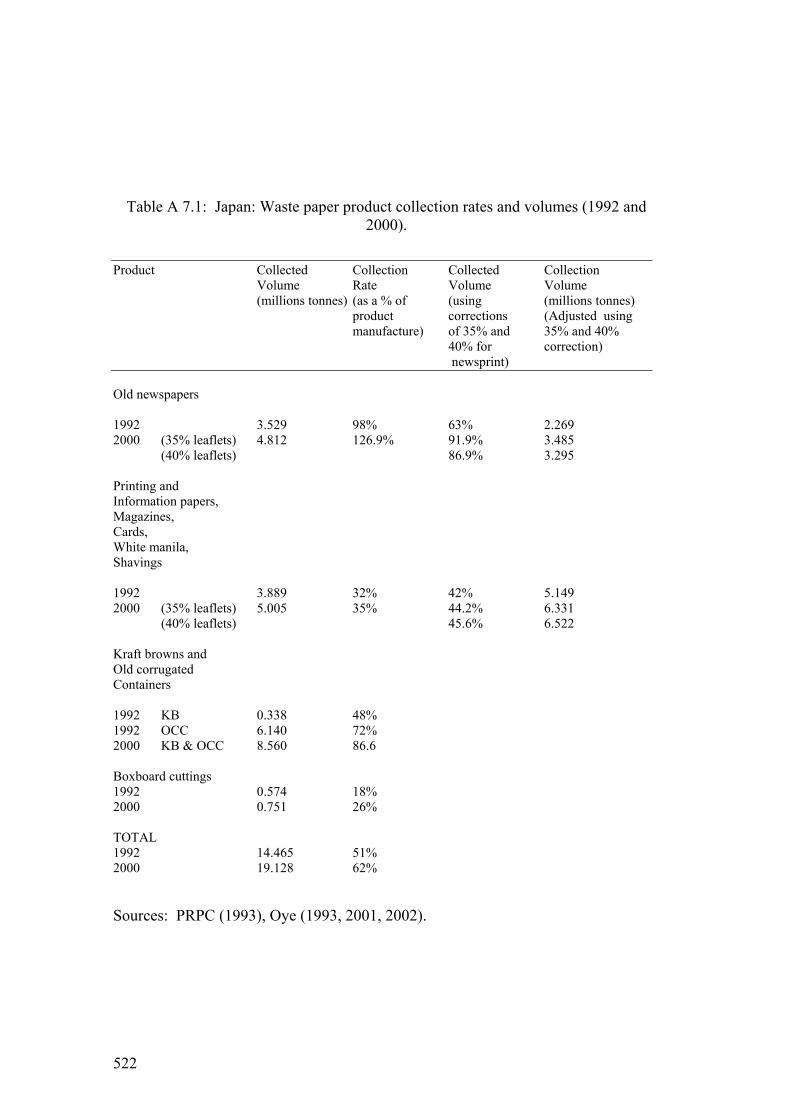

7.1 Introduction...................................................................................................179 7.2 Japan’s waste paper/board resources ............................................................179 7.3 Recycling technologies and ‘recovered fibre’ products................................185 7.4 Japan’s recycling legislation .........................................................................186 7.5 Recycling economics ....................................................................................190 7.6 Restructuring the supply of recovered fibre..................................................190

7.6.1 The waste paper/board collection sector .................................................190 7.6.2 Restructuring supply - 1945 to the 1980s................................................191 7.6.3 Restructuring supply – the 1980s to 2000...............................................197

7.7 The continuing cost-price squeeze................................................................203 7.8 Recovered fibre - reducing garbage and conserving forests? .......................206

7.8.1 Recycling for garbage reduction .............................................................206 7.8.2 Recycling for fibre resource conservation ..............................................208

7.9 Future environmental benefits ......................................................................212 7.10 Conclusions.................................................................................................214

Chapter 8: Restructuring the supply of foreign fibre...............................................217

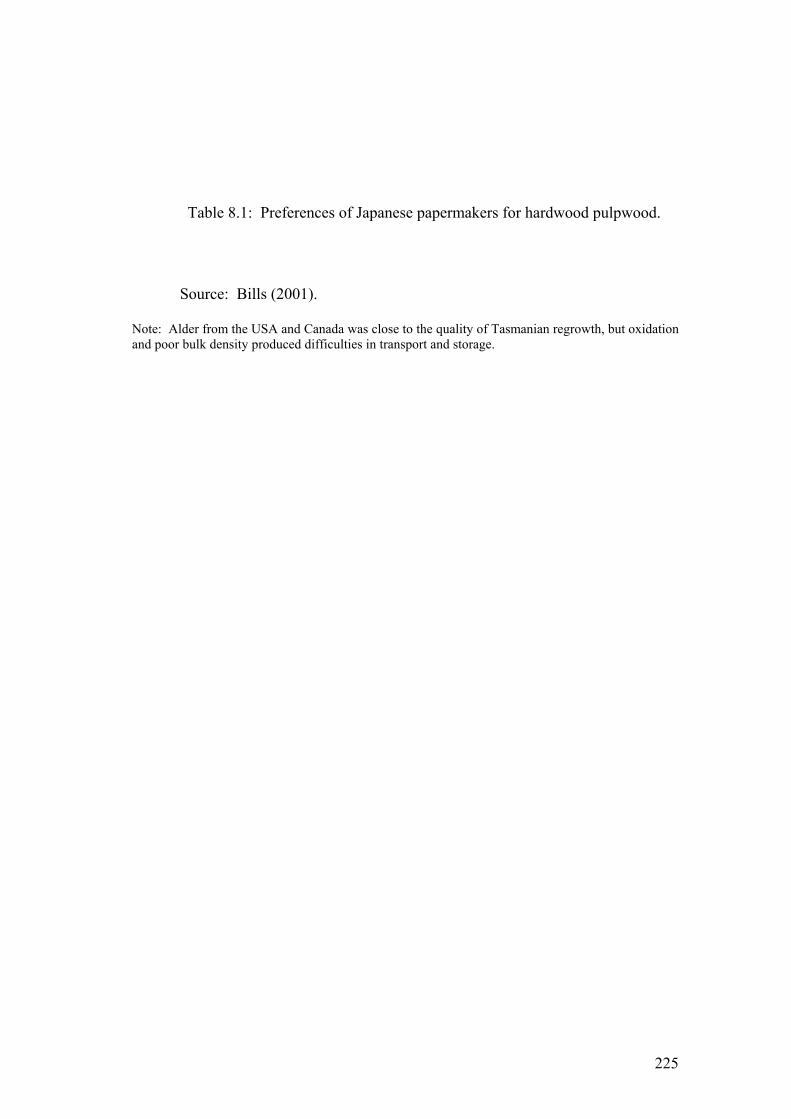

8.1 Introduction...................................................................................................217 8.2 The supply of foreign fibre since 1950 .........................................................217

8.2.1 Factors influencing fibre imports ............................................................217 8.2.2 Imported pulpwood .................................................................................218 8.2.3 Pulp imports ............................................................................................226 8.2.4 Imports of paper and paperboard ............................................................227 8.2.5 General trading companies and fibre imports .........................................231 8.2.6 Fibre imports - Overview ........................................................................232

8.3 Case studies...................................................................................................232 8.3.1 Introduction .............................................................................................232 8.3.2 Temperate forest hardwood chip supply .................................................233 8.3.3 Foreign hardwood plantations.................................................................253 8.3.4 Foreign pulpmill development ................................................................260

8.4 Conclusions...................................................................................................270 Chapter 9: Daishowa Paper Manufacturing Co. – A Case Study .............................273

9.1 Introduction...................................................................................................273 9.2 Company History ..........................................................................................273

