Embed Size (px)

Citation preview

The Muddle Through Economy

A Presentation by

John Mauldin, Author of Bull’s Eye Investing

And the Editor of Thoughts from the Frontline

“I have a confession to make, a sinful predilection to divulge.

Every week as I sweep through my emails, inadvertently zapping

precious letters from my children… I find myself helplessly

clicking through to the weekly commentary of John Mauldin…

thus joining some million morbid folk avidly consuming his casual

doom-laden prose.”

- George Gilder -

Inflation-adjusted consumer spending is up Inflation-adjusted consumer spending is up 3.6%3.6%

Residential housing investment is up 13.2% Residential housing investment is up 13.2%

Capital-goods investment by business is up Capital-goods investment by business is up 13.9%13.9%

Spending on machine tools for heavy-Spending on machine tools for heavy-industryindustry

manufacturing is up a whopping 54.2%manufacturing is up a whopping 54.2%

Exports and imports are up nearly 11%Exports and imports are up nearly 11%

Here’s the Good News…

After-tax corporate profits are up 19%After-tax corporate profits are up 19%

Industrial production is up 5.2%Industrial production is up 5.2%

High-tech production is up 23.7%High-tech production is up 23.7%

Productivity has reached an astonishing Productivity has reached an astonishing 4.6% rate4.6% rate

Household wealth is up 11.1% hitting a Household wealth is up 11.1% hitting a record high of $45.9 trillionrecord high of $45.9 trillion

The GDP deflator is up only 2.2%The GDP deflator is up only 2.2%

The GDP deflator is up only 2.2%The GDP deflator is up only 2.2%

The core consumer-spending deflator The core consumer-spending deflator (excluding food and energy) is up only (excluding food and energy) is up only 1.4%1.4%

Interest rates are at 45-year lows, with Interest rates are at 45-year lows, with short-term rates at less than 2%short-term rates at less than 2%

15-year mortgage rates are just above 5%15-year mortgage rates are just above 5%

Home ownership stands at a record 69.2%Home ownership stands at a record 69.2%

R & D Spending is Booming

While regularly incurring trade gaps and budgetary deficits, our economy has grown since the early 1980s from a level, depending on dollar valuation, between one-fifth and one-fourth of global GDP to close to one-third of global GDP last year. During this upsurge entirely unexpected by the same economists now advising Sen. Kerry, U.S. per capita GDP surged from 4.7 times per capita global GDP in 1980 to 6.5 times per capita global GDP in 2003.

The U.S. created some 36 million net new jobs at even higher levels of productivity and earnings, while Europe and Japan created scant employment at all outside of government and entered a productivity slump that continues today. Meanwhile, the U.S. won the Cold War, and since 1990 its stock markets soared from less than one-third to roughly one-half of global market cap.

The net wealth of U.S. households in real terms trebled to all-time records ($45.9 trillion at last report). Debt has been shrinking as a share of overall national assets, which now stand at a level near $80 trillion.

Why did we experience such an economic renaissance after the malaise of the 70’s?

Because we had the

Perfect Economic Environment

Perfect Economic EnvironmentPerfect Economic Environment

1. Ronald Reagan’s Tax Cuts

2. Paul Volker’s war on inflation and a two decades long drop in interest rates

3. The Birth of the Next New Thing –

The Information Age

4. The lowest Stock Market valuations in decades – which rose five times in the next 20 years

Perfect Economic EnvironmentPerfect Economic Environment

5. The Evolution of the US Financial Markets

It also brought about significant imbalances in the markets

resulting in the Stock Market Bubble.

When coupled with 9/11, we should have seen one of the worst

recessions in five decades.

Why didn’t we?

Because We had a Shock and Awe Arsenal of Recession Fighting

Weaponsa. George Bush’s Tax Cuts

b. Alan Greenspan’s Aggressive Interest Rate Cuts

c. The Stimulus of Deficit Spending

d. Massive Mortgage Refinancing

The Muddle Through Economy

- A long period of Below Trend Growth caused by a series of economic headwinds and the potential return of Stagflation

When we come to the next recession, the Recession Fighting Arsenal is bare of Conventional Weapons

