Embed Size (px)

Citation preview

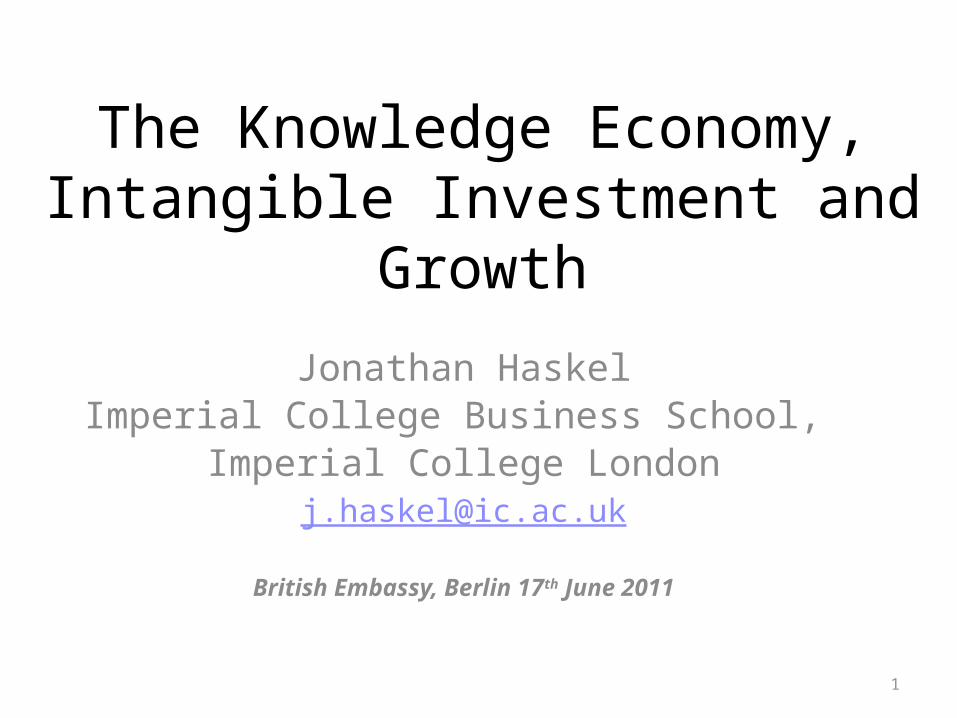

The Knowledge Economy, Intangible Investment and Growth

Jonathan HaskelImperial College Business School,

Imperial College [email protected]

British Embassy, Berlin 17th June 2011

1

Can Europe grow out of trouble? The enduring productivity deficit

19811982

19831984

19851986

19871988

19891990

19911992

19931994

19951996

19971998

19992000

20012002

20032004

20052006

20072008

20092010

201170

80

90

100

110

120

130

140

150

GDP per hour US v EU(1995=100)

