Embed Size (px)

Citation preview

31

Solution to question 1

Auric Gold

(a) BIK computation€ € €

HouseOption 1 Annual value 2,250,000 8%* 6/12 90,000

Option 2 Annual valuemarket rent 3,000 6 months 18,000

Use option 2 18,000 Less: Rent contributed 1,000 6 months (6,000)Chargeable BIK 12,000

FurnitureAnnual value 50,000 5% * 6/12 1,250

CarList price 90,000 Less cash discount (9,000)OMV 81,000

Alternative option:Standard % 30% Reduction - 20% (alternative to high mileage option) 6% Adjusted % 24%Cash equivalent 19,440

Prorate for actual use period days 122/365Chargeable BIK 6,498

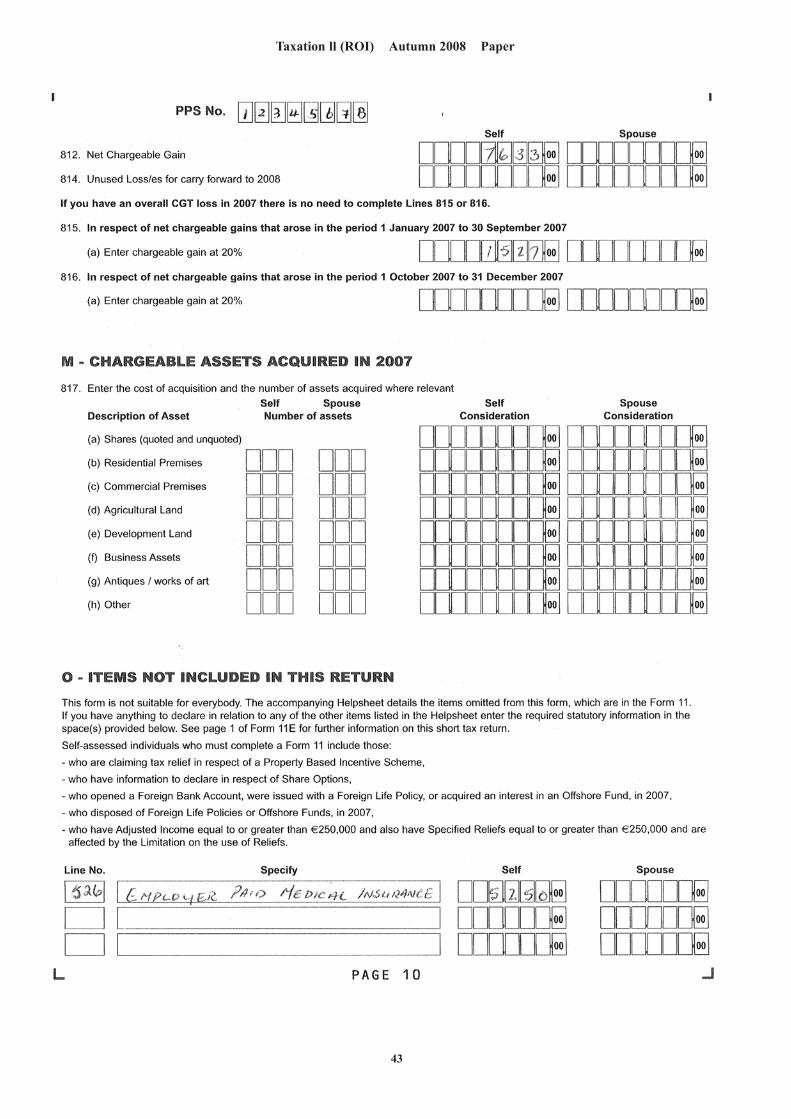

Medical insuranceAmount paid by company 4,200 Gross up for tax relief at source - 20% 0.80Chargeable BIK 5,250

Total c/fwd 24,998

Solution to question 1 continued on next page

The Institute of Accounting Technicians in Ireland

Admission Examination : Autumn 2008

SOLUTIONS TO PAPER 7

TAXATION II (Republic of Ireland)

Author : Mr Ciaran O’Sullivan, FCA

Solution to question 1 (Cont’d) € €B/Fwd 24,998

Preferential loanSpecified BIK rate 12% Rate paid 3% Chargeable rate 9%

Period Loan RateJan-Sep 30,000 9% 9 months 2,025 Oct - Dec 24,000 9% 3 months 540 Chargeable BIK 2,565

