Embed Size (px)

Citation preview

The Logic of Collective Action Revisited

Ian BensonSchool of Education

Froebel CollegeUniversity of Roehampton

ABSTRACTMancur Olson’s “Logic of Collective Action” predicts thatvoluntary action for the common good will only happen insmall groups. His theory of the structure and behaviourof organisations fails to account for the UK Labour Party’spromotion of, rejection and ultimate compliance with itsPolitical Parties Act (PPERA). I propose a revised com-putational theory to explain this behaviour. It negates keytenets of Olson’s work: that consumption of a common goodby one member inevitably reduces the quantity available toanother and that negotiation between members does not ingeneral affect a decision to work for the common good. Theapproach has application in private and public sector servicedesign.

Categories and Subject DescriptorsH.4 [Information Systems Applications]: Miscellaneous

KeywordsComputer-Mediated Communication; Social and Legal is-sues; Analysis Methods (Task/Interaction Modeling); De-sign Methods (Scenarios, Storyboards); Participatory De-sign; User and Cognitive models; Multidisciplinary Design;Software Engineering Methods - Mathematical / Proof-Based;Service Design

1. INTRODUCTIONIn his seminal work “The logic of collective action: public

goods and the theory of groups” economist Mancur Olsonsuggests that there are essentially two, mutually exclusive,forms of collective action - voluntary or coerced. His the-ory predicts that voluntary action for the common good willonly arise in small groups and then only in certain circum-stances. Coercion is necessary in almost every case becauseeach organisation produces goods (relationships) that arecommonly available to all their members. So “a state isfirst of all an organisation that provides public goods for

Permission to make digital or hard copies of all or part of this work forpersonal or classroom use is granted without fee provided that copies arenot made or distributed for profit or commercial advantage and that copiesbear this notice and the full citation on the first page. To copy otherwise, torepublish, to post on servers or to redistribute to lists, requires prior specificpermission and/or a fee.TBACopyright 2021 Sociality Mathematics CIC X-XXXXX-XX-X/XX/XX ...$.

its members, the citizens” and “other types of organisationssimilarly provide collective goods for their members.” [Olson1965] If organisations fail to provide these benefits then theywill eventually die. Since common goods are by definitionavailable without constraint to qualified individuals (citi-zens, employees) there is no incentive for any one individualto participate in the work of the organisation voluntarily.

We revisit Olson’s key assumptions on the behaviour ofpeople in organisations. These are:

1. that consumption of a common good by one memberreduces the quantity available to another and

2. that negotiation between members does not in generalaffect a decision to work for the common good

I propose an alternative computational theory and illus-trate this through a study of membership activity to recordand report political donations of volunteer effort, cash orkind (see http://www.electoralcommission.org.uk ).

The paper is in three parts.

• In Section 2, we recall the vocabulary of organisationalobjects, operations and relationships that Olson devel-oped to reason about membership associations. Theserepresent why an organisation exists (we call it an ac-counting unit) and those who are involved (donors,etc). We recount the criteria people adopt when theydecide whether to work for a common good, togetherwith Olson’s group cost/benefit analysis of the circum-stances in which they may choose to participate or ab-stain. Olson rejects negotiation as a factor that canaffect organisational behaviour. We reproduce his ar-gument by reference to Winograd and Flores’ Conver-sation for Action[Winograd & Flores 1986]. This isa ‘choreographed dance’ between two people witnessedby a third in which bilateral speech acts set out time,cost and quality conditions of satisfaction for a task.

• Then, in section 3 we follow Olson’s generalisationfrom a single unit to a group of units and apply theresulting analysis to the work of the Labour Party ac-tivists. Labour exhibits many of the characteristicspredicted by Olson and observed by Putnam [Putnam2000] and Resnick [Resnick et al. 2000], such as de-clining levels of membership and membership activ-ity. In our study the common good is the need for allunits to comply with the Political Parties, Electionsand Referendums’ Act (PPERA, 2000). According toOlson since the Party is not a small organisation, its

arX

iv:2

105.

0198

1v1

[cs

.SI]

5 M

ay 2

021

units should either conform to PPERA through co-ercion or additional legal sanctions are needed. Wedescribe the intention of PPERA and its sanctions,analyse the work that each Party unit needs to do asa generalisation of a Conversation for Action (CfA),and reproduce an account of their behavior from theUK national press. We observe a pattern of reluctantcompliance that cannot be explained within Olson’sframework, and conclude that his assumptions aboutthe nature of decision making and the common goodneed to be revised.

• To explain what happened we need to look again at Ol-son’s account of negotiation within and between units.In Section 4.1 we introduce a correct by constructioncomposition of CfA to form a collective decision pro-tocol – a quarterly cycle of inter-unit work. The con-sent of initially reluctant Party units was ultimatelywon by building a system for recording and reportingthat gives confidence that all recorded donations areproperly reported [Carpenter et al. 2004]. Because therecording process highlighted those units that were notcorrectly reporting donations it induced them to fallinto line.

