Embed Size (px)

Citation preview

The Outlook and Current Policy Challenges

RMA New England Annual Meeting May 4, 2018

Jeff Fuhrer EVP and Senior Policy Advisor Federal Reserve Bank of Boston

1

2

Disclaimer: The views represented in this presentation are solely those of the author, and do not reflect the views of the Federal Reserve Bank of Boston, the Board of Governors of the Federal Reserve System, or the Federal Open Market Committee

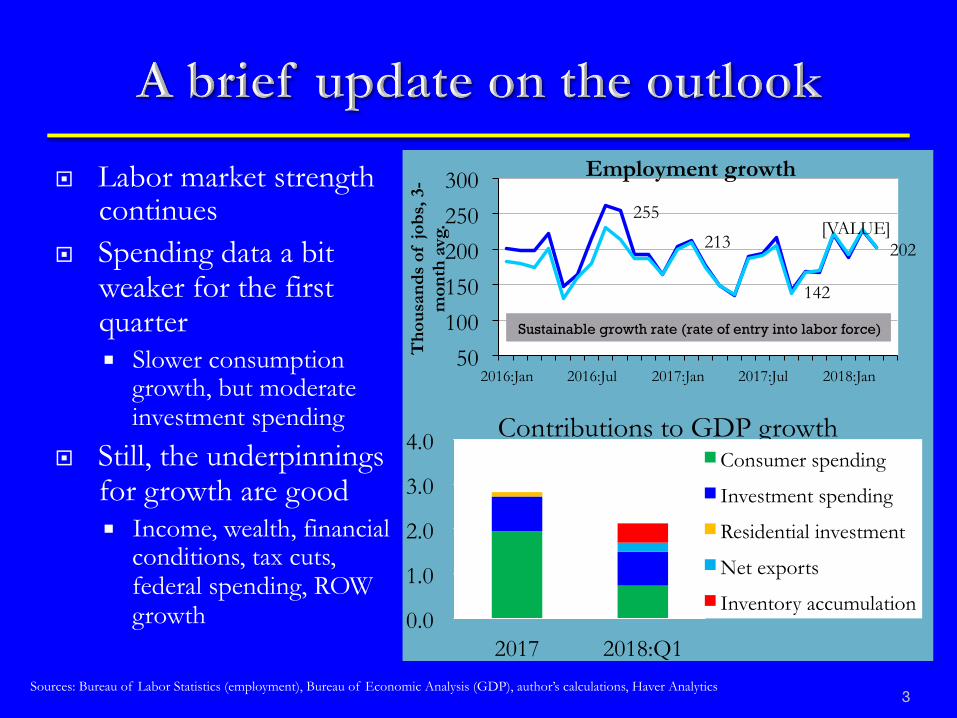

¨ Labor market strength continues

¨ Spending data a bit weaker for the first quarter ¡ Slower consumption

growth, but moderate investment spending

¨ Still, the underpinnings for growth are good ¡ Income, wealth, financial

conditions, tax cuts, federal spending, ROW growth

3

255

213

142

202 [VALUE]

50

100

150

200

250

300

2016:Jan 2016:Jul 2017:Jan 2017:Jul 2018:Jan

Tho

usan

ds o

f jo

bs, 3

-m

onth

avg

.

Employment growth

Sustainable growth rate (rate of entry into labor force)

Sources: Bureau of Labor Statistics (employment), Bureau of Economic Analysis (GDP), author’s calculations, Haver Analytics

