Embed Size (px)

Citation preview

1

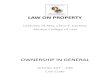

The most popular European Model:

the Ownership Unbundling (OU)

Totally separated companies (generation and supply

activities not compatible with transmission)

No common shareholders between generation/supply

activities and transmission

No common person in the management or boards of the

companies

The EU law says:

“it is clearly an effective and stable way to solve the inherent conflict of

interests between producers, suppliers and transmission system operators”,

“it is the most effective tool by which to promote investments in infrastructure

in a non-discriminatory way, fair access to the network for new entrants and

transparency in the market.”

[EU law 2009/72/EC]

But not the only way

2

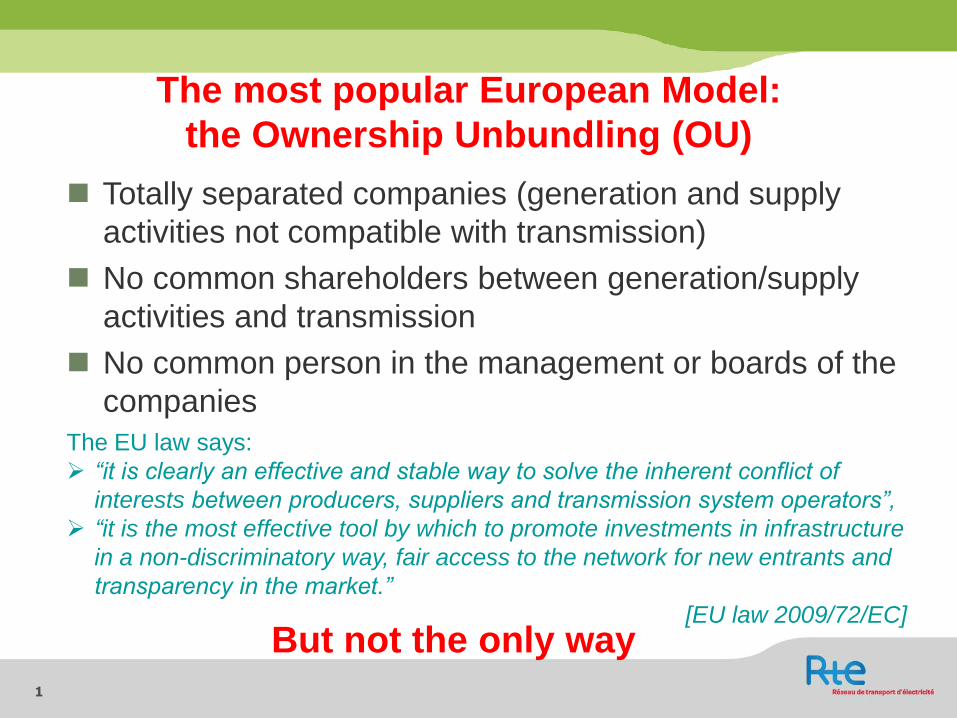

3 options in Europe

■ Ownership Unbundling (OU) : clear-cut separation

■ Independent System Operator (ISO) : a fully unbundled

System Operators without the grid assets (still belonging

to an integrated company)