We found that accountability was ultimately achieved throughnegotiation that built confidence in the correctness of thedecision process. Confidence is a category of common goodessential to the operation of teams, markets and systems.Furthermore, one unit’s confidence is not gained at the ex-pense of another. This negates Olson’s key tenets – that or-ganisational units only enjoy common goods at each other’sexpense and that negotiation does not affect behaviour.

1.1 Related WorkBenson et al [Benson et al. 1990] and Ciborra [Ciborra

1993] set out this approach to multidisciplinary design bycombining institutional economic analysis with software en-gineering methods. Winograd and Flores [Winograd & Flo-res 1986] pioneered and Weigand [Weigand 2006] reports onthe coming of age of Language/Action theory. Milner [Mil-ner 1989] illustrates how to model and reason about com-putation as communication with concurrency, and Pavlovic[Pavlovic & Mislove 2006] describes how to exploit the dual-ity of operational semantics and logic in a modern softwareengineering practice that uses tests (we call them decisions)as specifications.

2. OLSON’ S LOGIC OF COLLECTIVE AC-TION

Mansur Olson’s analysis of the conditions for successfulcollective action for a common good is shown in Figure 1[Olson 1965, p 32].

He considers an organisational accounting unit AU, thepeople involved (such as donorA, donorB) and the decisionsδ(donorA, P ), δ(donorB , P ) that A, B make to participateat some level of production P. δ( , ) is a predicate, a logicalfunction that returns true or false.

The graph shows his group cost/benefit analysis. The yaxis is cash ($) and the x axis the level of production (P).Olson plots the common good – that is the total value equalto

∑donor

value(donor, P ) – as a straight line and the cost

$

PV W

total value(P)

value(donor_A,P)

cost(P)

Figure 1: Olson’s group cost/benefit analysis (Value vs Pro-duction level)

of production cost(P) as a J shaped graph, with the initialfixed cost of the first unit cost(0) increasing with the volumeP produced.

2.1 The structure of negotiation in small groupsOlson considers two cases: a donorA whose share of the

total production value exceeds cost(P) at a level of pro-duction in the range [V,W], and a donorB whose share isnever greater than cost(P). We take Winograd and Floreslanguage/action theory as a model for negotiation and bar-gaining in small groups. They draw on Searle’s speech actsto classify utterances into a small number of categories whichfall into a particular pattern in discourse. The structure ofa typical Conversation for Action is shown in Figure 2, astate change protocol in which arcs are labelled by person(A or B) and type of speech act.

Figure 2: Conversation for Action

Olson assumes that there are only two classes of donor.He dismisses the possibility of “strategic bargaining” whichmight induce two donors to collaborate to meet the cost(P).He argues that the incentive for anyone to actively partic-ipate in creating the common good only exists in the cir-cumstance of donorA and then only in the interval [V,W].He says that bargaining will not be a viable alternative as

donorA and donorB will inevitably differ in the proportionof the common good that they will gain and the net ben-efit of meeting the cost of this negotiation. Consider thecase in which A gains much more than B from the com-mon good. All A can do to get B to comply is to threatenthe smaller member saying, in effect, if you do not providemore of the common good I will provide less myself, and youwill be worse off as a result. This is an empty threat sinceB:Counters that A will suffer more from the reduction inproduction since A has more to gain. Another factor thatmakes the threat less credible is that the maximum amountof the common good than B can contribute is small, andmay ourweigh A’s cost of bargaining. This is the oppositecase for B who has an incentive to prolong the negotiation,hence Olson predicts either B:Rejects or A:Withdraws [Ol-son 1965, p 12].

One consequence of Olson’s analysis is that the size ofa group will influence the likelihood that it will provideits members with a collective good without coercion (apartfrom access to the common good itself). In general it is onlysensible for individuals to engage voluntarily in group activ-ity at certain stages in the inception phase of small groupswhen the cost of production can be met by one memberalone. Once a group becomes established then each newmember will benefit from the common good without activeengagement. He argues that this is why people may vote butdo not join political parties (unless they seek office them-selves), why trade unions need the coercion of the “closedshop” and why the state needs laws of taxation to survive.His analysis provides a plausible explanation for Putnam’sobservations on the decline of mass associations [Putnam2000].

3. “LABOUR CHIEF SAYS HE FEARS JAILOVER SLEAZE”

In this section we apply Olson’s analysis to the group ofaccounting units that do the work of the UK Labour Party.At first glance the Labour Party exhibits many of the char-acteristics predicted by Olson and observed by Putnam –from decreasing levels of membership to declining member-ship activity. However we find on closer inspection thatOlson’s theory of groups cannot account for the observedpattern of behaviour (section 3.4). This leads us to questionhis assumptions about the nature of the common good andthe significance of negotiation.

