Embed Size (px)

Citation preview

The Insolvency and Bankruptcy Code, 2016Evolving Dynamics

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 1

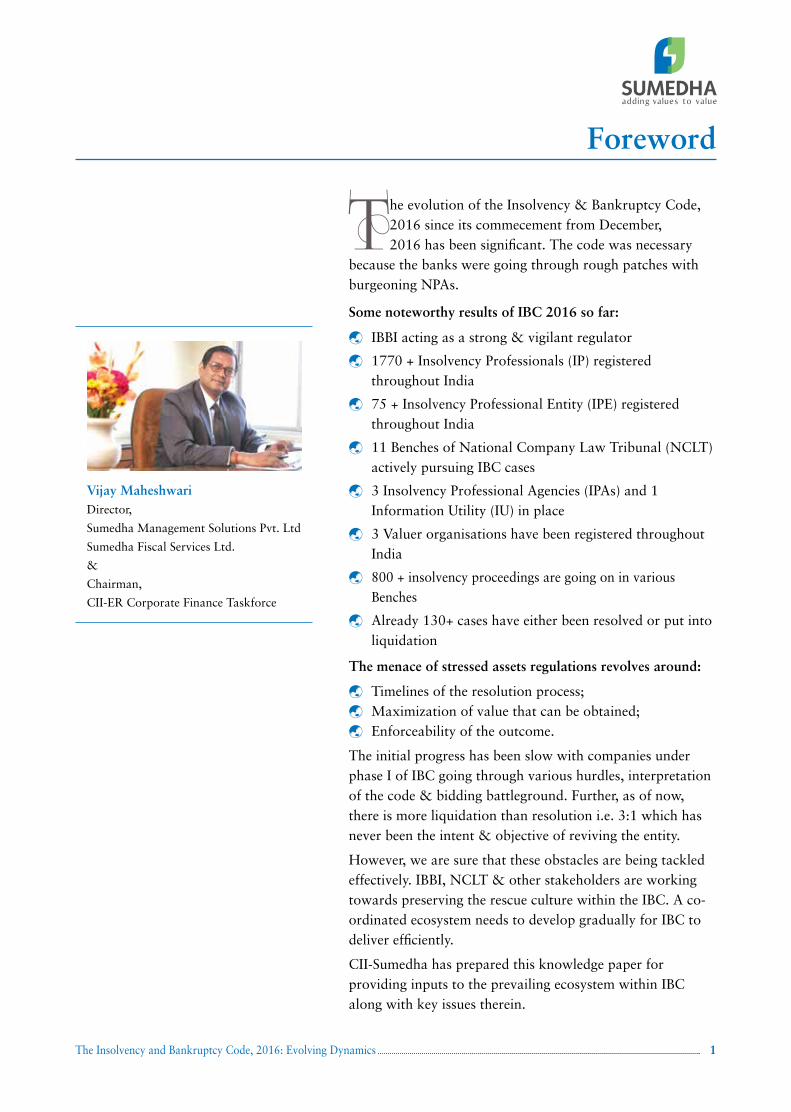

Foreword

1

The evolution of the Insolvency & Bankruptcy Code, 2016 since its commecement from December, 2016 has been significant. The code was necessary

because the banks were going through rough patches with burgeoning NPAs.

Some noteworthy results of IBC 2016 so far:

IBBI acting as a strong & vigilant regulator

1770 + Insolvency Professionals (IP) registered throughout India

75 + Insolvency Professional Entity (IPE) registered throughout India

11 Benches of National Company Law Tribunal (NCLT) actively pursuing IBC cases

3 Insolvency Professional Agencies (IPAs) and 1 Information Utility (IU) in place

3 Valuer organisations have been registered throughout India

800 + insolvency proceedings are going on in various Benches

Already 130+ cases have either been resolved or put into liquidation

The menace of stressed assets regulations revolves around:

Timelines of the resolution process; Maximization of value that can be obtained; Enforceability of the outcome.

The initial progress has been slow with companies under phase I of IBC going through various hurdles, interpretation of the code & bidding battleground. Further, as of now, there is more liquidation than resolution i.e. 3:1 which has never been the intent & objective of reviving the entity.

However, we are sure that these obstacles are being tackled effectively. IBBI, NCLT & other stakeholders are working towards preserving the rescue culture within the IBC. A co-ordinated ecosystem needs to develop gradually for IBC to deliver efficiently.

CII-Sumedha has prepared this knowledge paper for providing inputs to the prevailing ecosystem within IBC along with key issues therein.

Vijay Maheshwari Director,

Sumedha Management Solutions Pvt. Ltd

Sumedha Fiscal Services Ltd.

&

Chairman,

CII-ER Corporate Finance Taskforce

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics2

Contents

The Insolvency and Bankruptcy Code, 2016 3

Revisiting the code 6

The Code evaluation 8

Stress in the banking system 10

A revised framework for the resolution of stressed assets 14

A handful of resolutions 17

More liquidation than resolution 19

Important amendments suggested by Insolvency Law Committee in IBC Code 24

Operational Creditors are worse off 28

Top NCLT Cases 32

Selected Judgements 43

Annexures 48

Bibliography 52

Glossary 53

About CII 54

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 3

The Insolvency and Bankruptcy Code, 2016

The Insolvency and Bankruptcy Code, 2016

(the code, IBC) has been one of the biggest

economic reforms in India in recent

times. The code was formed with the following

objectives:

To balance the interest of all stakeholders by

consolidating and amending the existing laws

relating to insolvency and bankruptcy;

To promote entrepreneurship;

To make credit available;

To reduce the time of resolution for

maximizing the value of assets;

Highlights of the code

The Code brings a paradigm shift from

“Debtors in possession” to “Creditors in

Control”

Insolvency test moved from “erosion of net

worth” to “payment default”

Single insolvency and bankruptcy framework.

It replaces/modifies/amends certain existing

laws

Time-bound resolution process at each stage

Establishment of Insolvency and Bankruptcy

Board-a regulator as an independent body

A clearly defined distribution of recovery

proceeds

Insolvency Professional to take over

management and control of the Corporate

Debtor

Government dues would rank below the

claims of other creditors

Have provisions to deal with concealment,

fraud and /or manipulation leading to fine

and/or imprisonment

Provide confidence to Lenders and Investors

in the debt market

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics4

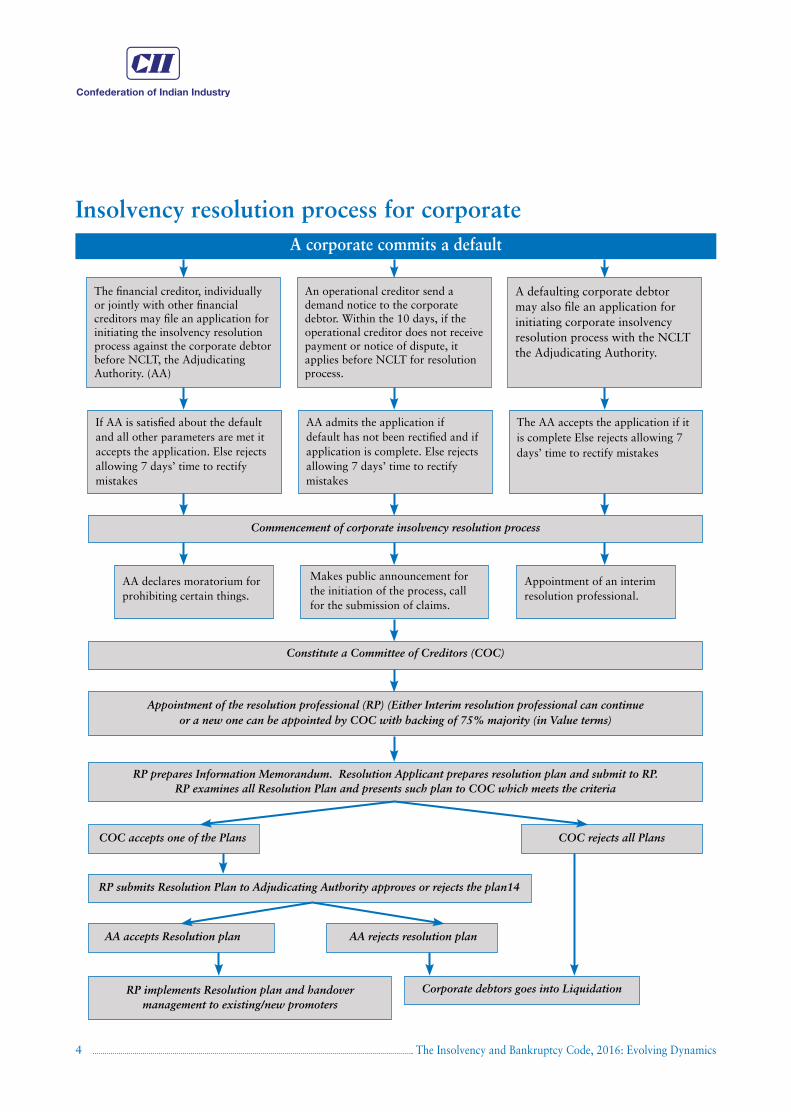

A corporate commits a default

The financial creditor, individually or jointly with other financial creditors may file an application for initiating the insolvency resolution process against the corporate debtor before NCLT, the Adjudicating Authority. (AA)

If AA is satisfied about the default and all other parameters are met it accepts the application. Else rejects allowing 7 days’ time to rectify mistakes

AA declares moratorium for prohibiting certain things.

Appointment of an interim resolution professional.

Makes public announcement for the initiation of the process, call for the submission of claims.

Commencement of corporate insolvency resolution process

Constitute a Committee of Creditors (COC)

COC accepts one of the Plans

AA accepts Resolution plan

RP implements Resolution plan and handover management to existing/new promoters

AA rejects resolution plan

Corporate debtors goes into Liquidation

RP submits Resolution Plan to Adjudicating Authority approves or rejects the plan14

COC rejects all Plans

RP prepares Information Memorandum. Resolution Applicant prepares resolution plan and submit to RP. RP examines all Resolution Plan and presents such plan to COC which meets the criteria

Appointment of the resolution professional (RP) (Either Interim resolution professional can continue or a new one can be appointed by COC with backing of 75% majority (in Value terms)

AA admits the application if default has not been rectified and if application is complete. Else rejects allowing 7 days’ time to rectify mistakes

The AA accepts the application if it is complete Else rejects allowing 7 days’ time to rectify mistakes

An operational creditor send a demand notice to the corporate debtor. Within the 10 days, if the operational creditor does not receive payment or notice of dispute, it applies before NCLT for resolution process.

A defaulting corporate debtor may also file an application for initiating corporate insolvency resolution process with the NCLT the Adjudicating Authority.

Insolvency resolution process for corporate

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 5

Liquidation

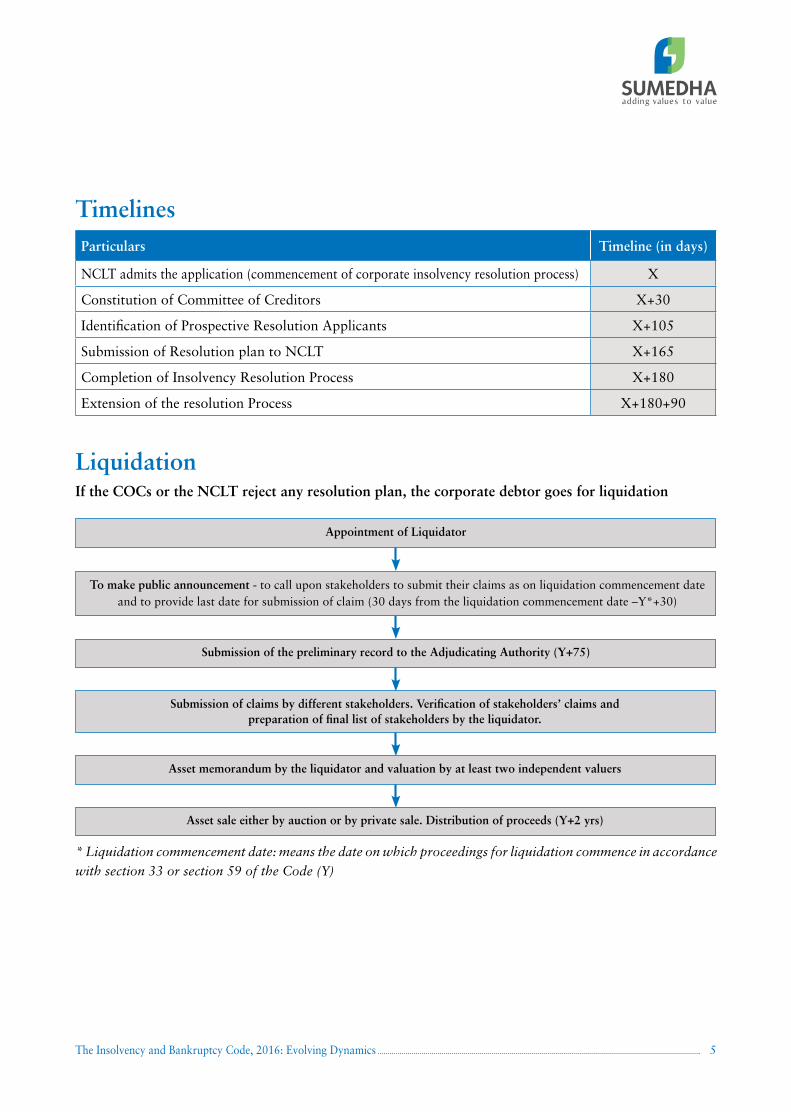

TimelinesParticulars Timeline (in days)

NCLT admits the application (commencement of corporate insolvency resolution process) X

Constitution of Committee of Creditors X+30

Identification of Prospective Resolution Applicants X+105

Submission of Resolution plan to NCLT X+165

Completion of Insolvency Resolution Process X+180

Extension of the resolution Process X+180+90

If the COCs or the NCLT reject any resolution plan, the corporate debtor goes for liquidation

Appointment of Liquidator

Submission of the preliminary record to the Adjudicating Authority (Y+75)

Submission of claims by different stakeholders. Verification of stakeholders’ claims and preparation of final list of stakeholders by the liquidator.

Asset memorandum by the liquidator and valuation by at least two independent valuers

Asset sale either by auction or by private sale. Distribution of proceeds (Y+2 yrs)

To make public announcement - to call upon stakeholders to submit their claims as on liquidation commencement date and to provide last date for submission of claim (30 days from the liquidation commencement date –Y*+30)

* Liquidation commencement date: means the date on which proceedings for liquidation commence in accordance

with section 33 or section 59 of the Code (Y)

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics6

Revisiting the code

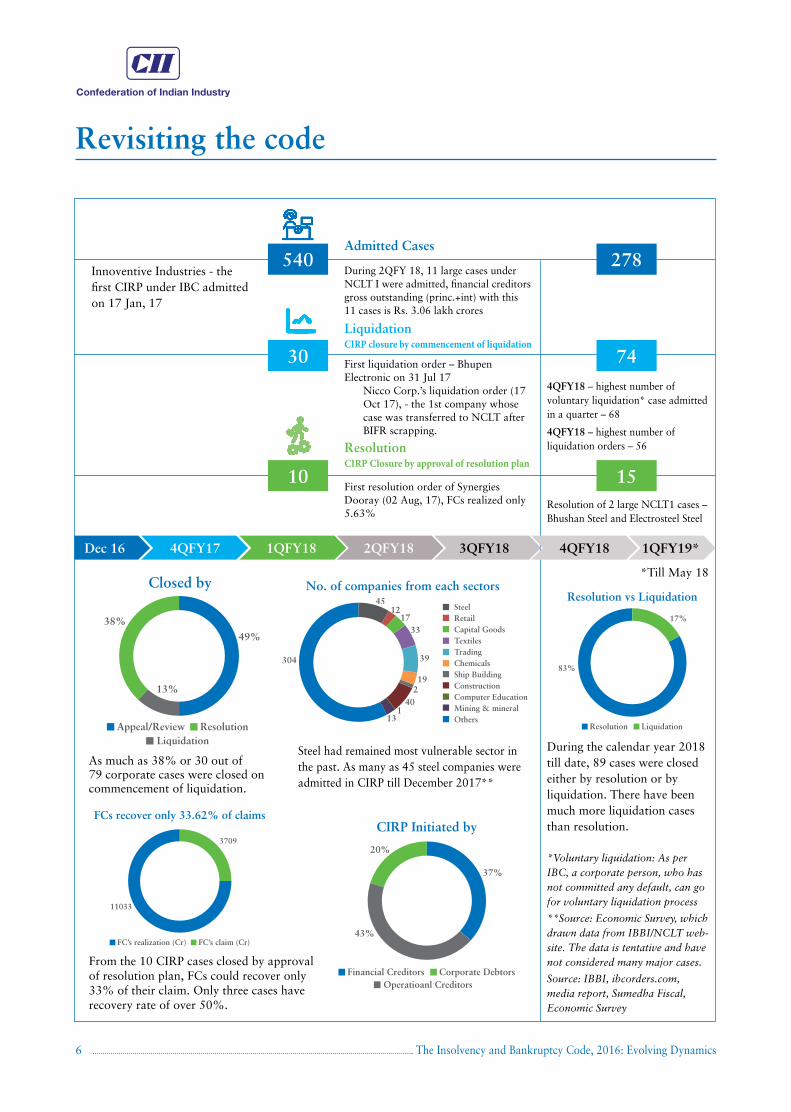

Innoventive Industries - the first CIRP under IBC admitted on 17 Jan, 17

As much as 38% or 30 out of 79 corporate cases were closed on commencement of liquidation.

From the 10 CIRP cases closed by approval of resolution plan, FCs could recover only 33% of their claim. Only three cases have recovery rate of over 50%.

Steel had remained most vulnerable sector in the past. As many as 45 steel companies were admitted in CIRP till December 2017**

During the calendar year 2018 till date, 89 cases were closed either by resolution or by liquidation. There have been much more liquidation cases than resolution.

*Till May 18

*Voluntary liquidation: As per IBC, a corporate person, who has not committed any default, can go for voluntary liquidation process

**Source: Economic Survey, which drawn data from IBBI/NCLT web-site. The data is tentative and have not considered many major cases.

