Embed Size (px)

Citation preview

Problem 14-20 (30 m

inutes) 1. Average w

eekly use of the auto wash and the vacuum

will be:

Auto wash: $1,350

$1.50900 uses. Vacuum

: 900 x 70% =

630 uses. =

The expected net annual cash receipts w

ill be:

Auto wash cash receipts ($1,350 × 52)...............

$70,200

Vacuum cash receipts (630 × $0.25 × 52)...........

8,190

Total cash receipts...........................................

78,390

Less cash disbursements:

Washer (900 × $0.23 × 52)..............................

$10,764

Electricity: (630 × $0.10 × 52).......................... 3,276

Rent ($1,700 × 12)...........................................

20,400

Cleaning ($450 × 12).......................................

5,400

Insurance ($75 × 12)........................................

900 M

aintenance ($500 × 12).................................

6,000 Total cash disbursem

ents..............................

46,740N

et annual cash receipts....................................

$31,650

©The M

cGraw

-Hill C

ompanies, Inc., 2000

Solutions Manual, C

hapter 14

1

2.

Item

Year(s)A

mount of

Cash Flow

s10%

Factor

Present Value of C

ash Flows

C

ost of equipment..

N

ow

$(150,000)1.000

$(150,000)W

orking capital needed

.................N

ow

(2,000 )

1.000

(2,000 )

Net annual cash

receipts (above)....1-8

31,650

5.335168,853

Salvage of equipm

ent.............8

15,000

0.4677,005

W

orking capital released................

8

2,0000.467

934

N

et present value...

$ 24,792

Yes, Mr. D

uncan should open the auto wash. It prom

ises more than a 10%

rate of return. ©

The McG

raw-H

ill Com

panies, Inc., 2000

M

anagerial Accounting, 9th Edition

2

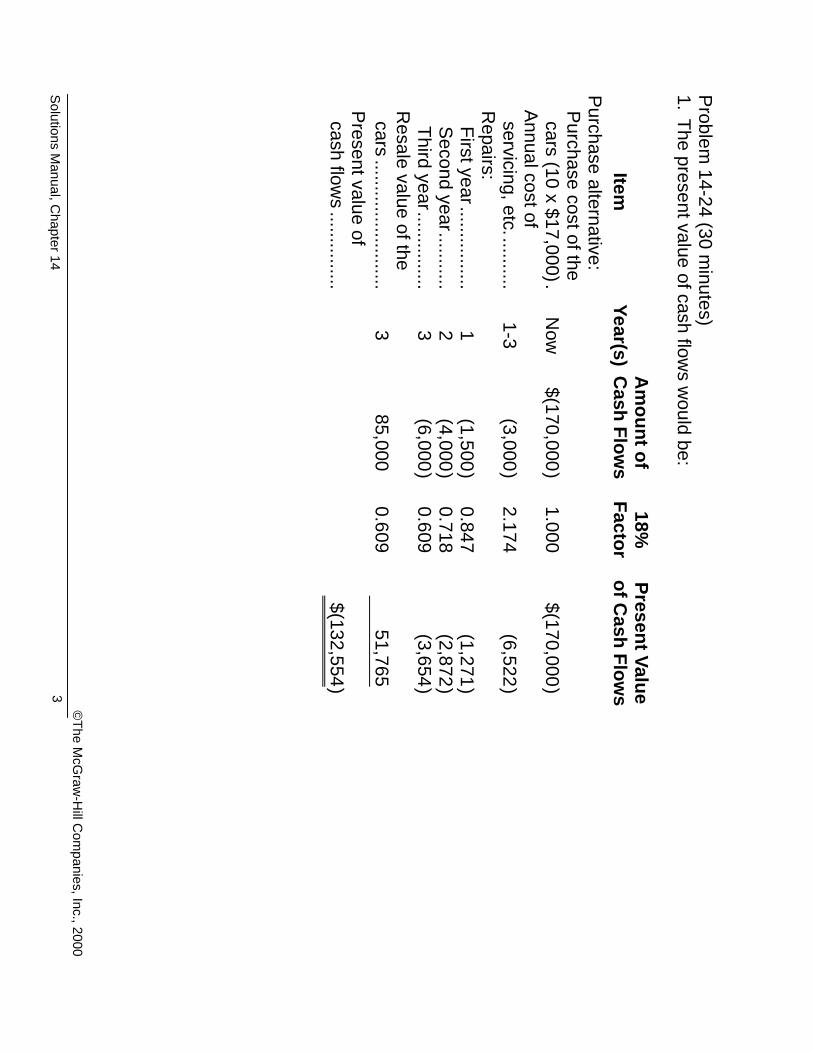

Problem 14-24 (30 m

inutes) 1. The present value of cash flow

s would be:

Item

Year(s)A

mount of

Cash Flow

s18%

Factor

Present Value of C

ash Flows

Purchase alternative:

Purchase cost of the cars (10 x $17,000).

