Embed Size (px)

Citation preview

The interplay btw. sovereign and banking risks: is EBU a right answer?

Angelo Baglioni

Bologna – 26 October 2017

Contents

• Three reasons for the European Banking Union

• Single Supervisory Mechanism (SSM) • Single Resolution Mechanism (SRM) • European Deposit Insurance System (EDIS)

(missing)

Baglioni - European Banking Union 2

Three reasons for the European Banking Union

• Reduce the fiscal cost of bank bailouts • Break-up the two-way link between sovereign

and bank risks at national level • Achieve a higher level of supervisory

convergence

Baglioni - European Banking Union 3

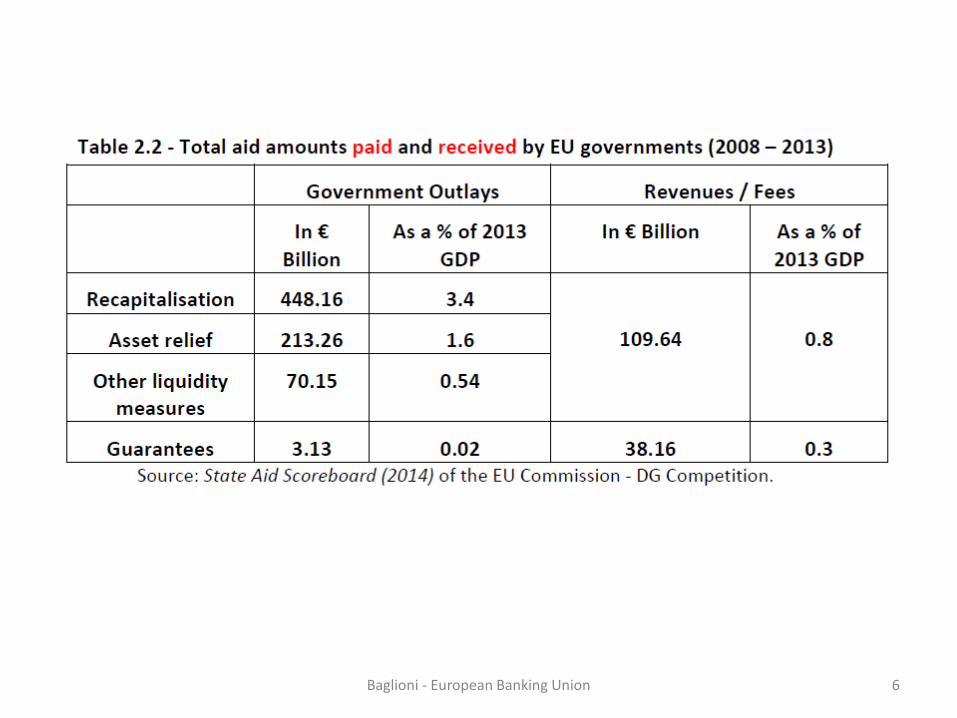

Reduce the fiscal cost of bank bailouts

• Fiscal cost of banking crisis: – direct support measures: recapitalization,

impaired assets relief, guarantee – indirect negative impact on primary balance

through business cycle and automatic stabilizers, and possibly on interest outlays

Baglioni - European Banking Union 4

Baglioni - European Banking Union 5

Baglioni - European Banking Union 6

Break the two-way link between sovereign and bank risks

• Risk goes from banks to governments: support

measures and implicit bail-out guarantee

• Risk goes from governments to banks: home bias in banks’ government bond portfolio

Baglioni - European Banking Union 7

Baglioni - European Banking Union 8

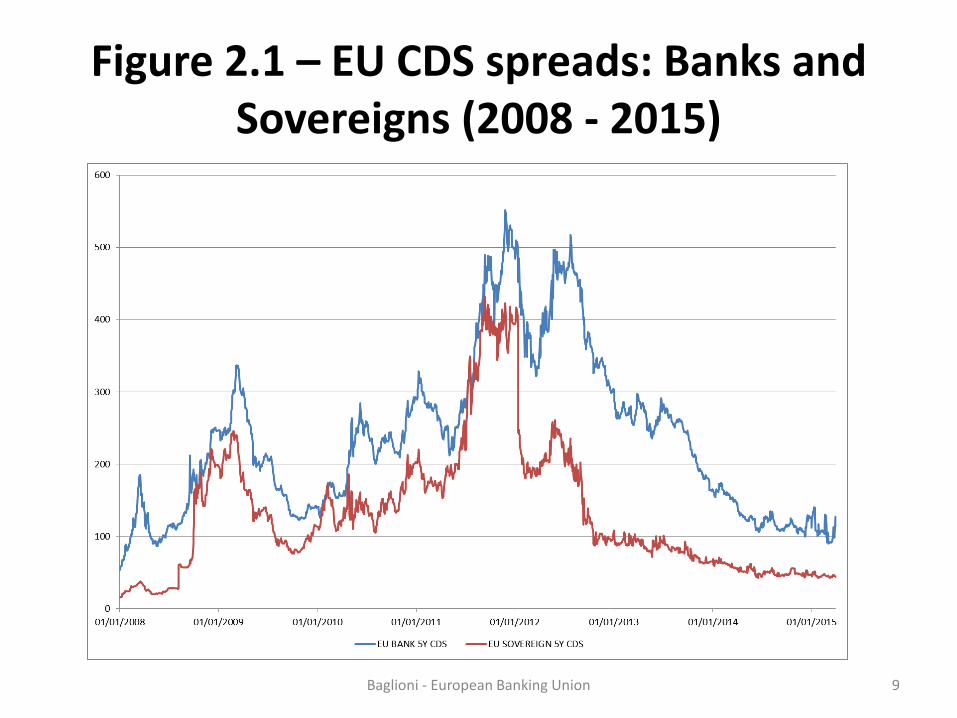

Figure 2.1 – EU CDS spreads: Banks and Sovereigns (2008 - 2015)

