Embed Size (px)

Citation preview

Preparing for $10 Billion and Beyond

Mike Guglielmo

Managing Director

David Ballas

Sr. Sales Executive

The Pathway to SuccessThursday, April 27 10:30-11:20

Page 2

Preparing for $10 Billion and Beyond

Page 3

A

B

C

D

Introduction

Key areas of focus, lessons learned (fact vs. fiction)

Dodd-Frank Act Stress Test (DFAST)

Regulatory context, goals, issues and challenges, major modeling decisions

Model Risk Management

MRM framework, the “three line of defense”, effective challenge

Concluding Thoughts

Getting strategic value from DFAST and MRM, Q&A

Survival PlanningPREPARING FOR $10 BILLION AND BEYOND

Page 4

A

B

C

D

Introduction

Key areas of focus, lessons learned (fact vs. fiction)

Dodd-Frank Act Stress Test (DFAST)

Regulatory context, goals, issues and challenges, major modeling decisions

Model Risk Management

MRM framework, the “three line of defense”, effective challenge

Concluding Thoughts

Getting strategic value from DFAST and MRM, Q&A

Survival PlanningPREPARING FOR $10 BILLION AND BEYOND

Page 5

Three Notable Areas of Focus

• Consumer Financial Protection Bureau (CFPB)

• Dodd-Frank Act Stress Testing (DFAST)

• Model Risk Management (MRM)

Page 6

Fact or Fiction: Lessons LearnedREALITIES AND MISCONCEPTIONS

• Regulators will give you time once you cross $10B in assets

• Stress testing is just for regulatory compliance

• Average DFAST development costs exceed $1m

• DFAST can be fully outsourced

• It is challenging to find/retain quality resources

• Good documentation is crucial to success

Page 7

A

B

C

D

Introduction

Key areas of focus, lessons learned (fact vs. fiction)

Dodd-Frank Act Stress Test (DFAST)

Regulatory context, goals, issues and challenges, major modeling decisions

Model Risk Management

MRM framework, the “three line of defense”, effective challenge

Concluding Thoughts

Getting strategic value from DFAST and MRM, Q&A

Survival PlanningPREPARING FOR $10 BILLION AND BEYOND

Page 8

DFAST

Page 9

Mandatory Stress Testing:

A Response to Taxpayer “Bailout”GOAL: PREVENT BAILOUTS; TOOLS: GOVERNANCE & IMPROVED RISK MANAGEMENT

• Initial focus upon top 5-6

Recovery Planning & Resolution Plans

Stress Testing

• Then CCAR top 18-19

Comprehensive Capital Analysis & Review

Consistent Stress Testing

• Then CapPR over $50B

Capital Plan Review

• Then $10B-$50B DFAST institutions

• Community Banks?

Page 10

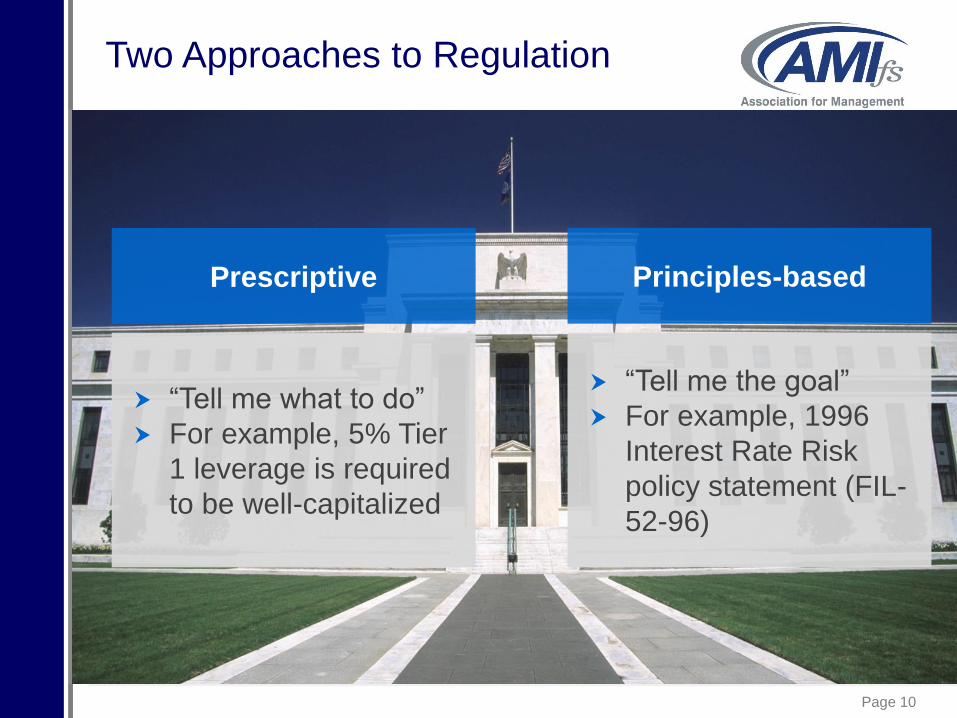

Two Approaches to Regulation

Prescriptive

“Tell me what to do”

For example, 5% Tier

1 leverage is required

to be well-capitalized

Principles-based

“Tell me the goal”

For example, 1996

Interest Rate Risk

policy statement (FIL-

52-96)

Page 11

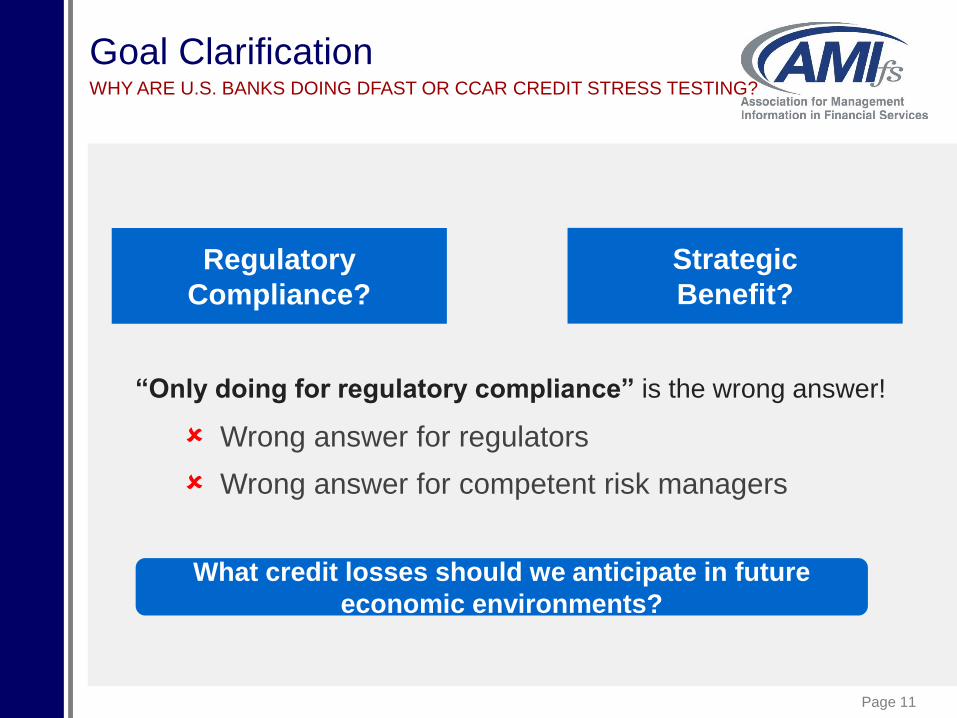

Goal ClarificationWHY ARE U.S. BANKS DOING DFAST OR CCAR CREDIT STRESS TESTING?

“Only doing for regulatory compliance” is the wrong answer!

