Embed Size (px)

Citation preview

doi:10.1016/j.emj.2005.10.010

European Management Journal Vol. 23, No. 6, pp. 648–662, 2005

� 2005 Elsevier Ltd. All rights reserved.

Printed in Great Britain

0263-2373 $30.00

The Limits of LeanManagement Thinking:Multiple Retailers andFood and FarmingSupply Chains

ANDREW COX, CBSP, Birmingham Business School

DAN CHICKSAND, CBSP, Birmingham Business School

This article discusses the strengths and weaknessesof lean management thinking in the food and farm-ing industry in the UK. Based on a case study of redmeat supply it is argued that the adoption of leanpractices internally may be appropriate for all par-ticipants in the industry, but the inter-organisa-tional aspects of lean may not be easy to apply inpractice, nor appropriate, for many participants.For some participants — especially the multipleretailers — the adoption of lean principles may leadto a positive outcome with stable and/or increasingprofitability. For the majority of participants inthese industry supply chains, however, the adop-tion of lean principles may result in a high levelof dependency on buyers and to low or declininglevels of profitability.� 2005 Elsevier Ltd. All rights reserved.

Keywords: Lean thinking, Power analysis, Supplychain management

Introduction

The article analyses the current crisis of profitabilityand competitiveness in the UK food industry andred meat supply chains, followed by a descriptionof the recent UK government and farming industryresponse––based primarily on the adoption of leanprinciples — to these problems. The article then pre-sents the findings from a study, based on the power

648 Europe

and leverage perspective on transactional exchange,into the UK fresh/frozen, beef supply chain. Thestudy shows that, while aspects of lean thinkingmay be appropriate internally for all participants inbeef supply chains, the ability to extend this way ofthinking beyond the boundaries of the firm into theextended supply chain for fresh/frozen beef is muchmore problematic. This is primarily because thepower and leverage resources do not exist to allowa lean supply chain management approach to beadopted throughout the chain. This means that leansupply is of limited utility for many participants inthe beef supply chain.

The Crisis in UK Red Meat Supply Chainsand the Government and Industry Response

The UK red meat industry is experiencing unparal-leled challenges and has been thinking radicallyabout its future. The major threats to the industryrange from health related problems––like the Footand Mouth Disease and BSE––to the de-coupling offarmers CAP subsidies after 2005. Relatedly therehave been changes in consumer preferences, withper capita meat consumption falling from 20.9 kgin 1980 to 16.6 kg in 2002 (Meat and Livestock Com-mission, 2005) and increasing concentration of mar-ket power, with 75% of fresh/frozen beef soldthrough multiple retailers. Recent health and safetyconcerns, coupled with changes in consumer life-styles and demand, have resulted in the share of

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005

THE LIMITS OF LEAN MANAGEMENT THINKING

red meat consumption within the total meat marketbeing under continuous pressure. This has had a ma-jor impact on the market price for red meat products(Simmons et al., 2003).

This uncertainty about the future is most evidentwithin the beef industry, due to changes to CAP sub-sidies (decoupling) and the reintroduction of overthirty-month-old beasts (OTMS) into the supplychain. The potential effects of the loss of subsidiesand an influx of approximately 150,000 tonnes oflower quality beef onto the market are not fullyknown. This has led to calls for increased collabora-tion to reduce risk and uncertainty, stimulate innova-tion and increase value creation for everyone in theindustry (Van der Vorst et al., 1998).

The UK Government’s response to this crisis was theformation of a Policy Commission, which produced aReport into the creation of a sustainable future forfarming (Curry Commission, 2002). This led to thecreation of three industry-wide agencies to facilitatenew thinking in red meat supply chains. The threeagencies are the Food Chain Centre (FCC), with a briefto support lean thinking and efficiency improvementacross all British agriculture sectors (dairy, cerealsand fresh produce), the Red Meat Industry Forum(RMIF), which was created to oversee ten projectsto assist in the improvement of efficiency and com-petitiveness in British red meat supply chains andthe English Farming and Food Partnership (EFFP) to fo-cus on the potential for collaboration within farming.

The RMIF embarked initially upon a Value ChainAnalysis (VCA) project to study and map ten valuechains within UK agriculture: sugar cane and pota-toes (1996/97); cereals (1997/98); beef, milk, oilseeds,pig, poultry, salads and vegetables and sugar beet(1998). These projects were based upon lean thinkingand integrated supply chain management principles(Womack and Jones, 1996). The rationale was that, byunderstanding the causes of waste and inefficiencyfrom poor co-ordination and uncertainty, it wouldbe possible to generate win-win outcomes for themajority of participants in the industry. Unfortu-nately, while there has been considerable success inidentifying the sources of waste in the ten valuechains analysed, the building of collaborative intra-company teams to generate win-win integratedsupply chain improvements has not been very suc-cessful. The major reason for this it is argued becauseit has been very difficult to achieve the desired levelsof trust between participants in the chain (Simmonset al., 2003). This is an explanation for failure that isoften used by analysts of non-integrated and poorlyco-ordinated buyer and supplier relationships (Car-lisle and Parker, 1989; Sako, 1992).

This apparent failure of inter-organisational collabo-ration requires explanation and, in the next section,recent critiques of the lean approach that explainwhy such failures may be predictable are discussed.

European Management Journal Vol. 23, No. 6, pp. 648–662, December 20

These explanations are based, first, upon operationalcriticisms of the lean paradigm and, second, on thecommercial critique from the power and leverageperspective. This discussion is then followed by ananalysis of the appropriateness of lean supply chainmanagement for the fresh/frozen beef supply chainsmanaged by multiple retailers and integrated foodprocessors. This study was primarily funded by theEPSRC, and undertaken in conjunction with theNorth West Food Alliance (NWFA), the RMIF andits consulting arm, the MLC.

Lean Thinking and the Power and LeveragePerspective on Appropriateness in Strategyand Relationship Management

There is considerable debate about the most effectiveway for companies to manage their buying and sell-ing relationships to achieve sustainable business suc-cess. Historically, Michael Porter (1980) argued thatcompanies should always think about buyer andsupplier power and their ability to augment this toachieve competitive advantage. More recently therehas been a radical re-appraisal in favour of win-win principles of commercial exchange (Branden-burger and Nalebuff, 1996); relationship marketing(Gummesson, 1999); and, partnership sourcing oralliancing (Macbeth and Ferguson, 1994).

It is clear that much of this thinking has informed re-cent government and food supply chain initiatives.The ten VCA studies outlined above were predicatedon emulating the lean and highly collaborative ap-proaches adopted, initially, by Toyota in the Japaneseautomotive sector. This approach seeks to find waysto deliver exceptional value to end customers byfinding ways of eradicating waste and inefficiencythroughout the supply chain (Womack and Jones,1996; Hines et al., 2000). There are, however, writerswho have argued that lean approaches may not haveuniversal applicability for all organisations. The cri-tique of the lean way of thinking can be dividedbroadly into those that focus primarily on opera-tional issues (agile and batch critiques) and those thatfocus on the limits imposed by the need to create acommercial and operational synergy before this ap-proach can be used by buyers and suppliers through-out a supply chain (the power and leverage critique).

(a) Agile and Batch Production: The OperationalCritique of LeanThere are two major operational critiques levelled atthe lean approach. The first is associated with the agileschool (Fisher, 1997; Christopher and Towill, 2002;Lee, 2002). This contends that the lean approach isnot always the most appropriate way to manageinternal processes or external relationships. The leanapproach operates best when there is high volume,predictable demand with supply certainty, so thatfunctional products can be created. In low volume,highly volatile supply chains, where customer

05 649

THE LIMITS OF LEAN MANAGEMENT THINKING

requirements are often unpredictable and suppliercapabilities and innovations are difficult to control,a more responsive or agile approach, based on inno-vative products, is appropriate operationally. Table1 shows the demand and supply characteristics thatoperate in primarily lean and agile supply chains.

It is clear, therefore, that supply chains cannot bemanaged using only lean techniques because theyhave very unique demand and supply characteristicsthat require very different operational ways of work-ing both internally and externally. Indeed, some-times ‘agilean’ approaches may be necessarybecause there are decoupling points in supply chainsthat require a lean approach at one point and a moreagile approach at another (Naylor et al., 1999).

