Embed Size (px)

Citation preview

The outlook for UK mailvolumes to 2023

PwC Strategy & Economics

15 July 2013

PwC

Important notice

This document has been prepared by PricewaterhouseCoopers LLP (“PwC” or “we”) for Royal Mail Group and solely for thepurpose and on the terms agreed with Royal Mail Group. We accept no liability (including for negligence) to anyone else inconnection with this document.

This document has been made publicly available for the purposes of general guidance on matters of interest only, and does notconstitute professional advice. You should not act upon the information contained in this document without obtaining specificprofessional advice.

Information in this document is obtained or derived from a variety of sources. PwC has not sought to establish the reliability ofthose sources or verify all of the information so provided. No representation or warranty of any kind (whether express or implied)is given by PwC to any person (except to Royal Mail Group under the relevant terms of the Engagement) as to the accuracy orcompleteness of the report, and, to the extent permitted by law, PwC, its members, employees and agents do not accept or assumeany liability, responsibility or duty of care for any consequences of anyone else acting, or refraining to act, in reliance on theinformation contained in this document or for any decision based on it.

2Outlook for UK mail volumes to 2023

PwC

Objectives

• Royal Mail Group commissioned PwC to provide anindependent view on the long-term outlook for UK mailvolumes

• Our projections use information and analysis from a varietyof sources, including Royal Mail Group

• However, our conclusions have been reached independently.Our projections are based on our own insights and analysis,supported by an extensive programme of interviews, surveysand industry research

• We have projected mail volumes (letters and parcels) on anannual basis over the period 2013 to 2023

PwC was asked todevelop a view onthe long-termoutlook for UK mailvolumes (lettersand parcels)

Outlook for UK mail volumes to 20233

PwC

We have made a number of simplifying assumptions about thefuture market structure

Key underlying assumptions

We assume that the overall structure of the UK mail market (e.g. delivery chain and model) will not change significantlyover the projection period

We assume that additional regulatory change during the projection period will have a limited impact on the structureand operations of the mail market. We assume there will be no material change to the Universal Service Obligation

We assume price changes will be marginally higher than RPI over the projection period

We have also used a number of macroeconomic assumptions in our modelling

Source 2013 2014 2015-2023

GDP growth, % p.a. Based on PwCeconomic forecasts

1.2 2.1 2.4

Growth in number ofhouseholds, % p.a.

Based on PwC andONS projections

1.0 1.0 1.0

Source: PwC Economic forecasts, Office for National Statistics (ONS)

Outlook for UK mail volumes to 20234

2

1

3

PwC

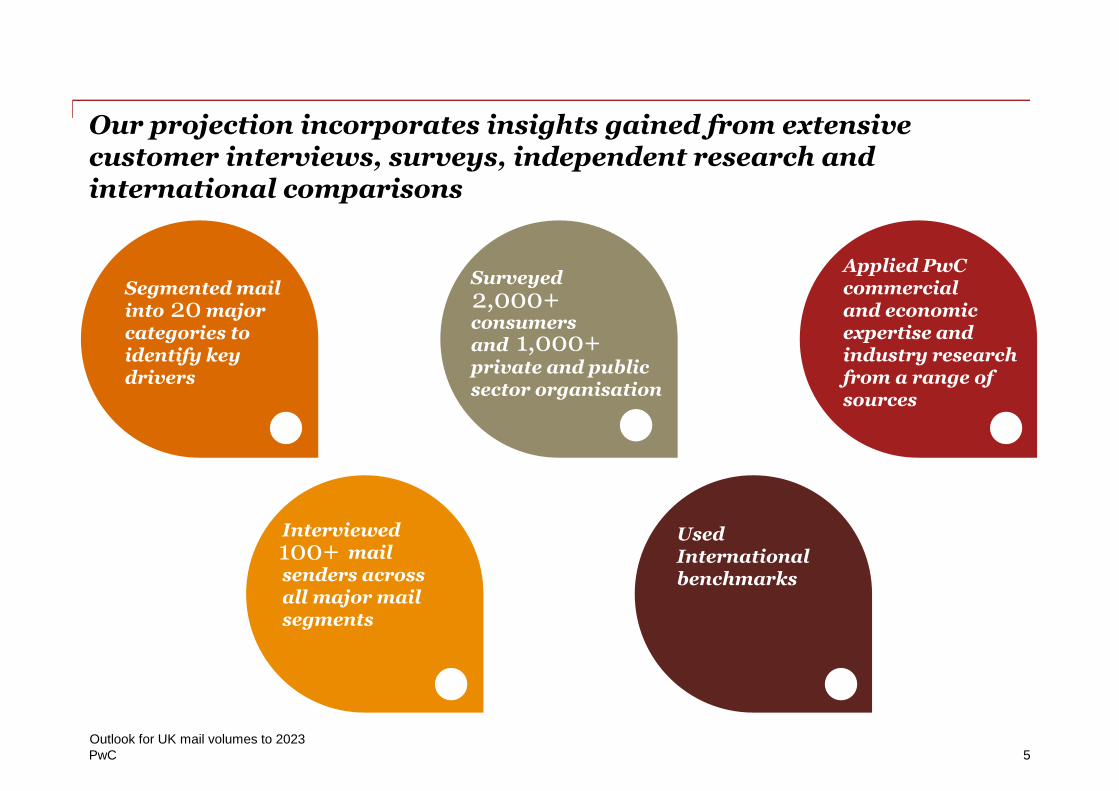

Our projection incorporates insights gained from extensivecustomer interviews, surveys, independent research andinternational comparisons

Outlook for UK mail volumes to 20235

UsedInternationalbenchmarks

Applied PwCcommercialand economicexpertise andindustry researchfrom a range ofsources

Segmented mailinto majorcategories toidentify keydrivers

Surveyed

consumersandprivate and publicsector organisation

Interviewedmail

senders acrossall major mailsegments

100+

2,000+

1,000+

20

PwC

Executive SummarySection 1

Outlook for UK mail volumes to 20236

PwC

• The mail delivered in the UK is highly varied and the total mailbag is highlyfragmented

• UK total inland letter volumes declined by 3.1% p.a. from 2005 to 2008,and by 6.3% p.a. from 2008-2013, as the economic downturn increased therate of decline

• UK parcel volumes grew by 4.3% p.a. from 2005 to 2008 and by 3.7% p.a.from 2008-2013, mainly reflecting increasing use of online shopping byconsumers

Key messages

Outlook for UK mail volumes to 20237

UK mail volumes have declined since 2004

The main driver of mail declines has been electronicsubstitution of paper communication

We expect the decline of letter volumes to continue but at aslower rate over the projection period

Our projection suggests letter volume declines of c.4% p.a.and parcel growth of c.3% p.a. from 2013 to 2023

• The principal cause of the overall mail volume decline has been thesubstitution of paper communication by electronic methods(e-substitution)

• However, the maturity of this transformation varies widely within differentsegments of the mail bag

- Some segments are already substantially online while others are justbeginning this transition

- The maximum likely level of electronic substitution also varies betweensegments depending on both recipients’ and senders’ attitudes toelectronic communication. This is affected by a range of factors such asinternet access and age (mail recipients) and mail costs (mail senders)

• We expect the rate of e-substitution in letters to slow gradually over thenext 10 years. In the initial years of e-substitution consumers with a highpropensity to switch move rapidly online, as do many lower-valuecommunications

• As time goes on, the remaining base becomes more skewed towards ‘paper-loyal’ consumers and those being sent higher value communications. Weexpect demographic changes and technology evolution to have a lessprominent impact on this segment

• A return to GDP growth as the recession ends is likely to increase overallcommunication volumes, partially offsetting the declining share of lettersin overall communication, particularly for Direct Mail

• Declines in letter volumes will also continue to be partially offset by robustgrowth of parcels traffic, driven by specific categories of online shopping

• We therefore expect the overall UK inland mail volumes to continue todecline albeit more slowly than we have seen historically

- Letters: 5% p.a. decline 2013-18; 4% p.a. decline 2018-23- Parcels: 3% p.a. increase 2013-18; 2% p.a. increase 2018-23- Overall: 4% p.a. decline 2013-18; 3% p.a. decline 2018-23