level GDP per hour, EU level GDP per hour, US

2Source: EUKLEMS and The Conference Board

The R&D deficit…

3

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20080.00

0.50

1.00

1.50

2.00

2.50

Business R&D as % of GDP

UKGermanyUS

%o

of G

DP

Source: OECD STI indicators

…and now with China

4

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20080.00

0.50

1.00

1.50

2.00

2.50

Business R&D as % of GDP

ChinaUKGermanyUS

%o

of G

DP

Source: OECD STI indicators

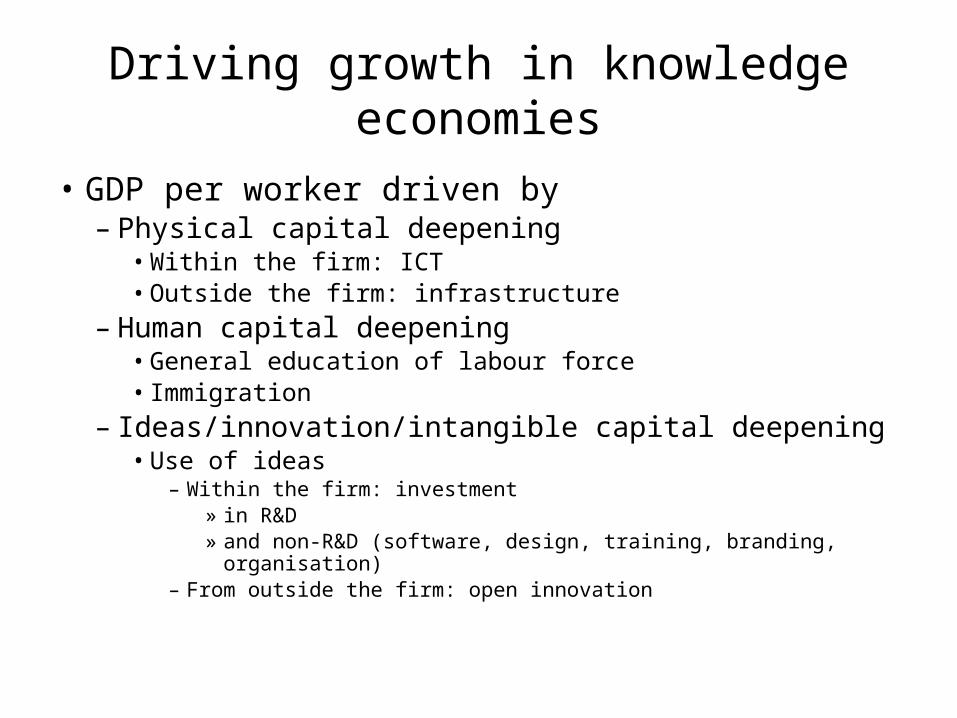

Driving growth in knowledge economies

• GDP per worker driven by – Physical capital deepening

• Within the firm: ICT • Outside the firm: infrastructure

– Human capital deepening• General education of labour force• Immigration

– Ideas/innovation/intangible capital deepening • Use of ideas

– Within the firm: investment » in R&D » and non-R&D (software, design, training, branding, organisation)

– From outside the firm: open innovation

So, why is Europe lagging?• Composition

– Larger public sector in Europe brings average down? – Too much financial services?

• Physical capital?– Lower computer adoption?

• Human capital?• Ideas/Innovation/Intangible capital?

– Low R&D. But is R&D the whole story?

6

Measuring all intangible investment

• Knowledge investment is more than just R&D– Software– Innovative property

• Scientific R&D• Design• Financial services product development• Artistic originals

– Economic competencies• Marketing• Training• Firm organisational capital

Greece

Slova

k Republic Ita

ly

Czech

RepublicJap

an

Australi

aSp

ain

Portuga

l

Sweden

Canad

a

Austria

Denmark

United St

ates

German

y

France

Finlan

d

United Kingd

om0.00

5.00

10.00

15.00

20.00

25.00

Tangible and Intangible Investment (% of 2006 market sector GDP)

Tangible Investment Intangible Investment

Intangible/tangible investment varies significantly across countries

Source: OECD/COINVEST project

How does composition of intangible investment vary?(Investment by intangible asset share in GDP, 2005 selected countries)

2.23 0.83 1.98 1.41 0.73 1.43 1.42

6.07

3.27

5.483.18 3.58

4.732.90

2.81

3.48

4.44

3.30 2.84

5.86

5.36

0

2

4

6

8

10

12

14

Japa

n

Port

ugal

Swed

en

Fran

ce

Ger

man

y US

UK

%GDP

Software and databases R&D and other intellectual property products Brand equity, firm training, organisational capital

Source: OECD/COINVEST project

Manufacturing is not manufacturing any more…

Intangible and Tangible investment as a share of VA by industry and by country, 2006

(VA adj for Intangibles)

0%5%

10%15%20%25%30%35%40%45%50%

UK Germany Sweden UK Germany Sweden UK Germany Sweden

Manufacturing Financial and business svc Retail hotel transport

Intangible Tangible

Source: COINVEST

Knowledge is the key to growth(growth accounting, 1995-06)

0.30 0.22 0.18 0.40-0.15

1.40

0.910.64 0.83

0.430.68

0.90

1.231.33

0.950.69 0.88

1.30

0.690.82

0.330.48 0.37

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Swed

en UK US

Japa

n

Fran

ce

Ger

man

y

% Labour quality Physical capital deepening Multifactor productivity Intangible capital deepening

11Source: OECD/COINVEST project

Policy?

