Embed Size (px)

Citation preview

Your guide to property investment

The Morello Matrix

Our initial connection was a shared interest in property- particularly as an investment- and the use of rising values and equity to buy more property.

I’ve known a lot of property investors, many of them very successful. But Andrew was a bit different. For a start, he was in his mid-twenties when I met him. He’d already built a sizeable property portfolio off his own back, from a running start.

Where many young people talk about getting rich quick, Andrew talks about the long game. Andrew is a fan of hard work, owning quality properties and being a good landlord.

His approach to investing in property is very smart and structured, but he does not pretend to know it all. To get the best deals, he uses a broker; for tax - related decisions, he uses accountants; and for repairs and alterations, he finds the best tradies.

In short, he has a financial approach for hard-working Australians to build property wealth and attain financial self - sufficiency.

Property is a good way for average Australians to build wealth, and I reckon the Morello Matrix is an excellent way for people to start on their own property portfolios.

Good luck,

ForewardI met Andrew Morello during the filming of Channel Nine’s The Apprentice show in 2009. He was immediately likeable and I picked him as someone who was motivated, intelligent, hard-working and would go far in life.

Foreword from Mark Bouris written by Mark Abernethy which was thought to be completed during initial discussions.

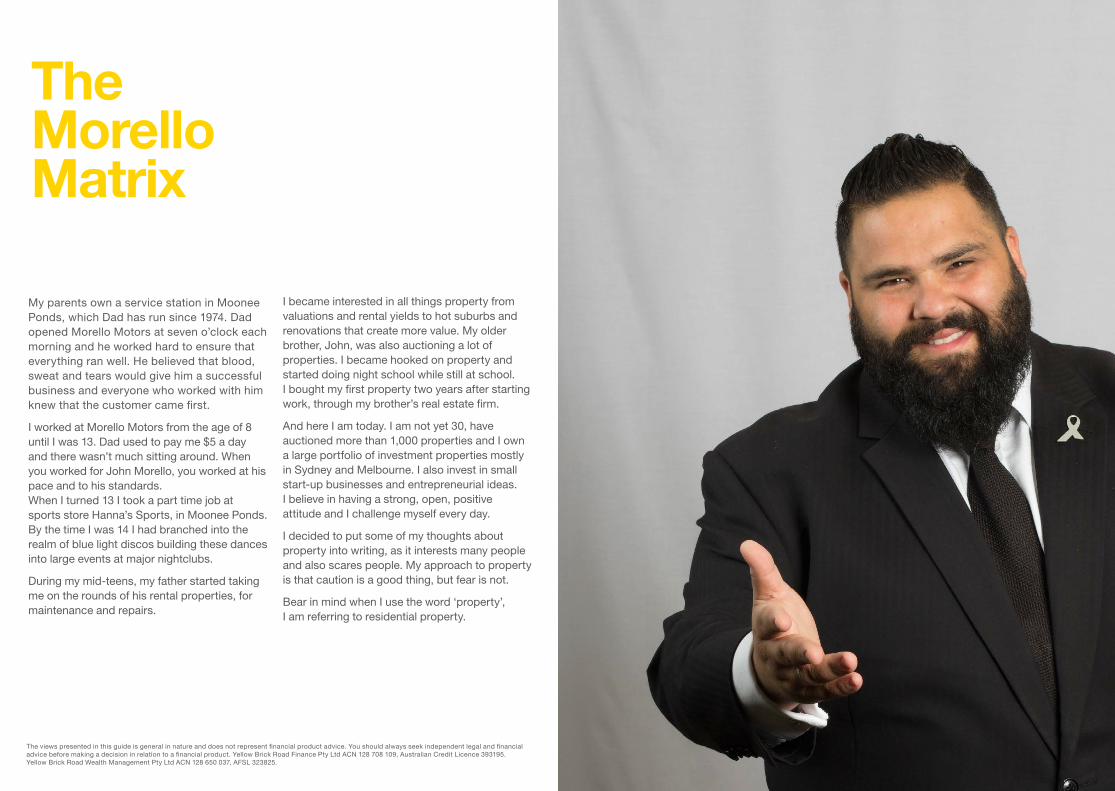

My parents own a service station in Moonee Ponds, which Dad has run since 1974. Dad opened Morello Motors at seven o’clock each morning and he worked hard to ensure that everything ran well. He believed that blood, sweat and tears would give him a successful business and everyone who worked with him knew that the customer came first.

I worked at Morello Motors from the age of 8 until I was 13. Dad used to pay me $5 a day and there wasn’t much sitting around. When you worked for John Morello, you worked at his pace and to his standards. When I turned 13 I took a part time job at sports store Hanna’s Sports, in Moonee Ponds. By the time I was 14 I had branched into the realm of blue light discos building these dances into large events at major nightclubs.

During my mid-teens, my father started taking me on the rounds of his rental properties, for maintenance and repairs.

The views presented in this guide is general in nature and does not represent financial product advice. You should always seek independent legal and financial advice before making a decision in relation to a financial product. Yellow Brick Road Finance Pty Ltd ACN 128 708 109, Australian Credit Licence 393195. Yellow Brick Road Wealth Management Pty Ltd ACN 128 650 037, AFSL 323825.

I became interested in all things property from valuations and rental yields to hot suburbs and renovations that create more value. My older brother, John, was also auctioning a lot of properties. I became hooked on property and started doing night school while still at school. I bought my first property two years after starting work, through my brother’s real estate firm.

And here I am today. I am not yet 30, have auctioned more than 1,000 properties and I own a large portfolio of investment properties mostly in Sydney and Melbourne. I also invest in small start-up businesses and entrepreneurial ideas. I believe in having a strong, open, positive attitude and I challenge myself every day.

I decided to put some of my thoughts about property into writing, as it interests many people and also scares people. My approach to property is that caution is a good thing, but fear is not.

Bear in mind when I use the word ‘property’, I am referring to residential property.

The MorelloMatrix

Savings

Compound interest Volatility

Money from scratch

BusinessShares Property

In this book, I’d like to share with you my method to convert cash into assets. I call it the Morello Matrix. The asset game I play is property and to do this, I use every tool in the tool box, as well as borrowing. Let’s look at some of the ways Australians invest to create wealth.

