Embed Size (px)

Citation preview

Copyright © 2021 GSM Association

The Mobile Economy

Europe 2021

GSMA Intelligence is the definitive source of global mobile operator data, analysis and forecasts, and publisher of authoritative industry reports and research. Our data covers every operator group, network and MVNO in every country worldwide – from Afghanistan to Zimbabwe. It is the most accurate and complete set of industry metrics available, comprising tens of millions of individual data points, updated daily. GSMA Intelligence is relied on by leading operators, vendors, regulators, financial institutions and third-party industry players, to support strategic decision-making and long-term investment planning. The data is used as an industry reference point and is frequently cited by the media and by the industry itself. Our team of analysts and experts produce regular thought-leading research reports across a range of industry topics.

www.gsmaintelligence.com

The GSMA represents the interests of mobile operators worldwide, uniting more than 750 operators with almost 400 companies in the broader mobile ecosystem, including handset and device makers, software companies, equipment providers and internet companies, as well as organisations in adjacent industry sectors. The GSMA also produces the industry-leading MWC events held annually in Barcelona, Los Angeles and Shanghai, as well as the Mobile 360 Series of regional conferences.

For more information, please visit the GSMA corporate website at www.gsma.com

Follow the GSMA on Twitter: @GSMA

ContentsExecutive summary 2

The mobile market in numbers 71.1 Subscriber growth slows as penetration edges upwards 8

1.2 The 5G era begins 10

1.3 Consumers embrace digital lifestyles 12

1.4 Stable financial outlook as operators recover from the pandemic 15

Key trends shaping the digital landscape 172.1 5G: moving through the gears 18

2.2 Telco of the future: open RAN gaining traction 21

2.3 Mobile network ownership: monetising assets 24

2.4 IoT: capturing a larger slice of the enterprise market 25

Mobile contributing to economic and social development

27

3.1 Mobile’s contribution to economic growth 28

3.2 The mobile industry’s response to Covid-19 32

3.3 Mobile supporting digital inclusion and addressing social challenges 33

Policies for shaping the post-pandemic digital economy

36

4.1 Realising 5G’s potential with spectrum 38

4.2 Enabling fast and efficient network build-outs 40

4.3 Improving coverage in hard-to-reach areas 41

4.4 Supporting the shift to open and virtualised RAN 42

1

2

3

4

The Mobile Economy Europe 2021

Executive summary2

Executive summary

Pandemic underscores the need for high-performance digital connectivityThe pandemic has had a profound impact on Europe and its citizens. Restrictions brought in to curb the spread of the virus have highlighted the value of connectivity for social wellbeing and economic prosperity. For many, telecoms services and applications are ingrained into everyday life. However, some still lack access to the data and/or devices needed to enable remote working or learning. The pandemic has strengthened the imperative to achieve universal access to fast, reliable broadband.

The European mobile industry has been instrumental in keeping consumers and businesses connected throughout the pandemic, despite changes in data consumption patterns and demand. Operators have acted to alleviate the impact of the pandemic on lives and livelihoods. Actions include zero-rating educational services, harnessing the power of mobile big data solutions for epidemiological modelling, and providing direct funding for hospitals, frontline workers and other healthcare initiatives.

Subscriber penetration is high, with data traffic on an upward trajectoryIn 2020, 472 million people in Europe (86% of the population) subscribed to mobile services. The total addressable market for the region’s operators is approaching saturation point, with larger mobile markets such as France, Germany and Spain accounting for the majority of new unique subscribers. Eastern and Southern European countries will see the fastest growth rates to 2025, but these will still be modest compared to those of Latin America or Sub-Saharan Africa.

A similar story is playing out in smartphone adoption, with variation in adoption levels between European markets leaving some with more room for growth than others. However, as the number of mobile internet users increases and engagement with bandwidth-hungry applications rises, data traffic will surge throughout the region, quadrupling overall by 2026.

The Mobile Economy Europe 2021

Executive summary 3

The 5G era takes shape as operators effect network capex programmesSince 2012, rapid adoption of 4G services has occurred across many European countries, establishing it as the region’s leading mobile technology. That said, connections are forecast to peak during 2022 as intensifying consumer interest, wide availability of compatible smartphones and expanding network coverage drive 5G uptake. By the end of 2025, the region will be home to 276 million 5G connections, with the Nordics and Western Europe recording the highest adoption rates.

Underpinning 5G rollout will be substantial operator investment, totalling €145 billion for the five-year period to 2025. Almost 90% of this will be specific to 5G, but some legacy network capex will remain as operators seek service quality improvements, particularly in rural areas. Limited unique subscriber growth, regulatory headwinds and intense competition make for a subdued yet stable core mobile revenue outlook. However, most operators appear to be recovering from the pandemic’s financial impacts.

Mobile continues to contribute to the economy and environmentIn 2020, mobile technologies and services generated 4.6% of GDP in Europe, a contribution that amounted to more than €740 billion of economic value added. The mobile ecosystem also supported approximately 2.4 million jobs (directly and indirectly) and made a substantial contribution to the funding of the public sector, with €84 billion raised through taxation. Over the period to 2030, 5G technologies will drive further contributions to the region’s economy, impacting key industries such as manufacturing and public administration.

Beyond economic impacts, operators are making significant contributions to the welfare of society more broadly, with progress against the UN’s 17 Sustainable Development Goals (SDGs). This includes providing access to life-enhancing educational tools and platforms, delivering the connectivity and solutions to drive enterprise productivity gains, and leading efforts to combat the effects of climate change.

Policy that recognises the vital role played by the mobile industryThe pandemic has brought into sharp focus the fundamental importance of connectivity, which has acted as a lifeline for citizens, businesses and institutions. With mobile networks vital to economic recovery and future crisis resilience, the industry needs a supportive, investment-friendly policy framework to drive infrastructure deployments, fuel sustainable growth and trigger a green and digital transformation across Europe.

5G has the potential to deliver a significant amount of value to the region, but the mobile sector remains heavily regulated and influenced by fragmented policy frameworks. To ensure Europe keeps up with the global 5G pacesetters, it is more important than ever that policymakers practise efficient spectrum management and move to eliminate network rollout barriers. Appropriate considerations should also be made around open RAN, where cross-sector collaboration will be central to creating a vibrant equipment ecosystem and facilitating supply chain diversification.

Penetration rate

Percentage of population

Penetration rate

Percentage of population

472m�����86% �����87%

UNIQUE MOBILE SUBSCRIBERS

4G

276m5G

Adoption(Percentage of total

connections excluding licensed cellular IoT)

�����40%

INTERNET OF THINGS

Mobile ecosystem contribution to public funding

Connections

(before regulatory and spectrum fees)

€84bnPUBLIC FUNDING

Jobs supported by the mobile ecosystem in 2020

1.17m +1.20m

EMPLOYMENT

�����69% �����54%

480m2025

2020

2020

2020

2020

2020

Total connections2.5bn

€800bn

MOBILE INDUSTRY CONTRIBUTION TO GDP

€740bn2020 2025

4.3bnTotal connections

2025

2025

2025

423m450m

MOBILE INTERNET USERS

�����77% �����82%

2025

Operator capex of €145 billion forthe period 2020–2025 (89% on 5G)

€144bn

€147bn

OPERATOR REVENUES AND INVESTMENT

2020

2025

Total revenues

2020-2025CAGR: 0.3%

2020-2025CAGR: 1.1%

2020

(excluding licensed cellular IoT)

674m 684m

SIM CONNECTIONS

Penetration rate

Percentage of population�����123% �����124%

2025

2020-2025CAGR: 0.1%

Adoption(Percentage of total connections excluding licensed cellular IoT)

SMARTPHONE ADOPTION

2020

�����78% �����83%

2025

Percentage of connections(excluding licensedcellular IoT)

EuropeMobile Economy

Indirect jobsDirect jobs

Penetration rate

Percentage of population

Penetration rate

Percentage of population

472m�����86% �����87%

UNIQUE MOBILE SUBSCRIBERS

4G

276m5G

Adoption(Percentage of total

connections excluding licensed cellular IoT)

�����40%

INTERNET OF THINGS

Mobile ecosystem contribution to public funding

Connections

(before regulatory and spectrum fees)

€84bnPUBLIC FUNDING

Jobs supported by the mobile ecosystem in 2020

1.17m +1.20m

EMPLOYMENT

�����69% �����54%

480m2025

2020

2020

2020

2020

2020

Total connections2.5bn

€800bn

MOBILE INDUSTRY CONTRIBUTION TO GDP

€740bn2020 2025

4.3bnTotal connections

2025

2025

2025

423m450m

MOBILE INTERNET USERS

�����77% �����82%

2025

Operator capex of €145 billion forthe period 2020–2025 (89% on 5G)

