Embed Size (px)

Citation preview

The Moray Council Feasibility Study:

Residual Waste Treatment

Prepared by Albion Environmental Ltd May 2014

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 1

Contents

Executive Summary ...................................................................................................................... 3

1.0 Introduction ........................................................................................................................ 6

2.0 Background ........................................................................................................................ 7

3.0 Current Situation ................................................................................................................ 9

3.1.1 Introduction .............................................................................................................. 9

3.1.2 Residual Analysis Commentary ........................................................................... 10

3.1.3 Waste Compositional Analysis Conclusion ......................................................... 12

4.0 Future Waste Growth ....................................................................................................... 15

4.1 Future Waste Generation ............................................................................................. 15

4.2 Recycling via a Material Recycling Facility (MRF) ...................................................... 20

4.2.1 Future Waste Predictions for Recycling via a MRF ............................................. 20

4.2.2 Advantages / Disadvantages of Recycling at Source versus recycling at MRF 22

4.3 Commercial Waste ........................................................................................................ 23

4.4 Level of confidence in residual waste tonnage .......................................................... 23

4.4.1 Residual Waste Tonnage ...................................................................................... 23

4.4.2 Waste Composition ............................................................................................... 24

5.0 Carbon Metric ................................................................................................................... 25

6.0 Residual Waste Treatment Technology .......................................................................... 29

6.1 Low Risk Technologies ................................................................................................ 29

6.1.1 Waste Transfer Station .......................................................................................... 29

6.1.2 “Dirty” Material Recycling Facility ........................................................................ 29

6.1.3 “Dirty” MRF with Refuse Derived Fuel Production (RDF) ................................... 30

6.1.4 Solid Recovered Fuel Production (SRF) .............................................................. 30

6.2 Conventional and advanced thermal treatment technologies ................................... 30

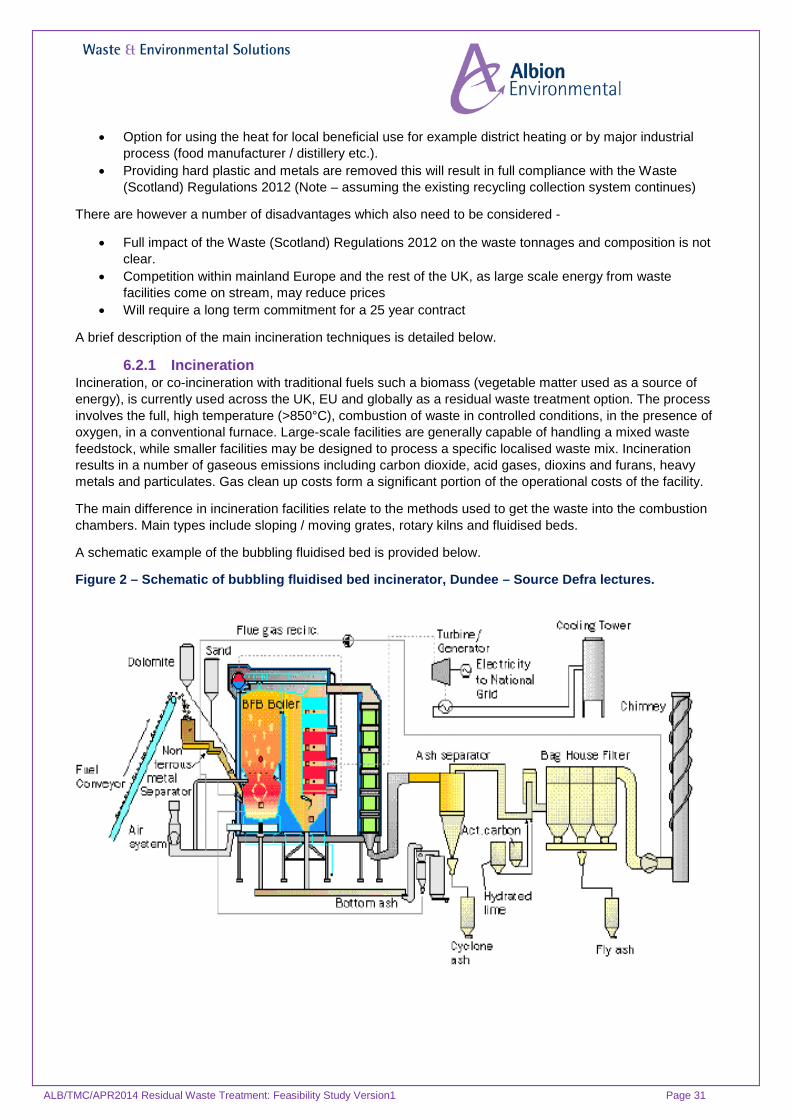

6.2.1 Incineration ............................................................................................................ 31

6.2.2 Pyrolysis................................................................................................................. 32

6.2.3 Gasification ............................................................................................................ 32

6.3 Opportunities to recover energy .................................................................................. 33

6.3.1 Calorific Value of Waste ........................................................................................ 33

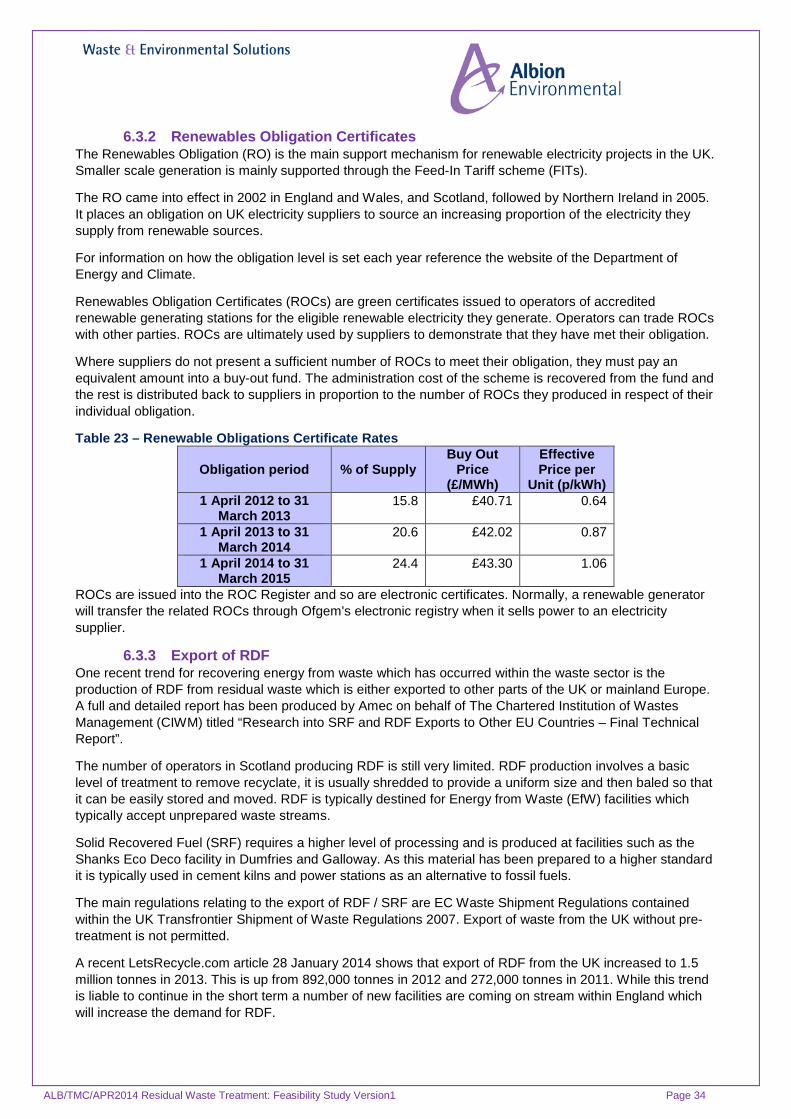

6.3.2 Renewables Obligation Certificates ..................................................................... 34

6.3.3 Export of RDF......................................................................................................... 34

7.0 Proposed Strategies for Residual Waste ........................................................................ 36

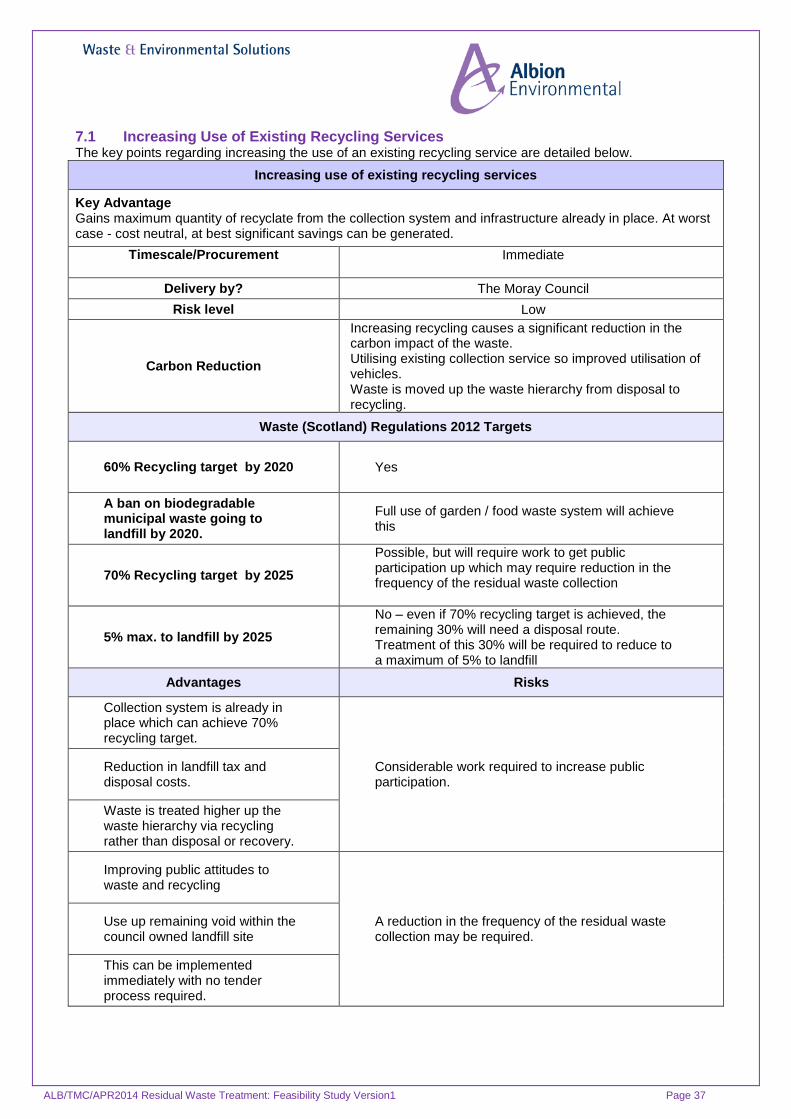

7.1 Increasing Use of Existing Recycling Services .......................................................... 37

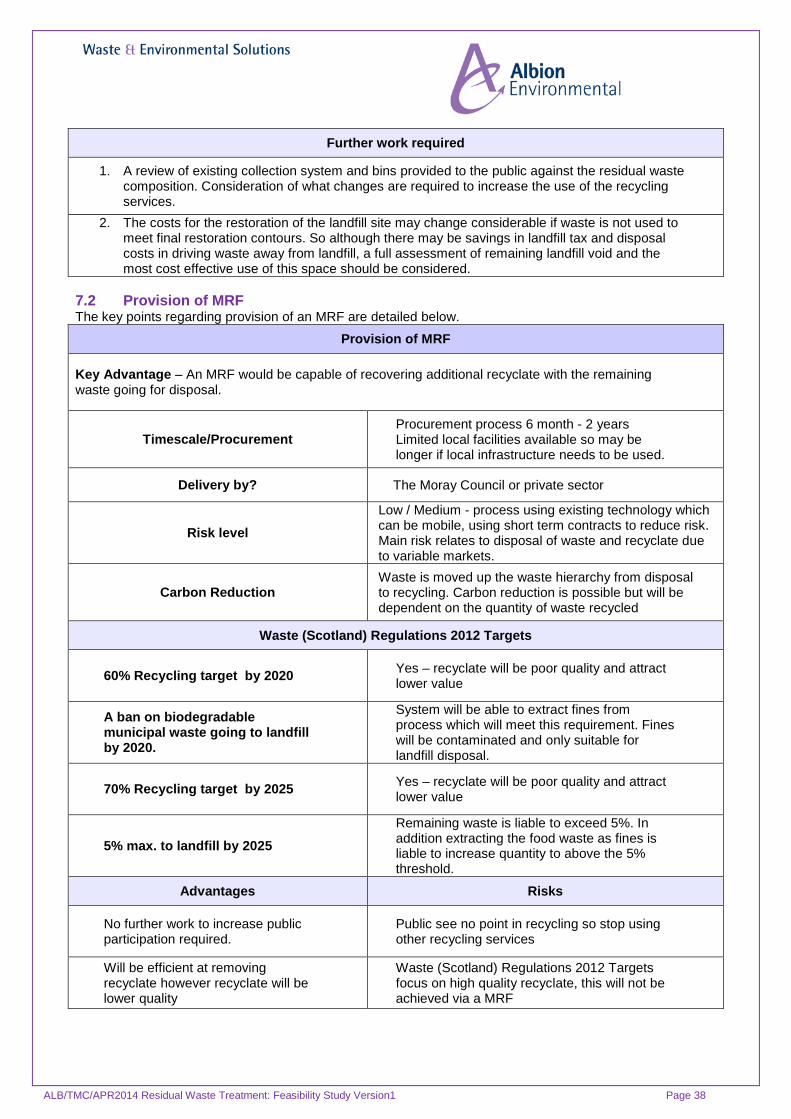

7.2 Provision of MRF .......................................................................................................... 38

