Embed Size (px)

Citation preview

THE OFFICIAL JOURNAL OF THE SOCIAL CREDIT SECRETARIAT £1# - - LTHE

For Political and Economic Realism Volume 80 No.2 March - April 2001

THEY DON'T OWE US, WE OWE THEMBy George Monbiot

(This article first appeared in The Guardian newspaper on 20.07.00 and is reproduced with permission of the author)

The banking systems of the firstworld create monstrous injustice.

Between 1503 and 1660, 185,000kilos of gold and 16 kilos of silver wereshipped from Latin America toEurope. The native American leaderGuaicaipuro Cuautemoc argues that

,his people should see this transfer not'-'" as a war crime, but as "the first of

several friendly loans granted byAmerica for European development".Were they to charge compoundinterest on this loan, levied at themodest rate of 10%, Europe wouldowe the indigenous people of LatinAmerica a stack of gold and silverwhich exceeded the weight of theplanet.

Curiously, this deficit is notscheduled for discussion at the G8summit in Japan to-morrow. The debtswhose forgiveness world leaders have

been urged to consider are thosewhich the impoverished nations of thesouth are deemed to owe the north.The seizures of land, labour, mineralsand timber by colonists andcorporations is a debt written offbefore it has even been accounted.The massive "climate change debt" therich owe to the poor remains,officially, invisible.

These injustices are welldocumented. But there is anotheraspect of the debt crisis which hasscarcely been considered. Third worlddebt is a fraud. It is not a debt at all,but the artefact of a deformedaccounting system. In his startling newbook, Goodbye America!, theeconomist Michael Rowbottom showsthat the debt is the inevitable outcomeof the 1944 Bretton Woodsconference. John Maynard Keynes,who led the British delegation, foresawthat unless international trade wasradically overhualed, debt wouldbecome self perpetuating. He proposedan "International Clearing Union" anda new currency, the bancor, in whichinternational transactions would beconducted. Nations would be chargedby the union for both overdrawn andsurplus bancor accounts, encouragingcreditors to spend their excess bancorsin debtor countries, thus swiftlywiping out their deficit.

The United States, by contrast, wasthe world's major creditor and wanted

to keep it that way. Its delegationproposed that nations could borrowfrom an international bank whichwould penalise debtors, but notcreditors. It insisted that gold, valuedin dollars, be used to set exchangerates, ensuring that the dollar becamethe international banking standard.Having threatened to withhold itsforthcoming war loan to Britain, theUS won. It established, through theWorld Bank and the IMF, a globaltrading system which secured both alasting US economic hegemony andthe irredeemable indebtedness ofpoorer nations.

The problem has beencompounded by the growth in"fractional reserve banking": theprocess by which banks create moneyout of nothing by lending far morethan they possess. As governments haveall but ceased to issue real notes andcoins, this magic now accounts forsome 95% of total money supply inmost developed nations. Indebtedness,in other words, has become thenecessary concomitant of moneycreation. This means that the total debtthe people of a nation owe can neverbe repaid. This is why, despite GordonBrown's brave efforts on Tuesday, ourmassive national debt repayments willonly dent the cumulative total. This iswhy our great "property owningdemocracy" has become mortgaged tothe hilt.

VOLUME 80 PAGE 13

THE SOCIAL CREDITER

It also explains why Third worlddebt has become un-payable. Forced totake loans from commercial banks, thedebtor nations create the money whichenables first world countries to sellthem their surplus goods and services.The debt, Rowbottom argues, is theresult not of corruption, incompetenceor economic failure on the part ofdeveloping nations. It is the inexorableand intentional product of a debt-basedfinancial system. The "debt" is no morethan a measurement of the bankingsystem's magical generation of money.

Interestingly, this could mean the"debt crisis" is much easier to solvethan world leaders imagine. As nearlyall money arises from the issue of debt,then debt redemption is largely amatter of accountancy. Were banks

allowed to cancel the debt bonds theyhold, yet keep them on their books,they could balance their accountswithout suffering any losses from theirreserves. It is a fiddle, of course, but afiddle of the kind which already keepsinternational banking afloat, as un-repayable debts are reported at theirfull theoretical value. And were theIMF and the World Bank to bereplaced by a system of the kindKeynes proposed, the mistakes of thepast 50 years could not be repeated.One outstanding task would remain:forgiveness. That we should presumeto 'forgive' the third world's debts islaughable. Rather, G8 leaders must begthe forgiveness of the third world forthe dreadful and deliberate mess theyhave made of the global economy.

«For centuries England has reliedupon protection, has carried it to

extremes, and has obtainedsatisfactory results from it. There is

no doubt that it is to this system that ~it owes its present strength. After two

centuries, England has found itconvenient to adopt free trade becauseit thinks that protection can no longer

offer it anything. Very well then,gentlemen, my knowledge of ourcountry leads me to believe thatwithin two hundred years, when

America has gotten out of protectionall it can offer, it too will adopt

free trade. JJ

General Ulysses S. Grant.

SOCIAL CREDIT: CLEARLY EXPLAINED100 QUESTIONS ANSWERED

By John HargraveFellow of the Royal Society of Arts; Economic Advisor To H.M. Government of Alberta (1936-1937);

Founder and Leader, The Social Credit party of Great Britain. ~(Originally published by SCP publishing house 1945 and to be reprinted, by kind permission, in serial form in The Social Crediter)

THE THREE DEMANDS OFSOCIAL CREDIT

1. Open the National Credit Office.2. Issue the National Dividend.3. Apply the Scientific PriceAdjustment atthe retail end.

Foreword

ALTHOUGH THERE ARE many booksand booklets on the subject of SocialCredit, we are always being asked for"A simple explanation - somethinganyone can understand." Experiencehas shown that the question andanswer method is the only one likelyto be effective in attempting to complywith this request.

This little booklet contains theanswers to 101 Questions about SocialCredit. All of them are real questionsthat have been asked from time to timeat Social Credit party meetings andtalks up and down the country. A teamof Social Credit advocates kindly

undertook to jot down all thequestions usually asked, and sent themto me. Originally, over 400 questionswere dealt with, but this number hashad to be drastically cut owing topaper restrictions.

In compiling the Answers I havehad the help and advice of recognisedSocial Credit technicians, including:

Arthur Brenton, Editor of The NewAge, 1923-38C. Marshall Hattersley, author ofThis Age of Plenty, etc., etc.N.Ridley Temperley, A.M.I.E.E.To these, and a number of others,

who have given very valuableassistance, I offer my sincere thanks. Itshould be clearly understood however,that I alone am responsible for thewording of the answers in thefollowing pages. I also wish to thankMrs. Ashley Lewis for typing theoriginal MS, and Mr. and Mrs IanAlastair Ross for sorting out the mostimportant Questions and arrangingthem in their present sequence.

It must, of course, be left to thegeneral public to determine whetherthis small volume does in fact provide"A simple explanation - somethingthat anyone can understand." That isthe one and only object, but, in ourphase of civilisation, adrift in a sea ofpseudo-scientific jargon and bemusedby a mass of seemingly unrelated"facts", it is the simple logic-tightstatement based upon careful reasoningthat is difficult to grasp.

