Embed Size (px)

Citation preview

1Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

The Mortgage

Lending Process

Chapter 2

2Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter Objectives

• Define the various roles mortgage professionals play

• Distinguish between pre-approval and pre-qualification

• Identify the steps in the loan process

• Discuss the information necessary to complete a standard loan application

• Identify criteria for evaluating borrowers

• Calculate housing and debt-to-income ratios

• Explain credit scoring

• Describe underwriting criteria for residential mortgage loans

3Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Mortgage Professional Functions

• Origination– Making or initiating a new loan

– Initial contact with borrower

– Ordering credit report and other required documentation

• Loan Processing– Verifying information in the loan file

– Employment and other verification

– Coordination of loan process

4Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Mortgage Professional Functions

• Underwriting– Evaluating risk and deciding whether to make a

new loan, and if so, on what terms

– Done by the funding source

– Evaluates income, credit scores/history, appraisals, job history, collateral, etc.

• Servicing– Continued maintenance of loan after closing

– Done by lender, servicing company, or other

– Mortgage and escrow statements, collecting payments, and pursuing late payments

5Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

The Loan Process

• Loan Inquiry

– Before person makes decision to apply

– MLOs must provide APR for interest rate inquiries

• Pre-Qualification

– Pre-determine what a person may be able to borrow

– MLO gathers info; no guarantee approval; not binding

– Does not require disclosure

• Pre-Approval

– Lender renders decision that person can (or cannot)

receive financing and for what amount

– Does NOT trigger mandated “complete application”

disclosures

6Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

The Loan Process

• Traditional Steps

1. Consulting with the mortgage loan originator

2. Completing a loan application

3. Processing a loan application

4. Analyzing the borrower and property

7Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Consulting with the MLO

• Best Practices Before Application

– Don’t interject personal judgement

– Inform customers its their decision

– Get help understanding policies as needed

– Adhere to MLO Compensation Rule

• Initial Discussions

– Gather information, identify options, provide

documentation

– Ensure sales contract can be complied with

8Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Consulting with MLO - Interest Rates

• Interest Rate– Amount charged by lender to borrower for use of the

lender’s assets, expressed as a percentage of the loan

amount (the principal)

• Basis Point– 1/100th of a percentage point

• Par Rate– Rate without points/discounts lenders offer only to

mortgage brokers

• Rate Lock– Lender commitment to specific interest rate for specific

period of time

• Float– Borrower chooses not to lock in the interest rate

9Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Consulting with MLO - Fees

• Loan Fees– Processing fees such as credit report and appraisal fee

– Fees paid at closing such as title insurance and recording fee

• Lender’s Return– Total amount lender can make from a loan in relation to amount

invested

– No compensation based on loan terms, except loan amount

• Origination Fees– Covers administrative costs of making and processing loan

• Points– 1% of the loan amount

– Origination points cover administrative costs

– Discount points buy down interest rate

• Yield Spread Premium– Lower upfront cash expense for higher monthly payments

10Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Qualifying Standards

• Two Qualifying Standards

– Housing expense ratio

– Total debt-to-income ratio

– Borrower must generally qualify under both ratios

• PITI Key Element

– Principal

– Interest

– Taxes (property and perhaps special assessment)

– Insurance (homeowners, mortgage, flood if applicable)

– Required homeowner association fees must be counted

11Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

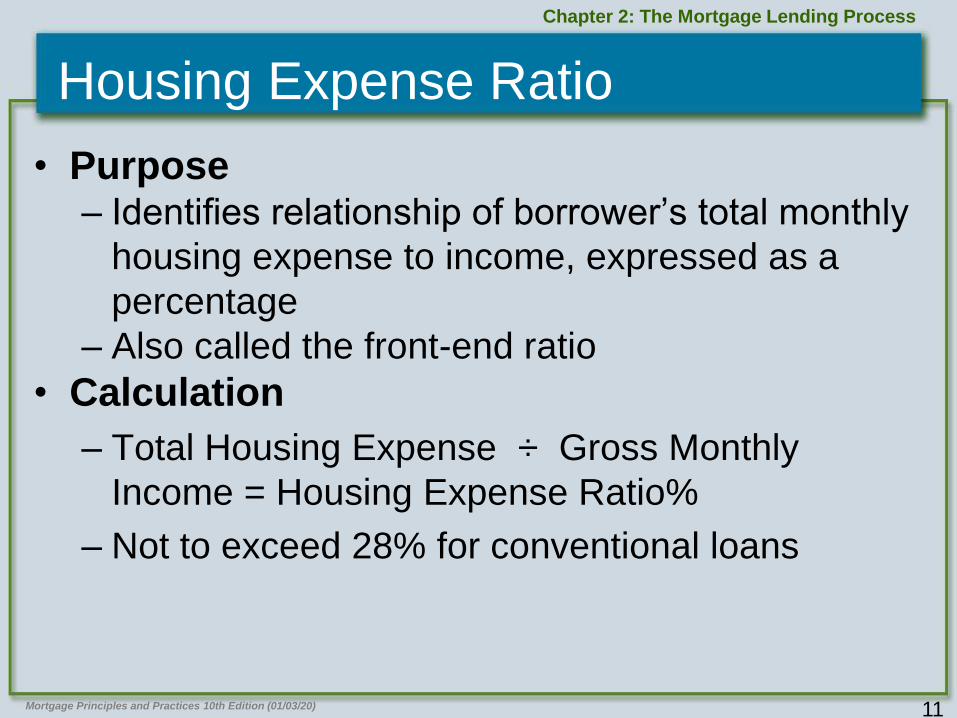

Housing Expense Ratio

• Purpose– Identifies relationship of borrower’s total monthly

housing expense to income, expressed as a

percentage

– Also called the front-end ratio

• Calculation

– Total Housing Expense ÷ Gross Monthly

Income = Housing Expense Ratio%

– Not to exceed 28% for conventional loans

12Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

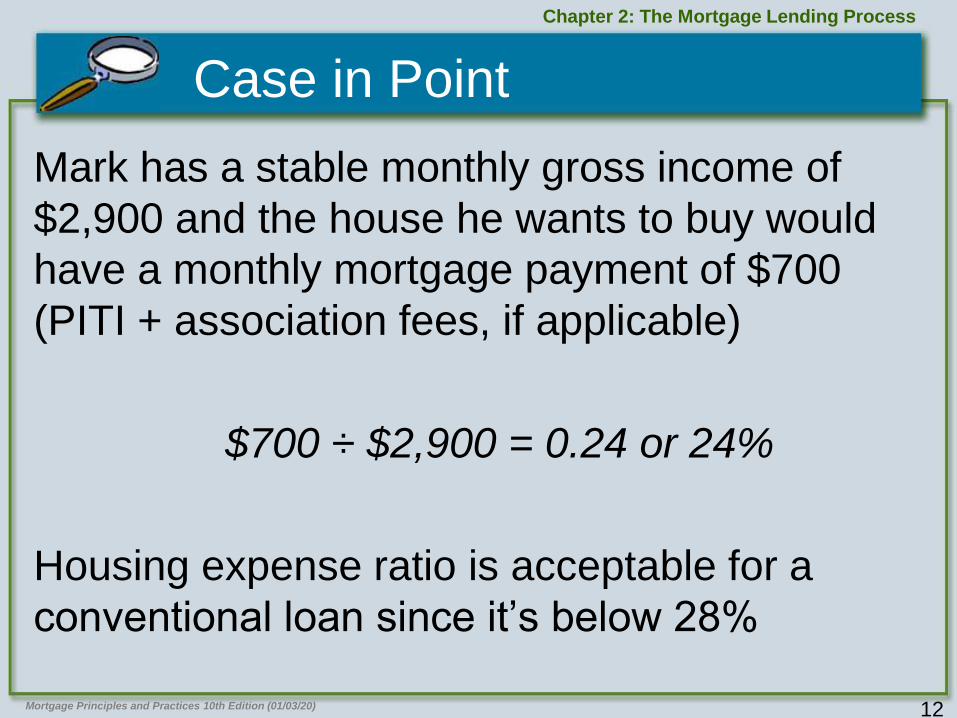

Case in Point

Mark has a stable monthly gross income of

$2,900 and the house he wants to buy would

have a monthly mortgage payment of $700

(PITI + association fees, if applicable)

$700 ÷ $2,900 = 0.24 or 24%

Housing expense ratio is acceptable for a

conventional loan since it’s below 28%

13

Total Debt-to-Income Ratio

• Purpose

– Relationship of borrower’s total monthly debt

obligations (PITI + long-term debts) to income,

expressed as a percentage

– Also called the back-end ratio, DTI, or total debt

service ratio

• Calculation

– Total Debt ÷ Gross Monthly Income = Total

Debt-to-Income Ratio %

– Not to exceed 36% for conventional loans

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

14Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Case in Point

$2,900 Stable Monthly Gross Income

$700 Proposed Mortgage Payment

$225 Auto Payment (18 payments left)

+ $100 Child Support

$1,025 Total

$1,025 ÷ $2,900 = 0.35 or 35%

Total DTI ratio is acceptable for a conventional loan

15

Maximum Mortgage Payment

• Determine Monthly Payment

– Using Housing Expense Ratio

• Borrower’s stable monthly income x maximum housing

expense ratio

• 0.28 conventional loan maximum housing expense ratio

– Using DTI Ratio

• Borrower’s stable monthly income x maximum total debt-to-

income ratio

• 0.36 conventional loan maximum DTI ratio

– Identifies allowable amount of long-term debt

– DTI more realistic measure of ability to support loan

payment

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

16

Compensating Factors

• Consideration of Compensating Factors

– Underwriting exceptions when strong borrower

qualifications offset weaker qualifications

– For example:

• Back-end debt to income ratio of 40% (in

excess of 36% limitation)

• Has significant cash reserves and/or is

borrowing at a low LTV

– Documentation of compensating factors crucial

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

17Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

2.1 Apply Your Knowledge

Mary Smith has a stable monthly gross income of

$3,200. She has three long-term monthly debt

obligations: $220 car payment, $75 personal loan

payment, and $50 revolving charge card payment.

1. What’s the maximum monthly mortgage

payment for which she can qualify?

2. What steps could Mary take to qualify for a

larger mortgage payment?

