Embed Size (px)

Citation preview

The International

CapitalMarkets Review

Law Business Research

Second Edition

Editor

Jeffrey Golden

The International Capital Markets Review

second edition

Reproduced with permission from Law Business Research Ltd.

This article was first published in The international capital Markets Review, 2nd edition(published in november 2012 – editor Jeffrey Golden).

For further information please [email protected]

The International

Capital Markets Review

second edition

editorJeffrey Golden

Law Business Research Ltd

The Law ReviewsThe Mergers and acquisiTions review

The resTrucTuring review

The PrivaTe coMPeTiTion enforceMenT review

The disPuTe resoluTion review

The eMPloyMenT law review

The Public coMPeTiTion enforceMenT review

The banking regulaTion review

The inTernaTional arbiTraTion review

The Merger conTrol review

The Technology, Media and TelecoMMunicaTions review

The inward invesTMenT and inTernaTional TaxaTion review

The corPoraTe governance review

The corPoraTe iMMigraTion review

The inTernaTional invesTigaTions review

The ProjecTs and consTrucTion review

The inTernaTional caPiTal MarkeTs review

The real esTaTe law review

The PrivaTe equiTy review

The energy regulaTion and MarkeTs review

The inTellecTual ProPerTy review

The asseT ManageMenT review

The PrivaTe wealTh and PrivaTe clienT review

The Mining law review

www.Thelawreviews.co.uk

Publisher gideon roberton

business develoPMenT Managers adam sargent, nick barette

MarkeTing Managers katherine jablonowska, alexandra wan

Publishing assisTanT lucy brewer

ediTorial assisTanT lydia gerges

ProducTion Manager adam Myers

ProducTion ediTors anne borthwick, joanne Morley

subediTor charlotte stretch

ediTor-in-chief callum campbell

Managing direcTor richard davey

Published in the united kingdom by law business research ltd, london

87 lancaster road, london, w11 1qq, uk© 2012 law business research ltd

© copyright in individual chapters vests with the contributors no photocopying: copyright licences do not apply.

The information provided in this publication is general and may not apply in a specific situation. legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts

or omissions contained herein. although the information provided is accurate as of november 2012, be advised that this is a developing area.

enquiries concerning reproduction should be sent to law business research, at the address above. enquiries concerning editorial content should be directed

to the Publisher – [email protected]

isbn 978-1-907606-48-9

Printed in great britain by encompass Print solutions, derbyshire

Tel: +44 870 897 3239

i

The publisher acknowledges and thanks the following law firms for their learned assistance throughout the preparation of this book:

ALLen & oveRy, A PĘdZich sPk

ALLen & oveRy LLP

ALLen & oveRy LuxeMBouRG

BBh, Advokátní kAnceLáŘ, v.o.s.

cLeARy GottLieB steen & hAMiLton LLP

de PARdieu BRocAs MAFFei

ens (edwARd nAthAn sonnenBeRGs)

Fenxun PARtneRs

FReshFieLds BRuckhAus deRinGeR LLP

GAikokuho kyodo-JiGyo hoRitsu JiMusho LinkLAteRs

GARRiGues

JuRis coRP

kiM & chAnG

kinG & wood MALLesons

MAPLes And cALdeR

AcknowLedGeMents

ii

Acknowledgements

MonAstyRsky, ZyuBA, stePAnov & PARtneRs

PAksoy

PLesneR

RusseLL McveAGh

sidLey Austin LLP

uLhôA cAnto, ReZende e GueRRA AdvoGAdos

wenGeR & vieLi AG

iii

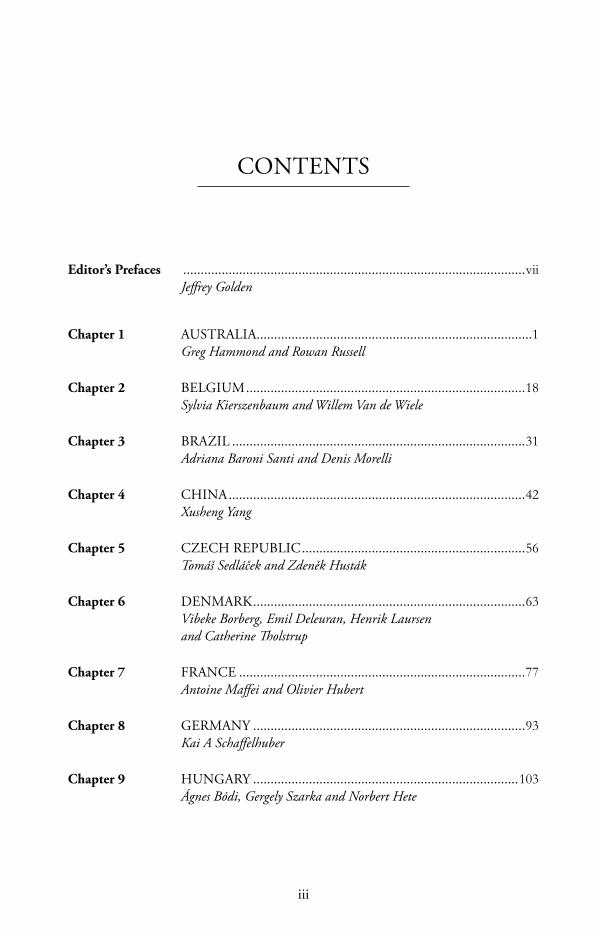

Editor’s Prefaces ..................................................................................................viiJeffrey Golden

Chapter 1 AustRALiA ...............................................................................1Greg Hammond and Rowan Russell

Chapter 2 BeLGiuM ................................................................................18Sylvia Kierszenbaum and Willem Van de Wiele

Chapter 3 BRAZiL ....................................................................................31Adriana Baroni Santi and Denis Morelli

Chapter 4 chinA .....................................................................................42Xusheng Yang

Chapter 5 cZech RePuBLic ................................................................56Tomáš Sedláček and Zdeněk Husták

Chapter 6 denMARk ..............................................................................63Vibeke Borberg, Emil Deleuran, Henrik Laursen and Catherine Tholstrup

Chapter 7 FRAnce ..................................................................................77Antoine Maffei and Olivier Hubert

Chapter 8 GeRMAny ..............................................................................93Kai A Schaffelhuber

