Embed Size (px)

Citation preview

The new name for City University Business School

Alistair MilneCass Business [email protected]

Risk Management in Insurance and Insolvency,The Hebrew University of Jerusalem,October 16th-17th 2006

The new name for City University Business School

Economic and Regulatory Capital: Applications in

Banking and Lessons for the Insurance Industry

Alistair MilneCass Business School

The new name for City University Business School

My research focus bank capital and shareholder value

i.e. risk-management and corporate finance

co-authors and papers

Giles and Milne (2004)

Dimou, Lawrence, and Milne (2005)

Milne and Onorato (2006a,2006b)

Milne (2006) “Three lessons”

theory informed by extensive interaction with practitioners

The new name for City University Business School

Agenda for today• The rise of bank risk management

• bank economic capital: current practice

• A critique of this thinking– Practical issues– Cost of regulatory capital requirements– Skewness

• Two proposed performance measures

• Implications for insurance industry

The new name for City University Business School

Rise of bank risk-management

The new name for City University Business School

Greater competitionCore business (retail deposits, lending to households and smaller business) remains profitable; but• Narrower margins in many markets

– Especially corporate & sovereign• New products creating exposure to

market risks

The new name for City University Business School

Governance centre stage

• Larger, more complex, institutions

• Less state ownership or support; more answerable to shareholders

• Pressure to increase shareholder returns

• Greater regulatory freedom in choice of activities– Regulatory oversight of risk-management

The new name for City University Business School

Databases and modelling• Cost of collecting, storing, and manipulating

data fallen dramatically

• New tools– Market risk – VaR– Portfolio models of corporate and sovereign

credit risks

• Search for enterprise wide measures of risk/ return e.g. “pricing tools”

The new name for City University Business School

Bank economic capital:current practice

The new name for City University Business School

A new language …

• Capital– Capital as a measures of “worst case” exposure

• Eg “value at risk”

– Efficient “allocation” of this capital, to activities earning the highest return

• Two birds with one stone– Solvency (enough capital); and – risk-reward tradeoffs (efficient allocation of capital)

The new name for City University Business School

RAROC• Standard formulation

• Economic Capital = ‘value at risk’ type measure to

cover all risks (market, credit, operational)

• Accept when RAROC exceeds hurdle

• Widely used, especially in trading floors and

corporate lending

capital economic''