Pay off installment debt to reduce long-term

monthly obligations

$807

18Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Complete the Loan Application

• Purpose– Detail borrower’s history, trends, and attitude

– Attempt to predict future loan repayment

behavior

• Uniform Residential Loan Application – Fannie Mae Form 1003

– Freddie Mac Form 65

– May be in writing or electronic

• Redesigned URLA– Effective November 1

– More efficient data collection

– Current 1 form versus redesigned 5 forms

19

Redesigned URLA – Which Form to Use

• Redesigned URLA Form to Use

– One Borrower - Borrower Information form

– Two or More Borrowers

• One URLA Borrower Information form and Additional

Borrower form for each additional borrower, or

• A Borrower Information form for each borrower (don’t

duplicate info)

• Co-Borrower

– Joint ownership interest in the security property

as indicated on the title

– Must have acceptable credit historyMortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

20Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

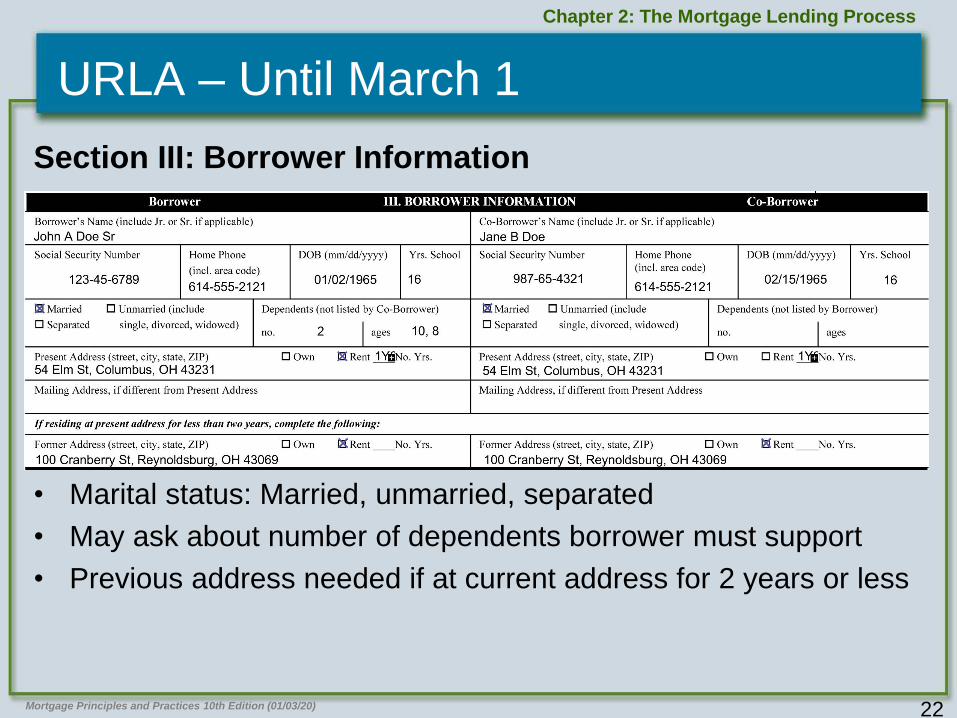

URLA – Until March 1

• Type of loan

• Loan amount

• Rates

• Term

Section I: Type and Terms

21Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA – Until March 1

• Do not assume or advise on how title should be held

• Occupancy determines interest rate, available programs, and overall risk

• FHA loans require bona fide occupancy as principal residence within 60 days

then for at least 12 months

Section II: Property and Purpose

22Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA – Until March 1

• Marital status: Married, unmarried, separated

• May ask about number of dependents borrower must support

• Previous address needed if at current address for 2 years or less

Section III: Borrower Information

23Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA – Until March 1

• Current and previous employment over two-year period

• Self-employed: Owning 25% or more of the business

Section IV: Employment Information

24Mortgage Principles and Practices 10th Edition (01/03/20)

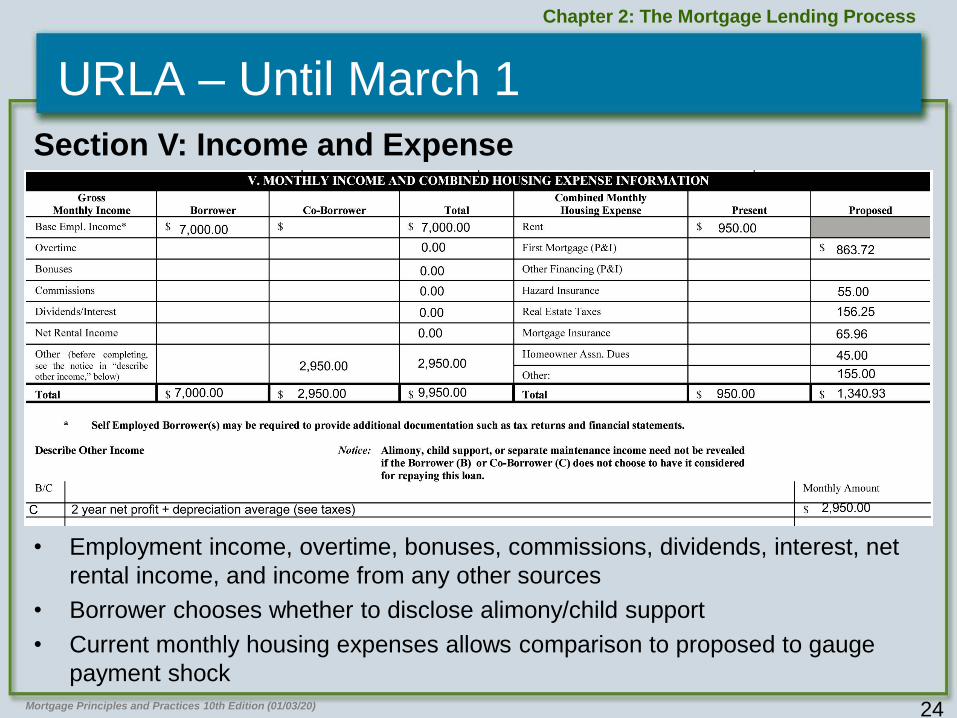

Chapter 2: The Mortgage Lending Process

URLA – Until March 1

• Employment income, overtime, bonuses, commissions, dividends, interest, net

rental income, and income from any other sources

• Borrower chooses whether to disclose alimony/child support

• Current monthly housing expenses allows comparison to proposed to gauge

payment shock

Section V: Income and Expense

25Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

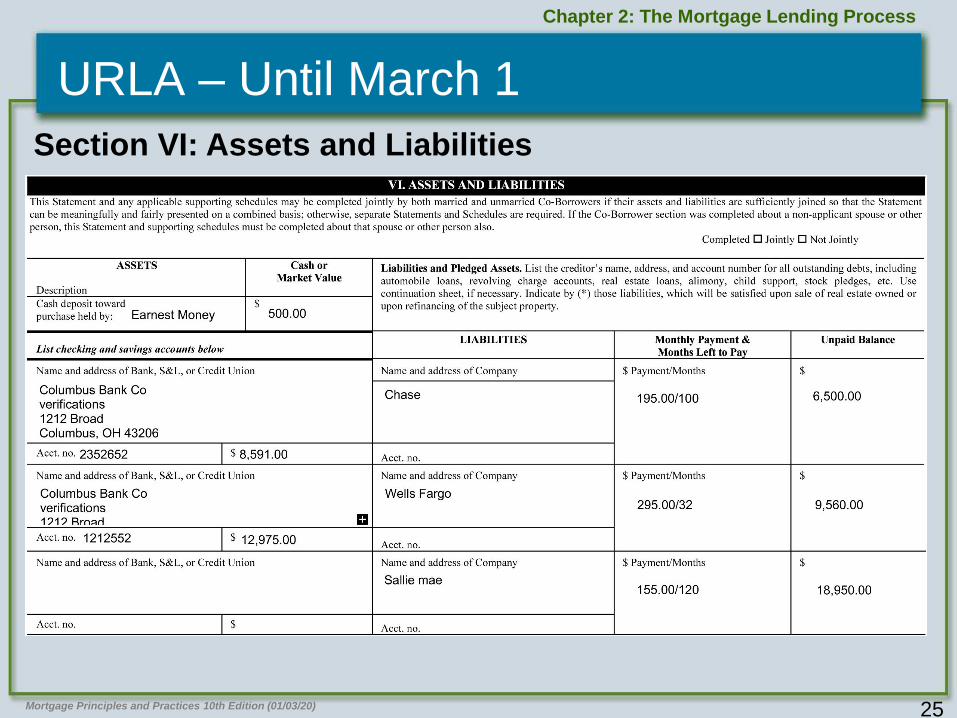

URLA – Until March 1

Section VI: Assets and Liabilities

26Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA – Until March 1

• Assets: Items of value

• Liabilities: Financial

obligations

• Debts: Any recurring

monetary obligation that will

not be cancelled

• Installment loan with 10 or

fewer monthly payments

left likely disregarded

• Pledged assets up to

amount owed

• Alimony or child support

to be paid

• Net worth: Subtract

liabilities from total assets

Section VI: Assets

and Liabilities

27Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

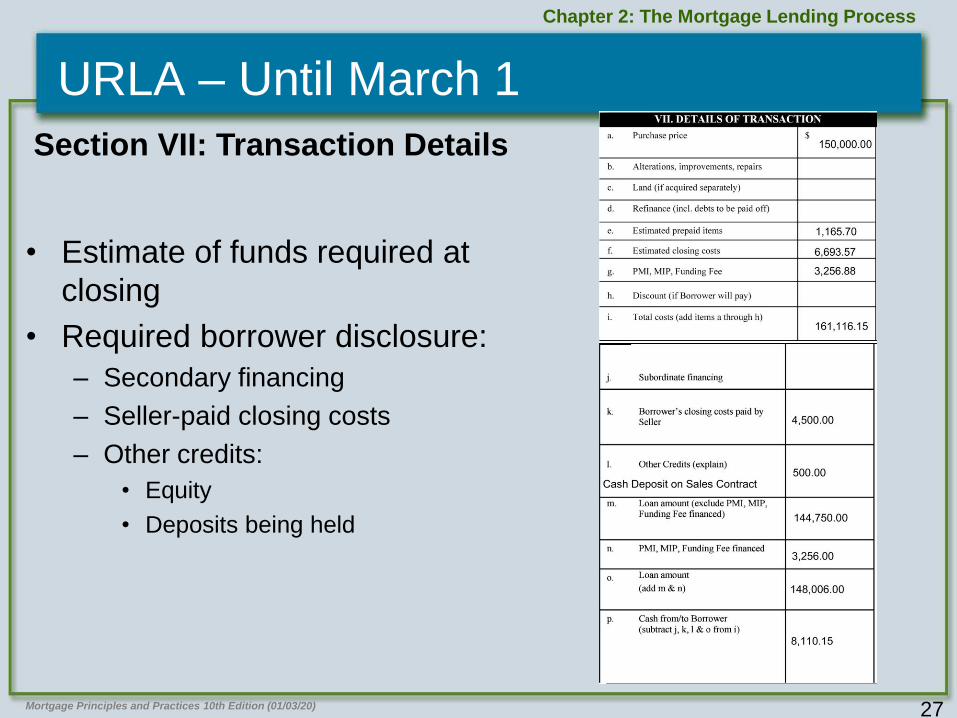

URLA – Until March 1

• Estimate of funds required at

closing

• Required borrower disclosure:

– Secondary financing

– Seller-paid closing costs

– Other credits:

• Equity

• Deposits being held

Section VII: Transaction Details

28Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA – Until March 1

• Outstanding judgments,

bankruptcies, foreclosures,

lawsuits, etc.