Chapter 9 hunGARy ............................................................................103Ágnes Bódi, Gergely Szarka and Norbert Hete

contents

iv

Contents

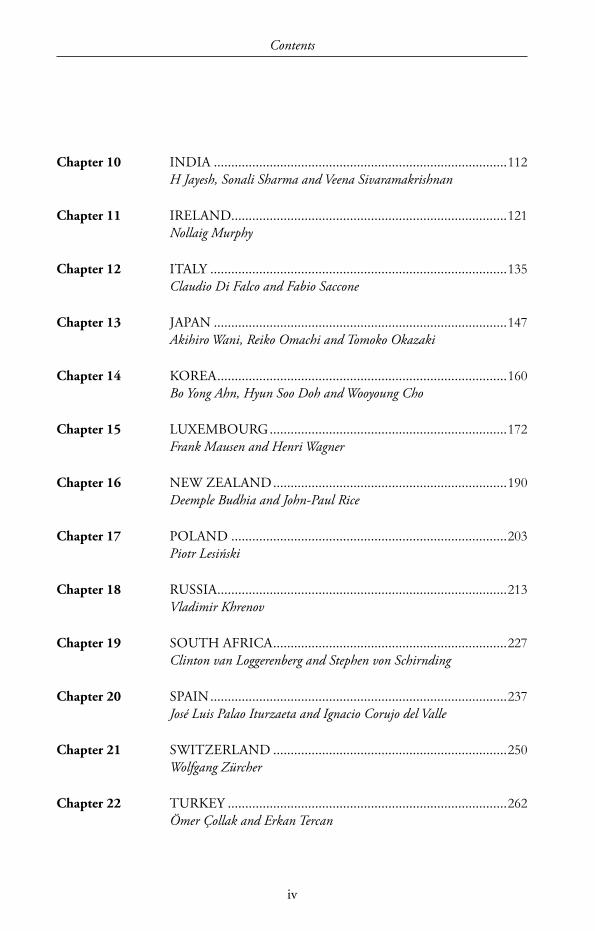

Chapter 10 indiA ....................................................................................112H Jayesh, Sonali Sharma and Veena Sivaramakrishnan

Chapter 11 iReLAnd...............................................................................121Nollaig Murphy

Chapter 12 itALy .....................................................................................135Claudio Di Falco and Fabio Saccone

Chapter 13 JAPAn ....................................................................................147Akihiro Wani, Reiko Omachi and Tomoko Okazaki

Chapter 14 koReA ...................................................................................160Bo Yong Ahn, Hyun Soo Doh and Wooyoung Cho

Chapter 15 LuxeMBouRG ....................................................................172Frank Mausen and Henri Wagner

Chapter 16 new ZeALAnd ...................................................................190Deemple Budhia and John-Paul Rice

Chapter 17 PoLAnd ...............................................................................203Piotr Lesiński

Chapter 18 RussiA ...................................................................................213Vladimir Khrenov

Chapter 19 south AFRicA ...................................................................227Clinton van Loggerenberg and Stephen von Schirnding

Chapter 20 sPAin .....................................................................................237José Luis Palao Iturzaeta and Ignacio Corujo del Valle

Chapter 21 switZeRLAnd ...................................................................250Wolfgang Zürcher

Chapter 22 tuRkey ................................................................................262Ömer Çollak and Erkan Tercan

v

Contents

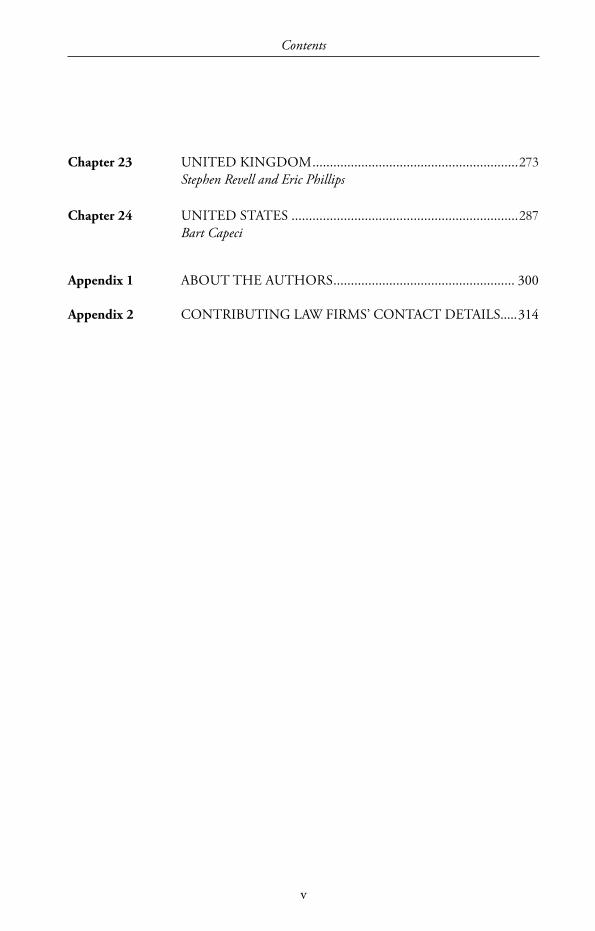

Chapter 23 united kinGdoM ...........................................................273Stephen Revell and Eric Phillips

Chapter 24 united stAtes .................................................................287Bart Capeci

Appendix 1 ABout the AuthoRs .................................................... 300

Appendix 2 contRiButinG LAw FiRMs’ contAct detAiLs.....314

vii

Editor’s PrEfacE totHE sEcoNd EditioN

it was my thought that we should also include in this second edition of The International Capital Markets Review my preface to the first edition. Written less than a year ago, it captures relevant background and sets out the rationale for this volume in the series. The contemporary importance of the global capital marketplace (and indeed you must again admire its resilience), the staggering volume of trading and the complexity of the products offered in it, and the increased scrutiny being given to such activity by the courts all continue. and, of course, so does the role of the individual – the difference that an informed practitioner can make in the mix, and the risk that follows from not staying up to date.

However, i was delighted, following the interest generated by our first edition, by the publisher’s decision to bring out a second edition so quickly and to expand it. There were several reasons for this. The picture on the regulatory front is much clearer for practitioners than it was a year ago – but no less daunting. according to one recent commentary, in the United states alone, rule-making under the dodd-frank report has seen 848 pages of statutory text (which we had before us when the first edition appeared) expand to 8,843 pages of regulation, with only 30 per cent of the required regulation thus far achieved. incomplete though the picture may look, the timing seems right to take a gulp of what we have got rather than wait for what may be a very long time and perhaps then only to choke on what may be more than any one person can swallow in one go! regulatory debate and reform in Europe and affecting other key financial centers has been similarly dramatic. Moreover, these are no longer matters of interest to local law practitioners only. indeed, the extraterritorial reach of the new financial rules in the United states has risen to a global level of attention and has been the stuff of newspaper headlines at the time of writing.