• Despite the slowing rate of decline in overall mail, these projections imply asignificant reduction from current levels of paper communication by 2023,as well as a substantial change in mix (we believe parcels will double theirshare of the mail bag to c.21%)

• We have identified a number of risks to our projections which mightincrease the rate of mail decline over the projection period. The potentialimpact of these is illustrated in Section 5 of the report

Section 1 – Executive Summary

1

2

3

4

PwC

UK inland letters and parcels market volumes - past, present, andfuture

8Outlook for UK mail volumes to 2023 •

20232005 2012

c.13.8bnitems

Note: International mail volumes not included due to limited data availability for the historical period. Please refer to the later section for projections by mail segmentSource: Royal Mail data, PwC analysis

54%31%

9%6%

56%32%

6%6%

50%

38%

6%6%

Transactional mail

Direct mail

Publishing mail

Social mail

c.1.7bnitems

UK

lett

er

sm

ar

ke

t

c.19.7bnitems

c.1.3bnitems

UK

pa

rc

els

ma

rk

et

c.2.3bnitems

c.8.3bnitems

Section 1 – Executive Summary

PwC

0

50

100

150

200

250

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Ind

ex

ed

ma

ilv

olu

me

s(1

98

1=10

0)

UK overall inland mail volumes, 1981-2012

From 2004, electronic substitution ofmail began to exceed macro driven mailvolume growth, leading to mail volumedeclines of 2.6% p.a. from 2005 to 2008

Mail volumes peaked in 2004 after longrun growth of 3.7% p.a. between 1981and 2004

Since the recession, macro factors (suchas GDP) have also driven lower mailvolumes with mail declines of 5.3% p.a.from 2008 to 2012

Total inland mail volumes peaked in 2004 and have since declined,with an acceleration in mail declines since the start of the recession

Outlook for UK mail volumes to 20239

Source: Royal Mail data, PwC analysis

1

1

2

2 3

3

Section 1 – Executive Summary

PwCOutlook for UK mail volumes to 2023

10

Section 1 – Executive Summary

Forecast

We expect UK letter volume declines to continue, albeit at a slowerrate, while parcel volumes will continue to grow

• We expect the rate of letter volume declines toreduce over the projection period as a result of:

- A return to the trend rate of GDP growthresulting in increased overall communicationvolumes (this will particularly affect Direct Mailwhich is highly cyclical)

- Slowdown in letter volume declines in othersegments, such as financial statements, as abaseline of non-online users or less willing onlineusers is reached

Note: Total inland letter volumes inclusive of Transactional, Social, Direct Mail and Publishing mail volumes. International letter volumes not included due to limited data availability for the historicalperiod. Please refer to the later section for projections by mail segmentSource: Royal Mail data, PwC analysis

0

20

40

60

80

100

120

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Total inland letters historical and projected volumes, 2005-23

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

(3.1%) (6.3%) (4.9%) (3.8%)

Forecast

0

20

40

60

80

100

120

140

160

180

200

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Total inland parcels historical and projected volumes, 2005-23

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

4.3% 3.7% 3.3% 2.1%

• The growth in parcel volumes is expected to continuethroughout the projection period

• We expect some slow down in the rate of growth inthe later years, mainly due to:

- The continued partial digital substitution of someproduct categories, especially Books

- The gradual slowdown in the growth rate ofonline shopping

PwCOutlook for UK mail volumes to 2023

11

Section 1 – Executive Summary

Our e-substitution scenario analysis suggests that in a negativecase, the total cumulative decline could be 5ppt below our base-caseby 2015, increasing to c.12ppt by 2023

• We have modelled upside and downside e-substitution scenarios to demonstrate thepotential impact on our projection of some of therisks we have identified

• These scenarios are based on changing a numberof assumptions underlying our individual mailsegment projections to create high and low casesfor each mail segment

− These are not ‘worst case’ scenarios, but represent plausible alternative outcomes

− Upside scenarios are based on factors such as a larger baseline of consumers and businessesretaining paper invoicing and slowerGovernment digital uptake while downsidescenarios are based on factors such as fasteradoption of paperless bank statements andslower parcel volume growth

• We have used Monte Carlo analysis to illustratethe range of possible outcomes from combiningthese scenarios (reflecting the fact that it isunlikely that all downsides will occur together)

• The scenarios do not include differing GDPassumptions (illustrated later in the report) andalso exclude large one off events which couldsignificantly affect mail volumes. Examples ofthese events are discussed in the ‘Main risks toprojection’ section of the report

0

20

40

60

80

100

120

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

012

=10

0)

Total inland mail projected scenarios, 2012-23

Source: Royal Mail data, PwC analysis

PwC

Historical trends and contextSection 2

Outlook for UK mail volumes to 202312

PwC

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

81/

82

82

/83

83

/84

84

/85

85

/86

86

/87

87/

88

88

/89

89

/90

90

/91

91/

92

92

/93

93

/94

94

/95

95

/96

96

/97

97/

98

98

/99

99

/00

00

/01

01/

02

02

/03

03

/04

04

/05

05

/06

06

/07

07/

08

Yo

Yg

ro

wth

(%)

Actual mail growth vs. modelled growth

Modelled growth Actual growth

Historically mail volumes closely correlated with socio-economicdrivers such as GDP growth, but in recent years technology and e-substitution have become important constraints on growth

“Tech

no

log

yw

edg

e”

• Historically econometric models have been good predictors ofmail growth. But from the early 2000s structural changes (such astechnology and e-substitution) have led to a gap between themodelled growth based on socio-economic factors and actual mailgrowth, sometimes referred to as the "technology wedge”

• While we still expect socio-economic factors to be importantdrivers of mail in the future, forecasting models need to makeallowances for these significant and ongoing trends

Outlook for UK mail volumes to 202313

Section 2 – Historical trends and context

Source: Royal Mail data, PwC analysis

Illustrative

PwC

0

100

200

300

400

500

600

700

800

Un

ited

Sta

tes

Net

her

lan

ds

Sw

eden

Un

ited

Kin

gd

om

Fra

nce

Fin

lan

d

Ger

man

y

Can

ada

No

rway

Den

ma

rk

#o

fp

os

tal

ite

ms

pe

rp

er

so

n

Total inland addressed letter volume per person, 2005and 2011

2005 2011

50%

60%

70%

80%

90%

100%

110%

2005 2006 2007 2008 2009 2010 2011

Decline in inland addressed letter volumes per personfrom 2005 to 2011 (2005=100%)

Germany

Finland

Sweden

France

Canada

Netherlands

United States

United Kingdom

Norway

Denmark

Other developed countries have also seen declines in mail volumes,but at widely varying rates...

Note: Mail volumes for each country are submitted by postal operators and therefore may not be entirely comparable depending on survey methodologies, country data forGermany, Sweden and the Netherlands adjusted based on assumed market share of largest postal operatorSource: IPC, PwC analysis

Letter volumes have been declining around the world, with widevariation in rates

Even before the declines started, letter volumes per head and thecomposition sent varied widely

Outlook for UK mail volumes to 202314

Section 2 – Historical trends and context

PwC

• Denmark has seen one of the fastest declines in physicalmail volumes

• The c.50% decline in addressed inland mail between 2005and 2011 was mostly the result of a decline in priority orstandard addressed mail

• The main driver of the decline was the continued push bythe government to move significant volumes ofcommunication online. The government is currently in theprocess of implementing an ambitious digital strategy tomake all government interactions paperless by 2015

• In 2005, Germany had a lower level of mail items per capitathan the UK and has experienced one of the slowest declinesamong developed countries

• The composition of the German mail bag was very differentfrom the UK. In 2005, Germany sent c.84 pieces of directmail per capita vs. 103 per capita in UK. Between 2005 and2011, UK direct mail declined by c.24% while German directmail declined by only c.11%. As a result, in 2011, bothcountries sent c.75 pieces of direct mail per person

• Physical transactional mail also appears to be preferred inGermany as there is lower acceptance of ‘digital signatures’

• In addition, the government has given comparatively lowpriority to the digitisation of government mail