3.1 Olson’s theory of groupsOlson recognises that any organisation or group will usu-

ally be divided into subgroups or factions that may be op-posed to one another. Nevertheless he argues that this doesnot weaken his assumption that organisations exist to servean overarching common interest of their members. “Theassumption (of common interest) does not imply that intra-group conflict is neglected. The opposing groups in an or-ganisation ordinarily have some interest in common (if notwhy would they maintain the organisation?), and the mem-bers of any subgroup or faction also have a common interestof their own.” [Olson 1965, p 13]

He adapts his framework to account for the conflict withingroups and organisations by considering “each organisationas a unit only to the extent that it does in fact attemptto serve a common interest, and considers the various sub-

groups as the relevant units with common interests to ana-lyze the factional strife.” [Olson 1965, p 13]

In our study the common good is a need for every account-ing unit to comply with the Political Parties, Elections andReferendum’s Act (PPERA, 2000) passed into law by the1997 Labour Government. This act was a political responseto a series of Tory funding scandals. The law came intoeffect in February 2001. We review the goal of PPERA,its sanctions and the work that needs to be done to ensurecompliance.

The objective of the law was to record and aggregate do-nations received from a donor at any of approximately 700accounting units every calendar quarter and report if theytotal more than a certain amount. Responsible party offi-cers, a new statutory role, could be fined up to £5,000 oneach count of non compliance and jailed for a year (althoughimprisonment was considered unlikely). The circumstancesin which donations are reported depend on which unit re-ceives the donation, how much the donor has given thatyear, and when it was accepted.

In order to comply with the Act the Party superimposedstatutory officers and accounting units on its constitutionalstructure of Constituency Labour Parties (CLP), trade unionliaison organisations (TULO), national parties (Wales, Scot-land) and English Regions. These new statutory posts arecalled Responsible Officers. The statutory reporting struc-ture, and the relevant thresholds for reporting each quarteron donations received at a accounting unit from a donor areshown in Figure 3. This shows the parallel and sequentialnature of decision making that the Party needs to perform.

3.2 Task Analysis: Roles and Decisions

TULO1 >1kCLP1 >1K Wales>1k Scotland >1k

Head Office >5k

National (S62) Reporting >5k

High Value ... English RegionSE Region other HO Unit

Unit Visible to Electoral Commission

Internal Units

..CLPn >1K TULOn >1k

report if Σ (below)breaches threshold

donations

Figure 3: Composition of Quarterly Decision Protocols

Every calendar quarter the Party Funding Manager takesfour steps to prepare the Party’s Report to the ElectoralCommission. These decision rules are in compliance withStatute and Regulations and the practice that has developedsince 2001. They are:

1. For the Head Office accounting unit, for each donorand donation, test if the amount donated is recordablefor reporting (that is more than £200), if not

2. for each local accounting unit, for each donor and do-nation, test if the amount donated is recordable forreporting, if not

3. for each donor and donation aggregate the total amountdonated this year to date and test if the aggregate ex-ceeds the National (also known as the virtual AU orSection 62(12)) threshold. If so report in aggregaterecordable donations (ie those not reported in steps

(1) or (2) or in prior quarters) to the Electoral Com-mission, and the constituent donations thereof in aninternal Section 62 audit report, and

4. finally, record by donor and accounting unit those do-nations that are not recordable in an internal CarriedForward report

3.3 Test PathsThe Quarterly decision tree in Figure 4 shows how we can

encode the reporting state of a donor to an accounting unitin a period using just two predicates. When interpreted inthe context of test data, predicates are a logical functionof accrued data. Since there are 3 possible outcomes eachperiod, we need as a minimum two predicates to encode thedonation reporting state for each donor, unit and quarter.

A donor’s report with respect to a physical accountingunit consists of zero or more quarters in which all the record-able donationsa are carried forward (c), followed by zeroof more quarters of Section 62(12) reporting (s), followedby zero or more Quarterly Reports that show their dona-tions as breaching the threshold of a physical accountingunit (AU) (r). We can encode these constraints as a per-missible path by adopting Party Funding Manager StephenUttley’s speech act notation: c for a quarter in which re-porting is carried forward, s for a Section 62(12) report andr for a regular quarterly report.

False

False

True

True

value to QuarteryReport

value to S62_audit value to CF

δ(au ,p)d

δ*(au ,p)d

Figure 4: Individual Donation Decision Tree (period p,donor d, unit au)

A path name is a permissible path string, consisting offour letters, corresponding to the sequence of transitionstaken to reach a terminal state (Figure 8). A path nameis built up by appending the speech act taken each quar-ter to the end of the “path string” eg, c, cs, csr, csrr. Wecan conveniently abbreviate these 15 path names using thehexadecimal numerals 1 to F as shown in Figure 5.

3.4 Observed BehaviourThe Funding Manager’s decision logic relies on correct

recording. It is a matter of public record that this did nothappen in the first two annual cycles of reporting.

