Embed Size (px)

Citation preview

The next Battleground for #Digital #Transformation

Philip Gomm

Capgemini

Friday 17th October 2014

FST Future of Banking - Singapore

1 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Banking of tomorrow will be defined by players responses, to the evolving

needs of customers

Supply Push

Demand Pull

Segmentation / Franchise - Gen Y Millenials

Experience management

Channel mix

Product mix

Transaction Systems

Efficiencies

Portfolio of change initiatives

Regulation Industry initiatives

Compliance Customer engagement

So will the winners be

2 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

With illustrations from our World Reports in the next 30 mins or so….

Key pillars driving customers’ digital expectations leading insights from the World Retail Banking Report 2014

Innovative hotspots in the global payments landscape Capgemini and RBS’s World Payments Report 2014

Symbiosis of traditional financial services and tech disrupters - what will the new normal look like in the next 5 years?

3 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

The World Retail Banking Report (WRBR) has provided insights into the

challenges of the Retail Banking industry for over ten years

2009 2010 2011 2008 2012 2013

World Retail

Banking Report

Exclusive Customer

Experience Index (CEI)

• 80 customer touch points

132 Executive interviews

11 Years of Banking

Insights

2014

Customer Experience

Index (CEI)

• 17,000 customers

• 32 countries across

six regions

Feature

on Social Media • Current state of social

media banking use

• The market

opportunity vis-à-vis

social media banking

• Recommended

banking approaches

to social media

2014

4 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Our Report Focused Specifically on Actual Customer-Facing Functionalities

Banks Are Providing Today or Plan to Provide in the Future

5 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Canada US Czech Republic Australia South Africa UK Argentina

2.52%

8.12% 3.04%

0.87%

3.08%

0.88%

1 2 3 4 5 6 7

60.0% 54.6% 50.7% 48.5% 47.7% 47.0% 45.8%

60.8% 57.0% 42.5% 51.5% 48.6% 50.1% 44.9%

0.80%

Top 7 Countries in Customer Experience

Norway UAE Spain Turkey Singapore Japan Hong Kong

11.01%

10.69%

7.22%

1.44% 1.61%

31.0% 29.0% 28.5% 27.7% 27.1% 23.4% 16.6%

43.3% 40.0% 34.4% 38.4% 34.4% 21.9% 15.0%

12.34%

Bottom 7 Countries in Customer Experience

24 25 26 27 28 29 30

5.89%

25% Countries Showed a Decrease in Positive Customer Experience of +10%

2014

2013

2014

2013

Since its launch in 2011, the banking CEI decreased for the first

time in 2014 (by 0.7% points)