9.2.1 Daishowa’s origin and growth ................................................................273 9.2.2 The Oji challenge and Saito Ryoei..........................................................275 9.2.3 Financial management and take-over......................................................280

9.3 Products.........................................................................................................284 9.3.1 Domestic products...................................................................................284 9.3.2 Foreign products......................................................................................286

9.4. Raw material supply......................................................................................290 9.4.1 Overview .................................................................................................290 9.4.2 Cariboo Pulp and Paper Co .....................................................................294 9.4.3 The Peace River pulpmill ........................................................................300 9.4.4 The Port Angeles papermill.....................................................................310 9.4.5 Harris-Daishowa export woodchip scheme.............................................311

9.5 Conclusions...................................................................................................334

xv

Chapter 10: Environmental issues and paper industry policies................................337 10.1 Introduction.................................................................................................337 10.2 The history of company environmental charters ........................................340 10.3 Company environmental charters ...............................................................342

10.3.1 General trading companies ...................................................................342 10.3.2 Paper companies ...................................................................................345 10.3.3 Charter overview...................................................................................349

10.4 Policy implementation and internal company and staff attitudes ...............350 10.4.1 Implementing environmental charters ..................................................350 10.4.2 Attitudes to fibre use and conservation issues ......................................357

10.5 Environmental charters and environmental outcomes................................367 10.6 Conclusions.................................................................................................370

Chapter 11: Conclusions..........................................................................................373

11.1 Introduction.................................................................................................373 11.2 Overview of the dissertation .......................................................................373 11.3 The subsidiary research questions ..............................................................375 11.4 The main research questions.......................................................................382

Bibliography .............................................................................................................391 Appendix 1.1: Pulp and paper mill location, ownership and production in Japan during the year 2000 .............................................................................463 Appendix 4.1: Interviewees and people who assisted with information .................465 Appendix 5.1: Japan’s early use of paper................................................................469 Appendix 5.2: Types of paper used in Japan...........................................................473 Appendix 5.3: Tissue production, waste paper use and industrial restructuring in Japan ......................................................................................481 Appendix 5.4: Recent trends in share prices of Japanese paper/board companies...483 Appendix 5.5: Oji Paper Co. – issues of structure and resource control.................485 Appendix 5.6: Mergers and acquisitions in Japan’s paper/board industry since the mid-1960s ........................................................................................505 Appendix 5.7: Japan’s general trading companies and their involvement in the Japanese paper/board industry ..............................................................509 Appendix 7.1: Statistics and terminology related to recovered fibre in Japan........519 Appendix 7.2: Public attitudes to ‘recycled paper’ products in Japan ....................523 Appendix 8.1: Diversification of foreign temperate hardwood chip supplies in the late-1980s ..............................................................................................531 Appendix 8.2: Calculations of the approximate areas of native forest needed to supply recent amounts of hardwood chips exported from Australia and south eastern USA ....................................................................545 Appendix 8.3: Extracts of interview with James Morrison.....................................549 Appendix 9.1: Saito Ryoei – a potted history..........................................................551 Appendix 9.2: Extracts of interview with Tom Hamaoka.......................................555 Appendix 9.3: Streamside reserve criteria in the Eden region ................................559 Appendix 9.4: Sawlog and pulplog criteria in the Eden region ..............................561 Appendix 9.5: The impact of woodchipping on some fauna in south eastern NSW..........................................................................................565 Appendix 10.1: Notes for Tables 10.1 to 10.10 ......................................................567 Appendix 10.2: Content of the questionnaires used to obtain information from Japanese paper companies and GTCs ....................................................585

xvi

Figures Figure 1.1: The general flow of fibre through the Japanese paper/board industry......4 Figure 1.2: The flow of fibre for pulp, paper and paperboard production in Japan during 2000. ..............................................................................................5 Figure 2.1: Mapping the market structure of raw material industries. ......................22 Figure 2.2: The spectrum of ‘greening’ positions......................................................40 Figure 3.1: The structure of a mature softwood fibre. ...............................................47 Figure 3.2: Pulping processes and characteristics. ....................................................49 Figure 3.3: Generalised production costs and profit for a pulpmill...........................55 Figure 3.4: Simplified comparison of the profit margin between baseline and incremental woodpulp production. .............................................................56 Figure 5.1: Paper use in Japan. ..................................................................................94 Figure 5.2: Paperboard use in Japan. .........................................................................95 Figure 5.3: Paper production in Japan. ......................................................................97 Figure 5.4: Paperboard production in Japan. .............................................................98 Figure 5.5: Prices for linerboard and corrugating medium in Japan. ......................101 Figure 5.6: Production of uncoated and coated printing papers in Japan. ...............106 Figure 5.7: Prices for uncoated and coated papers in Japan. ...................................107 Figure 5.8: Annual publication of books and magazines in Japan. .........................108 Figure 5.9: Exports of paper and paperboard from Japan........................................112 Figure 5.10: Forecasts and expectations of paper and paperboard use in Japan................................................................................................................113 Figure 5.11: The average profitability of Japanese paper/board manufacturers......117 Figure 5.12: Concentration of production within Japan’s paper/board industry. ....120 Figure 5.13: Pulp production in Japan. ....................................................................123 Figure 5.14: Capital expenditure by paper/board manufacturers in Japan. .............124 Figure 5.15: Employment and labour productivity in the pulp, paper and paperboard sectors in Japan.............................................................................126 Figure 5.16: Outline of the distribution of paper/board products in Japan..............133 Figure 6.1: The forest zones of Japan. .....................................................................138 Figure 6.2: Japan and areas of pulpwood supply referred to in Chapter Six. ..........141 Figure 6.3: Pulpwood supply to Japanese pulp and paper companies from 1913 to 1945. ..........................................................................................143 Figure 6.4: Pulpwood and woodchip supply within Japan from 1954 to 1970. ......150 Figure 6.5: Hardwood product output from Japan’s native broadleaf forests. ........153 Figure 6.6: Sources of hardwood chips in Japan. ....................................................154 Figure 6.7: Prices for hardwood and softwood pulpwood in Japan from 1952 to 1976. ..........................................................................................155 Figure 6.8: Relative prices for hardwood and softwood pulpwood in Japan from 1952 to 1976, based on Figure 6.7. ..............................................156 Figure 6.9: The establishment of new plantations and the production of hardwood pulpwood in Japan..........................................................................159 Figure 6.10: Nominal and real prices for domestic and imported hardwood chips in Japan. .................................................................................................160 Figure 6.11 Sources of softwood chips in Japan. .....................................................162 Figure 6.12: Nominal and real prices for domestic and imported softwood chips in Japan. .................................................................................................163 Figure 6.13: The number, employment level and production of woodchip mills in Japan...................................................................................................167 Figure 6.14: Wood-based industry log supply centred on public forests in Nagano Prefecture from 1963 to 1983. ...........................................................170