The Guardian newspaper reported on 13th February 2003that “All the political parties have been given a warning bySam Younger, the chairman of the Electoral Commission,that they must comply with regulations and register dona-tions in time or face prosecution. The warning comes after

Figure 5: AUdonor Paths through Reporting Space

Labour failed to report £236,952 on time for the first quar-ter of 2002, and £1,815,549 for the second quarter. Thesums were eventually reported in the third quarter. An-other £20,192 which Labour should have been reported pre-viously was included in the returns for the fourth quarter.The Conservatives also found themselves in trouble with thecommission after refusing to disclose the name of their newbiggest donor.” [Henke 2003]

Under the headline “Labour chief says he fears jail oversleaze” the Kevin Maguire [Maguire 2003] reported:

Labour’s general secretary has warned he couldbe heavily fined or even jailed over a growingnumber of breaches by the party of an anti-sleazelaw Tony Blair introduced to clean up politicaldonations.

David Triesman admits in an internal report,marked “private and confidential” and seen bythe Guardian, that Labour’s electoral prospectswill be harmed if the full extent of the crisis ismade public.

Boasting that it has been largely kept un-der wraps except in Scotland, he says the “prob-lems are getting worse” with more ConstituencyLabour Parties failing to file accounts or declaredonations worth £1,000 or more.

Mr Triesman describes the position as “seri-ous and intolerable” and accepts that it is em-barrassing as well as illegal when the party failsto comply with a law introduced by Labour aftera series of Tory funding scandals.

“Politically it is portrayed as party illegalityin relation to our own legislation.

“We have managed media effectively exceptto any great degree in Scotland where it is simplyhostile and will now have an impact on electoralprospects,” says the Triesman report.

“In strict legal terms, matters are still moreserious. First, we are already at risk of signifi-cant fines. Second, I am increasingly at risk ofcriminal action and I assess this risk as higher ifno credible steps are taken to do a huge amountmore than at present to demonstrate that I amnot willingly or recklessly failing to intervene.”

An investigation by Labour’s Old Queen StreetHQ into the finances of local Labour parties dur-ing the 18 months to September 2002 is under-stood to have uncovered more than 100 potentialbreaches of the law.

Donations worth more than £1,000 must bedeclared but the inquiry discovered an alarmingnumber of constituencies either did not file ac-counts or lodged inaccurate returns.

The general secretary is to propose at thismonth’s Labour spring conference in Glasgow thata single party bank account be introduced forconstituencies to allow officials to offer adviceto voluntary treasurers and ensure accounts arefiled correctly.

Mr Triesman wrote a letter of apology lastmonth to Sam Younger, Chairman of the Elec-toral Commission set up under the Labour legis-lation to regulate donations, and the Whitehall-appointed body is due to report next week.

3.5 Transition System Semantics for Work-loops

To encourage correct recording the Funding Manager spon-sored the creation of a system for computer-mediated com-munication to overcome the breakdowns in recording thathad put the General Secretary at risk. To develop a testsuite specification the structure and behaviour of the Partywas storyboarded with two commonplace diagrams. Thestructure of decision making was drawn with the conventionsof the London Underground: train lines represent phases ofa Conversation for Collective Action (these are the samephases as those in the CfA), interchange stations repre-sent decisions, and data is represented as coloured tokens.Coloured “fare zones” represent the roles of Responsible Of-ficer and Funding Manager. Decision making at each in-terchange station is drawn as an “act-decide transition sys-tem.” That is, a transition system labeled by speech acts,whose states are marked by formulae true in the prior state.The organisation of the Party as a whole is then taken tobe the sequential composition of the four quarterly decisionprotocols that make up the annual reporting cycle.

3.5.1 Decisions are Protocols tooWinograd and Flores’ general Conversation for Action

model for communication centres on the idea of a negoti-ated time, cost and quality “condition of satisfaction.” Thisis the basis for the initial A:Request act, and the groundsfor A to ultimately declare that the action is complete. Inthe case of PPERA the Condition of Satisfaction is that“forthis pair of donor and receiving Accounting Unit, on thelast day of each calendar quarter, either make a regular re-port to the Electoral Commission, a Section62(12) report orcarry the recorded donations forward.” But this model doesnot record what rules will be used to decide which reportto create, or how the conversations will interact with eachother to determine whether Section62 (National) reportingwill come into play.