...this reflects different initial mail bags, cultural factors andgovernment policies in each country

Outlook for UK mail volumes to 202315

Source: Royal Mail data, IPC, PwC analysis

Denmark Germany

Section 2 – Historical trends and context

PwC

100% 2%

5%

5%

2% (3%) (6%)

(5%)

(2%) (3%)(15%)

(3%)(1%) 76%

Vo

lum

e2

00

5

Tra

nsa

ctio

na

lm

ail

eco

no

mic

imp

act

Gro

wth

inp

arce

ls

Imp

act

of

gro

wth

inn

um

ber

of

ho

use

ho

lds

Imp

act

of

bu

sin

ess

pri

cech

an

ges

&D

SA

*

Dir

ect

Ma

ilec

on

om

icim

pa

ct

E-s

ub

stit

uti

on

of

dir

ect

mai

l

E-s

ub

stit

uti

on

of

ban

kst

ate

men

ts

E-s

ub

stit

uti

on

of

invo

ices

E-s

ub

stit

uti

on

of

new

slet

ters

Oth

ertr

an

sact

ion

alm

ail

dec

lin

e

Oth

erm

ail

dec

lin

e

Dec

lin

ein

soci

al

mai

l(e

-su

b&

pri

ce)

Vo

lum

e2

012

Estimate of macro and e-substitution factors driving the decrease in mailvolume, 2005-12

The overall decline in mail in the UK has been driven by e-substitution effects in many different mail categories

The UK economy isaround 4% largerthan in 2005driving an increasein transactionalmail

Total advertisingspend is lower thanits 2005 level,reducing spend onDirect Mail

E-substitution has occurred inmost of the mail categories andcannot be fully split into itsconstituent parts

In addition, DirectMail as a proportionof advertising spendhas declined, furtherreducing mailvolumes

Growth in parceldelivery has offsetsome letter volumedecline

The shift ofbusiness volumestowardsDownstream Accessproviders (e.g. UKMail and TNT) hasreduced averageprices and so beenbeneficial foroverall mailvolumes

Despite its highprofile, the impact ofsocial mail declinehas been relativelylow

Indicative

Outlook for UK mail volumes to 202316

Section 2 – Historical trends and context

Note: *Increased usage of downstream access providers has decreased average prices paid over this periodSource: Royal Mail data, PwC analysis

PwC

Most e-substitution is being caused by technologies which haveexisted for several years rather than very recent innovations

17

PhoneFaxTV

World wide weblaunched

First graphicalweb browser

1st onlinebank Google

AmazonE-bay Facebook

You Tube 75% of UK hashome internet

access

iPhone

iPad

50% of UKusing the

internet daily

60% of UKhas internet

access

GoogleAdwords

Major banks launch online portals enabling paperlessstatements

Email, PDF and electronic invoicing systems enable B2B electronic invoicing

Rich emails allow newsletter volumes to move online

Pay-Per-Click enables growth in internet advertising

Many of thetechnologiescurrentlydriving themajor mailreductionshave existedfor a numberof years

Recent technological enablers such as Social networks,smartphones and tablets are expected to drive furtherdeclines, e.g. impact on Direct Mail and magazines

The effects of recentinnovation e.g. 3D

printing is not likely tobe felt until towards end

of the plan at theearliest

Source: PwC analysis

HMRC launchesonline Self

Assessment

Outlook for UK mail volumes to 2023

Section 2 – Historical trends and context

1990 2000 2010 2013

PwC

Different segments of the mail bag have declined (or grown) at verydifferent rates

51% 50% 51% 51% 52%51% 50% 50%

30% 30% 30%29%

28%29%

29%29%

6% 7% 7%8%

8%9%

10%11%

8% 8% 7%

6%

6%6%

6%5%

5% 5% 5%

5%

6%

6%6%

5%

2005 2006 2007 2008 2009 2010 2011 2012

Pr

op

or

tio

no

fto

tal

ite

ms

(%)

UK mail volume split by application, 2005-12

Social mail

Publishing

Parcels

Direct mail

Transactional

CAGR 2005-12

(3.9%)

(9.5%)

4.1%

(4.6%)

(4.5%)

Note: International mail volumes not included due to limited data availability for the historical period. Please refer to later section for projections by mail segment; Historical parcel volumes have beenestimated using a combination of parcel volume datasets and parcel specific historical growth driversSource: Royal Mail data, PwC analysis

18

Section 2 – Historical trends and context

PwC

Factors influencing mail volumesSection 3

Outlook for UK mail volumes to 202319

PwC

The e-substitution trend varies considerably between mail types,with each in a different position on the ‘S-curve’

Pre decline Early stagee-substitution

Main phase ofdecline

Approachingbaseline

BaselineMail

volumes

YearsMail remains theprimary form ofcommunication

Remaining mailusers are those who

will not usesubstitute forms of

communication

Rate of declinedecelerates as

remaining mail usershave stronger

preferences forphysical mail

Mail volumesrapidly decline as

other channelsbecome increasingly

popular

Mail begins to besubstituted by other

forms ofcommunication

While the majority ofmail volumes willfollow an ‘s-curve’, thespeed of decline andsize of the baselinewill vary byapplication

Mail e-substitution s-curve

Government

Invoicing

Direct mail

Internationalletters

Financialsector

Payments

Publishing

Social

Outlook for UK mail volumes to 202320

Section 3 – Factors influencing mail volumes

Source: PwC analysis

Illustrative

PwC

The steepness of the s-curve and level of the base is determined by abalance of sender and receiver incentives

Relative receiverdemand forelectronic

substitution

Relative senderincentive to encourage

electronic adoption

Higher

Lower

Lower Higher

B2Cinvoice

B2Cinsurancecertificates

Bankstatements

B2Binvoices

B2Binsurancecertificates

Personaltax returns

Benefits

Incentives in example mail types

B2BMagazines

Sender incentives to e-substitute

To a high value customer

High volume

Requires a response

About a high value transaction

Mail for information only

Want prompt payment

Lower

Higher

Receiver receptiveness to e-substitution

Aimed at older groups

Frequent or large mailing

Mail item required quickly

Aimed at lower income groups

Response likely to be online

Has archive value

Lower

Higher

Slow e-substitution

Rapid e-substitution

Source: PwC analysis

Outlook for UK mail volumes to 202321

Section 3 – Factors influencing mail volumes

PwC

A significant proportion of consumers areincreasingly using online services tocommunicate

These consumers prefer to use onlineservices as they believe that they are moreconvenient. The services can be accessed atanytime from anywhere with an internetenabled device

55% of consumers prefer to use onlineservices to interact remotely withgovernment departments

Consumers can be split into those who embrace online services,those who do not use online services because they do not think theyare suitable, and those who have no internet access

A second group of consumers have theability to use online services but choose notto because:

• They may prefer to keep paper records

• They do not believe that online servicesare suitable for certain applications

A smaller group of consumers have limitedaccess to the internet and therefore areunable to use online services

This proportion of non internet users islikely decline over time

c.80% of consumers are split between those who can and do use online services wherepossible and those who can but prefer not to. However, preferences for online services

vary by mail segment

c. 20% of consumers currently havelimited access to online services

55% of consumers who receive onlinefinancial statements state‘convenience’ as the main reason forstopping paper

34% of consumers who receivefinancial statements by post do so tokeep paper records

42% of consumers who do not useinternet banking state the mainreason is concern over security

79%

4%15%

UK Internet take-up andintentions, 2012

Don't intend to get

Don't know if will get

Likely to get in next 12 months

Internet connection at home

Will continue to useonline services and

gradually reduceremaining mail received

May convert to onlineservices as systems

develop

Largely remain mailusers with some online

service adopters

Source: Ofcom Communication Market Report 2012, PwC surveys

Ma

ilo

utl

oo

k

Outlook for UK mail volumes to 202322

Section 3 – Factors influencing mail volumes

PwC

While cost is the primary driver for most senders engaging in e-substitution, the decision to move away from paper is not alwaysstraightforward

