Embed Size (px)

Citation preview

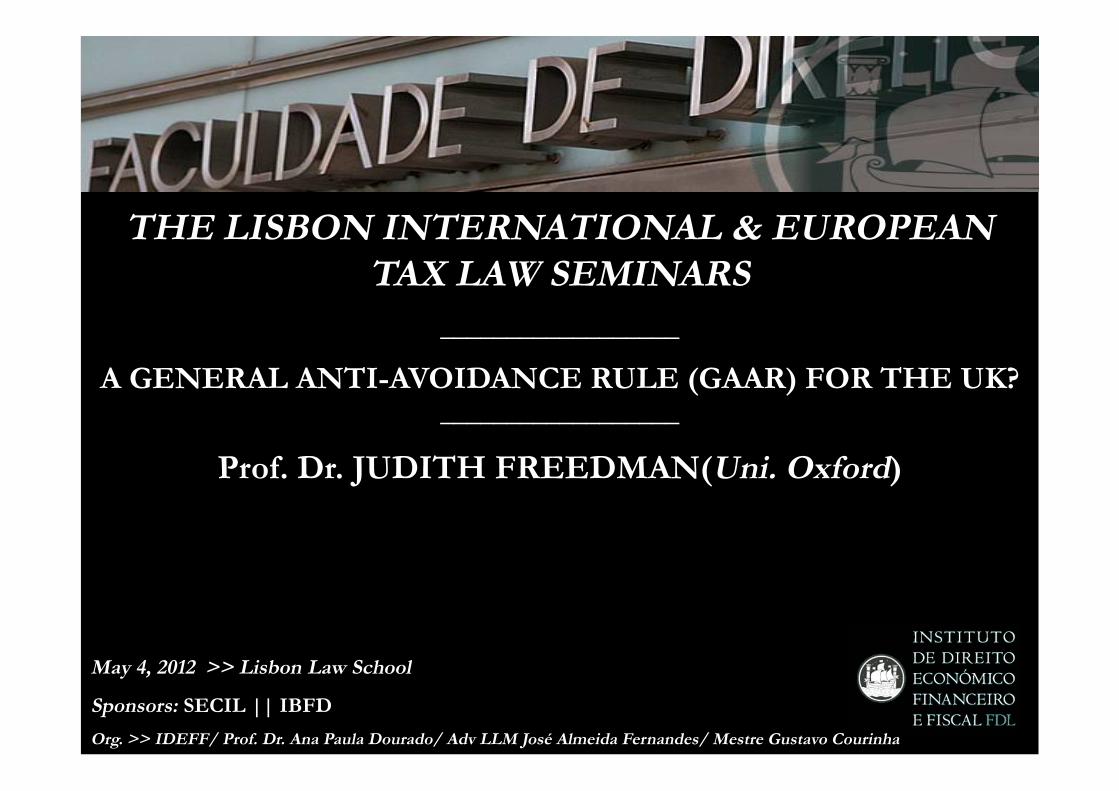

THE LISBON INTERNATIONAL & EUROPEAN TAX LAW SEMINARS

__________________

A GENERAL ANTI-AVOIDANCE RULE (GAAR) FOR THE UK? __________________

Prof. Dr. JUDITH FREEDMAN(Uni. Oxford)

May 4, 2012 >> Lisbon Law School

Sponsors: SECIL || IBFD

Org. >> IDEFF/ Prof. Dr. Ana Paula Dourado/ Adv LLM José Almeida Fernandes/ Mestre Gustavo Courinha

