Embed Size (px)

Citation preview

THE INFORMATION QUALITY OF DERIVATIVE DISCLOSURES IN CORPORATE ANNUAL REPORTS OF AUSTRALIAN FIRMS IN THE

EXTRACTIVE INDUSTRIES

Mohamat Sabri Hassan B.Ac (Hons.) (Universiti Kebangsaan Malaysia),

M.Social Science (Southampton)

A dissertation submitted for the degree of Doctor of Philosophy within the School of Accountancy at Queensland University of Technology

2004

ii

Keywords: Disclosure quality; transparency; disclosure index; financial instruments;

derivative instruments; market value; extractives industries.

iii

ABSTRACT

Recent events in the business world have focused attention on the importance of high

quality financial reporting. Of particular interest is where the collapse of prominent

companies such as Baring Plc. was due to the company’s involvement with derivative

instruments. In Australia, some derivative instruments are not recognised in the

balance sheet. However, the Australian accounting standard AASB 1033 Presentation

and Disclosure of Financial Instruments requires extensive disclosures to overcome

the lack of guidance with regard to the recognition and measurement. Therefore,

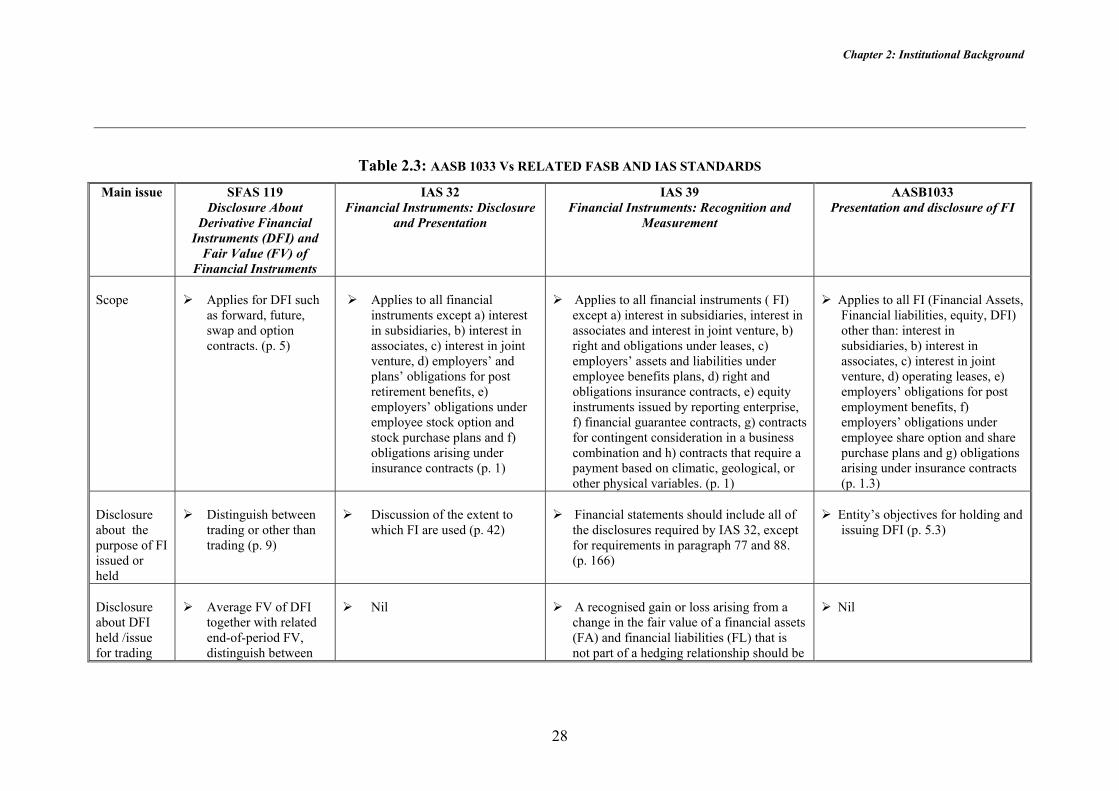

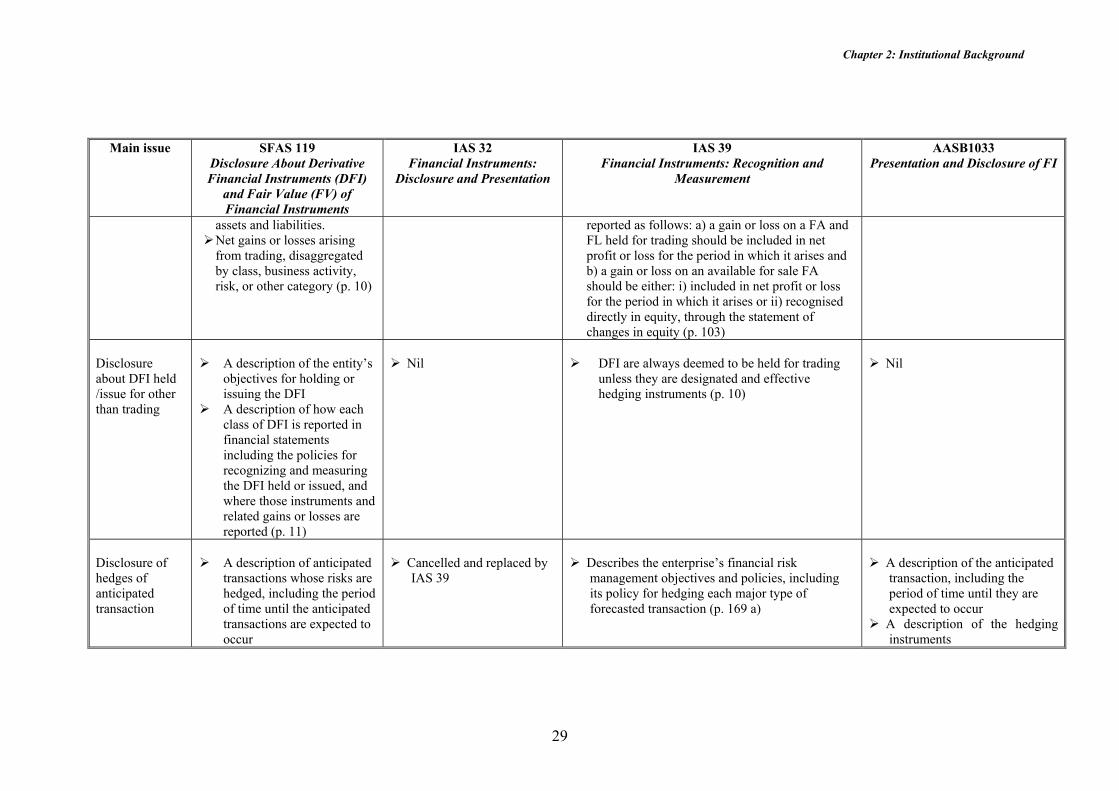

AASB 1033 may be regarded as a high quality disclosure standard.

This thesis investigates the transparency or information quality of derivative

disclosures of Australian firms in the extractive industries using 1998 to 2001

financial reports. The extractive industries play a major role in the Australian

economy, where they generated exports worth more than A$30billion in 2000 to 2002

(Department of Foreign Affairs and Trade, 2003a and 2003b). Further, firms in the

extractive industries extensively use derivative instruments for hedging purposes

(Berkman, Bradbury, Hancock and Innes, 1997). The objective of this study is, first,

to examine the relationship between the transparency or disclosure quality of

derivative information and firm characteristics. Second, this study investigates the

value relevance of derivative disclosures in particularly hedge information, net fair

value information and risk information. Quality is measured based on a disclosure

index developed from AASB 1033 Presentation and Disclosure of Financial

Instruments. A finding of concern is that the majority of firms in this study provide

less than complete information and therefore enforcement power is required to ensure

compliance (Kothari, 2000)

Prior studies have related disclosure quality of accounting information with firm

characteristics but no attempt has been made to relate those characteristics with the

disclosure quality of derivative instruments. The current study contributes to the

literature by examining the relationship between firm characteristics and the quality of

derivative disclosures. Firm characteristics investigated are size, profitability, price-

iv

earnings ratio, market-to-book ratio, research and development activity, auditor, debt-

to-equity ratio and type of extractive firm. This study finds that the variables, firm

size, price-earnings and debt-to-equity ratios are associated with the disclosure quality

of derivative information. To a lesser extent, the variables, market-to-book ratio and

profitability, are also associated with disclosure quality.

High disclosure quality has been argued to lead to a reduction in the cost of debt

(Sengupta, 1998) and equity (Botosan, 1997), resulting in higher security prices

(Miller and Bahnson, 2002). The results of this study indicate that high quality

derivative information, as represented by the disclosure index, is value relevant.

Market participants do consider hedge information and risk information components

as important for decision-making. However, examining the specific information

disclosed in the financial statements indicate that some of the disclosed information

such as the unrealised gain or loss on financial assets and liabilities and off-balance

sheet derivative financial instruments are not significant.

These results contribute to the value relevance literature as this study focuses on the

extractive industries which have been neglected in the literature. This study provides

important information for standard setters and regulators for future directions in

developing accounting standards and is particularly relevant for the impending

adoption of International Accounting Standards.

v

Table of Contents

Page

ABSTRACT ......................................................................................................................................... III ACKNOWLEDGEMENTS ...............................................................................................................XII CHAPTER 1 INTRODUCTION .....................................................................................................1

1.1 PURPOSE OF THE STUDY.........................................................................................................1 1.2 PRIOR RESEARCH AND THE MAIN FINDINGS OF THE THESIS...................................................3 1.3 MOTIVATION..........................................................................................................................6 1.4 PLAN OF THESIS .....................................................................................................................9

CHAPTER 2 INSTITUTIONAL BACKGROUND .....................................................................12 2.1 RISK MANAGEMENT.............................................................................................................12

2.1.1 To Hedge or Not to Hedge?............................................................................................14 2.2 INTERNATIONAL ACCOUNTING PRACTICES ..........................................................................16

2.2.1 Financial Accounting Standard Board ...........................................................................17 2.2.1.1 SFAS 133 Accounting for Derivative Instruments and Hedging Activities. ............................ 19

2.2.2 International Accounting Standards Board ....................................................................20 2.2.2.1 IAS 32 Financial Instruments: Disclosure and Presentation..................................................... 20 2.2.2.2 IAS 39: Financial Instruments: Recognition and Measurement ............................................... 22

2.2.3 Accounting for Financial Instruments in Australia ........................................................23 2.2.3.1 AASB 1033 Presentation and Disclosure of Financial Instruments ......................................... 23

2.3 FAIR VALUE ACCOUNTING...................................................................................................31 2.4 STUDIES OF ACCOUNTING PRACTICES IN AUSTRALIA ..........................................................35 2.5 RISK MANAGEMENT PRACTICES IN THE EXTRACTIVE INDUSTRIES ......................................37 2.6 SUMMARY............................................................................................................................39

CHAPTER 3 LITERATURE REVIEW: DISCLOSURE QUALITY........................................41 3.1 DISCLOSURE QUALITY: THE DEFINITIONS ...........................................................................42 3.2 DISCLOSURE QUALITY: REGULATION, ENFORCEMENT AND COMPLIANCE...........................44 3.3 STUDIES ON DISCLOSURE QUALITY .....................................................................................46

3.3.1 Disclosure Quality of Accounting Standards..................................................................46 3.3.2 Disclosure Quality of Accounting Information and the Impact on Firms.......................48

3.3.2.1 Disclosure Quality and Firms Characteristics .......................................................................... 48 3.3.2.2 Disclosure Quality of Specific Information.............................................................................. 52

3.3.3 Disclosure Quality of Accounting Information and Benefits to the Investors.................54 3.3.4 Disclosure Quality of Derivative Information ................................................................57

3.4 SUMMARY............................................................................................................................59 CHAPTER 4 LITERATURE REVIEW: DERIVATIVE DISCLOSURES AND VALUE RELEVANCE STUDIES.....................................................................................................................60

4.1 DISCLOSURE QUALITY OF ACCOUNTING INFORMATION AND INVESTORS’ DECISIONS .........60 4.2 DISCLOSURE AND CAPITAL MARKETS RESEARCH................................................................62

4.2.1 Capital Markets Research ..............................................................................................62 4.2.2 Relevance and Reliability of Accounting Information and Capital Markets Research...65 4.2.3 Value Relevance Studies .................................................................................................68

4.2.3.1 Other Value Relevance Studies ................................................................................................ 69 4.2.3.2 Research on Value Relevance in Australia............................................................................... 70

4.3 VALUE RELEVANCE OF FINANCIAL INSTRUMENTS...............................................................73 4.3.1 Studies on Value Relevance of Fair Value Disclosures..................................................73 4.3.2 Studies on Value Relevance of Derivative Financial Instruments Disclosures ..............76

4.4 SUMMARY............................................................................................................................78 CHAPTER 5 RESEARCH QUESTIONS.....................................................................................79

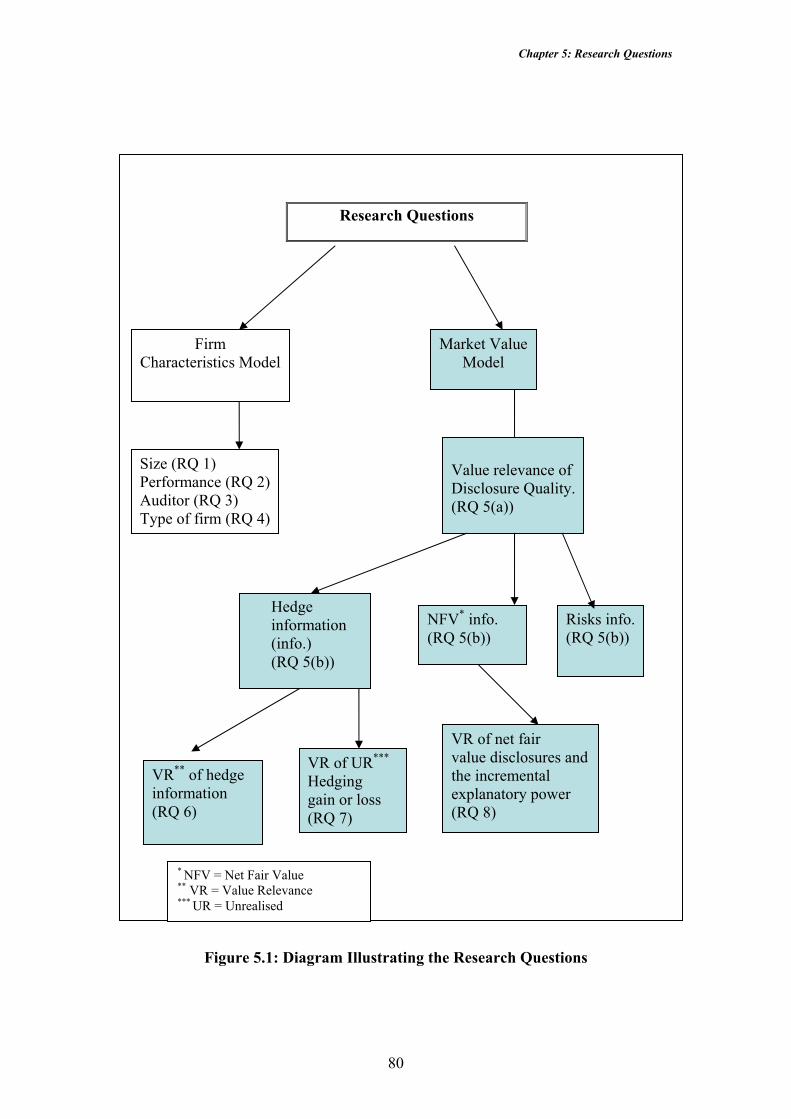

5.1 DISCLOSURE QUALITY OF DERIVATIVE INFORMATION AND FIRM CHARACTERISTICS .........81

vi

5.1.1 Size..................................................................................................................................83 5.1.2 High Performance Firms................................................................................................84 5.1.3 Auditor............................................................................................................................85 5.1.4 Type of Firm in the Extractive Industries. ......................................................................85

5.2 VALUE RELEVANCE OF DERIVATIVE DISCLOSURES .............................................................86 5.2.1 Disclosure Quality and the Market Value of Firms........................................................86 5.2.2 Value Relevance of Disclosure of Hedges of Anticipated Transactions .........................88 5.2.3 Value Relevance of Fair Value Disclosures ...................................................................91

5.3 SUMMARY............................................................................................................................92 CHAPTER 6 RESEARCH DESIGN, DATA COLLECTION AND DESCRIPTIVE STATISTICS ...................................................................................................................................93

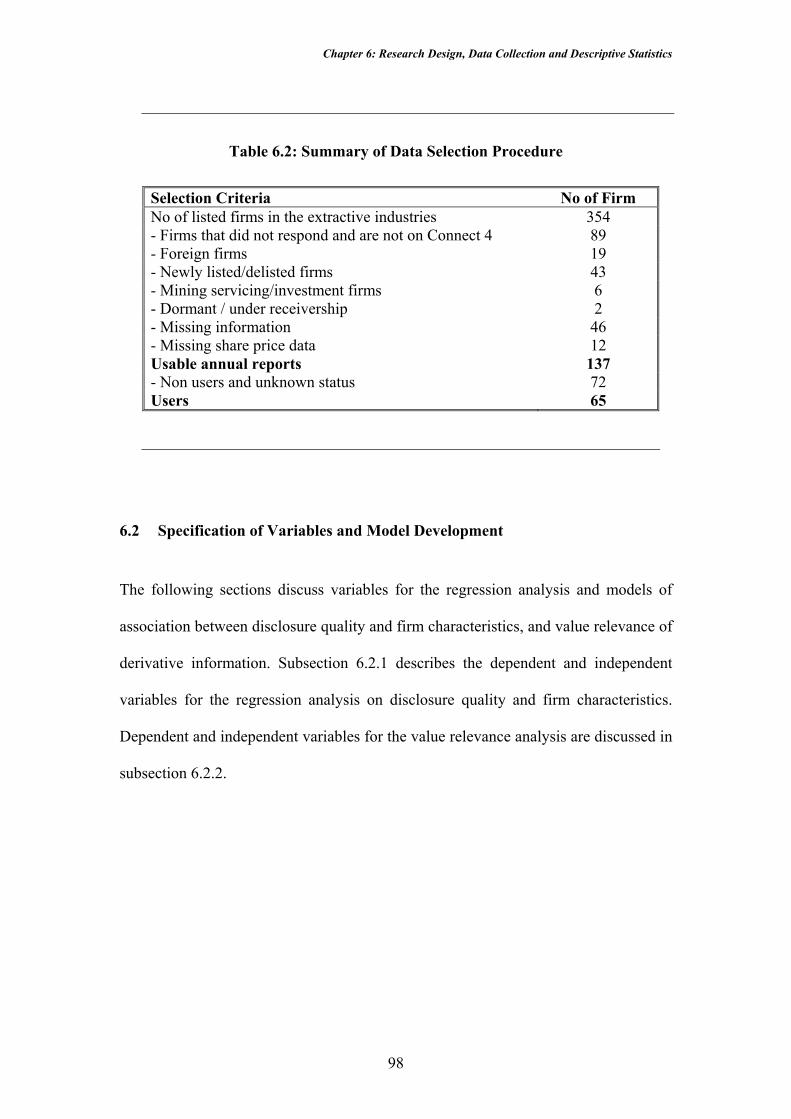

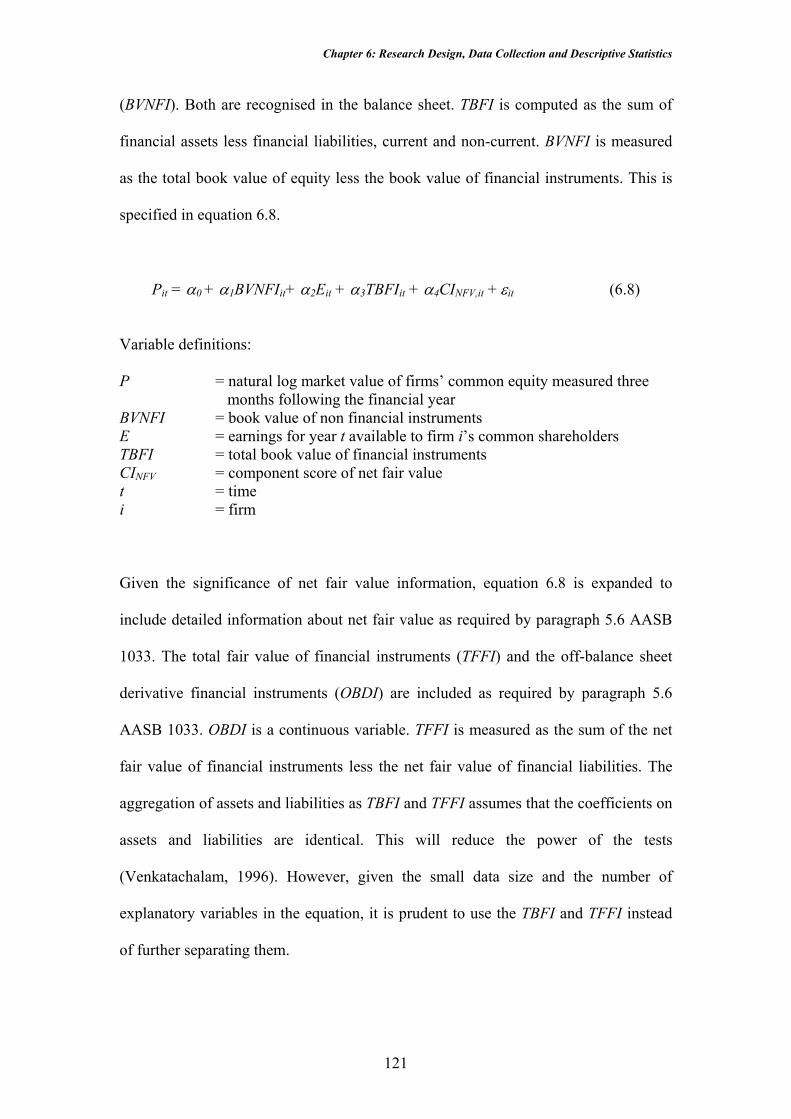

6.1 DATA SELECTION AND TEST PERIOD....................................................................................93 6.2 SPECIFICATION OF VARIABLES AND MODEL DEVELOPMENT................................................98