Having the option tochoose channel increases

customers’ satisfaction

High initial IT investment required

Forcing e-substitution oncustomers can annoy them

Physical mail is morelikely to be opened and

readCan improve corporate image

“I prefer not to be inundated with catalogues at all, I just put themin the recycling bin while moaning about how many trees were

wasted” - Consumer

Can generate hidden or unexpected costs

Can provide real timeinformation and live

updates

Not all customers might beready to move online

Improves quantity andquality of data collected

“We thought we could do most of the client’s communicationonline, but systems constraints prevented them from going

through with it - many firms don’t have the resources orappetite to do it” – Consultancy firm

Can offer long term costsavings and cheaper

scalability “Paper bill customers are much less likely to phone in withbilling enquiries than e-bill ones, the true cost of e-bills needs to

reflect the potential cost of phone enquiries”- Telco

Source: PwC interviews, PwC surveys, PwC analysis

Can improve immediacyand ease of communication

Potential benefits of e-substitution

Outlook for UK mail volumes to 202323

Potential costs of e-substitution

Section 3 – Factors influencing mail volumes

PwC

4%

21%

23%

27%

25%

16%

33%

17%

14%

20%

0%

5%

10%

15%

20%

25%

30%

35%

16-24 yrs 25-44 yrs 45-54 yrs 55-64 yrs 65+ yrs

Share of transactional mail vs. share ofpopulation, 2011

% of transactional mail % of population

Demographic changes are likely to contribute to declines in postalcommunication in the long term. However, we believe the impactwill be relatively small over the projection period

The primary driver of maildeclines in the short tomedium term is thechanging behaviour withinand across all age groups

All age groups increasinglyhave access to the internetthrough a range of internetenabled devices

However, as a person ages, thevolume of post they receiveincreases due to the ‘complexity’ oflife

On average, older age groupstypically have greater numbers of,and more complex, transactions(e.g. Life insurance) and assets (e.g.Houses, cars and bank accounts)

In the longer term, demographicchange will have a gradual effect onmail reduction, as older age cohortswith more limited internet accessmake up a smaller proportion ofthe population

84% 86% 87%

69%

51%

23%

90% 90% 88%75%

64%

27%

0%

20%

40%

60%

80%

100%

16-2

4

25

-34

35

-54

55

-64

65

-74

75

+

Home Internet access byage, 2010-2012

2010 2011 2012

46% of over 65’s have home

internet access vs. 80% for the

UK population in 2012

Source: Royal Mail data, Ofcom Communication Market Report 2012, PwC analysis

Demographic and behavioural drivers of mailvolumes

24Outlook for UK mail volumes to 2023

Section 3 – Factors influencing mail volumes

1

1

1

1

11

2

2

3

3

PwC

While e-substitution has largely been negative for letters, parcelvolumes have benefitted from growth in online shopping

Growth of remote retail Rise of online

Parcel deliveries have been growingwith the increasing uptake ofremote shopping

Consumers are increasingly optingfor home shopping as it allows forconvenient price and product rangecomparison

Parcels have traditionally been deliveredto home or work places. More recently,customer collection models such as Click& collect and lockers have been gainingtraction. These enhance flexibility,further increasing demand for remoteshopping

While the increased use ofsmart phones and tablets forleisure encourages impulsebuying, it also fuels digitalsubstitution for somecategories such as Books,Music & DVDs where c.30%and 60% of remote deliveriesrespectively are alreadydigital

86%

12%

TV2%

Online has been takingshare from the moretraditional (offline)remote ordering channelssuch as mail and phoneordering and driving theoverall remote retailcategory

Source: Royal Mail data, Mintel, Verdict, PwC interviews, PwC surveys, PwC analysis

While the growth rate is slowing down, online is outperforming total retailwith last year’s annual online expenditure in the UK increasing by c.12.9%compared to total retail growth of c.0.9% during the same time period

“Some items and sizes are not available in store and it saves time to orderfrom home... Others like the anonymity of the process.”

Clothing & Footwear retailer

Online

Digitisation

25Outlook for UK mail volumes to 2023

Section 3 – Factors influencing mail volumes

Remote retail spendby channel, 2012

Mail order6% 7% 7% 8% 8% 9% 10% 11%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

%o

fr

eta

ils

ale

s

UK home shopping sales as %of total retail sales

“Click & Collect service isgetting more popular... Itis very convenient for thecustomer as they do notneed to have someone athome to collect the parcel.”

Department store retailer

4 2771

138

261

20

07

20

08

20

09

20

10

20

11

20

12es

t

Sa

les

(£m

)

UK consumere-book market,2007-12est

n/a

CAGR2008-12est

184%

PwC

• International econometric comparisons indicate that a 1.0%increase in real prices leads to a 0.6% decline in mail volumes onaverage

• Although price elasticity is low for total mail, some applications aremore price sensitive than others, such as direct mail

• There are low risks of price rises causing mail volume decline iffuture price increases are in line with inflation. We haveassumed future price increases to be marginally higherthan RPI therefore further downside risks from price increases arelimited

• However, future price increases significantly above RPI couldreduce volumes considerably. In addition, continued priceincreases would be likely to increase the pace of e-substitution as itmakes electronic communication relatively more cost-efficient

• We believe the interaction between e-substitution and priceconstitute an unknown downside risk to mail volumes

Price rises above inflation both reduce mail volumes in the shortterm and can increase the future rate of e-substitution

Outlook for UK mail volumes to 202326

International comparison of the estimated impact of 1% increasein real prices on aggregate mail volumes*

-2

-1.8

-1.6

-1.4

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

Fin

lan

dB

usi

nes

sto

Co

nsu

mer

ma

il

UK

inla

nd

firs

tcl

ass

no

n-p

re-s

ort

Fin

lan

dB

usi

nes

sto

Bu

sin

ess

ma

il

US

stan

da

rd-m

ail

mar

ket

US

inla

nd

ma

ilm

ark

et

Sw

itze

rla

nd

inla

nd

mai

l

UK

inla

nd

seco

nd

clas

sn

on

-pre

-so

rtm

ark

et

UK

inla

nd

tra

nsa

ctio

na

lm

ail

ma

rket

US

inla

nd

firs

t-cl

ass

mai

l

Co

eff

icie

nt

Note:*Price elasticities based on ‘own-price’ elasticities and hence do not take into account switching between products such as first class volumes moving to second class due to price rises in thefirst class productsSource: Research papers as noted in the Appendix

Section 3 – Factors influencing mail volumes

PwC

Projections by mail segmentSection 4

Outlook for UK mail volumes to 202327

PwC

Our projection looks at the entire UK letter and parcel market,including Royal Mail’s various competitors

Section 4 – Projections by mail segment

Consumers

Businessand public

bodies

Recipient

Overnight express carriers, e.g. Yodel and Hermes

Down stream accesscompanies, e.g. TNT and

UK Mail

CollectionOutward

processingInward

processingDelivery

By-pass, e.g. TNT London trial

Royal Mailoutward

sorting centre Royal Mailinward

sorting centre

Royal Mailcollection

hubs

Deliveryoffices

Wholesale

Presorted

Internationalexport

Internationalimport

Unaddressedadvertising mail

Not covered inour projection:

2 man (items over30kg) deliveries

Irregular mailproducts, e.g.Election mail

Outlook for UK mail volumes to 202328

Food and Grocerydeliveries

Covered in our projection: the UK letter and parcel delivery market

PwC

Ov

er

lay

s

• Develop an econometric model of historical relationships betweenmail volumes and drivers

- Economic and cyclical factors (e.g. GDP, population etc.)