xvii

Figure 6.15: Log production from broadleaf forests on Amami Island. .................173 Figure 6.16: Clearfelling on Amami Island.............................................................174 Figure 7.1: Recovery of waste paper and paperboard in Japan. ..............................180 Figure 7.2: Imports and exports of recovered fibre by Japan..................................182 Figure 7.3: Rates for recovery and utilisation of waste paper and paperboard in Japan. .......................................................................................183 Figure 7.4: Composition of recovered fibre used for paper/board production in Japan. ..........................................................................................................184 Figure 7.5: Structure of Japan’s waste paper and paperboard collection sector......192 Figure 7.6: Prices paid for the main categories of recovered fibre by paper and paperboard manufacturers in Japan. ...............................................196 Figure 7.7: Community groups and collectors of waste paper and paperboard protest in Tokyo over the low price for recovered fibre during 1997.............201 Figure 7.8: Recent production of municipal garbage in Japan. ...............................207 Figure 7.9: Indicative trends for the end-use of waste paper/board to 2010, assuming the production of paper/board garbage from 1999 is constant........209 Figure 7.10: Fibre flows for newspapers and advertising inserts and theoretical financial relationships between the manufacture of newsprint and printing papers for some companies, and newspaper publishers, distributors and subscribers. .........................................................211 Figure 8.1: Imports of softwood chips into Japan. ..................................................221 Figure 8.2: Imports of hardwood chips into Japan. .................................................222 Figure 8.3: Sources of woodchips imported into Japan by fibre type. ....................223 Figure 8.4: Imports of pulp into Japan for artificial fibre production and paper production.......................................................................................228 Figure 8.5: Paper and paperboard imports into Japan. ............................................230 Figure 8.6: The location of export woodchip schemes in Australia during the late-1990s. .................................................................................................235 Figure 8.7: The location of export woodchip schemes in Chile during the late-1990s. .......................................................................................................237 Figure 8.8: The location of export woodchip schemes in south eastern USA during the late-1990s.......................................................................................238 Figure 8.9: Imports into Japan of hardwood chips from the leading suppliers by nation. .........................................................................................240 Figure 8.10: CIF prices in Japan of hardwood chips from the leading supplier nations compared to that for chips from Australia............................241 Figure 8.11: Amounts and prices of exports of hardwood chips from Australia. ...243 Figure 8.12: Amounts and prices of exports of hardwood chips from Chile. .........244 Figure 8.13: Amounts and prices of hardwood chip exports to Japan from south eastern USA...........................................................................................245 Figure 8.14: The location of Japanese-owned foreign hardwood and softwood plantation projects. ..........................................................................257 Figure 8.15: Pulpwood supply zones in south eastern Alaska for Alaska Pulp Co and Louisiana Pacific Ketchikan. .........................................263 Figure 8.16: Forest Management Areas for wood-using companies in Alberta......264 Figure 9.1: The corporate structure of Daishowa during the mid- to late-1990s. ...276 Figure 9.2: The location of pulp and paper mills and offices of Daishowa in Japan during much of the 1990s. ....................................................................277 Figure 9.3: The location of the foreign operations of Daishowa during much of the 1990s. ..........................................................................................278

xviii

Figure 9.4: The profitability of Daishowa through the last half of the 20th century. ...............................................................................................282 Figure 9.5: The nominal value of the profits of Daishowa through the last half of the 20th century. ...................................................................................283 Figure 9.6: The nominal and real prices for Daishowa’s major products during the 1990s. .............................................................................................285 Figure 9.7: Paper and paperboard production by Daishowa within Japan. .............287 Figure 9.8: The consumption of pulpwood and recovered fibre

by Daishowa within Japan...............................................................................291 Figure 9.9: Sources of hardwood chips imported by Daishowa into Japan during the 1990s. .............................................................................................293 Figure 9.10: The area of the pulpwood supply agreement of Cariboo Pulp and Paper in British Columbia. .......................................................................296 Figure 9.11: The Forest Management Area of Daishowa-Marubeni International in Alberta. ..................................................................................302 Figure 9.12: Lubicon Indian Nation Traditional Lands...........................................307 Figure 9.13: The location of the public forests in south eastern NSW supplying pulpwood to Harris-Daishowa........................................................313 Figure 9.14: Annual woodchip exports of Harris-Daishowa...................................315 Figure 9.15: Sources of pulpwood for Harris-Daishowa.........................................317 Figure 9.16: Sawlog and pulpwood availability from the Eden region. ..................324 Figure 9.17: The amount and price of woodchip exports by Harris-Daishowa........331 Figure 9.18: The nominal and real value of the annual net profit of Harris-Daishowa..............................................................................................332 Figure 9.19: Different measures of the profitability of Harris-Daishowa . .............333 Figure 10.1: Advertisement by Oji Paper Co promoting its care for the natural environment...................................................................................338 Figure 10.2: Advertisement by Nippon Paper Industries promoting its care for the natural environment. ............................................................................339

xix

xx

Tables Table 3.1: Differences between hardwood and softwood fibres

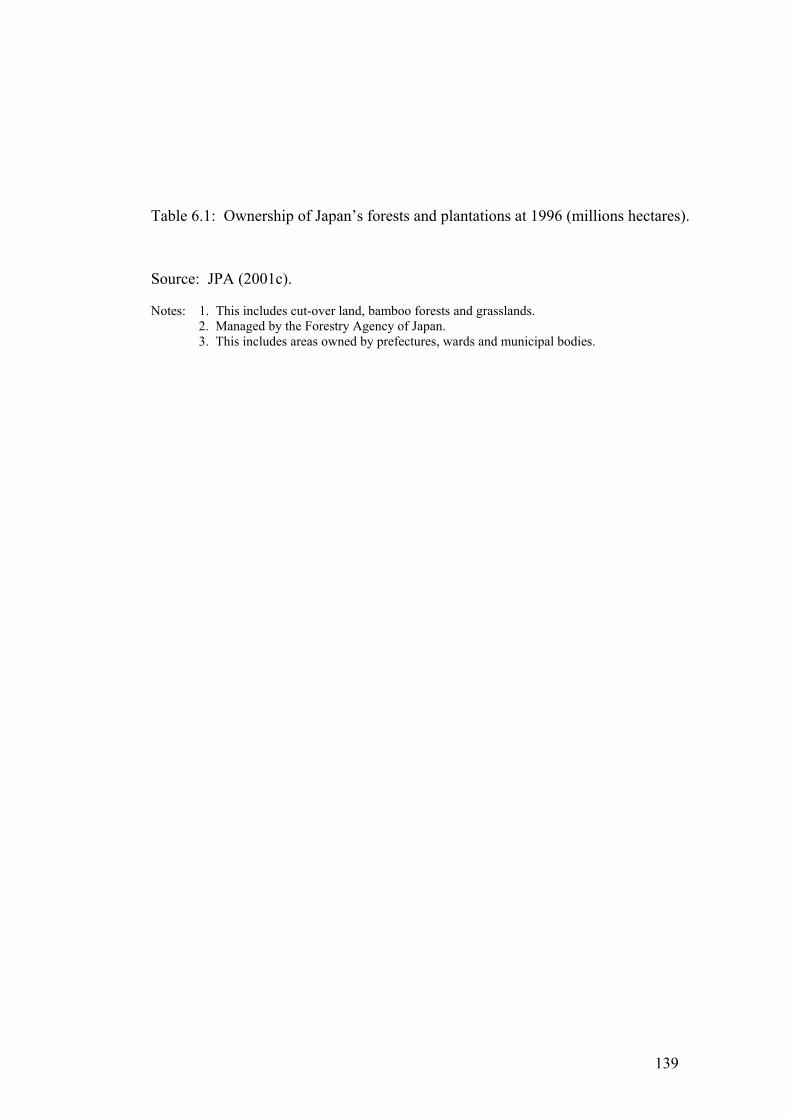

grown in Australia. ............................................................................................52 Table 3.2: Papermaking qualities of hardwood and softwood fibres. .......................53 Table 5.1: The use of corrugated cardboard boxes in Japan....................................100 Table 6.1: Ownership of Japan’s forests and plantations

at 1996 (millions hectares). .............................................................................139 Table 7.1: The theoretical upper limits for rates of recycling recovered

fibre in Japan that maintain product quality....................................................187 Table 7.2: Categories of waste paper and paperboard collectors in Japan. ..............193 Table 8.1: Preferences of Japanese papermakers for hardwood pulpwood. ............225 Table 9.1: The main products of Daishowa in Japan...............................................288 Table 9.2: The main commercial users in Japan of the products of

