Embed Size (px)

Citation preview

The market structure for small hydro electricity in Brazil

DECEMBER 2012

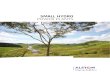

Source: ONS (National Electricity System Operator)

Brazilian Interconnected System (2012)

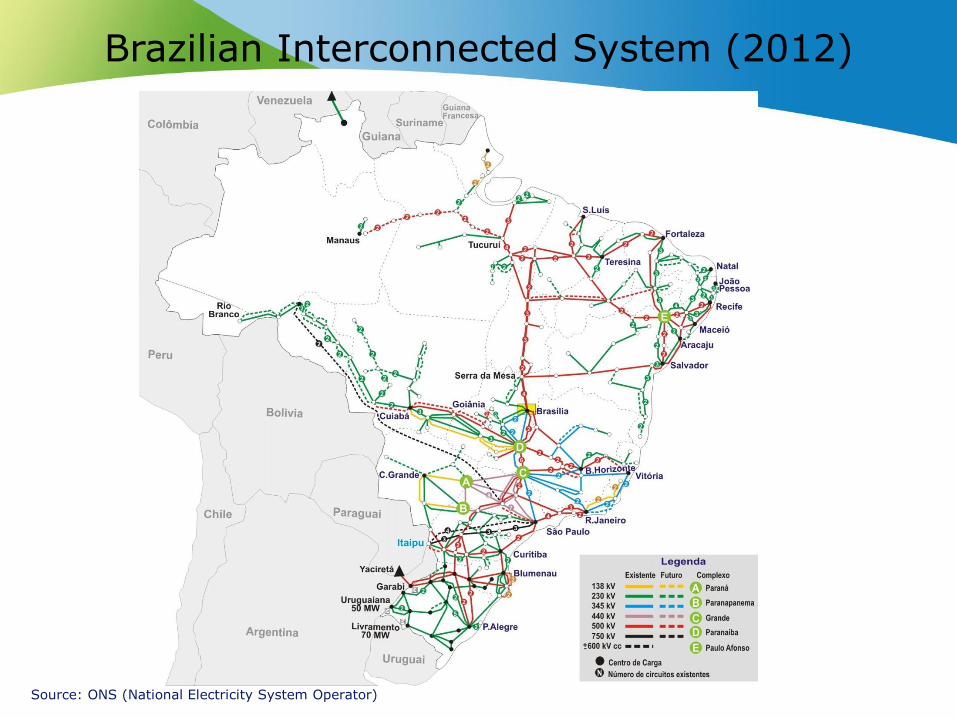

Evolution of the Installed Capacity by Source Brazil – National Interconnected System (SIN)

It is estimated that the total installed small hydro power (SHP) capacity will increase from 5 to 7 GW up to 2021. According to EPE (Brazilian Energy Research Company) the renewable sources (SHP, biomass and wind power plants) share of the total installed capacity will increase from 13% in 2011 to 20% in 2021.

Source: EPE (Brazilian Energy Research Company) (PDE 2021)

Nuclear

2% Thermal

14%

Small

Hydro

4%

Biomass

7%

Wind

9%

Hydro

64%

182 GW

December / 2021

Hydro;

72%

Wind;

1%

Biomass;

7%

Small

Hydro;

4%

Thermal;

15%

Nuclear;

2%

117 GW

December / 2011

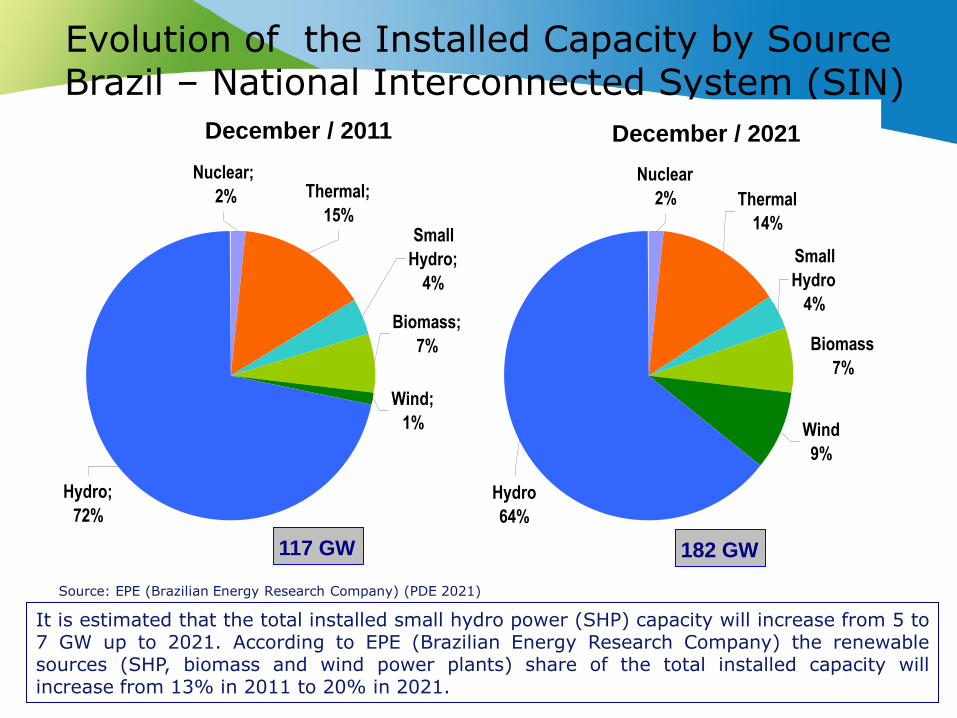

Brazilian classification of Hydro Power Project by its generating capacity

*According to ANEEL (National Electric Energy Agency): Small Hydroelectric Power

Plant (SHP) are hydro power plants with installed capacity greater than 1 MW and less

or equal to 30 MW with reservoir area of less than 3 km². (Independent Power

Production or Self-Production )

Installed

capacity

(MW)

Reservoir

area (km²)

Others

Requirements Classification

≤ 1 - CGH Hydroelectric Generating

Station

>1 and ≤ 30 < 3

Independent

Power Producers

or Self-Producers

PCH* Small Hydroelectric Power

Plant (SHP)

>30 - UHE Hydroelectric Power Plant

Source: ANEEL (National Electric Energy Agency)

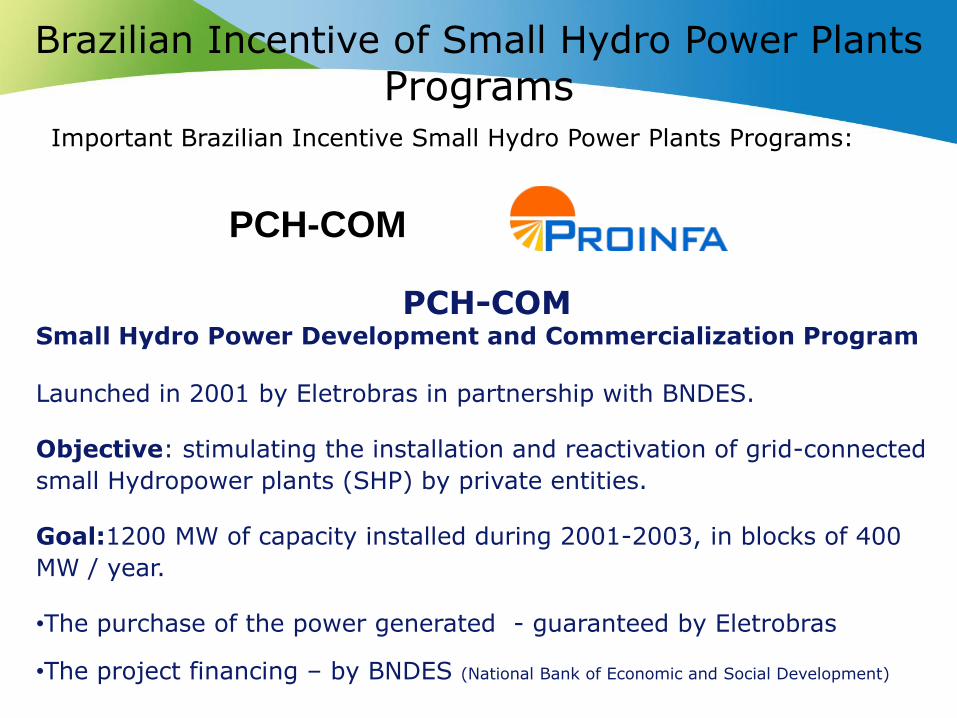

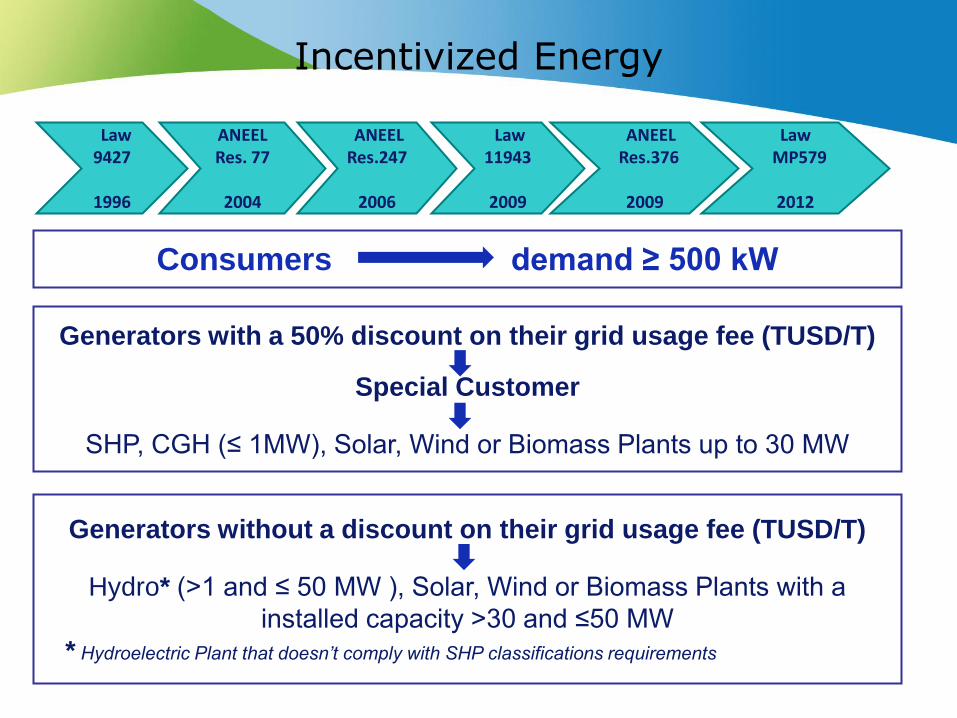

Important Brazilian Incentive Small Hydro Power Plants Programs:

Brazilian Incentive of Small Hydro Power Plants

Programs

PCH-COM

PCH-COM Small Hydro Power Development and Commercialization Program

Launched in 2001 by Eletrobras in partnership with BNDES.

Objective: stimulating the installation and reactivation of grid-connected

small Hydropower plants (SHP) by private entities.

Goal:1200 MW of capacity installed during 2001-2003, in blocks of 400

MW / year.

•The purchase of the power generated - guaranteed by Eletrobras

•The project financing – by BNDES (National Bank of Economic and Social Development)

1.191,24

1.422,92

685,24

1.152,54963,99

533,34

0

500

1.000

1.500

SHP Wind Plant Biomass

MWPROINFA - Installed capacity and total of plants in 31-12-2011

Planned Installed

63 59 54 41

27 19

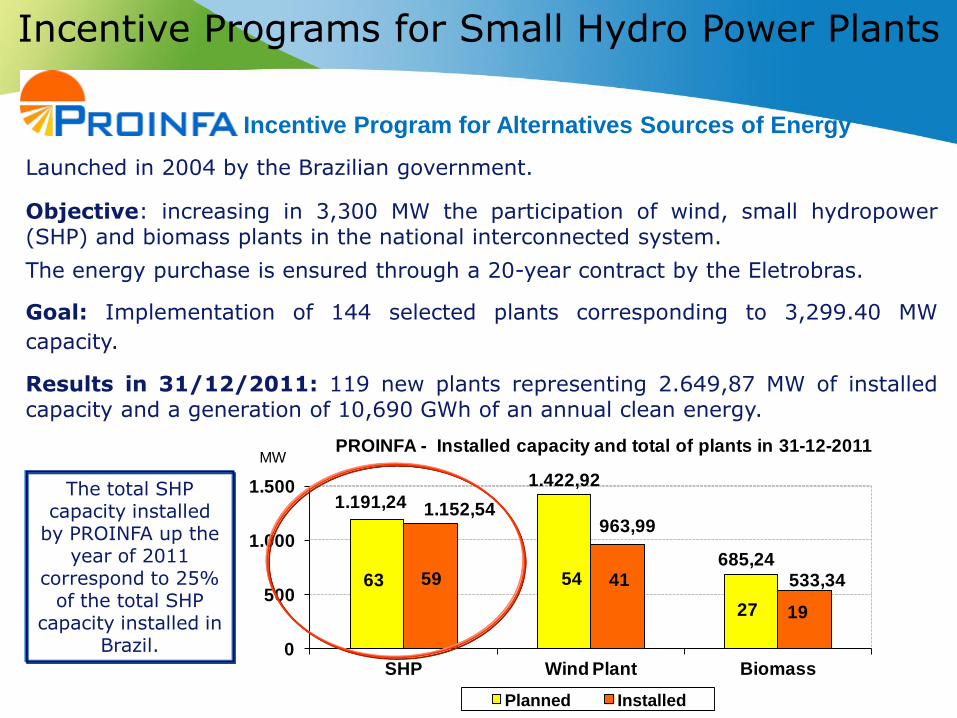

Incentive Programs for Small Hydro Power Plants

Launched in 2004 by the Brazilian government.

Objective: increasing in 3,300 MW the participation of wind, small hydropower (SHP) and biomass plants in the national interconnected system.

The energy purchase is ensured through a 20-year contract by the Eletrobras.

Goal: Implementation of 144 selected plants corresponding to 3,299.40 MW

capacity.

Results in 31/12/2011: 119 new plants representing 2.649,87 MW of installed capacity and a generation of 10,690 GWh of an annual clean energy.

Incentive Program for Alternatives Sources of Energy

The total SHP capacity installed

by PROINFA up the year of 2011

correspond to 25% of the total SHP

capacity installed in Brazil.

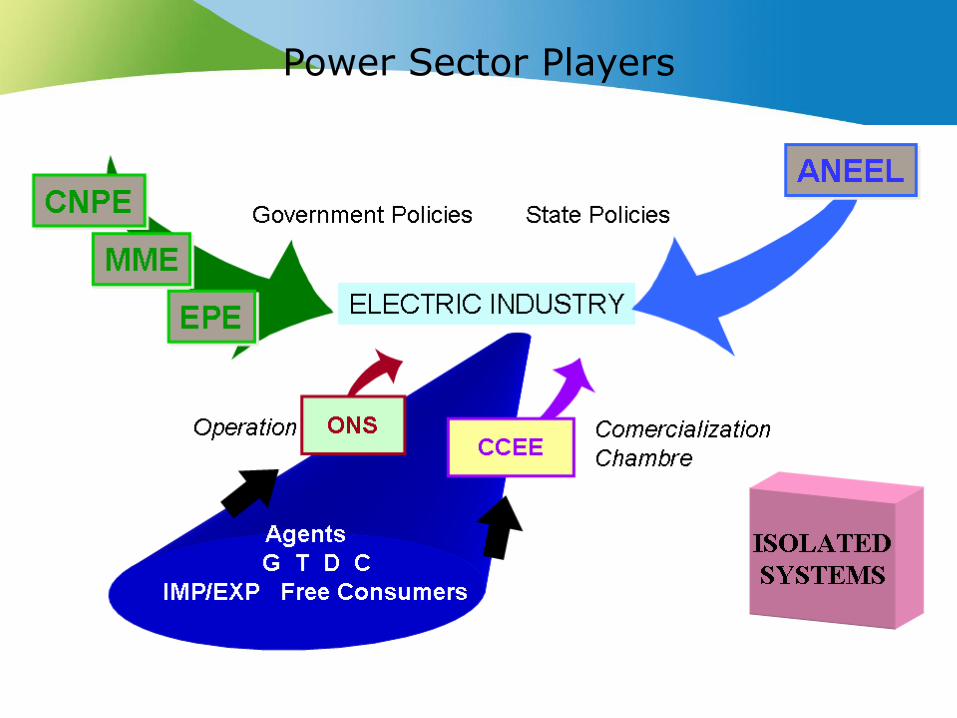

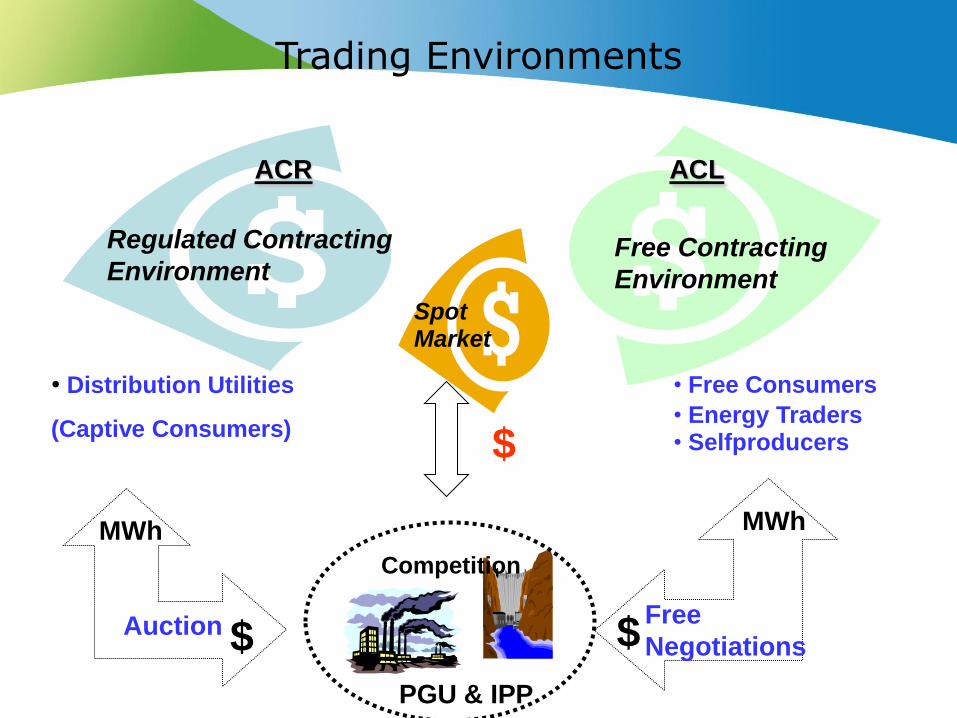

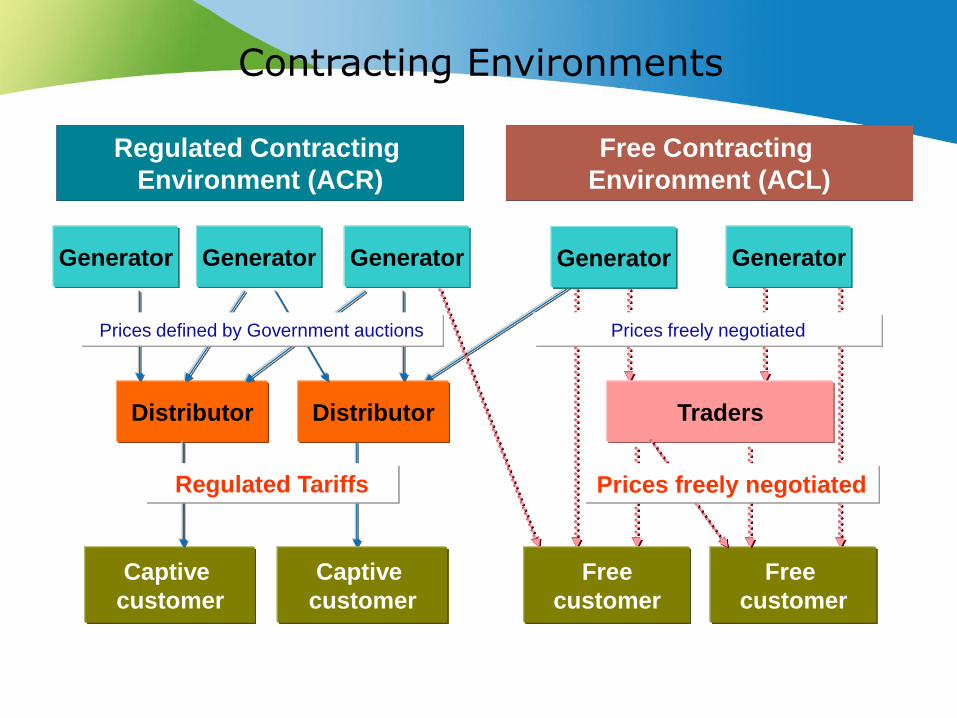

Power Sector Players

• Distribution Utilities

(Captive Consumers)

Regulated Contracting

Environment

ACR

PGU & IPP

Competition

MWh

$ Free

Negotiations

MWh

$ Auction

$

Spot Market

Free Contracting

Environment

ACL

• Free Consumers

• Energy Traders • Selfproducers

Trading Environments

Contracting Environments

Generator Generator Generator

Regulated Contracting

Environment (ACR)

Captive

customer

Captive

customer

Distributor Distributor

Prices defined by Government auctions

Regulated Tariffs

Prices freely negotiated

Generator Generator

Free Contracting

Environment (ACL)

Free

customer

Free

customer

Traders

Prices freely negotiated

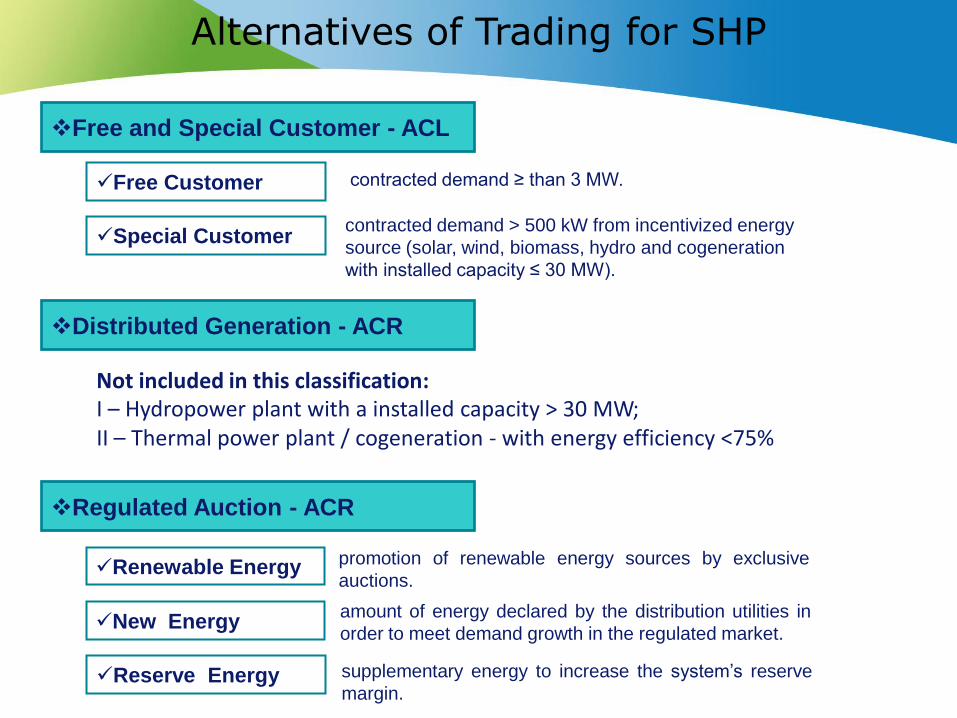

Alternatives of Trading for SHP

Regulated Auction - ACR

Renewable Energy

New Energy

Reserve Energy supplementary energy to increase the system’s reserve

margin.

amount of energy declared by the distribution utilities in

order to meet demand growth in the regulated market.

promotion of renewable energy sources by exclusive

auctions.

Distributed Generation - ACR

Not included in this classification: I – Hydropower plant with a installed capacity > 30 MW; II – Thermal power plant / cogeneration - with energy efficiency <75%

Free and Special Customer - ACL

Free Customer contracted demand ≥ than 3 MW.

Special Customer contracted demand > 500 kW from incentivized energy

source (solar, wind, biomass, hydro and cogeneration

with installed capacity ≤ 30 MW).

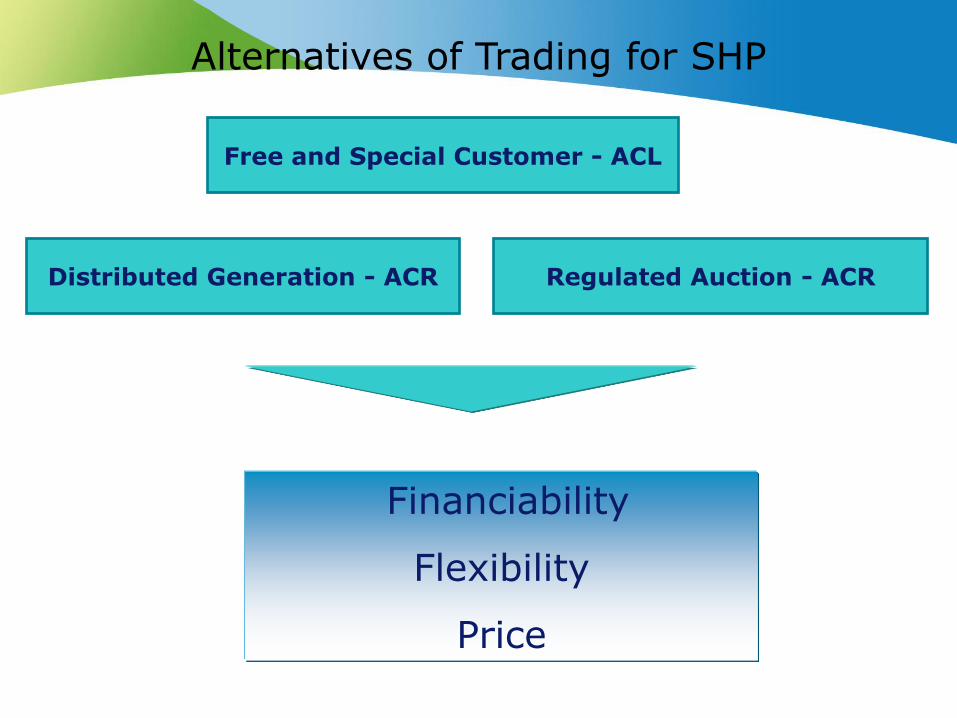

Alternatives of Trading for SHP

Financiability

Flexibility

Price

Regulated Auction - ACR Distributed Generation - ACR

Free and Special Customer - ACL

Consumers demand ≥ 500 kW

Incentivized Energy

Generators with a 50% discount on their grid usage fee (TUSD/T)

Special Customer

SHP, CGH (≤ 1MW), Solar, Wind or Biomass Plants up to 30 MW

Generators without a discount on their grid usage fee (TUSD/T)

Hydro* (>1 and ≤ 50 MW ), Solar, Wind or Biomass Plants with a

installed capacity >30 and ≤50 MW

* Hydroelectric Plant that doesn’t comply with SHP classifications requirements

Law 11943

2009

ANEEL Res. 77

2004

ANEEL

Res.247

2006

Law 9427

1996

Law MP579

2012

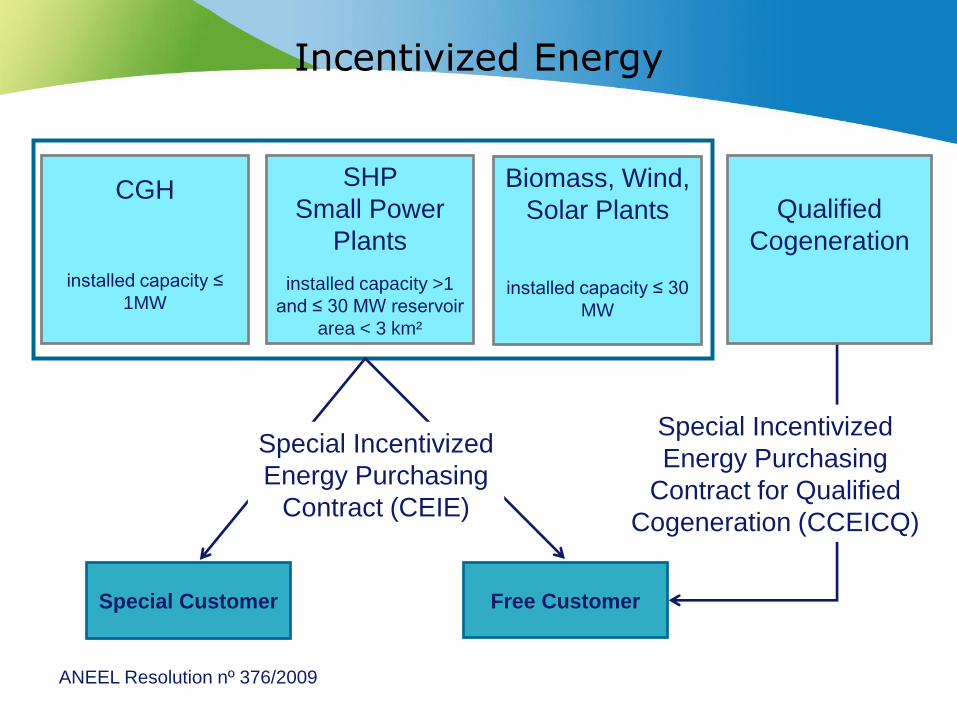

ANEEL Res.376

2009

CGH

installed capacity ≤

1MW

Special Customer Free Customer

Special Incentivized

Energy Purchasing

Contract for Qualified

Cogeneration (CCEICQ)

Incentivized Energy

ANEEL Resolution nº 376/2009

Special Incentivized

Energy Purchasing

Contract (CEIE)

Biomass, Wind,

Solar Plants

installed capacity ≤ 30

MW

Qualified

Cogeneration

SHP

Small Power

Plants

installed capacity >1

and ≤ 30 MW reservoir

area < 3 km²

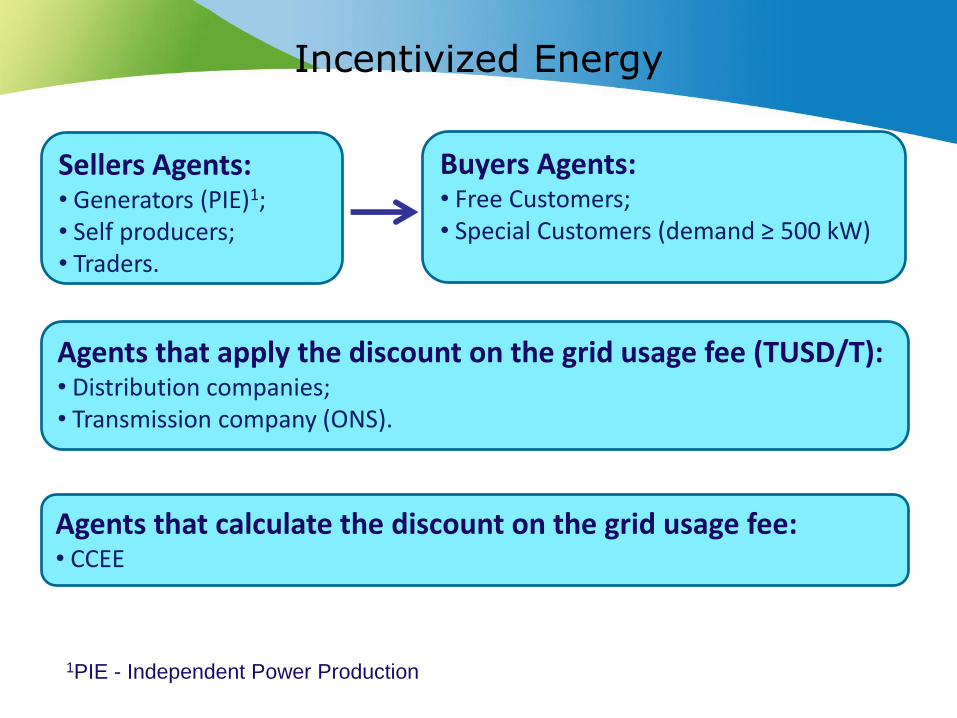

1PIE - Independent Power Production

Incentivized Energy

Sellers Agents: • Generators (PIE)1; • Self producers; • Traders.

Buyers Agents: • Free Customers; • Special Customers (demand ≥ 500 kW)

Agents that apply the discount on the grid usage fee (TUSD/T): • Distribution companies; • Transmission company (ONS).

Agents that calculate the discount on the grid usage fee: • CCEE

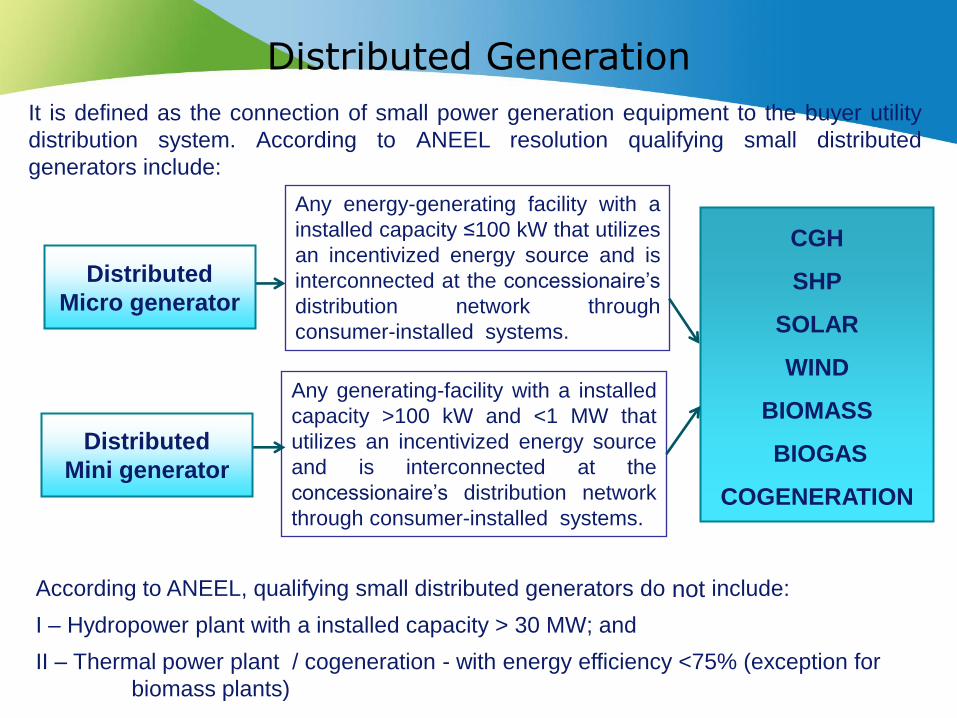

Distributed Generation

It is defined as the connection of small power generation equipment to the buyer utility

distribution system. According to ANEEL resolution qualifying small distributed

generators include:

Distributed

Micro generator

Distributed

Mini generator

Any energy-generating facility with a

installed capacity ≤100 kW that utilizes

an incentivized energy source and is

interconnected at the concessionaire’s

distribution network through

consumer-installed systems.

Any generating-facility with a installed

capacity >100 kW and <1 MW that

utilizes an incentivized energy source

and is interconnected at the

concessionaire’s distribution network

through consumer-installed systems.

CGH

SHP

SOLAR

WIND

BIOMASS

BIOGAS

COGENERATION

According to ANEEL, qualifying small distributed generators do not include:

I – Hydropower plant with a installed capacity > 30 MW; and

II – Thermal power plant / cogeneration - with energy efficiency <75% (exception for

biomass plants)

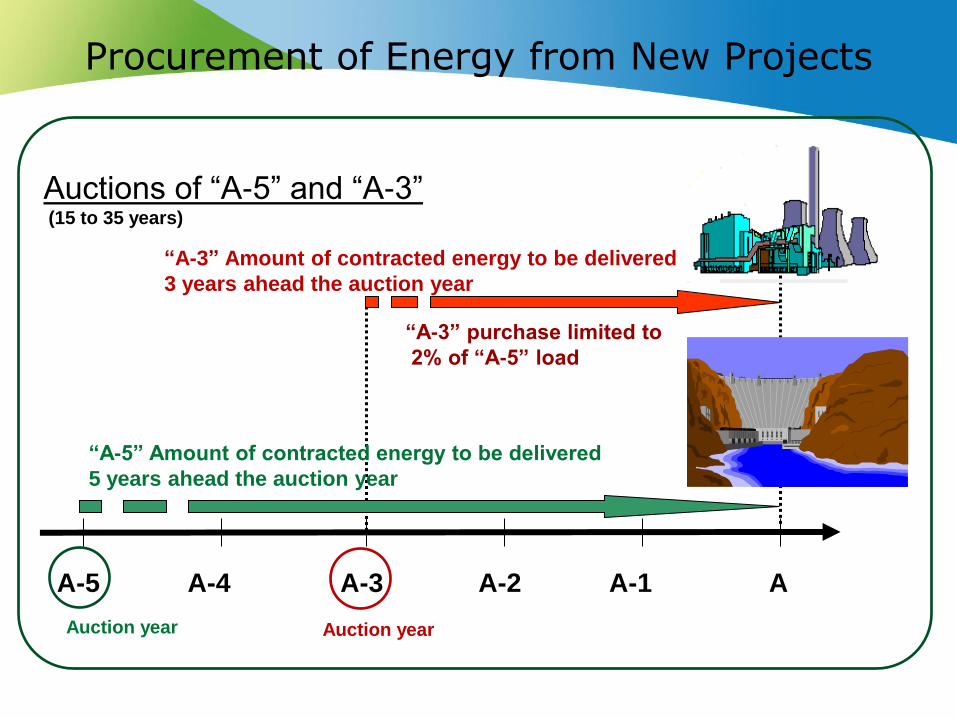

A A-1 A-2 A-3 A-4 A-5

“A-3” purchase limited to

2% of “A-5” load

Auctions of “A-5” and “A-3” (15 to 35 years)

Procurement of Energy from New Projects

“A-5” Amount of contracted energy to be delivered

5 years ahead the auction year

“A-3” Amount of contracted energy to be delivered

3 years ahead the auction year

Auction year Auction year

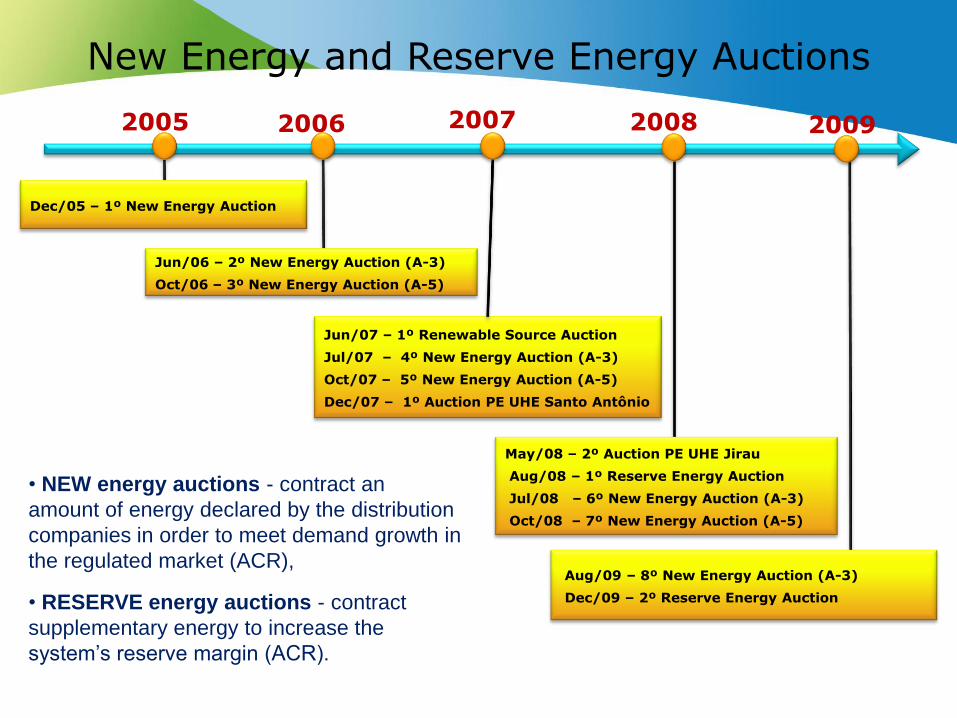

Dec/05 – 1º New Energy Auction

Jun/06 – 2º New Energy Auction (A-3)

Oct/06 – 3º New Energy Auction (A-5)

Jun/07 – 1º Renewable Source Auction

Jul/07 – 4º New Energy Auction (A-3)

Oct/07 – 5º New Energy Auction (A-5)

Dec/07 – 1º Auction PE UHE Santo Antônio

May/08 – 2º Auction PE UHE Jirau

Aug/08 – 1º Reserve Energy Auction

Jul/08 – 6º New Energy Auction (A-3)

Oct/08 – 7º New Energy Auction (A-5)

2005 2006 2007 2008 2009

Aug/09 – 8º New Energy Auction (A-3)

Dec/09 – 2º Reserve Energy Auction

New Energy and Reserve Energy Auctions

• NEW energy auctions - contract an

amount of energy declared by the distribution

companies in order to meet demand growth in

the regulated market (ACR),

• RESERVE energy auctions - contract

supplementary energy to increase the

system’s reserve margin (ACR).

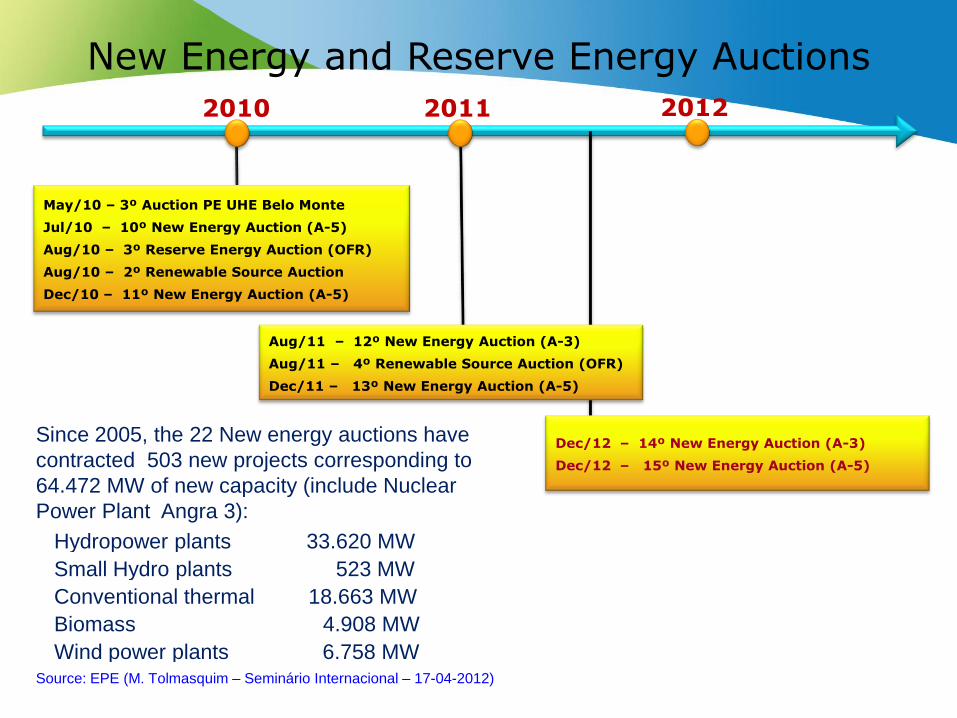

May/10 – 3º Auction PE UHE Belo Monte

Jul/10 – 10º New Energy Auction (A-5)

Aug/10 – 3º Reserve Energy Auction (OFR)

Aug/10 – 2º Renewable Source Auction

Dec/10 – 11º New Energy Auction (A-5)

2011 2010 2012

Aug/11 – 12º New Energy Auction (A-3)

Aug/11 – 4º Renewable Source Auction (OFR)

Dec/11 – 13º New Energy Auction (A-5)

Since 2005, the 22 New energy auctions have

contracted 503 new projects corresponding to

64.472 MW of new capacity (include Nuclear

Power Plant Angra 3):

Source: EPE (M. Tolmasquim – Seminário Internacional – 17-04-2012)

New Energy and Reserve Energy Auctions

Dec/12 – 14º New Energy Auction (A-3)

Dec/12 – 15º New Energy Auction (A-5)

Hydropower plants 33.620 MW

Small Hydro plants 523 MW

Conventional thermal 18.663 MW

Biomass 4.908 MW

Wind power plants 6.758 MW

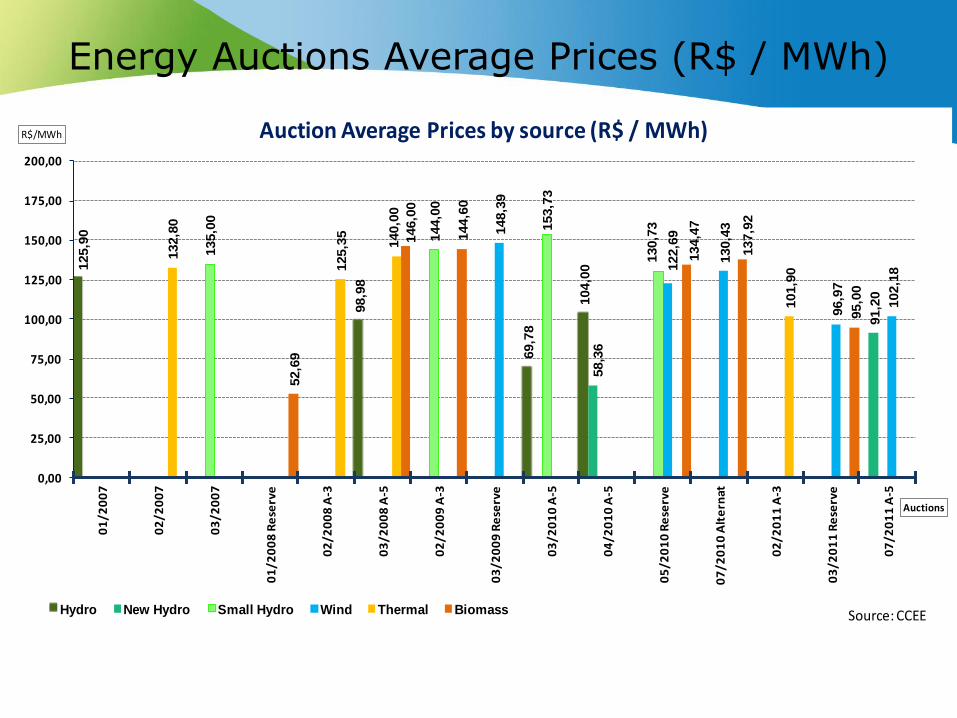

Energy Auctions Average Prices (R$ / MWh) 125,9

0

98,9

8

69,7

8

104,0

058,3

6

91,2

0

135,0

0

144,0

0

153,7

3

130,7

3148,3

9

122,6

9

130,4

3

96,9

7

102,1

8

132,8

0

125,3

5

140,0

0

101,9

0

52,6

9

146,0

0

144,6

0

134,4

7

137,9

2

95,0

0

0,00

25,00

50,00

75,00

100,00

125,00

150,00

175,00

200,00

01

/20

07

02

/20

07

03

/20

07

01

/20

08

Re

serv

e

02

/20

08

A-3

03

/20

08

A-5

02

/20

09

A-3

03

/20

09

Re

serv

e

03

/20

10

A-5

04

/20

10

A-5

05

/20

10

Re

serv

e

07

/20

10

Alt

ern

at

02

/20

11

A-3

03

/20

11

Re

serv

e

07

/20

11

A-5

R$/MWh

Auctions

Auction Average Prices by source (R$ / MWh)

Hydro New Hydro Small Hydro Wind Thermal Biomass Source: CCEE

Energy Relocation Mechanism (MRE) is a financial mechanism based on the transfer of exceeding energy generated by all MRE members to those members who do not reach their corresponding assured energy.

Objectives of this mechanism:

• sharing the hydrological risk among the MRE participants;

• optimizing energy supply of the National Interconnected System.

The Assured Energy of a hydroelectric plant is issued for each plant by Ministry of Mines and Energy, and serves essentially to:

• establish an upper limit for energy supply contracts;

• define the share of each generating plant on the total amount of energy generated in the system by hydro plants.

Energy Relocation Mechanism (MRE)

Verified Energy

Short Term Spot

PPA

CCEE accounting is based on differences between the amount of contracted energy and the amount of verified energy

Spot Market

Alternatives of Trading for Small Hydropower Plants (SHP)

Contracting Environment Financiability Flexibility Price

Distributed Generation - ACR High Medium Medium

Regulated Auction - ACR High Low Low

Free and Special Customer - ACL Medium High Medium