losses expected - costs -return expectedRAROC

The new name for City University Business School

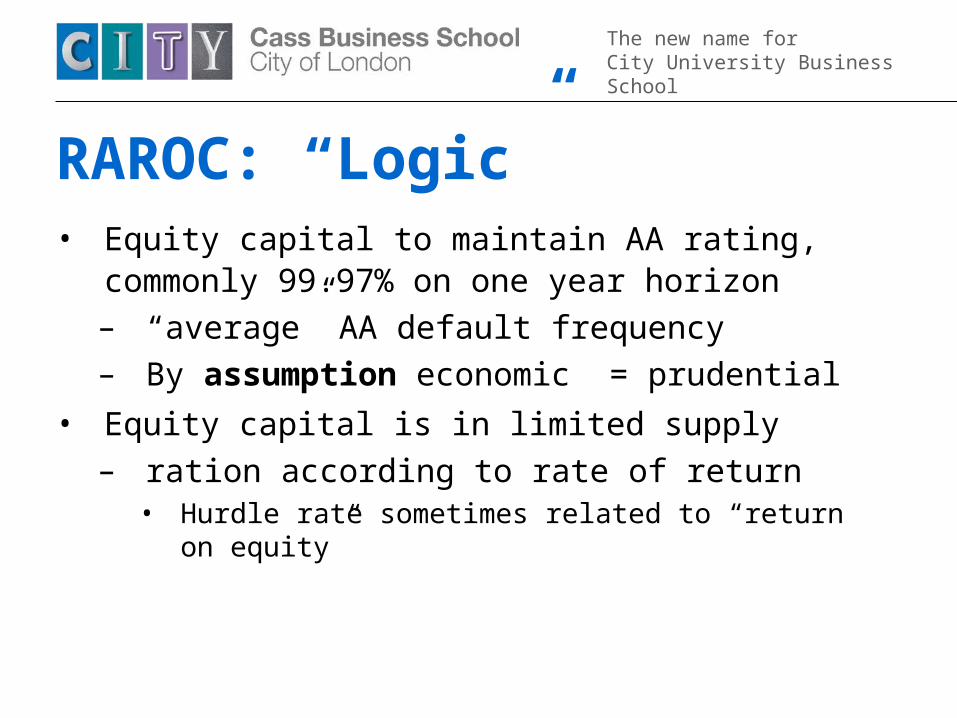

RAROC: “Logic”• Equity capital to maintain AA rating,

commonly 99.97% on one year horizon– “average” AA default frequency – By assumption economic = prudential

• Equity capital is in limited supply– ration according to rate of return

• Hurdle rate sometimes related to “return on equity”

The new name for City University Business School

Regulatory dimension• approved internal models for setting regulatory

requirements on trading book, since 1996

• Basel II aims to align regulatory and economic capital– Concerns about “regulatory arbitrage”– EU implementation 2007, delayed in US– IRB model based calculations of credit risk – not based on portfolio models, but asks banks to

compute PD, LGD as inputs, and these could be derived from same databases as a portfolio model

The new name for City University Business School

A critique

The new name for City University Business School

A critique1. Practical problems

2. Cost of regulatory capital?

3. Skewness

• Conclusions use alternative performance measures, distinguish tail risks and risk-return tradeoffs

The new name for City University Business School

Competitive advantage?

• Proposition 1: lower regulatory capital provides me with a competitive advantage

• Proposition 2: estimating tail risks and allocating economic capital provides me with a competitive advantage

• Both must be qualified– Competitive advantage of regulatory capital is small– Tail risks relatively unimportant to pricing

• focus on value creation– Requires different metrics than RAROC

The new name for City University Business School

1. Some practical issues

The new name for City University Business School

Data problems – credit risk• Larger corporates/ sovereigns fairly OK

– CreditMetrics/MKMV– US ratings history back to 1950s or earlier– Difficulties with LGD

• Retail (including smaller corporates): – a variety of scoring models, good for PD– a little work on CVaR– best UK institutions around 10-12 years data

• UK FSA transitional arrangements accept 5 years of data for Basel computations! 2 years for LGD

• Other low default portfolios, – even more severe data problems

• Correlations?

The new name for City University Business School

Data problems – op risk• Even greater than for credit risk

• High frequency/ low impact– Most firms have databases, for a few years– Little comparability between firms– Mostly EL (minor contribution to EC)

• Low frequency/ high impact– By their nature no data– Low correlation with market/ credit risks?

The new name for City University Business School

Outcome : • lacking data we extrapolate

– standard deviations, using arbitrary multipliers– PD as in Basel risk curves (Vasicek single factor

model plus arbitrary correlation loading)

• OP risk : low frequency high impact, no statistical basis at all

• We are confusing:– Risk/return tradeoff (does not need extreme tail)– prudential safety (cannot be based on statistical

models)

The new name for City University Business School

RAROC difficulty (1)• Liquidity facilities

– eg Lines of credit to a AAA/AA corporates– eg commercial paper underwriting

• Must back with capital– to maintain liquidity over (say) 24 months

• Loss v. unlikely: 99.97% appropriate• So VERY safe lending

– 15% required return on this committed capital leads to unreasonably high pricing …

– Cannot compete with market prices

The new name for City University Business School

RAROC difficulty (2)• Capital in trading operations

• Liquidity is “lifeblood”, need to survive temporary market fluctuations without being forced to close positions

• Well known examples LTCM, Metallgesellschaft

• Investors (shareholders) need to distinguish extreme tails and normal range of market fluctuations, only latter is priced risk

The new name for City University Business School

Back to basics• Ultimate objective: shareholder value

– Appropriate trade-offs between risk and reward– Protecting solvency of the institution– Incentives for employees and line management

• Well developed tools for these tasks for non-financial companies – Net Present Value (NPV)– Economic Value Added