Total BIK 27,563 P60 total (Note: The P60 will show all remuneration including BIK) 500,000Monetary remuneration 472,437

(b) PRSI payable by AuricPay per P60 500,000Calculation @ class S1 rates as Auric is a proprietory director First 1,925 5.0% 100,100 5,005.00 Balance 5.5% 399,900 21,994.50

26,999.50 500,000

(c) Capital Gains Tax computationDisposal proceeds May 07 10,500

Deductions:Cost Jul 93 1,200 Indexation 1.331

(1,597)

Gain 8,903 Annual exemption (1,270)

7,633

Tax @ 20% 1,527

(d) Auric GoldIncome Tax Computation 2007

Self Spouse Total€ € €

INCOME:Schedule D

Case IV Bank interest 5,200 3,250 3,250 6,500 Schedule E 500,000 72,000 572,000 GROSS INCOME 503,250 75,250 578,500 LESS DEDUCTIONS

Expenses in employment - (300) CHARGES - -TOTAL DEDUCTIONS - (300) (300)TOTAL INCOME 503,250 74,950 578,200 PERSONAL RELIEFS

Medical expenses see below 2,000 (2,000)

TAXABLE INCOME 576,200 TAX: Interest 20% 6,500 1,300.00

20% 43,000 8,600.00 Increase in standard band 20% 25,000 5,000.00

41% 501,700 205,697.00 TOTAL TAX 576,200 220,597.00 (c/fwd)

Solution to question 1(d) continued on next page

Taxation ll (ROI) Autumn 2008 Solutions

32

Solution to question 1(d) (Cont’d)€ € €

220,597.00 (B/Fwd)NON REFUNDABLE TAX CREDITS

Personal allowance 3,520 Employee *1 1,760 Rent relief 20% 6,000 1,200 Tuition fees 20% 4,000 800 Service charges 20% 200 40 Medical insurance 20% 5,250 1,050 DIRT 20% 6,500 1,300

(9,670.00)TAX DUE 210,927.00

PRSI Self Spouse Self Employed PRSI 3% - - Health contribution 2% 65.00 65.00 130.00

REFUNDABLE TAX CREDITSPaye Deducted 192,000.00 18,900.00

(210,900.00)Net Tax due 157.00

Preliminary Tax Paid

Balance of Tax payable for 2007 157.00

Health ExpensesSelf Sara Gold €

Routine health expenses 4,600 400

4,600 400 5,000 Less: Reimbursement from medical insurance (3,000)

Relief 2,000

Note: the personal excess deduction does apply from 2007.

(f) Filing obligations

Income taxAuric is a proprietary director and therefore the self assessment rules apply to him. He has to file his 2007 tax return by 31 October 2008 (or extended deadline date if filed by ROS).

CGTEvery person with a chargeable gain is required to make a return of that gain. CGT is part of the self assessment systemand therefore in the case of an individual a return of chargeable gains for 2007 has to be filed by 31 October 2008. Theseare normally filed by including them on the return of income Form 11/12. However if the individual is not required tofile a Form 11/12 a form CG1 should be filed.

A surcharge is payable if late; 5% up to 2 months late and 10% thereafter (subject to a maximum limit).

Taxation ll (ROI) Autumn 2008 Solutions

33

Taxation ll (ROI) Autumn 2008 Paper

34

Taxation ll (ROI) Autumn 2008 Paper

35

Taxation ll (ROI) Autumn 2008 Paper

36

Taxation ll (ROI) Autumn 2008 Paper

37

Taxation ll (ROI) Autumn 2008 Paper

38

Taxation ll (ROI) Summer 2004 Paper

39

Taxation ll (ROI) Autumn 2008 Paper

40

Taxation ll (ROI) Autumn 2008 Paper

41

Taxation ll (ROI) Autumn 2008 Paper

42

Taxation ll (ROI) Autumn 2008 Paper

43

Solution to question 2 (Multiple choice)

[1] (b) first accounting period 12 ME 31/3/07, 2nd accounting period 9 ME 31.12.07

[2] (d) €5,000 /.8 @ 20% = €1,250

[3] (a) 2nd year, first 12 mths tradingas a/c covered 12 month period i.e. €15,000

[4] (c) Any time between 1.10.06 and 31.03.07

[5] (c) a person, not a director, who pays all tax through PAYE

[6] (b) cost of audio system (BIK)

[7] (c) €11,000 outstanding for 18 months

[8] (b) Liable to VAT at point of importation

[9] (c) Place of supply of goods is where the goods are located at the time of supply.