€144bn

€147bn

OPERATOR REVENUES AND INVESTMENT

2020

2025

Total revenues

2020-2025CAGR: 0.3%

2020-2025CAGR: 1.1%

2020

(excluding licensed cellular IoT)

674m 684m

SIM CONNECTIONS

Penetration rate

Percentage of population�����123% �����124%

2025

2020-2025CAGR: 0.1%

Adoption(Percentage of total connections excluding licensed cellular IoT)

SMARTPHONE ADOPTION

2020

�����78% �����83%

2025

Percentage of connections(excluding licensedcellular IoT)

EuropeMobile Economy

Indirect jobsDirect jobs

* Percentage of total mobile connections (excluding licensed cellular IoT) Note: Totals may not add up due to rounding

SMARTPHONE ADOPTION

SUBSCRIBER PENETRATION

81%

90%89%

75%

Italy

2025 2020

2025 2020

TECHNOLOGY MIX*

15%

20%64%

1% 1%

61%

38%1%

4G 5G2G 3G

2020 2025

SMARTPHONE ADOPTION

SUBSCRIBER PENETRATION

85%

87%85%

82%

UK

2025 2020

2025 2020

TECHNOLOGY MIX*

3% 5%

90%

1%

58%

42%2%

4G 5G2G 3G

2020 2025

SMARTPHONE ADOPTION

SUBSCRIBER PENETRATION

84%

89%88%

78%

Germany

2025 2020

2025 2020

TECHNOLOGY MIX*

10% 1%

14%

75%

48%

52%

1%

4G 5G2G 3G

2020 2025

SMARTPHONE ADOPTION

SUBSCRIBER PENETRATION

87%

86%84%

84%

France

2025 2020

2025 2020

TECHNOLOGY MIX*

5%22%

3%

72%

49%

49%

4G 5G2G 3G

2020 2025

Subscriber and technology trends for key markets

The Mobile Economy Europe 2021

The mobile market in numbers 7

The mobile market in numbers

01

The Mobile Economy Europe 2021

The mobile market in numbers8

Over 99% MBB adoption

1.1 Subscriber growth slows as penetration edges upwards

Figure 1

Key milestones over the next five years in Europe

Source: GSMA Intelligence

3G connections fall below 100

million

Less than 10% of total connections

are 3G

Over 100 million 5G connections

Over 80% smartphone

adoption

Over 550 million smartphone connections

Over 80% of the population

subscribe tomobile internet

services

Over 500 million 4G connections

4G connections peak and begin

to decline

4G adoption falls below two thirds of total connections

UNIQUE MOBILE

SUBSCRIBERS

MOBILE INTERNET

SUBSCRIBERS

5G

3G

MOBILE BROADBAND

(MBB)

4G

SMARTPHONES

2021 2022 2023 2024 2025

Over 475 million unique

subscribers

Over 425 million mobile internet

subscribers

450 million mobile internet

subscribers

Over 25% 5G adoption

Over 275 million 5G connections

The Mobile Economy Europe 2021

The mobile market in numbers 9

Figure 2

High mobile subscriber penetration overall in Europe, with variation at the market levelMillions (2020)

Source: GSMA Intelligence

Unique subscribers

Subscriber penetration

(%)

2 25 7

15 17

40

73

Latvia SerbiaAlbania Netherlands SpainDenmark Romania Germany

86%

78%

89%

81%

85%86% 86%

88%

The Mobile Economy Europe 2021

The mobile market in numbers10

1.2 The 5G era begins

Figure 3

2G and 3G adoption are in decline, while 4G will reach its peak before longPercentage of total connections (excluding licensed cellular IoT)

Source: GSMA Intelligence

4G became Europe’s leading mobile technology in 2017 and will peak in terms of number and share of connections in 2022. Markets such as Denmark, Estonia and the Netherlands will record negative compound annual growth rates (CAGRs) in 4G connections to 2025. However, other European countries indicate 4G’s lifecycle is not yet over and

show some untapped potential to drive adoption, especially where it lags smartphone uptake. Meanwhile, the decline of 2G and 3G is ongoing, with several operators (e.g. BT, Cosmote, Swisscom, Telenor, Telia and Vodafone) announcing and/or effecting the shutdown of legacy networks in parts of their footprints.

2G 3G 4G 5G

20192015 20202016 20212017 20222018 2023 2024 2025

80%

70%

60%

50%

40%

30%

20%

10%

0%

54%

40%

5%

1%

The Mobile Economy Europe 2021

The mobile market in numbers 11

Figure 4

Western Europe and the Nordics will be among the world’s leading markets in terms of 5G take-up5G adoption in 2025 (percentage of total connections)

Source: GSMA Intelligence

6G discussions, planning and researchWhile a handful of European markets are yet to switch on a commercial 5G network, preparations are under way for 6G. Over the long term, it is hoped that future 6G technologies will be a fundamental pillar of sustainable growth, enabling the emergence of the ‘internet of senses’ and holographic telepresence.

The European Commission has earmarked €900 million for the Smart Networks and Services project to coordinate 6G research activities and pilots under the Horizon Europe initiative. Various European operators have shown an interest in 6G research. The industry will match the Commission’s investment, taking the total to at least €1.8 billion. In December 2020, the Hexa-X 6G project was formed with EU funding; this involves the likes of Ericsson, Orange, Nokia, Siemens and Telefónica.

Elsewhere, China, Japan, South Korea and the US have all pledged substantial financial support for public-private collaboration and research into 6G patents, technologies and use cases. Though 6G standards will not be developed until 2025 and networks not deployed before the latter part of the decade, current research programmes and funding commitments indicate the significance governments are placing on being at the forefront of the mobile technology’s progression.

South Korea

Japan

US

Finland

Belgium

Norway

Germany

Mainland China

Europe

73%

68%

68%

57%

55%

52%

52%

51%

40%

The Mobile Economy Europe 2021

The mobile market in numbers12

Figure 5

Mobile internet subscribers will reach 450 million in Europe by 2025Europe’s largest mobile internet markets (subscribers, 2025)

Source: GSMA Intelligence

1.3 Consumers embrace digital lifestyles

Germany

67.8 millionSpain

40.1 millionFrance

53.2 millionItaly

51.7 millionUK

57.2 million

The Mobile Economy Europe 2021

The mobile market in numbers 13

Figure 6

Mobile data traffic in Europe will grow fourfold by 2026, similar to North AmericaExabytes per month

Source: GSMA Intelligence, Ericsson

Data traffic trends: pandemic results in short-run fluctuations, but 5G will drive future growthRising smartphone adoption and the widespread availability of 4G have underpinned growth in Europe’s data traffic as consumers have become more engaged with mobile services such as internet-based messaging, social media, entertainment and e-commerce. Covid-19 has also had a notable impact on data traffic in Europe, with many people working and learning from home, and other daily activities shifting to online channels. Networks remained resilient during testing times, with many operators reporting an increase in mobile data traffic, a surge in residential broadband usage and even a temporary rebounding of fixed voice call volumes. In Malta, for example, the regulator found that mobile data consumption (excluding Wi-Fi) in 2020 was up 141% on the previous year.1

Traffic growth will continue as Europe adopts technologies and services underpinned by 5G, including augmented and virtual reality (AR/VR); solutions and applications for smart homes, cities and buildings; and emerging services such as drone delivery, consumer robotics and autonomous cars. In Finland, Elisa expects that “by 2023, data traffic over the 5G network will exceed that of 4G”.2

2019 2020 2026

Western Europe

Central and Eastern Europe

North America

1. “Market developments for electronic communications and post – a first review of outcomes for 2020 based on Q4 figures”, Malta Communications Authority, April 20212. Interim Report Q1 2021, Elisa, 2021

18

16

14

12

10

8

6

4

2

0

The Mobile Economy Europe 2021

The mobile market in numbers14

Smartphone trends: Chinese manufacturers target growth in EuropeCovid-19 has impacted the behaviours of European smartphone users, accelerating the use of video calling, paid-for online video and music, and e-commerce. Relatedly, Ofcom research found that between September 2019 and March 2021, the number of UK adult users of TikTok grew from 3.2 million to 13.9 million, while lockdowns also resulted in a big increase in online gaming, with smartphones the most commonly used device for this activity across all age groups.3

The pandemic has affected smartphone sales within the region, with manufacturing disruptions, store closures, softer demand and delays to the release of new models making for a turbulent 2020 for the industry. While Q4 2020 signalled a recovery in sales, the overall smartphone market in Europe is estimated to have shrunk by 14% compared to 2019.4 Although production has mostly returned to normal, vendors will likely have to contend with higher consumer price sensitivity and longer replacement cycles through 2021 as economic pressures persist, as well as chipset shortages and the possible consequences of future ‘right to repair’ laws.