• Delinquency, defaults on any

federal debt, other loan

• Alimony/child support

obligations

• Borrowed funds used for any

part of down payment

• Co-signers on other debts

• Citizen/permanent resident

• Occupy property as a primary

residence

• Ownership interest in other

properties in the past three

years

Section VIII: Declarations

29Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

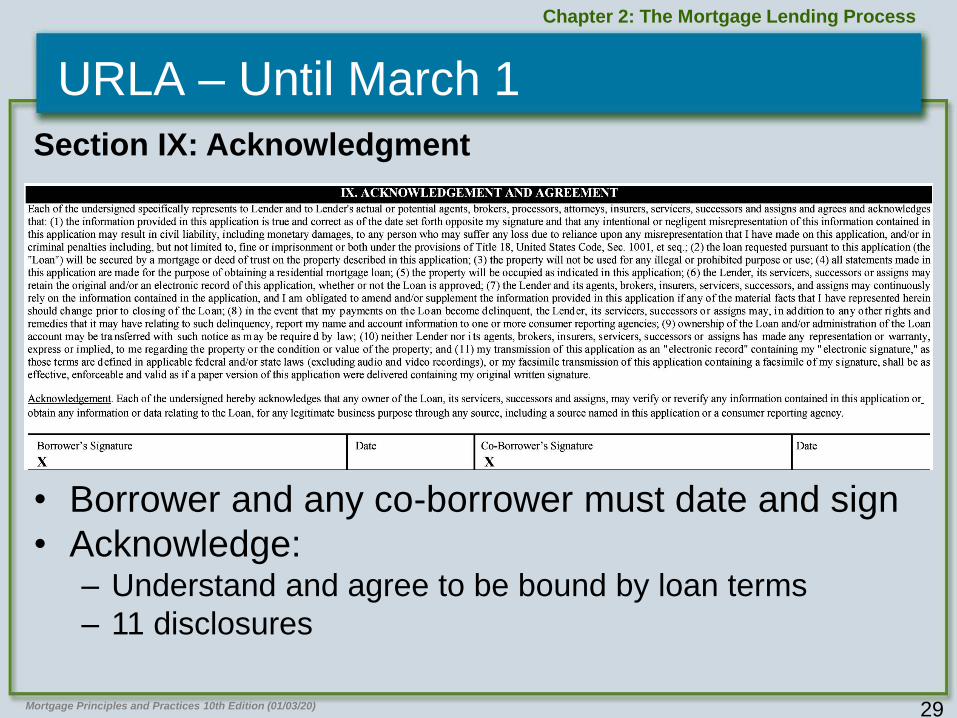

URLA – Until March 1

• Borrower and any co-borrower must date and sign

• Acknowledge:– Understand and agree to be bound by loan terms

– 11 disclosures

Section IX: Acknowledgment

30Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA – Until March 1

• Monitors compliance with equal credit/housing laws

• MLO must note ethnicity, race, sex– Applicant declines, MLO must note as possible

• MLO must sign application, NMLS unique ID

Section X: Government Monitoring

31

URLA - Effective March 1

• URLA effective March 1, 2021

• Sections

1. Borrower Information

2. Financial Information – Assets and Liabilities

3. Financial Information – Real Estate

4. Loan and Property Information

5. Declarations

6. Acknowledgment and Agreements

7. Military Service

8. Demographic Information

9. Loan Originator Information

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

32Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

• Similar to Section III of current URLA

• Provide information regarding citizenship status

• If Unmarried Marital Status is selected, use Unmarried Addendum form

• Email address has been added and the number and name of any

additional borrowers must be identified.

Section 1: Borrower Information

33Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

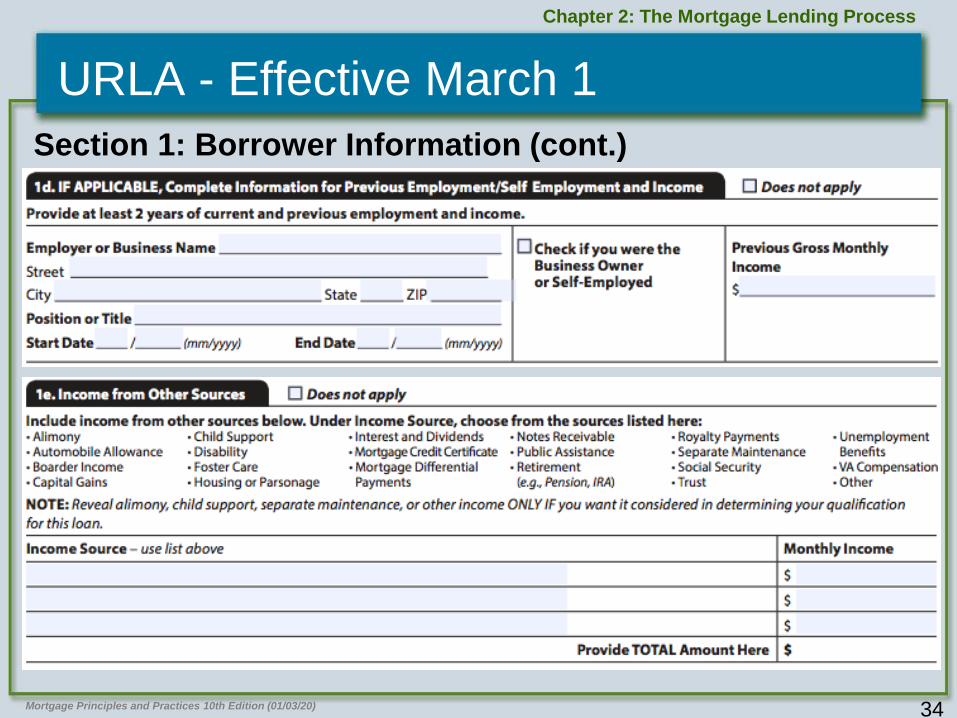

Section 1: Borrower Information (cont.)

34Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

Section 1: Borrower Information (cont.)

35Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

• Similar to Section VI of current URLA

• Enhancements

o Instructions

o Lists provided on the form

o Subsections

• Net worth is not calculated

• Use the Continuation Sheet if more space is needed

Section 2: Financial Information-Assets and Liabilities

36Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

Section 2: Financial Information-Assets and Liabilities

(cont.)

37Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

Section 2: Financial Information-Assets and Liabilities

(cont.)

38Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

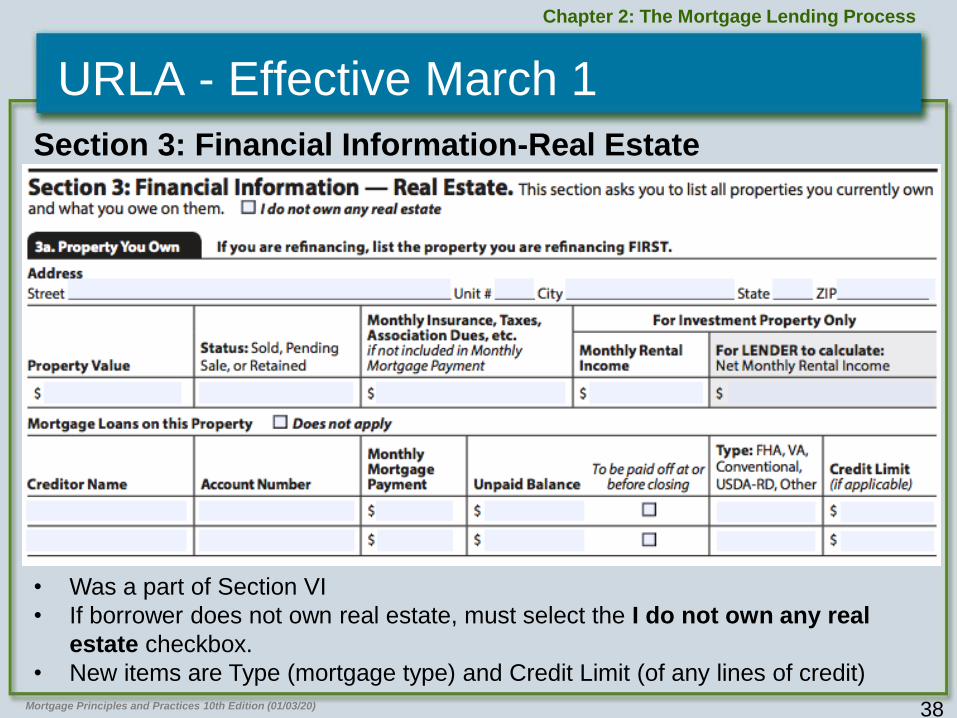

• Was a part of Section VI

• If borrower does not own real estate, must select the I do not own any real

estate checkbox.

• New items are Type (mortgage type) and Credit Limit (of any lines of credit)

Section 3: Financial Information-Real Estate

39Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

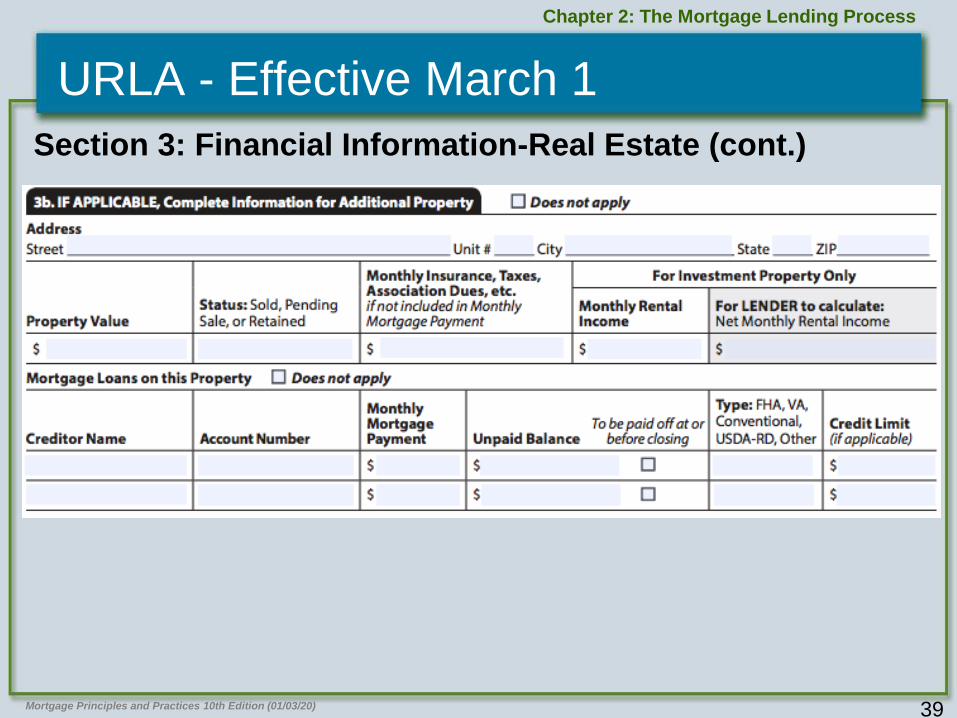

Section 3: Financial Information-Real Estate (cont.)

40Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

Section 3: Financial Information-Real Estate (cont.)

41Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

• Similar to Section II

• List other liens on the property

Section 4: Loan and Property Information

42Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

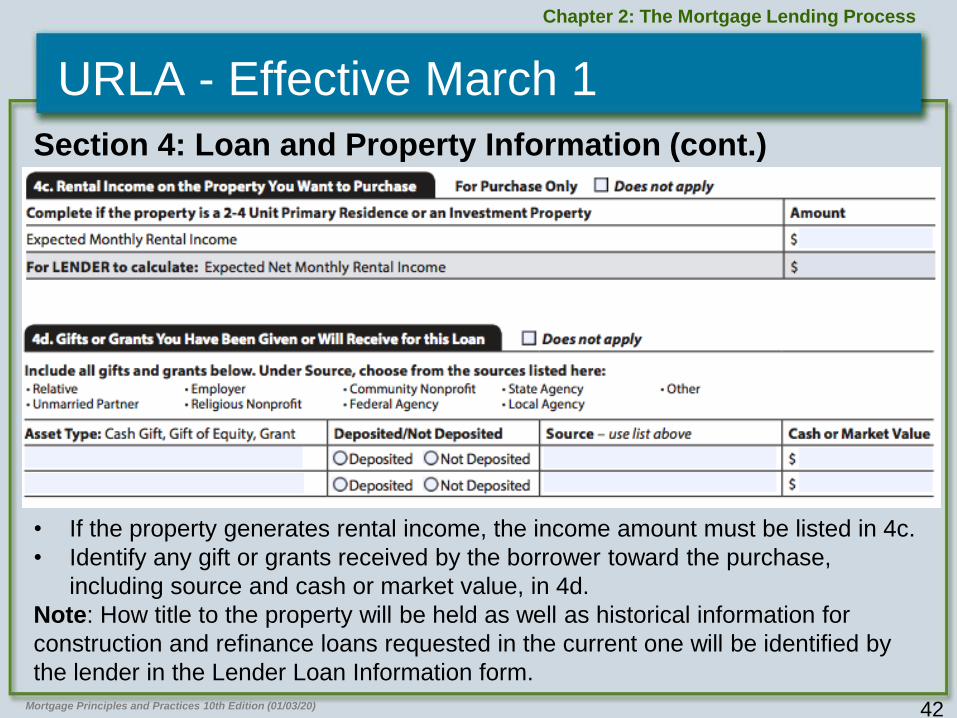

• If the property generates rental income, the income amount must be listed in 4c.