Baglioni - European Banking Union 9

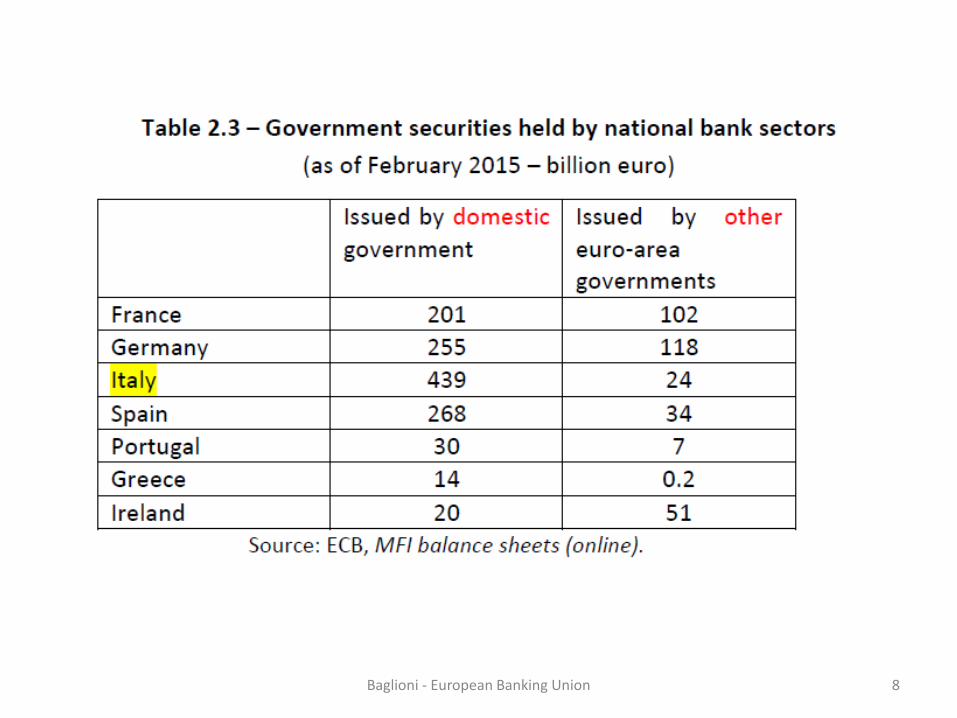

Two way link?

• Cross-country differences in risk transmission • Italy: from government to banks

• Ireland (and Germany): from banks to

government

• Spain and Greece: both ways Baglioni - European Banking Union 10

Achieve a higher and uniform level of supervision

• EU: common rules (Basel III) but implemented at national level – National discretion in implementation (e.g. validation

of internal models) – Cross-country divergences (e.g. definition of non-

performing loans)

• Competitive distortions • Possibility of loose supervision in some countries • Improvisation in crisis management (ex. Cyprus)

Baglioni - European Banking Union 11

SSM: organization • Separation between supervision and

monetary policy • Significant banks: direct supervision by ECB

– cooperation between ECB and NCAs (JST) • Less significant banks: supervised by NCAs

– under guidelines by ECB, which can take-up direct supervision

• Supervisory Review and Examination Process • Macro-prudential supervision: left to NCAs (?)