[10] (b) (1,500-750)*4/10

Solution to question 3 (VAT)

(a) Quickbuck Limited

Memorandum to the Directors of Quickbuck Limited From: Student Date: 26 August 2008

Further to the Revenue notification to conduct an audit of the company's tax affairs, and to your request forclarification regarding items not entitled to a VAT input credit, I set out below the usual items that fall into thatcategory.

Items on which input credit is not allowed:

1 Provision of personal services (food,drink, accommodation, personal care etc) supplied to the taxable person.

2 Entertainment expenses.

3 Passanger motor vehicles other than as stock in trade or use in motor related businesses, whether purchased or hired.

4 Petrol other than as stock in trade.

5 Any goods or services not used for the business or used for exempt activity.

6 Goods for which a valid VAT invoice is not held.

Voluntary disclosure

You asked for an explanation of the term "voluntary disclosure".

A voluntary disclosure is a disclosure to the Revenue of any underpayment of tax in advance of Revenue discoveringsuch underpayment.

A "qualifying" voluntary disclosure means that the taxpayer can avail of reduced tax penalties, non publication as atax defaultor, and immunity from criminal prosecution.

It is advisable to consider making a "voluntary disclosure" if there are any tax matters that have been treatedincorrectly and resulted in an underpayment of tax.

Taxation ll (ROI) Autumn 2008 Solutions

44

Solution to question 3 (VAT)

(b) Danny

Jan - Feb 2008

Gross Receipts VAT Input Credit Input VAT Outputs Output VAT E1 E2 Comment€ Rate € € € €

Outputs1 Sales of cigarettes 10,890 21% 9,000 1,890 2 Sales of foods items 24,700 0% 24,700 - - 3 Sales of hardware 3,872 21% 3,200 672

Net4 UK purchases 8,000 21% 8,000 1,680 8,000 deferred accounting

Inputs Net1 Cigarettes 9,200 21% 9,200 1,932 2 Food 26,400 0% 26,400 - 3 Hardware - UK supplier 8,000 21% 8,000 1,680 deferred accountng4 Hardware 1,600 21% 1,600 336 5 Hardware (6,000) 21% (6,000) (1,260)6 Trolley 1,300 21% 1,300 273 7 Repairs 1,600 13.5% 1,600 216 8 Diesel 200 21% 200 42 9 Rent 2,000 no vat generally, also see payment10 Fire insurance 800 no vat11 Electricity 400 13.5% 400 54 12 Car 28,000 no deduction13 Software support 2,200 21% 2,200 462 14 Telephone 300 21% 300 63 15 Legal re debt collection 700 21% 700 147 16 Promotional keyrings 500 21% 500 105

46,400 4,050 44,900 4,242 - 8,000 Payment due 192

Taxation ll (ROI) Autumn 2008 Solutions

45

Taxation ll (ROI) Autumn 2008 Solutions

46

DANNY

Solution to question 4 (Corporation tax)

Mansard Limited

(i) Adjusted Profits Computation year ended 31 December 2007€ €

Profit Per accounts 29,300 Add back Depreciation 25,900 Pension contribution (2,900-2,500) 400 Motor and travel see below 4,133 Repairs reception 12,500 Repairs let property 2,500 Legal new patent 1,400 Legal let property 4,000 Interest let property 11,000 Interest late payment of tax 100

61,933 Deduct Rental income 10,000 Bank deposit interest 1,100 Irish dividend income 2,800 Profit on FA disposal 2,200 Capital grant 13,000

(29,100)

Case I adjusted trading profits 62,133 Capital allowances see (ii) (4,375)

57,758 Case I Trade

Motor car add back

Lease costs 8,100 Allowable cost restricted to:

8,100 * 24,000/49,000 3,967 Disallow 4,133

Rental Income Computation YE 31.12.07

Rental income 10,000 Expenses Interest - restricted to period from date of first letting 3,000 Repairs to roof 2,500 (5,500)

4,500

Solution to question 4 continued on next page

Taxation ll (ROI) Autumn 2008 Solutions

47

Solution to question 4 (Cont’d)

(ii) Capital Allowances Computation YE 31.12.07Car Total€ €

12.5% SLCost:Tax Cost @ 31.12.07:

Motor vehicle 24,000 Restricted

24,000

WDV 31.12.06 8,375 Additions 24,000Disposals at wdv (8,375)