What the so-called "experts" say isof no consequence whatever - theiropinion is utterly and for everdiscredited by their support of afinancial policy and technique thatcontinually plunges mankind intopoverty and war. We all know that "Anod is as good as a wink to a blind -horse", but if you really do want to,--""understand Social Credit, I hope theseAnswers to Questions may be useful toyou.

VOLUME 80 PAGE 14

J.H.

THE SOCIAL CREDITER

Royal Societies Club, London, 1945.

PART 1 What is Social Credit?

1. WHAT DOES "SOCIALCREDIT" MEAN?IT MEANS (1) a dynamic idea, and (2)the financial technique for putting itinto operation.

The dynamic idea is: that we live ina world of abundance; and thefinancial technique is designed todistribute this abundance.

2. WHO ORIGINATED THESOCIAL CREDIT IDEA, ANDHOW DID HE HIT UPON IT?A SCOTS ENGINEER, Clifford HughDouglas, Maj. R.A.F. (Reserve), bornJanuary 20, 1879, M.l. Mech.E.,M.LE.E., originated the Social Creditidea. He was on the staff of theWestinghouse Company of America;late chief Reconstruction Engineer forthe British Westinghouse Company inIndia; deputy Chief Engineer ofBuenos Aires and Pacific RailwayCompany; Railway Engineer of the

~ London Post Office (Tube) Railway;Assistant Superintendent R.A.F.Factory, Farnborough during the FirstWorld War; witness before theCanadian Banking Enquiry, 1923, andbefore the Macmillan Committee,1930; author of: EconomicDemocracy; Credit Power andDemocracy; Social Credit; TheMonopoly of Credit; WarningDemocracy; etc.

While reorganising the working ofthe Farnborough Aircraft Factoryduring the 1914-18 war, Douglas'scuriosity was aroused by hisobservation that the total costsincurred each week were greater thanthe sums paid out for wages, salaries,and dividends each week.

If it is true, as presumably it mustbe, for all productive businesses, itwould seem to destroy the theoryupon which our whole financialsystem is supposed to work - namely,

~ that all costs are distributedsimultaneously as buying-power.

Douglas collected information fromover a hundred large businesses inGreat Britain, and found that in everycase the total costs incurred each week

were greater than the sums paid out aswages, salaries, and dividends - exceptin businesses heading for bankruptcy.

He published his conclusions in anarticle in the English Review: "That weare living under a system ofaccountancy which renders thedelivery of the nation's goods andservices to itself a technicalimpossibility." The importance of thiswas recognised by very few at the time,but the late A.R.Orage, then editor ofThe New Age, grasped what it meantclearly, and at once invited thediscussion of the idea in his paper.

3. ARE NOT SOCIALISM ANDSOCIAL CREDIT MUCH THESAME?NO, THE DIFFERENCE is fundamentaland clear cut:-

1. Socialism states that the social-economic conflict is capital versusLabour.2. Social Credit states that thesocial-economic conflict is Financeversus the Community.The fight between two rats shut in

a trap is not "much the same thing" astheir quarrel with the rat-catcher. It istotally different.

(Capital and Labour are the rats inthe trap. Finance-capital - the MoneyPower - is the rat catcher.)

4. IS IT NOT A FACT THATSOCIAL CREDIT HAS BEENTRIED IN ALBERTA ANDFAILED?NO. IT IS NOT. I went to Alberta in theWinter of 1936-37 to see for myselfwhat was happening, and acted asEconomic Adviser to the AlbertaGovernment Planning Committee.(see The Alberta Report, issued by theSocial Credit Party of Great Britain,1937.) I found that it was not SocialCredit that had failed - but the attemptto introduce it, a very different thing.

In August, 1935, the people ofAlberta voted for William Aberhartand his Social Credit Party, and thisresulted in a landslide victory for SocialCredit. During the next five years theAberhart Government struggled to beallowed to introduce Social Credit. In1940, when the Aberhart Governmentwas nearing the end of its term of

office, another general election washeld. All political wiseacres predictedthat Aberhart and his governmentwould be swept out. Yet in spite of fiveyears of not being allowed to introduceSocial Credit, the people of Albertawent to the polls - returned Aberhart andhis Social Credit Government for another

five years, with a strong working majority!And this Government, now led byPremier Manning, again went to thepolls in the autumn of 1944, and wasreturned with an even greater majority,gaining 51 seats out of a total of 57.Yet despite this Provincial majorityAlberta is still struggling to introduceSocial Credit in accordance with themandate of the people.

So far, every attempt to implementSocial Credit in the Province has beenthwarted and prohibited as"unconstitutional."

Thus, for example, the AlbertaLegislature passed the following Bills:-

1. "Credit of Alberta RegulationAct." - Disallowed by the DominionGovernment, Ottawa, August 17th1937.

2. "Bank Taxation Act." - Assentwithheld by Lieutenant-Governor.Declared unconstitutional by SupremeCourt of Canada. Appeal by Provincefrom Supreme Court decision to PrivyCouncil dismissed.

3. "Reduction and Settlement ofDebt Act." - Declared ultra vires of theProvince by the Courts.

4. "Act to Ensure Publication ofAccurate News Information." - Assentwithheld by Lieutenant-Governor.Declared unconstitutional by Supreme

"It has always seemed to me acurious fact that money isforthcomingin any quantity for a war, but that no

nation has ever yet produced themoney on the same scale tofight the

evils of peace - poverty, lack ofeducation, unemployment, ill health.

When we are prepared to spendmoney and our Worts against them as

freely and with the same spirit asagainst Hitler - we shall really be

making progress. JJ

Field Marshall Lord Wavellat a Pilgrim's luncheon,

September 16, 1943.

VOLUME 80 PAGE 15

THE SOCIAL CREDITER

Court of Canada. In the appeal by theProvince from the Supreme Court'sdecision, the Privy Council refused tohear Alberta's argument by theircounsel.

5. "Home Owners Security Act." -Disallowed by Dominion Government,Ottawa, June 15 1938.

6. "Security of Tax Act." -Disallowed by Dominion Government,Ottawa, June 15 1938.

7. "Credit of Alberta RegulationAct (1937 Amendment)." - Assentwithheld by Lieutenant-Governor.Declared unconstitutional by SupremeCourt of Canada. In the appeal by theProvince from the Supreme Court'sdecision, the Privy Council refused tohear Alberta's argument by theircounsel.

The truth is that democracy hasbeen denied to the people of Albertaby the Money Power.

5. WHAT IS THE BASIS OFTHE SOCIAL PHILOSOPHY OFSOCIAL CREDIT?THAT THE INDIVIDUAL is the allimportant unit. And that the onlyjustification for the existence of anyorganisation - from football team tothe State itself - is that it helps in someway the life and wellbeing of theindividual.

6. WHAT IS THE SOCIALCREDIT IDEA STATED ASSIMPLY AS POSSIBLE?THAT THE ONLY object ofProduction is Consumption, and that,of all the interests seeking satisfactionin the State, the interest ofCONSUMERS shall be paramount.You are a consumer. So am 1. We areall consumers.

In a modern community it is notdifficult to produce enough and tospare for everyone. Social Credit is aneconomic technique for giving youyour share of the things you want -including time to enjoy life, andtherefore culture.

Social Credit does this by allowingConsumption to keep pace withProduction - i.e. by seeing that totalConsumer Incomes balance totalRetail Prices all the time.