Regulatory

Compliance?

Strategic

Benefit?

Wrong answer for regulators

Wrong answer for competent risk managers

What credit losses should we anticipate in future

economic environments?

Page 12

The “board” is “regulatory compliance”

“beyond” is “strategic benefit”

Focus Beyond the Board

Banks who have focused on the

board have gotten hurt…

Page 13

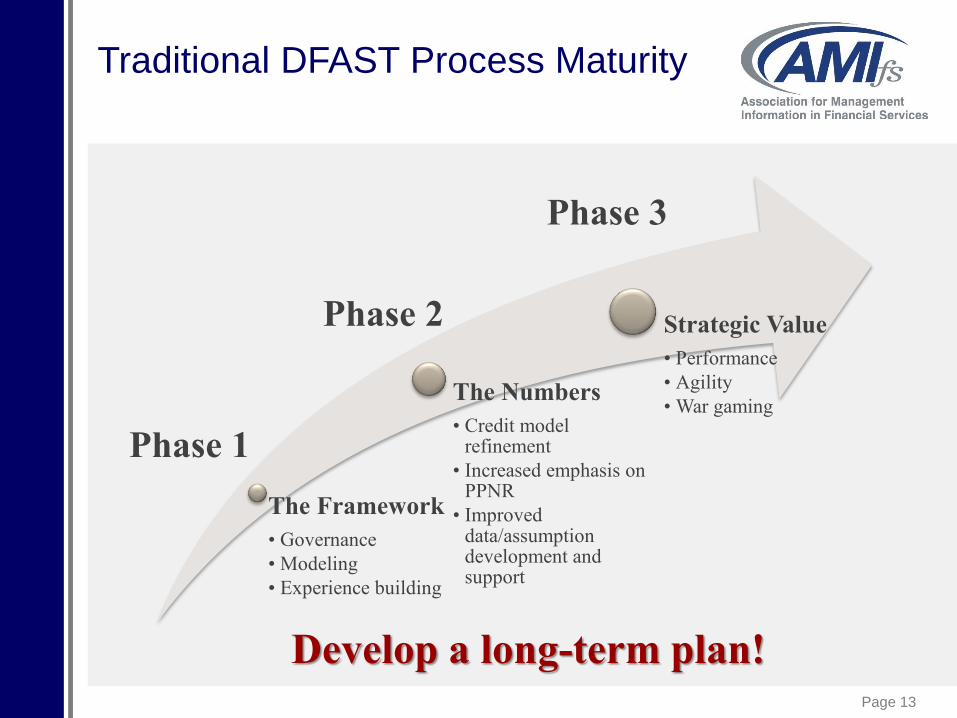

Traditional DFAST Process Maturity

The Framework

• Governance

• Modeling

• Experience building

The Numbers

• Credit model refinement

• Increased emphasis on PPNR

• Improved data/assumption development and support

Strategic Value

• Performance

• Agility

• War gaming

Phase 1

Phase 2

Phase 3

Develop a long-term plan!

Page 14

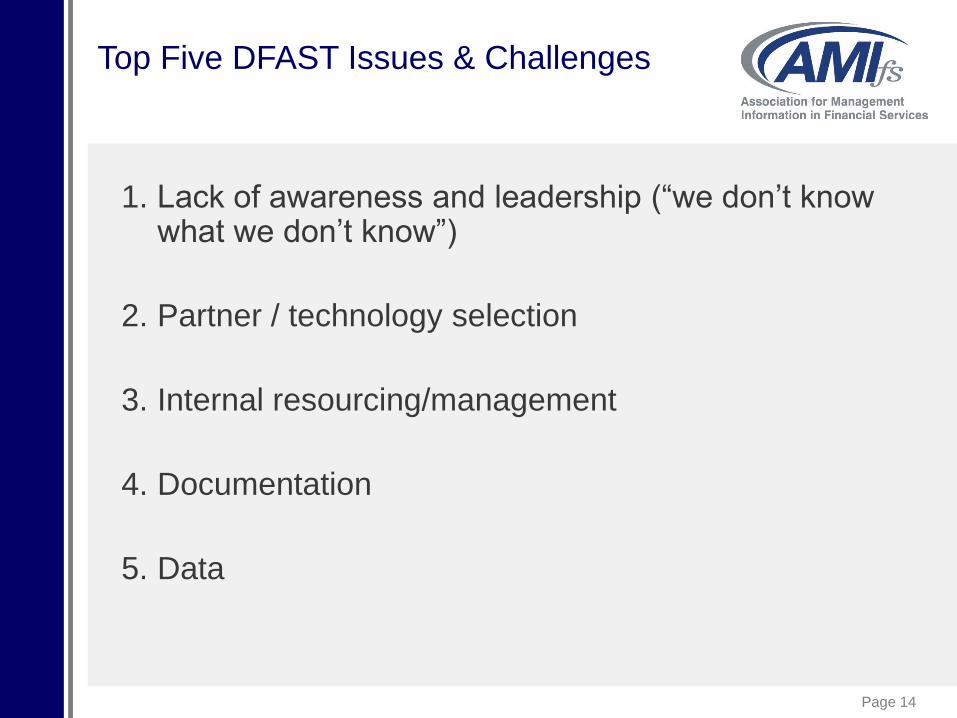

Top Five DFAST Issues & Challenges

1. Lack of awareness and leadership (“we don’t know what we don’t know”)

2. Partner / technology selection

3. Internal resourcing/management

4. Documentation

5. Data

Page 15

Strengthening Awareness

• Education

– Conferences/seminars

– In-house executive and Board table top discussions

– Regulatory forums

– Direct interactions with examiners

• Gap analysis

• Peer outreach

Leadership tone drives level of success

Page 16

Partner and Technology Selection

• Readiness assessments (gap analyses)

• Governance framework

• Development partner(s)