Now

$(170,000 )

1.000

$(170,000 ) Annual cost of servicing, etc...........

1-3

(3,000 )

2.174(6,522 )

Repairs:

First year................ 1

(1,500)

0.847(1,271)

Second year........... 2

(4,000)

0.718(2,872)

Third year............... 3

(6,000)

0.609(3,654)

Resale value of the

cars.........................3

85,000

0.60951,765

Present value of cash flow

s...............

$(132,554 )

©The M

cGraw

-Hill C

ompanies, Inc., 2000

Solutions Manual, C

hapter 14

3

Lease alternative:

Security deposit........

Now

$ (10,000)

1.000$ (10,000)

Annual lease paym

ents................

1-3

(55,000 )

2.174(119,570 )

Refund of deposit......

3

10,000 0.609

6,090 Present value of cash flow

s...............

$(123,480 )N

et present value in favor of leasing the cars............................

$ 9,074

As show

n above, the company should lease the cars since this alternative has the low

est present value of total costs.

2. When a com

pany has a high cost of capital, such as the company in this problem

, it is usually better to avoid tying up funds in equipm

ent and facilities and to use the funds in ways that provide for a

more rapid turnover of investm

ent. Food chains and other retail organizations, for example, prefer to

use funds to expand inventory rather than to purchase buildings. Although the purchase of equipment

and facilities allows a com

pany to claim a resale value at the end of useful life, this resale value

frequently has a very low present value if the com

pany’s cost of capital is high, as can be seen by the purchase alternative above. M

oreover, leased equipment and facilities are often ow

ned by pension funds and sim

ilar organizations that require a fairly low rate of return and thus can pass a savings on

to the lessee. “You should lease whenever m

oney is worth m

ore to you than it is to the other person.”

©The M

cGraw

-Hill C

ompanies, Inc., 2000

M

anagerial Accounting, 9th Edition

4

Problem 14-25 (60 m

inutes)

1. Factor of the InternalR

ate of Return

Investment in the Project

Annual Cash Inflow

$330,000$80,000

4.125

=

=

From

Table 14C-4, reading along the 9-period line, a factor of 4.125 falls betw

een 18% and 20%

. By interpolating:

18%

factor......... .4.303

4.303True factor......... .