Simply saving your money might not be the best way to build wealth.

Here’s why:Let’s say you put aside around $100 per week. You would save $5,200 per year. With interest of around 4 per cent per year, you would have saved $62,432 at the end of 10 years. Over a decade, you earned $10,432. Long-term inflation is around 3 per cent in Australia, as this is the increase in goods and services in the economy.

Owning a business can be a great source of personal success. In fact, there are over two million businesses in Australia, of all shapes and sizes, and 12 per cent of them are opening and closing each year.

A private business can create income for the owners and, over time, help to set up a network of customers and businesses building up goodwill.

The drawback is that in private business, you cannot take your investment out when you want cash. Also, there is no guaranteed business value and your selling options can be limited.

Remember that business ownership isn’t for everyone.

In this book, I advocate a different approach to savings, business and shares. It involves borrowing, property and equity, and it’s accessible to everyday Australians.

Savings accounts offer compound interest, and I’m in favour of it.

Compound interest earns money on your interest. The longer you leave your investment, the greater the compounding interest effect - and the whole pie grows bigger.

As a rule of thumb, if your savings are growing at 8% p.a. your money doubles every 10 years.

That’s why experts encourage us to start saving early.

Volatility is the variation of price over time. For shares, because their price is valued every second of every business day, the value may vary many times every day. For some people this volatility is unnerving.

Generally speaking, the higher the growth, the more volatile the ride. Because they are valued every day, shares tend to be more volatile than owning direct real estate.

Wealth occurs in two key waysFirstly, when you work, you produce cash-flow. The second way wealth occurs is when you own an asset which produces income and increases in value.

Turning cash-flow into asset wealthEssentially, you can use your cash-flow to invest in assets to build more wealth. This is called investing. At some point, you no longer have to work for cash - the assets do the work for you. This is the key to all investing.

Shares are a popular investment option, but are more variable than property.

Owning shares can be both lucrative and unpredictable. Almost four out of ten Australians own shares or are part of a managed fund that invests in shares. (Nearly everyone who has superannuation is invested in shares!)

When you buy shares in a publicly listed company you own a small portion of the company, so you achieve growth via both the market price of the share (share price) and the income it may distribute each year (dividend).

I call this The MorelloMatrix

$120K

$90K

$60K

$30K

$0

Simply saving your money might not be the best way to build wealth.

40months

8 12

Savings

16 20

Let’s say you put aside around $100 per week. You would save $5,200 per year. With interest of around 4 per cent per year, in 10 years, you would have $62,432. Over a decade, you earned $10,432. Long-term inflation is around 3 per cent in Australia, as this is the increase in goods and services in the economy.

Here’s why:

24 28 3632 40 44 48

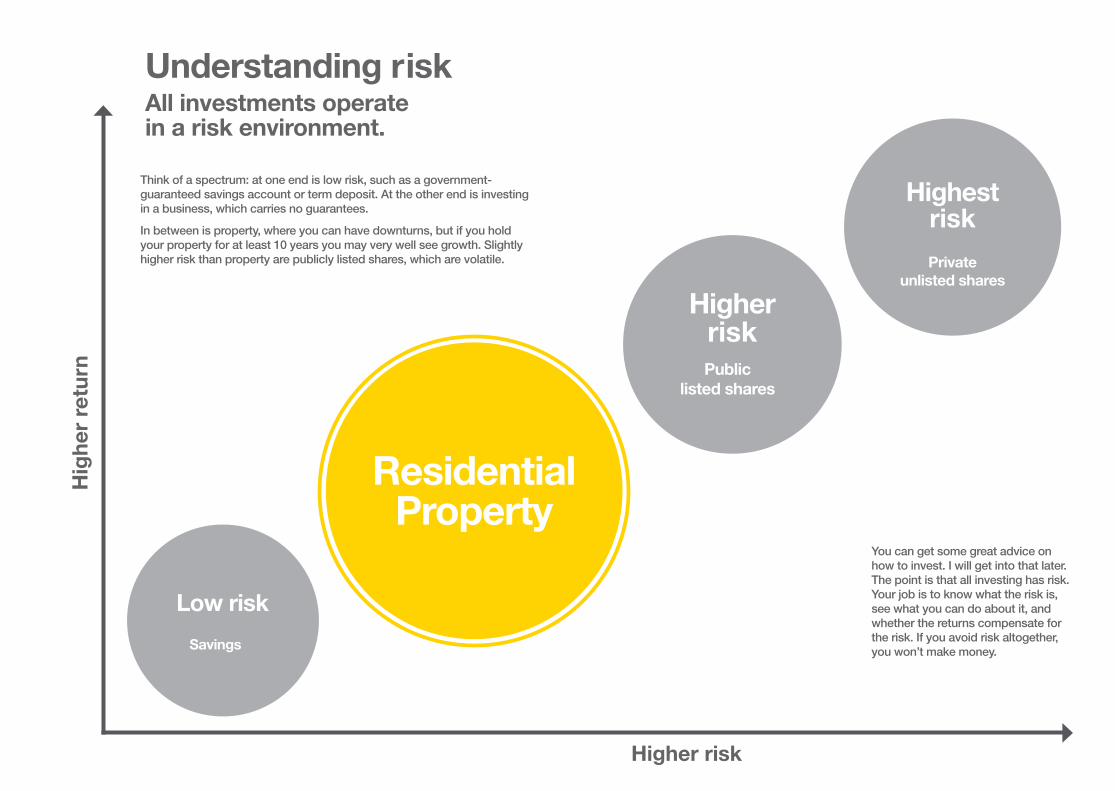

Understanding risk

Low risk

Savings

Residential Property

Think of a spectrum: at one end is low risk, such as a government-guaranteed savings account or term deposit. At the other end is investing in a business, which carries no guarantees.

In between is property, where you can have downturns, but if you hold your property for at least 10 years you may very well see growth. Slightly higher risk than property are publicly listed shares, which are volatile.

All investments operatein a risk environment.

Public listed shares

Private unlisted shares

Highest risk

Higher risk

You can get some great advice on how to invest. I will get into that later. The point is that all investing has risk. Your job is to know what the risk is, see what you can do about it, and whether the returns compensate for the risk. If you avoid risk altogether, you won’t make money.