Source: IBBI, ibcorders.com, media report, Sumedha Fiscal, Economic Survey

540

30

Dec 16 4QFY17 1QFY18 2QFY18 3QFY18 4QFY18 1QFY19*

10

278

74

15

During 2QFY 18, 11 large cases under NCLT I were admitted, financial creditors gross outstanding (princ.+int) with this 11 cases is Rs. 3.06 lakh crores

First liquidation order – Bhupen Electronic on 31 Jul 17

Nicco Corp.’s liquidation order (17 Oct 17), - the 1st company whose case was transferred to NCLT after BIFR scrapping.

4QFY18 – highest number of voluntary liquidation* case admitted in a quarter – 68

4QFY18 – highest number of liquidation orders – 56

Resolution of 2 large NCLT1 cases – Bhushan Steel and Electrosteel Steel

First resolution order of Synergies Dooray (02 Aug, 17), FCs realized only 5.63%

LiquidationCIRP closure by commencement of liquidation

Admitted Cases

ResolutionCIRP Closure by approval of resolution plan

Closed by

38%

49%

13%

Appeal/Review ResolutionLiquidation

Resolution vs Liquidation

83%

17%

Resolution Liquidation

FCs recover only 33.62% of claims

3709

11033

FC’s realization (Cr) FC’s claim (Cr)

CIRP Initiated by

20%

43%

37%

Financial Creditors Corporate DebtorsOperatioanl Creditors

No. of companies from each sectors

304

45 1245

1733

39

19

40

131

2

SteelRetailCapital GoodsTextilesTradingChemicalsShip BuildingConstructionComputer EducationMining & mineralOthers

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 7

900

162

116

140

234

12838

656

800700600500400300200100

04QFY17 1QFY18 2QFY18 3QFY18 4QFY18 1QFY19*

CIRP Cases admitted

120

100

80

60

40

20

0

18

8656

23

7004QFY17 1QFY18 2QFY18 3QFY18 4QFY18 1QFY19*

Closed by liquidation

IPs registered with IPA

150

582

1058

ICAI (CA) ICAI (Cost Accountants) ICSA (CS)

30

25

20

15

10

5

0

4

21

11

8

2004QFY17 1QFY18 2QFY18 3QFY18 4QFY18 1QFY19*

Closed by resolution

900

162

116

140

234

12838

656

800700600500400300200100

04QFY17 1QFY18 2QFY18 3QFY18 4QFY18 1QFY19*

Voluntary Liquidation Cases

2000

1600

1200

800

400

0Mar 17 Sep 17 Dec 17 May 18

IPs registration trend

ICAI (CA) ICSA (CS)ICAI (Cost Accountants)

*Till May 18

Source: IBBI, MCA, SBI, Sumedha

NCLT BenchesNew Delhi Principal Bench

Delhi Ahmedabad Allahabad Bengaluru Chandigarh Chennai Guwahati Hyderabad Kolkata Mumbai

Delhi Rajasthan

Gujarat MP

UP Uttarkhand

Karnataka HP J&K Punjab Haryana

Tamil Nadu Puducherry Kerala Lakshadweep

Entire North East

Telangana AP

WB Andaman Bihar Jharkhand Odisha

Maharashtra Goa Chhattisgarh

Active Companies 247204

Active Companies 84101

Active Companies 73118

Active Companies 65519

Active Companies 60375

Active Companies 106677

Active Companies 8047

Active Companies 88855

Active Companies 179227

Active Companies 238030

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics8

14 days periodAs per the section 7, 9 and 10 of the IBC, the NCLT shall admit or reject an application

for initiating insolvency proceedings within 14 days of filing. However, in many cases, it

has exceeded the 14-day timeline. In the case of Surendra Trading Company vs. J K Jute

Mills Company Ltd, NCLAT says that the 14-day timeline is an indicative period rather

than mandatory. The NCLT doesn’t have to adhere to this deadline.

Constitutional validityThere have been numerous petitions regarding the constitutional validity of the

Insolvency and Bankruptcy Code, 2016 or the National Company Law Tribunal in

different High Courts. However, in all the cases, the judgements have gone against the

petitioners and their appeals have not impacted the process. For example, in case of

Shivam Water Treaters Pvt Ltd vs. Union of India and Ors (SLP No.1740/2018), the

Supreme Court advised the High Court of Gujarat not to enter into the debate around

the constitutional validity of the IBC or the constitutional validity of NCLT. The

Supreme Court issued a notice to the Central Government in a petition challenging the

vires of various provisions of the IBC and, has prayed to declare Section 3(12), 5(7),

6, 7, 12, 29, 62, 214(f), 231 and 238 of the code as ultra vires of the Constitution of

India, 1950.

Extension of 270 days periodAs per the IBC, the resolution plan has to be finalized and approved within 270 days

from its admission to NCLT. However, there are few cases where NCLT has given

relaxation based on certain grounds. For example, in the case of Deccan Chronicle, the

NCLT has given an additional 87 days relaxation beyond 270-day initial deadline on

account of deducting the litigation period. The NCLT has similarly given extension in

other cases like KSS Petron, Mack Soft as well.

Promoters and disquieted applicants approaching courtsDuring the resolution approval stage, defaulting promoters, resolution applicants,

other stakeholders and sometimes unrelated parties have delayed the process by

pursuing legal option. In the case of Bhushan Steel the litigation made by Liberty

House or in the case of Electrosteel Steel litigation made by Renaissance ultimately

delayed the resolution process.

Decoding the basis of bidsIn certain cases, the NCLT ordered lenders to consider fresh bids offered by

unsuccessful resolution applicants. The court also allowed the erstwhile top bidder to

The code evolution

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 9

offer competitive bid under the process. For example, in the case of Binani Cement,

the Kolkata bench of NCLT has ordered the RP to accept the revised bid offered by

Ultratech Cement, which has not been the top bidder. The bid offered by a consortium

of Dalmia Cement, Piramal Enterprise and Bain Capital has been considered as top bid

by CoCs.

Status of personal guarantee/corporate guaranteeUnder IBC, the financial creditors can invoke personal guarantees calling upon the

guarantor to pay the debts of the debtors for which they stood surety in spite of the

fact that the corporate insolvency resolution process is still pending. On analysis of

Section 5(7) and 5(8) of IBC, 2016 along with Section 128, 140 and 141 of the Indian

Contract Act, 1872, it becomes clear that on payment of debt to financial creditors,

the surety steps into their shoes. He is entitled to recover from the principal debtor

any amount paid on his behalf and also gets the benefit of every security to which

the creditor was entitled to. It is worthwhile to mention here that although personal

guarantees can be invoked by financial creditors, personal assets of guarantors

cannot be liquidated during the moratorium period, in companies facing corporate

insolvency resolution process under IBC as decided in a landmark case of SBI against V

Ramakrishnan (Director as well as personal guarantor for Veesons Energy Systems).

Applicability of Limitation Act, 1963 to IBCLimitation Act, 1963 and/or the Schedule to it is applicable to the petitions filed under

the provisions of IBC, 2016 in view of Section 60 and 179 IBC, 2016 and Section

433 of the Companies Act, 2017. The period of limitation and the period from when

it starts shall be based on the description of the suit. However, there is a provision in

Section 238 in IBC, 2016 which enables the Code to override the other laws. In the

case of Deem Roll-Tech Ltd vs R.L Steel & Energy Ltd, the Principal Bench suggested

that the period of limitation would be applicable as the operational creditor’s claim

was barred by limitation and was made after the expiry of the period of three years.

In a contrast judgement, NCLAT in the case of M/s. Speculum Plast Pvt. Ltd. vs. PTC

Techno Pvt. Ltd. held by the Limitation Act shall not apply to IBC. However, the

NCLT may take into account the doctrine of laches while considering an application

for initiating the insolvency process.

We are sure that the code would evolve in maximization of value and amendment in

IBC code is round the corner to clear certain doubts.

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics10

Stress in the banking system

As bad loan near Rs. 9.5 lakh crore, the last

few years have not been good for the banking

sector in India. 19 out of 21 state-run

banks have reported losses in FY 2018. The

combined loss of these banks during 4QFY18

stand at Rs. 63117 crores.

The average NPA ratio for PSU banks has

shot up to 14.5%. The NPA of UCO Bank,

IOB and IDBI Bank is above 25%. The NPA

ratio for the banking sector as a whole is

12.1% at the end of FY 2018

The cumulative loss of PSU Banks during FY

2018 has exceeded the government’s capital

infusion on them during the year.

The reported CET 1 of six banks is lower

than the rate stipulated by the regulator.

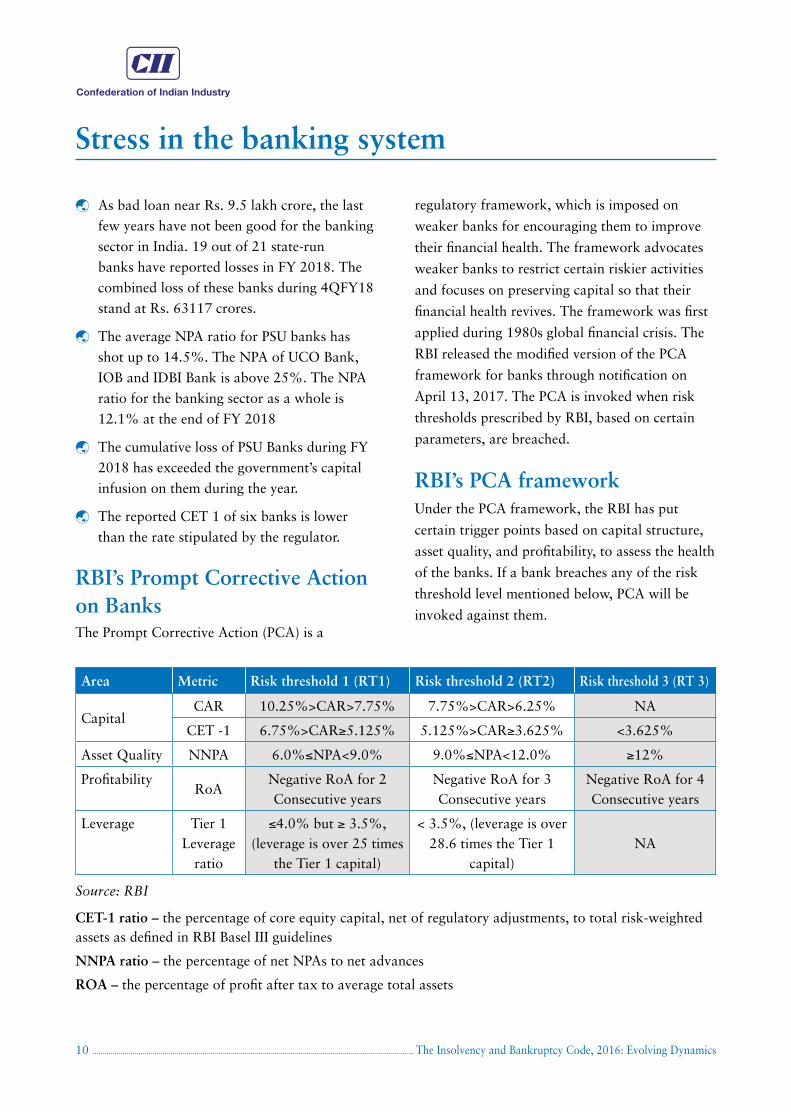

RBI’s Prompt Corrective Action on BanksThe Prompt Corrective Action (PCA) is a

regulatory framework, which is imposed on

weaker banks for encouraging them to improve

their financial health. The framework advocates

weaker banks to restrict certain riskier activities

and focuses on preserving capital so that their

financial health revives. The framework was first

applied during 1980s global financial crisis. The

RBI released the modified version of the PCA

framework for banks through notification on

April 13, 2017. The PCA is invoked when risk

thresholds prescribed by RBI, based on certain

parameters, are breached.

RBI’s PCA frameworkUnder the PCA framework, the RBI has put

certain trigger points based on capital structure,

asset quality, and profitability, to assess the health

of the banks. If a bank breaches any of the risk

threshold level mentioned below, PCA will be

invoked against them.

Area Metric Risk threshold 1 (RT1) Risk threshold 2 (RT2) Risk threshold 3 (RT 3)

CapitalCAR 10.25%>CAR>7.75% 7.75%>CAR>6.25% NA

CET -1 6.75%>CAR≥5.125% 5.125%>CAR≥3.625% <3.625%

Asset Quality NNPA 6.0%≤NPA<9.0% 9.0%≤NPA<12.0% ≥12%

ProfitabilityRoA

Negative RoA for 2 Consecutive years

Negative RoA for 3 Consecutive years

Negative RoA for 4 Consecutive years

Leverage Tier 1 Leverage

ratio

≤4.0% but ≥ 3.5%, (leverage is over 25 times

the Tier 1 capital)

< 3.5%, (leverage is over 28.6 times the Tier 1

capital)NA

Source: RBI

CET-1 ratio – the percentage of core equity capital, net of regulatory adjustments, to total risk-weighted assets as defined in RBI Basel III guidelines

NNPA ratio – the percentage of net NPAs to net advances

ROA – the percentage of profit after tax to average total assets

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 11

Restrictions

11 PSU banks placed under PCA framework

Mandatory Restriction on dividend (RT1+RT2+RT3)

Capital infusion by promoters/owners/parent in case of foreign banks

(RT1+RT2+RT3)

Restriction on branch expansion (R2+R3)

To make a higher provisions as a part of coverage regime (R2+R3)

Restriction on management compensation and directors’ fees as applicable (R3)

Discretionary Curbs on lending and deposits

Special audit/inspections

Restriction on investment in subsidiaries/associates

Restriction on business line expansion, staff expansion

Restriction on capital expenditure (other than technology upgradation)

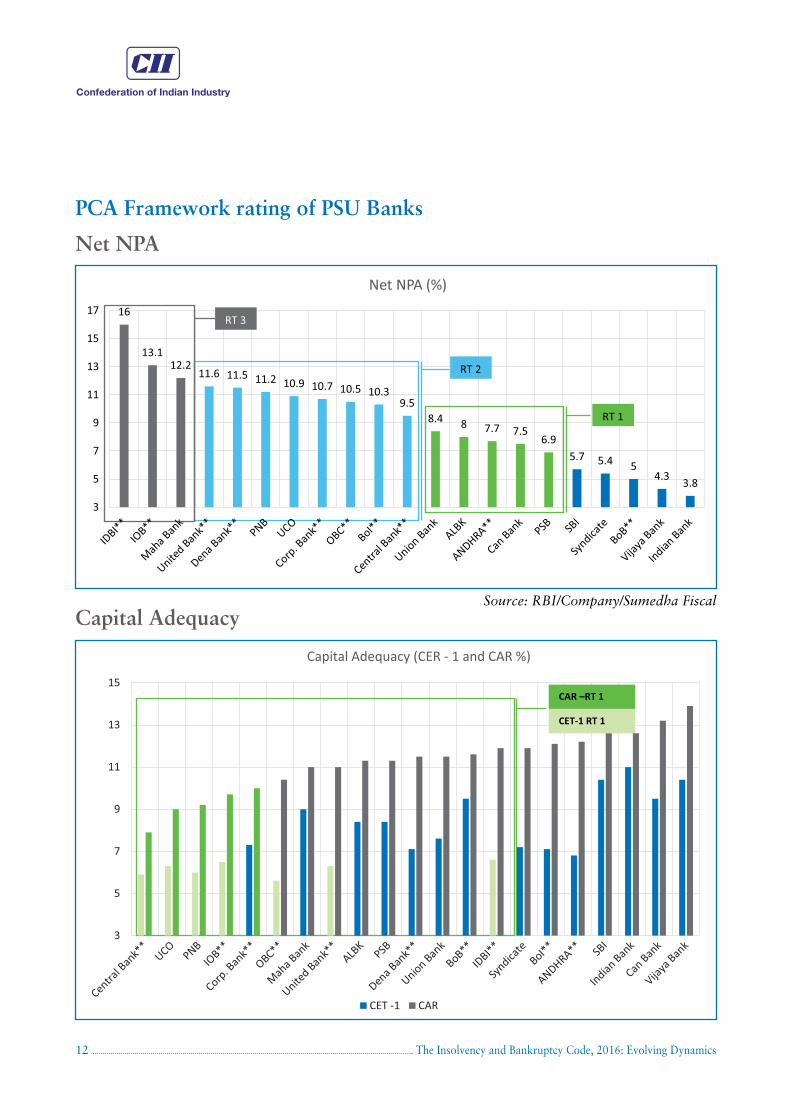

As per the latest position, 11 banks are already under PCA framework, as they have breached at least two of the top three conditions (capital, asset quality and profitability). Further, few banks have already breached one of the three conditions. Based on the current stress in the system and applicability of the revised framework for stressed assets resolution, they may be under PCA within the next few quarters.