0.0

1.0

2.0

3.0

4.0

2017 2018:Q1

Contributions to GDP growth Consumer spending

Investment spending

Residential investment

Net exports

Inventory accumulation

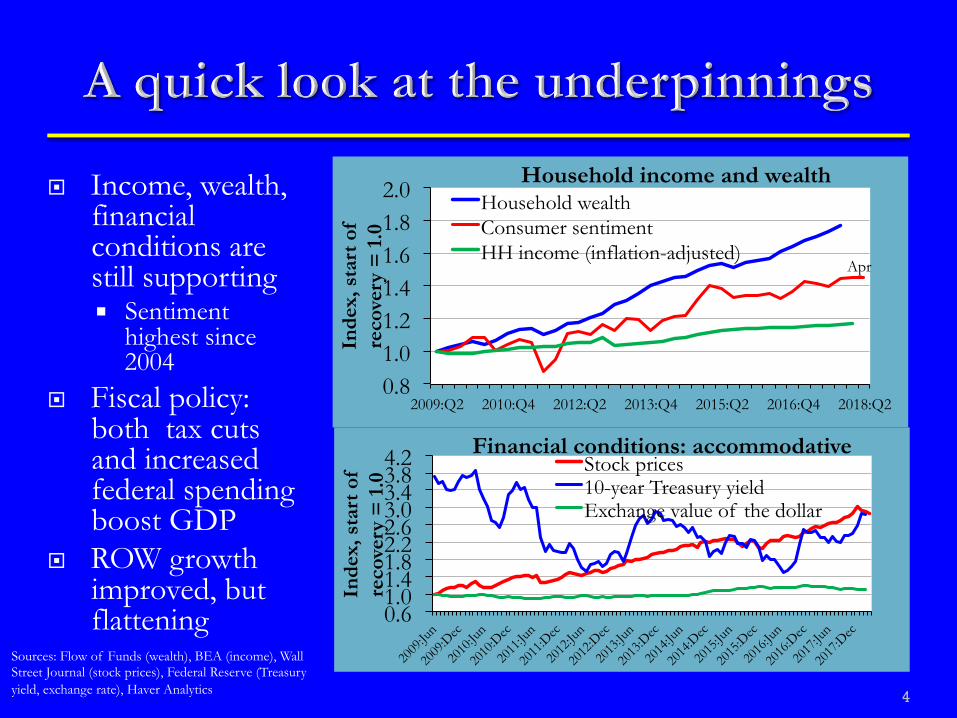

¨ Income, wealth, financial conditions are still supporting ¡ Sentiment

highest since 2004

¨ Fiscal policy: both tax cuts and increased federal spending boost GDP

¨ ROW growth improved, but flattening

4

0.8 1.0 1.2 1.4 1.6 1.8 2.0

2009:Q2 2010:Q4 2012:Q2 2013:Q4 2015:Q2 2016:Q4 2018:Q2

Inde

x, s

tart

of

reco

very

= 1

.0

Household income and wealth Household wealth Consumer sentiment HH income (inflation-adjusted)

Apr

0.6 1.0 1.4 1.8 2.2 2.6 3.0 3.4 3.8 4.2

Inde

x, s

tart

of

reco

very

= 1

.0

Financial conditions: accommodative Stock prices 10-year Treasury yield Exchange value of the dollar

Sources: Flow of Funds (wealth), BEA (income), Wall Street Journal (stock prices), Federal Reserve (Treasury yield, exchange rate), Haver Analytics