Hig

her

retu

rn

Higher risk

ProsR

esid

entia

l pro

pert

y ad

vant

ages

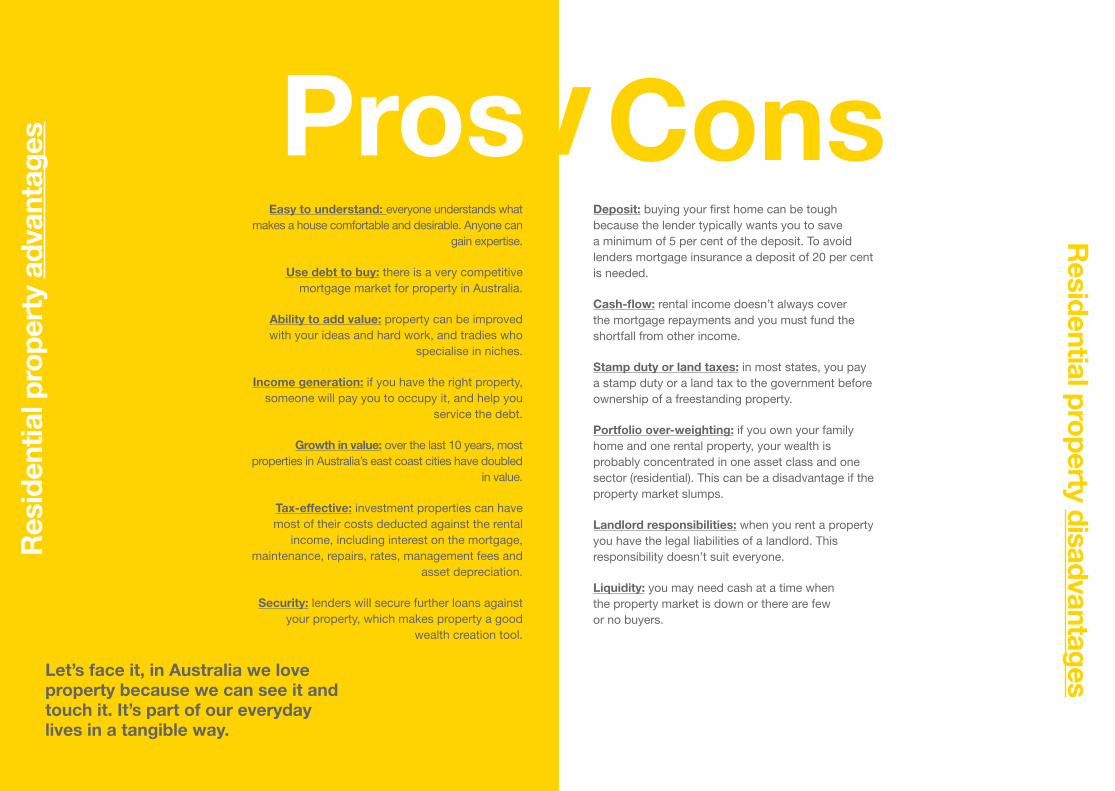

Easy to understand: everyone understands what makes a house comfortable and desirable. Anyone can

gain expertise.

Use debt to buy: there is a very competitive mortgage market for property in Australia.

Ability to add value: property can be improved with your ideas and hard work, and tradies who

specialise in niches.

Income generation: if you have the right property, someone will pay you to occupy it, and help you

service the debt.

Growth in value: over the last 10 years, most properties in Australia’s east coast cities have doubled

in value.

Tax-effective: investment properties can have most of their costs deducted against the rental

income, including interest on the mortgage, maintenance, repairs, rates, management fees and

asset depreciation.

Security: lenders will secure further loans against your property, which makes property a good

wealth creation tool.

Cons

9

Residential property disadvantages

Deposit: buying your first home can be tough because the lender typically wants you to save a minimum of 5 per cent of the deposit. To avoid lenders mortgage insurance a deposit of 20 per cent is needed.

Cash-flow: rental income doesn’t always cover the mortgage repayments and you must fund the shortfall from other income.

Stamp duty or land taxes: in most states, you pay a stamp duty or a land tax to the government before ownership of a freestanding property.

Portfolio over-weighting: if you own your family home and one rental property, your wealth is probably concentrated in one asset class and one sector (residential). This can be a disadvantage if the property market slumps.

Landlord responsibilities: when you rent a property you have the legal liabilities of a landlord. This responsibility doesn’t suit everyone.

Liquidity: you may need cash at a time when the property market is down or there are few or no buyers.

Let’s face it, in Australia we love property because we can see it and touch it. It’s part of our everyday lives in a tangible way.

Preparing for the matrixIn this book, I advocate a different approach to savings, business and shares. It involves borrowing, property and equity, and it’s accessible to everyday Australians. I call it the Morello Matrix. Before I take you through the elements of my system, there are some concepts you need to understand.

Local intelligence experts

Do your homework so you know an opportunity when it appears.

To play the property game, start by immersing yourself in everything property: - Look in real estate windows.

- Subscribe to agents’ newsletters and catalogues. - Look at the property pages in your local newspapers and attend open houses

and auctions.- Talk to agents and auctioneers. Become a collector of intelligence on property by

following an area, street, or type of house. - Do your homework so you know an opportunity when it appears.

- Start by getting online and subscribing to the factual statistics and reports that exist.

There are plenty of sources for real estate information freely available these days.

Advice

Attitude

I consult the experts for advice. With property, there’s paperwork and tax considerations that can be a big

headache if things go wrong. On the next page is a list of the experts I use to make the journey smoother.

Aim to have a winning attitude. Many people fail to make the leap into property because they can think of many reasons not to buy. Practice turning that around: start

thinking about how you’re going to build wealth. Focus on what the property must have, the rent it could earn and what price you’re willing to pay based on suburb

averages and rental returns, also known as rental yield.

Mortgage broker

Accountant

Depreciation expert

Conveyancer

Business approach

When you get into the guts of the Matrix, there’ll be complex decisions around valuations, refinancing and loan types. It’s good to have an experienced broker guiding you

through these decisions and giving you options.

When you own investment properties, you interact with the tax system and an accountant helps ensure you are paying

your taxes. This is crucial when you use negative gearing and particularly when you sell an investment property.