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 2

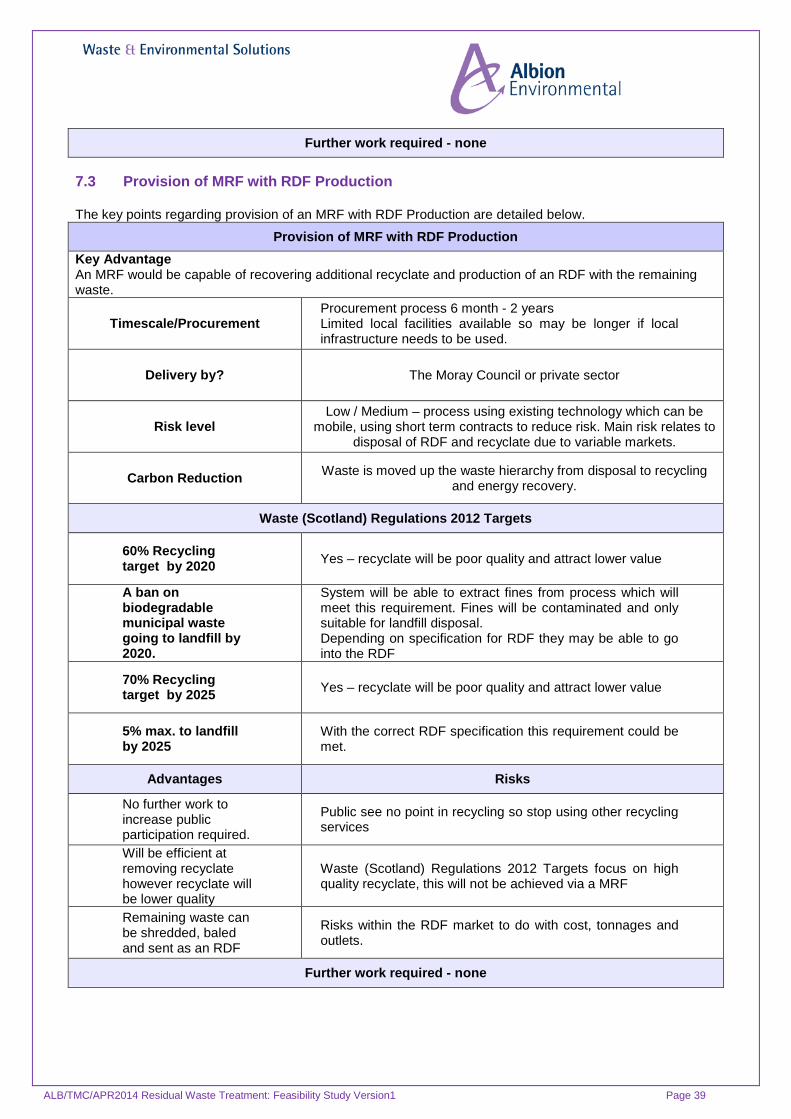

7.3 Provision of MRF with RDF Production ...................................................................... 39

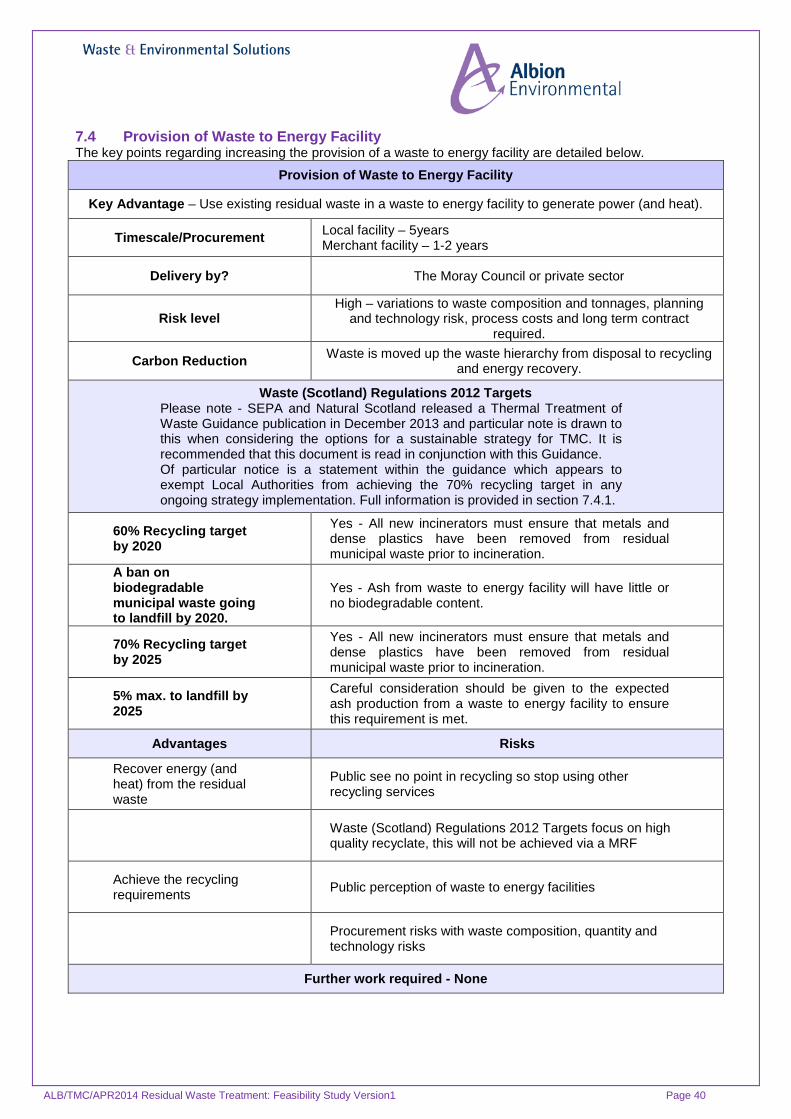

7.4 Provision of Waste to Energy Facility ......................................................................... 40

8.4.1 Thermal Treatment Footnote ................................................................................ 41

8.0 Neighbouring Authorities ................................................................................................ 42

8.1 The Highland Council ................................................................................................... 42

8.2 Aberdeenshire Council ................................................................................................. 42

8.3 Aberdeen City Council ................................................................................................. 42

9.0 Commercial Facilities....................................................................................................... 43

9.1 Facilities within TMC .................................................................................................... 43

9.1.1 Grays Recycling Services Ltd, .............................................................................. 43

9.1.2 J Gordon Williamson Ltd ...................................................................................... 43

9.2 Facilities outwith TMC .................................................................................................. 43

9.2.1 SITA UK .................................................................................................................. 43

9.2.2 Wm. Munro Construction (Highland) Limited ...................................................... 43

9.2.3 Shore Energy ......................................................................................................... 43

9.3 Review of Waste to Energy Facilities .......................................................................... 43

9.3.1 Clean Power Properties ......................................................................................... 44

9.3.2 J Gordon Williamson Ltd ...................................................................................... 44

9.3.3 Combined Power and Heat (Highlands) Ltd ......................................................... 44

9.3.4 Operational facilities within Scotland .................................................................. 44

10.0 Procurement Methods ...................................................................................................... 45

10.1 PFI (Public Finance Initiative) / PPP (Public Private Partnership) Contracts. ........... 45

10.2 Short Term Contracts 1- 5years ................................................................................... 45

10.3 Scotland EXCEL Framework Contracts ...................................................................... 45

10.4 Scotland Wide Brokerage............................................................................................. 46

11.0 Best Strategy Considerations ......................................................................................... 47

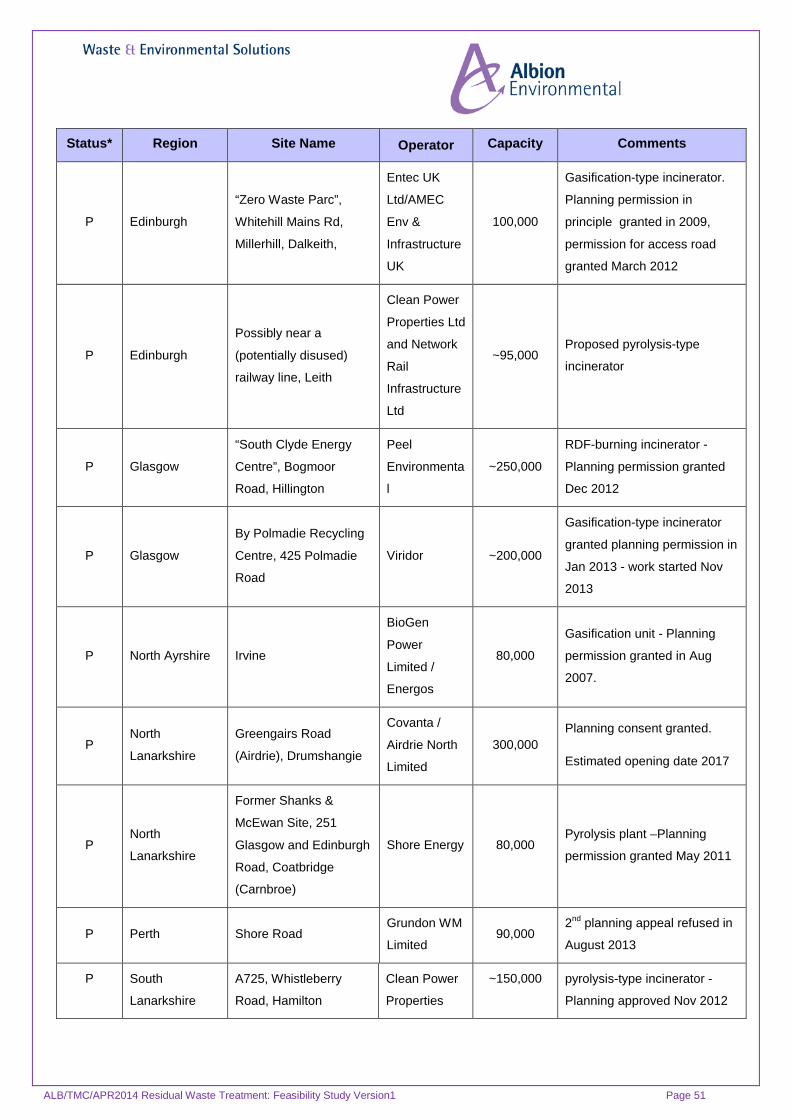

Appendix 1 Table of Energy from Waste projects across Scotland ........................................ 50

Appendix 2 Index of abbreviations ............................................................................................ 53

Appendix 3 Index of references ................................................................................................. 54

Appendix 4 Index of Tables and Graphs ................................................................................... 55

Tables .......................................................................................................................................... 55

Graphs ......................................................................................................................................... 55

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 3

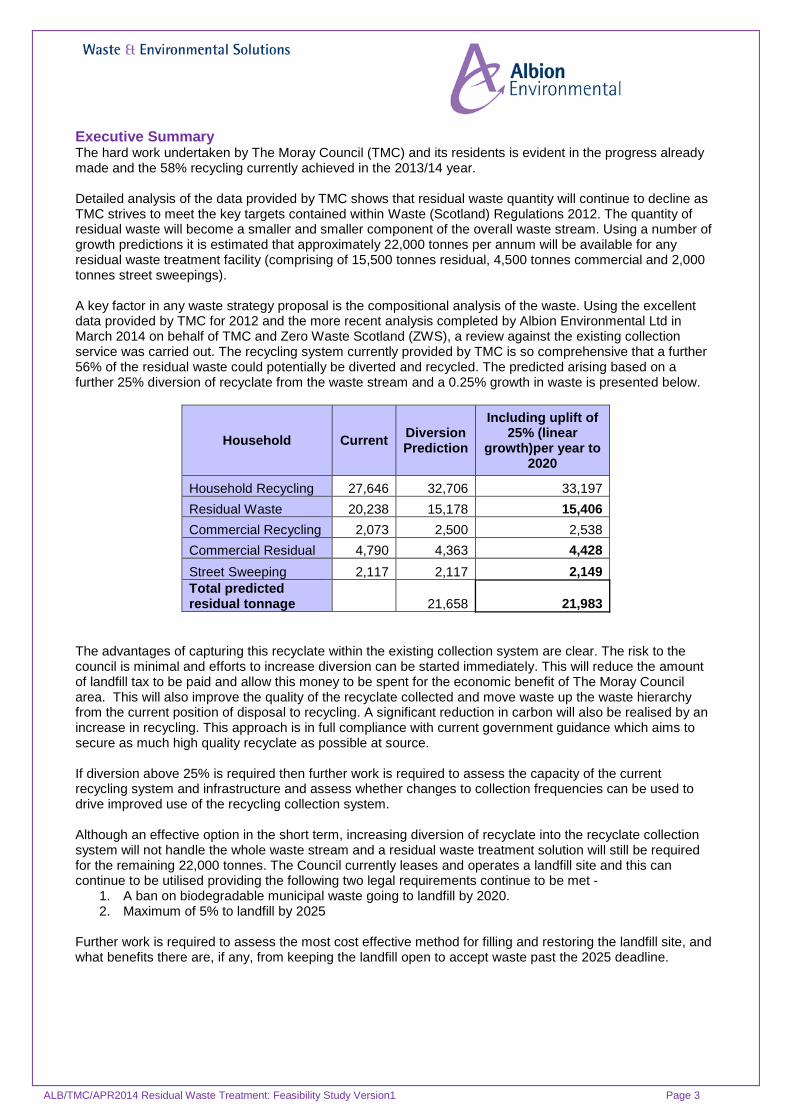

Executive Summary The hard work undertaken by The Moray Council (TMC) and its residents is evident in the progress already made and the 58% recycling currently achieved in the 2013/14 year. Detailed analysis of the data provided by TMC shows that residual waste quantity will continue to decline as TMC strives to meet the key targets contained within Waste (Scotland) Regulations 2012. The quantity of residual waste will become a smaller and smaller component of the overall waste stream. Using a number of growth predictions it is estimated that approximately 22,000 tonnes per annum will be available for any residual waste treatment facility (comprising of 15,500 tonnes residual, 4,500 tonnes commercial and 2,000 tonnes street sweepings). A key factor in any waste strategy proposal is the compositional analysis of the waste. Using the excellent data provided by TMC for 2012 and the more recent analysis completed by Albion Environmental Ltd in March 2014 on behalf of TMC and Zero Waste Scotland (ZWS), a review against the existing collection service was carried out. The recycling system currently provided by TMC is so comprehensive that a further 56% of the residual waste could potentially be diverted and recycled. The predicted arising based on a further 25% diversion of recyclate from the waste stream and a 0.25% growth in waste is presented below.

Household Current Diversion Prediction

Including uplift of 25% (linear

growth)per year to 2020

Household Recycling 27,646 32,706 33,197 Residual Waste 20,238 15,178 15,406 Commercial Recycling 2,073 2,500 2,538 Commercial Residual 4,790 4,363 4,428 Street Sweeping 2,117 2,117 2,149 Total predicted residual tonnage 21,658 21,983

The advantages of capturing this recyclate within the existing collection system are clear. The risk to the council is minimal and efforts to increase diversion can be started immediately. This will reduce the amount of landfill tax to be paid and allow this money to be spent for the economic benefit of The Moray Council area. This will also improve the quality of the recyclate collected and move waste up the waste hierarchy from the current position of disposal to recycling. A significant reduction in carbon will also be realised by an increase in recycling. This approach is in full compliance with current government guidance which aims to secure as much high quality recyclate as possible at source. If diversion above 25% is required then further work is required to assess the capacity of the current recycling system and infrastructure and assess whether changes to collection frequencies can be used to drive improved use of the recycling collection system. Although an effective option in the short term, increasing diversion of recyclate into the recyclate collection system will not handle the whole waste stream and a residual waste treatment solution will still be required for the remaining 22,000 tonnes. The Council currently leases and operates a landfill site and this can continue to be utilised providing the following two legal requirements continue to be met -

1. A ban on biodegradable municipal waste going to landfill by 2020. 2. Maximum of 5% to landfill by 2025

Further work is required to assess the most cost effective method for filling and restoring the landfill site, and what benefits there are, if any, from keeping the landfill open to accept waste past the 2025 deadline.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 4

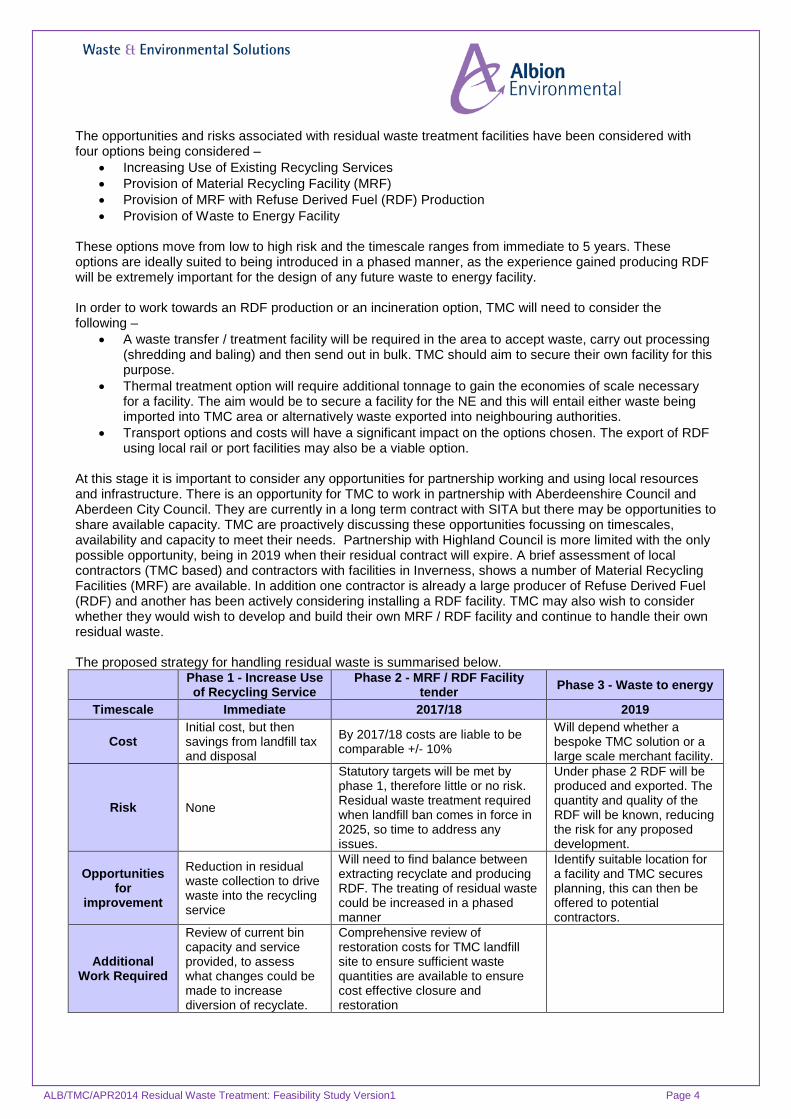

The opportunities and risks associated with residual waste treatment facilities have been considered with four options being considered –

• Increasing Use of Existing Recycling Services • Provision of Material Recycling Facility (MRF) • Provision of MRF with Refuse Derived Fuel (RDF) Production • Provision of Waste to Energy Facility

These options move from low to high risk and the timescale ranges from immediate to 5 years. These options are ideally suited to being introduced in a phased manner, as the experience gained producing RDF will be extremely important for the design of any future waste to energy facility. In order to work towards an RDF production or an incineration option, TMC will need to consider the following –

• A waste transfer / treatment facility will be required in the area to accept waste, carry out processing (shredding and baling) and then send out in bulk. TMC should aim to secure their own facility for this purpose.