– Credit loss modeling

– PPNR (Pre-Provision Net Revenue) modeling

– ALM model integration & reporting

• Documentation

• Validation

Due diligence is critical

Page 17

Major DFAST Modeling Decisions

1. Development Options

2. Aggregator Model Options

3. Peer Group Selection

Page 18

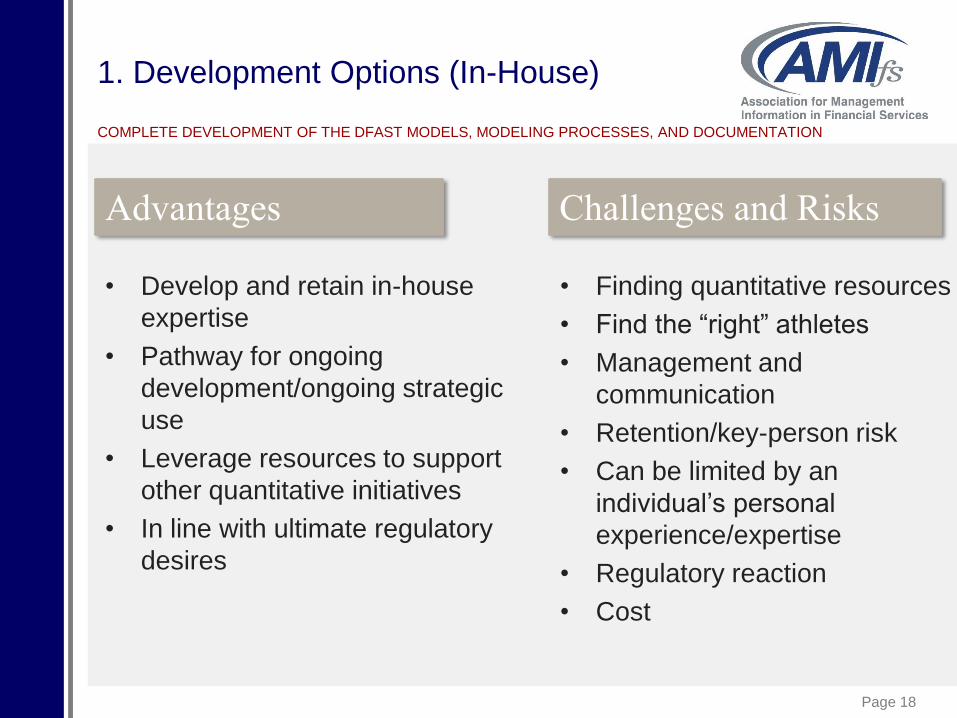

• Develop and retain in-house

expertise

• Pathway for ongoing

development/ongoing strategic

use

• Leverage resources to support

other quantitative initiatives

• In line with ultimate regulatory

desires

1. Development Options (In-House)

• Finding quantitative resources

• Find the “right” athletes

• Management and

communication

• Retention/key-person risk

• Can be limited by an

individual’s personal

experience/expertise

• Regulatory reaction

• Cost

Advantages Challenges and Risks

COMPLETE DEVELOPMENT OF THE DFAST MODELS, MODELING PROCESSES, AND DOCUMENTATION

Page 19

Staffing Challenges

• Underestimated budget

• Thinning talent pool

• Skillset gaps

• Communication

• Training

• Retention

Page 20

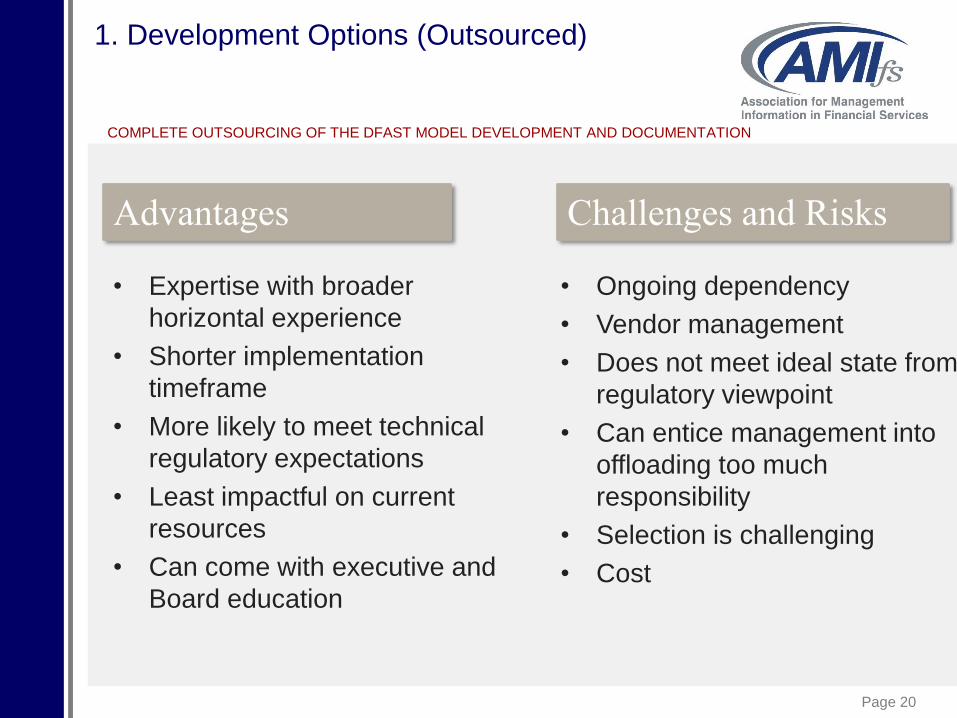

• Expertise with broader

horizontal experience

• Shorter implementation

timeframe

• More likely to meet technical

regulatory expectations

• Least impactful on current

resources

• Can come with executive and

Board education

1. Development Options (Outsourced)

• Ongoing dependency

• Vendor management

• Does not meet ideal state from

regulatory viewpoint

• Can entice management into

offloading too much

responsibility

• Selection is challenging

• Cost

Advantages Challenges and Risks

COMPLETE OUTSOURCING OF THE DFAST MODEL DEVELOPMENT AND DOCUMENTATION

Page 21

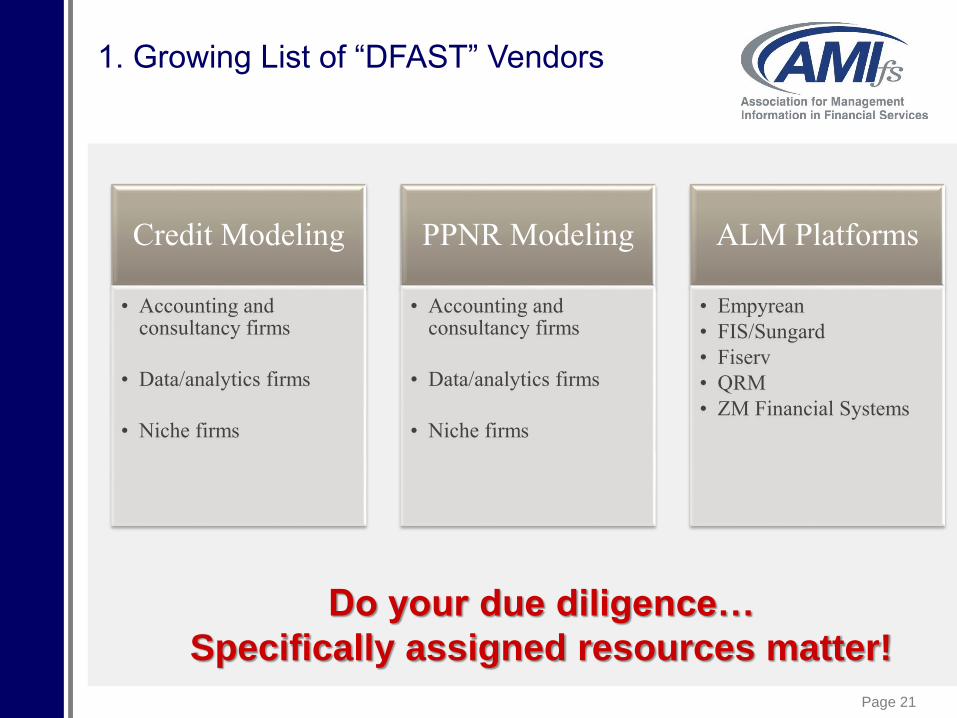

1. Growing List of “DFAST” Vendors

Credit Modeling

• Accounting and consultancy firms

• Data/analytics firms

• Niche firms

PPNR Modeling

• Accounting and consultancy firms

• Data/analytics firms

• Niche firms

ALM Platforms

• Empyrean

• FIS/Sungard

• Fiserv

• QRM

• ZM Financial Systems

Do your due diligence…

Specifically assigned resources matter!