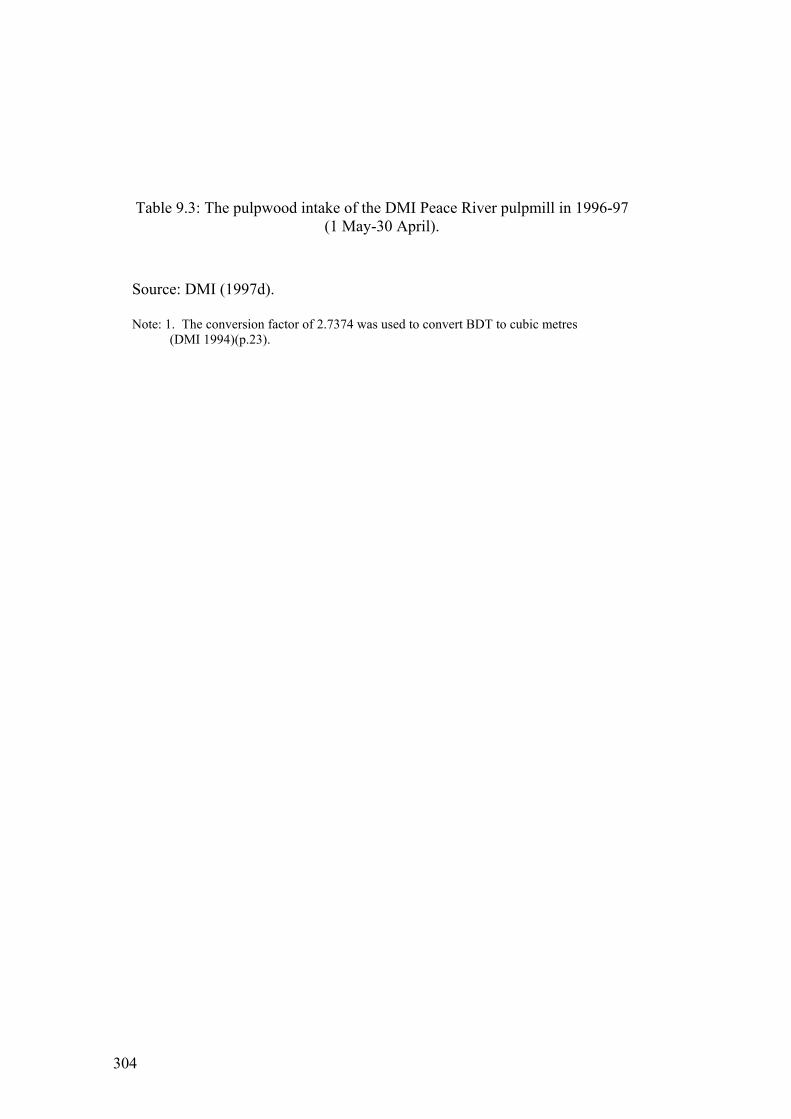

Daishowa during the 1990s. ............................................................................289 Table 9.3: The pulpwood intake of the DMI Peace River pulpmill

in 1996-97 (1 May-30 April)...........................................................................304 Table 10.1: Basic information on environmental protection interests

of general trading companies. .........................................................................343 Table 10.2: Main points from the environmental charters of selected

Japanese general trading companies................................................................344 Table 10.3: Basic information on environmental protection interests of

paper/board manufacturers. .............................................................................346 Table 10.4: Main points from the environmental charters of selected

Japanese paper/board manufacturers...............................................................347 Table 10.5: Awareness within general trading companies of forest

conservation issues in areas of foreign wood supply. .....................................358 Table 10.6: Awareness within paper/board manufacturers of forest

conservation issues in areas of foreign wood supply. .....................................359 Table 10.7: Attitudes of general trading companies to the establishment

of plantations and the use of plantation wood.................................................362 Table 10.8: Attitudes within paper/board manufacturers to the

establishment of plantations and the use of plantation wood..........................363 Table 10.9: Attitudes within general trading companies to the utilisation

of recovered fibre. ...........................................................................................364 Table 10.10: Attitudes within paper/board manufacturers to the utilisation

of recovered fibre. ...........................................................................................365 Table A 7.1: Japan: Waste paper product collection rates and volumes

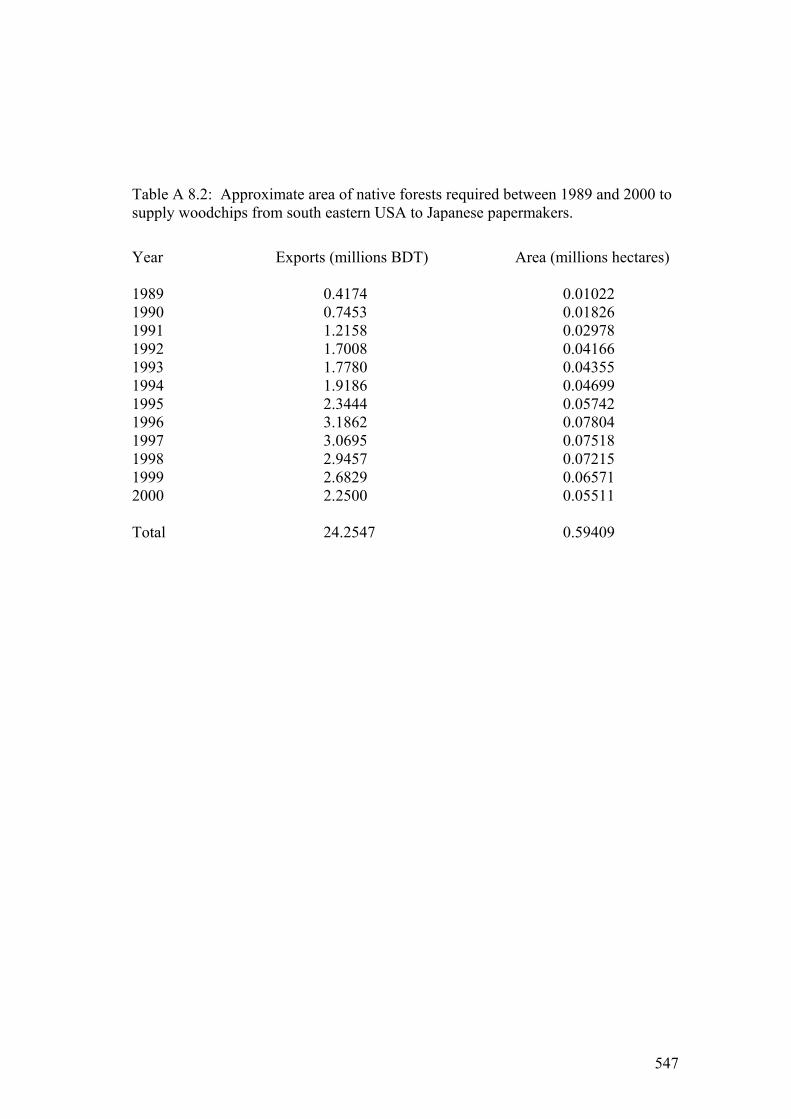

(1992 and 2000)...............................................................................................522 Table A 8.2: Approximate area of native forests required between 1989 and

2000 to supply woodchips from south eastern USA to Japanese papermakers.....................................................................................................547