4.12520%

factor......... .4.031

Difference

...........0.178

0.272

Internal Rate of R

eturn 18%

+

0.1780.272

2%=

×

Internal Rate of R

eturn = 19.3%

©The M

cGraw

-Hill C

ompanies, Inc., 2000

Solutions Manual, C

hapter 14

5

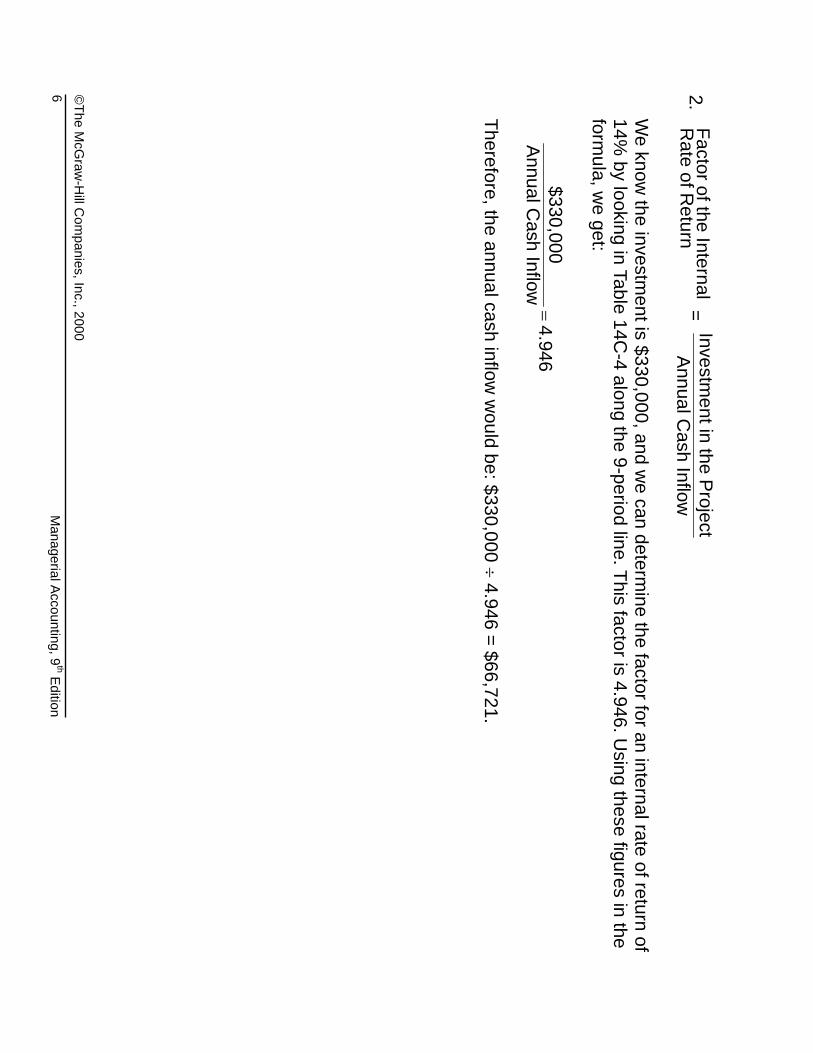

2. Factor of the InternalR

ate of Return

Investmentin the Project

Annual Cash Inflow

=

W

e know the investm

ent is $330,000, and we can determ

ine the factor for an internal rate of return of 14%

by looking in Table 14C-4 along the 9-period line. This factor is 4.946. U

sing these figures in the form

ula, we get:

$330,000Annual C

ash Inflow4.946

=

Therefore, the annual cash inflow

would be: $330,000 ÷ 4.946 = $66,721.

©The M

cGraw

-Hill C

ompanies, Inc., 2000

M

anagerial Accounting, 9th Edition

6

Problem 14-25 (continued)

3. a. 6-year useful life:

The factor for the internal rate of return would still be 4.125 [as com

puted in (1) above]. From Table

14C-4, reading along the 6-period line, a factor of 4.125 falls betw

een 10% and 12%

. By interpolating:

10%

factor..................... 4.355

4.355True factor..................... 4.125

12% factor.....................

4.111D

ifference...................... 0.2300.244

Internal R

ate of Return =

10% +

0.2300.244

2%×

Internal Rate of R

eturn = 11.9%

b. 12-year useful life: The factor of the internal rate of return w

ould again be 4.125. From Table 14C

-4, reading along the 12-period line, a factor of 4.125 falls betw

een 22% and 24%

. By interpolating:

22% factor..................... 4.127

4.127

True factor..................... 4.125

24%

factor..................... 3.851

Difference...................... 0.002

0.276

Internal R

ate of Return =

22% +

0.0020.275

2%×

Internal Rate of R

eturn = 22.0%

©The M

cGraw

-Hill C

ompanies, Inc., 2000

Solutions Manual, C

hapter 14

7

Problem 14-25 (continued)

The 11.9%

return in part (a) is less than the 14% m

inimum

return that Ms. W

inder wants to earn on

the project. Of equal or even greater im

portance, the following diagram

should be pointed out to Ms.

Winder:

As this illustration show

s, a decrease in years has a m

uch greater im

pact on the rate of return than an increase in years. This is because of the tim

e value of m

oney; added cash inflow

s far into the future do little to enhance the rate of

return, but loss of cash inflows in the near term

can do much to reduce it. Therefore, M

s. Winder

should be very concerned about any potential decrease in the life of the equipment, w

hile at the sam

e time realizing that any increase in the life of the equipm

ent will do little to enhance her rate of

return.

6Years11.9%

9Years19.3%

12Years22.0%

A loss of7.4%

A gain of only2.7%

3 years shorter3 years longer

©The M

cGraw

-Hill C

ompanies, Inc., 2000

M

anagerial Accounting, 9th Edition

8

Problem 14-25 (continued)

4. a. The expected annual cash inflow w

ould be:

$80,000 × 80% = $64,000.

$330,000$64,000

= 5.156 (rounded)

From Table 14C

-4, reading along the 9-period line, a factor of 5.156 falls between 12%

and 14%.

By interpolating:

12% factor..................... 5.328

5.328

True factor..................... 5.156

14%

factor..................... 4.946

Difference...................... 0.172

0.382

Internal R

ate of Return =

12% +

0.1720.382

2%×

Internal Rate of R

eturn = 12.9%

©The M

cGraw

-Hill C

ompanies, Inc., 2000

Solutions Manual, C

hapter 14

9

b. The expected annual cash inflow w

ould be:

$80,000 × 120% = $96,000.

