Embed Size (px)

Citation preview

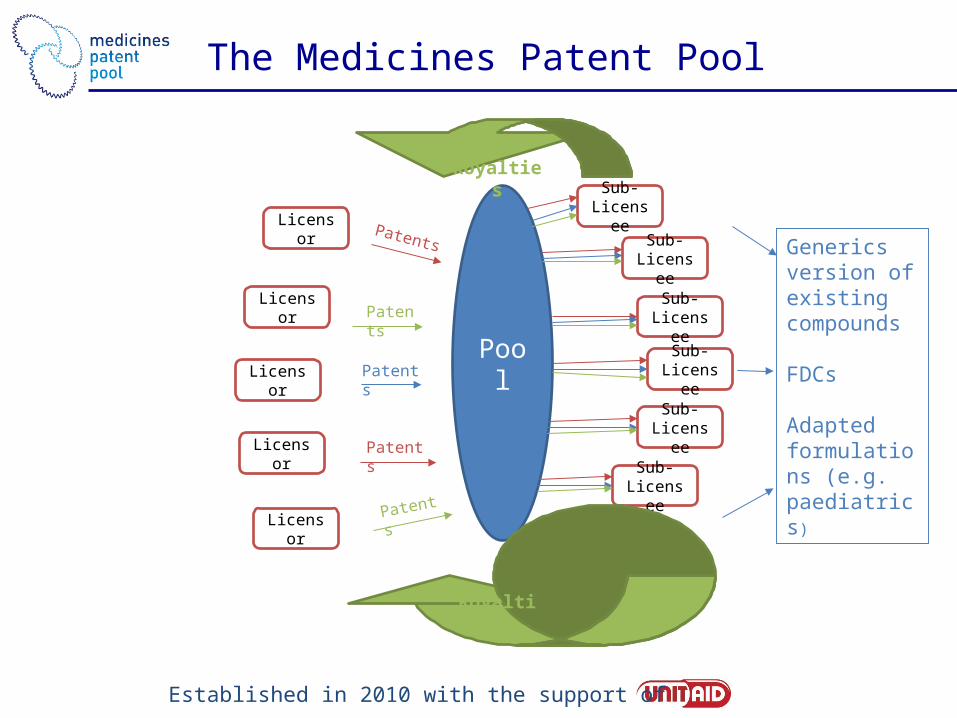

The Medicines Patent Pool

Ellen ‘t HoenUNITAID Consultative ForumGeneva, 4-5 October 2011

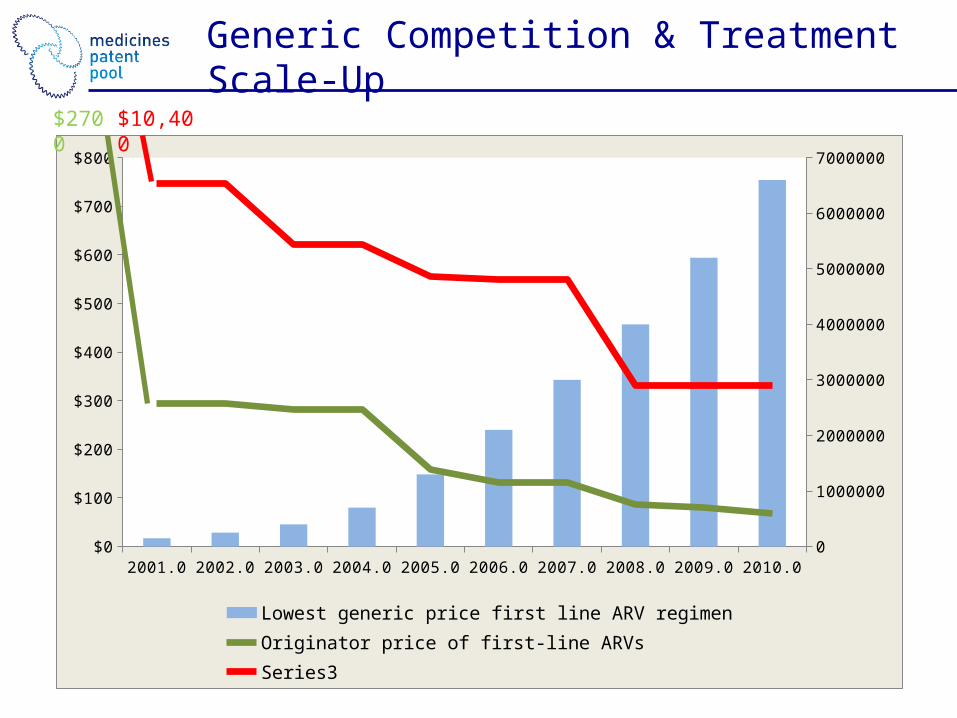

2001.0 2002.0 2003.0 2004.0 2005.0 2006.0 2007.0 2008.0 2009.0 2010.00

1000000

2000000

3000000

4000000

5000000

6000000

7000000

$0

$100

$200

$300

$400

$500

$600

$700

$800

Lowest generic price first line ARV regimenOriginator price of first-line ARVsSeries3

$10,400$2700

Generic Competition & Treatment Scale-Up

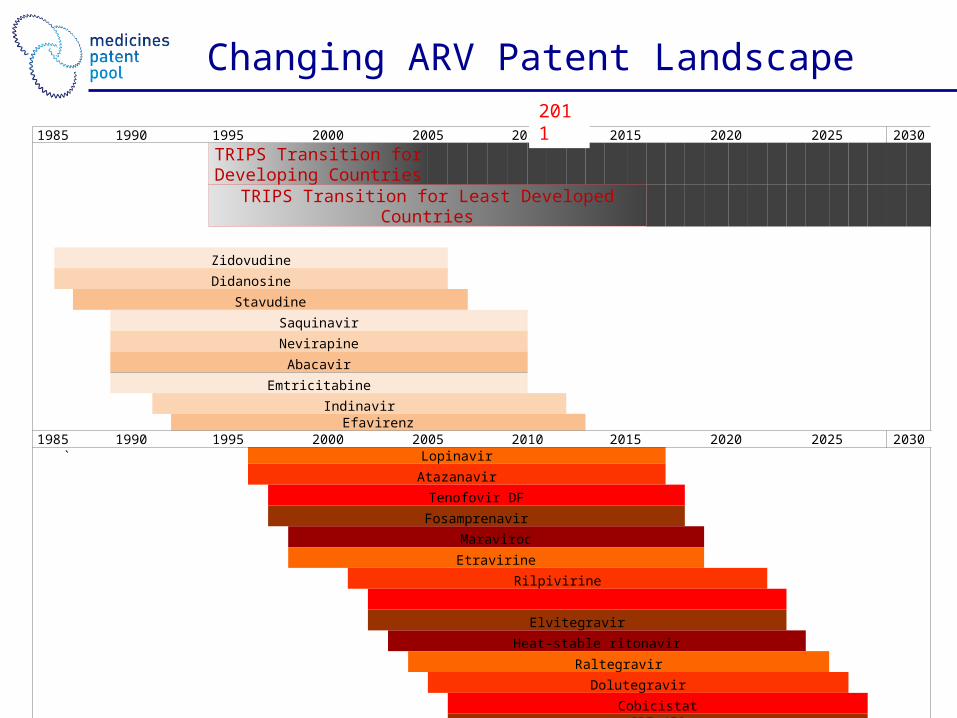

1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

TRIPS Transition for Developing Countries

TRIPS Transition for Least Developed Countries Zidovudine Didanosine Stavudine Saquinavir Nevirapine Abacavir Emtricitabine Indinavir Efavirenz 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 ` Lopinavir Atazanavir Tenofovir DF Fosamprenavir Maraviroc Etravirine Rilpivirine Elvitegravir Heat-stable ritonavir Raltegravir Dolutegravir Cobicistat SPI-452 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

2011

Changing ARV Patent Landscape

Pool

Sub-License

eSub-

Licensee

Sub-License

e

Sub-License

e

Sub-License

eSub-

Licensee

Sub-License

e

Royalties

Royalties

Patents

Patents

Patents

Patents

Patents

Licensor

Licensor

Licensor

Licensor

Licensor

Generics version of existing compounds

FDCs

Adapted formulations (e.g. paediatrics)

The Medicines Patent Pool

Established in 2010 with the support of

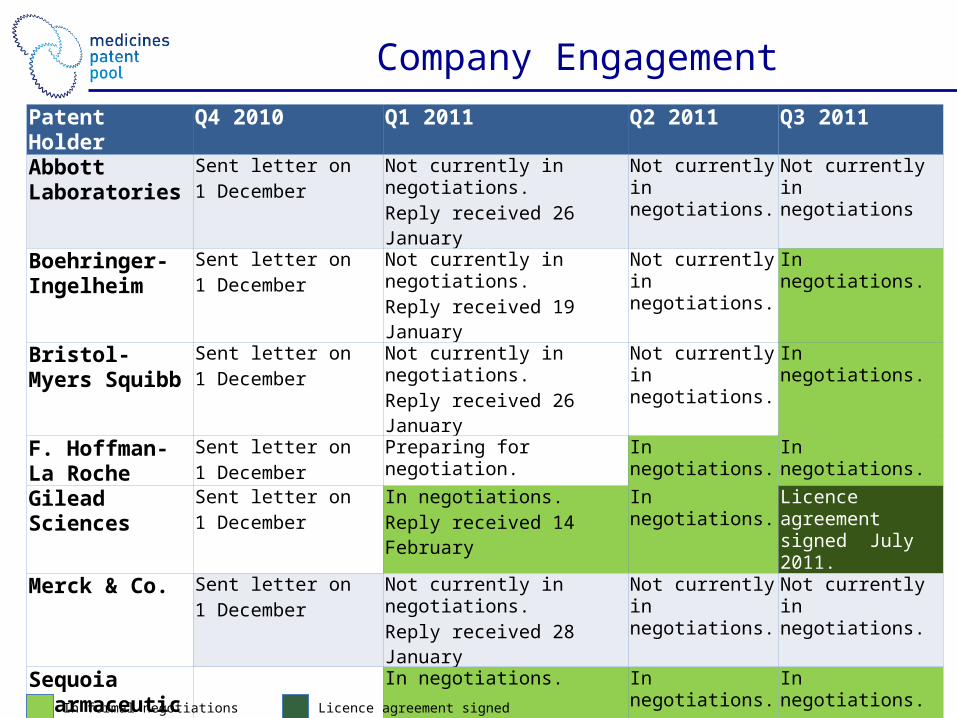

Company Engagement

Patent Holder Q4 2010 Q1 2011 Q2 2011 Q3 2011

Abbott Laboratories

Sent letter on 1 December

Not currently in negotiations. Reply received 26 January

Not currently in negotiations.

Not currently in negotiations

Boehringer-Ingelheim

Sent letter on 1 December

Not currently in negotiations. Reply received 19 January

Not currently in negotiations.

In negotiations.

Bristol-Myers Squibb

Sent letter on 1 December

Not currently in negotiations. Reply received 26 January

Not currently in negotiations.

In negotiations.

F. Hoffman-La Roche

Sent letter on 1 December

Preparing for negotiation. In negotiations. In negotiations.

Gilead Sciences Sent letter on 1 December

In negotiations.Reply received 14 February

In negotiations. Licence agreement signed July 2011.

Merck & Co. Sent letter on 1 December

Not currently in negotiations. Reply received 28 January

Not currently in negotiations.

Not currently in negotiations.

Sequoia Pharmaceuticals

In negotiations. In negotiations. In negotiations.

Tibotec/Johnson & Johnson

Sent letter on 1 December

Not currently in negotiations. Reply received 31 January

Not currently in negotiations.

Not currently in negotiations.

US NIH Licence agreement signed Sept 2010.

In negotiations. In negotiations. In negotiations.

ViiV Healthcare Sent letter on 1 December

In negotiations. In negotiations. In negotiations.

In formal negotiations Licence agreement signed

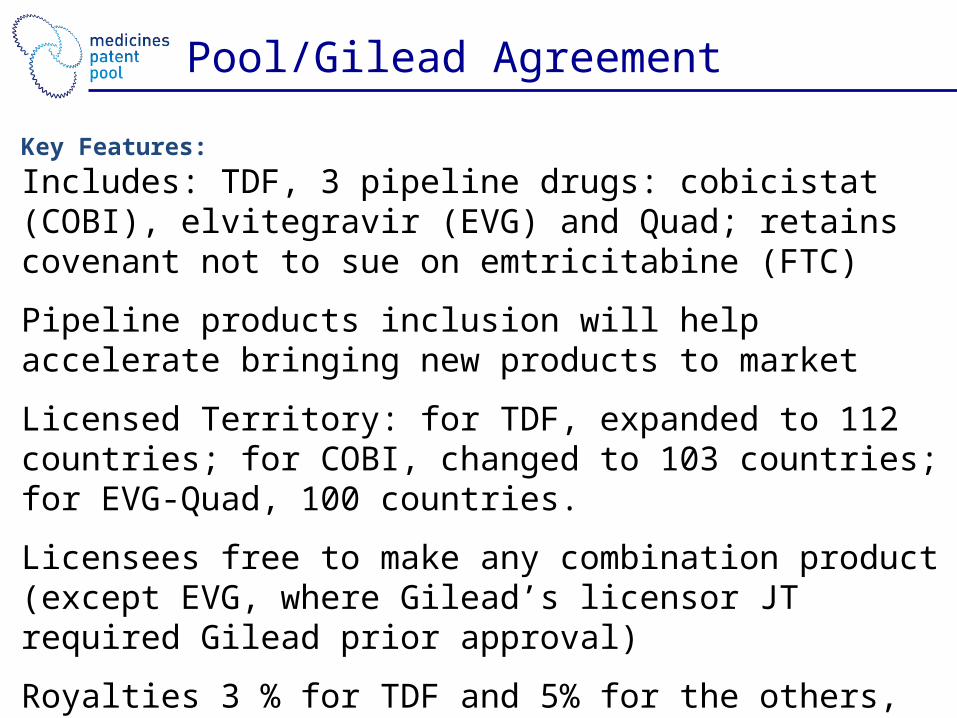

Pool/Gilead Agreement

Key Features:

Includes: TDF, 3 pipeline drugs: cobicistat (COBI), elvitegravir (EVG) and Quad; retains covenant not to sue on emtricitabine (FTC)

Pipeline products inclusion will help accelerate bringing new products to market

Licensed Territory: for TDF, expanded to 112 countries; for COBI, changed to 103 countries; for EVG-Quad, 100 countries.

Licensees free to make any combination product (except EVG, where Gilead’s licensor JT required Gilead prior approval)

Royalties 3 % for TDF and 5% for the others, 0% pediatric formulations

Paediatric formulations: royalties waived for any paediatric formulations developed by licensee; allows for paediatric formulations to be made available outside Territory via licence to Gilead distributors, with appropriate compensation to licensee

Waiver of any data exclusivity rights, where applicable

Licensee can pick and choose licences (agreement is not bundled)

Provisions to ensure ability of Sub-licensees to supply countries outside the territory where a compulsory license for export has been issued

One time tech transfer (but with no extra obligation to pay royalty)

Provides for publication of licence agreement

Concerns:Limited to licensees based in India

Sourcing of API

Geographical scope

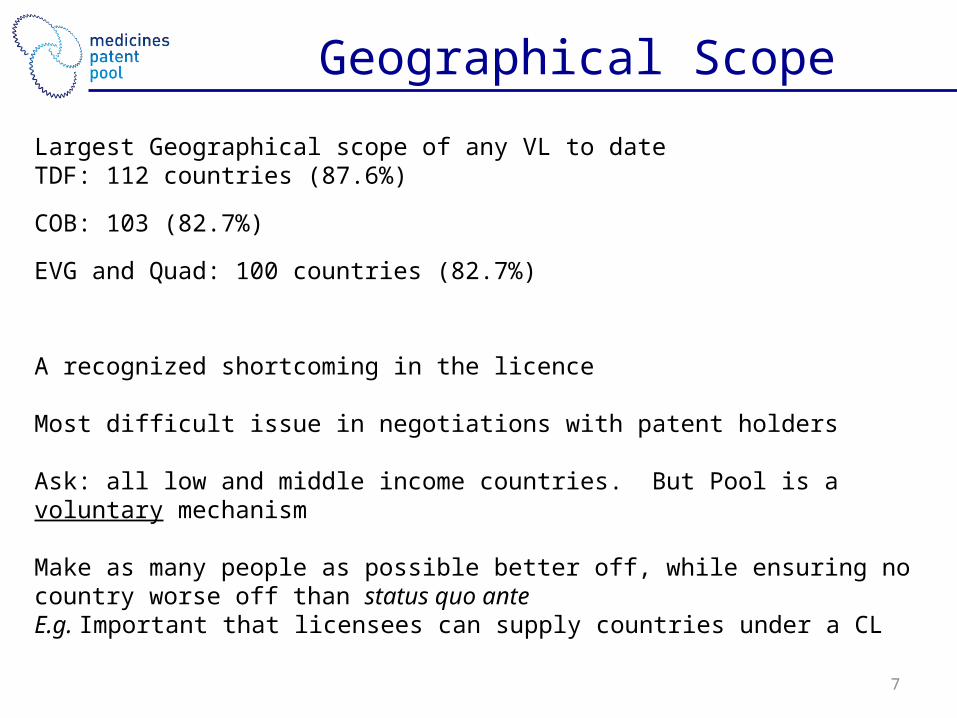

Geographical Scope

Largest Geographical scope of any VL to dateTDF: 112 countries (87.6%)

COB: 103 (82.7%)

EVG and Quad: 100 countries (82.7%)

A recognized shortcoming in the licence

Most difficult issue in negotiations with patent holders

Ask: all low and middle income countries. But Pool is a voluntary mechanism

Make as many people as possible better off, while ensuring no country worse off than status quo anteE.g. Important that licensees can supply countries under a CL

7

8

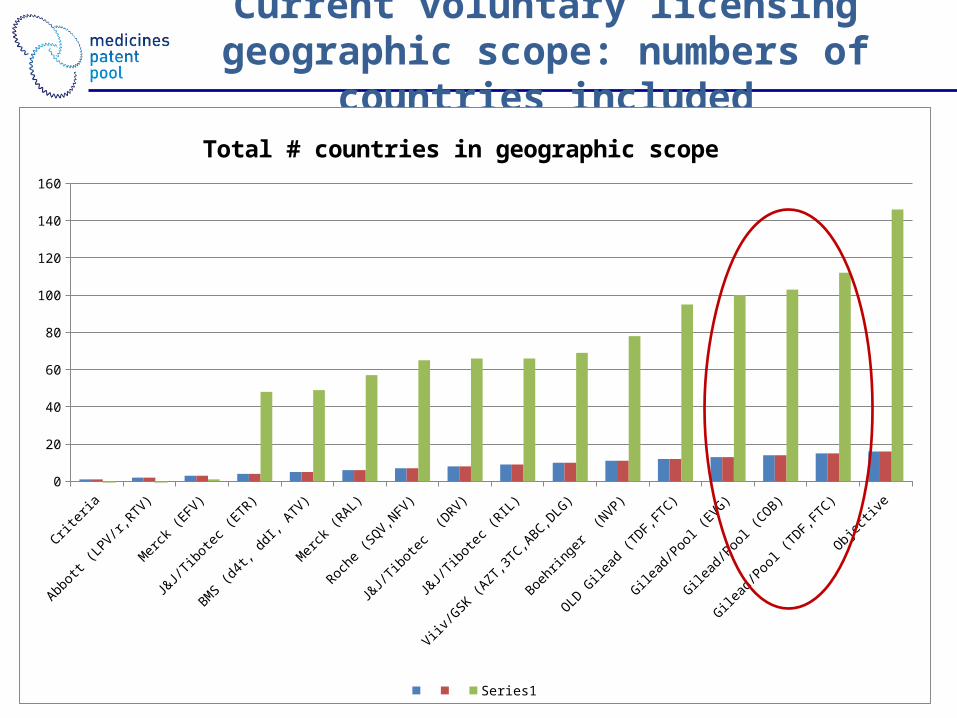

Current voluntary licensing geographic scope: numbers of

countries included

Criter

ia

Abbot

t (LP

V/r,RTV

)

Mer

ck (E

FV)

J&J/T

ibot

ec (E

TR)

BMS

(d4t

, ddI

, ATV

)

Mer

ck (R

AL)

Roche

(SQV,N

FV)

J&J/T

ibot

ec (

DRV)

J&J/T

ibot

ec (R

IL)

Viiv/G

SK (A

ZT,3T

C,ABC,D

LG)

Boehr

inge

r (N

VP)

OLD G

ilead

(TDF,

FTC)

Gilead

/Poo

l (EV

G)

Gilead

/Poo

l (COB)

Gilead

/Poo

l (TD

F,FT

C)

Objec

tive

0

20

40

60

80

100

120

140

160

Total # countries in geographic scope

Series1

9

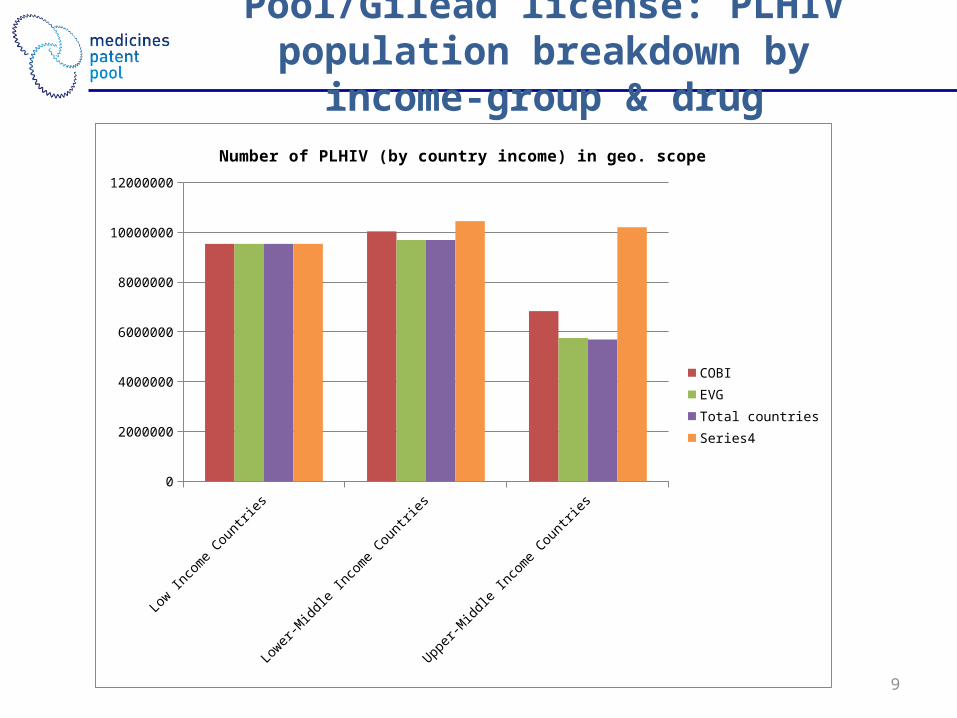

Pool/Gilead license: PLHIV population breakdown by

income-group & drug

Low In

com

e Cou

ntrie

s

Lower

-Mid

dle

Inco

me

Count

ries

Upper

-Mid

dle

Inco

me

Count

ries

0

2000000

4000000

6000000

8000000

10000000

12000000

Number of PLHIV (by country income) in geo. scope

COBIEVGTotal countriesSeries4

Concluding comments

• License with Gilead not a template – agreements with other companies are likely to be different

• we will continue to work on improvements of existing licenses• We benefit from comments we receive and public debate on the

licenses

UNITAID

• UNITAID with others to encourage all HIV patent holders to enter into negotiations with the Pool

• IP goes beyond access -> role in innovation - I+A agenda -> • encourage uptake of licenses • encourage and steer/create the market for the development of

adapted formulations • To develop an i+a agenda beyond the pool• Put challenges for middle income countries on the agenda

THANK YOU

www.medicinespatentpool.org