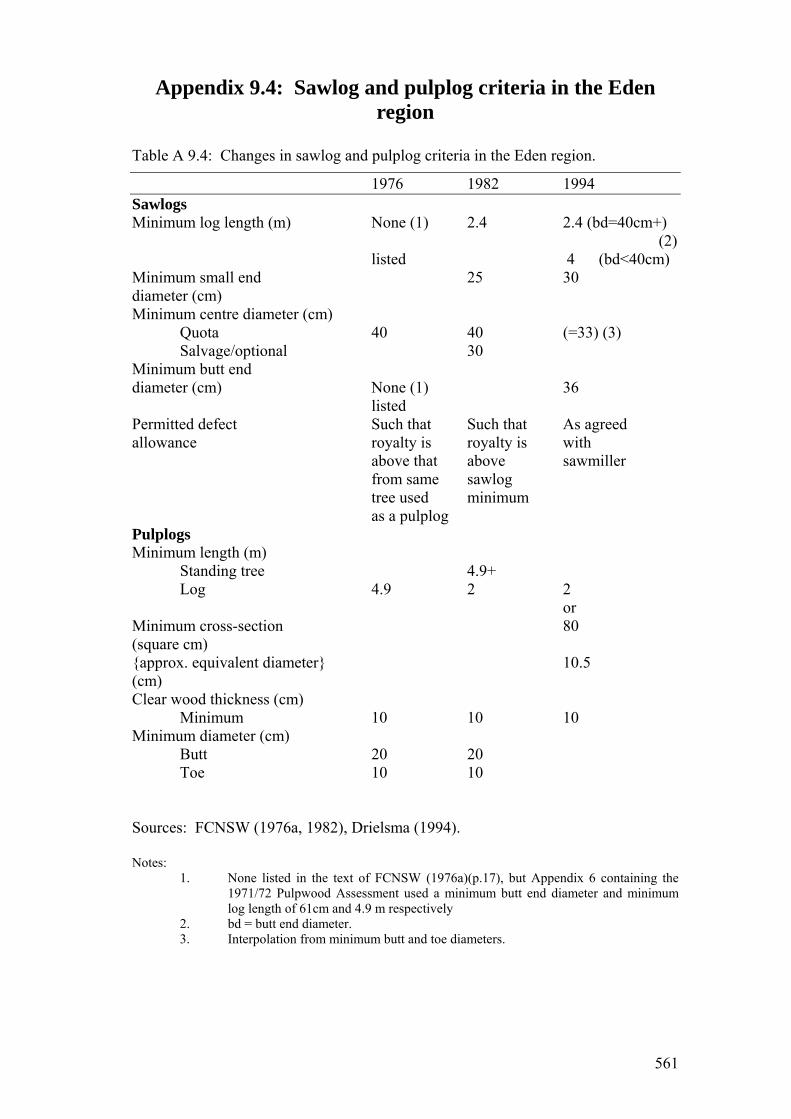

Table A 9.4: Changes in sawlog and pulplog criteria in the Eden region. ..............561

xxi

xxii

Abbreviations and special terms AAC Annual Allowable Cut. This is the amount of wood

permitted by the forest owner or manager to be removed by logging from an area of forests each year.

Alpac Alberta-Pacific Forest Industries. ALPC Alaska Lumber and Pulp Company. BDT Bone Dry Tonne. This is a common unit of measure for

woodchips that closely expresses their net fibre content. It is equivalent to 2203 pounds or 0.918 Bone Dry Units (BDU), where a BDU is 2400 pounds and a Green Metric Tonne is 2204.6 pounds (Neilson and Flynn 1997).

Burst strength “A measure of the ability of a sheet to resist rupture when or pressure is applied to one of its sides by a specified Bursting strength instrument, under specified conditions. It is largely

determined by the tensile strength and extensibility of the paper or paperboard” (Kouris 1996)(p.45).

Cellulose This substance is comprised of a large number of repeating

sugar molecules, so has the chemical formula ‘(C6H10O5)n’. The amount of repetition, referred to as the ‘degree of polymerisation’, reflects the strength of the cellulose and any organic fibre within which it occurs. There are various kinds of hemicelluloses that are also polymers of sugars, and they contribute to paper strength (Smook 1992, Biermann 1996).

CIF Cost, Insurance, Freight. CPPEI Council for Pulp and Paper Equipment Investment. Deinked pulp Pulp made from recovered fibre that has had the ink from its

previous use removed. Dissolving pulp High quality chemical pulp used to manufacture artificial

fibres. DMI Daishowa-Marubeni International. Ecological footprint The measure of an individual’s or population’s environmental

impact determined by converting the consumed resources into a land area equivalent. The measurement is not exact and outcomes depend on the assumptions used. It helps illustrate the relative impacts of lifestyles and policies (GDRC 2000).

EDF Environmental Defence Fund. EIS Environmental Impact Statement.

xxiii

EMS Environmental Management System. Esparto The generic name given to two species of grass from southern

Spain and northern Africa which contain high levels of cellulose that can easily be extracted for making paper (Magee 1997).

FOB Free On Board. Forest residues Wood of low industrial quality below that required to meet or the commercial criteria for sawlogs at any particular time Forest wastes taken from forests or plantations. Forestry services A general term to cover the public service departments of

national or state governments with responsibility for managing publicly-owned forests.

GTC General Trading Corporation. ha Hectares. HDA Harris-Daishowa (Australia) Pty. Ltd. Hinoki The conifer tree species, Chamaecyparis obtusa, also known

as Japanese cypress. It is one of the main species in Japan’s timber plantations.

IIED International Institute for Environment and Development. ISC The Industrial Structure Council that advised Japan’s

Ministry for International Trade and Industry. JANT The Japan and New Guinea Timber Co. established to operate

an export woodchip scheme at Madang in Papua New Guinea.

JPA Japan Paper Association. kg Kilograms. m3 Cubic metres. MAI Mean Annual Increment. MITI Japan’s Ministry for International Trade and Industry, now

the Ministry for Economy, Trade and Industry.

xxiv

NGO Non-governmental organisation. This term is mainly used in the dissertation in relation to community conservation organisations.

NIPF Non-industrial private forest. This term is used in relation to

one type of owner of private forests in south eastern USA. Sawmill residues Wood produced in sawmills or veneer mills from the or conversion of a round log into sawn timber or veneer sheets Sawmill wastes that may be chipped and sold for another commercial use. ppc Per capita consumption. PPC Plain paper copier. A term used in Japan for this type of

photocopier and also to refer to the paper used in such machines – PPC paper.

PRPC The Paper Recycling Promotion Center located in Tokyo,

Japan. Pulpwood Wood used to manufacture pulp for paper, paperboard or

artificial fibres. Recovered fibre A convenient and common term used to mean waste paper

and paperboard collected for utilisation as a fibre source for reuse, such as in paper and paperboard manufacturing.

Recovery rate The recovery rate for waste paper/board is used to provide an or an idea of the amount of waste paper/board collected in a Collection rate year. It is calculated by dividing ‘the net volume of waste

paper and paperboard recovered’ by ‘the net volume of paper and paperboard supplied for domestic consumption’. ‘Net recovery’ is calculated by subtracting waste paper and paperboard imports from the volumes received by manufacturers’ mills (including deinked pulp) and adding the volumes exported. The net volume of paper and paperboard supplied for domestic consumption is ‘the volume of paper and paperboard shipped from the manufacturers’ plus ‘imports’ minus ‘exports’ (PRPC 1998b, JPA 2001c).

Refining The mechanical treatment of pulp fibres to develop their or papermaking properties. It softens the fibres and roughens beating their outer layer so increasing their bonding ability and the

strength of the paper sheet, but at the expense of the strength of individual fibres (Biermann 1996).

Refiner groundwood A form of mechanical pulping that passes woodchips between pulping two rotating discs. The wood may be softened first using

heat or chemicals. Resource An available asset that can be used to achieve an objective

(Hawkins 1988).

xxv

Ringi “The process of obtaining the sanction (of executives) to a

plan by circulating the draft prepared by a person in charge (of the matter) (Masuda 1996).