• Identify any gift or grants received by the borrower toward the purchase,

including source and cash or market value, in 4d.

Note: How title to the property will be held as well as historical information for

construction and refinance loans requested in the current one will be identified by

the lender in the Lender Loan Information form.

Section 4: Loan and Property Information (cont.)

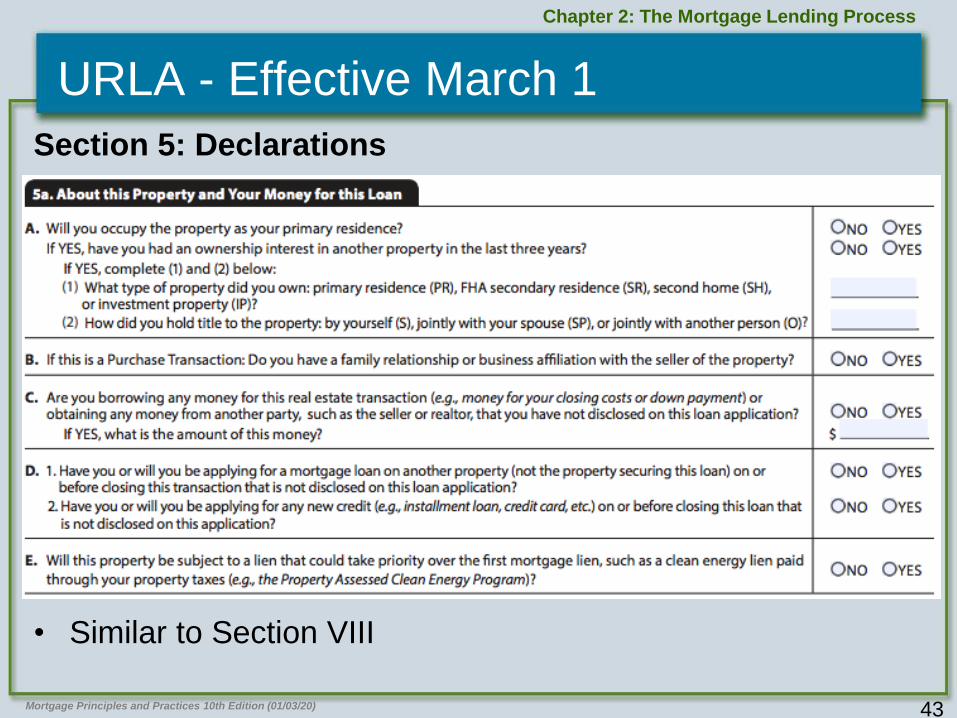

43Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

• Similar to Section VIII

Section 5: Declarations

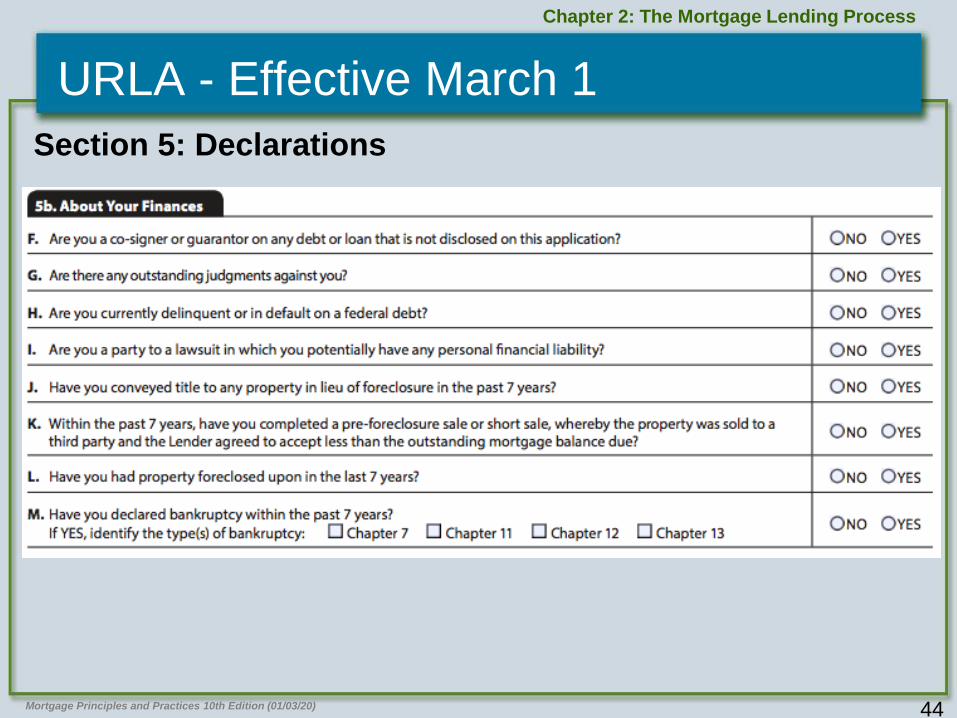

44Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

Section 5: Declarations

45Mortgage Principles and Practices 10th Edition (01/03/20)

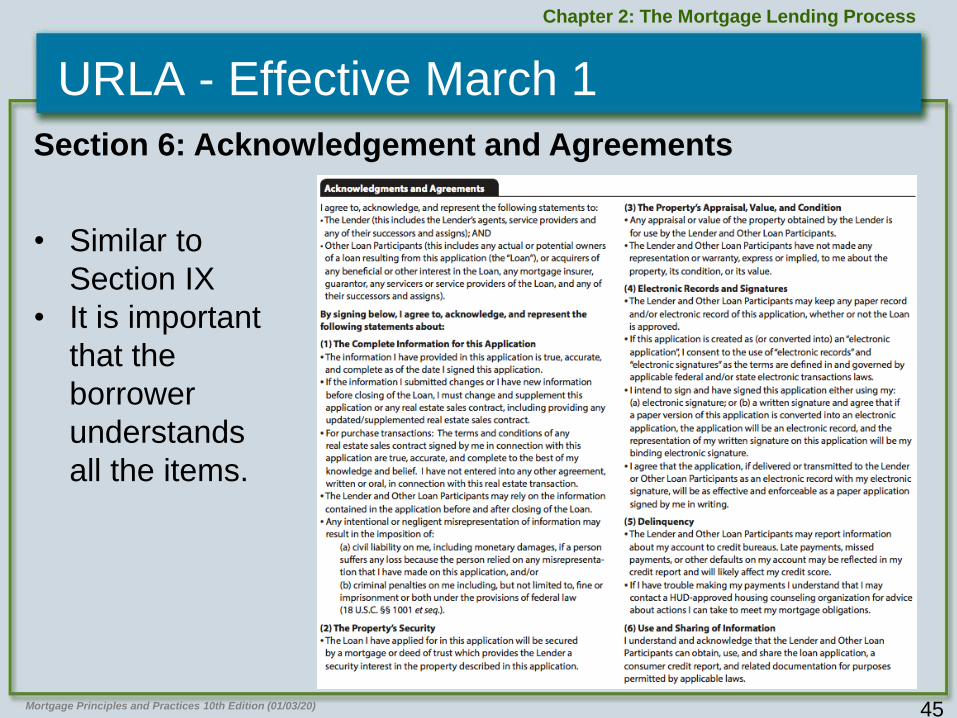

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

• Similar to

Section IX

• It is important

that the

borrower

understands

all the items.

Section 6: Acknowledgement and Agreements

46Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

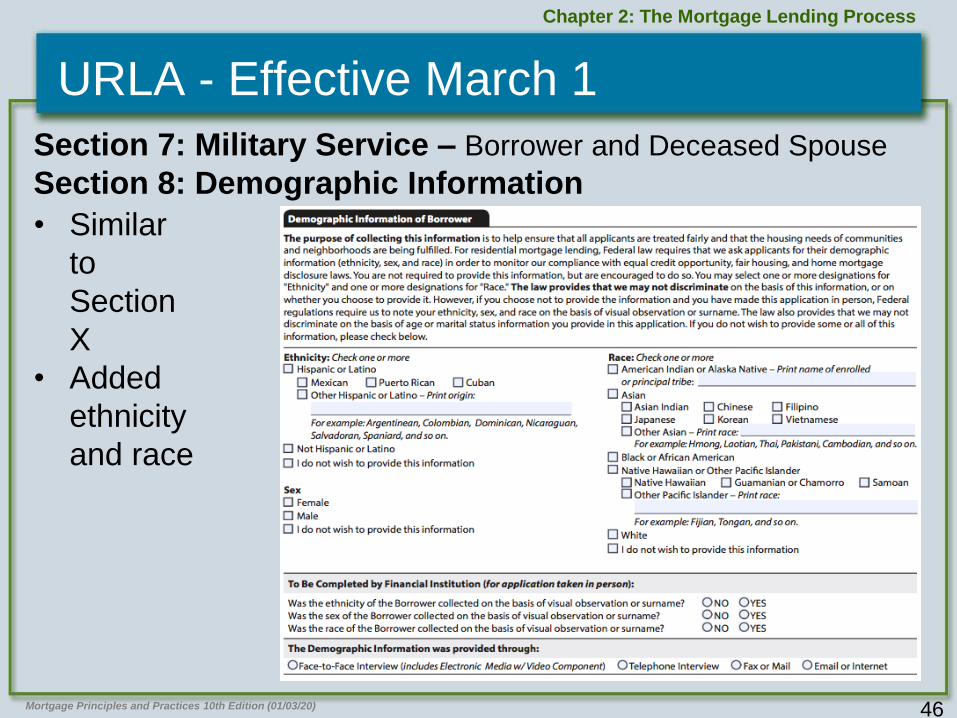

URLA - Effective March 1

• Similar

to

Section

X

• Added

ethnicity

and race

Section 7: Military Service – Borrower and Deceased Spouse

Section 8: Demographic Information

47Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

URLA - Effective March 1

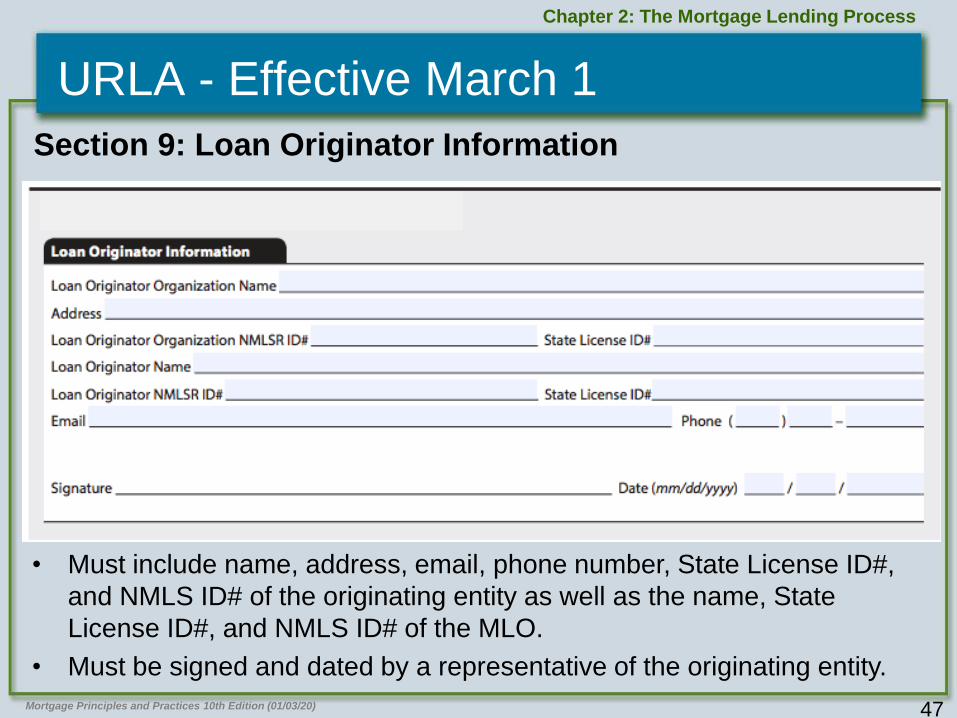

• Must include name, address, email, phone number, State License ID#,

and NMLS ID# of the originating entity as well as the name, State

License ID#, and NMLS ID# of the MLO.