This is often an accountant who can calculate the depreciation of your assets such as washing machines

and dryers. This can be done quickly and accurately by a professional, ensuring you get all your tax deductions

right.

Many people use a solicitor to do their conveyancing but when you use a dedicated conveyancer they are

experts in just one thing: property transactions. They’re usually faster too.

When you buy a rental property you become a landlord. You have customers and your product is accommodation. Get yourself into this mindset; don’t buy an investment property and then baulk at the responsibilities of being

a landlord. Also remember that your investment property has to include the things that make it better to live in – not the things you personally like. Don’t

fall in love with your investment property - treat it like a business.

Experts and attitude

Take the leap into property

nlocking the matrixI’d like to make a comment about committing yourself to property and wealth.

I speak to a lot of people who are afflicted by two mortal enemies of wealth creation: “umm and aah”. They second-guess themselves; they find reasons not to act; they listen to barbeque chatter and scare themselves silly. They find incredible excuses not to go to auction or return a mortgage broker’s phone call.

I am reminded of the saying by the once richest man in the world, Andrew Carnegie. He said: “Most people will lose more to indecision than they will to a bad decision”.

There is nothing wrong with being cautious; there’s nothing wrong with checking and rechecking. However I see millions of dollars in future wealth going begging when buyers get cold feet.

Don’t let fear rule your wealth creation dreams

Andrew Morello

“Don’t fall in love with your investment property, treat it like a business.”

Andrew Morello

The Morello Matrix

Pha

se A

1B

orr

ow

Find a low-cost loan to buy a

house that will increase in value

over time.

2Rent out your property and

use this income to repay the loan, cover the property costs and allow growth over time.

Rent

Phase A

3Equity

Generally your property will increase in value over time. Equity is the difference between what your home is worth and how much you owe on

it. Once you have built up some equity, use it to buy more property.

4Understanding negative gearing and capital

gains tax is critical to the Morello matrix.

Tax

Once you create a ladder of income, you need to protect it with the right tenants, insurance and owner’s equity via good

cash flow management.

Phase A

1BorrowGetting your first property

To start the matrix, you need to get onto the property ladder. Every portfolio starts with the

first property. This is usually your principal place of residence, although some choose to buy an

investment.

The first property is important because it’s a chance to build equity. Once you have one

property, you can start to build on that foundation.

Save for a deposit: The first step is to get a deposit, usually 5-10 percent of the purchase price plus costs.

Live with mum and dad while you save the deposit.

Map it out: Establish what you want to buy, the likely cost of it, and how much your lender will require as a deposit.

Make a budget and stick to it.

Do your homework: find out the actual amount you will need for stamp duty and conveyancing fees.

Use a high-interest savings account or managed fund, that is separated from your daily account.

Set a deadline on your goal of saving this money.

Cut out luxuries and bank the savings, such as coffees, eating out and exotic beers or wines.

Accept it will take some sacrifice.

Get a second job, and save all the income from that job.

The golden rule is to pay yourself first, direct from employer into an account that doesn’t have a plastic card attached.

Look for overtime, do the worst shifts, then bank the extra pay.

Pay a regular amount into your savings, which you don’t have easy access to.

Start with a plan:

Ways to save

BORROW | ROUND 1

How much as a percentage of my income should I borrow? The first step is to work out how much you can afford to pay out each week. Then, find out through your mortage broker how much this will allow you to borrow. Add your deposit to this amount, and this will tell you the maximum

price you can afford to start the shopping process! It is important to know your budget before you start, so you don’t fall in love with a property and then try to

stretch your money to buy it.

Phase A

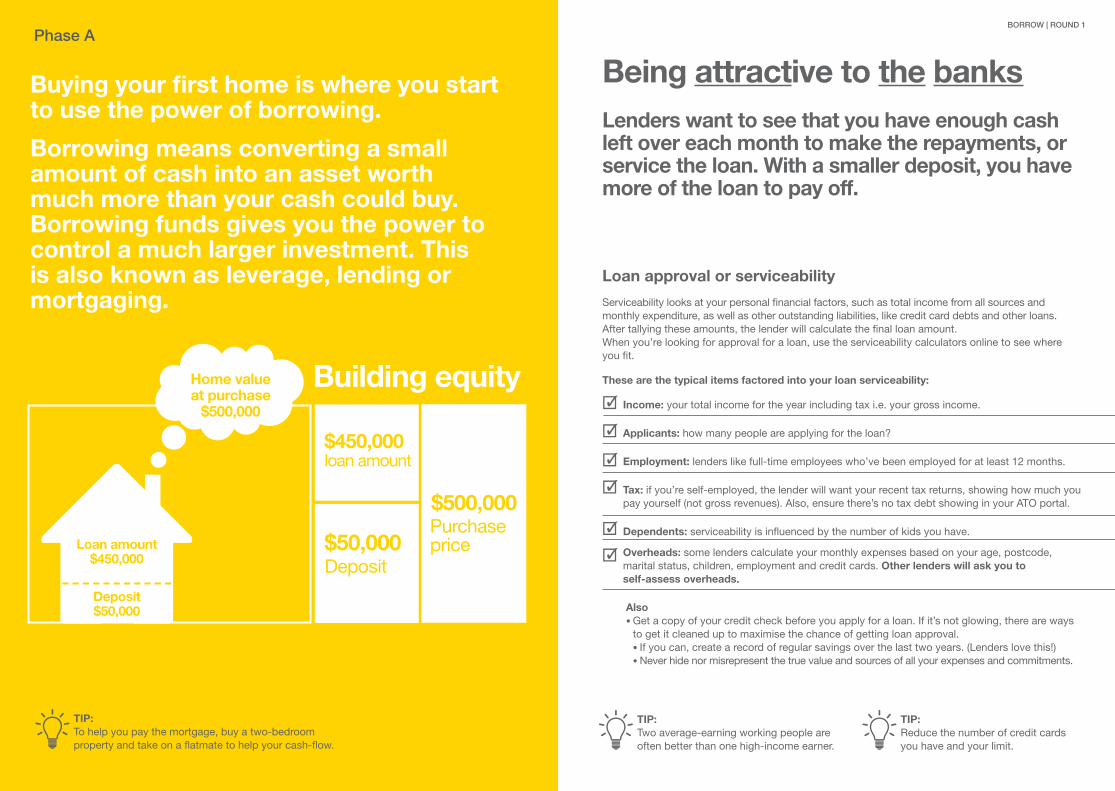

Buying your first home is where you start to use the power of borrowing.