Seishi The Japanese word for ‘paper manufacturing company’. This

word is used in the dissertation mainly as part of citations for companies that provided confidential information, eg Aseishi, Bseishi.

seNSW South eastern New South Wales. seUSA South eastern United States of America. Shosha The Japanese word for ‘trading company’. This word is used

in the dissertation mainly as part of citations for companies that provided confidential information, eg Ashosha, Bshosha. Sogo shosha are general trading companies.

Senkashi The Japanese word used for a low quality paper made or primarily of recovered fibre. Senka Stumpage The price charged/paid for wood purchased from a forest or owner. Royalty Sugi The conifer tree species, Cryptomeria japonica, also known

as Japanese cedar. It is one of the main species in Japan’s timber plantations.

Tear strength “The force required to tear a specimen under standardized

conditions” (Kouris 1996)(p.303). Tensile strength “The maximum tensile stress developed in a specimen before

rupture under prescribed conditions” (Kouris 1996)(p.304). TSA Timber Supply Area. This is the term is used in British

Columbia. A TSA is “an integrated resource management unit established in accordance with Section 6 of the Forest Act” used for administrative purposes (BCMOF 1994c)(p.1).

US United States of America. or USA Utilisation rate The utilisation rate for waste paper/board is used to provide or an idea of the amount of recovered fibre used by paper/board Recycling rate manufacturers. It is calculated by dividing the ‘volume of

recovered fibre used by the manufacturers’ by ‘the total volume of domestic and imported pulp’ used by those manufacturers (PRPC 1998b, JPA 2001c).

xxvi

Washi Japanese traditional-style paper. Woodchips Pulpwood converted to small pieces by mechanical methods

that can be used for production of paper, paperboard or particleboard.

Wood containing Paper containing mechanical pulp in which lignin remains. paper Woodfree paper Paper produced from chemical pulp that has had almost all

lignin removed. WW1 World War One. WW2 World War Two. The order of Japanese personal names presented in the dissertation follows the East Asian practice of writing the family name first.

xxvii

xxviii

Chapter 1: Introduction

1.1 International fibre resource links During early 1989, almost a thousand protestors were arrested in south eastern

Australia trying to stop logging of ‘wilderness’ forests for what they said was “the

most wasteful and least beneficial of all timber products – woodchips” (Salmon

1989)(p.12).1

One morning in early November 1990, landowners from the Gogol-Naru area of

northern Papua New Guinea, angry at the destruction caused by logging of local

rainforests, began a 5-day blockade of forest roads (Gogol 1991). Coordinated

international protests against this logging during May 1991 included a demonstration

in Tokyo (Jagoff and Seed 1991).

Also in November 1990, opponents of logging in native forests claimed by

Canadian aborigines as traditional lands burnt logging machinery used to supply

wood to a large pulpmill in Alberta Province (Goddard 1992, Pratt and Urquhart

1994).

In December 1995, forest conservation activists entered a woodchip loading

facility at the port of Mobile in southern United States of America (USA). They

interrupted the loading of a ship and hung a large banner on one of the cranes that

read "STOP EXPORTING FORESTS AND JOBS" (EF! 1996, NFN 1996b).

In April 1997, Japanese collectors and dealers of waste paper and paperboard

joined concerned citizens at a rally and public meeting in Tokyo to urge greater

recycling and protest at a dramatic slump in prices for recovered fibre (NSKS 1997).

These seemingly unrelated incidents are linked by a common element - the

Japanese paper and paperboard industry.2 This industry converts organic fibre from

these and other places into paper/board for use primarily in Japan. As well as being

1 Other references on this protest include: Bailey (1989a, 1989b); Garcia (1989); and Hinchey (1991). 2 For the sake of convenience and unless otherwise stated, the terms “the Japanese paper and paperboard industry”, “the Japanese paper/board industry” and "the Japanese paper industry" are used interchangeably in general discussions to include: companies located in Japan or elsewhere but ultimately owned by companies located in Japan that manufacture and/or distribute pulp, paper, paperboard and/or products made from them; as well as Japanese general trading companies (GTCs) involved in the trade of (i) wood and other paper-making fibre resources supplied to the Japanese paper/board companies and/or (ii) products made by them.

1

controversial, this international flow of fibre links the politics, economies,

communities and environments of widely dispersed nations and regions.

The subject of this dissertation is the Japanese paper/board industry and the

relationships and links it generates within and between the processes of fibre supply,

paper/board manufacture and distribution, and product use. The objective is to

understand the role that these fibres play within the industry and how these

relationships and links operate so that fibres from such disparate sources can be used

as manufactured products.

This chapter introduces the dissertation. First, the current Japanese paper/board

industry and its use of fibre are outlined. This overview is then used to illustrate the

importance of the research endeavour. Next, the questions investigated in the

dissertation are explained. Finally, the dissertation’s arguments are presented

through a description of each chapter’s themes.

1.2 Japan’s paper use and the Japanese paper industry Every day in Japan, countless paper and paperboard products are used for industrial,

commercial, cultural, educational and personal purposes. The four main categories

of products are: ‘printing and communication papers’ for writing, magazines and

books; ‘newsprint’ for newspapers; ‘sanitary papers’ for tissues and similar products;

and ‘containerboard’ for packaging. Through much of the late-20th century, Japan

was the world’s second largest paper/board producing nation – although well behind

the USA. Nearly all the production is used within Japan, and the nation’s use of

paper/board is directly related to its gross domestic product (JPA 2001b, 2001c).

In 2000, use totalled 31.74 million tonnes; Japanese people have the world’s

third highest apparent annual per capita consumption of paper/board at 250

kilograms (JPA 2001c). However, most Japanese citizens would not actually make

physical contact with this amount. Some is used within the social and economic

infrastructure that supports each person’s lifestyle, such as in offices, factories or

transport. Of that directly ‘consumed’, some would be used for the direct service

that it provides (paper for writing, reading or sanitary uses), while some would be the

result of a demand for other goods (packaging) and some may be unwanted

(advertising leaflets).

2

Japan produced 31.83 million tonnes of paper/board in 2000, of which 1.42

million tonnes were exported. Paper/board imports totalled 1.33 million tonnes (JPA

