Embed Size (px)

Citation preview

The Path to the Crisis of 2008:Beware of Future Expectations

Jean-Paul RodrigueDepartment of Global Studies & Geography, Hofstra University

Theo NotteboomITMMA - University of Antwerp and Antwerp Maritime Academy

Terminal Operators Conference - EuropeValencia (Spain), June 8-10 2010

The Crisis is Over: Long Live the Crisis

• Many unfounded assumptions behind the recovery:- Randomness and uniqueness.- The cause (debt) is the solution (more debt)- The soundness of economic theory (Keynesianism).- “Appropriate” response from central banks and

governments.- No unintended consequences of moral hazard.

• Recession:- Clear the stupidity out of the system.- We have been very stupid (depression?).

Hoocoodanode?

The First Crisis of Globalization: Reaping the Consequences of Misallocations

CAUSESMonetary system

(fractional reserve banking, fiat currencies)

SYMPTOMSDebt, asset inflation

Production

Consumption

Distribution

CONSEQUENCESMisallocations

(bubbles)

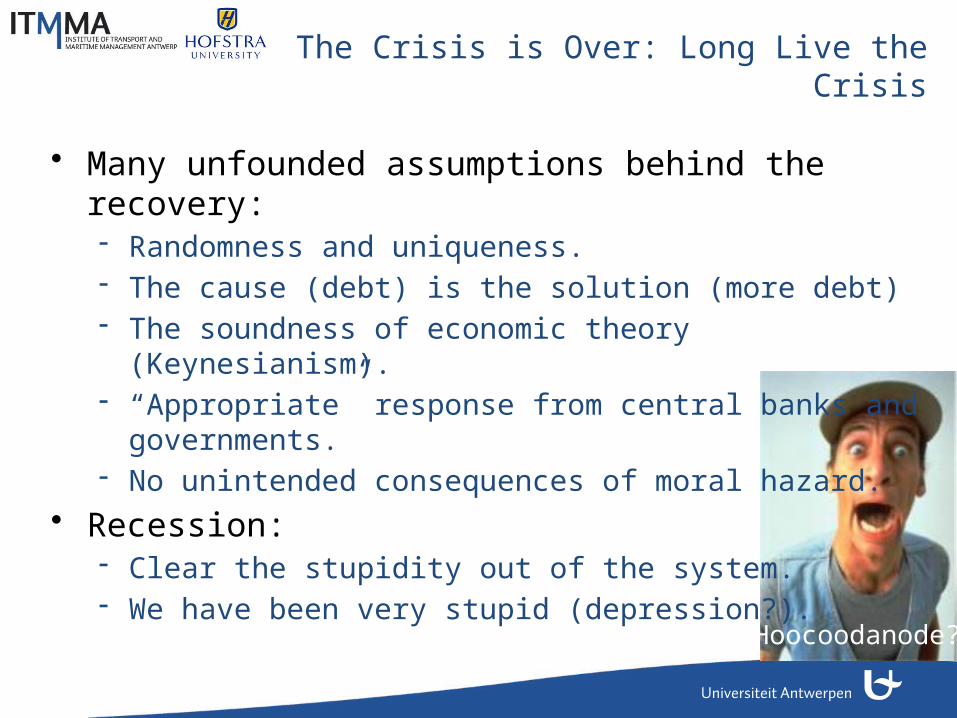

Business Cycles: The Trend that Time Forgot

Expansion Recession

Peak

Trough

Expansion

Credit-Driven Boom

Credit-Driven Bust

Depression

Demand Transfer of future demand into the present.

Supply Misallocations because of distorted expectations about the future.Asset price distortions.

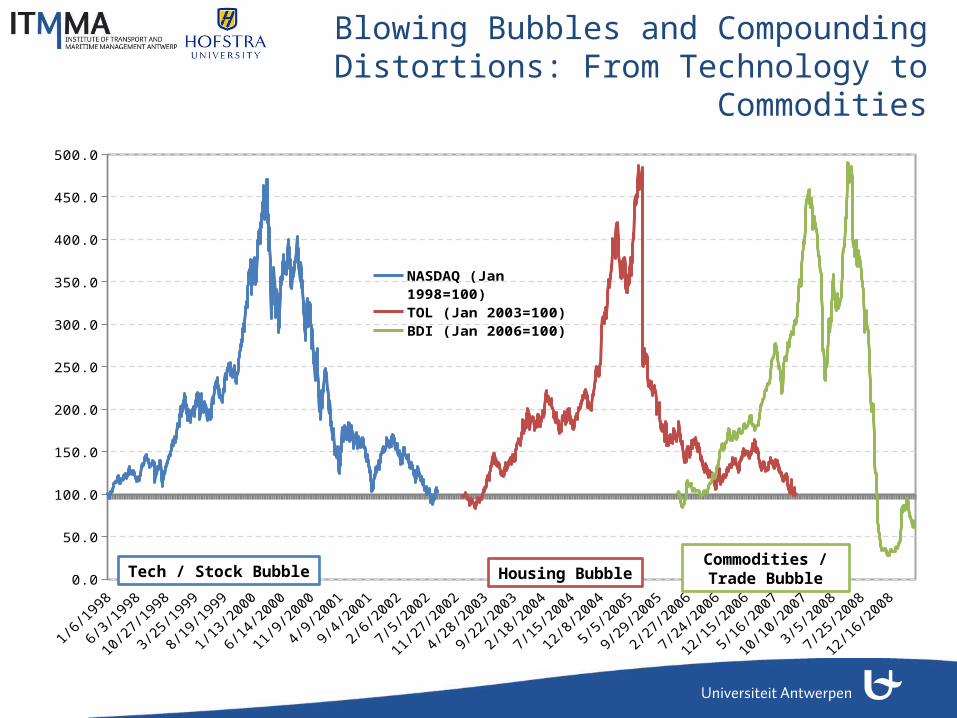

Blowing Bubbles and Compounding Distortions: From Technology to

Commodities

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

NASDAQ (Jan 1998=100)

TOL (Jan 2003=100)

BDI (Jan 2006=100)