No. PCA Banks No. Potential PCA No. Relatively Strong1 Bank of India 1 PNB 1 SBI

2 IDBI Bank 2 Canara Bank 2 Bank of Baroda

3 Central Bank 3 Union Bank 3 Indian Bank

4 I O B 4 Andhra Bank 4 Vijaya Bank

5 Oriental Bank 5 Pun. & Sind Bank 5 Syndicate Bank

6 Allahabad Bank

7 Corporation Bank

8 UCO Bank

9 Bank of Maharashtra

10 Dena Bank

11 United Bank

Source: RBI/Company/Sumedha Fiscal

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics12

PCA Framework rating of PSU Banks

Net NPA

Capital Adequacy

3

5

7

9

11

13

15

17

Net NPA (%)

16

13.112.2

11.6 11.5 11.2 10.9 10.7 10.5 10.39.5

8.4 8 7.7 7.56.9

5.7 5.4 54.3

3.8

RT 3

RT 2

RT 1

3

5

7

9

11

13

15

Capital Adequacy (CER - 1 and CAR %)

CET -1 CAR

CAR –RT 1

CET-1 RT 1

Source: RBI/Company/Sumedha Fiscal

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 13

Profitability

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

RoA (%)

FY15 FY16 FY17 FY18

RT 3

RT 2

RT 1

** Based on 9MFY 18 results and annualized thereon Source: Company/RBI/Sumedha

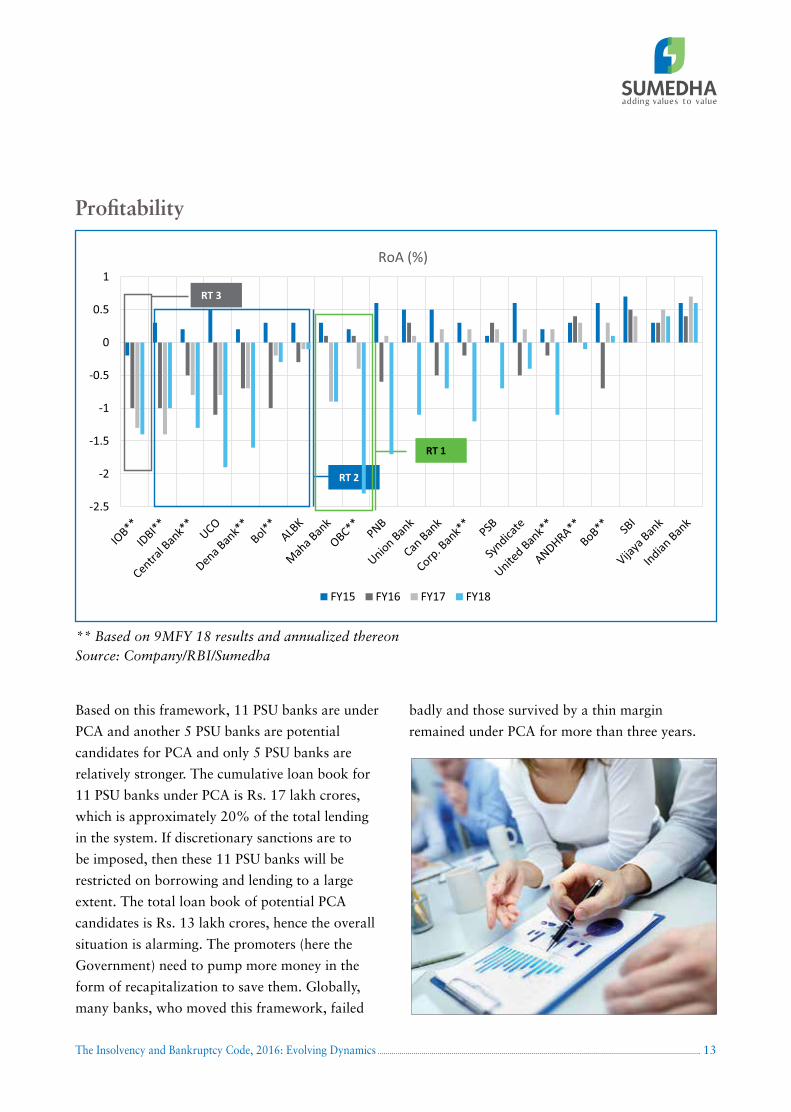

Based on this framework, 11 PSU banks are under

PCA and another 5 PSU banks are potential

candidates for PCA and only 5 PSU banks are

relatively stronger. The cumulative loan book for

11 PSU banks under PCA is Rs. 17 lakh crores,

which is approximately 20% of the total lending

in the system. If discretionary sanctions are to

be imposed, then these 11 PSU banks will be

restricted on borrowing and lending to a large

extent. The total loan book of potential PCA

candidates is Rs. 13 lakh crores, hence the overall

situation is alarming. The promoters (here the

Government) need to pump more money in the

form of recapitalization to save them. Globally,

many banks, who moved this framework, failed

badly and those survived by a thin margin

remained under PCA for more than three years.

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics14

A revised framework for resolution of stressed assets

The Reserve Bank of India vides its circular

on 12th February 2018, has set a new

framework for the resolution of stressed

assets in the banking system. The framework

has been set with an objective of early detection

of stressed assets and immediate action thereon,

which is in synchronization with the Insolvency

and Bankruptcy Code, 2016. With this new

framework, all existing schemes like CDR, JLF,

SDR, and S4A has been officially dismantled.

All such mechanisms have hardly produced any

fruitful outcomes so far and bad loans in the

banking system have been growing at an alarming

rate. With this rule, NPA recognition will be

simplified and will be done in a transparent

manner.

Lenders, like all scheduled commercial banks and

all India Financial Institutions, shall identify initial

stress on loan accounts immediately on non-

payment of debts (principal or interest or both)

for more than 30 days. These accounts should be

classified as ‘Special Mentioned Accounts (SMA)’

based on a number of days overdue.

Early identification

Key Features

Early IdentificationIdentification of stress accounts immediately on non-payment of debt for more for than 30 days

Monitoring Weekly (accounts in default with exposure Rs. 5 crore and above) and monthly (accounts with exposure Rs. 5 crore +) reporting of credit information to CRILC

ResolutionsResolution on a time-bound manner either through regularisation of the accounts, sale of the exposure by creditors or restructuring

To be referred to the IBC (Rs. 2000 crore or above accounts)If the resolution plans not implemented within the timeline then lenders shall file insolvency application under IBC.

SMA 0

(1-30 days overdue)

SMA 2

(61-90 days overdue)

SMA 1

(31-60 days overdue)

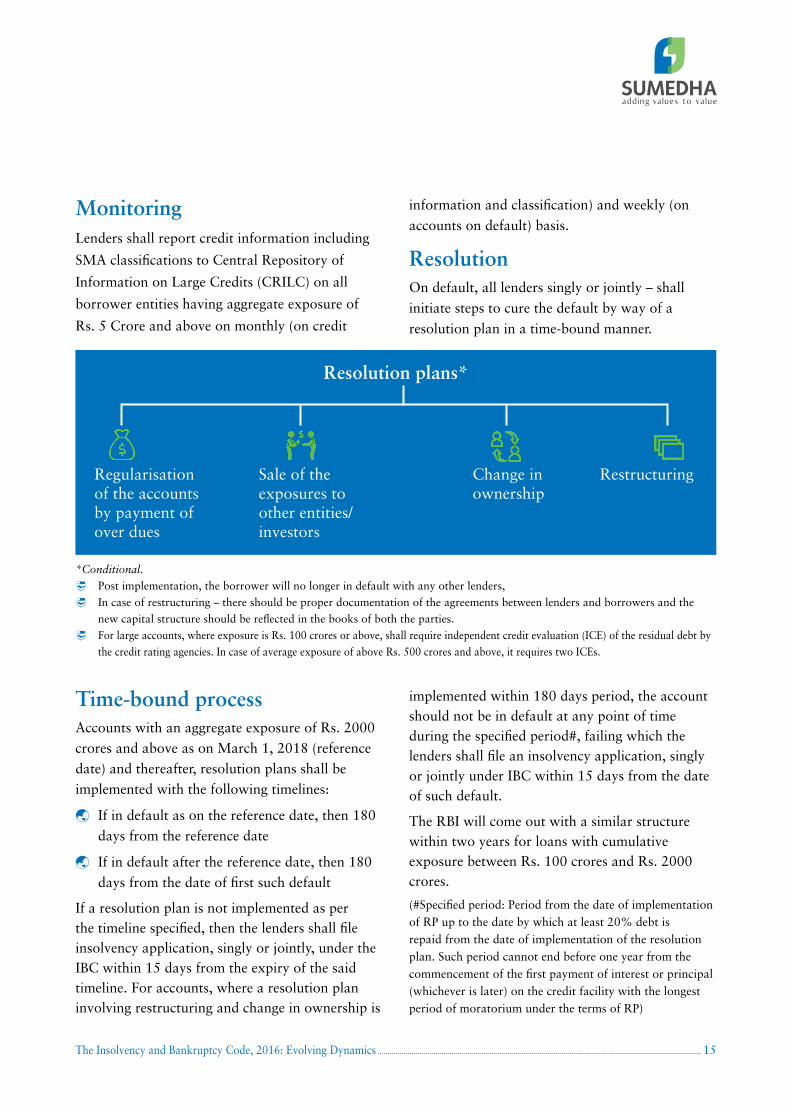

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 15

MonitoringLenders shall report credit information including

SMA classifications to Central Repository of

Information on Large Credits (CRILC) on all

borrower entities having aggregate exposure of

Rs. 5 Crore and above on monthly (on credit

information and classification) and weekly (on

accounts on default) basis.

Resolution On default, all lenders singly or jointly – shall

initiate steps to cure the default by way of a

resolution plan in a time-bound manner.

Time-bound processAccounts with an aggregate exposure of Rs. 2000

crores and above as on March 1, 2018 (reference

date) and thereafter, resolution plans shall be

implemented with the following timelines:

If in default as on the reference date, then 180

days from the reference date

If in default after the reference date, then 180

days from the date of first such default

If a resolution plan is not implemented as per the timeline specified, then the lenders shall file insolvency application, singly or jointly, under the IBC within 15 days from the expiry of the said timeline. For accounts, where a resolution plan involving restructuring and change in ownership is

implemented within 180 days period, the account should not be in default at any point of time during the specified period#, failing which the lenders shall file an insolvency application, singly or jointly under IBC within 15 days from the date of such default.

The RBI will come out with a similar structure within two years for loans with cumulative exposure between Rs. 100 crores and Rs. 2000 crores.

(#Specified period: Period from the date of implementation of RP up to the date by which at least 20% debt is repaid from the date of implementation of the resolution plan. Such period cannot end before one year from the commencement of the first payment of interest or principal (whichever is later) on the credit facility with the longest period of moratorium under the terms of RP)

Resolution plans*

Regularisation of the accounts by payment of over dues

Sale of the exposures to other entities/investors

Change in ownership

Restructuring

*Conditional.

Post implementation, the borrower will no longer in default with any other lenders, In case of restructuring – there should be proper documentation of the agreements between lenders and borrowers and the

new capital structure should be reflected in the books of both the parties. For large accounts, where exposure is Rs. 100 crores or above, shall require independent credit evaluation (ICE) of the residual debt by

the credit rating agencies. In case of average exposure of above Rs. 500 crores and above, it requires two ICEs.

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics16

Strict regulation

Needs banks to downgrade loan first to NPA before implementing the resolution

Time-bound process – needs to resolute within 180 days otherwise refer to IBC (for Rs. 2000 crore and above exposure)

Stringent upgrade norm – will be upgraded only if a minimum 20% debt is repaid from the date of implementation. Earlier upgrade is possible after one year of good performance

Independent credit evaluation by credit rating agencies before resolution if the loan amount is Rs. 100 crores and above

The immediate impact of this rule will be a sudden

jump in NPA in the banking system in the next few

quarters. As per the different media and brokerage

reports, assets under various dispensations is

between Rs. 2.5 and 3 lakh crores, out of which

30-35% would be converted into NPA. So, expected

slippage would be around Rs. 0.65 – 0.90 lakh

crores during the Q4FY18 and 1QFY19.

For banks, the resolution of such huge NPA accounts would be an enormous job within the stipulated timeframe of 180 days. So many large accounts, where cumulative exposure is Rs. 2000 crores and above would be referred to IBC in the

next 3-4 quarters.

Impact

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 17

Resolution of corporate debtor is said to be

the sole of the IBC, however, the outcome

of closed cases till date shows a different

picture. During the first one year of IBC, only 10

cases were closed by approval of proper resolution

plan, as against 30 companies which had gone for

liquidation, i.e. ratio of firms facing liquidation

to resolution is 3:1. The ratio worsened during

the calendar year 2018 to 5:1. Few companies

admitted under CIRP, have been struggling since the

past few years, so for them, liquidation is almost

inevitable. Till date, 25 CIRP cases were closed after

resolution plans were approved. Among 25 cases

of resolution, 5 cases were reported each from steel

and engineering sector and two each from the auto

component, infra, and hotels respectively.

Synergy Dooray was the first company to

be resolved under the IBC. During 1st year,

the recovery rate in 10 resolution cases was

as low as 33.62%. The resolution case of

Trinity Auto Components was unique in

the sense the financial creditor Axis Bank

extended credit limit to the corporate

debtor rather going for recovery. In case

of MBL Infrastructure, the resolution plan

submitted by the promoter was accepted by

the CoCs.

A handful of resolutions

18

8 8

9

7

BIFR Non BIFR Operational Creditors

Corporate Debtors

Financial Creditors

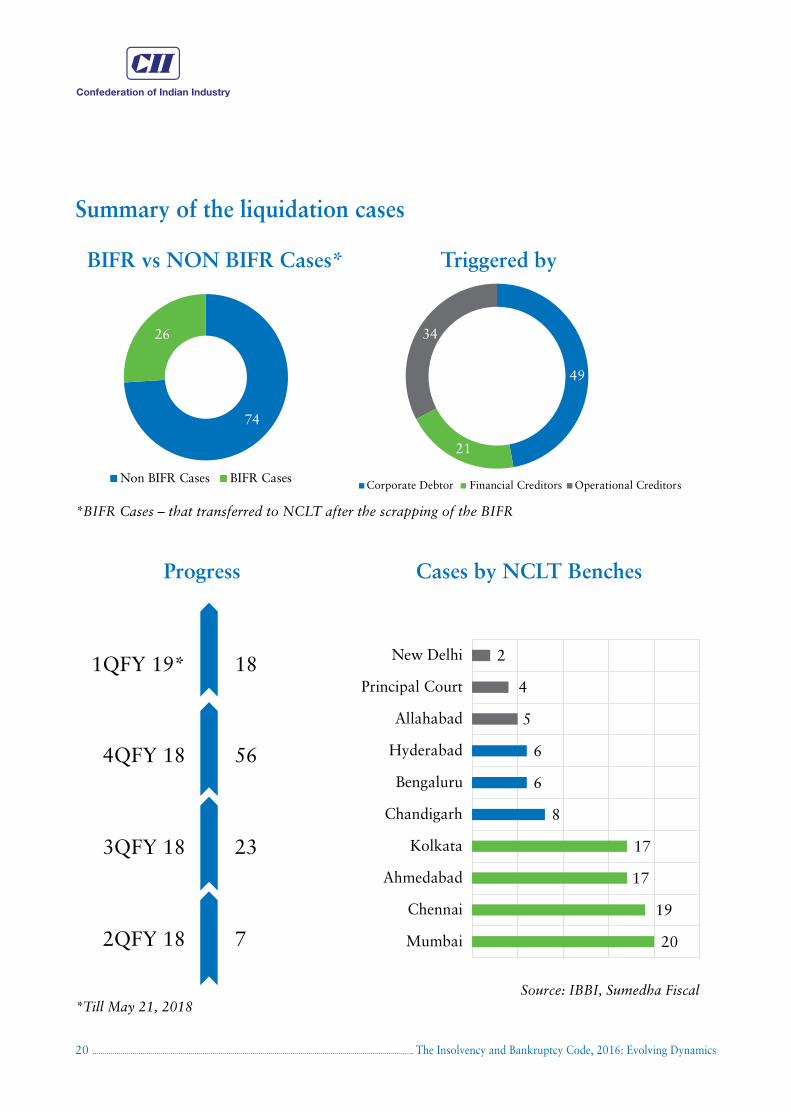

BIFR vs NON BIFR Cases* Triggered by

*BIFR Cases – that transferred to NCLT after the scrapping of the BIFR

5

5

22

2

10

Engineering

Steel

Auto Compoent

Infrastructure

Hotels

Others

Resolution by sectors

Source: IBBI, Sumedha Fiscal

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics18

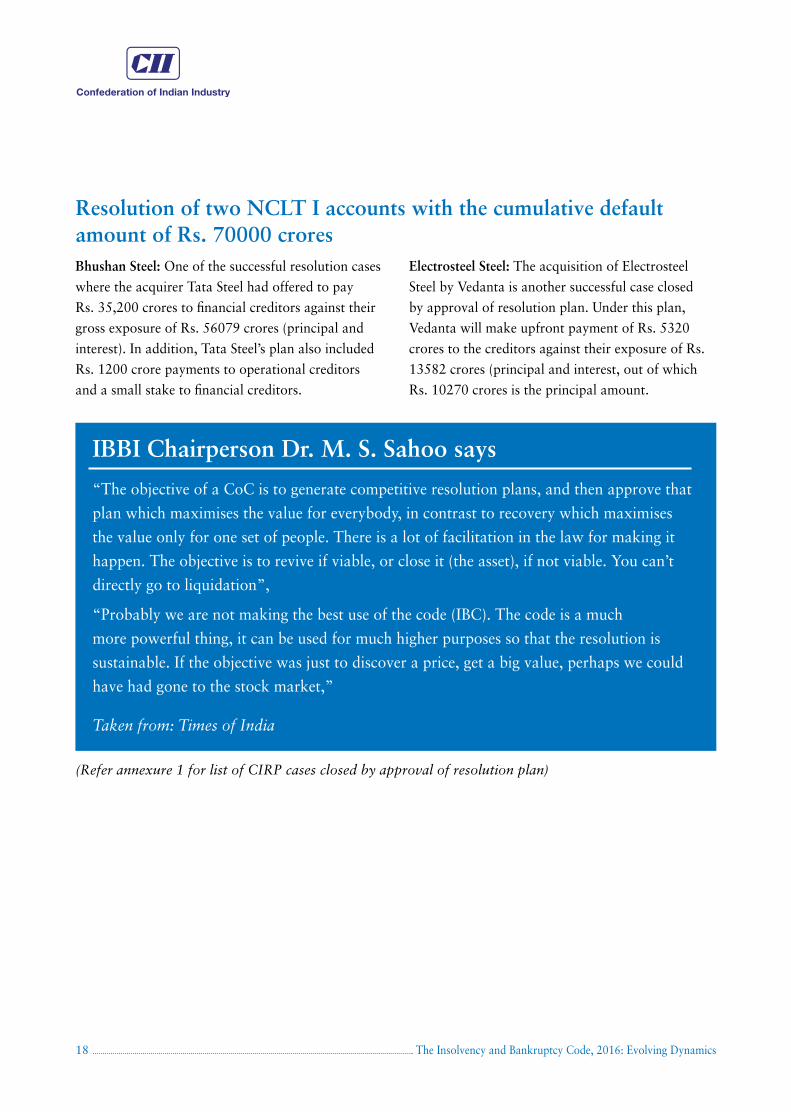

Bhushan Steel: One of the successful resolution cases

where the acquirer Tata Steel had offered to pay

Rs. 35,200 crores to financial creditors against their

gross exposure of Rs. 56079 crores (principal and

interest). In addition, Tata Steel’s plan also included

Rs. 1200 crore payments to operational creditors

and a small stake to financial creditors.