• Thermal treatment option will require additional tonnage to gain the economies of scale necessary for a facility. The aim would be to secure a facility for the NE and this will entail either waste being imported into TMC area or alternatively waste exported into neighbouring authorities.

• Transport options and costs will have a significant impact on the options chosen. The export of RDF using local rail or port facilities may also be a viable option.

At this stage it is important to consider any opportunities for partnership working and using local resources and infrastructure. There is an opportunity for TMC to work in partnership with Aberdeenshire Council and Aberdeen City Council. They are currently in a long term contract with SITA but there may be opportunities to share available capacity. TMC are proactively discussing these opportunities focussing on timescales, availability and capacity to meet their needs. Partnership with Highland Council is more limited with the only possible opportunity, being in 2019 when their residual contract will expire. A brief assessment of local contractors (TMC based) and contractors with facilities in Inverness, shows a number of Material Recycling Facilities (MRF) are available. In addition one contractor is already a large producer of Refuse Derived Fuel (RDF) and another has been actively considering installing a RDF facility. TMC may also wish to consider whether they would wish to develop and build their own MRF / RDF facility and continue to handle their own residual waste. The proposed strategy for handling residual waste is summarised below.

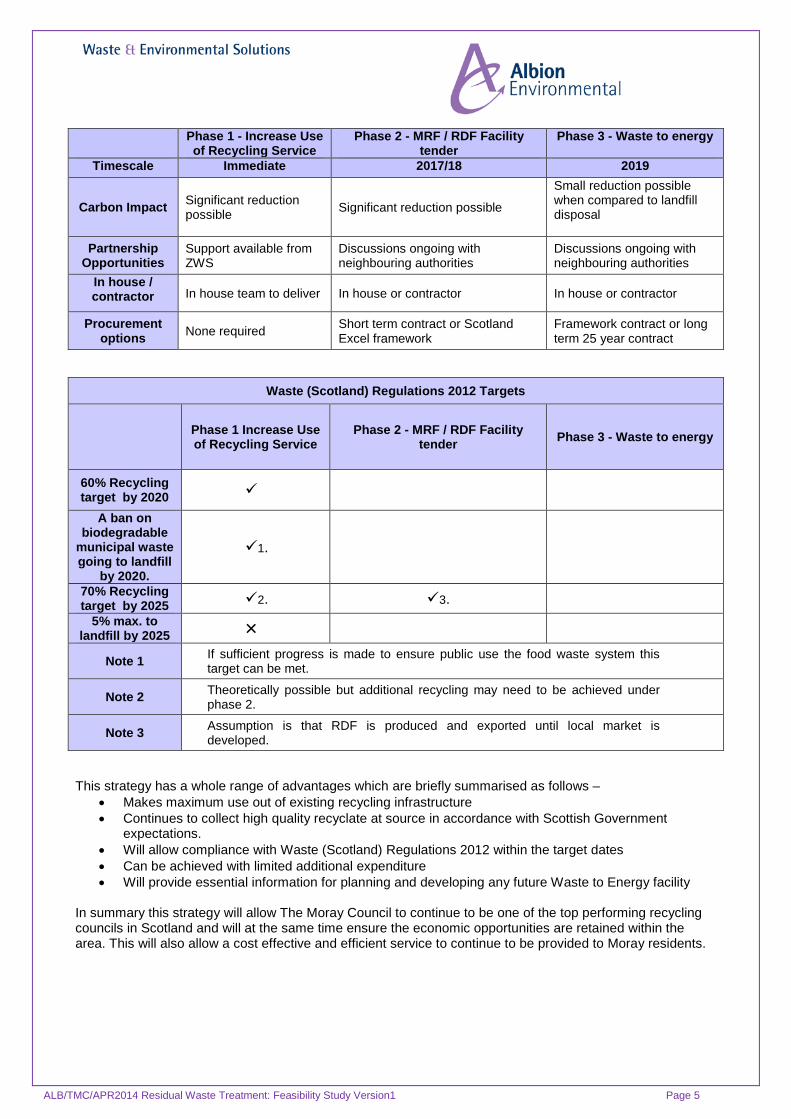

Phase 1 - Increase Use of Recycling Service

Phase 2 - MRF / RDF Facility tender Phase 3 - Waste to energy

Timescale Immediate 2017/18 2019

Cost Initial cost, but then savings from landfill tax and disposal

By 2017/18 costs are liable to be comparable +/- 10%

Will depend whether a bespoke TMC solution or a large scale merchant facility.

Risk None

Statutory targets will be met by phase 1, therefore little or no risk. Residual waste treatment required when landfill ban comes in force in 2025, so time to address any issues.

Under phase 2 RDF will be produced and exported. The quantity and quality of the RDF will be known, reducing the risk for any proposed development.

Opportunities for

improvement

Reduction in residual waste collection to drive waste into the recycling service

Will need to find balance between extracting recyclate and producing RDF. The treating of residual waste could be increased in a phased manner

Identify suitable location for a facility and TMC secures planning, this can then be offered to potential contractors.

Additional Work Required

Review of current bin capacity and service provided, to assess what changes could be made to increase diversion of recyclate.

Comprehensive review of restoration costs for TMC landfill site to ensure sufficient waste quantities are available to ensure cost effective closure and restoration

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 5

Phase 1 - Increase Use of Recycling Service

Phase 2 - MRF / RDF Facility tender

Phase 3 - Waste to energy

Timescale Immediate 2017/18 2019

Carbon Impact Significant reduction possible Significant reduction possible

Small reduction possible when compared to landfill disposal

Partnership Opportunities

Support available from ZWS

Discussions ongoing with neighbouring authorities

Discussions ongoing with neighbouring authorities

In house / contractor

In house team to deliver In house or contractor In house or contractor

Procurement options None required Short term contract or Scotland

Excel framework Framework contract or long term 25 year contract

Waste (Scotland) Regulations 2012 Targets

Phase 1 Increase Use of Recycling Service

Phase 2 - MRF / RDF Facility tender Phase 3 - Waste to energy

60% Recycling target by 2020

A ban on biodegradable

municipal waste going to landfill

by 2020.

1.

70% Recycling target by 2025 2. 3.

5% max. to landfill by 2025 ×

Note 1 If sufficient progress is made to ensure public use the food waste system this target can be met.

Note 2 Theoretically possible but additional recycling may need to be achieved under phase 2.

Note 3 Assumption is that RDF is produced and exported until local market is developed.

This strategy has a whole range of advantages which are briefly summarised as follows – • Makes maximum use out of existing recycling infrastructure • Continues to collect high quality recyclate at source in accordance with Scottish Government

expectations. • Will allow compliance with Waste (Scotland) Regulations 2012 within the target dates • Can be achieved with limited additional expenditure • Will provide essential information for planning and developing any future Waste to Energy facility

In summary this strategy will allow The Moray Council to continue to be one of the top performing recycling councils in Scotland and will at the same time ensure the economic opportunities are retained within the area. This will also allow a cost effective and efficient service to continue to be provided to Moray residents.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 6

1.0 Introduction The Moray Council (TMC) needs to procure a long term sustainable solution other than landfill for approximately 30,000 tonnes per annum of residual waste. This residual waste may contain recyclable elements. The legal definition of waste in the UK is derived from the EU Waste Framework Directive. In basic terms a waste is anything which you decide to, or are required to, discard. Even if the substance or article is given to someone else to be reused or recycled, it is still legally considered to be waste if it is no longer required by the person who holds it. All Local Authorities across Scotland have been tasked with meeting strict targets to reduce the volume of waste requiring disposal, these targets are: • To achieve a recycling/composting rate of 50% of municipal waste by 2013 • Increasing to 60% by 2020 • And further increasing to 70% by 2025 • Additionally a ban on biodegradable municipal waste going to landfill by 2020. • And no more than 5% should be landfilled by 2025 • It is also a requirement to remove dense plastics and metals from residual waste prior to incineration

In an effort to fulfil these requirements in 2004 The Moray Council implemented the Kerbside Recycling Scheme. By 2013 the kerbside recycling scheme had been rolled out to all households in Moray and had been changed to include an increased number of material streams being collected. It is testament to all those who regularly recycle that Moray is now one of the highest performing authorities in Scotland. With a recycling rate of almost 60% The Moray Council has made great progress, however, that still means that almost 40% of waste is currently being sent to landfill. In coming years this will cause an issue for the following reasons: • From 1

st April 2014, landfill tax rose from £72/tonne to £80/tonne. With approximately 27,000 tonnes of

residual waste being sent to landfill this will result in a landfill tax bill of £2.2million for 2014/15 tax year, of which approximately £0.4million is recoverable from traders.

• The 2025 target of no more than 5% to landfill (Waste (Scotland) Regulations 2012), although over 10 years away, will prove to be a difficult target to achieve.

An alternative solution must comply with all current related legislation and this high level study has been carried out to provide an overview of requirements and costs, and identify what areas need to be developed further.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 7

2.0 Background The Moray Council (TMC) needs to procure a long term sustainable solution other than landfill for approximately 30,000 tonnes per annum of residual waste. This residual waste may contain recyclable elements. Residual Waste is that which has been subjected to all reasonably practicable efforts to extract and recover re-usable and recyclable materials. Recent analysis has indicated that with the introduction of food waste collections and an extended range of recyclate material services, the residual waste can still contain between 30-50% material which could be more cost effectively handled by these other services. One aspect we will consider is the impact of increasing the focus on the food and recyclate collection and reducing the frequency of residual waste collection to drive a change in public attitudes. The remaining residual waste will be composed of a variety of different types of material which can be treated in a number of ways. Treatment options can range from a simple shred and screen type operation all the way through to incineration, pyrolysis and gasification. Usually incineration, pyrolysis and gasification require a certain economy of scale and it is likely that the tonnage available from The Moray Council will not be sufficient to secure funding for a facility without working in partnership with other councils. Residual waste can be ‘pre-treated’, for reducing biodegradable components via composting or anaerobic digestion which can stabilise and derive energy from the waste. Recyclable components recovered from residual waste may be used to produce low quality recycled outputs. The Scottish Government has a vision for a zero-waste society where disposal is minimised and all waste is seen as a resource. Elaborating on the aims of the Waste (Scotland) Regulations 2012 and the Scottish Government’s Zero Waste Plan, the Scottish Environment Protection Agency (SEPA) note that legislation ‘aims to maximise levels of closed loop recycling in Scotland through the collection and processing of material resources back into new products and organic wastes back into nutrient cycles.’ The Waste (Scotland) Regulations 2012 require a reduction in quantities of waste sent to landfill by increasing recycling rates, removing biodegradable content from the mixed waste stream and optimising the recovery of materials and energy from residual waste prior to disposal. The 2012 Regulations also require separate waste collections for recyclable and biodegradable waste and introduce a ban on the landfilling or incineration of materials collected separately for recycling by the end of 2013. Together these regulations are likely to have a significant impact on the future composition and quantity of Scotland’s residual waste stream. The residual waste should also be processed as high up the waste hierarchy as possible. Currently waste is either being recycled or landfilled. The aim is to move more waste up to being recycled, with energy being recovered from the remainder.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 8

Figure 1 – Waste Hierarchy

As a result of the 2012 Regulations, the composition of residual waste from all sources will change significantly with increased recovery of recyclables and the segregated collection of different waste streams. This will influence the way in which the remaining material is most effectively treated. Waste management policy and practice have changed significantly over the past fifteen years. With landfill tax increasing and now £80 tonne from 1st April 2014 this has seen an increase in the popularity of alternative treatments. Note - Powers devolved to Scotland in the Scotland Act 2012 mean that from April 2015 the Scottish Parliament will be empowered to introduce and manage taxes on the disposal of waste to landfill, allowing more targeted implementation of the Waste (Scotland) Regulations 2012. In England and Wales the standard and lower rates of landfill tax are to rise in line with inflation from April 2015. At this stage it is not clear whether Scotland intends to also apply this increase. Recent Environment Agency figures show that Refuse Derived Fuel exports have increased from 272k tonnes in 2011 to 1.5 million tonnes in 2013. This trend is liable to continue for the short term while the infrastructure in the UK is fully developed. Residual waste treatment options are important in reducing the amount of waste requiring disposal, as they offer the last opportunity in the current treatment schemes to capture materials and energy from waste before it is ultimately sent to landfill. The Waste (Scotland) Regulations 2012 mark a significant shift from historic practices. The most appropriate approaches for dealing with residual waste will be needed to meet the ‘5% of all waste to landfill’ target by 2025. The Scottish Government considers that the selection and implementation of residual waste treatment options should be a significant part of the waste hierarchy and an area of national policy focus. The current conditions in Scotland in relation to existing and pending thermal treatments/RDF have been affected by the main drivers which include the new obligations arising from the European Waste Framework Directive 2008/98/EC revised, the publication of Scotland’s Zero Waste Plan (2010) and the supporting Waste (Scotland) Regulations 2012. There is broad agreement that while residual waste treatment is a useful and necessary stage of the waste hierarchy, it is economically and environmentally important to manage waste as far up the hierarchy as possible. Residual waste treatment should not be allowed to present a more attractive option than reduction, reuse or recycling, and provision should be made for improved capacity to take action at these earlier stages. Scotland’s Zero Waste Plan (Scottish Government 2010) stated that ‘the Scottish Government will introduce regulatory measures to support the delivery of landfill bans, by ensuring energy from waste treatment is only used to recover value from resources that cannot offer greater environmental and economic benefits through reuse or recycling.’ This measure was formally introduced in the Waste (Scotland) Regulations 2012 and as a result residual waste treatment should only be developed to a capacity fit for, not exceeding, this purpose.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 9