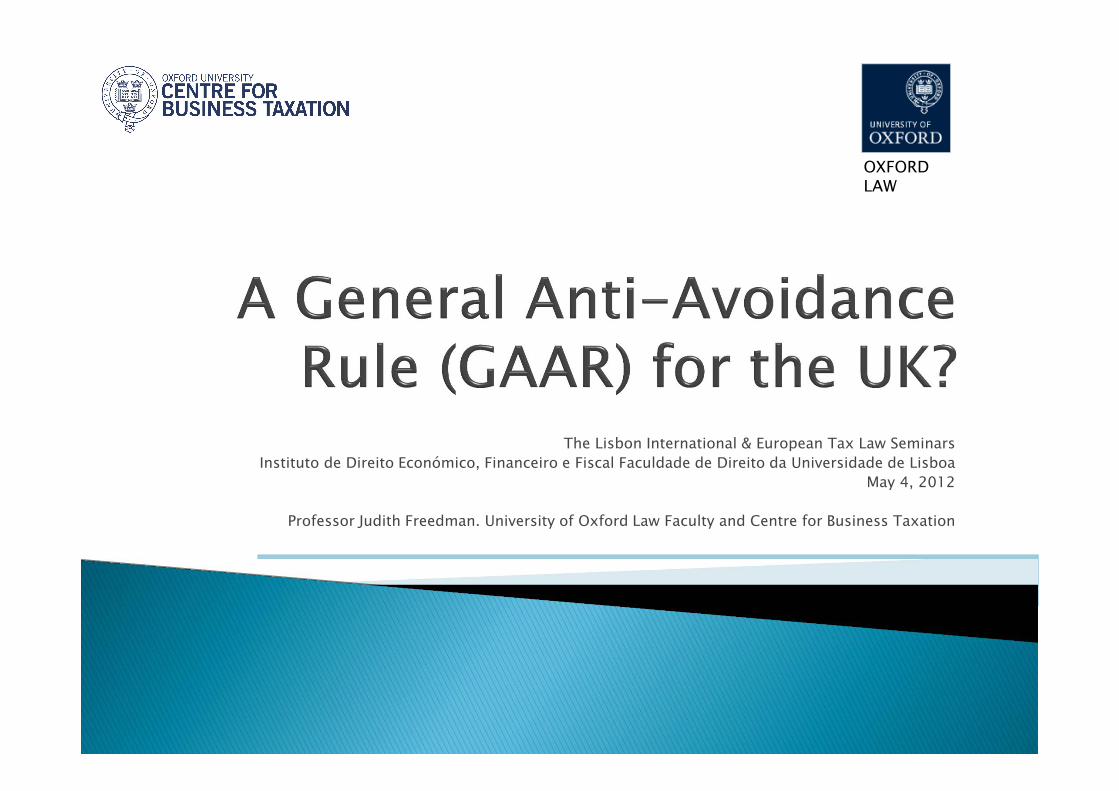

The Lisbon International & European Tax Law Seminars

Instituto de Direito Económico, Financeiro e Fiscal Faculdade de Direito da Universidade de Lisboa

May 4, 2012

Professor Judith Freedman. University of Oxford Law Faculty and Centre for Business Taxation

OXFORD LAW

o Aaronson GAAR study November 2011 proposes ‘moderate rule targeted at abusive arrangements but not applying to reasonable tax planning’.

o NOT a broad spectrum anti-avoidance rule

o I was member of Aaronson study group but speaking entirely personally. Report is Aaronson’s QC. Study group members- three judges (one retired- Lord Hoffmann), two academics and one tax director (BP)

o Aaronson published report and illustrative draft

o UK Budget announces there will be a GAAR in 2013 but consultation document not yet published – detail of proposal not known- draft clauses being drawn up by Parliamentary draftsman- publication expected in June 2012.

o No statutory general anti-avoidance rule (GAAR)o No judicial doctrine?o UK has no general concept of abuse of legal forms

although abuse of law applies to VAT via Court of Justice

o Disclosure provisions for selected transactions within five days of being made available by promoter

o Specific provisions and over 300 targeted anti-avoidance rules- main purpose or one of main purposes.

o No penalties for avoidanceo No general statutory clearance (binding

rulings)system , but some individual provisions have clearances

o Uncertainty for business under current system

o Competitive pressure on business to engage in schemes

o Increasing complexity of specific provisions

o Attempts by HMRC to use ‘voluntary methods-‘tax law in the boardroom, CSR, Bank Code.

o Barclays case- retrospective legislation

o Increasing NGO and media criticism in climate of austerity.

o Coalition agreement

Do we still have a Ramsay principle? House of Lords (now Supreme Court) says

o Ramsay case did not introduce a new doctrine operating within the special field of revenue statutes but rescued tax law from ‘island of literal interpretation’

o ‘Going too far to say that transactions or elements of transactions with no commercial purpose should always be disregarded’.

o Transaction using capital allowances valid despite money going round in a circle- just happenstance!