Some Chinese manufacturers are now aiming to use their diverse portfolios and competitive pricing to build presence and sales in Europe.5 In October 2020, Vivo began selling handsets in six large European markets, while Oppo is looking to challenge Apple and Samsung to become one of the region’s top smartphone brands – through partnerships with operators and sports teams/tournaments. The availability of premium and mass-market 5G handsets from Chinese vendors (as well as Apple’s iPhone 12 series) could influence the pace of 5G adoption in Europe, where the ability to connect to next-generation networks will be an important motivating factor in more than 60% of smartphone purchasing decisions.6

Figure 7

Europe will add over 45 million smartphone connections between 2020 and 2025, with the highest growth rates seen in Eastern and Southern marketsSmartphones as a percentage of total connections

Source: GSMA Intelligence

2025

Europe North Macedonia

Kosovo Bosnia and Herzegovina

Albania

78%83%

68%

86%

66%

81%

68%

87%

67%

86%

Germany 98.4m

France 60.8m

UK 59.6m

Spain 46.4m

Italy 60.7m

Europe’s largest smartphone markets (connections, 2025)

3. Online Nation 2021 Report, Ofcom, 20214. “European Smartphone Market Down 14% YoY in 2020; Xiaomi Gains While Huawei and Samsung Lose”, Counterpoint Research, February 20215. For more details, see: Future of Devices: 5G and services shape new market frontiers, GSMA Intelligence, 20216. Smartphone Market Intelligence Dashboard, GSMA Intelligence, 2020

2020

The Mobile Economy Europe 2021

The mobile market in numbers 15

Figure 8

Steady revenue outlook after a short-term decline

Source: GSMA Intelligence

1.4 Stable financial outlook as operators recover from the pandemic

Slowing unique subscriber growth, regulatory headwinds and intense competition have led to sustained pressure on European operators’ core mobile revenues. In 2020, the pandemic introduced a significant financial challenge, with certain factors (e.g. reductions in roaming, equipment sales and new customer acquisitions) weighing on revenue growth. That said, recent earnings results suggest an accelerating recovery in the sector, with operators

already seeking to exploit opportunities unearthed or enhanced by the pandemic, including in digital services and fibre broadband. In a competitive and near-saturated regional market (compounded by macroeconomic pressures), mobile revenue projections remain subdued; GSMA Intelligence forecasts low, single-digit growth to level off from 2022.

Operator revenue (€ billion)

Annual growth rate (%)

20192015 20202016 20212017 20222018 2023 2024 2025

150

145

140

135

130

125

3%

2%

1%

0%

-1%

-2%

-3%

144.5 144.1

146.9

The Mobile Economy Europe 2021

The mobile market in numbers16

Figure 9

5G set to dominate capex in Europe over the coming yearsOperator capex (€ billion)

Source: GSMA Intelligence

2020–2025 spend

Total

5G

€145bn

89%

Mobile operators will invest €145 billion in their networks over the 2020–2025 period, with total spend increasing annually before tailing off from 2024. 5G already accounts for the majority of European capex and will continue to do so as operators expand and enhance deployments. Some have set ambitious rollout targets – for

example, Deutsche Telekom is aiming to achieve 90% population coverage in Germany using 2.1 and 3.6 GHz spectrum by the end of 2021.7 Non-5G investment will fall out to 2025 but will not disappear entirely – for example, Three UK is rolling out 1400 MHz spectrum at its 4G sites to boost speeds and capacity.

30

25

20

15

10

5

0

5G Non-5G

19

4

22

2

2020 2021 2022 2023 2024 2025

7. “Deutsche Telekom to cover 90% of German population with 5G this year”, RCR Wireless, March 2021

The Mobile Economy Europe 2021

Key trends shaping the digital landscape 17

Key trends shaping the digital landscape

02

The Mobile Economy Europe 2021

Key trends shaping the digital landscape18

Following use case testing and lab/field trials, 5G rollouts in Europe began in earnest in H2 2019. Deployments have continued despite the pandemic (and the misinformation linking 5G technology to Covid-19 that has inspired numerous arson attacks against operator infrastructure). As a result, 5G coverage is now ramping up. For example, Telefónica has reached over 80% of Spain’s population with 5G using 1800 MHz, 2.1 GHz and 3.5 GHz spectrum, while A1 is targeting nationwide coverage in Austria by 2023. In Germany, Vodafone activated the region’s first commercial 5G standalone (SA) network while O2’s is live though not yet accessible to customers.

Despite some early commercial launches in Europe, in terms of 5G build-out and adoption, China, the US and South Korea are proving to be the front-runners. Only four European mobile operators have reported 5G connections data so far.8 Of these, EE revealed that it had reached the 1 million customer mark in April 2021. GSMA Intelligence forecasts that Europe will reach 276 million 5G connections by the end of 2025, accounting for 40% of total regional connections. The largest mobile markets (Germany, France, Italy and the UK) will drive take-up in absolute terms.

2.1 5G: moving through the gears

8. EE, Elisa, Telia and Virgin Media

The Mobile Economy Europe 2021

Key trends shaping the digital landscape 19

GSMA Intelligence’s 5G Consumer Scorecard finds that early adopters in the region are largely satisfied with their experience: 75% of 5G users report that the service has met or exceeded their expectations.9 Unsurprisingly, 5G subscribers are most likely to remark on the network’s speed. Coverage, often thought to be a potential frustration of 5G users, is satisfactory more often than not for current users, as is value (with many European operators not charging a premium over 4G).

Rising upgrade intentions will provide further encouragement for the region’s mobile industry. Europeans were much more likely to want to

upgrade to 5G in 2020 than in 2019, with the prospect increasing by an average of 10 percentage points.10 While consumers remain less enthusiastic about the technology than their counterparts in China and South Korea, the launch of the iPhone 12 series in Western markets, where Apple holds significant brand cache, should help convert some latent demand into new 5G subscriptions. Together with positive word of mouth and the downward trend in 5G handset prices, the signs are that 2021 could be a transitional year for 5G.

Figure 10

5G adoption is building gradually, as operator deployments progress beyond the largest urban centresMillion, % of total connections

Source: GSMA Intelligence

Connections Adoption (%)

300

250

200

150

100

50

020202019 2021 2022 2023 2024 2025

40%

9. 5G Consumer Scorecard, GSMA Intelligence, 202110. 5G report card: consumers give the thumbs up as outlook for 2021 improves, GSMA Intelligence, 2020

The Mobile Economy Europe 2021

Key trends shaping the digital landscape20

5G expands the opportunity for fixed wireless access11

One of the most interesting potential applications of 5G is in providing home broadband through fixed wireless access (FWA) – a hybrid approach combining aspects of traditional mobile and fixed-line delivery methods. The technology has been employed in the 3G and 4G eras, particularly in serving rural areas that lack fixed broadband access or have low speeds. However, household penetration rates were less than 1% in both France and Switzerland, for example, at the end of 2020.

With a spectral efficiency advantage of 2.0–3.5× compared to 5G mobile broadband (for smartphones), typically lower upfront deployment costs relative to fixed options and increased volumes of lower-cost customer premises equipment (CPE), 5G will enable FWA to target a broader addressable market. This has implications for a range of broadband scenarios, including mature fixed-line markets (such as Europe, Gulf States and the US). Europe accounted for four in 10 commercial launches of 5G FWA globally as of February 2021. For example, Three has launched 5G FWA in Austria and the UK, targeting xDSL households, which account for more than half of broadband connections in both markets.

The outlook for 5G FWA rests on a combination of network deployment pace, spectrum availability and refarming, and the marketing and pricing strategies of operators. Regulatory acknowledgement of FWA as a high-performance option to help achieve national broadband goals will also be important. The Body of European Regulators for Electronic Communications (BEREC) guidelines issued in October 2020 provide a good example, explicitly noting FWA as one of several technologies that will be used to construct very high capacity networks (VHCNs) in the EU.