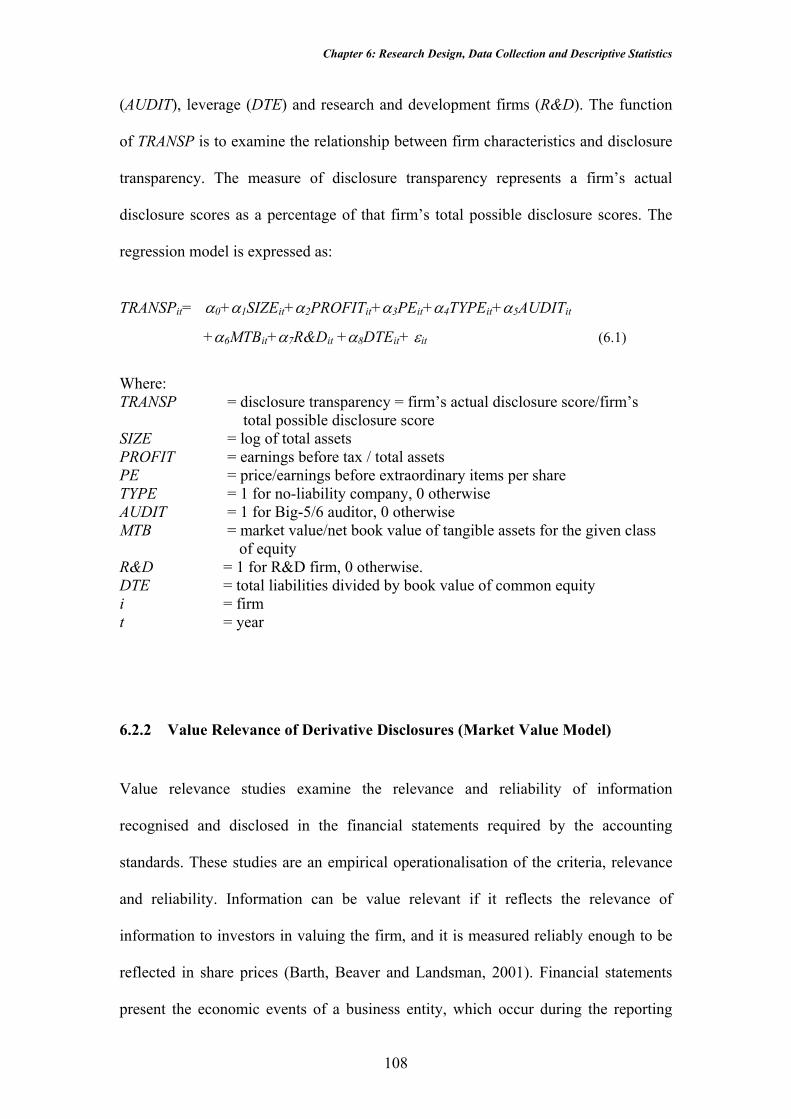

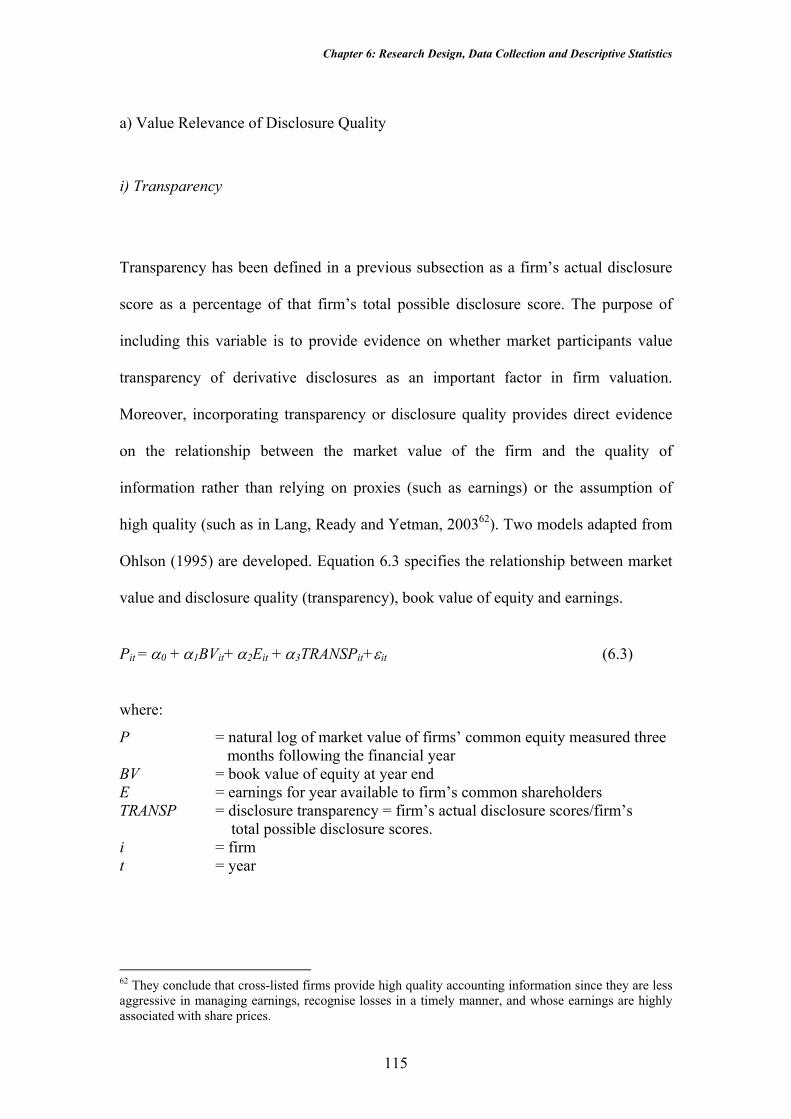

6.2.1 Disclosure Quality and Firm Characteristics (Firm Characteristics Model) ................99 6.2.1.1 Variables .................................................................................................................................. 99 6.2.1.2 Regression Model................................................................................................................... 107

6.2.2 Value Relevance of Derivative Disclosures (Market Value Model) .............................108 6.2.2.1 Dependent Variable................................................................................................................ 112 6.2.2.2 Independent Variables............................................................................................................ 112

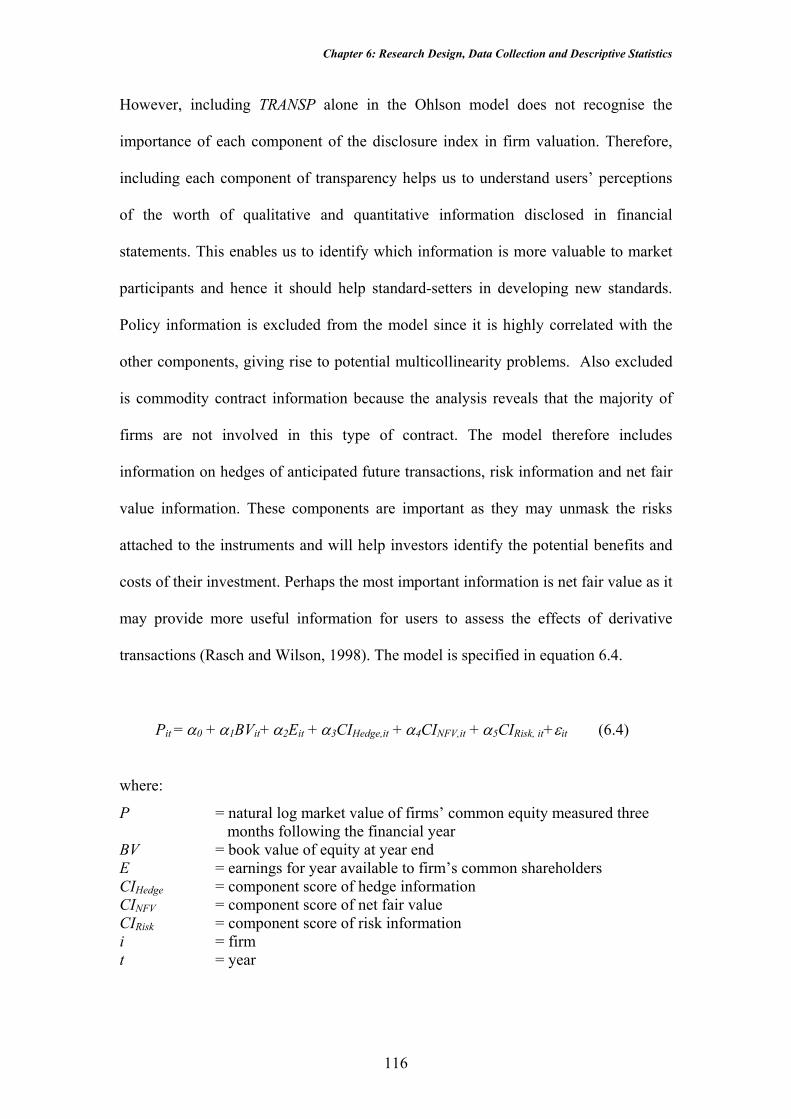

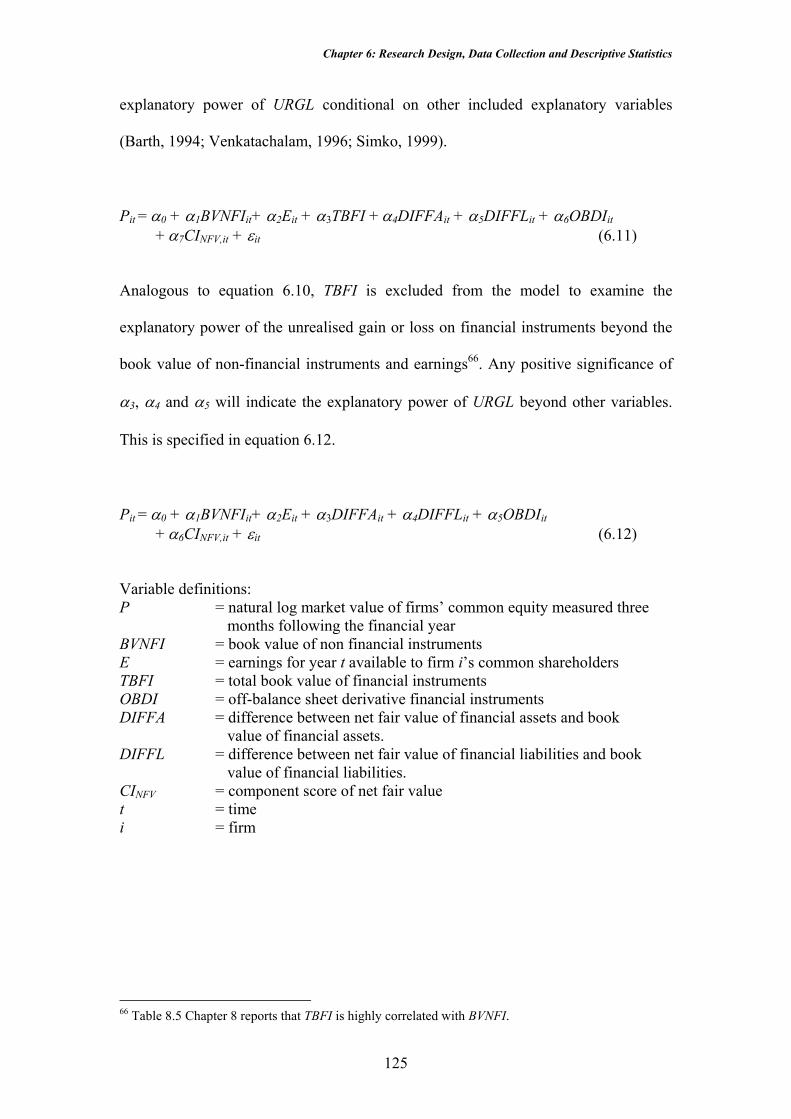

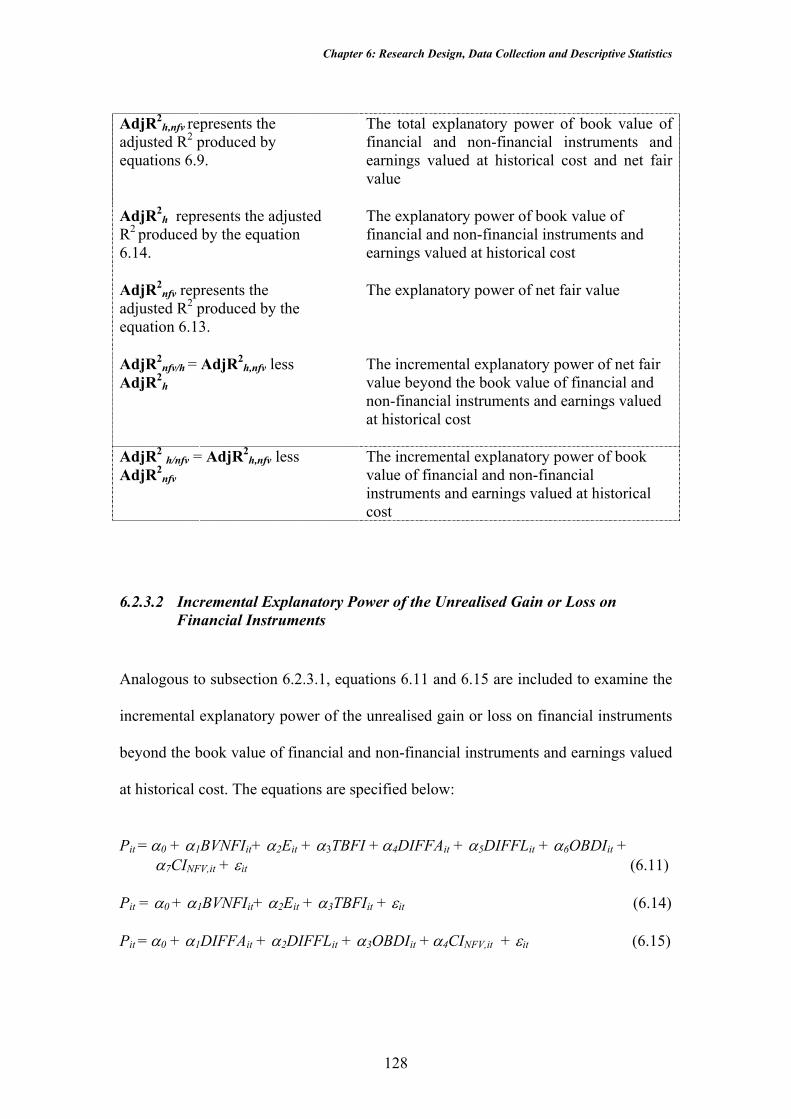

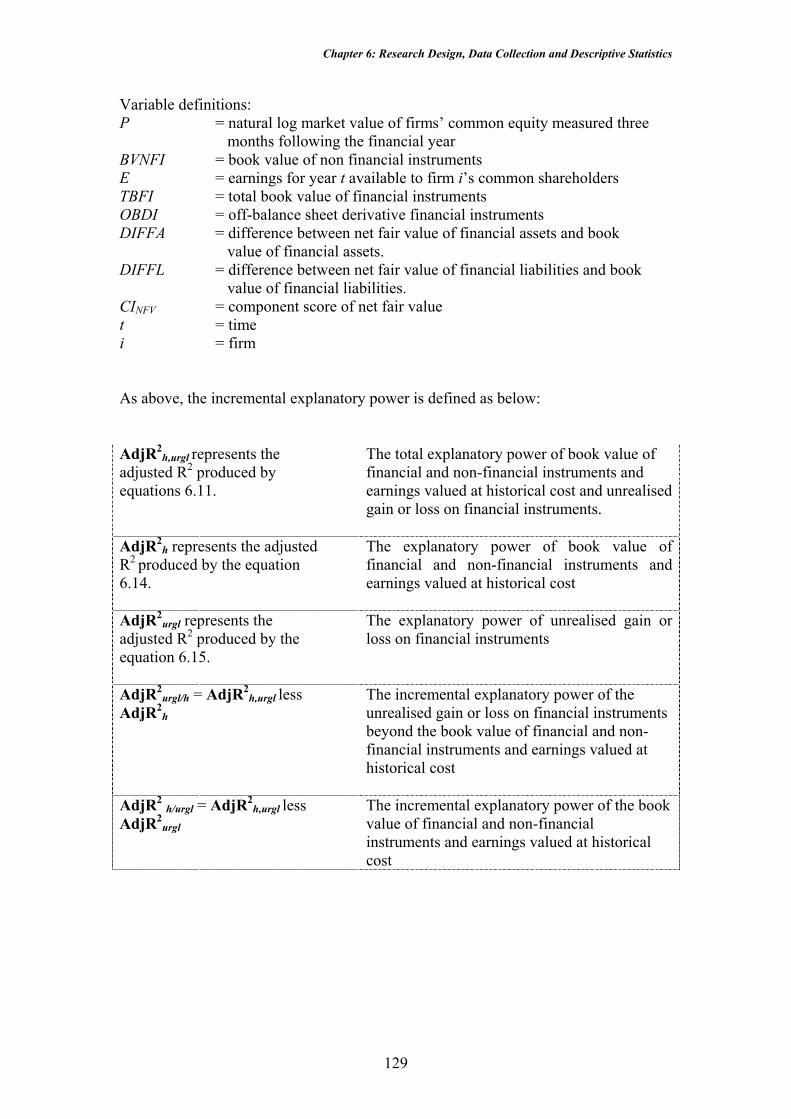

6.2.3 Incremental Explanatory Power of the Net Fair Value and the Unrealised Gain or Loss on Financial Instruments Beyond the Book Value of Financial and Non-Financial Instruments and Earnings Valued at Historical Cost .....................................................................................126

6.2.3.1 Incremental Explanatory Power of Net Fair Value................................................................. 126 6.2.3.2 Incremental Explanatory Power of the Unrealised Gain or Loss on Financial Instruments ... 128

6.3 ESTIMATION PROCEDURES .................................................................................................130 6.4 DESCRIPTIVE STATISTICS ...................................................................................................132

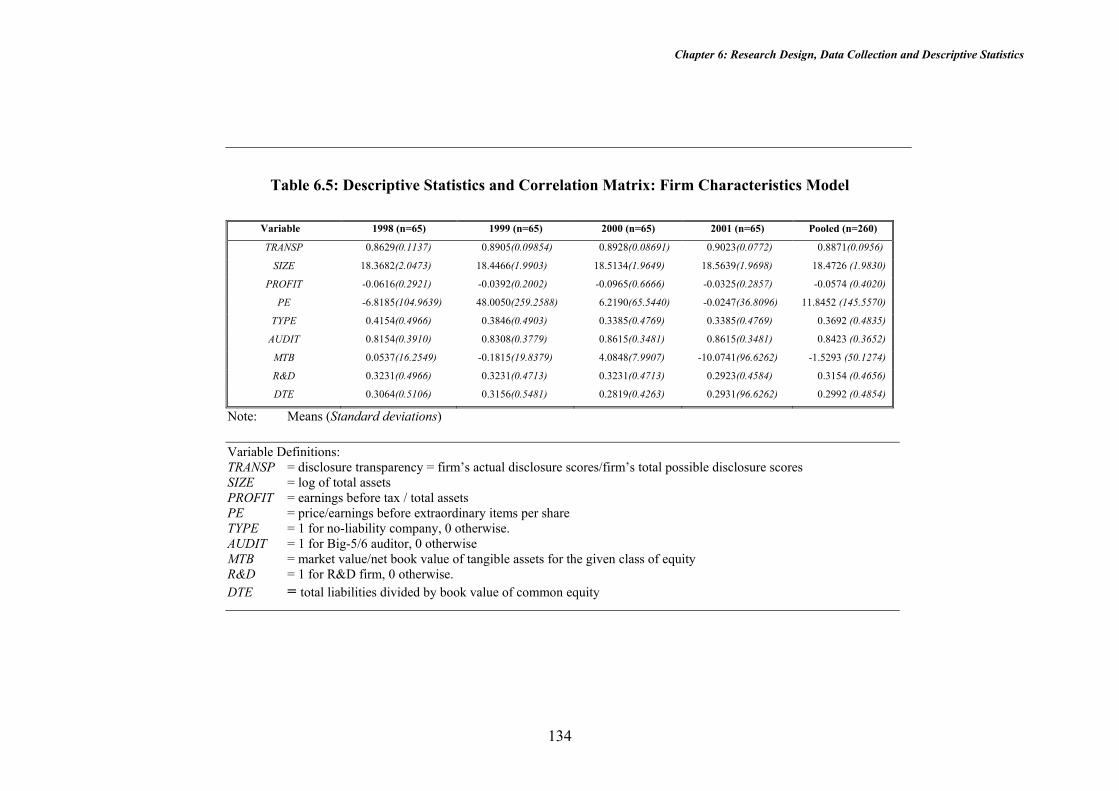

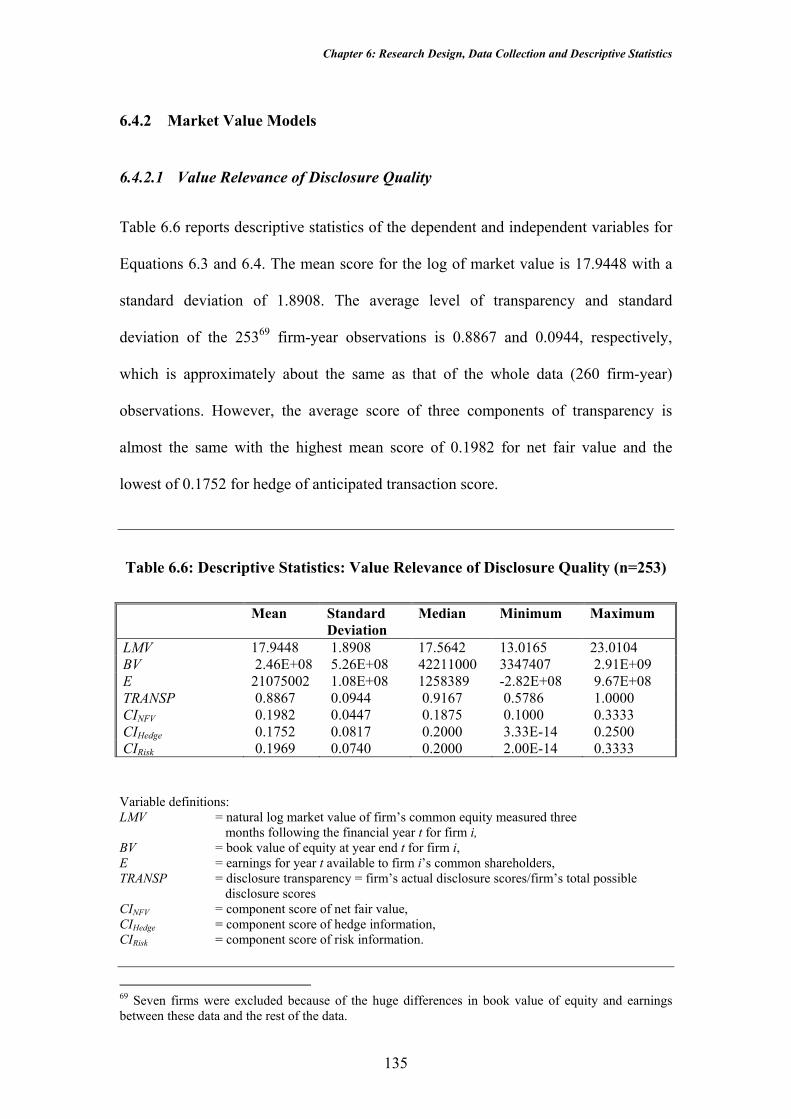

6.4.1 Firm Characteristics Model .........................................................................................132 6.4.2 Market Value Models....................................................................................................135