a. No more tax cuts

b. Mortgage Refinancing is over

c. No more deficit spendingd. Only a few interest rate cut bullets left

Headwind # 1

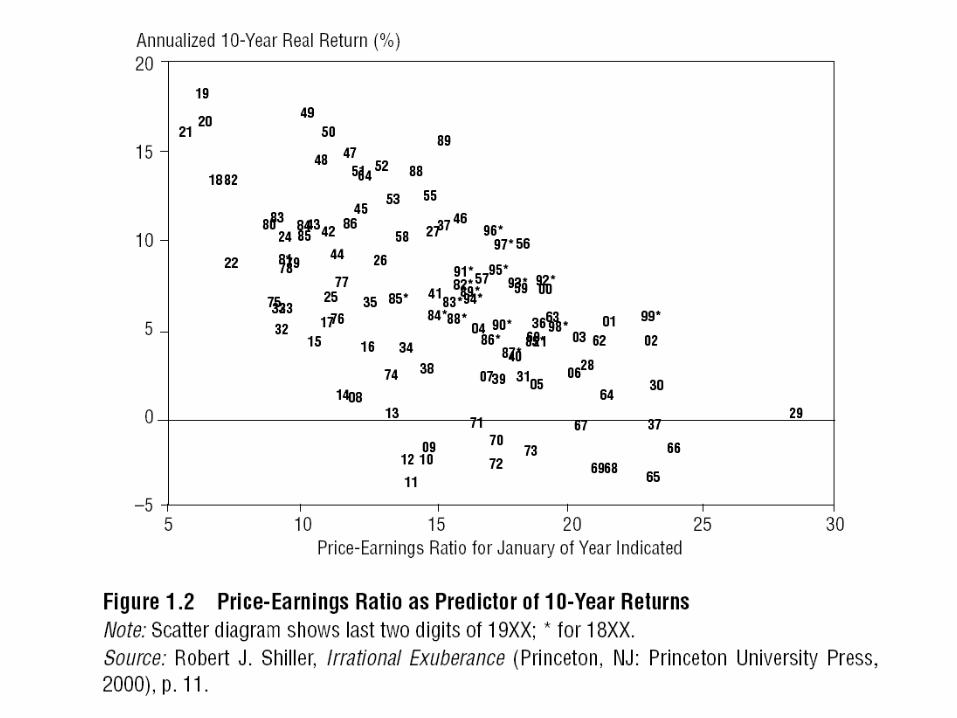

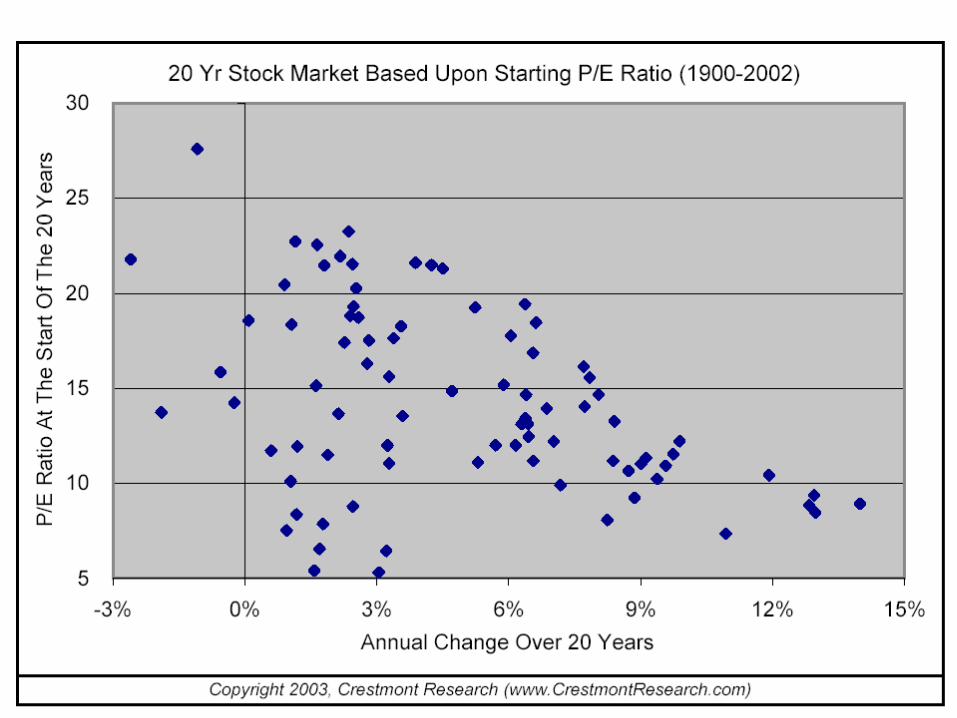

A Secular Bear Market

Headwind # 2

A period when overall market valuation falls rather than rises.

If valuations were at 1982 levels, the S&P 500 would be below 450

Over the Long Run, Value is King

They all start with period’s of high price to earnings (P/E) ratio’s

Secular Bear Markets

Consumer Spending Will Slow Down

Headwind # 3a. A recession will mean a falling stock market and falling retirement accounts. Consumers,

especially Boomers, will have to save more for retirement.

b. Rising oil prices

c. Little Room for Increased Debt

Source: Hoisington Investment Management Company

Source: Northern Trust

d. We have tapped the home equity lines

e. Income Growth is Slowing

Source: Bureau of Labor Statistics and Hoisington

Headwind # 4We are Approaching Stall Speed on the Jobs Arena

We need roughly 150,000 jobs per month to simply meet the growth in population

a. Lack of corporate investment

b. Low average hours

c. International Labor Arbitrage

d. Lack of job growth means lack of consumer spending growth

Headwind # 5Interest Rate Will Rise Over the

Longer Terms

a. This will impact the housing market and home values

b. Rising rates hurt consumers and corporate profits

Headwind # 6The Federal Reserve

The use of Unconventional Weapons

Will bring us to a falling dollar and our old friend Stagflation

Headwinds # 7 & 8

The Dollar and The Trade Deficit

Headwind # 9

The Shakeout from the Information Age

Economy Innovation Growth Boom Shakeout Maturity Boom

Agricultural / Commerce -- -- -- -1809

Cotton / Textile 1762-1794 1794-1834 1834-1843 1843-1861

Railroad / Industrial 1831-1847 1847-1888 1888-1895 1895-1917

Mass Production 1882-1908 1908-1937 1937-1944 1944-1973

Information 1961-1981 1981-2007? 2007-2014? --

Why I am a Long Term Optimist