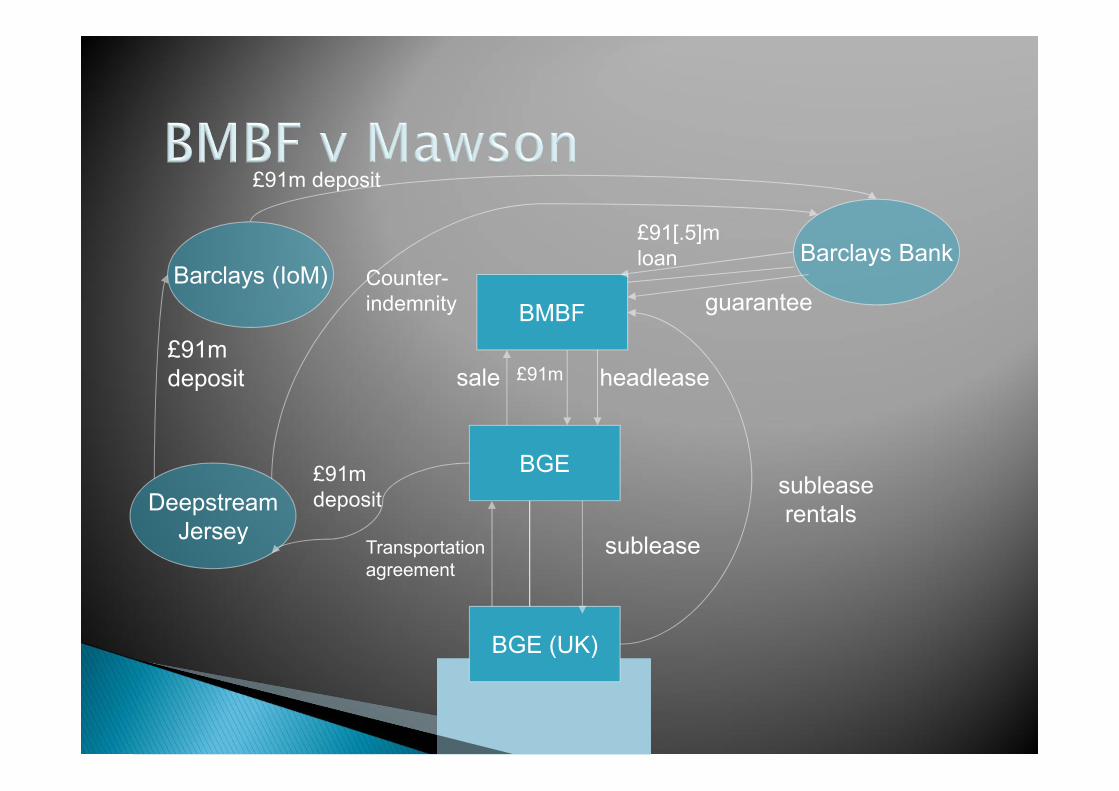

BMBF

BGE

BGE (UK)

Barclays Bank

DeepstreamJersey

Barclays (IoM)