6.4.2.1 Value Relevance of Disclosure Quality.................................................................................. 135 6.4.2.2 Value Relevance of Hedge Transaction, Net Fair Value and the Unrealised Gain or Loss on Financial Instruments ............................................................................................................................. 136

6.5 SUMMARY..........................................................................................................................136 CHAPTER 7 RESULTS: DISCLOSURE QUALITY AND FIRM CHARACTERISTICS...138

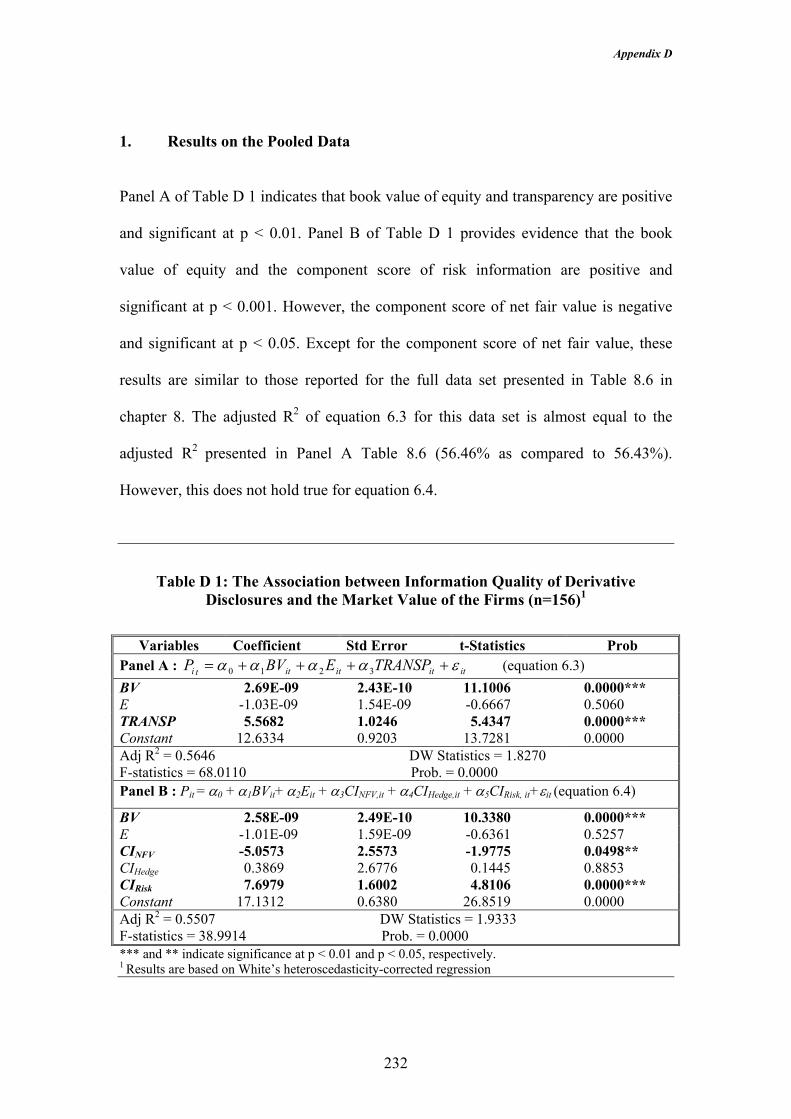

7.1 DIAGNOSTIC TESTS ............................................................................................................138 7.1.1 Normality Test ..............................................................................................................139 7.1.2 Autocorrelation Test .....................................................................................................139 7.1.3 Heteroscedasticity Test.................................................................................................140 7.1.4 Multicollinearity Test ...................................................................................................141

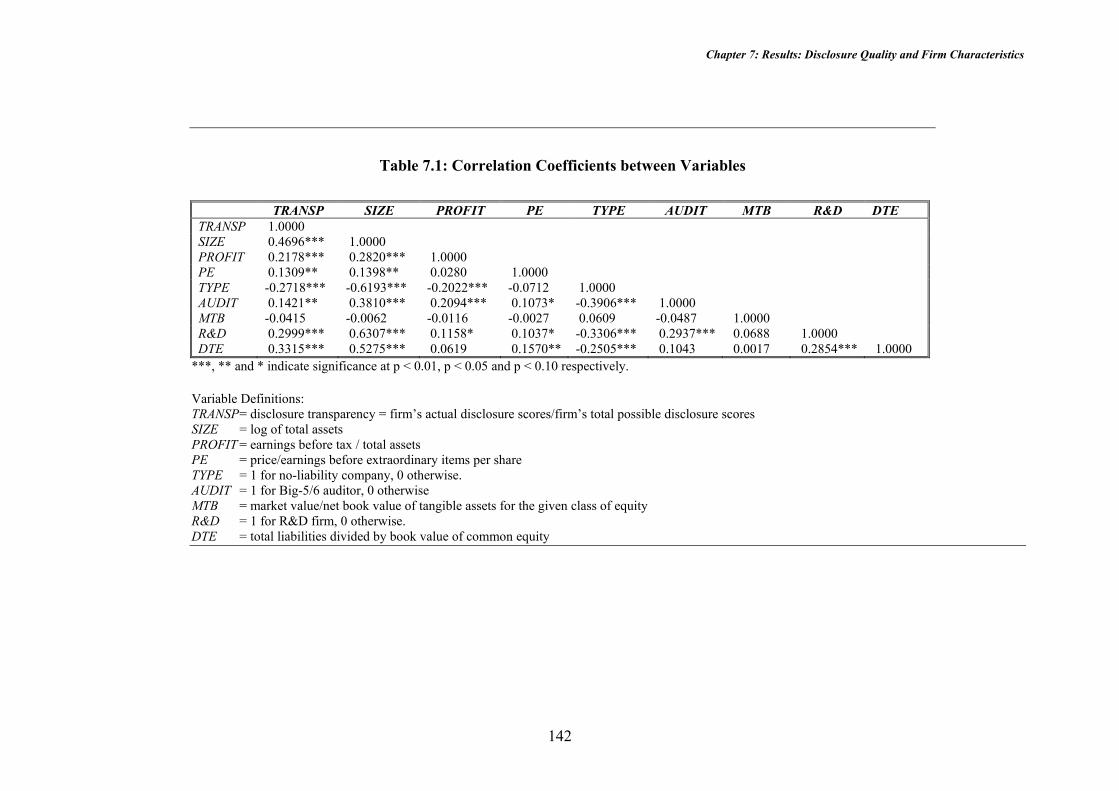

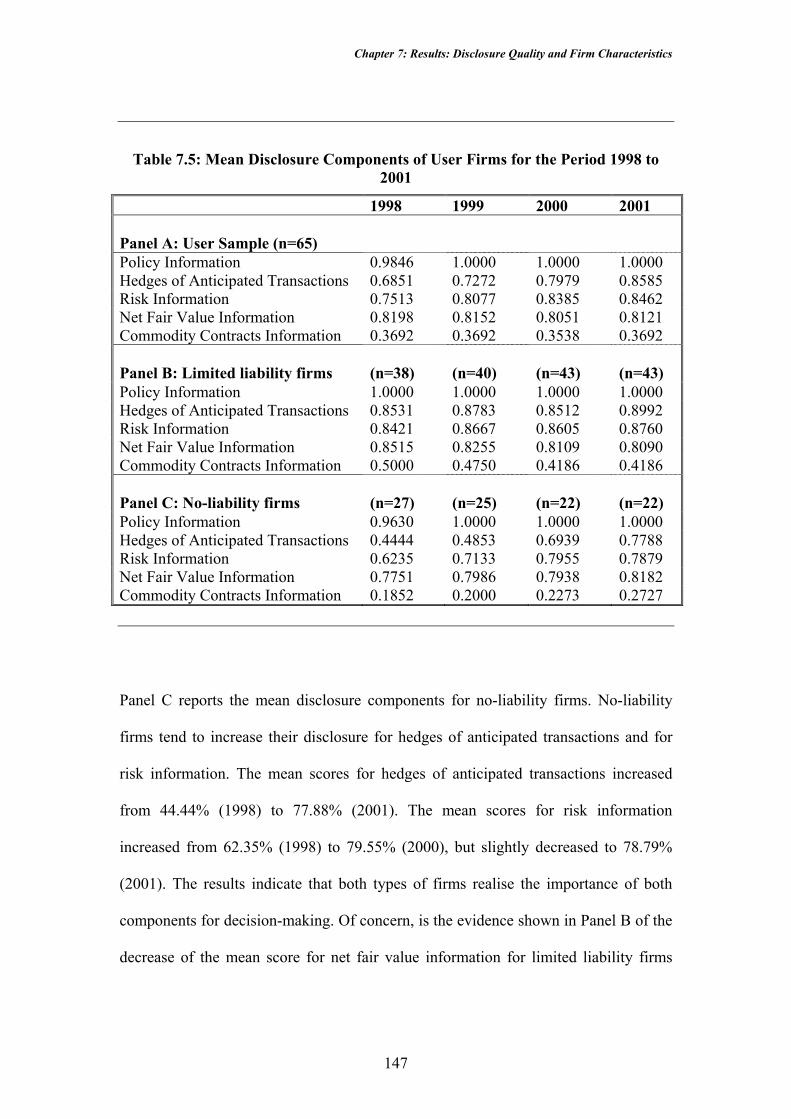

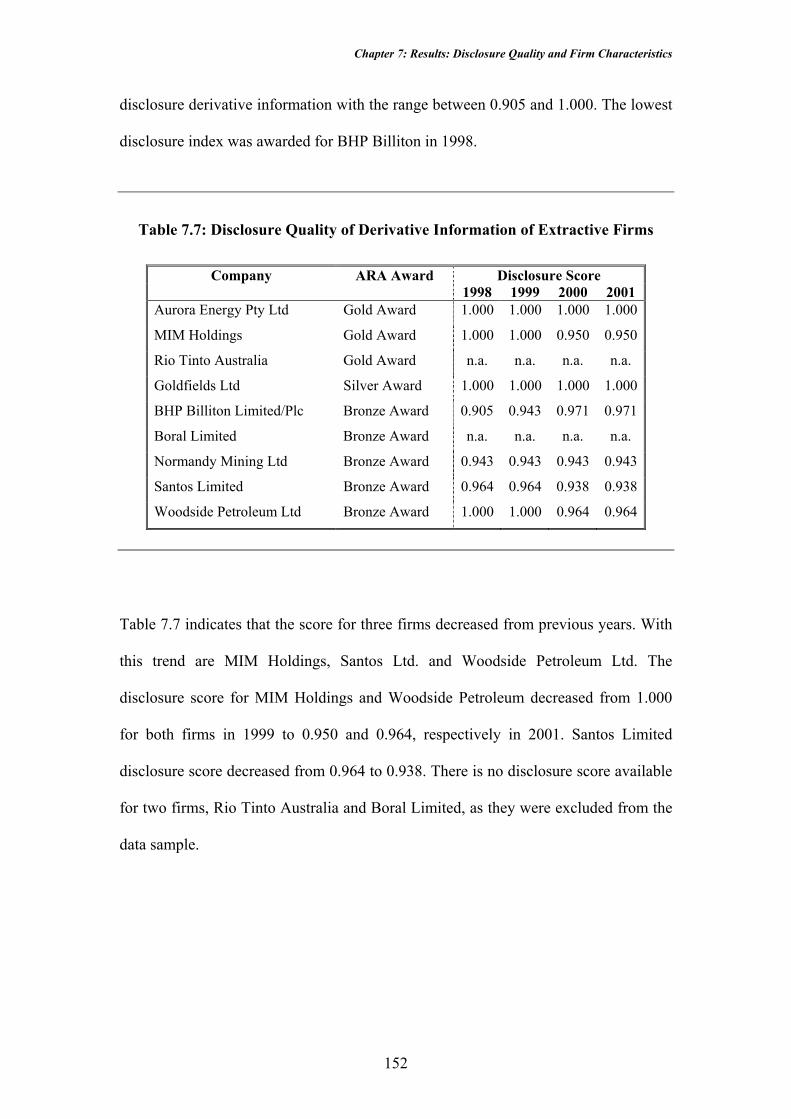

7.2 DESCRIPTIVE RESULTS.......................................................................................................143 7.2.1 Firms’ Disclosure Scores .............................................................................................143 7.2.2 Disclosure Components ................................................................................................145

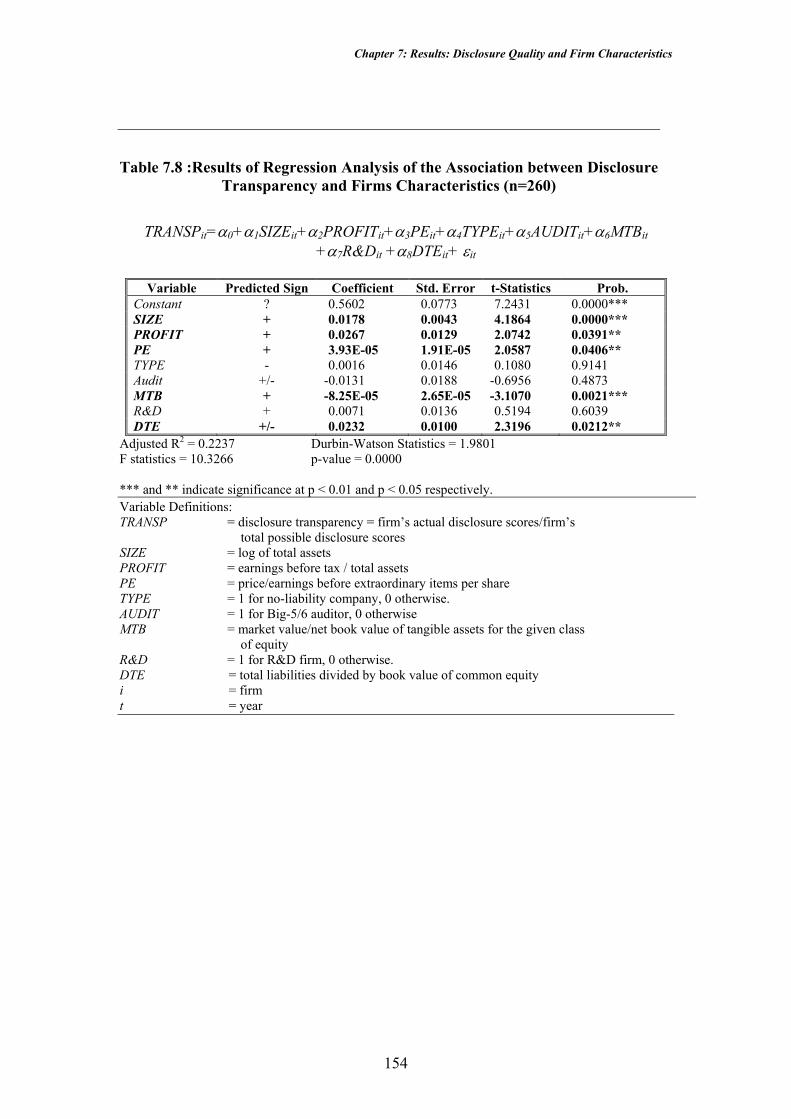

7.3 VALIDITY OF THE DISCLOSURE QUALITY SCORE (DISCLOSURE INDEX).............................148 7.4 MULTIPLE REGRESSION RESULTS ......................................................................................153

7.4.1 Standard Regression Procedures..................................................................................153 7.4.2 Sensitivity Analyses.......................................................................................................155

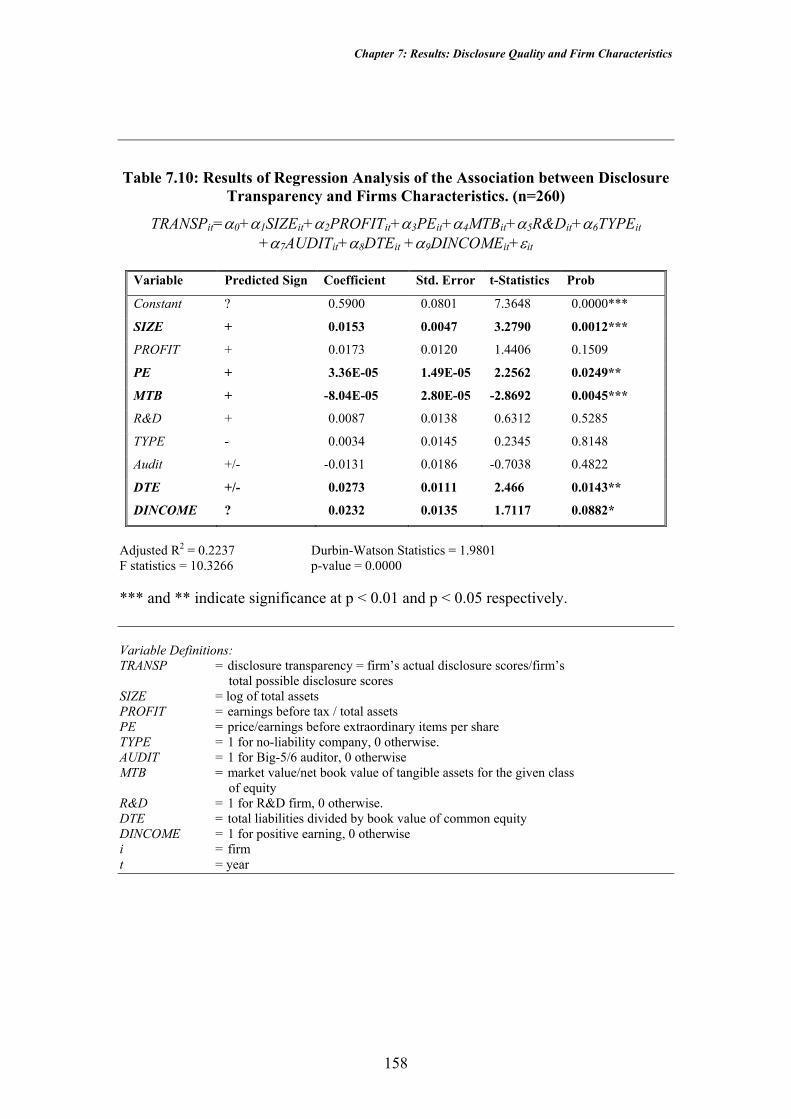

7.4.2.1 Ranked Regression................................................................................................................. 155 7.4.2.2 Profit Vs Loss Making Firms ................................................................................................. 157

7.5 DISCUSSION AND ANALYSIS...............................................................................................160 7.5.1 Disclosure Quality ........................................................................................................160 7.5.2 Comparison with Prior Studies ....................................................................................162

7.6 SUMMARY..........................................................................................................................166 CHAPTER 8 RESULTS: VALUE RELEVANCE OF DERIVATIVE DISCLOSURES .......168

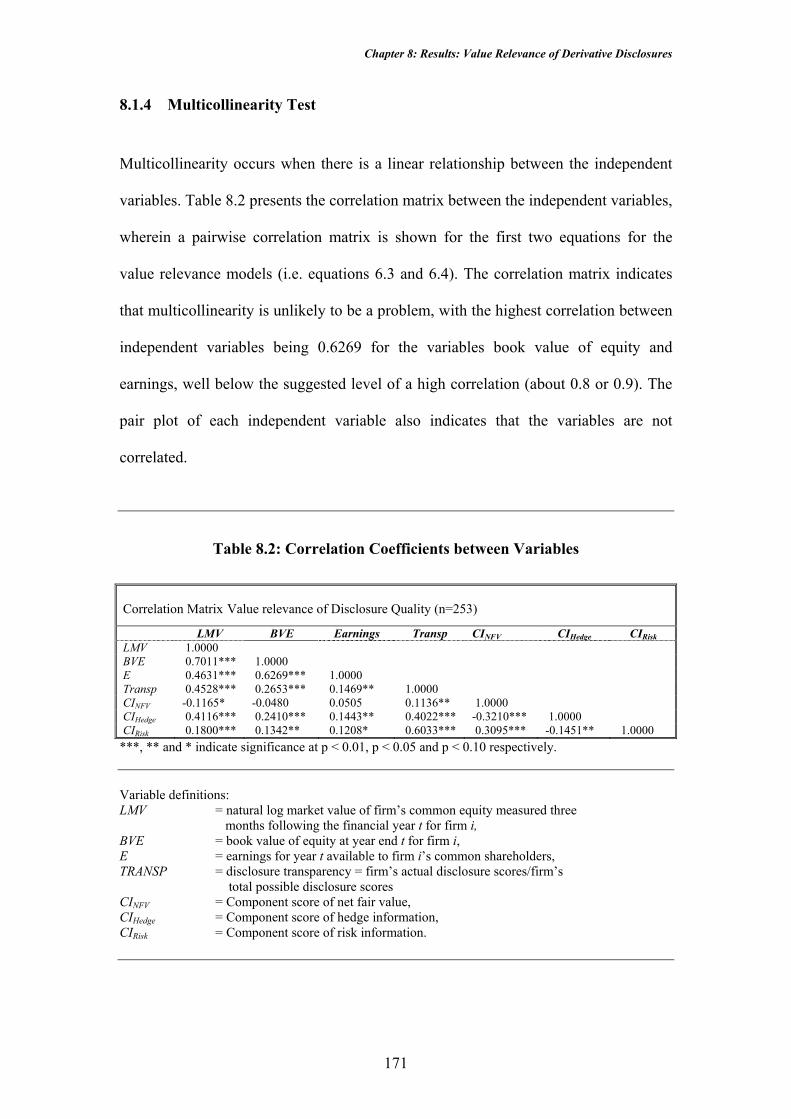

8.1 DIAGNOSTIC TESTS ............................................................................................................169 8.1.1 Normality Tests.............................................................................................................169 8.1.2 Autocorrelation Tests ...................................................................................................170 8.1.3 Heteroscedasticity Tests ...............................................................................................170 8.1.4 Multicollinearity Test ...................................................................................................171