We call the parallel composition of individual Conversa-tions for Action between donors and accounting units whichresolves these questions the Labour Donor Workloop (Fig-ure 6). In the workloop communication is by handshake,with no latency, just like the transitions in the CfA statechange conversation. We model the decisions by A and Bon whether and how to proceed by a decision agent locatedat each CfA state. This agent is illustrated in Figure 8 – alabelled transition system for the workloop interchange sta-tion Build Report for Commission in Quarter 4. The Figure

shows the 15 permitted paths for an accounting unit’s re-port. Let α be the speech act: r, s or c. Then we write

α→ δpfor the p’th decision δp that the action α be taken. As inFigure 4 states are labelled by formula over two predicatesδp and δ∗p . The start of the year is the leftmost node in thegraph. Transition arcs are labelled by the action taken withthe donor’s donations to the AU when the quarter is closed.Unlabelled states take the formula

¬(δp ∨ δ∗p)

. We can infer from this that the decision made in the priorstate was to make a carried forward report.

advise organisationaldonation

advise individual donation

review active submissions accept

query

decline

build report forcommission

reviewaccepteddonations

review activedonations

reviewdonations

to verify

review declineddonations

home

re-submit

cancel

Produced for and licenced to The Labour Party by Ian Benson & Partners Limited.

‘Sociality’, ‘Sociality Workloop’ and‘Trustworthy Representation’ aretrade marks of Ian Benson andPartners Limited.

Part no. 46.08_IaBe_042901_PetriNet

© Ian Benson & Partners Ltd 2001 All Rights Reserved.

verify donorpermissibility

clarify declineddonations

The Labour Donor Workloop

donate

clarify

validate

build report

complete

under constructionsociality-trustworthy representation ™

party funding manager zone

responsible officer zone

acknowledgedonation report

close accountingperiod

Figure 6: Labour donor workloop: a storyboard for c2800labour donor decision protocols

As the year progresses there is a need to process retro-spectively donations that come to light after the end of aquarter. This means that the individual quarter decisionagents become increasingly complicated. (Figure 9 to 11)

4. DECISION PROTOCOLSWe rely on the combination of our set of decision agents

and their tests to prove that decision making covers all even-tualities. We cannot rely on observation alone to demon-strate this, since for each donor we have to consider theinteraction between the virtual AU and perhaps 700 physi-cal AU aggregation levels (Head Office thresholds and localAU donor thresholds).

To show that the decision agents together do indeed sat-isfy the goal of the legislation we introduce a number of for-mal definitions in bold font (section 4.1). These correspondto custom, practice and Statute. The key Section 62(12) ofPPERA which deals with National donations is reproducedat http://sociality.tv/s62.

Our task is simplified by the fact that the set of donationsfrom a donor to an AU in a given period are all treated inthe same way. We can therefore reason about the sum ofthese donations as if it was a single donation without com-promising the integrity of a formal proof. Secondly we canassume that the Head Office units - although independentas receiving units - are part of a single accounting unit witha single threshold. We can therefore consider all donationsfrom a donor to any Head Office unit as a single compounddonation to Head Office itself.

r

r

s

r r

s s s

c

c c c

r r r

s

r r

s

r

s

cccc

sssscsssccsscccs

rrrrcrrrsrrrssrrcsrrccrrcccrccsrcssr

δ*1

δ2 δ

3 δ4

δ1

δ*2

δ*3

δ*4

δp δ*

p∨

sssr

Figure 7: AUDonor act-decide labelled transition system(Q4)

Furthermore, the interaction between local, Head Officeand Section 62 is carefully constrained. There is no connec-tion between reports of a donor’s activity with two differ-ent physical AU except the coupling demanded by Section62(12).

To prove that this reasoning is correct we further refinethe storyboard workloop to form a quarterly decision pro-tocol. This consists of the following elements:

1. The set of all recordable donations of cash or kindfrom a donor in a period to an AU gives rise to twoconcurrent Conversations for Action: one between thedonor and the receiving accounting unit and one be-tween the donor and the national (virtual) accountingunit. We call this compound CfA, along with its as-sociated data and decision logic, a Conversation forCollective Action (CfCA).

2. Each CfCA decision is modelled as a first order pred-icate calculus formula. This tests for an expected re-porting outcome.

3. For each CfCA decision agent we develop a suite oftest cases to exercise all legal recording and reportingoutcomes in the quarter. We prove that there are noother test cases.

4. For the CfCA as a whole there is a proof of test cov-erage. That is, we prove that the decision logic (1)considered as a logical theory satisfies the test formu-lae (2) in each scenario (3).

4.1 Decision LogicWe illustrate our approach by constructing decision agents

for reporting to the Electoral Commission at the end of thefirst and fourth quarters. To implement the rules for physi-cal AU reporting (section 3.2 Rules (1 and 2)) we constructthe deltaPredicate δ(aud,q) over the set of donors d, units

aud and reporting quarters q, p = 1, . . . ,4. Informally, ifδ is true then this signals that the donations received in theunit from the donor will be reported this quarter.

Section 62(12) and carry forward reporting (Rules 3 and4) use the deltaStarPredicate δ∗(aud, q). This is true if thecumulative total to date of all the donations received at anyunit exceeds the Section62(12) (National) threshold of £5kand the unit aud is not reporting.