Baglioni - European Banking Union 12

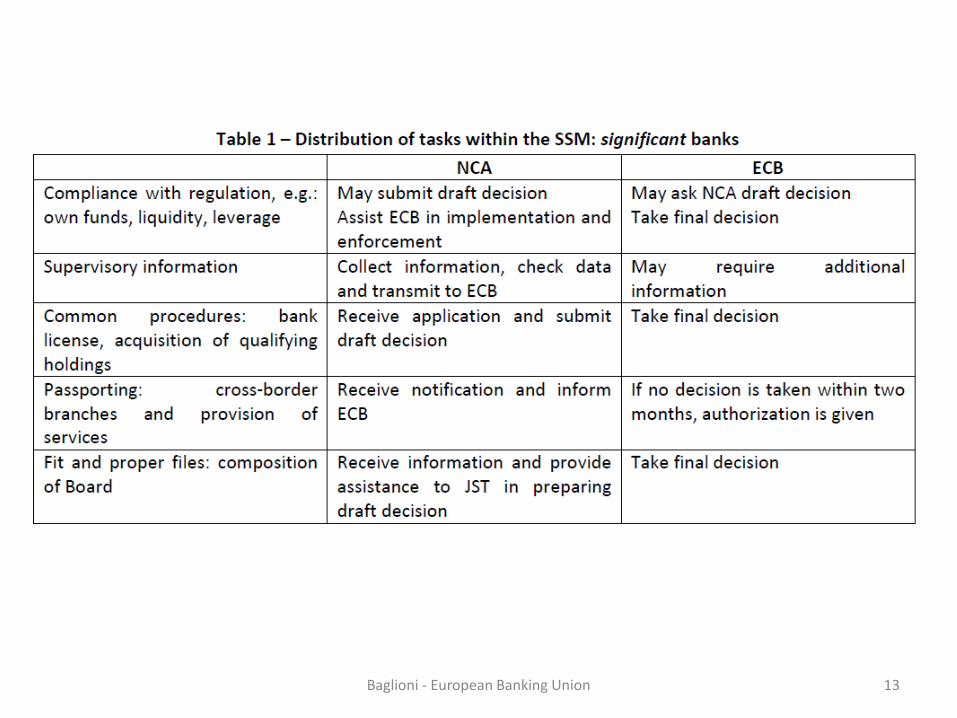

Baglioni - European Banking Union 13

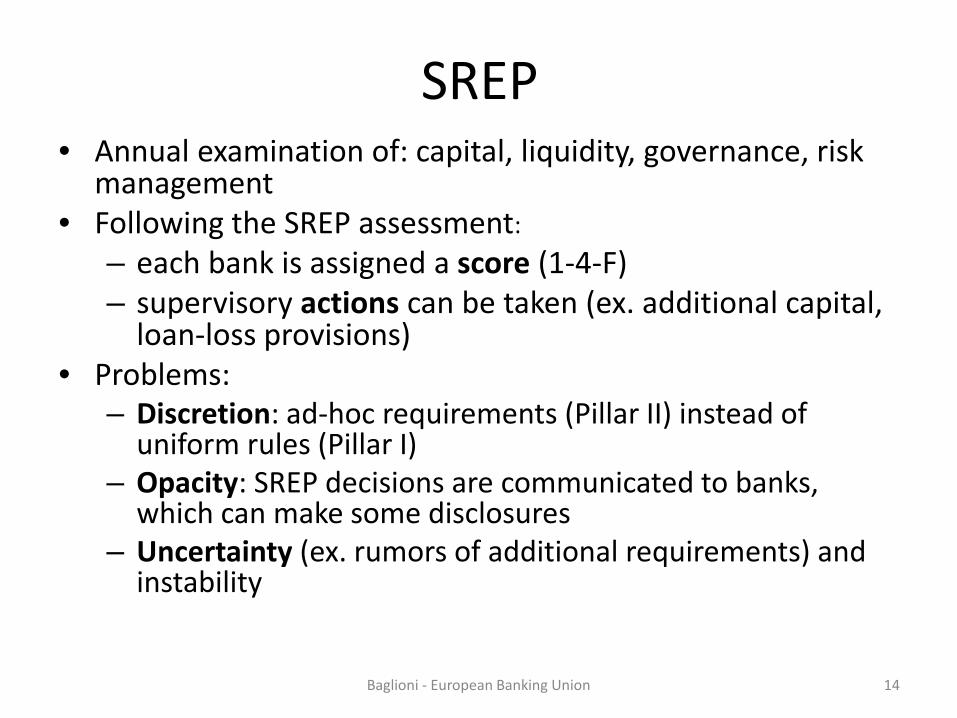

SREP • Annual examination of: capital, liquidity, governance, risk

management • Following the SREP assessment:

– each bank is assigned a score (1-4-F) – supervisory actions can be taken (ex. additional capital,

loan-loss provisions) • Problems:

– Discretion: ad-hoc requirements (Pillar II) instead of uniform rules (Pillar I)

– Opacity: SREP decisions are communicated to banks, which can make some disclosures

– Uncertainty (ex. rumors of additional requirements) and instability

Baglioni - European Banking Union 14

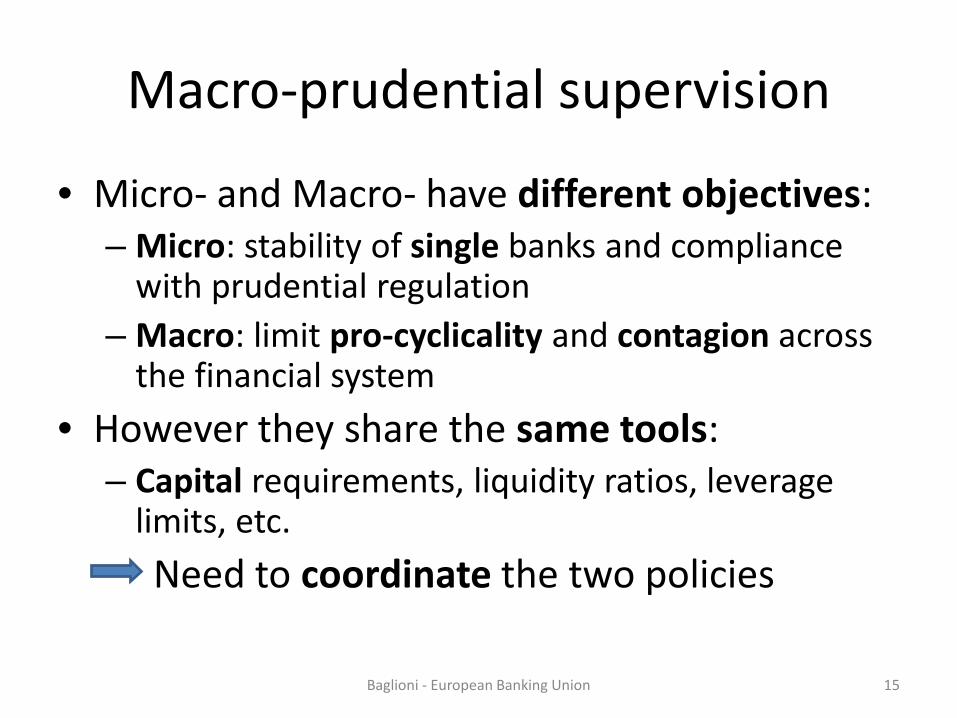

Macro-prudential supervision

• Micro- and Macro- have different objectives: – Micro: stability of single banks and compliance

with prudential regulation – Macro: limit pro-cyclicality and contagion across

the financial system • However they share the same tools:

– Capital requirements, liquidity ratios, leverage limits, etc.

