Embed Size (px)

Citation preview

THE MATURITY OF INFORMATION TECHNOLOGY

COMPETENCIES: A CASE OF ACCOUNTING PRACTITIONERS

IN THE MALAYSIAN ACCOUNTING SERVICE

Ku Maisurah Ku Bahador, University of South Australia, Adelaide, Australia,

Abrar Haider, University of South Australia, Adelaide, Australia,

Abstract

Information technology plays a significant role in the accounting industry. Accounting practitioners,

therefore, are expected to possess necessary IT competencies to execute the day to day activities.

However, IT competencies as always been viewed as a uni-dimensional construct, where focus in on

imparting technical knowledge. There is a different between the ability to operate IT and IT

competencies. IT competency stands for using technology for the execution of routine business, so that

it contributes to the sustenance, growth, evolution of the business. Therefore, IT competencies should

be viewed as a multi-dimensional construct where technical ability is complement with

organisational, people and conceptual skills. This study reports the results of a study which analyses

the maturity level of IT competencies among accounting practitioners. These IT competencies were

examined under four major dimensions, namely; technical skills, organisational skills, people skills

and conceptual skills. In doing so, this study presents a scorecard of IT competencies and highlights

the underachieving areas the results of this case study, thus, enable learning and work as a role map

for the continues improvement of IT competencies of accounting practitioners within the organisation.

This study makes a significant contribution to academic and professional body of knowledge and

provides an empirically tested based for developing IT competencies for knowledge workers in

general and professional accountants in particular.

Keywords: Information technology, maturity, skills, competencies, accounting practitioners.

1 INTRODUCTION

Advances in information Technology (IT) have transformed many organisation/firms in accounting

professional services industries. This type of organisation/firms undergone major changes at the turn

of the millennium, triggered by rapid changes in its IT environment (Elliot 1998). As a result,

employers of these organisations/firms are looking for a diverse range of IT skills and attributes

amongst new accounting graduates in order to maintain a competitive advantage in a dynamic

business environment.

IT has changed the way data is collected, processed, stored, and aggregated for preparation of

accounting and finance-related information required by management to control and manage business

activities (Winograd et al. 2000). The importance of IT skills to the accounting profession is also

highlighted by many parties, including accounting practitioners, academics and professional bodies

(IFAC 2003; Chang and Hwang 2003). In a joint statement, the CEOs of the six largest international

audit firms state that, ‘today, it would be almost impossible to find an auditor (accountant) without a

personal computer, or without the skills to operate any of a wide variety of software programs that

companies now use to organise and analyse information about their operations’ (Stoner 2009, p. 8).

This study adopts an interpretive paradigm with a qualitative approach through one case study of

small to medium-sized accounting practices in Malaysia in order to identify the maturity of IT

competency amongst accounting practitioners and their view in dealing with their business processes.

This paper is structured as follows. The first section provides the related work of IT competencies

based on relevant literature. The second section is research methodology and the third is the main

focal point in presenting case findings in IT competencies within the organisational issues. Finally the

paper draws conclusions from the case study.

2 RELATED WORK

Globalisation has brought new technology and made the accountant's works changes rapidly. The

element of changes comes from many sources including technological change and advancement.

These changes has have resulted in increased demand on the accounting profession, in that they now

need to achieve an agreed level of competencies through education and practical experience to fulfil

the needs of investors and clients (IFAC 2003). Accountants are expected to possess necessary IT

competencies and the credibility of the accounting profession depends on their success in fulfilling

this obligation (IFAC 2003). Every professional accountant is expected to act as a user, designer,

manager, planner or evaluator of information systems, or a combination of these roles (Wessel 2008).

It has to be acknowledged that these roles require technical skills, organisational skills, interpersonal

skills, and other social skills, challenging professional accountants to develop both technical IT skills

and professional/soft skills).

The involvement of IT-related skills development in the accounting curriculum of higher learning

institutions is widely recognised as a means of reflecting the realities of the use of various forms of

information systems that are increasingly required in the current business world (DeLange Jackling

and Gut 2006). The National Information Technology Taskforce in Australia predicts that the role of

accountants will change significantly, and new skills will need to be developed to adapt technology

advancement (DeLange Jackling and Gut 2006). According to Ainsworth in 2001, IT was not at that

time included in the accounting curriculum as existing accounting programs were already

overcrowded. However, advancements in data/information management and the need for more

efficient systems in conducting business has resulted educators modifying accounting curriculum by

incorporating more exposure to IT (Chang and Hwang 2003).

In the 1980s to the early 1990s, studies on IT-related skills of accountants focused on systems

development and programming related areas (Rai et al. 2010). Rai (2010) reveals that accountants’

perceive systems initiation, design, implementation and control as the most necessary IT topics. This

finding is also supported by Van Meer and Adams (1996), who state that systems analysis, design and

development, IT applications, internal control, documentation, IT audit, spreadsheet, and basic

hardware and software components should be included in the accounting curriculum. Despite

Ainsworth’s (2001) study finding an overcrowded accounting curriculum without IT integration,

Mohamed and Lashine (2003) believe that knowledge of basic technology not only makes entry-level

accounting trainees ‘creative’ in the workplace, but also helps them to adapt to the new environment

faster. The Burnett (2003) study of the future of accounting education indicates that IT or technology-

related skills are becoming important for accounting professionals. The study finds that spreadsheet

software (e.g. Microsoft Excel), Windows, word-processing software (e.g. Microsoft Word) and the

World Wide Web are the top four technology skills, in order of importance, considered by employers

and CPA practitioners. These findings are in line with Helliar et al. (2006), who state that accounting

graduates are required to attain skills in using word processors, spreadsheets and presentation

software when entering their profession. These basic technology skills help accountants to adapt to the

new environment, rather than just making them creative in their workplace (Mohamed and Lashine

2003).

Greenstein-Porsch and McKee (2004) conducted a literature review that resulted in the identification

of 36 critical information technologies. Their study focused on determining IT knowledge levels and

perceptions of accounting information systems and auditing academics and audit practitioners in the

US. The authors found a relatively low level of knowledge of e-commerce and advanced technologies

and audit automation constructs among both educators and practitioners, but a relatively high level of

knowledge of office automation and accounting firm office automation constructs. They also

identified a potential ‘learning gap’ between educators and practitioners that may occur in five of the

36 critical technologies that they examined. Greenstein-Porsch et al. (2005) extended their study by

investigating the comparing their results with Germany and the US. Their study shows a relatively

low level of knowledge for the general constructs of e-commerce, systems design and implementation

and audit automation technologies for both German and US auditors. However, the knowledge of

German auditors was found to be higher for e-commerce technologies than US auditors, while the

knowledge of US auditors was found to be higher for systems design and implementation and office

automation technologies than German auditors. Mgaya and Kitindi (2008) report on a study

completed to identify the level of IT skills of practicing and accounting educators in Botswana. The

results indicate that the self-reported IT skills of practicing and accounting educators are lower than

they think practicing accountants should have.