Borrowing means converting a small amount of cash into an asset worth much more than your cash could buy. Borrowing funds gives you the power to control a much larger investment. This is also known as leverage, lending or mortgaging.

$500,000

$50,000 Deposit

Building equity

$450,000loan amount

TIP: To help you pay the mortgage, buy a two-bedroom property and take on a flatmate to help your cash-flow.

Home value at purchase

$500,000

Deposit $50,000

Loan amount $450,000

Being attractive to the banks

Loan approval or serviceability

Serviceability looks at your personal financial factors, such as total income from all sources and monthly expenditure, as well as other outstanding liabilities, like credit card debts and other loans.After tallying these amounts, the lender will calculate the final loan amount.When you’re looking for approval for a loan, use the serviceability calculators online to see where you fit.

These are the typical items factored into your loan serviceability:

Income: your total income for the year including tax i.e. your gross income.

Applicants: how many people are applying for the loan?

Employment: lenders like full-time employees who’ve been employed for at least 12 months.

Tax: if you’re self-employed, the lender will want your recent tax returns, showing how much you pay yourself (not gross revenues). Also, ensure there’s no tax debt showing in your ATO portal.

Dependents: serviceability is influenced by the number of kids you have.

Overheads: some lenders calculate your monthly expenses based on your age, postcode, marital status, children, employment and credit cards. Other lenders will ask you to self-assess overheads.

Also • Get a copy of your credit check before you apply for a loan. If it’s not glowing, there are ways

to get it cleaned up to maximise the chance of getting loan approval. • If you can, create a record of regular savings over the last two years. (Lenders love this!) • Never hide nor misrepresent the true value and sources of all your expenses and commitments.

TIP: Two average-earning working people are often better than one high-income earner.

TIP: Reduce the number of credit cards you have and your limit.

Lenders want to see that you have enough cash left over each month to make the repayments, or service the loan. With a smaller deposit, you have more of the loan to pay off.

BORROW | ROUND 1

Phase A

Purchase price

What lenders are looking for

Lenders want to see that your deposit amount came from genuine savings. You should have six months worth of savings with regular deposits, rather than a few lump sums.

Lenders conduct credit checks on mortgage applicants to see if they have credit defaults or significant money owing or in arrears.

Try to have the same address for at least six months.

+ +

Savings Credit worthy Address

Low doc loan

Along with serviceability, the lender is looking for:

If you are a small business owner or self-employed, you may not have access to an employment contract or pay-as-you-go statements (PAYG),you can still be considered for a ‘low documentation loan’, if you can show documents that substantiate your income (usually tax returns).

TIP: I advise any first-time home buyer who does not fit the standard borrower profile to use a mortgage broker to find a low-doc alternative. You may pay a slightly higher interest rate but it can usually be refinanced after a year.

Matrix of borrowingGetting your first property is the key to the Morello Matrix.

Yes, borrowing at 90 per cent ratio with lenders mortgage insurance is more expensive. I say, if the property is right for you and you are comfortable to make the purchase, lenders’ mortgage insurance gets you into the game.

My approach is:

You have to buy your first property to get into the game.

Lenders’ mortgage insurance (LMI) is a necessary cost, allowing you to buy now rather than another year, when the property may be more expensive.

If the cost of LMI isn’t significantly more than a year of savings or growth in the value of your home is likely to provide, then go now.

BORROW | ROUND 1

Phase A

Rent it out

From first home to income

Your property strategy has just begun.

Once you’ve secured your first property, you are going to turbocharge your investment and use it to buy a second property within the next two years.

You’ll achieve this by doing three things:• Locking in the capital appreciation of the property;

• Paying more into your mortgage than you have to, which will increase the equity in your property; and

• Factoring in tax. This is always a great low-risk way to add to your savings after taking your income tax rate into account.

For the first year of owning your property, you should continue to cut expenses. Make a budget and stick to it. This is what successful investors do when they start out.

TIP: When you do these three things together, you create wealth very quickly.