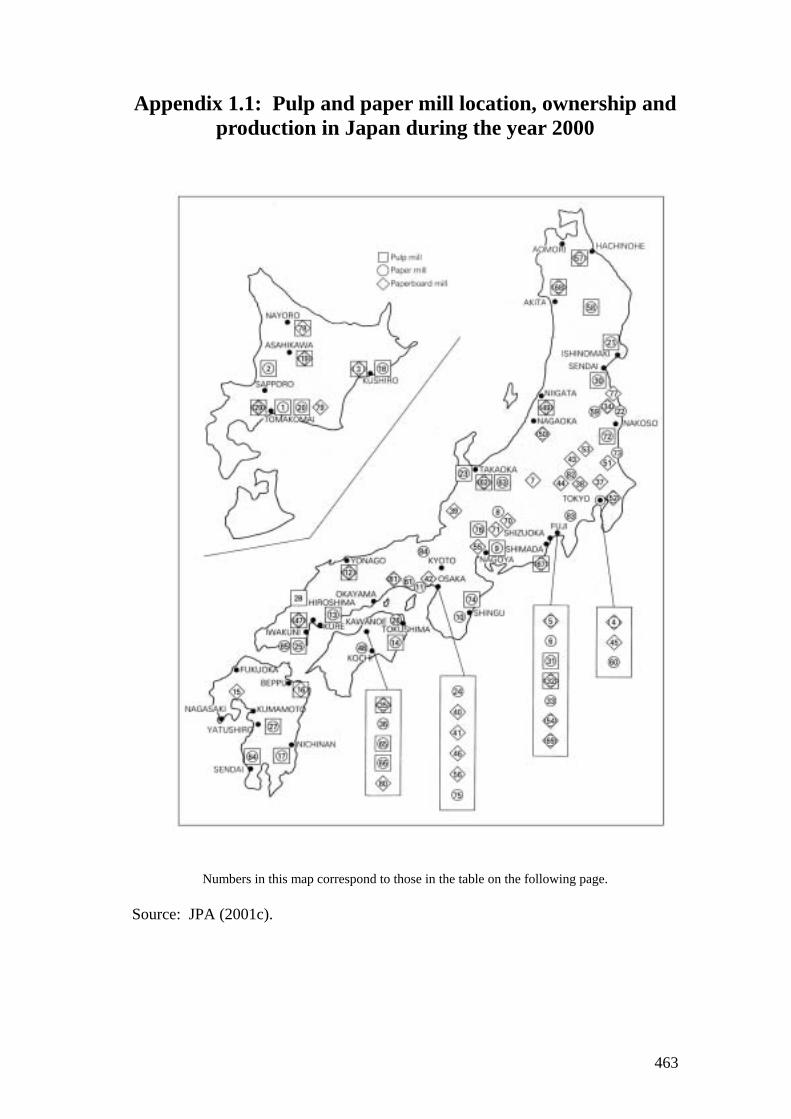

2001c). Pulp and papermills are dispersed throughout Japan (Appendix 1.1), but

despite the large number of companies related to manufacturing paper and

paperboard products in Japan (476 in 1998), production is highly concentrated. In

2000, 5 companies produced 50.7% of the nation’s paper and paperboard output; 10

produced 67.2%. Five companies produced 91% of all newsprint, 3 companies

produced 55% of all printing and communication papers, and 4 companies produced

45% of all paperboard products (JPA 2001b). These products are distributed to

commercial converters and users through a network of agents, general trading

companies (GTCs) and wholesalers who may also be linked through shareholdings

with manufacturers (Ausnewz 1998b). Most paper and paperboard production passes

through agents; GTCs have a large share of paperboard distribution and wholesalers

have a large share of paper distribution (JPA 2001c).

The flow of fibre through Japan’s paper/board industry (Figures 1.1 and 1.2) has

specific characteristics.

• Virtually all new fibres are from wood. Non-wood fibres comprised only 0.2%

(19,000 tonnes) of new pulp used in 1999 (JPA 2001a, 2001c).

• The great majority of new fibre goes into paper products, while paperboard

production uses most of the recovered fibre. In 2000, 57.2% of the industry’s

fibre was recovered from waste paper/board. Thirty two percent of the recovered

fibre went into paper products and 68% was used for paperboard (JPA 2001c).

• The industry is highly dependent on foreign sources for new fibre. Of the

pulpwood used to make pulp in Japan during 2000, 70% was directly imported.

Of the hardwood pulpwood, 85% was directly imported. Of the softwood

pulpwood, 56% was directly imported, but a substantial portion of the softwood

pulpwood supplied domestically is from imported sawlogs processed in Japan.

Further, 18.5% of pulp used in Japan for paper/board production was imported;

much of this comes from mills in which Japanese companies have invested (JPA

2001a, 2001c).

3

Figure 1.1: The general flow of fibre through the Japanese paper/board industry.

4

Figure 1.2: The flow of fibre for pulp, paper and paperboard production in Japan during 2000.

Source: JPA (2001c).

Note: Some losses of fibre occur between different stages and some values were rounded off.

5

• Hardwood fibre dominates pulpwood used to make pulp in Japan (61%); 39% is

softwood pulpwood. Particular fibre types are directed to specific pulp grades.

For example, in 2000, 75% of pulp made in Japan was bleached chemical pulp,

and 85% of its fibres were hardwood pulpwood. Unbleached chemical pulp was

13.4% of domestically manufactured pulp, and comprised 94% softwood

pulpwood (JPA 2001a).

• Almost all the pulpwood used for pulp manufacture in Japan is supplied as

woodchips. In 2000, only 2.5% of pulpwood consumption was logs, which came

predominantly from within Japan (JPA 2001a).

• Most hardwood pulpwood used for pulp manufacture in Japan during 1999 came

directly from native forests (63%), while softwood pulpwood came

predominantly from sawmill chips (57%) (JPA 2001a).

• Most imported woodchips are traded through one of Japan's large GTCs (PBR

2001). These companies are shareholders in many foreign plantation and

woodchip supply projects (Neilson and Flynn 1997, JPA 2001c). They also

import pulp and paper (JP&P 1990g), are shareholders in paper and paperboard

manufacturers (TKI 1994), and are involved in foreign pulp, paper and

paperboard mills with Japanese paper companies (JPA 2001c).

1.3 The research importance of Japan’s paper industry

1.3.1 Research issues and Japan’s paper industry These characteristics of Japan’s recent paper/board use, manufacturing and

distribution, and fibre supply express the interaction of economic and other

relationships directing the flow of fibres from the site of extraction to the end-user.

The international protests focus attention on the importance of the industry’s fibre

use for three linked issues relevant to modern societies:

• the relationships between industrial structure and the flows of natural resources

and environmental impacts;

• the application by companies of policies for environmental protection and

resource use; and

• the consumption of resources and the natural environment by Japan and Japanese

companies.

6

1.3.2 Industrial structure and natural resources Complex and changing flows of capital, resources and products now stretch across

national boundaries to meet investor requirements for profits, the political objectives

of governments and market demands for manufactured goods. There is considerable

debate about the appropriate theoretical perspectives from which to analyse the

emergence of, and changes in, such transnational flows. Interactions between local,

national and international forces are particularly important (Broad 1995, Fagan and

Webber 1996, Dicken 1998).

Economy–environment interactions are important forces in creating industrial

structures, while the environmental impacts of an industry’s activities are influenced

by its structure. Many environmental impacts now extend across national borders in

association with economic linkages such as the trade in natural resources,

manufactured goods and financial services. As such, they are of major international

political concern (Brown et al 1999). For example, the national and international

trade in industrial wood products increased substantially during the 20th century

(FAO 1998). Supplying primary resources to wood products industries, particularly

in wealthy developed countries, is important to the management of the world’s

forests. Japan’s wood products industry is seen as a major force in the development

of ‘the global forest economy’, and linked to the deterioration and destruction of

forest values in some areas (Dudley 1992, Marchak 1995, Dauvergne 1997b).

Forest degradation caused by agricultural clearing, wood extraction and other

uses is of such global significance that the 1992 United Nations Conference on

Environment and Development formulated programs to reduce destructive pressures

on forests and wood resources (Quarrie 1992). Given international trade links and

the high resource use in developed countries, lower rates of logging in those

countries for conservation objectives may encourage destructive logging elsewhere

and/or the greater use of energy-intensive non-renewable resources (Lippke 1992,

Perez-Garcia 1993). Conservation interests promote reduced consumption of wood-

based products in high-use nations (Buitenkamp et al 1993, Rice 1995).

However, interpreting the contribution of economy–environment interactions to

industrial restructuring, especially at an international level, is undeveloped relative to

the effort spent on studying the organisation of production and its social implications

(Taylor 1996). Environmental factors need greater integration into theories

7

explaining patterns of industrial structure and resource use. Such factors include the

influence of: the characteristics of natural resources; control over resource

exploitation; and regulation of environmental impacts from international trade

(Broad 1995, Taylor 1996, Dicken 1998). Because paper/board companies consume

natural resources from different nations and manufacture products for national and

multinational markets (FAO 1998) they have transnational economic and

environmental links. Such links are important in shaping the future development of

the world’s paper/board companies (IIED 1996). This dissertation’s examination of

fibre use by the Japanese paper/board industry further exposes the relationships

between environment-economy interactions and industrial structures.