Need to coordinate the two policies

Baglioni - European Banking Union 15

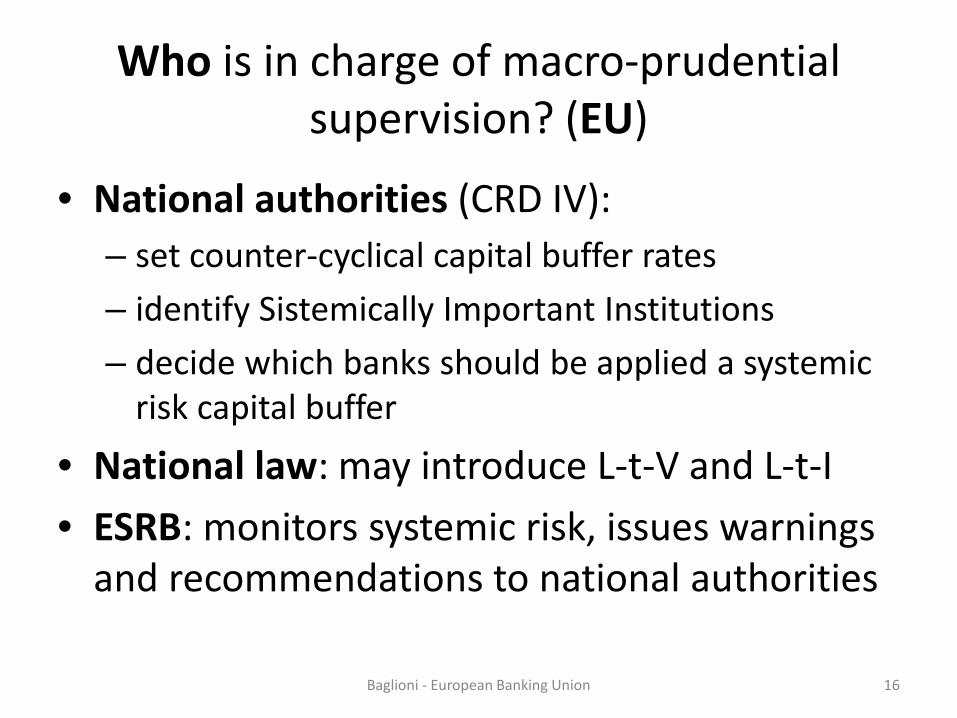

Who is in charge of macro-prudential supervision? (EU)

• National authorities (CRD IV): – set counter-cyclical capital buffer rates – identify Sistemically Important Institutions – decide which banks should be applied a systemic

risk capital buffer

• National law: may introduce L-t-V and L-t-I • ESRB: monitors systemic risk, issues warnings

and recommendations to national authorities Baglioni - European Banking Union 16

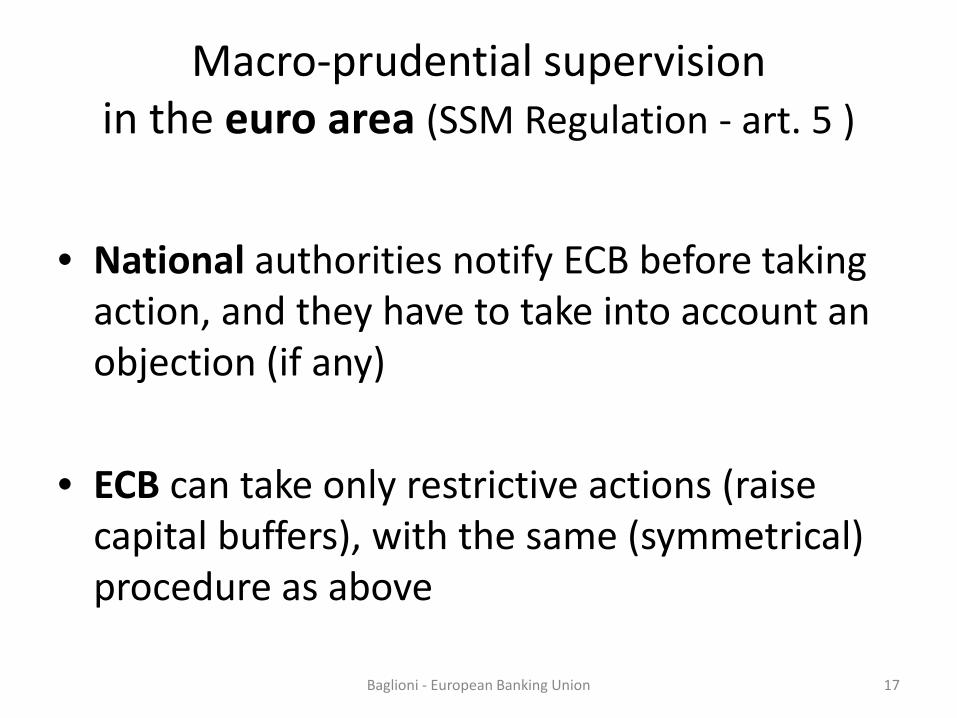

Macro-prudential supervision in the euro area (SSM Regulation - art. 5 )

• National authorities notify ECB before taking

action, and they have to take into account an objection (if any)

• ECB can take only restrictive actions (raise capital buffers), with the same (symmetrical) procedure as above

Baglioni - European Banking Union 17

Critical issues:

• Externalities: systemic risk has a strong cross-country dimension, that national authorities might understate

• Heterogeneity: lack of cross-country coordination may introduce segmentation, jeopardizing the levelling-the-playing-field target of EU regulation

• Coordination between national authorities and ECB • Conflicts bwt. policies: micro vs. macro, prudential

vs. monetary policies

Baglioni - European Banking Union 18

Policy implications:

• Need for a simplification and centralization (at the supra-national level) of macro-prudential supervision

• In the euro-area, the ECB (within SSM) should be given full responsibility for macro-prudential policy