Figure 11

Positive 5G experiences reported by early adopters as Europe sees rising upgrade intentionsDo you intend to upgrade to 5G? (Percentage of respondents who said yes)

Source: GSMA Intelligence Consumers in Focus Survey 2020

Note: figures are weighted by smartphone penetration in each market to estimate national upgrade intention

2019 2020

33%40%

61% 61%62%67%

37%

51%

71% 74%

Germany Italy Spain Sweden UK

11. 5G fixed wireless: a renewed playbook, GSMA Intelligence, 2021

The Mobile Economy Europe 2021

Key trends shaping the digital landscape 21

Before Covid-19, the telecoms sector was already undergoing a period of significant change. Models of infrastructure ownership and operation have altered significantly in recent years, with open radio access network (RAN) vendors making inroads by competing on pricing and flexibility with reduced lock-in. Results from a GSMA Intelligence survey indicate that the use of open networking technologies is already very or extremely important to 40% of European operators’ network transformation strategies.12

The potential benefits of open RAN for operators include cost savings, greater flexibility, efficiency and agility in the rollout of network elements, and the potential introduction of new suppliers. Although most open network deployments in Europe today remain relatively small, there is mounting support for this new type of architecture. The testing conducted during trials should provide operators with the knowhow and confidence to commit to much larger, commercial deployments of the technology over the medium term. Deutsche Telekom, Orange, Telefónica and Vodafone signed a Memorandum of Understanding (MoU) for the development of open RAN in Europe, in a bid to ensure the region keeps up with front-runners Japan (Rakuten) and

the US (Dish). TIM later signed the MoU and the five European telcos have since outlined a set of technical priorities. Progress with open RAN is also being driven by innovation, collaboration and open specifications from various groups, including the O-RAN Alliance and TIP.

Operators want to adopt the technology once it has scaled, but scale is only possible once operators adopt the technology.13 To mitigate this challenge, Vodafone UK has announced the launch of an open RAN Test and Validation Lab to support the developing ecosystem. It hopes to avoid a situation where operators wait to embrace open RAN, while vendors need investment to finesse their products and bring them to market.14 The operator will deploy the open interface, disaggregated technology at a minimum of 2,600 sites by 2027, around 15–20% of its national footprint. Though this will limit open RAN’s participation to targeted/tactical applications (e.g. in rural areas), there is scope for suppliers to make inroads. In the short term, the more visible impacts are likely to be in enterprise settings, such as manufacturing plants, where network deployments are more targeted and allow operators to modularise services such as edge and slicing.

2.2 Telco of the future: open RAN gaining traction

12. GSMA Intelligence Network Transformation Survey 202013. 2021 telecoms preview: open RAN, towers and enterprise digitisation, GSMA Intelligence, 202114. “OpenRAN: Vodafone to open new UK research and testing lab”, Vodafone, April 2021

The Mobile Economy Europe 2021

Key trends shaping the digital landscape22

Figure 12

Open RAN continues to make progress in Europe – selected examples

Source: GSMA Intelligence17

In June 2021, Deutsche Telekom switched on its ‘O-RAN town’ in Neubrandenburg, Germany. It will work with a range of partners and use open RAN fronthaul interfaces and Massive MIMO radios to deliver 4G and 5G across up to 25 sites.

Orange has presented a plan to solely deploy open RAN compatible network equipment from 2025. While Orange wants to “encourage a strong European open RAN ecosystem”, it has emphasised that the objective is not to attack existing providers.15

In December 2020, Telefónica Deutschland claimed a German market first, with pilot deployments of open RAN technology at three sites in Bavaria. It has since communicated plans to advance the conversion of its radio network from H2 2021, outlining a goal to deploy open RAN in 1,000 mobile sites.

In April 2021, TIM introduced open RAN technology into its commercial mobile network in Faenza, the first operator in Italy to do so. TIM is working with several partners on the deployment (which will have city-wide coverage in 2021), while other cities will be added to the rollout schedule in time.16

In November 2020, Vodafone announced a partnership with Parallel Wireless on Ireland’s first open RAN deployment, bringing 4G coverage to 30 new locations.

15. “Orange sticks with Nokia, Ericsson in open RAN era”, Mobile World Live, April 202116. “TIM takes its first step into Open RAN territory”, TelecomTV, April 202117. Region in Focus: Europe, Q4 2020, GSMA Intelligence, 2021

The Mobile Economy Europe 2021

Key trends shaping the digital landscape 23

Safeguarding 5GAn accelerating factor behind open RAN momentum in Europe and other regions is telecoms supply chain diversification, which has been driven by geopolitical tensions and cybersecurity issues.18 The EU has released a 5G security ‘toolbox’, which provides best-practice information for member states but does not impose legally binding rules. The toolbox aims to move the bloc forward in a coordinated manner based on an objective assessment of identified supply chain risks and proportionate mitigation. It recommends national regulators impose restrictions for vendors deemed high risk and exclude specific firms from supplying “key assets” to 5G networks. Further, operators should limit dependency on any one supplier and instead employ a multi-vendor strategy.

In January 2020, the UK government stopped short of banning specific “high-risk vendors” from participating in 5G networks, limiting their involvement to 35% in the access network. However, in July 2020 (following US-applied sanctions), the UK government announced that it would exclude Huawei from the UK’s existing and future 5G infrastructure.19 Elsewhere, Germany’s approach to Chinese vendors in the recently passed IT-Security Law largely follows the EU toolbox guidelines, whereas Scandinavian and Eastern European markets have taken a tougher stance. The Italian government is considering a ban on Huawei, while Dutch and Portuguese operators look set to eschew the vendor (without official state direction).20 In France, new rules on licences for Huawei equipment will work to reduce the Chinese manufacturer’s presence from French telecoms networks over time. This presents a relatively bigger challenge for Bouygues and SFR, which are more reliant on Huawei kit than Iliad and Orange.

Policymakers are looking to improve supplier diversity and foster growth of the open RAN ecosystem, mainly through working groups and some direct funding. In November 2020, the UK government published its 5G supply chain diversification strategy, which is backed by an initial £250 million from the Treasury to start work on priority measures and build momentum. In June 2020, the German government unveiled a €130 billion economic stimulus and future technologies package, designed to aid national recovery, support families and local authorities, and reshape the future of the country’s economy. The plan’s €2 billion telecoms package includes €250 million for 5G network deployment and €237 million for 6G research, as well as more than €300 million for open RAN.21

However, the diversification exercise will be a costly one. Vodafone has stated that removing high-risk firms from EU core networks could cost it €200 million over the next five years. Under the UK’s original 35% plan, BT/EE estimated that reducing its reliance on Huawei for RAN equipment would cost £500 million over a five-year period. In presenting details of its subsequent ban on Huawei from 5G networks entirely, the UK government conceded that its decision could result in rollout delays of up to three years and a cost of up to £2 billion.

18. Region in Focus: Europe, Q4 2019, GSMA Intelligence, 202019. Region in Focus: Europe, Q2 2020, GSMA Intelligence, 202020. “EU countries keep different approaches to Huawei on 5G rollout”, Euractiv, May 202121. “Germany’s €300 Million Open RAN Push Sets Tone for European Debate”, Tech Times, February 2021

The Mobile Economy Europe 2021

Key trends shaping the digital landscape24

Tower sell-offs and spin-outs continue at pace. The proceeds allow operators to pay down debt and/or invest in new projects or business lines. With European telecoms remaining highly competitive, an increasing number of operators have recognised the need to monetise extensive, underutilised assets but are not all following the same approach.

Some consider that towers give little operational leverage over their rivals, opting for sale and leaseback deals to free up financial resources for more productive use, with positive implications for costs and capital intensity. Independent tower companies have been the main acquirers of operator sites, using multi-tenancy as the driver of profitability. During 2020, Cellnex strengthened its position in Ireland, Portugal and the UK, and agreed with Iliad to buy a 60% stake in a network of around 7,000 sites belonging to Play in Poland. It has also acquired Hutchison’s European site portfolio in a deal

valued at €10 billion and is aiming to raise €4 billion in equity funding to fuel growth across the region.

Other operators have spun off infrastructure in partnerships with private equity groups, resulting in a leaner cost structure. Altice has hived off towers in a joint venture with KKR in France (SFR) and Portugal (PT), citing the opportunity to wholesale capacity to other operators as its rationale. Telia has reached an agreement to sell 49% of its Finnish and Norwegian towers (now overseen by Telia Asset Management) to Brookfield and pension fund Alecta for €722 million. Deutsche Telekom has sold its towers in the Netherlands to Cellnex but has signalled a preference to retain control of most of its assets rather than sell.22 Similarly, Orange has created TOTEM, an independent company to house its tower assets in France and Spain, and possibly even compete with tower companies by hosting and deploying sites for other operators in the future.