■ Independent Transmission Operators (ITO) : a

Transmission System Operator owning the assets and

belonging to a vertically integrated company, with special

rules to guarantee its independence

RTE is an ITO

3

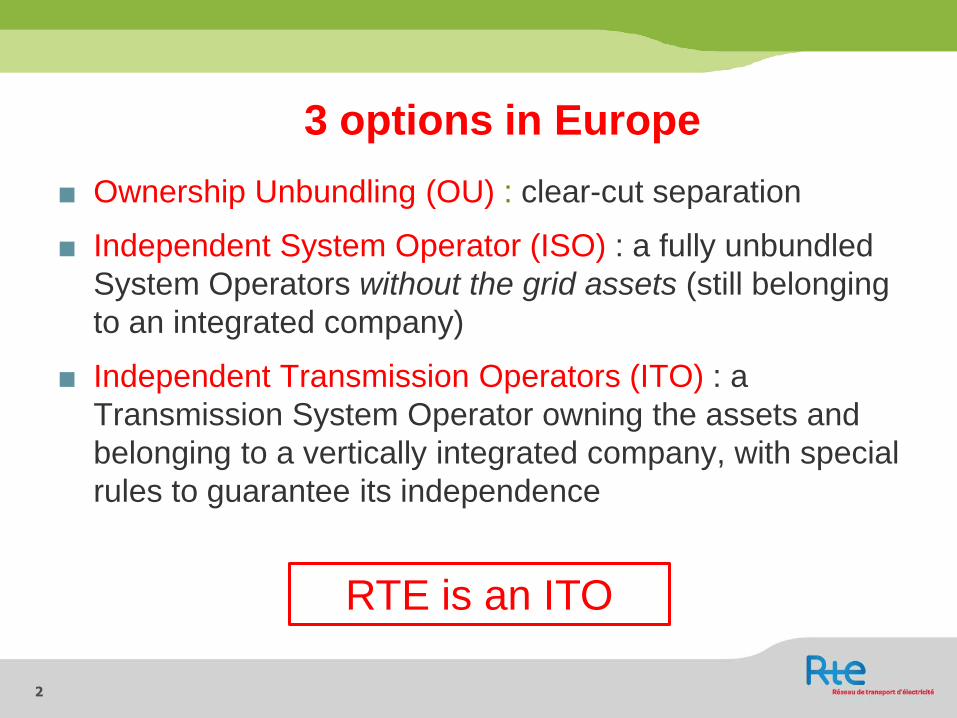

OU

ITO

ISO

Coexistence of two models

Transmission System Operators : the 3 models in Europe

(OU)

4

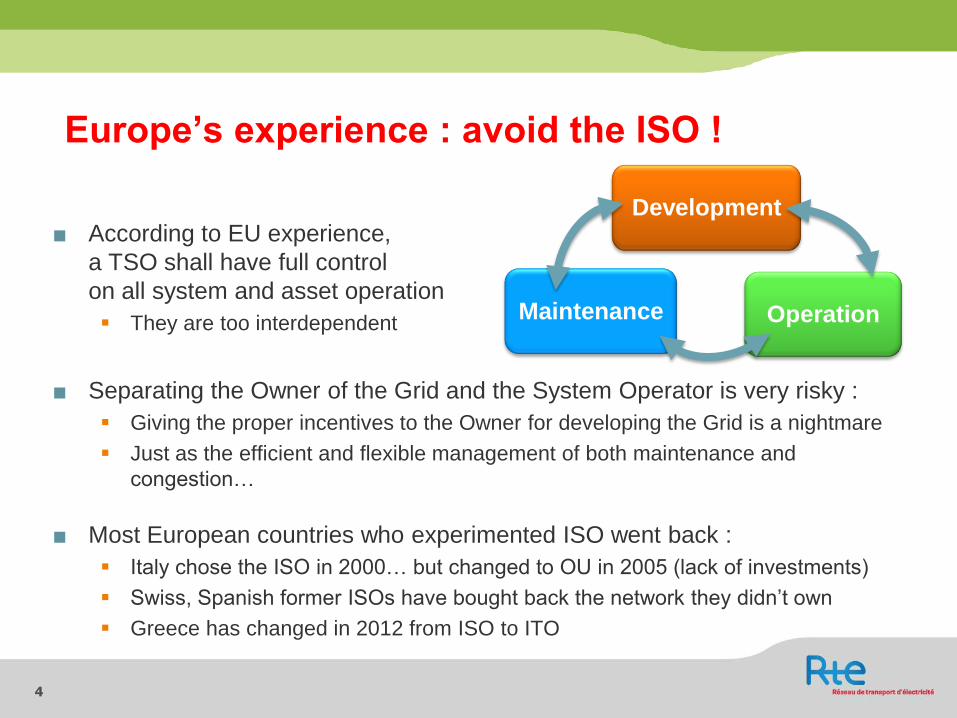

Europe’s experience : avoid the ISO !