Page 22

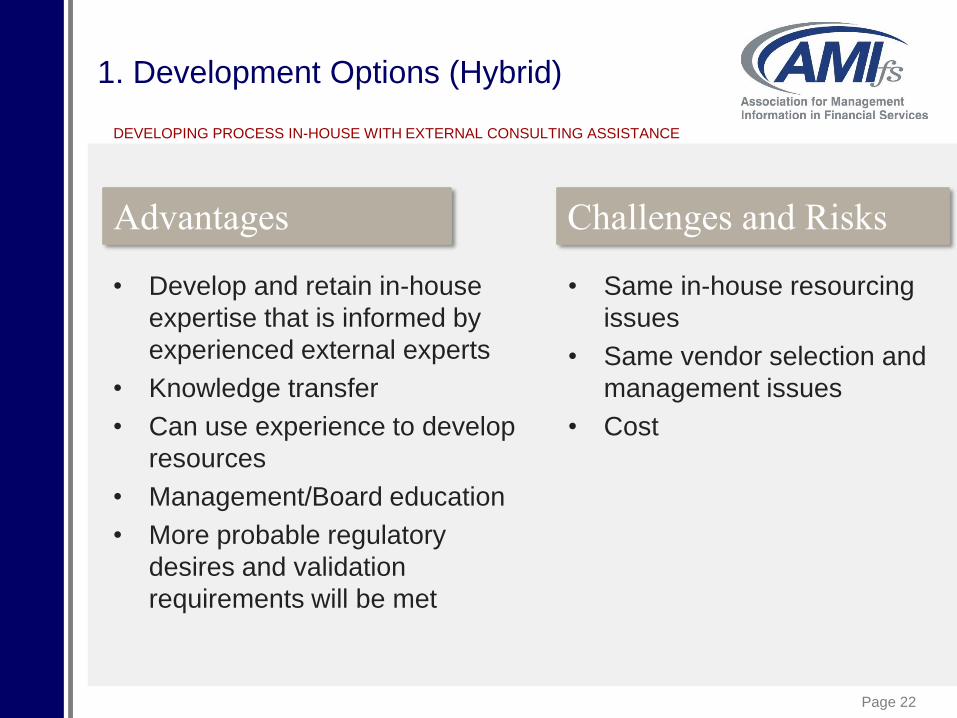

• Develop and retain in-house

expertise that is informed by

experienced external experts

• Knowledge transfer

• Can use experience to develop

resources

• Management/Board education

• More probable regulatory

desires and validation

requirements will be met

1. Development Options (Hybrid)

• Same in-house resourcing

issues

• Same vendor selection and

management issues

• Cost

Advantages Challenges and Risks

DEVELOPING PROCESS IN-HOUSE WITH EXTERNAL CONSULTING ASSISTANCE

Page 23

Major DFAST Modeling Decisions

1. Development Options

2. Aggregator Model Options

3. Peer Group Selection

Page 24

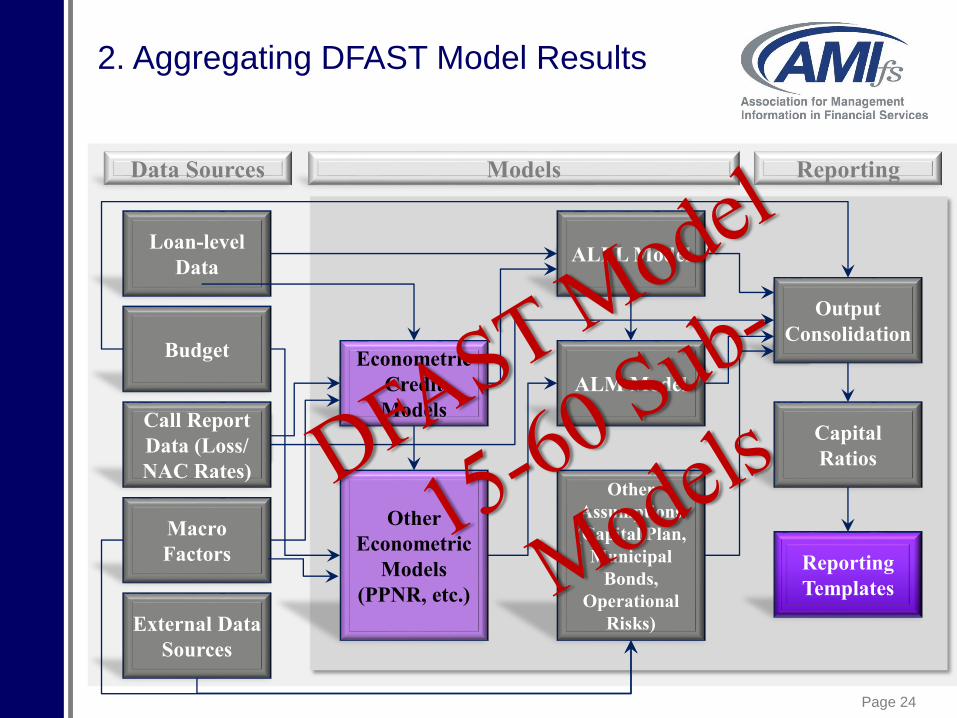

2. Aggregating DFAST Model Results

Call Report

Data (Loss/

NAC Rates)

Macro

Factors

Budget

Loan-level

Data

Econometric

Credit

Models

Other

Econometric

Models

(PPNR, etc.)

ALM Model

ALLL Model

Other

Assumptions

(Capital Plan,

Municipal

Bonds,

Operational

Risks)