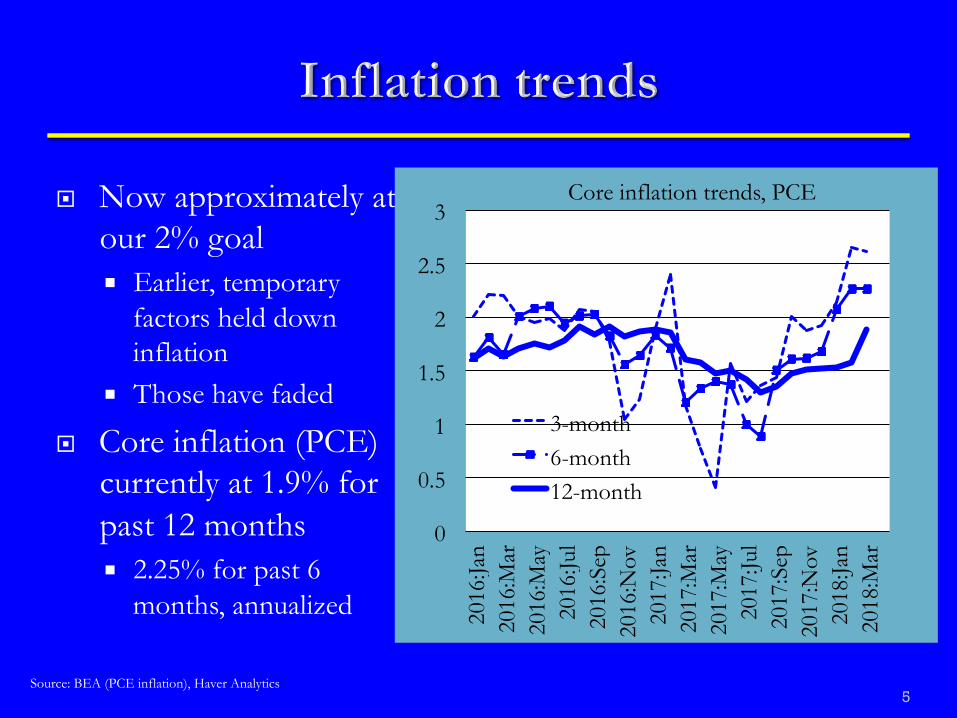

¨ Now approximately at our 2% goal ¡ Earlier, temporary

factors held down inflation

¡ Those have faded

¨ Core inflation (PCE) currently at 1.9% for past 12 months ¡ 2.25% for past 6

months, annualized

5

0

0.5

1

1.5

2

2.5

3

2016

:Jan

2016

:Mar

20

16:M

ay

2016

:Jul

2016

:Sep

20

16:N

ov

2017

:Jan

2017

:Mar

20

17:M

ay

2017

:Jul

2017

:Sep

20

17:N

ov

2018

:Jan

2018

:Mar

Core inflation trends, PCE

3-month 6-month 12-month

Source: BEA (PCE inflation), Haver Analytics

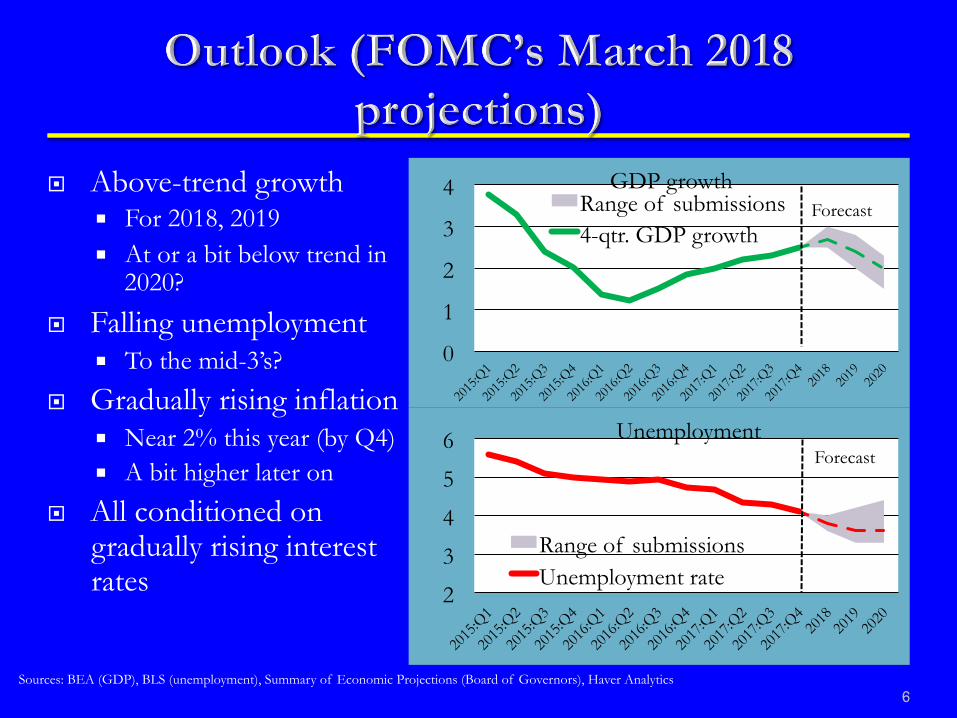

¨ Above-trend growth ¡ For 2018, 2019 ¡ At or a bit below trend in

2020?

¨ Falling unemployment ¡ To the mid-3’s?

¨ Gradually rising inflation ¡ Near 2% this year (by Q4) ¡ A bit higher later on

¨ All conditioned on gradually rising interest rates

6

0

1

2

3

4 GDP growth Range of submissions 4-qtr. GDP growth

2

3

4

5

6 Unemployment

Range of submissions Unemployment rate

Forecast

Sources: BEA (GDP), BLS (unemployment), Summary of Economic Projections (Board of Governors), Haver Analytics

