Embed Size (px)

Citation preview

Mary-Jo LaHood, CAMS-Audit

THE MONEY SERVICE BUSINESS IN THE USA: HOW TO COMPLY WITH FEDERAL AND

STATE LAWS & REGULATIONS AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

1

Contents

Definition of Money Service Business (MSB) | MSBs in the 21st century ..………………….…………. 2

MSBs in the 21st Century ………….……………..…………….……………………………………………………….……. 3

MSBs Duty to Comply at Federal and State Levels……………………………………………………..………….. 4

Federal Rules and Regulations……………………………………………………………………………………………….. 5

AML Compliance Program | OFAC ………....…………………………………………………………..…………………. 6

Dodd Frank Protections …………………………………………………………………………………….…………………… 7

State Banking Departments …………………………….………………………………………………………..………….. 8

Risk Assessment ....…………………………………………………………………………………………..…….….……….…. 9

Risk Based Approach ………………………………………………………………………………………….…………….….. 10

MSBs’ Best Practices to Satisfy Federal & State Regulations ……………………………….………………… 11

KYC Know Your Customer | Review Observations ..………………………………………………………………. 12

Review Observations ……………….…………………………………………………………………………………….…….. 13

Additional Practices for Consideration …………………………………………………………….…………………... 15

Conclusion ………………………………………………….……………………………………………………………………….. 16

References …………………………………………………………………………………………………………………………... 18

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

2

Definition of Money Services Business (MSB)

Money services Businesses (MSBs), as by the Financial Crimes Enforcement Network’s (FinCENs) last definition released on November 13, 2013, are types of financial institutions that involve one or more of the following entities:

Money transmitter

Dealer in foreign exchange

Issuer, seller or redeemer of travelers checks and money order

Check casher

Provider and seller of prepaid card

Agent

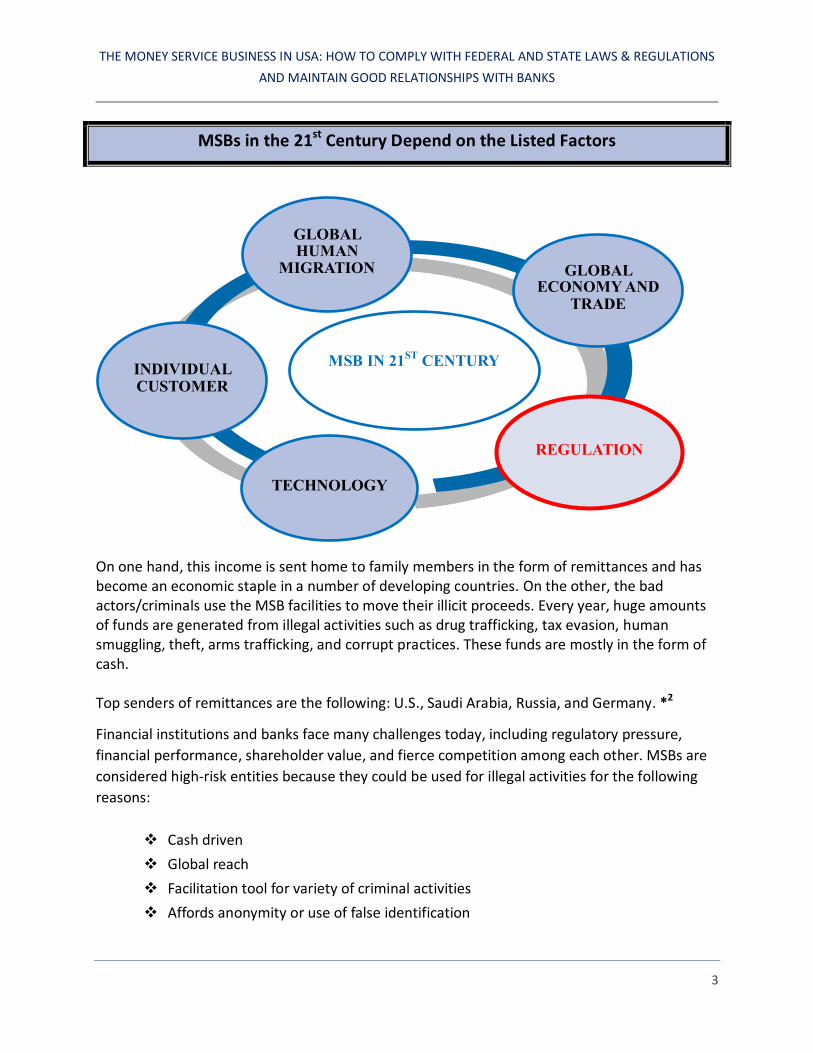

MSBs in the 21st Century

Money transmission businesses are taking the next step into the 21st century with more advanced technology. The remittance is navigating from the traditional way of transferring money at the agent's physical locations to cyber channels. Migration for work in the 21st century has become a popular way for individuals in developing countries to obtain sufficient income for survival. The service is largely dependent on the following factors:

Global human migration

Global economy and trade

Technology

Individual customer

Regulation

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

3

MSBs in the 21st Century Depend on the Listed Factors

On one hand, this income is sent home to family members in the form of remittances and has become an economic staple in a number of developing countries. On the other, the bad actors/criminals use the MSB facilities to move their illicit proceeds. Every year, huge amounts of funds are generated from illegal activities such as drug trafficking, tax evasion, human smuggling, theft, arms trafficking, and corrupt practices. These funds are mostly in the form of cash. Top senders of remittances are the following: U.S., Saudi Arabia, Russia, and Germany. *2

Financial institutions and banks face many challenges today, including regulatory pressure,

financial performance, shareholder value, and fierce competition among each other. MSBs are

considered high-risk entities because they could be used for illegal activities for the following

reasons:

Cash driven

Global reach

Facilitation tool for variety of criminal activities

Affords anonymity or use of false identification

MSB IN 21ST

CENTURY

GLOBAL HUMAN

MIGRATION GLOBAL ECONOMY AND

TRADE

TECHNOLOGY

INDIVIDUAL CUSTOMER

REGULATION

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

4

Located in corridors of operation

Seasonal/regional factors

Ease of agent exploitation

MSBs as financial institutions are under the scrutiny of many regulatory bodies.

MSBs have a Responsibility to Comply with Obligatory Laws and Regulations

at the Federal and State Level

The MSBs are regulated by:

The Financial Crimes Enforcement Network (FinCEN)

The Internal Revenue Services (IRS)

The States Banking Departments and Regulators *3

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

5

Federal Rules and Regulations | FinCEN

FinCEN, a bureau of the U.S. Department of the Treasury, administers and issues regulations

pursuant to the Bank Secrecy Act (BSA). Through certain BSA reporting and recordkeeping

requirements, paper trails of transactions are created, which law enforcement and others can

use in criminal, tax and regulatory investigations.

BSA Regulations

BSA regulations require certain MSBs to be registered with FinCEN, and to prepare and

maintain a list of agents, if any. In addition, BSA regulations require certain MSBs to

report suspicious activity and currency transactions to FinCEN (See 31 CFR103.20).

THE BSA REQUIREMENTS

• Registration with FinCEN

• Agent list (updated in January each year)

• Suspicious activity report (SAR)

• Currency transaction report (CTR)

• Anti-money laundering (AML) compliance program

• Monetary instrument log

• Record retention (five years): Receipts, handbooks, training material, etc.

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

6

How can MSBs help to prevent money laundering and terrorist financing AML/CTF?

By implementing the four pillars of the AML compliance programs:

OFAC

The Office of Foreign Assets Control (OFAC) of the U.S. Department of the Treasury administers and enforces economic and trade sanctions against targeted foreign countries, terrorism sponsoring organizations, and international narcotic traffickers based on U.S. foreign policy and national security goals. MSBs should establish and maintain an effective OFAC compliance program through:

Written policies and procedures for filtering transactions for possible OFAC

violations;

Designating an individual responsible for day-to-day compliance; and

Procedures for maintaining current lists of blocked countries, entities, and

individuals, and process for rejecting/blocking and reporting.