- Time trends to account for e-substitution and e-commercetrends

- Price elasticity, i.e. sensitivity to changes in the price of lettersand parcels

• Apply forecasts of the underlying drivers to produce a projection foreach of the main categories of mail

• 100+ interviews with large senders, 4 online surveys with c.3,000respondents (including consumer, business and public bodies),desktop research and interviews with mail stakeholders

• Analyse each sub-segment of the mail bag to understand keyindustry drivers and trends

• Estimate the likely macro and e-substitution trends for eachsegment

We have projected mail volumes using both bottom-up and top-down approaches

Outlook for UK mail volumes to 202329

Section 4 – Projections by mail segment

Triangulation and harmonizationof results

Integrated view

Sensitivity analysis Short term risks Long term risks

Final projection

The top-down approach allows us to understand the macrodrivers behind changes in mail use

The bottom-up approach allows us to understand the specificdrivers behind changes in each mail segment

PwC

Our top down approach uses econometric models with time trendsto account for technology and e-substitution

Section 4 – Projections by mail segment

E-substitution, linear and non-linear time trend*

Time

Le

tte

rv

olu

me

s

Linear trend(best fit based onhistorical data)

Non-linear trend(best fit based onhistorical data)

E-substitution

Historical data

Note:*Most suitable shape of the time trend varies by applicationSource: PwC analysis

We have considered two ways to include technological factors in oureconometric modelling

2. Estimate the shape and impact oftechnology on mail volumes byincluding time trends in themodel (while remaining agnosticabout what technology is drivingthe trend). Different types of timetrends (linear and non-linear)can be used to estimate the shapeof the historical technologywedge and then applied toestimate future mail volumes

• The limitation of this approach isthat the past may not be a fairrepresentation of the future. Forexample, a trend that has beenincreasing historically may flattenout or even start to decrease

1. Analyse the impact of differenttechnological drivers for e-substitution, e.g. social media usefor social mail or online bankingpenetration for financial mail.There are two limitations to thisapproach:

• Technology is continuouslyevolving and so it is impossible toinclude an exhaustive list of thetechnological factors that mightimpact each mail type in thefuture;

• Forecasting how the selecteddriver will evolve in the future isoften as difficult as forecastinghow mail volumes will evolve

On balance, we believe that time trends provide the best way to create asensible and robust model

Outlook for UK mail volumes to 202330

Illustrative

PwC

Our bottom-up projection breaks down the mail bag into c.20 mainsegments and looks at the drivers and outlook for each

Source: Royal Mail data, PwC analysis

Transactional mail Direct mail Publishing

Socialmail Parcels

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 20% 40% 60% 80% 100%

Ke

ys

eg

me

nts

Key mail type

UK inland and international mail volume by type, 2012

+

Parcels

Letters

Internationalmail

CentralGovernment

LocalGovernment

Healthcare

Ed

uca

tion

Financial Servicesstatements

Financial Services Legal / Terms and Conditions

Financial ServicesInsurance

Financial ServicesOther

Invoices B2B B2C bills

Other C2X

Other B2B

Other B2C

Payments

Catalogues

Advertising

Ma

ga

zines

New

sletters

B2B

C2X

B2C

Outlook for UK mail volumes to 202331

Section 4 – Projections by mail segment

PwC

These high level categories in turn break down into thousands ofdifferent types of mail from different senders. Each of these types ofmail exhibits different growth dynamics

Total Mail

Transactional Mail

GovernmentMail

Central Government

Source: Royal Mail data, PwC analysis

Not to Scale

32

Section 4 – Projections by mail segment

PwC

Forecast

Total inland letter volumes have been declining historically. Thecontraction is expected to continue albeit at a slower rate year-on-year

Outlook for UK mail volumes to 202333

Section 4 – Projections by mail segment

Note: Above analysis exclusive of parcel, i.e. reflecting letter volumes only. International letter mail volumes not included due to limited data availability for the historical period. Please refer to thelater section for projections by mail segmentSource: Royal Mail data, PwC analysis

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Total inland letters historical and projected volumes, 2005-23

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

(3.1%) (6.3%) (4.9%) (3.8%)

Position on s-curve

PwC

Forecast

While letter volumes continue to fall, parcels will grow their shareof total inland mail volume

Note: International mail volumes not included due to limited data availability for the historical period. Please refer to the individual section for projectionsSource: Royal Mail data, PwC analysis

50% 49% 48% 47% 46% 45% 44% 43% 42% 41% 40% 39%

29% 28% 28% 28% 28% 29% 29% 29% 30% 30% 30% 30%

11% 12% 13% 14% 15% 16% 17% 18% 19% 19% 20% 21%

5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5%

5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Pr

op

or

tio

n(%

)

Total mail volume forecast by type, 2012-23

Social mail

Publishing mail

Parcels

Direct mail

Transactional mail

Outlook for UK mail volumes to 202334

Section 4 – Projections by mail segment

PwC

Forecast

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Transactional mail historical and projected volumes, 2005-23

Rapid decline in transactional mail volumes is expected to continuebefore slowing down towards the end of the projection period

Note: Excludes Royal Mail Large Letters (packets) which are included in parcel estimatesSource: Royal Mail data, PwC analysis

Position on s-curve

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

(2.5%) (6.2%) (5.4%) (4.5%)

Outlook for UK mail volumes to 202335

Transactional Mail – Financial ServicesSection 4 – Projections by mail segment

PwC

Financial institutions have already captured many of the ‘quickwins’ from e-substitution. Consequently substitution of the morefragmented remainder will be slower

We expect growth in the penetration of online banking to slow in thenext five years as the remaining offline consumers become harder toconvert

There will be a continued shift to paperless among online bankingusers. The current 44% of consumers who state they will always wantto receive paper statements is likely to reduce over the projectionperiod

RBS changed from monthly to quarterly statements in Feb 2013 andwe expect other banks may follow suit. This will have a significantimpact on current account volumes, but monthly credit cardstatements are seen as more important as they prompt payment andother statements are already sent less frequently

25% of transactional mail in the

UK is sent by the top 5 banks, withother financial services companies

accounting for another 10%

Statements constitute approximately

half of mail sent by banks, 50%

of which is current accounts

Paperless current accounts are now

c.40% of the total

“The direction banksare going in is aboutcommunicating inthe medium ofchoice. Paper is nowjust one of a numberof media and wehave been verysuccessful atimproving theonline proposition”

Top five UK bank

“As our digitisation increases it isn’tstraightforward that our letter volumesdecrease. There’s baseline growth and asignificant amount of non-statement mail, e.g.credit card renewals. Digitisation cannot offera viable substitute for many of these items”

Top five UK bank

We estimate that of the non-statement mail sent by financial services companies, around 30% isdifficult to substitute due to regulation (e.g. the requirement for a ‘wet’ signature) or is the deliveryof a physical item (e.g. a credit card)

While the substitutable remainder isearly on in its substitution S-curve, itsfragmented nature means the rate ofdecline is likely to be longer and flatterthan that of statements

0%

20%

40%

60%

80%

100%

199

8

20

00

20

02

20

04

20

06

20

08

20

10

Proportion of UK individualsregistered for internetbanking, 1998-2011

Source: British Banking Association Annual Abstract 2012, PwC interviews, PwC surveys, PwC analysis

Outlook for UK mail volumes to 202336

Transactional Mail – Financial ServicesSection 4 – Projections by mail segment

PwC

Sent togeneral

population

Sent tovulnerable

groups

Central government mail sent to thegeneral population vs. vulnerablegroups (Illustrative)

The majority of Government mail is transactional in nature, relatingto services such as benefits and taxation

We believe the Government sector as a whole is towards the beginningof the s-curve with significant scope for further mail reductions

However, there are large variations as some government services haveachieved significant online penetration, while others are not expectedto substitute at all

We expect a continued decline in Government mailvolumes as a result of:

• Increased budgetary pressures. Governmentsurveys estimate the cost of a digital transactioncan be c.30x lower than a postal transaction

• Demand for a better digital service forcustomers

However, in a number of areas, declines will belimited by customer acceptance and technologicalchallenges

• Many online services will need to seamlesslylink to multiple government databases

• Certain customer groups have more limitedonline access, e.g. only 46% of people aged 65and over have home internet access

We expect Government mail volumes to decline faster thanhistorically driven by budgetary pressures and CentralGovernment’s Digital by Default strategy

Outlook for UK mail volumes to 202337

The Government’s Digital Strategy was released in November2012 to drive the development and use of online governmentservices to reduce non-digital transactions (post, phone and faceto face meetings).