2Rent

Equity is

the diffe

rence between w

hat your home is worth

and h

ow m

uch y

ou ow

e on i

t...3

Equity

Phase A

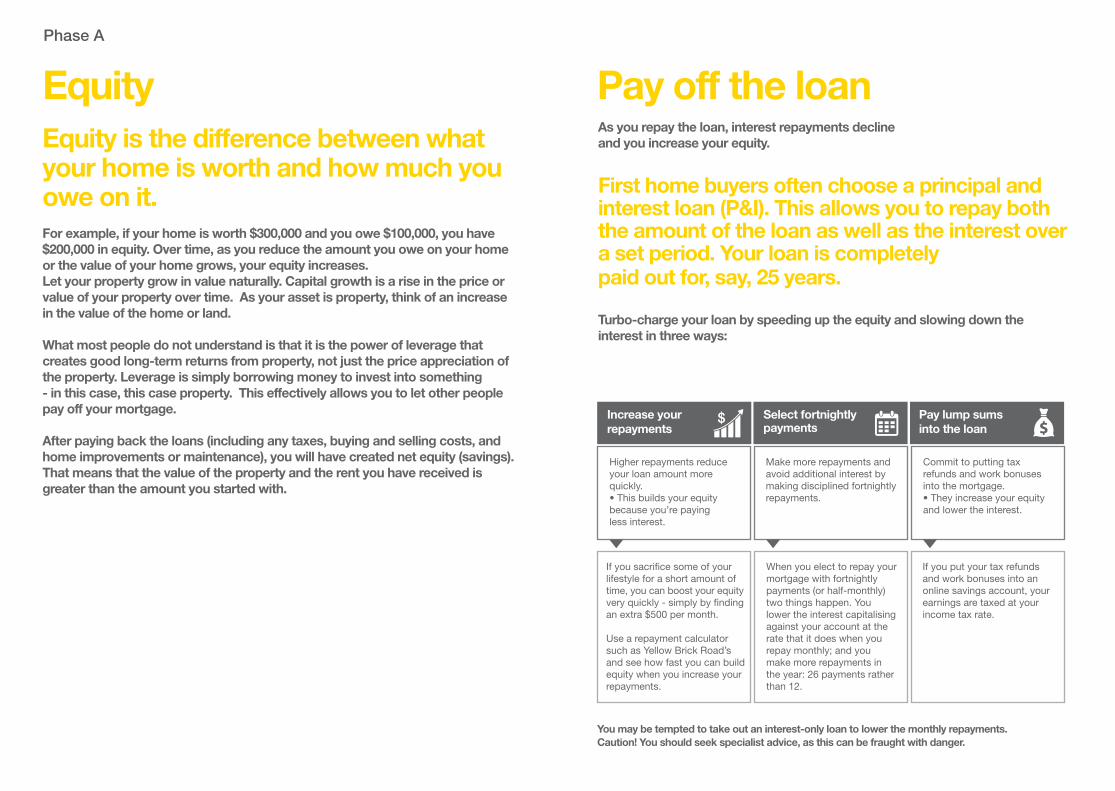

EquityEquity is the difference between what your home is worth and how much you owe on it.For example, if your home is worth $300,000 and you owe $100,000, you have $200,000 in equity. Over time, as you reduce the amount you owe on your home or the value of your home grows, your equity increases.Let your property grow in value naturally. Capital growth is a rise in the price or value of your property over time. As your asset is property, think of an increase in the value of the home or land.

What most people do not understand is that it is the power of leverage that creates good long-term returns from property, not just the price appreciation of the property. Leverage is simply borrowing money to invest into something - in this case, this case property. This effectively allows you to let other people pay off your mortgage.

After paying back the loans (including any taxes, buying and selling costs, and home improvements or maintenance), you will have created net equity (savings). That means that the value of the property and the rent you have received is greater than the amount you started with.

Pay off the loan

First home buyers often choose a principal and interest loan (P&I). This allows you to repay both the amount of the loan as well as the interest over a set period. Your loan is completely paid out for, say, 25 years.

Turbo-charge your loan by speeding up the equity and slowing down the interest in three ways:

Increase your repayments

Select fortnightly payments

5% 4% Pay lump sums into the loan

Higher repayments reduce your loan amount more quickly.• This builds your equity because you’re paying less interest.

When you elect to repay your mortgage with fortnightly payments (or half-monthly) two things happen. You lower the interest capitalising against your account at the rate that it does when you repay monthly; and you make more repayments in the year: 26 payments rather than 12.

Commit to putting tax refunds and work bonuses into the mortgage. • They increase your equity and lower the interest.

If you sacrifice some of your lifestyle for a short amount of time, you can boost your equity very quickly - simply by finding an extra $500 per month.

Use a repayment calculator such as Yellow Brick Road’s and see how fast you can build equity when you increase your repayments.

Make more repayments and avoid additional interest by making disciplined fortnightly repayments.

If you put your tax refunds and work bonuses into an online savings account, your earnings are taxed at your income tax rate.

As you repay the loan, interest repayments decline and you increase your equity.

You may be tempted to take out an interest-only loan to lower the monthly repayments. Caution! You should seek specialist advice, as this can be fraught with danger.

Phase A

Turbocharging the matrix

For those interested in an offset account, get guidance from an adviser about how best to operate one.

Shift money across twice a month.

• Ask your lender to set up an offset account linked to your mortgage.

• Pay any cheques, bonuses, tax refunds and other income into this offset account. In this account, the cash balance is offset against your mortgage balance, reducing it daily by as much as you have in there. The mortgage repayments are taken out of this account. Along the way every dollar in the account reduces your interest.

• Keep the balance as high as possible. Many people put all their income into the offset. Cut your household spending and pay often into the offset account. Then the balance stays high and you can significantly reduce the interest and boost your equity.

• Offset accounts are for disciplined people who work to household budgets. Attached to these accounts are transaction cards. Skip the card so you are not tempted to spend.

EQUITY | ROUND 1

• Get your regular bills (insurance, utilities, health, etc) paid by BPay into those companies.

Phase A

Another way to take the equity- boosting strategy to another level.

My golden rules are:Buy wellto achieve a 5-10 per cent rise in house prices in your area. Your $500,000 house could be worth $525,000 after the first year.

Fortnightly repaymentsmake the change to fortnightly repayments, rather than monthly.

Pay every bonus into the mortgagesuch as tax refunds and work bonuses totalling straight into the mortgage.

Add extra paymentsinto the mortgage, by starting with adding $500 per month.

Add everything into the mortgage.

Once you have your first property, it is time to

supercharge the growth in equity to leverage

into a second property.

Me? I throw everything but the kitchen sink

into these strategies. I put every spare penny into the

mortgage. I find a mortgage broker to find me the best refinancing deal,

including a lender hungry for my business or who is a believer in the area

I’ve bought in.

to buy new cars (or any cars) with the loan. Over time, these savings mean you’ll be able to buy nicer cars all the time or more importantly build up wealth from property much, much faster.

Don’t be tempted

Phase A

3. Fortnightly repayments$500,000 $540,000

$50,000 equity

Start

Year 1Start

Building equity*

$450,000loan

$435,000 loan (Pay down loan)

$105,000 equity (Capital growth improvements)

Year 5 Year 10

$375,000 loan (Pay down loan)

$300,000

$282,877 equity (Capital growth improvements)

$539,636 equity

Year 10

$839,636

*This is for illustration purposes only.

The information presented is intended as a guide only and does not take into account your objectives, financial situation or needs. You should obtain independent legal and financial advice specific to your situation before making any financial decisions.

The information is based on a $450,000 loan over 30 years at 4% interest rate and 8% capital growth. Loan to value ratio, interest rate changes, inflation rates and other market conditions have not been taken into consideration. Figures are based on an assumption of $1250 monthly repayments.

Well spent money on renovations can INCREASE your valuation.

Making your property investment shineHome improvementsWhile you keep paying off the loan and building equity, your property grows in value over time. Now let’s look at the active side of capital growth: capital improvement. This is also known as renovations, repairs or additions.

The trick to improvements is to add value to the property, without spending too much.

