Embed Size (px)

Citation preview

The Medical and Dental Accounting Services Guide to Service Entities

MAY 2006

Terry McMaster Barrister and Solicitor

Medical and Dental Accounting Services Pty Ltd A.C.N. 076 047 400

144 Church Street Brighton Victoria 3186 Level 5 The Edgecliff Centre

203-233 New South Head Road Edgecliff NSW 2029

www.mcminvestors.com.au

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

2

INDEX 1 Executive summary 2 A brief history of service entities 3 Should you use a service entity? 4 Is there a smarter way? Alternatives structures and strategies 5 How to make sure your service entity arrangements satisfy the ATO’s rules 6 Is there a risk you will be audited? 7 Frequently asked questions An invitation This manual is intended to help doctors, dentists and other health professionals understand how the Australian Taxation Office’s new ruling and guide on service entity arrangements applies to their practices. Please do not hesitate to contact us on [email protected] or 03 9592 9888 should you wish to discuss the materials in this manual or need any specific assistance with your service entity arrangements or any other aspect of your practice. Terry McMaster & Co Pty, Solicitors and Consultants, have prepared hundreds of service agreements for doctors and dentists and can prepare a fresh agreement for you that complies with the new ruling and the guide. The fee is $200 plus GST. You can order a service agreement by e-mailing Terry on [email protected]. We hope this manual is of some interest and assistance to you. Regards Terry McMaster www.mcminvestors.com.au 4 May 2006

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

3

PART 1 EXECUTIVE SUMMARY

On 20 April 2006 the Australian Taxation Office (ie “the ATO’) released Income Tax Ruling TR 2006/2 dated 20 September 2006 “Income Tax: deductibility of service fees paid to associated service entities: Phillips arrangements” (ie “the Ruling”) and the related “Your Service Entity Arrangements” Guide (ie “the Guide”).

The Ruling and the Guide set out the ATO’s views of how the income tax law applies to service entity arrangements. The Ruling and the Guide are not the law. They are just the ATO’s view of the law. However, doctors using service entity arrangements or considering using service entity arrangements are well advised to observe the Ruling and the Guide and how it impacts their arrangements and to only depart from its benchmark rates on specific legal advice, ideally supported by a private ruling from the ATO.

The Guide states that the ATO is generally allowing doctors and other professionals 12 months to 30 April 2007 to review their existing service entity arrangements and to ensure that they comply with the law.

It is unlikely that a medical practice, except for very large medical practices, will be selected for a tax audit either before or after 30 April 2007.

The Guide says that most medical practices will be able to claim a deduction for service fees paid to a related service entity equal to 40% of gross practice income (45% for sole practitioners and rural doctors). We expect that this 40%/45% rule will establish itself as a benchmark rate over time, and will apply to most medical practices unless they have an unusual cost profile. The 40%/45% benchmark is quite low and means that most service entities will not make a significant operating profit and many will make an operating loss. Once could say that the long awaited “safe harbors” have turned out to be very shallow harbors and many practices will run aground.

Doctors should carefully consider the cost and benefit of retaining their service entity arrangements and we expect in many cases they will decide to not continue with these arrangements because:

(i) they are not economic; and/or

(ii) because other practice structures and tax planning strategies achieve are simpler and cheaper to use and achieve better income tax planning results.

In many cases we are recommending that wherever possible doctors evolve their practices to satisfy the ATO’s rules and the income tax law definitions of what comprises a business, and then re-structure their practices to a practice trust format. This is simpler, cheaper and easier to administer and has better income tax planning potential than a service entity arrangement.

In other cases we are recommending clients use superannuation based tax planning and

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

4

investment strategies, in some cases run together with gearing strategies, to achieve better tax planning results than are possible with service entity arrangement.

Many doctors will find that service entities will no longer be economically viable from 30 March 2007 on, once the Ruling and Guide take full operational effect. This is because of the low benchmark service fees prescribed by the ATO. The exceptions will be: (i) many rural doctors, particularly sole practitioners, (ii) metropolitan doctors, particularly sole practitioners, with abnormally high patient

income; (iii) metropolitan doctors, particularly sole practitioners, with abnormally low operating

costs; and/or (iv) practices that receive large practice incentive payments, large pathology rents and

similar payments not directly connected to patient consultations. Our general advice to clients is to cease using service trusts at 30 April 2007, or earlier (30 June 2006 is a convenient date) if another structure or strategy can achieve a similar or better result. We expect that the only clients that will be using service entities after 30 April 2007 will be the clients covered by items (i) to (iv) in the preceding paragraph.

Disclaimer

The comments in this manual are intended to be general comments only and doctors should obtain their own specific legal advice before making any decisions based on the information contained in this manual.

No responsibility is taken for any error or omission unless you are a client of Medical and Dental Accounting Services Pty Ltd or Terry McMaster, barrister and solicitor.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

5

PART 2 A BRIEF HISTORY OF SERVICE ENTITIES Before we consider the specific content and import of the Ruling and the Guide it pays to briefly explain the history of service entities, including what is a service entity, the law of service entities and the ATO’s views of service entities, as well as the reasons for the ATO releasing the Ruling and the Guide in 20 April 2006. What is a "service entity"? A "service entity" is usually a trust that provides administrative services to a professional practice. A service trust can be either a discretionary trust (ie. a family trust), a unit trust or a hybrid trust. The service trust of a solo practice will normally be a discretionary trust (ie the practitioner's family trust) and the service trust of a partnership or an associateship will normally be a unit trust or a hybrid trust, with the units owned by the practitioners' family trusts in accordance with their partnership percentages. In a small number of cases a company or a partnership of trusts or companies provides the administrative services to the professional practice. These are relatively rare because they tend to have either less efficient income tax results or higher set up and running costs. But they are sometimes encountered and therefore the Ruling and the Guide deliberately use the phrase “service entity” rather than the narrower, but more common, phrase “service trust”. The service entity provides the services to the professional practice, whether it is a solo practitioner, a partnership, a practice company or an associateship. These services are provided for a fee, and the fee will include a profit component. It is this profit component that has caused the concerns: is it a reasonable reward for the work actually done, and the risk actually borne, by the service trust? Or is it just a tax device, a ruse designed to shift taxable income away from the hands of the high income practitioner to the hands of lower taxed family members? A brief look at the law The leading case in this area came before the Full Federal Court in 1978. The decision in FCT v Phillips 78 ATC 4361 is commonly known as "Phillips case" and involved a service trust set up some seven years earlier to provide non-professional services to a firm of accountants. This case is reproduced in full at part 5.4 of the Business of Medicine, which can be downloaded at www.mcminvestors.com.au. Previously the accountants performed these tasks. In Phillips’ case the service entity was a unit trust and the units were owned by the partners' family trusts. But there is nothing in Phillips case suggesting the decision is limited to unit trusts and the draft ruling, and the ATO’s earlier pronouncements, show that the Commissioner accepts that Phillips case has general application to all service entity arrangements. The particular services provided by the service entity in Phillips case were:

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

6

(i) secretarial services and general clerical services; (ii) share registry services; (iii) insurance agency; (iv) internal training; (iv) office furniture and plant and equipment; and (vi) finance. The partnership claimed a tax deduction for the amount of the management fees invoiced to it by the service entity. This management fee was calculated on a costs plus basis (for example, labor was charged at cost plus fifty per cent). This, in effect, resulted in an amount of taxable income equal to the mark-up amount being shifted out of the partners' hands into the hands of their family trusts. Generally the partner's family trusts had better tax profiles than the partners. This meant overall less tax was paid than would have been had the service entity not been set up and these management fees not been paid to it. The Commissioner of Taxation rejected the arrangement. He disallowed the deduction for management fees claimed by the partnership. The partnership objected and, eventually, the matter ended up in court. Once there, Phillips, one of the partners, stated the setting up of the service entity was intended to: (i) protect valuable assets from litigation; (ii) increase the amount of valuable assets owned by the partners' families; (iii) reduce the risk of death duties eroding partnership wealth; and (iv) reduce income tax. The Full Federal Court's view The Full Federal Court accepted the re-structure for income tax purposes and allowed the partnership a deduction for the management fees paid. The court thought the amounts paid to the service entity by the partnership were commercially realistic and were not excessive. It found the main reason the partnership incurred the management fee was to secure the management services provided to it by the service entity. This meant that the management fees were deductible losses and outgoings under general principles and that the anti-tax avoidance rules of the day (ie the old section 260) did not apply to the arrangement.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

7

The ATO’s view The ATO accepted the Full Federal Court’s decision in Phillips case. In paragraphs 4 and 5 of Income Tax Ruling IT 276 the ATO writes: “…Given the view of the facts which the court adopted…that is, a re-arrangement of business affairs for commercial reasons and realistic charges not in excess of commercial rates, the decision to allow the deduction must be accepted as reasonable… The decision indicates the need for a close examination of all relevant facts before deductions are allowed in cases of this kind…” There are numerous other examples of the ATO accepting the general concept of a service trust. And of course the Ruling and the Guide accept the general concept of a service trust. The area of contention is, and always has been, what is a commercial rate? Newspaper reports indicate that in around 1999 a number of very large accounting practices and legal practices set up service entity arrangements involving grossly excessive charges and that were otherwise not commercially justified. The ATO detected these arrangements during other audit activity (which, interestingly, involved aggressive tax schemes) and this led to a general review of service entities by the ATO. The review rasied a lot of concerns, particularly about what the big end of town was up to with its service trust arrangements. These concerns were raised publicly in the Commissioner of Taxation’s Annual Report to Parliament for 2000 and 2001 and subsequent speeches by the Commissioner and other senior ATO staff. These concerns were raised in a number of other forums. For example, in 2002 speaking at the American Chamber of Commerce presentation the then Commissioner of Taxation, Mr Michael Carmody, said that the ATO accepted Phillips Case but was concerned about a number of specific cases where: (i) the service entity was not a fixed unit trust; (ii) the service entity did not have substantial assets; (iii) there were substantial profits in the service trust that were a large proportion of the

total profit of the practice. The general review culminated in the release of a draft ruling and related booklet on 4 May 2005. Our thoughts on this draft ruling were set out in a special edition of our Dollar Notes newsletter dated 8 May 2006. This Dollar Notes newsletter can be download from our website www.mcminvestors.com.au or it can be accessed directly via this link: http://www.mcminvestors.com.au/docs/DollarNotes8May2005_Special_EditionATO_Draft_Ruling_on.pdf.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

8

In this Dollar Notes newsletter we wrote: “The ATO’s bottom line is quite clear: service entities are OK. They are not dead. And solo practitioners can use them still. The ATO accepts service trusts. But, like most ATO acceptances, there are provisos, and the ATO says here the provisos boil down to the service entity arrangements being real, the service fees being commercial and the whole arrangement not being something done just to get a tax benefit. This is actually nothing new. It’s what the ATO has been saying for years and the court cases are pretty much on their side.

More specifically, on 4 May 2005 the, Tax Commissioner Michael Carmody said: "The draft ruling reflects our long-standing view that service arrangements are acceptable provided they are entered into for commercial reasons and at commercially realistic rates." And as Anne Lampe wrote in the Sydney Morning Herald on 5 May 2005:

“The draft sets out the features of such arrangements which involve a primary business or partnership, a separate trust entity owned or controlled by the taxpayer or associates, and an agreement entered into between the parties whereby the business pays certain fees and charges to the service entity in return for the provision of services. Typically the fees and charges are calculated on a cost-plus basis, giving rise to profits for the service company.

“The draft ruling makes it clear that the Tax Office will not attack genuine arrangements, but will come down on cases where the service company overcharges, where fees set are arbitrary and bear no relation to the value of the services provided, where the service fees are disproportionate to the benefits conferred, and where there is no clear separation between the service entity's business activities and those of the business which is paying for those services.”

The release of the draft ruling and associated booklet was followed by a consultative process with both the general tax profession industry groups, such as the Taxation Institute of Australia, and the major professional representative bodies, such as the AMA. It is fair to say that this consultative process accepted the ATO’s position on service entities in principal, but did not accept some of the detail, particularly its conservative view of what comprises an arms length charge and a reasonable mark up on costs.

Income Tax Ruling TR 2006/2 dated 20 September 2006 “Income Tax: deductibility of service fees paid to associated service entities: Phillips arrangements” and the “Your Service Entity Arrangements” Guide

The consultative process culminated with the release of Income Tax Ruling TR 2006/2 dated 20 September 2006 “Income Tax: deductibility of service fees paid to associated service entities: Phillips arrangements” (ie “the Ruling”) and the “Your Service Entity Arrangements” Guide on 20 April 2006 (ie “the Guide”). The Ruling and the Guide can be downloaded at the ATO’s website www.ato.gov.au and can be accessed at the

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

9

following direct links:

http://law.ato.gov.au/atolaw/view.htm?docid=TXR/TR20062/NAT/ATO/00001

http://www.ato.gov.au/content/downloads/N13086-04-2006.pdf

How does the Ruling and the Guide change things for doctors? The ATO’s current view of service entities is best summed up in the introductory pages of the Guide, where it says: “If you have a conventional service arrangement where your payments are correctly calculated and the services are reasonably connected to the conduct of your business, then the presumption will be that your service fees and charges are a real and genuine cost of your business and are deductible in full. If your payments are grossly excessive or the services are not reasonably connected to the conduct of your business, then the purpose, and the deductibility, of some or all of your service fees is open to question. We may ask you to explain your entitlement to the deduction claimed. If we are not satisfied with your explanation we may disallow some or all of your deduction.” Most tax commentators would accept these two paragraphs as a fair and reasonable summary of the law relating to service trusts and a reasonable position for the person responsible for administering the law, ie the Commissioner of Taxation, and the Australian Taxation Office, to adopt. We certainly have no problem with this summary and position. The difficulty, as usual, is in the detail. In the Guide the ATO sets out its views of what is and what is not a commercial service entity arrangement. Numerous examples are provided of what is acceptable to the ATO and what is not acceptable to the ATO. The Guide provides at page 24 and 25 in parts 15 and 16 two examples that relate directly and specifically to doctors (and presumably indirectly to dentists and other health professionals). These examples and the ATO’s comments are reproduced at appendix 2A. In summary, the ATO says that for GPs a commercial service fee will generally be no more than 40% of gross practice fees and 45% of gross practice fees for sole practitioners and rural practitioners. The ATO says that the higher service fee for sole practitioners and rural practitioner is justified because they have higher costs experience. We believe that, as a practical matter, the 40%/45% benchmark is likely to become a de-facto rule for GPs and that similar benchmarks will emerge for doctors other than GPs and other health professionals as time goes by. The difficulty is that the 40%/45% benchmarks is too low and means that in most cases it will not be economic to run a service entity. This raises many questions for doctors and these are discussed in the following sections of this manual.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

10

PART 3 SHOULD YOU USE A SERVICE ENTITY? In a nutshell We believe the Ruling and the Guide will increase the tendency for practices to abandon service entity structures in favor of other structures and strategies. This is because for many doctors service entities will no longer be economically viable, due to the low benchmark service fees prescribed by the ATO. The exceptions will be: (v) many rural doctors, particularly sole practitioners, (vi) metropolitan doctors, particularly sole practitioners, with abnormally high patient

income; (vii) metropolitan doctors, particularly sole practitioners, with abnormally low operating

costs; and/or (viii) practices that receive large practice incentive payments, large pathology rents and

similar payments not directly connected to patient consultations. Our general advice to clients is to cease using service trusts at 30 April 2007, or earlier (30 June 2006 is a convenient date) if another structure or strategy can achieve a similar or better result. We expect that the only clients that will be using service entities after 30 April 2007 will be the clients covered by items (i) to (iv) in the preceding paragraph. Doctors whose service trusts do not provide a significant amount of services, such as GPs working in larger practices or anesthetists, in particular should stop using their service entities now, or in any event by say 30 June 2006 unless they have specific legal advice to a private ATO ruling to the contrary. Introduction This part of the manual is intended to help doctors decide what they use a service entity before 30 April 2007. Please do not hesitate to contact Terry McMaster on [email protected] or 03 9592 9888 should you wish to discuss your practice’s specific circumstances or need any other assistance in this area. Should you use a service entity? We believe the Ruling and the Guide will significant reduce the incidence of service entities within the medical profession and most other types of professional practices. The incidence of service entities was in fact decreasing even before the draft ruling and booklet were released in May 2005. This is because the cost of setting up and running a

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

11

service trust, compared to the asset protection and tax planning advantages it creates, was often not comparable with the cost of setting up and running alternative structures and strategies. Many practices are concluding that they do not need a service entity and alternative legal structures and strategies are cheaper and easier to set up and run and may produce a better tax result. These alternative legal structures and strategies are discussed in Part 4 of this manual. They include: (i) practice trusts, practice companies and partnerships of trusts to run medical

practices where the practice is a business; (ii) large deductible superannuation strategies; (iii) gearing strategies; (iv) employment of related persons; and (v) various other structures and strategies depending on the particular profile and

circumstances of the individual practice. The relatively low 40%/45% benchmark set out in the Guide The decreasing incidence of service entities will be sped up by the relatively low benchmarks set for medical practices in the Guide. The bottom line is that after 30 April 2007 many doctors will find that service trusts are not justified. The benchmark rates for medical practices set out in the Guide are low and mean that most medical practice service entities will end up making an operating loss, or at best a small profit that does not justify the risk and effort incurred in running a service entity. General practice costs, on average, tend to be between 40% and 50% of total fee income (but can fall as low as 30% for larger practices due to economies of scale). However, the Guide prescribes a management fee of no more than 40% of the practice’s patient fees, and 45% of the practice’s fees in the case of sole practitioners and rural doctors. This means that the service entity’s income will probably be less than its costs and the service entity will make a loss. Even if the service entity’s costs are, say, just 35% of the practice’s patient fees, the net income of just 5% of practice fees (ie 40% less 35%) means that the time and trouble of setting up and running a practice entity will probably not be worth it. This is particularly once the extra costs of running a service entity, including extra management time, extra BAS and GST compliance costs and extra external accounting fees are considered. The Guide prescribes 40% as a commercially acceptable management fee (45% for sole practitioners and for rural doctors) is on the grounds that arms length providers of practice management services charge this amount.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

12

The low benchmark of 40%/45% means that most practices will not be interested in running service entities except for: (i) many rural doctors, who typically have higher patient fees and lower costs than

metropolitan doctor; (ii) metropolitan doctors, particularly sole practitioners, with abnormally high gross

income; and/or (iv) metropolitan doctors, particularly sole practitioners, with abnormally low

operating costs. Some worked examples Appendix 3A sets out some worked examples based on a typical general practice. The worked examples indicate that gross practice fees approaching $350,000 are needed to make a service entity arrangement financially viable. This is a well above average level of fee income and it means that most GPs with lower billings will find that a service entity is not worth the bother of setting up and running each year. This is particularly the case when one remembers that it is highly probable that alternative legal structures and tax planning strategies probably provide better results anyway, making the tax benefits of a service entity arrangement redundant. Complimentary ready reckoner If you would like to modify the original Excell spread sheet used for appendix 3A for use in your own practice e-mail [email protected] and we will send you a copy. Rural doctors: a special case The 45% for rural GPs is interesting. The Guide says that here service fees of up to 45% of gross practice fees “would not warrant further examination”. This means that rural The higher percentage is justified, the Guide says, by the higher costs incurred in rural practice. I do not think this is correct. Rural practice costs tend to be lower than metropolitan practice costs, not higher. Compare rents in Toorak with rents in Dubbo. And compare labor costs in Double Bay with labor costs in Woomera. And bear in mind that in the more remote locations the doctors costs may be heavily subsidized by the local community, particularly through low or no rent accommodation. This higher percentage (ie the 45%), coupled with the much higher gross practice fees and the much lower practice costs typical of rural practice, will make service entities more attractive for rural GPs than they are for metropolitan GPs.

GPs with abnormally high incomes and/or abnormally low costs: a special case More generally GPs with abnormally high incomes and/or abnormally low costs, irrespective of whether they are in a rural area or a metropolitan area, may find that a service trust still makes sense, particularly if they are sole practitioners and can use the ATO higher benchmark rate of 45%. In fact in some cases it may make more sense than it does now, at least from an income tax planning point of view. For example, we know of two separate GP sole practices with patient billings of more than $500,000 a year each and costs of no more than about $100,000. Each of these practices can, under the Guide’s 40%/45% benchmark, in effect move $125,000 of profit into their service trust. This $125,000 is calculated as follows: Practice management fee in service entity (45% of $500,000) $225,000 Less third party costs $100,000 Net income in service entity $125,000 Each doctor needs to consider his or her own income and costs profile. To help doctors do this we have prepared a table to help calculate the benefit of using a service trust. This table is reproduced at appendix 7A, and can be customized to suit your particular practice. If you would like an automated Excel spreadsheet version of this appendix please e-mail me at [email protected]. GPs with high practice incentive payments The Practice Incentive Payments Program (“PIPP”) may make the creation or maintenance of a service entity worth the effort. This is because there are strong arguments that the PIP can be derived by the service entity. And in fact a large percentage of all PIPs are derived by service entities. This issue was discussed in an Australian Doctor article published in early 2004 and a copy of this article is attached as appendix 3B. It is quite possible that creating or maintaining a service entity in order to derive the PIP and distribute this income to lower tax rate family members makes sense for many GPs. The extent of a practice’s PIP and whether they can be treated as derived by the service entity should be considered when determining whether or not to create or maintain a service entity. PIP is considered in the sample calculations set out in appendix 7A. GPs with pathology rents and other “non-practice” income The comments under “GPs with high practice incentive payments too” apply equally to practices with significant pathology rents. It is not uncommon for these rents to be as high as $40,000 per year. In fact these comments apply equally whenever a practice receives significant income other than patient fees that can be derived by the service

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

14

entity. The extent of a practice’s pathology rents and other “non-practice” income should be considered when determining whether or not to create or maintain a service entity. Pathology rents are considered in the table reproduced at appendix 7A. The same logic applies to other income that is not directly connected to patient services. What about larger practices that provide services to other GPs? Many doctors own practices and, apart from practicing at the site themselves, also provide services to other doctors who practice at the site. These services usually include everything the other doctor needs to practice at the site other than car costs, training costs, insurances and memberships. The net income derived from providing these services can be significant, and in some cases can be greater than the income derived from the owner doctors own efforts. In these circumstances the continued use of a service entity may make sense. However, we expect that such practices will usually be better off changing to a practice trust or company based model, and this is discussed in more detail in Part 4 of this manual. Where does the 40%/45% rule come from? The Guide says that the ATO surveyed the rates charged by various arms length service providers and that these vary between 35% and 50%, depending on factors like the location of the practice, cost structures and the relative bargaining position of the parties. It appears that the ATO looked at the range of fees charged to arms length doctors by independent service providers, and concluded that 40% and 45% were appropriate industry benchmarks. The Guide presents an example of a three GP practice using a service entity. This example and the ATO’s comment on it bear reproducing in full: “MEDICAL PRACTICE ARRANGEMENTS 15 A practice management arrangement where the payments are correctly calculated

and reasonably connected to the business. Three general practitioners (GPs) form a service entity to render a comprehensive suite of services to conduct a medical practice. The GPs provide their medical services through the practice. The service entity employs a practice manager, reception staff, clerical support staff and a nurse. It conducts the entire business of the medical practice including premises, equipment, medical and office systems ad supplies, patient records, general administration, marketing, legal and regulatory obligations (excluding the professional obligations personal to the practitioners) and incurs all the expenses involved in running the practice. The medical practitioners focus solely on providing medical services to patients. Each practitioner pays a service fee that results in the service entity earning 40% of each practitioner’s gross fees from patient consultations

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

15

and procedures and this is paid on the same basis by each of the doctors out of their separate fees. Arm’s length practice management arrangements used in the medical profession are broadly similar to this arrangement. In these circumstance it is reasonable to conclude that the benefits provided by the practice management company to the doctors us reasonably connected to the business carried on by each doctor, as it clearly supports the doctors’ ability to provide medical services to patients and to earn income from clinical activities. Similar commercial arrangements providing a comprehensive suite of services to GPs exist in the medical profession by practice management companies. Our examination of independent practice management arrangements show that service fees of up to 40% of gross practice fees are likely to be appropriate regardless of the context and circumstances of a particular arrangement. As the fees in this arrangement are set at 40% we consider that the risk that the fees claimed are not deductible is low and any further examination of the fee level is not appropriate. This practice would be at low risk of a tax audit.” Can you use a rate other than 40%/45%? A practice can use a rate above 40% (45% for sole practitioners or rural doctors). However, if it does so it must be able to explain why it is using a higher rate, and document its reasons for doing so. The best explanations will include detailed documentation and refer to location and costs structures. Be careful about using a higher rate as the Guide warns that “the risk of being audited will increase according to the degree of divergence above 40%”. Make sure you have your facts right and make sure you can prove why a rate greater than 40% or 45% is appropriate to your practice. Our advice is if you believe a rate greater than 40% then you should seek a private ruling from the ATO. Your private ruling request should set out the reasons why the higher rate represents a commercial fee. The desire to create a profit in the service entity will not be an acceptable reason. The ruling request should focus on comparable practices and arms length amounts, and explain why the comparator of 40% is not appropriate to your practice. Perhaps the strongest argument will be that your service entity does more for you, in terms of quality and quantity, than the benchmark service providers do for their doctors. Specifying minimum service standards, that are greater than the benchmark service providers average standards in the service agreement will help your case here, since the follow on from the maxim “you get what you pay for” is that “you have to pay for what you get”. And if you get a higher level service then it makes sense that you have to pay more for it. On page 4 of the Guide the ATO sets out a number of circumstances that may be used to show that a higher rate is appropriate. These include: (i) industry specific comparable data;

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

16

(ii) the specialized or highly skilled nature of the service provided; (iii) the extent to which services are provided in excess of comparable third part

arrangements; (iv) the economic contribution to profits of the main business that is attributable to the

activities of the service entity (the activities of on-hired staff are mot activities of the service entity); and

(v) the level of business risk associated with the activities of the service entity and the

nature of the service model used. Be careful of just pointing to a nearby corporate and saying “it charges its doctors 50%, and so will I”. The nearby corporate is unlikely to be a comparable practice. A comparable practice is one with a similar location, size, facilities, support staff and clinical staff as your practice. And it is possible that such practices are charging doctors as little as 30%. We know of one practice which charges doctors just 25%. And the corporate do not always charge 50%. This rate is usually reserved for doctors who have sold their practices and the higher service fee is connected to the sale price calculations. In some cases the large corporates charge other doctors as little as 35%. The 40%/45% rule is not cast in stone. It is not an absolute and unbreakable rule. If a management fee of 40% or 45% means the service entity arrangement is at low risk of an audit then it is unlikely that a management fee that is one or two per cent higher means there is a significantly higher risk of audit. One can contemplate circumstances where a much higher management fee is appropriate, for example, where the particular service entity does a lot more for the practice than the arms length providers do for their clients. But as a general proposition one can expect that the further one moves beyond the 40%/45% benchmark the greater one’s chances of a tax audit, and the less likely it will be that the actual percentage will be accepted as an arms length charge should a court look at the arrangement. As a practical matter we expect that the 40%/45% benchmark will quickly become a de-facto rule. Certainly practices that depart from it should have good reasons for doing so and should be able to objectively demonstrate that the higher charge is a commercially reasonable amount and is supported by independent evidence. Practices that charge significantly more than the 40%/45% can expect to be, if not audited, the object of enquiry from the ATO. If the practice’s responses are not adequate it can expect the allowable deductible service fee to be reduced to 40%/45%, or some other investigative action from the ATO.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

17

What about medical practices other than general practices? The Guide does not specifically deal with medical practices other than general practices, ie, specialists, and it is not clear whether the examples and 40%/45% benchmark put forward in parts 15 and 16 of the Guide are intended to apply to specialists. Specialists with a practice profile similar to GPs, such as pediatricians, will probably subject to the 40%/45% rule. This is because from an income and costs point of view the pediatric practices tend to be similar to general practices, although in some cases patient billings can be much higher. Patient billings tend to be about the same where bulk billing is involved, and many pediatric practices do bulk bill. On one hand parts 15 and 16 of the Guide refer generally to “medical practitioners”, “the medical profession” and “medical practice arrangements”, which indicates that the 40%/45% benchmark is intended to apply to specialists. But on the other hand the specific examples refer explicitly to GPs and the general commentary includes the words: “…it is important to consider any relevant differences between your service arrangement and those between independent enterprises. It is important to compare like with like.” and this suggest that a specialist practice should modify the 40%/45% rule if it does not have an income and a costs profile similar to a general practice. These specialists will not be able to use the 40%/45% benchmark and may be forced back to general principles. The base proposition is simple: the allowable deductible service fee is limited to what would be charged for providing similar services by an arms length supplier of those services. In tax law the burden of proof is on the taxpayer, not the ATO. This means that as a practical matter the specialist must be able to prove that the service fee does not exceed the amount what would be charged for providing similar services by an arms length supplier. This means, for example, that: (i) a recently qualified orthopedic surgeon will be able to claim a deduction for service

fees paid to a service entity up to the amount that would have been charged by an un-related service entity controlled by a group of older orthopedic surgeons located in a nearby public hospital. This assumes that the actual services supplied are comparable. If more services are provided by the service entity the deductible service fee will be greater, and if less services are provided by the service entity the deductible service fee will be less;

(ii) an obstetrician who was previously charged a service fee equal to 50% of her

billings by an arms length service provider, and this had been the amount charged to previous generations of obstetricians practicing at the same site, will have strong grounds for claiming a deduction for a service fee of 50% paid to her own service entity once she sets up her own shop down the road; and

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

18

(iii) an older psychiatrist whose service entity provides administrative services to two

younger psychiatrists for a fee equal to 35% of their gross billings will be able to claim a deduction for a service fee equal to 35% of his own billings paid to the same service entity. This amount may even be able to be increased if it can be shown that for whatever reason the service entity does more work for the older psychiatrist than it does for the two younger psychiatrists.

We expect that either the ATO will confirm that the 40%/45% benchmark rate extends to specialists or alternative benchmarks for specialists will emerge over time. In the meanwhile specialists should use the 40%/45% benchmark rates, unless they are clearly inappropriate given the cost structure of their practice, but keep an eye on things, particularly up to 30 April 2007, and be prepared to modify the service fee charges if the ATO indicates that these rates do not apply to them. What about dentists and other health professionals? The Guide does not refer to dentists or other health professionals such as psychologists and chiropractors. However, the Guide does provide some indirect guidance on what rates could be regarded as benchmark rates. It does this by recognizing that in the medical profession it is normal for service entities to provide “a complete suite of services” in return for a single global fee is charged rather than a set of individual services, such as a debt collection, computer hire and staff for which individual service fees are charged. It follows that dentists and other health professionals who also receive “a complete suite of services” from a service provider should be looking at what other dentists are charging. As a practical matter this may be an amount of, say, 65% of billings, less laboratory costs. But this will vary depending on factors such as the location of the practice, the total dentist’s total billings (ie level of activity), cost structures and the relative bargaining position of the dentist and the service entity. We expect that established benchmark rates for dentists and other health professionals will emerge over time. There is every prospect that these benchmark rates will be published by either or both the ATO and the relevant professional body, based on discussions and representations from the professional bodies. But until then the emphasis dentists and other health professional should make sure that they establish and document a comparable arms length transaction as a base for their service entity fees. Is the ATO bound by the 40%/45% benchmark? The ATO is not bound by the 40%/45% benchmark. In fact the ATO carefully limits its comments about the first practice example in Part 16 to a statement that: “This practice would be at low risk of a tax audit.” It does not say that the practice will not be audited and it does not say that if the practice

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

19

is audited the ATO will automatically accept that 40%/45% of gross practice income is a commercially verifiable, and hence deductible, amount. In strictness the practice will still need to show that the fee is commercially verifiable and is in line with the principles established in Phillips Case. However, day to day tax administration is often different from strict theory and as a practical matter doctors using the 40%/45% benchmark may expect that it will be accepted by the ATO. This means that they will not be required to otherwise prove the commerciality of the service fee charges, unless the practice has a unusual cost structure. If for any reason your practice has an unusual cost structure you should get specific legal advice on this issue. Are there any practice types that are particularly likely to not be covered by the 40%/45% benchmark? Yes. For example, we expect that GPs who practice at sites owned by other doctors (“the host practice”) will not be able to use the 40%/45% benchmark. This is because the bulk of their costs (other than car costs, training costs, insurances and memberships) are in effect covered by the management fee paid to the host practice. These GPs could consider using a service entity to provide their car costs, training costs, insurances and memberships, and to liaise with the host practice. These services could be marked up using the other methods described in the Guide, specifically: (i) comparable market prices (of which the 40%/45% benchmark is one example); (ii) comparable profits; (iii) net mark up on costs; and (iv) gross mark up on costs. (Each of these methods can be a sensible approach to determining “what is an arms length price for a transaction between two related parties?” and can be used for medical practice service trust arrangements. Each of them could be the object of many paragraphs of discussion but instead interested readers are referred to page 7 and 8 of the Guide.) However, in the case of GPs practising at sites owned by other doctors the Guide makes it clear that the ATO will only accept relatively low mark ups for these items. As a practical matter, and as explained above, we expect this means most GPs who practice at host practices and who do not have significant other costs will not use service entities. These GPs should stop using service entities now (ie March 2006) or in any event by 30 June 2006.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

20

What about anesthetists? Anesthetists are in a similar position. Anesthetists usually have low practice costs compared to other doctors due to the itinerant nature of their work. Separate sessions at up to five or more different locations each week are not uncommon. Most anesthetists do not have significant practice costs other than car costs, training costs, insurances and memberships, and in particular do not pay rent or significant wages (some may employ a part time bookkeeper or administrator). Once again, the Guide makes it clear that the ATO will only accept relatively low mark ups for these items. As a practical matter, we expect this means most anesthetists will not use service entities. These GPs should stop using service entities now (ie March 2006) or in any event by 30 June 2006. There is no rule that doctors in these circumstances cannot use service entities. The law applies to them as much as it applies to any other doctor. But it is unlikely that the ATO will accept mark ups of significant size to justify the time and cost of setting up and running a service entity.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

21

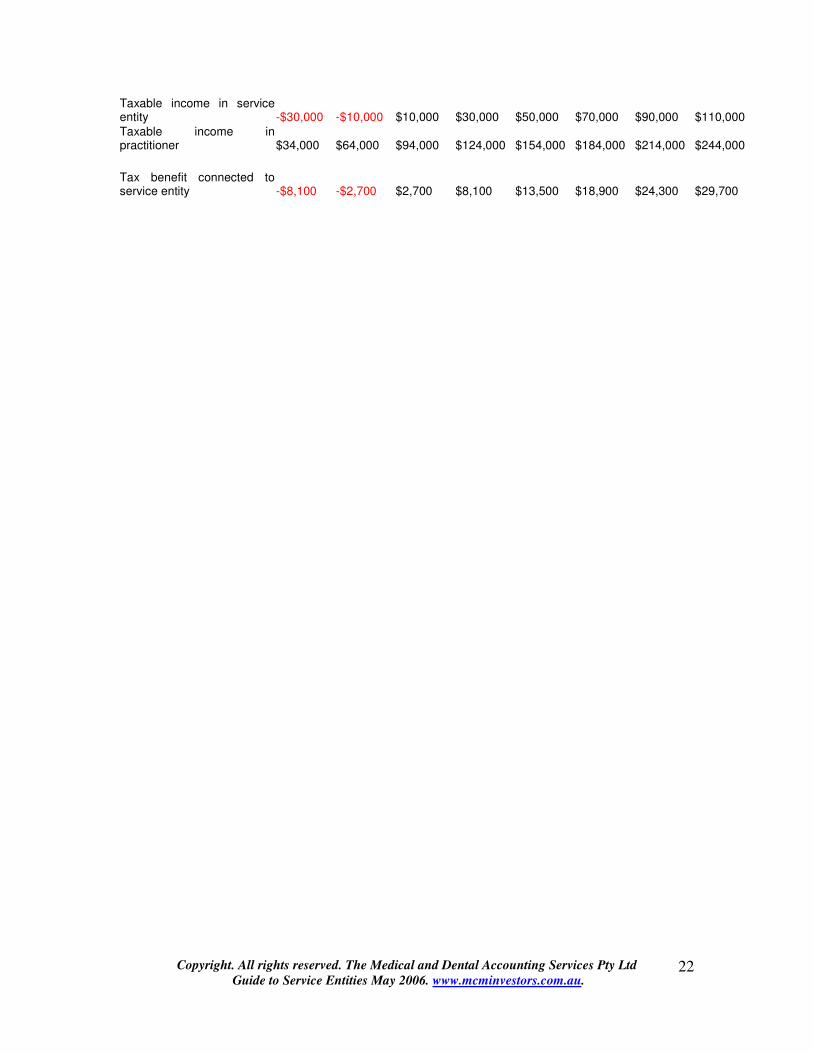

APPENDIX 3A: SERVICE FEE READY RECKONER Model Showing Service Entity Decision Tree Acceptable service fee % 40% PIP and similar payments $10,000 Marginal tax rate practitioner 47% Average tax rate 20% Elective personal deductible costs : Professional indemnity insurances $10,000 Training costs $10,000 Professional memberships $10,000 Overseas travel and training $1,000 Deductible superannuation contributions $20,000 Deductible car costs $15,000 Other special costs $1,000 Patient fees $250,000 $300,000 $350,000 $400,000 $450,000 $500,000 $550,000 PIP and pathology rents $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 Total income $210,000 $260,000 $310,000 $360,000 $410,000 $460,000 $510,000 $560,000 Costs Personal deductible costs Professional indemnity insurances $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 Training costs $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 Professional memberships $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 Overseas travel and training $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 Deductible superannuation contributions $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 Car costs $25,000 $25,000 $25,000 $25,000 $25,000 $25,000 $25,000 $25,000 Other special costs $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $1,000 $86,000 $86,000 $86,000 $86,000 $86,000 $86,000 $86,000 $86,000 Practice costs : Rent $25,000 $25,000 $25,000 $25,000 $25,000 $25,000 $25,000 $25,000 Salaries:unrelated persons $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 $40,000 Salaries:related persons $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 Depreciation $15,000 $15,000 $15,000 $15,000 $15,000 $15,000 $15,000 $15,000 Other $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $120,000 $120,000 $120,000 $120,000 $120,000 $120,000 $120,000 $120,000 Taxable income from entire practice $4,000 $54,000 $104,000 $154,000 $204,000 $254,000 $304,000 $354,000 Practice costs as a percentage of billings 60% 48% 40% 34% 30% 27% 24% 22%

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

22

Taxable income in service entity -$30,000 -$10,000 $10,000 $30,000 $50,000 $70,000 $90,000 $110,000 Taxable income in practitioner $34,000 $64,000 $94,000 $124,000 $154,000 $184,000 $214,000 $244,000 Tax benefit connected to service entity -$8,100 -$2,700 $2,700 $8,100 $13,500 $18,900 $24,300 $29,700

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

23

APPENDIX 3B: AUSTRALIAN DOCTOR ARTICLE ON PRACTICE INCENTIVE PAYMENTS

Dollar Notes

Who gives a PIPP?

The Practice Incentive Program (“the PIP”) has been has been around for many years and is accepted as part of the financial make up of most general practices. Most GPs are familiar with its operation, and those who are not come become familiar with it by visiting the HIC’s website and similar sources of information.

This article looks at the income tax implications of the PIP payments (“the PIPP”), and in particular, who derives it for income tax purposes?

The two contenders are usually the GPs who work in the practice and the service entity that provides the necessary support and infrastructure to the GPs who work in the practice. The fact that the GPs have agreed with the service entity that one or the other can keep the PIPP cash does not determine who has primarily derived it for income tax purposes. The question of who derives income will always be a question of fact, and no one fact will be determinative; rather, the correct answer will reflect the weight of each fact, and may even differ from practice to practice.

The question of who derives the PIPP for income tax purposes does not seem to be considered by the HIC, or any of its advising committees. The question is an interesting one, because usually less tax is paid if the service entity derives the income. At the tax planning level we advise GPs to treat as much income as possible as belonging to the service trust, provided this is in accordance with the law. This usually means less tax is paid. Treating the PIPP as the service trust’s income will be in accordance with the law if the facts show that the PIPP relates to the services provided to the GPs by the service trust rather than the services provided to patients by the GPs. This raises three questions: “What is the PIPP? How is it calculated? And who is it paid to?”

Space limits forbid a detailed review of the answers to these three questions. In summary, they show that usually the better view will be that the PIPP are connected more to the services provided by the service trust, ie, the overall infrastructure required by the GPs to practice medicine, than they are to the services provided by the GPs themselves, ie, the clinical services to patients. For example, information technology and the provision of data to the Federal Government are provided by the service trust and after hours care is facilitated by the service trust. Practice size, as measured by “whole patient equivalents” or “WPES”, is not a function of any individual GP’s efforts.

The PIPP philosophy suggests the PIPP is primarily derived by the service trust for tax purposes. This philosophy seeks a financial supplement to the traditional emphasis on patient payments and Medicare rebates for clinical services to patients. Achieving and maintaining accreditation status, the replacement of plant and equipment and the up-grading of the practice’s facilities feature here.

Industry practice suggests the service trust derives the PIPP. Most service agreements are silent on the issue, and if it is mentioned at all will say that the GP will be paid some of it, pre-supposing that it is the service trust’s income in the first place. Most PIPPs are paid to service trusts or similar entities, and the HIC literature, while not being specific, clearly distinguishes between the practice as an entity and the GPs engaged in the practice, and allows payments to the directed to the practice if this is the preferred option.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

24

APPENDIX 3C EXTRACT FROM THE GUIDE ON MEDICAL PRACTICES “MEDICAL PRACTICE ARRANGEMENTS 16 A practice management arrangement where the payments are correctly calculated and reasonably

connected to the business. Three general practitioners (GPs) form a service entity to render a comprehensive suite of services to conduct a medical practice. The GPs provide their medical services through the practice. The service entity employs a practice manager, reception staff, clerical support staff and a nurse. It conducts the entire business of the medical practice including premises, equipment, medical and office systems ad supplies, patient records, general administration, marketing, legal and regulatory obligations (excluding the professional obligations personal to the practitioners) and incurs all the expenses involved in running the practice. The medical practitioners focus solely on providing medical services to patients. Each practitioner pays a service fee that results in the service entity earning 40% of each practitioner’s gross fees from patient consultations and procedures and this is paid on the same basis by each of the doctors out of their separate fees. Arm’s length practice management arrangements used in the medical profession are broadly similar to this arrangement. In these circumstance it is reasonable to conclude that the benefits provided by the practice management company to the doctors us reasonably connected to the business carried on by each doctor, as it clearly supports the doctors’ ability to provide medical services to patients and to earn income from clinical activities. Similar commercial arrangements providing a comprehensive suite of services to GPs exist in the medical profession by practice management companies. Our examination of independent practice management arrangements show that service fees of up to 40% of gross practice fees are likely to be appropriate regardless of the context and circumstances of a particular arrangement. As the fees in this arrangement are set at 40% we consider that the risk that the fees claimed are not deductible is low and any further examination of the fee level is not appropriate. This practice would be at low risk of a tax audit.” As discussed in Step 2 on Page 9, when using this comparable market prices approach it is important to consider any relevant differences between your service arrangement and those between independent enterprises. It is important to compare like with like. For the purposes of considering the commerciality of the service fees paid to the service entity, the nature of the relationship between the practitioners is not considered material (for example, whether they practice as partners or associates). The service arrangements in the medical profession, which provide a complete suite of services for conducting the medical practice, are significantly different to conventional service arrangements where particular services are provided to a professional service. A service arrangement where a fee split of this kind is comparable involves the service entity effectively conducting the business of the medical practice. The service entity takes responsibility for all the expenses of the practice while the doctor is responsible for meeting the costs of indemnity, personal work related transport, and costs incurred in meeting their professional obligations. These include training and education, medical registration and membership of professional bodies. The arm’s length practice management arrangements involve the practice company conducting the business of the medical practice. While these arrangements involve a different business model, we consider that they are broadly comparable to those types of arrangements in the medical profession where a complete suite of services is provided for the purpose of considering the commerciality of the fees charged and the level of costs involved in running a medical practice. We have observed that fees generally vary between 35% and 50% of gross practice fees depending on factors such as the location of the practice, cost structures and the relative bargaining position of the parties. Fees of up to 40% of gross practice fees will not generally be sufficient to warrant further

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

25

examination. However, for fees over 40% you will be expected to explain the reasons for the higher fee. The risk of being audited will increase according to the degree of divergence above 40%. For rural and sole medical practitioners, costs can represent a higher percentage of revenues and in these situations we would consider that service fees of up to 45% of gross practice fees would not warrant further examination. 16. A practice management arrangement where the payments are not correctly calculated and may not be reasonably connected to the business. A related service entity rents premises for a GP and employs a receptionist on-hired to the GP. Annual rental is $65,000 and the receptionist’s salary is $38,000. The GP’s gross fees from the practice for the year total $300,000, out of which the GP meets all other clinical, regulatory and practice and personal professional expenses which come to about $80,000. The service entity charges a service fee of 40% of gross fees earned. As the service entity only provides limited services (the premises and receptionist), the GP continues to meet the general costs of the practice. This contrasts with the arrangement in the previous example (where the service entity effectively conducted the business of the medical practice by taking responsibility for all the expenses of the practice other than the GP’s indemnity insurance and personal work related transport costs). Unless there is evidence of a comparable arm’s length arrangement, a share of gross consultation fees is not considered to be a correct basis of charging for these limited services. Charges for these services should be in line with the approach in this guide for conventional services arrangements providing staff and premises. The non-commercial nature of this arrangement is reinforced by the high percentage of gross consultation fee used in this case. Both this method and the rate used bear no discernible commercial relationship to the nature or value of the services provided. The income left in the hands of the GP is also considered to be substantially less than the income earned by other GPs, and the relative income of the GP and the service entity is not considered commensurate with the contribution to the profit of the medical practice. The firm would be at high risk of a tax audit.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

26

PART 4 IS THERE A SMARTER WAY? ALTERNATIVE LEGAL STRUCTURES AND TAX PLANNING STRATEGIES

Introduction The Goods and Services Tax (“GST”) started on 1 July 2000. Since then we have been dissatisfied with service trusts and have believed that they are often not appropriate to medical practices, particularly larger medical practices. This is because: (i) they can be costly to set up and run each year; (ii) they take up scarce management and family time and distract doctors from more

valuing adding activities; (iii) they increase external accountants’ fees; (iv) they make GST compliance more difficult, with complicated and self-canceling

calculations each quarter; (v) may not achieve significant asset protection advantages; (vi) may create unnecessary payroll tax liabilities if the practice employs doctors; and (vii) are often relatively inefficient tax planning devices It’s fair to say that the ATO’s Ruling and Guide exacerbate at least the first four of these concerns. Doctors who continue with service entity structures now have more work to do than ever before, or at least their practice managers do. And the costs will be higher than ever before too. This raises the fundamental threshold question of whether your practice should use a service entity or whether it should abandon the service entity arrangement and use a simpler legal structure and or an alternative tax planning strategy. This part of the manual briefly considers some of the alternative structures and tax planning strategies open to doctors currently using service trusts or who are contemplating using service trusts. Practice trust or company Most GPs and many specialists currently using service trusts do, or within a reasonable period of time, can, satisfy the ATO’s rule of thumb for determining whether a practice is a business. This rule of thumb is set out in sub-paragraph 10(a) of Income Tax Ruling IT 2639 and, paraphrasing, says that the ATO will accept that a medical practice is a business if it has as many or more material fee earners who are not owners as it has owners, on an equivalent full time basis. “Material fee earners” is not exhaustively defined and includes other doctors, practice nurses, counselors, dieticians and

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

27

various other medical technicians who are involved in fee generating work (even if they do not have their own service provider number). Paragraph 2639, and indeed the general question of when a medical practice is a business, is discussed in the Business of Medicine 2002. This manual can be downloaded from our website at www.mcminvestors.com.au. Practices that satisfy the ATO’s rule of thumb, ie which have as many or more material fee generating material fee earners who are not owners as it has owners, on an equivalent full time basis, can use a practice trust or a practice company to run their practice. They do not need to obtain a private ruling from the ATO before they do this. IT 2639 is a public ruling and it applies generally to all professional practices including doctors. Using a practice company or trust means has a number of serious advantages over a traditional service entity arrangement and these include: (viii) they are cheap to set up and to run each year; (ix) they take up less scarce time and are less likely to distract doctors from more

valuing adding activities; (x) they decrease external accountants’ fees relative to service entity arrangements; (xi) they make GST compliance easier as there are fewer BASs and complicated and

self-canceling GST calculations each quarter; (xii) they do not have the inherent uncertainty implicit in using service trusts after the

Ruling and, in particular, using the ATO’s 40%/45% mark up rules for service entities and the general; and

(xiii) their equivalents are used every day in other businesses, ranging from the local milk

bar to BHP Billington. Companies and trusts are conventional ways of owning businesses and have been in use for more than one hundred years;

(xiv) the ATO recognizes them and the income tax law contains literally thousands of

different provisions dealing specifically with companies and trusts. In addition, it is probable that a practice company or a practice trust will lead to less income tax being paid. This is because the practice company or trust does not have to be owned by one individual doctor and can be owned, for example, by a family trust. This means the whole profit of the practice can be distributed to the beneficiaries of the trust including the doctor’s spouse, children, other family members and any other company that a beneficiary owns a share in. This typically leads to a lot less tax being paid than otherwise would have been the case. We routinely recommend that practices which are businesses for taxation purposes use

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

28

practice companies and practice trusts rather than service entity arrangements. We also routinely recommend that doctors who are not businesses for taxation purposes seriously consider changing this and evolving to a business format. The extra profit created by the extra fee earner and, possibly, the extra goodwill created by the extra profit, make this a sensible strategy irrespective of the other advantages listed above. Large deductible superannuation contributions The 12.5% superannuation surcharge was abolished in the May 2005 Federal Budget, with effect from 1 July 2005. This means the only tax charge applying to superannuation contributions is the 15% tax applying to the fund’s net income, which includes its taxable contributions. Superannuation is now a very powerful tax planning tool. The amount of deductible superannuation contributions is determined by the doctor’s age and the limits for the year ending 30 June 2006 are:

Under age 35 at 30 June $14,603 Between age 35 and age 50 $40,560 Over age 50 $100,587

As a general comment, doctor’s spouses can be superannuated by the practice provided they are either a director of the payer company or a general law (ie genuine) employee. The only limit on the amount of the contribution is the spouse’s age based deductible superannuation contribution limit. This means that as a practical matter the real deductible contribution superannuation limits faced by a married doctor can be as much as double those shown above. For example, if a 51 year old doctor has a 49 year old spouse, their combined deductible superannuation contribution limits will be $141,147 (ie $40,560 plus $100,587) and if a 51 year old doctor has a 52 year old spouse their combined deductible superannuation contribution limits will be $201,174 (ie $100,587 plus $100,587). Most doctors and their spouses are over age 35. This means for most married doctors the effective deductible superannuation contribution limit is at least $81,120 (ie twice $40,560) and can be as high as $201,174 (ie twice $100,587). In some cases these limits can be increased further by, for example: (i) superannuating adult children; and/or (ii) arranging one or more separate employment with an arms length employer to

achieve a further and additional deductible superannuation contribution limit. (We have one client who has five such employments and can choose to be superannuated up to his age based limit five times if he wishes to be.)

Assuming the doctor pays tax at a rate of 48%, and the fund pays tax at 15%, superannuation contributions generate a tax benefit equal to 33% of the amount contributed. This is a very significant saving which has to be seriously considered by all doctors and particularly those closer to age 55, where superannuation benefits can be

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

29

accessed if need be. Gearing deductible superannuation contributions An employer entity, such as a practice company or a practice trust, can borrow to pay all or part of a large deductible superannuation contribution. The interest on the borrowed will be tax deductible. This means, for example, that a 55 year old GP with a 55 year old spouse who owns an unencumbered home worth say $1,000,000 can borrow at home loan rates through a practice trust up to $201,174 against the security of the home and pay this amount to a superannuation fund. The amount paid to the superannuation fund will generate a tax benefit of 33% even though it has been funded in all or part by debt. In practice we find that few superannuation contributions are 100% geared. More usually they are a cocktail of cash flow from the practice, cash flow from reinvesting the tax benefit of previous contributions and debt. However, as a matter of economic analysis, whenever a doctor with debt pays a large deductible superannuation contribution out of cash flow, the effect is the same as if the contribution was paid using debt. This is because the doctor could have used the cash to pay off the debt and then re-borrowed to pay the contribution. Most superannuation contributions are at least notionally geared, in that debt repayment was an alternative strategy. The ability to gear large deductible superannuation contributions means that most married doctors over the age of 55 do not need to use a service trust to achieve a tax efficient practice profile. Gearing investments generally Doctors are generally able to gear investments and where they do so any interest shortfall (ie the gearing loss, ie the excess of the interest charge plus other holding costs over the income from the investment) will be deductible against any other income derived by the doctor. Gearing strategies, and the role of debt in the financial planning process, are discussed in detail the Doctors’ Guide to Financial Planning. This manual can be downloaded at our website at www.mcminvestors.com.au. In more complicated cases doctors can gear investments and practice outgoings in their own names while building up income producing assets in the name of a related party, such as a family trust. In one case this led to more than $400,000 collecting debt free in a family trust, ready to be invested in shares. The expected income stream from the share investments plus the tax benefit of the gearing strategy will more than compensate for the tax effect of the now abandoned service trust arrangement. We have some clients with negative gearing losses of more than $100,000 which make the tax planning advantages of any service entity arrangement completely superfluous. Changing from an employment situation to a non-employment situation

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

30

Doctors who are employed by their practice company may consider changing to a practice trust structure using a special deed that complies with the ATO’s rules for incorporating medical practices even where the practice income is personal services income and is not business income. An advantage of the change is that the doctor will jump from the Pay As You Go (ie “PAYG”) Withholdings system to the PAYG Instalments system. This means the doctor will in effect get a tax holiday on his or her practice income from the date of the change say 1 July 2006 to, say, April 2008, being the expected time for lodgment of the income tax return for the year ended 30 June 2007. This does not of itself decrease the amount of tax payable, but it does defer the due date for payment and this is of some benefit. In some cases the doctor can use the enhanced cash flow created by changing from being an employee to running his or her own practice to pay off a non-deductible home loan as fast as possible. The interest on this loan is effectively costing 14% pa before tax and its the early retirement of this loan is the best available investment opportunity. When the tax bill does finally come in the trustee of the practice will borrow to pay the tax bill (technically a borrowing to pay out a distribution to a beneficiary) and the interest on the amount borrowed will be tax deductible in the hands of the trustee. The trustee can speed up this process by using debt to pay its practice costs (for example, the doctor’s insurance premiums, training costs, car costs and other outgoings) while streaming the cash out to the doctor to be used to retire debt. Other legitimate tax planning strategies One can literally write books on tax planning strategies for doctors. And this small part of this short manual cannot possibly cover the wide range of alternative legal structures and tax planning strategies open to doctors who prefer to not use service entity based arrangements. But our basic point is quite simple and straightforward: most doctors can arrange their affairs, even if this includes becoming a practice owner or even employing/engaging extra fee earning staff, so that simpler and better legal structures and tax planning strategies are available to them. And this means that the traditional service entity arrangements will not be of any benefit to them and therefore should not be continued with. All clients of Medical and Dental Accounting Services Pty Ltd have written financial plans which include written taxation planning strategies. This is sound practice management and takes the guesswork out of year end tax planning. This year tax planning needs to seriously consider what needs to be done regarding any service trust arrangements and specifically consider whether the service trust should be continued with. Need to get specific and qualified advice There is no such thing as off the shelf tax advice and doctors should get specific advice

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

31

from a person who is qualified to advise on income tax, ie, a solicitor or a registered tax agent, and the tax implications of superannuation, ie, a solicitor, a financial planner or a member of a recognized accounting body before adopting any of the suggested tax strategies discussed in this part of the manual. Be particularly vigilant for unqualified advisors. You should ask your advisor to demonstrate to you that they are qualified to advise on taxation issues, superannuation issues and legal issues and that they are members of all appropriate professional bodies. You will be surprised at some of their responses.

Copyright. All rights reserved. The Medical and Dental Accounting Services Pty Ltd Guide to Service Entities May 2006. www.mcminvestors.com.au.

32

PART 5 HOW TO MAKE SURE YOUR SERVICE ENTITY ARRANGEMENTS SATISFY THE ATO’S RULES Assuming that despite reading Part 3 and part F of this manual you have still determined that you should use a service entity to provide administrative to your practice, what should you do next? That is, what should you be doing to make sure your service arrangements satisfy the ATO’s rules as set out the Ruling and the Guide? The general answer to these two questions is “read the Ruling and read the Guide”. The Guide in particular sets out what needs to be done to make sure that your service entity arrangements pass muster with the ATO. The difficulty with the Ruling and the Guide is that, apart from two limited examples dealing only with GPs, no specific guidance is given to doctors, particularly doctors other than GPs, or other health professionals. The purpose of this part of the manual is to provide doctor specific guidance on what should be done to make sure your service entity arrangements satisfy the ATO’s rules as set out in the Ruling and the Guide. Bear in mind that the ATO has allowed doctors to 30 April 2007 to review their existing arrangements and make appropriate changes. Practical issue one: actually provide the services The first issue is the need to ensure the services are actually provided by the service entity to the practice. This may sound obvious, but you would be surprised at how often this is not the case. More than once a service entity has been set up, and a client advised in detail as to how to run a service entity, only to turn around a year or two later to find nothing ever happened and the exercise has been a waste of time. But more commonly one of the following errors is made: (i) the lease should be in the name of the service entity, and not in the name of the