Baglioni - European Banking Union 19

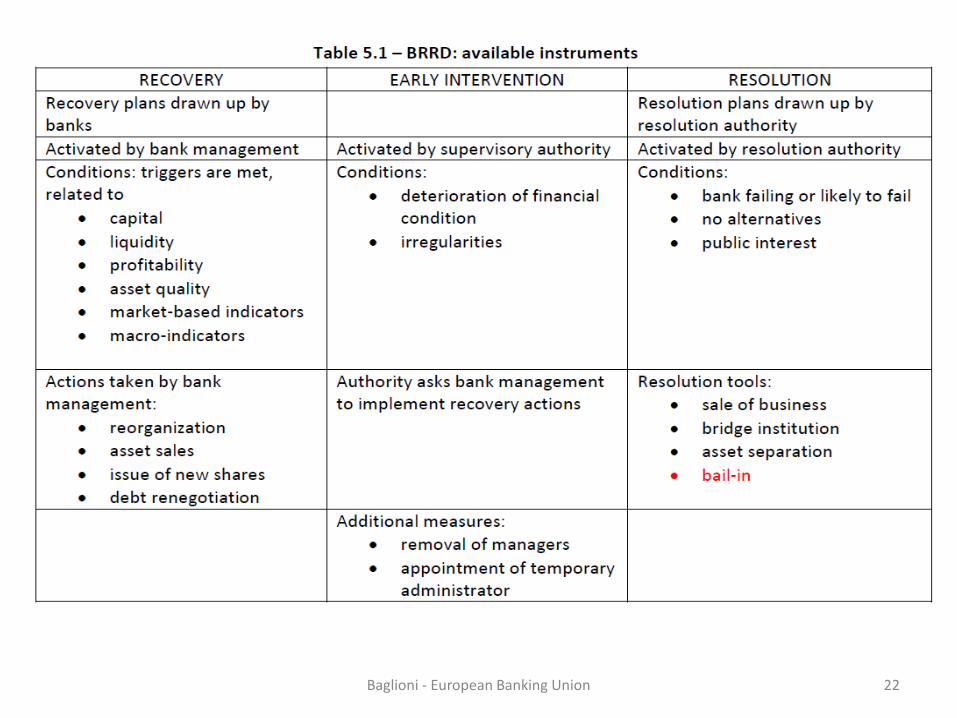

Resolution and bail-in • Two building blocks:

– Bank Recovery and Resolution Directive (BRRD) introduces in all EU countries some new legal tools to manage bank crises; effective as of 1/1/2015 (bail-in: 1/1/2016)

– Single Resolution Mechanism introduces in euro-area some new institutions, applying the BRRD:

• Single Resolution Board (SRB) – National Resolution Authorities (NRA)

• Single Resolution Fund (SRF) – National resolution funds (transitory)

Baglioni - European Banking Union 20

BRRD: motivation • Bank liquidations have disruptive effects on

financial/economic system, creating contagion (trough interbank transactions and reputation); see Lehman Brothers

• Bank bail-outs imply costs for taxpayers and moral hazard (“I take profits, you take losses”)

• Need to introduce a third way to manage bank crises: let a bank survive, but make some stakeholders bear losses (imposed by resolution authority), minimizing state aid

Baglioni - European Banking Union 21

Baglioni - European Banking Union 22

Resolution objectives

• Ensure continuity of critical bank functions • Avoid contagion • Minimize resort to public funds • Protect small depositors

Baglioni - European Banking Union 23

Resolution conditions (all to be met)

• Bank is failing or likely to fail: – assets less then liabilities, unable to repay obligations,

losses have depleted own funds, bank has received public support (except as a follow-up of AQR – stress test)

• Last resort procedure: no alternative private sector solution or supervisory action is able to avoid liquidation

• Public interest: resolution necessary to reach objectives (better than insolvency procedures)

Baglioni - European Banking Union 24

Resolution tools

• Sale of business: some assets/liabilities are transferred to another existing bank

• Bridge institution (good bank): profitable lines of business are transferred to a new (temporary) solvent bank controlled by the resolution authority

• Asset separation (bad bank): loss-generating lines of business are transferred to a vehicle, with the purpose of orderly liquidation

Baglioni - European Banking Union 25

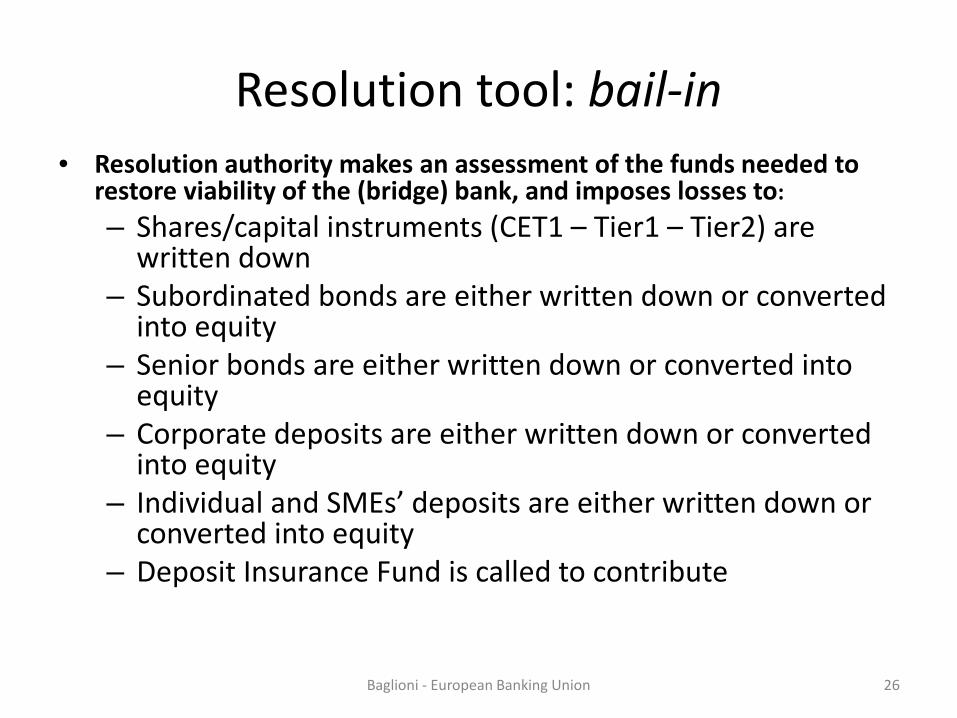

Resolution tool: bail-in • Resolution authority makes an assessment of the funds needed to

restore viability of the (bridge) bank, and imposes losses to: – Shares/capital instruments (CET1 – Tier1 – Tier2) are