Ismail and Abidin (2009) attempted to coordinate the alignment between IT knowledge and

importance to current accountants’ roles (as auditors) in Malaysia. Their findings indicate that the

respondents perceived the highest knowledge in general office automation and accounting automation

skills, while knowledge in audit automation, advanced and systems development skills were low.

Overall, the IT knowledge levels of respondents were lower than the perceived importance of these

skills in their careers. Another study on alignment between IT importance and knowledge levels was

conducted by Rai et al. (2010) in Australia. Overall, the IT knowledge levels among Australian

accountants are lower than the perception of the importance of IT knowledge. This study indicates

that accountants have high levels of IT knowledge in email and communication software, and

electronic spreadsheets, while knowledge of systems development and programming tools is low.

2.1 Information Technology Skills and Competencies Required by Accounting Practitioners

IT competencies can be identified as a set of IT-related knowledge and experience that a knowledge

worker possesses (Basselier, Reich and Benbasat 2003). Carnaghan (2003) views IT competencies as

the qualities which are demonstrated by activities such as the capacity to create a spread sheet or

database for a particular purpose, or the ability to use software. According to IFAC (2003),

accounting practitioners are expected to possess necessary IT competencies. In fact, the credibility of

the accounting profession in general depends on their success in fulfilling this obligation. Thus, every

professional accountant is expected to act as a user, designer, manager, planner or evaluator of

information systems; or in a combination of these roles (Wessel 2008). The advancement of

technology is the greatest element that changes accountants’ roles from merely information provision

to extended information facilitation (Jones and Abraham 2007). IT has greatly affected accountants’

careers since it has altered the way accounting is processed and conducted in organisations (Granlund

2007). Some of the effects also include organisations’ hiring policies, training policies, and even the

formal curriculum in higher academic institutions (Chang and Hwang 2003; Sürmen,and Daştan

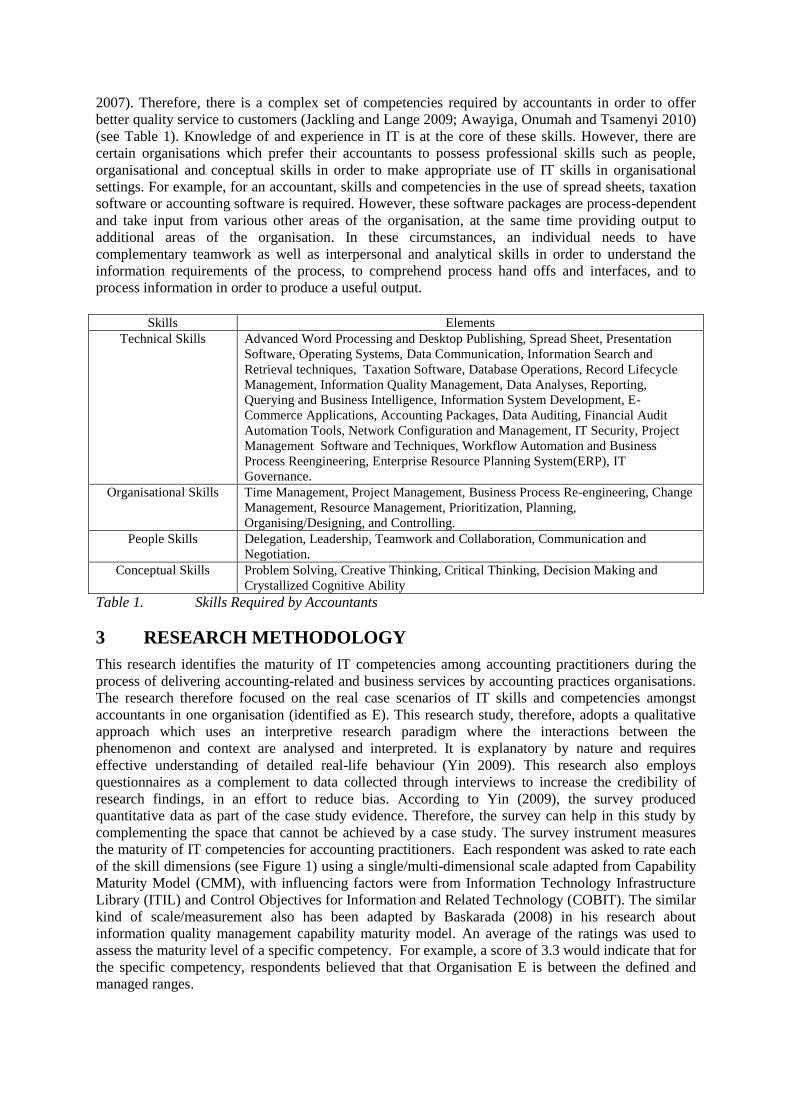

2007). Therefore, there is a complex set of competencies required by accountants in order to offer

better quality service to customers (Jackling and Lange 2009; Awayiga, Onumah and Tsamenyi 2010)

(see Table 1). Knowledge of and experience in IT is at the core of these skills. However, there are

certain organisations which prefer their accountants to possess professional skills such as people,

organisational and conceptual skills in order to make appropriate use of IT skills in organisational

settings. For example, for an accountant, skills and competencies in the use of spread sheets, taxation

software or accounting software is required. However, these software packages are process-dependent

and take input from various other areas of the organisation, at the same time providing output to

additional areas of the organisation. In these circumstances, an individual needs to have

complementary teamwork as well as interpersonal and analytical skills in order to understand the

information requirements of the process, to comprehend process hand offs and interfaces, and to

process information in order to produce a useful output.

Skills Elements

Technical Skills Advanced Word Processing and Desktop Publishing, Spread Sheet, Presentation

Software, Operating Systems, Data Communication, Information Search and

Retrieval techniques, Taxation Software, Database Operations, Record Lifecycle

Management, Information Quality Management, Data Analyses, Reporting,

Querying and Business Intelligence, Information System Development, E-

Commerce Applications, Accounting Packages, Data Auditing, Financial Audit

Automation Tools, Network Configuration and Management, IT Security, Project

Management Software and Techniques, Workflow Automation and Business

Process Reengineering, Enterprise Resource Planning System(ERP), IT

Governance.

Organisational Skills Time Management, Project Management, Business Process Re-engineering, Change

Management, Resource Management, Prioritization, Planning,

Organising/Designing, and Controlling.

People Skills Delegation, Leadership, Teamwork and Collaboration, Communication and

Negotiation.

Conceptual Skills Problem Solving, Creative Thinking, Critical Thinking, Decision Making and

Crystallized Cognitive Ability

Table 1. Skills Required by Accountants

3 RESEARCH METHODOLOGY

This research identifies the maturity of IT competencies among accounting practitioners during the

process of delivering accounting-related and business services by accounting practices organisations.