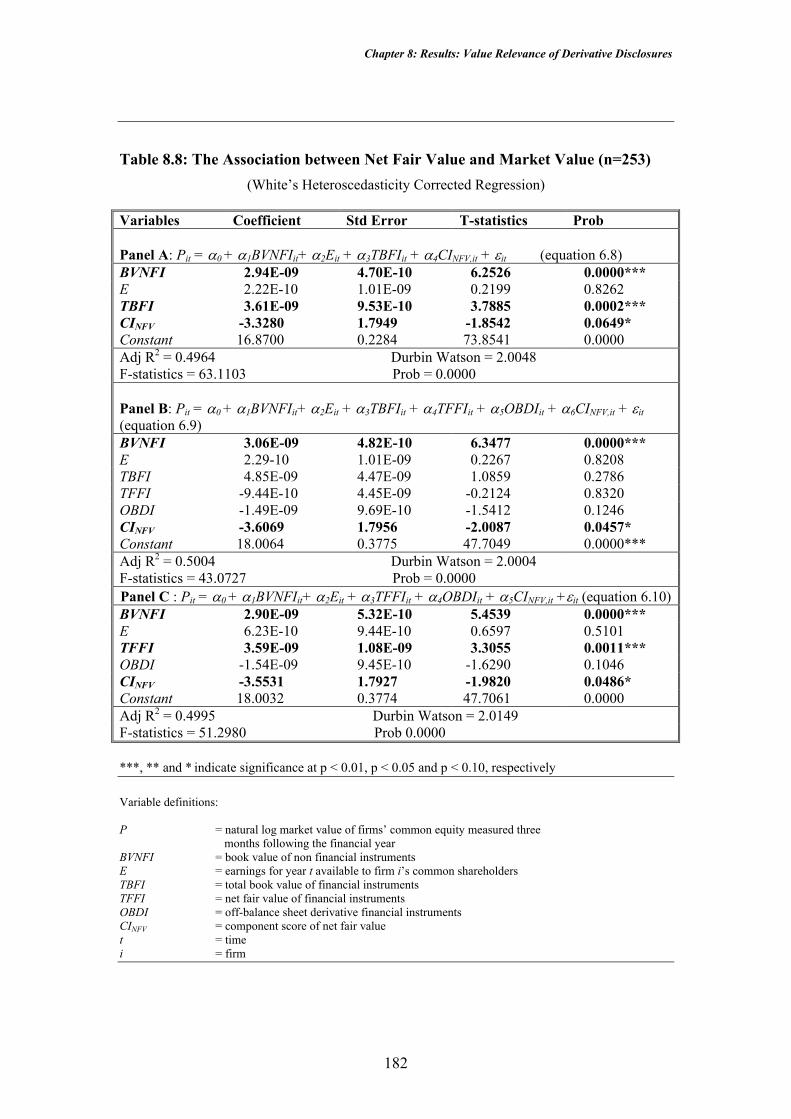

8.2 MULTIPLE REGRESSION RESULTS ......................................................................................176

vii

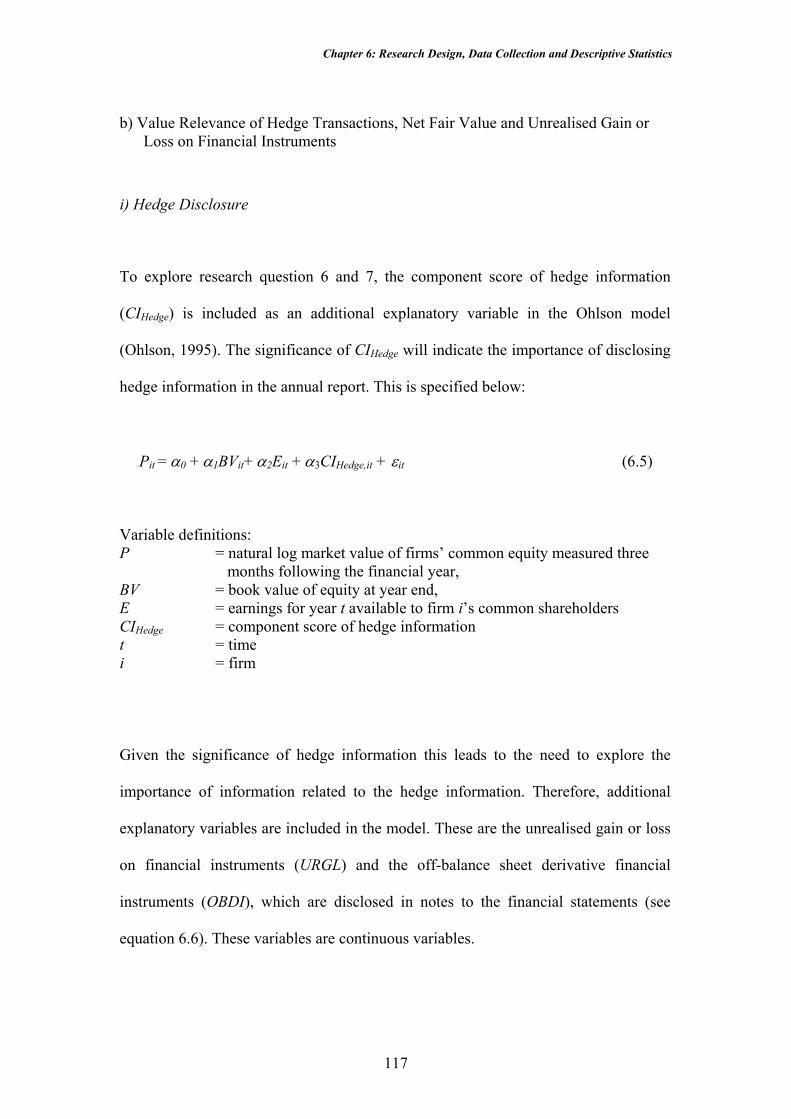

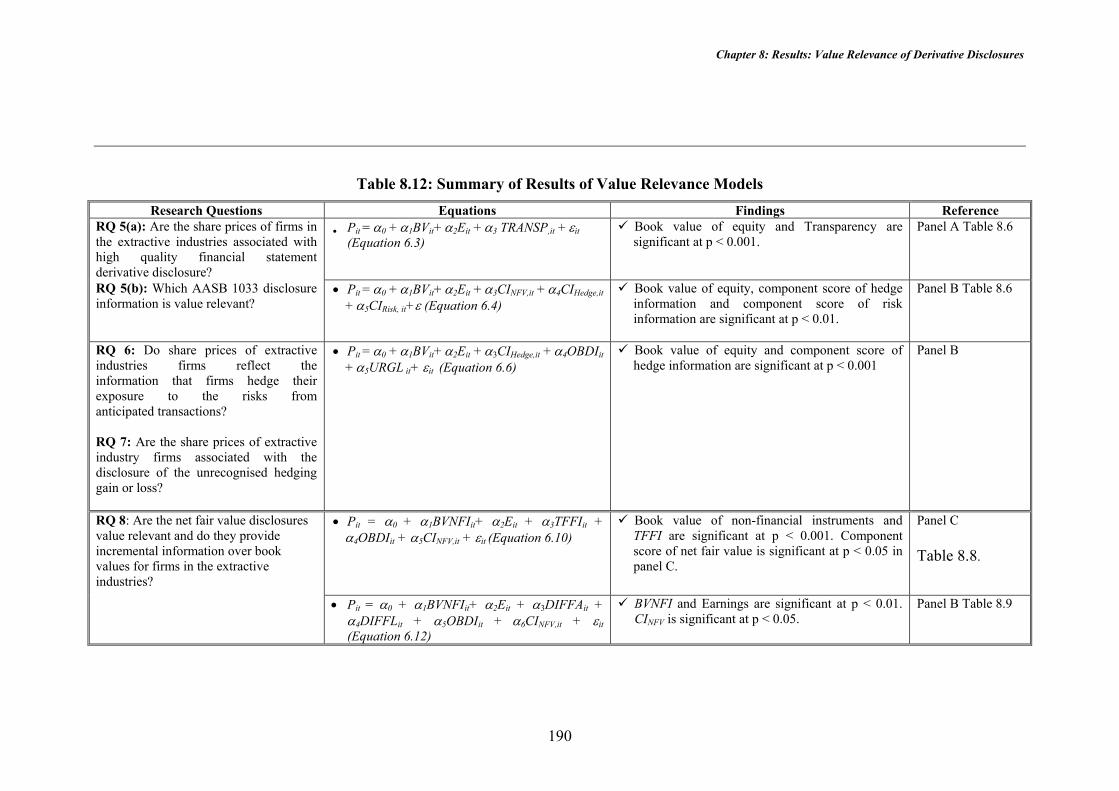

8.2.1 Disclosure Quality of Derivative Information and the Market Value of Firms ............176 8.2.2 Value Relevance of Hedge Disclosures ........................................................................179 8.2.3 Value Relevance of Net Fair Value Disclosures...........................................................180 8.2.4 Value Relevance of the Unrealised Gain or Loss of Financial Instruments .................183

8.3 INCREMENTAL EXPLANATORY POWER OF NET FAIR VALUE AND THE UNREALISED GAIN OR LOSS OF FINANCIAL INSTRUMENTS ..................................................................................................186 8.4 DISCUSSION OF THE RESULTS.............................................................................................189

8.4.1 Disclosure Quality of Derivative Information and the Market Value of Firms ............191 8.4.2 Value Relevance of Hedge Disclosures ........................................................................192 8.4.3 Value Relevance and the Incremental Explanatory Power of Net Fair Value Disclosure and the Unrealised Gain or Loss of Financial Instruments........................................................192

8.5 SUMMARY..........................................................................................................................195 CHAPTER 9 SUMMARY AND CONCLUSIONS ....................................................................196

9.1 SUMMARY..........................................................................................................................196 9.1.1 Firm Characteristics Model .........................................................................................196 9.1.2 Market Value Model .....................................................................................................199

9.2 CONTRIBUTIONS OF THE STUDY .........................................................................................202 9.3 LIMITATIONS......................................................................................................................203 9.4 DIRECTIONS FOR FUTURE RESEARCH.................................................................................205