Social Credit is, in reality, a

"But where's the money tofi ;l JJcome rom ....

A chorus of mass ignorance supportedby "experts", hack journalists, and

bankers' yes-men.

technique for allowing people theopportunity of living the Good Life -of living splendidly, instead ofdrudging and money-grubbing andsnatching. You know what you wantout of life - Social Credit makes itpossible for you to get it.

7. STATED SIMPLY,WHAT DIDDOUGLAS DISCOVER - ANDHOW DID HE PRESENT IT?HE DISCOVERED (1) that there is, inpeace time, a chronic shortage ofconsumer buying-power, and (2) howthis shortage can be corrected so thatpeople can buy all the goods andservices that are ready for sale at anygiven moment.

He presented the Social credit ideain a twofold manner:-1. AN ANALYSIS OF COSTING,which has become known as the "A +B Theorem".2. A SET OF PROPOSALS, of whichthe essentials are:-

(i) The establishment of a CreditAuthority or National Credit Office.

(ii) The debt-free financing of theconsumer apart from the employmentsystem.

(iii) The application of theScientific Price Adjustment at the retailend; and

(iv) New credits for newproduction.

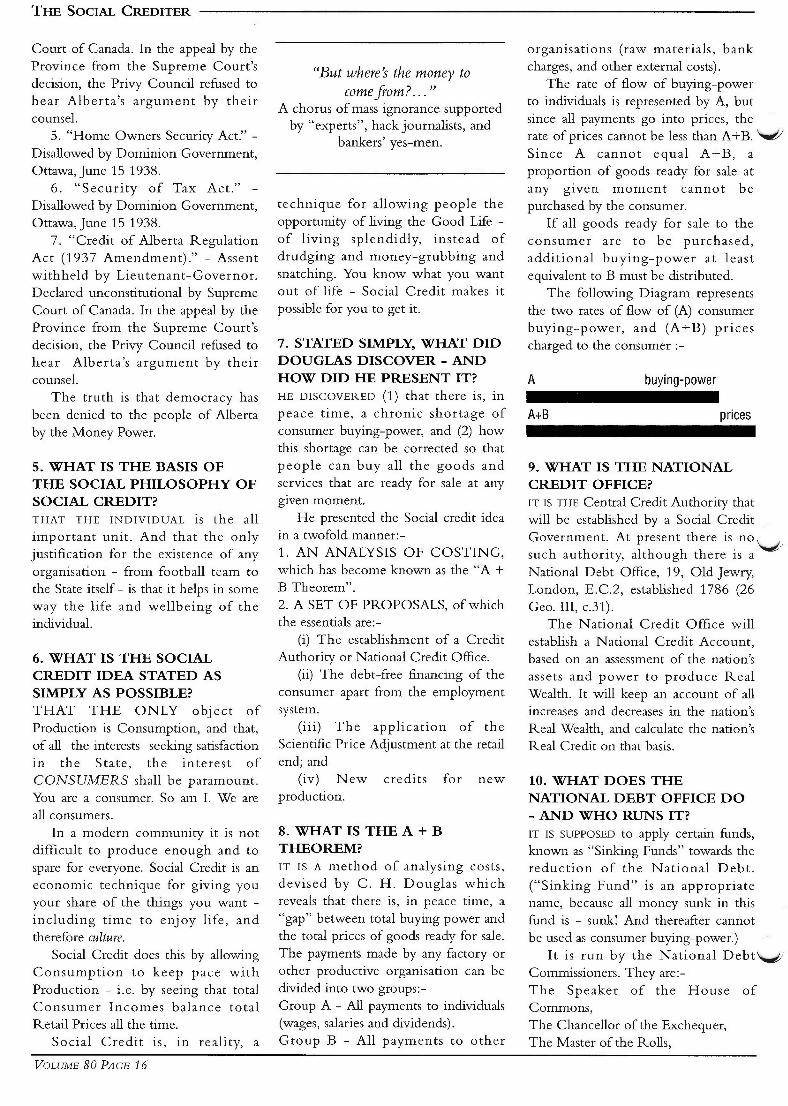

8. WHAT IS THE A + BTHEOREM?IT IS A method of analysing costs,devised by C. H. Douglas whichreveals that there is, in peace time, a"gap" between total buying power andthe total prices of goods ready for sale.The payments made by any factory orother productive organisation can bedivided into two groups:-Group A - All payments to individuals(wages, salaries and dividends).Group B - All payments to other

organisations (raw materials, bankcharges, and other external costs).

The rate of flow of buying-powerto individuals is represented by A, butsince all payments go into prices, therate of prices cannot be less than A+B. ~Since A cannot equal A +B, aproportion of goods ready for sale atany given moment cannot bepurchased by the consumer.

If all goods ready for sale to theconsumer are to be purchased,additional buying-power at leastequivalent to B must be distributed.

The following Diagram representsthe two rates of flow of (A) consumerbuying-power, and (A +B) pricescharged to the consumer :-

A buying-power

prices

9. WHAT IS THE NATIONALCREDIT OFFICE?IT IS THE Central Credit Authority thatwill be established by a Social CreditGovernment. At present there is no ~.,such authority, although there is aNational Debt Office, 19, Old Jewry,London, E.C.2, established 1786 (26Geo. III, c.31).

The National Credit Office willestablish a National Credit Account,based on an assessment of the nation'sassets and power to produce RealWealth. It will keep an account of allincreases and decreases in the nation'sReal Wealth, and calculate the nation'sReal Credit on that basis.

10. WHAT DOES THENATIONAL DEBT OFFICE DO- AND WHO RUNS IT?IT IS SUPPOSED to apply certain funds,known as "Sinking Funds" towards thereduction of the National Debt.("Sinking Fund" is an appropriatename, because all money sunk in thisfund is - sunk! And thereafter cannotbe used as consumer buy.ing-power.)

It is run by the National Debt~Commissioners. They are:-The Speaker of the House ofCommons,The Chancellor of the Exchequer,The Master of the Rolls,

VOLUME 80 PAGE 16

THE SOCIAL CREDITER

The Lord Chief Justice,The Paymaster-General, andThe Governor and Deputy Governorof the Bank of England.

11. SURELY THE TREASURYHASCONTROLOVERTHEBANK OF ENGLAND?You WOULD THINK SO, but it has not.The Treasury is "advised" by the Bankof England - in actuality, by theGovernor - and always follows that"advice". Any Chancellor of theExchequer who did not do so wouldfind himself in Queer Street veryquickly. This was so even in the timeof Gladstone, and it is much more sotoday.

Gladstone wrote: "From the time Itook office as Chancellor of theExchequer (1852) I began to learn thatthe State held, in the face of the Bankand the City, an essentially falsepositron as to finance. TheGovernment itself was not to be thesubstantive power, but was to leave theMoney Power supreme and unques-tioned. In the conditions of thissituation I was reluctant to acquiesce,and I began to fight against it byfinancial self assertion from the first. Iwas tenaciously opposed by theGovernor and the Deputy-Governorof the Bank (of England) who hadseats in Parliament, and I had the Cityfor an antagonist on almost every

. "occasion.(Morley's "Life of Gladstone")

"On one memorable occasion theGovernor of the Bank (Mr. MontagueNorman) was asked the relationship ofthe Court of Directors (of the Bank)and the Treasury. He replied that it wasthe relationship of Tweedledum andTweedledee."