written down – Subordinated bonds are either written down or converted

into equity – Senior bonds are either written down or converted into

equity – Corporate deposits are either written down or converted

into equity – Individual and SMEs’ deposits are either written down or

converted into equity – Deposit Insurance Fund is called to contribute

Baglioni - European Banking Union 26

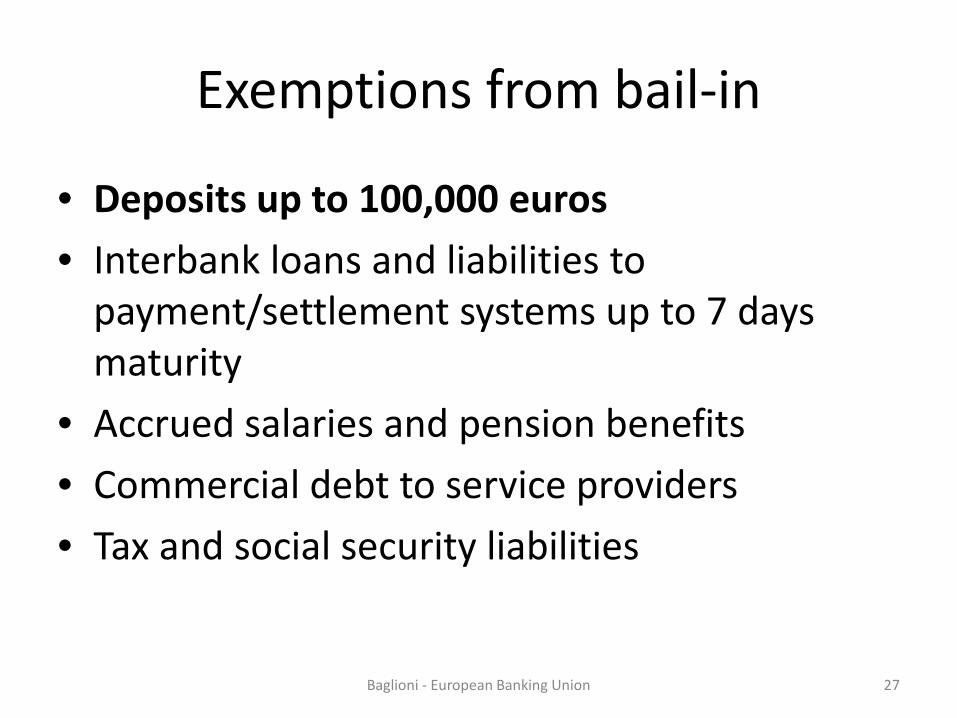

Exemptions from bail-in

• Deposits up to 100,000 euros • Interbank loans and liabilities to

payment/settlement systems up to 7 days maturity

• Accrued salaries and pension benefits • Commercial debt to service providers • Tax and social security liabilities

Baglioni - European Banking Union 27

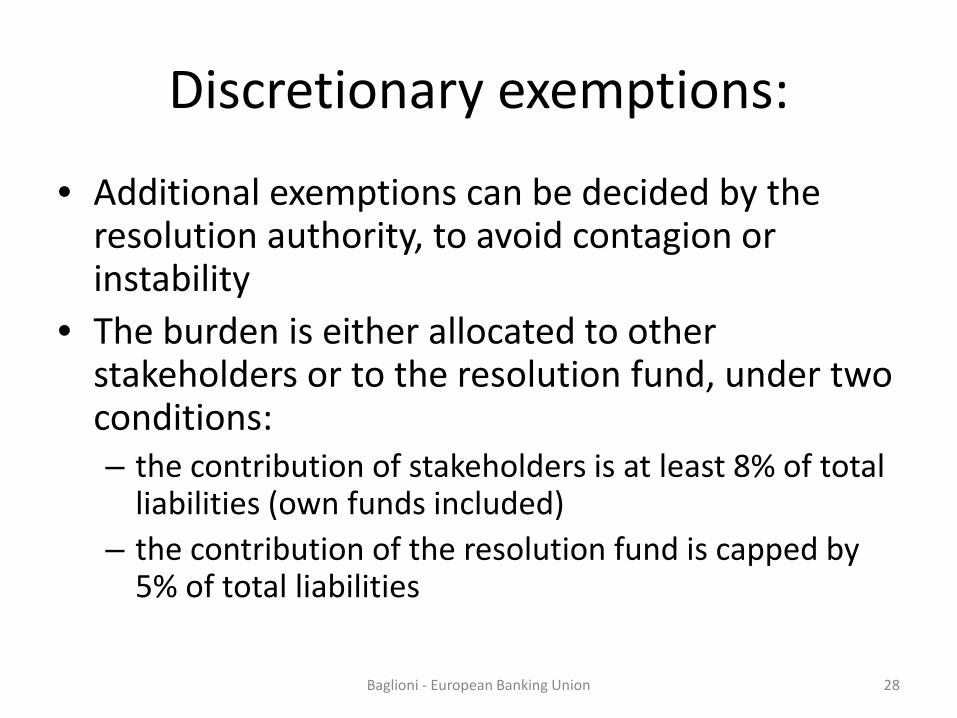

Discretionary exemptions:

• Additional exemptions can be decided by the resolution authority, to avoid contagion or instability

• The burden is either allocated to other stakeholders or to the resolution fund, under two conditions: – the contribution of stakeholders is at least 8% of total

liabilities (own funds included) – the contribution of the resolution fund is capped by