Electrosteel Steel: The acquisition of Electrosteel

Steel by Vedanta is another successful case closed

by approval of resolution plan. Under this plan,

Vedanta will make upfront payment of Rs. 5320

crores to the creditors against their exposure of Rs.

13582 crores (principal and interest, out of which

Rs. 10270 crores is the principal amount.

Resolution of two NCLT I accounts with the cumulative default amount of Rs. 70000 crores

IBBI Chairperson Dr. M. S. Sahoo says

“The objective of a CoC is to generate competitive resolution plans, and then approve that

plan which maximises the value for everybody, in contrast to recovery which maximises

the value only for one set of people. There is a lot of facilitation in the law for making it

happen. The objective is to revive if viable, or close it (the asset), if not viable. You can’t

directly go to liquidation”,

“Probably we are not making the best use of the code (IBC). The code is a much

more powerful thing, it can be used for much higher purposes so that the resolution is

sustainable. If the objective was just to discover a price, get a big value, perhaps we could

have had gone to the stock market,”

Taken from: Times of India

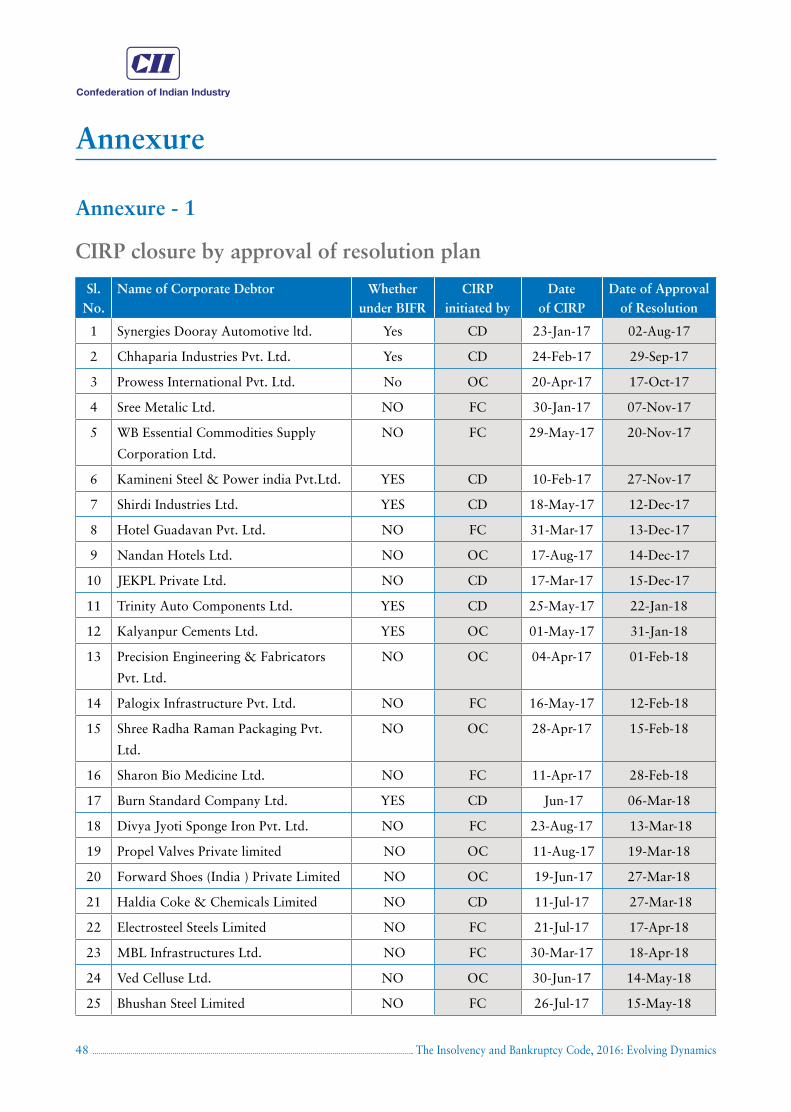

(Refer annexure 1 for list of CIRP cases closed by approval of resolution plan)

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 19

From the first few closed cases, it is clearly seen that liquidation has dominated over resolution. From the 129 cases closed as on May 29, 2018, as many as 104 cases ended up with the commencement of liquidation as against only 25 cases closed with proper resolution plan.

Why are more firms going for liquidation

More liquidation than resolution

The core object of the Code is to frame and implement a proper resolution plan

so as to keep a corporate going and to maximize the value of its assets. However,

the liquidation rate is very high owing to certain limitations, which are beyond

the scope of CoCs or resolution professionals. From the admitted cases, it has

been observed that the corporate debtors did not co-operate with the resolution

professionals, and thus there was no other option left other than liquidation.

In certain cases, the responsible parties have failed to submit a resolution plan

within the statutory time limit of 270 days. In case of Nicco Corporation Ltd,

the statutory time limit of 270 days for submission of resolution plan was over,

and, the corporate debtor had gone for liquidation.

Many SME and MSME are under liquidation, where there is no interest among

the investors other than its own promoters, who are not allowed to invest in

own companies till date. However, this norm would be relaxed as there is a

proposal, where promoters of companies with turnover of up to Rs. 250 crores

might be allowed to bid.

1

2

3

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics20

26

21

34

74

49

Non BIFR Cases BIFR CasesCorporate Debtor Financial Creditors Operational Creditors

BIFR vs NON BIFR Cases* Triggered by

*BIFR Cases – that transferred to NCLT after the scrapping of the BIFR

1QFY 19*

4QFY 18

3QFY 18

2QFY 18

18

56

23

7 Mumbai

Chennai

Ahmedabad

Kolkata

Chandigarh

Bengaluru

Hyderabad

Allahabad

Principal Court

New Delhi

20

19

17

17

8

6

6

5

4

2

Progress Cases by NCLT Benches

*Till May 21, 2018Source: IBBI, Sumedha Fiscal

Summary of the liquidation cases

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 21

0 2000 4000 6000 8000 10000 12000

Rei Agro

Gujarat NRE

Roofit Industries

Rotomac Global

Gupta Corp

JODPL

Gupta Coal

Rotomac Exports

Cethar Ltd.

Innoventive

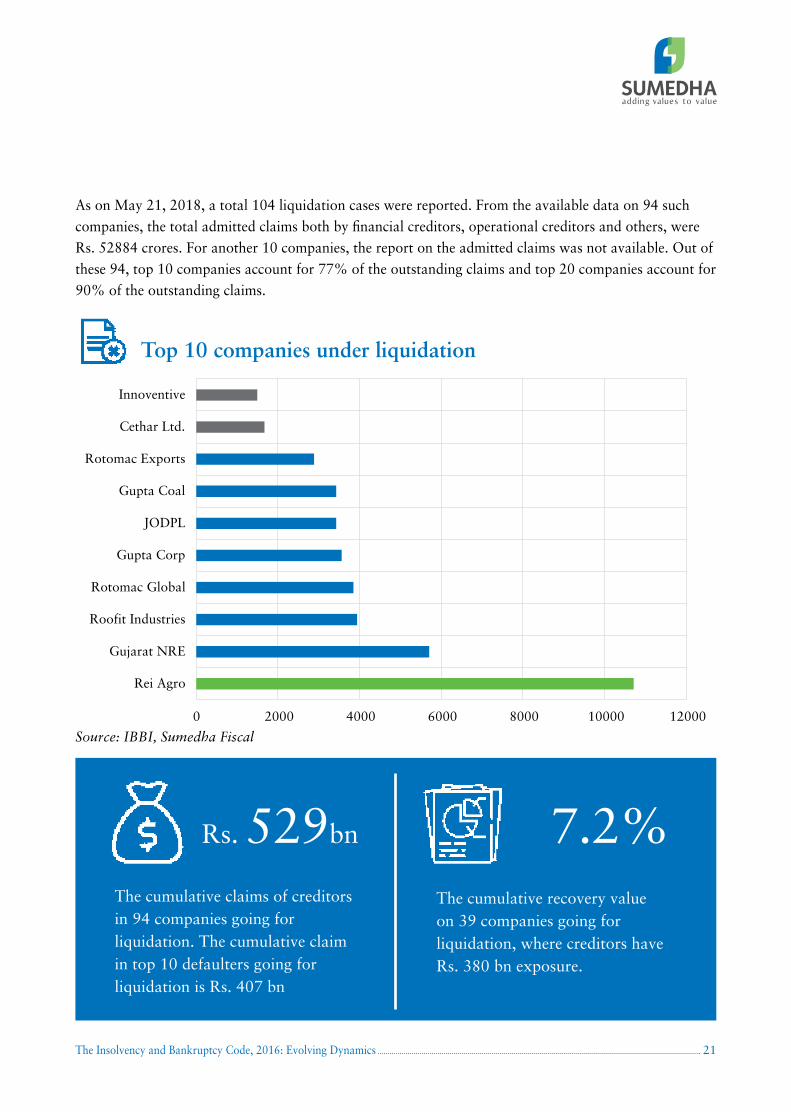

Top 10 companies under liquidation

As on May 21, 2018, a total 104 liquidation cases were reported. From the available data on 94 such companies, the total admitted claims both by financial creditors, operational creditors and others, were Rs. 52884 crores. For another 10 companies, the report on the admitted claims was not available. Out of these 94, top 10 companies account for 77% of the outstanding claims and top 20 companies account for 90% of the outstanding claims.

Rs. 529bn 7.2%The cumulative claims of creditors in 94 companies going for liquidation. The cumulative claim in top 10 defaulters going for liquidation is Rs. 407 bn

The cumulative recovery value on 39 companies going for liquidation, where creditors have Rs. 380 bn exposure.

Source: IBBI, Sumedha Fiscal

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics22

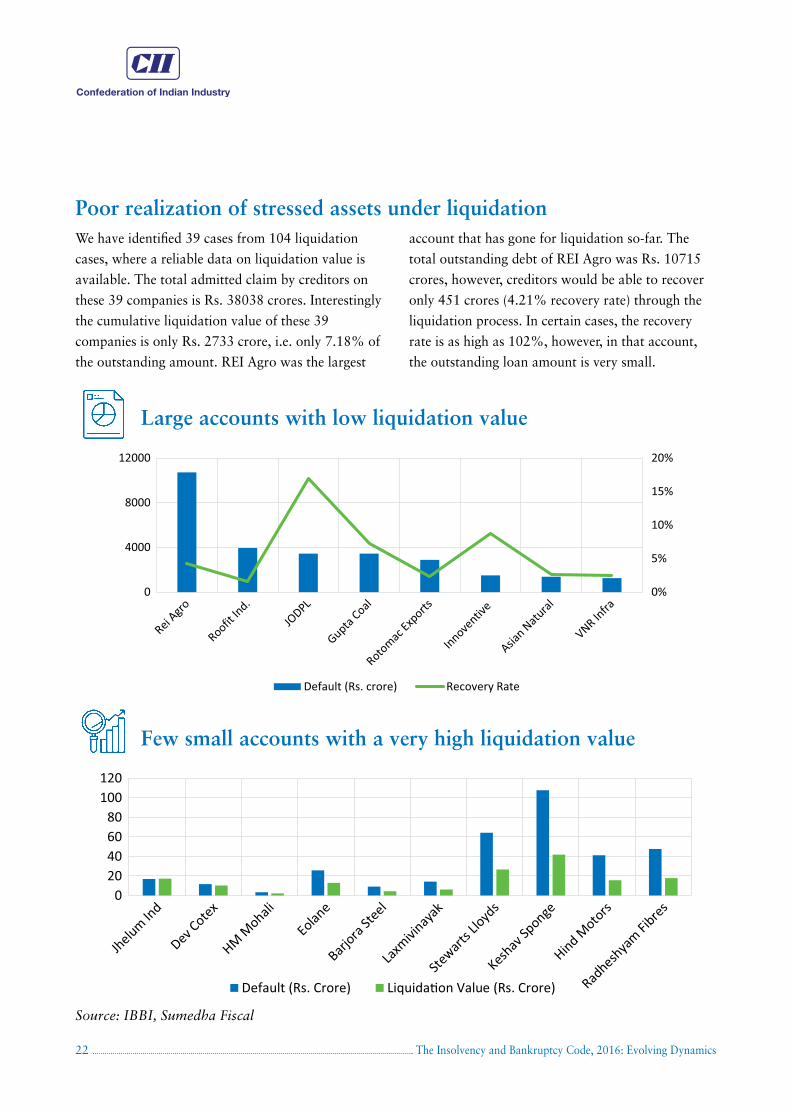

We have identified 39 cases from 104 liquidation

cases, where a reliable data on liquidation value is

available. The total admitted claim by creditors on

these 39 companies is Rs. 38038 crores. Interestingly

the cumulative liquidation value of these 39

companies is only Rs. 2733 crore, i.e. only 7.18% of

the outstanding amount. REI Agro was the largest

account that has gone for liquidation so-far. The

total outstanding debt of REI Agro was Rs. 10715

crores, however, creditors would be able to recover

only 451 crores (4.21% recovery rate) through the

liquidation process. In certain cases, the recovery

rate is as high as 102%, however, in that account,

the outstanding loan amount is very small.

Poor realization of stressed assets under liquidation

0%

5%

10%

15%

20%

0

4000

8000

12000

Default (Rs. crore) Recovery Rate

Large accounts with low liquidation value

020406080

100120

Default (Rs. Crore) Liquida�on Value (Rs. Crore)

Few small accounts with a very high liquidation value

Source: IBBI, Sumedha Fiscal

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 23

IBBI has amended the regulation, where it removed

the requirement for disclosing the liquidation

value of an asset under the resolution. The move

is expected to help better price discovery for the

stressed assets under the code. So, the data on

liquidation value is not available for all companies.

SBI Chairman Mr. Rajnish Kumar’s view on liquidation

It is important that we give a message that if potential bidders are trying to suppress the values, then banks are not going to accept it;

If bidders or the indebted firm cannot service even 5 percent or 7 percent of outstanding credit obligations, then I don’t see any reason for reviving each and every enterprise;

If the recovery could be more than 25 percent, then resolution is always an option;

(Taken from Mr. Rajnish Kumar’s interview to Bloomberg TV)

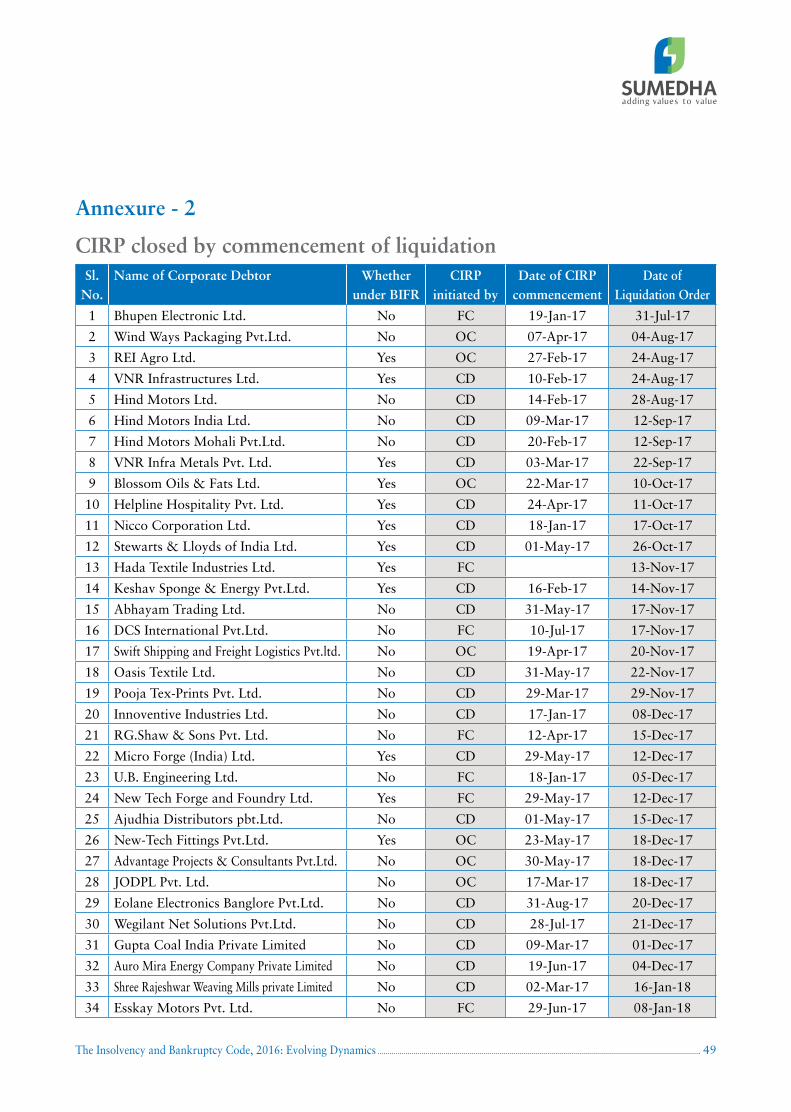

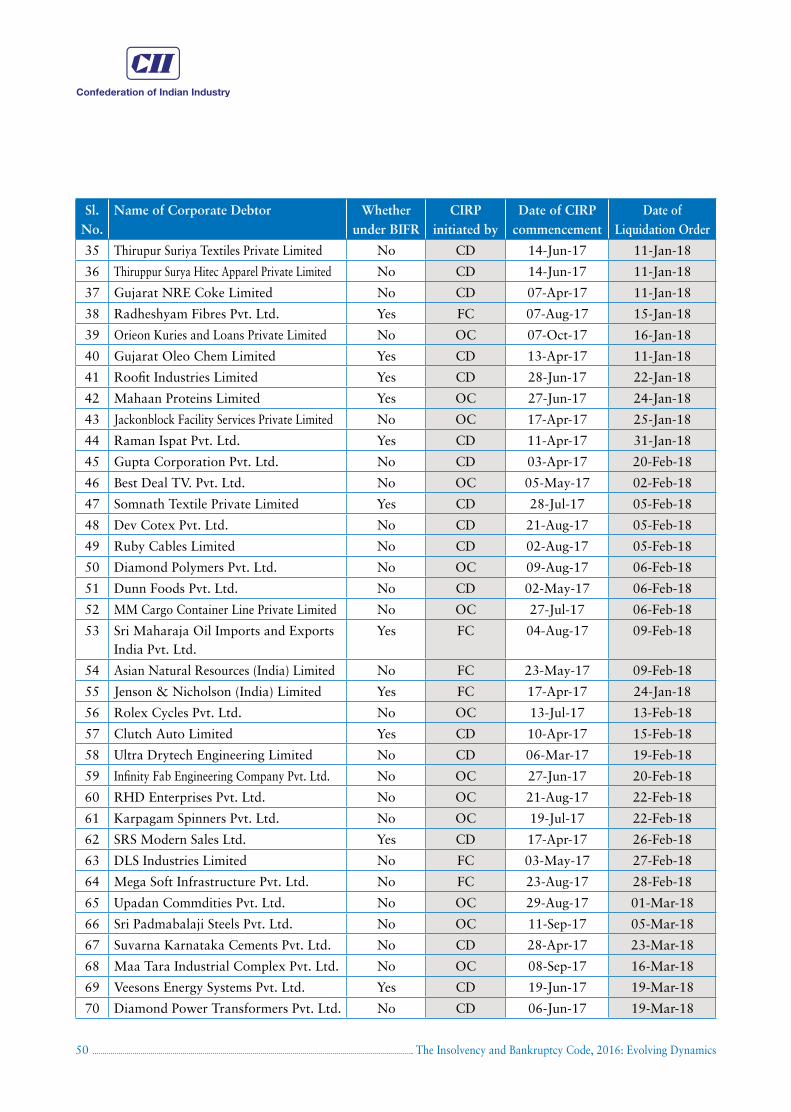

(Refer Annexure 2 for a list of CIRP cases closed by the commencement of liquidation)