Forecast

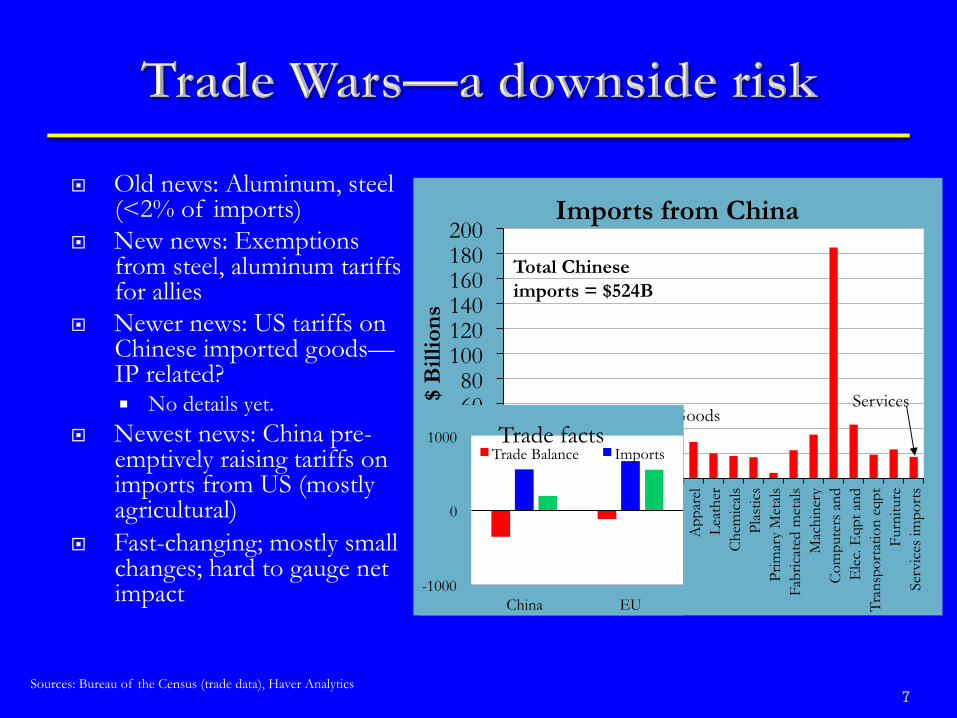

¨ Old news: Aluminum, steel (<2% of imports)

¨ New news: Exemptions from steel, aluminum tariffs for allies

¨ Newer news: US tariffs on Chinese imported goods—IP related? ¡ No details yet.

¨ Newest news: China pre-emptively raising tariffs on imports from US (mostly agricultural)

¨ Fast-changing; mostly small changes; hard to gauge net impact

7 Sources: Bureau of the Census (trade data), Haver Analytics

0 20 40 60 80

100 120 140 160 180 200

Agr

icul

tura

l Li

vest

ock

Fore

stry

Fi

sh

Oil&

Gas

M

iner

als

Food

B

ever

ages

&to

bacc

o Te

xtile

s an

d fa

bric

s A

ppar

el

Leat

her

Che

mic

als

Plas

tics

Prim

ary

Met

als

Fabr

icat

ed m

etal

s M

achi

nery

C

ompu

ters

and

E

lec.

Eqp

t and

Tr

ansp

orta

tion

eqpt

Fu

rnitu

re

Serv

ices

impo

rts

$ B

illio

ns

Imports from China

Total Chinese imports = $524B

Goods Services

-1000

0

1000

China EU

Trade facts Trade Balance Imports

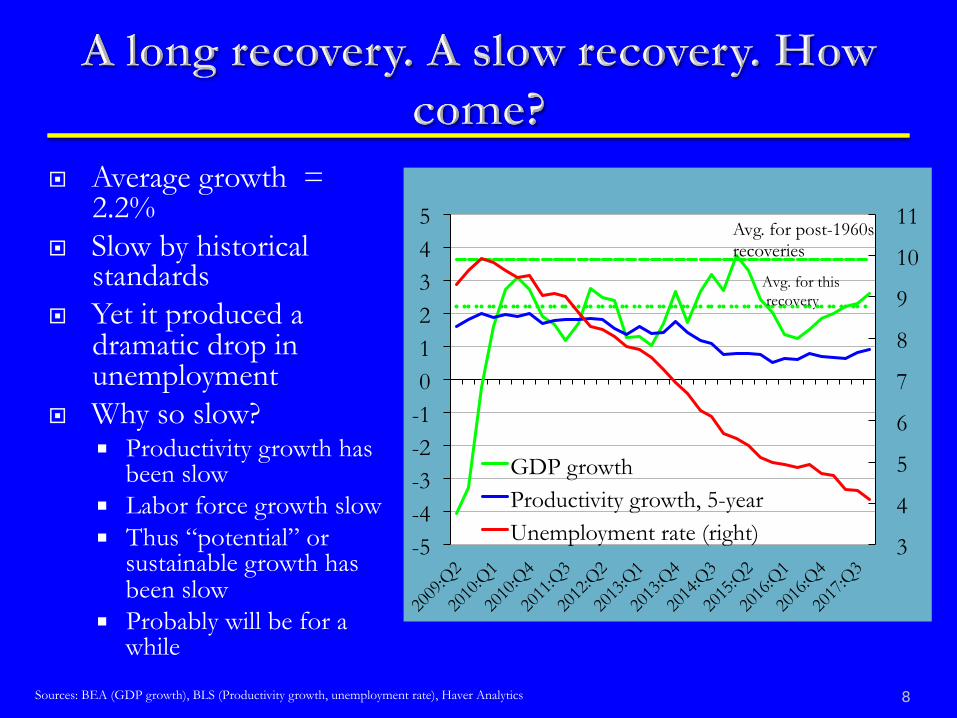

¨ Average growth = 2.2%

¨ Slow by historical standards

¨ Yet it produced a dramatic drop in unemployment

¨ Why so slow? ¡ Productivity growth has

been slow ¡ Labor force growth slow ¡ Thus “potential” or

sustainable growth has been slow

¡ Probably will be for a while

8

3

4

5

6

7

8

9

10

11

-5 -4 -3 -2 -1 0 1 2 3 4 5

GDP growth Productivity growth, 5-year Unemployment rate (right)