Tech / Stock Bubble Housing BubbleCommodities / Trade Bubble

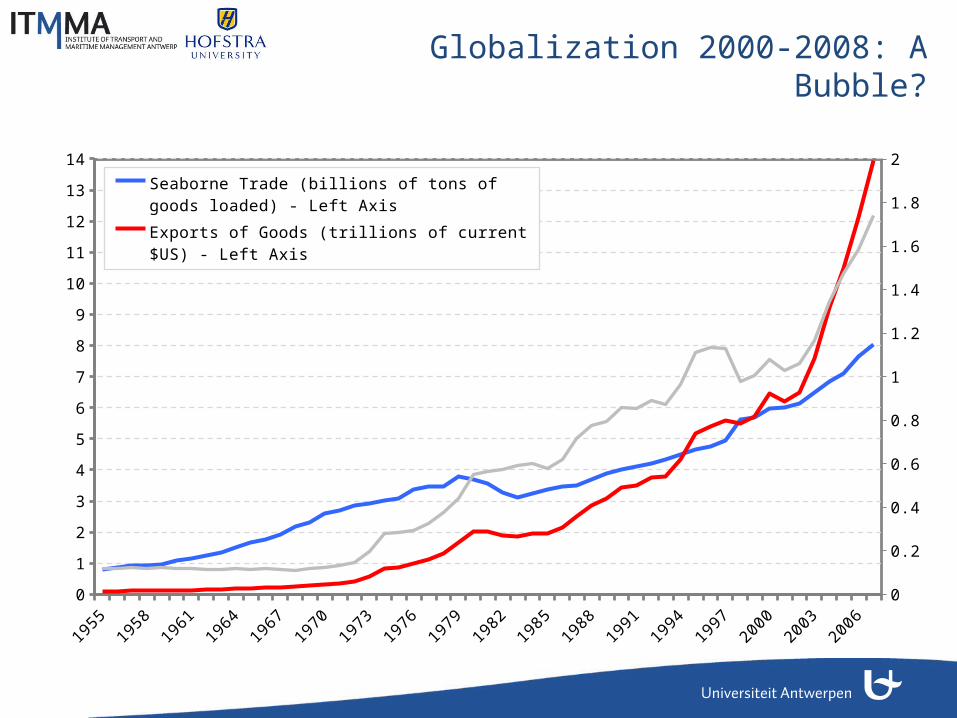

Globalization 2000-2008: A Bubble?

1955

1957

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Seaborne Trade (billions of tons of goods loaded) - Left Axis

Exports of Goods (trillions of current $US) - Left Axis

Ratio Exports / Seaborne Trade - Right Axis

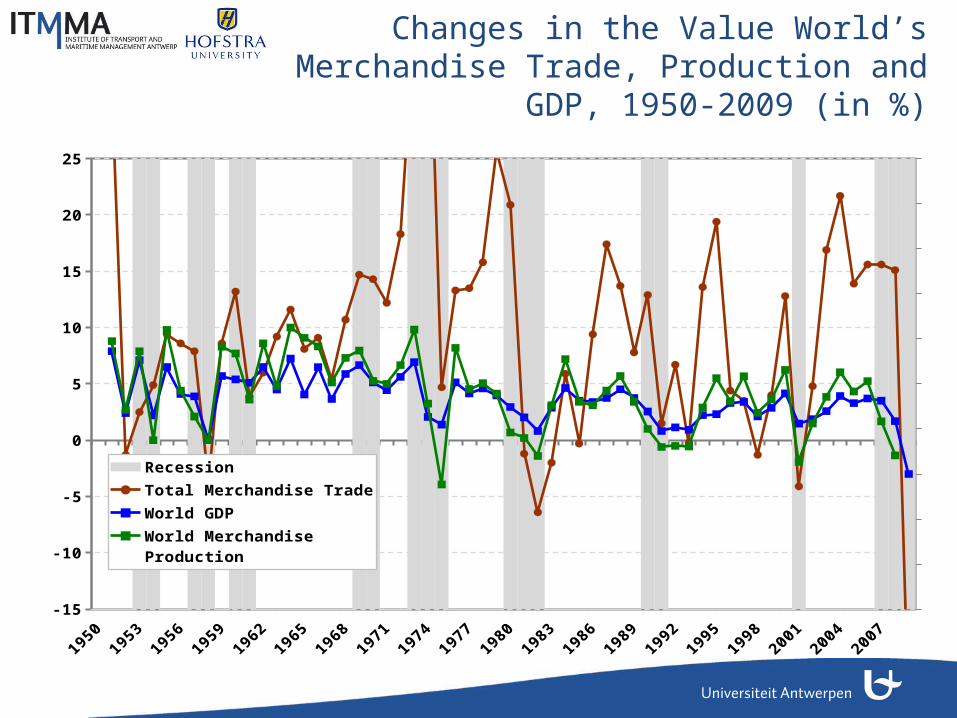

Changes in the Value World’s Merchandise Trade, Production and GDP,

1950-2009 (in %)