1.3.3 The application of environmental policies Paper production consumes large amounts of organic fibre, water, chemicals and

energy, and generates large amounts of waste (IIED 1996). However, the industry

has improved its treatment of liquid effluent, increased recycling of waste paper and

increased its efficiency of resource use (Wrist 1992, Dunwoody 1998). Also,

industrial forestry techniques, including genetic manipulation, are promoted as

improving forest quality (Ow Yang and Coleman 1998). Paper is claimed to have

“an ecocycle advantage over most competitive materials” (Colasurdo 1998)(p.77)

because of its renewable and reusable characteristics (Anon 1993, Dunwoody 1998).

Industry members also fear governments may impose stringent environmental

protection standards and regulations that will damage the use of paper and the

competitiveness of paper companies (von Ungern-Sternberg 1995, Glowinski 1997).

However, the introduction of advanced pulping, bleaching and pollution control

technologies by south-east Asian papermakers is argued to have assisted their

competitiveness and been the result of business, regulatory and community pressures

(Sonnenfeld 1998a, 1998b). In Australia, environmental protection standards that

made high waste production incompatible with low production costs encouraged

paper companies to adopt new corporate structures, products and technologies that

all assisted their competitiveness (Waitt 1997). Japan’s paper and trading companies

now promote many of their policies and actions in the fields of fibre supply,

pollution control and product development as being friendly to the environment

(Marubeni 1994, Sumitomo 1996, Nippon 1999a, Oji 1999c).

8

However, the recent study by the International Institute for Environment and

Development on the environmental sustainability of the world’s paper industries

(IIED 1996) contains little information on fibre resource management by the

Japanese paper industry. This was seen within the industry as a flaw in the study

(AP&P 1996b), but there is no detailed research that relates the environmental

consequences of the industry’s fibre use to its structure, company policies and

attitudes, and Japan’s paper/board use. This dissertation addresses this deficiency.

1.3.4 Japan and Japanese companies as resource consumers Japan’s international links are now essential for the operation of its economy and

important for the economic activity of other nations. In 1998, Japan accounted for

13.4% of the world’s gross domestic product and is a major global locus for

manufacturing, international trade, investment funds and foreign aid (Helton and

Imai 1997, Dicken 1998). It depends heavily on foreign raw materials and food

products (Kawai and Suzuki 2000). As a result, the ‘ecological footprint’ generated

by Tokyo’s population is calculated at 2 to 3 times the total area of Japan (GDRC

2000).

These international trade and aid links transfer with them Japanese economic,

political, environmental and cultural priorities. They interact with priorities in other

nations to generate impacts and shape their mutual development (Dauvergne 1997b).

The way Japanese investment and resource acquisition occurs in other countries is of

considerable research interest (Hollerman 1988, Bunker 1994a, Marques 1994).

However, the foreign activities of Japanese industries should be related to their

domestic experiences if the dynamics of international interactions are to be

understood thoroughly (Cameron 1996). For example, the pollution problems

generated by Japan’s economic growth are considered “an essential part of the

structure” of Japan’s economy (Ui 1974)(p.574).

Japan’s environmental performance has been evaluated as the worst – an

‘environmental predator’ (Maull 1991) – and as one of the best – an ‘ecological

front-runner’ (Mol and Sonnenfeld 2000). Yellowlees (1998)(p.20) states that

“(d)uring the past 15 years many of corporate Japan’s environmental efforts have

been cosmetic, public relations-related attempts at convincing the public that the

firms are eco-friendly.” However, he concludes that more recently “the substance

and the underlying forces below these efforts are becoming increasingly real” (p.23).

9

Mitsuhashi (2000) argues that Japan’s senior industrialists want to lead the world

in creating a resource-efficient society. A recent report by Japanese industrialists and

academics considers that Japanese industry will become more recycling-oriented and

construct “economic growth that is harmonious with the environment” (JCIP

1997)(p.381). However, as with other studies of Japan’s economy, it ignores the

paper industry. Detailed research on Japan’s industrial use of domestic and foreign

forests has also tended to concentrate on the supply of wood for construction rather

than paper (Handa 1988a, Nectoux and Kuroda 1989, Robertson and Waggener

1992, Dauvergne 1997b).3

Research within Japan’s paper industry on technical aspects of fibre supply and

papermaking continues. However, as articles in the journal of the Japan Technical

Association of the Pulp and Paper Industry illustrate, fibre resource issues are

primarily addressed from within a paradigm that is supportive of industrial

production.4 Major Japanese academic research on the industry concentrates on

domestic activities and wood supply, but does not detail the recent consequences for

foreign resources (Suzuki 1967, Narita 1980, Ishii 1992, Hagino 1996). However, as

the industry’s fibre supply became more international, research interest broadened to

include:

• foreign consultants examining fibre markets (Fenton 1988, Neilson and Flynn

1997, Ausnewz 1998b, Ausnewz 2001);

• Japanese government researchers concerned with the implications of foreign

environmental policies on Japan’s international relations (Morita 1987);

• non-government organisations and activists concerned with environmental and

social impacts (ACF 1987, Nectoux and Kuroda 1989, Penna 1992, Shimizu

1996); and

• foreign academic researchers studying regional forest issues (Routley and

Routley 1975, Lamb 1988, Pratt and Urquhart 1994, Dargavel 1995).

However, this literature does not integrate the long-term historical relationships

between changing industrial structure, products, and fibre supply with domestic and

3 See also issues of the irregular journal of the Japanese Forest Economics Society, ‘The Current State of Japanese Forestry - Its Problems and Future’. 4 This is the ‘Kamiparupu gijutsu kyoukai zasshi’ (or Japan TAPPI Journal).

10

foreign social and environmental issues. This dissertation helps fill this gap and

contributes to understanding the interactions of a significant Japanese industry with

domestic and foreign environments.

1.4 Research questions Thus, studying the flow of fibre associated with the Japanese paper industry brings

together issues of international social and environmental importance. This

dissertation addresses these issues by investigating several questions. The central

questions tackle the historical relationships underlying the characteristics listed in

Section 1.2:

How are the development, structure and operation of the Japanese paper industry

related to the use, management and control of its fibre resources? How do these

relationships influence both the industry's development and its use of fibre

resources?

Three subsidiary questions make the research more comprehensive. An

important consideration for how a forest is exploited is the amount of protection

given to non-wood values, as they can be diminished by wood production. It is thus

necessary to examine the interaction between the fibre demands of paper companies,

resource characteristics and the desires of forest owners or managers. The first

subsidiary question is:

How do patterns of fibre supply to the Japanese paper industry affect fibre-related

environmental values?

The attitudes of senior management and planners in Japanese paper/board

companies towards environmental problems must influence the industry’s

development. Of concern are the values and priorities that dominate within

companies and whether they are sufficient to protect fibre-related environmental

values while satisfying a company’s resource demands. The second subsidiary

question is:

How do decision-makers within the Japanese paper industry perceive fibre supply

strategies, forest management issues and waste paper recycling, and then

incorporate those perceptions into their decision-making processes to meet

corporate objectives?

11

The Japanese paper industry is heavily dependent on fibre from foreign sources.

Thus, Japanese companies and Japan’s paper use interact with changes at the

international and global levels in markets, fibre resources, and flows of capital and

fibre. The third subsidiary question is:

How do Japanese paper/board companies contribute to international economic and

environmental restructuring through their fibre sourcing strategies?

1.5 Structure of the dissertation The dissertation begins answering these questions by reviewing literature about the

relationships between industrial structure and resource use and the operation of the

paper industry and the roles of fibre in papermaking. This is done over two chapters.

Chapter Two presents the main theoretical base used in the dissertation. It

integrates perspectives on resource exploitation, industrial structure and economy-

environment interactions to develop an analytical position within the ‘political

ecology’ paradigm. This paradigm seeks to explain “the topography of a politicised

environment” through the “integration of human activities and environmental