(Lord Strathbolgi, thenLt-Commander Kenworthy,

in the New Leader,October 9, 1931.)

12. WHAT IS THE NATIONALDIVIDEND AND WHY IS IT

~REQUIRED?IT IS THE method whereby everycitizen will become a birthrightshareholder in the common wealth ofthe community.

The National Dividend is the

share-out mechanism of a modernPower-Age society. It will be paid as aflat rate to everyone - rich or poor -who chooses to draw it. It will bebased on the total productive capacityof the community, and will rise and fallwith production. It will be paid over andabove the wages and salaries of thoseengaged in production.

By means of the National Dividendand the Price Adjustment the HomeMarket will be made effective, whichmeans that the people of this countrywill be able to buy the goods andservices ready for sale.

It eliminates the miserable, miserlyunemployment "dole" and ensures toeveryone economic security - ANDfreedom. Economic security withoutfreedom is Totalitarian Serfdom - theServile State.

A National Dividend is requiredbecause we - by which I mean we inthis country - have left behind aScarcity-and- Work Age and haveentered an Abundance-and-LeisureAge, in which more and more goodsand services can be produced with lessand less human Labour. A Power-Agesociety, using modern productivetechnique - i.e. labour-saving devicesof all kinds - does not need the labour-power of a very large number of"workers" who were requiredheretofore. The National Dividend -the "Wages of the Machine" - isneeded in order (a) to free industryfrom being clogged with unwanted"workers" seeking jobs in order to getmoney, and (b) to enable these released"work-wage-slaves" to buy and use thegoods and services that can be mademore efficiently without their labour.Without the National Dividend amodern community is bound to havean ever-increasing horde of poverty-stricken unemployed.

There is no solution in the ideathat "everyone could be employed fora few hours a day," because beforelong only a few will be required towork even a few hours a day! Thesefew - a highly skilled minority ofproduction technicians - ought to bepaid for their services to thecommunity over and above theNational Dividend. That is the onlylogical solution to this Power-Age

"problem" which is not really aproblem at all, but a fear of leisurehangover from the Ages of Scarcity. ASocial Credit Government will,however, leave this question to besettled by the community. If amajority decide that "everyone mustdo his or her quota of work", such awork-decree will come into force. Butafter a time, sooner or later, peoplewill discover that the common-senseplan is for those to work who are bestable to do the job, and who lovedoing it.

13. WHERE IS THE MONEY TOCOME FROM?FROM THE NATIONAL Credit Officewhere it will be created by entering upthe financial value of the Nation'scredit - i.e. its ability to produce RealWealth (goods and services).

People ask: "Where is the moneyto come from?" - as though moneywere some kind of Sacred Ju-Ju-Magic. That of course is nonsense.Money - i.e., Credit - is created byBankers "out of nothing" and at verylittle cost; and banking is, in fact, firstof all a money-creating and then amoney-lending business. But, in aSane Economic System, money willnot be a commodity. It will be merelytickets-for-goods, having no specialvalue itself.

14. WHAT IS THE PRICEADJUSTMENT, AND WHY ISIT REQUIRED?IT IS a calculation designed to "closethe gap" between the total buying-power of individuals and the totalprices of goods ready for sale. Bymeans of this calculation goods will besold to the consumer below cost (asnow calculated). The technical formulacan be set out as follows:-

Cost: Price: : Production: Consumption. . . Price per ton =

Cost per ton x

Cost value of TotalConsumption

Money value of TotalConsumption

A simple explanation of thisformula is: that the scientific price ofany article to the consumer is the cost

VOLUME 80 PAGE 17

THE SOCIAL CREDITER

of consumption ("using up" of otherarticles) during the period ofproduction.

Anyone can see that this is plaincommon sense, without necessarilybeing able to understand the formulaitself.

It is required (1) to counteractinflation, and (2) to regulateproduction in relation to consumerdemand.

The price adjustment at the retailend is the most important part of theSocial Credit technique. It eliminatesthe "boom" and "slump" of theBankers' Debt-system. In effect, it islike the governor on an engine. Itregulates the flow of buying-power inrelation to production. It makes surethat total spendable incomes equal totalretail prices. That means that peoplecan buy the goods and servicesproduced and offered for sale.

15. WHAT DO ECONOMICEXPERTS THINK ABOUTSOCIAL CREDIT?THERE ARE NO "economic experts"because economics as preached byorthodox economists is not a sciencebut a mystagogy wrapped in a pseudo-technical jargon.

Those who call themselves, or aresupposed to be "economic experts"usually consider that Social Credit is"based upon a fallacy".

16. WHAT IS THE "FALLACY"THESE "ECONOMICEXPERTS" THINK THEYDISCOVER - AND WHAT ISTHE SOCIAL CREDIT REPLY?THAT AS "B" costs have been paid outas wages, salaries, dividends or profitsin the past, they are available asconsumer buy.ing-power in the present;and that therefore the public has all themoney needed to buy all the goodsand services ready for sale to the finalconsumer.

The Social Credit reply is: that themoney spent yesterday cannot be spentagain today. A spent coin is like a spentbullet - and so is a spent £1 or lOs.note. "A" costs become "B" costs, but'B" costs never become "A" costsagain. It is no use one addingtogether:-

1. Money spentyesterday

2. Money ready tospend to-day

£10 ("8" Costs)

£10 (UA" Costs)

Falling Down! Please give yourpennies to our Rebuilding Fund." Thiscan lead to a state of affairs in whichthe community is so unprepared in theorganisation, equipment, and trainingof its Army, Navy and Air Force, that '-f)it is in danger of being attacked,blockaded, starved out, and invaded.Britain was in that position in 1939.And we shall be in the same positionagain in a few years after this Hitler-war - if we allow the Bankers to keepus sunk in debt. "Out of debt, out ofdanger", says the old proverb, and verytrue it is.So, you see, now, why Social Creditadvocates are so much against theBankers?

18. IS THERE ANY EVIDENCETO SHOW THAT BANKERSAND FINANCIERS WIELD ALIFE-AND-DEATH POWEROVER THEIR FELLOW MEN?PLENTY. I could compile a large bookfull of it. Here are a few of the"exhibits" that would be included: -

(1) From The Financial Times,September 26, 1921: "Whoever may ~ ..be the indiscreet Minister who revivesthe money-trust bogy at a momentwhen the Government (LloydGeorge's) has most need to be polite tothe banks, should be put through anelementary course of instruction, infact, as well as in manners. Does he, dohis colleagues, realise that half a dozenmen at the top of the big five bankscould upset the whole fabric ofGovernment finance by refrainingfrom renewing Treasury Bills?"

(2) Meyer Rothschild, father of theHouse of Rothschild and founder ofthe great chain of banking housesthroughout the world, said: "Permitme to issue the money of a nation andI care not who makes its laws."

(3) From the United States Banker'sMagazine of 1892: "We must proceedwith caution, and guard well everymove made, for the lower orders ofpeople are already showing signs ofrestless commotions. Prudence will, Vtherefore, dictate a policy of apparentlyyielding to the popular will until allour plans are so far consummated thatwe can declare our designs withoutfear of any organised resistance. The

VOLUME 80 PAGE 18

£20

- and pretending that you now have£20 with which you can buy goodspriced at £20, when in fact all younow have is £10, and it cannot buygoods priced beyond that sum. Thus,you cannot spend today what youspent yesterday - and this applies toeach individual, and to all groups ofindividuals.