Avg. for this recovery

Avg. for post-1960s recoveries

Sources: BEA (GDP growth), BLS (Productivity growth, unemployment rate), Haver Analytics

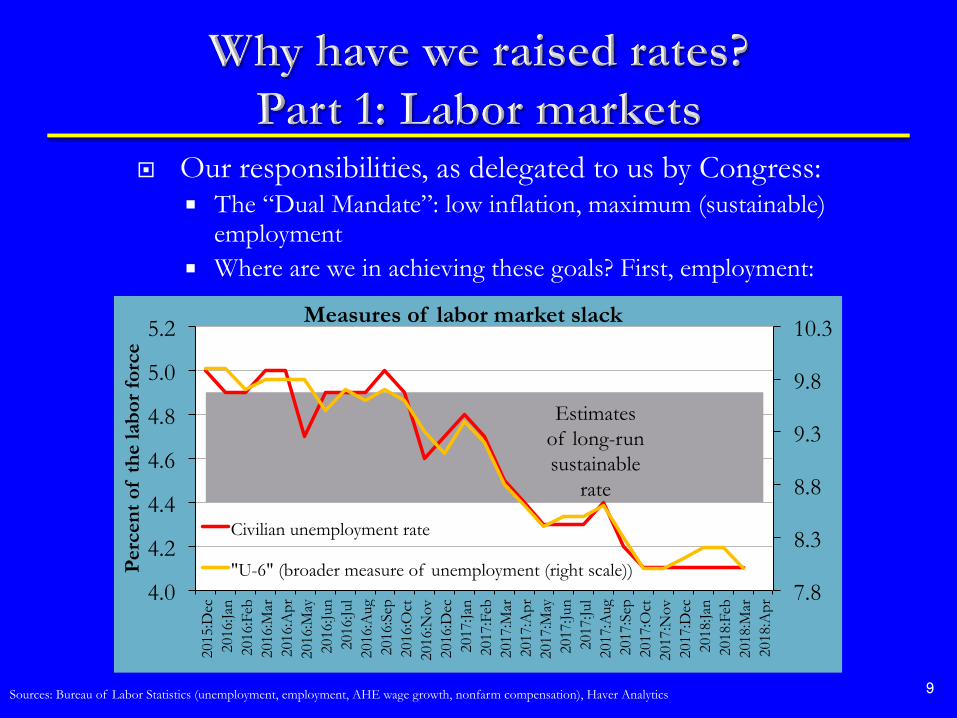

¨ Our responsibilities, as delegated to us by Congress: ¡ The “Dual Mandate”: low inflation, maximum (sustainable)

employment ¡ Where are we in achieving these goals? First, employment:

Sources: Bureau of Labor Statistics (unemployment, employment, AHE wage growth, nonfarm compensation), Haver Analytics 9

7.8

8.3

8.8

9.3

9.8

10.3

4.0

4.2

4.4

4.6

4.8

5.0

5.2

2015

:Dec

20

16:Ja

n 20

16:F

eb

2016

:Mar

20

16:A

pr

2016

:May

20

16:Ju

n 20

16:Ju

l 20

16:A

ug

2016

:Sep

20

16:O

ct

2016

:Nov

20

16:D

ec

2017

:Jan

2017

:Feb

20

17:M

ar

2017

:Apr

20

17:M

ay

2017

:Jun

2017

:Jul

2017

:Aug

20

17:S

ep

2017

:Oct

20

17:N

ov

2017

:Dec

20

18:Ja

n 20

18:F

eb

2018

:Mar

20

18:A

pr

Per

cent

of

the

labo

r fo

rce

Measures of labor market slack

Civilian unemployment rate

"U-6" (broader measure of unemployment (right scale))