5% of total liabilities

Baglioni - European Banking Union 28

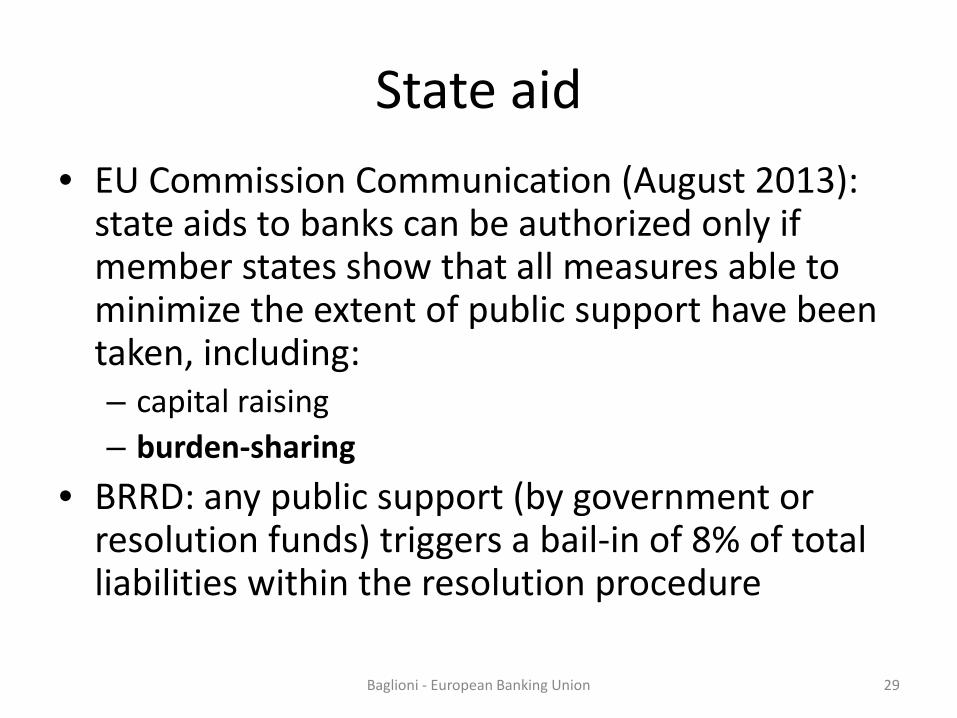

State aid • EU Commission Communication (August 2013):

state aids to banks can be authorized only if member states show that all measures able to minimize the extent of public support have been taken, including: – capital raising – burden-sharing

• BRRD: any public support (by government or resolution funds) triggers a bail-in of 8% of total liabilities within the resolution procedure

Baglioni - European Banking Union 29

Exception: financial stability

• Public support (guarantee, capital injection) does not trigger resolution if it is needed to preserve the financial stability of a country (art. 32.4 BRRD), within the State aid framework

• State aid framework: burden-sharing can be waived if it would endanger financial stability or lead to disproportionate results (art. 45 EU Commission Communication)

Baglioni - European Banking Union 30

Problems with bail-in

• Retail customers should be exempted, since they lack information to assess bank risk. Their inclusion creates – social issues – transparency / communication problems – instability

• Bail-in should apply only to new contracts, not to outstanding instruments

Baglioni - European Banking Union 31

A possible solution • BRRD introduces MREL: resolution authorities

have to set a minimum level for MREL = (own funds + eligible liabilities) /

(own funds + total liabilities) • Proposed requirement:

(own funds + junior and senior un-preferred bonds) / (own funds + total liabilities) ≥ 8%

• Junior bonds (hit by bail-in and burden-sharing) and Senior un-preferred bonds (hit by bail-in, not by burden-sharing) should be sold to institutional investors only

Baglioni - European Banking Union 32

SRM organization

• SRB: responsible for resolution of significant and cross-border groups, and for using the SRF

• NRA: responsible for resolution of other banks (not using SRF) – Both apply rules introduced by BRRD

• ECB decides if a bank is “failing or likely to fail” (triggering resolution)

• A resolution scheme adopted by the SRB can be objected by the EU Commission and Council

Baglioni - European Banking Union 33

Governance issues

• Governance of SRM is too complex and prone to political interference

• EU Council involvement should be limited to general rules and overall amount of available resources, not to single resolution decisions

• EU Commission involvement should be limited to the application of State aid rules

Baglioni - European Banking Union 34

SRF

• It can provide resources within a resolution procedure

• Target size: 1% of covered deposits (55 billion), by 1.1.2024

• Funded by contributions from banks: – ex ante (flat and risk-adjusted) – possible ex post additional contributions – national compartments gradually merged during

transitional period (2016 - 2023)

Baglioni - European Banking Union 35

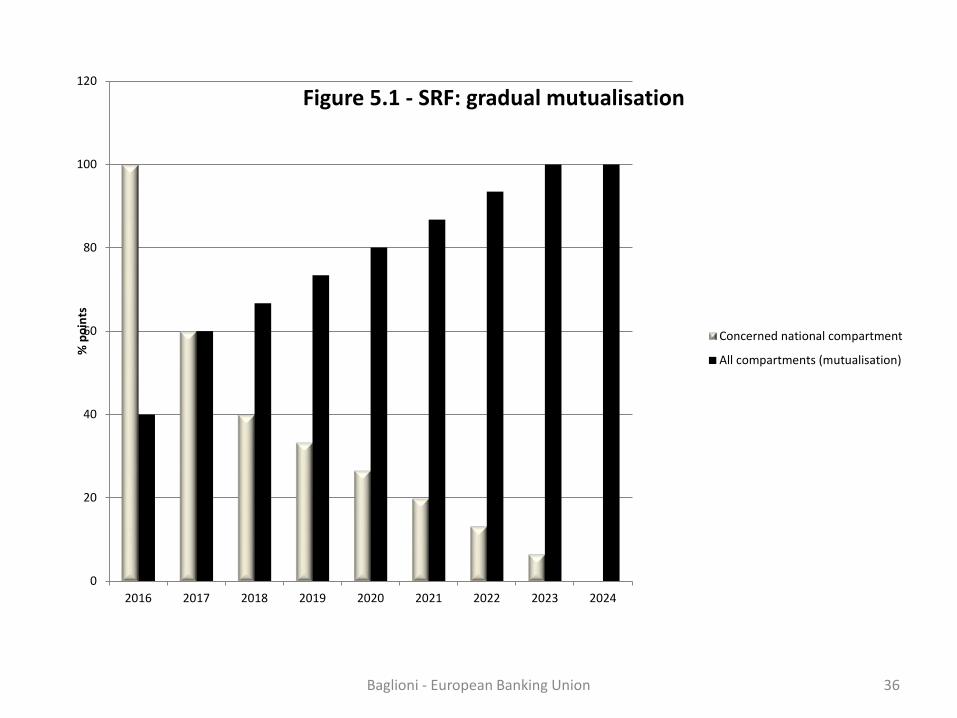

Baglioni - European Banking Union 36

0

20

40

60

80

100

120

2016 2017 2018 2019 2020 2021 2022 2023 2024

% p

oint

s Figure 5.1 - SRF: gradual mutualisation

Concerned national compartment

All compartments (mutualisation)

Problems with SRF

• Limited size (8-year transition period) – somewhat balanced by possibility of raising ex-

post contributions and borrowing from banks and governments

• Need to introduce a common fiscal backstop: SRF should be enabled to borrow from ESM

• SRF interventions should not qualify as State aid: they should not trigger bail-in (?)