17. WHY ARE SOCIAL CREDITADVOCATES SO MUCHAGAINST BANKERS?BECAUSE THE BANKERS operate asystem that places the wholecommunity in financial debt to themand forces the community to go onborrowing from them."Well", you may say, "is there anythingwrong about that?" The answer is :Yes,very wrong. You know that anindividual who is in debt financially isalways under the thumb of someoneelse - i.e., the person from whom hehas borrowed. That is why mostpeople try not to "get into the handsof moneylenders" - little knowing thatthey are in the hands of moneylenders(the Bankers) from the day they areborn, and even before.

A community that is in debtfinancially is under the thumb ofsomeone else- i.e., the Bankers fromwhom they borrow their own credit.The results of this are extremelydangerous. Suppose the communityneeds ships, or the development ofagriculture, or new schools andhospitals. Instead of setting to work tomake and do these things, they are toldand come to actually believe, that "thecost is prohibitive" - in spite of the factthat, quite obviously, what is physicallypossible, is, and must be, financiallypossible. And so, because of the Mythof Financial Debt, they let theirshipyards stand idle, let their fields andfarms go to rack and ruin, let theirchildren go to schools that ought to bepulled down, and put up noticessaying: "The So-and So Hospital is

THE SOCIAL CREDITER

Farmers' Alliance and the Knights ofLabour organisations in the UnitedStates should be carefully watched byour trusted men, and we must takeimmediate steps to control theseorganisations in our interests or disruptthem. The coming OmahaConvention, to be held July 4th., ourmen must attend and direct itsmovements, or else there will be set onfoot such antagonisms to our designs asmay require force to overcome. This,at the present time, would bepremature. We are not yet ready forsuch a crisis. Capital must protect itselfin every possible manner throughcombination and legislation. Thecourts must be called to our aid. Debtsmust be collected, bonds andmortgages foreclosed as rapidly aspossible. Where, through a process oflaw, the common people have losttheir homes, they will be moretractable and easily governed throughthe influence of the strong arm ofgovernment, applied by central powerof imperial wealth, under the controlof leading financiers. The truth is well

~ known among our principal men nowengaged in forming an imperialism ofcapital to govern the world. Whilethey are doing this the people must bekept in a condition of politicalantagonism. The question of tariffreform must be urged through theorganisation known as the DemocraticParty, and the question of protectionand reciprocity must be forced to viewthrough the Republican Party. By thusdividing the voters we can get them toexpend their energies fighting overquestions of no importance to us,except as teachers to lead the commonherd. Thus by discreet actions we cansecure all that has been so generouslyplanned and successfullyaccomplished."

(4) Extracts from a letter writtenfrom London by the firm ofRothschild, well known internationalbankers, to their New York Agents,when arranging to introduce modern

~ banking methods into America. "Thefew who can understand the systemwill either be so interested in itsprofits, or so dependent on its favours,that there will be no opposition fromthat class, while, on the other hand,

that great body of people, mentallyincapable of comprehending thetremendous advantage that Capitalderives from the system, will bear itsburden without complaint and,perhaps, without even suspecting thatthe system is inimical to theirinterests."

19. IS IT BANKERS, OR THESYSTEM THEY OPERATE,THAT SOCIAL CREDITADVOCATES WISH TOABOLISH?THEY WISH TO abolish the debt-generating system operated by thebankers. By abolishing financial debt,Social Credit will so modify the systemas to remove the evils that inevitablyresult from its present operation.

Under Social Credit the Bankerswill be required by law to operate adebt-free monetary system, and, bythus modifying the technique ofcredit-accountancy, Social Credit willentirely "evaporate" the power of theBankers, confining them to theirproper work, which is: to act as thebookkeepers of the nation's Productionand Consumption.

20. IS IT A FACT THAT BANKSCREATE CREDIT "OUT OFNOTHING"?YES, I'M AFRAID it is. It's hard luck forthe so-called "economic experts" whomade fools of themselves at the outsetof the Social Credit revelation byasserting that "banks do not createcredit out of nothing". The "banks donot create credit", and that "banks canonly lend the money deposited withthem by their customers". The facts,however, are otherwise, as you willsee:-Encyclopaedia Britannica, vol. 15, under"Money": "Banks lend by creatingcredit; they create the means ofpayment out of nothing."

Encyclopaedia Britannica (14th.edition), vol. 3, under "Banking andCredit": "Banks create credit. It is amistake to suppose that Bank Credit iscreated to any important extent by thepayment of money into the banks."

William Paterson, born 1658, theScots economist and financier, whofounded the so-called "Bank of

England" said, in explaining hisscheme at the time: "The Bank hathbenefit of interest on all moneys whichit creates out of nothing."

R. G. Hawtrey, Assistant Secretaryto the Treasury, in a B.B.e. broadcast,March 22, 1933, said: "I agree withhim (Douglas) that Banks createmoney, and that trade depression arisesfrom faults in the Banking System inthe discharge of that vital function .."

The late Reginald McKenna,Chairman, the Midland Bank, and exChancellor of the Exchequer,addressing the shareholders of theMidland Bank, January 29, 1920, said:"When a bank makes a loan to acustomer or allows him an overdraft inthe ordinary course the loan will bedrawn upon, or the overdraft will bemade, by cheque drawn by thecustomer upon the bank and paid in tosomeone's credit at the same oranother bank. The drawer of thecheque will not have reduced anydeposit already in existence because weare supposing a case in which he hasbeen given a loan or allowed anoverdraft. The receiver of the cheque,however, when he pays it into his ownaccount, will be credited with its valueand thereby a new deposit will becreated."

Addressing the shareholders of theMidland Bank, January 25, 1924, thelate Reginald McKenna said: "I amafraid the ordinary citizen will not liketo be told that the banks can, and do,create money. The amount of moneyin existence varies only with the actionof the banks in increasing anddecreasing deposits and bankpurchases. Every loan, overdraft, orbank purchase creates a deposit, andevery repayment of a loan, overdraft,or bank sale destroys a deposit."

Addressing the shareholders of theMidland Bank, January 22, 1930, thelate Reginald McKenna said: "TheBank of England is the supremeauthority in determining the quantityof money available for the use of thepublic."

The Report of the MacmillanCommittee, 1929, page 34, para. 74,states: "It is not unnatural to think ofthe deposits of a bank as being createdby the public through the deposit of

VOLUME 80 PAGE 19

THE SOCIAL CREDITER

cash representing either savings oramounts which are not for the timebeing required to meet expenditure.But the bulk of the deposits arise outof the action of the banks themselves,for by granting loans, allowing moneyto be drawn on an overdraft, orpurchasing securities, a bank creates acredit in its books which is equivalentto a deposit ... The bank can carry onthe process of lending, or purchasinginvestments, until such time as thecredits created, or investmentspurchased, represent nine times theamount of the original deposit."