1) Written policies and procedures and system of internal controls

2) Designated compliance officer

3) Ongoing training

4) Independent review and test

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

7

Dodd Frank Regulations Provide New Customers Protection

Effective October 28, 2013

Dodd-Frank Act: Section 1073 2010; the Dodd-Frank Act expanded the scope of the Electronic Fund Transfer Act to impose requirements regarding certain international fund transfers. The Consumer Financial Protection Bureau (CFPB) was created in 2010 by the Dodd-Frank Wall Street Reform Act. It seeks to protect consumers' financial security by regulating credit, debit and prepaid cards, payday and consumer loans, as well as credit reporting, debt collection, and financial advisory services. The CFPB wrote user-safety rules for all consumer financial products. CFPB Remittance Rule: The CFPB amended Regulation E, which implements the Electronic Fund Transfer Act and the official interpretation to the regulation. The amendments are effective as of October 28, 2013, as subpart B of Regulation E. The amendments provide new protections, which includes the following requirements:*6

− Prepayment disclosures and receipts

− Error resolution (up to 180 days from the promised delivery date of the receipt)

− Cancellation right (oral or written request within 30 minutes of payment)

− Foreign language disclosure requirement (in English and the foreign language)

− Disclosure on foreign taxes and institution fees

− Disclosure on taxes in foreign country

− Errors from incorrect account information: the provider would be required to

attempt to recover the funds but would not bear the cost of the funds that cannot

be recovered

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

8

Review Observations

Receipts can simply be changed to comply with Dodd Frank rules by providing transparency to

the consumer, disclosing the detailed fees and adding the following Important Notice at the

bottom of the consumer’s receipt:

“You have the right to dispute errors in your transaction. You can request cancellation for a full refund

within thirty (30) minutes of payment if the money has not been paid out or deposited. If you think

there is an error, contact us within 180 days. For questions or complaints about (your Company name),

you may also contact:

- Appropriate State Department of Banking. Tel No, and Website (The State where the

transaction has been generated)

- Consumer Financial Protection Bureau, (855) 411-2372, (855) 729-2372 (TTY/TDD),

www.consumerfinance.gov

State Banking Departments and Regulations

Licenses and Reporting: MSBs are required to be licensed in the states where they

operate and have periodic reporting obligations to the states’ banking departments;

transactions volume, outstanding transactions, bonds verification certifications, entity

information and status update and others depending on the state.

Regulatory BSA compliance examinations

Can impose fines, penalties and issue consent orders

Risk Assessment

Although MSBs are not required by regulation to create a written risk assessment, management

is encouraged to document its risk assessment in writing in order to provide a clear basis for

MSB’s policies and procedures. According to the Bank Secrecy Act/Anti-Money Laundering

Examination Manual for Money Services Businesses *5

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

9

Risk Analysis and Mitigation

MSBs should conduct a risk analysis of various parameters such as geography, product, agent

and customer to identify and analyze the money laundering and terrorism funding risks.

Risk based on the following factors:

− Products and services

− Customers

− Agents

− Beneficiaries

− Paying Agents/correspondents

By adopting a risk-based approach, the MSBs will be able to identify the areas of higher risk.

Once the area of high risk is identified, then proper controls can be implemented to determine

the reliability and genuineness of the information obtained and to mitigate the risks.

Based on the analysis performed on the various parameters, a risk rating is assigned to each

factor depending on the residual risk obtained after the mitigation controls have been factored

in.

The risk-based approach is dependent on:

− Ability to quantify or score risk

− Risk triage process

− Risk monitoring capability

− Risk management policy

− Paying agents/correspondents

According to the Federal Financial Institutions Examination Council (FFIEC), BSA Exam Manual

Revision 2004; MSBs are included in the list of “high risk” clients for banks.

Bank examiners begin to question how banks oversee their MSB client’s AML compliance and

what they know about their client’s clients.

Banks, under the regulators and law enforcements pressure, respond by closing some existing

MSB accounts and refusing to accept new MSB customers.

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

10

MSBs must deal with an aggressive banking industry, driven by bank regulators, who oppose

banking MSBs.