6 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

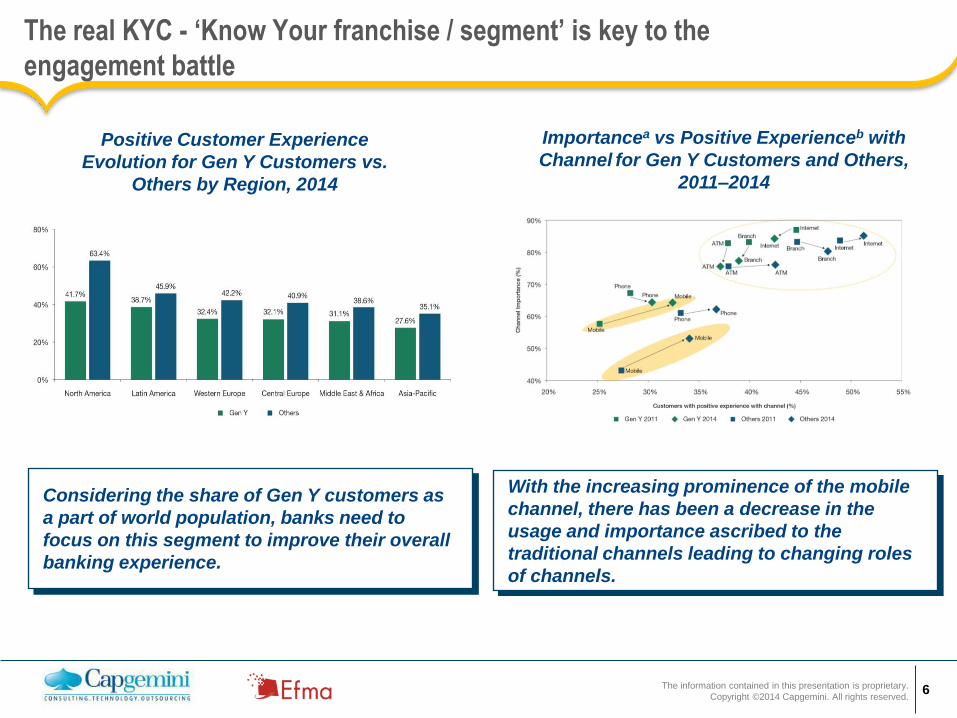

The real KYC - ‘Know Your franchise / segment’ is key to the

engagement battle

Positive Customer Experience

Evolution for Gen Y Customers vs.

Others by Region, 2014

Considering the share of Gen Y customers as

a part of world population, banks need to

focus on this segment to improve their overall

banking experience.

Importancea vs Positive Experienceb with

Channel for Gen Y Customers and Others,

2011–2014

With the increasing prominence of the mobile

channel, there has been a decrease in the

usage and importance ascribed to the

traditional channels leading to changing roles

of channels.

7 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

10% of Banking Customers Already Are Interacting with Their Banks via Social Media at Least Once Per Week

Customers Interacting with Different Banking

Channels at Least Once per Week (%), 2013-2014

% of Customers Spending More than One Hour Per Day

on Social Media Sites vs.

% of Customers with Social Media Accounts (%), 2014

Emerging Markets and Gen Y Are the Highest Users of Social Media, but Other Demographics Are Also

Relatively Active Users

Channel mix is changing and the demand is not concentrated

8 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

With illustrations from our World Reports in the next 30 mins or so….

Key pillars driving customers’ digital expectations leading insights from the World Retail Banking Report 2014

Innovative hotspots in the global payments landscape Capgemini and RBS’s World Payments Report 2014

Symbiosis of traditional financial services and tech disrupters - what will the new normal look like in the next 5 years?

9 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Capgemini World Payments Report - celebrating 10 years of analyzing the

quickly evolving global non-cash market

2005 2006 2007

2008

2012 2011

2010 2009

2013

The industry’s point of reference

for global non-cash transaction

market data

At the forefront of understanding

regulations and their interaction

with business models and

operations

The clear thought leader on the

various levers for successful

payments strategies and

innovation

WPR13 analyzed the client-end of

the value chain, WPR14

examines the fulfillment i.e. the

non-customer facing part of the

value chain -‘Payments

Processing’

WPR 2014

2014

10 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Global non-cash transactions volume growth decelerated in 2012, but is

expected to have accelerated in 2013

The mobile payments space is increasingly more competitive, with banks and non-banks striving for insightful data, market influence and consumer loyalty