2.3 Mobile network ownership: monetising assets

The future will see network ownership continue to shift away from traditional vertical integration and towards shared and/or leased access and the creation of independent tower units. Regulators may

affect the scale and pace of change, with recent reviews of Cellnex acquisitions by several European competition authorities indicating an increasing focus on mobile network ownership.

Figure 13

Examples of operators offloading or restructuring tower assets

Source: GSMA Intelligence23

Created a global infrastructure unit called Telxius in 2016, later merging it into a new division, Telefónica Infra. In January 2021, Telefónica agreed to sell a controlling stake in Telxius to American Tower for €7.7 billion.

Established INWIT in 2015 and has since sold stakes in the group to investment firms such as Ardian (whose consortium has acquired 49% of TIM’s share in the tower unit).

Created Vantage Towers in 2020, an 82,000-strong European tower company, and conducted an IPO in 2021. Vantage will expand its portfolio by assimilating the sites of the Vodafone/O2 UK network share.

22. “Blog: The great big tower debate”, Mobile World Live, March 202123. Global Mobile Trends 2021, GSMA Intelligence, 2020

The Mobile Economy Europe 2021

Key trends shaping the digital landscape 25

The pandemic has affected virtually all sectors, resulting in enterprises rethinking their operational processes and how they interact with the rest of the economy. Covid-19 has accelerated the digitisation plans of some firms as they look to boost productivity and efficiency. The latest GSMA Intelligence Enterprise in Focus Survey shows that, at the end of 2020, 61% of enterprises in Europe had deployed IoT as part of a wider transformation agenda, up from 58% the previous year.24

However, Covid-19 caused considerable disruption to the European IoT market in 2020, with squeezed IoT budgets resulting in delays to the start of projects, particularly for small and medium-sized enterprises.25 This has had the effect of reducing

GSMA Intelligence’s IoT connections forecast for the next five years versus its original forecast in 2020. Nevertheless, there will be more than 4.3 billion IoT connections in Europe by 2025, with the region recording a 10% CAGR in connections over the period.26 The biggest increase is expected in enterprise IoT; this will account for 45% of total connections by 2025, driven in particular by growth in connections for smart buildings. For example, in May 2021, Telefónica Tech and Siemens announced an agreement to jointly develop smart building services for the Spanish market, including solutions relating to energy efficiency, data and video analysis, smart lighting and parking, and predictive maintenance.27

2.4 IoT: capturing a larger slice of the enterprise market

Figure 14

Over 1.9 billion new IoT connections in Europe by 2025, with smart homes and smart buildings two particular growth areasMillion

Source: GSMA Intelligence

Tota

l: 20

19

Con

sum

er e

lect

roni

cs

Smar

t ho

me

Wea

rabl

es

Smar

t ve

hicl

es

Con

sum

er o

ther

s

Smar

t ci

ty

Smar

t ut

ilitie

s

Smar

t re

tail

Smar

t m

anuf

actu

ring

Smar

t bu

ildin

gs

Smar

t he

alth

Ente

rpris

e ot

hers

Tota

l: 20

25

24. Enterprise in Focus Survey Dashboard: State of the IoT Market, GSMA Intelligence, 202125. Covid-19 reverberations put IoT projects on pause, GSMA Intelligence, 202126. IoT connections forecast: the impact of Covid-19, GSMA Intelligence, 202027. For more details, see: “Siemens and Telefónica Tech will offer combined solutions for smart buildings”, Telefónica, May 2021

2,404

4,325

179

49462

10417

3112

206

72

493 27269

The Mobile Economy Europe 2021

Key trends shaping the digital landscape26

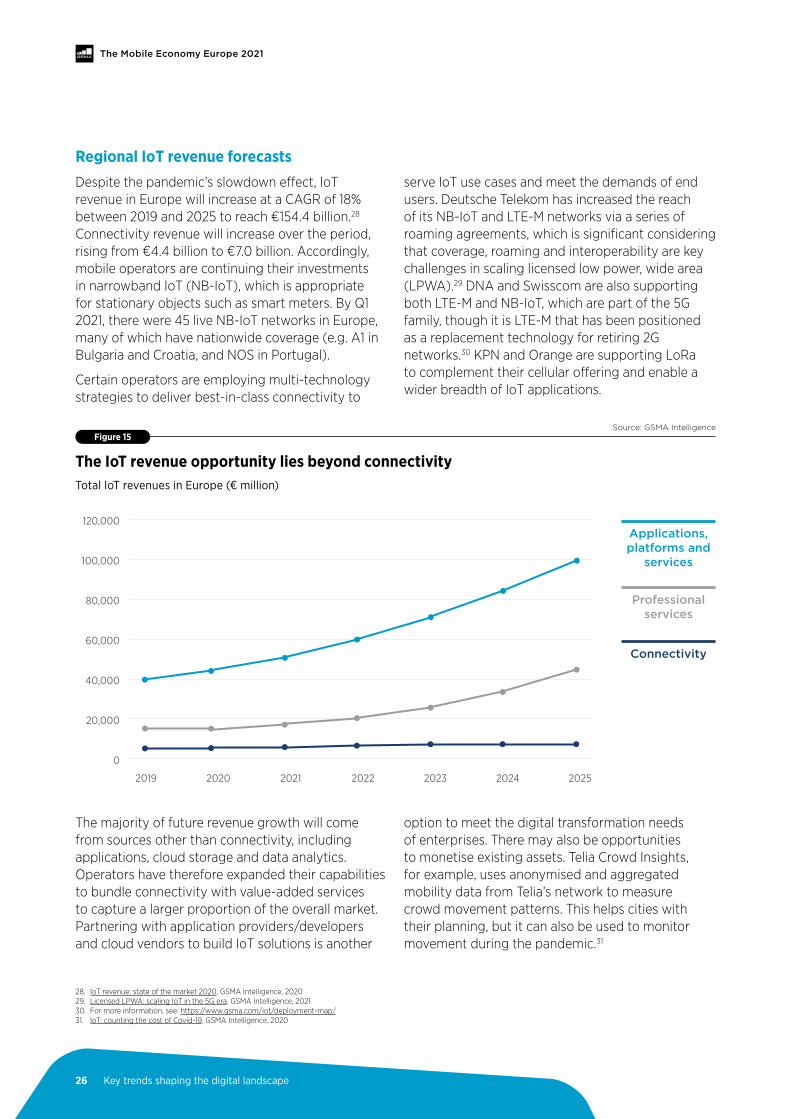

Regional IoT revenue forecastsDespite the pandemic’s slowdown effect, IoT revenue in Europe will increase at a CAGR of 18% between 2019 and 2025 to reach €154.4 billion.28 Connectivity revenue will increase over the period, rising from €4.4 billion to €7.0 billion. Accordingly, mobile operators are continuing their investments in narrowband IoT (NB-IoT), which is appropriate for stationary objects such as smart meters. By Q1 2021, there were 45 live NB-IoT networks in Europe, many of which have nationwide coverage (e.g. A1 in Bulgaria and Croatia, and NOS in Portugal).

Certain operators are employing multi-technology strategies to deliver best-in-class connectivity to

serve IoT use cases and meet the demands of end users. Deutsche Telekom has increased the reach of its NB-IoT and LTE-M networks via a series of roaming agreements, which is significant considering that coverage, roaming and interoperability are key challenges in scaling licensed low power, wide area (LPWA).29 DNA and Swisscom are also supporting both LTE-M and NB-IoT, which are part of the 5G family, though it is LTE-M that has been positioned as a replacement technology for retiring 2G networks.30 KPN and Orange are supporting LoRa to complement their cellular offering and enable a wider breadth of IoT applications.