-15

-10

-5

0

5

10

15

20

25

Recession

Total Merchandise Trade

World GDP

World Merchandise Production

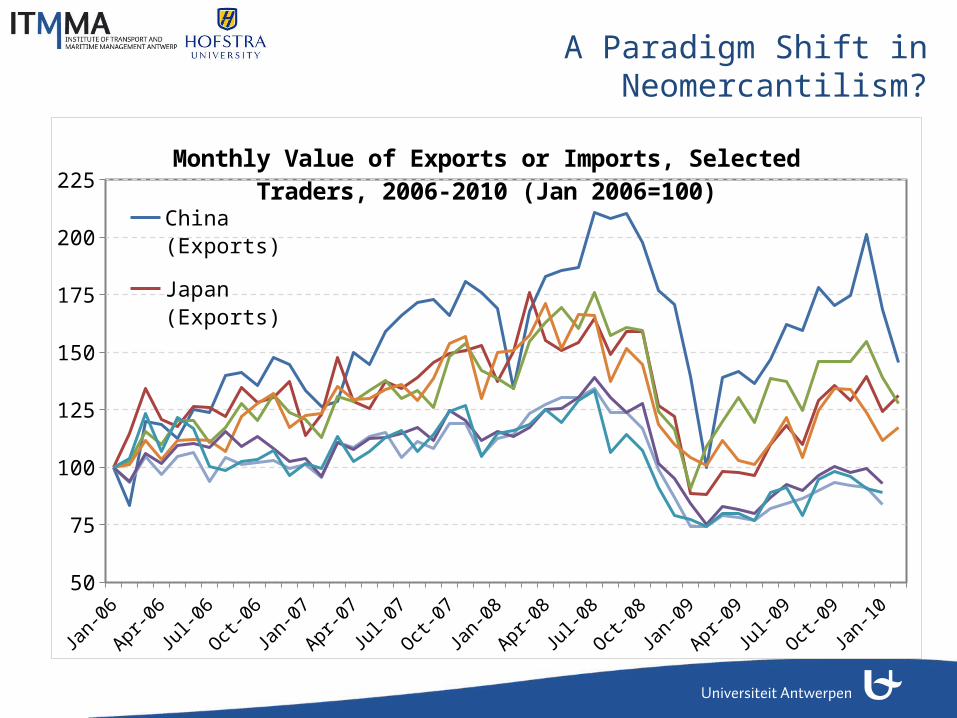

A Paradigm Shift in Neomercantilism?

Jan-0

6

Mar-06

May-06

Jul-0

6

Sep-06

Nov-06Ja

n-07

Mar-07

May-07

Jul-0

7

Sep-07

Nov-07Ja

n-08

Mar-08

May-08

Jul-0

8

Sep-08

Nov-08Ja

n-09

Mar-09

May-09

Jul-0

9

Sep-09

Nov-09Ja

n-10

50

75

100

125

150

175

200

225Monthly Value of Exports or Imports, Selected Traders, 2006-2010 (Jan

2006=100)China (Exports)Japan (Exports)Korea (Exports)Germany (Exports)Canada (Exports)USA (Imports)UK (Imports)

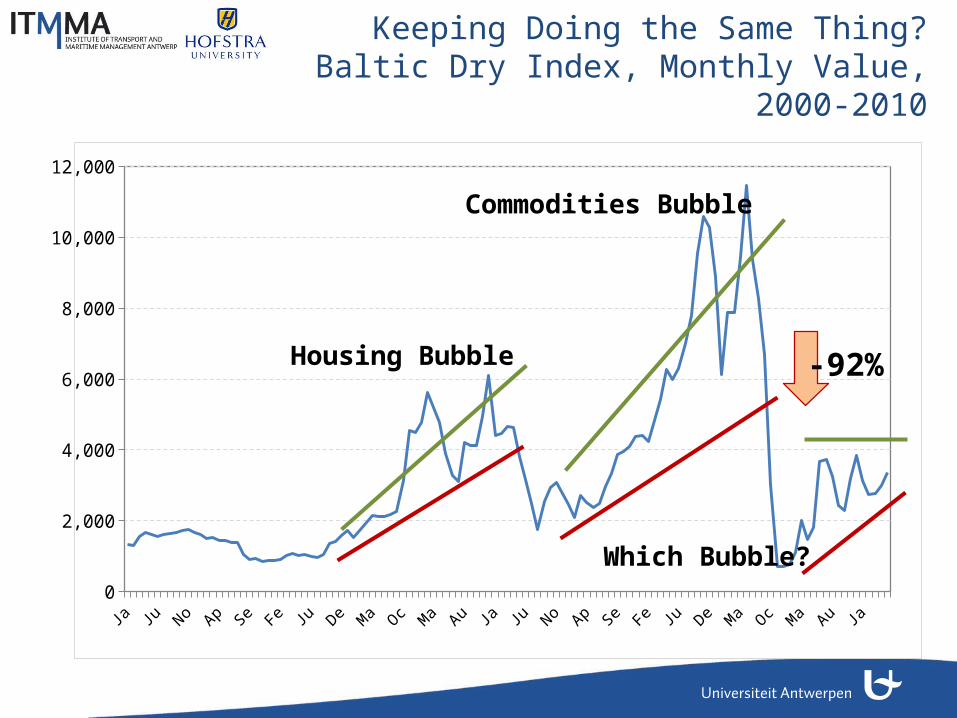

Keeping Doing the Same Thing? Baltic Dry Index, Monthly Value, 2000-2010

0

2,000

4,000

6,000

8,000

10,000

12,000

-92%Housing Bubble

Commodities Bubble

Which Bubble?

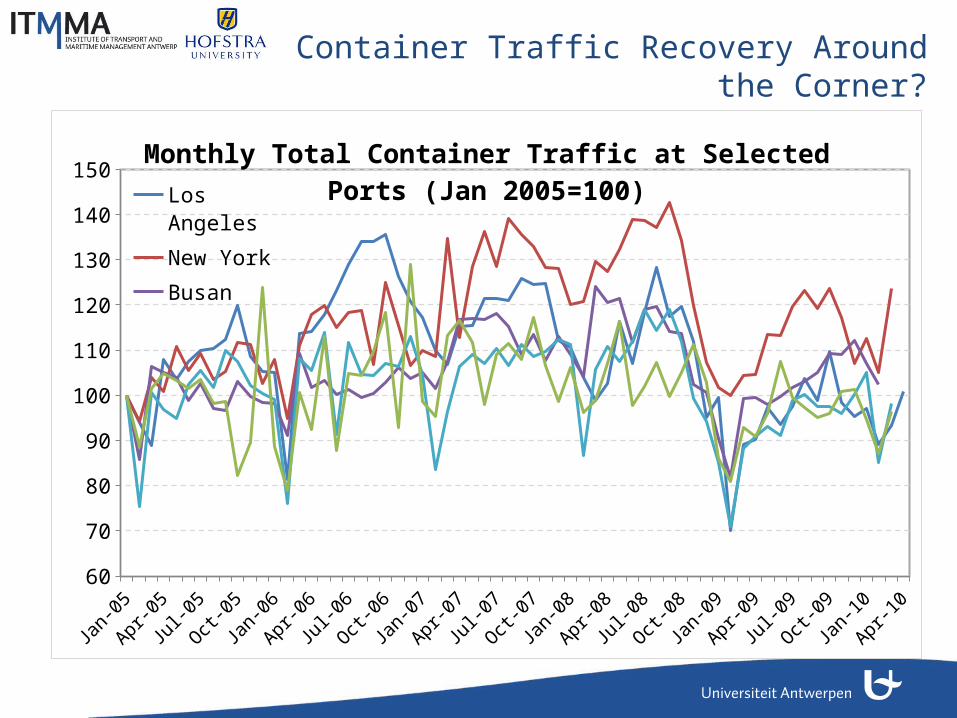

Container Traffic Recovery Around the Corner?