The deltaPrimePredicate establishes whether the cumu-lative total to date of all the donations received at any unitexceeds the Section62(12) (National) threshold of £5k. It isused in the definition of the deltaStarPredicate.

The Section62Function S62(aud, q) returns zero or one,depending whether a donor is to be reported as Section62(12) for their donations to this unit this quarter (0), or isto report via the AU, or have these donations carried for-ward (1). It uses the deltaStarPredicate and is used in theformal definition of the deltaPredicate to exclude donationsreported as Section62(12) from the physical AU thresholdtest.

We write δ, δ∗ and ∆′ for these predicates to signify cir-

cumstances in which they are true. δp (δ∗p, ∆

′p) signify a

quarter, p, in which the δp (δ∗p , ∆′p) predicate is false.

Figure 8: Definitions for Decision Logic

4.2 Test FormulaeWith these predicates in place we can revisit the act-

decide transition system and prove that each formula thatlabels a state in the system is satisfied by an execution of

the decision agent with appropriate data. We represent de-cision making as a state chart (Figure 9 to 11) that acceptsdonations in the compound state (⊥,⊥∗) and moves themto their external reporting states (if any) according to thefollowing rules:

δpdef= (δ(aud, p), δ

∗(aud, p))

δ∗pdef= (⊥, δ∗(aud, p))

In section 4.4 we show that the test scenarios systemati-cally explore just the permitted paths, as they are exercisedover a year by two physical AU interacting through the vir-tual accounting unit for the donor.

The state chart Figure 9 shows how the classification pro-ceeds in the first quarterly decision protocol. Here two con-current state machines - AUdonor and AUS62donor - awaita new set of donations from the donor to the AU for the pe-riod in a compound start state marked (⊥,⊥∗). When theperiod is closed all accepted donations for the unit in theyear to date advance via transition (1) into the compoundstate δ, δ∗.

In this aggregation state each machine tests to see ifthe threshold is exceeded for the set of donations that havecollected there. We distinguish the two distinct aggrega-tion rules, that is, to include or exclude previously reportedS62 donations, by the state labels agg (exclude) and agg∗(include) (Figure 10).

Depending on the result of these tests, a set of AU dona-tions will either transition (4) back to this compound state(and be recorded as CF), advance to a Quarterly Report(transition 2) or be reported under S62 (transition 3).

Donation sets that advance to the S62 report in the AUS62donormachine will simultaneously revert to the AUdonor startstate. This will exclude them from future AU donor thresh-old tests.

At the end of this classification process the set of AUdonations may be in any reachable compound state except(⊥,⊥∗) (Figure 10).

⊥

repstart 1 agg 2

AU_donor

AUS62donor

rep*start 1 agg* 3

2,4

3 δδ

⊥*

⊥

δ* δ*

4

Figure 9: Individual Donation Reporting State Chart (Q1)

Each period this calculation will be repeated and all priorreports will be recalculated. This is necessary to revert back-dated donations to the period in which their accepted datefell.

Figure 11 shows the decision protocol AUdonor at theend of the fourth quarter. Donations which are not carriedforward at the end of the year may have taken transition2.1, . . . , 2.4 to be allocated to a Quarterly Report δ1, . . . , δ4,or they may have taken transition 3.1, . . . , 3.4 to be included

δ

Transitions

c:

δ*

δ*,δ

δ*

δ δ*,

δ δ*,

rep*

1

2

3

⊥ , ⊥'

AUdonor

AUS62donor

start* agg*

⊥ , ⊥*start

agg

rep unreachable

unreachable

unreachable

unreachable

unreachable

Compound States

4

δ δ*,

δ*, δ δ*,

δ δ*,

δ*,δ

r:

s:

Figure 10: Reachable Reporting States (Q1) (NB accu-mulation is asymmetric - All donations count towards S62threshold (agg*), but only non-S62 donations count towardsAUdonor (agg))

in aggregate in a Section 62(12) Report for the donor for aquarter δ∗1 , . . . , δ

∗4 .

⊥ rep

2.1rep2.2

rep2.3

rep

2.4

AUS62donor

⊥*

start 1

AUdonor

start* 1

2.1(4.1) ..2.4(4.4)

3.1..3.4 δ

start

rep*

3.1rep*3.3.2

rep*3.3

rep*

3.4

δ1

δ2

δ3

δ4

δ* δ* 1

δ* 2

δ* 3

δ* 4

4.1..4.4

agg*

agg

terminal state

p

p

Figure 11: Individual Donation Reporting State Chart(Q4)

4.3 Test ScenariosEach quarter takes into account the history of donation

reporting by the donor to the accounting unit. Dependingwhether Section 62(12) is active, or the AU has a prior Quar-terly report from a donor, a recordable donation may eitherbe carried forward, aggregrated in S62, or published in theQuarterly Report. We have shown how for each accountingunit and donor there are 15 possible histories, or AUdonorpaths, linking reachable states of the reporting space (Fig-ure 7). In this section we consider how many combinationsof AUdonor paths we need to prove that the reporting logicalways works.