subleaserentals

subleaseTransportationagreement

sale headlease

£91mdeposit

£91m£91mdeposit

Counter-indemnity guarantee

£91m deposit

£91[.5]mloan

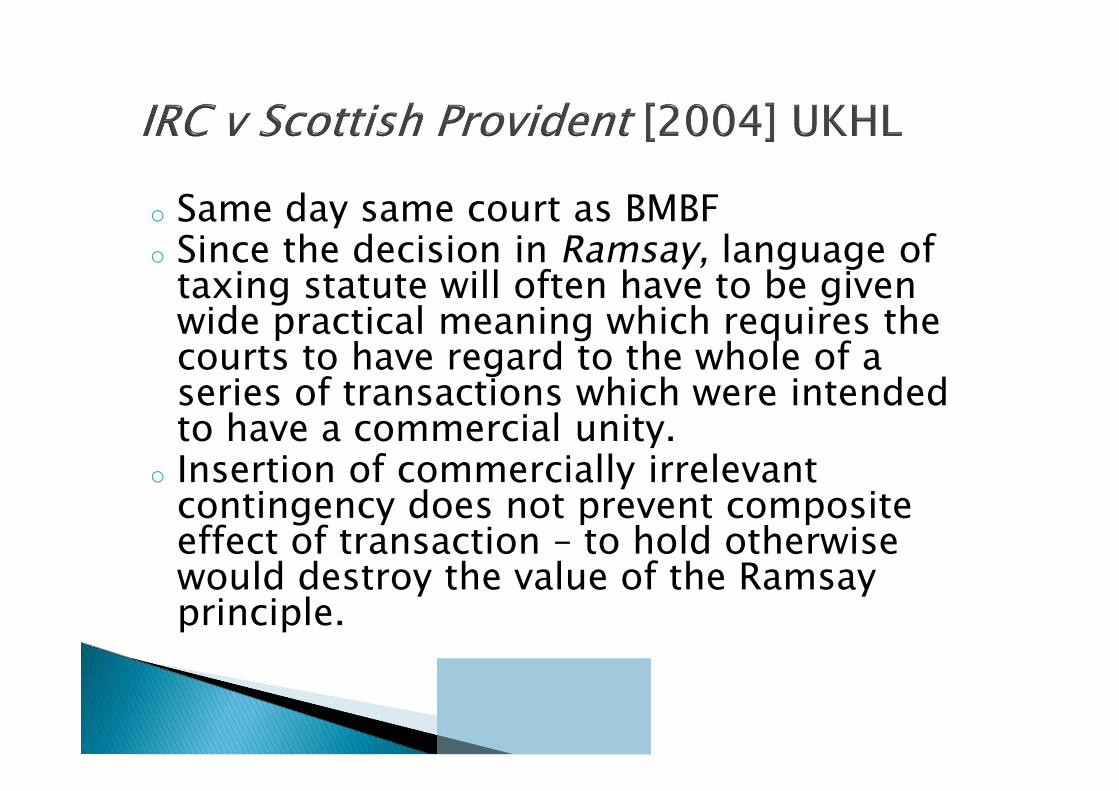

o Same day same court as BMBFo Since the decision in Ramsay, language of

taxing statute will often have to be given wide practical meaning which requires the courts to have regard to the whole of a series of transactions which were intended to have a commercial unity.

o Insertion of commercially irrelevant contingency does not prevent composite effect of transaction – to hold otherwise would destroy the value of the Ramsay principle.

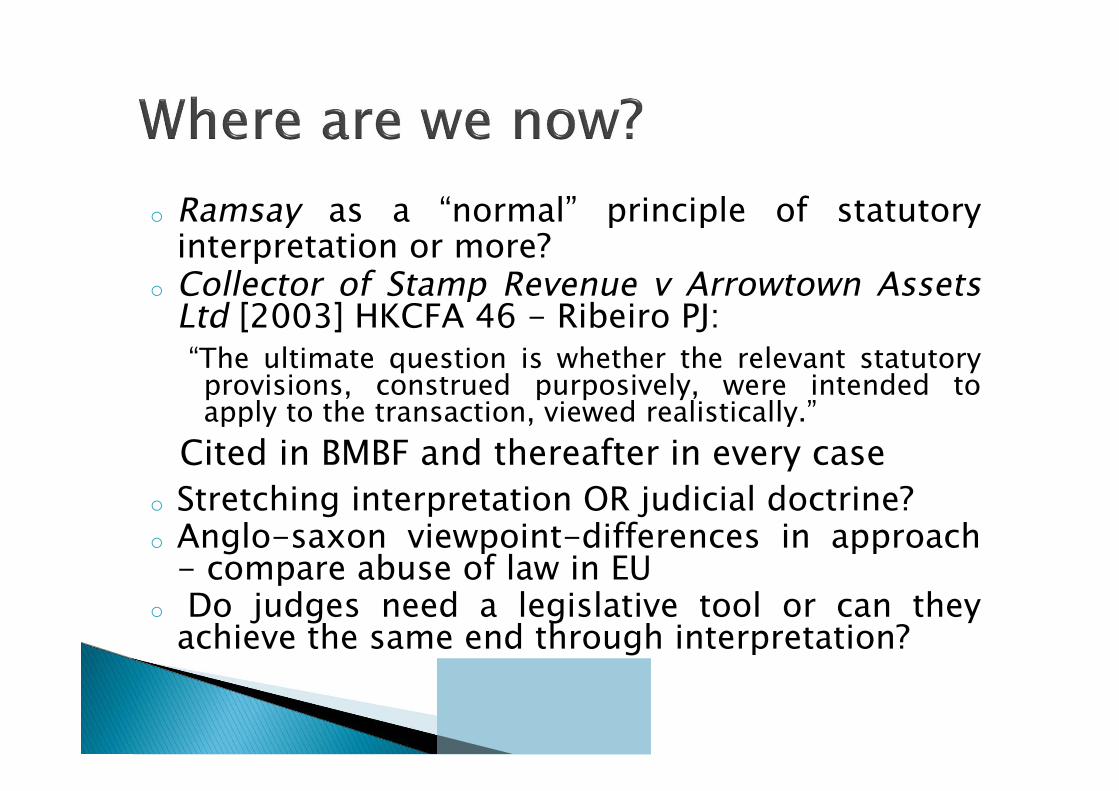

o Ramsay as a “normal” principle of statutoryinterpretation or more?

o Collector of Stamp Revenue v Arrowtown AssetsLtd [2003] HKCFA 46 - Ribeiro PJ:“The ultimate question is whether the relevant statutoryprovisions, construed purposively, were intended toapply to the transaction, viewed realistically.”

Cited in BMBF and thereafter in every case

o Stretching interpretation OR judicial doctrine?o Anglo-saxon viewpoint-differences in approach

- compare abuse of law in EUo Do judges need a legislative tool or can they

achieve the same end through interpretation?