Jan-0

5Apr-

05Ju

l-05

Oct-05

Jan-0

6Apr-

06Ju

l-06

Oct-06

Jan-0

7Apr-

07Ju

l-07

Oct-07

Jan-0

8Apr-

08Ju

l-08

Oct-08

Jan-0

9Apr-

09Ju

l-09

Oct-09

Jan-1

0Apr-

1060

70

80

90

100

110

120

130

140

150Monthly Total Container Traffic at Selected Ports (Jan 2005=100)

Los AngelesNew YorkBusanHong KongAlgeciras

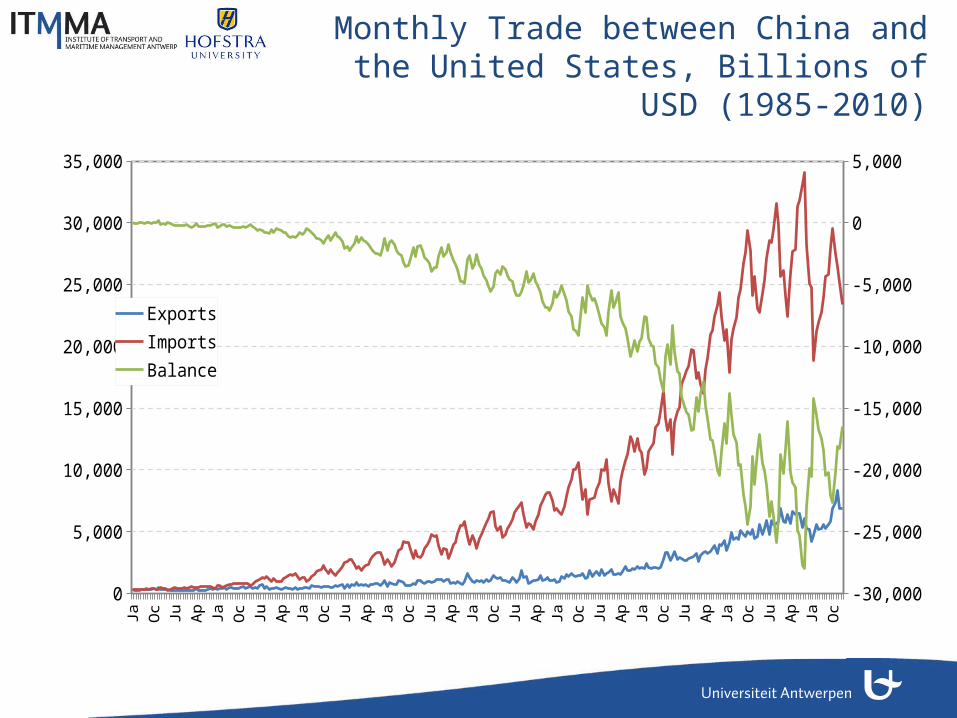

Monthly Trade between China and the United States, Billions of USD (1985-

2010)Ja

n-85

Jan-

86

Jan-

87

Jan-

88

Jan-

89

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

-30,000

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

ExportsImportsBalance

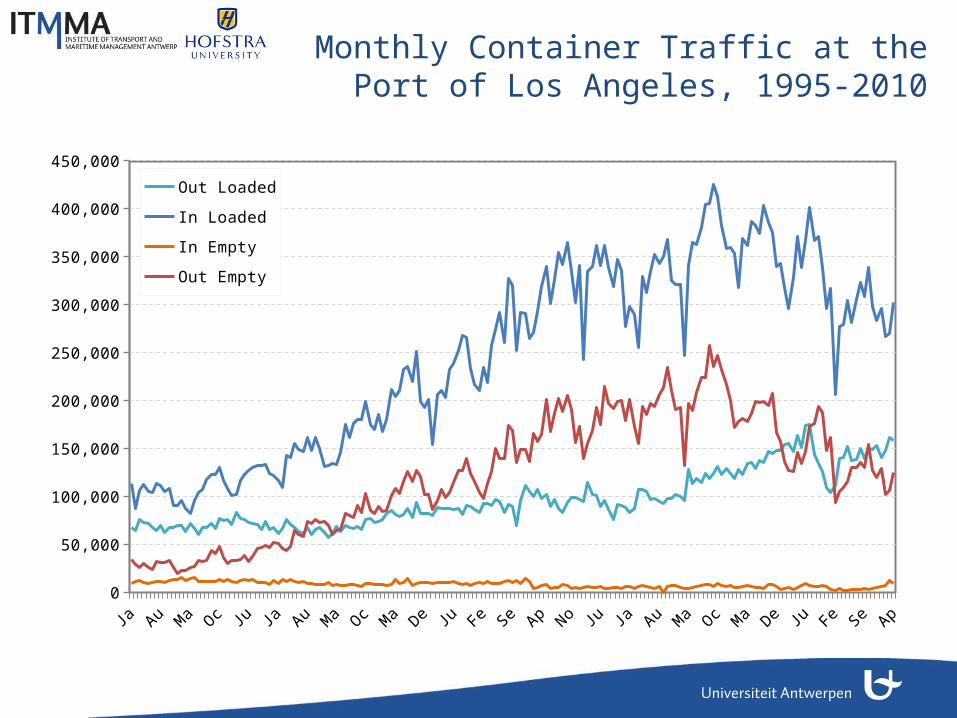

Monthly Container Traffic at the Port of Los Angeles, 1995-2010

Jan-9

5Ju

l-95Ja

n-96Ju

l-96Ja

n-97Ju

l-97Ja

n-98Ju

l-98Ja

n-99Ju

l-99Ja

n-00Ju

l-00Ja

n-01Ju

l-01Ja

n-02Ju

l-02Ja

n-03Ju

l-03Ja

n-04Ju

l-04Ja

n-05Ju

l-05Ja

n-06Ju

l-06Ja

n-07Ju

l-07Ja

n-08Ju

l-08Ja

n-09Ju

l-09Ja

n-10

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Out Loaded

In Loaded

In Empty

Out Empty