In his great textbook, The Theory

and Practice of Banking, H.D. McLeod,M.A., a recognised authority on thesubject, states: "The essential anddistinctive feature of a bank and abanker is to create and issue creditpayable on demand, and this credit isintended to be put into circulation andserve all the purposes of money. Abank, therefore, is not an office for theborrowing and lending of Money, it isa manufactory of credit."

A.L.G. Mackay, Professor ofEconomics, University of Rangoon,states: "By means of a loan, anadvance, an overdraft, or by thecashing of bills, the banks are able to

increase the volume of deposits in thecommunity, and because of this processit is not correct to say that a bank loansout deposits which people make withit. It is clear that it creates the depositby the issue of the loan; the loan travels~back to the bank, or another bank, andassumes the form of a deposit."

Branch Banking, July, 1938, stated:"There are enough substantialquotations in existence to prove to theuninitiated that Banks do create creditwithout restraint and that they createthe means of repayment withinthemselves."

(To be continued)

IT'S YOUR MONEYBy William F. Hixson

Continuing our periodic reprinting, with permission, of excerpts from William E Hixson's small book with theabove title. Chapters 11 and 12 seem highly relevant as international indebtedness and volatility in international

financial markets are greatly increased. In the Preface to his book Hixson confirms, and we agree, that "This bookis about 'YOUR MONEY' no matter in what country you reside. It may at first appear to be solely about the

monetary system of the USA but the systems are so similar in all countries that most of what is written here aboutthe USA applies everywhere."

Chapter 11

THE MOST COMMONFALLACY ABOUT BANKING

PRECEDING CHAPTERS HAVE DEALT

with certain aspects of the process bywhich bank-created money has comeinto existence in the past and presentlycomes into existence in our economy.Much remains to be said, however,about both the banking system andabout the properties of Bank-CreatedMoney.

The most persistent misunder-standing about banks is the belief that,first, individuals or companies makedeposits in banks and that,subsequently, the banks loan out toborrowers the depositors' money.

Put another way, the mostpersistent fallacy about banking is thatbanks are "intermediators" betweenlenders and borrowers. This does notat all reveal the way the system actuallyworks.

Between 1950 and 1990 the totaldeposits in the commercial banks of

the USA increased by about $2500billion. We must now considerpreviously unexplored aspects of theprocess by which this enormousincrease in bank deposits came about.

As contrary as it may be to what isgenerally believed and as strange as itmay at first seem, the $2500 billionincrease in deposits did not comeabout because of deposits made byindividuals and companies thatconstitute "the public." For the mostpart, the increase in deposits cameabout because banks created depositsin the course of making loans. Thecardinal function of banks is not"intermediation" but money-creation.

Coming to an understanding ofthis must begin with the obvious factthat "the public" can deposit money inthe banking system in only two ways:1) by depositing legal tender, or 2) bydepositing checks. But the $2500billion increase in bank deposits didnot come about in either of these twoways and therefore did not comeabout because of deposits made by thepublic. Let us consider in turn and in

more detail these two ways.Every day members of the public

deposit legal tender in banks andwithdraw legal tender from banks. Onaverage and in the long run, however,the public withdraws vastly more legaltender from banks than it deposits inthem. Except for some freakishcoincidence quickly offset, thedeposits of the banking system neverincrease because the public depositsmore legal tender than it withdraws.This is easily comprehended once oneis reminded of the fact that between1950 and 1990, for example, theamount of Currency Held by thepublic increased by $229 billion. Thisis the amount of more currencywithdrawn from the banking systemby the public than the amountdeposited in it by the public.

Let us assume an average of 250banking days per year for the four~decades or 10,000 days total. Dividingthe $229 billion by 10,000 gives $22.9million. This is the average amountmore cash per day that peoplewithdrew from banks than they

VOLUME 80 PAGE 20

THE SOCIAL CREDITER

deposited with them. This may soundlike an astonishing amount of netwithdrawal of cash each banking daybut it averages only 11c or 12c morewithdrawn than deposited per day perIadult citizen of the USA. And so, torepeat, the deposits of the bankingsystem did not increase by the $2500billion because of deposits of legaltender by the public.

N or did the deposits of thebanking system increase by the $2500billion because of deposits of checksby the public.

The deposit of a check may, ofcourse, increase the deposits of thebank in which it is deposited. But itwill decrease the deposits of the bankon which it is drawn by precisely thesame amount. The total deposits of thebanking system, considered as a whole,will remain unchanged - will not at allincrease. And so, to repeat, thedeposits of the banking system did notincrease by the $2500 billion becauseof deposits of checks by the public.

If the $2500 billion increase indeposits of the banking system did not

vcome about as a result of deposits (cashor check) by the public, and itabsolutely did not, then how, indeed,did it come about? For the most part,it came about by banks creatingmoney as they created deposits in thename of the borrower in the process ofmaking loans. By far the greater partof what we call "the nation's moneysupply" is bank deposits that werecreated by banks as they made loans.

The capability or capacity of thebanking system to create deposits onsuch a large scale, however, depended,in turn, on the Fed creatingNotes/Credits year after year, gettingthe money it created deposited in thebanking system, and thereby increasingdeposits and, in turn, increasing thereserves of the banking system.

As earlier noted, from 1950 to1990, for example, the Fed created$277 billion in legal tender and used itto purchase government bonds and

~other securities. All the $277 billionoriginally got deposited in the bankingsystem. The public gradually withdrew$229 billion. Forty-eight billion dollarsremained in banks, increased thereserves of the banking system, and

thus increased the capacity of thebanking system to make loans. Everylast cent of the net increase in thecapacity of the system to make loanscame from the Fed. None of it camefrom deposits of legal tender by thepublic or the deposit of checks by thepublic.

Readers will observe that I saidabove that "for the most part" the$2500 billion increase in deposits cameabout by banks creating money as theycreated deposits in the name of theborrower in the process of makingloans. The increase in deposits cameabout "in small part" because bankscreate deposits by lending their capitalas well as by lending money theycreate. I estimate that between 1950and 1990 less than $150 billion of theincrease in deposits held by the publicwas due to the lending of bank capitaland more than $2350 billion was dueto the lending of Bank-CreatedMoney. Our error would be only ofthe order of 6 percent if we said thatthe entire $2500 billion in increase indeposits of the system came about bybanks creating money.

I have seen it stated in numerousplaces, as I am sure my readers have aswell, that the business of bankinginvolves "receiving deposits andmaking loans." The implication is thatbanks are intermediaries betweenmembers of the public as depositorsand borrowers. The implication is thatwhat banks loan is depositors' moneyand the banks only loan pre-existingmoney. But the fact is that what banksloan is "for the most part" money theycreate -- non-pre-existing money.

It not only deserves mention butvery considerable emphasis that ifbanks had never in the past createddeposits in the process of makingloans, there would be virtually nodeposits whatever in the bankingsystem and therefore no "depositorsfunds" to loan. Or look at the matteranother way, barely overstated. If allbank loans were to be paid-off, checksto banks would have to be written tothe full amount of all bank deposits.No deposits would remain. Or, asRobert Hemphill of the AtlantaRegional Fed once remarked "If allbank loans were repaid, no one would

have a bank deposit."At year-end 1994 the total amount

of Federal Reserve Notes plus FederalReserve Credits, the total amount ofGovernment-created Money was $419billion. If every cent of this had beendeposited in banks instead of most of itbeing held by the public fortransactions purposes, Bank Depositswould have totalled $419 billion.Instead total bank Deposits amountedto $2875 billion. Virtually all the$2875 billion was money created bythe banking system in the process ofmaking loans. It was bank lending andbank money creation for that purposethat gave rise to the $2875 billion indeposits held by the public, notdeposits made by the public that gaverise to the bank loans.