There are also signs that any ‘big freeze’ on post-crisis capital markets transactional work may be thawing. in the debt markets, the search for yield continues. Equities are seen as a potential form of protection in the face of growing concerns about inflation. Participants are coming off the sidelines. Parties can be found to be taking risks. They are not oblivious to risk. They are taking risks grudgingly. But they are taking them. and derivatives (also covered in this volume) are seen as a relevant tool for managing that risk.

viii

Editor’s Preface to the Second Edition

Most importantly, it is a big world, and international capital markets work hugs a bigger chunk of it than do most practice areas. By expanding our coverage in this second edition to include six new jurisdictions, we also, by virtue of three of them, complete our coverage of the important Bric countries with the addition of reporting from Brazil, russia and china. Three other important pieces to the international capital markets puzzle – Belgium, the czech republic and New Zealand – also fall into place.

The picture now on offer in these pages is therefore more complete. None of the 24 jurisdictions now surveyed has a monopoly on market innovation, the risks associated with it or the attempts to regulate it. in light of this, international practitioners benefit from this access to a comparative view of relevant law and practice. Providing that benefit – offering sophisticated business-focused analysis of key legal issues in the most significant jurisdictions – remains the inspiration for this volume.

as part of the wider regulatory debate, there have been calls to curtail risk-taking and even innovation itself. This wishful thinking seems to miss the point that, if they are not human rights, risk-taking and innovation are hardwired into human nature. More logical would be to keep up, think laterally from the collective experience of others, learn from the attention given to key issues by the courts (and from our mistakes) and ‘cherry-pick’ best practices wherever these can be identified and demonstrated to be effective.

once again, i want to thank sincerely and congratulate our authors. They have been selected to contribute to this work based on their professional standing and peer approvals. Their willingness to share with us the benefits of their knowledge and experience is a true professional courtesy. of course, it is an honour and a privilege to continue to serve as their editor in compiling this edition.

Jeffrey GoldenLondon school of Economics and Political scienceLondonNovember 2012

ix

Editor’s PrEfacE totHE first EditioN

since the recent financial markets crisis (or crises, depending on your point of view), international capital markets (‘icM’) law and practice are no longer the esoteric topics that arguably they once were.

it used to be that there was no greater ‘show-stopper’ to a cocktail party or dinner conversation than to announce oneself to be an icM lawyer. Nowadays, however, it is not unusual for such conversations to focus – at the initiation of others and in an animated way – on matters such as derivatives or sovereign debt. indeed, even taxi drivers seem to have a strong view on the way the global capital markets function (or at least on the compensation of investment bankers). icM lawyers, as a result, can stand tall in more social settings. Their views are thought to be particularly relevant, and so we should not be surprised if they are suddenly seen as the centre of attention – ‘holding court’, so to speak. This edition is designed to help icM lawyers speak authoritatively on such occasions.

in part, the interest in what icM lawyers have to say stems from the fact that the amounts represented by current icM activities are staggering. The volume of outstanding over-the-counter derivatives contracts alone was last reported by the Bank for international settlements (‘Bis’) as exceeding $700 trillion. add to this the fact that the Bis reported combined notional outstandings of more than $180 trillion for derivative financial instruments (futures and options) traded on organised exchanges. crisis or crises notwithstanding, icM transactions continue apace: one has to admire the resilience. at the time of writing, it is reported that the ‘iPo machine is set to roar back into life’, with 11 flotations due in the United states in the space of a single week. as Gandhi said: ‘capital in some form or another will always be needed.’

The current interest in the subject also stems from the fact that our newspapers are full of the stuff too. No longer confined to the back pages of pink-sheet issues, stories from the icM vie for our attention on the front pages of our most widely read editions. Much attention of late has been given to regulation, and much of the coverage in the pages of this book will also report on relevant regulation and regulatory developments; but regulation is merely ‘preventive medicine’. to continue the analogy, the courts are our ‘hospitals’. accordingly, we have also asked our contributors to comment on any lessons to be learned from the courts in their home jurisdictions. Have the judges got it right? Judges

x

Editor’s Preface to the First Edition

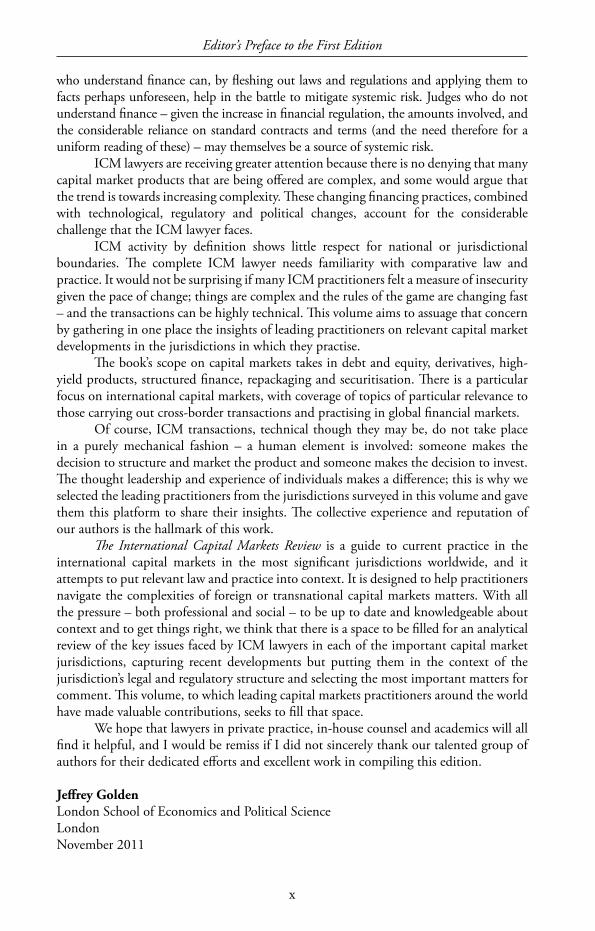

who understand finance can, by fleshing out laws and regulations and applying them to facts perhaps unforeseen, help in the battle to mitigate systemic risk. Judges who do not understand finance – given the increase in financial regulation, the amounts involved, and the considerable reliance on standard contracts and terms (and the need therefore for a uniform reading of these) – may themselves be a source of systemic risk.

icM lawyers are receiving greater attention because there is no denying that many capital market products that are being offered are complex, and some would argue that the trend is towards increasing complexity. These changing financing practices, combined with technological, regulatory and political changes, account for the considerable challenge that the icM lawyer faces.

icM activity by definition shows little respect for national or jurisdictional boundaries. The complete icM lawyer needs familiarity with comparative law and practice. it would not be surprising if many icM practitioners felt a measure of insecurity given the pace of change; things are complex and the rules of the game are changing fast – and the transactions can be highly technical. This volume aims to assuage that concern by gathering in one place the insights of leading practitioners on relevant capital market developments in the jurisdictions in which they practise.