• So lets apply these tools to banks

The new name for City University Business School

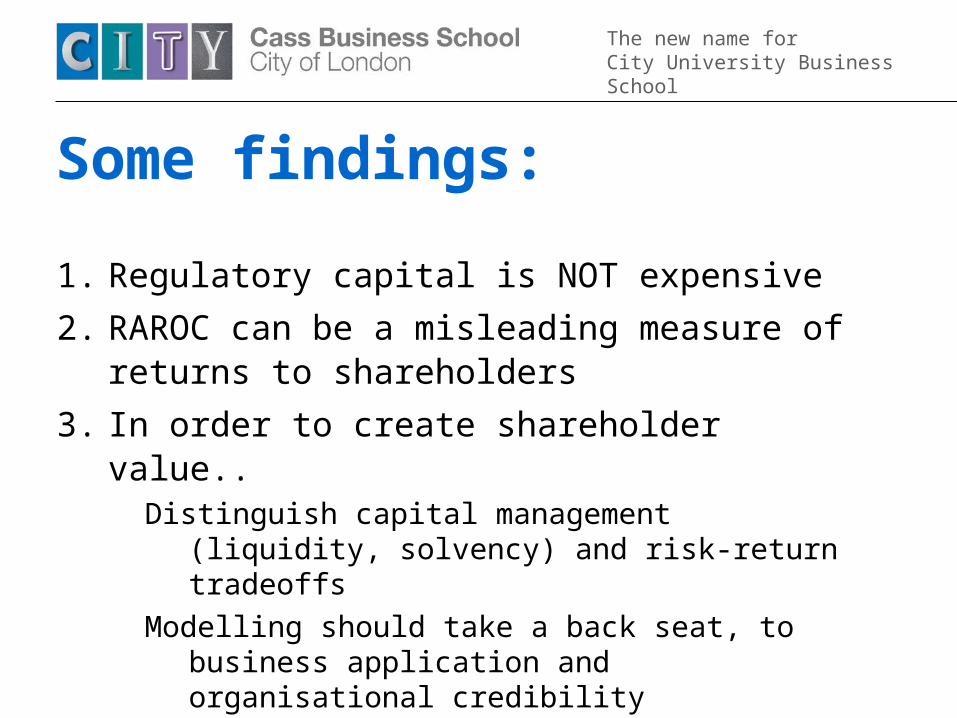

Some findings:

1. Regulatory capital is NOT expensive

2. RAROC can be a misleading measure of returns to shareholders

3. In order to create shareholder value.. Distinguish capital management (liquidity,

solvency) and risk-return tradeoffs

Modelling should take a back seat, to business application and organisational credibility

The new name for City University Business School

2. The cost of regulatory capital

The new name for City University Business School

Basic argument • WACC = weighted average cost of capital

– Sum of debt and equity components

• Changing reg cap: only small change WACC– linked to Modigliani-Miller (1958)

• Detail (Milne and Giles (2004))– Equity capital small proportion of total funding – regulatory capital < 1:1 impact on equity capital

• e.g. if following rating agency target

– Leverage adjustment• Higher equity capital makes equity capital less risky,

lowers cost of equity

The new name for City University Business School

Table 3: Change in cost of mortgage lending (Giles – Milne (2004)) Standardapproach

IRB Change

Value of loans € (1) 100.0 100.0Risk weighting (2) 50% 25%Capital requirement: tier 1 € (3) (1) (2) 4% 2.0 1.0 -1.0Capital requirement: tier 2 € (4) (1) (2) 4% 2.0 1.0 -1.0

Cost of Tier 2 debt employed € (5) (4) 5% 0.1 0.1Cost of other debt employed € (6) [(1) - (3) - (4)] 5% 4.8 4.9Gross cost of debt employed € (7) (5) + (6) 4.9 5.0Tax € (8) -(7) 30% -1.5 -1.5After tax cost of debt employed € (9) (7) + (8) 3.430 3.4650 0.035

Leverage adjusted COE (10) 4% + [15% - 4%] (2)1 (2)2] 15.00% 26.00%

After tax cost of tier 1 equity € (11) (3) (10) 0.30 0.26 -0.040

After tax break even loan charge (12) [(9) + (11)] (1) 3.730% 3.725% -0.005%Pre tax break even loan charge (13) (12) [1 - 30%] 5.329% 5.321% -0.007%