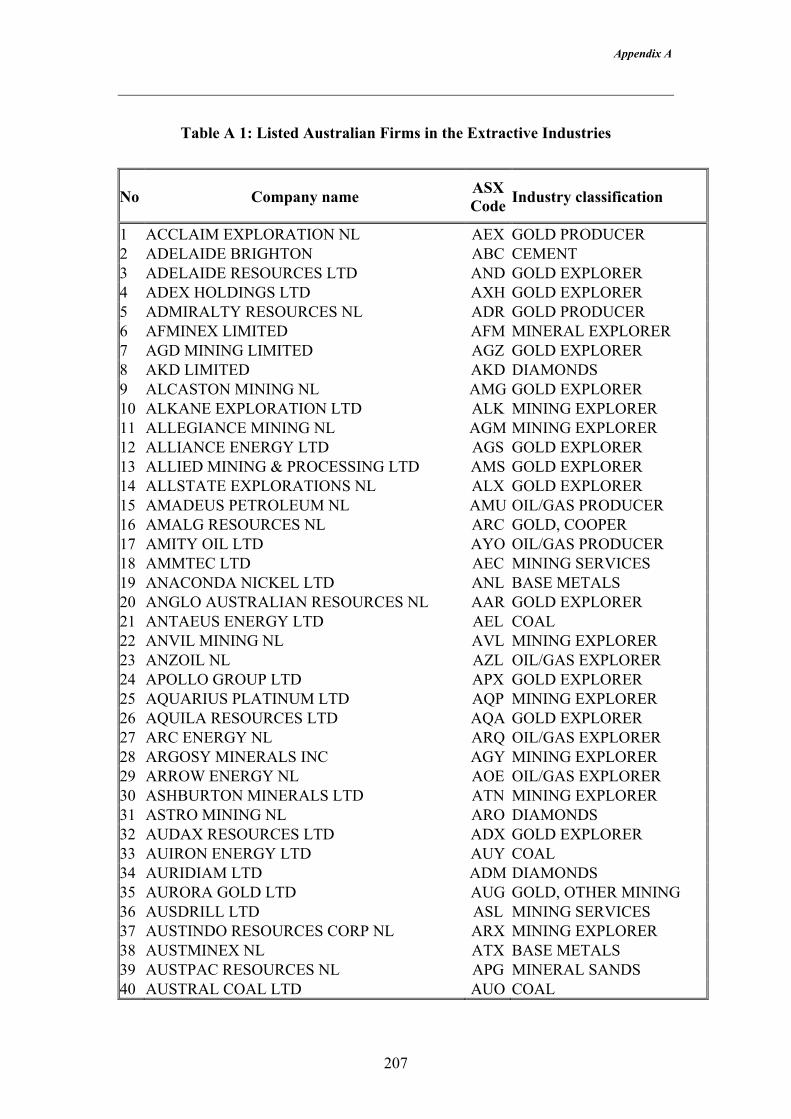

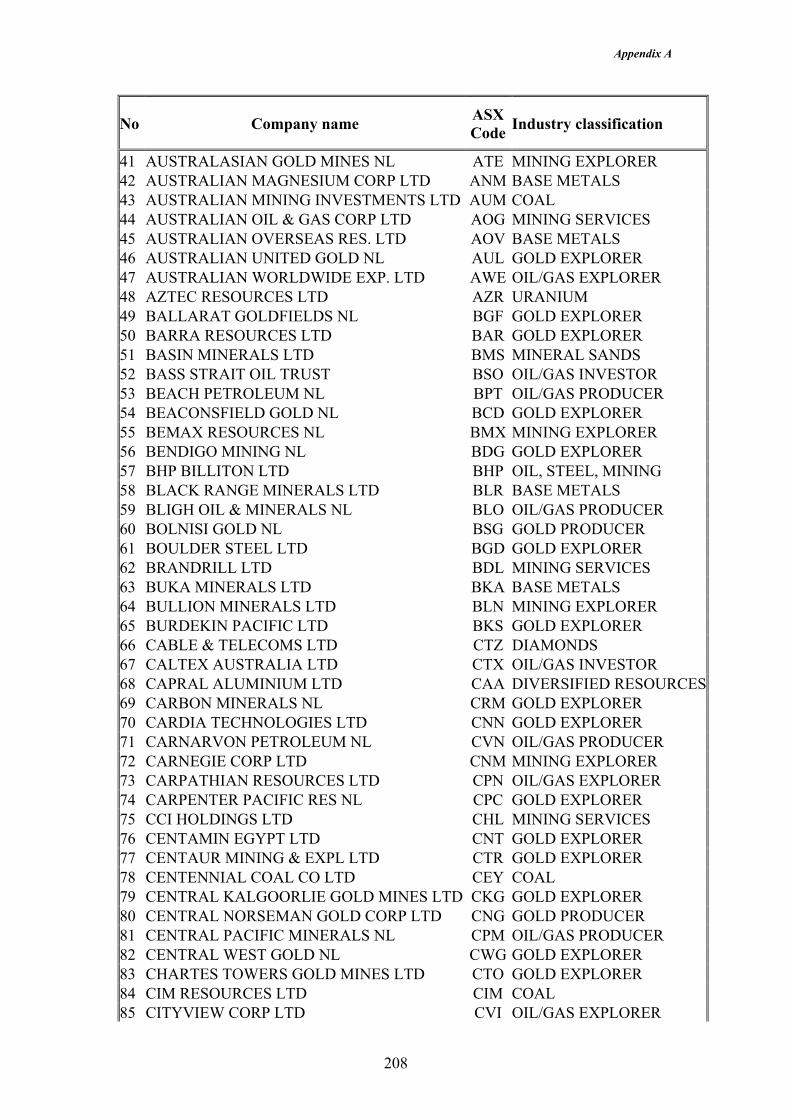

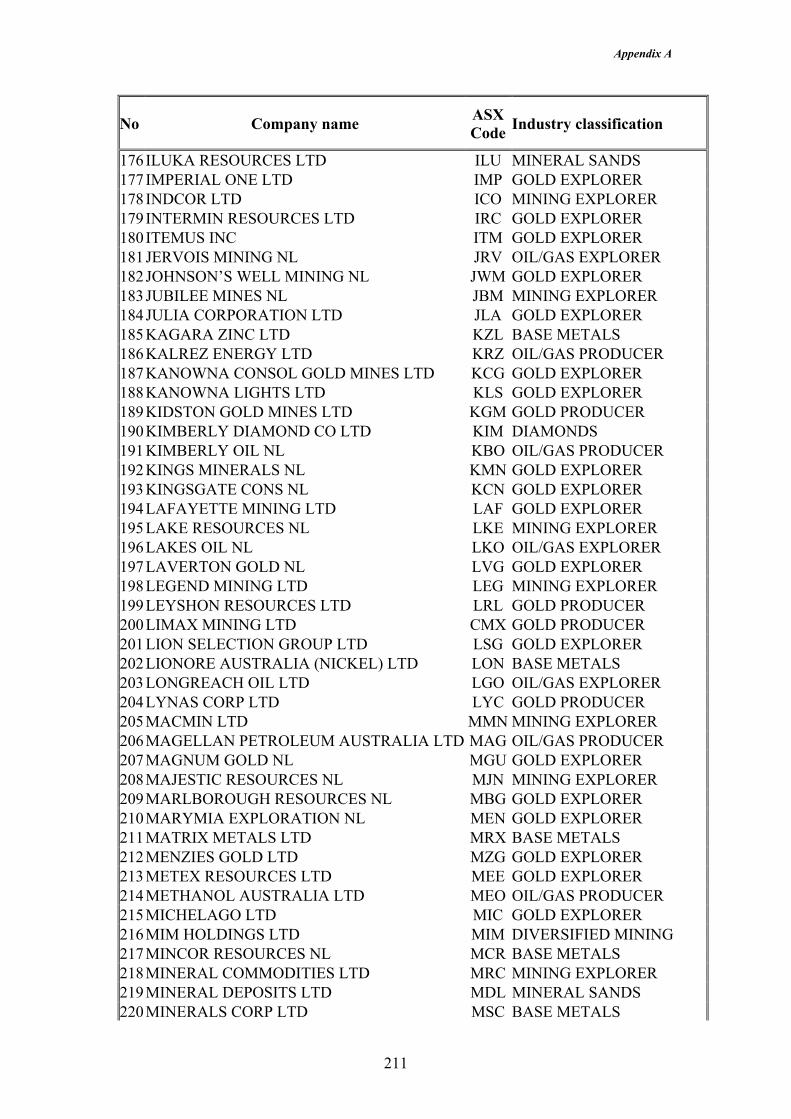

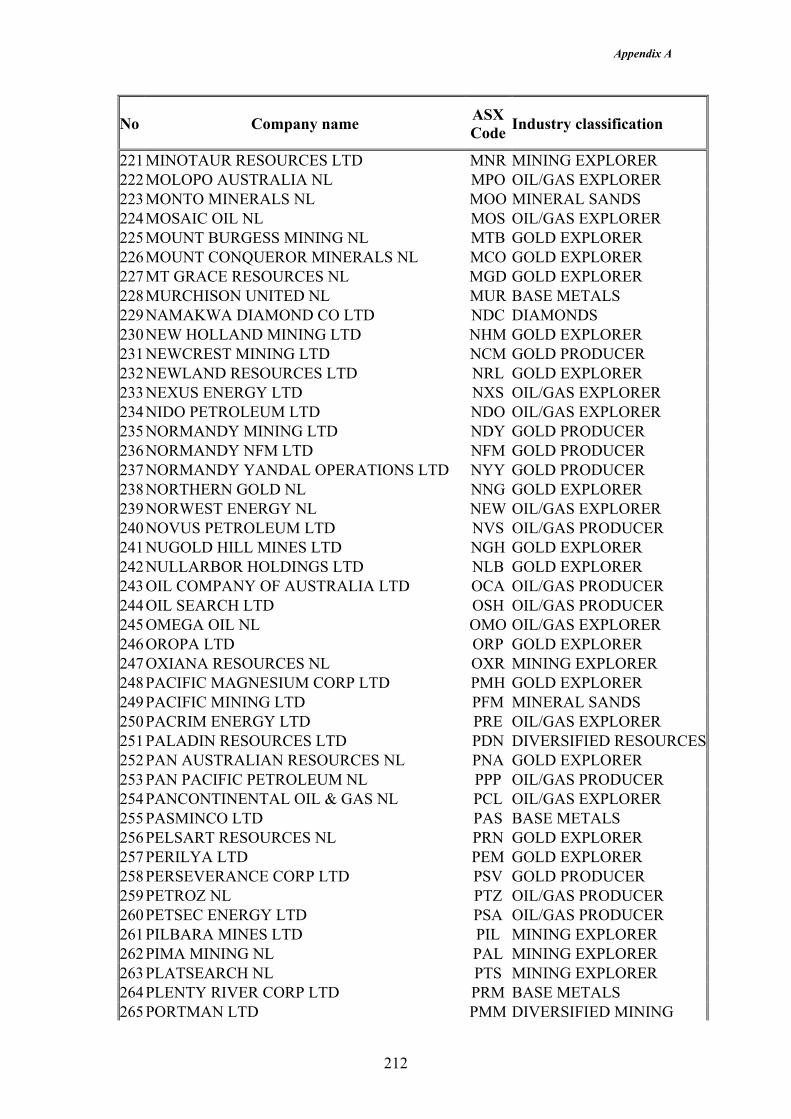

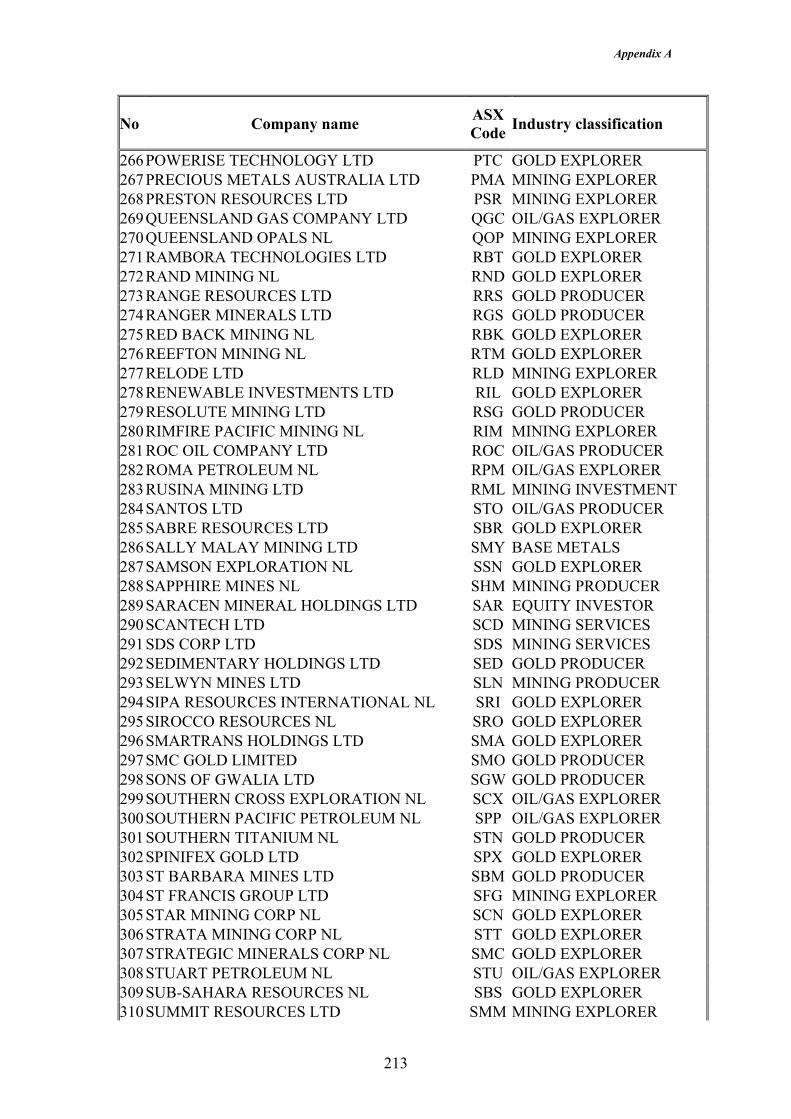

APPENDIX A: AUSTRALIAN FIRMS IN THE EXTRACTIVE INDUSTRIES LISTED ON THE ASX IN 1998 TO 2001 ..............................................................................................................206 APPENDIX B: FIRM CHARACTERISTICS MODEL YEAR-BY-YEAR AND AVERAGE FOUR YEARS ANALYSES..............................................................................................................218 APPENDIX C: RESULTS ON MARKET VALUE MODEL FOR YEAR-BY-YEAR ANALYSIS..............................................................................................................................................................223 APPENDIX D: FURTHER TEST.....................................................................................................230 APPENDIX E: FIRM CHARACTERISTICS MODEL ESTIMATION WITHOUT THE OUTLIERS (REFINED DATA)........................................................................................................247 APPENDIX F: RESULTS ON MARKET VALUE MODEL FOR FULL DATA........................252 REFERENCES ...................................................................................................................................262

viii

Table of Tables and Figure

Page

TABLE 2.1: FASB FINANCIAL INSTRUMENTS ACCOUNTING PRONOUNCEMENTS ....................................18 TABLE 2.2: SUMMARY OF DEVELOPMENT OF ACCOUNTING PRONOUNCEMENTS RELATED TO FINANCIAL

INSTRUMENTS IN AUSTRALIA ........................................................................................................24 TABLE 2.3: AASB 1033 VS RELATED FASB AND IAS STANDARDS..............................................28 TABLE 6.1: THE USE OF DERIVATIVE FINANCIAL INSTRUMENTS FOR HEDGING PURPOSES.....................97 TABLE 6.2: SUMMARY OF DATA SELECTION PROCEDURE .......................................................................98 TABLE 6.3: COMPONENTS OF DERIVATIVE DISCLOSURE INDEX ............................................................101 TABLE 6.4: SUMMARY OF INDEPENDENT VARIABLES EMPLOYED IN THE MARKET VALUE MODELS ....113 TABLE 6.5: DESCRIPTIVE STATISTICS AND CORRELATION MATRIX: FIRM CHARACTERISTICS MODEL .134 TABLE 6.6: DESCRIPTIVE STATISTICS: VALUE RELEVANCE OF DISCLOSURE QUALITY (N=253) ...........135 TABLE 6.7: DESCRIPTIVE STATISTICS: VALUE RELEVANCE OF HEDGE TRANSACTION, NET FAIR VALUE

AND UNREALISED GAIN OR LOSS ON FINANCIAL INSTRUMENTS. (N=253)...................................137 TABLE 7.1: CORRELATION COEFFICIENTS BETWEEN VARIABLES ..........................................................142 TABLE 7.2: NUMBER OF FIRMS THAT REPORT ALL INFORMATION REQUIRED BY AASB 1033 (100%

DISCLOSURE) ...............................................................................................................................143 TABLE 7.3: DISCLOSURE QUALITY OF FIRMS IN THE AUSTRALIAN EXTRACTIVE INDUSTRIES..............144 TABLE 7.4: DESCRIPTIVE STATISTICS OF DISCLOSURE COMPONENTS (POOLED SAMPLE) .....................145 TABLE 7.5: MEAN DISCLOSURE COMPONENTS OF USER FIRMS FOR THE PERIOD 1998 TO 2001 ...........147 TABLE 7.6: CORRELATION COEFFICIENTS BETWEEN VARIABLES ..........................................................151 TABLE 7.7: DISCLOSURE QUALITY OF DERIVATIVE INFORMATION OF EXTRACTIVE FIRMS ..................152 TABLE 7.8 :RESULTS OF REGRESSION ANALYSIS OF THE ASSOCIATION BETWEEN DISCLOSURE

TRANSPARENCY AND FIRMS CHARACTERISTICS (N=260) ............................................................154 TABLE 7.9: RESULTS OF REGRESSION ANALYSIS OF THE ASSOCIATION BETWEEN DISCLOSURE

TRANSPARENCY AND FIRMS CHARACTERISTICS: RANKED TRANSFORMATION (N=260)..............156 TABLE 7.10: RESULTS OF REGRESSION ANALYSIS OF THE ASSOCIATION BETWEEN DISCLOSURE

TRANSPARENCY AND FIRMS CHARACTERISTICS. (N=260) ...........................................................158 TABLE 7.11: RESULTS OF REGRESSION ANALYSIS OF THE ASSOCIATION BETWEEN DISCLOSURE

TRANSPARENCY AND FIRMS CHARACTERISTICS. .........................................................................159 TABLE 7.12: RESULTS ON THE ASSOCIATION BETWEEN DISCLOSURE QUALITY AND FIRM

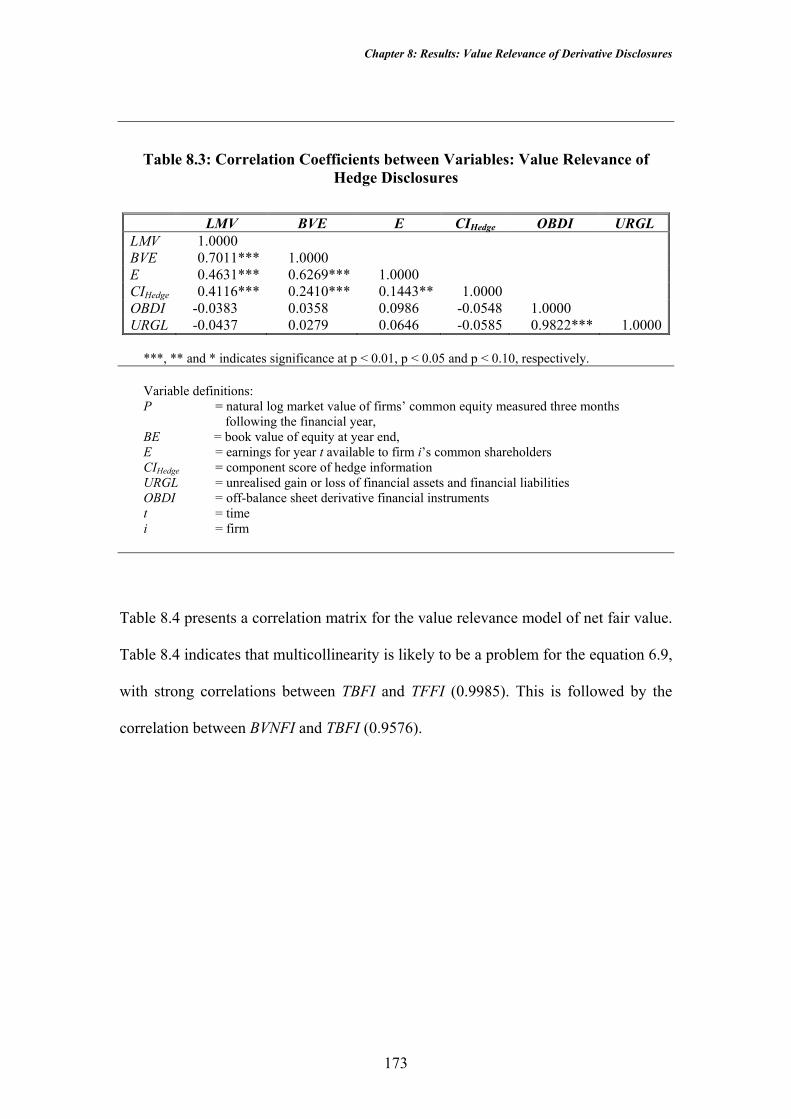

CHARACTERISTICS.......................................................................................................................163 TABLE 8.1:NORMALITY TEST OF VALUE RELEVANCE MODELS ............................................................169 TABLE 8.2: CORRELATION COEFFICIENTS BETWEEN VARIABLES ..........................................................171 TABLE 8.3: CORRELATION COEFFICIENTS BETWEEN VARIABLES: VALUE RELEVANCE OF HEDGE

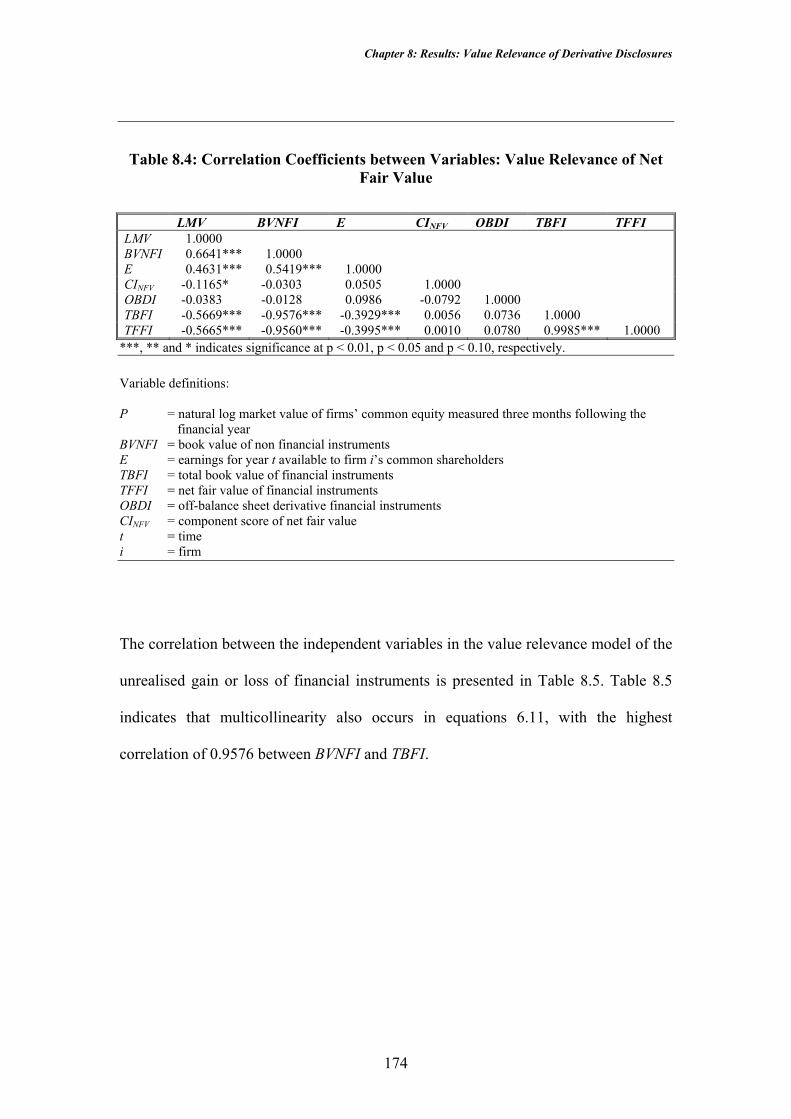

DISCLOSURES ..............................................................................................................................173 TABLE 8.4: CORRELATION COEFFICIENTS BETWEEN VARIABLES: VALUE RELEVANCE OF NET FAIR

VALUE.........................................................................................................................................174 TABLE 8.5: CORRELATION COEFFICIENTS BETWEEN VARIABLES: VALUE RELEVANCE OF UNREALISED

GAIN OR LOSS OF FINANCIAL INSTRUMENTS ...............................................................................175 TABLE 8.6: THE ASSOCIATION BETWEEN INFORMATION QUALITY OF DERIVATIVE DISCLOSURES AND

THE MARKET VALUE OF FIRMS (N=253)1 ....................................................................................177 TABLE 8.7: THE ASSOCIATION BETWEEN HEDGE DISCLOSURE AND MARKET VALUE OF THE FIRMS

(N=253)1......................................................................................................................................180 TABLE 8.8: THE ASSOCIATION BETWEEN NET FAIR VALUE AND MARKET VALUE (N=253)..................182 TABLE 8.9: THE ASSOCIATION BETWEEN THE MARKET VALUE OF FIRMS AND THE DIFFERENCE

BETWEEN NET FAIR VALUE AND BOOK VALUE OF FINANCIAL INSTRUMENTS (N=253)1.............184 TABLE 8.10: THE INCREMENTAL EXPLANATORY POWER OF NET FAIR VALUE BEYOND THE BOOK VALUE

OF FINANCIAL AND NON-FINANCIAL INSTRUMENTS AND EARNINGS VALUED AT THE HISTORICAL COST............................................................................................................................................187

TABLE 8.11: THE INCREMENTAL EXPLANATORY POWER OF UNREALISED GAIN OR LOSS OF FINANCIAL INSTRUMENTS BEYOND THE BOOK VALUE OF FINANCIAL AND NON-FINANCIAL INSTRUMENTS AND EARNINGS VALUED AT THE HISTORICAL COST (N=253)..............................................................188

TABLE 8.12: SUMMARY OF RESULTS OF VALUE RELEVANCE MODELS .................................................190 TABLE A 1: LISTED AUSTRALIAN FIRMS IN THE EXTRACTIVE INDUSTRIES ...........................................207 TABLE A 2: LIST OF DATA FIRMS IN THE STUDY...................................................................................215

ix

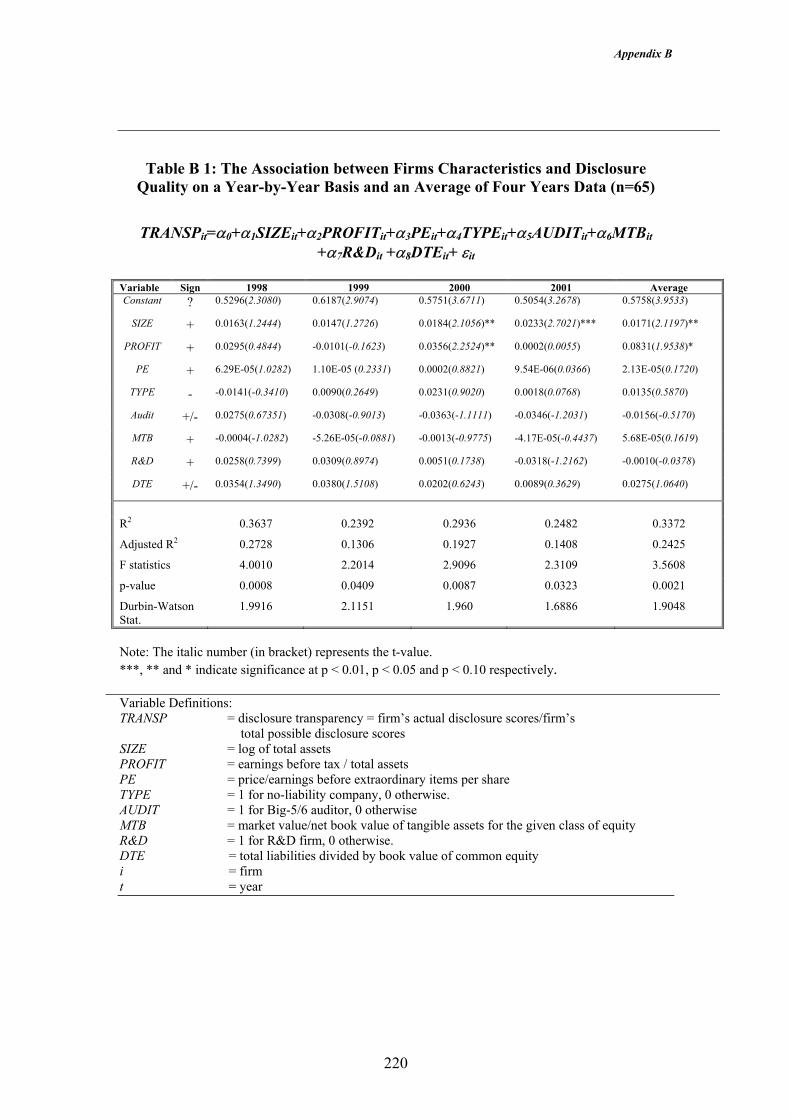

TABLE A 3: COMPONENTS OF DERIVATIVE DISCLOSURE INDEX FOR BHP BILLITON (2001).................217 TABLE B 1: THE ASSOCIATION BETWEEN FIRMS CHARACTERISTICS AND DISCLOSURE QUALITY ON A

YEAR-BY-YEAR BASIS AND AN AVERAGE OF FOUR YEARS DATA (N=65) ..................................220 TABLE B 2: RESULTS OF REGRESSION ANALYSIS OF THE ASSOCIATION BETWEEN DISCLOSURE

TRANSPARENCY AND FIRMS CHARACTERISTICS: RANKED TRANSFORMATION YEAR-BY-YEAR BASIS AND AN AVERAGE OF FOUR YEARS DATA (N=65).............................................................222

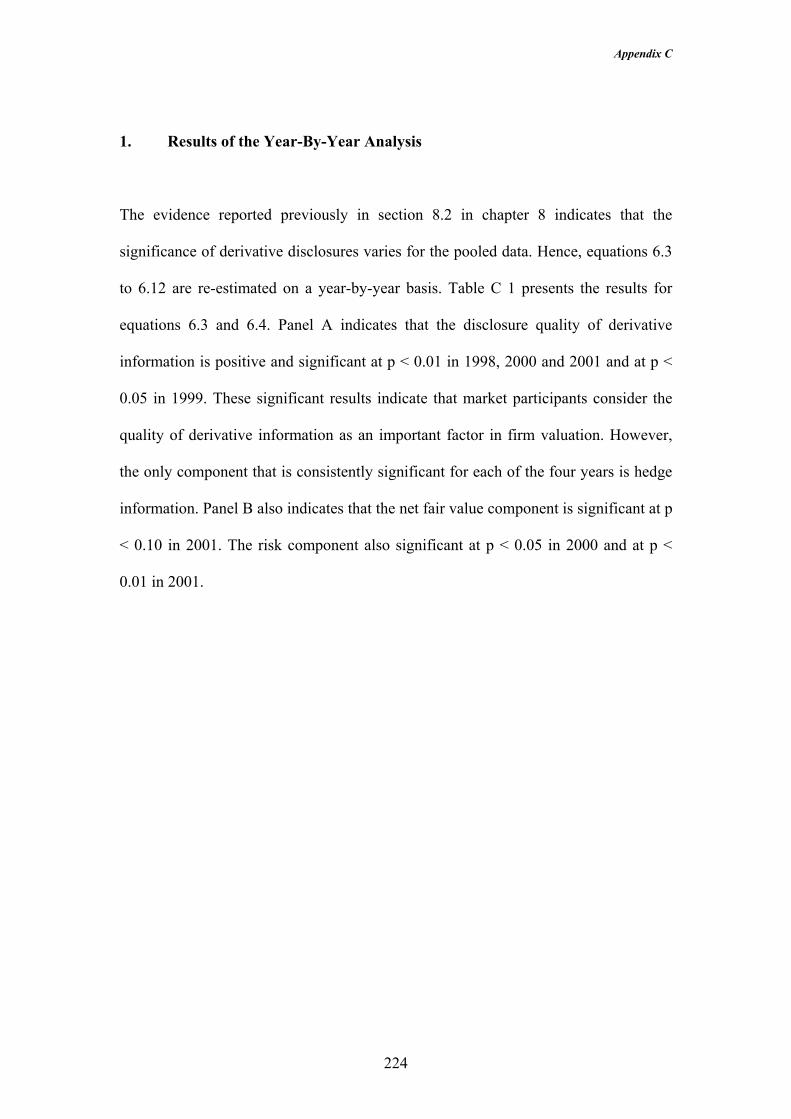

TABLE C 1: THE ASSOCIATION BETWEEN THE INFORMATION QUALITY OF DERIVATIVES DISCLOSURES

AND THE MARKET VALUE OF THE FIRMS: YEAR-BY-YEAR ANALYSIS ........................................225 TABLE C 2: THE ASSOCIATION BETWEEN HEDGE DISCLOSURES AND THE MARKET VALUE OF THE FIRMS:

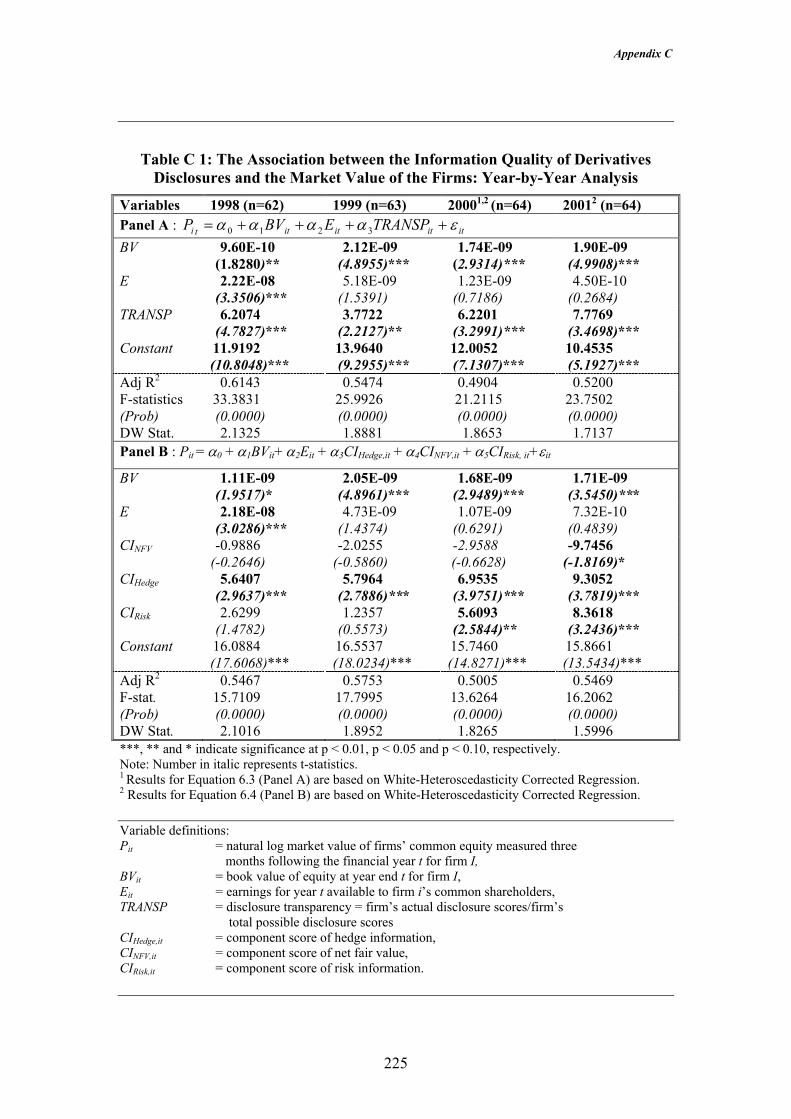

YEAR-BY-YEAR ANALYSIS..........................................................................................................226 TABLE C 3:THE ASSOCIATION BETWEEN NET FAIR VALUE AND MARKET VALUE: YEAR-BY-YEAR

ANALYSIS ....................................................................................................................................227 TABLE C 4: THE ASSOCIATION BETWEEN THE MARKET VALUE OF FIRMS AND THE DIFFERENCE BETWEEN

NET FAIR VALUE AND BOOK VALUE OF FINANCIAL INSTRUMENTS (UNREALISED GAIN OR LOSS)....................................................................................................................................................228

TABLE D 1: THE ASSOCIATION BETWEEN INFORMATION QUALITY OF DERIVATIVE DISCLOSURES AND

THE MARKET VALUE OF THE FIRMS (N=156)1 .............................................................................232 TABLE D 2: THE ASSOCIATION BETWEEN HEDGE DISCLOSURE AND THE MARKET VALUE OF THE FIRMS

(N=156)1......................................................................................................................................233 TABLE D 3: THE ASSOCIATION BETWEEN NET FAIR VALUE AND MARKET VALUE (N=156).................234 TABLE D 4: THEASSOCIATION BETWEEN THE MARKET VALUE OF FIRMS AND THE DIFFERENCE BETWEEN

NET FAIR VALUE AND BOOK VALUE OF FINANCIAL INSTRUMENTS (N=156) ..............................235 TABLE D 5:THE ASSOCIATION BETWEEN THE INFORMATION QUALITY OF DERIVATIVES DISCLOSURES

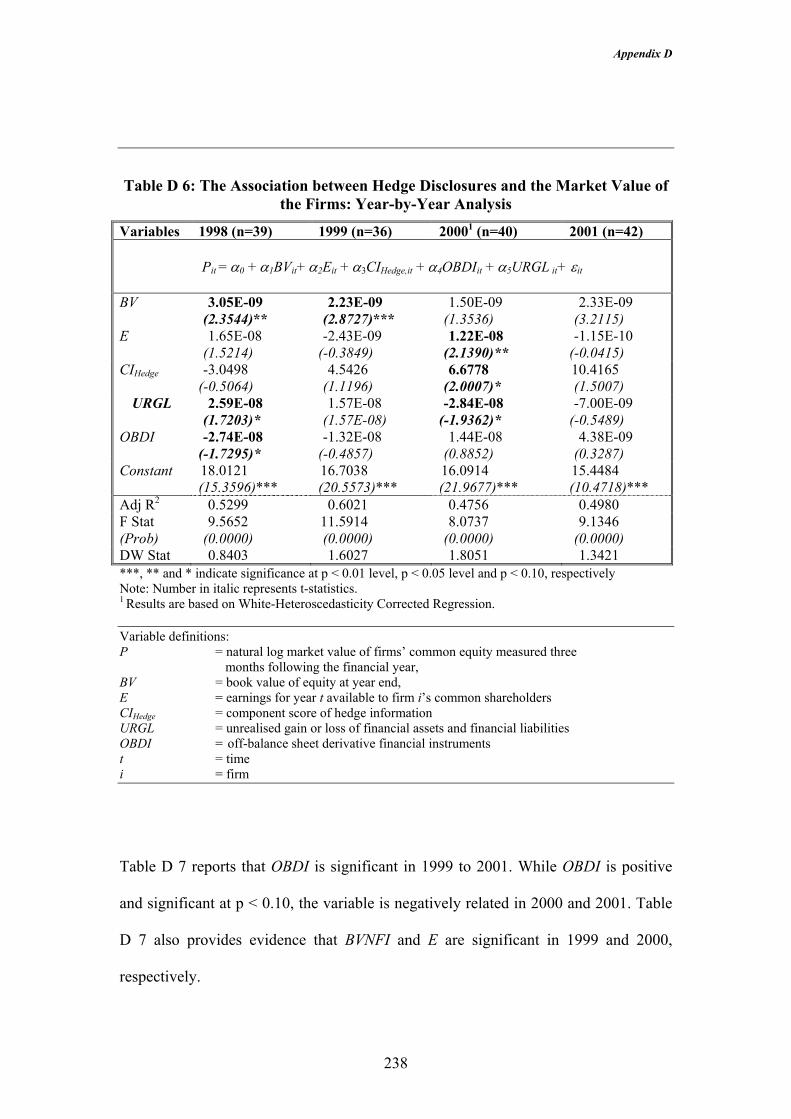

AND THE MARKET VALUE OF THE FIRMS: YEAR-BY-YEAR ANALYSIS ........................................236 TABLE D 6: THE ASSOCIATION BETWEEN HEDGE DISCLOSURES AND THE MARKET VALUE OF THE FIRMS:

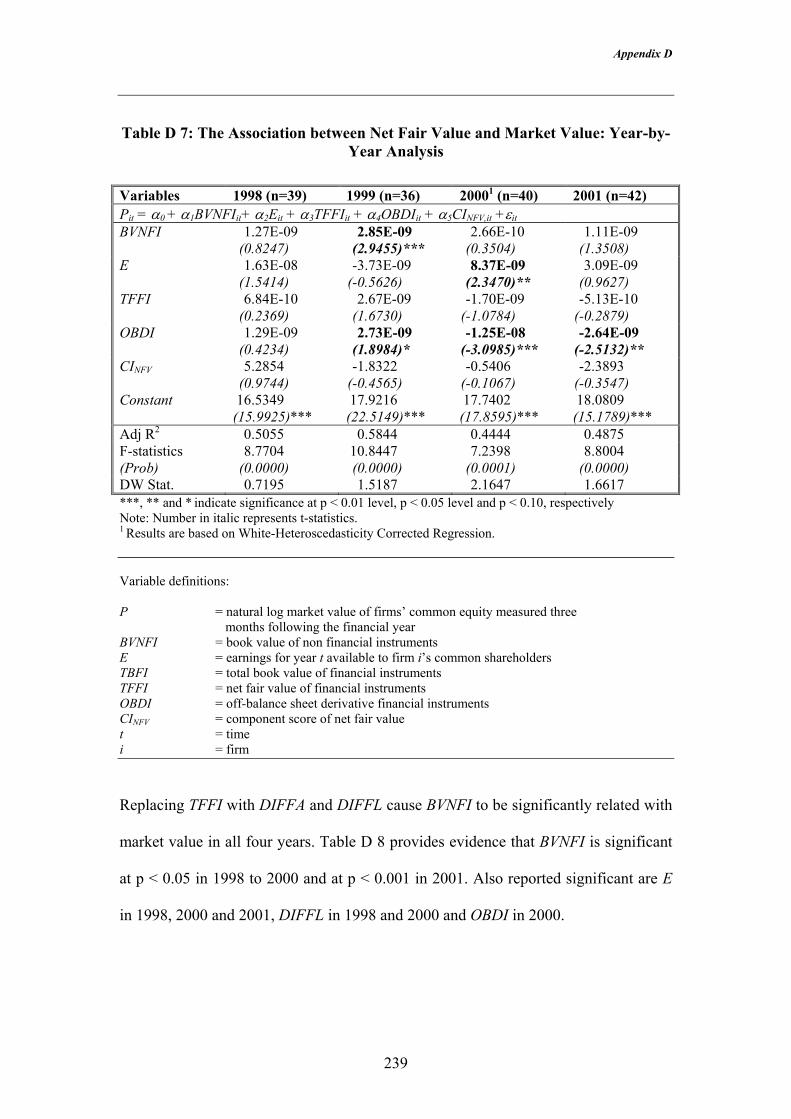

YEAR-BY-YEAR ANALYSIS..........................................................................................................238 TABLE D 7: THE ASSOCIATION BETWEEN NET FAIR VALUE AND MARKET VALUE: YEAR-BY-YEAR

ANALYSIS ....................................................................................................................................239 TABLE D 8: THE ASSOCIATION BETWEEN THE MARKET VALUE OF FIRMS AND THE DIFFERENCE

BETWEEN NET FAIR VALUE AND BOOK VALUE OF FINANCIAL INSTRUMENTS ............................240 TABLE D 9: INCREMENTAL EXPLANATORY POWER OF NET FAIR VALUE BEYOND THE BOOK VALUE OF

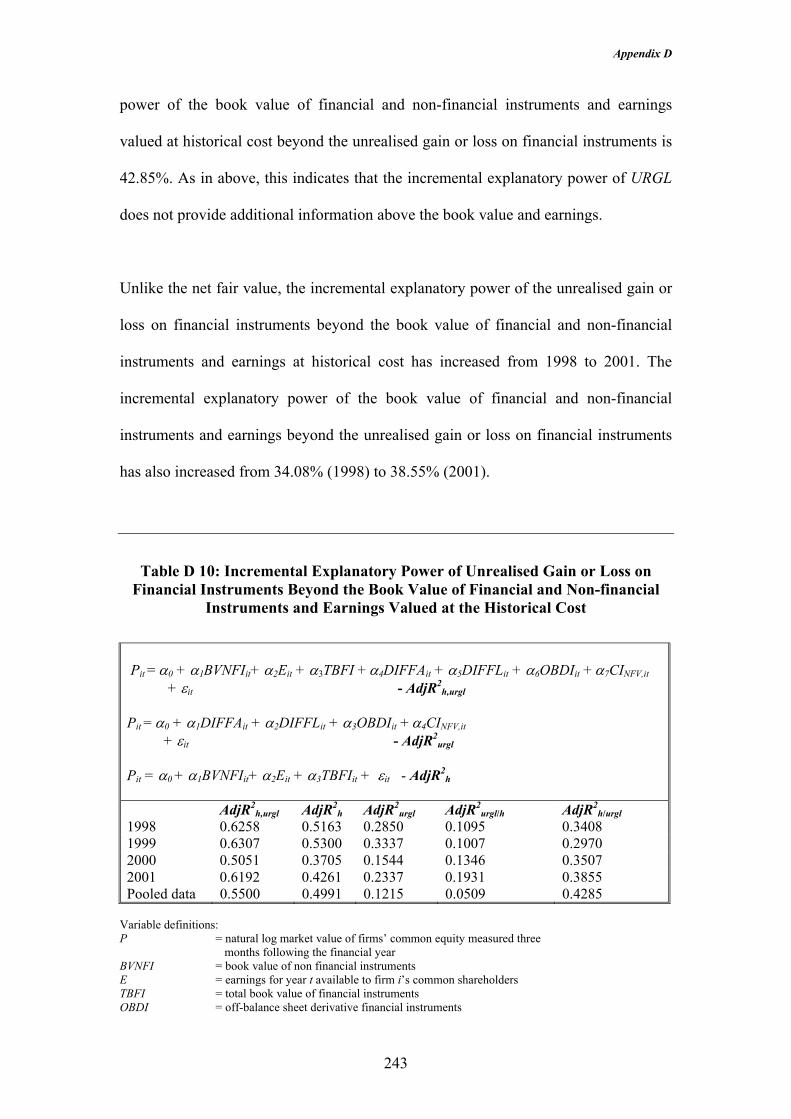

FINANCIAL AND NON-FINANCIAL INSTRUMENTS AND EARNINGS VALUED AT THE HISTORICAL COST............................................................................................................................................242

TABLE D 10: INCREMENTAL EXPLANATORY POWER OF UNREALISED GAIN OR LOSS ON FINANCIAL INSTRUMENTS BEYOND THE BOOK VALUE OF FINANCIAL AND NON-FINANCIAL INSTRUMENTS AND EARNINGS VALUED AT THE HISTORICAL COST............................................................................243

TABLE E 1: RESULTS OF REGRESSION ANALYSIS OF THE ASSOCIATION BETWEEN DISCLOSURE

TRANSPARENCY AND FIRMS CHARACTERISTICS (N=254) ............................................................248 TABLE E 2: THE ASSOCIATION BETWEEN FIRMS CHARACTERISTICS AND DISCLOSURE QUALITY ON A

YEAR-BY-YEAR BASIS AND AN AVERAGE OF FOUR YEARS DATA ..............................................249 TABLE E 3: RESULTS OF REGRESSION ANALYSIS OF THE ASSOCIATION BETWEEN DISCLOSURE

TRANSPARENCY AND FIRMS CHARACTERISTICS: RANKED TRANSFORMATION (N=254)..............250 TABLE E 4: REFINED DATA: ASSOCIATION BETWEEN DISCLOSURE TRANSPARENCY AND FIRMS

CHARACTERISTICS: RANKED TRANSFORMATION YEAR-BY-YEAR BASIS AND AN AVERAGE OF FOUR YEARS DATA .....................................................................................................................251

TABLE F 1: THE ASSOCIATION BETWEEN INFORMATION QUALITY OF DERIVATIVE DISCLOSURES AND

THE MARKET VALUE OF THE FIRMS (N=260)1 .............................................................................253 TABLE F 2: THE ASSOCIATION BETWEEN INFORMATION QUALITY OF DERIVATIVE DISCLOSURES AND

THE MARKET VALUE OF THE FIRMS – RANKED BASED ON LARGE AND SMALL (N=128) .............254 TABLE F 3: THE ASSOCIATION BETWEEN INFORMATION QUALITY OF DERIVATIVE DISCLOSURES AND

THE MARKET VALUE OF THE LARGE AND SMALL FIRMS .............................................................255 TABLE F 4: THE ASSOCIATION BETWEEN INFORMATION QUALITY OF DERIVATIVES DISCLOSURES AND

MARKET VALUE OF THE FIRMS: YEAR-BY-YEAR ANALYSIS (N=65) ...........................................256

x

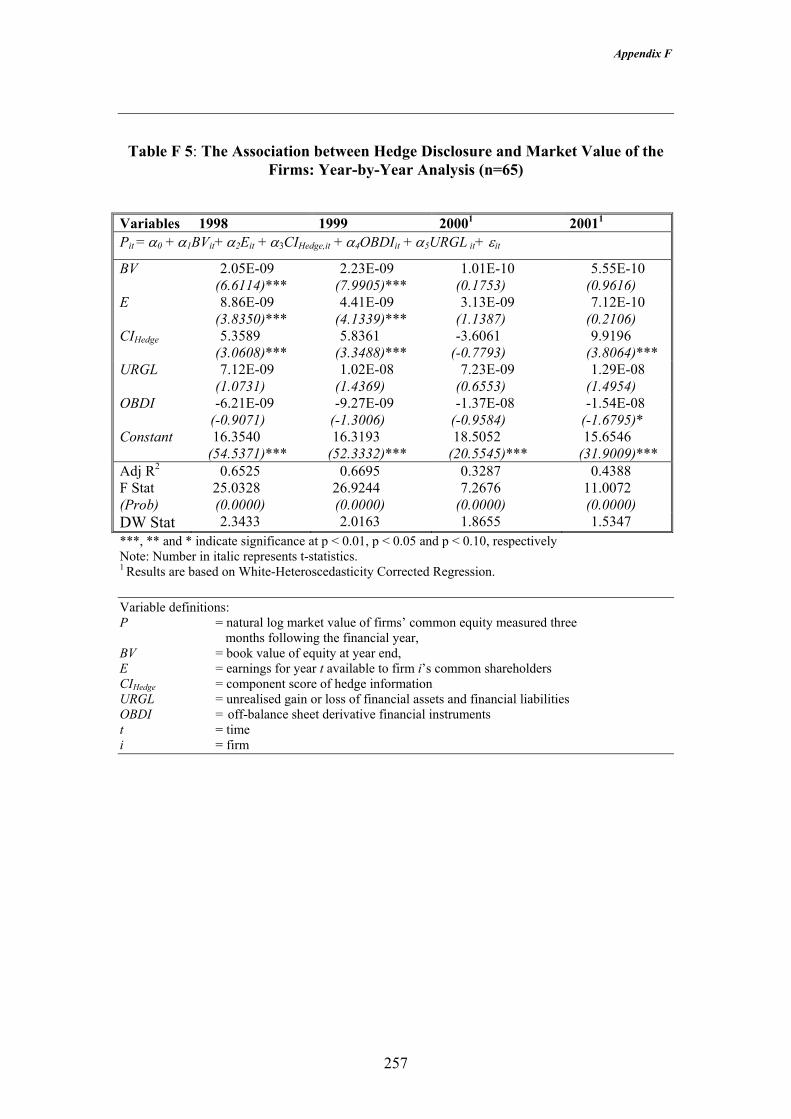

TABLE F 5: THE ASSOCIATION BETWEEN HEDGE DISCLOSURE AND MARKET VALUE OF THE FIRMS: YEAR-BY-YEAR ANALYSIS (N=65)..............................................................................................257

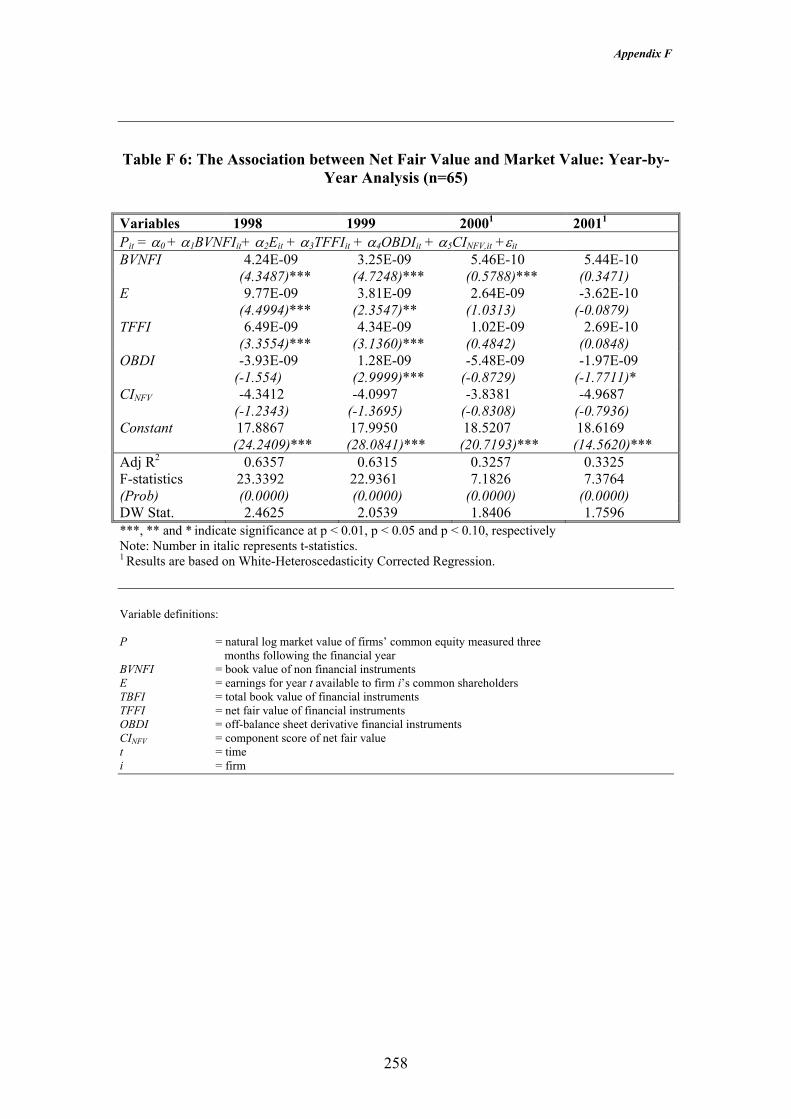

TABLE F 6: THE ASSOCIATION BETWEEN NET FAIR VALUE AND MARKET VALUE: YEAR-BY-YEAR ANALYSIS (N=65) ........................................................................................................................258