Moreover, MSBs are facing the most significant challenge to open active bank accounts and

maintain good relationships with the banks.

Best Practices to Satisfy Federal and State Regulations and

Maintain Good Relationships with Banks

MSBs should have global security standards in place, undertake risk mitigation measures with

respect to their business, and conduct periodic internal and independent review of the BSA/

AML program. They also should satisfy the following requirements:

FinCEN registration

Compliance with BSA requirements

Implementation of an AML/CTF program as by the USA PATRIOT Act

States licensing and reporting

Risk assessment approach

Comprehensive onboarding process of agents and correspondents

Robust AML software implementation to ensure real time transaction monitoring, data

scanning and analysis, watch list screening and filtering

MSBs have to demonstrate to the banks that they have a comprehensive BSA/AML compliance

program as required by the USA PATRIOT Act and that they comply with the federal and states

laws and regulations.

In certain cases, the banks’ consultants are conducting both the review and testing to assess

the risks associated with the MSBs before entering in a business relationship with them.

MSBs have to establish a sound BSA program; the management has to understand the

seriousness of BSA and to be determined on satisfying all of its applicable requirements for

money service businesses. MSBs should maintain an automated BSA monitoring system, which

allows them to track and analyze customer activities. An aggressive CIP program that validates

both the legal standing of the corporate customer as well as the individual owner has to be

established. Also, a comprehensive OFAC system to be adopted that permits up-to-date checks

on all customers.

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

11

Know Your Customer

Laws and regulations are a crucial component to effective compliance with the government’s AML program. Preventing money laundering can only be accomplished if the MSB and its agents institute measures to “know” their customers. Although there is no official “know your customer” (KYC) statute or regulation, it is necessary for the MSB and its agents to take all reasonable steps to understand the facts and circumstances of each transaction relate to the particular customer executing the transaction. This is accomplished by:

Accurately identifying MSB’s customers through the effective gathering of information

Understanding the normal and expected transactions typically conducted by those customers

Consequently, identifying those transactions conducted by MSB’s customers that are suspicious in nature

Review Observations

Many MSBs have several mechanisms in place for developing a clear and concise understanding of their customers so that they may be able to detect suspicious and illicit activities, such as the identification requirements, as well as the record keeping requirements for funds transfers. To ensure that the KYC is well implemented for every transaction, regardless of the amount, requirements the sender to may include: Source of funds

Purpose of the transaction

Sender and receiver’s names, addresses and nationalities

At least one form of valid government issued ID and retain the ID number, ID

type, state and/or country of issuance and ID expiration date

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

12

The dollar thresholds of the BSA applicable for the MSB:

$1,000 currency exchange

$2,000 SAR threshold

$3,000 ID/ record keeping:

Name

Address

DOB (Date of Birth)

ID (Identification Document)

SSN (Social Security Number) / 2nd ID

Occupation

$10,000 Filing of CTR

In certain states, identification is required for transactions below than the BSA requirements. For example, in Oklahoma and Arizona, the ID is required for $1,000.

Review Observations

MSBs internal policies are implemented often to ascertain the identity for all transactions regardless the dollar amount of the transaction. Often, MSBs will require the SSN or second ID and occupation as requirements for transactions $2,500 and above. The most important aspect of the KYC policy is that the company and its agents are forbidden from acting as a mere conduit for the funds that they receive for transfer abroad. They are charged with the responsibility of being aware of both the nature of their customers, as well as the various types of transactions that their customers execute. By adhering to the KYC policy, they will greatly reduce their chances of being found responsible for violations of the laws and regulations governing money laundering. This practice will satisfy the bank’s requirements, provide the assurance that they know well their customers as well as all the transactions’ circumstances, and prove that their internal policies and procedures are substantially more demanding than the BSA regulatory requirements.

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

13

Review Observations

Independent reviews: MSBs are subject to multiple reviews during the operational year period:

The IRS, the states’ banking departments in the states where they operate, and the

indispensable independent review to fulfill the BSA requirements. Failure to do so may cost

thousands in fines and/or implementation of additional burdensome AML compliance

measures, not to mention possible reputational exposure.