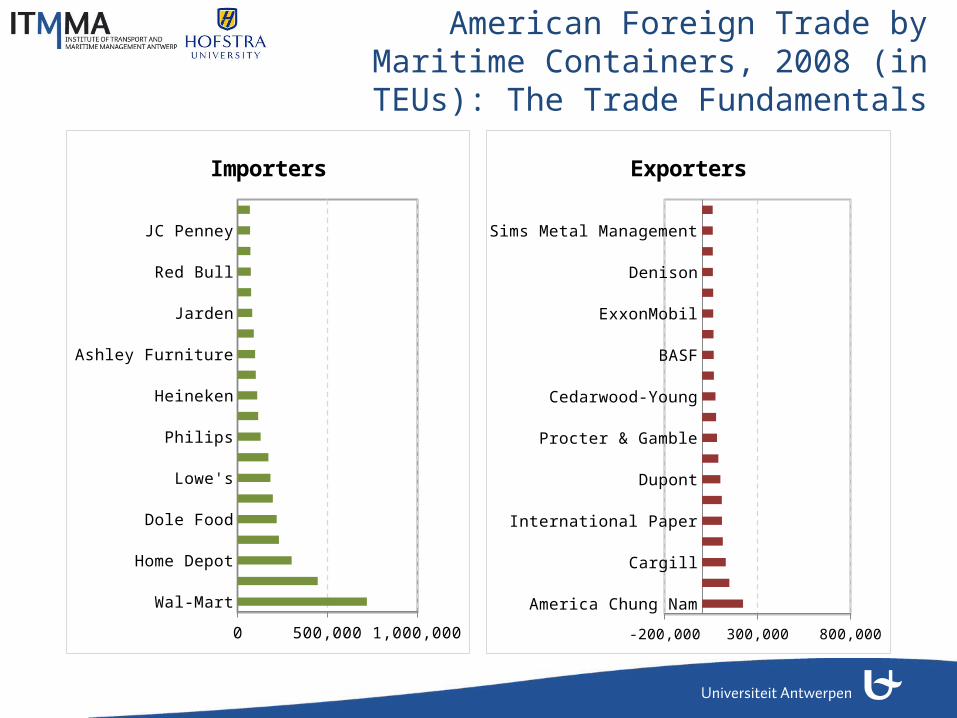

Wal-MartTarget

Home DepotSears Holding

Dole FoodCostco Wholsale

Lowe'sLG Group

PhilipsChiquita

HeinekenIkea

Ashley FurnitureGeneral Electric

JardenSamsungRed Bull

NikeJC Penney

Whirlpool

0 200,000 400,000 600,000 800,000

Importers

America Chung NamWeyerhaeuser

CargillKoch Industries

International PaperDow Chemical

DupontPotential Industries

Procter & GambleMeadwestvaco

Cedarwood-YoungArcher Daniels Midland

BASFDelong

ExxonMobilJC Horizon

DenisonCGB Enterprises

Sims Metal ManagementNewport Chinternational

0 200,000 400,000 600,000 800,000

Exporters

American Foreign Trade by Maritime Containers, 2008 (in TEUs): The Trade

Fundamentals

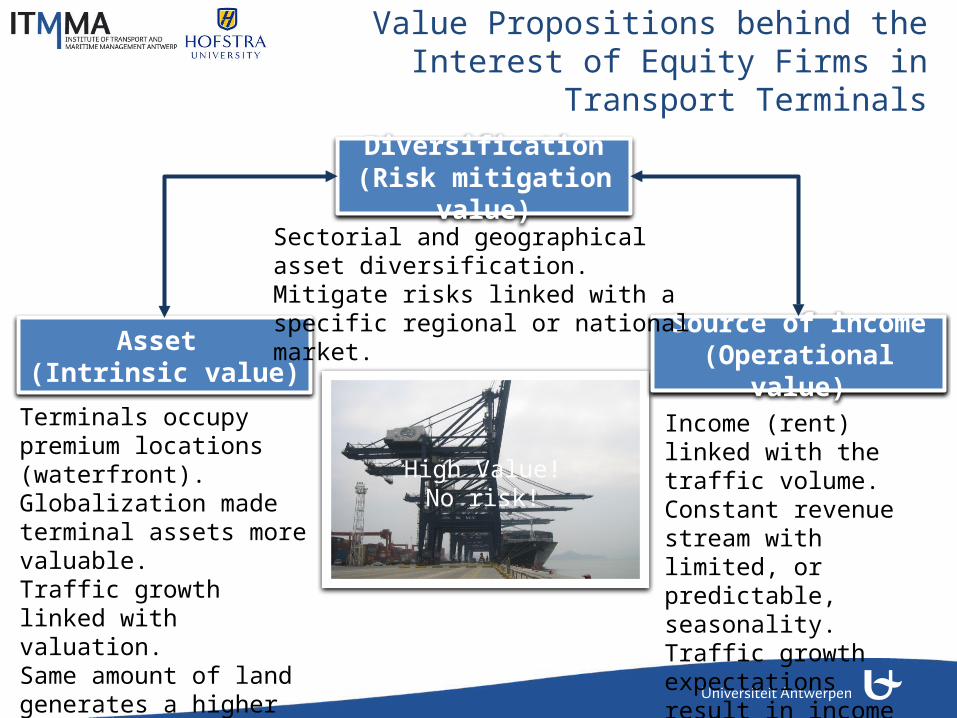

Value Propositions behind the Interest of Equity Firms in Transport Terminals

Diversification(Risk mitigation value)

Source of income(Operational value)

Asset (Intrinsic value)

Terminals occupy premium locations (waterfront).Globalization made terminal assets more valuable.Traffic growth linked with valuation.Same amount of land generates a higher income.Terminals as fairly liquid assets.