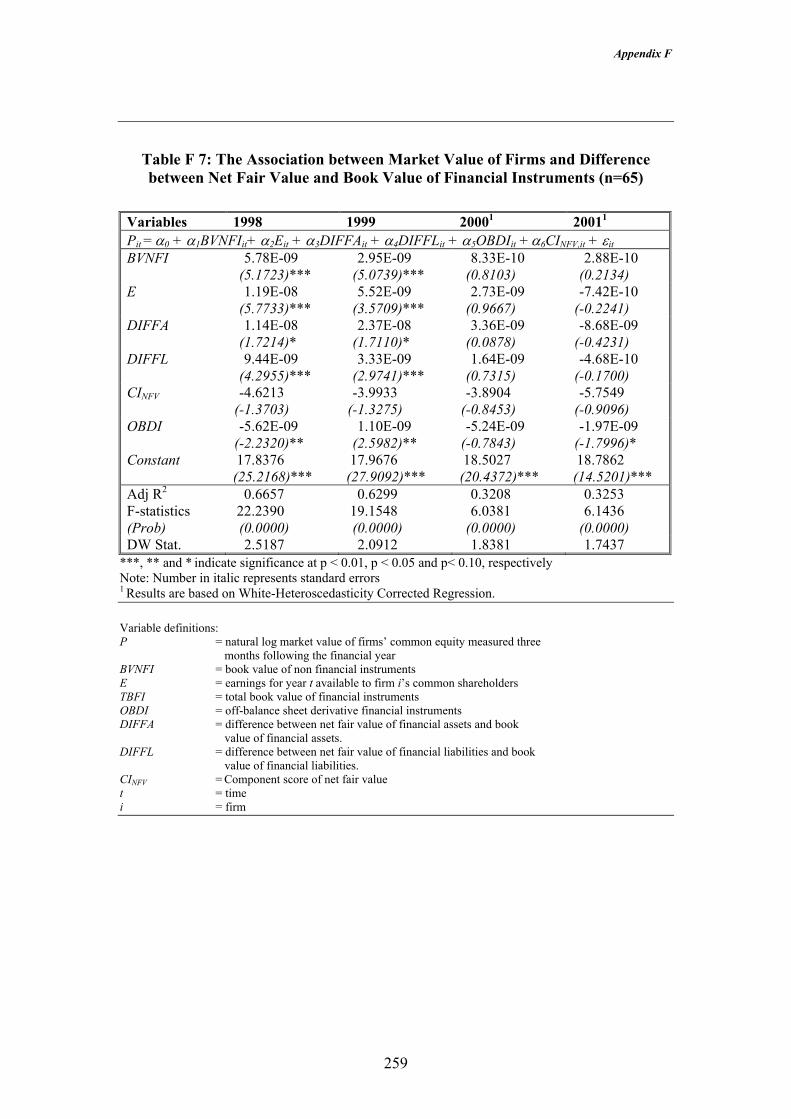

TABLE F 7: THE ASSOCIATION BETWEEN MARKET VALUE OF FIRMS AND DIFFERENCE BETWEEN NET FAIR VALUE AND BOOK VALUE OF FINANCIAL INSTRUMENTS (N=65) ........................................259

TABLE F 8: INCREMENTAL EXPLANATORY POWER OF NET FAIR VALUE BEYOND BOOK VALUE OF FINANCIAL AND NON-FINANCIAL INSTRUMENTS AND EARNINGS VALUED AT HISTORICAL COST....................................................................................................................................................260

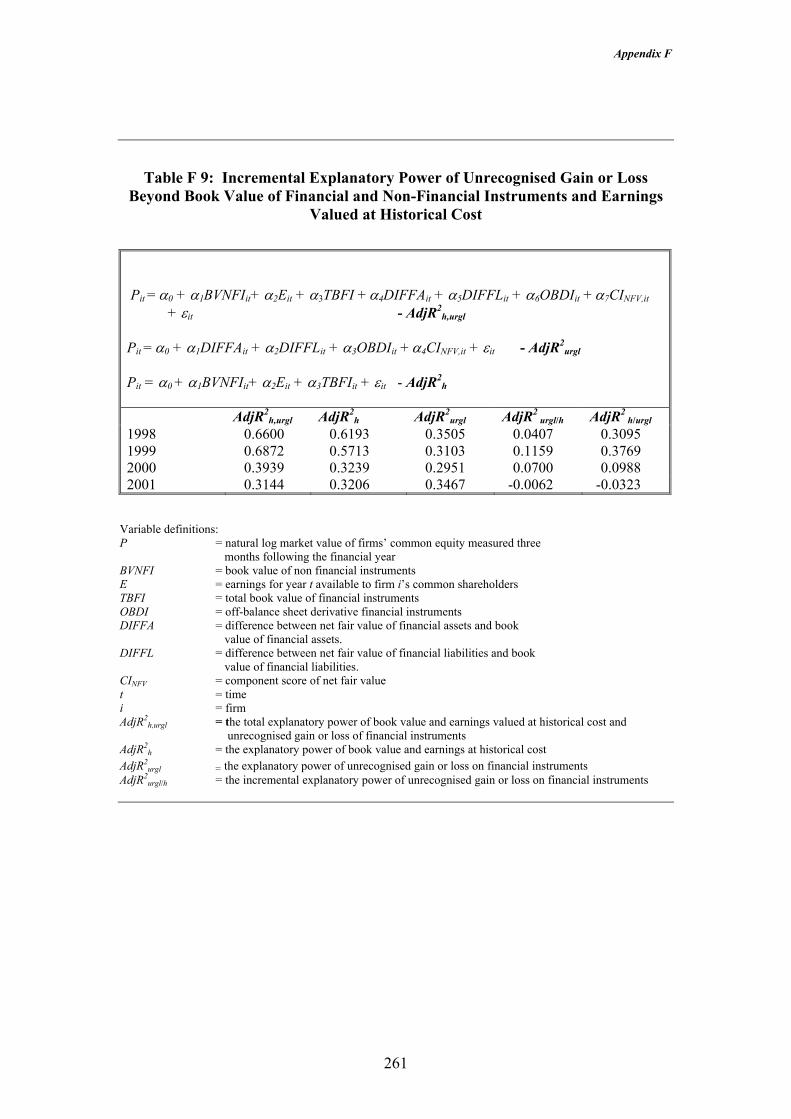

TABLE F 9: INCREMENTAL EXPLANATORY POWER OF UNRECOGNISED GAIN OR LOSS BEYOND BOOK VALUE OF FINANCIAL AND NON-FINANCIAL INSTRUMENTS AND EARNINGS VALUED AT HISTORICAL COST .......................................................................................................................261

FIGURE 5.1: DIAGRAM ILLUSTRATING THE RESEARCH QUESTIONS.........................................................80

xi

THE STATEMENT OF ORIGINAL AUTHORSHIP

“The work contained in this thesis has not been previously submitted for a degree or diploma at any other higher education institution. To the best of my knowledge and belief, the thesis contains no material previously published or written by another person except where due reference is made” Signed : ______________________________ Date : _____________________________

xii

ACKNOWLEDGEMENTS

I am deeply indebted to my supervisor, Dr. Majella Percy, for her excellent direction

and support provided to me throughout all stages of this dissertation. I am also very

grateful to my associate supervisor, Prof. Roger Willett, for his helpful comments and

support.

I would like to acknowledge Universiti Kebangsaan Malaysia and the Malaysian

Government for their moral support and assistance with a scholarship to undertake

study leave to do my Doctorate at the Queensland University of Technology. I would

also like to acknowledge the advice and support provided to me by Prof. Greg Clinch,

Assoc. Prof. Jenny Goodwin, Helen Kang, Christine Tan, Suzanna Yuen, Wilson

Tong and participants at AFAANZ 2003 in Brisbane, Doctorate Business Students

Symposium at the Queensland University of Technology and the APJAE Symposium

2004 in Kuala Lumpur.

I am particularly indebted to my fellow PhD students, Eko Suwardi, Steve Su,

Victoria Clout, Chun-Wei Huang and Teruyo Omura for their insightful comments

and support offered to me over this long process. I also would like to thank Danielle

Horton for providing me with some of the share price data.

Finally, I wish to express my appreciation for the encouragement and support of my

wife Anida Sidek, my children Muhammad Ameer Zharfan, Hanis Afifah, Hanis

Nadhirah, Hanis Aqilah Aiman and Muhammad Ammar Zhakwan. To my parents

Hassan Mat and Siti Fatimah Bidin and parents in-law Sidek Abd Rashid and Mariam

Marzuki, I would not be here without their love and support.

Chapter 1: Introduction

1

CHAPTER 1 INTRODUCTION

1.1 Purpose of the Study The objective of this study is, first to examine the relationship between the

transparency, or disclosure quality, of derivative information and firm characteristics.

Second, this study investigates the value relevance of derivative disclosures in

particular hedge information, net fair value information and risk information.

Derivative financial instruments are financial instruments whose value is derived from

the value of the underlying asset, liability, interest rate, index, or a hedge. Most of

these instruments, such as interest rate swaps and option contracts, are executory

contracts1 and require either no initial cash outlay or only a small initial outlay

(Johnson and Swieringa, 1996; Wilson and Smith, 1997).

Firms use derivative financial instruments to manage (hedge) exposure to foreign

exchange risk, interest rate risk and commodity price changes. However, due to their

nature, these instruments are not recognised as assets and liabilities in the balance

sheet and nor is the unrealised gain or loss recorded in the income statement.

Nevertheless, information about them (voluntary and mandatory) is disclosed in the

notes to the financial statements to enhance financial statement users’ understanding

of the significance of these derivative financial instruments and the associated risks.

To examine the significance of recognised and unrecognised financial information in

decision-making, researchers examine the quality of the information. The U.S.

1 A contract under which the obligations of both parties to the contract are so far unperformed and the failure of either to complete performance would constitute a material breach excusing the performance of the other (U.S. Department of Justice, 1998).

Chapter 1: Introduction

2

Security Exchange Commission (SEC) assesses the quality of financial statements of

cross-listed firms (non-U.S. firms listed on U.S. exchanges) based on three criteria:

transparency, comparability and full disclosure. However, the existing research in this

area investigates the quality of the information directly by studying the comparability

of non-U.S. Generally Accepted Accounting Principles (GAAP) to U.S. GAAP and

thus measuring indirectly the transparency of disclosures (Pownall and Schipper,

1999).

Prior studies indicate that disclosure quality (referred to in some studies as disclosure

level) is related to firm characteristics. This association has been linked to explanatory

variables from the research on agency costs, political costs, corporate governance and

information asymmetry (Ahmed and Courtis, 1999). Several studies investigate the

quality of accounting information based on the impact of corporate disclosure

practices and the usefulness of the information in decision-making. These studies

measure quality of disclosure based on the perception of the users, such as financial

analysts, shareholders, creditors and researchers, on the accounting numbers, and the

association of accounting information with share prices. In the association studies,

researchers examine the value relevance of accounting information, where value

relevance refers to the information being related to equity value.

A disclosure index is used in this thesis as a measure of disclosure quality. Five

categories of information required by AASB 1033 Presentation and Disclosure of

Financial Instruments are used to develop the index. These are disclosures of

accounting policy, hedges of anticipated transaction, risk information, net fair value

information and commodity contracts which are regarded as financial instruments. A

Chapter 1: Introduction

3

score is given for each item disclosed in each category. To make each category add

equally to the disclosure index, the score category is divided by the number of items

in each component of the index.

This study addresses the questions of whether the disclosure quality of derivative

information is related to specific firm characteristics and whether this quality is

perceived as an important factor in firm valuation (i.e. value relevant). This study

adds to the literature on the disclosure quality of derivative information in the

specialised setting of firms in the extractive industries.

The next section discusses prior research and the main findings of this thesis. Section

1.3 describes the motivation for this study. The structure of the thesis is outlined in

section 1.4.

1.2 Prior Research and the Main Findings of the Thesis

Prior studies indicate that disclosure quality is associated with certain firm

characteristics. Studies, dating back to 1971, have been providing evidence that a)

size of the firms (Singhvi and Desai, 1971; Firth, 1979; Cooke, 1989 and 1991;

Wallace, Naser and Mora, 1994; Ahmed and Nicholls, 1994; Riahi-Belkaoui, 2001;

Ali, Ahmed and Henry, 2003), b) auditor (Singhvi and Desai, 1971; Ahmed and

Nicholls, 1994; Wallace and Naser, 1995) and c) performance of the firm (Ali et al.,

2003) are positively related to disclosure quality. However, specific to the oil and gas

industries, Malone, Fries and Jones (1993) indicate that there is no association

between the size of the firm and auditor choice (Big 5 or Non-big 5) and disclosure

quality.

Chapter 1: Introduction

4

There is no direct evidence available on the association between disclosure quality

and the market value of the firm. Lang, Ready and Yetman (2003) and Gelb and

Zarowin (2002) provide indirect evidence on the association between disclosure

quality and share prices. Lang et al. (2003) provide evidence on the association

between disclosure quality and share prices based on the association between

accounting data (earnings) and share price. Gelb and Zarowin (2003) provide

evidence that the corporate level of disclosure is associated with share prices since

high disclosure firms have higher earnings response coefficients than low disclosure

firms.

The value relevance of financial instruments has been examined in the U.S. These

studies examine the value relevance of fair value under different accounting

standards. Barth (1994), Eccher, Ramesh and Thiagarajan (1996), Barth, Beaver and

Landsman (1996) and Park, Park and Ro (1999) provide evidence on the value

relevance of banks’ fair value disclosures under SFAS 107 Disclosures about Fair

Value of Financial Instruments. Simko (1999), on the other hand, extends the research

to non-financial firms. Venkatachalam (1996) extends these studies by examining the

implications of fair value disclosures under SFAS 119 Disclosure about Derivative

Financial Instruments and Fair Value of Financial Instruments. Mixed results are

reported.

The results of the current study indicate that the quality of derivative disclosures

among firms in the extractive industries has increased since the accounting standard,

AASB 1033 Presentation and Disclosure of Financial Instruments, was applicable.

Chapter 1: Introduction

5

However, firms still use discretion in the disclosure of derivative information,

especially in relation to net fair value. Overall, the multivariate analysis indicates that

larger firms tend to provide transparent derivative information within the extractive

industries. These findings hold for both the ranked regression technique and the

average of four years’ data (see Appendix B). Other variables significantly related to

derivative disclosure quality include the price-earnings ratio, profitability, market-to-

book ratio and the debt-to-equity ratio (leverage).

The multiple regression results from the market value models indicate that market

participants regard derivative information as value relevant. However, when

comparing net fair value information with other derivative information components,

i.e. hedge information and risk information components, the net fair value information

component is not value relevant. The incremental explanatory power of net fair value

and the unrealised gain or loss of financial instruments is very low compared to the

incremental explanatory power of the book value of financial and non-financial

instruments and earnings valued at historical costs. Nevertheless, the incremental

explanatory power of net fair value and the unrealised gain or loss on financial

instruments beyond book value of financial and non-financial instruments and

earnings valued at historical costs has increased from 1998 to 2001. However, the

opposite direction is reported for the incremental explanatory power of book value of

financial and non-financial instruments and earnings valued at historical cost. To a

limited extent, net fair value of financial instruments is value relevant. However, the

unrealised gain or loss of financial liabilities and off-balance sheet derivative financial

instruments are recorded as value relevant in the year-by-year analysis (see Table C 4

Appendix C).

Chapter 1: Introduction

6

1.3 Motivation Recent events in the business world, for example, the collapse of prominent

companies such as Enron, HIH Insurance and Barings Plc. have focused attention on

the importance of high quality financial reporting. Of relevance to this study is where

the collapses were due to the involvement of the company with derivative

instruments. In Australia some derivative instruments are not recognised in the

balance sheet. Therefore, extensive disclosures are required to ensure financial

statement users are aware of the significance of these instruments to an entity’s

financial position. The first motivating factor of this study is the limited research on

derivative disclosures in Australia. Prior studies have examined the quality of

accounting information in general, but only a limited number provide evidence on

derivative disclosures in Australia. The finance literature provides evidence on the

association between the use of derivatives and firm characteristics (e.g. Berkman,

Bradbury, Hancock and Innes, 2002; Nguyen and Faff, 2002). No attempt has been

made to examine the relationship between the disclosure quality of derivatives and

firm characteristics. The few Australian studies on derivative disclosures have been

surveys of accounting practice before the implementation of the AASB 1033

Presentation and Disclosure financial Instruments, for example Hancock (1994),

Berkman, Bradbury, Hancock and Innes (1997), Chalmers and Godfrey (2000) and

Chalmers (2001). The current study provides evidence of the association between

disclosure quality of derivative information and firm characteristics.

The second source of motivation justifies selecting firms in the extractive industries.

Prior studies have indicated that firms in the extractive industries extensively use

Chapter 1: Introduction

7

derivative instruments for hedging purposes (Berkman, Bradbury, Hancock and Innes,

1997) as compared to other industries. This is because of the significant exploration

and production risks inherent in the extractive industries2. Also derivatives are used

by extractive firms to underwrite and protect revenue. Moreover, Chalmers (2001) has

indicated that prior to AASB 1033 these firms provided information in their annual

reports. Therefore, it is relevant to examine the association between disclosure

practice and firm characteristics and the importance of the information in firm

valuation. Perhaps the most important factor is that these industries play a significant

role in the Australian economy, where they generate exports worth more than $30

billion in 2000 to 2002 and represent approximately 25% of the listed companies on

the Australian Stock Exchange (ASX). Therefore, examining this specific industry

may affect inferences regarding the value relevance of accounting information

(Simko, 1999).

The third motivating factor is that fair value accounting and hedge disclosures have

become significant topics of study in the U.S. since the Statement of Financial

Accounting Standards No 107 (SFAS 107) Disclosures about Fair Values of

Financial Instruments and SFAS 119 Disclosure about Derivative Financial

Instruments and Fair Value of Financial Instruments issued in 1991 and 1994,

respectively. However, the findings of these studies were based on samples from

banking industries in the U.S. and may not represent other industries and jurisdictions.

The reliability of these disclosures is questionable because fair value is based on

subjective estimates with potential for significant measurement error (Simko, 1999).

Therefore, research on the value relevance of derivative financial instruments, in

2 Includes oil, gas and mining industries, as per the IASC (2000). Please refer to section 2.5 chapter 2.

Chapter 1: Introduction

8

particular fair value disclosures and hedge disclosures, in the context of the extractive

industries in Australia will provide useful information on this complex area for both

Australian and international standard setters.

The fourth source of motivation is the impending harmonisation of accounting

standards. In 2005 Australia is expected to adopt most of the accounting standards

issued by the International Accounting Standards Board3. This includes IAS 39

Financial Instruments: Recognition and Measurement. The standard deals with

recognition and measurement of financial instruments at fair value. Given the fact that

ED 59 Financial Instruments, issued by AASB, has been rejected due to the

recognition and measurement issues, results from this study will provide evidence on

the readiness of Australian firms and investors to adopt IAS 39, i.e. to move towards a

fair value accounting regime.

The fifth source of motivation is that most regression models adopted in previous

value relevance studies (such as Barth 1994; Venkatachalam, 1996) are based on the

balance sheet model4. In this study the value relevance models are developed based on

the Ohlson (1995) model. The model provides a direct link between accounting

amounts and firm value, which is absent from other models (Barth, 2000). Results

from this study provide evidence on the robustness of prior results within this

methodology.

3 The International Accounting Standards Committee (IASC) became the International Accounting Standard Board (IASB) in 2001. 4 Where market value of equity represented by the market value of assets minus market value of liabilities.

Chapter 1: Introduction

9

1.4 Plan of Thesis

This thesis is structured in the following way. The following chapter describes the

institutional background surrounding financial reporting of derivative instruments in

Australia. The chapter begins by explaining the motivation for firms to use derivative

instruments. The comparative practices of accounting for financial instruments

between the U.S. and the IASC are then reviewed. This is followed by a discussion of

accounting for financial instruments in Australia. The discussion is based on the

disclosure and presentation of financial instruments required by the AASB 1033. One

important issue which has been investigated in the U.S. is the value relevance of fair

value required by various standards issued by the Financial Accounting Standard

Board (FASB). Surveys of Australian accounting practice are also discussed. Finally,

the chapter discusses the risk management practices in the extractive industries,

providing background evidence of the importance of derivatives for this industry. This

evidence indicates that studies on disclosure practice in this industry are important for

the economy.

Chapters three and four review prior studies on disclosure quality and value

relevance. Chapter three examines the association between disclosure quality and firm

characteristics. Studies investigating the quality of accounting information are

reviewed. The chapter begins by reviewing studies that examine disclosure quality in

different ways. Several studies indicate that to ensure high quality disclosures of

mandatory information, enforcement is an important issue. Selected empirical studies

are then reviewed as evidence of the association between disclosure quality

Chapter 1: Introduction

10

(disclosure level) and firm characteristics. Two Australian studies that have examined

the quality of derivative disclosures are also reviewed.

Chapter four discusses prior research on the value relevance of financial instruments.