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics24

Important amendments suggested by Insolvency Law Committee in IBC Code (Awaits Notification)**

Recent Key Recommendation of the Insolvency Law Committee

Streamlined section 29A by barring only those bidders who contributed to

default by the company

MSME promoters except wilful defaulters can

bid for troubled MSME Cos

Home Buyers should be treated as financial

creditors

Voting thresholds re-calibrated to 66% creditors vote required for passing resolution plan. 90% vote required for

removing company from insolvency process

Home buyers to be treated as Financial Creditor The union cabinet approved ordinance to amend the IBC code for treatment of home

buyers at par with financial creditor in the liquidation process of the defaulting

builder. The ordinance has very recently come into force after getting approval from

the president. Home buyers were treated as unsecured creditors/operational creditors

who came after secured and institutional creditors in terms of priority for recovery

of dues. As operational creditors home buyers interest are also not fully optimised.

This change is likely infuse confidence in millions of home buyers to invest their

money. This move is also likely to have positive impact on the claims of homebuyers

in pending court cases against leading real estate group such as Jaypee Infratech and

Amrapali Group.

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 25

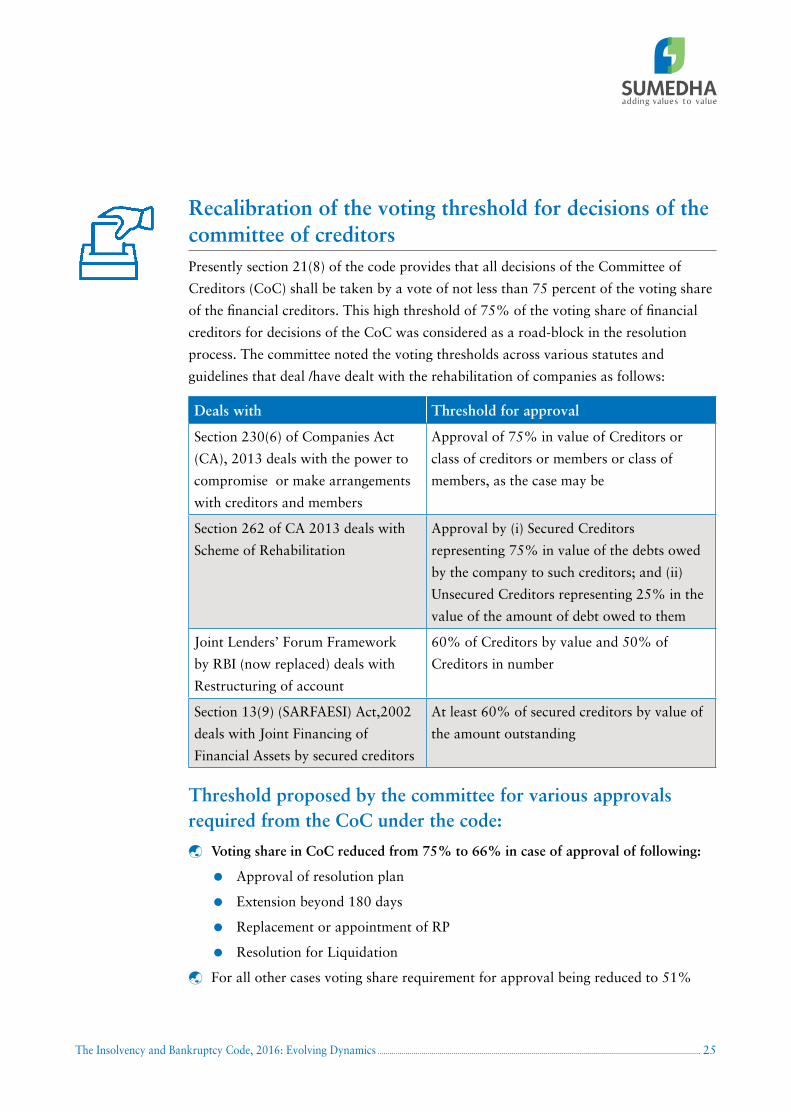

Recalibration of the voting threshold for decisions of the committee of creditorsPresently section 21(8) of the code provides that all decisions of the Committee of

Creditors (CoC) shall be taken by a vote of not less than 75 percent of the voting share

of the financial creditors. This high threshold of 75% of the voting share of financial

creditors for decisions of the CoC was considered as a road-block in the resolution

process. The committee noted the voting thresholds across various statutes and

guidelines that deal /have dealt with the rehabilitation of companies as follows:

Threshold proposed by the committee for various approvals required from the CoC under the code:

Voting share in CoC reduced from 75% to 66% in case of approval of following:

Approval of resolution plan

Extension beyond 180 days

Replacement or appointment of RP

Resolution for Liquidation

For all other cases voting share requirement for approval being reduced to 51%

Deals with Threshold for approval

Section 230(6) of Companies Act

(CA), 2013 deals with the power to

compromise or make arrangements

with creditors and members

Approval of 75% in value of Creditors or

class of creditors or members or class of

members, as the case may be

Section 262 of CA 2013 deals with

Scheme of Rehabilitation

Approval by (i) Secured Creditors

representing 75% in value of the debts owed

by the company to such creditors; and (ii)

Unsecured Creditors representing 25% in the

value of the amount of debt owed to them

Joint Lenders’ Forum Framework

by RBI (now replaced) deals with

Restructuring of account

60% of Creditors by value and 50% of

Creditors in number

Section 13(9) (SARFAESI) Act,2002

deals with Joint Financing of

Financial Assets by secured creditors

At least 60% of secured creditors by value of

the amount outstanding

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics26

RP to continue management even after expiry of CIRP period till NCLT takes a decision on the resolution planTo insert a provision to section 23(1) to state that the RP shall continue to manage the operations of the corporate debtor after the expiry of the CIRP period post submission of the

resolution plan under section 30(6) until an order is passed by the NCLT under section 31.

Withdrawal of an insolvency application post admission Withdrawal of an insolvency application post admission is permitted with the approval

of 90% voting share of the CoC on certain conditions.

Applicability of Limitation ActThe Committee recommends applicability of Limitation Act to the proceedings under the Code. It is proposed to insert a new section 238A to state that the provisions of the Limitation Act, 1963 shall, as far as may be, apply to proceedings or appeals under the Code before the NCLT or the NCLTA, as the case may be.

Accordingly, changes have been proposed in the affidavit required to be furnished along with Forms B/C/D/E/F to include a requirement to affirm that the claim is not time-

barred under the Limitations Act, 1963.

Relaxation in section 29Aa) By limiting the scope of applicability of the disqualifications in section 29A by

deleting reference to “person acting jointly or in concert”

b) Amendment in section 21(6) by disqualifying the participation of authorized representative of FC being the related party.

c) Resolution applicants not to attract disqualification under Section 29 A in respect of NPA account if such account was acquired pursuant to a prior resolution plan approved under this Code for a period of three years from the date of approval of such prior resolution plan by the NCLT.

d) Pure play Financial Entities such as ARC, AIF etc which are regulated by financial regulator, shall not attract disqualifications on holding NPA account, in case they are not related party of CD.

e) Expansion of definition of NPA to include declaration of NPA by other financial regulators such as Housing Finance Bank.

f) Disqualification on account of NPA to be considered at the time of submission of resolution plan.

g) Schedule of offence attracting disqualification to be decided by Central Government akin Companies Act.

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 27

h) Section 29A (d) to be further amended stating that disqualification shall extend from the date of conviction and shall continue for a period of seven years from the date of conviction or from the date of release from imprisonment, whichever is later.

i) Disqualification in case of classification as a wilful defaulter (section 29A(b)), conviction for certain offences (section 29A(c)), disqualification to act as director under the CA 2013 (section 29A(e)), prohibition by SEBI (section 29A (f)) and so on not to attract if an appeal has been preferred against the concerned order within prescribed period.

j) Narrow downed the disqualification u/s 29A (g), by exempting those RAs who has acquired a CD in which a preferential, undervalued, extortionate credit transaction or fraudulent transaction has taken place prior to the acquisition of the CD pursuant to a resolution plan approved under the Code or pursuant to a scheme or plan approved by a financial sector regulator or a court of law.

k) Disqualification of guarantors is now being restricted to guarantees invoked - This will remove ambiguity as earlier provision literally meant even if guarantee is issued but not invoked shall result in disqualification.

l) Insertion of Section 240A exempting from all eligibility criteria of section 29A except the criteria that they should not be a wilful defaulter to RAs of MSME going under CIRP.

A) Implication: This shall enable promoters of very large section of companies to bid for their own companies provided they are not classified as wilful defaulter. MSME has been defined to have annual turnover of less than Rs.250 crore.

Others:1) Related party is defined to include

a) Members of a Hindu Undivided Family, husband, wife, father, mother, son, daughter, son’s daughter and son, daughter’s daughter and son, grandson’s daughter and son, granddaughter’s daughter and son, brother, sister, brother’s son and daughter, sister’s son and daughter, father’s father and mother, mother’s father and mother, father’s brother and sister, mother’s brother and

b) Wherever the relation is that of a son, daughter, sister or brother, their spouses shall also be included.

2) Filling under Section 10 by Corporate Applicant now will require approval from shareholder by way of special resolution or approval from three fourth of the total number of partners of the CD.

3) Moratorium shall not be applicable to a surety in a contract of guarantee to a corporate debtor.

4) Amendment of section 16 to provide that the term of the IRP shall continue till the appointment of the RP.

** The Government of India has notified amendments vide “The Insolvency and Bankruptcy Code (Amendment) Ordinance 2018” dated 6 June, 2018. Most of the provisions are highlighted above.

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics28

Operational Creditors are worse off

Unlike the Companies Act 2013, IBC has

classified creditors into financial and

operational creditors. According to the

section 5(7) of the IBC, a financial creditor means

any person to whom a financial debt is owed and

indicates a person to whom such debt has been

legally assigned or transferred. Section 5(20) of

the IBC defines operational creditor as a person to

whom an operational debt is owed and includes

any person to whom such debt has been legally

assigned or transferred.

Insolvency proceedings

Financial creditors can initiate the insolvency process even the debt is disputed one

Operational creditors cannot initiate the process in case of a disputed debt. For

operational creditors to initiate a resolution process, it must satisfy the NCLT

with respect to certain documentation. If the corporate debtor doesn’t admit the

obligation, there is a chance that the case may not be accepted.

Committee of creditors

Section 21(2) of the IBC explains that the Committee of Creditors (CoC) shall

comprise of all financial creditors of the corporate debtor. That means, all decisions

including acceptance of resolution plans, liquidation etc. will be taken by a

committee where financial creditors are the only representatives. However, Section

24(3) states that an operational creditor can participate in the meeting of CoCs, if

the amount of their aggregate dues is not less than 10% of the debt.

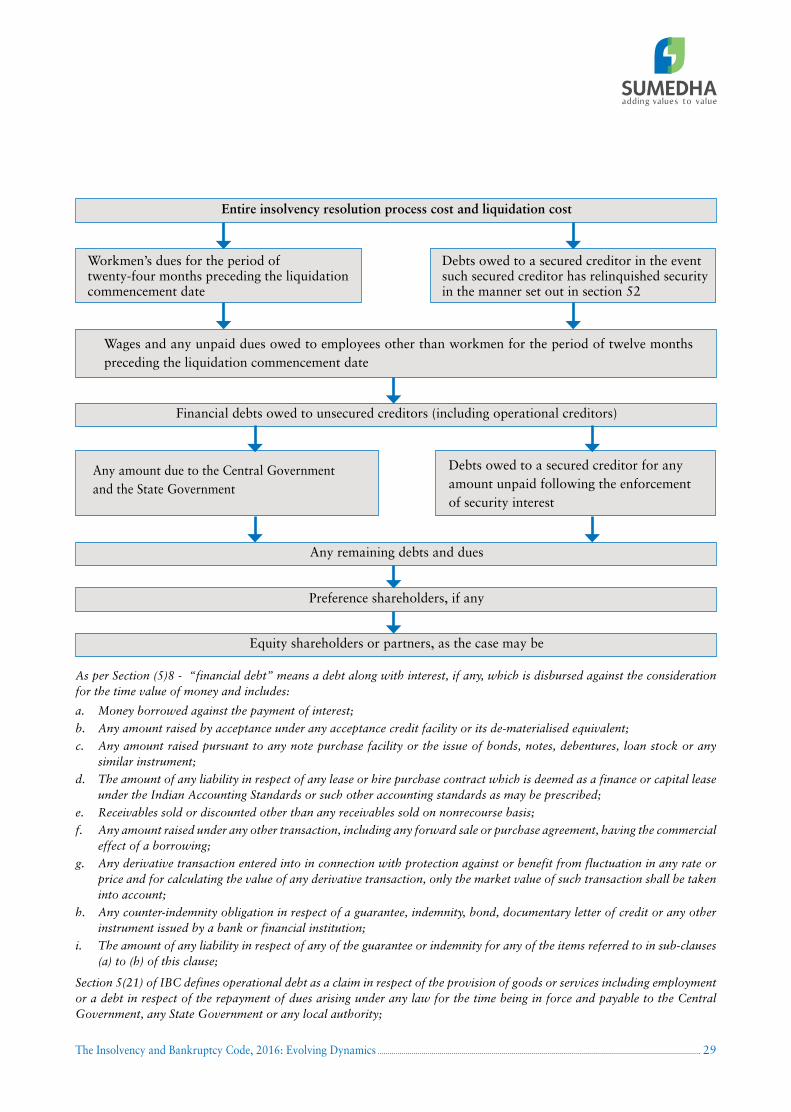

Liquidation waterfall

Section 53 of the Code deals with distribution of assets sale proceeds along with

liquidation waterfall. Here also, secured financial creditors have the priority over

operational creditors, who are considered as unsecured creditors

Major differences

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 29

Wages and any unpaid dues owed to employees other than workmen for the period of twelve months preceding the liquidation commencement date

Financial debts owed to unsecured creditors (including operational creditors)

Entire insolvency resolution process cost and liquidation cost

Any remaining debts and dues

Preference shareholders, if any

Equity shareholders or partners, as the case may be

Workmen’s dues for the period of twenty-four months preceding the liquidation commencement date

Debts owed to a secured creditor in the event such secured creditor has relinquished security in the manner set out in section 52

Any amount due to the Central Government and the State Government

Debts owed to a secured creditor for any amount unpaid following the enforcement of security interest

As per Section (5)8 - “financial debt” means a debt along with interest, if any, which is disbursed against the consideration for the time value of money and includes:

a. Money borrowed against the payment of interest;

b. Any amount raised by acceptance under any acceptance credit facility or its de-materialised equivalent;

c. Any amount raised pursuant to any note purchase facility or the issue of bonds, notes, debentures, loan stock or any similar instrument;

d. The amount of any liability in respect of any lease or hire purchase contract which is deemed as a finance or capital lease under the Indian Accounting Standards or such other accounting standards as may be prescribed;

e. Receivables sold or discounted other than any receivables sold on nonrecourse basis;

f. Any amount raised under any other transaction, including any forward sale or purchase agreement, having the commercial effect of a borrowing;

g. Any derivative transaction entered into in connection with protection against or benefit from fluctuation in any rate or price and for calculating the value of any derivative transaction, only the market value of such transaction shall be taken into account;

h. Any counter-indemnity obligation in respect of a guarantee, indemnity, bond, documentary letter of credit or any other instrument issued by a bank or financial institution;

i. The amount of any liability in respect of any of the guarantee or indemnity for any of the items referred to in sub-clauses (a) to (h) of this clause;

Section 5(21) of IBC defines operational debt as a claim in respect of the provision of goods or services including employment or a debt in respect of the repayment of dues arising under any law for the time being in force and payable to the Central Government, any State Government or any local authority;

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics30

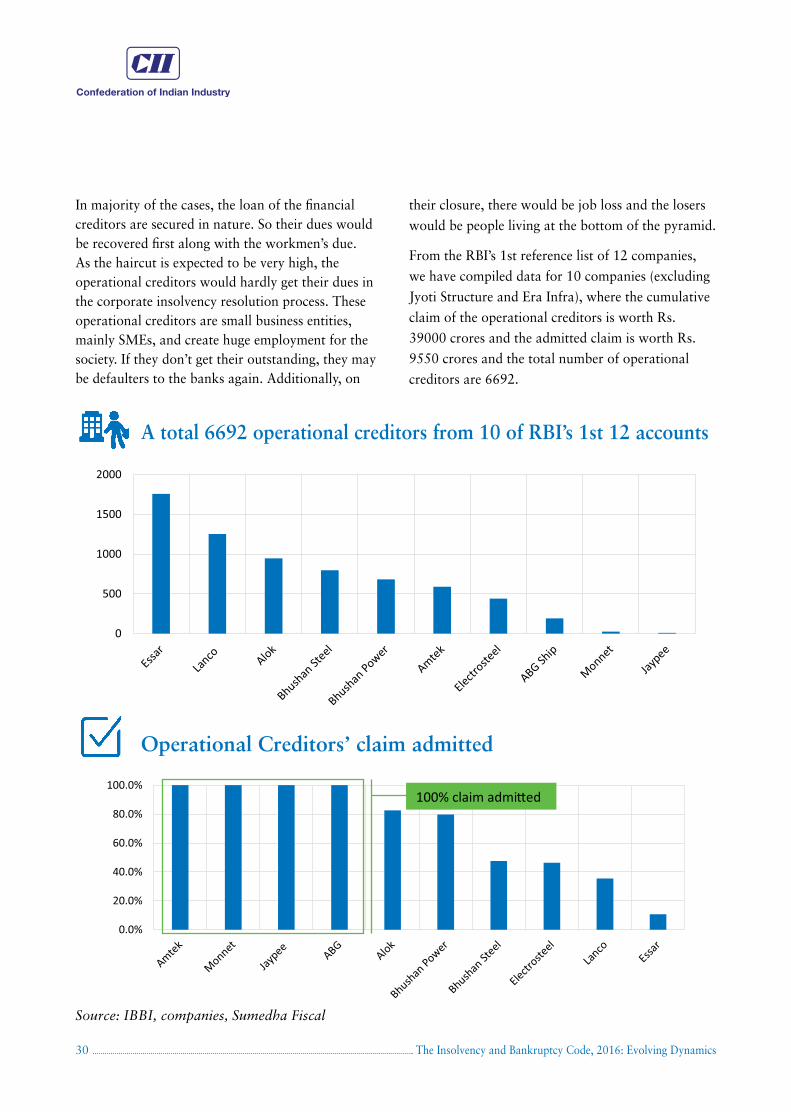

In majority of the cases, the loan of the financial creditors are secured in nature. So their dues would be recovered first along with the workmen’s due. As the haircut is expected to be very high, the operational creditors would hardly get their dues in the corporate insolvency resolution process. These operational creditors are small business entities, mainly SMEs, and create huge employment for the society. If they don’t get their outstanding, they may be defaulters to the banks again. Additionally, on

their closure, there would be job loss and the losers

would be people living at the bottom of the pyramid.