Strict employment protection correlated with low intangible investment…

13Source: COINVEST

Aus tral ia

Aus tria

Canada

Czech Republic

Denmark

Finland

France

Germany

Greece

Italy

Japan

Netherlands

Slovak ia

Spain

Sweden

UK

US.0

2.0

4.0

6.0

8.1

.12

Inta

ngib

le in

vest

men

t as

% o

f GD

P

.5 1 1.5 2 2.5 3OECD index of employment protection strictness

Intangible investment and employment protection strictness

…as is many days to start a business.

14Source: COINVEST

Aus tral ia

Aus tria

Canada

Czech Republic

Denmark

Finland

France

Germany

Greece

Italy

Japan

Netherlands

Slovak ia

Spain

Sweden

UK

US

.02

.04

.06

.08

.1.1

2In

tang

ible

inve

stm

ent a

s %

of G

DP

0 50 100 150World Bank index of days to start a business ( 2004 )

Intangible investment and days to start a business

Government R&D can help…

15Source: COINVEST

Aus tria

Canada

Czech Republic

Denmark

Finland

France

Germany

Greece

Italy

Netherlands

Slovak ia

Spain

Sweden

UK

US.0

2.0

4.0

6.0

8.1

.12

Inta

ngib

le in

vest

men

t as

% o

f GD

P

1 2 3 4 5Goverment R & D spend as % of total government spend ( 2004 )

Intangible investment and goverment R & D spend

…and note that strictness positively correlated with tangibles. ….

16Source: COINVEST

Aus tral ia

Aus tria

Canada

Czech Republic

Denmark

FinlandFrance

Germany

Greece

Italy

JapanNetherlands

Slovak ia

SpainSweden

UK

US

.1.1

5.2

.25

.3Ta

ngib

le in

vest

men

t as

% o

f GD

P

.5 1 1.5 2 2.5 3OECD index of employment protection strictness

Tangible investment and employment protection strictness

Implications• Key importance of knowledge

– Knowledge = Intangibles and TFP = major contributors to growth – It’s not just R&D– Manufacturing is not manufacturing any more

• Policy : what not to do– Stop obsessing about manufacturing and just R&D

• Policy: what to do– All investment needs long term tax and regime certainty. Bank

regulation?– Government Science Budgets and public R&D will help– Employment regulation

• Part of overall social contract• Helps tangibles, hurts intangibles• So the choice: do we want growth from catch-up or innovation?

spares

Manufactur-ing Sweden

Manufactur-ing Germany

Manufactur-ing UK

Retail Sweden

Retail Ger-many

Retail UK Financial and business svcs

Sweden

Financial and business svcs

Germany

Financial and business svcs

UK

Intangible cap deep

1.21 0.58 0.50 0.33 0.21 0.24 0.23 0.41 0.54

Tangible cap deep

0.43 0.24 0.21 0.77 0.35 0.49 0.42 0.45 0.23

Labour quality

0.12 0.07 0.17 0.12 -0.01 0.16 0.075 -0.03 0.12

Intermedi-ate Inputs

1.65 3.10 1.70 1.42 1.16 1.22 1.19 -0.04 2.40

TFP 0.79 0.56 1.06 0.84 0.63 0.60 0.62 -1.24 0.81

-1

0

1

2

3

4

5

1.210.58 0.50 0.33 0.21 0.24 0.23 0.41 0.54

0.430.24 0.21 0.77

0.35 0.49 0.42 0.45 0.23

1.65 3.101.70 1.42

1.161.22 1.19

-0.04

2.40

0.790.56

1.06 0.84

0.630.60 0.62

-1.24

0.81

Components of Labour Productivity GrowthTFP Intermediate Inputs Labour quality Tangible cap deep Intangible cap deep