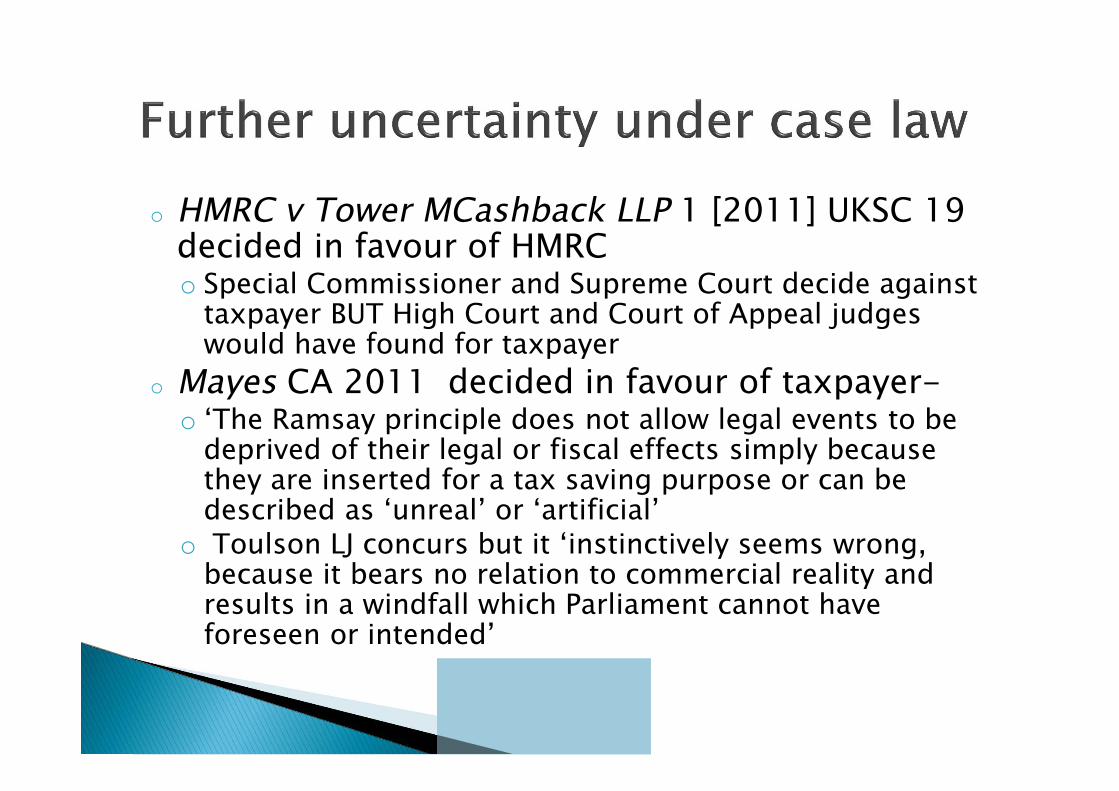

o HMRC v Tower MCashback LLP 1 [2011] UKSC 19 decided in favour of HMRCo Special Commissioner and Supreme Court decide against

taxpayer BUT High Court and Court of Appeal judges would have found for taxpayer

o Mayes CA 2011 decided in favour of taxpayer-o ‘The Ramsay principle does not allow legal events to be

deprived of their legal or fiscal effects simply because they are inserted for a tax saving purpose or can be described as ‘unreal’ or ‘artificial’

o Toulson LJ concurs but it ‘instinctively seems wrong, because it bears no relation to commercial reality and results in a windfall which Parliament cannot have foreseen or intended’