From the RBI’s 1st reference list of 12 companies,

we have compiled data for 10 companies (excluding

Jyoti Structure and Era Infra), where the cumulative

claim of the operational creditors is worth Rs.

39000 crores and the admitted claim is worth Rs.

9550 crores and the total number of operational

creditors are 6692.

0

500

1000

1500

2000

A total 6692 operational creditors from 10 of RBI’s 1st 12 accounts

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%100% claim admi�ed

Operational Creditors’ claim admitted

Source: IBBI, companies, Sumedha Fiscal

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 31

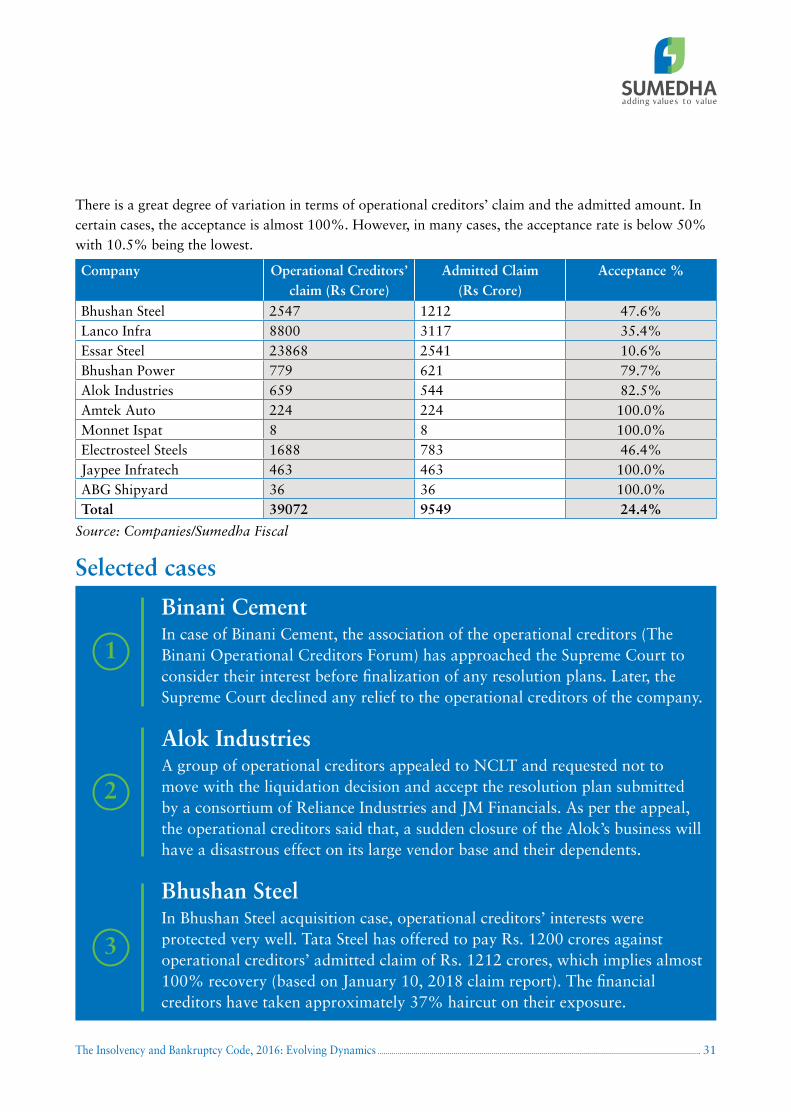

There is a great degree of variation in terms of operational creditors’ claim and the admitted amount. In certain cases, the acceptance is almost 100%. However, in many cases, the acceptance rate is below 50% with 10.5% being the lowest.

Company Operational Creditors’ claim (Rs Crore)

Admitted Claim (Rs Crore)

Acceptance %

Bhushan Steel 2547 1212 47.6%Lanco Infra 8800 3117 35.4%Essar Steel 23868 2541 10.6%Bhushan Power 779 621 79.7%Alok Industries 659 544 82.5%Amtek Auto 224 224 100.0%Monnet Ispat 8 8 100.0%Electrosteel Steels 1688 783 46.4%Jaypee Infratech 463 463 100.0%ABG Shipyard 36 36 100.0%Total 39072 9549 24.4%

Source: Companies/Sumedha Fiscal

Selected cases

Binani CementIn case of Binani Cement, the association of the operational creditors (The Binani Operational Creditors Forum) has approached the Supreme Court to consider their interest before finalization of any resolution plans. Later, the Supreme Court declined any relief to the operational creditors of the company.

Alok IndustriesA group of operational creditors appealed to NCLT and requested not to move with the liquidation decision and accept the resolution plan submitted by a consortium of Reliance Industries and JM Financials. As per the appeal, the operational creditors said that, a sudden closure of the Alok’s business will have a disastrous effect on its large vendor base and their dependents.

Bhushan SteelIn Bhushan Steel acquisition case, operational creditors’ interests were protected very well. Tata Steel has offered to pay Rs. 1200 crores against operational creditors’ admitted claim of Rs. 1212 crores, which implies almost 100% recovery (based on January 10, 2018 claim report). The financial creditors have taken approximately 37% haircut on their exposure.

1

2

3

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics32

Top NCLT Cases

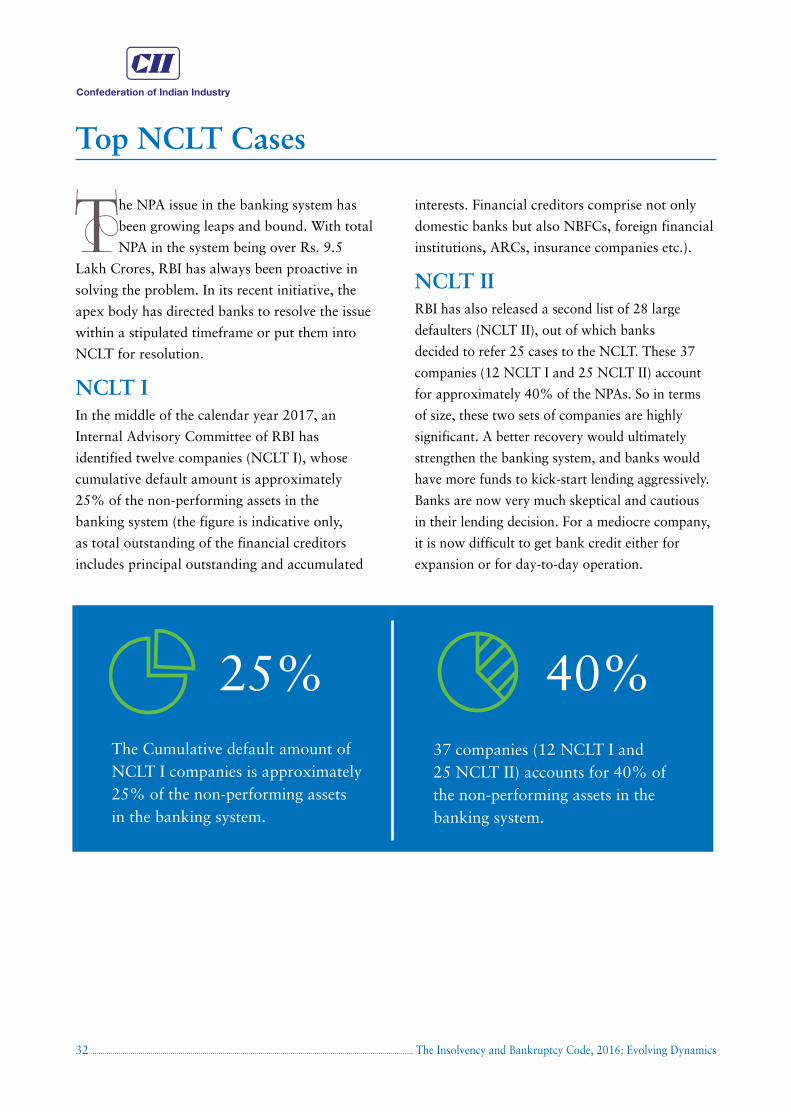

The NPA issue in the banking system has

been growing leaps and bound. With total

NPA in the system being over Rs. 9.5

Lakh Crores, RBI has always been proactive in

solving the problem. In its recent initiative, the

apex body has directed banks to resolve the issue

within a stipulated timeframe or put them into

NCLT for resolution.

NCLT IIn the middle of the calendar year 2017, an

Internal Advisory Committee of RBI has

identified twelve companies (NCLT I), whose

cumulative default amount is approximately

25% of the non-performing assets in the

banking system (the figure is indicative only,

as total outstanding of the financial creditors

includes principal outstanding and accumulated

interests. Financial creditors comprise not only

domestic banks but also NBFCs, foreign financial

institutions, ARCs, insurance companies etc.).

NCLT IIRBI has also released a second list of 28 large

defaulters (NCLT II), out of which banks

decided to refer 25 cases to the NCLT. These 37

companies (12 NCLT I and 25 NCLT II) account

for approximately 40% of the NPAs. So in terms

of size, these two sets of companies are highly

significant. A better recovery would ultimately

strengthen the banking system, and banks would

have more funds to kick-start lending aggressively.

Banks are now very much skeptical and cautious

in their lending decision. For a mediocre company,

it is now difficult to get bank credit either for

expansion or for day-to-day operation.

25% 40%The Cumulative default amount of NCLT I companies is approximately 25% of the non-performing assets in the banking system.

37 companies (12 NCLT I and 25 NCLT II) accounts for 40% of the non-performing assets in the banking system.

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 33

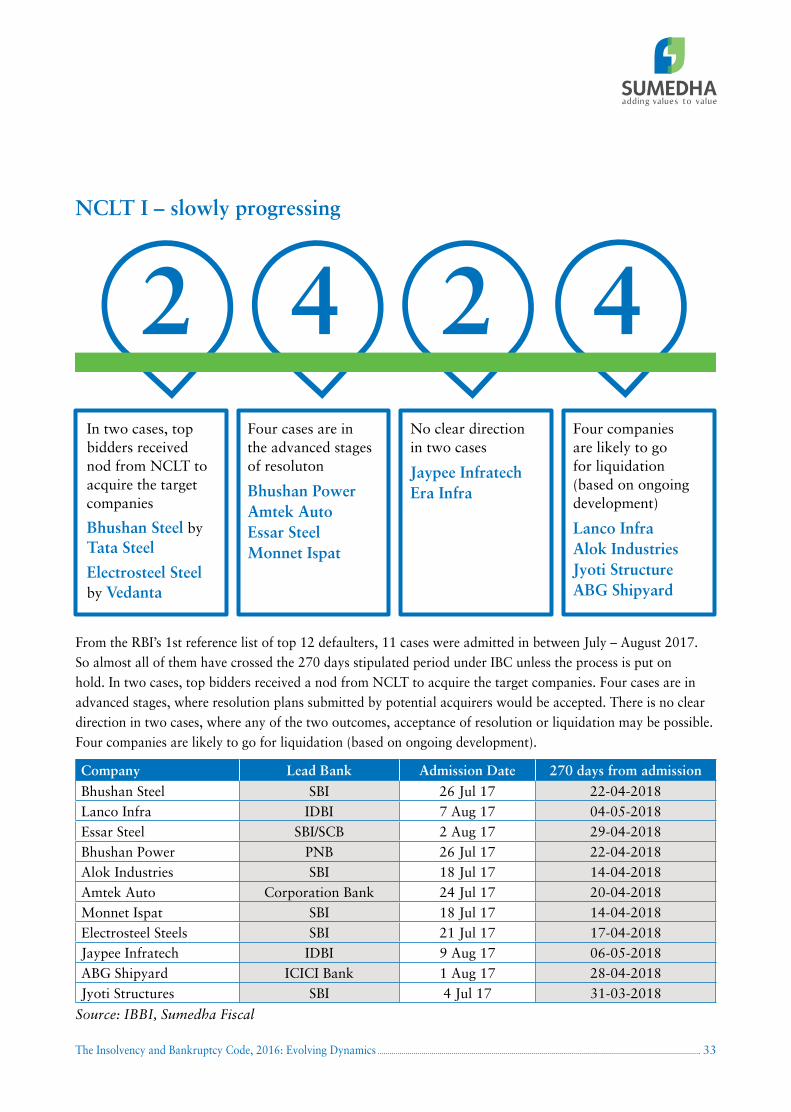

From the RBI’s 1st reference list of top 12 defaulters, 11 cases were admitted in between July – August 2017. So almost all of them have crossed the 270 days stipulated period under IBC unless the process is put on hold. In two cases, top bidders received a nod from NCLT to acquire the target companies. Four cases are in advanced stages, where resolution plans submitted by potential acquirers would be accepted. There is no clear direction in two cases, where any of the two outcomes, acceptance of resolution or liquidation may be possible. Four companies are likely to go for liquidation (based on ongoing development).

NCLT I – slowly progressing

2 2 44In two cases, top bidders received nod from NCLT to acquire the target companies

Bhushan Steel by Tata Steel

Electrosteel Steel by Vedanta

Four cases are in the advanced stages of resoluton

Bhushan PowerAmtek AutoEssar SteelMonnet Ispat

No clear direction in two cases

Jaypee InfratechEra Infra

Four companies are likely to go for liquidation (based on ongoing development)

Lanco Infra Alok IndustriesJyoti StructureABG Shipyard

Company Lead Bank Admission Date 270 days from admissionBhushan Steel SBI 26 Jul 17 22-04-2018Lanco Infra IDBI 7 Aug 17 04-05-2018Essar Steel SBI/SCB 2 Aug 17 29-04-2018Bhushan Power PNB 26 Jul 17 22-04-2018Alok Industries SBI 18 Jul 17 14-04-2018Amtek Auto Corporation Bank 24 Jul 17 20-04-2018Monnet Ispat SBI 18 Jul 17 14-04-2018Electrosteel Steels SBI 21 Jul 17 17-04-2018Jaypee Infratech IDBI 9 Aug 17 06-05-2018ABG Shipyard ICICI Bank 1 Aug 17 28-04-2018Jyoti Structures SBI 4 Jul 17 31-03-2018

Source: IBBI, Sumedha Fiscal

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics34

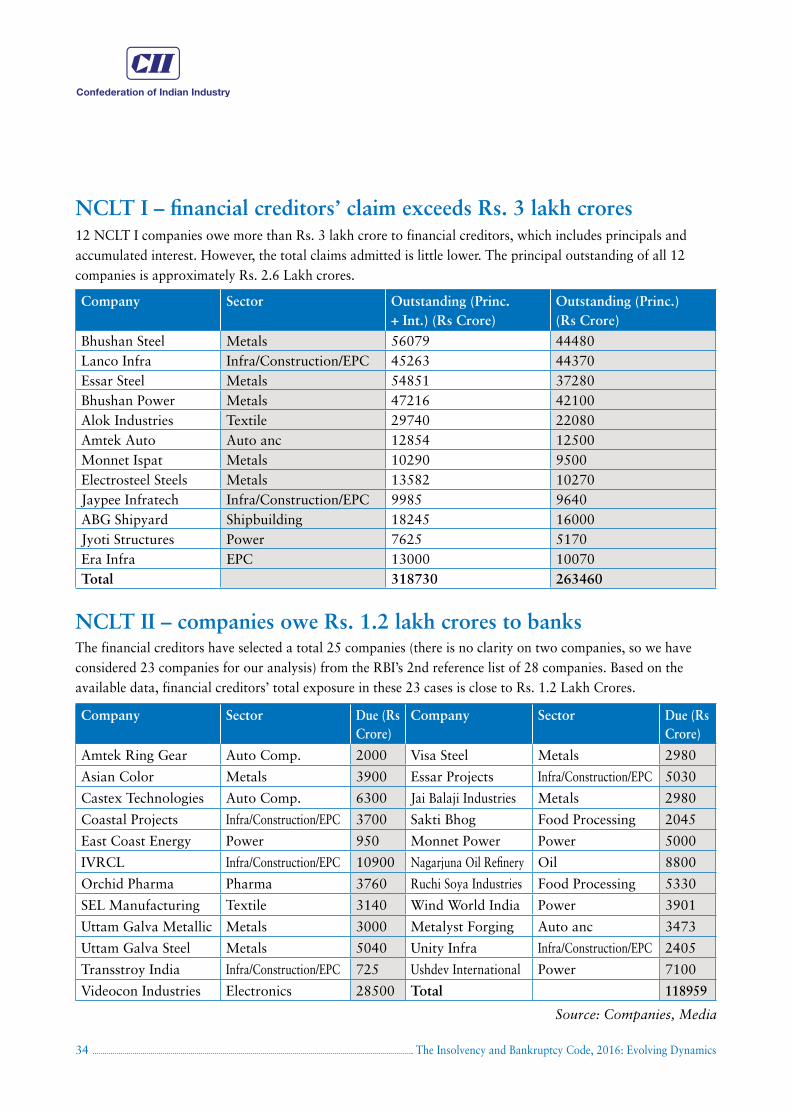

12 NCLT I companies owe more than Rs. 3 lakh crore to financial creditors, which includes principals and accumulated interest. However, the total claims admitted is little lower. The principal outstanding of all 12 companies is approximately Rs. 2.6 Lakh crores.