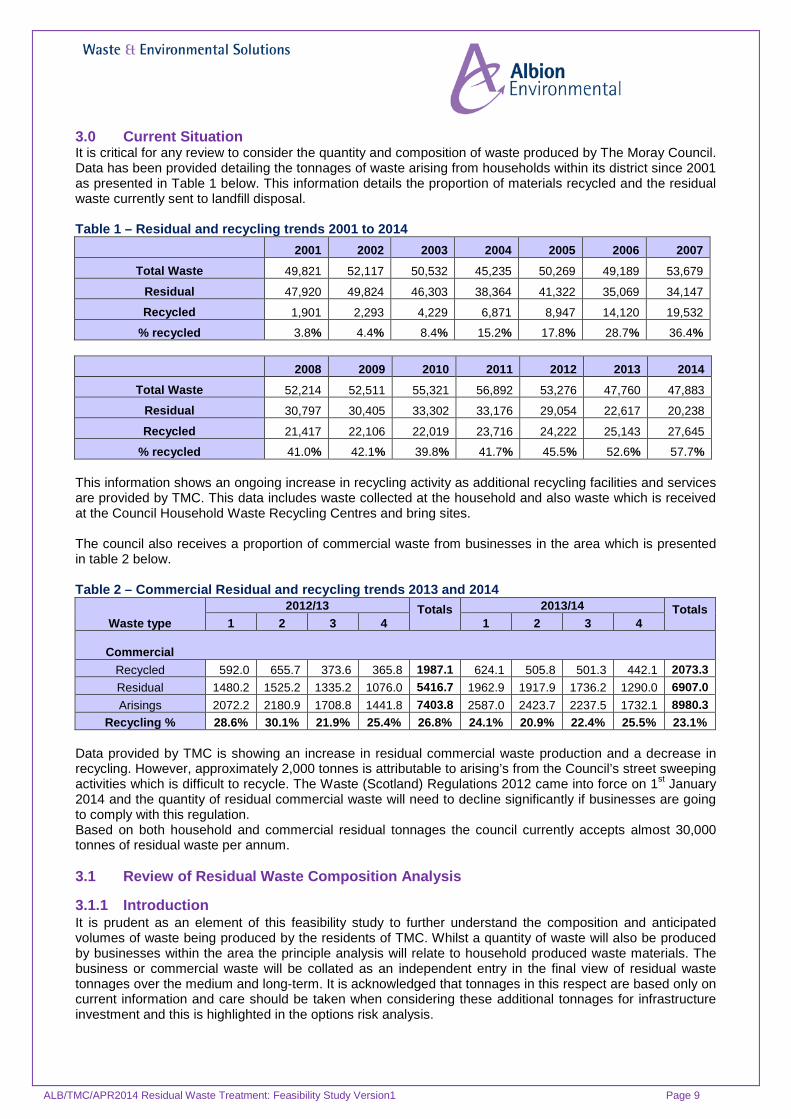

3.0 Current Situation It is critical for any review to consider the quantity and composition of waste produced by The Moray Council. Data has been provided detailing the tonnages of waste arising from households within its district since 2001 as presented in Table 1 below. This information details the proportion of materials recycled and the residual waste currently sent to landfill disposal. Table 1 – Residual and recycling trends 2001 to 2014

2001 2002 2003 2004 2005 2006 2007

Total Waste 49,821 52,117 50,532 45,235 50,269 49,189 53,679

Residual 47,920 49,824 46,303 38,364 41,322 35,069 34,147

Recycled 1,901 2,293 4,229 6,871 8,947 14,120 19,532

% recycled 3.8% 4.4% 8.4% 15.2% 17.8% 28.7% 36.4%

2008 2009 2010 2011 2012 2013 2014

Total Waste 52,214 52,511 55,321 56,892 53,276 47,760 47,883

Residual 30,797 30,405 33,302 33,176 29,054 22,617 20,238

Recycled 21,417 22,106 22,019 23,716 24,222 25,143 27,645

% recycled 41.0% 42.1% 39.8% 41.7% 45.5% 52.6% 57.7% This information shows an ongoing increase in recycling activity as additional recycling facilities and services are provided by TMC. This data includes waste collected at the household and also waste which is received at the Council Household Waste Recycling Centres and bring sites. The council also receives a proportion of commercial waste from businesses in the area which is presented in table 2 below. Table 2 – Commercial Residual and recycling trends 2013 and 2014

Waste type 2012/13 Totals

2013/14 Totals

1 2 3 4 1 2 3 4

Commercial Recycled 592.0 655.7 373.6 365.8 1987.1 624.1 505.8 501.3 442.1 2073.3 Residual 1480.2 1525.2 1335.2 1076.0 5416.7 1962.9 1917.9 1736.2 1290.0 6907.0 Arisings 2072.2 2180.9 1708.8 1441.8 7403.8 2587.0 2423.7 2237.5 1732.1 8980.3

Recycling % 28.6% 30.1% 21.9% 25.4% 26.8% 24.1% 20.9% 22.4% 25.5% 23.1% Data provided by TMC is showing an increase in residual commercial waste production and a decrease in recycling. However, approximately 2,000 tonnes is attributable to arising’s from the Council’s street sweeping activities which is difficult to recycle. The Waste (Scotland) Regulations 2012 came into force on 1st January 2014 and the quantity of residual commercial waste will need to decline significantly if businesses are going to comply with this regulation. Based on both household and commercial residual tonnages the council currently accepts almost 30,000 tonnes of residual waste per annum. 3.1 Review of Residual Waste Composition Analysis

3.1.1 Introduction It is prudent as an element of this feasibility study to further understand the composition and anticipated volumes of waste being produced by the residents of TMC. Whilst a quantity of waste will also be produced by businesses within the area the principle analysis will relate to household produced waste materials. The business or commercial waste will be collated as an independent entry in the final view of residual waste tonnages over the medium and long-term. It is acknowledged that tonnages in this respect are based only on current information and care should be taken when considering these additional tonnages for infrastructure investment and this is highlighted in the options risk analysis.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 10

3.1.2 Residual Analysis Commentary The TMC provided annual residual waste compositional analysis data which has been carried out on a regular basis (at least annually) since 2002. For the purpose of this exercise we have used the most recent data from 2012 and worked through the product descriptions to assess whether this material should be recycled or should remain within the residual waste as per the current council guidance which is readily available to the general public. This recycled material could be segregated in the household and placed in the existing recycling bin service provided by TMC. Please note we have not assessed for any volume restrictions on the recycling bins caused by this increase in recycling activity and this may require further consideration. Table 3 – 2012 Waste compositional analysis

Material Residual

Waste Total %

% Potential

for Recycling

% Remaining

in Residual

Paper, card, newsprint etc. 12.47 7.52 4.95

Plastic Film 7.89 NIL 7.89 Hard Plastic, bottles etc. 11.68 9.98 1.70

Clothing 5.08 5.08 NIL Glass 3.85 3.35 0.50

Metals, batteries, WEEE 4.80 4.80 NIL Disposable Nappies 10.50 NIL 10.50 Hazardous Materials 0.95 NIL 0.95

Hardcore/rubble 4.57 4.57 NIL Kitchen & Garden 34.10 31.03 3.07

Fines 4.11 NIL 4.11 Total 100 66.33 33.67

2012 waste compositional analysis shows that an additional 66% of this waste if segregated properly could be placed in the recycling bins and services provided by TMC. To support this analysis TMC also provided the results from the recent waste compositional analysis which has been completed in conjunction with Zero Waste Scotland and Albion Environmental Ltd. This work involved a sample size of 250 bins and work was completed in March 2014. Again we worked through the product descriptions to assess whether this material should be recycled or should remain within the residual waste as per the current council guidance which is readily available to the general public.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 11

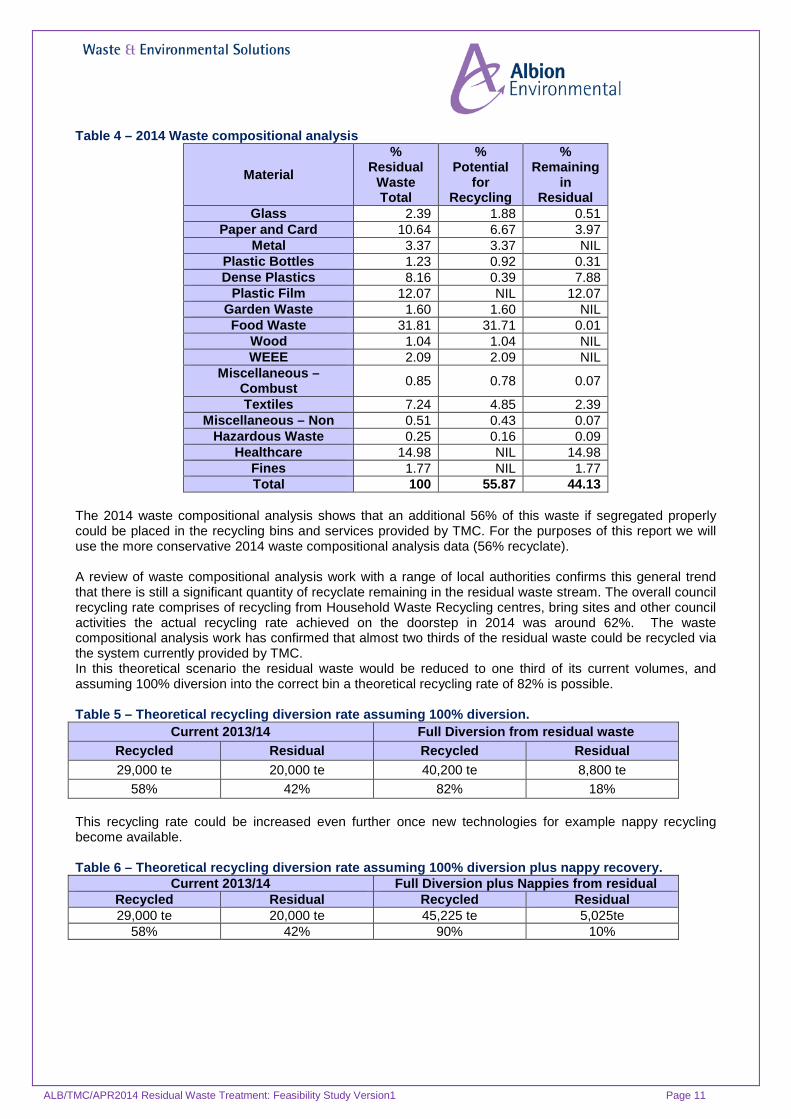

Table 4 – 2014 Waste compositional analysis

Material %

Residual Waste Total

% Potential

for Recycling

% Remaining

in Residual

Glass 2.39 1.88 0.51 Paper and Card 10.64 6.67 3.97

Metal 3.37 3.37 NIL Plastic Bottles 1.23 0.92 0.31 Dense Plastics 8.16 0.39 7.88

Plastic Film 12.07 NIL 12.07 Garden Waste 1.60 1.60 NIL Food Waste 31.81 31.71 0.01

Wood 1.04 1.04 NIL WEEE 2.09 2.09 NIL

Miscellaneous – Combust 0.85 0.78 0.07

Textiles 7.24 4.85 2.39 Miscellaneous – Non 0.51 0.43 0.07

Hazardous Waste 0.25 0.16 0.09 Healthcare 14.98 NIL 14.98

Fines 1.77 NIL 1.77 Total 100 55.87 44.13

The 2014 waste compositional analysis shows that an additional 56% of this waste if segregated properly could be placed in the recycling bins and services provided by TMC. For the purposes of this report we will use the more conservative 2014 waste compositional analysis data (56% recyclate). A review of waste compositional analysis work with a range of local authorities confirms this general trend that there is still a significant quantity of recyclate remaining in the residual waste stream. The overall council recycling rate comprises of recycling from Household Waste Recycling centres, bring sites and other council activities the actual recycling rate achieved on the doorstep in 2014 was around 62%. The waste compositional analysis work has confirmed that almost two thirds of the residual waste could be recycled via the system currently provided by TMC. In this theoretical scenario the residual waste would be reduced to one third of its current volumes, and assuming 100% diversion into the correct bin a theoretical recycling rate of 82% is possible. Table 5 – Theoretical recycling diversion rate assuming 100% diversion.

Current 2013/14 Full Diversion from residual waste Recycled Residual Recycled Residual 29,000 te 20,000 te 40,200 te 8,800 te

58% 42% 82% 18% This recycling rate could be increased even further once new technologies for example nappy recycling become available. Table 6 – Theoretical recycling diversion rate assuming 100% diversion plus nappy recovery.

Current 2013/14 Full Diversion plus Nappies from residual Recycled Residual Recycled Residual 29,000 te 20,000 te 45,225 te 5,025te

58% 42% 90% 10%

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 12

3.1.3 Waste Compositional Analysis Conclusion Based on the Council waste compositional analysis and the recent 2014 ZWS / Albion analysis it is clear that a significant portion of recyclate remains in the residual waste. Analysis results would also indicate it is possible to achieve over 70% recycling using the existing system and infrastructure that TMC has in place. Further analysis of the waste quantities would establish whether the frequency of collections would need to be changed. These changes to the actual collection system are likely to be cost neutral as any increase in recycling collections would result in a corresponding decrease in residual waste collections. It is clear from the above rates that TMC has not yet maximised the recycling rates and potential which could be achieved at a household level. There are clear advantages to this approach of maximising recycling rates which include –

• Collection costs – cost neutral • Landfill tax savings (see 3.1.4) • Waste is moved higher up the waste hierarchy, from disposal to recycling. • Increasing recycling and participation will improve public attitudes to waste and resources.

The main disadvantage is that additional resources will need to be allocated to improve public participation and encourage the public to use the service correctly. Costs are likely to relate to –

• Additional Awareness / Enforcement officers • Rigorous application of contamination policy including both contamination of recyclate and

contamination of residual waste with recyclate • Increasing training for crews and call centre staff to drive change • Local awareness raising campaigns • Increasing waste and resource education in schools

The savings generated from reduced disposal costs and reduced landfill tax costs should therefore be viewed as an opportunity to improve public participation and encourage the public to use the service correctly. This will provide significant social and economic benefits to TMC, in comparison to paying landfill tax which has little or no benefit for the local community. The diversion of large quantities of waste into the recyclate stream is obviously going to reduce the overall quantity of residual waste which will need to be treated. The impact of this will be considered further in section 4.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 13

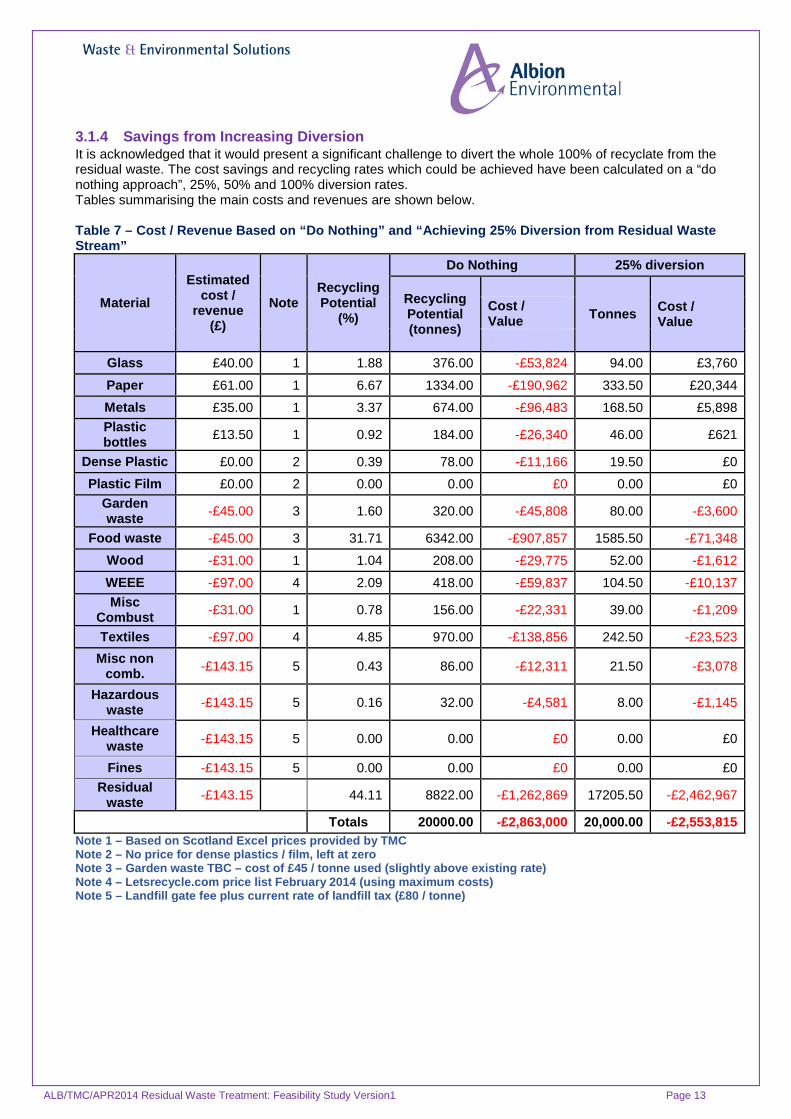

3.1.4 Savings from Increasing Diversion It is acknowledged that it would present a significant challenge to divert the whole 100% of recyclate from the residual waste. The cost savings and recycling rates which could be achieved have been calculated on a “do nothing approach”, 25%, 50% and 100% diversion rates. Tables summarising the main costs and revenues are shown below. Table 7 – Cost / Revenue Based on “Do Nothing” and “Achieving 25% Diversion from Residual Waste Stream”