Income (rent) linked with the traffic volume.Constant revenue stream with limited, or predictable, seasonality.Traffic growth expectations result in income growth expectations.

Sectorial and geographical asset diversification.Mitigate risks linked with a specific regional or national market.

High Value!No risk!

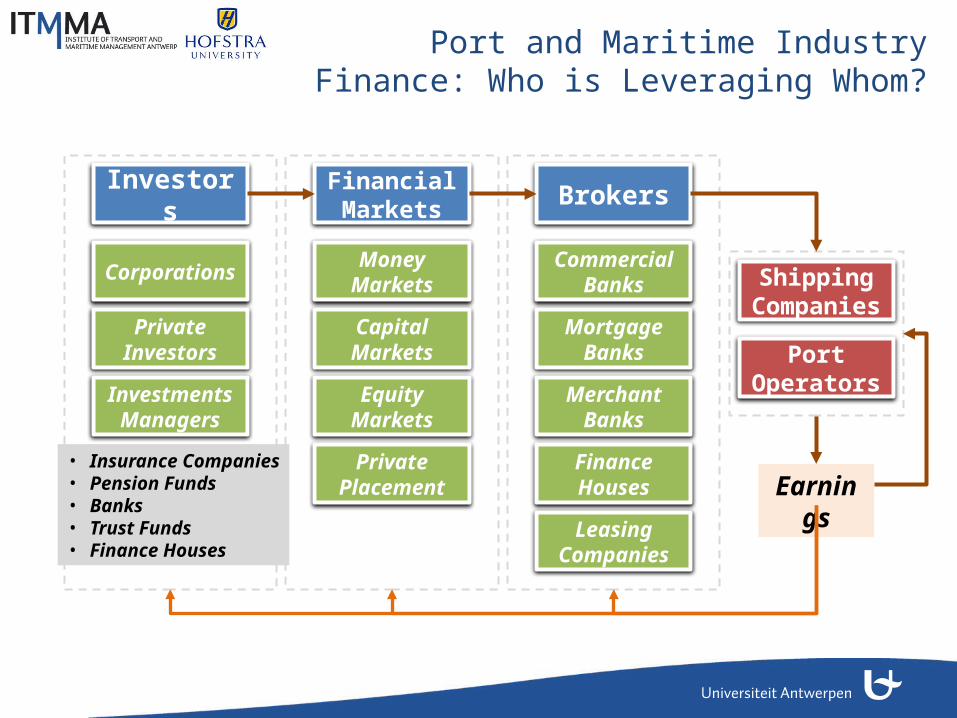

Port and Maritime Industry Finance: Who is Leveraging Whom?

BrokersFinancial MarketsInvestors

Commercial Banks

Mortgage Banks

Merchant Banks

Finance Houses

Leasing Companies

Money Markets

Capital Markets

Equity Markets

Private Placement

Corporations

Private Investors

Investments Managers

• Insurance Companies• Pension Funds• Banks• Trust Funds• Finance Houses

Shipping Companies

Port Operators

Earnings

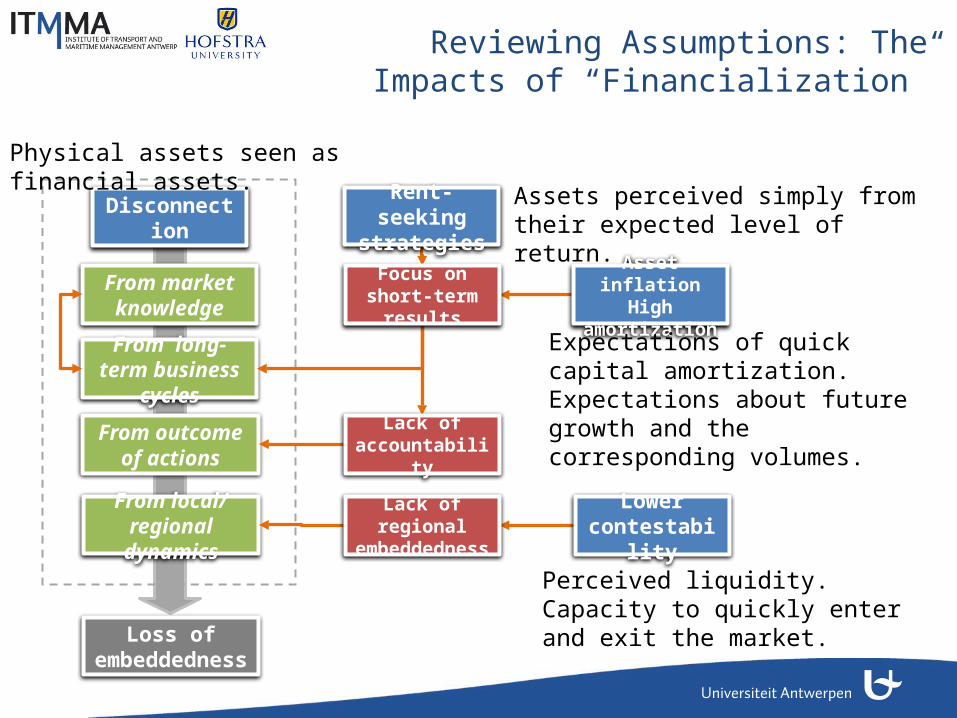

Reviewing Assumptions: The Impacts of “Financialization”

Disconnection

From market knowledge

From long-term business cycles

From local/ regional dynamics

From outcome of actions

Loss of embeddedness

Lower contestability

Rent-seeking strategies

Lack of accountability

Lack of regional embeddedness

Focus on short-term results

Asset inflationHigh amortization

Assets perceived simply from their expected level of return.

Expectations of quick capital amortization.Expectations about future growth and the corresponding volumes.

Perceived liquidity.Capacity to quickly enter and exit the market.