The book’s scope on capital markets takes in debt and equity, derivatives, high-yield products, structured finance, repackaging and securitisation. There is a particular focus on international capital markets, with coverage of topics of particular relevance to those carrying out cross-border transactions and practising in global financial markets.

of course, icM transactions, technical though they may be, do not take place in a purely mechanical fashion – a human element is involved: someone makes the decision to structure and market the product and someone makes the decision to invest. The thought leadership and experience of individuals makes a difference; this is why we selected the leading practitioners from the jurisdictions surveyed in this volume and gave them this platform to share their insights. The collective experience and reputation of our authors is the hallmark of this work.

The International Capital Markets Review is a guide to current practice in the international capital markets in the most significant jurisdictions worldwide, and it attempts to put relevant law and practice into context. it is designed to help practitioners navigate the complexities of foreign or transnational capital markets matters. With all the pressure – both professional and social – to be up to date and knowledgeable about context and to get things right, we think that there is a space to be filled for an analytical review of the key issues faced by icM lawyers in each of the important capital market jurisdictions, capturing recent developments but putting them in the context of the jurisdiction’s legal and regulatory structure and selecting the most important matters for comment. This volume, to which leading capital markets practitioners around the world have made valuable contributions, seeks to fill that space.

We hope that lawyers in private practice, in-house counsel and academics will all find it helpful, and i would be remiss if i did not sincerely thank our talented group of authors for their dedicated efforts and excellent work in compiling this edition.

Jeffrey GoldenLondon school of Economics and Political scienceLondonNovember 2011

18

Chapter 2

Belgium

Sylvia Kierszenbaum and Willem Van de Wiele1

I INTRODUCTION

On 1 April 2011, the ‘Twin Peaks’ model of financial supervision was introduced into Belgian law. Under this model, the National Bank of Belgium (‘the NBB’) is responsible for macro and micro-prudential supervision of the financial sector. The Belgian Banking, Finance and Insurance Commission has been renamed the Financial Services and Markets Authority (‘the FSMA’) and is responsible for the supervision of the financial markets and financial services, and the conduct of business rules in the financial sector. It has a specific role in the field of consumer protection.

In this chapter, we highlight a number of significant developments in Belgium, specifically focusing on debt capital markets.

II THE YEAR IN REVIEW

i Developments affecting debt offerings

Regulatory developmentsFast-track procedure for approval of corporate bond prospectusesA noteworthy development is the existence and application of the fast-track procedure for the approval of corporate bond prospectuses. This procedure, which was introduced on 20 December 2010, has been applied frequently by the FSMA over the past year.

1 Sylvia Kierszenbaum is a partner and Willem Van de Wiele is a senior associate at Allen & Overy LLP. The authors would like to acknowledge the contributions of Joost Everaert, Hannes Laloo and Anthony Verhaegen.

Belgium

19

Under the Prospectus Law,2 the FSMA must approve a prospectus for an issuer (other than a first-time issuer) within 10 working days of the date of the submission of a complete file (unless it has further comments). The FSMA has stated that, for certain types of bonds issued by certain issuers, it considers it ‘sound practice’ to reduce this term to five working days, but the FSMA retains the right to proceed with a standard – non-accelerated – review procedure. The fast-track procedure is designed for plain vanilla bonds (i.e., ordinary fixed-rate (including zero coupon) or variable-rate bonds issued by certain issuers).

The fast-track procedure is only open to issuers that satisfy the following conditions:a the shares or bonds of the issuer have been listed for at least three years and the

periodic information is subject to a posteriori review by the FSMA;b the issuer has responded satisfactorily to any remarks made by the FSMA over the

past three years in the course of exercising its right to supervise financial information. This applies equally to the (limited) review of the interim financial statements;

c the issuer has confirmed in writing to the FSMA that it currently meets all its obligations to its creditors; and

d the issuer’s net assets have not fallen below one-half of the company’s capital as a result of a loss sustained.

Good practices and the issue of corporate bondsAs a result of certain issues that came to the FSMA’s attention in the context of corporate bond issues, and after consultation with the financial sector, the FSMA has identified a number of good practices. It published a communication in this respect in December 2011. Compliance with these good practices will be subject to regular evaluation and has been a particular point of attention for retail bond issues in 2011 and 2012. Two of the key recommendations are as follows.

a Allotment methods based on a proportional reduction of orders are recommendedIn the event of oversubscription, the FSMA recommends allotment methods based on a proportional reduction of orders, instead of an allotment on a ‘first-come, first-served basis’.

If the allotment must nonetheless be made in the order of subscriptions received (e.g., if the offer has an international dimension), financial intermediaries should not accept subscriptions prior to the opening of the offer and the publication of the prospectus. All investors should be treated on an equal footing.

Regardless of the choice of allotment method, the public should be informed of the manner in which the allotment will be made, in order to ensure a degree of predictability.

b The prospectus must be made available within the legal time periodsThe prospectus must be made available at least six working days before the end of the offer in the case of an IPO (initial public offering of shares) and at least three working days before the closing of the offer for offers other than IPOs. This is a requirement under

2 The Law of 16 June 2006 on the public offer of investment instruments and the admission to trading of investment instruments on a regulated market.

Belgium

20

the Prospectus Law (also in relation to passported offers). In practice, the entire offer of corporate bonds is often fully subscribed within a few hours after the opening of the offer.

The FSMA recommends that, in cases where the prospectus is not available before the opening of the offer, the offer must remain open for three working days. It should be possible to validly subscribe during these three working days. Allotment criteria must be established that permit a fair treatment of subscriptions received during the entire offer period. Where bonds are to be allotted on a ‘first-scome, first-served’ basis, the prospectus should be available at least two working days before the opening of the offer.

FSMA Communication regarding the implementation of the PD Amending DirectiveDirective 2010/73/EU (‘the PD Amending Directive’) amending Directive 2003/71/EC (‘the Prospectus Directive’) had to be implemented by Member States into national law by 1 July 2012. The PD Amending Directive is supplemented by Commission-delegated regulations. These implementing measures amend European Regulation No 809/2004 of 29 April 2004 (‘the European Regulation’), which contains the prospectus schedules. Most of these delegated regulations entered into force on 1 July 2012. These will not require any implementation measures under Belgian law.

Belgium has not yet implemented the PD Amending Directive. No specific date for implementation of the PD Directive in Belgium is currently known. The FSMA published the ‘Communication of the FSMA on the policy in effect as from 1 July 2012 for the treatment of dossiers relating to public offers and admission to trading on a regulated market’ (‘the FSMA Communication’). The FSMA Communication sets out the FSMA’s policy awaiting the implementation of the PD Amending Directive in Belgium.