A second operational critique of lean is the operationalappropriateness school that denies the universal appli-cability of the approach as a system of production(James-Moore and Gibbons, 1997; Lowe et al., 1997).It is argued that there is considerable evidence inthe automotive sector of the continuation of batchand craft based systems of production amongst spe-ciality and specialist component manufacturers. Fur-thermore, there is little evidence that all productionsystems are moving towards the lean model in allindustries. This is because just-in-time flow for pro-duction cannot be sustained unless production level-ling is possible within the organisation internally andwith the suppliers in the supply chain externally(Cooney, 2002).

(b) The Power and Leverage Perspective: The Strategic andCommercial Critique of LeanThere is also a school of thinking that questions theuniversal applicability of the lean paradigm from astrategic and commercial perspective. Some writersin this school (the anti-power school of writing) havecommented on the difficulty of achieving win-winoutcomes when there is a dominant buyer in the sup-ply chain. Writers in this school tend to emphasise theone–sided commercial benefits that flow from suppli-ers to buyers when lean partnering approaches areadopted, and call for a more equitable approach tothe sharing of value in the chain fromwaste reduction

Table 1 Lean and Agile Product Profiles

Distinguishing Attributes Lean Supp

Typical products Functional p

Marketplace demand Predictable

Product variety Low

Product life cycle Long

Customer drivers Cost

Profit margin Low

Dominant costs Physical cos

Stockout penalties Long-term c

Purchasing policy Buy materia

Informatioin enrichment Highly desir

Forecasting mechanism Algorithmic

650 Europe

and inefficiency improvement programmes (Ramsey,1996; Maloni and Benton, 2000; Emiliani, 2003).

The power and leverage perspective provides a less nor-mative critique. This approach contends that there cannever be any one single best way (lean or agile) ofmanaging business strategy and operational delivery.On the contrary any approach that claims universalapplicability must be false because the business envi-ronment is in constant flux and this requires compa-nies to be flexible about which operational means arethe most conducive for sustaining business strategy.Managers, therefore, should have an openmind aboutwhether or not they should adopt any particular oper-ational means and, as a result, the lean collaborativeapproach to external relationships cannot be a univer-sally applicable operational delivery mechanism forall companies in all circumstances (Cox, 2004a).

The first requirement for companies, therefore, is todecide on what their commercial rather than theiroperational strategy should be. When devising acommercial strategy it is essential that companies de-cide whether they are trying to achieve above normalreturns (double digit profitability), or whether theyare attempting to achieve low or normal returns.Whatever the operational means that are devised todeliver a particular commercial goal––based on dif-ferentiation or cost leadership––the consequence willbe that it either leads to above normal returns or lowor normal returns commercially.

This approach also holds that whether or not a com-pany can pursue any operational means to achieveits commercial ends successfully depends, ulti-mately, on the power circumstances it finds itself incurrently, and whether or not it has opportunitiesto leverage the desired outcome in the future. Allcompanies act as both buyers and suppliers andFigure 1 provides a way of thinking about the powerand leverage position that can exist between buyersand suppliers as they strive to achieve their preferredoperational means and commercial ends.

The Figure shows that buyers normally will be in aposition to achieve all that they desire operationally

ly Agile Supply

roducts Innovative products

Volatile

High

Short

Availability

High

ts Marketability costs

ontractual Immediate and volatile

ls Assign capacity

able Obligatory

Consultative

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005

THE LIMITS OF LEAN MANAGEMENT THINKING

and commercially at the expense of suppliers if theyare in a position of buyer dominance (>) and, some-times, when they experience independence (0). Whensituations of interdependence (=) occurs it is normalfor the buyer and supplier to share the value fromthe exchange relationship; when supplier dominance(<) occurs it is normally the supplier who is able toachieve all of their operational and commercial goalsat the expense of the buyer. From the perspective ofany individual company in a supply chain thismeans that the most desirable leverage position isto be able to dominate relationships with both its cus-tomers and its suppliers (i.e. to impose price andquality standards both downstream and upstream).

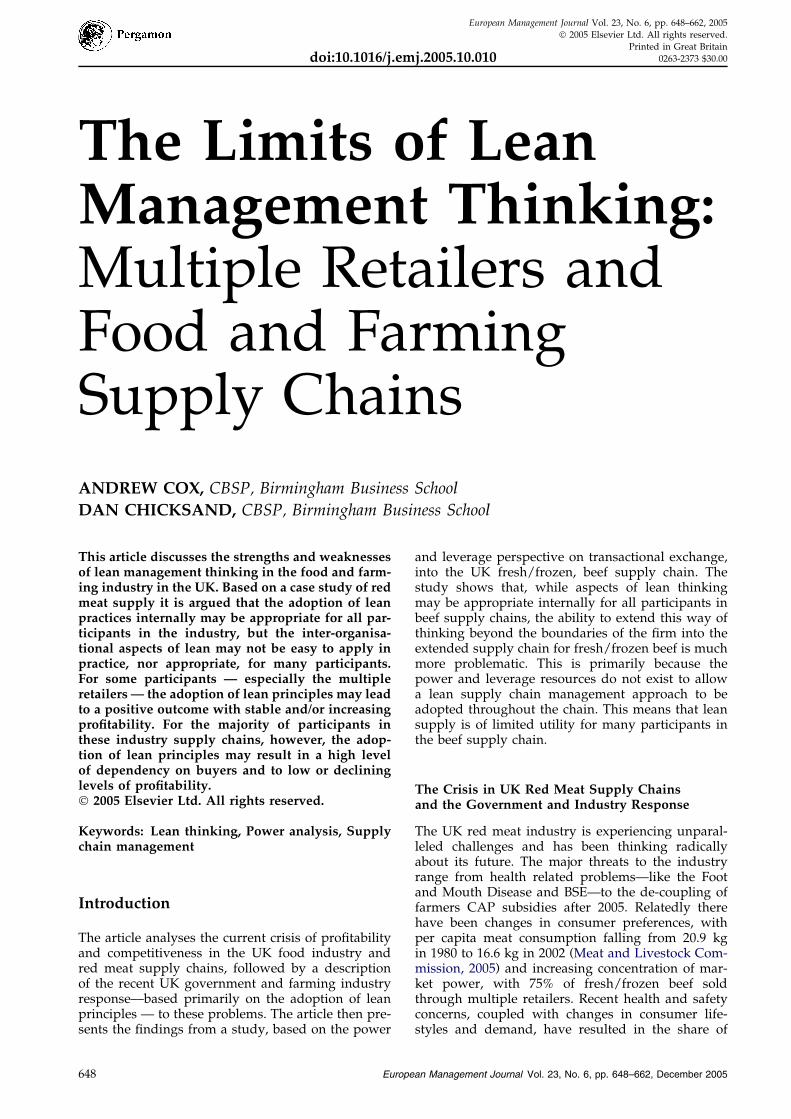

This is known as Janus-faced Dominance (Cox et al.,2000): it occurs when a company appropriates themaximum share of value for itself in the form ofabove normal returns (rents) by achieving both buyerdominance upstream and supplier dominance down-stream (Figure 2). It is under these circumstances thatone might expect companies to be able to consis-tently earn above normal returns commercially. The

BUYER DOMINA

Few buyers/many suppliersBuyer has high % share of tsupplierSupplier is highly dependentrevenue with few alternativeSupplier's switching costs arBuyer's switching costs are Buyer's account is attractiveSupplier's offering is a standcommodityBuyer's search costs are lowSupplier has no information advantages over buyer

INDEPENDENC

Many buyers/many suppliersBuyer has relatively low % smarket for supplierSupplier has little dependenrevenue and has many alterSupplier's switching costs arBuyer's switching costs are Buyer's account is not particto supplierSupplier's offering is a standcommodityBuyer's search costs are relSupplier has very limited infoasymmetry advantages over

HIGH

LOW

Attributesto Buyer

Power Relative to

Supplier

LOW

Robertson Cox Ltd. 2000 All Rights Reserved Source: Adap

Figure 1 The Power Matrix: Attributes of Buyer and Supp

European Management Journal Vol. 23, No. 6, pp. 648–662, December 20

problem for companies is, however, that, if they arenot able to operate as sellers in supplier dominance(<) or interdependence (=) downstream, then it is un-likely that above normal returns will be made. If thisis compounded by an inability to achieve buyer dom-inance (>) upstream, then it is likely that the companywill be on a treadmill to oblivion commercially––it willmake only low or normal returns.