“Digital by Default is a major initiative which may accelerate thepost decline”

Central Government Department

“We willcontinue topush formore peopleto usepaperless asit is so muchcheaper”

Local Authority

46% of the

public have useda governmentonlinetransactional

service 83%of Annual SelfAssessment formswere submittedonline to HMRCin 2011/12*

Digital by Default

“We areconstrainedby what ourICT canhandle”

Local Authority

Note: *Of on time Self Assessment submissionsSource: Royal Mail data, Central Government data, Digital Efficiency Report, Government Digital Strategy, Ofcom Communications Report 2012

Transactional Mail – GovernmentSection 4 – Projections by mail segment

PwC

B2C companies are increasingly encouraging consumers to switchto online communications to reduce costs. Rapid declines aretherefore expected to continue

B2C businesses with large customerbases are increasingly seeking toswitch customers from paper todigital interactions to reduce costs

As a result we expect B2C businessesto significantly reduce mail usageover the next ten years

Billing

B2C invoicing continues to move online andwe expect significant mail declines in thenext 3 years as businesses develop theironline billing processes

“We are targeting a significant increase inthe amount of online billing so the vastmajority is online”B2C Company

Examples

Insurance

Recent regulation changes allowedinsurance certificates to be sentelectronically. Companies have plans tomove significant volumes online, but manyare held back by the IT investmentrequired. The largest impact is likely to bein the middle of the projection period

53% of B2C businesses will encourage

their customers to switch to digital with a

further 16% planning to stop paper

transactions at some point in the future

“We will never get everybody online butwe are aiming for as many as possible tocut down our mailing costs”

B2C company

Businesses recognise that aproportion of their customer base willcontinue to prefer paper copies oftransactions, predominantly forrecord keeping. As companies reachthis baseline of paper customers, therate of mail decline will reduce

47% of B2C SMEs will continue to use

mail because their customers will continue torequest paper

Mail costs are an increasing focusof B2C businesses...

Mail costs are an increasing focusof B2C businesses...

...however, customer demand forpaper is likely to act as a

significant inhibitor

...however, customer demand forpaper is likely to act as a

significant inhibitor

“We are dependent on customerpreferences and some will not switch offpaper billing as they like to file the bill”

B2C company

Source: PwC surveys, PwC interviews

38Outlook for UK mail volumes to 2023

Transactional Mail – B2B mailSection 4 – Projections by mail segment

PwC

B2B transactional mail volumes are more fragmented than B2C,but the inhibitors to substitution are lower

The barriers to reducing mail are lower, with less investmentoften required to allow online communication and a smallerbase of businesses resistant to electronic interaction than thebase of consumers

Invoicing

B2B invoicing is likely to follow a similartrend to B2C, with declines in the next fewyears leading to a low baseline of businesseswhich prefer paper by the end of theprojection

“Some businesses like to receive a one pagepaper summary for their accounts”

B2B Invoicer

Mail costs aregenerally less of a

direct focus for B2Bcompanies than

B2C...

Insurance

Rate of decline is lower than for consumerinsurance, with relatively low demand forpaperless insurance in the marketplace.

“There’s some element of demand, but wehaven’t seen a massive appetite”

B2B Insurance advisor

63% of B2B businesses

encourage their customers to switch todigital vs. 53% for B2C

“If we’re insuring something for multimillions, like an ocean liner wesend fancy documents. We send a lot physically as it makes people feellike they have bought something valuable. It’s the bottom-end, massmarkets that will go more online, like car insurance”

Large Insurance Company

...but lower barriersmean the mail

reduction isexpected to

accelerate anddecline to a smaller

base

B2B mail is more fragmented and represents lower volume,higher value transactions than B2C mail. The printing andmailing costs are usually a lower proportion of the overalltransaction or customer value than in B2C, reducing theincentive to reduce mail

Source: PwC surveys, PwC analysis

39Outlook for UK mail volumes to 2023

Transactional Mail – B2B mailSection 4 – Projections by mail segment

Examples

PwC

Forecast

0

20

40

60

80

100

120

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Direct mail historical and projected volumes, 2005-23

We expect direct mail volumes to stabilise towards the end of theperiod. The weak economy was a major driver of the rapid declinesseen in recent years

Note: Excludes Royal Mail Large Letters (packets) which are included in parcel estimatesSource: Royal Mail data, PwC analysis

Position on s-curve

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

(2.7%) (6.1%) (2.9%) (1.3%)

Outlook for UK mail volumes to 202340

Direct MailSection 4 – Projections by mail segment

PwC

0%

5%

10%

15%

20%

25%

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Direct mail share of total advertising spend, 1982-2011

Historically, direct mail declined as a share of total advertising,but it is likely to reach a new equilibrium level as internetadvertising matures

Source: The Advertising Association/ WARC Expenditure Report, PwC interviews, PwC surveys, PwC analysis

Total advertising expenditure follows GDP and is now recovering fromthe recession. Direct mail declined along with total advertising, but alsolost share of marketing spend to fast growing online marketing. Thedecline rate is slowing as online advertising matures and the economyrecovers

The companies that are most successful at using direct mail integrate itwith other channels to use all the available data to improve thetargeting and relevance of direct mail messages

“Direct mail is a relationship builder and for high-value customers itcan demonstrate the value of the relationship”

Leading advertising agency

Return on investment (ROI) in direct mail is comparable with othermedia and is becoming more measureable due to innovation in directmail response tracking

“Direct mail is a massively important medium and it works”

Marketing consultant

There remains a threat that new technologies such as mobile will upsetthe balance of ROI in the industry again, but declining volumesincrease the attractiveness of direct mail as mailings stand out moreeasily

“When volumes drop below a certain threshold some savvy marketerswill realise the channel is underutilised and ‘rediscover’ it”

Mailing house

1/3 of British consumers

still prefer to receive postedcatalogues rather than usingwebsites

47% of British retailers

use mail as a marketingchannel

Growth due toimprovements in printingquality and costs

Outlook for UK mail volumes to 202341

Direct MailSection 4 – Projections by mail segment

PwC

Forecast

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Publishing mail historical and projected volumes, 2005-23

The rapid decline in publishing mail in recent years was largelydriven by the majority of newsletters going online...

Note: Excludes Royal Mail Large Letters (packets) which are included in parcel estimatesSource: Royal Mail data, PwC analysis

Position on s-curve

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

(9.1%) (9.4%) (5.0%) (3.0%)

Outlook for UK mail volumes to 202342

Publishing MailSection 4 – Projections by mail segment

PwC

NewslettersB2B magazinesB2C magazines

... the publishing segment is now largely comprised of magazines,which have proven more resilient to e-substitution, resulting in aslower decline over the projection period

Source: Enders, Mintel, PwC Entertainment and Media Outlook, PwC interviews, PwC surveys, PwC analysis

His

tor

ica

ltr

en

ds

Consumer print magazine circulationdeclined by c.34% between 2007-2012but subscriptions grew by c.17%

The uptake of digital editions has beenslower then expected and has notreplaced print

Digital brands generated an estimated15% of consumer magazine publisherrevenues in 2012

“We believe digital subscriptions areattracting new customers and notreplacing existing ones”

Leading publisher

Substitution will accelerate slightly butremain relatively slow

Business media customers aregenerally high value, paying muchhigher subscriptions than consumersand are targets for on-sell of data andother services

“The print and distribution costs area small percentage of our revenueper customer”

Large B2B publisher

The incentives for both the senderand receiver to stop the print editionare low so we expect declines tocontinue to be relatively slow

Newsletters moved online veryquickly, only 25% are still offline

“We switched about 2 years agobecause it was not cost-effective “

University

This decline will slow towards theend of the period as a baseline isreached of senders that see a benefitfrom newsletters sent physically,such as charities encouragingdonation

“We send newsletters to previousdonors, to make them aware of theresults of their help. Newsletters arecostly but they will stay offline”

National charity

0

200

400

600

800

2007 2008 2009 2010 2011 2012

Ite

ms

(m)

Estimated newsletter volumes2007-12

0

50

100

150

200

2007 2008 2009 2010 2011 2012

Ite

ms

(m)

B2B Magazine subscriptionvolumes 2007-12

0

50

100

2007 2008 2009 2010 2011 2012

Ite

ms

(m)

B2C Magazine subscriptionvolumes 2007-12

Cu

rr

en

td

ev

elo

pm

en

ts

Outlook for UK mail volumes to 202343

Publishing MailSection 4 – Projections by mail segment

PwC

Forecast

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Social mail historical and projected volumes, 2005-23