According to the FSMA Communication, the PD Amending Directive is a ‘maximum harmonisation’ directive, which means that it sets out mandatory rules intended to harmonise, as far as possible, the regulations of the Member States; Member States have little or no margin for manoeuvre when implementing the PD Amending Directive.

The FSMA refers to the considerations of the Court of Justice of the European Union (‘the CJEU’), which holds that the provisions of a directive that have not been implemented in due time by Member States have ‘vertical direct effect’, provided they are sufficiently clear, precise and unconditional.

Without prejudice to any interpretation to the contrary by the CJEU, all the provisions of the PD Amending Directive that must be implemented in Belgian law are, in the FSMA’s opinion, sufficiently clear, precise and unconditional to be capable of vertical direct effect as just described. Vertical direct effect, combined with the principle of the primacy of Community legislation, means that the provisions of the PD Amending Directive will be applied on the FSMA’s initiative as from 1 July 2012, unless they impose new constraints upon issuers. Issuers may nonetheless voluntarily apply the more stringent provisions of the the PD Amending Directive. Doing so will enable them to benefit from the Community-wide approval of the prospectus (passport).

Without prejudice to a case-by-case examination of every transaction by the FSMA’s services, the FSMA considers, for instance, that as from 1 July 2012: a the offers of transferable securities addressed to fewer than 150 people will not be

considered public;b the new definition of qualified investors, which refers to definitions of professional

or institutional clients and eligible counterparties within the meaning of MiFID,

Belgium

21

shall apply without prejudice to the possibility, for issuers, to continue to make use of the register of qualified investors published on the FSMA’s website in compliance with the Royal Decree of 26 September 2006 extending the concepts of qualified investors and of institutional or professional investor;

c abbreviated prospectus schedules, drawn up for the benefit of SMEs in particular, as contained in the European Regulation, will in principle be applicable;

d offers made to (former or existing) directors or employees will be governed by the provisions of the PD Amending Directive, which are less stringent;

e in the event of the resale of transferable securities by financial intermediaries, the latter may reuse a prospectus that is still valid, provided the issuer or the person responsible for drawing up the prospectus agrees to its reuse; and

f issuers or offerors who wish to benefit from the Community-wide approval of the prospectus (passport) must ensure that they include the ‘key information’ provided for in the PD Amending Directive in the summary of the prospectus, and they must present that information in accordance with the schedules for the purpose contained in the European Regulation.

Market developmentsRetail bondsIn 2011 and 2012, Belgian issuers have been very active on the debt capital markets. In particular, there have been a number of highly successful retail bonds, placed through the retail network and private banking network of the Belgian banks. Belgian issuers continue to seek to diversify their sources of funding and the disintermediation trend continues. SMEs are also looking at bond issuances as potential sources of funding.

Perpetual bonds issued by a corporate issuerIn March 2011, the Belgian market saw a significant debt capital market transaction in the form of a fixed-to-floating rate perpetual subordinated securities issue by a global biopharmaceutical company. Belgian financial institutions have issued perpetual bonds in the past, but this transaction was a first for the Belgian market, as it was the first issue of listed perpetual bonds by a Belgian corporate.

ii Developments affecting derivatives, securitisations and other structured products

Financial Collateral Law On 10 November 2011, the law implementing EU Directive 2009/44/EC (‘the 2011 Law’) was published in the Belgian official journal. The 2011 Law implements EU Directive 2009/44/EC (‘the Directive’) amending Directive 98/26/EC (‘the Settlement Finality Directive’) and Directive 2002/47/EC (‘the Financial Collateral Directive’). The 2011 Law amends the Belgian law of 28 April 1999 implementing Directive 98/26/EC on settlement finality in payment and securities settlement systems (‘the Settlement Finality Law’) and the Financial Collateral Law.3 It is important to stress that this Law

3 The Law of 15 December 2004 on financial collateral.

Belgium

22

does not merely implement the Directive, but also makes some other important changes to the Financial Collateral Law.

The Financial Collateral Law implementing the Financial Collateral Directive became effective on 1 February 2005 and had a significant impact on (1) financial collateral arrangements relating to cash and financial instruments and (2) netting and close-out netting arrangements. The Financial Collateral Directive was implemented in a very broad way so as to apply to financial collateral arrangements and netting, regardless of the nature of the parties or the transactions involved (except title transfer collateral arrangements involving individuals). However, there was criticism of the Financial Collateral Law’s broad scope of application, in particular in the context of judicial reorganisation procedures and with respect to individuals. In addition, some uncertainty remained regarding issues such as the scope of application of the Financial Collateral Law as regards financial instruments and the dispossession requirement in relation to cash.

In line with the Directive, the 2011 Law widens the definition of ‘financial collateral’ to cover credit claims, which can also include consumerr loans (in addition to cash and financial instruments), and therefore provides a welcome expansion of the general scope of the current rules. The 2011 Law also seeks to address some of the uncertainty raised by the Financial Collateral Law as regards the definition of ‘financial instruments’ and ‘possession’ as regards cash. However, the 2011 Law also limits the application of certain provisions in the context of a judicial reorganisation and with respect to individuals (who are non-merchants).

In particular, limitations have been introduced on close-out netting and the enforcement of pledges on cash and credit claims during a judicial reorganisation where one of the parties involved is not a public or financial entity. This means that netting and close-out netting can no longer be applied, and a pledge on cash and credit claims can no longer be enforced, during a judicial reorganisation where the judicial reorganisation relates to (1) an entity that is not a public or financial entity regardless of the nature of the creditor concerned or (2) a public or financial entity if the creditor is not a public or financial entity.

This limitation does not apply:a when there is an actual payment default;b when the creditor that invokes netting does not rely on a close-out provision

entitling such creditor to close-out positions and contracts;c to netting and close-out netting upon enforcement of a financial collateral

arrangement relating to financial instruments or upon enforcement of a title transfer collateral arrangement (including repos); or

d to financial collateral arrangements, netting agreements and close-out provisions that are entered into in the context of certain derivatives transactions defined by royal decree (safe-harboured derivatives transactions).

Financial collateral arrangements regarding financial instruments are not affected. Netting and close-out netting arrangements and pledges of cash or credit claims between public and financial entities also remain unaffected.

The 2011 Law includes a list of public and financial entities, which includes credit institutions, investment firms, insurance companies, management companies of collective investment undertakings, collective investment undertakings, central counterparties, clearing and settlement institutions, certain financial institutions as defined in the 2011

Belgium

23

Law, security agents as provided for in the 2011 Law, public authorities, the National Bank of Belgium, the European Central Banks and other listed financial institutions, and any other foreign legal entity that belongs to the categories of entities defined in Articles 1.2(a) to 1.2(d) of the Financial Collateral Directive.