The review provides a basis for understanding the benefits of disclosure to capital

market participants and firms. This chapter describes how capital market research has

emerged in accounting and how researchers use capital market data to explain the

relevance and reliability of financial statement information. Studies examining the

value relevance of financial instruments in the U.S., especially the fair value of

financial instruments, are reviewed. This helps to explain the need for extending value

relevance studies in other jurisdictions.

Chapter five describes the research questions developed based on the Australian

institutional environment and the prior literature. This study proposes questions that

relate to the disclosure quality of derivative information to the size of the firm,

performance of the firm, auditor, type of the extractive firm (limited liability or no-

liability firm), leverage and growth opportunities. Five research questions are

proposed that relate to the value relevance of derivative disclosures in firm valuation.

Chapter six describes the research methods and data collection procedures adopted.

Two main models are developed based on research questions presented in chapter

five. These are the firm characteristics model and market value model. Results on the

firm characteristics model are presented in chapter seven. Chapter seven provides

evidence that the quality of derivative disclosures has increased. The higher quality

Chapter 1: Introduction

11

derivative disclosures are associated with larger firms, performance of the firms and

high leverage firms.

Chapter eight presents the results of the market value model. The results indicate that

market participants regard disclosure quality as value relevant. However, the net fair

value information component is not significant, whereas the hedge information and

risk information components are value relevant. Also significant, to a limited extent,

is the net fair value of financial instruments. However, the incremental explanatory

power of net fair value and the unrealised gain or loss on financial instruments beyond

the book value of financial and non-financial instruments and earnings valued at

historical cost is very low. Nevertheless, the incremental explanatory power of net fair

value and the unrealised gain or loss on financial instruments has increased from 1998

to 2001.

Chapter nine provides some concluding comments. The chapter discusses the

contributions of the thesis to the literature, the limitations of the study and some

potential avenues for future research.

Chapter 2: Institutional Background

12

CHAPTER 2 INSTITUTIONAL BACKGROUND This chapter describes the institutional background surrounding financial instruments,

particularly derivative instruments. The organisation of this chapter is as follows. The

following section provides the institutional background, focusing on the current

situation for financial reporting of derivative instruments. Section 2.1 provides

background on the risks attached to the use of financial instruments and how firms

can manage their exposure to risks. Subsection 2.1.1 discusses whether firms should

use derivative instruments to hedge their exposure. Section 2.2 describes the

accounting standards issued by both the Financial Accounting Standards Board

(FASB) and the International Accounting Standard Board (IASB). This is followed by

a discussion of the accounting standard on derivative disclosures issued by the

Australian Accounting Standards Board (AASB). Section 2.3 describes fair value

accounting and section 2.4 presents research on derivative instruments in Australia.

Section 2.5 discusses risk management practices commonly used in the extractive

industries. Section 2.6 summarises the chapter.

2.1 Risk Management

Financial instruments5 expose firms to financial, economic and operational risks.

Changes in market conditions or the financial position of the parties to the financial

instruments or transactions expose firms to financial and economic risks. These risks

5 AASB 1033 defines a financial instrument as any contract that gives rise to both a financial asset of one entity and a financial liability or equity instrument of another entity.

Chapter 2: Institutional Background

13

are credit risk6, interest rate risk7, foreign exchange risk8, market risk9 and liquidity

risk10. Firms generally use the most common and practical methods to reduce or

eliminate the risks. These include limiting the exposure to both individual

counterparties and the number of specific instruments held, or through hedging the

risks with sophisticated instruments such as forward contracts or swaps. Operational

risks include fraud, failure to collect the amount due and human error (Sarwal, 1989).

These risks can be reduced through internal control. The focus of this section is on the

financial and economic risks, whereby derivative instruments are used to reduce these

risks.

Banks and financial institutions first introduced derivative instruments to help firms

manage their exposure to these risks. It has been documented in the U.S. that

derivatives are used by large corporations to reduce their exposure to a variety of risks

(Géczy, Minton and Schrand, 1997). Competition among banks and financial

institutions led to the development of innovative derivative instruments. To enable

firms to better manage the risks and uncertainties, financial institutions in particular,

have developed a variety of complex financial instruments (Scott, 1997). These

innovative instruments are based on four basic derivative instruments, including

forward contracts, future contracts, options and swaps. A recent market survey by the

International Swaps and Derivatives Association (ISDA) indicates that the global

6 The risk that a borrower will not able to meet its obligations. The risk can be classified into country risk, industry risk, counterparty risk, settlement risk and transfer risk. 7 The risk of loss through mismatching the interest bases of assets and liabilities. The risk can be classified further into net interest risk, spread risk and basis risk 8 The risk of loss as a result of an unfavourable movement in exchange rates. 9 The risk of loss resulting from changes in the market value of negotiable instruments due to factors other than interest and exchange rates. 10 The risk can be classified as cash liquidity or market liquidity. Cash liquidity is the risk of loss resulting from the inability to meet financial obligations as they arise, due to a lack of liquid resources. Market liquidity refers to the risk of loss from not being quickly able to sell financial instruments at full market value, when required.

Chapter 2: Institutional Background

14

over-the-counter (OTC) derivatives volumes increased by 8.14% in 2000. The volume

globally totalled US$63.009 trillion at year-end 2000. According to Mr. Thomas K.

Montag, the vice-chairman of the ISDA, this is due to the continuing growth in

interest rates and currency products that influence managers to use the most effective

tools to manage potentially adverse economic movements (ISDA, 2002).

2.1.1 To Hedge or Not to Hedge?

Exposure to the risks can cause earnings volatility (Nance, Smith and Smithson, 1993;

and Pincus and Rajgopal, 2002) and financial managers can manage the risks in

several ways. They can either do nothing, or alternatively they can hedge the risks.

Managers can hedge the exposure internally or externally (Hassan, 1994, p. 11;

Hassan, Mohd Saleh and Ismail, 1996; 1998). Internal hedging requires firms to use a

variety of in-house options such as matching techniques, intercompany netting

systems, pricing considerations and asset and liability management. On the other

hand, external hedging requires firms to use a variety of hedging products, such as

forward contracts, swaps and futures contracts11, available in the market to minimise

or offset the risk.

Previous studies have examined the motivation for firms to purchase hedging

instruments. These include the perception that hedging can increase firm value, by

reducing expected taxes, expected costs of financial distress or other agency costs

(Nance et al., 1993). Guay (1999) indicates that firms use derivatives to hedge the

entity risks. Perhaps by hedging managers are able to present the true earnings

11 These instruments are known as derivative financial instruments.

Chapter 2: Institutional Background

15

capacity of the firms since hedging reduces factors that are outside of managerial

control (DaDalt, Gay and Nam, 2001). However, Koonce, McAnally and Mercer

(2000) indicate that investors are less willing to invest in a company that uses

derivatives as they judge derivatives as riskier than non-derivatives.

Under certain circumstances hedging firm risk increases a firm’s value (Nance et al.,

1993). The value of the firm increases by reducing expected taxes, the costs

associated with financial distress and agency costs. Koonce et al. (2000) conduct three

experimental studies to provide evidence on risk. They document that investors do

consider traditional risk factors, i.e. probabilities and outcomes, when judging the risk

of financial items. However, investors put greater weight on loss probabilities and loss

outcomes than on gain probabilities and gain outcomes.

Barnes (2001) indicates that two factors motivating firms to hedge the risks are: a)

maximisation of shareholder value and b) maximisation of managerial utility. Prior

studies investigate three issues that are associated with corporate risk management

within the shareholder maximisation hypotheses. These are financial distress,

investment policy and taxation. Managerial risk aversion and signalling managerial

skills are two variables that are associated with corporate risk management within the

managerial utility maximisation hypothesis.

Tufano (1996) extends research by Smith and Stulz (1985), Stulz (1984, 1990),

DeMarzo and Duffie (1995), Nance et al. (1993), Lessard (1990) and Breeden and

Viswanathan (1996) (in Tufano, 1996) in the gold mining industry. He found that the

predictions of shareholder maximisation hypothesis are not well supported by the

Chapter 2: Institutional Background

16

data. However, Tufano found that firms whose managers own more stock options

manage less gold price risk and those firms whose managers have more wealth

invested in common stock manage more gold price risk (managerial utility

maximisation hypothesis).

Géczy, Minton and Schrand (1997) extend previous studies by examining the use of

currency derivatives of firms that have ex ante exposure to foreign exchange-rate risk.

They found that firms with greater growth opportunities and tighter financial

constraints are more likely to use currency derivatives. Further, they found that firm

characteristics were related to the costs of implementing a specific derivatives

strategy. They also provide evidence that the benefits of using currency derivatives

are related to the general decision to use currency derivatives and the specific choice

between the various types of currency instruments.

2.2 International Accounting Practices

Investors have been alerted to the importance of transparent financial reporting of risk

and uncertainty as recent significant losses experienced by prominent companies, such

as Barings Plc., Proctor and Gamble and Gibson Greeting, resulted from the

inappropriate use of derivatives. Since then, financial reporting has witnessed an

increase in the disclosure of risk information by U.S. and U.K. companies. Most

accounting standard setters (especially in the U.S.), the International Accounting

Standard Board (IASB) and those in the U.K. have been forced to respond by

requiring more disclosures. The following subsections discuss the development of the

Chapter 2: Institutional Background

17

respective accounting standard issued by the Financial Accounting Standard Board

(FASB) and the IASB.

2.2.1 Financial Accounting Standard Board

The Financial Accounting Standards Board (FASB) in the United States has issued

seven accounting pronouncements pertaining to financial instruments since 1990.

Compared to other accounting standards boards, the FASB is more advanced in

regulating the accounting treatment for derivative instruments, even though the

approach employed has been piecemeal (Blankley and Scroeder, 2000). However, the

development of the regulation for derivative instruments (SFAS 133 Accounting for

Derivative Instruments and Hedging Activities) took the FASB 10 years.

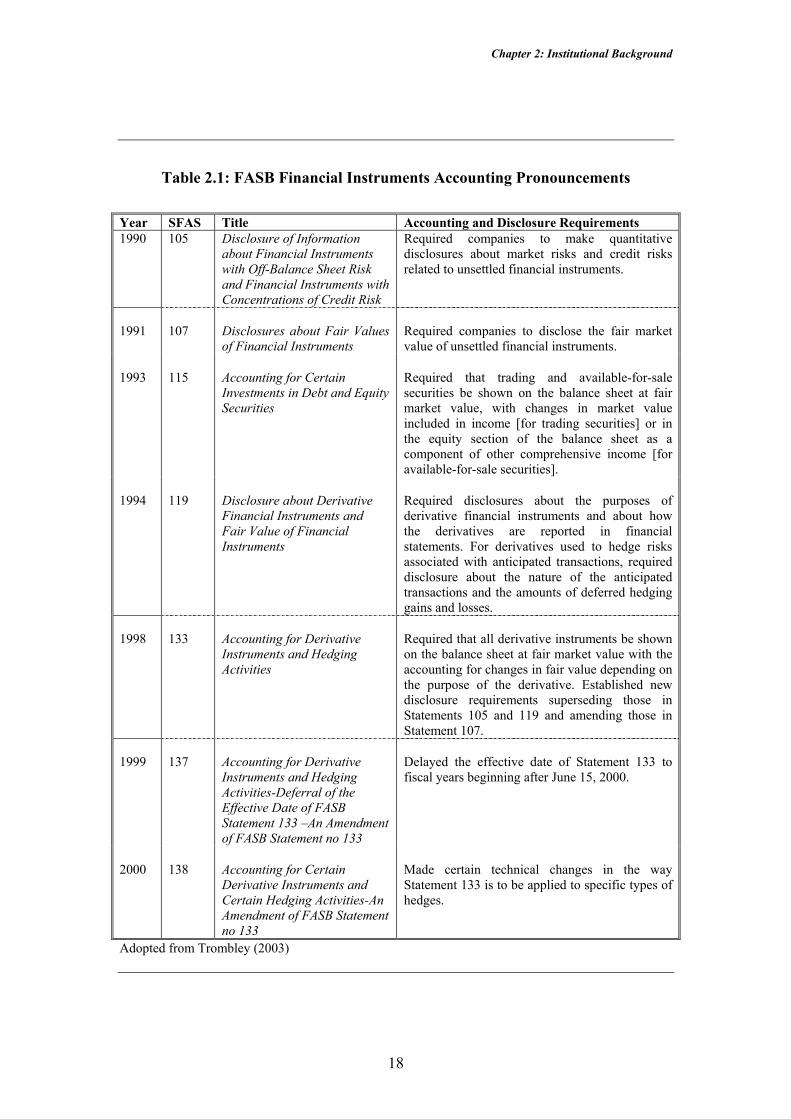

Table 2.1 summarises the progress of the FASB financial instruments accounting

pronouncements. Prior to the issuance of SFAS 133, the FASB has issued SFAS 119

Disclosure about Derivative Financial Instruments and Fair Value of Financial

Instruments, to improve the previous standards12. In 1998 the FASB issued SFAS

133. However, its implementation was deferred until 2000. The standard requires all

derivative instruments to be shown on the balance sheet at fair market value.

Nevertheless, the FASB issued SFAS 138 as an amendment to SFAS 133, wherein

certain technical changes from SFAS 133 are introduced.

12 Summary of this standard is presented in Table 2.3.

Chapter 2: Institutional Background

18

Table 2.1: FASB Financial Instruments Accounting Pronouncements Year SFAS Title Accounting and Disclosure Requirements 1990 105 Disclosure of Information

about Financial Instruments with Off-Balance Sheet Risk and Financial Instruments with Concentrations of Credit Risk

Required companies to make quantitative disclosures about market risks and credit risks related to unsettled financial instruments.

1991

107

Disclosures about Fair Values of Financial Instruments

Required companies to disclose the fair market value of unsettled financial instruments.

1993

115

Accounting for Certain Investments in Debt and Equity Securities

Required that trading and available-for-sale securities be shown on the balance sheet at fair market value, with changes in market value included in income [for trading securities] or in the equity section of the balance sheet as a component of other comprehensive income [for available-for-sale securities].

1994

119

Disclosure about Derivative Financial Instruments and Fair Value of Financial Instruments

Required disclosures about the purposes of derivative financial instruments and about how the derivatives are reported in financial statements. For derivatives used to hedge risks associated with anticipated transactions, required disclosure about the nature of the anticipated transactions and the amounts of deferred hedging gains and losses.

1998

133

Accounting for Derivative Instruments and Hedging Activities

Required that all derivative instruments be shown on the balance sheet at fair market value with the accounting for changes in fair value depending on the purpose of the derivative. Established new disclosure requirements superseding those in Statements 105 and 119 and amending those in Statement 107.

1999

137

Accounting for Derivative Instruments and Hedging Activities-Deferral of the Effective Date of FASB Statement 133 –An Amendment of FASB Statement no 133

Delayed the effective date of Statement 133 to fiscal years beginning after June 15, 2000.

2000

138

Accounting for Certain Derivative Instruments and Certain Hedging Activities-An Amendment of FASB Statement no 133

Made certain technical changes in the way Statement 133 is to be applied to specific types of hedges.

Adopted from Trombley (2003)

Chapter 2: Institutional Background

19

2.2.1.1 SFAS 133 Accounting for Derivative Instruments and Hedging Activities.

This standard requires that all derivative instruments are to be measured at fair value

and recognised in the statement of financial position either as assets or liabilities. The

derivatives can be designated into three types of exposures: fair value exposure, cash

flow exposure and exposure to changes in the value of net investment in a foreign

operation (Trombley, 2003, p.34), if certain conditions are met13. The derivatives are

to be accounted for in the financial statements based on their intended use and their

resulting designation14. The gain or loss for a fair value hedge15 is recognised in

earnings in the period of change together with the offsetting loss or gain on the

hedged item attributable to the risk being hedged. The treatment also applies to a

derivative designated as a hedge of the foreign currency exposure of an unrecognised

firm commitment or available for sale security.

The total gain or loss for a cash flow hedge16 has to be separated into the effective and

ineffective portions. The effective portion of the gain or loss is initially reported as a

component of other comprehensive income and subsequently reclassified as an

earnings component when the forecasted transaction affects earnings. However, the

ineffective portion will immediately be reported in the earnings component. This

treatment also applies to a derivative designated as a hedge of the foreign currency

exposure of a foreign-currency-denominated forecasted transaction.

13 The conditions where hedge accounting is allowed relate to: a) the nature of the hedged risk (interest rate risks, price risks, foreign currency exchange risks and credit risks), b) the hedge effectiveness and c) documentation. 14 The intended use or designation refers to the purpose of the hedging. The results from the designation is the gain or loss that can off-set the loss or gain from the hedged item. 15 Refers to derivatives designated as hedging the exposure to changes in the fair value of a recognised asset, liability or an unrecognised firm commitment. 16 A derivative designated as hedging the exposure to variable cash flows of a forecasted transaction.

Chapter 2: Institutional Background

20

The gain or loss for a foreign currency hedge on foreign currency exposure of a net

investment in a foreign operation is to be reported in other comprehensive income as

part of the cumulative translation adjustment. The gain or loss for a derivative not

designated as a hedging instrument is recognised in earnings in the period of change.

2.2.2 International Accounting Standards Board

2.2.2.1 IAS 32 Financial Instruments: Disclosure and Presentation IAS 32 was approved by the International Accounting Standards Committee (IASC)17

Board in March 1995 to deal with the disclosure and presentation of financial

instruments. This standard was the result of a joint project with the Canadian Institute

of Chartered Accountants. The standard was amended twice, (once in 1998 and again

in 2000) to be consistent with IAS 39 Financial Instrument: Measurement and

Recognition, issued after IAS 32 and to eliminate any disclosure requirements made

redundant by IAS 39. Basically, IAS 32 deals with the: a) classification of financial

instruments as liabilities or equity, by the issuers, and the classification of related

interest, dividends and gain or loss, b) offsetting of financial assets and financial

liabilities and c) disclosure of information about financial instruments.

The standard requires:

the issuer of a financial instrument to classify the instrument (or its component parts) as a liability or as equity in accordance with the substance of the contractual arrangement on initial recognition and the definitions of a financial liability and an equity instrument.

17 The IASC became the International Accounting Standard Board (IASB) in 2001.

Chapter 2: Institutional Background

21

The instrument is classified as a financial liability when the issuer is obliged to deliver

cash or another financial asset to another party. The classification continues until the

financial instrument is removed from the enterprise’s balance sheet. As an example, a

company issues a mandatory redemption preferred share for a fixed amount at a fixed

date. Since there is a contract that obliges the issuer to redeem the instrument at the

predetermined amount and date, the instrument must be reported as a financial

liability.

However, when the issuer issues a financial instrument that contains both a liability

and equity element, the standard requires a separate presentation of the instrument’s

components on the issuer’s balance sheet. A convertible bond is an example of such a

financial instrument.

The standard also requires the enterprise to present a financial asset and a financial

liability on a net basis when it:

i.has a legally enforceable right to set off the recognised amounts; and

ii.intends either to settle on a net basis, or to realise the asset and

settle the liability simultaneously. The standard requires firms to disclose: a) risk management policies, including the

policy for hedging each major type of forecasted transaction (paragraph 43A, IAS 32),

b) terms, conditions and accounting policies for each class of financial asset, financial

liability and equity instruments, both recognised and unrecognised (paragraph 47), c)

interest rate risk exposure (paragraph 56), d) credit risk exposure (paragraph 66), e)

fair value of each class of financial assets and liabilities, recognised and unrecognised

Chapter 2: Institutional Background

22

(paragraph 77) and f) financial assets carried at an amount in excess of fair value

(paragraph 88).

2.2.2.2 IAS 39: Financial Instruments: Recognition and Measurement

The second phase of the joint project between the IASC and the Canadian Institute of

Chartered Accountants addresses the issues of recognition, de-recognition,

measurement and hedge accounting. As a result, IAS 39 was issued in December

1998. The standard addresses the issues of recognition and measurement only. The

standard requires: a) all financial assets and financial liabilities, including derivatives,

to be recognised on the balance sheet and measured at cost (which is the fair value of

the consideration given or received to acquire the financial asset or liability), b)

subsequent to initial recognition, all financial assets should be re-measured at fair

value (except for loans and receivables originated by the enterprise, other mixed

maturity investments and financial assets whose fair value cannot be reliably

measured), c) most financial liabilities (except for derivatives and liabilities held for

trading which should be remeasured to fair value) be measured at their original

recorded amount less principal repayments and amortisation and d) those financial

assets and liabilities that are remeasured to fair value, a firm has the option to either: i)

recognise the entire adjustment in net profit or loss for the period, or ii) recognise

changes in fair value (the period only) of financial assets and liabilities held for

trading in net profit or loss, and for non-trading instruments, the change in value is

reported in equity until the financial asset is sold, at which time the realised gain or

loss is reported in net profit or loss.

Chapter 2: Institutional Background

23

2.2.3 Accounting for Financial Instruments in Australia

2.2.3.1 AASB 1033 Presentation and Disclosure of Financial Instruments

AASB 1033 Presentation and Disclosure of Financial Instruments was issued in 1996

and developed based on ED 65 Presentation and Disclosure of Financial Instruments.

The predecessor of ED 65, ED 59 Financial Instruments, was released in March 1993.

However, ED 59, which attempted to introduce recognition and measurement rules for

financial instruments in addition to disclosure requirements, was withdrawn.

Extensive lobbying against the recognition and measurement of financial instruments

caused the Australian standard setters to defer the recognition and measurement issue

until an equivalent international standard was issued.

All publicly listed companies in Australia, which issue or hold financial instruments,

should comply with the requirements of AASB 1033. The standard focuses only on

the presentation and disclosure of financial instruments. AASB 1033 was

subsequently amended in 1999 to include the requirement of converting financial

instruments to achieve greater harmonisation with the international standard, IAS 32

Financial Instruments: Disclosure and Presentation, which was amended to reflect

the issuance of IAS 3918 as discussed in a previous subsection. Table 2.2 presents a

summary of the development of accounting standards for financial instruments in

Australia.

18 With the move to full harmonisation in 2005, it is planned that Australia will adopt the requirements of IAS 39 Financial Instruments: Recognition and Measurement issued in 1999.

Chapter 2: Institutional Background

24

Table 2.2: Summary of Development of Accounting Pronouncements Related to Financial Instruments in Australia

Date

issued Pronouncement Title Application