The research therefore focused on the real case scenarios of IT skills and competencies amongst

accountants in one organisation (identified as E). This research study, therefore, adopts a qualitative

approach which uses an interpretive research paradigm where the interactions between the

phenomenon and context are analysed and interpreted. It is explanatory by nature and requires

effective understanding of detailed real-life behaviour (Yin 2009). This research also employs

questionnaires as a complement to data collected through interviews to increase the credibility of

research findings, in an effort to reduce bias. According to Yin (2009), the survey produced

quantitative data as part of the case study evidence. Therefore, the survey can help in this study by

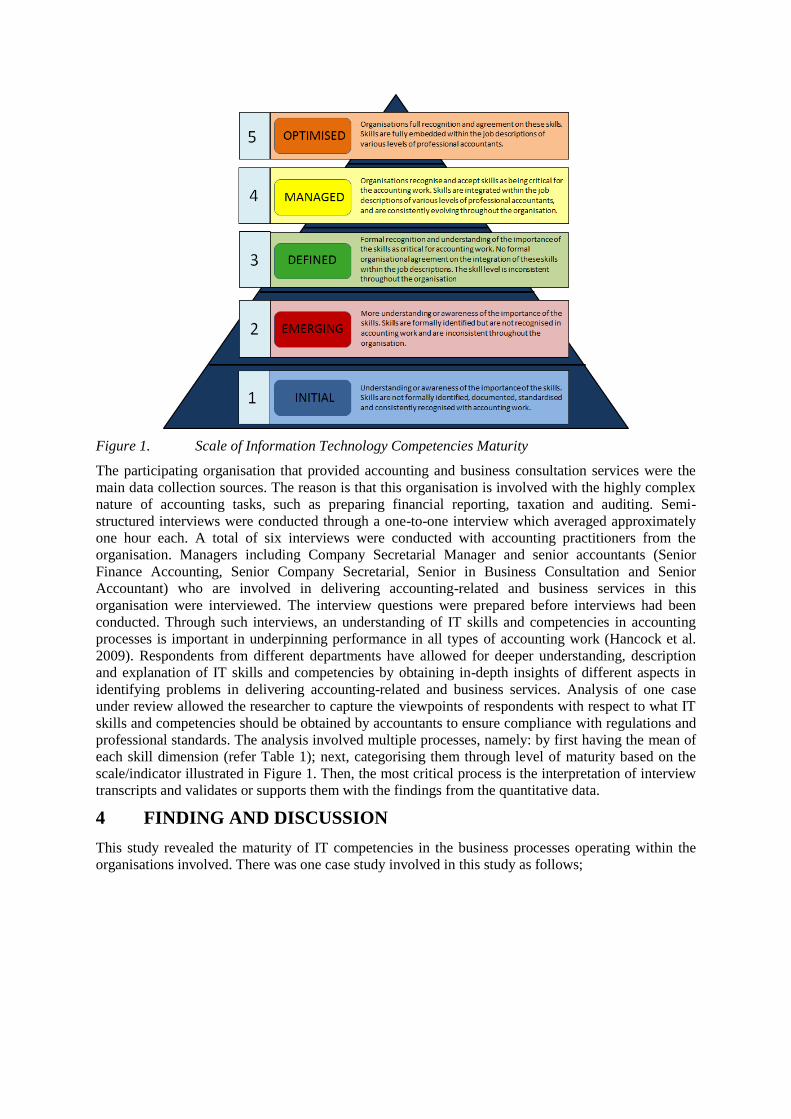

complementing the space that cannot be achieved by a case study. The survey instrument measures

the maturity of IT competencies for accounting practitioners. Each respondent was asked to rate each

of the skill dimensions (see Figure 1) using a single/multi-dimensional scale adapted from Capability

Maturity Model (CMM), with influencing factors were from Information Technology Infrastructure

Library (ITIL) and Control Objectives for Information and Related Technology (COBIT). The similar

kind of scale/measurement also has been adapted by Baskarada (2008) in his research about

information quality management capability maturity model. An average of the ratings was used to

assess the maturity level of a specific competency. For example, a score of 3.3 would indicate that for

the specific competency, respondents believed that that Organisation E is between the defined and

managed ranges.

Figure 1. Scale of Information Technology Competencies Maturity

The participating organisation that provided accounting and business consultation services were the

main data collection sources. The reason is that this organisation is involved with the highly complex

nature of accounting tasks, such as preparing financial reporting, taxation and auditing. Semi-

structured interviews were conducted through a one-to-one interview which averaged approximately

one hour each. A total of six interviews were conducted with accounting practitioners from the

organisation. Managers including Company Secretarial Manager and senior accountants (Senior

Finance Accounting, Senior Company Secretarial, Senior in Business Consultation and Senior

Accountant) who are involved in delivering accounting-related and business services in this

organisation were interviewed. The interview questions were prepared before interviews had been

conducted. Through such interviews, an understanding of IT skills and competencies in accounting

processes is important in underpinning performance in all types of accounting work (Hancock et al.

2009). Respondents from different departments have allowed for deeper understanding, description

and explanation of IT skills and competencies by obtaining in-depth insights of different aspects in

identifying problems in delivering accounting-related and business services. Analysis of one case

under review allowed the researcher to capture the viewpoints of respondents with respect to what IT

skills and competencies should be obtained by accountants to ensure compliance with regulations and

professional standards. The analysis involved multiple processes, namely: by first having the mean of

each skill dimension (refer Table 1); next, categorising them through level of maturity based on the

scale/indicator illustrated in Figure 1. Then, the most critical process is the interpretation of interview

transcripts and validates or supports them with the findings from the quantitative data.

4 FINDING AND DISCUSSION

This study revealed the maturity of IT competencies in the business processes operating within the

organisations involved. There was one case study involved in this study as follows;