Output

Consolidation

External Data

Sources

Reporting

Templates

Capital

Ratios

Data Sources Models Reporting

Page 25

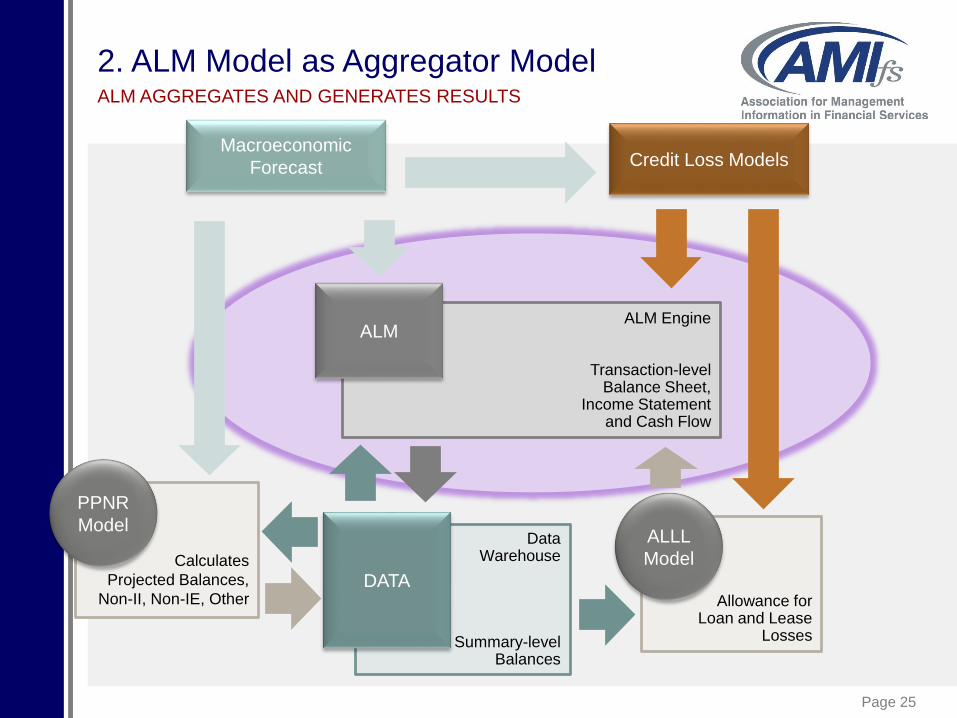

2. ALM Model as Aggregator ModelALM AGGREGATES AND GENERATES RESULTS

Macroeconomic

Forecast

DataWarehouse

Summary-level Balances

DATA

Credit Loss Models

Calculates

Projected Balances,

Non-II, Non-IE, Other

PPNR

Model

Allowance for Loan and Lease

Losses

ALLL

Model

ALM Engine

Transaction-levelBalance Sheet,

Income Statementand Cash Flow

ALM

Page 26

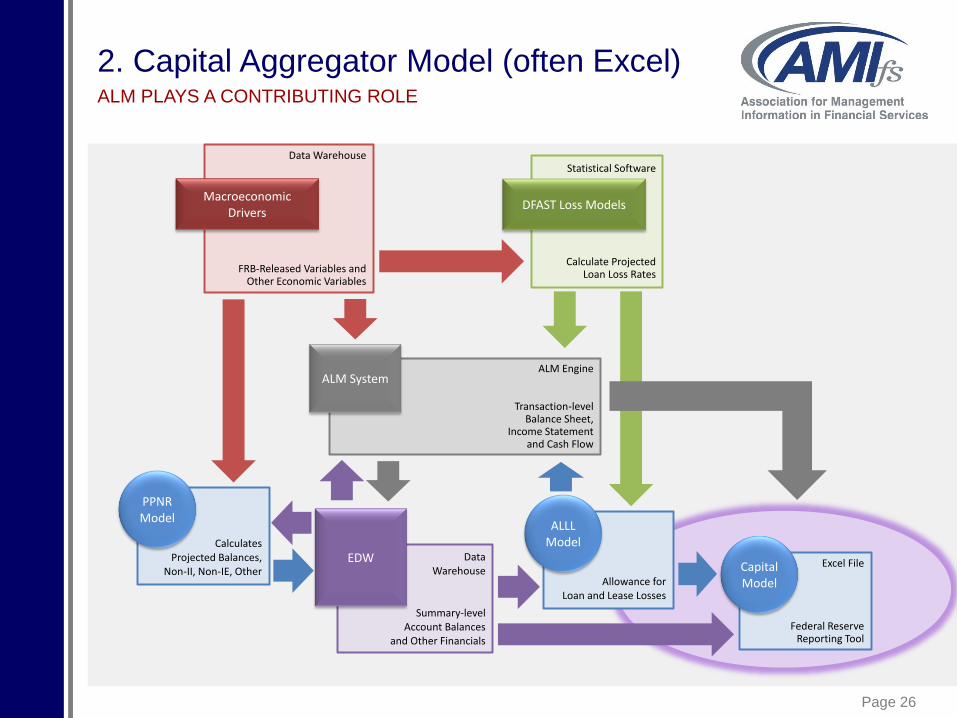

2. Capital Aggregator Model (often Excel)ALM PLAYS A CONTRIBUTING ROLE

Data Warehouse

FRB-Released Variables and Other Economic Variables

MacroeconomicDrivers

DataWarehouse

Summary-levelAccount Balances

and Other Financials

EDW

Statistical Software

Calculate ProjectedLoan Loss Rates

DFAST Loss Models

CalculatesProjected Balances,

Non-II, Non-IE, Other

PPNRModel

Excel File

Federal Reserve Reporting Tool

CapitalModelAllowance for

Loan and Lease Losses

ALLLModel

ALM Engine

Transaction-levelBalance Sheet,

Income Statementand Cash Flow

ALM System

Page 27

Major DFAST Modeling Decisions

1. Development Options

2. Aggregator Model Options

3. Peer Group Selection

Page 28

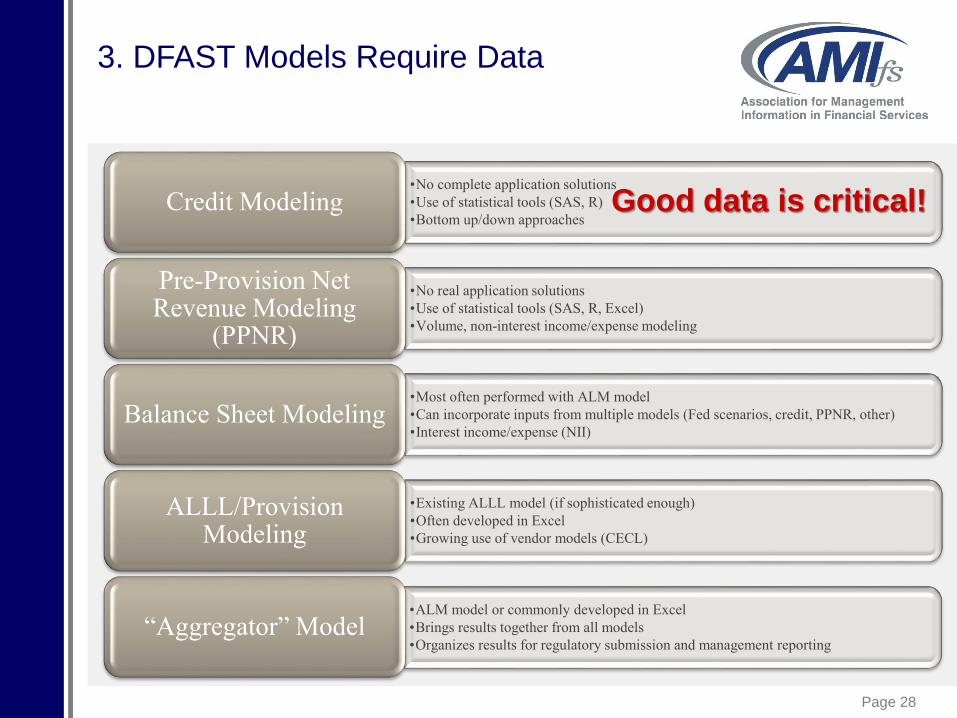

3. DFAST Models Require Data

•No complete application solutions

•Use of statistical tools (SAS, R)

•Bottom up/down approachesCredit Modeling

•No real application solutions

•Use of statistical tools (SAS, R, Excel)

•Volume, non-interest income/expense modeling

Pre-Provision Net Revenue Modeling

(PPNR)

•Most often performed with ALM model

•Can incorporate inputs from multiple models (Fed scenarios, credit, PPNR, other)

•Interest income/expense (NII)Balance Sheet Modeling

•Existing ALLL model (if sophisticated enough)

•Often developed in Excel

•Growing use of vendor models (CECL)

ALLL/Provision Modeling

•ALM model or commonly developed in Excel

•Brings results together from all models

•Organizes results for regulatory submission and management reporting“Aggregator” Model

Good data is critical!

Page 29

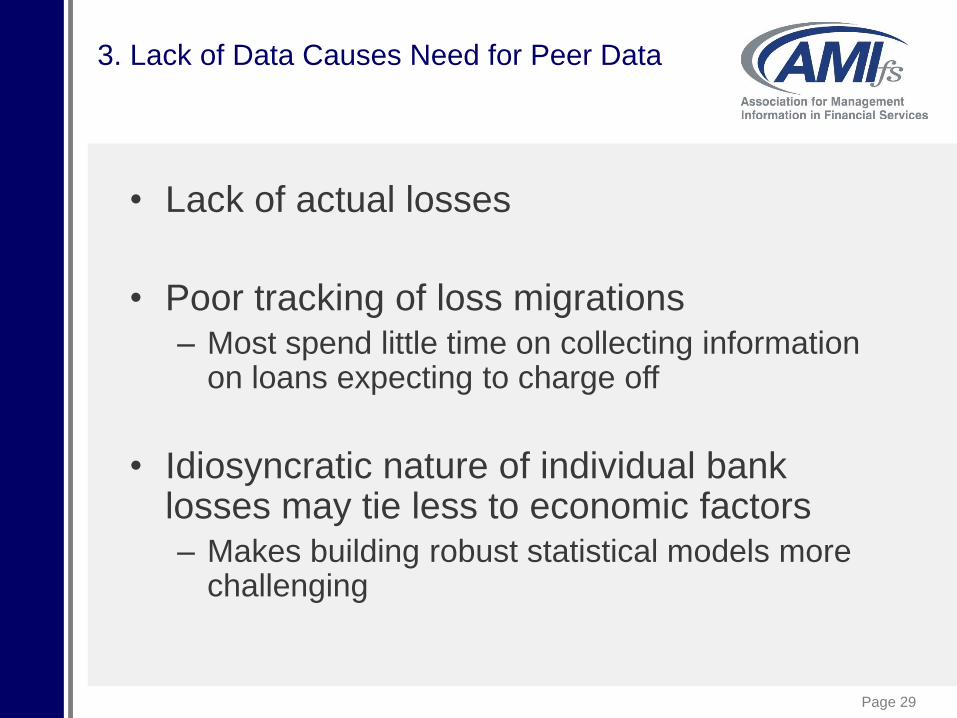

3. Lack of Data Causes Need for Peer Data

• Lack of actual losses

• Poor tracking of loss migrations – Most spend little time on collecting information