Don’t impress yourself when buying or renovating a property. Only spend money on those things that are valued by a potential purchaser. This may not reflect your own tastes.

When it comes to smart improvements, you have one audience: the valuer. The valuer is an independent professional engaged by lenders to appraise properties to buy or refinance. Let’s say you bought a property for $500,000 and a year later you want to refinance it with a valuation of $550,000. The lender seeks an independent valuation to see if the property is valued at - or close to - that price.

Impress the valuer

What does the valuer look for?

First impressions count. Valuers are looking for things such as:

- A tidy garden and some basic landscaping and flower beds

- Well-presented kitchen and bathroom

- A fresh lick of paint

- Extras such as an adjoining garage, ensuites, ceiling fans, air conditioning, new carpets, etc.

Phase A

Making your property investment shine

Smart renovationsWell-spent money on renovations can increase your valuation. The main areas of improvements are bathroom, kitchen, garden and paint.

• buy an apartment with a parking space on a separate title, sell the parking space and reinvest in your mortgage.

Other ways to add valueThere are many ways to make capital improvements:

• buy a run-down house and completely renovate it;

• buy a good piece of land with a run-down house and build a new house on the site;

• buy a house on a large block of land, subdivide it, build a new house and sell it;

• subdivide the land, get a development approval on the vacant block and sell it for a premium; or

A trap to watch for is over-capitalisation. If you knock down an old cottage and build a new home and you end up with not much more equity, you have probably spent too much.

In my opinion, there’ll be many years to renovate your family home with all the comforts you desire. It doesn’t have to be done in the first year.

The swimming pools, outdoor pizza ovens and gazebos can wait.

The first aim is to renovate to add value, so that you can refinance and release cash from the growing equity.

If you spend $100,000 on a renovation and it only yields $50,000 in increased value, you have over-capitalised.

TIP: Don’t spend too much. In the first year, you’re trying to turn your cash-flow wealth into asset wealth. You have to stay focused on creating more value for your asset.

Understanding over-capitalisation

Phase A

Life mistakesEvery property investor makes mistakes at some point.

When you stumble, you have to get back to the winning attitude. The journey with property, through all the economic cycles, is at least 10 years. If you make a mistake, realise it sooner, not later. Dust yourself off and get back on the saddle.

I bought an apartment in Melbourne in 2012 for $435,000. My father had owned the land since the 1970s and I thought it would have been a travesty for a Morello not to own one of the properties subsequently built there.

“Hindsight is a beautiful tutor.” I regret making a business decision with my emotional brain, because as I write this the identical apartment next door to mine just sold, after being on the market for months. The sale price was $380,000. I will have to follow my own advice and hold this property for at least 10 years before I can see the advantages of capital appreciation after inflation has been taken into account.

I can live with one episode of bad buying. But when it’s your first property, be vigilant about what you pay.

My life lesson: Don’t buy on emotion

Working with taxLet’s look at tax in Australia

and making the most of capital gains tax.

Keep in mind the difference between the original

purchase price and the future sale price of your

home. This is where capital gains tax works to your

advantage.

Phase A

4

Working with taxLet’s look at the tax system in Australia and making the most of capital gains tax.

Keep in mind the difference between the original purchase price and the future sale price of your home. This is where capital gains tax works to your advantage.

Principal place of residence

For your investment properties, these are some types of costs you can claim against the income from the rent:

• advertising for tenants• repairs and maintenance• cleaning, gardening and pest control• bank charges, insurances• body corporate fees and charges• borrowing costs i.e. valuation, conveyancing• interest repayment cost on mortgage• council rates, land tax• depreciation of assets• legal expenses, property agent fees and commissions• stationery, postage and property-related travel• undertakings to inspect, maintain or collect the rent• water charges

Income deductions

Investment properties

Investment properties

TIP: If you hold onto the property for more than 12 months, your capital gains tax will have halved.

Negative gearing

Firstly, negative gearing only applies if you are renting out your property.

Negative gearing is when your investment costs are higher than your rental income, which you claim in your tax to reduce your taxable income.

You can think of negative gearing as a tool for reducing your losses.

When property investors own several properties, all of them negatively geared, they can pool their losses and reduce their assessable income accordingly.

So property investment can be seen from two perspectives:

• investment property as wealth creation, using cash-flow positive properties to cover the mortgage repayments so a portfolio of properties can be built;

• investment property as tax planning for high income earners, who use negatively geared properties to reduce their tax bracket; they might end up with a capital gain when they sell the property, or hold the property and eventually make it cash-flow positive.

Positive gearing is where the income your property produces is greater than the ongoing costs, including loan repayments.

The question of whether to own investment properties that are cash-flow positive or that are negatively geared is one of personal taste.

I definitely lean towards cash-flow positive.

I believe that a good business is one that makes more money than it spends, and so that’s how I like to do it.

101

Rental income

Costs incurred

Tax deducution $2,000

$12,000

$10,000

TAX | ROUND 1

If you make a capital gain on your principal place of residence, the gain is usually exempt from capital gains tax (CGT) if the property is held for more than a year. Investment property has its net capital gain taxed at your marginal income tax rate, in the year the contract for sale is signed.

It is never a waste of money to obtain professional taxation advice from a registered tax agent before purchasing a property. Don’t wait until the purchase is in train.

Phase A

The Morello Matrix

Pha

se B

At this point you are preparing to own two properties: - The first, you will live in as your primary place of

residence- Your second, you will rent to tenants as it will become

your investment property

You will use the equity in one to make a deposit on the other. And if you handle it correctly, the rent from your second property will cover its own mortgage and other costs. You will have capital appreciation from two properties, but you only pay the mortgage on one.

Most people who work fulltime have the ability to build this scenario even further, so they eventually have two rental properties and one family home. They’ll own three properties, but only have to fund one mortgage out of their income.

Matrix in five yearsThe plan takes place over five years:

Morello Matrix round two

Year 1 Year 2 Year 3 Year 4 Year 5

Save the deposit and buy the property.

Pay down as much on the principal as you can.

Refinance and use the cash to buy a rental property.

Buy a second investment property from refinancing the other two properties.

TIP: Use the equity in one to make a deposit on the other

Investment property

In the Morello Matrix, you must be clear about which investment properties to buy so your hard-won equity is not wasted on the wrong rental property.