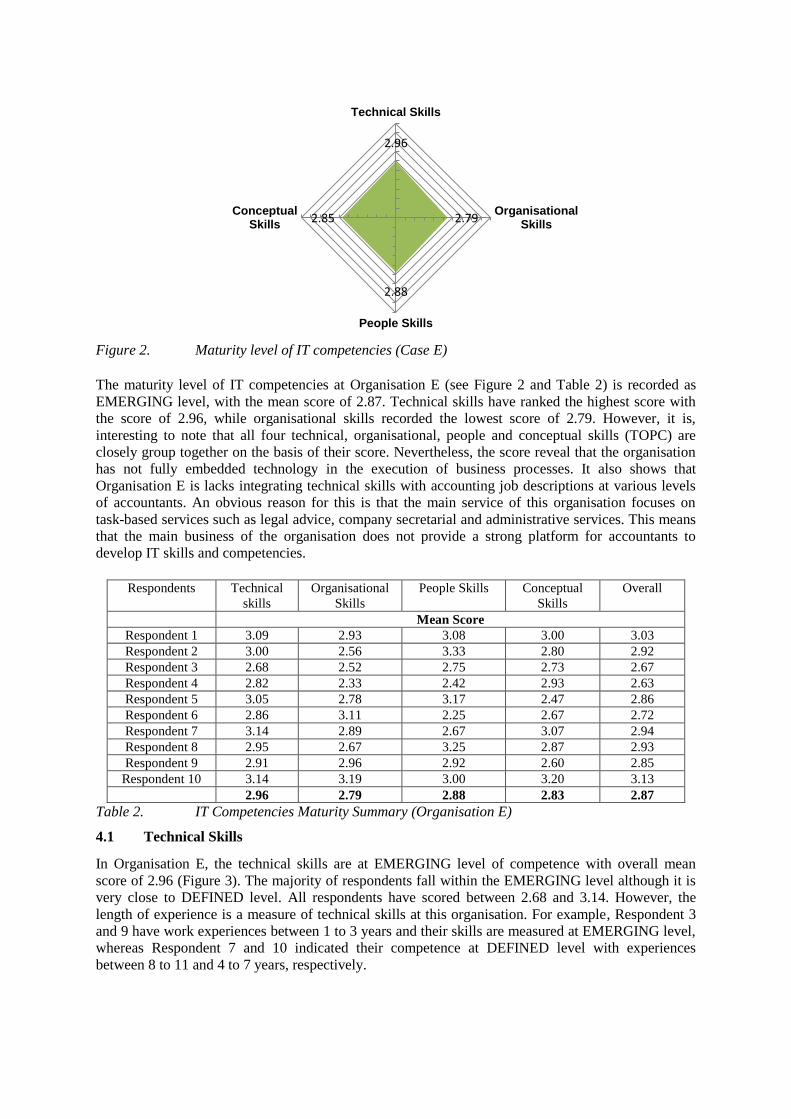

Figure 2. Maturity level of IT competencies (Case E)

The maturity level of IT competencies at Organisation E (see Figure 2 and Table 2) is recorded as

EMERGING level, with the mean score of 2.87. Technical skills have ranked the highest score with

the score of 2.96, while organisational skills recorded the lowest score of 2.79. However, it is,

interesting to note that all four technical, organisational, people and conceptual skills (TOPC) are

closely group together on the basis of their score. Nevertheless, the score reveal that the organisation

has not fully embedded technology in the execution of business processes. It also shows that

Organisation E is lacks integrating technical skills with accounting job descriptions at various levels

of accountants. An obvious reason for this is that the main service of this organisation focuses on

task-based services such as legal advice, company secretarial and administrative services. This means

that the main business of the organisation does not provide a strong platform for accountants to

develop IT skills and competencies.

Respondents Technical

skills

Organisational

Skills

People Skills Conceptual

Skills

Overall

Mean Score

Respondent 1 3.09 2.93 3.08 3.00 3.03

Respondent 2 3.00 2.56 3.33 2.80 2.92

Respondent 3 2.68 2.52 2.75 2.73 2.67

Respondent 4 2.82 2.33 2.42 2.93 2.63

Respondent 5 3.05 2.78 3.17 2.47 2.86

Respondent 6 2.86 3.11 2.25 2.67 2.72

Respondent 7 3.14 2.89 2.67 3.07 2.94

Respondent 8 2.95 2.67 3.25 2.87 2.93

Respondent 9 2.91 2.96 2.92 2.60 2.85

Respondent 10 3.14 3.19 3.00 3.20 3.13

2.96 2.79 2.88 2.83 2.87

Table 2. IT Competencies Maturity Summary (Organisation E)

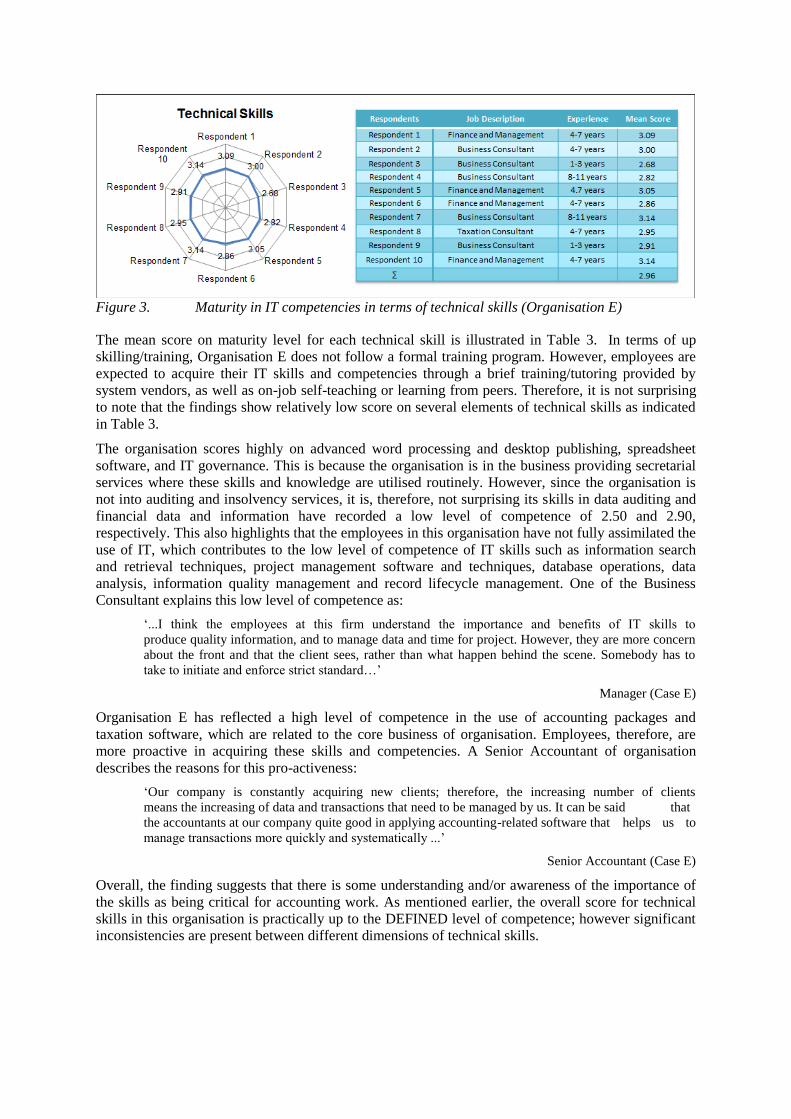

4.1 Technical Skills

In Organisation E, the technical skills are at EMERGING level of competence with overall mean

score of 2.96 (Figure 3). The majority of respondents fall within the EMERGING level although it is

very close to DEFINED level. All respondents have scored between 2.68 and 3.14. However, the

length of experience is a measure of technical skills at this organisation. For example, Respondent 3

and 9 have work experiences between 1 to 3 years and their skills are measured at EMERGING level,

whereas Respondent 7 and 10 indicated their competence at DEFINED level with experiences

between 8 to 11 and 4 to 7 years, respectively.