19

Manufacturing: Ge leads, but mostly intermediates. Sw intangible basedRetail: Sw leads. TFP importantFinBizServices: UK lead, intangibles important

Manufacturing Sweden

Manufacturing Germany

Manufacturing UK

Retail Sweden Retail Ger-many

Retail UK Financial and business svcs

Sweden

Financial and business svcs

UK

Intangible cap deep

29% 13% 14% 9% 9% 9% 9% 13%

Tangible cap deep

10% 5% 6% 22% 15% 18% 17% 5%

Labour quality

0.0285714285714286

0.0153846153846154

0.0467032967032969

0.0344827586206897

-0.0042735042

7350427

0.0590405904059041

0.0297029702970298

0.0293040293040293

Interme-diate In-puts

39% 68% 47% 41% 50% 45% 47% 59%

TFP 19% 12% 29% 24% 27% 22% 24% 20%

5%15%25%35%45%55%65%75%85%95%

29%13% 14% 9% 9% 9% 9% 13%

10%

5% 6% 22% 15% 18% 17% 5%

39%68%

47%41%

50%45% 47% 59%

19% 12%29% 24% 27% 22% 24% 20%

Components of Labour Productivity Growth, %TFP Intermediate Inputs Labour quality Tangible cap deep Intangible cap deep

20

1995 1996 1997 1998 1999 2000 2001 2002 2003 20040.07

0.08

0.09

0.1

0.11

0.12

0.13

0.14

0.15

0.16

Total Intangible Investment to MSVA(MSVA excluding real estate and adjusted for intangibles)

FRA_COI

GER_COI

PRT

SWE

UK_COI

FRA_CHS

GER_CHS

UK_CHS

21

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

0 10000 20000 30000 40000 50000

Inta

ngib

le In

vest

men

t (%

GD

P)

GDP per capita (PPP $)

Intangible Investment and GDP per Capita (2001-04)

SK

CZ

EL

USJPUK

AUSE

FINL

DKFR

DEAU

IT

ES

Source: Hao et al. (2009) for Germany, France, Italy and Spain; CHS (2009) for the US , Marrano et al. (2009) for the UK, Jalava et al. (2007) for Finland, Fukao et al. (2009) for Japan, Edquist (2009) for Sweden, Van Rooijen-Horsten et al. (2008) for the Netherlands and Barnes and McClure (2009) for Australia. GDP per capita is from the Total Economy Database of The Conference Board. 22

Sweden and UK are most intangible intensive….with Germany following…..

.08

.1.1

2.1

4.1

6

1995 2000 2005year

FRA GER PRT SWE UK

VA excluding real estate and adjusted for intangiblesTotal Intangible Investment to Market Sector Value Added

