Embed Size (px)

Citation preview

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK

company limited by guarantee, and forms part of the international BDO network of independent member firms.

The New World of Healthcare

Revenue Recognition, ASC 606 –

PRACTICALITIES &

PITFALLS

June 21, 2018

ASC 606 – Practicalities and Pitfalls2

CPE and SupportCPE Participation Requirements ‒ To receive CPE credit for this webcast:

• You’ll need to actively participate throughout the program.

• Be responsive to at least 75% of the participation pop-ups.

• Please refer the CPE & Support Handout in the Handouts section for more information

about group participation and CPE certificates.

Q&A:

Submit all questions using the Q&A feature on the lower right corner of the screen. At the

end of the presentation, the presenter(s) will review and answer all questions submitted.

*Please note that questions and answers submitted/provided via the Q&A feature are visible to all

participants as well as the presenters.

Technical Support:

If you should have technical issues, please contact LearnLive:

• Click on the Live Chat icon under the Support tab, OR call: 1-888-228-4088

Audio

Audio will be streamed through your computer speakers. If you experience audio issues

during today’s presentation please dial into the teleconference: 1.855.233.5756,

teleconference code: 568-172-7969

ASC 606 – Practicalities and Pitfalls3

With you today

VENSON WALLIN, CPAManaging Director,

Healthcare Advisory

BDO USA, LLP

804-614-1188

KAREN FITZSIMMONS, CPAAssurance Partner,

Healthcare

BDO USA, LLP

703-336-1466

4 ASC 606 – Practicalities and Pitfalls

OVERVIEW OF ASC 606

ASC 606 – Practicalities and Pitfalls5

SCOPE

• All contracts with customers/patients/payors, except

o Lease contracts

o Insurance contracts

o Financial instruments

o Guarantees

o Non-monetary exchanges in the same line of business to facilitate sales to

customers

• Contracts not with customers/patients/payors are excluded:

o Contributions

o Collaborative arrangements

ASC 606 – Practicalities and Pitfalls6

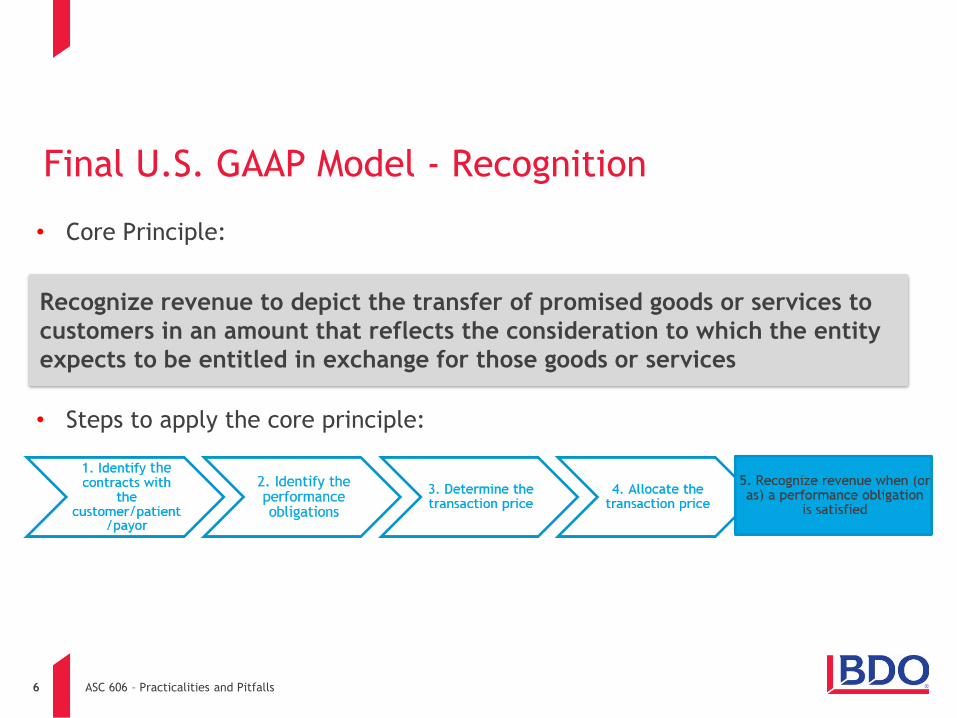

Final U.S. GAAP Model - Recognition

• Core Principle:

• Steps to apply the core principle:

Recognize revenue to depict the transfer of promised goods or services to

customers in an amount that reflects the consideration to which the entity

expects to be entitled in exchange for those goods or services

ASC 606 – Practicalities and Pitfalls7

ScopingStep “0” – Contribution vs exchange transaction

Contribution -

• An unconditional transfer of cash or other assets to an entity or a settlement or

cancellation of its liabilities in a voluntary non-reciprocal transfer by another entity

acting other than as an owner.

• Because a contribution is both voluntary and non-reciprocal, it is scoped out of ASC 606

by definition.

Exchange Transaction –

• A reciprocal transfer between two entities that results in one of the entities acquiring

assets or services or satisfying liabilities by surrendering other assets or services or

incurring other obligations.

• Because an exchange transaction is reciprocal transaction in which two parties exchange

something of commensurate value, it is scoped into ASC 606 by definition.