From this perspective the lean approach may sufferfrom serious flaws strategically. Toyota developedthe lean approach, but it makes only low returns. Itfollows from this that, even before one considerswhether or not the lean approach is desirable opera-tionally, one must question whether this commercialmodel (based on passing value to customers in orderto win volume, but with relatively low returns) is onethat companies should be seeking to emulatestrategically.

There is a further commercial issue with the deliverymechanism favoured by advocates of both leanand agile operational approaches. Writers in these

INTERDEPENDENCE (=)

Few buyers/few suppliersBuyer has relatively high % share of total market for supplierSupplier is highly dependent on buyer for revenue with few alternativesSuppliers switching costs are highBuyers switching costs are highBuyers account is attractive to supplierSupplier s offering is relatively uniqueBuyers search costs are relatively highSupplier has moderate information asymmetry advantages over buyer

NCE (>)

otal market for

on buyer for se highlowto supplierardized

asymmetry

E (0)

hare of total

ce on buyer for nativese lowlowularly attractive

ardized

atively lowrmation buyer

SUPPLIER DOMINANCE (<)

Many buyers/few suppliersBuyer has low % share of total market for supplierSupplier has no dependence on buyer for revenue and has many alternativesSupplier's switching costs are lowBuyer's switching costs are highBuyer's account is not particularly attractiveto supplierSupplier's offering is relatively uniqueBuyer's search costs are very highSupplier has substantial information asymmetry advantages over buyer

HIGH

Attributes toSupplier Power

Relative to Buyer

ted from Cox, A (2001), p. 14

lier Power

05 651

BUYERSBUYERS

Individualand/or

CorporateCustomers

Individualand/or

CorporateCustomers

JANUS-FACED DOMINANCEJANUS-FACED DOMINANCE SUPPLIERSSUPPLIERS

All types ofsuppliers of

products andservices

All types ofsuppliers of

products andservices

Demandmanagementcompetence

Demandmanagementcompetence

Procurement and supplycompetence

Procurement and supplycompetence

SupplierDominance

(<)

BuyerDominance

(>)

Company able to makeabove normal returns

at this point in thesupply chain

Company able to makeabove normal returns

at this point in thesupply chain

RENTS

Source: Robertson Cox Ltd, 2000. All Rights Reserved.

Figure 2 Janus-Faced Dominance in Business and the Supply Chain

THE LIMITS OF LEAN MANAGEMENT THINKING

schools normally recommend that operational collab-oration should be based on win-win (equity based)approaches to commercial exchange. It has beenargued that, while equitable sharing of commercialvalue is one approach to exchange, it may not be thebest way to maximise commercial returns for eitherparty. If there is an alternative for either party thatprovides a higher share of value than equity, andwhich is also just as sustainable overtime, then thisapproach may be seen to be commercially superiorfor whichever party is able to achieve it (Cox, 2004b).

It has also been argued that power circumstancesunderpin the successful operational and commercialimplementation of exchange relationships. This is be-cause, unless there is a power situation of buyer dom-inance or interdependence, long-term collaborationcannot be sustained by a buyer. Conversely, collabo-ration cannot be sustained overtime for a supplierunless there is a power circumstance of supplier dom-inance or interdependence (Cox et al., 2004). This per-spective also holds, therefore, that lean approachescannot be implemented successfully within supplychains as a whole unless they are characterised by ex-tended dyadic exchange transactions of buyer domi-nance and/or interdependence. This means thatwithout an understanding of the power and leveragecircumstances that prevail it is not possible to predictwhich operational means are capable of successfulcommercial implementation in relationships.

From this perspective lean is normally a strategy forlow commercial returns (a treadmill to oblivion), espe-cially when it is based on passing value to customersusing equity-based collaboration. In these circum-stances value will have to be shared but, since mostof it is to be passed to customers, there is unlikelyto be much value left for participants in the chain.Lean can potentially be a recipe for above normal re-turns, however, if one player in the chain is able to

652 Europe

appropriate the lion’s share of the value for them-selves through Janus-faced Dominance. The problemis, of course, that such an approach cannot be sus-tained for long unless aligned exchange partnerscan be found––i.e. willing supplicants making lowreturns. If such supplicants cannot be found, and ifcustomers can insist on receiving continuousimprovement in value, then it is unlikely that leancan provide the basis for above normal returns.

It is also argued that, while lean approaches may berelatively easy to implement internally, they may bevery difficult to implement externally–particularlyif the power and leverage circumstances are non-conducive, and also if suppliers lack the competen-cies internally to undertake what is required (Coxet al., 2004). Given this, the full scale operationalisa-tion of lean, agile and agilean supply chain manage-ment thinking is fraught with significant commercialand operational difficulties for companies imple-menting these approaches beyond their own organi-sational boundaries.

The power and leverage perspective, while acceptingthat lean approaches may be viable strategies forsome companies, provides therefore a way of pre-dicting the likelihood of success or failure for suchapproaches in specific dyadic exchange relationshipsand within particular supply chains and markets.The research findings reported here test out the util-ity of this perspective based on an analysis of thesupply chain for fresh/frozen beef in the UK.

Testing Lean Thinking in the Beef IndustryUsing Power and Leverage Analysis

Since 2002 lean has been the approach favoured bygovernment agencies for the creation of sustainablefarming in the UK. In recent years, however, there

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005

THE LIMITS OF LEAN MANAGEMENT THINKING

has been a growing scepticism amongst some indus-try participants about the utility of lean thinking foreveryone in the industry (interviews with NWFAand RMIF personnel and industry participants).The industry had assumed that the lean approachwould provide an opportunity for all participantsin the chain to improve their commercial returnsfrom working together. When this did not material-ise there has been disappointment and growing scep-ticism. In particular there has been a concern that theten VCA studies have not provided any new under-standing of, or solutions for, ‘carcass imbalance’.

This problem arises because there is rarely a balanceof specific types of meat cuts from the beasts that areslaughtered upstream to allow for a sustainable andpredictable supply, enabling productive efficiency,downstream (Simmons et al., 2003). As a result of amismatch between demand requirements and sup-ply availability there is nearly always inefficiencyand undesirable commercial costs to be borne atthe primary production (processor) stage of the sup-ply chain that is almost impossible to eradicate.Unfortunately the VCA studies did not find any rad-ical ways of overcoming this problem, nor of eradi-cating the relatively high levels of opportunismendemic within red meat supply chains, as a resultof short-term demand and supply misalignments.

Given this the RMIF and the NWFA have looked foran alternative way of thinking about how to developstrategies for UK red meat supply chains. The re-search findings reported here are part of a researchproject into the applicability of power and leveragethinking, as a way of understanding, to what extentlean or alternative strategies can be implementedsuccessfully within UK food supply chains. This arti-cle specifically addresses the problems of managingwithin fresh/frozen beef supply chains in the UKand shows why it is that lean approaches are verydifficult to implement throughout the chain andwhy, even when it is feasible for some participants,it may not be the basis for above normal returns com-mercially for all of them. It also explains why oppor-tunism and a lack of trust––which are often regardedas the curse of red meat supply chains––is a perfectlyrational response by industry participants experienc-ing unavoidable demand and supply misalignmentsand high levels of uncertainty.

The research project was undertaken using a struc-tured questionnaire and interviews with key indus-try players within the fresh/frozen beef supplychain. The questions were derived to allow theresearchers to map the power relationships betweenbuyers and suppliers at each dyad in the chain.Questions specifically addressed demand and sup-ply characteristics; the nature of competitive forces;and, the issues of utility, scarcity and informationasymmetry between buyers and suppliers at eachdyad in the chain (Figure 1). The interview responseswere supplemented with extensive market informa-

European Management Journal Vol. 23, No. 6, pp. 648–662, December 20

tion provided by the Red Meat Industry Forum andthe Meat and Livestock Commission. From this itwas possible to describe the power regimes withinthe UK fresh/frozen beef industry.