Physical assets seen as financial assets.

Dumb Money at Work?

Date Transaction Price compared to EBITD2005 DP World takes over CSX World Terminals 14 timesEarly 2006 PSA acquires a 20% stake in HPH 17 timesMid 2006 DP World acquires P&O Ports 19 timesMid 2006 Goldman Sachs Consortium acquires ABP 14.5 timesEnd 2006 AIG acquires P&O Ports North America 24 times

Early 2007 Ontario Teachers’ Pension Fund acquires OOIL Terminals

23.5 times

Mid 2007 RREEF acquires Maher Terminals 25 times

EBITDA = Earnings Before Interest, Taxes, Depreciation and Amortization

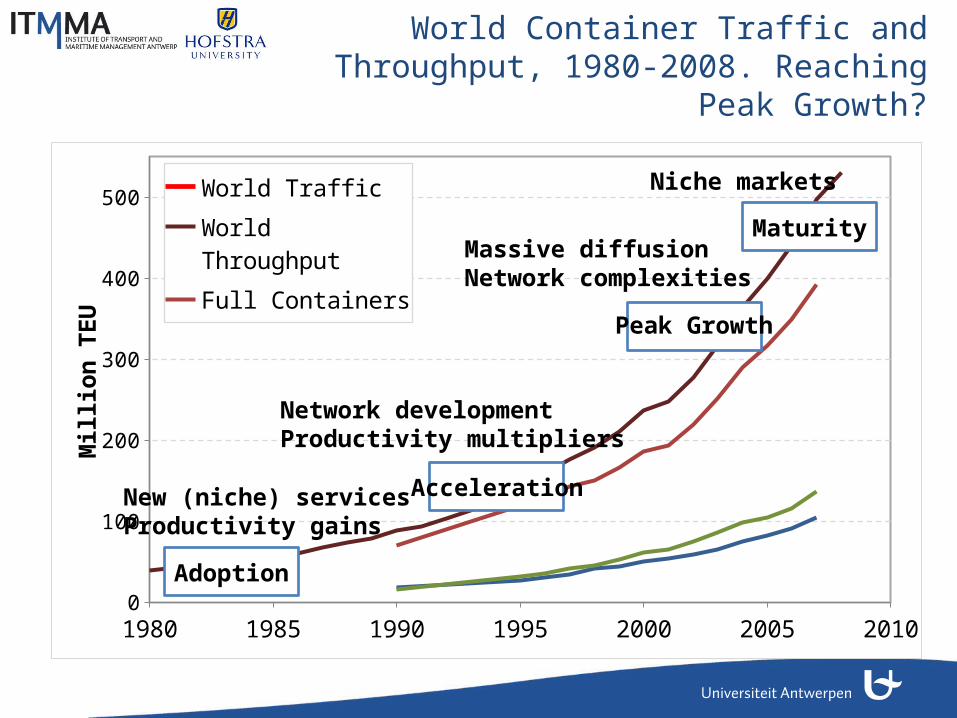

World Container Traffic and Throughput, 1980-2008. Reaching Peak Growth?

1980 1985 1990 1995 2000 2005 20100

100

200

300

400

500World TrafficWorld ThroughputFull ContainersTransshipmentEmpty Containers

Mill

ion

TEU

Adoption

Acceleration

Peak Growth

Maturity

New (niche) servicesProductivity gains

Network developmentProductivity multipliers

Massive diffusionNetwork complexities

Niche markets

Fallacies of Forecasting: 2020 Throughput Forecast, Selected Large

Ports, Linear and CAG ScenarioPort / Traffic 2007, M TEU

R2 / CAG (1998-2007) Traffic 2020 (Linear Scenario) / CAG

Traffic 2020 (CAG 1998-2007 Scenario)

New York / 5.3 0.996 / +7.9% 9.6 M TEU / +4.7% 14.2 M TEU

Savannah / 2.6 0.968 / +13.5% 4.9 M TEU / +5.1% 13.6 M TEU

Los Angeles / 8.3 0.966 / +9.5% 16.6 M TEU / +5.4% 27.1 M TEU

Antwerp / 8.2 0.974 / +9.6% 14.5 M TEU / +4.5% 26.9 M TEU

Algeciras / 3.4 0.961 / +6.5% 6.0 M TEU / +4.4% 7.7 M TEU

Busan /13.3 0.983 / +8.4% 24.3 M TEU / +4.8% 38.1 M TEU

Shanghai / 26.1 0.948 / +23.9% 56.5 M TEU / +6.1% 423.8 M TEU

From under estimating to over estimating trendsLinearity prevalent in growth trends (1998-2007)Compound annual growth common in forecastsNon-contestability assumption

Advanced forecasting(c. 2007)