The financial creditors have selected a total 25 companies (there is no clarity on two companies, so we have considered 23 companies for our analysis) from the RBI’s 2nd reference list of 28 companies. Based on the available data, financial creditors’ total exposure in these 23 cases is close to Rs. 1.2 Lakh Crores.

NCLT I – financial creditors’ claim exceeds Rs. 3 lakh crores

NCLT II – companies owe Rs. 1.2 lakh crores to banks

Company Sector Outstanding (Princ. + Int.) (Rs Crore)

Outstanding (Princ.) (Rs Crore)

Bhushan Steel Metals 56079 44480Lanco Infra Infra/Construction/EPC 45263 44370Essar Steel Metals 54851 37280Bhushan Power Metals 47216 42100Alok Industries Textile 29740 22080Amtek Auto Auto anc 12854 12500Monnet Ispat Metals 10290 9500Electrosteel Steels Metals 13582 10270Jaypee Infratech Infra/Construction/EPC 9985 9640ABG Shipyard Shipbuilding 18245 16000Jyoti Structures Power 7625 5170Era Infra EPC 13000 10070Total 318730 263460

Source: Companies, Media

Company Sector Due (Rs Crore)

Company Sector Due (Rs Crore)

Amtek Ring Gear Auto Comp. 2000 Visa Steel Metals 2980

Asian Color Metals 3900 Essar Projects Infra/Construction/EPC 5030

Castex Technologies Auto Comp. 6300 Jai Balaji Industries Metals 2980

Coastal Projects Infra/Construction/EPC 3700 Sakti Bhog Food Processing 2045

East Coast Energy Power 950 Monnet Power Power 5000

IVRCL Infra/Construction/EPC 10900 Nagarjuna Oil Refinery Oil 8800

Orchid Pharma Pharma 3760 Ruchi Soya Industries Food Processing 5330

SEL Manufacturing Textile 3140 Wind World India Power 3901

Uttam Galva Metallic Metals 3000 Metalyst Forging Auto anc 3473

Uttam Galva Steel Metals 5040 Unity Infra Infra/Construction/EPC 2405

Transstroy India Infra/Construction/EPC 725 Ushdev International Power 7100

Videocon Industries Electronics 28500 Total 118959

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 35

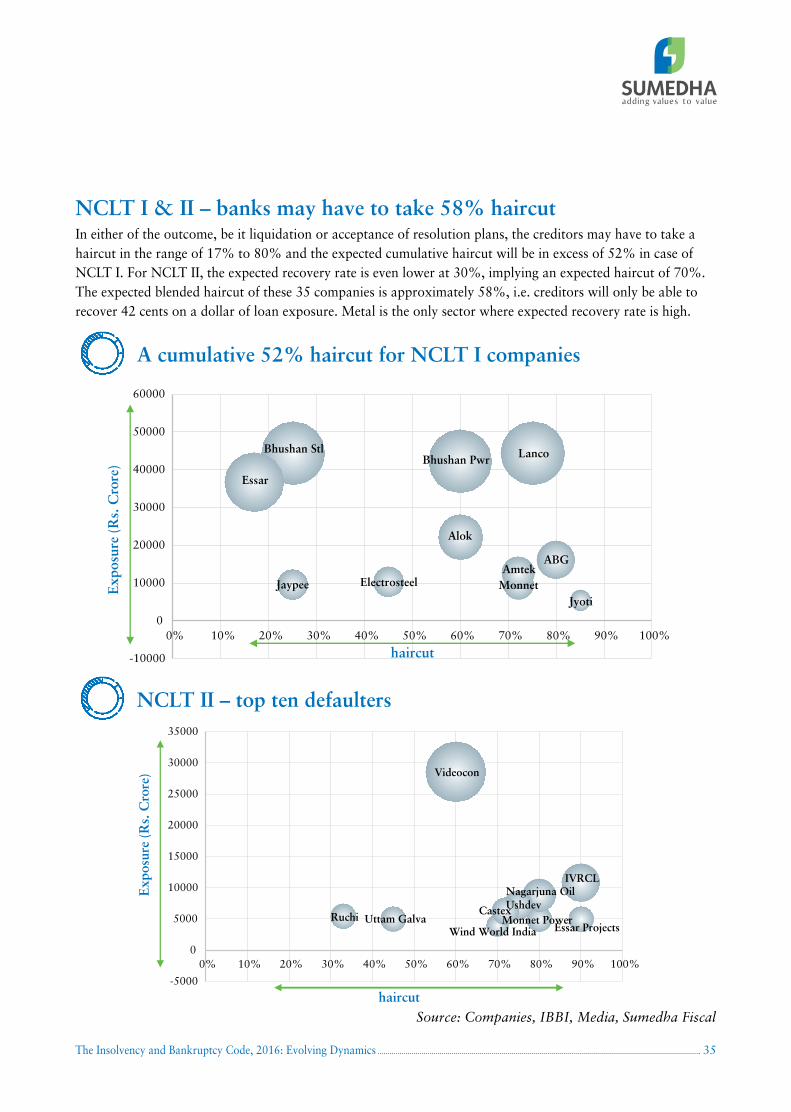

In either of the outcome, be it liquidation or acceptance of resolution plans, the creditors may have to take a haircut in the range of 17% to 80% and the expected cumulative haircut will be in excess of 52% in case of NCLT I. For NCLT II, the expected recovery rate is even lower at 30%, implying an expected haircut of 70%. The expected blended haircut of these 35 companies is approximately 58%, i.e. creditors will only be able to recover 42 cents on a dollar of loan exposure. Metal is the only sector where expected recovery rate is high.

NCLT I & II – banks may have to take 58% haircut

-10000

0

10000

20000

30000

40000

50000

60000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

haircut

Exp

osur

e (R

s. C

rore

)

Bhushan Stl Lanco

Essar

Bhushan Pwr

Alok

AmtekMonnetElectrosteelJaypee

ABG

Jyoti

A cumulative 52% haircut for NCLT I companies

-5000

0

5000

10000

15000

20000

25000

30000

35000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Exp

osur

e (R

s. C

rore

)

haircut

Videocon

IVRCLNagarjuna OilUshdevCastexRuchi Uttam Galva

Essar ProjectsMonnet Power

Wind World India

NCLT II – top ten defaulters

Source: Companies, IBBI, Media, Sumedha Fiscal

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics36

52%

58%

Cumulative haircut in NCLT I cases will be in excess of 52% of the total exposure

The blended haircut of NCLT I and II companies is expected to be 58% of the total exposure

Data Source: Media Reports/Sumedha/Business Standard

Source: Companies, IBBI, Media, Sumedha Fiscal

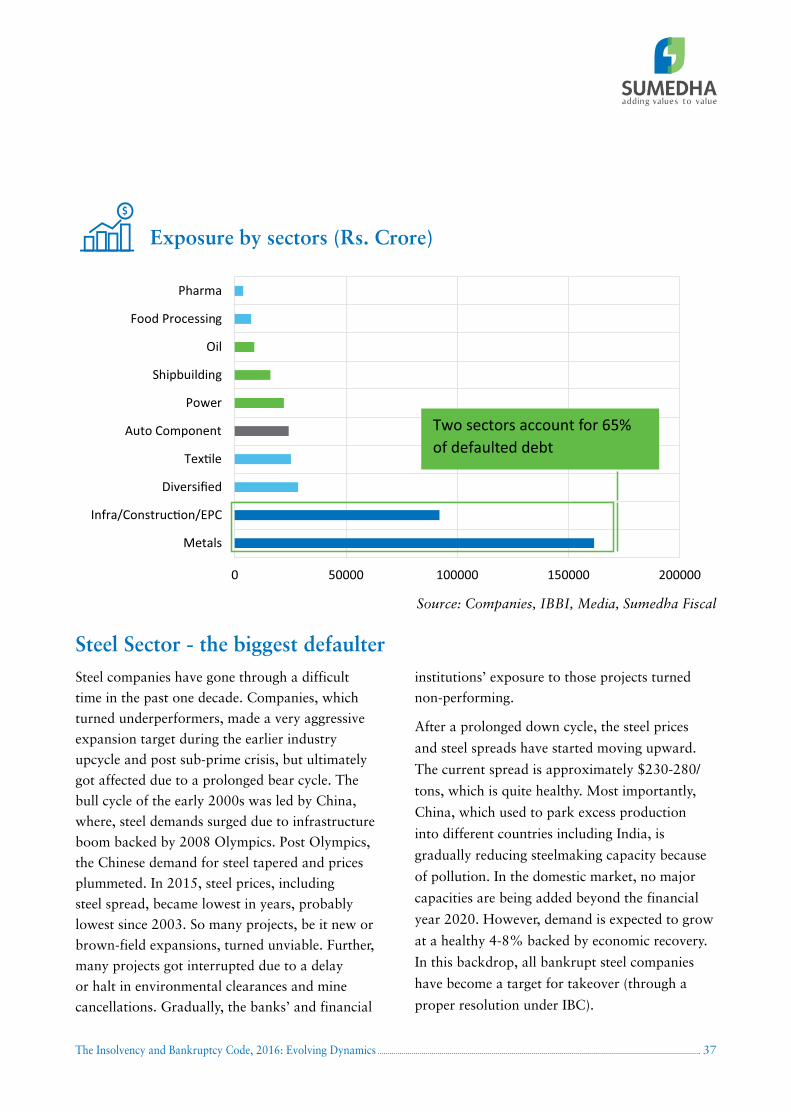

From the RBI’s reference list of 35 companies, financial creditors’ total exposure in term of principal

outstanding is Rs. 3.84 Lakh Crores. Among sectors, the financial creditors have the highest exposure

in metal, predominantly steel companies (Rs. 1.63 lakh crore), followed by EPC, diversified (Videocon

Industries is the only representative), Textiles, Auto-Components, Power and Shipping. A total 10 metal

companies and 9 EPC companies are in the list of these 35 companies.

Sectoral Update

0.00% 20.00% 40.00% 60.00% 80.00%

Metals

Food Processing

Diversified

Pharma

Tex�le

Auto Component

Infra/Construc�on/EPC

Power

Oil

Shipbuilding

70% and above haircut

70% and above expected haircut in five sectors

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 37

Source: Companies, IBBI, Media, Sumedha Fiscal

Steel companies have gone through a difficult

time in the past one decade. Companies, which

turned underperformers, made a very aggressive

expansion target during the earlier industry

upcycle and post sub-prime crisis, but ultimately

got affected due to a prolonged bear cycle. The

bull cycle of the early 2000s was led by China,

where, steel demands surged due to infrastructure

boom backed by 2008 Olympics. Post Olympics,

the Chinese demand for steel tapered and prices

plummeted. In 2015, steel prices, including

steel spread, became lowest in years, probably

lowest since 2003. So many projects, be it new or

brown-field expansions, turned unviable. Further,

many projects got interrupted due to a delay

or halt in environmental clearances and mine

cancellations. Gradually, the banks’ and financial

institutions’ exposure to those projects turned

non-performing.

After a prolonged down cycle, the steel prices

and steel spreads have started moving upward.

The current spread is approximately $230-280/

tons, which is quite healthy. Most importantly,

China, which used to park excess production

into different countries including India, is

gradually reducing steelmaking capacity because

of pollution. In the domestic market, no major

capacities are being added beyond the financial

year 2020. However, demand is expected to grow

at a healthy 4-8% backed by economic recovery.

In this backdrop, all bankrupt steel companies

have become a target for takeover (through a

proper resolution under IBC).

Steel Sector - the biggest defaulter

0 50000 100000 150000 200000

Metals

Infra/Construc�on/EPC

Diversified

Tex�le

Auto Component

Power

Shipbuilding

Oil

Food Processing

Pharma

Two sectors account for 65% of defaulted debt

Exposure by sectors (Rs. Crore)

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics38

-10000

0

10000

20000

30000

40000

50000

60000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Bhushan Steel

Essar Steel

Bhushan Power

MonnetElectrosteel

Asian ColorU�am Gal. Met.U�am Gal. Steel

VisaJai Balaji

Steel Companies – Exposure (Rs crore) and haircut (%)

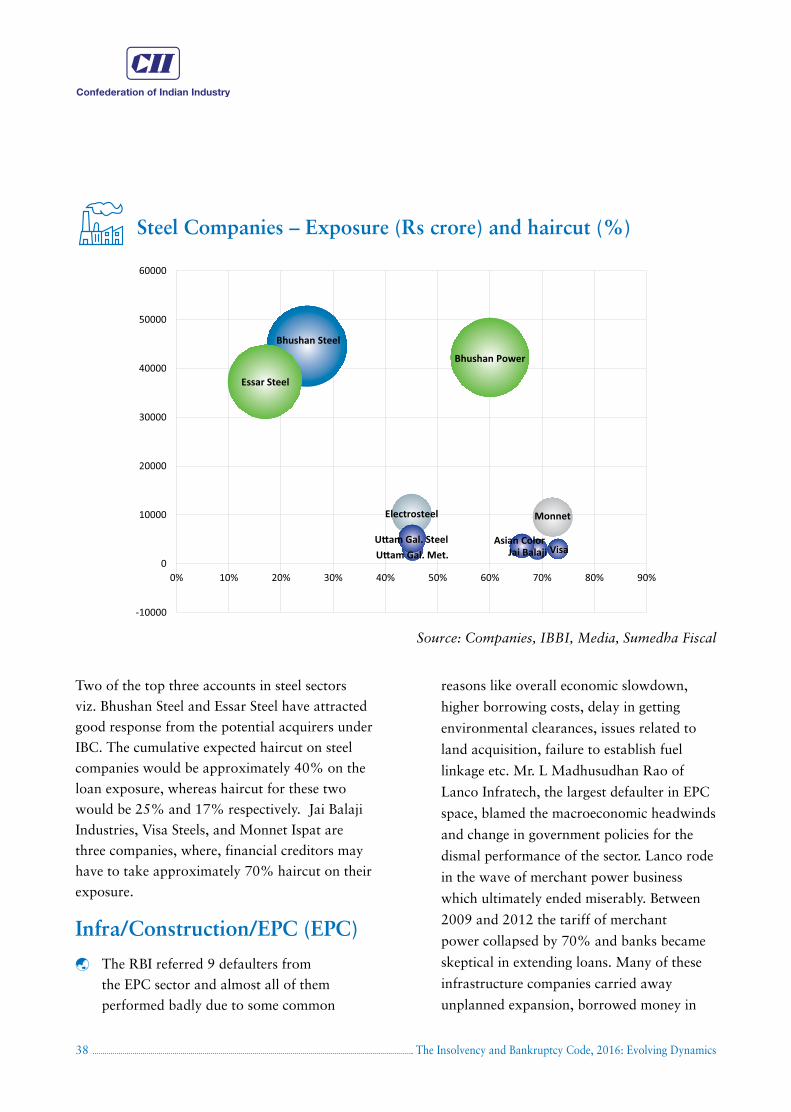

Two of the top three accounts in steel sectors

viz. Bhushan Steel and Essar Steel have attracted

good response from the potential acquirers under

IBC. The cumulative expected haircut on steel

companies would be approximately 40% on the

loan exposure, whereas haircut for these two

would be 25% and 17% respectively. Jai Balaji

Industries, Visa Steels, and Monnet Ispat are

three companies, where, financial creditors may

have to take approximately 70% haircut on their

exposure.