23

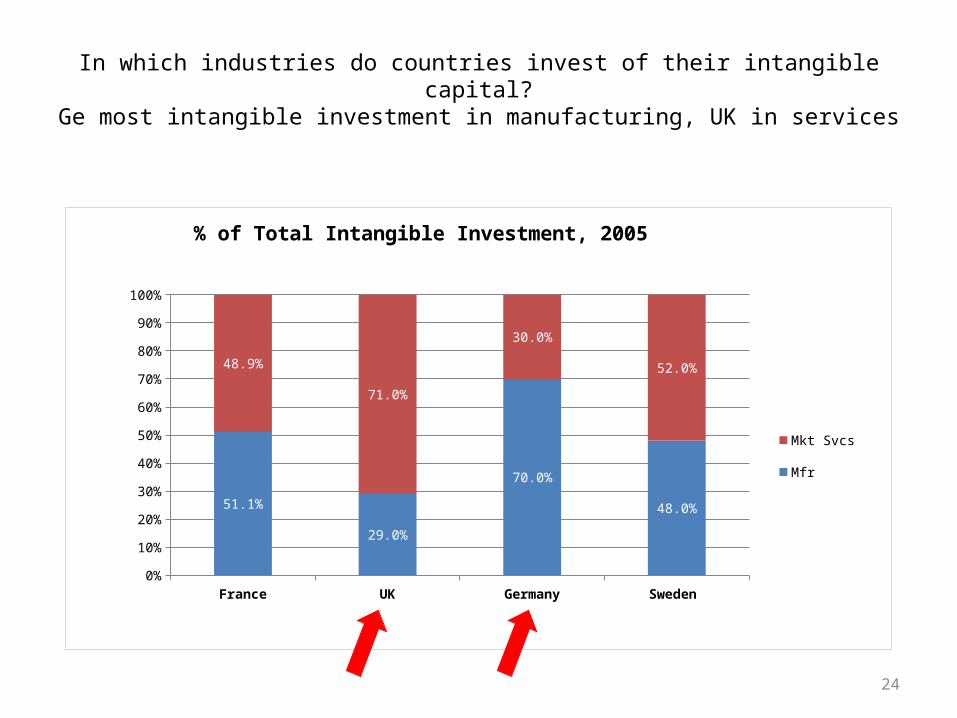

In which industries do countries invest of their intangible capital?Ge most intangible investment in manufacturing, UK in services

France UK Germany Sweden 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

51.1%

29.0%

70.0%

48.0%

48.9%

71.0%

30.0%

52.0%

% of Total Intangible Investment, 2005

Mkt Svcs Mfr

24

Intangible contributionsRetail: similar; Mfr: Sweden high; Finance: UK high

Components of Labour Productivity Growth, %

29%13% 14% 9% 9% 9% 9% 13%

10%

5% 6% 22% 15% 18% 17% 5%

39%68%

47%41%

50%45% 47% 59%

19% 12%29% 24% 27% 22% 24% 20%

-20%

0%

20%

40%

60%

80%

100%

Intangible cap deep Tangible cap deep Labour quality Intermediate Inputs TFP

TFP 19% 12% 29% 24% 27% 22% 24% 20%

Intermediate Inputs 39% 68% 47% 41% 50% 45% 47% 59%

Labour quality 3% 2% 5% 3% 0% 6% 3% 3%

Tangible cap deep 10% 5% 6% 22% 15% 18% 17% 5%

Intangible cap deep 29% 13% 14% 9% 9% 9% 9% 13%

Sweden Germany UK Sweden Germany UK Sweden UK

Manufacturing Retail Financial and business svcs

An innovation gap?

26

EU

-27

(2

)

Ge

rma

ny

Luxe

mb

ou

rg

Be

lgiu

m

Port

ug

al

Ire

lan

d

Est

on

ia

Au

stri

a

Cyp

rus

Cze

ch R

ep

ub

lic

Sw

ed

en

Ita

ly

Fin

lan

d

De

nm

ark

Slo

ven

ia

Fra

nce

Un

ite

d K

ing

do

m

Ne

the

rla

nd

s

Sp

ain

Ma

lta

Slo

vaki

a

Ro

ma

nia

Bu

lga

ria

Lith

ua

nia

Hu

ng

ary

Pola

nd

Latv

ia

No

rwa

y

Cro

ati

a

US

A

0

25

50

75

100

% of enterprises reporting process or product innovation 2006-8

% o

f e

nte

rpri

ses

![BOURBON/RYE $6 [24,600] THE LOUNGE MENU · East Imperial Soda Water / East Imperial Burma Tonic Water / East Imperial Grapefruit Tonic / East Imperial Yuzu Tonic / East Imperial Thai](https://img.pdfslide.us/doc/110x75/5e6ccd6cbdaeea1277122949/bourbonrye-6-24600-the-lounge-menu-east-imperial-soda-water-east-imperial.jpg)