on loans expecting to charge off

• Idiosyncratic nature of individual bank losses may tie less to economic factors– Makes building robust statistical models more

challenging

Page 30

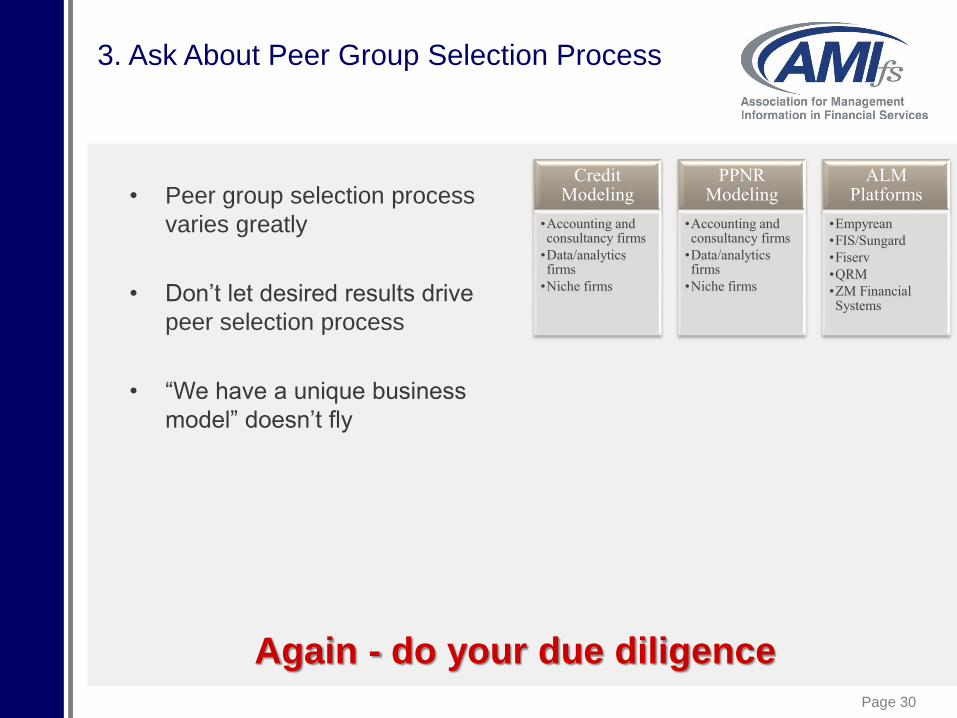

3. Ask About Peer Group Selection Process

• Peer group selection process

varies greatly

• Don’t let desired results drive

peer selection process

• “We have a unique business

model” doesn’t fly

Again - do your due diligence

Credit Modeling

•Accounting and consultancy firms

•Data/analytics firms

•Niche firms

PPNR Modeling

•Accounting and consultancy firms

•Data/analytics firms

•Niche firms

ALM Platforms

•Empyrean

•FIS/Sungard

•Fiserv

•QRM

•ZM Financial Systems

Page 31

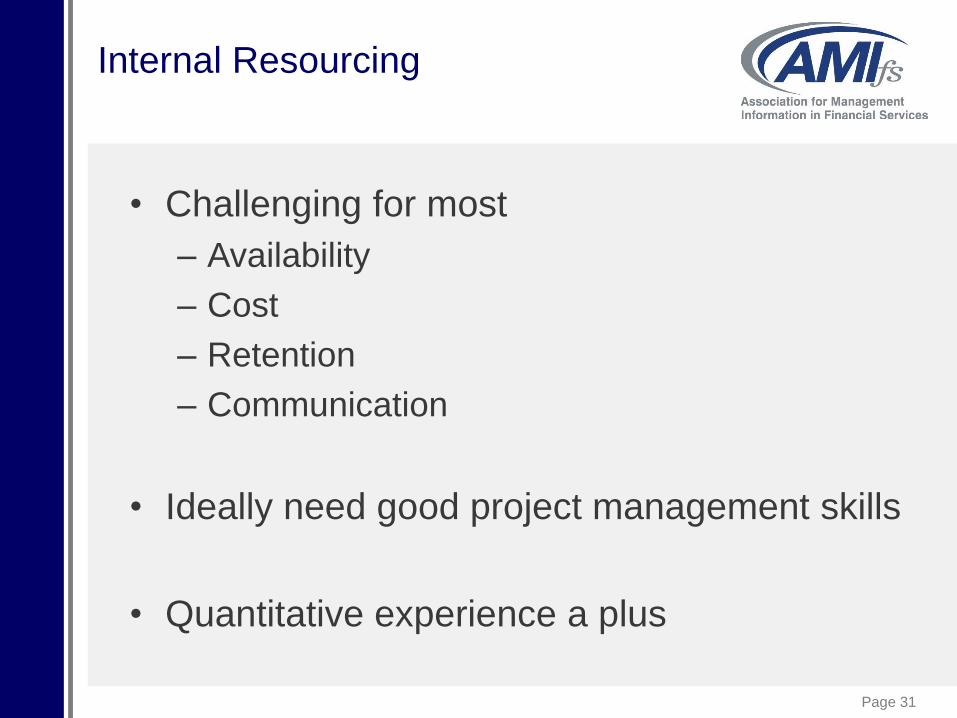

Internal Resourcing

• Challenging for most

– Availability

– Cost

– Retention

– Communication

• Ideally need good project management skills

• Quantitative experience a plus

Page 32

Common Sources

• Former consultants or advisors

• Former DFAST managers or developers

• Former examiners

• Internal staff with appropriate skills

Page 33

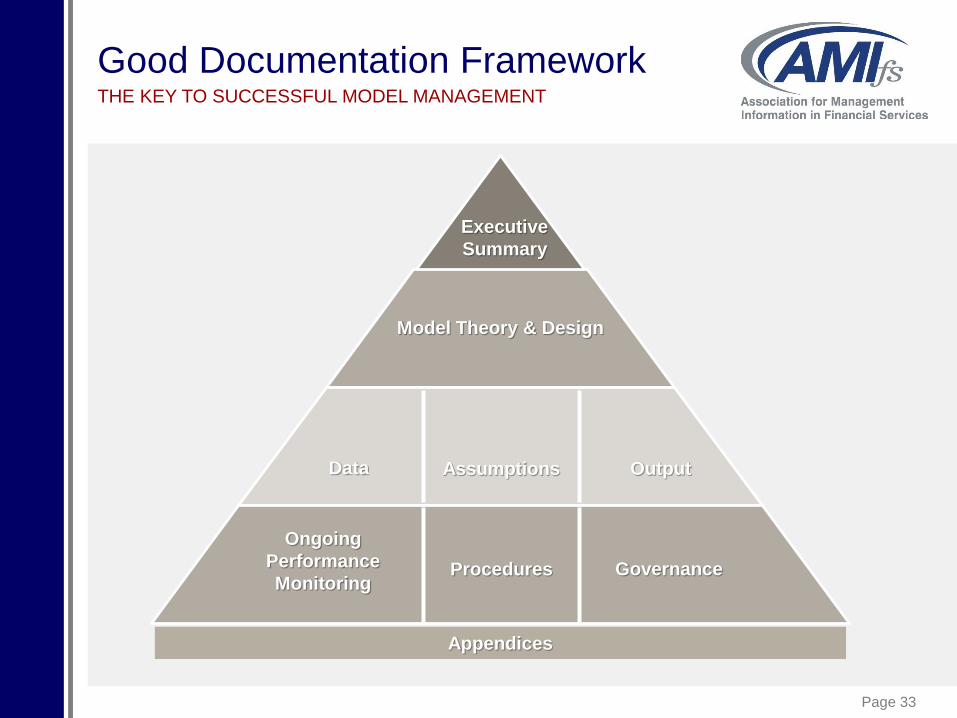

Good Documentation FrameworkTHE KEY TO SUCCESSFUL MODEL MANAGEMENT

Model Theory & Design

Data

Executive

Summary

Assumptions Output

Ongoing

Performance

MonitoringProcedures Governance

Appendices

Page 34

DataEVERY INSTITUTION’S CHALLENGE

• We have not been good data stewards

• Most organizations deficient in data quality,

reliability, and availability

• Inconsistent capture, retention, reconciliation, use

• Organizations large and small affected

Page 35

Data Solutions

• Formalized data development and management initiatives

• Centralized accountability framework

• Leadership (Chief Data Officer/Scientist)

• Operational and technological changes

• Goal: “Single Source of Truth”

Page 36

Validation

• Validation should ideally occur through the development and

implementation process

– Conceptual review

– Full end-to-end of dry run model

– Full end-to-end of submission model

• Not a once and done activity

– Model Risk Management framework will dictate scope and ongoing frequency

– DFAST model/model group most often rated high-risk and subject to annual

validation

• Timing is challenging

– Pre-submission vs. submission model

– Time for remediation

• Governance, documentation, processes and controls is as important as

the math

– Poor documentation will get an instant “needs improvement”

Page 37

A

B

C

D

Introduction

Key areas of focus, lessons learned (fact vs. fiction)

Dodd-Frank Act Stress Test (DFAST)