Estimates of long-run sustainable

rate

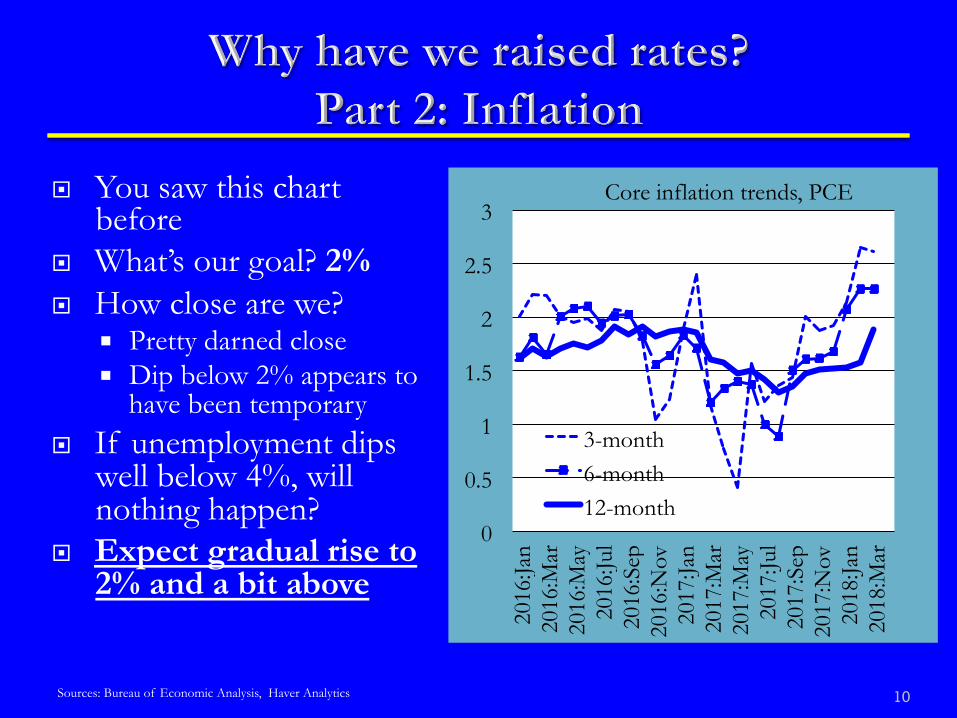

¨ You saw this chart before

¨ What’s our goal? 2% ¨ How close are we?

¡ Pretty darned close ¡ Dip below 2% appears to

have been temporary ¨ If unemployment dips

well below 4%, will nothing happen?

¨ Expect gradual rise to 2% and a bit above

Sources: Bureau of Economic Analysis, Haver Analytics 10

0

0.5

1

1.5

2

2.5

3

2016

:Jan

2016

:Mar

20

16:M

ay

2016

:Jul

2016

:Sep

20

16:N

ov

2017

:Jan

2017

:Mar

20

17:M

ay

2017

:Jul

2017

:Sep

20

17:N

ov

2018

:Jan

2018

:Mar

Core inflation trends, PCE

3-month 6-month 12-month

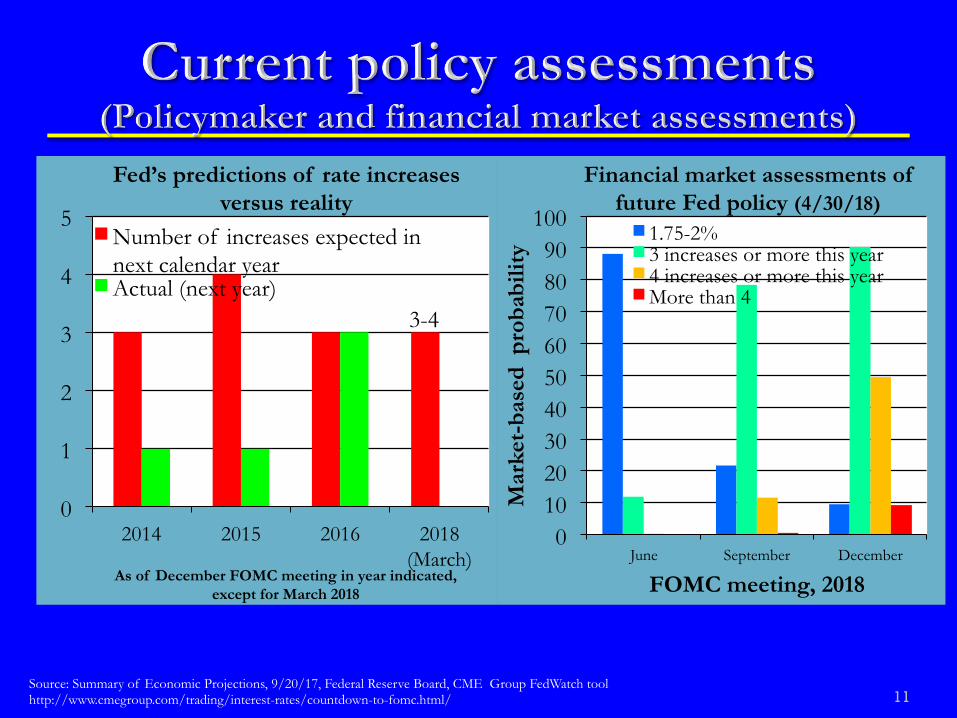

11 Source: Summary of Economic Projections, 9/20/17, Federal Reserve Board, CME Group FedWatch tool http://www.cmegroup.com/trading/interest-rates/countdown-to-fomc.html/

0 10 20 30 40 50 60 70 80 90

100

June September December

Mar

ket-

base

d p

roba

bilit

y

FOMC meeting, 2018

Financial market assessments of future Fed policy (4/30/18)