2.96

2.79

2.88

2.85

Technical Skills

OrganisationalSkills

People Skills

ConceptualSkills

Figure 3. Maturity in IT competencies in terms of technical skills (Organisation E)

The mean score on maturity level for each technical skill is illustrated in Table 3. In terms of up

skilling/training, Organisation E does not follow a formal training program. However, employees are

expected to acquire their IT skills and competencies through a brief training/tutoring provided by

system vendors, as well as on-job self-teaching or learning from peers. Therefore, it is not surprising

to note that the findings show relatively low score on several elements of technical skills as indicated

in Table 3.

The organisation scores highly on advanced word processing and desktop publishing, spreadsheet

software, and IT governance. This is because the organisation is in the business providing secretarial

services where these skills and knowledge are utilised routinely. However, since the organisation is

not into auditing and insolvency services, it is, therefore, not surprising its skills in data auditing and

financial data and information have recorded a low level of competence of 2.50 and 2.90,

respectively. This also highlights that the employees in this organisation have not fully assimilated the

use of IT, which contributes to the low level of competence of IT skills such as information search

and retrieval techniques, project management software and techniques, database operations, data

analysis, information quality management and record lifecycle management. One of the Business

Consultant explains this low level of competence as:

‘...I think the employees at this firm understand the importance and benefits of IT skills to

produce quality information, and to manage data and time for project. However, they are more concern

about the front and that the client sees, rather than what happen behind the scene. Somebody has to

take to initiate and enforce strict standard…’

Manager (Case E)

Organisation E has reflected a high level of competence in the use of accounting packages and

taxation software, which are related to the core business of organisation. Employees, therefore, are

more proactive in acquiring these skills and competencies. A Senior Accountant of organisation

describes the reasons for this pro-activeness:

‘Our company is constantly acquiring new clients; therefore, the increasing number of clients

means the increasing of data and transactions that need to be managed by us. It can be said that

the accountants at our company quite good in applying accounting-related software that helps us to

manage transactions more quickly and systematically ...’

Senior Accountant (Case E)

Overall, the finding suggests that there is some understanding and/or awareness of the importance of

the skills as being critical for accounting work. As mentioned earlier, the overall score for technical

skills in this organisation is practically up to the DEFINED level of competence; however significant

inconsistencies are present between different dimensions of technical skills.

Elements Mean

Score

Maturity

Level

Advanced Word Processing and Desktop Publishing 4.60 Level 4

Spreadsheet Software 4.50 Level 4

Presentation Software 3.30 Level 3

Data Communication/Sharing (email, social networks, web 2.0) 3.60 Level 3

Information Search and Retrieval Techniques 2.90 Level 2

Taxation Software (tax return, tax reconciliation, direct and indirect tax) 3.80 Level 3

Accounting Packages (Mind your Own Business, User Business System Accounting(UBS),

Bizztrak)

4.40 Level 4

Data Auditing (audit trail, fraud control, etc.) 2.50 Level 2

Financial Audit Automation Tools (generalised audit software and embedded audit module) 2.90 Level 2

Project Management Software and Techniques 2.50 Level 2

Database Operations (creation, manipulation and management of data; data coding, data

dictionary, data control and extraction; ETL; data warehouse)

2.70 Level 2

Data Analyses, Reporting, Querying, and Business Intelligence 2.40 Level 2

Information Quality Management (including data cleansing, purification, aggregation, etc.) 2.30 Level 2

Record Lifecycle Management (creation exchange, storage retrieval and retirement/

deletion)

2.10 Level 2

Information System Development/Procurement Life Cycle 2.20 Level 2

E-Commerce Applications (electronic Payment System, Customer Relationship

Management, website development/maintenance)

2.20 Level 2

Workflow automation and business process reengineering 2.30 Level 2

Operating Systems (Windows and Linux) 2.90 Level 2

Network Configuration and Management 2.40 Level 2

IT Security (antivirus software, firewall, backup and recovery, etc.) 2.50 Level 2

Enterprise Resource Planning System(ERP) 2.40 Level 2

IT Governance (IT resources management, risk management, IT performance evaluation,

IT value delivery, business IT alignment)

3.80 Level 3

Table 3. Maturity level of accountants’ in terms of technical skills (Organisation E)

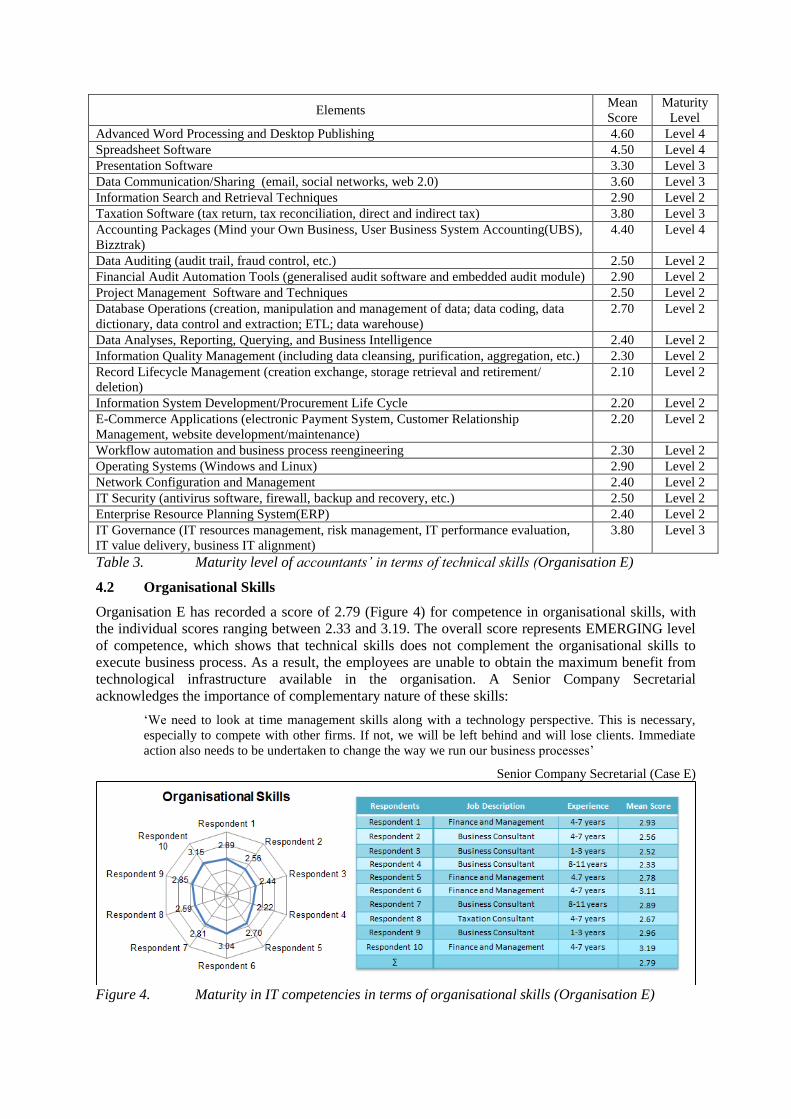

4.2 Organisational Skills

Organisation E has recorded a score of 2.79 (Figure 4) for competence in organisational skills, with

the individual scores ranging between 2.33 and 3.19. The overall score represents EMERGING level

of competence, which shows that technical skills does not complement the organisational skills to

execute business process. As a result, the employees are unable to obtain the maximum benefit from

technological infrastructure available in the organisation. A Senior Company Secretarial

acknowledges the importance of complementary nature of these skills:

‘We need to look at time management skills along with a technology perspective. This is necessary,

especially to compete with other firms. If not, we will be left behind and will lose clients. Immediate

action also needs to be undertaken to change the way we run our business processes’

Senior Company Secretarial (Case E)

Figure 4. Maturity in IT competencies in terms of organisational skills (Organisation E)

Although Organisation E has been operating for 15 years in the industry, the average accountant’s

experience is only around four to seven years. The organisation scores low on business, project

management, resource management and controlling skills which is consistent with the low scores of

technical skills in project management software, database operations and workflow automation (refer

Table 4). It is also important to note that the culture of this organisation is static and change resistant

which is why employees cannot find the synergy between technical skills and organisational skills. As

a small and medium-sized accounting organisation that is involved in the rapidly changing

technological environment, Organisation E needs to dynamically cope with the constant change in

both the internal or external environment of the organisation. However, the low scores in change

management skills (2.80), and business process re-engineering skills (2.00) is a little surprising, since

the organisation’s core business is secretarial services. It could be due to the fact that the organisation

has a uni-dimensional view of IT and does not account for the complementary nature of organisational

skills. Overall, this suggests that organisational skills are not integrated with technical skills. A senior

in Financial Accounting commented:

‘From the point of view, I can see that in dealing with issues related to time management and work

planning, technology infrastructure is not used wisely. For example, to monitor schedule and to

prioritize projects to be completed, a simple ad-hoc as spreadsheet is used to update project

information’

Senior in Finance Accounting (Case E)

Elements Mean Score Maturity Level

Time Management Skills 3.00 Level 3

Project Management Skills 2.83 Level 2

Business Process Re-engineering Skills 2.00 Level 2

Change Management Skills 2.80 Level 2

Resource Management Skills 2.65 Level 2

Prioritization Skills 3.10 Level 3

Planning Skills 2.84 Level 2

Organising/Designing Skills 3.05 Level 3

Controlling Skills 2.83 Level 2

Table 4. Maturity level in terms of organisational skills (Organisation E)

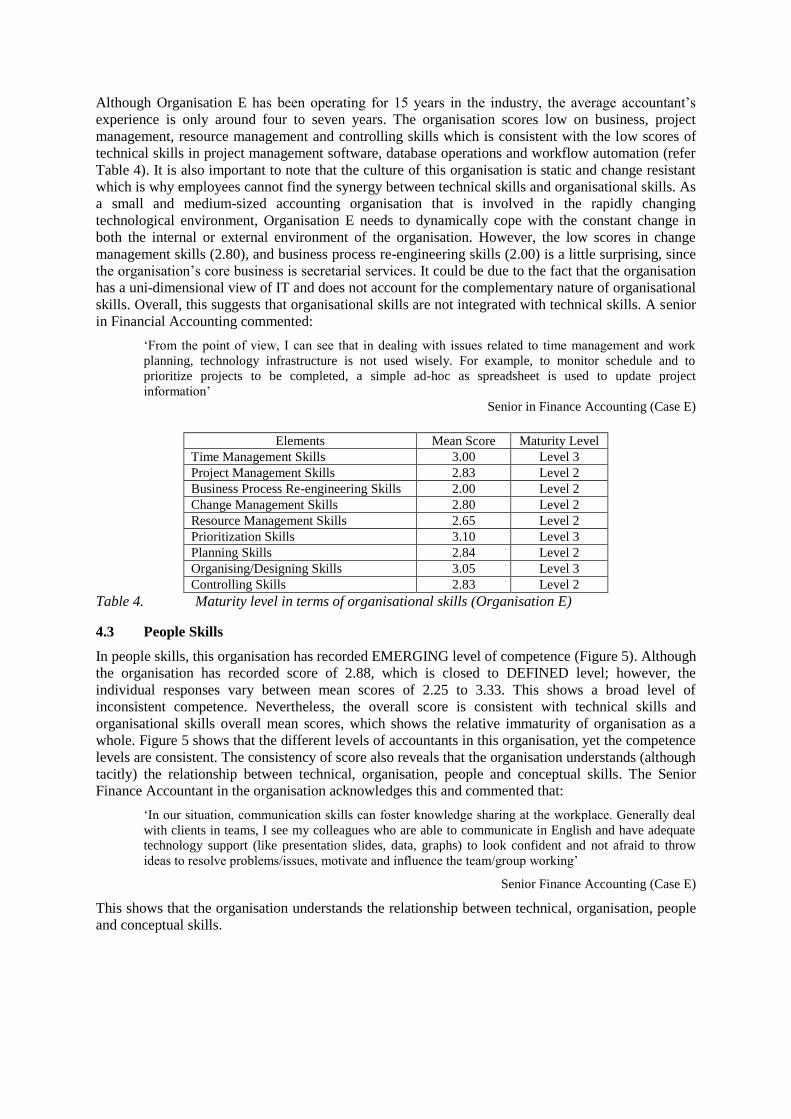

4.3 People Skills

In people skills, this organisation has recorded EMERGING level of competence (Figure 5). Although

the organisation has recorded score of 2.88, which is closed to DEFINED level; however, the

individual responses vary between mean scores of 2.25 to 3.33. This shows a broad level of

inconsistent competence. Nevertheless, the overall score is consistent with technical skills and

organisational skills overall mean scores, which shows the relative immaturity of organisation as a

whole. Figure 5 shows that the different levels of accountants in this organisation, yet the competence

levels are consistent. The consistency of score also reveals that the organisation understands (although

tacitly) the relationship between technical, organisation, people and conceptual skills. The Senior

Finance Accountant in the organisation acknowledges this and commented that:

‘In our situation, communication skills can foster knowledge sharing at the workplace. Generally deal

with clients in teams, I see my colleagues who are able to communicate in English and have adequate

technology support (like presentation slides, data, graphs) to look confident and not afraid to throw

ideas to resolve problems/issues, motivate and influence the team/group working’

Senior Finance Accounting (Case E)

This shows that the organisation understands the relationship between technical, organisation, people

and conceptual skills.

Figure 5. Maturity in IT competencies in terms of people skills (Organisation E)

Table 5 explains the maturity level of individual category of people skills. It reveals grouping of all

these skills, which is consistent with the organisation and technical skills. For example, the score of

negotiation skills (2.90) is consistent with the score project management skills (2.83), which are

consistent with the project management software and techniques score of 2.50. This shows that the

level of competence in either of between technical, organisation, people and conceptual dimensions

affect other dimensions. The table also reveals the scores of 3.00 for delegation and 2.70 for

leadership, which is consistent with the change management skills (2.80) and information search and

retrieval score of 2.90 and data analyses, reporting, querying, and business intelligence score of 2.40.