Hurdle interest rate on lending

Reduced IRB capital requirement for mortgages

Regulatory requirements

Cost of debt

Cost of equity

The new name for City University Business School

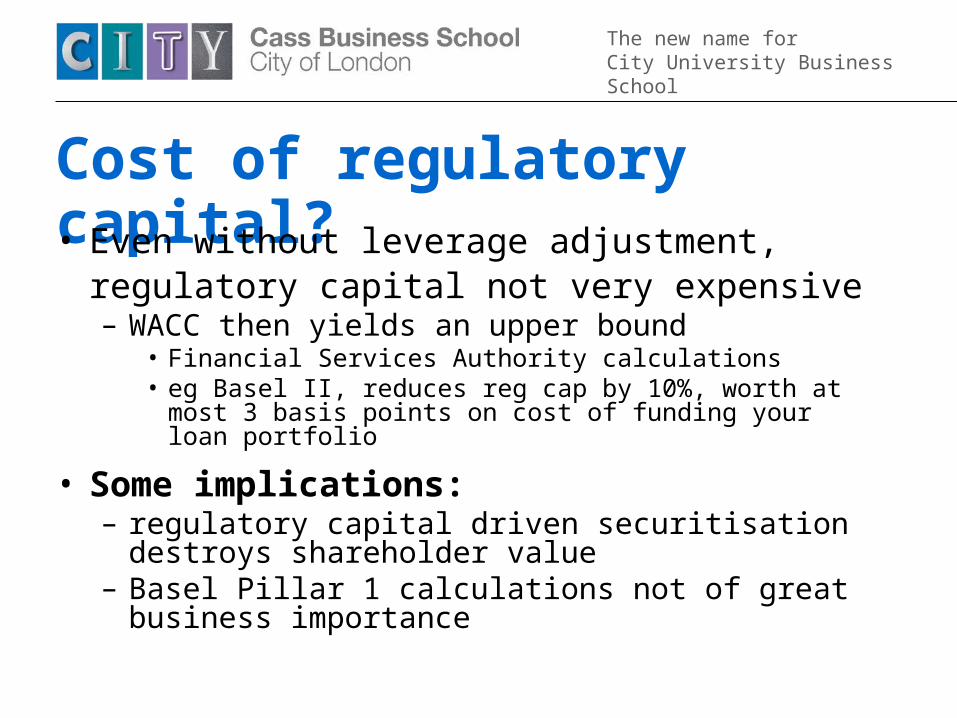

Cost of regulatory capital?• Even without leverage adjustment, regulatory

capital not very expensive– WACC then yields an upper bound

• Financial Services Authority calculations• eg Basel II, reduces reg cap by 10%, worth at most 3

basis points on cost of funding your loan portfolio

• Some implications:– regulatory capital driven securitisation destroys

shareholder value– Basel Pillar 1 calculations not of great business

importance

The new name for City University Business School

Dimou, Lawrence, Milne (2005)• Increases tax exposure

– higher equity capital reduces tax shield– a transfer: a private but NOT a social cost

• Reduces access to bank ‘safety net’– Higher equity capital forces bank owners to accept more risk– a transfer: a private but NOT a social cost

• Lowers expected costs of bankruptcy– Higher capital reduces probability of bankruptcy/ financial distress– a benefit: Social benefits likely to exceed private benefits.

• Agency costs– Bank managers look after themselves, not shareholders– Equity capital gives managers freedom to pursue their own ends– Reg cap is different, it is a discipline on managers just like debt– neutral No private cost of reg cap, if not used as risk measure

The new name for City University Business School

3. Skewness

The new name for City University Business School

Theory• Proposition 1 (Onorato-Milne (2006))

– Economic capital = prudential capital• iff insurance cost of hedging risk w is proportional to

prudential tail H-1(w)

• Corollary– RAROC hurdle delivers shareholder value if all risk

distributions have the same skew– Turnbull-Crouhy-Wakeman (1999) special case

• Log normal asset returns so (right) skew increasing with σ• As σ rises, prudential tail rises less than insurance cost• So RAROC threshold rises with σ

The new name for City University Business School

Illustrations• Taken from Milne and Onorato (2006a)

“Apples and Pears? The comparison of bank economic and prudential capital.”