■ According to EU experience,

a TSO shall have full control

on all system and asset operation

They are too interdependent

■ Separating the Owner of the Grid and the System Operator is very risky :

Giving the proper incentives to the Owner for developing the Grid is a nightmare

Just as the efficient and flexible management of both maintenance and

congestion…

■ Most European countries who experimented ISO went back :

Italy chose the ISO in 2000… but changed to OU in 2005 (lack of investments)

Swiss, Spanish former ISOs have bought back the network they didn’t own

Greece has changed in 2012 from ISO to ITO

Maintenance Operation

Development

5

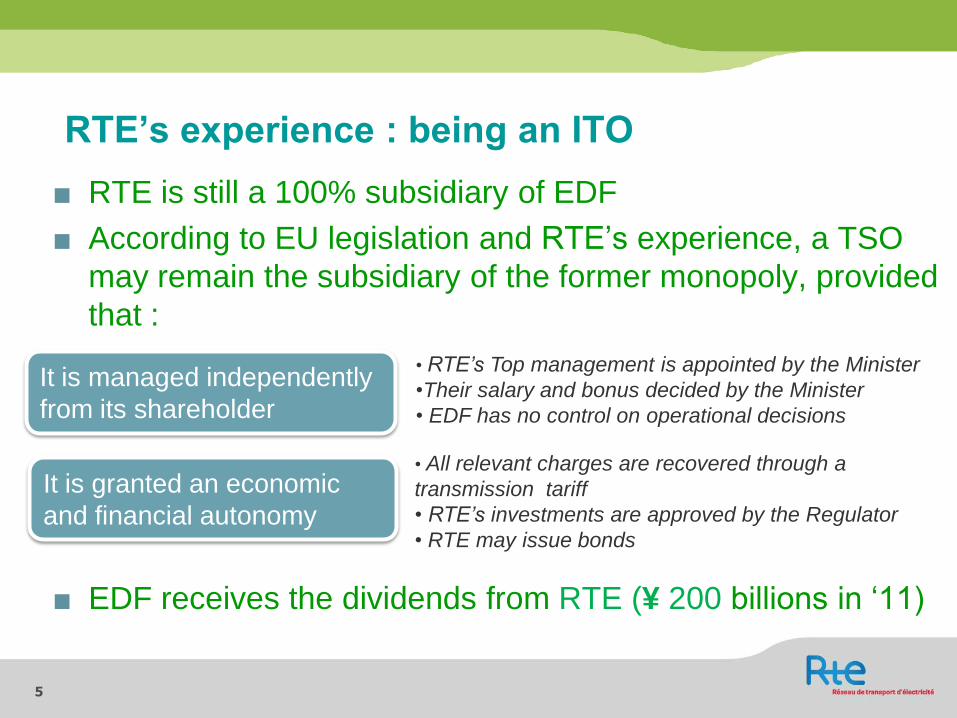

RTE’s experience : being an ITO

■ RTE is still a 100% subsidiary of EDF

■ According to EU legislation and RTE’s experience, a TSO

may remain the subsidiary of the former monopoly, provided

that :

■ EDF receives the dividends from RTE (¥ 200 billions in ‘11)

It is managed independently

from its shareholder

• RTE’s Top management is appointed by the Minister

•Their salary and bonus decided by the Minister

• EDF has no control on operational decisions

It is granted an economic

and financial autonomy

• All relevant charges are recovered through a

transmission tariff

• RTE’s investments are approved by the Regulator

• RTE may issue bonds

6

A pragmatic step-by-step approach

■ In 2000: RTE as a division of EDF, with an independent

management reporting to the Regulator

■ In 2004: RTE becomes a company, its legal name is « RTE

EDF Transport »

■ In 2012: RTE changes its legal name into « RTE » and is

certified by the Regulator.