Company Secretarial Manager commented:

‘This firm emphasises communication, negotiation and teamwork skills. It will help employees to plan

project as well as the ability to share information for analysing issues before make decision. It is

important for us to evaluate the system / software that will help us to respond quickly to any issues, and

help us to implement strategies to achieve positive and effective interaction with people in the

workplace as well as clients’

Company Secretarial Manager (Case E)

Elements Mean Score Maturity Level

Delegation Skills 3.00 Level 3

Leadership Skills 2.70 Level 2

Teamwork and Collaboration Skills 2.93 Level 2

Communication Skills 2.87 Level 2

Negotiation Skills 2.90 Level 2

Table 5. Maturity level of accountants’ in terms of people skills (Organisation E)

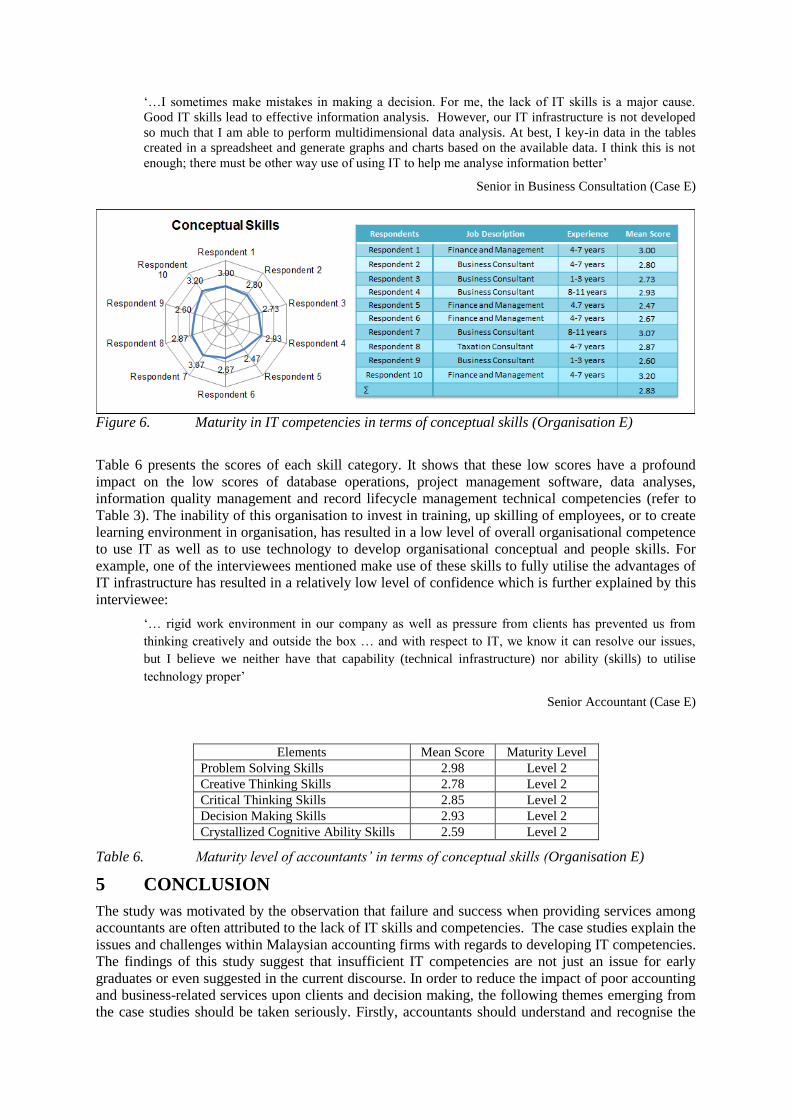

4.5 Conceptual Skills

The Organisation E has recorded an EMERGING level of competence in conceptual skills, Figure 6

illustrates that all respondents are scored between EMERGING and DEFINED level with the score

ranging between 2.47 and 3.20. This shows that conceptual skills are not well-developed in this

organisation. However two respondents (Respondent 1 and 10) have shown a higher level of

competence in conceptual skills. Both of these respondents have work experiences closed to seven

years in the organisation and there are from the Finance and Management service. The low level of

competence in conceptual skills is consistent with the low level of competence in technical skills such

as database operations (2.70), data analyses and reporting (2.40), data auditing (2.50), information

search and retrieval (2.90) (refer Table 3). These are the prerequisite of analysing of situation of

decision-making. Once the organisation is not competence enough in these technical skills, it is not

surprising that the organisation has scored low on conceptual skills. This also shows that the

organisation does not provide right environment for employees to develop their conceptual skills,

because they have trained or up skills employees in enhancing these technical skills. This is

summarised in the respond from the Senior Accountants from the business consultation service who

stated that:

‘…I sometimes make mistakes in making a decision. For me, the lack of IT skills is a major cause.

Good IT skills lead to effective information analysis. However, our IT infrastructure is not developed

so much that I am able to perform multidimensional data analysis. At best, I key-in data in the tables

created in a spreadsheet and generate graphs and charts based on the available data. I think this is not

enough; there must be other way use of using IT to help me analyse information better’

Senior in Business Consultation (Case E)

Figure 6. Maturity in IT competencies in terms of conceptual skills (Organisation E)

Table 6 presents the scores of each skill category. It shows that these low scores have a profound

impact on the low scores of database operations, project management software, data analyses,

information quality management and record lifecycle management technical competencies (refer to

Table 3). The inability of this organisation to invest in training, up skilling of employees, or to create

learning environment in organisation, has resulted in a low level of overall organisational competence

to use IT as well as to use technology to develop organisational conceptual and people skills. For

example, one of the interviewees mentioned make use of these skills to fully utilise the advantages of

IT infrastructure has resulted in a relatively low level of confidence which is further explained by this

interviewee:

‘… rigid work environment in our company as well as pressure from clients has prevented us from

thinking creatively and outside the box … and with respect to IT, we know it can resolve our issues,

but I believe we neither have that capability (technical infrastructure) nor ability (skills) to utilise

technology proper’

Senior Accountant (Case E)

Elements Mean Score Maturity Level

Problem Solving Skills 2.98 Level 2

Creative Thinking Skills 2.78 Level 2

Critical Thinking Skills 2.85 Level 2

Decision Making Skills 2.93 Level 2

Crystallized Cognitive Ability Skills 2.59 Level 2

Table 6. Maturity level of accountants’ in terms of conceptual skills (Organisation E)

5 CONCLUSION

The study was motivated by the observation that failure and success when providing services among

accountants are often attributed to the lack of IT skills and competencies. The case studies explain the

issues and challenges within Malaysian accounting firms with regards to developing IT competencies.