The list of safe-harboured derivatives transactions has been determined by a royal decree, which was published on 10 November 2011 (‘the Royal Decree’).4 The safe-harboured derivatives transactions include:a derivatives: defined in a broad manner, including OTC transactions, as well as

transactions traded on a regulated market or an MTF (multilateral trading facility), cash settled as well as physically settled transactions, cleared via a clearing house, a central counterparty or directly between the parties or their representatives;

b the sale and purchase, lending or delivery of securities, money market instruments, fund units, derivatives, emission allowances, electricity certificates or similar instruments; and

c FX spot transactions.

In order to fall under the safe harbour provisions, the transactions must fall within one of the following two categories:a transactions whereby parties apply one of the following standard agreements:

• the ISDA Master Agreement, the Rahmenvertrag für Finanztermingeschäfte, the European Master Agreement for Financial Transactions, the Global Master Securities Lending Agreement, the Global Master Repurchase Agreement or similar standard agreements (governed by Belgian or foreign law), if such agreements are used by credit institutions in the Belgian market; or

• the rules or a contractual framework of a regulated market, MTF, clearing house, central counterparty or a system (as defined in the Settlement Finality Law (as amended)); or

b transactions that fall within the type of transactions that can be traded on a Belgian or foreign regulated market or MTF, or that can be cleared via a clearing house, central counterparty or a system (as defined in the Settlement Finality Law (as amended)).

The safe harbour also extends to certain financing arrangements with respect to the safe-harboured derivatives transactions (loans and advances, guarantees and letters of credit).

Netting and close-out netting agreements with individuals (who are non-merchants) are no longer protected by the Financial Collateral Law, subject to certain limited exceptions. This amendment follows a decision by the Belgian Constitutional Court. In a case relating to a collective settlement of debts procedure with respect to an individual, the Constitutional Court held that the application of the Financial Collateral Law to netting agreements concluded with individuals (who are non-merchants) was unconstitutional.

4 The Royal Decree determining derivatives and other financial transactions referred to in Article 4, § 3 and § 4 of the Act of 15 December 2004 on financial collateral and various tax provisions relating to collateral arrangements and actual loans on financial instruments.

Belgium

24

Moratorium on the sale of structured products and public consultation in this respectThe regulation of the distribution of structured products to retail investors remains a major area of development for the FSMA, as demonstrated by a number of recent initiatives. Below we summarise the new voluntary moratorium regarding the sale of these products and certain important proposals by the FSMA for a new regime regulating this area. These proposed regulations would have a significant impact on the relationship between manufacturers, distributors and consumers, internal compliance requirements, standards of liability applied and the litigation of claims for mis-selling.

On 20 June 2011, the FSMA launched a voluntary moratorium on the distribution of certain complex structured products to retail investors (‘the Moratorium’). By signing up to the Moratorium, financial institutions undertake not to distribute those structured products to retail investors, unless certain specific criteria are met. The Moratorium came into effect on 1 August 2011 and only applies to structured products marketed after that date.

The Moratorium gained widespread acceptance from Belgian market participants, with the vast majority of Belgian distributors of structured products signing up. Since 1 September 2011, financial intermediaries, such as brokers and agents (tied agents), have also been able to sign up to the Moratorium.

Adherence to the Moratorium gives rise to a number of considerations, such as:a its impact on product development and distribution models;b its impact on liability (e.g., how will adherence to the Moratorium affect the

liability standards applied to Belgian distributors?);c uncertainty as to how it will apply in practice;d the use of potentially very broad criteria to determine the scope of it; ande the transitory nature of the Moratorium and its interplay with various European

rules.

Public consultation regarding a regulatory frameworkOn 12 August 2011, the FSMA launched a public consultation on the introduction of a regulatory framework for the distribution of structured products to retail consumers (the Consultation). The Consultation ran until 15 October 2011.

According to the FSMA, the objective of the future regulatory regime should be twofold: enhancing transparency and reducing the complexity of structured products.

The FSMA is also questioning whether, in addition to covering structured products, the new regime should also apply to other complex or potentially risky products (e.g., subordinated or perpetual bonds and actively managed funds).

The FSMA is contemplating regulations that, if adopted, will have a far-reaching impact on the distribution and sale of structured products to retail customers in Belgium, at all stages of the ‘product cycle’, i.e., starting from the manufacture of the product and its internal approval, through to the marketing and the after-sales service in relation to the product and the secondary market. These regulations may also have a significant impact on the manufacturer–distributor relationship. Without being exhaustive, below are some noteworthy points in the consultation:a Distributor internal approval process: before a structured product can be

distributed to retail investors, the distributor should have carried out a positive

Belgium

25

internal approval of the product. The process must show that, in comparison with other alternatives available on the market, the product offers the target group an added value and that the service provided is in the consumer’s interest. Senior management involvement is required. The FSMA proposes that, for some aspects of this process, distributors may refer to information provided by the entity responsible for the structuring (i.e., the manufacturer). However, the distributor would continue to hold ultimate responsibility and would have to be in a position to verify, by itself or via an external provider, the information received.

b Transparency: the FSMA is suggesting that distributors would use a classification system that covers the major risks, including credit risk and market risk, and would be applied, ideally, to all types of products. The FSMA envisages a common risk classification method that would be developed in conjunction with the financial sector.

c After sales service: the FSMA states that it is important that the value of the products remains traceable by customers, including after acquisition. It is suggested that the distributor should inform customers upon the occurrence of every significant change in the risk profile or value of the product, as well as periodically. Information should also be provided about the amount paid at each date when a return is paid out or upon repayment of the capital, with an explanation of the formula that was applied. It is also proposed that the final return on all structured products that the distributor has distributed over the past 10 years should be published on the distributor’s website.

d Secondary market: according to the FSMA, it is necessary to question whether there should be minimum standards for the organisation of the secondary market (e.g., regarding the costs that may be charged or the consistency of the valuation method and a comparison of the parameters used at that point with the parameters that were applied at the time of the initial distribution).

ii Publication of feedback statement following the ConsultationOn 10 July 2012, the FSMA published its feedback statement regarding the Consultation. The FSMA identified three topics which will be investigated further in the first instance:a transparency of the expected value of structured products as alternative for

transparency of the structuring costs;b extension of certain aspects of the moratorium to other financial products (than

structured products); andc a feasibility study of a labelling system of financial products.