If you build it they will come…

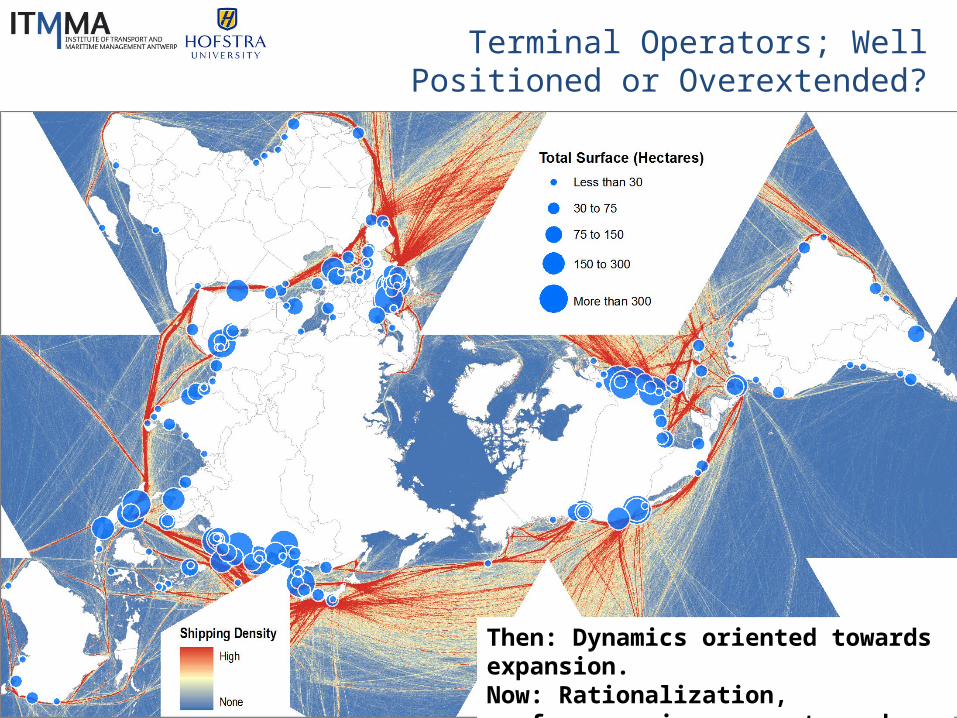

Terminal Operators; Well Positioned or Overextended?

Then: Dynamics oriented towards expansion.Now: Rationalization, performance improvements and the search for niche markets.

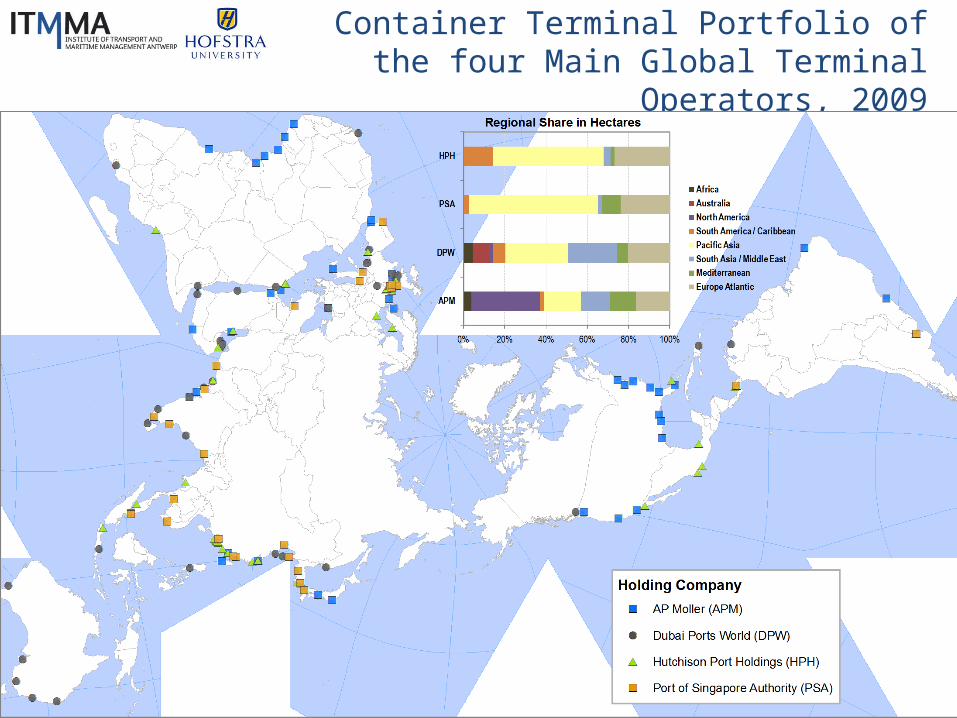

Container Terminal Portfolio of the four Main Global Terminal Operators, 2009

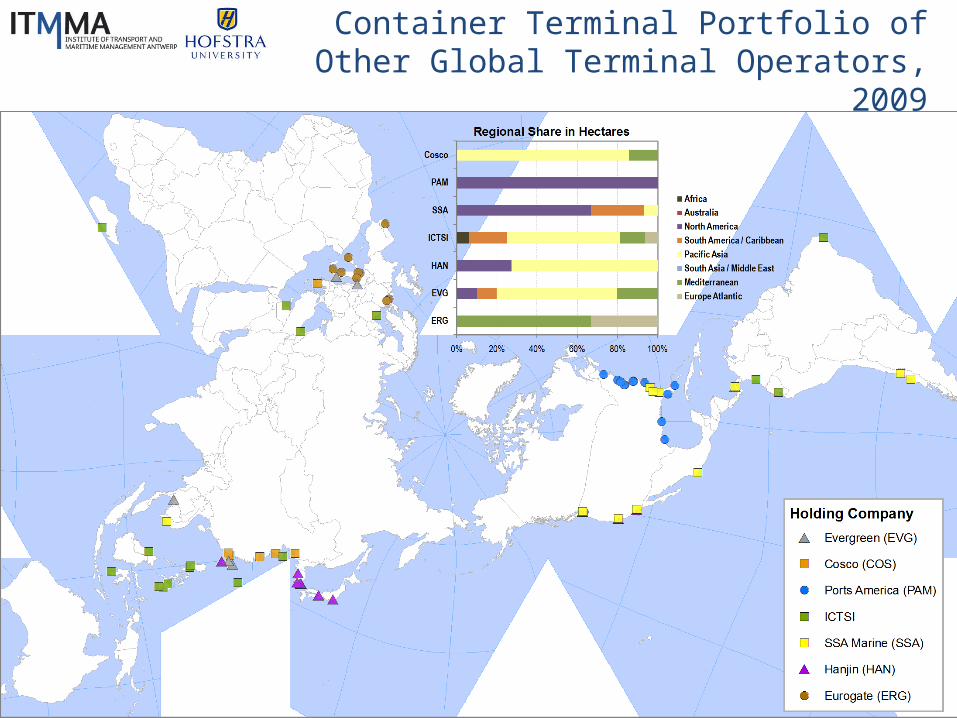

Container Terminal Portfolio of Other Global Terminal Operators, 2009

Conclusion: Beware of Future Expectations

• Intense phase of capital accumulation in the shipping and port sectors.

• Some of the growth expectations based on unsubstantiated assumptions.

• “Financialization” transformed the industry and expanded misallocations.

• What could be some specific consequences on the maritime industry?

It’s the debt stupid…