Social mail volumes are not expected to decline radically in the next10 years. While some contraction is expected, most of the electronicsubstitution has already occurred

Note: Excludes Royal Mail Large Letters (packets) which are included in parcel estimatesSource: Royal Mail data, PwC analysis

Position on s-curve

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

(1.9%) (5.3%) (3.8%) (3.2%)

Outlook for UK mail volumes to 202344

Social MailSection 4 – Projections by mail segment

PwC

Personal letter use has declined rapidly, but greetings cards aremore resilient and now represent the majority of social mail

18

16

13

2006 2009 2012

Average social mail received perperson, 2006, 2009 & 2012

Split of social mail, 2012

Greetings cards80%

Letters/Postcards

20%

Social letters and postcards have beendeclining rapidly as consumers move tothe wide range of alternatives

Consumers are also sending fewergreetings cards, but the decline is sloweras electronic alternatives have notgained wide acceptance

The overall decline in social mail is likelyto slow as the mix continues to movetowards greetings cards

Innovation

Some decline in Social mail may bemitigated by innovative platforms thatdrive usage of mail:

• Moonpig allows online design andpersonalisation of cards

• The TouchNote app sendssmartphone photos as postcards

Source: Royal Mail data, Ofcom Postal Tracker Q4 2012, PwC analysis

Econometric drivers

Historical relationships suggest socialmail has a number of underlyingeconomic drivers such as number ofhouseholds, price and quality ofservice. Price rises have contributed tomore than half of the decline in socialmail volumes during the last five years

Outlook for UK mail volumes to 202345

Social MailSection 4 – Projections by mail segment

2% 5%

65%

16%8%

Incr

ease

sig

nif

ican

tly

Incr

ease

slig

htl

y

Sta

yth

esa

me

Dec

rea

sesl

igh

tly

Dec

rea

sesi

gn

ific

an

tly

Re

sp

on

se

fre

qu

en

cy

(%)

How will the number of cards you sendthrough the post this Christmas comparewith last year?

PwC

Forecast

Parcel volumes have been growing steadily and this is expected tocontinue during the projection period

Outlook for UK mail volumes to 202346

Note: Includes Royal Mail Large Letters (packets), DSA parcels and couriersSource: Royal Mail data, PwC analysis

ParcelsSection 4 – Projections by mail segment

0

20

40

60

80

100

120

140

160

180

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

00

5=

100

)

Parcels historical and projected volumes, 2005-23

Position on s-curve

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

4.3% 3.7% 3.3% 2.1%

PwC

• The market is less exposed to the risks of digitalsubstitution because it is mainly composed ofphysical items that need to be delivered

Despite strong growth in B2C, overall growth in parcels is reducedby the lower growth rates of B2B and C2X

• Social parcelvolumes willremain stable withonly limitedpopulation growthand behaviouralchange expected

Consumer-to-consumer/ business (C2X)

77% of

consumersthink the

number ofparcels they

send willstay the

same

• Growth will bemainly driven byonline sales (e.g.eBay) • Volumes are expected to

grow at c.2-4% p.a. by 2023,trending with the improvingUK economy

• The growing popularity ofClick & Collect and similardelivery formats will createan additional uplift in themedium term**

61% of

retailers thinkclick & collect

will reachgrowth limitsin 3-5 years

or evenearlier

Business-to-consumer (B2C)

• Increased uptake of online shoppingvia PC, tablet or smart phone is toremain the key growth driver,especially in Clothing, Footwear andHealth & Beauty

• Volumes through traditional remotechannels (mail, phone, store orders)are expected to continue declining andrepresent a gradually smaller portionof overall B2C volumes (now c.15%)

• Fulfilment of Music & DVDs, VideoGames and Books (c.40% of currentparcel deliveries) will remain underpressure until 2023 due to intensifyingdigital substitution

“Online is growing but the growth rateis slowing down” Health &

Beauty retailer

“Online growth is fast for clothingwhere it has been encouraged by freereturns” Department store retailer

Note: *Click and collect parcels transported by retailers’ own fleets; **As the Click & Collect delivery is within the retailer’s network, this drives the B2B market rather than B2CSource: Royal Mail data, PwC interviews, PwC surveys, PwC analysis

Business-to-business (B2B)

Outlook for UK mail volumes to 202347

ParcelsSection 4 – Projections by mail segment

1 2

3

3.7%

2.0%

3.0%

2.3%1.8%

1.0%

3.3%

2.1%

2013-18 2018-23

CA

GR

(%)

Parcel projected volume growth by segment,2013-23

B2C B2B C2X TOTAL

PwC

Underpinning the growth in B2C parcels is greater online orderingof items such as clothing and footwear. However, this will be offsetby ongoing digital substitution of categories such as books and DVDs

Outlook for UK mail volumes to7 202348

Source: PwC analysis

ParcelsSection 4 – Projections by mail segment

CAGR2013-18

(4.2%)

9.3%

4.5%

3.7%Total

41% 37% 34% 31% 29% 27% 25% 24% 22% 21% 19% 18%

36% 39% 42% 44% 47% 49% 50% 52% 53% 54% 55% 56%

23%24%

24%24%

25%25%

25%25%

25%25% 25% 26%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

To

tal

ite

ms

UK B2C parcels market volumes, 2012-23

Other

High growth

Substitutable

• Homewares

• DIY and gardening

• Other

• Clothing and footwear

• Health and beauty

• Electricals

• Music and DVDs

• Books

• Video games

CAGR2018-23

(4.7%)

4.5%

2.7%

2.0%

PwC

Forecast

Forecast

Outlook for UK mail volumes to 202349

Despite the historical contraction in letter volumes, internationalmail volumes have benefited from the growth in parcels

Source: Royal Mail data, PwC analysis

Position on s-curve

Position on s-curve

International Mail

0

20

40

60

80

100

120

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

012

=10

0)

International letters historical and projected volumes, 2012-23

0

20

40

60

80

100

120

140

160

180

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

012

=10

0)

International parcels historical and projected volumes, 2012-23

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

n/a n/a (5.5%) (4.8%)

CAGR2005-08

CAGR2008-13

CAGR2013-18

CAGR2018-23

n/a n/a 4.4% 3.2%

Section 4 – Projections by mail segment

PwC

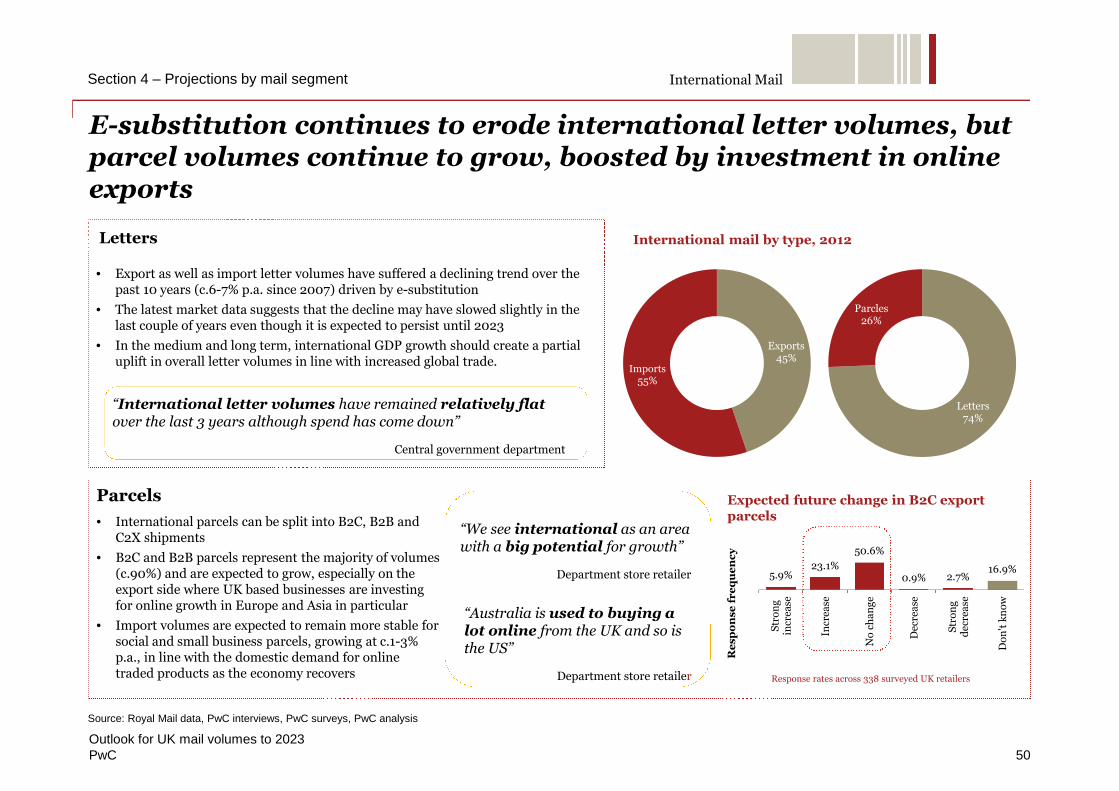

E-substitution continues to erode international letter volumes, butparcel volumes continue to grow, boosted by investment in onlineexports