The FSMA has not yet published draft regulations following the Consultation.

iii Covered bonds and Mobilisation Law

A very significant development in Belgium is the introduction of a legal framework for the issue of covered bonds. Belgium was one of the last countries in Europe to not have such a legal framework in place.

Belgium

26

While a full discussion of the legal framework is outside the scope of this contribution, we note that the Covered Bonds Law5 contemplates a full-on balance sheet structure and does not make use of a special purpose vehicle. Belgian covered bonds may only be issued by Belgian credit institutions that are specifically authorised to do so by the NBB. The estate of a credit institution that has issued Belgian covered bonds is legally composed of a general estate and one or more ring-fenced special estates. The holders of Belgian covered bonds and certain identified creditors have exclusive recourse against the relevant special estate, and at the same time maintain a right of recourse against the general estate. The Covered Bonds Law introduces adequate protection mechanisms that make the proposed legal framework particularly robust.

Simultaneously with the Covered Bonds Law, a law on various measures to facilitate the mobilisation of claims in the financial sector has been adopted (‘the Mobilisation Law’).6 The aim of the Mobilisation Law is to address certain legal impediments to the transfer of credit claims and to remove potential claw-back concerns as regards the registration of cover assets in the cover register for the special estate in the context of covered bonds.

However, the scope of the Mobilisation Law is broader than facilitating and protecting the transfer or registration of cover assets in the context of covered bonds. It removes a number of uncertainties and grants additional protection in relation to the transfer of credit claims in general. It addresses a number of issues such as the transfer of credit claims against public authorities in the context of public procurement, the maintenance of security interests on the transfer of credit claims, set-off and certain open questions that arose in the context of securitisation transactions involving mortgage receivables.

iv Cases and dispute settlement

In one significant case, on 21 May 2012, the Brussels Court of Appeal handed down a judgment in what can be considered one of the most important Belgian prosecutions emerging from the financial crisis of 2008. This decision has important implications for financial parties. It confirms the application of the Market Practices Act7 in an area where there was previously a lack of clarity, which imposes more stringent requirements on finance parties, and also means that, in addition to the FSMA, the Economic Inspectorate has jurisdiction over publicly offered financial products using a prospectus.

The case related to certain principal protected structured notes issued by Lehman Brothers Treasury Co BV and guaranteed by its ultimate parent Lehman Brothers Holding International Inc (‘the Notes’). On 8 October 2008, Lehman Brothers Treasury Co BV filed for bankruptcy after Lehman Brothers Holding International Inc entered into Chapter 11 proceedings. As a consequence, the Notes lost most of their value.

5 The Law of 3 August 2012 establishing a legal regime for Belgian covered bonds.6 The Law of 3 August 2012 on various measures to facilitate the mobilisation of receivables in

the financial sector.7 The Law of 6 April 2010 on market practices and consumer protection.

Belgium

27

In August 2009, the Brussels public prosecutor accused a Belgian distributor of the Notes and three of its managers (the CEO and the previous chief legal officer and current chief legal officer) of having obtained illegal profits for the distributor by deceiving customers about the risks related to the Notes.

The Court of Appeal overturned the previous decision of 1 December 2010 of the Brussels Tribunal of First Instance ruling that (1) certain rights of the defence had been violated by the administrative authority in charge of the supervision of the Market Practices Act (the Economic Inspectorate) and by the prosecution, and (2) the Market Practices Act was applicable only to certain limited aspects of the sale of publicly offered products using a prospectus.

The Court of First Instance considered that the Market Practices Act applies to certain aspects of the marketing of financial products that are the subject of a prospectus. This was controversial, as it had previously been assumed that general consumer protection legislation did not apply to the marketing of publicly offered financial products as the marketing of, and the promotional material for, these products were governed by the Prospectus Law and by the more specific MiFID rules.

The Court of Appeal held that while the Market Practices Act does not apply to marketing material (that has been approved by the regulator under the Prospectus Law), it does nevertheless apply to other parts of the sales process (e.g., discussions with customers at a distributor’s branch).

Employees in the local branches of the distributor and third-party self-employed agents had recommended that clients should purchase the Notes on the basis of the client’s risk profile and explained to them the functioning and the characteristics of the Notes. According to the Court of Appeal, this constituted investment advice that falls within the definition of ‘services’ under the Market Practices Act. The payment of a commission to the distributor was also considered to be an element likely to demonstrate the existence of a service.

However, the Court of Appeal ruled there was no evidence of any wrongdoing by the distributor or the managers in respect of those parts of the sales process to which the Market Practices Act did apply.

The Court of First Instance also ruled that there had been a technical breach of the Prospectus Law because not all promotional material had been submitted ne varietur (i.e., in final form) to the FSMA, and the marketing material had not been updated after Lehman Brothers’ downgrade in June 2008.

The Prospectus Law charges were dismissed by the Court of Appeal. The Public Prosecutor and the Economic Inspectorate had violated the defendants’ right to remain silent by threatening to impose a fine on the distributor under the Market Practices Act if it did not provide the requested information. The Court of Appeal ruled that as soon as criminal sanctions are contemplated by investigators, the right to remain silent applies. All documents submitted by the distributor, as a consequence of threats by the Economic Inspectorate and the prosecution under the Market Practices Act, had to be set aside. This meant that there was no valid evidence to convict under the Prospectus Law. The Court of Appeal, therefore, did not have to consider whether the Court of First Instance had been correct to find that there had been a technical breach of the Prospectus Law.

It should be noted that the Court of Appeal’s interpretation of the right to remain silent is an extensive one, applying not only to statements made by a defendant, but

Belgium

28

also to the communication of documents in the possession of the defendant. An appeal against this part of the decision by the Public Prosecutor is currently pending before the Belgian Supreme Court.

Although in the past in-house counsel who participate in criminal offences have been convicted, this was the first time that in-house counsel had been accused of negligence in the organisation of the legal department, leading to the facilitation of a criminal offence. It was alleged that the in-house counsel at the distributor had failed to train its staff adequately in the application of the Market Practices Act, thus leading to the commission of a breach of the Market Practices Act as a result of their criminal negligence. The Court of Appeal annulled the conviction of the Tribunal of First Instance in this respect. Even if certain individual third-party self-employed agents may have violated the Market Practices Act in specific contacts with customers, there was no evidence of any criminal negligence by the management or legal department of the distributor.

The impact of this judgment on the financial sector is significant for a number of reasons. First, the Court of Appeal ruled that the Market Practices Act applies to some services related to publicly offered financial products. This raises the bar for financial institutions: unlike the position under the Prospectus Law, the criminally sanctioned provisions on misleading publicity in the Market Practices Act apply even if there was no intent to mislead.