Material Estimated

cost / revenue

(£) Note

Recycling Potential

(%)

Do Nothing 25% diversion

Recycling Potential (tonnes)

Tonnes Cost / Value

Cost / Value

Glass £40.00 1 1.88 376.00 -£53,824 94.00 £3,760

Paper £61.00 1 6.67 1334.00 -£190,962 333.50 £20,344 Metals £35.00 1 3.37 674.00 -£96,483 168.50 £5,898 Plastic bottles £13.50 1 0.92 184.00 -£26,340 46.00 £621

Dense Plastic £0.00 2 0.39 78.00 -£11,166 19.50 £0 Plastic Film £0.00 2 0.00 0.00 £0 0.00 £0

Garden waste -£45.00 3 1.60 320.00 -£45,808 80.00 -£3,600

Food waste -£45.00 3 31.71 6342.00 -£907,857 1585.50 -£71,348 Wood -£31.00 1 1.04 208.00 -£29,775 52.00 -£1,612

WEEE -£97.00 4 2.09 418.00 -£59,837 104.50 -£10,137 Misc

Combust -£31.00 1 0.78 156.00 -£22,331 39.00 -£1,209

Textiles -£97.00 4 4.85 970.00 -£138,856 242.50 -£23,523 Misc non

comb. -£143.15 5 0.43 86.00 -£12,311 21.50 -£3,078

Hazardous waste -£143.15 5 0.16 32.00 -£4,581 8.00 -£1,145

Healthcare waste -£143.15 5 0.00 0.00 £0 0.00 £0

Fines -£143.15 5 0.00 0.00 £0 0.00 £0 Residual

waste -£143.15 44.11 8822.00 -£1,262,869 17205.50 -£2,462,967

Totals 20000.00 -£2,863,000 20,000.00 -£2,553,815 Note 1 – Based on Scotland Excel prices provided by TMC Note 2 – No price for dense plastics / film, left at zero Note 3 – Garden waste TBC – cost of £45 / tonne used (slightly above existing rate) Note 4 – Letsrecycle.com price list February 2014 (using maximum costs) Note 5 – Landfill gate fee plus current rate of landfill tax (£80 / tonne)

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 14

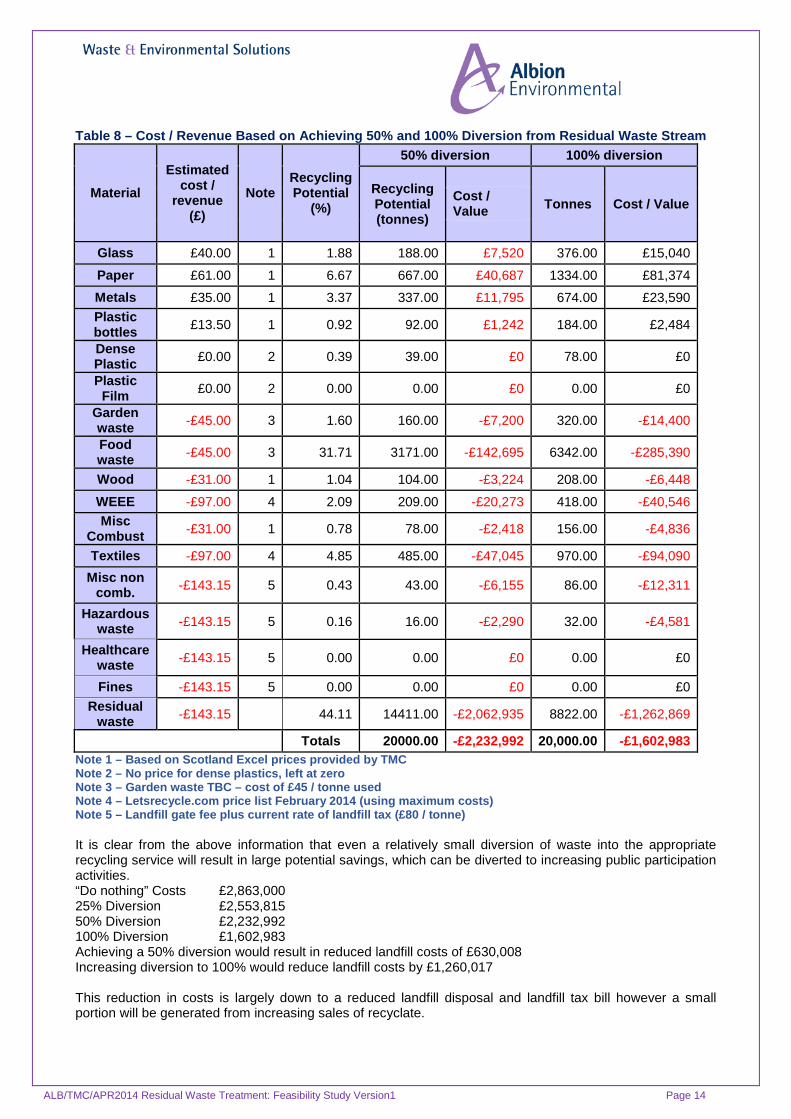

Table 8 – Cost / Revenue Based on Achieving 50% and 100% Diversion from Residual Waste Stream

Material Estimated

cost / revenue

(£) Note

Recycling Potential

(%)

50% diversion 100% diversion

Recycling Potential (tonnes)

Tonnes Cost / Value Cost / Value

Glass £40.00 1 1.88 188.00 £7,520 376.00 £15,040

Paper £61.00 1 6.67 667.00 £40,687 1334.00 £81,374 Metals £35.00 1 3.37 337.00 £11,795 674.00 £23,590 Plastic bottles £13.50 1 0.92 92.00 £1,242 184.00 £2,484

Dense Plastic £0.00 2 0.39 39.00 £0 78.00 £0

Plastic Film £0.00 2 0.00 0.00 £0 0.00 £0

Garden waste -£45.00 3 1.60 160.00 -£7,200 320.00 -£14,400

Food waste -£45.00 3 31.71 3171.00 -£142,695 6342.00 -£285,390

Wood -£31.00 1 1.04 104.00 -£3,224 208.00 -£6,448

WEEE -£97.00 4 2.09 209.00 -£20,273 418.00 -£40,546 Misc

Combust -£31.00 1 0.78 78.00 -£2,418 156.00 -£4,836

Textiles -£97.00 4 4.85 485.00 -£47,045 970.00 -£94,090 Misc non

comb. -£143.15 5 0.43 43.00 -£6,155 86.00 -£12,311

Hazardous waste -£143.15 5 0.16 16.00 -£2,290 32.00 -£4,581

Healthcare waste -£143.15 5 0.00 0.00 £0 0.00 £0

Fines -£143.15 5 0.00 0.00 £0 0.00 £0 Residual

waste -£143.15 44.11 14411.00 -£2,062,935 8822.00 -£1,262,869

Totals 20000.00 -£2,232,992 20,000.00 -£1,602,983 Note 1 – Based on Scotland Excel prices provided by TMC Note 2 – No price for dense plastics, left at zero Note 3 – Garden waste TBC – cost of £45 / tonne used Note 4 – Letsrecycle.com price list February 2014 (using maximum costs) Note 5 – Landfill gate fee plus current rate of landfill tax (£80 / tonne) It is clear from the above information that even a relatively small diversion of waste into the appropriate recycling service will result in large potential savings, which can be diverted to increasing public participation activities. “Do nothing” Costs £2,863,000 25% Diversion £2,553,815 50% Diversion £2,232,992 100% Diversion £1,602,983 Achieving a 50% diversion would result in reduced landfill costs of £630,008 Increasing diversion to 100% would reduce landfill costs by £1,260,017 This reduction in costs is largely down to a reduced landfill disposal and landfill tax bill however a small portion will be generated from increasing sales of recyclate.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 15

The best return that can be achieved for both the extent of materials presented for recycling and the greatest value achieved commercially is to segregate at source. TMC have shown great progress in achieving almost 60% recycling rates using intelligent methods of collection. With the residents supporting the established systems it is clear that there is a culture to support efforts to drive solutions up the waste hierarchy. Improving the use of the recycling services provides a simple opportunity for TMC to drive up recycling rates, reduce costs and reduce the quantity of residual waste which needs to be handled. This can all be achieved at little or no risk to the Council, and complies with the current Scottish Government strategy of maximising the quality of recyclate by collecting at source.

4.0 Future Waste Growth The general trend across Scotland is that residual waste quantities have been in slow decline in recent years partially due to the poor economic climate and partially due to better quality of data recording. The general consensus is that waste quantities will gradually increase as the economic environment improves. This is a particularly difficult time to try and predict future tonnages as the impact and increased awareness around the implementation of the Waste (Scotland) Regulations 2012 will not be fully established for a number of years. The following predictions have been based on the following information –

• Base data - year 2013/14 data and mean average for the period 2006/12 • Growth data of 0.25%, 0.4% and 0.6% • An assumption that recycling at source as per the spirit of the Waste (Scotland) Regulations 2012

will be the preferred option

4.1 Future Waste Generation To facilitate the understanding of the potential growth in waste volumes to be treated by TMC a model was constructed to highlight the strands of data which could affect the estimated volume of residual waste. The following tables are constructed to build a picture of the arisings both through to the target date for compliance in 2025, and a longer-term prediction through to 2045. The methods to achieve further recovery of the materials highlighted in the residual waste analysis section of this report where potentially 56% of the residual waste could be presented for recycling and material recovery. WRAP reports that ongoing population growth and associated waste generation in households across the UK will potentially increase by 2% year-on-year. However for the utilising data specific to the area we can consider three growth scenarios

1. Using the historic growth of waste data this demonstrates a 4% growth over the previous 16 years and a linear extrapolation of this data is presented at 0.25% per year.

2. Using the Moray Demographics Factsheet published in 2014 using 2012 data this predicts an increase in population in the area of 0.40% per year. This is presented as a linear extrapolation over the period.

3. Using the Moray Demographics Factsheet published in 2014 using 2012 data this predicts an increase in dwellings in the area of 0.60% per year. This is presented as a linear extrapolation over the period.

It should be noted that these factsheets predict population through to 2035 and the analysis below does not take into account the differing recycling behaviours observed by the population when stratified across different social criteria. The historic data supplied to particularise the waste tonnages generated since 2001 show two distinct patterns where from the period 2006 -2012 a total tonnage of the combined recycled and residual waste is noticeably higher than the figures for the following years. To aid understanding of each of the scenarios detailed below two base tonnage levels have been used. Firstly the annualised waste production data for the year 2013/14 and secondly a mean average for the period 2006/12.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 16

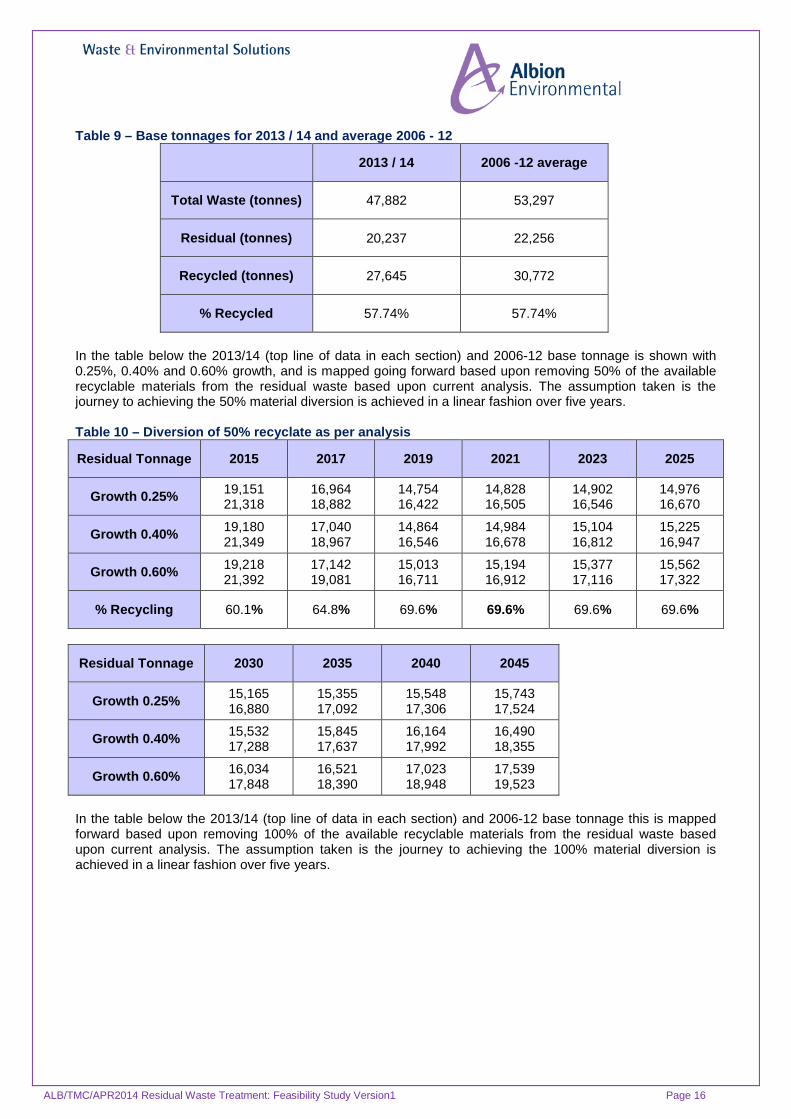

Table 9 – Base tonnages for 2013 / 14 and average 2006 - 12

2013 / 14 2006 -12 average

Total Waste (tonnes) 47,882 53,297

Residual (tonnes) 20,237 22,256

Recycled (tonnes) 27,645 30,772

% Recycled 57.74% 57.74%

In the table below the 2013/14 (top line of data in each section) and 2006-12 base tonnage is shown with 0.25%, 0.40% and 0.60% growth, and is mapped going forward based upon removing 50% of the available recyclable materials from the residual waste based upon current analysis. The assumption taken is the journey to achieving the 50% material diversion is achieved in a linear fashion over five years. Table 10 – Diversion of 50% recyclate as per analysis

Residual Tonnage 2015 2017 2019 2021 2023 2025

Growth 0.25% 19,151 21,318

16,964 18,882

14,754 16,422

14,828 16,505

14,902 16,546

14,976 16,670

Growth 0.40% 19,180 21,349

17,040 18,967

14,864 16,546

14,984 16,678

15,104 16,812

15,225 16,947

Growth 0.60% 19,218 21,392

17,142 19,081

15,013 16,711

15,194 16,912

15,377 17,116

15,562 17,322

% Recycling 60.1% 64.8% 69.6% 69.6% 69.6% 69.6%

Residual Tonnage 2030 2035 2040 2045

Growth 0.25% 15,165 16,880

15,355 17,092

15,548 17,306

15,743 17,524

Growth 0.40% 15,532 17,288

15,845 17,637

16,164 17,992

16,490 18,355

Growth 0.60% 16,034 17,848

16,521 18,390

17,023 18,948

17,539 19,523

In the table below the 2013/14 (top line of data in each section) and 2006-12 base tonnage this is mapped forward based upon removing 100% of the available recyclable materials from the residual waste based upon current analysis. The assumption taken is the journey to achieving the 100% material diversion is achieved in a linear fashion over five years.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 17