Source: Royal Mail data, PwC interviews, PwC surveys, PwC analysis

Outlook for UK mail volumes to 2023

International mail by type, 2012

• Export as well as import letter volumes have suffered a declining trend over thepast 10 years (c.6-7% p.a. since 2007) driven by e-substitution

• The latest market data suggests that the decline may have slowed slightly in thelast couple of years even though it is expected to persist until 2023

• In the medium and long term, international GDP growth should create a partialuplift in overall letter volumes in line with increased global trade.

Letters

“International letter volumes have remained relatively flatover the last 3 years although spend has come down”

Central government department

Parcels

• International parcels can be split into B2C, B2B andC2X shipments

• B2C and B2B parcels represent the majority of volumes(c.90%) and are expected to grow, especially on theexport side where UK based businesses are investingfor online growth in Europe and Asia in particular

• Import volumes are expected to remain more stable forsocial and small business parcels, growing at c.1-3%p.a., in line with the domestic demand for onlinetraded products as the economy recovers

“We see international as an areawith a big potential for growth”

Department store retailer 5.9%23.1%

50.6%

0.9% 2.7%16.9%

Str

on

gin

crea

se

Incr

ease

No

cha

ng

e

Dec

rea

se

Str

on

gd

ecre

ase

Do

n't

kn

ow

Re

sp

on

se

fre

qu

en

cy

Response rates across 338 surveyed UK retailers

“Australia is used to buying alot online from the UK and so isthe US”

Department store retailer

50

Expected future change in B2C exportparcels

Section 4 – Projections by mail segment International Mail

Exports45%

Imports55%

Letters74%

Parcles26%

PwC

Main risks to projectionSection 5

Outlook for UK mail volumes to 202351

PwC

There are a number of short term risks which could have one offnegative impacts on the projection which we have not modelled

1. Macroeconomic downturn

• Our projection assumes a return to trend GDP growth in 2015

• A future macroeconomic downturn would have a significant impact onpostal volumes by reducing transaction volumes and direct mail

Source: PwC interviews, PwC analysis

Outlook for UK mail volumes to 2023PwC

3. EU Regulation on Direct Mail

• The EU Commission has recently proposed changes to consumer dataprotection rules

• The proposed changes include the ‘right to be forgotten’ to allow peopleto have their data deleted and limitations on the use of customerprofiling

• The requirement for more explicit consent for personal data to be usedcould significantly impact the ability of companies to engage in DirectMarketing, both by mail and in digital formats

2. Service disruptions

• The disruption of delivery volumes (e.g. from weather or industrialaction) can have a significant impact on mail volumes

• The majority of this impact is temporary. However, service disruptionsmay also encourage greater e-substitution as a result of customerswitching to alternative methods of communication

• The impact of service disruptions on postal volumes can be modelled onthe basis of the historic correlation between previous disruptions andmail volumes.

4. VAT Treatment

• Royal Mail Wholesale (Downstream Access) is currently VAT exempt.However, Royal Mail’s exemption may become subject to a judicialreview

• If all Wholesale services became VAT taxable, organisations that areunable to reclaim VAT, such as charities and financial services firms,would see a significant effective price increase and this could encouragefurther e-substitution of mail

“If Downstream Access becomes taxable, it would lead to a 20%increase in our costs and would have a serious impact on our mail use”

Insurance company

52

Section 5 – Main risks to projection

PwC

Some of the longer term risks applicable to mail volume projectionscannot yet be quantified and so are included in a contingencywithin the projection

Source: PwC analysis

Outlook for UK mail volumes to 202353

Section 5 – Main risks to projection

Potential projection risks

• Identifiable one-offsthat could fall withinthe time frame of theprojection, e.g.:

o Large scale Internetsecurity breach thatencouragesconsumers to revertto mail

o Widespreadadoption of digitalmailboxes

• Rare ‘black swan’event that cannotbe predicted easilybut could have asignificant impacton projected mailvolumes and thestructure of thepostal market

• Shifts could occurthrough anychannel, e.g.technological,political, macroeconomic

• Identifiable trendsthat will materialiseeventually but areunlikely to take placewithin the projectionperiod, e.g.:

o Electronic invoicesmandated for allgovernmentprocurement

o 3D printing ofremotelypurchased goodsthat would reduceparcel deliveries

• Risks arising fromknown trends (e.g.technologydevelopment, ageingpopulation) whichcannot currently bespecifically identified,e.g.:o The development of

new marketingtechnologies thatfurther reducedirect mail’s shareof advertising spend

• Risks arising from anychanges to ourprojection assumptionsrelating to theoperation and structureof the market

Known risks Unknown risks

Unlikely but possiblewithin projection period

Unlikely withinprojection timescale

Identified Unidentified

PwC

Our e-substitution scenario analysis suggests that in a negativecase, the total cumulative decline could be 5ppt below our base-caseby 2015, increasing to c.12ppt by 2023

Outlook for UK mail volumes to 202354

• We have modelled upside and downside e-substitution scenarios to demonstrate thepotential impact on our projection of some of therisks we have identified

• These scenarios are based on changing a numberof assumptions underlying our individual mailsegment projections to create high and low casesfor each mail segment

− These are not ‘worst case’ scenarios, but represent plausible alternative outcomes

− Upside scenarios are based on factors such as a larger baseline of consumers and businessesretaining paper invoicing and slowerGovernment digital uptake while downsidescenarios are based on factors such as fasteradoption of paperless bank statements andslower parcel volume growth

• We have used Monte Carlo analysis to illustratethe range of possible outcomes from combiningthese scenarios (reflecting the fact that it isunlikely that all downsides will occur together)

• The scenarios do not include differing GDPassumptions (illustrated later in the report) andalso exclude large one off events which couldsignificantly affect mail volumes. Examples ofthese events are discussed in the ‘Main risks toprojection’ section of the report

Source: PwC analysis

0

20

40

60

80

100

120

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

012

=10

0)

Total inland mail projected scenarios, 2012-23

The balance is towardsmore downside risk

Section 5 – Main risks to projection

PwC

0

20

40

60

80

100

120

2012 2023

Ind

ex

ed

ma

ilv

olu

me

s(2

012

=10

0)

In addition, the total cumulative decline in mail volumes could bec.6ppt below our base-case by 2023 if GDP growth were to be at thebottom of our projected range

• We have also consideredupside and downside GDPscenarios and their impact onour mail projections

• Our upside GDP caseassumes a stronger thanexpected recovery andmarginally higher trendgrowth over our base-case inthe outer years

• Our downside GDP caseassumes a period ofstagnation and lower trendgrowth than our base-case inthe outer years

• The shaded area shows therange of potential outcomesresulting from the GDPscenarios described above

Outlook for UK mail volumes to 2023

Total inland mail projected GDP scenarios, 2012 & 2023

Our upside GDP scenario assumes a strongerrecovery of the UK economy with c.4% growthin 2014 and a return to trend growth rate of2.5% p.a.