• Assume market price of risk proportional to standard deviation– Compare symmetric and right-tailed returns– What then is NPV=0 hurdle rate for

RAROC?

The new name for City University Business School

The new name for City University Business School

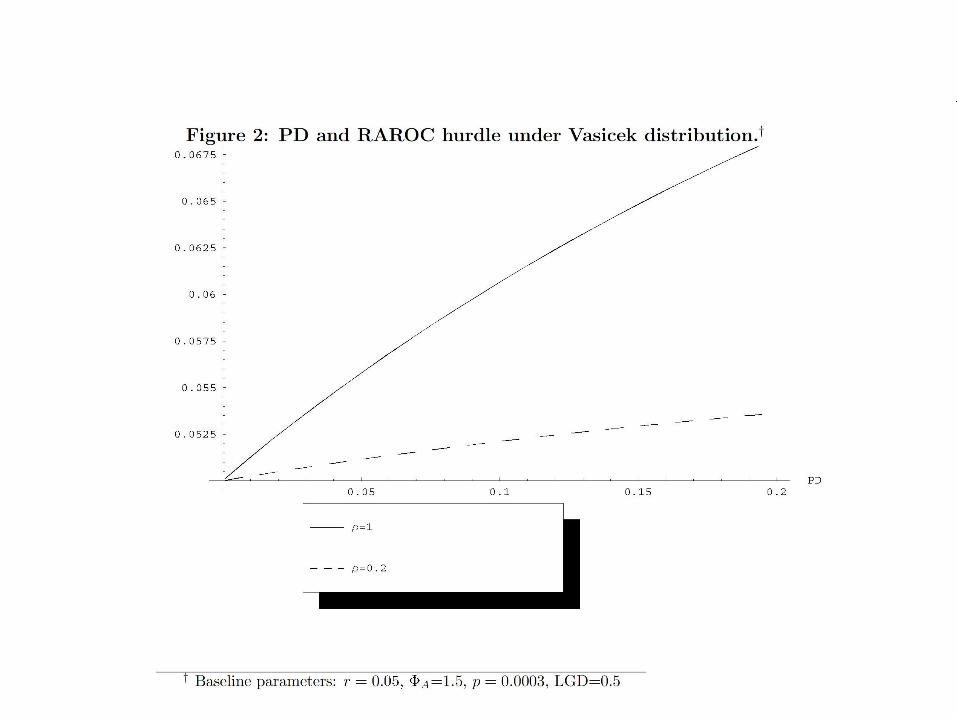

A credit risk distribution• Credit risk left skew

• Vasicek “asymptotic” single factor model– Model used for Basel IRB risk curves– Left skew , so smaller NPV =0 RAROC

• More detail on parameters– PD : probability of default– ρ : correlation of credit risk driver with market– R2 : correlation with aggregate (systematic) risk

• How do these parameters affect RAROC hurdle?

The new name for City University Business School

The new name for City University Business School

Critique: summarised• Two different objectives

– Prudential (avoiding financial distress, satisfying regulator)

– Risk-return tradeoffs

• Using one measure of capital for both purposes creates conflicts – If tail risk is uncertain– If tail risk is skewed

• If regulators take a conservative view of risks– Again does not matter to the business

The new name for City University Business School

Two proposed performance measures

The new name for City University Business School

Proposed measures• Milne and Onorato (2006a): discount with market

based risk-premium φ

• Milne and Onorato (2006b): use Wang transform

pWT ETL

WTRAROC

Capital Prudential

1/Loss Expected -return ExpectedrEC

fr

The new name for City University Business School

More theory• Inventory models

– Incorporate costs of financial distress, or penalty costs of raising capital

– Froot and Stein (1998), Milne (2004)

• Outcome: additional internal beta “G”– Measures the risk of capital shortage– Depends upon:

• Probability of capital shortage• Costs of financial distress

• For well capitalised bank, G can be ignored– Probability of capital shortage is negligible

The new name for City University Business School

Implication • Longer term : equity capital not

constrained– Retain earnings or rights issue– No need to ration, adjust to minimise WACC

• Measuring NPV (shareholder value):– right WACC input

• e.g. “betas” (cost of risk)• depend on correlation with market NOT with balance sheet

– Equivalent to cost of insuring exposure

• Capital constrained? – Additional cost of risk: internal or portfolio beta G, for rationing

capital

The new name for City University Business School

With market prices for risk • If risk can be priced on market, proceed as

follows (Milne and Onorato (2006a))– Discount future returns with risk-premium taken

from market prices– equivalently: estimate the cost of hedging

completely on the market and deduct this cost from expected return

(“risk neutral pricing”)– Divide by contribution to prudential capital

• Hurdle rate? Zero if unconstrained. Otherwise chosen to ration equity capital

The new name for City University Business School

No market prices for risk • Use “distortion measure” (Milne and Onorato

(2006b )) eg Wang transform– Portfolio based– Satisfies axioms of coherence and second

order stochastic dominance– Divide by contribution to prudential capital

• Hurdle rate? Zero if unconstrained. Otherwise chosen to ration equity capital

The new name for City University Business School

Merits of Wang transform• Yields an “expected value”

– Analagous to “risk neutral pricing” – “distort” the probability density of returns

• “risk appetive” can be parameterized using a single parameter p

The new name for City University Business School

In practice very limited data• Especially for tail risks

• Sophisticated modellign of tail risks not ormally appropraite– Simple stress or scenario analysis– Aim to achieve credibility, within the

organisation and also with shareholders.

The new name for City University Business School

Implications for insurance

Some preliminary thoughts: open to discussion

First general insurance, then life

The new name for City University Business School

When re-insurance markets availableLogic of Milne and Onorato (2006a) applies.

– Price risk according to what it would cost to transfer onto re-insurance market – deduct from premium income

– Set a hurdle rate “cost of equity capital”• Zero if unconstrained, > zero if rationing

The new name for City University Business School

When reinsurance limited• Use of the Wang transform can help

systematise thinking about “risk-appetite”

• Needs to be supplemented by e.g. stressed scenarios, to check capital adequacy

The new name for City University Business School

Data sometimes available• For some products extensive data available

– Also the products where reinsurance markets are most liquidy

• Models can be used for computing capital, but pricing best done off the market

• For other products, very limited data and illiquid markets for re-insurance. – Here focus on the simplest possible modelling tools

The new name for City University Business School

One difference: insurance and banking - segmentation

• Banks all seek to maintain high credit ratings

• Some insurers may opt for lower capitalisation, and lower premium pricing to customers, with the understanding that they may fail in the event of a large aggregate rise in claims

• Customers carry aggregate tail risks

• Other insurers may choose high capitalisation, high pricing

The new name for City University Business School

Life insurance• Very long term mortality risks

• No possibility of precise quanitification

• Operate with conservative capitalisation– Should not restrict business, provided need

for capital is understood by sharholders

The new name for City University Business School

Summary

The new name for City University Business School

I have discussed• The rise of bank risk management

• bank economic capital: current practice

• A critique of this thinking– Practical issues– Cost of regulatory capital requirements– Skewness

• Two proposed performance measures

• Implications for insurance industry

The new name for City University Business School

Some findings:1. Regulatory capital is NOT expensive

2. RAROC can be a misleading measure of returns to shareholders

3. In order to create shareholder value.. Distinguish capital management (liquidity,

solvency) and risk-return tradeoffs

Modelling should take a back seat, to business application and credibility in the organisation

4. Similar issues in insurance: no problem with conservative capitalisation

The new name for City University Business School

Priority: better risk language• Simple enough to be understood throughout

the organisation

• Key concepts

1. Balance sheet commitment and liquidity• Not a pricing issue

2. Expected loss

3. Cost of carrying risk What reward do shareholders require for holding

risk? Use models where appropriate (market risk,

corporate credit risk, retail insurance)