Table 11 – Diversion of 100% recyclate as per analysis

Residual Tonnage 2015 2017 2019 2021 2023 2025

Growth 0.25% 19,151 21,318

16,964 18,882

14,754 16,442

12,521 13,937

10,266 11,427

9,152 10,187

Growth 0.40% 19,180 21,349

17,040 18,967

14,864 16,546

12,653 14,084

10,405 11,582

9,304 10,356

Growth 0.60% 19,218 21,392

17,142 19,081

15,013 16,711

12,830 14,281

10,593 11,791

9,510 10,585

% Recycling 60.1% 64.8% 69.6% 74.3% 79.0% 81.4%

Residual Tonnage 2030 2035 2040 2045

Growth 0.25% 9,267 10,315

9,384 10,445

9,502 10,576

9,621 10,709

Growth 0.40% 9,492 10,565

9,683 10,778

9,878 10,995

10,077 11,217

Growth 0.60% 9,799 10,907

10,096 11,238

10,403 11,579

10,719 11,931

In the table below the 2013/14 (top line of data in each section) and 2006-12 base tonnage this is mapped forward to hit the legal minimum requirements for 60% recycling by 2020, 70% recycling by 2025, the diversion of all metals and dense plastics and no more than 5% material permitted to landfill disposal diverting available recyclable materials from the residual waste based upon current analysis. The assumption taken is the journey to achieving this will be completed in a linear manner to hit the target dates Table 12 – Diversion as per legal targets

Residual Tonnage 2015 2017 2019 2021 2023 2025

Growth 0.25% 19,720 21,950

19,590 21,806

19,458 21,659

18,864 20,997

17,220 19,167

14,743 16,411

Growth 0.40% 19,749 21,983

19,678 21,904

19,832 21,571

19,062 21,218

17,453 19,427

14,988 16,683

Growth 0.60% 19,788 22,026

19,796 22,035

19,801 22,040

19,330 21,516

17,769 19,778

15,320 17,052

% Recycling 58.9% 59.4% 59.9% 61.3% 64.8% 70%

Residual Tonnage 2030 2035 2040 2045

Growth 0.25% 14,929 16,617

15,116 16,826

15,306 17,037

15,498 17,251

Growth 0.40% 15,290 17,019

15,598 17,362

15,913 17,713

16,234 18,070

Growth 0.60% 15,785 17,570

16,264 18,103

16,758 18,653

17,267 19,219

Using this information a best estimate and data map can be drawn building on the baseline data and elevated sensitivity with a predicted waste growth from population increase of 0.25%, 0.4%, 0.6% and the extraction of recoverable materials from the residual waste of both 50% and 100%.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 18

See over the page for Graph 1. The trend and information indicate that it will be several years until a stable waste output picture can be understood as TMC achieve the recycling targets. It is clear that there is an opportunity to increase recycling, decrease disposal costs and meet recycling targets by an increased focus on ensuring the correct waste is placed in the correct bin. On the assumption that TMC would wish to encourage the use of waste further up the waste hierarchy, and utilise the existing collection service this analysis would indicate that a residual waste solution should be designed with a tolerance between 9,500 tonnes per annum and 18,000 tonnes per annum with an anticipated arising of circa 14,000 tonnes per annum. Tonnages relating to commercial waste should also be considered and they are included in section 4.3.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 19

Graph 1 – Projected Waste Tonnages

0

5,000

10,000

15,000

20,000

25,000

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

Combined Residual Waste Statistical View

Flex of 2013/14 with 0.25% annual waste growth recovering 50% of recyclable materials in residualwaste plus metals and plastic

Flex of 2006/12 average with 0.25% annual waste growth recovering 50% of recyclable materials inresidual waste plus metals and plastic

Flex of 2013/14 with 0.4% annual waste growth recovering 50% of recyclable materials in residualwaste plus metals and plastic

Flex of 2006/12 average with 0.4% annual waste growth recovering 50% of recyclable materials inresidual waste plus metals and plastic

Flex of 2013/14 with 0.6% annual waste growth recovering 50% of recyclable materials in residualwaste plus metals and plastic

Flex of 2006/12 average with 0.6% annual waste growth recovering 50% of recyclable materials inresidual waste plus metals and plastic

Flex of 2013/14 with 0.25% annual waste growth recovering 100% of recyclable materials in residualwaste

Flex of 2006/12 average with 0.25% annual waste growth recovering 100% of recyclable materials inresidual waste

Flex of 2013/14 with 0.4% annual waste growth recovering 100% of recyclable materials in residualwaste plus metals and plastic

Flex of 2006/12 average with 0.4% annual waste growth recovering 100% of recyclable materials inresidual waste plus metals and plastic

Flex of 2013/14 with 0.6% annual waste growth recovering 100% of recyclable materials in residualwaste plus metals and plastic

Flex of 2006/12 average with 0.6% annual waste growth recovering 100% of recyclable materials inresidual waste plus metals and plastic

Average

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 20

4.2 Recycling via a Material Recycling Facility (MRF) An alternative to continued efforts to source segregate the recyclable waste streams would be to establish a facility to extract the recyclable materials presented as co-mingled. As this facility would accept residual waste it would be classified as a “dirty MRF” with the capability to extract recyclate. This recyclate will be dirty and is likely to achieve a lower commercial value. It is also less likely to be able to extract the maximum amount of recyclables from the residual waste. The materials are generally cross contaminated and with the maturity of markets for recyclable materials, lower grade materials are seen as less desirable and could realistically have no buyer at all. 4.2.1 Future Waste Predictions for Recycling via a MRF To facilitate the understanding of the potential growth in waste volumes to be treated by TMC a model was constructed to highlight the strands of data which could affect the estimated volume of residual waste. The following tables are constructed to build a picture of the arisings both through to the target date for compliance in 2025 and a longer-term prediction through to 2045 Within the strategy section of this report it is discussed the methods to achieve further recovery from the residual waste of the materials highlighted in the residual waste analysis section of this report where potentially two thirds of the residual waste could be presented for recycling and material recovery. An alternative solution where all residual waste is presented to a TMC facility, or contractor designated by TMC, is discussed here to understand the size of facility to receive waste and the ultimate expected tonnage of residual waste for treatment after the extraction of recyclable materials WRAP reports that ongoing population growth and associated waste generation in households across the UK will potentially increase by 2% year-on-year. However for the utilising data specific to the area we can consider three growth scenarios

1. Using the historic growth of waste data this demonstrates a 4% growth over the previous 16 years and a linear extrapolation of this data is presented at 0.25% per year.

2. Using the Moray Demographics Factsheet published in 2014 using 2012 data this predicts an increase in population in the area of 0.40% per year. This is presented as a linear extrapolation over the period.

3. Using the Moray Demographics Factsheet published in 2014 using 2012 data this predicts an increase in dwellings in the area of 0.60% per year. This is presented as a linear extrapolation over the period.

It should be noted that these factsheets predict population through to 2035 and the analysis below does not take into account the differing recycling behaviours observed by the population when stratified across different social criteria. The historic data supplied to particularise the waste tonnages generated since 2001 show two distinct patterns where from the period 2006 -2012 a total tonnage of the combined recycled and residual waste is noticeably higher than the figures for the following years. To aid understanding of each of the scenarios detailed below two base tonnage levels have been used. Firstly the annualised waste production data for the year 2013/14 (top line of data in each section) and secondly a mean average for the period 2006/12.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 21

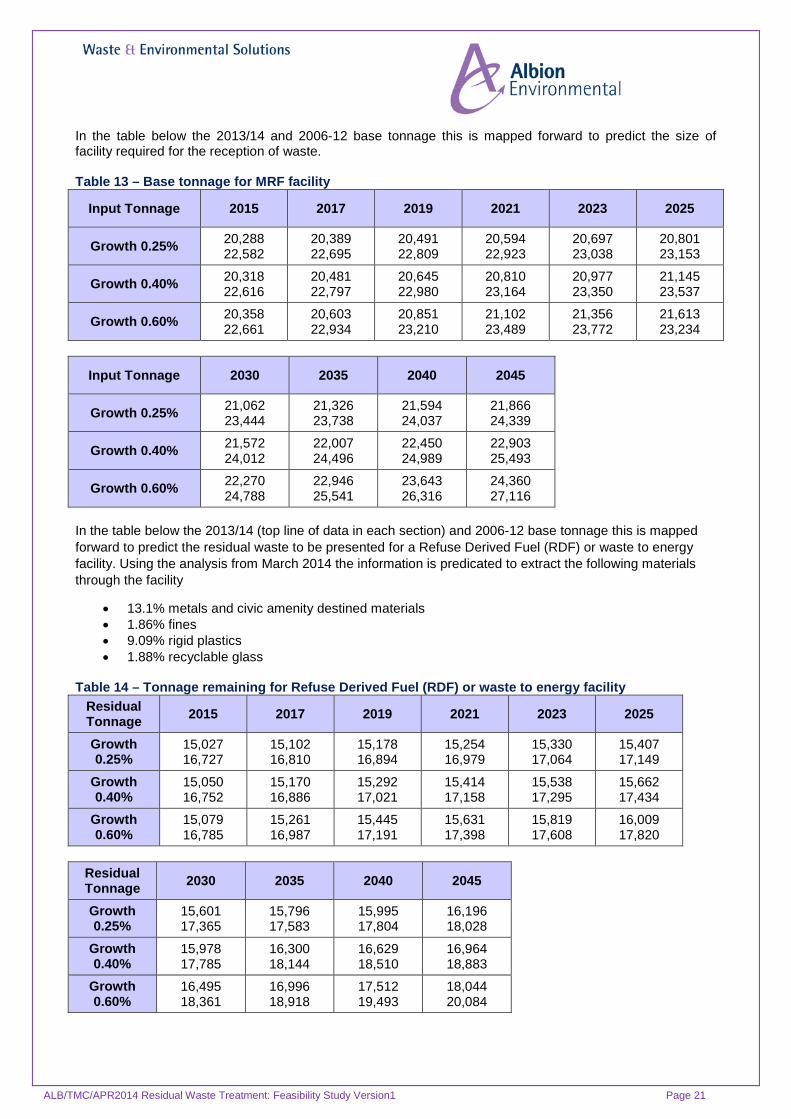

In the table below the 2013/14 and 2006-12 base tonnage this is mapped forward to predict the size of facility required for the reception of waste. Table 13 – Base tonnage for MRF facility

Input Tonnage 2015 2017 2019 2021 2023 2025

Growth 0.25% 20,288 22,582

20,389 22,695

20,491 22,809

20,594 22,923

20,697 23,038

20,801 23,153

Growth 0.40% 20,318 22,616

20,481 22,797

20,645 22,980

20,810 23,164

20,977 23,350

21,145 23,537

Growth 0.60% 20,358 22,661

20,603 22,934

20,851 23,210

21,102 23,489

21,356 23,772

21,613 23,234

Input Tonnage 2030 2035 2040 2045

Growth 0.25% 21,062 23,444

21,326 23,738

21,594 24,037

21,866 24,339

Growth 0.40% 21,572 24,012

22,007 24,496

22,450 24,989

22,903 25,493

Growth 0.60% 22,270 24,788

22,946 25,541

23,643 26,316

24,360 27,116

In the table below the 2013/14 (top line of data in each section) and 2006-12 base tonnage this is mapped forward to predict the residual waste to be presented for a Refuse Derived Fuel (RDF) or waste to energy facility. Using the analysis from March 2014 the information is predicated to extract the following materials through the facility

• 13.1% metals and civic amenity destined materials • 1.86% fines • 9.09% rigid plastics • 1.88% recyclable glass

Table 14 – Tonnage remaining for Refuse Derived Fuel (RDF) or waste to energy facility

Residual Tonnage 2015 2017 2019 2021 2023 2025

Growth 0.25%

15,027 16,727

15,102 16,810

15,178 16,894

15,254 16,979

15,330 17,064

15,407 17,149

Growth 0.40%

15,050 16,752

15,170 16,886

15,292 17,021

15,414 17,158

15,538 17,295

15,662 17,434

Growth 0.60%

15,079 16,785

15,261 16,987

15,445 17,191

15,631 17,398

15,819 17,608

16,009 17,820

Residual Tonnage 2030 2035 2040 2045

Growth 0.25%

15,601 17,365

15,796 17,583

15,995 17,804

16,196 18,028

Growth 0.40%

15,978 17,785

16,300 18,144

16,629 18,510

16,964 18,883

Growth 0.60%

16,495 18,361

16,996 18,918

17,512 19,493

18,044 20,084

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 22

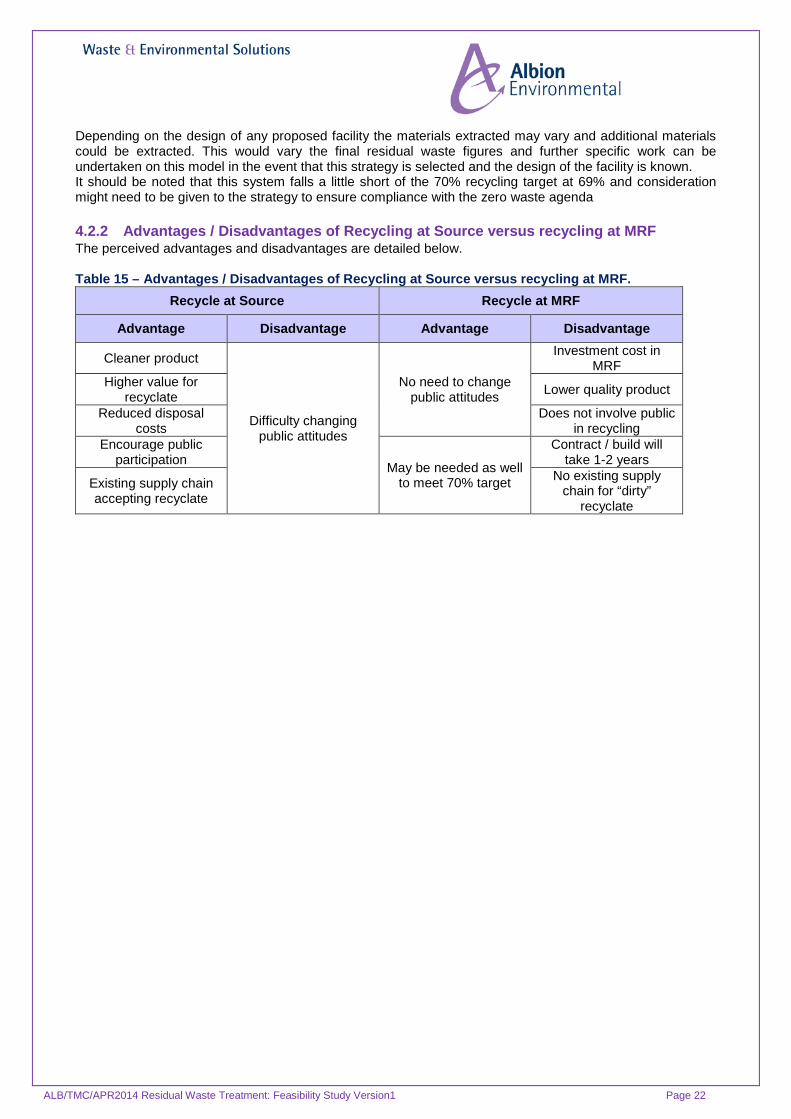

Depending on the design of any proposed facility the materials extracted may vary and additional materials could be extracted. This would vary the final residual waste figures and further specific work can be undertaken on this model in the event that this strategy is selected and the design of the facility is known. It should be noted that this system falls a little short of the 70% recycling target at 69% and consideration might need to be given to the strategy to ensure compliance with the zero waste agenda 4.2.2 Advantages / Disadvantages of Recycling at Source versus recycling at MRF The perceived advantages and disadvantages are detailed below. Table 15 – Advantages / Disadvantages of Recycling at Source versus recycling at MRF.