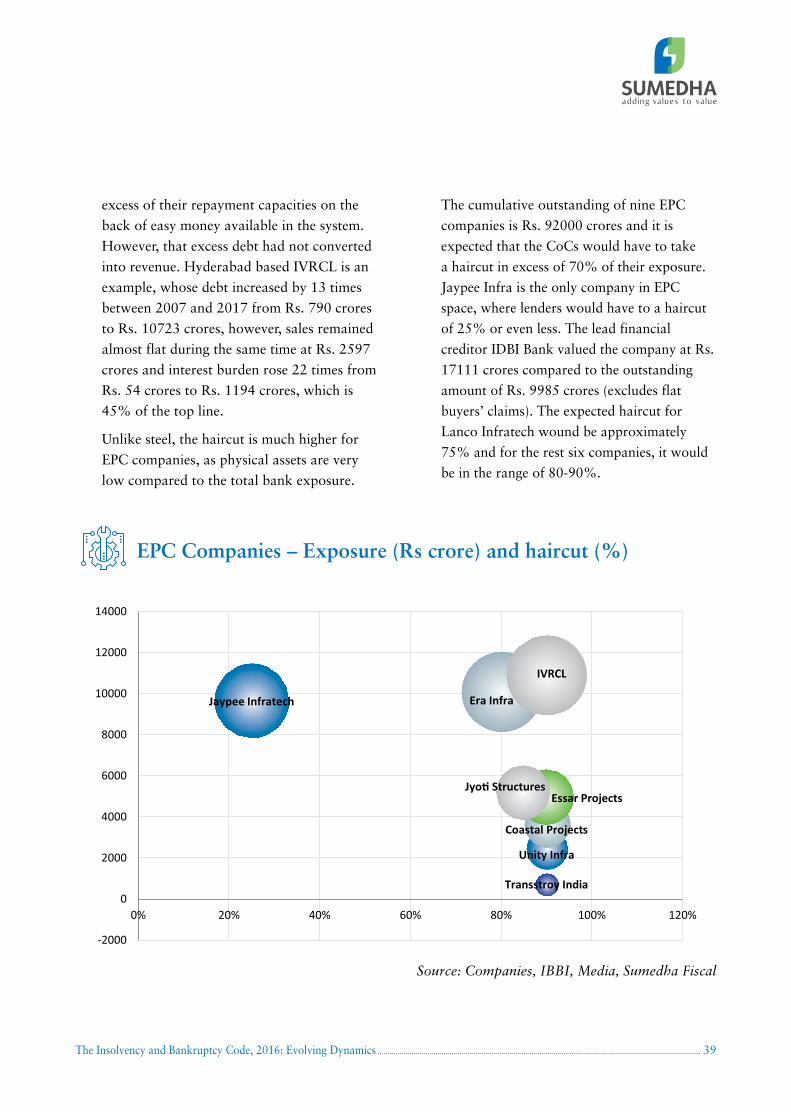

Infra/Construction/EPC (EPC)

The RBI referred 9 defaulters from

the EPC sector and almost all of them

performed badly due to some common

reasons like overall economic slowdown,

higher borrowing costs, delay in getting

environmental clearances, issues related to

land acquisition, failure to establish fuel

linkage etc. Mr. L Madhusudhan Rao of

Lanco Infratech, the largest defaulter in EPC

space, blamed the macroeconomic headwinds

and change in government policies for the

dismal performance of the sector. Lanco rode

in the wave of merchant power business

which ultimately ended miserably. Between

2009 and 2012 the tariff of merchant

power collapsed by 70% and banks became

skeptical in extending loans. Many of these

infrastructure companies carried away

unplanned expansion, borrowed money in

Source: Companies, IBBI, Media, Sumedha Fiscal

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 39

excess of their repayment capacities on the

back of easy money available in the system.

However, that excess debt had not converted

into revenue. Hyderabad based IVRCL is an

example, whose debt increased by 13 times

between 2007 and 2017 from Rs. 790 crores

to Rs. 10723 crores, however, sales remained

almost flat during the same time at Rs. 2597

crores and interest burden rose 22 times from

Rs. 54 crores to Rs. 1194 crores, which is

45% of the top line.

Unlike steel, the haircut is much higher for

EPC companies, as physical assets are very

low compared to the total bank exposure.

The cumulative outstanding of nine EPC

companies is Rs. 92000 crores and it is

expected that the CoCs would have to take

a haircut in excess of 70% of their exposure.

Jaypee Infra is the only company in EPC

space, where lenders would have to a haircut

of 25% or even less. The lead financial

creditor IDBI Bank valued the company at Rs.

17111 crores compared to the outstanding

amount of Rs. 9985 crores (excludes flat

buyers’ claims). The expected haircut for

Lanco Infratech wound be approximately

75% and for the rest six companies, it would

be in the range of 80-90%.

-2000

0

2000

4000

6000

8000

10000

12000

14000

0% 20% 40% 60% 80% 100% 120%

Jaypee Infratech Era Infra

Coastal Projects

IVRCL

Transstroy India

Essar Projects

Unity Infra

Jyo� Structures

EPC Companies – Exposure (Rs crore) and haircut (%)

Source: Companies, IBBI, Media, Sumedha Fiscal

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics40

AutoComponent

Power

Textiles

Shipbuilding

Leader Speaks “The basic issue is that the entire infrastructure space we are in has serious macro issues and most of the macro issues came out, I would say, sometime in October-November 2011... That was the time when, one after another, the macro surprises kept coming. And various policies kept coming out,” L Madhusudhan Rao/Lanco Infratech (Source: Mint)

In auto-component sector, a total four companies are in the list referred by RBI and all four belong to the Amtek Auto Group. The sector in general is performing well, backed by revival of CV segment and superior growth in passenger cars and two wheelers segment. However, this group made a few aggressive acquisitions that were funded by debts, which ultimately went against the company. Its interest coverage ratio started deteriorating since financial year 2014 and went down below one at the end of FY 2015 and ultimately turned negative in FY 2017.

ABG Shipyard, part of 1st list referred by RBI, was a victim of the world wide downtrend in shipbuilding industry. Post 2008, the global seaborne trade witnessed a prolonged slowdown, which resulted some leading names in the shipbuilding industry across the world went bankrupt.

In the textiles sector, Alok Industries and SEL Manufacturing are the two companies with cumulative exposure of Rs. 25000 crores (principal outstanding). The expected haircut for Alok Industries is 60%, whereas for SEL it is 80%. The resolution plans received for Alok is not satisfactory and the 270 days period stipulated under the IBC is over, the company may go for liquidation.

In power, four companies (Monnet Power, Wind World India, Ushdev, East Coast Energy) are in the list of top 35 defaulters with cumulative outstanding of Rs. 22000 crores. This is however a very small list compared to the total stress in the power sector. As per media report, 2/3rd of the private power companies are struggling due to multiple headwinds in the industry like lack of proper coal linkage or power purchase tie-ups and poor payment structure of distribution companies.

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 41

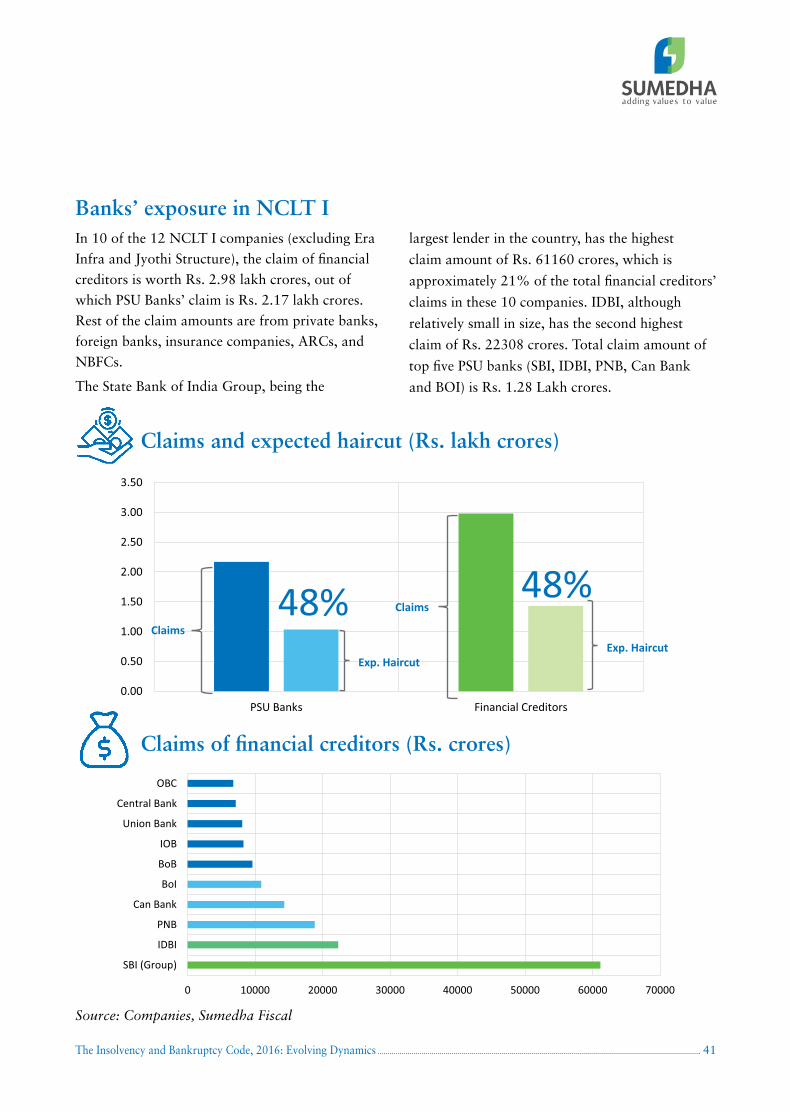

In 10 of the 12 NCLT I companies (excluding Era

Infra and Jyothi Structure), the claim of financial

creditors is worth Rs. 2.98 lakh crores, out of

which PSU Banks’ claim is Rs. 2.17 lakh crores.

Rest of the claim amounts are from private banks,

foreign banks, insurance companies, ARCs, and

NBFCs.

The State Bank of India Group, being the

largest lender in the country, has the highest

claim amount of Rs. 61160 crores, which is

approximately 21% of the total financial creditors’

claims in these 10 companies. IDBI, although

relatively small in size, has the second highest

claim of Rs. 22308 crores. Total claim amount of

top five PSU banks (SBI, IDBI, PNB, Can Bank

and BOI) is Rs. 1.28 Lakh crores.

Banks’ exposure in NCLT I

0 10000 20000 30000 40000 50000 60000 70000

SBI (Group)

IDBI

PNB

Can Bank

BoI

BoB

IOB

Union Bank

Central Bank

OBC

Claims of financial creditors (Rs. crores)

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

48% 48%

PSU Banks Financial Creditors

Exp. Haircut Exp. Haircut

Claims

Claims

Claims and expected haircut (Rs. lakh crores)

Source: Companies, Sumedha Fiscal

Confederation of Indian Industry

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics42

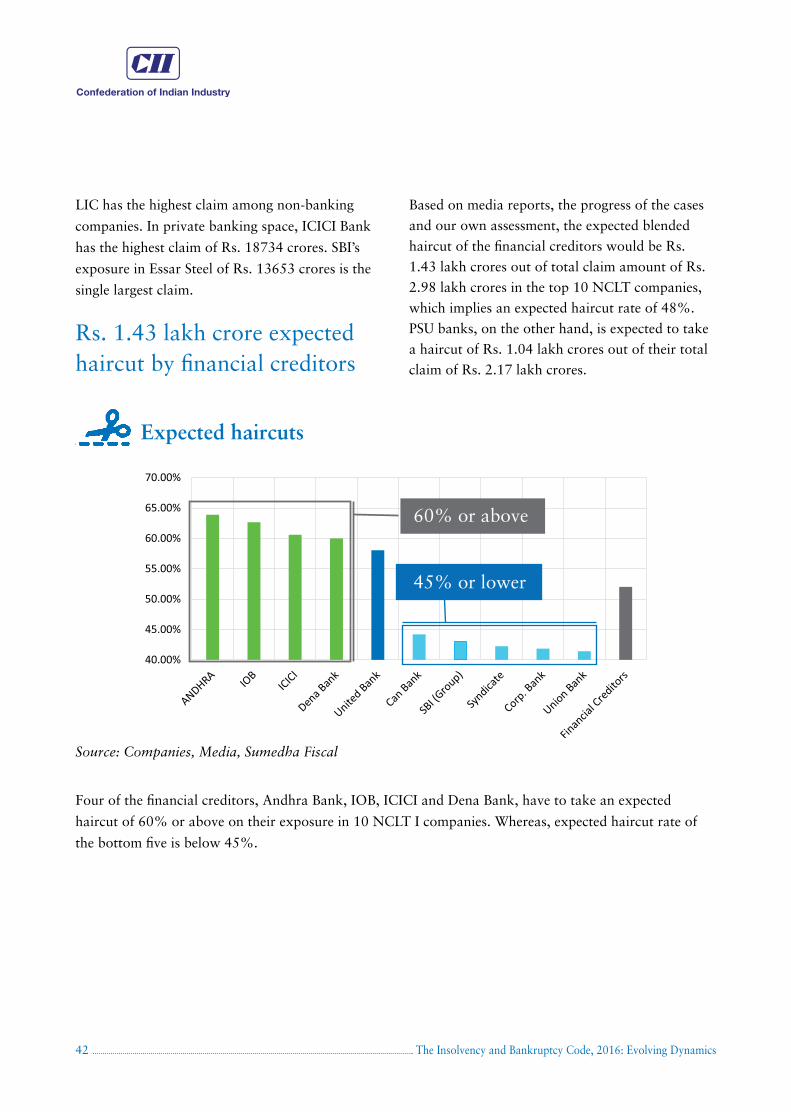

LIC has the highest claim among non-banking

companies. In private banking space, ICICI Bank

has the highest claim of Rs. 18734 crores. SBI’s

exposure in Essar Steel of Rs. 13653 crores is the

single largest claim.

Rs. 1.43 lakh crore expected haircut by financial creditors

Based on media reports, the progress of the cases

and our own assessment, the expected blended

haircut of the financial creditors would be Rs.

1.43 lakh crores out of total claim amount of Rs.

2.98 lakh crores in the top 10 NCLT companies,

which implies an expected haircut rate of 48%.

PSU banks, on the other hand, is expected to take

a haircut of Rs. 1.04 lakh crores out of their total

claim of Rs. 2.17 lakh crores.

Four of the financial creditors, Andhra Bank, IOB, ICICI and Dena Bank, have to take an expected

haircut of 60% or above on their exposure in 10 NCLT I companies. Whereas, expected haircut rate of

the bottom five is below 45%.

Source: Companies, Media, Sumedha Fiscal

40.00%

45.00%

50.00%

55.00%

60.00%

65.00%

70.00%

60% or above

45% or lower

Expected haircuts

Selected Judgements

The Insolvency and Bankruptcy Code, 2016: Evolving Dynamics 43

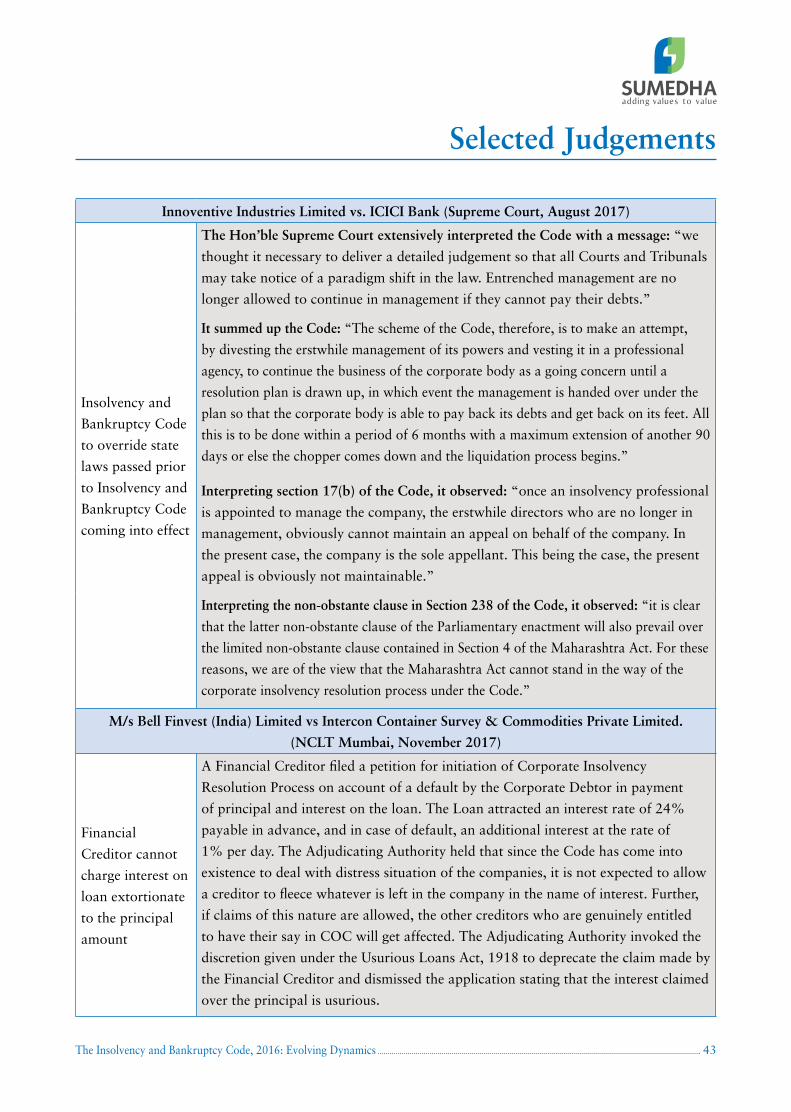

Innoventive Industries Limited vs. ICICI Bank (Supreme Court, August 2017)

Insolvency and

Bankruptcy Code

to override state

laws passed prior

to Insolvency and

Bankruptcy Code

coming into effect

The Hon’ble Supreme Court extensively interpreted the Code with a message: “we

thought it necessary to deliver a detailed judgement so that all Courts and Tribunals

may take notice of a paradigm shift in the law. Entrenched management are no

longer allowed to continue in management if they cannot pay their debts.”

It summed up the Code: “The scheme of the Code, therefore, is to make an attempt,

by divesting the erstwhile management of its powers and vesting it in a professional

agency, to continue the business of the corporate body as a going concern until a

resolution plan is drawn up, in which event the management is handed over under the

plan so that the corporate body is able to pay back its debts and get back on its feet. All

this is to be done within a period of 6 months with a maximum extension of another 90

days or else the chopper comes down and the liquidation process begins.”

Interpreting section 17(b) of the Code, it observed: “once an insolvency professional

is appointed to manage the company, the erstwhile directors who are no longer in

management, obviously cannot maintain an appeal on behalf of the company. In

the present case, the company is the sole appellant. This being the case, the present

appeal is obviously not maintainable.”

Interpreting the non-obstante clause in Section 238 of the Code, it observed: “it is clear

that the latter non-obstante clause of the Parliamentary enactment will also prevail over

the limited non-obstante clause contained in Section 4 of the Maharashtra Act. For these

reasons, we are of the view that the Maharashtra Act cannot stand in the way of the

corporate insolvency resolution process under the Code.”

M/s Bell Finvest (India) Limited vs Intercon Container Survey & Commodities Private Limited.

(NCLT Mumbai, November 2017)