The majority of future revenue growth will come from sources other than connectivity, including applications, cloud storage and data analytics. Operators have therefore expanded their capabilities to bundle connectivity with value-added services to capture a larger proportion of the overall market. Partnering with application providers/developers and cloud vendors to build IoT solutions is another

option to meet the digital transformation needs of enterprises. There may also be opportunities to monetise existing assets. Telia Crowd Insights, for example, uses anonymised and aggregated mobility data from Telia’s network to measure crowd movement patterns. This helps cities with their planning, but it can also be used to monitor movement during the pandemic.31

Figure 15

The IoT revenue opportunity lies beyond connectivityTotal IoT revenues in Europe (€ million)

Source: GSMA Intelligence

Connectivity

Applications, platforms and

services

Professional services

120,000

100,000

80,000

60,000

40,000

20,000

0

20202019 2021 2022 2023 2024 2025

28. IoT revenue: state of the market 2020, GSMA Intelligence, 202029. Licensed LPWA: scaling IoT in the 5G era, GSMA Intelligence, 202130. For more information, see: https://www.gsma.com/iot/deployment-map/31. IoT: counting the cost of Covid-19, GSMA Intelligence, 2020

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

27

Mobile contributing to economic and social development

03

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

28

Benefits driven by mobile technology in developed markets amounted to $1.5 trillion of economic value (2.8% of GDP) over the last two decades. In Europe, income per capita has risen by $550 over the last 20 years due to the expansion of mobile technology, accounting for approximately 8% of total income per capita growth.32 With the outbreak of Covid-19, the mobile industry has emerged as a lifeline, enabling many business activities to continue and mitigating the impact of social restrictions on economic output. In a post-pandemic world, mobile technology will likely play an even more crucial role in facilitating new business models for enterprises and digital experiences for consumers. By 2030, upgrades to 5G and the new services enabled by the technology will add €102 billion annually to the European economy, with manufacturing and public administration driving 60% of the benefit.

Figure 16

The mobile ecosystem directly generated more than €125 billion of economic value in Europe in 2020, with operators accounting for over half of it€ billion, percentage of GDP (2020)

Source: GSMA Intelligence

3.1 Mobile’s contribution to economic growth

17

93

8 80.1%

0.04%

0.6%

0.1%

Infrastructure providers

Mobile operators

Distributors and retailers

Content, applications and other services

32. Mobile technology and economic growth: Lessons to accelerate economic growth and recovery, GSMA, 2020

Note: totals may not add up due to rounding

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

29

Figure 17

Additional indirect and productivity benefits bring the total contribution of the mobile industry in Europe to more than €740 billion € billion, percentage of GDP (2020)

Source: GSMA Intelligence

4.6%

0.6%0.2%

0.5%

3.3%

Mobile operators

IndirectRest of mobile ecosystem

Productivity Total

9334

76

538 740

MOBILE ECOSYSTEM

Figure 18

The mobile ecosystem employs almost 2.4 million people in Europe, either directly or indirectly through adjacent industriesThousands of jobs (2020)

Source: GSMA Intelligence

Note: totals may not add up due to rounding

Note: totals may not add up due to rounding

370 210

180 1,170

1,200 2,380

Mobile operators

Distributors and retailers (formal and

informal)

Rest of mobile

ecosystem

Direct Indirect Total

410

Content, apps and service

providers

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

30

Figure 19

In 2020, the mobile ecosystem contributed almost €85 billion to the funding of the European public sector through consumer and operator taxes€ billion

Source: GSMA Intelligence

Figure 20

Driven mostly by continued expansion of the mobile ecosystem, the economic contribution of mobile in Europe will increase by around €60 billion by 2025€ billion

Source: GSMA Intelligence

Services VAT, sales taxes and excise duties

Handset VAT, sales taxes, excise

and customs duties

Corporate taxes on profits

Employment taxes and social

security

Total

34 88

34 84

2022 2025202420232020 2021

Direct ProductivityIndirect

150

86

568

146

84

560

141

81

551

139

80

542

137

79

532

128

74

535

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

31

Figure 21

5G will deliver a total economic value add of more than €600 billion for Europe during 2020–2030, with manufacturing and services accounting for the majorityShare of total economic benefit

Source: GSMA Intelligence

Manufacturing

Services (public administration, finance, healthcare, education)

Utilities management, transport, construction, mining, agriculture

ICT

Retail

7% 1%

8%

41%

43%

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

32

During the pandemic, the mobile industry has strived to keep consumers and businesses connected, and has engaged with public and private organisations to provide targeted support for vulnerable individuals and communities. Covid-19 response measures implemented by operators include removing data

limits; offering additional entertainment options; closing retail stores to minimise contact between citizens; providing funding for hospitals and other healthcare initiatives; and utilising mobile big data solutions for epidemiological modelling and population mobility analysis.33

Figure 22

Selected operator response measures to the Covid-19 pandemic in Europe

Source: GSMA34 and company websites

3.2 The mobile industry’s response to Covid-19

Market Initiatives

Austria A subsidiary of A1 Telekom Austria partnered with the state of Tyrol and the Red Cross to create a digital screening platform, which it claimed enables “a large number of tests” to be conducted “faster, more reliably and more securely than before”.

Italy Telecom Italia pledged to donate €1 million to four hospitals across the country through the TIM Foundation, as part of its efforts to tackle the crisis. The operator said it will give €250,000 to healthcare institutions in Milan, the Veneto region, Rome and Naples.

Multiple Orange established an €8 million crisis fund to supply personal protective equipment, provide support to medical professionals and fund initiatives to contain the spread of the disease in countries within its EMEA footprint. The operator also joined a French government-backed research and development project, bringing together national players to establish a contact tracing app, as part of the country’s fight against the pandemic.

Multiple Telefónica joined a group of international companies (including accelerator Airbus BizLab and investment bank Citi) to launch Restarting Together – a programme designed to identify SME and start-up projects that could help boost economic recovery from the effects of Covid-19.

Norway Since January 2020, Telenor has been providing mobility data on movement in Norway’s 356 municipalities to the Institute of Public Health’s Covid-19 taskforce. Telenor’s mobility data has been used to inform modelling of the potential spread of the virus, to develop predicted incidence in each municipality and simulate the number of hospitalisations, intensive care patients and deaths.

UK In March 2020, UK telecoms companies announced the removal of data caps to ensure vulnerable customers remained connected during the pandemic. Operators agreed to provide support for customers struggling to make payments, offer new packages for frontline workers and job seekers, and provide alternative communication methods in the event of outages.

33. For more examples, see: “Keeping Everyone and Everything Connected in Europe: European Mobile Network Operators respond to COVID-19 pandemic”, GSMA, April 2020 34. Utilising mobile big data and AI to benefit society: Insights from the Covid-19 response, GSMA, 2021

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

33

As the first industry to have committed fully to the UN Sustainable Development Goals (SDGs), the mobile industry continues to have substantial positive effects on lives and livelihoods.35

Figure 23

Mobile’s impact on the SDGs in Europe, 2019

Source: GSMA

3.3 Mobile supporting digital inclusion and addressing social challenges

Highest SDG scores Most improved SDG scores

35. 2020 Mobile Industry Impact Report: Sustainable Development Goals, GSMA, 2020

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

34

Investing in infrastructure, industries and the environmentSDG 9 aims to build resilient infrastructure, promote inclusive and sustainable industrialisation, and deliver affordable internet access for all. In Europe, mobile technology contributes to this goal as a provider of critical infrastructure and as a platform for innovation. The region’s high score for SDG 9 is mainly a function of increasing mobile broadband adoption, which is driven by operators’ network investments – especially those targeted at expanding coverage and improving quality in hard-to-reach areas, as well as closing the urban/rural digital divide.

Europe’s performance is also driven by mobile’s effect for adjacent sectors. The connectivity provided by mobile operators enables industrial processes and manufacturing to utilise technological advancements in IoT, AI and big data analytics, which in turn facilitates productivity gains. For example, Sunrise has established an innovation centre with Huawei to work on 5G-enabled services, including for Industry 4.0. Sunrise and Huawei have implemented a 5G-based predictive maintenance solution at GF Machining’s factory in Switzerland, which has reduced the failure rate

of the manufacturer’s milling process, with the improvements in product quality saving it €30 million per plant per year.36

The mobile sector’s support for SDG 9 also has knock-on effects for other goals, including SDG 13 (Climate Action). Mobile technology contributes to SDG 13 by improving energy efficiency, bringing about changes in behaviour and reducing greenhouse gas (GHG) emissions. Research from the GSMA and the Carbon Trust shows that mobile technologies can help avoid 10× more emissions than they cause.37

The GSMA and operators have developed an industry-wide climate action roadmap to achieve net-zero GHG emissions by 2050, in line with the Paris Agreement. More than 50 mobile operators now disclose their climate impacts and GHG emissions via the internationally recognised CDP global disclosure system. These include regional operators BT, Deutsche Telekom, KPN, Proximus, Telefónica and Vodafone, which were acknowledged for their climate efforts at the CDP’s Europe Awards 2021, along with Cellnex and Nokia.