ASC 606 – Practicalities and Pitfalls8

Effective Date of Topic 606

ASC 606 – Practicalities and Pitfalls9

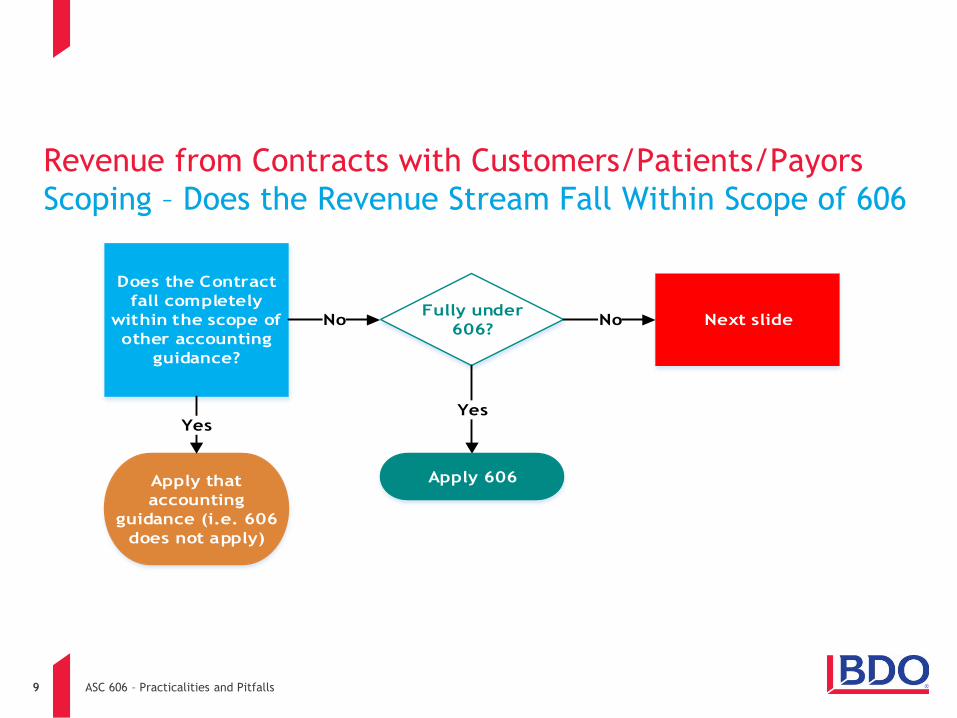

Revenue from Contracts with Customers/Patients/Payors

Scoping – Does the Revenue Stream Fall Within Scope of 606

Does the Contract

fall completely

within the scope of

other accounting

guidance?

Apply that

accounting

guidance (i.e. 606

does not apply)

Yes

NoFully under

606?

Yes

Apply 606

No Next slide

ASC 606 – Practicalities and Pitfalls10

Revenue from Contracts with Customers/Patients/Payors

Scoping – Does the Revenue Stream Fall Within Scope of 606

The parties to the contract must

approve it and be committed to

perform their respective

obligations.

Use the other accounting

guidance to separate the

contract and initially

measure the non-606

element of the contract.

Exclude the amount of the

contract that is under other

accounting guidance and use

that as the transaction price

for part of the contract

under 606

Apply the guidance

in 606 to separate

and initially measure

the part of the

contract that falls

under other

accounting guidance

and the part of the

contract that falls

under 606.

Does the other

accounting standard

have guidance

related to initial

measurement that

applies?

Yes No

Yes

11 ASC 606 – Practicalities and Pitfalls

HEALTHCARE CHALLENGES OF ASC 606

ASC 606 – Practicalities and Pitfalls12

Challenges of ASC 606 in Healthcare

• Healthcare industry consolidation

• Integration of various provider types into one system – diversity of contracts

and associated revenue recognition models

• Hospitals

• SNFs

• Home Health

• etc.

• Shift to Value-Based Care

• Estimation of transaction price may be challenging

• Use of clinical and operational metrics, in addition to traditional financial

metrics, will require a more astute reader (i.e., auditor, regulator, private

equity investor, shareholder, etc.) to understand revenue recognition

implications

ASC 606 – Practicalities and Pitfalls13

Challenges of ASC 606 in Healthcare

• Increased opportunities for fraud and abuse given the increased importance of

clinical and operational metrics

• More challenging to “audit” those metrics

• Estimation of allowance for doubtful accounts

• Determination of willingness and ability of patient to pay can be challenging

• Price concessions vs. bad debts

• Bundled services provided in a long-term care setting and the revenue

recognition model

ASC 606 – Practicalities and Pitfalls14

ConclusionThank you for your participation!

Certificate Availability – If you participated the entire time and responded to at

least 75% of the polling questions, click the Participation tab to access the print

certificate button.

Please exit the interface by clicking the red “X” in the upper right hand corner

of your screen.

![VMW Earnings Press Release[1] - VMware · During May 2014, the Financial Accounting Standards Board issued updates to accounting standards related to revenue recognition ("ASC 606")](https://img.pdfslide.us/doc/110x75/5ed43e211e109569e121442d/vmw-earnings-press-release1-vmware-during-may-2014-the-financial-accounting.jpg)