Some additional statistics from thepast may help to make all of the abovemore easily understood. The principalassets of banks are listed in bankingstatistics as "cash", "loans", and"investments" .

Much of what banks call their"investments" is nothing but loans.They differ, however, from what bankscall "loans" in that they are ordinarilyof very high quality and are usuallyeasier to liquidate for cash should thenecessity arise. I will follow a frequentpractice of the Fed in its Flow of Fundsstatistics and lump "Loans" and"Investments" together under the head"Total Bank Credit" (TBC).

Banks have a few assets other thanTBC and Cash but the other assets areusually of relatively minor importance.The principal liabilities of banks listedin banking statistics are "DemandDeposits" or "Checking Accounts"and "Time Deposits" or "SavingsDeposits". I will lump them alltogether under the head "Total BankDeposits" (TBD). Banks have a fewliabilities other than TBD but they areusually of relatively minor importance.

Remember that by bookkeepingconvention assets and liabilities arealways made exactly equal. Andbecause other assets and liabilities areof minor importance it turns out thatTotal Bank Credit and Total BankDeposits are normally very nearlyequal. From 1900 to 1929, forexample, Total Bank Deposits

VOLUME 80 PAGE 21

THE SOCIAL CREDITER

increased by $42.6 billion and TotalBank Credit increased by $43.3 billion- within 1.6 percent of the amount ofthe increase in deposits. The increasein deposits of the banking system wasnot because people were carrying legaltender to banks. The amount ofCurrency Held by the Public was $1.2billion in 1900 and $3.9 billion in1929. Nor, of course, was the increasein deposits of the system due to peopledepositing checks drawn againstdeposits. Total Bank Depositsincreased because deposits werecreated as banks made loans. And it isthe increase in loans that accounts forthe increase in deposits, not vice versa.

The Department of Commercepublications Historical Statistics of theUnited States shows that for the period1896 to 1970 other assets and liabilitiesof banks notwithstanding, Total BankCredit and Total Bank Depositsincreased by virtually the same averageannual percentage rate - TBC by6.33% per year and TBD by 6.5. TBCand TBD increased in step for theoverall period because deposits werecreated in the process of banks makingloans. TBD was created in the processof TBC being created, not vice versa.

We may now consider to whatextent the above described processworks in reverse. Assuming that allbank loans are repaid by check and thisis almost always the method ofrepayment, the repayment of loansobviously brings about a disappearanceof a deposit of equal amount.Assuming the loan was repaid by cash,the cash had to be obtained bysomeone somewhere writing a checkfor it. In any case, just as deposits arecreated when a bank makes a loan,deposits are de-created when theborrower repays the loan. In any case,just as money is created when a bankmakes a loan, money is de-createdwhen the borrower repays the loan.

When a loan is repaid, a bankalmost invariably replaces itimmediately with a new loan of equalor greater amount, thus creating a newdeposit of equal or greater amount.This, however, in no way invalidatesthe proposition that the repayment ofa loan means the disappearancesomewhere in the banking system of a

deposit equal to that created when theloan was made.

In making loans banks create enoughmoney for the principal amount of the

loan to be repaid but do not createenough for the interest as well as the

principal to be repaid.

Chapter 12.

MONEY CREATION TOPAY INTEREST

A loan, if it is to be properly repaid,must be repaid with interest.Depending on the term of the loanand the rate of interest charged, thetotal interest that must be paid can beimpressively large.

A credit card holder who carries a$1000 balance, who pays, say, 1.5percent interest monthly (18% annualrate), and who pays only the interestdue each month, would pay $1800interest after 10 years.

If the card holder then repaid theprincipal amount, he would havehanded the bank a total of $2800 or2.8 times the amount he borrowed.

A borrower of $1000 at 10%interest payable annually and withprincipal repayable after 10 yearswould, after 10 years, have paid a totalof $1000 of interest. If the borrowerthen repaid the principal amount, thetotal amount received by the bankwould be $2000. In other words, theborrower had to repay 2.0 times theamount borrowed.

The best terms my local bank willgive me as of this writing for a 15-year$100,000 home mortgage is 8.75percent interest. The bank wouldrequire 180 monthly payments of$999.80 each. At the end of 15 years Iwould have repaid the bank the$100,000 principal amount plus$79,964 in interest. In other words, Iwould have to repay the bank about1.8 times the amount borrowed.

The fact that any borrower mustrepay an amount larger than theamount borrowed (larger by theamount of the interest) brings us toanother very interesting fact - that in

making loans banks create enoughmoney for the principal of the loan tobe repaid but do not create enough forthe interest as well as the principal tobe repaid.

Another way of looking at the~matter may be helpful. Imagine thatthe only money in existence is Bank-Created Money and imagine that allbank loans were made on January 1and due to be repaid with interest onDecember 31 of the same year. Saythat on January 1 banks create$1 billion and loan it at 10 percent perannum interest. On December 31,$1.1 billion would be due to be repaidto the banks, but only $1billion wouldbe in existence. Some borrowerswould necessarily have to default. It isin the very nature of the system tocreate this type of problem.

If all the $2650 billion of the bankdeposits of 1990 had been created bythe making of 10 percent loans onJanuary 1, 1990, and if all were dueDecember 31, 1990, then $2650 ofprincipal and $265 billion of interest,$2915 would be due and only $2650billion in existence. The problemwould be one of very large \Jproportions.

It would have been possible for allmentioned loans to be repaid withinterest in 1990 only if something likethe following had happened. If the Fedhad created $26.5 billion in newGovernment-Created money and ifthe banks' reserve requirement hadbeen 10 percent so that this enabledthem to create $265 billion in newloans, then there could have been$2915 billion in the system. But, ofcourse this would mean that anotherbatch of loans had been createdwithout the money to pay the intereston them having been created. It issignificant to note in passing thatbetween 1990 and 1994 the Fed triedto do its part - it averaged adding anaverage of $27 billion of Government-Created Money to the system eachyear.

The important point, however, isVthat the size of the money supplyalways tends to lag the size necessaryfor all loans to be repaid with interest.Banks are always in a "need to catch-up" situation. Put another way, every

VOLUME 80 PAGE 22

THE SOCIAL CREDITER

year on average the supply of Bank-Created Money needs to be increasedby at least the average rate of interestthat banks charge on their loans. Thisassertion, while true enough to besignificant, greatly oversimplifies verycomplex matters.

There is another tendency withinthe system that makes eventual defaulttrouble even more likely. In order tounderstand this, imagine that a personborrows $1000 from Bank A and BankA creates a deposit in the borrower'sname. Imagine that the borrower thenwrites a check for $1000 to somemerchant and the $1000 is transferredto the merchant's bank account inBank B. Imagine that the merchantthen writes checks for $500 each totwo of his suppliers whose accountsare with Bank C and Bank D. In somesuch manner, all connection betweenthe $1000 that Bank A created and theloan Bank A extended tends to get"lost in the shuffle". But in any case,once the borrower writes a check for$1000 the recipient has clear title tothe $1000 and those that receive $500

~ checks likewise have a clear title.Thus, although most deposits are

created by making loans, neverthelessmost holders of deposits are not theoriginal borrowers and are not thepersons that are in debt for theirdeposits. People who borrow moneyand have deposits created in theirnames and thus owe a bank for themoney ordinarily write checks quicklyand transfer the money to people whodo not owe the bank (and perhaps oweno one else) for it.