36. For more details, see: 5G Era IoT Manufacturing Benefits & Use Cases – GF Machining, GSMA, 2020 37. The Enablement Effect: The impact of mobile communications technologies on carbon emission reductions, GSMA, 201938. For more details, see: “Companies take action to support the green and digital transformation of the EU”, European Commission, June 2021

Sustainability in Europe and the Green Digital CoalitionEuropean operators are committed to supporting national climate change policies and the EU Green Deal, and leading the global transition towards a zero-carbon economy. Telia has bolstered its sustainability commitment with new goals, while Deutsche Telekom has brought forward its climate deadlines. The German operator is aiming for neutrality for in-house emissions by 2025 (previously 2030) and to achieve net-zero status across its whole supply chain by 2040 (10 years earlier than originally planned).

The CEOs of 13 telecoms firms, including Ericsson, NOS, Orange and TDC, were among the 26 initial signatories of the European Green Digital Coalition – a cross-sector agreement to take action to support the green and digital transformation of the EU. The chief executives committed on behalf of their companies to take action in the following areas:

• Invest in the development and deployment of greener digital technologies and services that are more energy and material efficient.

• Develop methods and tools to measure the net impact of green digital technologies on the environment and climate by joining forces with NGOs and relevant expert organisations.

• Co-create with representatives of other sectors recommendations and guidelines for the green digital transformation of these sectors that benefits the environment, society and economy.38

The Mobile Economy Europe 2021

Mobile contributing to economic and social development

35

39. “UK’s first 5G immersive classroom brings richer learning experience to pupils”, BT, March 2021

Delivering access to educational content, tools and platformsSDG 4 seeks to ensure inclusive and equitable quality education, and to promote lifelong learning opportunities for all. Mobile technology contributes to SDG 4 by allowing students, teachers and employees to learn/teach from any location and on the move. It can help education through the dissemination of online content and support, and by promoting the use of ICT in education and bridging the digital divide through e-learning. The benefits of e-learning have been amplified during the pandemic, with the majority of students at some point away from classrooms and using communications platforms and video conferencing applications to study remotely.

Many mobile operators have enabled access to digital content during the pandemic by zero-rating online educational services, lifting data caps and distributing devices to teachers and students. In one Scottish school, BT delivered the UK’s first 5G-enabled immersive classroom. The concept could be adapted for other industries, such as fitness and tourism.39 By 2025, the Vodafone Foundation has committed €20 million to advancing digital education and skills across 14 European markets. Operators have also taken steps to ensure online safety for children as they look to support learning and build digital skills. For example, Telenor Norge’s Bruk Hue campaign provides a free, interactive, mobile-based teaching programme focused on combatting cyberbullying.

The Mobile Economy Europe 2021

Policies to support the future of mobile36

Policies to support the future of mobile

04

The Mobile Economy Europe 2021

Policies to support the future of mobile 37

Since the current European Commission leadership was established at the end of 2019, policymakers have articulated a vision for Europe’s Digital Decade. They have implemented policies, directives and regulations – for example, on digital gatekeepers, broadband deployment, industrial policy and AI. These measures, broadly supported by the mobile industry, have the potential to accelerate Europe’s digital evolution and economic strength. In response to the pandemic, the European Commission has mobilised a new €750 billion recovery instrument, known as Next Generation EU, and reinforced the EU’s long-term budget by €1.1 billion. Disbursement of funds will require that member states’ recovery and resilience plans sufficiently demonstrate, among other things, effective contribution to the green and digital transitions. This recognises the vital role digital technologies will play in laying the groundwork for a prosperous and thriving Europe, while also realising the targets of the Green Deal.

However, the European telecoms environment does not sufficiently support private network investment, with the cost of capital often higher than its return.40

The European Investment Bank (EIB) estimates the EU digital infrastructure investment gap at €42 billion per year between 2020 and 2025.41 To achieve widespread 5G rollout, adoption and usage – and fulfil the infrastructure dimension of the EC’s March 2021 Digital Compass priorities42 – appropriate regulatory frameworks are a prerequisite. Making decisions on policy now can have a lasting impact, ensuring no one is left behind in the emerging post-pandemic digital era. Policymakers should collaborate with the private sector to stimulate the investment in next-generation networks that will form a backbone for Europe’s economic recovery by enabling employment, entrepreneurship and innovation, while supporting the achievement of essential climate-related goals.

40. Mapping a New World with the EU Digital Compass: Priorities for Economic Recovery, ERT, 202141. Identifying Europe’s recovery needs, European Commission, 202042. For more details, see: “Europe’s Digital Decade: digital targets for 2030”, European Commission, March 2021

The Mobile Economy Europe 2021

Policies to support the future of mobile38

4.1 Realising 5G’s potential with spectrum5G’s advanced capabilities offer the potential to underpin a range of consumer and enterprise applications, and provide a platform for socioeconomic growth and industrial digitisation. To harness its full benefits, forward-looking policies and regulations are required, particularly in the area of spectrum. Access to the right amount and type of spectrum under fair terms and pricing conditions is essential to deploying high-performance next-generation networks. The speed, reach and quality of 5G services depend on a significant amount of new harmonised mobile spectrum in large and contiguous blocks across three key ranges.

Low band (<1 GHz)700 MHz spectrum is needed to provide increased capacity and performance of mobile services in rural areas and for deeper in-building coverage, as well as to support important new applications and use cases. Combined with recent trends in consumption and distribution of media and the decline in linear broadcasting, this should prompt more decisive actions to make 700 MHz band available for mobile.

The EC supports the use of the 700 MHz band for 5G services. Although several markets have now assigned this band, Europe is lagging behind on low-band allocations overall. More than half of the EU member states missed the Commission’s extended deadline of the end of 2020 to license sub-1 GHz spectrum.43

Mid band (1–6 GHz)If 5G new radio (NR) is to work optimally, it requires wide, contiguous spectrum blocks for operation. Spectrum in the 3.4–3.8 GHz range is widely viewed as offering an optimal balance of coverage and capacity, and is accepted as the primary range for 5G in Europe. This spectrum can enable myriad potential use cases beyond enhanced mobile broadband (eMBB). Clearing the relevant bands for 5G should be a primary regulatory objective. As a first step, regulators should release 80–100 MHz of contiguous spectrum per operator within the 3.4–3.8 GHz range to help alleviate network congestion in major cities, while also minimising the costs of site densification.

In terms of amount of spectrum and pricing, Finland offers a positive example:

• Amount of spectrum – Finland released 390 MHz of spectrum for auction in 2018, with each operator receiving 130 MHz. This is the highest amount of spectrum any operator currently has obtained in the C-band via an auction.

• Pricing44 – On a €/MHz/pop/year (PPP) basis, Finnish operators paid less than €0.003. This compares to prices paid in Italy of €0.03, Germany €0.01 and Taiwan €0.06 (the latter is the highest globally so far). The comparison with reserve prices is important as Finnish operators paid only marginally higher than the total reserve price, with DNA winning the spectrum at reserve. The total reserve price for all spectrum was €65 million, with total auction proceeds of €77.6 million.45

Some administrations in Europe (e.g. in the UK) are eyeing the opportunity to utilise additional mid-band spectrum in the 3800–4200 MHz range for 5G. To ensure 5G’s potential, a long-term approach to mid-band licensing is needed. It is estimated that 1–2 GHz of additional mid-band spectrum is required in the 2025–2030 timeframe.46 This would deliver the 5G vision of a downlink user experienced data rate of 100 Mbps, and satisfy the 50 Mbps uplink target in urban areas. Additional mid-band spectrum in the 3800–4200 MHz range should be part of this expansion, but licensed spectrum bands such as 6 GHz are also needed to meet demand.

43. Spectrum Navigator, Q1 2021: new insights and trends to watch, GSMA Intelligence, 202144. € figures converted from $ values stated in published report.45. How spectrum will shape the outlook for 5G in Russia, GSMA, 202046. IMT spectrum demand: Estimating the mid-bands spectrum needs in the 2025-2030 timeframe, Coleago, 2021

The Mobile Economy Europe 2021

Policies to support the future of mobile 39

High band (above 6 GHz)The advanced performance capabilities of millimetre wave (mmWave) spectrum can deliver the massive capacity, gigabit speeds and low latencies needed to power new use cases and cutting-edge services, and drive the revolutionary impact of 5G across Europe. Assigning around 1 GHz of this spectrum per operator will be necessary to meet the demand for many enhanced mobile data services and in turn realise 5G’s full socioeconomic benefits.