$330,000$96,000

= 3.438 (rounded)

From Table 14C

-4, reading along the 9-period line, a factor of 3.438 falls between 24%

and 26%.

By interpolating:

24% factor..................... 3.566

3.566

True factor..................... 3.438

26%

factor..................... 3.366

Difference...................... 0.128

0.200

©The M

cGraw

-Hill C

ompanies, Inc., 2000

M

anagerial Accounting, 9th Edition

10

Problem 14-25 (continued)

Internal R

ate of Return =

24% +

0.1280.200

2%×

Internal Rate of R

eturn = 25.3%

Unlike changes in tim

e, increases and decreases in cash flows at a given point in tim

e have basically the sam

e impact on the rate of return, as show

n below:

$64,000C

ash Inflow12.9%

$80,000C

ash Inflow19.3%

$96,000C

ash Inflow25.3%

A loss of 6.4%

A gain of 6.0%

20% decrease

20% increase

Problem 14-25 (continued)

5. Since the cash flows are not even over the 8-year period (there is an extra $135,440 cash inflow

from

sale of the equipment at the end of the eighth year), it w

ill be necessary to use a trial-and-error approach to com

pute the internal rate of return. A good way to start is to estim

ate what the rate of

return would be w

ithout the sale of equipment:

$330,000 Investment

$50,000 Annual Cash Inflow

= 6.600 Factor

Looking in Table 14C

-4, and scanning along the 8-period line, we can see that a factor of 6.600 w

ould represent an internal rate of return of less than 5%

. If we now

consider the fact that an additional cash inflow

of $135,440 will be realized at the end of the eighth year, it becom

es obvious that the true internal rate of return w

ill be greater than 5%. By a trial-and-error process, and m

oving upward from

5%

, we can eventually determ

ine that the actual internal rate of return will be 10%

(to the nearest w

hole percent):

Item

Year(s)

Am

ount of C

ash Flows

10%

FactorPresent Value of C

ash Flows

Investm

ent in the equipm

ent..............N

ow

$(330,000 )

1.000

$(330,000 )

Annual cash inflow..

1-8

50,000 5.335

266,750

Sale of the equipm

ent.............. 8

135,440

0.46763,250

N

et present value....

$ -0- ©

The McG

raw-H

ill Com

panies, Inc., 2000

M

anagerial Accounting, 9th Edition

12

Problem 14-28 (30 m

inutes) 1. Present cost of using students

...................

$15,000

Less out-of-pocket costs for the car wash:

Salary of student operator.......................

$6,300

U

tilities..................................................... 1,800

Insurance and maintenance

.................... 900

9,000

Annual savings in cash operating costs.....

$ 6,000

2. The formula for the sim

ple rate of return when a cost reduction project is involved is:

Sim

ple Rate of R

eturn =C

ost Savings ion

Initial Investment

$6,000 $2,100* = $3,900$21,000

18.6% (rounded)

D

epreciat

=

−

−

*$21,000 ÷ 10 years = $2,100 per year.

N

o, the car wash w

ould not be purchased. It does not provide the 20% return required by H

onest John.

©The M

cGraw

-Hill C

ompanies, Inc., 2000

Solutions Manual, C

hapter 14

13

3. The formula for payback is:

Payback Period Investm

ent Required

Net Annual C

ash Inflow$21,000$ 6,000

*3.5 years.

=

=

*In this case, the cash inflow

is measured by the annual savings in

cash operating costs.

Yes, the car wash w

ould be purchased. The payback period is less than the maxim

um 4 years

required by Honest John. N

ote that this answer conflicts w

ith the answer in part 2. The conflict points

out the fact that the simple rate of return m

ethod and the payback method w

ill often give different signals to the m

anager. ©

The McG

raw-H

ill Com

panies, Inc., 2000

M

anagerial Accounting, 9th Edition

14

©The M

cGraw

-Hill C

ompanies, Inc., 2000

Solutions Manual, C

hapter 14

15

Problem 14-28 (continued)

4. The formula for the internal rate of return is:

Factor of the Internal R

ate of Return

Investment R

equiredN

et Annual Cash Inflow

$21,000$ 6,000

3.500

=

=

Looking in Table 14C

-4, and reading along the 10-period line, a factor of 3.500 would represent an

internal rate of return of approximately 26%

.

No, the sim

ple rate of return would not norm

ally be an accurate guide in investment decisions. It w

ill tend to understate the rate of return, as show

n in this problem.