24,000

W & T 2007 (3,000) 3,000 Balancing allowance below 1,375 Total capital allowances 4,375 WDV 31.12.07 21,000

Fixed asset additionsCost Tax cost

Car € € Purchased 01.09.07 30,000 24,000

30,000 24,000

Balancing allowance/charge computation€

CarDisposals @ tax wdv 8,375 Disposal proceeds (7,000) (no restriction on proceeds as cost < 22K) Balancing Allowance 1,375Note: Replacement option not relevant

(iii) Corporation tax Computation for the accounting year ended 31.12.07€

Case I Trade 57,758 Loss forward S396 (1) (22,000)

35,758 Case IV Interest received 1,100 Case V Rental income 4,500

Total Income 41,358

Chargeable Gains (adjusted) -

Total Profit 41,358

Taxable as follows :Trade & CG 35,758 @ 12.5% 4,470 Investment income 5,600 @ 25% 1,400 Corporation Tax 5,870

41,358

DIRT 1,100 @ 20.0% (220)

Corporation tax due 5,650

Taxation ll (ROI) Autumn 2008 Solutions

48

Solution to question 5 (CGT)

Patricia and PeterCapital Gain tax computation 2007 - Calculation of Gains and losses

(a) Sale of land € € €Sales Proceeds May 07 150,000 Less Disposal costs:

Selling expenses 3,000 (3,000)

147,000

Allowable Costs:Balance of cost - see below Jun 94 2,857Indexation 1.309

(3,740)Gain 143,260

Cost allocated to first disposal € cost 10,000 ratio 212,500/(212,500+85,000)% 71.43%= 7,143

Balance of cost 2,857

(b) Shares(2 separate computations are required)

Sales Proceeds Feb 07 5,000 3.30 16,500

Allowable Costs:Acquired May 01 (75,000) Loss (restricted to monetary loss) (58,500)

Sales Proceeds Feb 07 5,000 3.30 16,500

Allowable Costs:Acquired Sep 06 5,000 2.00 (10,000)Gain 6,500

(c) Painting Sales Proceeds Nov 07 10,000

Allowable Costs:Purchased Jun 92 3,000 Indexation 1.356

(4,068)

Gain 5,932

Capital Gain tax computation 2007 - Calculation of Gains and losses

(d) Building € € €Sales Proceeds Sep 07 740,000

Allowable Costs:Purchased Sep 96 650,000 Indexation 1.251

(813,150) Enhancement costs Feb 02 40,000 Indexation 1.049 (41,960)

(855,110) No loss no gain -

Solution to questionn 5 continued on next page

Taxation ll (ROI) Autumn 2008 Solutions

49

Solution to question 5 (Cont’d)

(e) Ring €Insurance Proceeds Dec 07 5,000

Allowable Costs:Acquired Jul 98 1,250Indexation 1.212

(1,515)

Gain 3,485

Patricia and Peter - Capital Gains Tax Computation 2007

Patricia Peter€ €

Farmland May 07 143,260 Shares Feb 07 Loss (58,500) Shares Feb 07 6,500 Painting Nov 07 5,932 Building Sep 07 - Ring Dec 07 3,485

Total (48,515) 149,192 Losses utilised 48,515 (48,515)

Chargeable Gains 100,677

Personal Exemption (1,270) Taxable Gains 99,407

Tax @ 20% - 19,881

Taxation ll (ROI) Autumn 2008 Solutions

50

General comment

The results were poor. The pass rate was a significant disimprovement on the figure for the corresponding examlast year but in line with results of years prior to that. Difficulties were experienced, in particular, with questions1 (compulsory Income Tax question); and question 2 multiple choice question.

A fundamental problem with many of the scripts was a lack of familiarity with the subject matter. The exam papercovers a lot of basic tax and to get good marks it is necessary to adequately study and practice all aspects of thesyllabus.

Comments on individual questions

Question 1 - Income Tax (compulsory)

The question required the calculation of the taxable amounts arising ona number of benefits in kind situations,preparation of the income tax computation and the completion of the tax return. Candidates generally handled theIncome Tax computation competently, however most had serious difficulties with the BIK aspects.

Particular issues and failings:

Failing to use the market rent as an alternative to the annual value based on the property value.Inability to calculate the motor BIK correctly and ignoring the alternative option to the high mileage relief.Regarding the medical insurance paid by the employer, very few gave a credit for the income tax paid by theemployer.Many did not realise that the P60 figure for Auric included the taxable BIK amounts. This had consequencesfor the PRSI calculation and the income tax computation. This was an important point that was missed bymany.Few were able to calculate the PRSI correctly, whether it was identifying the correct PRSI class or calculatingthe bands correctly.When calculating the CGT it was important to ignore part of the disposal costs. Most did not.

51

EXAMINERS REPORT

TAXATION ll (Republic of Ireland)

Autumn 2008

NUMBER OF CANDIDATES 227

Pass Rate 23.3%

AVERAGE MARKS PER QUESTION

IT MC VAT CT CGT

Question 1 2 3 4 5 Total

Marks available 40 20 20 20 20 100

Average % 14.9 6.5 10.8 9.2 9.2 40.8 No. attempting 220 187 158 179 151 227

% 96.9% 82.4% 69.6% 78.9% 66.5%

On the income tax computation most included the BIK amounts. This was incorrect as the amounts werealready included in the P60 figure.Many treated tuition fee as a deduction from total income instead of treating it as a tax credit.Granting the employee allowance to Auric.Not granting rent relief.Ignoring PRSI.There was a tendency to ignore the latter pages of the tax return.The requirement to state the tax filing obligations were dealt with inadequately. What was required werereturn filing dates for Income Tax and CGT. The CGT aspect was almost always ignored.

Question 2 - (Multiple Choice)

This was the usual multiple-choice question ranging over different aspects of the syllabus. The averagemark was 6.5 making it the worst answered question, nonetheless that did not diminish its popularity.

Well answered (relatively speaking)Part 8– VAT and imports.Part 6– Schedule D deduction.Part 3– Calculation of 2nd year trading profits.

Poorly answeredPart 1– CT accounting period on commencement to trade.Part 2– Close company loan.Part 7– Interest on late payment of income tax.

Question 3 - (VAT)

Part (a) required the candidates to prepare a memorandum itemising items on which a VAT input is allowed andexplaining what is meant by the expression “voluntary relatively straightforward requirements and should havebeen better answered. The weaker answers simply did not deal with the issues.

Part (b) required a VAT computation to be prepared from various pieces of information. Candidates needed toidentify the appropriate information to be utilised in their answer in respect of a trader accounting for VAT on thecash receipts basis. Generally the answers to this part were reasonable. Some candidates laid out their answerpoorly, making it difficult to see the derivation of the figures, consequently, possibly losing marks.

Common errors were: Mixing up “gross” and “net” amounts.

Not properly applying the deferred accounting procedure regarding intra EU acquisitions.

Question 4 - (Corporation Tax)

This was a standard adjusted profits, capital allowance and CT computations question. Many of the answers werereasonable, with the usual difficult areas such as capital allowances being ignored. Surprisingly, there were notmany scripts scoring high marks.

Points of difficulty were: Pension addback. Many added back the closing accrual only. It was also necessary to adjust for the openingaccrual. Motor and travel. The leasing addback had to be adjusted by reference to the cost of the car and wasfrequently ignored. Capital grant. This should be added back and no further adjustment is made. Some included incorrectly, inthe CT computation. Rental income. The interest paid relating to the acquisition of the property needed to be time apportioned tothe period the property was let and deducted from the gross rents. Irish Dividends. Frequently this was included on the CT computation, which was incorrect.

Taxation ll (ROI) Autumn 2008 Examiners Report

52

Question 5 - (CGT)

This question required the candidates to prepare the CGT computation for a number of disposals occurring withina tax year. Some disposals were universally badly handled, particularly part (b) dealing with the share disposals.Workings for this part of the question and part (a) re sale of land produced a lather of figures which were tortuousto follow. To get good marks workings must be clear.

Noteworthy points were: Part (a) sale of land. The difficulty in this part was the calculation of the cost of the land to be allocated tothe sales proceeds. Candidates needed to realise that part of the original land cost had been allocated alreadyagainst a previous sale and they needed to calculate the balance of the cost. Some candidates have difficultywith the concept of allocating costs to disposals by reference to market values, and with this addedcomplication, produced some very confused answers. Sale of shares. The key here was to realise that sales of shares which were originally acquired at differentdates are treated as separate disposals and separate computations are required. Insurance and engagement ring. Many thought that this was not taxable. The ring is a “wasting chattel” isonly exempt when the disposal proceeds do not exceed €2,540.

Taxation ll (ROI) Autumn 2004 Paper

53