Although some operators (in Czechia, Luxembourg and Poland) have indicated a lack of immediate interest in mmWave spectrum, momentum is

building around the 26 GHz band. This is adjacent to the 28 GHz band, allowing wide harmonisation, low handset complexity, economies of scale and early equipment availability. Italy was the first European market to assign spectrum in the 26 GHz band, but a number of other markets in the region have followed suit and more are poised to do so. Compared to using 3.5 GHz spectrum alone, mmWave can offer a compelling option in terms of total cost of ownership (TCO) in various 5G rollout settings, including dense urban areas, FWA and indoor enterprise deployments.47

Eschew set-asides in priority bandsAmid increasing appetite from sectors to deploy dedicated networks, some European markets have considered or determined to set aside spectrum for industry verticals. The concern, however, is that setting aside 5G spectrum in priority bands could mean a valuable resource goes unused in many areas, limiting the amount of spectrum available for mobile operators to provide public and private 5G services, with a direct impact on speeds, coverage and cost. Set-asides for restricted use cases and limited coverage areas could also lead to inefficient spectrum usage, which defeats the fundamental policy objective of spectrum planning. In Germany, reserving spectrum in a key 5G band for verticals drove higher prices. This was further compounded by the successful bid of a new-entrant operator (not subject to the minimum coverage obligations imposed on the three incumbent operators). This induced scarcity resulted in mobile operators paying €3.59 billion for 300 MHz of spectrum.

National exclusive licensing to mobile operators continues to be the most effective and efficient spectrum assignment mechanism. Mobile operators continue to be well placed to address concerns by providing dedicated 5G services for verticals, which can benefit from network slicing, small cells and wider geographical coverage. Additionally, operators can leverage their larger and more diverse spectrum assets and large-scale deployment experience to build networks more efficiently and effectively. Regulators can also utilise market mechanisms, such as a sunset clause, to mitigate the risk of set-aside spectrum going unused.

47. The economics of mmWave 5G, GSMA Intelligence, 2021

The Mobile Economy Europe 2021

Policies to support the future of mobile40

4.2 Enabling fast and efficient network build-outsEven where spectrum is assigned early and in sufficient quantities, operators face challenges in effecting planned rollouts. In some regions of Switzerland, for example, 5G deployment has faced significant obstacles due to a lack of acceptance of the new technology and concerns it may pose health risks. Mobile operators have successfully appealed a law passed in February 2020 by the Grand Council of Geneva, which could have introduced a three-year moratorium on 5G permissions. While operators should therefore be able to deploy new antennas

more easily, local authorities remain responsible for authorising mobile sites and could continue to put obstacles in the way. To speed up mobile broadband deployments, European policymakers should strive to reduce regulatory barriers and fragmented processes, and create pro-investment environments to facilitate universal coverage. The EU Connectivity Toolbox and the upcoming review of the Broadband Cost Reduction Directive (BCRD) will play an important role in ensuring more cost-effective network deployment in Europe.

Simplified and streamlined planning approval processesTo incentivise and accelerate 5G deployments, policymakers should implement streamlined application and approval processes for mobile networks, while respecting environmental and community impact considerations. Leveraging a single digital administrative channel can improve coordination between government entities at all levels (municipal, local, regional and national), driving cost efficiencies and saving valuable rollout time.

As the number of small cell sites increases as part of evolving deployments, governments may consider exemptions for small cell installations, reduce antenna height regulations to maximise coverage, allow colocations or certain site upgrades, as well as establish ‘one-stop shopping’ licensing procedures and even implicit approval. These interventions can lower the barriers and bureaucracy involved in designing and deploying mobile networks, resulting in more cost-effective rollouts to reach rural areas.

Non-discriminatory and timely access to public infrastructurePolicymakers can support operator efforts to expand mobile broadband coverage by facilitating timely and affordable access to public infrastructure such as buildings, roads, street furniture, railways and ducts for utility services. Such access can be easily implemented, will remove or reduce barriers to

deployment and significantly accelerate the network rollout process. This policy approach can save on the upfront and operating costs of setting up a tower, and provide additional capacity in congested areas where space for sites is limited – particularly important in the case of building dense 5G networks.

Aligning wireless exposure standards with international best practicePublic interest in the health effects of electromagnetic fields associated with mobile networks can arise with the introduction of any new generation of mobile technology – 5G is no exception. Last year’s updated radio frequency (RF) exposure guidelines by the International Commission on Non-Ionizing Radiation Protection (ICNIRP) – which include frequencies above 6 GHz, including mmWave 5G – confirm that the international limits remain protective of all people, including children, against all established health hazards.

It is important that all European countries adopt the updated guidelines. Disparities between national limits and international guidelines can foster confusion for both regulators and policymakers, increase public anxiety and provide a challenge to manufacturers and operators of communications systems which need to tailor their products to each market. In the view of ICNIRP, national limits that are more restrictive than the international guidance do not offer any additional health protection.

The Mobile Economy Europe 2021

Policies to support the future of mobile 41

4.3 Improving coverage in hard-to-reach areasDespite significant operator investment in expanding the reach of mobile broadband networks, there remain pockets of European countries unserved or underserved by 3G or 4G services. The coverage gap brought about by these ‘not-spots’ is largely confined to the most rural, sparsely populated geographies where rollout cost is a major factor. Mobile networks in remote areas can be considerably more expensive to deploy and run than in urban areas, while the revenue opportunities are several times lower due to smaller populations. As such, partnerships between authorities and operators are needed to further extend mobile coverage and support the sustainability of network operations. In two of Europe’s largest markets, collaborative and innovative action to address rural connectivity issues provides useful case studies:

• France’s New Deal for Mobile has seen mobile operators taking on new, additional coverage obligations in exchange for a non-compete on renewals of spectrum in the 900 MHz, 1800 MHz and 2.1 GHz frequency bands, with an aim of providing 4G services on all sites operational in 2018 by the end of 2020.48 On 10 November 2020, the Secretary of State for the Digital Transition and Electronic Communications confirmed that the transition to 4G was on track, while Arcep

welcomed the achievements made under the scheme, which is “thanks to the mobilisation of operators, local players and public authorities”.49

• The UK’s voluntary Shared Rural Network brings together public and private funding, through a combination of investment and infrastructure sharing, to deliver 95% geographic coverage of 4G by the end of 2026.

As mobile operators press ahead with 5G rollouts, a similarly collective approach is required to drive coverage of next-generation services into the hardest to reach rural areas and communities, safeguarding against the creation of a new digital divide. Voluntary network sharing agreements are a vital long-term solution, on which governments, regulators and mobile operators should collaborate. Such arrangements can lower the risks and cost of expanding 5G coverage in remote areas by allowing operators to jointly use resources, avoiding unnecessary duplication of infrastructure. This can create efficiencies and help bridge identified investment gaps without comprising competition. Policymakers should encourage voluntary sharing of passive and active network elements to facilitate the swift expansion of high-performance networks across Europe.50

Avoiding wholesale 5G networksThe experiences of markets that have rolled out a 4G single wholesale network (SWN) highlight clear difficulties with the successful rollout of this approach, typically offering an inferior alternative to the traditional network deployment model. The lessons should serve as examples to European countries that may consider a SWN in the 5G era. To ensure next-generation services are available to as many citizens as possible, policymakers should instead put in place the building blocks of mobile connectivity, including cost-effective access to low-frequency spectrum, support for voluntary network sharing, and non-discriminatory access to public infrastructure.51

48. A similar policy has been introduced in Portugal, while operators in Sweden have been able to claim back part of the amount they bid at spectrum auctions in order to pay for base stations in rural areas defined by the regulator.

49. “New Deal for Mobile: 4G for everyone in France”, Arcep, November 202050. For more details, see: https://cp.gsma.com/expanding-mobile-coverage/51. Single Wholesale Networks: Lessons From Existing and Earlier Projects, GSMA, 2019

The Mobile Economy Europe 2021

Policies to support the future of mobile42

4.4 Supporting the shift to open and virtualised RANAs mobile operators build out 5G connectivity, they are embracing new architectures based on technology principles of virtualisation, cloud computing and network automation, while also supporting the opening up of proprietary elements and interfaces in the RAN. However, enabling mass deployment of these principles means overcoming a number of challenges. While the main vehicle for taking forward open and virtualised RAN is wide industry cooperation in international fora and standardisation, policymakers can play a role in supporting initiatives to mix and match RAN elements: