Embed Size (px)

Citation preview

The Management ofService centers

NCURA REGIONS VI and VII CONFERENCE

April 7, 2009

2© 2007 BearingPoint, Inc.

Authors

This document is protected under the copyright laws of the United States and other countries. This document contains information that is proprietary and confidential to BearingPoint, Inc., its subsidiaries, or its alliance partners, which shall not be disclosed outside or duplicated, used, or disclosed in whole or in part for any purpose other than to evaluate BearingPoint, Inc. Any use or disclosure in whole or in part of this information without the express written permission of BearingPoint, Inc. is prohibited.© 2007 BearingPoint, Inc. All rights reserved.

•Bob Klein•Consulting Associate•Higher Education/ Academic Medical Centers Practice •Mobile +1-510-847-0525•[email protected]

3© 2007 BearingPoint, Inc.

Introduction- Service Centers

Importance of structured program

Components of program

Policy

Procedures

Roles and responsibilities

4© 2007 BearingPoint, Inc.

Introduction- Service Centers

5© 2007 BearingPoint, Inc.

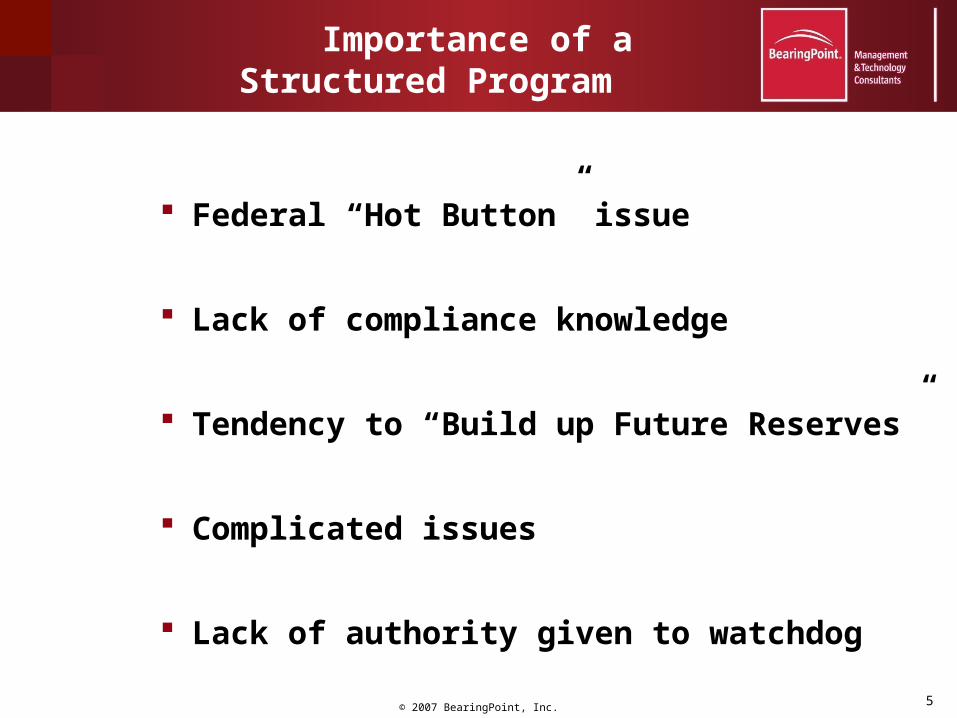

Importance of a Structured Program

Federal “Hot Button” issue

Lack of compliance knowledge

Tendency to “Build up Future Reserves”

Complicated issues

Lack of authority given to watchdog

6© 2007 BearingPoint, Inc.

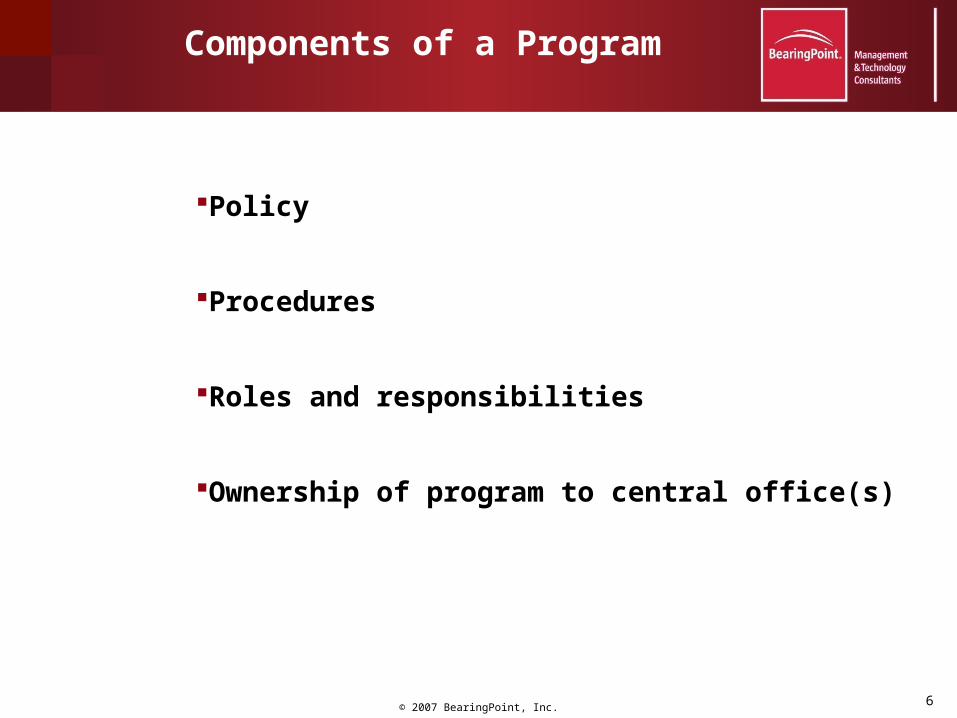

Components of a Program

Policy

Procedures

Roles and responsibilities

Ownership of program to central office(s)

7© 2007 BearingPoint, Inc.

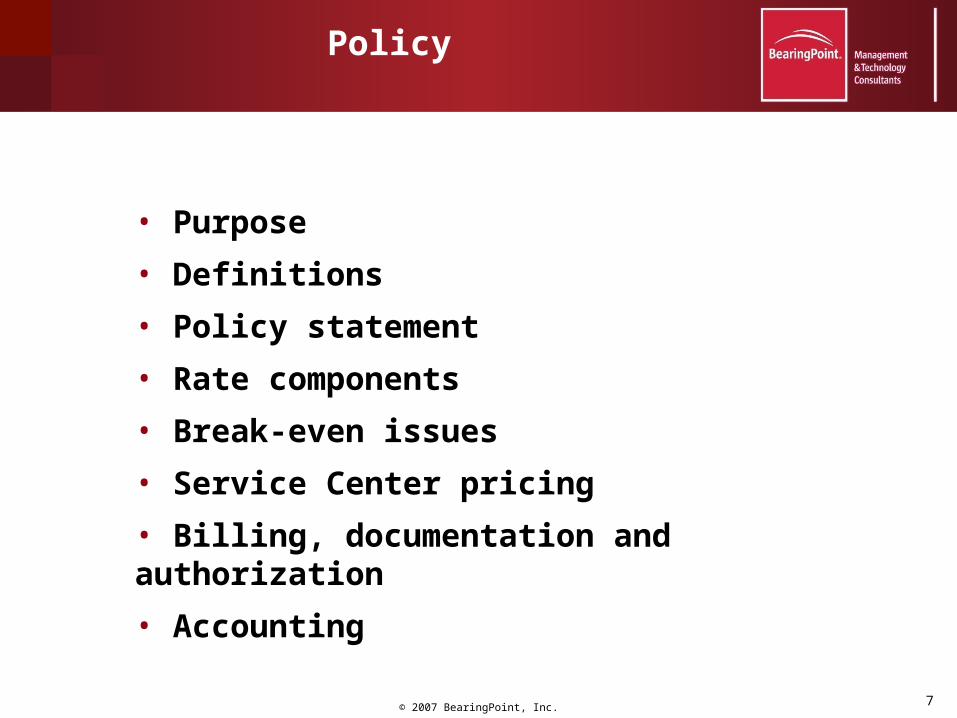

Policy

• Purpose

• Definitions

• Policy statement

• Rate components

• Break-even issues

• Service Center pricing

• Billing, documentation and authorization

• Accounting

8© 2007 BearingPoint, Inc.

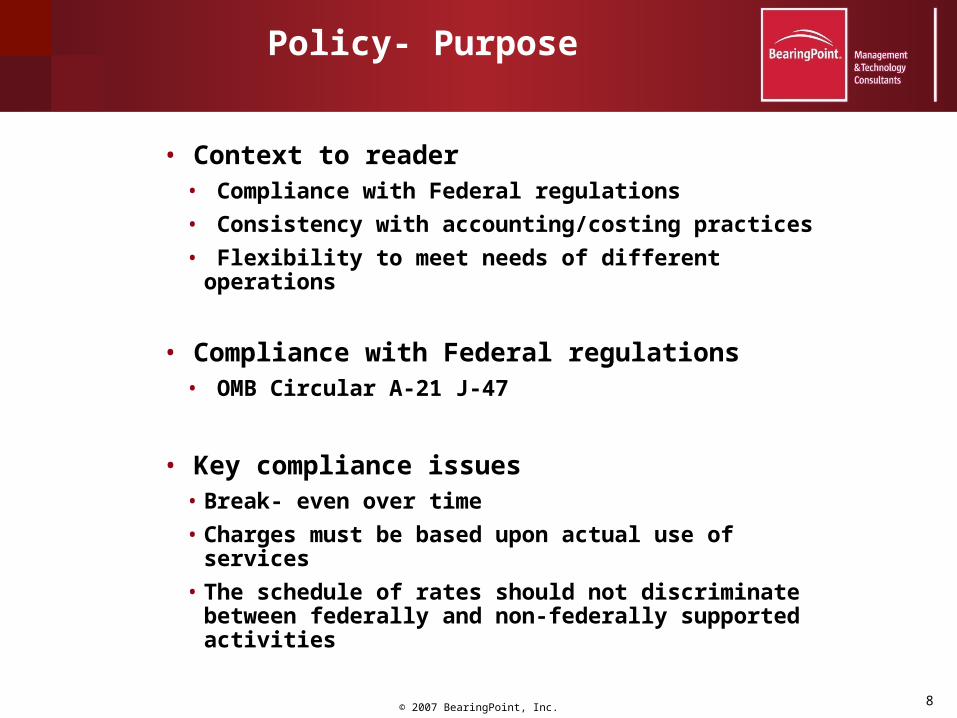

Policy- Purpose

• Context to reader• Compliance with Federal regulations

• Consistency with accounting/costing practices

• Flexibility to meet needs of different operations

• Compliance with Federal regulations• OMB Circular A-21 J-47

• Key compliance issues• Break- even over time

• Charges must be based upon actual use of services

• The schedule of rates should not discriminate between federally and non-federally supported activities

9© 2007 BearingPoint, Inc.

Policy- Purpose (Continued)

• Identification of different exposures• Possible pay-back to Federal Government

• Possible adverse publicity for institution

10© 2007 BearingPoint, Inc.

Policy- Definitions

Service Center Provides goods or services

Supported by re-charges

Specialized Service Facility Highly complex or specialized activity

Activity level material to the institution

Auxiliary Services Generally support students, faculty, alumni

and staff in a personal capacity

11© 2007 BearingPoint, Inc.

Policy- Definitions (Continued)

Internal Users• Users with sources of funds from within the

institution

• Can include closely affiliated institutions

External Users• Users with sources of funds from outside the

institution

• Different pricing policy

Capital Equipment• Utilize institutional definition of capital equipment

12© 2007 BearingPoint, Inc.

Policy- Policy Statement

• Rate components• All costs related to the activity• Included in the rate calculation

• Direct personnel• Salary and wages of personnel directly related to the

service center activity

• Administrative staff• Salary and wages of personnel supporting or

managing the service center activity

• Fringe benefits

13© 2007 BearingPoint, Inc.

Policy- Policy Statement (Continued)

• Materials and supplies•Rates should not include year end build up of inventory

• Other expenses

• Capital equipment depreciation•Rates should not include the cost of the equipment•Depreciation can be charged to the service center

• Interest on debt- funded equipment•Must be externally funded

14© 2007 BearingPoint, Inc.

Policy- Policy Statement (Continued)

•Facilities costs• Service Centers’ space costs can be included in indirect

cost pools, allocation based upon use•Specialized Service facilities must build space costs into

rates or be subsidized by the institution

•Unallowable costs•Must be excluded from the rates

15© 2007 BearingPoint, Inc.

Policy- Break-even

• Surpluses•Generally carry forward and adjusted in the rates

• Deficits•Smaller deficits carried forward and adjusted in the rates

•Larger deficits may need to be funded by the PI or department head

• Long term Break- Even agreement•Alternative costing arrangements may be worked out

with the cognizant Federal agency.

16© 2007 BearingPoint, Inc.

Policy- Break even (Continued)

•Transfers•Important to monitor that surpluses are not transferred to general use accounts

17© 2007 BearingPoint, Inc.

Policy- Pricing

• Non- Discriminatory rates•Same rate for all internal users (excludes special

Federal grants and subsidized users)

•Subsidized users•Rates must be calculated on total units of output

•Generally easier to charge full amount to funding account

18© 2007 BearingPoint, Inc.

Policy- pricing (Continued)

•External users•Must be charged at least internal user rate

•Can have surplus from external users

•Sales tax applicable if they are not tax- exempt

• Pricing of multiple services•No cross subsidization allowed

•Generally easier to track each service separately

19© 2007 BearingPoint, Inc.

Policy- Billing, Documentation and Authorization

• Billing timing•Best to require process billing at least monthly

•If occasionally, then can have problems preparing FSRs

•Billing should occur after service is performed

• Invoice documentation•Nature of the services

•Number of units provided

•Amount charged per unit

20© 2007 BearingPoint, Inc.

Policy- Billing, Documentation and Authorization (Continued)

•Rate Schedule documentation•Files should contain calculations of rates

• Charge authorization•Service center manager should have received approval for services provided

21© 2007 BearingPoint, Inc.

Policy- accounting

• Account size threshold•Determine institutional activity level for a separate service center account

• Set up of account•Determine components required from service center manager

• Establish a Service Center or Specialized Service Facility account

•Confirm all institutional requirements are met

22© 2007 BearingPoint, Inc.

Procedures

• Initial budget approval

• Monthly financial reports

• Quarterly/ annual breakeven reviews

• Annual budget review

• Capital/ depreciation accounts

• Subsidized users

• Multiple Services

23© 2007 BearingPoint, Inc.

Procedures- Initial Budget Approval

• Institutional budget forms to include:•Direct expenditures estimate

•Capital costs

•Types of services

•Types of users

•Units of production estimate

•Service unit charge

•Location

• Approvals•Budget Office

•Restricted Funds Department

•Financial officer for subsidies, deficits, etc.

24© 2007 BearingPoint, Inc.

Procedures- Reports/ Break-even Reviews

• Monthly financial reports•Coordinated controls from restricted funds department (RFD)

•Breakeven and compliance issues

•Special reports to help track activity

• Quarterly reviews•Summary reports identify break-even variances

•Administrators identify plan for outliers

•Break even plans approved by Financial Officer

25© 2007 BearingPoint, Inc.

Procedures- Annual Budget/ Capital

• Annual budget submitted for institutional review• Restricted Funds Department

• Budget Office

• Significant variances from plan approved by Financial Officer

• Capital Purchases/ Depreciation• Use institutional definition of capital purchase

• Use institutional standard for depreciation calculation

• Separate account to purchase equipment

• Charge depreciation to fund separate capital account

26© 2007 BearingPoint, Inc.

Roles- Service Center Manager

27© 2007 BearingPoint, Inc.

Roles- Service Center Manager

•Create initial budget and process paperwork

•Estimate number of units of production and sets rate

•Obtain Department Head approval for activity and budget

•Monitor progress of account set-up

•Review break-even and rates on a periodic basis

•Submits annual information/ budget requested by institution

• Keeps center compliant with Federal and institutional policy

28© 2007 BearingPoint, Inc.

Roles- Department Head/ Budget Office

• Department head responsible for financial position

• Approve initial activity and budget

• Funds excessive deficits

•Ensures compliance with institutional policy

• Budget Office initially approves service center budget

• Reviews annual budget submission with rate setting and breakeven analysis

29© 2007 BearingPoint, Inc.

Roles- Costing Department

30© 2007 BearingPoint, Inc.

Roles- Costing Department

• Reviews initial budget for compliance relating to:

• Estimated break-even reasonable

• Structure of billing

• Special items of cost, i.e. capital purchases

• Periodically monitors compliance, including break-even

•Provides training for user community

•Assigns facility costs to Specialized Service Facilities

•Reviews special requests to Financial Officer, i.e. deficit carryovers

31© 2007 BearingPoint, Inc.

Roles- Senior Financial Manager

32© 2007 BearingPoint, Inc.

Roles- Senior Financial Manager

•Overall financial and compliance responsibility for Service Centers

•Approves initial and annual spending plans

•Directs review process

•Ability to say “No”

33© 2007 BearingPoint, Inc.

Wrap Up/ Questions

•Questions/ Comments