11 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

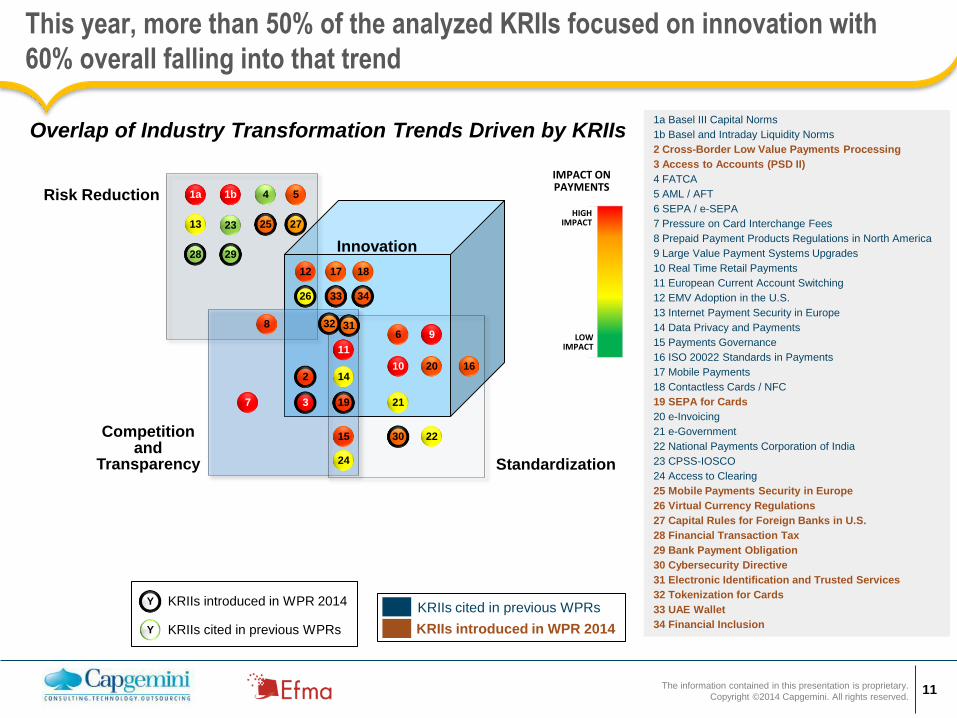

This year, more than 50% of the analyzed KRIIs focused on innovation with

60% overall falling into that trend

LOW IMPACT

HIGH IMPACT

IMPACT ON PAYMENTS

Standardization

Competition and

Transparency

Innovation

1a

27

4

6

28

3

30

9 8

20

5 Risk Reduction

2

23

11

14

31

7

10

1b

19

25

26

29

34

32

33

12

13

15

16

17 18

21

22

24

Overlap of Industry Transformation Trends Driven by KRIIs 1a Basel III Capital Norms

1b Basel and Intraday Liquidity Norms

2 Cross-Border Low Value Payments Processing

3 Access to Accounts (PSD II)

4 FATCA

5 AML / AFT

6 SEPA / e-SEPA

7 Pressure on Card Interchange Fees

8 Prepaid Payment Products Regulations in North America

9 Large Value Payment Systems Upgrades

10 Real Time Retail Payments

11 European Current Account Switching

12 EMV Adoption in the U.S.

13 Internet Payment Security in Europe

14 Data Privacy and Payments

15 Payments Governance

16 ISO 20022 Standards in Payments

17 Mobile Payments

18 Contactless Cards / NFC

19 SEPA for Cards

20 e-Invoicing

21 e-Government

22 National Payments Corporation of India

23 CPSS-IOSCO

24 Access to Clearing

25 Mobile Payments Security in Europe

26 Virtual Currency Regulations

27 Capital Rules for Foreign Banks in U.S.

28 Financial Transaction Tax

29 Bank Payment Obligation

30 Cybersecurity Directive

31 Electronic Identification and Trusted Services

32 Tokenization for Cards

33 UAE Wallet

34 Financial Inclusion

Y

Y

KRIIs introduced in WPR 2014

KRIIs cited in previous WPRs

KRIIs cited in previous WPRs

KRIIs introduced in WPR 2014

12 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

• 800 billion number of non-cash payments transactions by 2024

• Developing countries growing to half of the total non-cash market by 2021

• Developing markets to be the focus of the majority of new solution development

• Entry by large numbers of non-banks into the customer-facing segments

• In several major countries, banks may no longer be the only party at the center of payments governance

• More PSP’s sharing parts of the value chain due to regulatory and industry changes

Radical Shift In Roles And Influence of Key Stakeholders

Innovation And Convergence will Change Pricing and Product Mix

• Continued acceleration of innovation and convergence

• Emergence of additional currencies

• Rising usage of closed loop payments instruments (prepaid)

• Increased biometric identification

• Rising potential risk of fraud or failure of PSPs

• Continued proliferation of financial industry regulation

• Focus on consumer protection by regulators to continue

• Increased cross-border e-commerce

The 10 year horizon: potential changes in the payments industry

13 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Banks need to choose their zone of play, aligned to customer franchise

In 2013 we successfully forecast the emergence of

four “value hot spots” in the payments value chain In 2012 we identified 12 value spaces in payments

business

In 2014 we forecast the pressure now building to renovate the back office to support front end differentiation themes

14 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

In addition to the client-facing segment of the value chain, customer demands

are driving the need for payment processing transformation and innovation

In 2014 we forecast increasing Customer Demands Driving a Need for Innovation in Payments Processing

Real-time Capability

‘Anytime’ /‘Anywhere’ Payments

Multiple Payments Modes/Channels

Enterprise-wide Visibility (Cash and Working Capital)

Cost Control via Efficient Payments Processing

Risk Management

Treasury Technology Compliant with

Corporate IT

Ease of Payments

Value-Added Services

Visibility/Insights from Payments Data

Retail Corporate Retail/Corporate

15 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

With illustrations from our World Reports in the next 30 mins or so….

Key pillars driving customers’ digital expectations leading insights from the World Retail Banking Report 2014

Innovative hotspots in the global payments landscape Capgemini and RBS’s World Payments Report 2014

Symbiosis of traditional financial services and tech disrupters - what will the new normal look like in the next 5 years?

16 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

What does the new normal look like: from our research digital banking future

best practices cover seven Digital Transformation Areas

Cross-channel, self-service, personalised

experience

Customer understanding through

digital channels

Customer analytics

Use of mobile channels with customers

Use of social media with customers

Worker enablement

Process digitisation

17 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Digital Globalisation Enterprise Integration

Redistribution decision authority

Shared digital services

New Digital Businesses Digital products

Reshaping organisational boundaries

Worker enablement Working anywhere anytime

Broader and faster communication

Community knowledge sharing

Customer touch points Customer service

Cross-channel coherence

Self service

Performance management Operational transparency

Data-driven decision-making

Top line growth Digitally-enhanced selling

Predictive marketing

Streamlined customer processes

Customer understanding Analytics-based segmentation

Socially-informed knowledge

Digitally-modified businesses

Product/service augmentation

Transitioning physical to digital

Digital wrappers

Process digitalisation Performance improvement

New features

Digital Capabilities

Customer Experience

Operational Processes

Business Model

Unified Data and Processes

Analytics Capability

Business and IT Integration

Solution Delivery

Source: Capgemini Consulting-MIT Analysis – Digital Transformation: A roadmap for billion-dollar organizations (c) 2012

Organisations must now drive digital transformation in

three key areas of their value proposition

Effective digital transformation is about changing the core of how business is done

18 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

Globally, banks have chosen different focus for their digital journey to align

with their growth or positioning strategy

Customer understanding through digital

channels

Customer analytics

Use of mobile channels with

customers

Use of social media with customers

Worker enablement

Process digitisation

Cross-channel, self-service, personalised experience

“Easy Bank” “Tu cuentas” “Compass virtual banker” (USA) "Finest Online”

“Best Self Service Bank”

“Finest Online” “Crowd-sourced credit card”

“Business insights”

"Mobile based personalised offers”

"Customer Analytics”

“Tablet Banking Application”

"PremiaT - Mobile Geopositioning”

“iPhone voice recognition and assistance”

"Using Social Media”

"PremiaT – Online Community”

“Online Facebook Integration”

“ Social Media Credit Card"

“Real-time processing " “Apple iPad/iPhone» "Google Cloud " "Customer Assistant Lola"

"Online Collaboration – The Wall”

"Video chat with representatives"

"Virtual Operation" "Business Intelligence”

"Alior Sync - Virtual Bank"

"Remote mobile check deposit”

19 The information contained in this presentation is proprietary.

Copyright ©2014 Capgemini. All rights reserved.

In the Digital Transformation landscape , the portfolio of change initiatives,

(constitution and execution) will separate the winner(s) from the also rans’

Supply Push

Demand Pull

Segmentation / Franchise - Gen Y

Experience management

Channel mix

Product mix

Transaction Systems

Efficiencies

Regulation Industry initiatives

Compliance Customer engagement

Portfolio of change initiatives

Disintermediation

through - franchise

redefinition /

ownership of

consumption context

The information contained in this presentation is proprietary. © 2014 Capgemini. All rights reserved.

We’d like to hear from you at:

About Capgemini

With more than 131,000 people in 44 countries, Capgemini

is one of the world's foremost providers of consulting,

technology and outsourcing services. The Group reported

2013 global revenues of EUR 10.1 billion.

Together with its clients, Capgemini creates and delivers

business and technology solutions that fit their needs and

drive the results they want. A deeply multicultural

organization, Capgemini has developed its own way of

working, the Collaborative Business ExperienceTM, and

draws on Rightshore ®, its worldwide delivery model.

Rightshore® is a trademark belonging to Capgemini

Leading with Financial Insights www.worldretailbankingreport.com