Regulatory context, goals, issues and challenges, major modeling decisions

Model Risk Management

MRM framework, the “three line of defense”, effective challenge

Concluding Thoughts

Getting strategic value from DFAST and MRM, Q&A

Survival PlanningPREPARING FOR $10 BILLION AND BEYOND

Page 38

MRM

Page 39

Model Risk ManagementA CRITICAL DFAST COMPANION

• Organizations preparing to cross $10B threshold also need to

develop robust MRM framework

• Not something you can implement afterwards

• Can take a few years to effectively develop

• Will continue to evolve

Page 40

MRM Framework

• Governance– MRM Policy

– Processes and controls

– Committee composition and structure

– “Three lines of defense” roles and responsibilities

• Model inventory management

• Model risk rating methodology

• Model documentation standards

• Model validation standards– Documentation

– Sourcing

– Review frequency

– Issue tracking

– Annual touch

• Model lifecycle management

Page 41

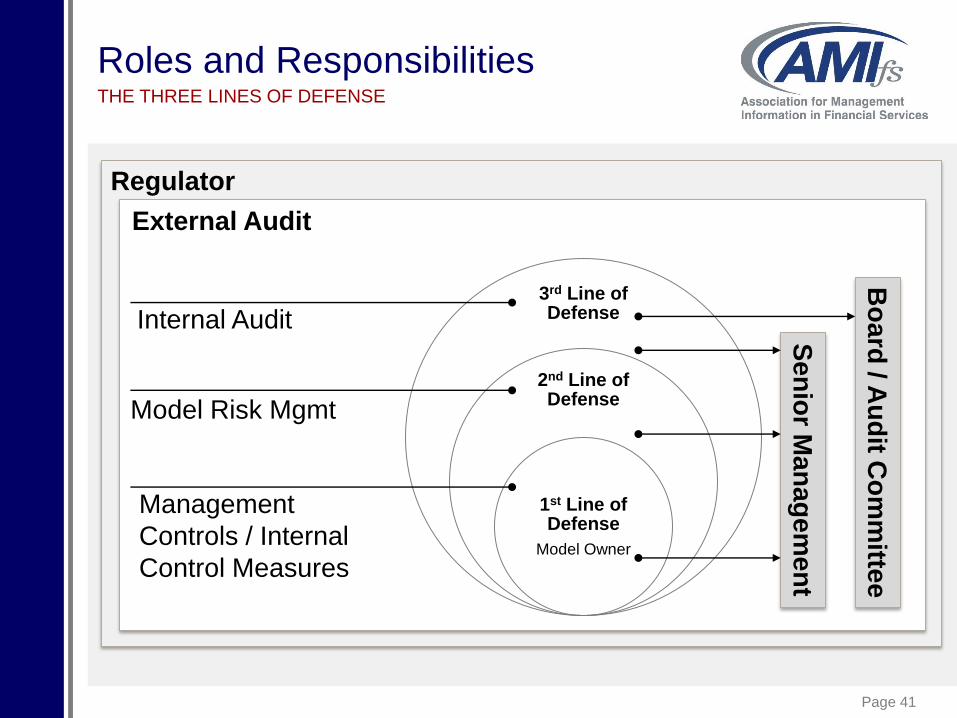

Roles and ResponsibilitiesTHE THREE LINES OF DEFENSE

3rd Line of Defense

2nd Line of Defense

1st Line of Defense

Model Owner

Management

Controls / Internal

Control Measures

Internal Audit

Model Risk Mgmt

Se

nio

r Ma

na

ge

me

nt

Bo

ard

/ Au

dit C

om

mitte

e

External Audit

Regulator

Page 42

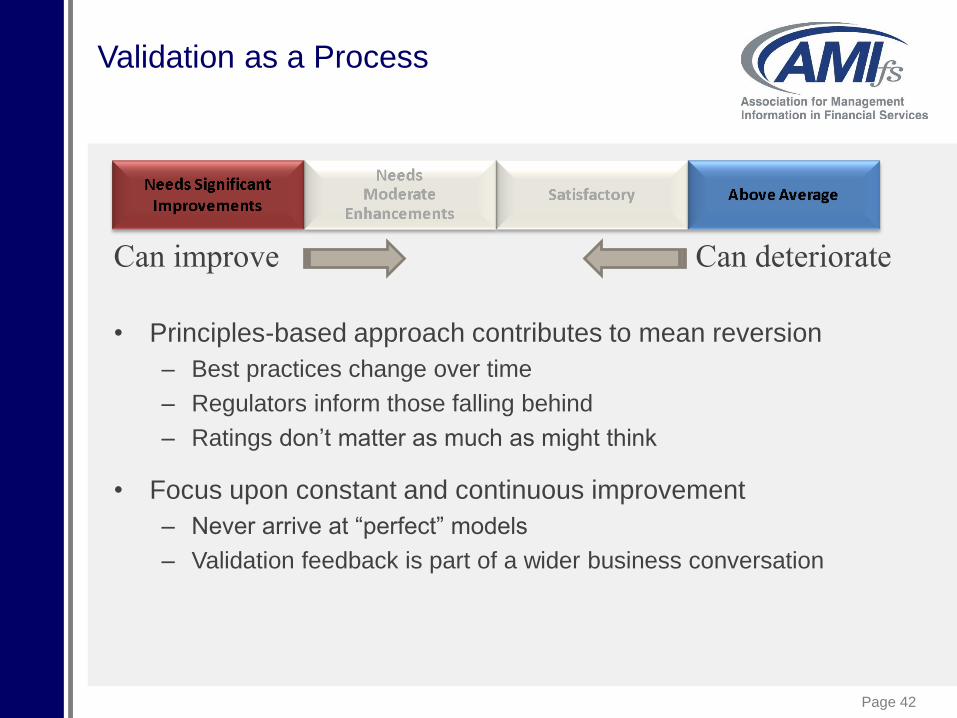

Validation as a Process

• Principles-based approach contributes to mean reversion

– Best practices change over time

– Regulators inform those falling behind

– Ratings don’t matter as much as might think

• Focus upon constant and continuous improvement

– Never arrive at “perfect” models

– Validation feedback is part of a wider business conversation

Can improve Can deteriorate

Page 43

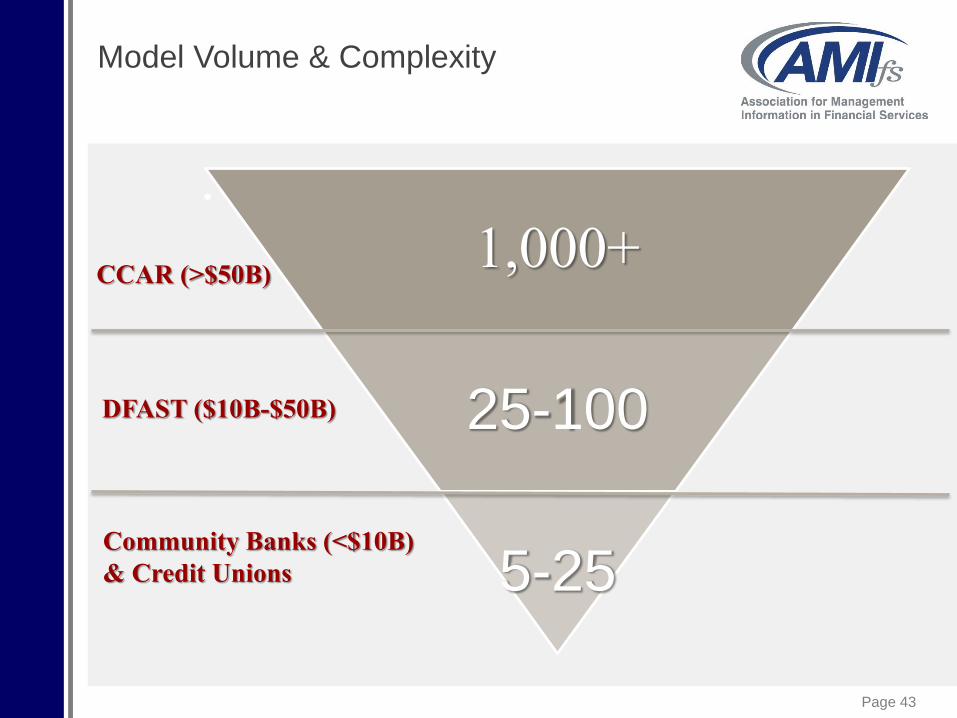

Model Volume & Complexity

• Number of “Models" by Institution Size

1,000+

25-100

5-25

CCAR (>$50B)

DFAST ($10B-$50B)

Community Banks (<$10B)

& Credit Unions

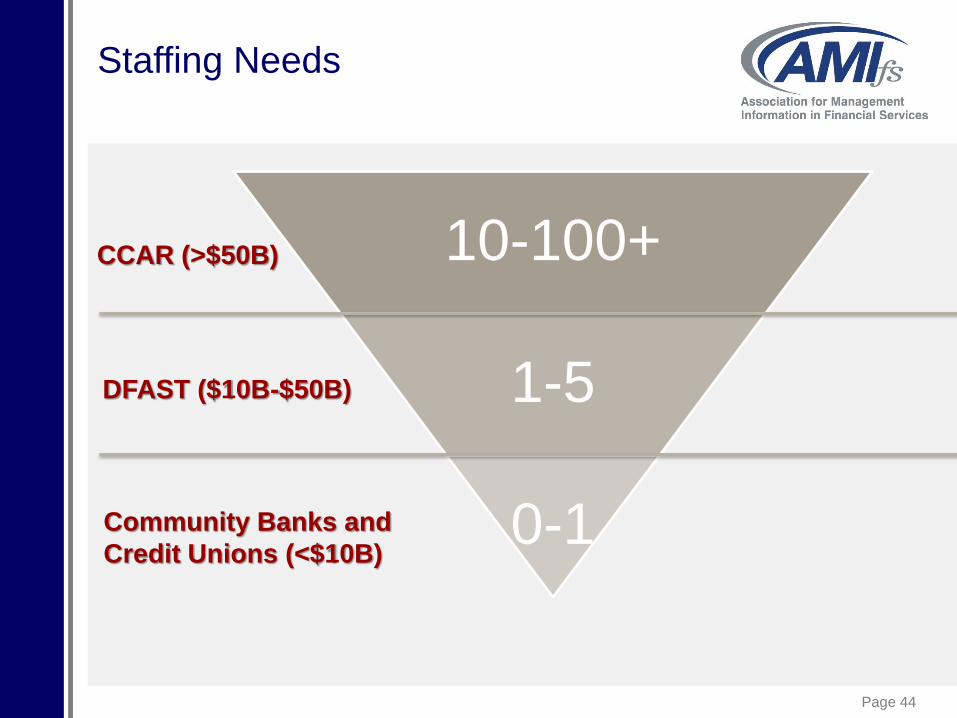

Page 44

10-100+

1-5

0-1

CCAR (>$50B)

DFAST ($10B-$50B)

Community Banks and

Credit Unions (<$10B)

Staffing Needs

Page 45

Effective Challenge

GUIDANCE ON MODEL RISK MANAGEMENT (OCC 2011-12/ FED SR 11-7)