On the Nature of Power and Leveragein UK Beef Supply Chains

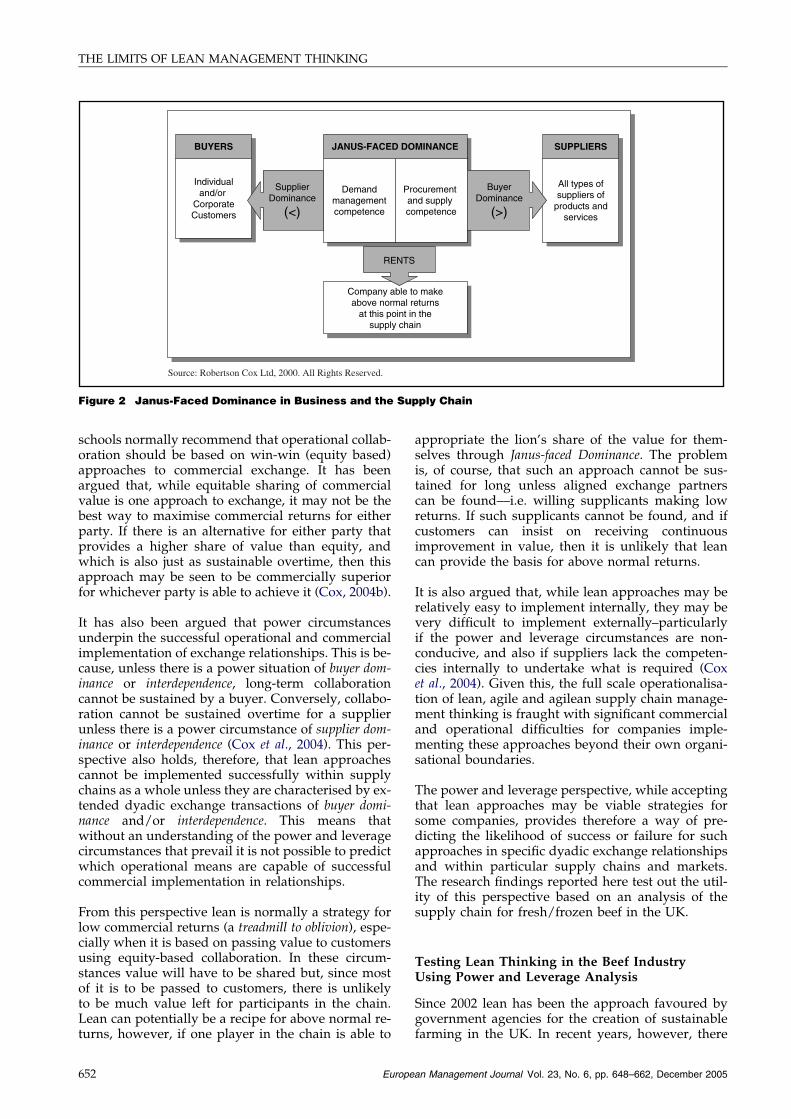

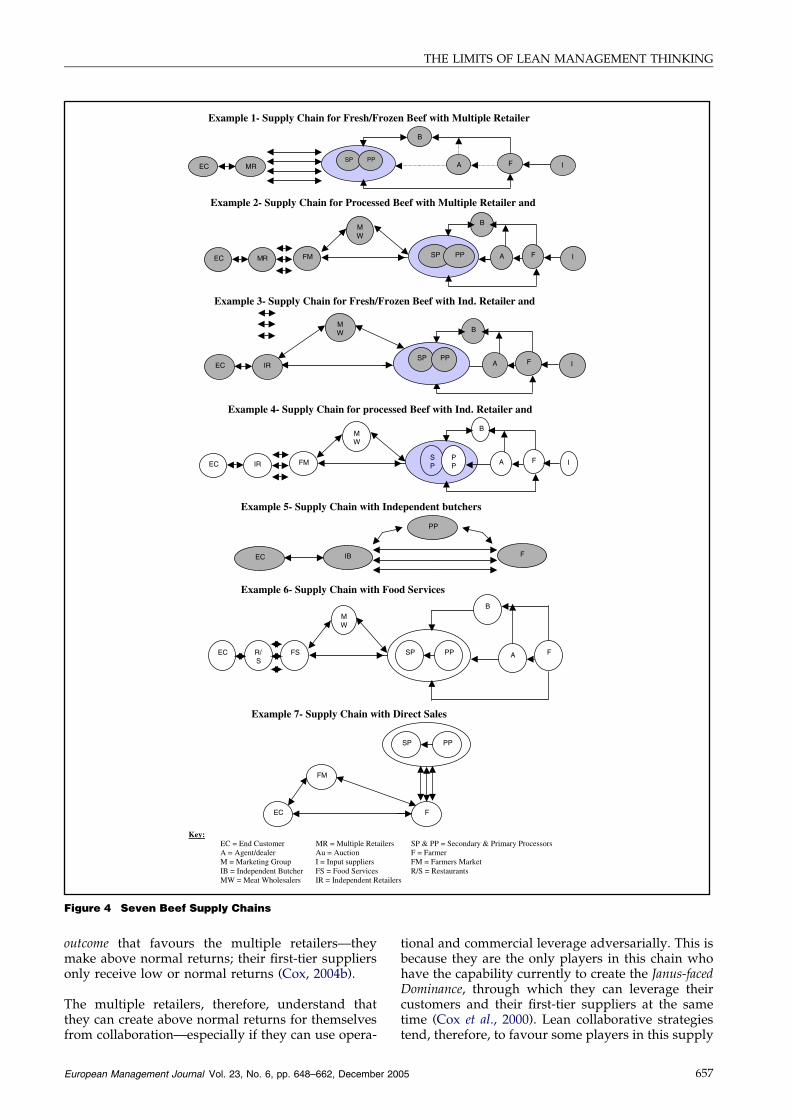

(a) The Complexity of UK Beef Supply ChainsThe UK beef supply chain cannot be described as onebecause it is characterised by many different supplychains. Figure 3 provides an indication of the overalllevel of complexity that arises from the very differentroutes to market for beef, with a generic representa-tion of both the value and physical flows from farmerthrough to the end customer.

Figure 4 provides an overview of seven (although notall) of the sub-supply chains that characterise thegeneric UK beef supply chain. This indicates thatthe supply chain as a whole is quite varied in thestructure and number of routes to market. These dis-tinct supply chains have both fairly regular and stan-dardised demand and supply for certain products,but they also experience tremendous irregularityand uncertainty of demand and supply for otherproducts and services, all of which are derived fromthe same raw material––a cow or a bull.

One of the most important factors, directly impactingon the power of buyers and sellers at all points inbeef supply chains, is the fact that different types ofbeef products are created from an ‘exploding beast’.This means that, unlike many supply chains that areprimarily constructed to bring together complex sup-ply inputs into one finished product, the beef supplychain is partially characterized by the opposite. Theprimary processing stage (abattoirs) is a disassemblyprocess, although elsewhere in the chain––at the sec-ondary processing stage–a traditional assembly pro-cess exists (Bourlakis and Weightman, 2004).

The beef supply chain is, therefore, characterised bycomplexity. There are variable qualities of beastsentering the chain, with different eating and variablemarketing potentials. Beef beasts also have differentorigination characteristics––purebred, continentalcross or bull-beast as a by-product from the dairyherd. Whatever its origination, the beast does not be-come one, but ‘explodes’ into many different prod-ucts (both fresh & frozen e.g. rump, sirloin, minceand processes e.g. pies and ready meals etc.). Eachof these products has its own unique demand andsupply problems for participants in the chain.

On the demand side, while at the national level thedemand for beef is known and fairly predictablegiven seasonal and weather fluctuations, for an indi-vidual producer demand has often been uncertain.Farmers typically receive poor forecasts and haveno certainty of demand or price, because there areno formal contracts in place with customers for the

05 653

THE LIMITS OF LEAN MANAGEMENT THINKING

suckler beef producers, with most sales taking placethrough agents or direct with processors. Meat pro-cessors also do not have formal contracts in placewith their customers (including the multiple retail-ers). Processors normally have non-legally binding‘Supply Agreements’ with multiple retail customers,which typically run for one year.

This is true even though consolidation of supply hasoccurred. Recently, Sainsbury’s consolidated its de-mand into one supplier for beef (ABP), and fromthree suppliers to one for lamb (Rose County-Partof Dungannon Meats). This consolidation may, infuture, provide a greater certainty for preferred sup-pliers from the major multiples, and further consoli-dation to single sourcing by species continues to bethe most likely trend in the future. Despite this, with-in a ‘Supply Agreement’, even for preferred suppli-ers, there is still a high level of uncertainty bothabout the relationship being continued and aboutthe level of demand that will occur.