To do the proof we will need an additional convention

to account for null reports. These are quarters when nodonations are received by an accounting unit from a specificdonor. Our null reporting convention [Rule1b] mandatesthat if S62(12) is active in a quarter and the AU is nototherwise reporting, then where no donation is received byan AU from the donor, the S62 report will contain a notionalnull report. However, if the AU is reporting, that is thethreshold for the AU has been breached in a prior quarter,then the notional donation will form part of the Quarterlyreport for the new quarter. If neither S62 or prior Quarterlyreporting applies, then the null report is a notional CarriedForward entry.

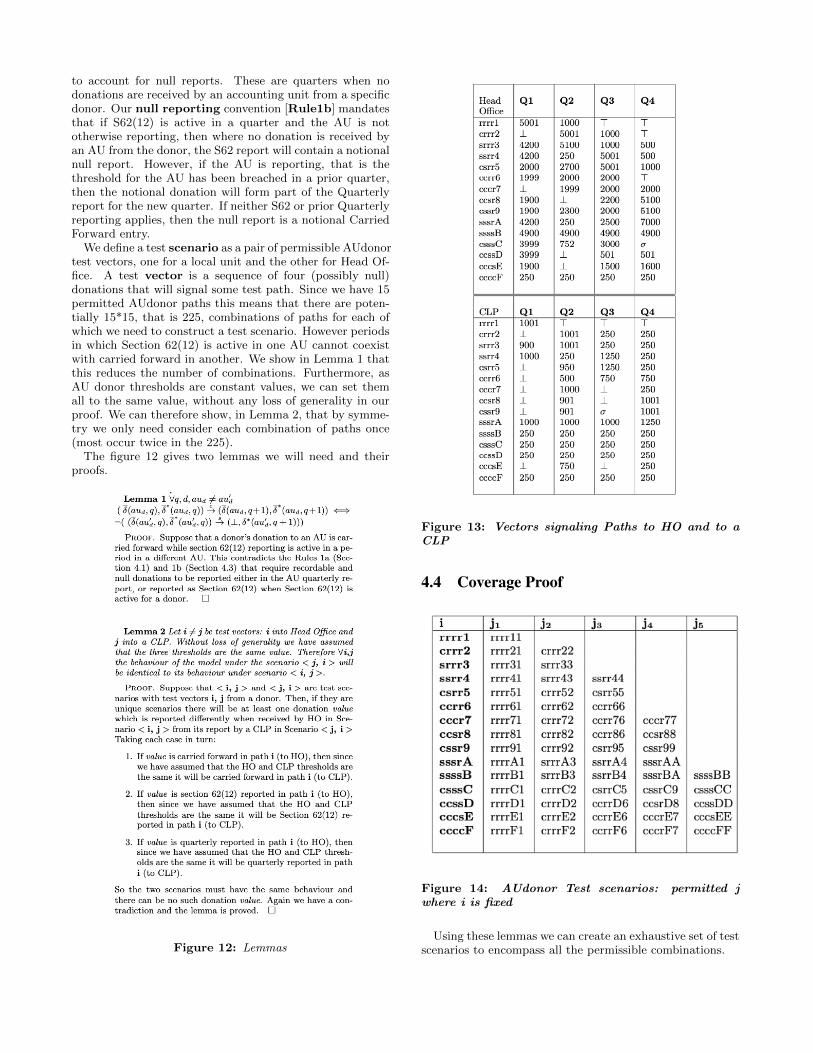

We define a test scenario as a pair of permissible AUdonortest vectors, one for a local unit and the other for Head Of-fice. A test vector is a sequence of four (possibly null)donations that will signal some test path. Since we have 15permitted AUdonor paths this means that there are poten-tially 15*15, that is 225, combinations of paths for each ofwhich we need to construct a test scenario. However periodsin which Section 62(12) is active in one AU cannot coexistwith carried forward in another. We show in Lemma 1 thatthis reduces the number of combinations. Furthermore, asAU donor thresholds are constant values, we can set themall to the same value, without any loss of generality in ourproof. We can therefore show, in Lemma 2, that by symme-try we only need consider each combination of paths once(most occur twice in the 225).

The figure 12 gives two lemmas we will need and theirproofs.

Figure 12: Lemmas

Figure 13: Vectors signaling Paths to HO and to aCLP

4.4 Coverage Proof

Figure 14: AUdonor Test scenarios: permitted jwhere i is fixed

Using these lemmas we can create an exhaustive set of testscenarios to encompass all the permissible combinations.

Proof. In Figure 14 each unique test scenario < i, j >is represented by a label hexadecimal “ij” i ≥ j where “i,j”are hexadecimal path numbers (Figure 5) and i ≥ j. Byinspection there are no other pairs that are permitted byLemma 1.