Baglioni - European Banking Union 37

ESM - DRI • Direct Refinancing Instrument: introduced in 2013 as an

additional tool of ESM (never used so far) • ESM is endowed with 60 billions, that can be used to

provide capital injections into troubled banks • Problems:

– Reserved to systemic banks, under the condition that the member State is unable to provide support and private resources are unavailable (last resort tool)

– Precondition: 8% bail-in – Member State has to contribute (burden-sharing) – Political decision-making: decisions taken by Finance Ministers

(ESM Board), MoU imposes conditions on overall economic policy of member State

Baglioni - European Banking Union 38

The missing pillar: EDIS

• 2014 Directive: only harmonization of national DIS, supervised at national level – Coverage: confirmed at 100,000 euros (interbank

excluded) – Funding:

• ex-ante risk-based contributions (target level: 0.8% of covered deposits in 2024) (cash + commitments)

• ex-post extraordinary contributions (capped at 0.5% of covered deposits yearly)

• loans from governments

Baglioni - European Banking Union 39

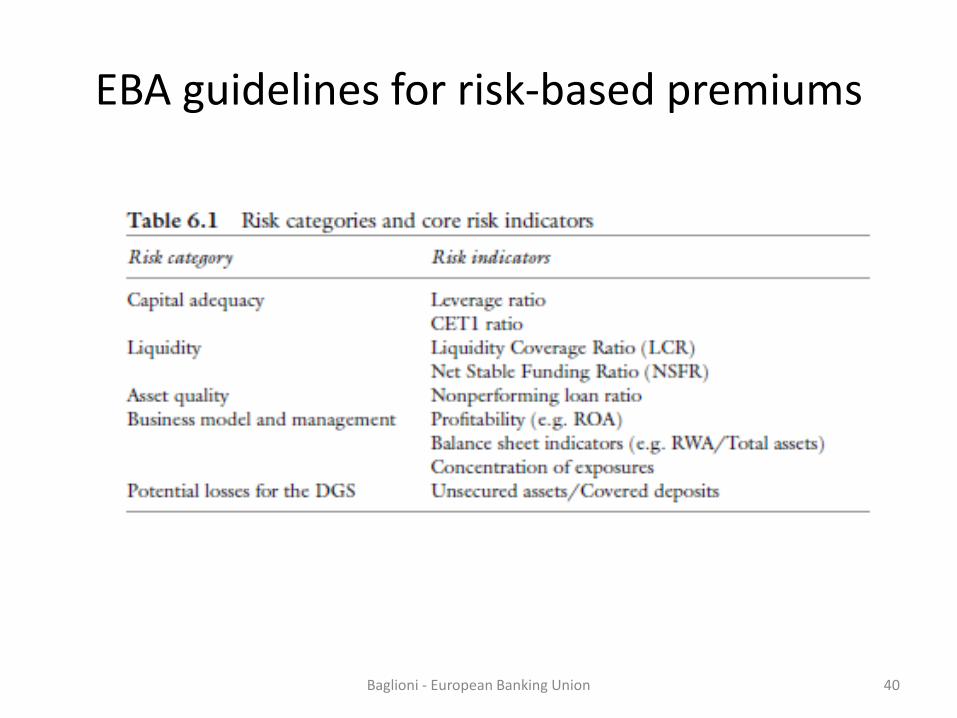

EBA guidelines for risk-based premiums

Baglioni - European Banking Union 40

…2014 Directive

• Scope of intervention: • Repayment of depositors • Contribution in resolution (bail-in) • Early intervention: financial assistance outside resolution

• Payout time: 7 days (in 2024) • Transparency: banks should provide information to

customers

Baglioni - European Banking Union 41

The way forward • Need to introduce an EDIS, in order to:

– make deposit insurance stronger, by pooling resources across member States

– reduce likelihood of public support • How? By expanding the scope of SRF – SRB,

rather than introducing a new institution – The role of DIS is contribute to resolution, rather

than repay depositors of liquidated banks – Avoid duplication of administrative bodies (see FDIC) – BRRD allows the same institution to administer both

resolution fund and DIS

Baglioni - European Banking Union 42

EU Commission proposal (November 2015)

• Up to July 2020: European re-insurance system, providing financial assistance to national insurance schemes

• 2020 – 2024: co-insurance. EDIS contribution in direct repayment of depositors , together with national schemes, increases through time

• 2024: EDIS fully in place, replacing national schemes

• EDIS managed by SRB

Baglioni - European Banking Union 43

EU Commission proposal (October 2017)

• Re-insurance: EDIS loans to national DIS • Co-insurance: conditional on AQR positive

outcome (by 2022)

• Full EDIS replacing national DIS: never!

Baglioni - European Banking Union 44

Has the Banking Union achieved its goals? • Reduce the fiscal cost of bank bailouts:

– Yes (direct link through bail-outs reduced), but at the cost of increasing instability due to application of bail-in

• Break-up the two-way link between sovereign and bank risks at national level: No – Bail-in makes the cost of bank crises be paid by local

stakeholders, with negative impact on national economies and public budgets (indirect link)

– Lack of common fiscal backstop for SRF (and EDIS) makes national governments implicitly be the last resort

– Home bias in bank securities portfolio is still strong

Baglioni - European Banking Union 45

Baglioni - European Banking Union