• Must be signed and dated by a representative of the originating entity.

Section 9: Loan Originator Information

48

URLA - Effective March 1

• Lender Loan Information Sections

– Section L1: Property and Loan Information

– Section L2: Title Information

– Section L3: Mortgage Loan Information

– Section L4: Qualifying the Borrower- Minimum

Required Funds or Cash Back

• Must be filled out by the lender

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

49Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

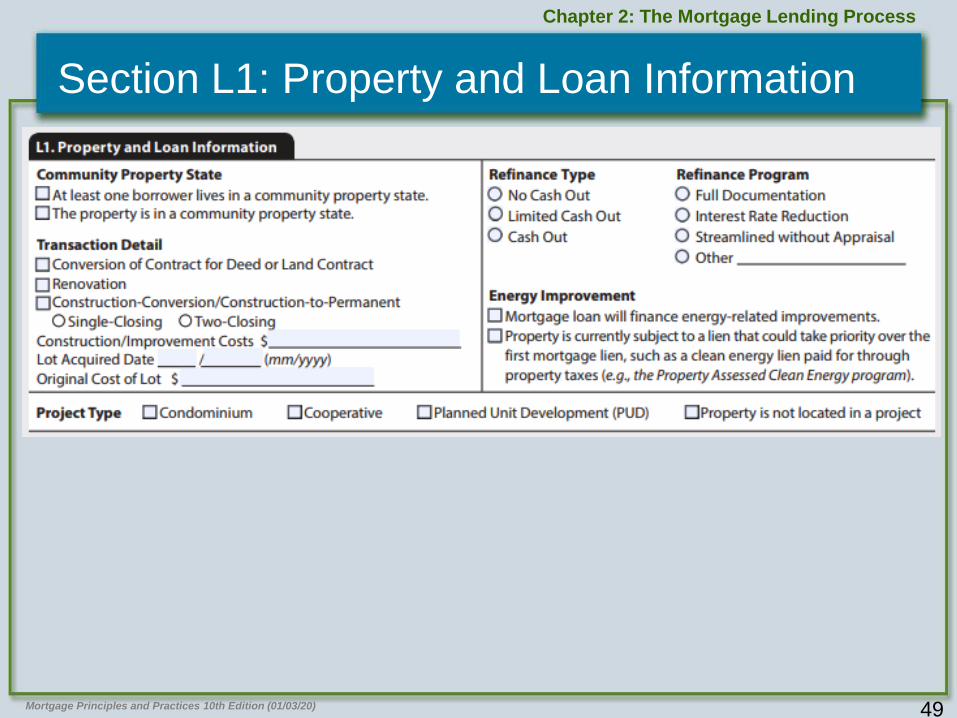

Section L1: Property and Loan Information

50Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

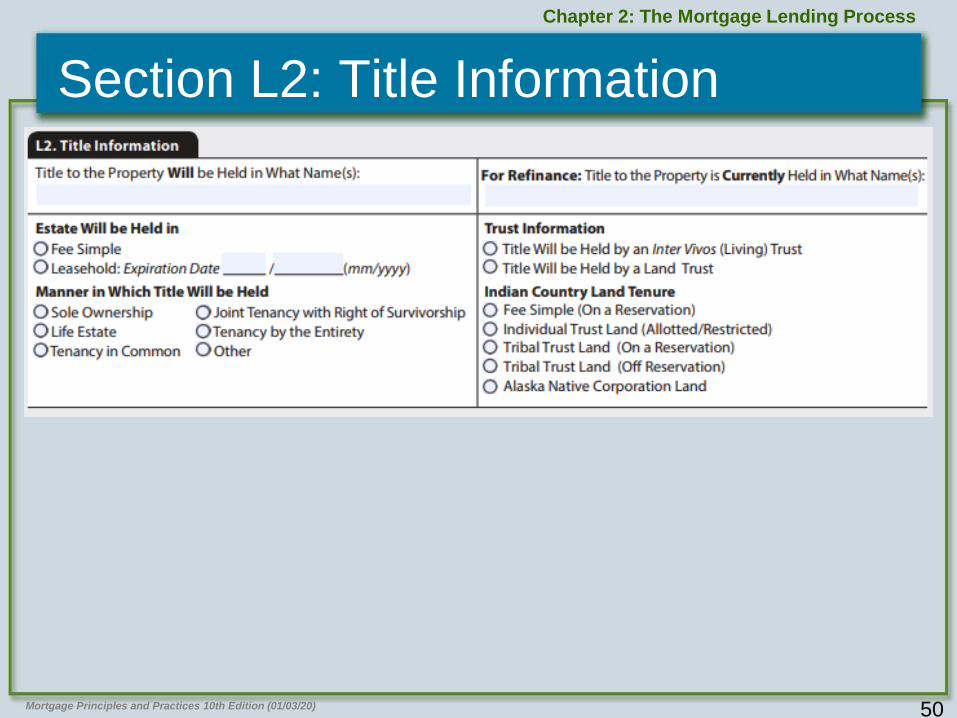

Section L2: Title Information

51Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

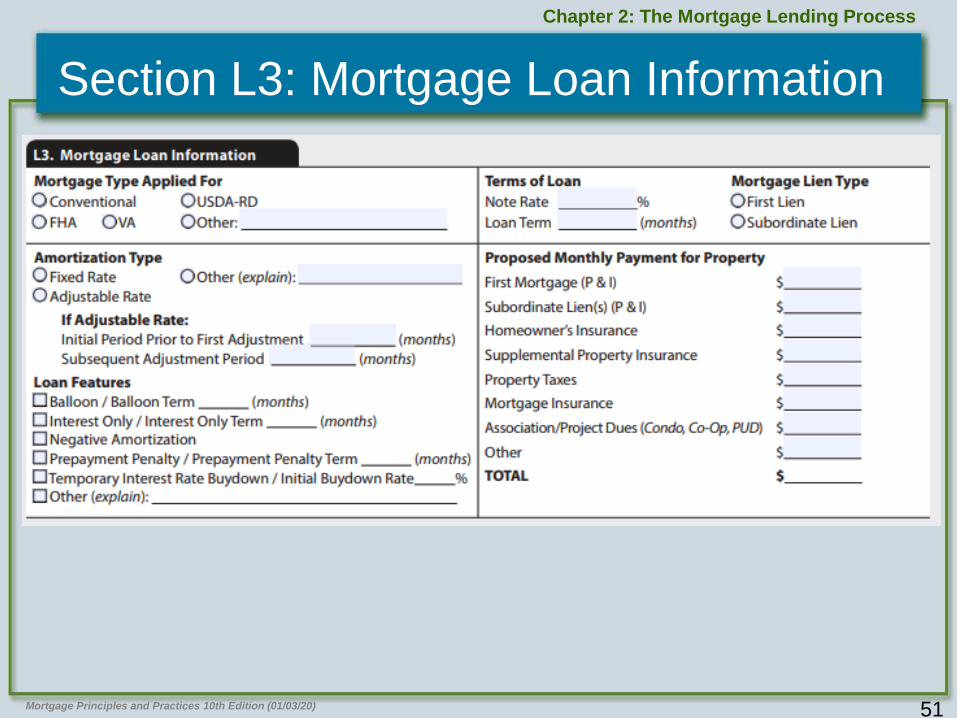

Section L3: Mortgage Loan Information

52Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

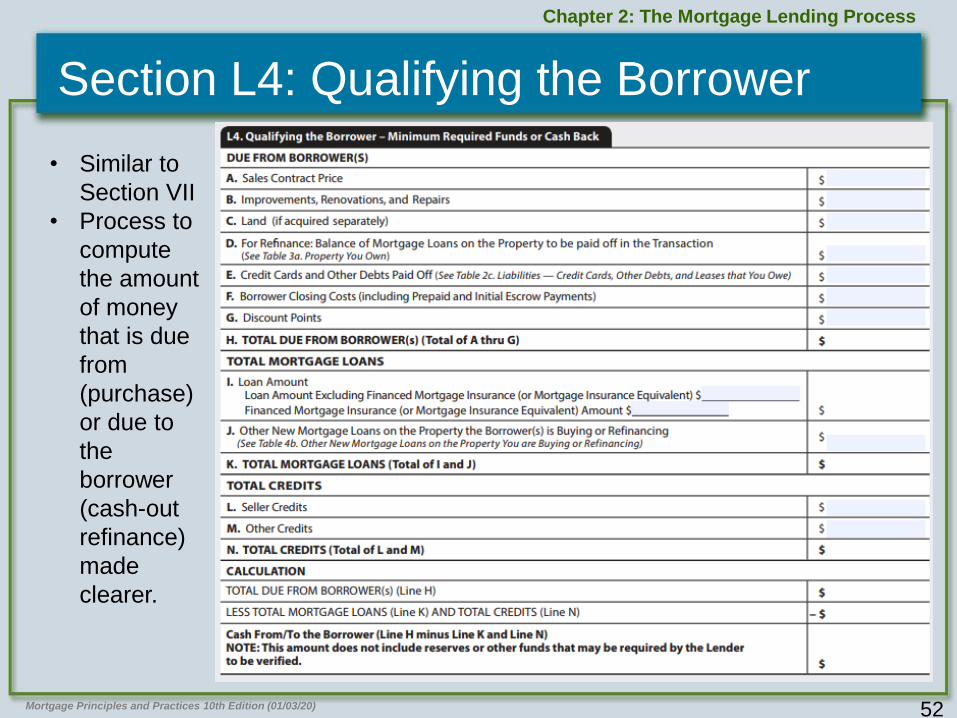

Section L4: Qualifying the Borrower

• Similar to

Section VII

• Process to

compute

the amount

of money

that is due

from

(purchase)

or due to

the

borrower

(cash-out

refinance)

made

clearer.

53Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Additional URLA Information

• Balloon Mortgage

– Fannie Mae requires MLOs using the 1003

URLA to insert a special notice regarding the

nature of the balloon features

– If an attachment is used, the borrower(s) must

sign the attachment

• Electronic Signatures

– Cannot be forced to use electronic signatures

– Legally valid; consumer must receive disclosure

information

54Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

A Complete Application - Defined

• Required “Complete Application”

Information

– Borrower's name, income, and Social Security

number to obtain a credit report

– Subject property address

– Estimate of the value of the property

– Loan amount applied for

A complete application triggers federal

disclosure requirements.

55Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Process Loan Application

• Role of Loan Processor

– Gather pertinent documents

– Complete verification of income

– Obtain credit report

– Obtain preliminary title report

– Contact approved appraisal management company to obtain appraisal

56Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Analyze Borrower and Property

• Borrower’s Ability to Qualify

– Factors related income, credit history, and assets

• 4 Cs of Underwriting

– Credit history of the borrower, which indicates the

borrower’s willingness to repay debt

– Capacity to repay the loan, which includes income

and employment history

– Cash assets, which are available to close the

mortgage

– Collateral, which evaluates the value of the home

57

Income

• Stable Monthly Income

– Monthly income that can reasonably be expected

to continue in the future

– Gross base income from a primary job;

predictable earnings from acceptable secondary

sources

• Quality Source of Income

– Reasonably reliable

• Durable Source of Income

– Expected to continue for a sustained period

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

58Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Income – Secondary Sources

• Bonuses, Commissions, and Part-time– Consistent for two years; average may be used

– Verify with W-2s, pay stubs, income tax returns

• Overtime– Eligible if shows a consistent pattern

• Disability Payments– Count if permanent

– If expiring, must continue for 3 years

• Social Security– Permanent if retirement age

– If disability, requires no greater documentation than for regular-paid employee

• Pensions and Retirement Benefits– Must be stable and solvent

59Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Income – Secondary Sources

• Auto Allowance– Average for 2 years to be considered income for loan

qualification

• Foster Care Income– Obtain letter from state agency case worker to

substantiate foster worker’s ongoing placement

– Document receipt of reimbursement for the previous 24 months

– Borrower letter in loan file stating intention to continue foster care

• Capital Gains– Show monthly average for previous 2 years

• Interest-Yielding Investments– Durable if sound and consistent

60Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Income – Secondary Sources• Rental Income

– Stable pattern of positive cash flow

– Gross Rental Income – PITI x 75% = Net Income

• Alimony, Child Support, and Maintenance– Consistent (written agreement or court decree)

– Should continue for minimum of 3 years

• Unemployment and Welfare– Verifiable, continuous and ongoing

– Must not discriminate for receipt of public assistance

• Boarder Income– Acceptable stable income if in an amount up to 30% of the

total gross income used to qualify the borrower

61Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Income – Secondary Sources

• Housing Parsonage Allowance– 12-month documentation of received income

– Allowance likely to continue for next 3 years

• VA Benefits Income

– Letter or distribution form from the VA

– Income likely to continue for next 3 years

• Self-Employment Income– Must own 25% of business

– Provide personal and entity tax returns for 2 years

– May require financial statements

62Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Income and Employment • Nontaxable Income

– May add 25% to non-taxable income to develop adjusted gross income

• Evaluating Income– Each type to be evaluated separately

• Employment History – Continuous for 2 years unless explainable

– Documentation: W-2 forms for the previous two years; Payroll stubs for the previous 30-day period

• Verification of Employment Form – Used to verify income and employment history

• IRS Form 4506-T– Used to request federal tax returns from the IRS

63Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Income and Employment

• Monthly Income Calculation

– Multiply the hourly wage by the number of hours

worked in a week X 52 weeks = annual income

– Annual income / 12 months = monthly income

64Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Case in Point

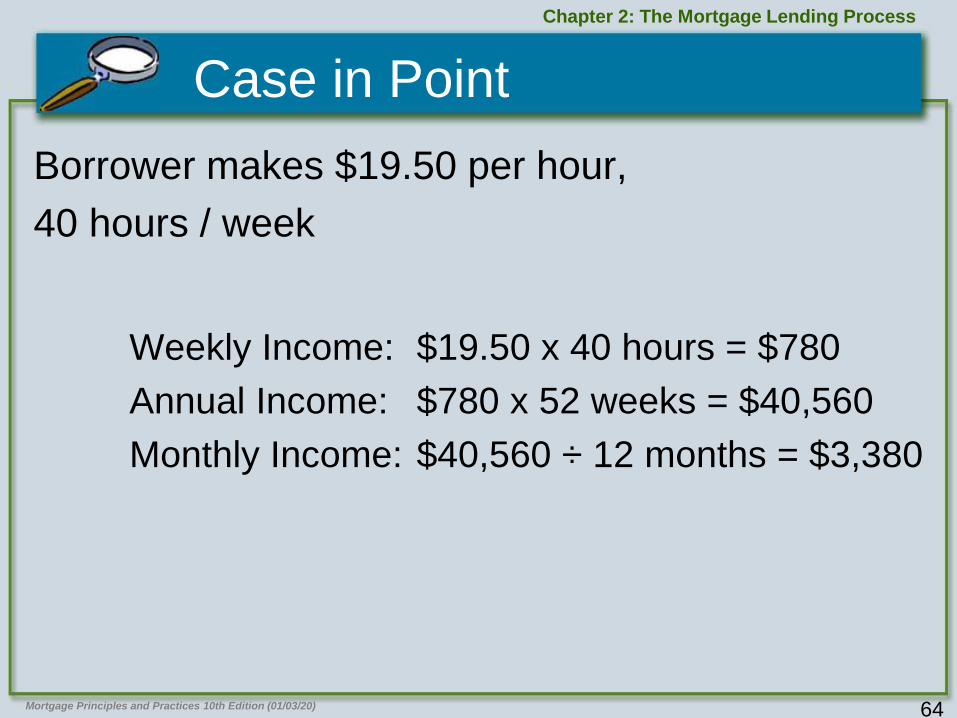

Borrower makes $19.50 per hour,

40 hours / week

Weekly Income: $19.50 x 40 hours = $780

Annual Income: $780 x 52 weeks = $40,560

Monthly Income: $40,560 ÷ 12 months = $3,380

65Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Apply Your Knowledge 2.2

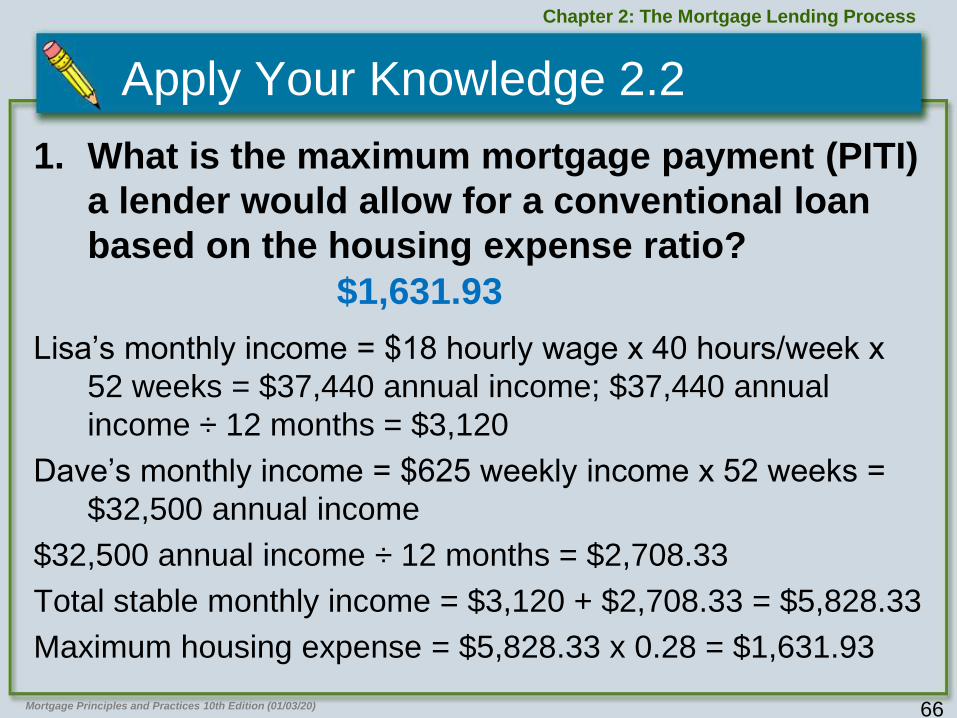

Two months ago, Lisa was honorably discharged from

the Air Force where she spent 4 years training as an

airplane mechanic. After discharge, she relocated to

take a 40 hour per week apprentice mechanic job with

a major airline company where she earns $18 an hour.

Last month, her husband Dave, who has worked the

past 2 years as a registered nurse, found a nursing job

with a local hospital making $625 per week.

They just bought a new car and pay $400 each month

on that loan and have no other monthly debts.

66Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Apply Your Knowledge 2.2

1. What is the maximum mortgage payment (PITI)

a lender would allow for a conventional loan

based on the housing expense ratio?

Lisa’s monthly income = $18 hourly wage x 40 hours/week x

52 weeks = $37,440 annual income; $37,440 annual

income ÷ 12 months = $3,120

Dave’s monthly income = $625 weekly income x 52 weeks =

$32,500 annual income

$32,500 annual income ÷ 12 months = $2,708.33

Total stable monthly income = $3,120 + $2,708.33 = $5,828.33

Maximum housing expense = $5,828.33 x 0.28 = $1,631.93

$1,631.93

67Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Apply Your Knowledge 2.2

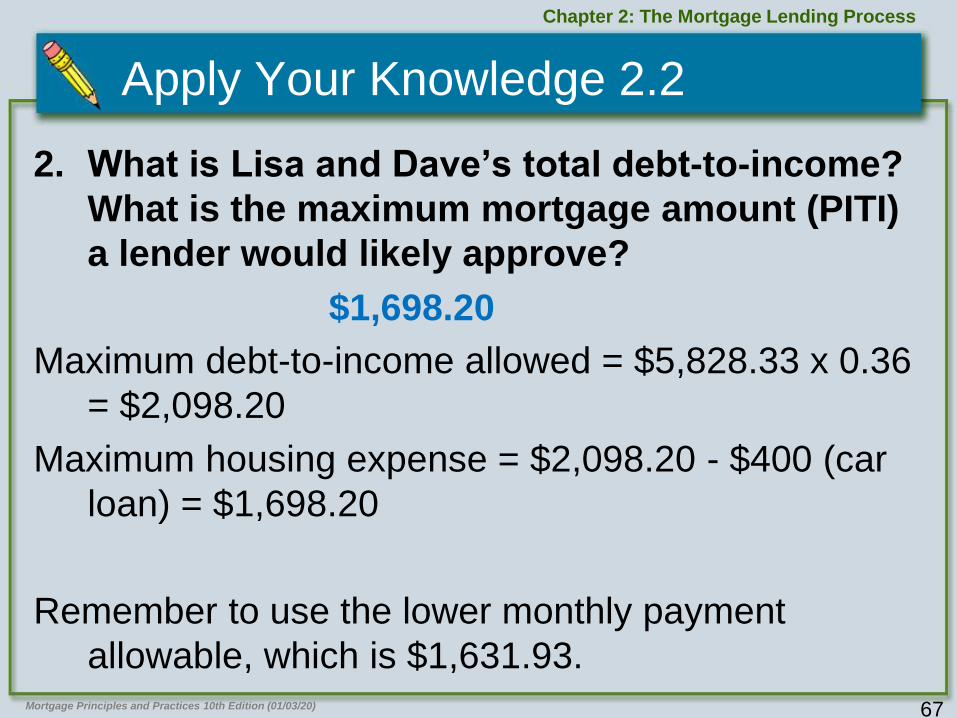

2. What is Lisa and Dave’s total debt-to-income?

What is the maximum mortgage amount (PITI)

a lender would likely approve?