Test vectors are shown in Figure 13.This shows one test vector for each path π to HO and to

a CLP: we can call them HO(π) and CLP(π).We use ⊥ to indicate that a null carried forward donation

is reported, > to indicate a null donation in a QuarterlyReport, and σ for a null donation in a Section 62 (12) Report(Rule 1b Section 4.3).

From Lemma 2 it follows that for every test scenario< HO(πi), CLP (πj) > in table 14 there is a test scenarioof the form < HO(πj), CLP (πi) >.

By construction there are no other test scenarios.

5. CONCLUSIONIn this paper we have developed a new computational

theory to account for voluntary behaviour for the commongood. We built on a vocabulary of objects, operations andrelationships first proposed by the economist Mancur Olsonin his “Logic of Collective Action.” Olson predicted that ac-tion for the common good would only be taken voluntarilyin small groups where the total cost of the first productionof the good could be met profitably by one person. In allother cases coercion would be needed.

We tested his predictions by observing first the promo-tion, then the rejection and finally the compliance of theUK Labour Party with the Political Parties, Elections andReferendums’ Act (2000). We found that compliance wasachieved after two annual reporting cycles without augment-ing the sanctions regime – which would have been neededto deal with the initial non-compliance in Olson’s theory.Rather compliance was achieved by reifying the process ofinner and intra-unit negotiation. The process model wasused to win confidence in a recording and reporting sys-tem built to this specification by means of a formal proof oftest coverage. We found that confidence – a key aspect offunctioning teams, markets and systems – was a category ofcommon good that fell outside Olson’s theory.

The language used in the Act itself to describe the opera-tion of PPERA is much more complex than our structuredmathematical treatment. This lends itself to intuitive dia-gram conventions such as those used in a Conversation forAction or London Underground map and in our act-decidetransition system. Further research is needed on techniquesfor automating test coverage analysis for decision protocolsand to explore the application of this approach in other pub-lic services, such as health, welfare or education. In the caseof these common goods there remain major risks of systemdevelopment and process failure. We have shown that theirroot cause may lie not only in the limitations of traditionalsystems analysis, first highlighted by Winograd and Floresin “Computers and Cognition” but also in archaic formsof parliamentary draughtsmanship and outmoded economicthought.

6. ACKNOWLEDGMENTSThe author is grateful to Mikulas Teich, Kristen Nygaard,

Charles Clarke, Paul Corrigan, Terry Winograd, ClaudioCiborra, David Holloway, William Clocksin, Ben Galewsky

and others for discussions over many years on the successesand failures of systems development and to the anonymousreviewers of earlier drafts of this paper which led to improve-ments.

7. REFERENCESBenson, I., Ciborra, C., & Proffitt, S. (1990). Some socialand economic consequences of groupware for flight crew.In Proceedings of the ACM Conference on ComputerSupported Cooperative Work. ACM Press, New York.

Carpenter, K., Nardi, B., Moore, J., Robertson, S.,Drezner, D., Benson, I., Foot, K., & Jett, Q. (2004).Online political organizing: lessons from the field. InProceedings of the ACM Conference on ComputerSupported Cooperative Work. ACM Press, New York.

Ciborra, C. (1993). Teams, markets, and systems :business innovation and information technology.Cambridge, England ; New York : Cambridge UniversityPress.

Henke, D. (2003). Big donors avert cash crisis. GuardianNewspaper.

Maguire, K. (2003). Labour chief says he fears jail oversleaze. Guardian Newspaper.

Milner, R. (1989). Communication and Concurrency.Prentice Hall International, New York.

Olson, M. (1965). The Logic of Collective Action: PublicGoods and the Theory of Groups. Harvard UniversityPress.

Pavlovic, D. & Mislove, M. (2006). Testing semantics:Connecting processes and process logics. In 11thInternational Conference on Algebraic Methodology andSoftware Technology.

Putnam, R. (2000). Bowling alone: the collapse andrevival of American community. Simon and Schuster,New York.

Resnick, P., Bikson, T., Mynatt, E., Puttnam, R.,Sproull, L., & Wellman, B. (2000). Beyond bowlingtogether. In Proceedings of the ACM Conference onComputer Supported Cooperative Work. ACM Press,New York.

Weigand, H. (2006). Two decades of Language/Action.Communications of the ACM, 49 (5).

Winograd, T. & Flores, F. (1986). UnderstandingComputers and Cognition: A New Foundation forDesign. Ablex Pub. Corp., New Jersey.

![LT Revisited: Explanation-Based Learning and the Logic of ...1022647915955.pdf · and Bertrand Russell's Principia Mathematica [Whitehead, Russell, 1962]. The calculus deals with](https://img.pdfslide.us/doc/110x75/5f7f545c09f91466a6735f62/lt-revisited-explanation-based-learning-and-the-logic-of-1022647915955pdf.jpg)