The ‘Supply Agreement’ normally has detailedspecification parameters (e.g. farm assured beef,conformity & leanness requirements, packagingspecifications and future requirements — althoughdemand is uncertain and one week processors mayhave to supply X amount of mince, the followingweek 2X of mince). Multiple retailers also normallyspecify that beef to be sold as fresh or frozen cannotbe procured via the auction markets for ‘animal wel-fare’ reasons. This structure provides an effective

Key:E = Exports, E/I = Exports/Imports, EC= End Customer,Butchers, IR= Independent Retailers, MR= Multiple RetAgents, A= Auctions, F= Farmers, I= Inputs

FLOW

PHYSICA

EC

IB

FS

MR

IR

DS

SECONDBY-

PRODUSUPPLCHAIN

LIVERS, HEARTS, OFFAL AND OTHER BY-PRODUCTS

E

MW

Sec.Proc

E/I

Figure 3 The Beef Herd in the UK: Understanding the Flow

654 Europe

mechanism through which dominant customers canretain control operationally and commercially oftheir preferred processors.

On the supply side farmers are supported by subsi-dies (although no longer subsidised to produce),but there are relatively low levels of capital requiredto set up given the small scale of most farms. Mostproduction is extensive and seasonal; there are longlead times (it usually takes between 24–30 monthsto produce and finish an extensively reared sucklerbeast); and, the primary meat cut products are of rel-atively high variety and heterogeneous. Primary pro-cessing (the abattoirs) is dispersed throughout thecountry and complex, with considerable secondaryprocessing required, serviced by a widely dispersedfarming supply base.

Given all of this there is often a problem of aligningdemand and supply for particular cuts of meat to pro-vide the optimal volumes to ensure that just-in-time(continuous pull and flow rather than push andbatch) production can occur. This creates the problemof ‘carcass imbalance’ that directly affects power andleverage positions within the chain, and which is cru-cial for an understanding of which relationship strat-egies are commercially and operationally appropriatefor particular participants in the chain. The analysisthat follows, of the supply chain through which themultiple retailers obtain fresh/frozen beef productsfrom integrated (primary/abattoir and secondary)food processors, explains how and why.

FS= Food Services, IB= Independent ailers, MW = Meat Wholesalers, B= Buying

OF VALUE

L FLOW

A F I

Beef from pure bred beasts from suckler herd

Beef from continental cross beasts from dairy

Beef from bull beasts as by-product of the

ARY

CTY

Prim.Proc

B

E/I

B

of Value and Physical Flow

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005

THE LIMITS OF LEAN MANAGEMENT THINKING

(b) The Power Regime for Fresh/Frozen Beef ProductsAs Figure 5 indicates the power relationship betweenthe end consumer and the multiple retailers in thischain are characterised by independence (0) or supplierdominance (<). This means that end consumers havelimited power to extract value from multiple retail-ers. If value improvement occurs (either in the formof lower prices or better quality for particular prod-ucts) it is normally determined by the supplier in re-sponse to competitive pressures in local markets.

This is due to the following major factors:

v the relatively low number of alternative multiple retailsuppliers to choose from in specific local markets;

v there are many potential alternative customers;v the volumes being purchased by consumers are rela-

tively low;v the switching costs for both the supplier and buyer are

low;v search costs are low for the buyer but bundled supply

offerings within particular retail outlets creates lock-in within particular localities; and,

v the products-many are relatively standardised butinformation asymmetry favours the supplier.

Given this, the power structure oscillates betweenindependence (when there are many alternativesources of supply for fresh/frozen beef close-by, withconstant price wars taking place and the product is alow value commodity) or supplier dominance (whenthere are no real alternative sources of supply close-by, with no price wars and the product is a high valuepremium product). Value (either as better quality orlower prices or both) will only pass to the end con-sumer, therefore, when independence occurs. But thisis driven primarily by market contestation and theend consumer is always a price and quality receiver.

In such an environment there are few incentives forbuyers or sellers to enter into long-term collaborativerelationships. This is because it is logical for end con-sumers to either buy what is convenient locally or, ifthey have available alternatives, to search the marketfor better deals. If end consumers opt for the formerapproach they would adopt the non-adversarialarm’s-length relationship management style outlinedin Figure 6. If they chose instead to search for betterlocal deals they would be operating in the adversarialarm’s-length relationship style. Both of these arm’s-length relationship management approaches areperfectly rational and logical responses for end con-sumers given the power circumstances prevailing.

The same logic is true for multiple retailers. This isbecause there are few benefits to be obtained as sell-ers from extensive forms of collaboration with endcustomers. The multiple retailers will use all typesof loyalty programmes or loss leaders (and other pro-motional campaigns) to stop end customers switch-ing to alternative sources of supply but, while they

European Management Journal Vol. 23, No. 6, pp. 648–662, December 20

may seek lock-in to their overall offerings, this can-not be regarded as a form of collaboration with theend consumer.

The multiple retailers oscillate, therefore, betweenmore or less adversarial forms of arm’s-length rela-tionship management with their customers. Whenthere are loss leaders they are operating non-advers-arially, when they are premium pricing particularproducts they are operating adversarially to maxi-mise returns. In both cases, however, the relationshipis arm’s-length operationally because neither party ismaking the dedicated investments in one another, ordeveloping the relationship specific adaptations orthe cultural norms, classically associated with highlevels of operational collaboration (Cannon and Per-reault, 1999). This is because the switching costs forconsumers in food supply chains are relatively lowand this reduces the scope for operational and com-mercial collaboration.

This is not necessarily the case at the next dyad in thechain. As Figure 5 indicates the power structure be-tween the multiple retailers and the integrated foodprocessors (secondary and primary production/abattoirs combined) is normally characterised bybuyer dominance (>). Multiple retailers normally havebuyer dominance when they source commoditisedproducts that are to be sold on a price basis relativeto a given quality standard. This is because they havethe following key power levers over suppliers:

v Few buyers, with many potential suppliers;v High volume relative to supplier business turnover;v Supplier switching costs high, those of the buyer rela-

tively low;v Buyer account is very attractive to suppliers for

revenue;v Supplier offerings are standard and commoditised;v Buyer search costs low; and,v Information asymmetry favours the buyer.

These power attributes ensure that when multipleretailers negotiate with integrated processors therelationship is normally commercially unequal. Thisis because the processors are normally highly depen-dent on the multiple retailers (due to the need to at-tain high utilisation of fixed assets and to aid inovercoming the issue of ‘carcass balance’), and mustsupply standard products at a price that minimisesthe returns earned by the processors. This power cir-cumstance can change in the short-term if there areseasonal variations in supply for particular cuts ofmeat, however, as the multiple retailers are in a posi-tion to switch to alternative suppliers with relativeease, it is unlikely that the processor will be able topass on extra costs due to supply shortages to themultiple retailers.

With the existence of longer-term collaborativerelationships between the multiple retailers and the

05 655

THE LIMITS OF LEAN MANAGEMENT THINKING

processors, and further consolidation (driven by thestrategy of multiple retailers to single source) at theprocessors stage, coupled with circumstances of po-tential supply shortages (due to decoupling), it couldbe argued that the integrated processors could createsituations of interdependence (=) in the future. How-ever, at present there is still overcapacity at the pro-cessing stage, resulting in high levels of contestationand weak returns for processors. This suggests that,at the present moment, operational collaborationwith preferred processing suppliers is occurring ina power situation of buyer dominance favouring themultiple retailers.

The power position of the processors could theoreti-cally be improved if they were to sell their own pre-mium branded products. In this circumstance itwould be the supplier’s brand that had customer rec-ognition and allegiance and, if the brand was verypopular, it is unlikely that multiple retailers wouldrefuse to stock it. In this circumstance the power po-sition would tend towards interdependence (=). This isbecause the power attributes of the buyer and sup-plier would be as follows:

v Few buyers, with one or few suppliers;v Buyer may have a large, but not total, share of market

sales for the supplier;v Supplier has some alternative channels to market;v Supplier and buyer switching costs relatively high;v Supplier finds buyer’s account attractive but buyer

highly values the supplier’s brand;v Search and transactions costs to find alternatives are

high for the buyer; and,v Supplier may have some product information asymme-

tries against the buyer.

In these circumstances the supplier is in a strongerbargaining position with the retailers, and they oughtto be able to extract a higher share of the commercialvalue from the exchange (and therefore higher re-turns). The retailers, because they need the brandedproducts in their stores, would have to forgo some oftheir commercial leverage in order to ensure supply.