Effective Challenge:

“critical analysis by objective, informed parties that can identify model limitations and produce appropriate changes. Effective challenge depends on a combination of incentives, competence, and influence.”

• Incentives to provide effective challenge to models are stronger when: – Greater separation of that challenge from the model development process

– Well-designed compensation practices

– Corporate culture

• Competence is a key to effectiveness since technical knowledge and modeling skills are necessary to conduct appropriate analysis and critique

• Challenge may fail to be effective without the influence to ensure that actions are taken to address model issues

– Explicit authority

– Stature within the organization

– Commitment and support from higher levels of management

Page 46

A

B

C

D

Introduction

Key areas of focus, lessons learned (fact vs. fiction)

Dodd-Frank Act Stress Test (DFAST)

Regulatory context, goals, issues and challenges, major modeling decisions

Model Risk Management

MRM framework, the “three line of defense”, effective challenge

Concluding Thoughts

Getting strategic value from DFAST and MRM, Q&A

Survival PlanningPREPARING FOR $10 BILLION AND BEYOND

Page 47

Recipe for Success

• Education/communication

• Short- and long-term planning

• Reach beyond compliance – envision

strategic value

• Address data as early as you can

• Choose your partners wisely

Page 48

Due Diligence TipsPARTNER/VENDOR SELECTION

• Seek specialized experience – DFAST – each aspect of modeling

– MRM – right-sized model management process

– CFPB

• Horizontal perspective with DFAST – DFAST experience over CCAR

• Seek A-teams– Solid due diligence on the specific resources (not just the firm)

Page 49

Getting Strategic ValueHOW INSTITUTIONS ARE USING STRATEGICALLY

• Merger and acquisition modeling

• Business line growth/diversification evaluation

• More holistic capital planning / stress testing

– Integrated risk assessments (credit, IRR, liquidity, ops,

capital/earnings)

• Expanded vulnerability risk assessments

• Better informed risk monitoring

• Risk Appetite Statements

Page 50

Questions?

Page 51

Preparing for $10 Billion and Beyond

Thank

You!