Maximum debt-to-income allowed = $5,828.33 x 0.36

= $2,098.20

Maximum housing expense = $2,098.20 - $400 (car

loan) = $1,698.20

Remember to use the lower monthly payment

allowable, which is $1,631.93.

$1,698.20

68Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Apply Your Knowledge 2.2

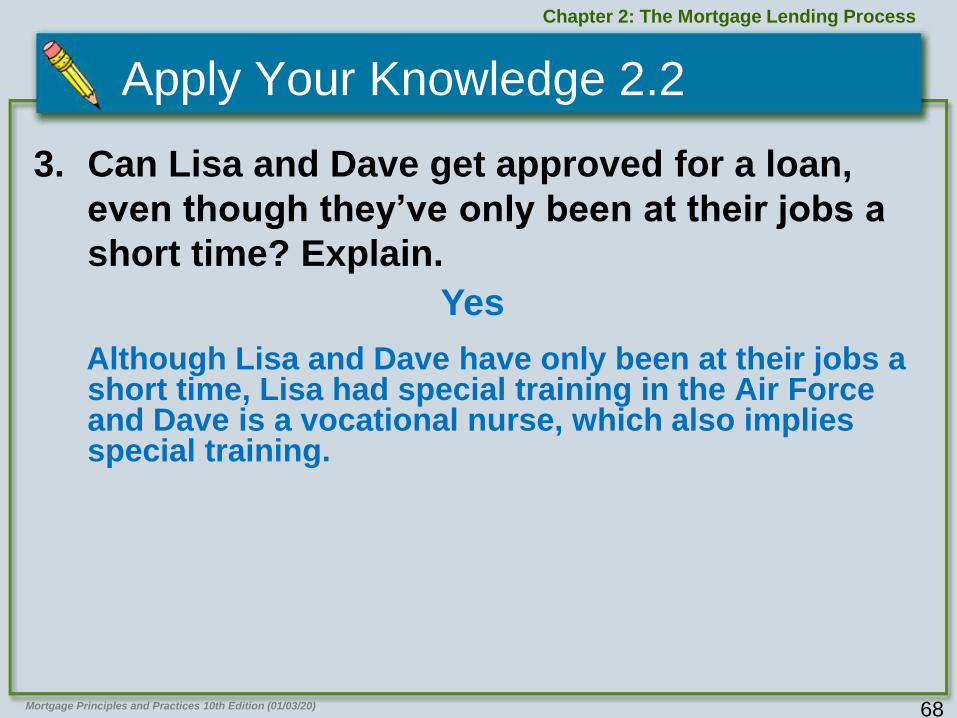

3. Can Lisa and Dave get approved for a loan,

even though they’ve only been at their jobs a

short time? Explain.

Although Lisa and Dave have only been at their jobs a short time, Lisa had special training in the Air Force and Dave is a vocational nurse, which also implies special training.

Yes

69Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Credit History• Credit History

– Record of debt repayment

– Underwriters analyze credit report from a national credit

reporting company

• Debt

– Money owed; secured or unsecured recurring monetary

obligation that will not be canceled until paid in full

– Borrower must inform of all debt; even debt not on credit report

– Slow payment records or derogatory credit may cause loan

decline or to be placed in high-risk category

• ECOA

– Prohibits discrimination in lending based on age (except minors

under 18), sex, race, marital status, color, religion, national

origin, or receipt of public assistance

70

Credit History – Credit Scoring

• Credit Scoring

– Objective means of determining creditworthiness of

potential borrowers based on a number scoring system

• Credit Score

– Numeric representation of the borrower’s credit profile

compiled by assigning specified numerical values to

different aspects of the borrower’s credit makeup

• Mortgage Performance & Credit Score

Correlation

– High credit score = better credit risk

– Low credit score = higher credit risk

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

71

Credit History – Credit Scoring

• Credit Scoring Systems

– FICO®, BEACON®, EMPERICA®

• Calculation

– 3 main credit bureau score differently

– All credit bureaus score 300 to 850

• >720 acceptable credit risk

• 720-620 marginal credit

• <620 high credit risk

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

72Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

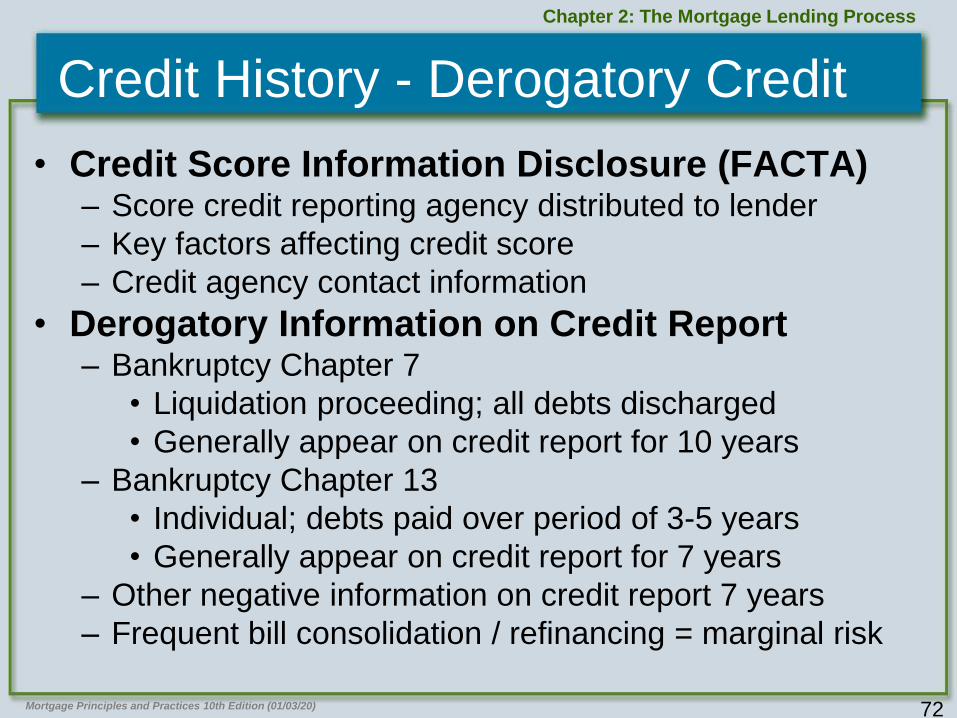

Credit History - Derogatory Credit

• Credit Score Information Disclosure (FACTA)– Score credit reporting agency distributed to lender

– Key factors affecting credit score

– Credit agency contact information

• Derogatory Information on Credit Report – Bankruptcy Chapter 7

• Liquidation proceeding; all debts discharged

• Generally appear on credit report for 10 years

– Bankruptcy Chapter 13

• Individual; debts paid over period of 3-5 years

• Generally appear on credit report for 7 years

– Other negative information on credit report 7 years

– Frequent bill consolidation / refinancing = marginal risk

73

Assets

• Asset

– Item of value

• Liquid Asset

– Cash and other assets that can be quickly

converted to cash, such as savings account,

mutual funds, or cash value of life insurance

• Non-Liquid Asset

– More difficult to turn into cash, such as proceeds

from a property being sold or trade equity

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

74

Assets - Evaluating

• Down Payment

– Must have sufficient liquid assets to make down payment

and other closing costs

– Must know source of down payment

– Special considerations for borrowed funds or gifts

• Reserves

– Cash / Highly liquid assets after loan funding

– Prefer enough to pay 2 months of PITI

• Other Assets

– Real estate equity important

Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

75Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Assets - Evaluating

• Down Payment and Reserves Verification– Two months of bank statements– Verification of Deposits

• Verify current and average bank statement balance

– Underwriter considerations:

• Does the verified information conform to statements in the loan application?

• Is there enough money in the bank to pay costs of buying the property?

• Has the bank account been opened recently (within the last few months)?

• Is the present balance notably higher than the average balance?

76Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Insurance and Escrow Requirements

• Homeowner’s Hazard Insurance– Covers loss or damage to property in the event

of fire or other disaster; sufficient to replace

home or reimburse mortgage amount

– Lenders may place insurance to cover loan

value

– 1 year of premiums required prior to closing

– Annual insurance costs escrowed; prorated

over the next 12 months to determine a monthly

insurance and property tax payment amount

77Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Insurance and Escrow Requirements

• Flood Insurance– Required for federally-designated special flood

hazard area (SFHA); Flood Zone A or V

– Purchased from National Flood Insurance

Program (NFIP)

• Private Mortgage Insurance– Insures lender against default on loan where

there is a loss of collateral value

– Fannie Mae and Freddie Mac require on loans

with < 20% borrower equity; insure upper

portion of loan exceeding the standard 80%

LTV

78Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

2.3 Apply Your Knowledge

Sam Able wants to buy a home It’s estimated that an 80% conventional loan will have a mortgage payment of $878.

• He has an automobile payment of $212 a month with 14 installments remaining. He earns $700 per week.

• His down payment and closing costs are estimated at $18,400.

• Sam is selling a home with equity of $14,000. He has a checking and savings account with a local bank and plans to draw on that account to close the transaction.

• The VOD showed Sam’s savings account has an average monthly balance of $1,000 and a current balance of $3,600.

79Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

2.3 Apply Your Knowledge

1. What is Sam’s housing expense ratio?

29%

$700 weekly income x 52 weeks = $36,400 annual income.

$36,400 annual income ÷ 12 months = $3,033.33 monthly

income.

$878 mortgage payment ÷ $3,033.33 monthly income = 0.29

2. What is Sam’s total debt-to-income ratio?

36%

$878 mortgage payment + $212 auto payment = $1,090 total

debt service.

$1,090 total debt service ÷ $3,033.33 monthly income = 0.36

80Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

2.3 Apply Your Knowledge

3. Will Sam have any problems closing this

transaction? Explain.

Yes. Housing expense ratio exceeds guidelines.

4. Do you see any problems with Sam’s VOD?

Explain.

Yes. His current balance of $3,600 is significantly

higher than his average balance of $1,000.

81Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Underwriting

• Loan Underwriting– Underwriter evaluates documentation, borrower

information, and risk factors associated with a

loan to make decision

• MLO Role– Take ownership of loan file

• Keep borrowers informed throughout process

– Review application and documentation for

accuracy and ensure everything is included

– Identify issues that may be problematic• Consider including “Dear Underwriter” letter to

acknowledge special circumstances

– Use a secure transmission method

82Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Underwriting: Loan File Evaluation

• Degree of Risk Evaluation

– Sufficient value in collateral property?

– Marketable property title?

– Hazards or issues affecting the property?

– Can borrower make monthly payments?