Recycle at Source Recycle at MRF

Advantage Disadvantage Advantage Disadvantage

Cleaner product

Difficulty changing public attitudes

No need to change public attitudes

Investment cost in MRF

Higher value for recyclate Lower quality product

Reduced disposal costs

Does not involve public in recycling

Encourage public participation May be needed as well

to meet 70% target

Contract / build will take 1-2 years

Existing supply chain accepting recyclate

No existing supply chain for “dirty”

recyclate

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 23

4.3 Commercial Waste The waste data and understanding of the demographics and geography of the location of TMC shows historic evidence that a high proportion of local commercial business currently direct residual waste to the council owned landfill facility. Businesses in Scotland have the same obligations, responsibilities and targets from the zero waste agenda and as such could support an alternative solution for the residual waste when targets for diversion of material from landfill hit threshold dates. Whilst these obligations exist and the geography of TMC indicate that any residual waste treatment strategy may be supported by the residual waste tonnage from commercial businesses in the area this should not be relied upon. The quantity of commercial waste accepted by TMC has varied considerably in the last 10 years from a low of 5,246 tonnes (2007/08) to a high of 8,482 tonnes (2004/05). The overall commercial recycling rate has also varied considerably from a high of 56.71% (2007/08) to a recent low of 24.69% (2012/13). However, approximately 2,000 tonnes is attributable to arising’s from the Council’s street sweeping activities which is difficult to recycle. The Waste (Scotland) Regulations 2012 place a requirement on businesses to

• Present metal, plastic, glass, paper and card separately for collection from 1st January 2014. • If they run a food business which produces over 50kg of food waste per week, they must present it

for separate collection from 1st January 2014. • The requirement to present food waste for separate collection will extend to all food businesses

which produces over 5kg of food waste per week 1st January 2016. This is likely to have a significant reduction in the quantity of residual waste which is available for any waste treatment facility. Businesses are only obligated to reach the targets and no responsibility to direct their residual waste to a council sponsored facility. The data supplied does not support a reliable planning tool and as such it is recommended that commercial waste volumes and commitments should either be

• Not considered in any decision to determine the feasibility of solutions for household residual waste. • Further work should be carried out on the raw data to establish trends and possible commercial

waste quantities. In summary taking into account the lack of facilities in the area there is likely to be some commercial residual waste available for any proposed facility however further work is required to determine quantities in future years. 4.4 Level of confidence in residual waste tonnage One of the outcomes of this report is to provide a statement on the level of confidence that can be given to annual residual waste tonnage and composition, forecasting over the short to medium term (5 years) and the lifetime. The following statements can be provided.

4.4.1 Residual Waste Tonnage Analysis of the tonnage data suggests that a residual waste solution should be designed with a tolerance between 9,500 tonnes per annum and 18,000 tonnes per annum with an anticipated arising of circa 14,000 tonnes per annum. Confidence in this range will be wholly dependent on the effort which is applied by TMC to increase use of the recycling service. The more successful TMC are the lower the overall tonnage which will be available for a treatment facility. Due to the varying tonnage of commercial residual waste and the varying recycling level being achieved it is not possible to determine with any accuracy the commercial residual waste tonnage which may be available for a new facility. As the Waste (Scotland) Regulations 2012 take effect and businesses put in place separate collection systems it would be reasonable to expect the commercial residual waste quantities to decline. It may be possible to determine the expected quantity of commercial residual waste by a very detailed analysis of the raw weighbridge data. However even if historical trends can be established there will be little data to determine the impact of the Waste (Scotland) Regulations 2012 on commercial residual waste tonnages, apart from the fact they are liable to decline.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 24

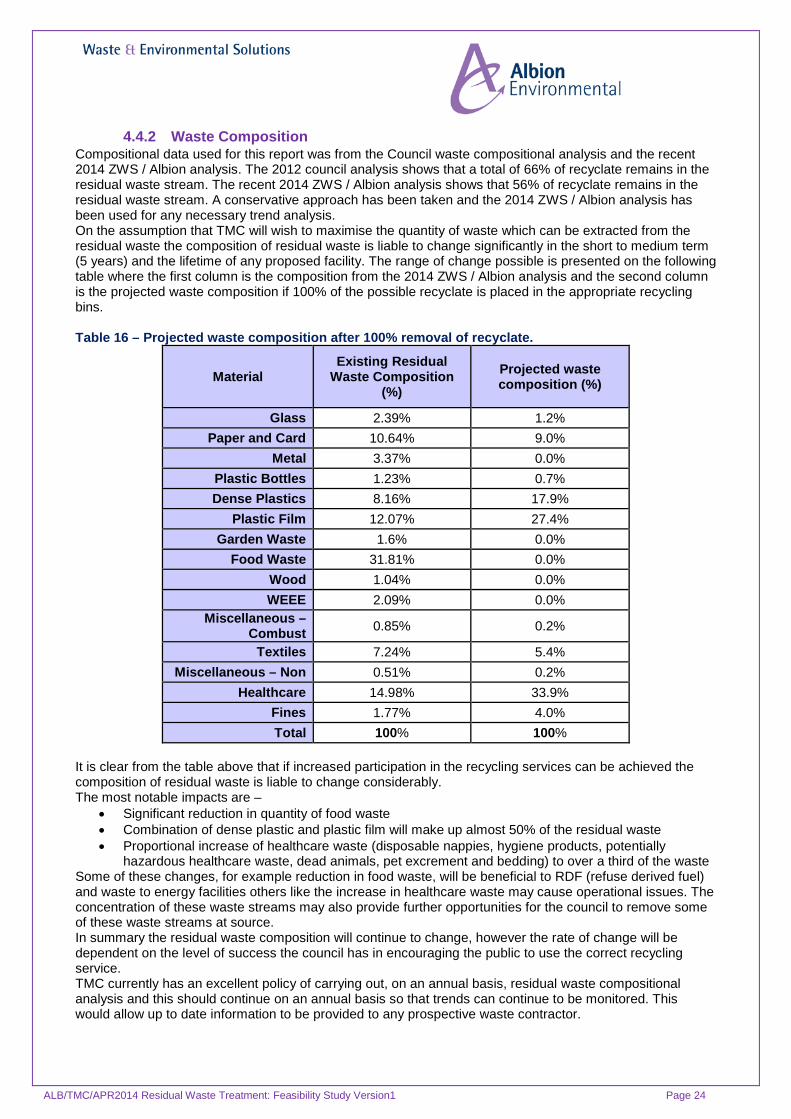

4.4.2 Waste Composition Compositional data used for this report was from the Council waste compositional analysis and the recent 2014 ZWS / Albion analysis. The 2012 council analysis shows that a total of 66% of recyclate remains in the residual waste stream. The recent 2014 ZWS / Albion analysis shows that 56% of recyclate remains in the residual waste stream. A conservative approach has been taken and the 2014 ZWS / Albion analysis has been used for any necessary trend analysis. On the assumption that TMC will wish to maximise the quantity of waste which can be extracted from the residual waste the composition of residual waste is liable to change significantly in the short to medium term (5 years) and the lifetime of any proposed facility. The range of change possible is presented on the following table where the first column is the composition from the 2014 ZWS / Albion analysis and the second column is the projected waste composition if 100% of the possible recyclate is placed in the appropriate recycling bins. Table 16 – Projected waste composition after 100% removal of recyclate.

Material Existing Residual

Waste Composition (%)

Projected waste composition (%)

Glass 2.39% 1.2% Paper and Card 10.64% 9.0%

Metal 3.37% 0.0% Plastic Bottles 1.23% 0.7% Dense Plastics 8.16% 17.9%

Plastic Film 12.07% 27.4% Garden Waste 1.6% 0.0%

Food Waste 31.81% 0.0% Wood 1.04% 0.0% WEEE 2.09% 0.0%

Miscellaneous – Combust 0.85% 0.2%

Textiles 7.24% 5.4% Miscellaneous – Non 0.51% 0.2%

Healthcare 14.98% 33.9% Fines 1.77% 4.0% Total 100% 100%

It is clear from the table above that if increased participation in the recycling services can be achieved the composition of residual waste is liable to change considerably. The most notable impacts are –

• Significant reduction in quantity of food waste • Combination of dense plastic and plastic film will make up almost 50% of the residual waste • Proportional increase of healthcare waste (disposable nappies, hygiene products, potentially

hazardous healthcare waste, dead animals, pet excrement and bedding) to over a third of the waste Some of these changes, for example reduction in food waste, will be beneficial to RDF (refuse derived fuel) and waste to energy facilities others like the increase in healthcare waste may cause operational issues. The concentration of these waste streams may also provide further opportunities for the council to remove some of these waste streams at source. In summary the residual waste composition will continue to change, however the rate of change will be dependent on the level of success the council has in encouraging the public to use the correct recycling service. TMC currently has an excellent policy of carrying out, on an annual basis, residual waste compositional analysis and this should continue on an annual basis so that trends can continue to be monitored. This would allow up to date information to be provided to any prospective waste contractor.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 25

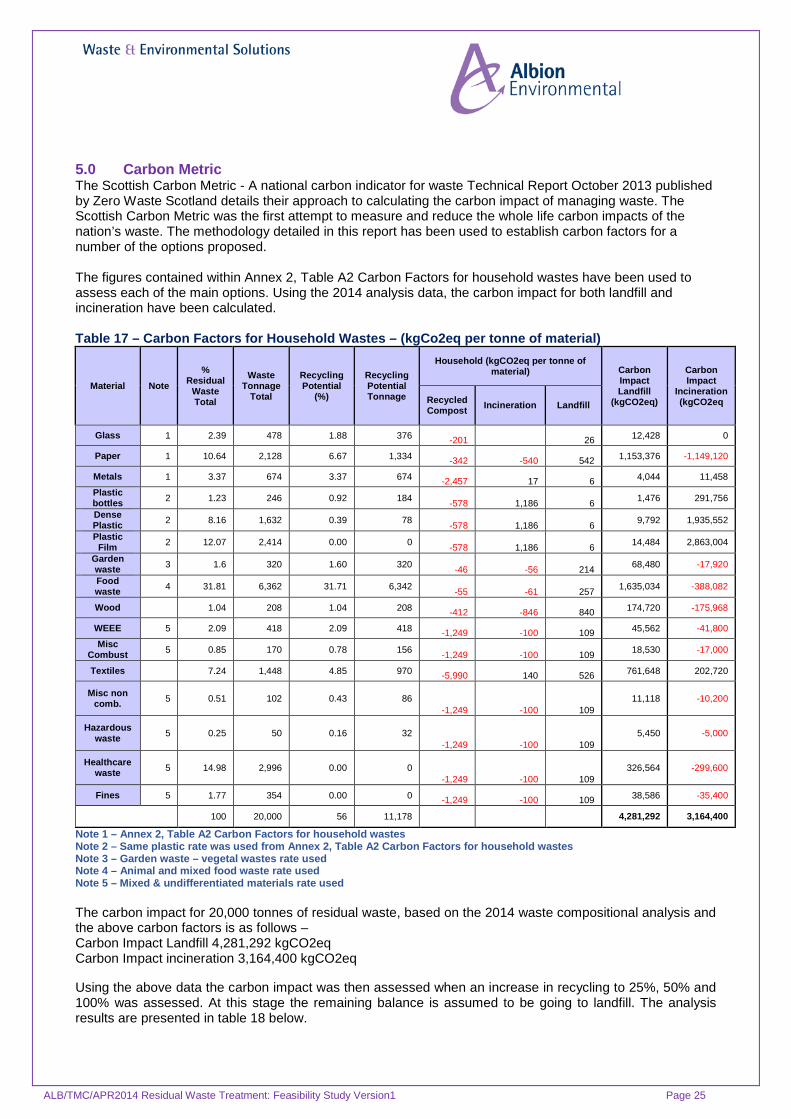

5.0 Carbon Metric The Scottish Carbon Metric - A national carbon indicator for waste Technical Report October 2013 published by Zero Waste Scotland details their approach to calculating the carbon impact of managing waste. The Scottish Carbon Metric was the first attempt to measure and reduce the whole life carbon impacts of the nation’s waste. The methodology detailed in this report has been used to establish carbon factors for a number of the options proposed. The figures contained within Annex 2, Table A2 Carbon Factors for household wastes have been used to assess each of the main options. Using the 2014 analysis data, the carbon impact for both landfill and incineration have been calculated. Table 17 – Carbon Factors for Household Wastes – (kgCo2eq per tonne of material)

Material Note %

Residual Waste Total

Waste Tonnage

Total

Recycling Potential

(%)

Recycling Potential Tonnage

Household (kgCO2eq per tonne of material) Carbon

Impact Landfill

(kgCO2eq)

Carbon Impact

Incineration (kgCO2eq Recycled

Compost Incineration Landfill

Glass 1 2.39 478 1.88 376 -201 26 12,428 0

Paper 1 10.64 2,128 6.67 1,334 -342 -540 542 1,153,376 -1,149,120

Metals 1 3.37 674 3.37 674 -2,457 17 6 4,044 11,458

Plastic bottles 2 1.23 246 0.92 184 -578 1,186 6 1,476 291,756

Dense Plastic 2 8.16 1,632 0.39 78 -578 1,186 6 9,792 1,935,552

Plastic Film 2 12.07 2,414 0.00 0 -578 1,186 6 14,484 2,863,004

Garden waste 3 1.6 320 1.60 320 -46 -56 214 68,480 -17,920

Food waste 4 31.81 6,362 31.71 6,342 -55 -61 257 1,635,034 -388,082

Wood 1.04 208 1.04 208 -412 -846 840 174,720 -175,968

WEEE 5 2.09 418 2.09 418 -1,249 -100 109 45,562 -41,800

Misc Combust 5 0.85 170 0.78 156 -1,249 -100 109 18,530 -17,000

Textiles 7.24 1,448 4.85 970 -5,990 140 526 761,648 202,720

Misc non comb. 5 0.51 102 0.43 86

-1,249 -100 109 11,118 -10,200

Hazardous waste 5 0.25 50 0.16 32

-1,249 -100 109 5,450 -5,000

Healthcare waste 5 14.98 2,996 0.00 0

-1,249 -100 109 326,564 -299,600

Fines 5 1.77 354 0.00 0 -1,249 -100 109 38,586 -35,400

100 20,000 56 11,178 4,281,292 3,164,400

Note 1 – Annex 2, Table A2 Carbon Factors for household wastes Note 2 – Same plastic rate was used from Annex 2, Table A2 Carbon Factors for household wastes Note 3 – Garden waste – vegetal wastes rate used Note 4 – Animal and mixed food waste rate used Note 5 – Mixed & undifferentiated materials rate used The carbon impact for 20,000 tonnes of residual waste, based on the 2014 waste compositional analysis and the above carbon factors is as follows – Carbon Impact Landfill 4,281,292 kgCO2eq Carbon Impact incineration 3,164,400 kgCO2eq Using the above data the carbon impact was then assessed when an increase in recycling to 25%, 50% and 100% was assessed. At this stage the remaining balance is assumed to be going to landfill. The analysis results are presented in table 18 below.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 26