1.75-2% 3 increases or more this year 4 increases or more this year More than 4

3-4

0

1

2

3

4

5

2014 2015 2016 2018 (March)

As of December FOMC meeting in year indicated, except for March 2018

Fed’s predictions of rate increases versus reality

Number of increases expected in next calendar year Actual (next year)

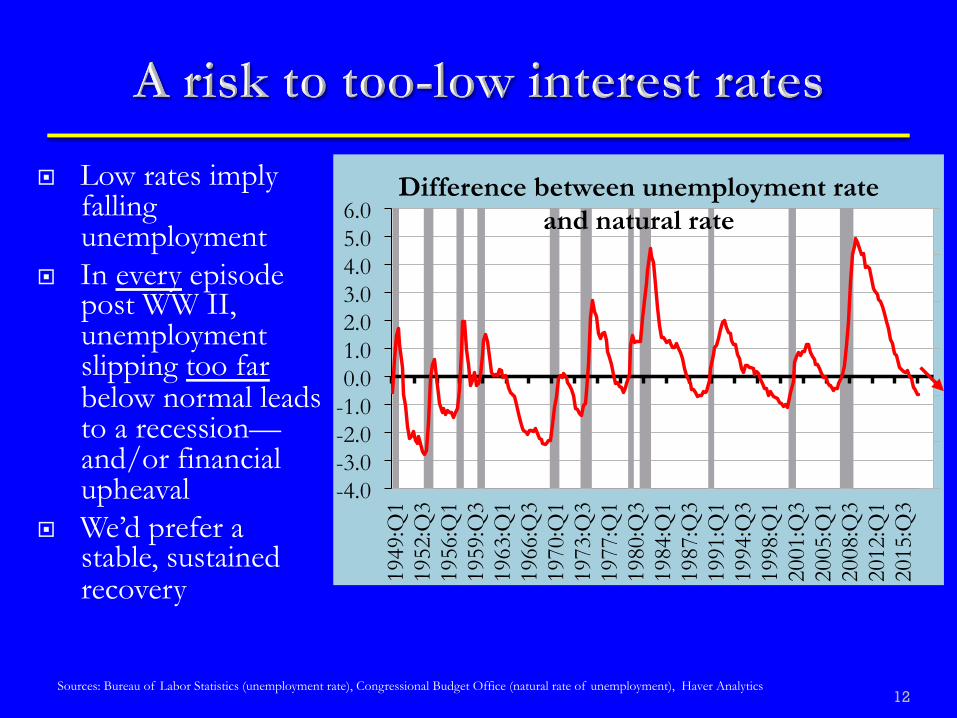

¨ Low rates imply falling unemployment

¨ In every episode post WW II, unemployment slipping too far below normal leads to a recession—and/or financial upheaval

¨ We’d prefer a stable, sustained recovery

-4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0 3.0 4.0 5.0 6.0

1949

:Q1

1952

:Q3

1956

:Q1

1959

:Q3

1963

:Q1

1966

:Q3

1970

:Q1

1973

:Q3

1977

:Q1

1980

:Q3

1984

:Q1

1987

:Q3

1991

:Q1

1994

:Q3

1998

:Q1

2001

:Q3

2005

:Q1

2008

:Q3

2012

:Q1

2015

:Q3

Difference between unemployment rate and natural rate

Sources: Bureau of Labor Statistics (unemployment rate), Congressional Budget Office (natural rate of unemployment), Haver Analytics 12