Second, the application of the Market Practices Act implies that the Economic Inspectorate now also has authority over parts of the sales process of publicly offered financial products offered under a prospectus that the Court of Appeal found to fall under the Market Practices Act. Prior to this decision, the FSMA was generally presumed to be the only authority competent for the control of marketing materials for financial products.

Finally, it was the first complex case in which a Belgian prosecutor directly summoned the parties to appear before the court and thus bypassed the intervention of an investigating magistrate, which would have resulted in a review of the validity of the investigation measures by the Chambre du Conseil (the pre-trial chamber). The Court of Appeal stated that the public prosecutor’s decision not to instruct an investigating magistrate and to keep control of the investigation is legal, but that if following this strategy the prosecutor must be careful that the rights of defendants are observed.

v Relevant tax law (withholding tax and wealth tax)

Under the 2011 Program Law,8 the reduced dividend withholding tax rate (applicable to, inter alia, VVPR9 dividends) and the standard interest withholding tax rate have both been raised from 15 per cent to 21 per cent. In addition, the withholding tax rate applicable to share buy-backs has been increased from 10 per cent to 21 per cent (but liquidation bonuses remain subject to a 10 per cent rate).

Individuals investing on a non-professional basis are now subject to an additional tax of 4 per cent on income taxable at the new 21 per cent rate (resulting in an aggregate

8 The Law of 14 April 2011 laying down miscellaneous provisions.9 Verminderde Voorheffing Précompte Réduit (Belgium dividend coupon).

Belgium

29

tax rate of 25 per cent), subject to certain exceptions and with the possibility to benefit from an exempt tranche of €20,020 per annum (the threshold amount for tax year 2013). The taxpayer can elect for the additional tax to either be withheld at source, or for the amount of his or her income to be notified to the tax authorities such that the additional tax can be levied in the framework of his or her annual personal income tax assessment.

Accordingly, companies distributing interest or dividends (and Belgian intermediaries, as applicable) will need to put systems in place to either make the withholding or pass on the required information. This may be a challenge in relation to listed shares and bonds, as the text of the law suggests that information needs to be transmitted unless the investor opts for the levy of the additional 4 per cent, whereas the issuer will often not know the identity of its investors and will thus not be able to transmit any information.

vi Other considerations

Bank resolutionBelgium did not wait for initiatives to be introduced at a European level and in fact introduced measures regarding bank resolution back in 2010. These measures related to, among others, forced sales and the creation of ‘good banks’, ‘bad banks’ and ‘bridge banks’. Despite having already been proposed by some politicians, living wills were not provided for in the 2010 laws. In 2011, the newly formed government announced that, in consultation with the NBB, a living will for financial institutions would be introduced. We will have to continue to monitor how measures with respect to bank resolutions are implemented at a Belgian level. The interplay between any such Belgian measures and the measures introduced at a European and global level (e.g., the Likkanen report10).

Ring-fencing The Belgian government requested that the NBB conduct a study into whether it is both opportune, and practically and financially feasible, to (1) introduce a split between savings banks and investment banks or (2) to introduce a retail ring fence. In conducting this study, the NBB had to analyse what has been done in the eurozone and in other European countries. The NBB had to carry out a global analysis of the impact of the proposed measures on the Belgian financial sector and the Belgian economy.

The NBB published an interim report in June 2012 and plans to publish a final report by the end of 2012. The NBB has not yet adopted a final position, but has already indicated that there are a number of arguments against unilaterally imposing a bank split in Belgium. Hence, the interplay between the position of the Belgian government and the initiatives at European Union level will have to be closely monitored.

Financial planningThe Belgian FSMA has carried out a public consultation on the proposed legal regulation of the status of financial planners.

10 Report of the High-level Expert Group on reforming the structure of the EU banking sector (final report 2 October 2012).

Belgium

30

The Belgian FSMA has prepared a set of draft legal texts on the status of independent financial planners. A financial planner gives personalised advice on investments or strategies for investing in financial products (ranging from savings accounts to the most sophisticated investment instruments). Their advice is intended to help with asset planning in order to prepare for one’s retirement or succession, or to build up savings or acquire real estate.’

The FSMA sets out the following conditions for financial planners:a Independence: the status may not be combined with any other financial

profession or with any other profession that might give rise to conflicts of interest. An independent financial planner may not receive commission and may only be remunerated by his or her clients.

b Organisation of the firm: in order to obtain an authorisation, a financial planner must satisfy various conditions (e.g., regarding the reliability, competence and appropriate experience of the senior managers, minimum capital, appropriate organisation and professional liability insurance coverage).

Independent financial planners will be subject to rules of conduct based on the MiFID rules. Regulated undertakings (credit institutions, investment firms, etc) will also have to comply with the MiFID rules when providing financial planning services.

III OUTLOOK AND CONCLUSIONS

We expect the recent high levels of activity in the debt capital markets to continue, as Belgian issuers continue to seek to diversify their sources of funding and the disintermediation trend continues. In particular, for certain Belgian issuers, retail bond issues may continue to be an interesting option. For Belgian credit institutions, the introduction of the covered bond legal framework is a key development.

We also anticipate that the Belgian regulators will continue to focus on consumer protection. Further initiatives with respect to structured products are to be expected, but the interplay between these Belgian initiatives and the initiatives at the European level will need to be closely monitored.

Bank resolution and ringfencing are also points for attention. Again, in these areas the interplay with the measures introduced at a European and global level will have to be borne in mind.

300

Appendix 1

about the authors

SylviA KierSzenbAumAllen & Overy LLPPartner Sylvia Kierszenbaum practises in areas including capital markets, banking and financial services and regulation. She advises on capital markets transactions and financial instruments, structured finance transactions, securitisations and trade receivables finance, regulation of banking activities and financial services, corporate reorganisations, corporate finance and bank lending. She is an expert member of the Febelfin working group advising on the new covered bond legislation.

Ms Kierszenbaum received her law degree from the University of Antwerp and an LLM from Cornell University. She is admitted as advocate in Belgium and is fluent in English, French and Dutch.

According to Chambers & Partners, 2012, ‘Sylvia Kierszenbaum receives particular mention for her technical prowess. Clients appreciate that she is “very open and available”.’

Willem vAn de WieleAllen & Overy LLPSenior Associate Willem Van de Wiele specialises in debt capital markets transactions and has particular experience in advising on bond issuances and securitisations. He also advises on financial law, in particular on the regulation of banking activities and financial services. Mr Van de Wiele is admitted to the Antwerp and New York Bars. He received his law degree from the University of Ghent and an LLM (in corporate law) from the New York University School of Law.

About the Authors

301

Allen & Overy llPUitbreidingstraat 802600 AntwerpBelgium Tel: +32 3 287 [email protected]@allenovery.com

www.allenovery.com