• Automated versus Manual

• Underwriting Decision

– Reject loan as applied for (bad risk or

incomplete file)

– Make loan on terms applied for

– Make loan on different terms

83Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Underwriting: Loan File Evaluation

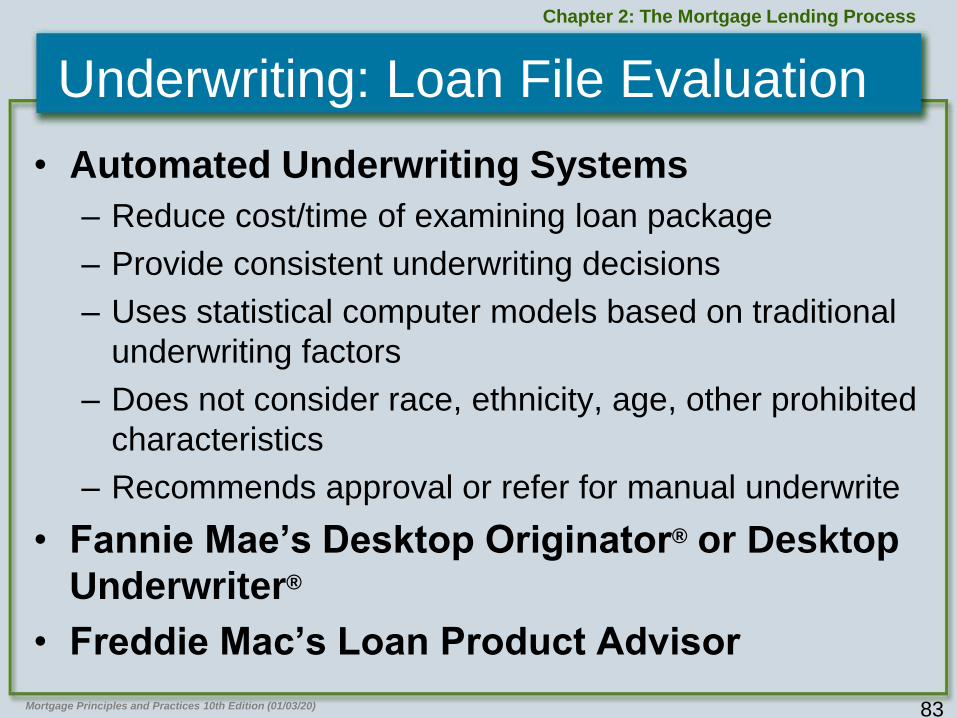

• Automated Underwriting Systems

– Reduce cost/time of examining loan package

– Provide consistent underwriting decisions

– Uses statistical computer models based on traditional

underwriting factors

– Does not consider race, ethnicity, age, other prohibited

characteristics

– Recommends approval or refer for manual underwrite

• Fannie Mae’s Desktop Originator® or Desktop

Underwriter®

• Freddie Mac’s Loan Product Advisor

84Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

1. Joe buys a house for $150,000, making a $30,000 down payment and paying three discount points to buy down the interest rate. What is the total cost of the discount points?

A. $1,500

B. $3,000

C. $3,600

D. $4,500

85Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

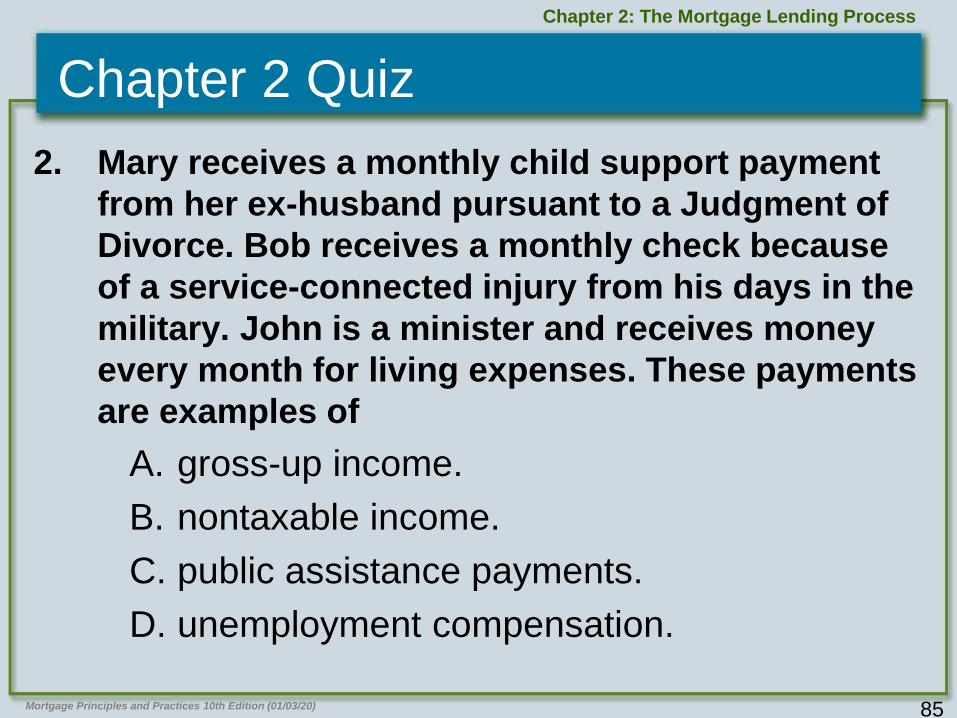

2. Mary receives a monthly child support payment

from her ex-husband pursuant to a Judgment of

Divorce. Bob receives a monthly check because

of a service-connected injury from his days in the

military. John is a minister and receives money

every month for living expenses. These payments

are examples of

A. gross-up income.

B. nontaxable income.

C. public assistance payments.

D. unemployment compensation.

86Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

3. If a borrower is self-employed, he should

provide

A. an average monthly income amount earned

over the previous two years.

B. employment verification from the last

employer.

C. profit and loss statements for the previous

six years.

D. tax returns for the previous two years.

87Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz4. Bob & Mary are providing a gift to their daughter, Amy,

as down payment for the purchase of her new home.

They provide a current bank statement for their

account, a copy of their check to Amy, and a copy of

the deposit slip into Amy’s account. Amy provides a

current ledger from her checking account that verifies

the deposit was made and the amount of the current

balance. What key document is missing?

A. agreement signed by all parties stating when the gift is to be

repaid

B. copy of the deposit receipt from the settlement agent

C. gift letter signed by the donor stating no repayment is

expected

D. letter from Amy’s bank stating the gift funds have been

deposited

88Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

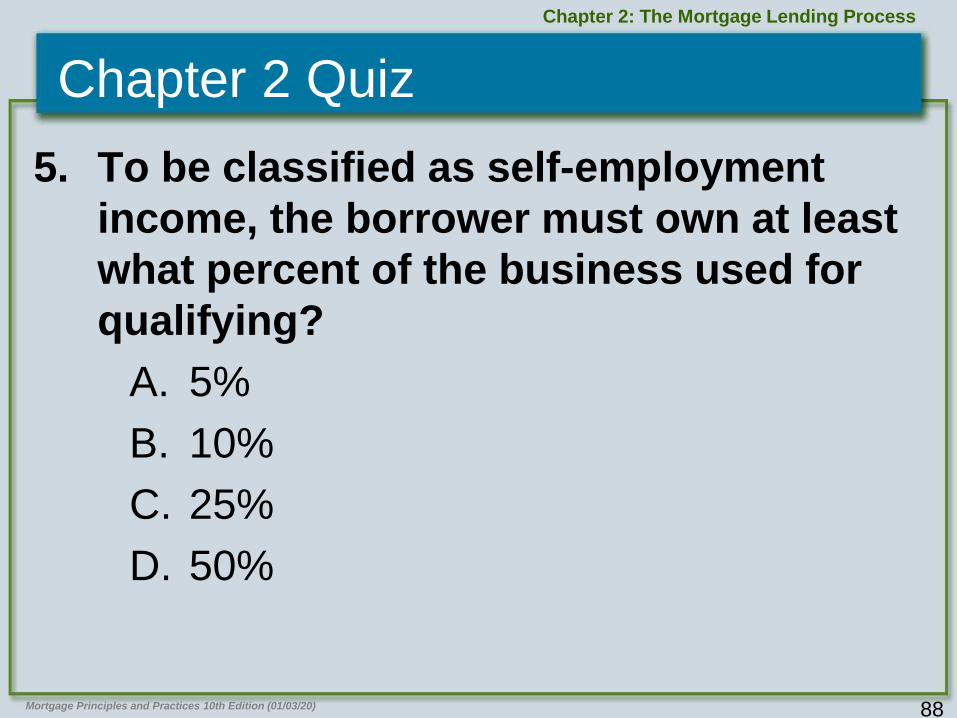

5. To be classified as self-employment

income, the borrower must own at least

what percent of the business used for

qualifying?

A. 5%

B. 10%

C. 25%

D. 50%

89Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

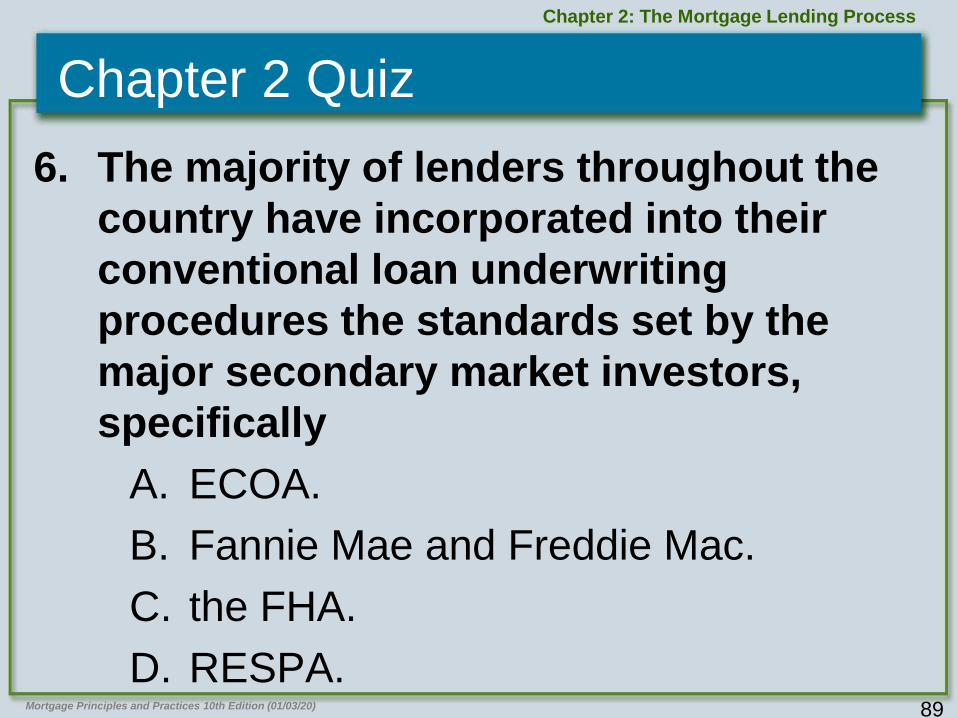

6. The majority of lenders throughout the

country have incorporated into their

conventional loan underwriting

procedures the standards set by the

major secondary market investors,

specifically

A. ECOA.

B. Fannie Mae and Freddie Mac.

C. the FHA.

D. RESPA.

90Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

7. When qualifying for a conventional loan,

stable gross monthly income can

include

A. alimony received (that a borrower

chooses to reveal).

B. a bonus received for the first time last

year.

C.erratic unemployment earnings.

D. income from other family members.

91Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

8. To combat income-related mortgage

fraud, lenders require a review of the

income provided to the IRS. What

document authorizes the lender to

obtain income transcripts from the IRS?

A. 1003 and Verification of Income

B. 4506-T

C.Schedule 15

D.URAR

92Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

9. Joe wants to get a loan to buy a house.

When evaluating his credit obligations,

which would LEAST LIKELY be

considered as debt?

A. car loan payment

B. cell phone service payment

C. child support payment

D. credit card payment

93Mortgage Principles and Practices 10th Edition (01/03/20)

Chapter 2: The Mortgage Lending Process

Chapter 2 Quiz

10.A borrower’s stable monthly income is $3,000. He has three monthly debts: $350 car payment, $50 personal loan payment, and $50 credit card payment. What is the maximum monthly mortgage payment he would qualify for on a conforming loan?

A. $390

B. $630

C. $840

D. $1,080