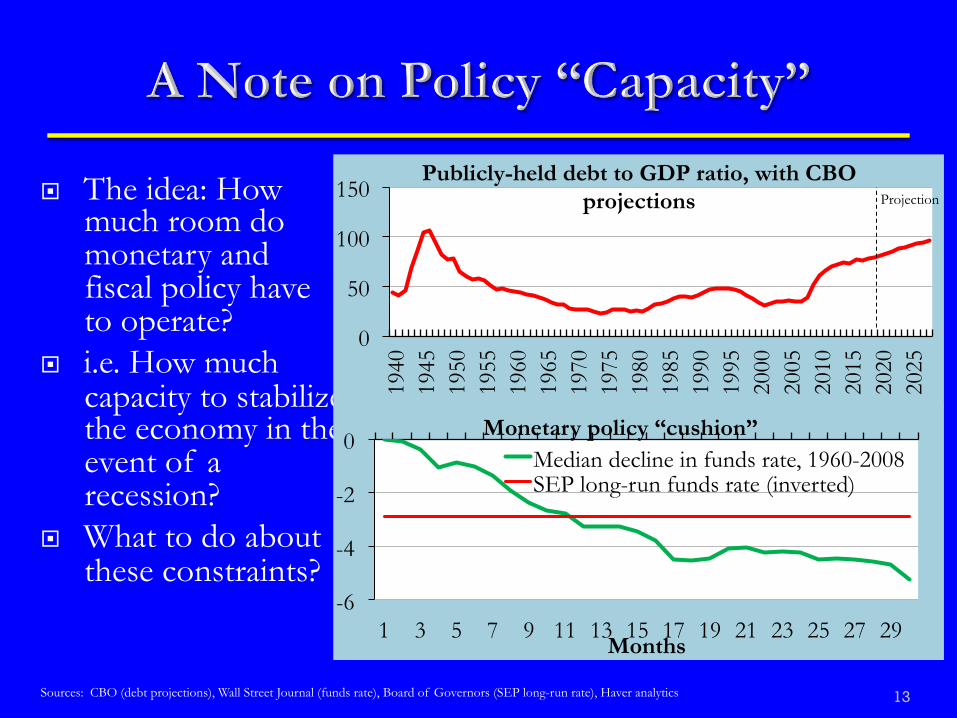

¨ The idea: How much room do monetary and fiscal policy have to operate?

¨ i.e. How much capacity to stabilize the economy in the event of a recession?

¨ What to do about these constraints?

13

0

50

100

150

1940

19

45

1950

19

55

1960

19

65

1970

19

75

1980

19

85

1990

19

95

2000

20

05

2010

20

15

2020

20

25

Publicly-held debt to GDP ratio, with CBO projections Projection

-6

-4

-2

0

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 Months

Monetary policy “cushion” Median decline in funds rate, 1960-2008 SEP long-run funds rate (inverted)

Sources: CBO (debt projections), Wall Street Journal (funds rate), Board of Governors (SEP long-run rate), Haver analytics

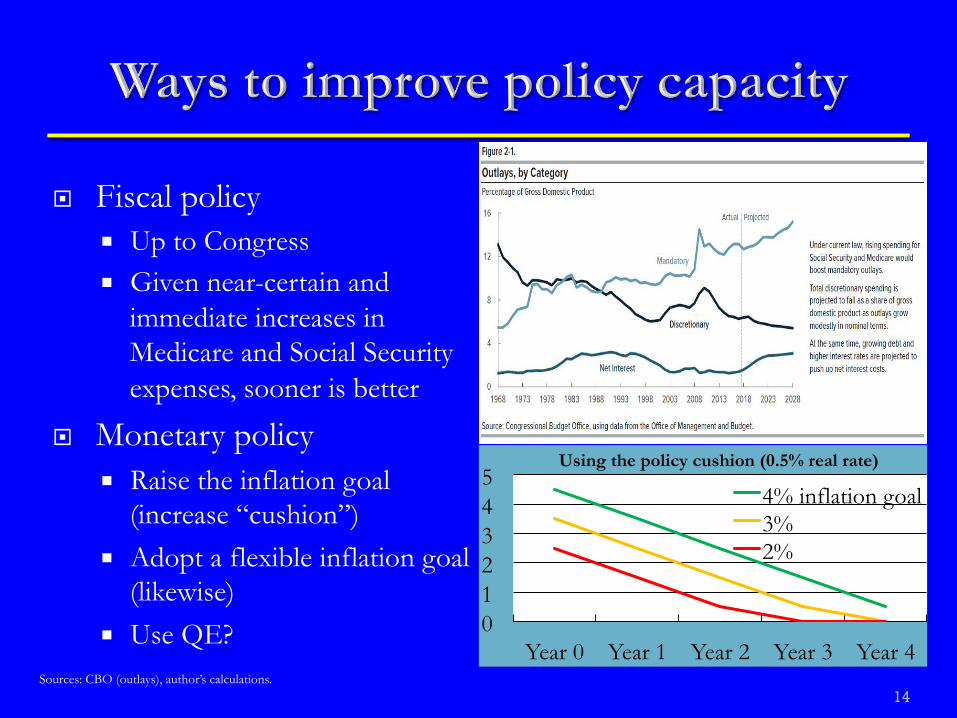

¨ Fiscal policy ¡ Up to Congress ¡ Given near-certain and

immediate increases in Medicare and Social Security expenses, sooner is better

¨ Monetary policy ¡ Raise the inflation goal

(increase “cushion”) ¡ Adopt a flexible inflation goal

(likewise) ¡ Use QE?

14

0 1 2 3 4 5

Year 0 Year 1 Year 2 Year 3 Year 4

Using the policy cushion (0.5% real rate)

4% inflation goal 3% 2%

Sources: CBO (outlays), author’s calculations.

¨ Change at the top ¨ What does it mean?

¡ Mostly, continuity, on ú Monetary Policy, and ú Regulation

¨ Other openings ¡ Vice Chairman of the Board of Governors (Clarida,

new!) ¡ Three other Governor slots (one community banker

nominated!) ¡ President of the NY Fed (Williams, new!)

15

Janet Yellen Jay Powell