Supervisory Board: 4 members appointed by the government,

4 by EDF, 4 elected by RTE’s employees

Executive Board « the only body competent for decisions and

actions related to operation, maintenance and development of

the French transmission grid and power system »

7

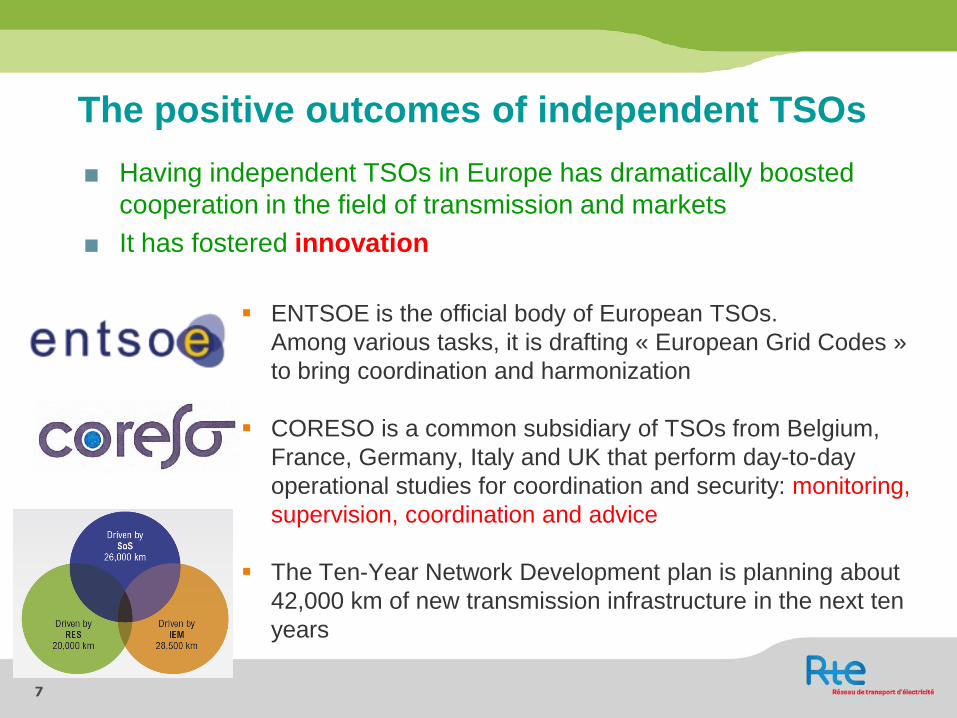

The positive outcomes of independent TSOs

■ Having independent TSOs in Europe has dramatically boosted

cooperation in the field of transmission and markets

■ It has fostered innovation

ENTSOE is the official body of European TSOs.

Among various tasks, it is drafting « European Grid Codes »