Some of the bank deposits held bypeople who do not owe for it callmoney their "savings". And suchsavings are frequently invested bylending the money. The money thatpeople thus save and then loan is, forthe most part, Bank-Created Money.It came into existence bearing say, 10percent interest. If the saver makes aloan of it and also charges 10 percent,it is now money that bears 20 percent

Vinterest - ten percent owed by theoriginal borrower to the bank thatcreated it and 10 percent owed by thesecond borrower to the second lender.It is not impossible for the money tobe again saved and again be loaned at

10 percent and bear 30 percent interestor more.

But all the while only enoughBank-Created Money has come intoexistence to repay the principalamount of the first borrowing. In thisconnection, the record shows that in1929, for example, Total Private Debtin the USA amounted to about $162billion although the total amount ofBank-Created Money amounted toabout $42 billion. All money appearsto have been loaned nearly four timesover.

We may also note that from 1919to 1929 Total Private Debt increasedby 66.5 percent although NationalIncome out of which the debt had tobe serviced increased only 23.1percent.

The process of increasing debtfaster than either the money supply orthe national income is a process thatcannot go on for ever withoutproducing at least a "credit crunch"or, perhaps, bringing about a GreatLiquidation. Such a liquidation beganin 1929 with the ratio of debt tonational income at 189 percent. Bythe eve of World War II the ratio hadbeen brought down to 135 percent.By 1990, although calculated a littledifferently than previously, the ratiostood at 188 percent.

It would be handy to have statisticson the ratio of total interest paid in theeconomy to national income in 1929and subsequent years. No such figuresare available but we do have data onthe ratio of total interest paid topersons (or received by persons) tototal income of persons from allsources. I call this the Personal InterestIncome: Total Personal Income ratio -PII:TPI ratio.

Because of the enormous over-indebtedness of the economy in 1929,interest income was high. The PII:TPIratio for 1929 was 8.1 percent. Duringwhat is usually called the GreatDepression but which I prefer insome contexts to call the GreatLiquidation, the indebtedness of theeconomy came way down. By 1945the PII:TPI ratio had dropped to 2.8percent. By 1994 the indebtedness wasback to near the 1929 level but interestrates were higher in 1994 than 1929.

Thus by 1994 the PII:TPI ratio hadsoared to 11.5 percent. Exactly howlarge the PII:TPI ratio has to risebefore it sets off another GreatLiquidation no one knows.

IT'S YOUR MONEY by William EHixson. Published by COMER(Committee on Monetary andEconomic Reform), Toronto, Ontario,Canada. Available from ComerPublications, 245 Carlaw Avenue,Suite 107, Toronto, Ontario, CanadaM4M 2S6.

Price $10 Canadian, plus post &packing.

William EHixson, now retired, was formany years a Registered ProfessionalMechanical Engineer in Kentucky anda managing partner in a successfulsmall business in Louisville. He holds adegree from Oklahoma StateUniversity. He has published articles inthe Eastern Economic Journal, TheHistory of Economic Society Bulletin andEconomics et Societies (France) as well asbook reviews in Review of RadicalPolitical Economics.

He is the author of A Matter ofInterest: Re-examining Money, Debt andReal Economic Growth (Preager 1991)and Triumph of the Bankers: Money andBanking in the Eighteenth and NineteenthCenturies (Preager 1993).

We hope to reprint further chaptersfrom "Its Your Money" in future issuesofTSC.

Copyright © 1998. Permission granted forreproduction with appropriate credit.

If you wish to comment on an article inthis, or the previous issues, or discuss

submission of an essay for a future issueof The Social Crediter, please contact the

Editor directly:Alan Armstrong,

Gilnockie, 32 Kilbride Avenue,Dunoon, Argyll,

Scotland PA23 7LH.Tel/Fax: 01369701102

E-mail: [email protected]

If you do not wish to cut the coupon on theback page, please forward your subscription

with your address details.

VOLUME 80 PAGE 23

THE SOCIAL CREDITER

The Social Crediter is the official journal

of the Social Credit Secretariat. It

promulgates the analysis and prescription

for radical change to the current

financial! economic system developed by

C. H. Douglas in the 1920s. At the

centre of our concern is the need for

.radical reform of the international

fractional reserve, debt-money system.

Only then might other major socio-

economic changes, including theintroduction of a National Dividend,

follow and help to ensure that all of the

world's people have the potential to

enjoy economic sufficiency, while

simultaneously living a full and satisfying

life in harmony with each other and the

natural environment. It is our

conviction that whatever is physicallypossible and socially desirable CANbe made financial possible. This should

be everyone's concern and radical

reform is urgent, so that this potential

might be realised.

SUBSCRIPTIONS

Annual rates:UK inland £6.00

Airmail £9.00

In Australia, subscriptions and businessenquiries should be addressed to

3 Beresford Drive, Draper,Queensland 4520.

Published by KRP Ltd,16 Forth Street, Edinburgh EH1 3LH.

Tel 0131 5503769

r...... - ...... ••••· ..·- .... ·---- ..·- .... ·- ........ •...... ·-- ...... -· ..l!

THE SOCIAL CREDITER IIIIIi!IIiiI

IiIIII!!1Iii1

IIi

!___________________________________________________________________J

Please send me The Social Crediter for one year.(Make cheques/Money Orders payable to KRPLtd and send to The Social Credit Secretariat,

16 Forth Street, Edinburgh, EH1 3LH, Scotland.)

Name

Address

Post Code

Enclosed £

Recommended ReadingBooks by Major C.H. Douglas

Social CreditThe Monopoly if CreditEconomic DemocracyWarning DemocracyCredit Power and DemocracyThe Control and Distributionif Production

Frances Hutchinson andBrian BurkittThe Political Economy of SocialCredit and Guild Socialism

Eric de MareA Matter if Life or Debt

Alan D. ArmstrongTo Restrain the Red Horse*The Urgent Need for RadicalEconomic Riform (1996)£11.95 including P&P

THEMONOPOLY

OFCREDIT

c. H. DOUGLAS

41itZ;~'

A MATTEROF LIFEOR DEBT

EricdCMare

Books and booklets on the subject of Social Credit are available from Bloomfield Books,26 Meadow Lane, Sudbury, Suffolk, England COlO 6TD.* Also available from Towerhouse Publishing, 32 Kilbride Avenue, Dunoon,Argyll, Scotland PA23 7LH.

WEBSITE http://www.ecn .net.au/-sacredlE-MAIL ADDRESS: sacialcredit@FSBDial,co.uk

THE SOCIAL CREDITER BUSINESS ADDRESSSubscribers are requested to note the address for all business related to KRPLimited and The Social Credit Secretariat is: 16 Forth Street, Edinburgh EH1 3lH.Telephone 0131 5503769 e-mail: [email protected]

VOLUME 80 PAGE 24