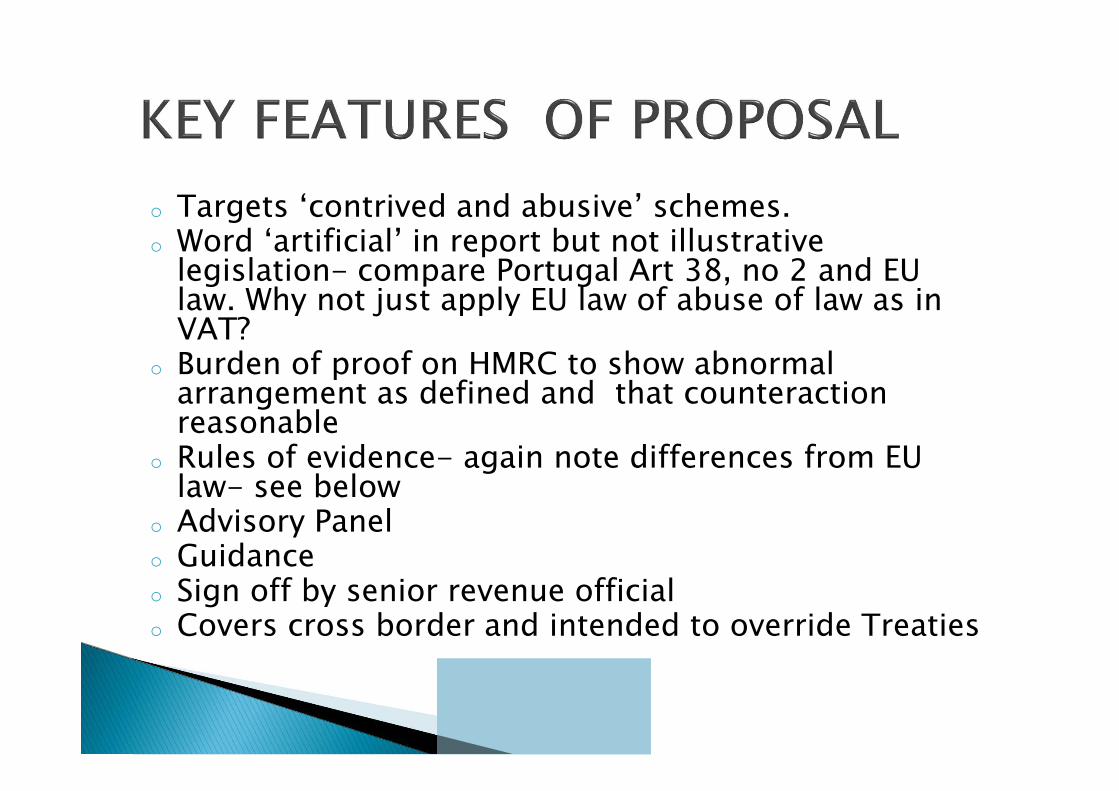

o Targets ‘contrived and abusive’ schemes.o Word ‘artificial’ in report but not illustrative

legislation- compare Portugal Art 38, no 2 and EU law. Why not just apply EU law of abuse of law as in VAT?

o Burden of proof on HMRC to show abnormal arrangement as defined and that counteraction reasonable

o Rules of evidence- again note differences from EU law- see below

o Advisory Panelo Guidance o Sign off by senior revenue officialo Covers cross border and intended to override Treaties