Banks have concerns about regulatory scrutiny, the risks presented by MSB accounts, and the

costs and burdens associated with maintaining such accounts.

Banks inquire the independent review and testing reports as well as the regulators’

examination reports if any, from their MSB clients. Banks are looking at many factors in the

presented evaluations:

The auditors or the consulting firm conducting the independent audit & testing for

compliance

The independent testing for compliance must be conducted by a professional or

by a “qualified” outside party. MSBs must ensure that the AML independent

testing is truly independent, accurate, and thorough.

Findings and recommendations

The reviewers could also provide process improvement recommendations,

compliance advice, feedback based on interviews with personnel, and a hands-

on review of the risk and AML compliance practices. Also, they can assist the

MSBs in managing their reputational risk and regulatory standing.

MSBs will improve their practices accordingly to promote the development and implementation

of sound anti-money laundering policies.

MSBs should be transparent with their banks, be assertive that they have carried out

successfully multiple audit reviews conducted by the auditors and the regulators. The reports

should show that they are abiding by the federal and state laws and regulations. MSBs could

also provide remedy action plans towards the findings. Moreover, they can make available

subsequent examination reports showing the remedy actions and the proper testing of the

correction of the discrepancies, if any.

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

14

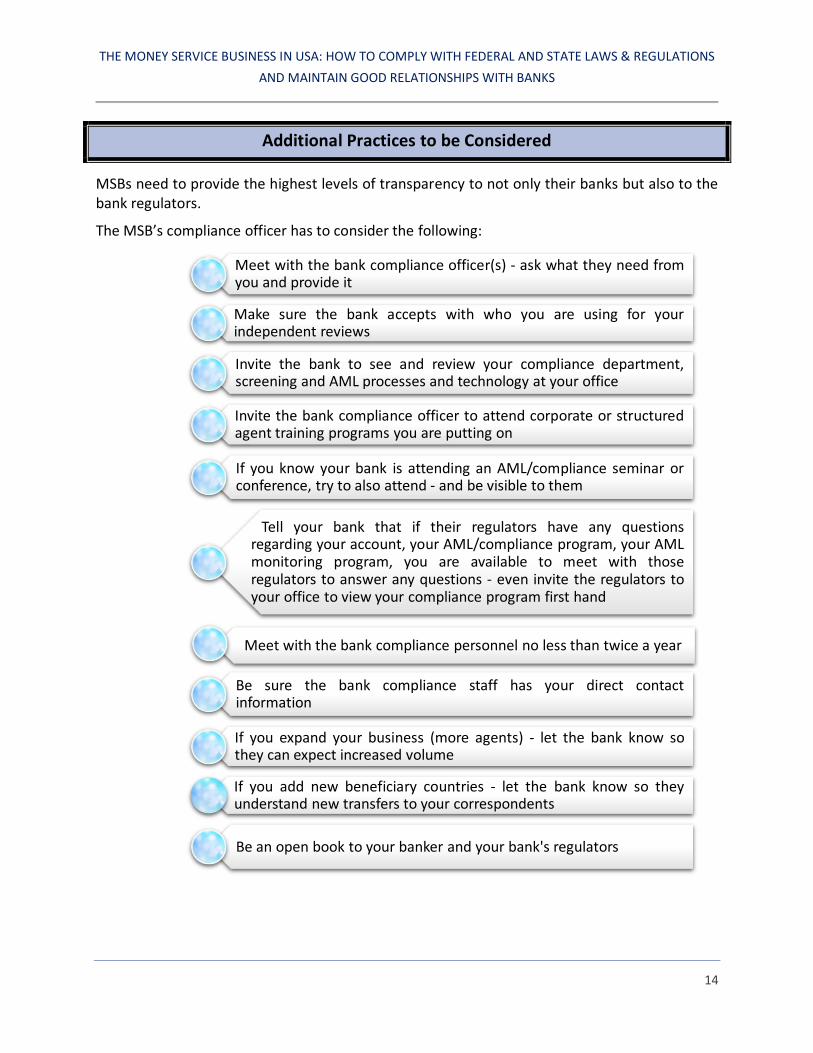

Additional Practices to be Considered

MSBs need to provide the highest levels of transparency to not only their banks but also to the bank regulators.