to bring coordination and harmonization

CORESO is a common subsidiary of TSOs from Belgium,

France, Germany, Italy and UK that perform day-to-day

operational studies for coordination and security: monitoring,

supervision, coordination and advice

The Ten-Year Network Development plan is planning about

42,000 km of new transmission infrastructure in the next ten

years

8

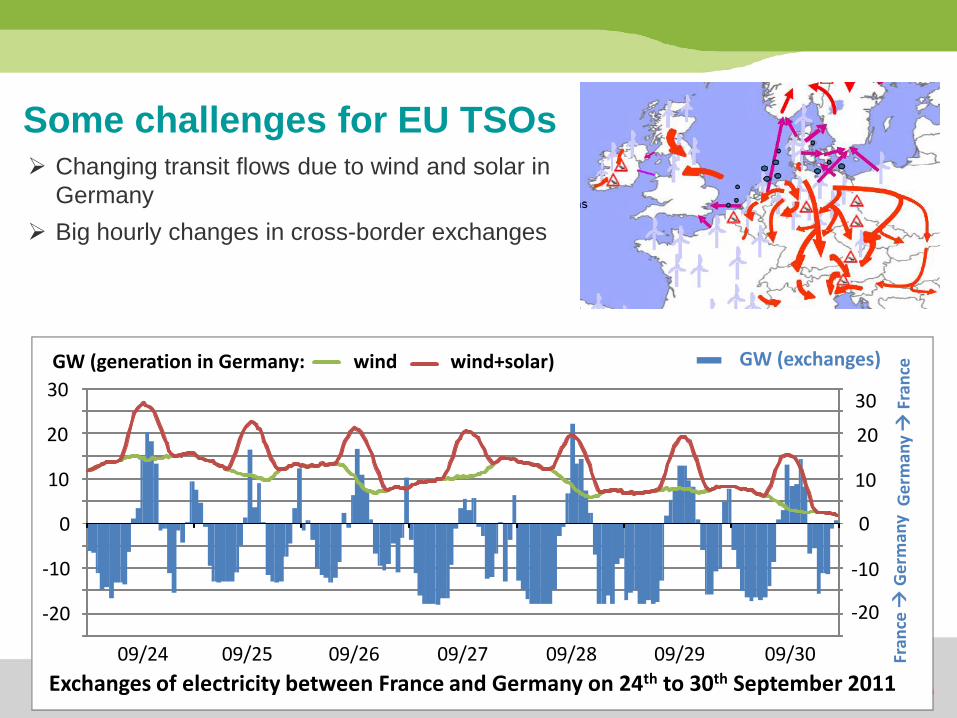

Some challenges for EU TSOs

-20

-10

0

10

20

30

GW (generation in Germany: wind wind+solar)

09/24 09/25 09/26 09/27 09/28 09/29 09/30

GW (exchanges)

Exchanges of electricity between France and Germany on 24th to 30th September 2011

Fran

ce

Ge

rman

y G

erm

any

Fra

nce

Changing transit flows due to wind and solar in

Germany

Big hourly changes in cross-border exchanges

30

20

10

0

-10

-20

9

The question of « independent Regulators » ■ Transmission System Operators must be regulated (not

in competition on a given territory)

■ The EU law asks for Regulators « independent from any

other public or private entity »

■ Necessary in Europe because of many state-owned

utilities (conflict of interest for several governments)

Potential inconsistencies between government and

regulator’s strategies and decisions

When creating the Regulator, difficulty to find competent

and « independent » staff: long learning process

Some EU Regulators are weak

Drawbacks:

10

Conclusion: it works !

■ A well shared opinion that current situations (extensive

cross-border trade, 94 GW of wind power installed

capacity, 50 GW of solar in Europe…) would be impossible

to manage with the old organization

■ A better power system security (despite 2 major incidents in

the last 10 years… initiated in still integrated companies!)

■ A necessary and continuous evolution of the rules to make

possible the changes in the European energy policy

■ A cooperative spirit between TSOs, regulators and market

parties

■ Innovation has been stimulated

11

Are Japan and Europe similar? ■ Both at a key change in their energy policy

■ Both need to increase inter-regional exchanges and improve

coordination

■ Both need for major grid investments

■ Same tradition of integrated utilities…

■ …and reluctance to change a very complex industry

But… Different culture

Japan is an archipelago with far less loop flows than EU

One single government in Japan: no need for an Independent

Regulator, possible regulation by the Ministery

Stronger links between employees and their companies

12

Key (and humble) recommendations

■ Keeping System Operation together with transmission

assets is crucial

■ Unbundling with the ITO model is a reasonable, well

functioning evolution

■ Coordination through a ‘CORESO type’ entity, in charge

of monitoring and advising for operation for congestion

management and global security, is very efficient

■ First class regulation needed, an opportunity for a

specific Japanese governance to avoid drawbacks of

Independent Regulators, because no state-owned utility

Most important:

■ The good solution will be… a Japanese one

13

+ THANK YOU

www.rte-france.com