It must be recognised, however, that this situation isnot unforeseen by the multiple retailers. One of themost contested areas in the relationship betweenmultiple retailers and food manufacturers (such asBernard Matthews, Cadbury’s, Coke, Nestle, Unile-ver, to name just a few) today is over branded items.The multiple retailers have recognised that, in orderfor them to appropriate the maximum share of value,it is essential that they minimise the power of sup-plier brands by creating their own premium brands.Thus, in the beef supply chain, Sainsburys has cre-ated its Jamie Oliver premium cuts range and ‘Tastethe Difference’; Tesco has ‘Tesco Finest’.

In this way the multiple retailers are attempting toundermine the leverage of processors in the chain.Furthermore, currently, there is no processor (or

656 Europe

farmer) owned fresh/frozen branded beef productthat is sold through the multiple retailers (althoughthere are brands such as Lakeland Beef and Cum-brian Fellbred which target service sector and directsales customers). Mark & Spencer and Waitrose selland market ‘Aberdeen Angus’ but this is a breed thathas been developed into a brand that is not owned byany specific farmer group/and or processor. Further-more, since there are currently many potential pro-cessors who are willing to produce the multipleretailers’ own premium brands, and because, thereis no direct competition from processor/producersdriven branded premium meat products, when themultiple retailers develop their own premium brand,their power and leverage position is, therefore, alsonormally one of buyer dominance (>) over processors.

Even though the power structures for premium andstandard products are characterised by buyer domi-nance, with most of the commercial returns being re-tained by the multiple retailers, there is stillconsiderable scope for buyers and processors toundertake operational collaboration based on leanprinciples at this point in the chain. First, there is nor-mally a high level of volume from the multiple retail-ers for both branded and non-branded goods. In thiscircumstance it is logical for preferred suppliers towork closely with multiple retailers to align theiroperational processes and systems in such a way asto minimise waste and inefficiency in the chain,and also to optimise service and quality delivery atthe lowest possible transaction costs possible.

To say that lean collaboration is operationally desir-able at this stage is one thing, whether or not it iscommercially a sensible idea is another. In situationsof buyer dominance the commercial benefits fromoperational collaboration tend to flow to the multipleretailers, who maximise value appropriation byusing adversarial collaboration and by forcing sup-pliers to collaborate non-adversarially (Figure 6).The fact that the multiple retailers have targeted sup-plier own brands demonstrates that they fully under-stand that they must do everything in their power tomake it difficult for processors to create their ownpremium brands. Their collaboration is aimed atensuring that they retain the maximum share of com-mercial value, even when they provide preferredsupplier relationships for standard products and/orpremium brands to some integrated processors.

This means that the commercial benefits of lean oper-ational collaboration are passed to the multiple retai-ler and not retained by the processor, who remainshighly dependent operationally and commerciallyon the multiple retailer, and acts as willing suppli-cant to their every requirement. The processorsmay receive higher volumes but only at the priceof operational and commercial dependency. Thismeans that the win-win is not based on equal shares:rather than a positive-sum outcome in which both par-ties make above normal returns this is a nonzero-sum

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005

EC MR SP PP

B

A I

Example 1- Supply Chain for Fresh/Frozen Beef with Multiple Retailer

EC MR SP PP

B

F IFM

MW

Example 2- Supply Chain for Processed Beef with Multiple Retailer and

EC

B

F I

MW

SP PPIR

Example 3- Supply Chain for Fresh/Frozen Beef with Ind. Retailer and

EC IRSP

PP

B

F IFM

MW

Example 4- Supply Chain for processed Beef with Ind. Retailer and

A

A

A

F

Key:EC = End Customer MR = Multiple Retailers SP & PP = Secondary & Primary ProcessorsA = Agent/dealer Au = Auction F = FarmerM = Marketing Group I = Input suppliers FM = Farmers MarketIB = Independent Butcher FS = Food Services R/S = Restaurants MW = Meat Wholesalers IR = Independent Retailers

IBEC F

PP

Example 5- Supply Chain with Independent butchers

FSEC R/S

SP PP

B

FA

MW

Example 6- Supply Chain with Food Services

FM

EC F

SP PP

Example 7- Supply Chain with Direct Sales

Figure 4 Seven Beef Supply Chains

THE LIMITS OF LEAN MANAGEMENT THINKING

outcome that favours the multiple retailers––theymake above normal returns; their first-tier suppliersonly receive low or normal returns (Cox, 2004b).

The multiple retailers, therefore, understand thatthey can create above normal returns for themselvesfrom collaboration––especially if they can use opera-

European Management Journal Vol. 23, No. 6, pp. 648–662, December 20

tional and commercial leverage adversarially. This isbecause they are the only players in this chain whohave the capability currently to create the Janus-facedDominance, through which they can leverage theircustomers and their first-tier suppliers at the sametime (Cox et al., 2000). Lean collaborative strategiestend, therefore, to favour some players in this supply

05 657

UNEQUAL

EQUAL

Commercial Exchange Favours One Party Rather than Another

Operational Exchange Based onLimited Transactional Linkages

Commercial Exchange Based onEquitable Returns

Operational Exchange Based onLimited Transactional Linkages

Commercial Exchange Favours One Party Rather than Another

Operational Exchange Based onExtensive Transactional Linkages

Commercial Exchange Based onEquitable Returns

Operational Exchange Based onExtensive Transactional Linkages

NATURE OF

COMMERCIAL

EXCHANGE

ADVERSARIAL ARMS-LENGTH ADVERSARIAL COLLABORATION

NON-ADVERSARIAL ARMS-LENGTH NON-ADVERSARIALCOLLABORATION

ARMS LENGTH COLLABORATIVE

NATURE OF OPERATIONAL EXCHANGE

Figure 6 Commercial and Operational Relationship Management Styles� Robertson Cox, 1998 All Rights Reserved. Source: Adapted from Cox, A (1999), p. 23

< / 0 / >=B

SP PPEC MR A F I

>0/ < >/ = / 0 / <

> / = / <

Key: EC = End Customers MR = Multiple Retailers SP = Secondary Processors

PP = Primary Processors B =Buying Agents

A= Auctions (Not Officially Used) F = Farmers I = Input Suppliers

Figure 5 The Frozen/Fresh Beef Power Regime with Multiple Retailers and Integrated Processors

THE LIMITS OF LEAN MANAGEMENT THINKING

chain more than others. This is not an abuse of powerby the multiple retailers but merely the logical out-come of dominant players using market and supplychain leverage to appropriate value for themselves.

The problem is, however, that in doing so it is possi-ble that they may be creating ‘‘treadmills to oblivion’’for those integrated processors who specialise incommoditised non-branded products, and thoseown branded suppliers who are not able to sustaindifferentiation in the face of direct competition fromthe multiple retailers’ own brands. Those that cannotdefend their brands will see their current collabora-tion shift from interdependence to buyer dominance,with the supplier increasingly locked into the multi-ple retailers’ control of this supply chain. They canonly expect lower commercial returns from collabo-ration when this occurs. This explains why in recentyears there has been increasing consolidationamongst integrated processors (in 2002/3 there were314 abattoirs, a quarter of the 1980 level). Consolida-tion on the supply-side is a classic response to buyerdominance as particular suppliers seek to increase

658 Europe

their negotiating power by reducing the number ofsuppliers in the market relative to the number ofbuyers (i.e. in an attempt to create a power positionof interdependence).

In the beef supply chain, therefore, lean collaborationis being used at the first-tier between the multipleretailers and the integrated processors, but this rela-tionship is one that is undertaken under a power sit-uation of buyer dominance that favours the multipleretailers. Despite this the scope for fully integratedsupply chain management based on lean principlesis much more tenuous further upstream in the UKbeef supply chain. Figure 5 shows that, apart fromthe relationship between the processors and somepreferred buying agents, the power structures inthe UK beef supply chain are not conducive to ex-tended forms of operational or commercial collabora-tion. As a result, relationships, historically, have beenshort-term arm’s-length and opportunistic. This isprimarily because demand and supply misalign-ments occur frequently further upstream in thechain, and this means that there are few operational

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005

THE LIMITS OF LEAN MANAGEMENT THINKING

or commercial incentives for any party to enter intolong-term collaborative relationships. Rather thanthis retreat into short-termism being seen as evidenceof poor relationship management this outcome canbe seen as a perfectly rational response to demandand supply uncertainty by the majority of upstreamparticipants in the chain.