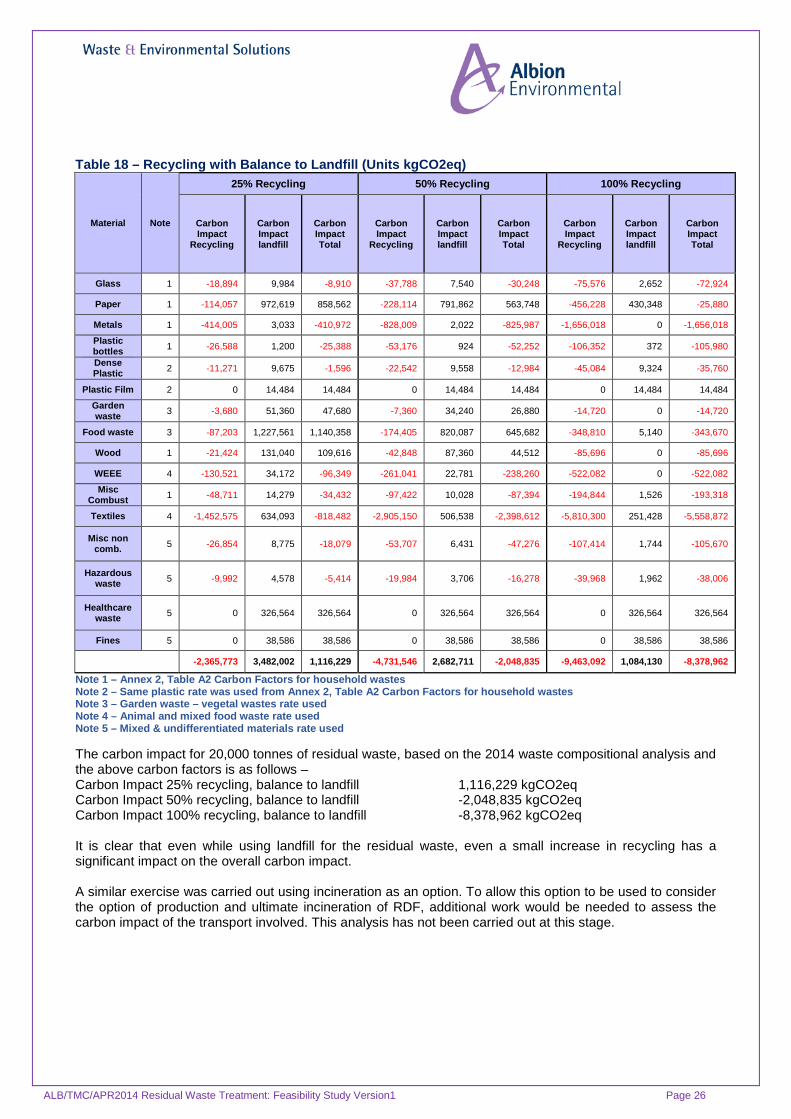

Table 18 – Recycling with Balance to Landfill (Units kgCO2eq)

Material Note

25% Recycling 50% Recycling 100% Recycling

Carbon Impact

Recycling

Carbon Impact landfill

Carbon Impact Total

Carbon Impact

Recycling

Carbon Impact landfill

Carbon Impact Total

Carbon Impact

Recycling

Carbon Impact landfill

Carbon Impact Total

Glass 1 -18,894 9,984 -8,910 -37,788 7,540 -30,248 -75,576 2,652 -72,924

Paper 1 -114,057 972,619 858,562 -228,114 791,862 563,748 -456,228 430,348 -25,880

Metals 1 -414,005 3,033 -410,972 -828,009 2,022 -825,987 -1,656,018 0 -1,656,018

Plastic bottles 1 -26,588 1,200 -25,388 -53,176 924 -52,252 -106,352 372 -105,980

Dense Plastic 2 -11,271 9,675 -1,596 -22,542 9,558 -12,984 -45,084 9,324 -35,760

Plastic Film 2 0 14,484 14,484 0 14,484 14,484 0 14,484 14,484

Garden waste 3 -3,680 51,360 47,680 -7,360 34,240 26,880 -14,720 0 -14,720

Food waste 3 -87,203 1,227,561 1,140,358 -174,405 820,087 645,682 -348,810 5,140 -343,670

Wood 1 -21,424 131,040 109,616 -42,848 87,360 44,512 -85,696 0 -85,696

WEEE 4 -130,521 34,172 -96,349 -261,041 22,781 -238,260 -522,082 0 -522,082

Misc Combust 1 -48,711 14,279 -34,432 -97,422 10,028 -87,394 -194,844 1,526 -193,318

Textiles 4 -1,452,575 634,093 -818,482 -2,905,150 506,538 -2,398,612 -5,810,300 251,428 -5,558,872

Misc non comb. 5 -26,854 8,775 -18,079 -53,707 6,431 -47,276 -107,414 1,744 -105,670

Hazardous waste 5 -9,992 4,578 -5,414 -19,984 3,706 -16,278 -39,968 1,962 -38,006

Healthcare waste 5 0 326,564 326,564 0 326,564 326,564 0 326,564 326,564

Fines 5 0 38,586 38,586 0 38,586 38,586 0 38,586 38,586

-2,365,773 3,482,002 1,116,229 -4,731,546 2,682,711 -2,048,835 -9,463,092 1,084,130 -8,378,962

Note 1 – Annex 2, Table A2 Carbon Factors for household wastes Note 2 – Same plastic rate was used from Annex 2, Table A2 Carbon Factors for household wastes Note 3 – Garden waste – vegetal wastes rate used Note 4 – Animal and mixed food waste rate used Note 5 – Mixed & undifferentiated materials rate used

The carbon impact for 20,000 tonnes of residual waste, based on the 2014 waste compositional analysis and the above carbon factors is as follows – Carbon Impact 25% recycling, balance to landfill 1,116,229 kgCO2eq Carbon Impact 50% recycling, balance to landfill -2,048,835 kgCO2eq Carbon Impact 100% recycling, balance to landfill -8,378,962 kgCO2eq It is clear that even while using landfill for the residual waste, even a small increase in recycling has a significant impact on the overall carbon impact. A similar exercise was carried out using incineration as an option. To allow this option to be used to consider the option of production and ultimate incineration of RDF, additional work would be needed to assess the carbon impact of the transport involved. This analysis has not been carried out at this stage.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 27

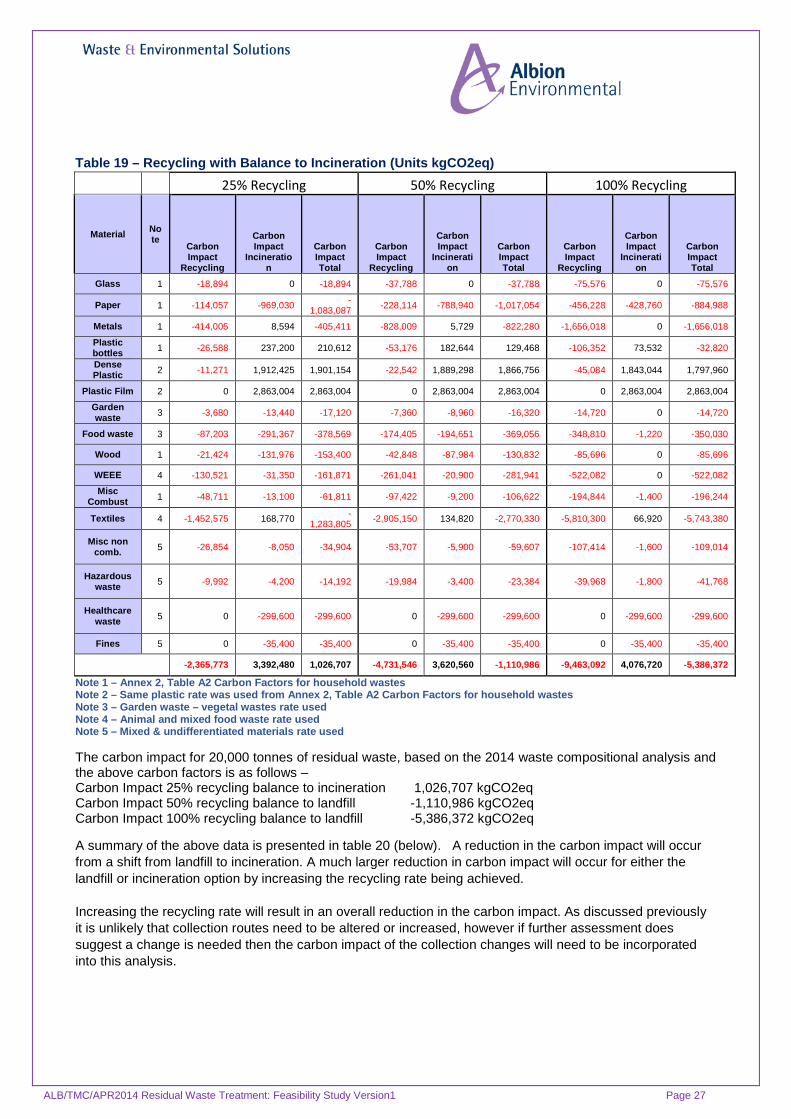

Table 19 – Recycling with Balance to Incineration (Units kgCO2eq)

25% Recycling 50% Recycling 100% Recycling

Material Note

Carbon Impact

Recycling

Carbon Impact

Incineration

Carbon Impact Total

Carbon Impact

Recycling

Carbon Impact

Incineration

Carbon Impact Total

Carbon Impact

Recycling

Carbon Impact

Incineration

Carbon Impact Total

Glass 1 -18,894 0 -18,894 -37,788 0 -37,788 -75,576 0 -75,576

Paper 1 -114,057 -969,030 -1,083,087 -228,114 -788,940 -1,017,054 -456,228 -428,760 -884,988

Metals 1 -414,005 8,594 -405,411 -828,009 5,729 -822,280 -1,656,018 0 -1,656,018

Plastic bottles 1 -26,588 237,200 210,612 -53,176 182,644 129,468 -106,352 73,532 -32,820

Dense Plastic 2 -11,271 1,912,425 1,901,154 -22,542 1,889,298 1,866,756 -45,084 1,843,044 1,797,960

Plastic Film 2 0 2,863,004 2,863,004 0 2,863,004 2,863,004 0 2,863,004 2,863,004

Garden waste 3 -3,680 -13,440 -17,120 -7,360 -8,960 -16,320 -14,720 0 -14,720

Food waste 3 -87,203 -291,367 -378,569 -174,405 -194,651 -369,056 -348,810 -1,220 -350,030

Wood 1 -21,424 -131,976 -153,400 -42,848 -87,984 -130,832 -85,696 0 -85,696

WEEE 4 -130,521 -31,350 -161,871 -261,041 -20,900 -281,941 -522,082 0 -522,082

Misc Combust 1 -48,711 -13,100 -61,811 -97,422 -9,200 -106,622 -194,844 -1,400 -196,244

Textiles 4 -1,452,575 168,770 -1,283,805 -2,905,150 134,820 -2,770,330 -5,810,300 66,920 -5,743,380

Misc non comb. 5 -26,854 -8,050 -34,904 -53,707 -5,900 -59,607 -107,414 -1,600 -109,014

Hazardous waste 5 -9,992 -4,200 -14,192 -19,984 -3,400 -23,384 -39,968 -1,800 -41,768

Healthcare waste 5 0 -299,600 -299,600 0 -299,600 -299,600 0 -299,600 -299,600

Fines 5 0 -35,400 -35,400 0 -35,400 -35,400 0 -35,400 -35,400

-2,365,773 3,392,480 1,026,707 -4,731,546 3,620,560 -1,110,986 -9,463,092 4,076,720 -5,386,372

Note 1 – Annex 2, Table A2 Carbon Factors for household wastes Note 2 – Same plastic rate was used from Annex 2, Table A2 Carbon Factors for household wastes Note 3 – Garden waste – vegetal wastes rate used Note 4 – Animal and mixed food waste rate used Note 5 – Mixed & undifferentiated materials rate used

The carbon impact for 20,000 tonnes of residual waste, based on the 2014 waste compositional analysis and the above carbon factors is as follows – Carbon Impact 25% recycling balance to incineration 1,026,707 kgCO2eq Carbon Impact 50% recycling balance to landfill -1,110,986 kgCO2eq Carbon Impact 100% recycling balance to landfill -5,386,372 kgCO2eq

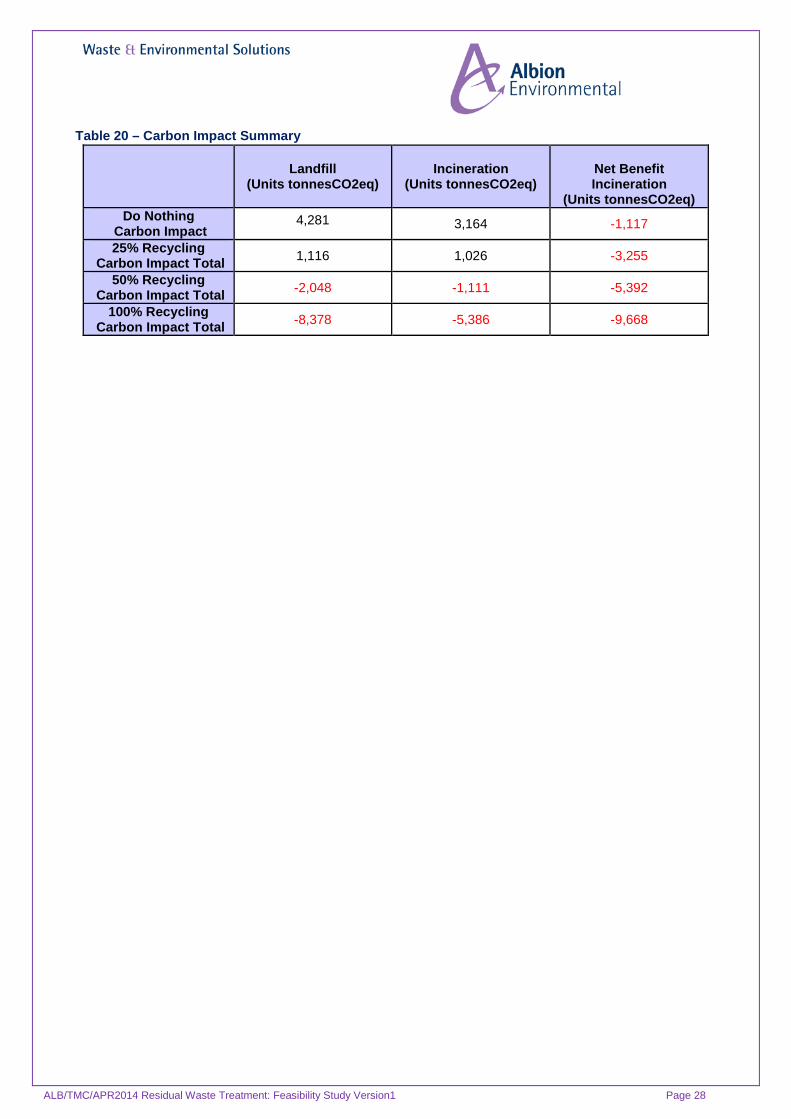

A summary of the above data is presented in table 20 (below). A reduction in the carbon impact will occur from a shift from landfill to incineration. A much larger reduction in carbon impact will occur for either the landfill or incineration option by increasing the recycling rate being achieved. Increasing the recycling rate will result in an overall reduction in the carbon impact. As discussed previously it is unlikely that collection routes need to be altered or increased, however if further assessment does suggest a change is needed then the carbon impact of the collection changes will need to be incorporated into this analysis.

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 28

Table 20 – Carbon Impact Summary

Landfill (Units tonnesCO2eq)

Incineration (Units tonnesCO2eq)

Net Benefit Incineration

(Units tonnesCO2eq) Do Nothing

Carbon Impact 4,281 3,164 -1,117

25% Recycling Carbon Impact Total 1,116 1,026 -3,255

50% Recycling Carbon Impact Total -2,048 -1,111 -5,392

100% Recycling Carbon Impact Total -8,378 -5,386 -9,668

ALB/TMC/APR2014 Residual Waste Treatment: Feasibility Study Version1 Page 29

6.0 Residual Waste Treatment Technology As landfill costs continue to increase the number of residual waste treatment technologies continues to evolve and change. Many of these technologies are not particularly new but are simply a linking together of a number of technologies or processes. The following technologies will be considered in this section.

• Low risk technologies that recover and process residual waste in a form optimised for further treatment (e.g. solid recovered fuel)

• Conventional and advanced thermal treatment technologies • Opportunities to recover energy