The findings of this study suggest that insufficient IT competencies are not just an issue for early

graduates or even suggested in the current discourse. In order to reduce the impact of poor accounting

and business-related services upon clients and decision making, the following themes emerging from

the case studies should be taken seriously. Firstly, accountants should understand and recognise the

specific issues regarding services to clients and elements of IT skills. This behaviour will allow them

to determine which elements of IT skills and competencies are appropriate to the issues and to ensure

the level of services are at a satisfactory level. Secondly, organisations should come up with a

development plan of comprehensive IT competencies program at all levels of an accountant’s

lifecycle. This program should provide training for managers, partners, senior accountants and junior

accountants in order to recognise issues in providing and delivering services; identify root causes and

construct possible skills and competencies, thereby embedding these skills as part of their jobs.

References

Ainsworth, P. (2001). Changes in accounting curricula: discussion and design, Accounting Education,

10(3), 279-297.

Awayiga, J.Y. Onumah, J.M. and Tsamenyi, M. (2010). Knowledge and skills development of

accounting graduates: the perceptions of graduates and employers in Ghana, Accounting

Education: An International Journal, 19(1-2), 139-158.

Eide, B.J. (2000). Integrating learning strategies in accounting courses, J. Edward Ketz, in (ed.)

Advances in Accounting Education Teaching and Curriculum Innovations (Advances in

Accounting Education, Volume 2), Emerald Group Publishing Limited, 37-55.

Elliott, R.K. (1998). Who are we as a profession—And what must we become? Journal of

Accountancy (February), 81-85.

Bassellier, G. Benbasat, I. and Reich, B.H. (2003). The influence of business managers’ IT

competence on championing IT, Information Systems Research, 14(4), 317-336.

Baskarada, S. (2008). IQM-CMM: Information quality management capability maturity model, PhD

Thesis, University of South Australia, August.

Boyatzis, R. (1998). Transforming qualitative information: thematic analysis and code development,

Thousand Oaks: Sage.

Burnett, S. (2003). The future of accounting education: a regional perspective, Journal of Education

for Business, 78, 129–134.

Carnaghan, C. (2004). Discussion of IT assurance competencies, International Journal of Accounting

Information Systems, 5, 267-273.

Carruthers, J. (1990). A rationale for the use of semi-structured interviews, Journal of Educational

Administration 28, 63 – 68.

Chang, C. and Hwang, N. (2003). Accounting education, firm training and information technology: a

research note, Accounting Education, 12(4), 441-450.

De-Lange, P. Jackling, B. and Gut, A.M. (2006). Accounting graduates’ perceptions of skills

emphasis in undergraduate courses: an investigation from two Victorian universities’, Accounting

and Finance, 46(3), 365 – 386.

Greenstein-Prosch, M. and McKee, T.E. (2004). Assurance practitioners and educators self-perceived

IT knowledge level: an empirical assessment”, International Journal Accounting Information

Systems, 5, 213-243.

Greenstein-Prosch, M. McKee, T.E. Quick, R. (2005). A comparison of the information technology

knowledge of United States and German auditors”, paper presented at the 8th European

Conference on Accounting Information Systems, Goteborg, Sweden.

Helliar, C.V. Monk, E.A. and Stevenson, L.A. (2006) The skill-set of trainee auditors, National

Auditing Conference, University of Manchester, March.

International Federation of Accountants Education Committee (IFAC) (2003). Information

Technology for Professional Accountants, available at https://www.imanet.org/pdf/ITPA.pdf,

[accessed 30 December 2010].

Ismail, N. and Abidin, Z. (2009). Perception towards the importance and knowledge of information

technology among auditors in Malaysia, Journal of Accounting and Taxation, 1(4), 061-069.

Jackling, B. and De-Lange, P. (2009). Do accounting graduated skills meet the expectations of

employers? A matter of convergence or divergence, Accounting Education: An International

Journal, 18(4-5), 369 – 385.

Jones, G. and Abraham, A. (2007). Educational implications of the changing role of accountants’

perceptions of practitioners, academic and students, In the Quantitative Analysis of Teaching and

Learning in Business. Economics and Commerce, Forum Proceeding, the University of

Melbourne, 9 February 2007, 89-105. [Online} Available: http://ro.uow.edu.au/commpapers/296/

(March 19, 2012).

Kavanagh, M.H. and Drennan, L. (2008). What skills and attributes do an accounting graduate need?

evidence from student perceptions and employer expectations, Accounting and Finance, 48, 279 –

300.

Kermis, G. and Kermis, M. (2011). Professional presence and soft skills: a role for accounting

education, Journal of Instructional Pedagogies, 1 – 10.

Lai, M.L. and Nawawi, N.H.A. (2010). Integrating ICT skills and tax software in tax education: a

survey of Malaysian tax practitioners’ perspectives, Campus-Wide Information Systems 27(5),

303.

Lewins, A. and Silvers, C. (2007). Using Qualitative Software: A Step by Step Guide, Sage, London.

Memiyanty, A.R. Rozainun, A.A. and Shith-Putera, M. (2010). Better skills? Better service?

Malaysian evidence’, International Conference on Financial Theory and Engineering, Proceedings

of 2009 (ICIFE), International Association of Computer Science and Information Technology

(IACSIT), IEEE Computer Society.

Mgaya, K.V. and Kitindi, E.G. (2008). IT Skills of academics and practising accountants in

Botswana, World Review of Entrepreneurship, Management and Sustainable Development, 4(4),

366-379.

Mohamed, E.K.A. and Lashine, S.H. (2003). Accounting knowledge and skills and the challenges of a

global business environment, Managerial Finance, 29(7), 3-16.

Rai, P. Vatanasakdakul, S. and Aoun, C. (2010). Exploring perception of it skills among Australian

accountants: an alignment between importance and knowledge’, Proceedings of the Sixteenth

Americas Conference on Information Systems, 12 - 15 August 2010: Lima, Peru, 1-10.

Sekaran, U. (2003). Research Methods for Business: A Skill Building Approach, Wiley & Sons

Australia.

Senik, R. and Broad, M. (2011). Information technology skills development for accounting graduates:

intervening conditioned, International Education Studies, Canadian Centre of Science and

Education, 4(2), 105-110.

Stoner, G. (2009). Accounting students' IT application skills over a 10-year period, Accounting

Education, 18(1), 7-31.

Wessel, P.J. (2008). The identification and discussion of strategies for implementing an IT skills

framework in the education of professional accountants, South African Journal of Accounting

Research, 22(1), 147-181.

Winograd, B.N. Gerson, J.S. and Berlin, B.L. (2000). Audit practices of Pricewaterhouse Coopers’,

Auditing, Journal of Practitioner Theory, 19(2), 175-182.

Yin, R.K. (2009). Case Study Research: Design and Methods, Sage, Beverly Hills, CA 5.

![[SurgeryB] Surgical Complications - Dr. Guinto (Pacis, Sazon)](https://img.pdfslide.us/doc/110x75/55cf921d550346f57b93bae3/surgeryb-surgical-complications-dr-guinto-pacis-sazon.jpg)