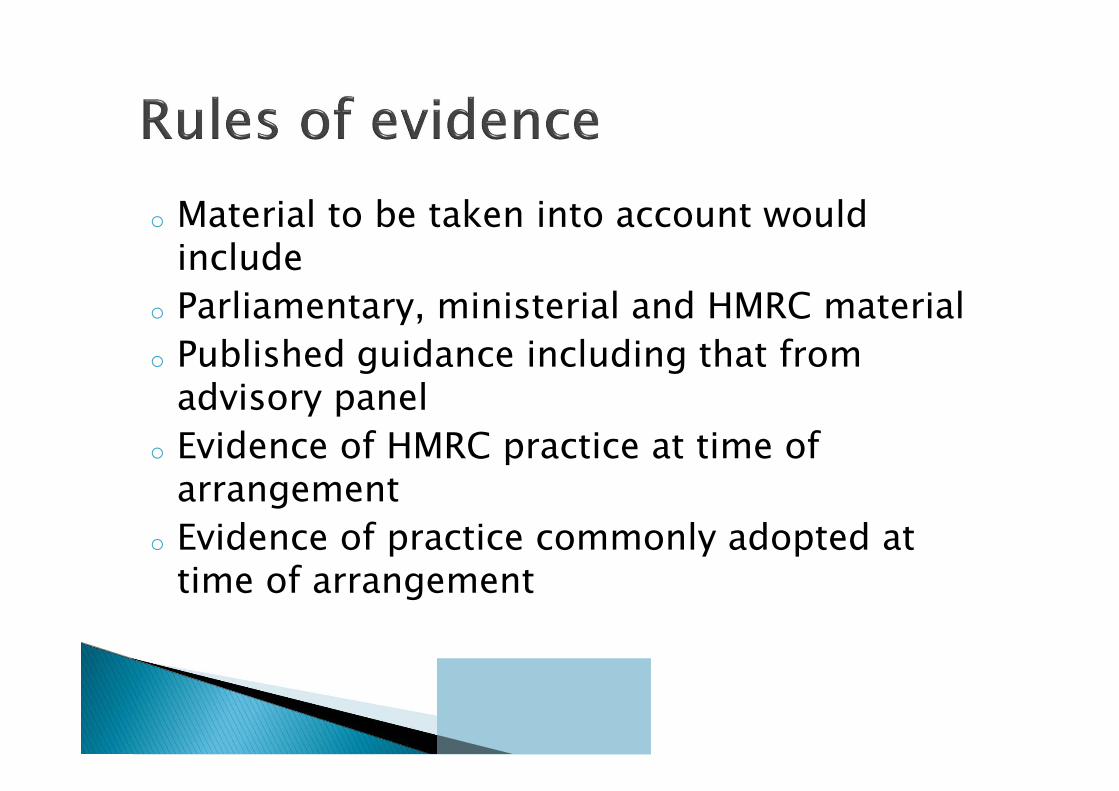

o Material to be taken into account would include

o Parliamentary, ministerial and HMRC material

o Published guidance including that from advisory panel

o Evidence of HMRC practice at time of arrangement

o Evidence of practice commonly adopted at time of arrangement

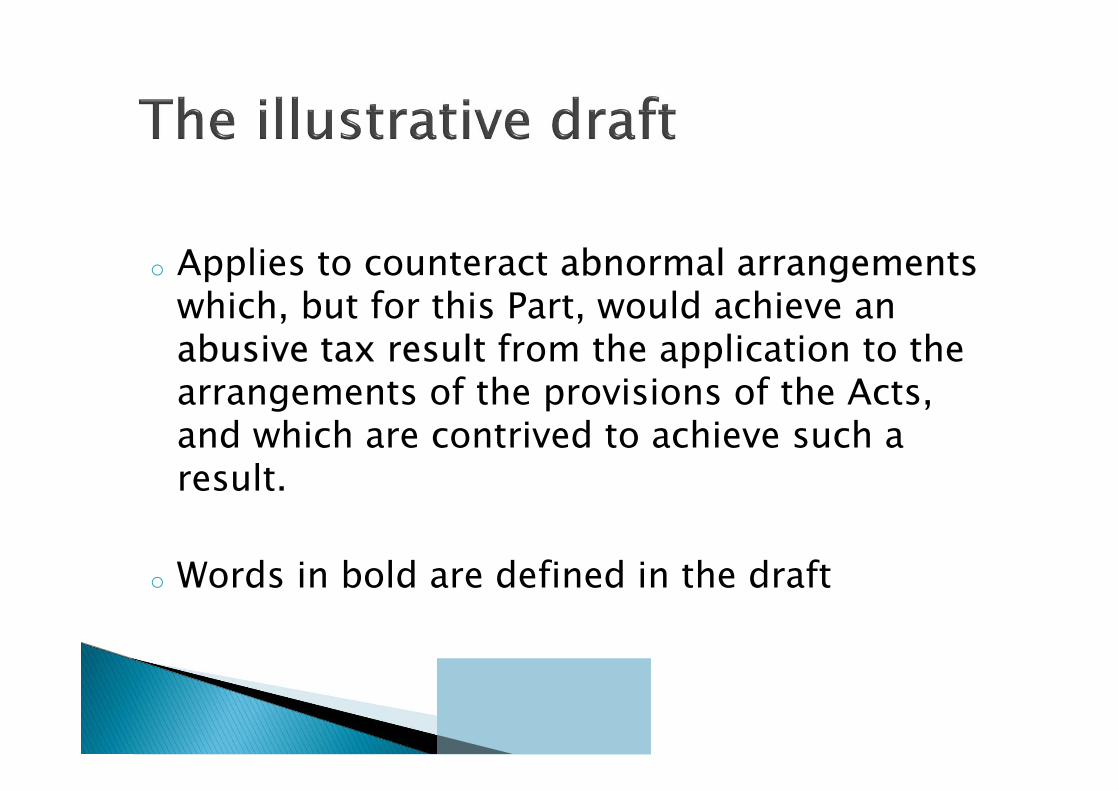

o Applies to counteract abnormal arrangements which, but for this Part, would achieve an abusive tax result from the application to the arrangements of the provisions of the Acts, and which are contrived to achieve such a result.