Creating a portfolio of at least three properties is generally an ideal number for most people and how many Australians develop wealth.

What you wantIn your search for an investment property, you are looking for a long-term total return of inflation plus 5 per cent.Other things to look for:• Rental income that covers most, if not all, of the mortgage and outgoings• The likelihood that tenants will always be easy to find• Proven demand and a history of rental income• Low maintenance costs• Saleablility of the property (transport, zoning, community facilities, etc.)

Do your researchSubscribe to a property service such as property data and analytics, which tracks prices in postcodes each quarter. They offer rental yield reports, but you can do your own research too.• Go into five real estate agencies, pick up their rentals lists and study them. • Look at what rents are being charged, for what sort of properties. • It’s not what properties list for, it’s what they sell for and how long they take to sell

(days on the market) that’s important.

Rental incomeRemember, you are looking for rental income as close to 5 per cent p.a. of the market value as possible. This not only makes a good return on your investment, but it is likely to produce the majority of the income required to cover your mortgage.

Selecting your investment propertyOnce you own a rental property, you are a landlord and you’re in the business of accommodation.

Phase B

Your product is accommodation. Take it seriously.

Consider the type of person who will want to rent your property, i.e families want schools, why young professionals want restaurants and public transport Close proximity to shops Distance to schools, universities, colleges Close to churches, playing fields and parks Proximity to public transport If on the edges of the city, close to a freeway Near to cultural hubs such as cinemas and theatres Near to a waterway, such as a beach, harbour or river In a place with character, such as colonial or federation style In a building with community features such as tennis courts, pool or barbecue area Close to a major employment centre

All of these may seem basic, but you must consider them. There are other things to look for in the actual rental property:

Modern, clean kitchen Clean, functional bathroom New floor coverings Good paint job Garden Extras such as paid television connection, storage shed, barbecue area Good laundry (if renting to families)

Type of tenant:

Try to get a tenant to sign up for longer than a year Ask yourself: is the highest payer better than a tenant who is most likely

to really look after your property?

Here’s some of the criteria to look for in a rental property:

Outsourcing service: if you don’t have a lot of time or willingness to invest in learning about legal matters, maintenance and collections, then strongly consider outsourcing this to specialised businesses that do: property management businesses.

Learn your rights and obligations as an owner. Know your tenant’s rights and obligations as well.

Phase B

First property (Principle residence)

Second property(Investment)

Third property(Investment)

Property examples

Let’s say you purchased a $500,000 property for $450,000 loan at the beginning of your journey. Between capital growth, rental income and home improvements, the value of the property has gone up by 10 per cent per annum.

Whilst consciously making repayments to the principle loan, this will set you up for step two and three of this example.

Let’s say you are looking at a one bedroom apartment and wanting to spend $400,000. At 90 per cent loan to value ratio, you’ll need $40,000 in deposit and $360,000 in borrowings. You are going for an interest-only loan at 5 per cent interest which will cost you around $1,500 per month in repayments.

Now let’s look at another number: its current rental is $350 per week. That’s $1,516 per month, or $18,200 per annum.

This apartment has a rental yield of 5 per cent, and its monthly rental income more than covers the mortgage.

The capital appreciation average is 5 per cent per annum in the area, so in the first year of owning the apartment, you make approximately $20,000 from your $400,000 property, for no outgoings. At the end of year two, it’s worth just under $440,000 and you haven’t had to pay the mortgage.

You should be aiming to buy a third rental property, in the first three to five years.

So what do you do? Revalue both properties at this stage. After three years, your first property would now be worth approximately $600,000, against a loan of $400,000. Also revalue your second property that you bought two years ago.

Property two is now worth $440,000 against a loan of $350,000.

Now you are in the advantageous position to utilise your increased equity from one or both of your properties to purchase another.

And so on, and so on...

Perhaps the greatest two questions that people ask are: ‘When should I buy?’ and ‘When should I sell?’. For selling, the answer is easy: don’t ever sell it if it produces a good income, unless someone offers you a price so far above the market price you’d be a fool not to take it.

For purchasing, it generally comes down to your timeframe. If you figure on holding property for the next 20 or 30 years, it generally doesn’t really matter when you purchase it. If you’re speculating (buying and selling inside ten years) be very careful not to buy near a property market peak.

Phase B

The Morello Matrix is not a secret. Thousands of Australians build their wealth this way. But many more Australians stand on the sidelines and choose not to play. This is a pity, as Australia has a really good lending system for property.

It has a vibrant property market that generally doubles every 10 years, particularly in metro areas, and we have a culture of hard work and solid income from employment. These things make property a great way to build wealth.

Borrowing allows you to speed up the process, the rental market allows you to cover mortgage repayments with income, and capital growth allows you to use equity to fund other properties.

The system is sitting beneath our noses, and we have to make the decision to be part of it. And then we have to act.

I hope that these ideas inspire you to browse through those real estate windows, go back to your pens, papers and calculators and then talk to a mortgage broker.

Conclusion The Morello Matrix

More money has been lost by indecision than

by wrong decision.

$

Phase B

My name is Andrew Morello. I’m just a simple boy from

Moonee Ponds, working hard and trying to get ahead in life.

Good luck! Andrew Morello

I’d like to dedicate this eBook to my mother and father, John and Pauline Morello. They have been great role models of the rewards that come from sacrifice and hard work through blood, sweat and tears, in the greatest country in the world: Australia. Andrew Morello

The views presented in this guide is general in nature and does not represent financial product advice. You should always seek independent legal and financial advice before making a decision in relation to a financial product. Yellow Brick Road Finance Pty Ltd ACN 128 708 109, Australian Credit Licence 393195. Yellow Brick Road Wealth Management Pty Ltd ACN 128 650 037, AFSL 323825.

![[Drum] Joe Morello - Rudimental Jazz.pdf](https://img.pdfslide.us/doc/110x75/577c80b51a28abe054a9d86c/drum-joe-morello-rudimental-jazzpdf.jpg)

![[Drum] Joe Morello - Rudimental Jazz](https://img.pdfslide.us/doc/110x75/553d3ce04a7959222a8b458a/drum-joe-morello-rudimental-jazz.jpg)