The MSB’s compliance officer has to consider the following:

Meet with the bank compliance officer(s) - ask what they need from you and provide it

Make sure the bank accepts with who you are using for your independent reviews

Invite the bank to see and review your compliance department, screening and AML processes and technology at your office

Invite the bank compliance officer to attend corporate or structured agent training programs you are putting on

If you know your bank is attending an AML/compliance seminar or conference, try to also attend - and be visible to them

Tell your bank that if their regulators have any questions regarding your account, your AML/compliance program, your AML monitoring program, you are available to meet with those regulators to answer any questions - even invite the regulators to your office to view your compliance program first hand

Meet with the bank compliance personnel no less than twice a year

Be sure the bank compliance staff has your direct contact information

If you expand your business (more agents) - let the bank know so they can expect increased volume

If you add new beneficiary countries - let the bank know so they understand new transfers to your correspondents

Be an open book to your banker and your bank's regulators

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

15

Conclusion

MSBs are governed by intense federal and state laws, rules and regulations from customer

identification documentation to reporting large cash and suspicious transactions.

Banks are under scrutiny from their regulators to have robust AML compliance programs in

place to ensure any MSB account at the institution is fully compliant with not only the BSA and

state laws and regulations, but sufficient to prevent money laundering.

One element of the required AML program regulations facing all financial institutions including

MSBs is to have an independent review of their AML program to test the program for

compliance and risk.

The independent audit of the MSB is the single most important element for a bank to properly

manage the MSB account and risk associated with the account. The bank should ensure that

the audit is done by competent individuals with experience in the specific industry. Once that is

established, the report should cover:

Full coverage of the fundamental AML regulatory requirements including FinCEN

registration and state licensing

Qualifications and training of the compliance officer and compliance staff’

Transaction testing to verify that the MSB is, in fact, complying with its own policies and

procedures on customer identification and the required dollar levels

Transaction testing of senders to identify unusually high dollar volume of traffic

Transaction testing of agents to identify unusual patterns of remittance activity

Transaction testing of beneficiaries to identify potential structuring activity analysis of

the MSB’s own monitoring system in real time to ensure all transactions are constantly

being reviewed to prevent money laundering

The MSB’s bank should be able to use the Report from the Independent Review as a completed

KYC document covering every element of the MSB’s BSA Compliance and AML Program. The

bank should be able to rely on the complete report to respond to any and all inquiries from

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

16

their own regulators regarding the financial activity and legal compliance measures of the

institution’s MSB accounts.

By presenting the bank with a thorough and complete report of the independent audit, the

bank should able to rely upon the report to satisfy its own KYC requirements for the MSB

account. If the banking institution identifies issues within the report that they feel need further

support, they should reach out to the MSB to have those items resolved and then documented

in a supplemental review or send a consultant from the bank end to conduct the BSA/AML

review.

Maintaining activity bank accounts is crucial for the continuity of MSBs. The environment of this

business will help millions of U.S. residents to send money to their loved ones back in their

home country or domestically for many good and legal purposes.

THE MONEY SERVICE BUSINESS IN USA: HOW TO COMPLY WITH FEDERAL AND STATE LAWS & REGULATIONS

AND MAINTAIN GOOD RELATIONSHIPS WITH BANKS

17

References

1) ACAMS 17th annual international AML Conference 19-21, 2013 Hollywood-Florida, The 21st

Century MSB Parts I and II

2) Source: Migration and Remittances Fact Book 2012, the World Bank

3) ACAMS Webinar: MSB Spotlight: Crucial Information on the Current State of the Industry,

October 9, 2013

4) Money laundering Prevention-A Money Services Business Guide- FinCEN

5) http://www.fincen.gov/news_room/rp/files/MSB_Exam_Manual.pdf

6) http://www.consumerfinance.gov/remittances-transfer-rule-amendment-to-regulation-e