o Words in bold are defined in the draft

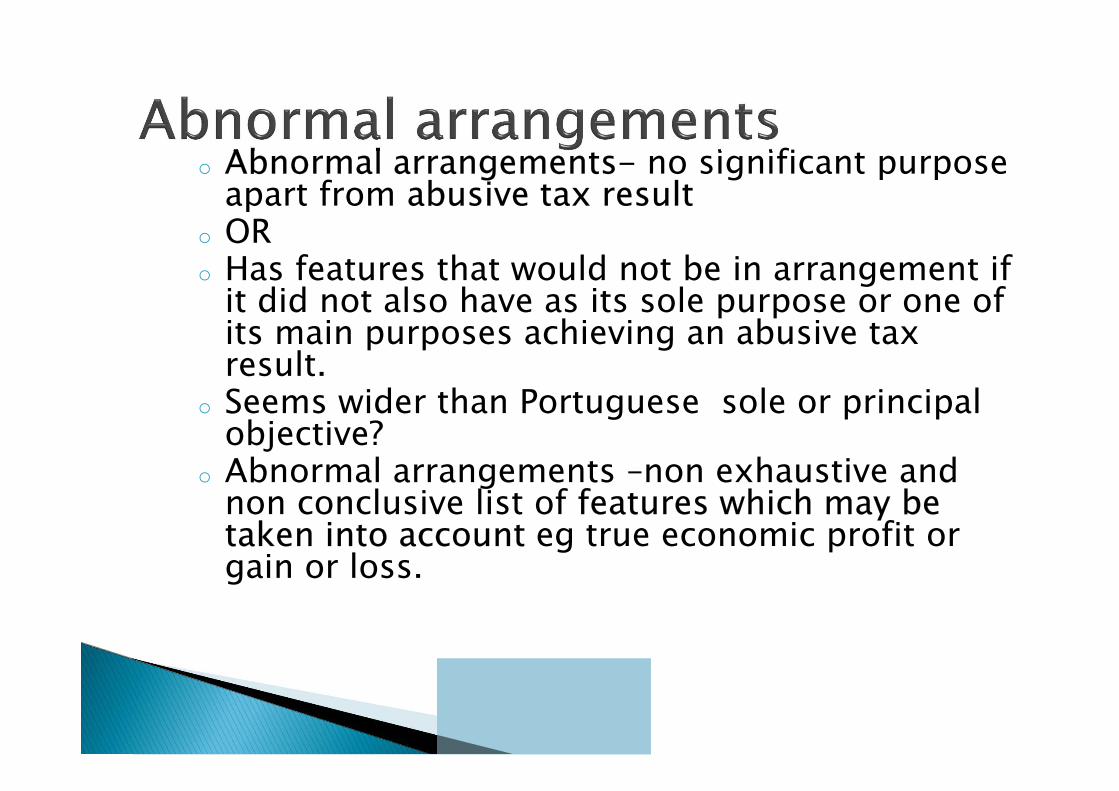

o Abnormal arrangements- no significant purpose apart from abusive tax result

o ORo Has features that would not be in arrangement if

it did not also have as its sole purpose or one of its main purposes achieving an abusive tax result.

o Seems wider than Portuguese sole or principal objective?

o Abnormal arrangements –non exhaustive and non conclusive list of features which may be taken into account eg true economic profit or gain or loss.

o An abusive tax result is an advantageous tax result which would be achieved by an arrangement that is neither reasonable tax planning nor an arrangement without tax intent

o Advantageous tax result achieves a reduction in tax, an increase in deductions or a deferral or acceleration.

o An arrangement does not achieve an abusive tax result ◦ if it can reasonably be regarded as a reasonable

exercise of choices of conduct afforded by the provisions of the Act (reasonable tax planning)

◦ If advantaged party shows it was not designed or carried out with intention of achieving advantageous tax result (arrangements without tax intent)

o Overriding statutory principle to which other taxlegislation is subject , not a rule of construction[Aaronson Report para 5.4]

o Not a move away from Parliamentary intention -the principle is part of the statutory language

o Should reduce need for retrospective legislationand/or strengthen argument against it

o Better underlying legislation is only fundamentalsolution but GAAR should increase the case forprincipled legislation as GAAR only works iftaxpayer is not exercising reasonable choice ofconduct under Acts.

Importance of several issues beyond theGAAR – management of discretion; guidanceetc

Advisory panel as part of regulatoryconversation

GAAR giving us a language and focus forpublic debate

Await consultation document fromgovernment

THE LISBON INTERNATIONAL & EUROPEAN TAX LAW SEMINARS

__________________

UPCOMING SEMINAR – 11.05.2012

THE CONCEPT OF ‘BENEFICIAL OWNER’ IN THE DUTCH TAX SYSTEM AND DOUBLE TAX CONVENTIONS

_________________

Prof. Dr. ERIC KEMMEREN (Fiscal Institute Tilburg - Univ. Tilburg)

Sponsors: SECIL || IBFD

Org. >> IDEFF/ Prof. Dr. Ana Paula Dourado/ Adv LLM José Almeida Fernandes/ Mestre Gustavo Courinha