As Figure 5 indicates the integrated processors in thechain potentially have upstream relationships withthree major suppliers. These are the auctions (A),the buying agents (B) and the farmers (F). However,for fresh/frozen beef there is no direct relationshipbetween the processor and auction markets as trace-ability, provenance, conformability and animal wel-fare are critical for the buyer. Processors will,therefore, never (officially) buy beef for multipleretailers from the auction markets, as typically thesecustomers specify that processors buy direct fromfarmers or via their own or contracted agents directfrom farms. Multiple retailers insist beef is sourcedfrom either the National Farm Assured Programme(Red Tractor) or from their own supply programmes.Auctions are avoided as an unnecessary link and foranimal welfare reasons.

Farmers in general, whether they are supplyingthrough agents or auctions, experience value erosionin favour of those further downstream. This is dem-onstrated by the fact that average farm price for beefin the 3rd quarter of 2004 was 193 pence per kgagainst 419 pence per kg once retailed. The pricespread between farm and retail price has also signif-icantly widened from 40% in 1993 to 54% in 2004(Meat and Livestock Commission, 2005). There arealso many other suppliers in the chain providing sup-ply inputs (I) for farmers. These relationships are notdiscussed in detail here because, whatever power andleverage farmers have over their supply inputs thepower structures vary (>/=/0/<) based on the scaleand size of the farmers being serviced and the partic-ular products and services being sourced.

Buying agents play an important, if often over-looked, role within the beef supply chain. They arethe interface between the producers and the proces-sors and are highly skilled individuals with the abil-ity to determine the quality of beasts from visualinspections on the farm. Processors, therefore, relyon agents to procure the right quality beasts fromthe market place. Agents or buyers have varyingpower resources depending upon the type of rela-tionship they have with the processor and who theend customer is. When buying on behalf of proces-sors for the multiple retailers the relationship is nor-mally one of interdependence (=). This is because thebuying agent works predominantly with one proces-sor (or a small number of clients) as a contract buyer.Their relationship is very close and collaborative.

In the case of a contract buyer, therefore, the powerattributes of the buyer and supplier are as follows:

European Management Journal Vol. 23, No. 6, pp. 648–662, December 20

v Few buyers, with one or more supplier;v Buyer may have a large, but not necessarily the total,

share of market sales for the supplier;v Supplier and buyer switching costs relatively high (in

terms of perceived risks of finding either a new buyerand appropriate supplier);

v Supplier finds buyer’s account attractive but buyerhighly values the supplier’s knowledge and contacts;

v Although search and transactions costs to find alterna-tives are relatively low for the buyer;

v The supplier has potentially product information asym-metries against the buyer (knowledge of where to sourceproducts that conform to end user requirements) andhas long-term relationships established with theproducers.

As the agents are close to the supply market in termsof their relationships with suppliers they often posseskey information resources over both the farmers andthe processors. Whether they use their role as a mid-dleman to act opportunistically will depend upon thenature of the relationship. As a contracted buyer for alarge multiple retailer the incentive to act opportunis-tically and use their potential power position duringtimes of supply scarcity is restricted by the risk of los-ing their contract with their primary customers. Thenormal relationship management style for buyingagents working with the multiple retailers and pro-cessors is therefore also non-adversarial collaborationbased on lean management principles.

The power position between the integrated proces-sors and the farmers is very different. This is be-cause, due to the problem of ‘carcass imbalance’, itcan oscillate between buyer dominance (>), interdepen-dence (=) or supplier dominance (>). The power of thefarmer vis-a-vis the processors varies dependingupon supply scarcity. When a particular quality beef(for instance R4 on the Euro Grid system), as speci-fied by the customer, is in shortage, then farmers inpossession of the desired beasts, during a shortwindow of opportunity, may be able to obtain veryhigh returns from supplier dominance (<). There canalso be interdependence (=) power outcomes whenlong-term collaborative relationships are establishedbetween farmers and processors, whereby abovenormal returns are offered to farmers in return forgreater levels of guaranteed supply. This is an at-tempt by processors to lock-in opportunistic farmersto ensure supply continuity and conformity and,thereby, reduce supply risk. When there is over-sup-ply farmers tend to become price-takers and proces-sors take advantage of this buyer dominance (>)situation.

When there are long-term agreements in place, witha high degree of information flow between the pro-cessors and the farmers regarding demand forecasts,delivery, quality and conformity, the relationshipsare collaborative. Where there is equitable sharingof any of the gains from improved efficiency and orconformity then the relationships is best described

05 659

THE LIMITS OF LEAN MANAGEMENT THINKING

as non-adversarial collaborative. (The Waitrose sup-ply chain operates in this way because end customersare willing to pay for better quality and traceabilityin the supply chain and processors and farmers re-ceive above normal industry returns). In most othermultiple retailers’ supply chains the relationship isbetter described as adversarial collaboration withthe benefits from close working relationships beingunequally shared in favour of the processor, who inturn is forced to pass the majority of the value ontothe multiple retailer.

Overall, however, both the processors and the farmersnormally operate on a short-term adversarial or non-adversarial arm’s-length basis. This is because–giventhe volatility and uncertainty in demand and supplyand the problem of ‘carcass imbalance’––there are fewincentives available for both parties to pursue leansupply principles. As a result both parties have tendedto behave opportunistically depending on which ofthem has the balance of power given the shortage orabundance of supply for particular types of beef cuts.

The power position between the buying agents andthe farmers is similar and can be described as oscillat-ing between buyer dominance (>), independence (0) andsupplier dominance (>). The reasons for these changingpower circumstances can be attributed to the sameconditions that operate in the relationship betweenprocessors and farmers. In periods of supply short-ages the farmer is often in a strong position, and willhave the option to sell via a range of marketing routesto obtain the highest returns (for farmers this will in-clude auction markets). Conversely, in some circum-stances, the buying agent may find themselves in astrong position due to their position as middlemen,especially during periods of excess supply. Withprices depressed, and with high levels of price obscu-rity, buyers/agents may find themselves in a positionto maximise returns. Again, due to the large numberof potential buying agents within the market as awhole and the large number of potential suppliers,the relationship is often one of independence (0), withthe market driving the price. This is similar to the cir-cumstances that exist within a spot market.

The appropriate relationship management styles,therefore, vary depending on the power relation-ships that exists but there is a tendency––given thevolatility and uncertainty of demand and supply––for all relationships to be managed in a short-termand arm’s-length manner. A buyer or supplier willnormally choose adversarial over non-adversarialarm’s-length relationship styles whenever the powercircumstances favour their bargaining position andvice versa when it does not. Opportunism is normallyrife in such circumstances and is driven as a rationalresponse by buyers and sellers to the volatility of de-mand and supply. This, as we shall see below, ishardly a conducive environment for the develop-ment of a fully integrated and lean supply chainmanagement approach.

660 Europe

Conclusions: Is a Lean Supply Strategy Feasiblein the Multiple Retailer Fresh/Frozen BeefSupply Chain?

The findings demonstrate that the power regime thatexists in the fresh/frozen beef supply chain for mul-tiple retailers and integrated processors is not onethat lends itself to the comprehensive adoption oflean supply or network sourcing. This does not meanthat there is no scope for lean ideas to be introducedin this chain because individual companies do haveopportunities internally to eradicate non-value add-ing waste and inefficiency. The findings demon-strate, however, that in this power regime leaninter-organisational supply relationships based oncollaboration are only really appropriate for the mul-tiple retailers, the integrated processors and theirpreferred agents in the chain. This is because it isonly at these points in the chain that the power struc-tures tend towards the buyer dominance and/or inter-dependence situations that support longer-termcollaborative and lean approaches.

The problem for the integrated processors and buy-ing agents is, however, that this type of collaborationmay not be as beneficial as some proponents of leansuppose. One of the major critiques of the lean ap-proach is that it may be difficult to implement oper-ationally if flow production is not possible. Theproblem of ‘carcass imbalance’ in this supply chainmilitates against continuous flow in production andthis often necessitates a batch production approach.Relatedly, there is the issue of who will benefit com-mercially from any long-term collaboration. In thissupply chain it would appear that the major benefi-ciaries of collaboration are the multiple retailers. Thisis because they have the power resources to appro-priate the maximum share of value from their ownpremium branded products and, while they maymake lower returns from commoditised products,they can still force their integrated processing part-ners to pass the majority of value that lean collabora-tion generates to them.

This leverage is, if anything, increasing against theintegrated processors as the multiple retailers devel-op their own premium brands. This leads to the con-clusion that over time, unless even more effectiveconsolidation occurs at the integrated processor stageto counter-balance the power of the multiple retail-ers, their Janus-faced Dominance will ensure that col-laboration becomes a ‘‘treadmill to oblivion’’ ofcontinuous operational and commercial improve-ment by the integrated processors in return forhigher volumes, but with only low returns.

Upstream there is some scope for collaboration be-tween the integrated processors with buying agents,who are sourcing defined quality beasts from partic-ular farmers, but this relationship does not encom-pass all buying agents (many of whom behaveopportunistically with multiple clients and suppliers

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005

THE LIMITS OF LEAN MANAGEMENT THINKING

as demand and supply fluctuates). Elsewhere up-stream the scope for continuous collaboration basedon lean is quite challenging because of the problemof ‘carcass imbalance’ associated with short-term de-mand and supply fluctuations. In these circum-stances power structures tend to oscillate betweenbuyer dominance in gluts and supplier dominance inperiods of shortage. These factors explain whyopportunism is rife in the industry upstream andtrust is so low. Rather than criticising supply chainparticipants for this behaviour our findings supportthe view that short-term, adversarial arm’s-lengthrelationship management is a perfectly rational andappropriate response to the vagaries of demandand supply upstream in this supply chain.

This means that, overall, attempts to drive lean col-laboration based on flow principles throughout thefresh/frozen beef supply chain are bound to fail be-cause the problem of ‘carcass imbalance’ cannot befully resolved. Furthermore, even if it could be, it islikely that the major beneficiaries of this would bethe multiple retailers who can use their Janus-facedDominance (dominant power and leverage position)to extract value from lean collaboration elsewherein the chain. The lessons for participants upstreamis that they must either use opportunism as best theycan by playing the market, or transform the currentpower situation to their advantage by developingand marketing their own premium brands. Failingthat, upstream members of the chain will be forcedeither to exist in their current state of uncertainty,or be forced to align themselves operationally withparticular multiple retailers, integrated processorsand buying agents and trade low commercial returnsfor guaranteed demand operationally. That is to ac-cept the role of a willing supplicant in the beef sup-ply chain.

It means that the adoption of lean managementthinking in red meat supply chains for fresh/frozenbeef in the UK may assist some industry participantsoperationally and commercially, but it does not ap-pear to be a recipe for sustainable competitive advan-tage for very many participants outside the multipleretailing stage of the chain. It will be interesting tosee if further research confirms that this is a generalrule in food and farming supply chains or unique tothe fresh/frozen beef supply chain in the UK. What-ever the outcome from future research the findingshere provide a note of caution for managers who em-bark unthinkingly on the adoption of lean manage-ment approaches that have worked in someindustries and supply chains but which may not beeasily replicable elsewhere.

Acknowledgements

(The authors wish to thank the generous support forthis research from the Engineering and Physical Sci-

European Management Journal Vol. 23, No. 6, pp. 648–662, December 20

ences Research Council under Grant No: GR/T09064/01, the Red Meat Industry Forum and TheNorth West Food Alliance. Special thanks is alsodue to Martin Palmer of the Meat and LivestockCommission for his advice and support).

References

Bourlakis, M. and Weightman, P. (2004) Food Supply ChainManagement. Blackwell, Oxford.

Brandenburger, A.M. and Nalebuff, B.J. (1996) Co-opetition.Doubleday, New York.

Cannon, J.P. and Perreault, W.D. (1999) Buyer and sellerrelationships in business markets. Journal of Marketing36, 4.

Carlisle, J.A. and Parker, R.C. (1989) Beyond Negotiation.Wiley, New York.

Christopher, M. and Towill, D.R. (2002) Developing marketspecific supply chain strategies. International Journal ofLogistics Management 13, 1.

Cooney, R. (2002) Is ‘‘Lean’’ a universal productionsystem? batch production in the automotive industry.International Journal of Operations and Production Man-agement 22, 9/10.

Cox, A. (2004a) The art of the possible: Relationshipmanagement in power regimes and supply chains.Supply Chain Management: An International Journal 9, 5.

Cox, A. (2004b) Win–Win? The Paradox of Value and Interestin Business Relationships. Earlsgate Press, Stratford-upon-Avon.

Cox, A., Lonsdale, C., Sanderson, J. and Watson, G. (2004)Business Relationships for Competitive Advantage: Man-aging Alignment and Misalignment in Buyer and SupplierTransactions. Palgrave Macmillan, Basingstoke.

Cox, A., Sanderson, J. and Watson, G. (2000) Power Regimes:Mapping the DNA of Business and Supply Chain Rela-tionships. Earlsgate Press, Stratford-upon-Avon.

Curry Commission, (2002). Farming and Food: A SustainableFuture. Cabinet Office, HMSO, London.

Emiliani, M.L. (2003) The inevitability of conflict betweenbuyers and suppliers. Supply Chain Management: AnInternational Journal 8, 2.

Fisher, M.L. (1997). What is the right supply chain for yourproduct? Harvard Business Review, March/April.

Gummesson, E. (1999) Total Relationship Marketing: Rethink-ing Marketing Management. Butterworth/Heinemann,London.

Hines, P., Lamming, R., Jones, D., Cousins, P. and Rich, N.(2000) Value Stream Management: Strategy and Excellencein the Supply Chain. Prentice Hall, London.

James-Moore, S. and Gibbons, A. (1997) Is lean manufac-ture universally relevant? An investigative methodol-ogy. International Journal of Operations and ProductionManagement 17, 9.

Lee, H.L. (2002) Aligning supply chain strategies withproduct uncertainties. California Management Review44, 3.

Lowe, J., Delbridge, R. and Oliver, N. (1997) High perfor-mance manufacturing: evidence from the automotivecomponents industry. Organization Studies 18, 5.

Macbeth, D. and Ferguson, N. (1994) Partnership Sourcing:An Integrated Supply Chain Approach. Pitman, London.

Maloni, M. and Benton, W.C. (2000) Power influences inthe supply chain. Journal of Business Logistics 21, 1.

Meat and Livestock Commission, (2005). The British RedMeat Industry, Red Meat Industry Forum, MiltonKeynes.

Naylor, M., Naim, D. and Berry, D. (1999) Leagility:Integrating the lean and agile supply chain. Interna-tional Journal of Production Economics, 62.

05 661

THE LIMITS OF LEAN MANAGEMENT THINKING

Porter, M.E. (1980) Competitive Strategy: Techniques forAnalysing Industries and Competitors. Free Press, NewYork.

Ramsey, J. (1996) The case against purchasing partnerships.International Journal of Purchasing and Materials Man-agement 32, 4.

Sako, M. (1992) Prices, Quality and Trust. CambridgeUniversity Press, Cambridge.

Simmons, D., Francis, M., Bourlakis, M. and Fearne, A.(2003) Identifying the determinants of value in the UK

ANDREW COX, Bir-mingham Business School,University of Birmingham,University House, Bir-mingham, B15 2TT. E-mail: [email protected] [email protected]

Andrew Cox is Professorand Director of the Centrefor Business Strategy andProcurement at Birming-ham Business School. He is

also Chairman of Newpoint Consulting and author ofWin-Win?: The Paradox of Value and Interests inBusiness Relationships/Earthgate Press (2004).

662 Europe

red meat industry: A value chain analysis approach.Journal of Chain and Network Science, 109–121.

Van der Vorst, J., Beulens, A., De Wit, W. and Van Beek, P.(1998) Supply chain management in food chains:Improving performance by reducing uncertainty.International Transactions in Operational Research.

Womack, J.P. and Jones, D.T. (1996) Lean Thinking: BanishWaste and Create Wealth in Your Organisation. SimonSchuster, New York.

DAN CHICKSAND,Birmingham BusinessSchool, University of Bir-mingham, UniversityHouse, Birmingham, B152TT. E-mail: [email protected]

Dan Chicksand is ResearchFellow in the Centre forBusiness Strategy andProcurement (CBSP) atBirmingham Business

School. His research interests include business strategyand supply chain management, international businessmanagement and e-commerce.

an Management Journal Vol. 23, No. 6, pp. 648–662, December 2005