Embed Size (px)

Citation preview

THE INFLUENCE OF THE ORIGINAL LOCAL

GOVERNMENT REVENUE (PAD) AND GENERAL

ALLOCATION OF FUNDS (DAU) TO LOCAL GOVERNMENT

EXPENDITURES

(Case Study in 10 Districts/Cities in Lampung Province)

Written by :

Merdiansyah

NIM. 109082100008

INTERNATIONAL PROGRAM

ACCOUNTING DEPARTMENT

FACULTY OF ECONOMIC AND BUSINESS

STATE ISLAMIC UNIVERSITY SYARIF HIDAYATULLAH

JAKARTA

1434 H / 2013 M

iii

v

ii

CURRICULUM VITAE

PERSONAL DATA

Name :

Merdiansyah

Place, date of birth :

Karta, march 22nd

1990

Current Address :

Jl. H. ir. Juanda, gang karyawan no.39 RT 004/ RW 001 kel. Ciputat tanggerang selatan, banten

Permanent Address :

Jl. Ratu Pengadilan no. 3 RT 002/ RK 002 karta, Tulang Bawang Barat, Lampung.

Nationality :

Indonesia

Phone :

+6281284518282

Email :

[email protected] [email protected]

Hobbies & Interests :

Dragbike, futsal & learning new thing

GPA :

3,43

CAREER OBJECTIVE

EDUCATION

2009 – 2013

syarif hidayatullah Islamic state university, Jakarta

International accounting

2006 – 2009

Al-Kautsar Senior High School

Social

2005 - 2006

Al-Kautsar Junior High School

2003 - 2005

Public 2 Junior High School

1997 - 2003

Public 2 Elementary school

WORKING EXPERIENCE & INTERNSHIP

2012 CV. Buana Mahardika Field Supervisor

2011 CV. Radin Sebuai Field Supervisor

ORGANIZATION EXPERIENCE

2010-2012

“Himpunan Mahasiswa Lampung’ tanggerang selatan

Humas

ACHIEVEMENT

2010 One of Founder of “himpunan mahasiswa lampung” Syarif Hidayatullah Islamic State University”

TRAINING & SEMINAR

2012 DAAD Study trip go to Germany “democracy”

2011 “Learning how to be rich” Savinaturssalam social entity

2009 Moderate Muslim Society ”islam in the west and the east: boosting democracy, Human Rights, Freedom and peaceful coexistence”

LANGUAGE & SKILLSLANGUAGE

English Good

COMPUTER

Ms Office (MS Words, Ms Excel, Ms PowerPoint)

RELEVANT CERTIFICATE

Training Certificates

Implementing my knowledge which I learn from university and environment and develop it to enrich my experience..

vi

vii

ABSTRACT

This research aimed to analyze the influences of Original Local

Government Revenues (PAD) and General Allocation Funds (DAU) partially and

simultaneously to the Local Government Expenditures and analyze the which

Flypaper Effect occurred or not in 10 Districts/Cities in Lampung province at

2008- 2010.

This research is using purposive sampling method, that is aimed by the

researcher are likely to obtain information from specific target groups, the

sampling here is confined to specific types of people/sample which can provide

the desired information, either because they are the only ones which have it, or

conform to some criteria set by the researcher.

Among the number of districts / cities submitting the realization, APBD

Report between 2008 and 2010 to the www.djpk.depkeu.go.id site and

www.bps.go.id site are as many as 10 districts / cities in the Lampung Province

This research founds that local government revenues (PAD) has no

significant effect to Local Government Expenditures. The higher the PAD in

Local Government Revenue and Expenditure Budget (APBD), the higher

allocation of local government expenditures. The General Allocation Funds

(DAU) has a significant positive effect on the Local Expenditures (BD). Local

Government Revenue and Expenditure budget (APBD) with higher DAU will

have higher local government expenditures. This research has discovered that

Original Local Government Revenues (PAD) and the General Allocation Funds

(DAU) have a simultaneously impact on Local Government Expenditures (BD).

The authors concluded that there has been a Flypaper effect in 10

districts / cities in the Lampung province by analyze the composition of the Local

Government Revenue and Expenditure Budget (APBD) between the PAD, and the

Balanced Fund is much different.

Keyword : General allocation fund (DAU),Original Local Government

Revenues (PAD),the Local Expenditures (BD), Flypaper effect

viii

ABSTRAK

Penelitian ini bertujuan untuk menganalisis pengaruh Pendapatan Asli

Daerah (PAD) dan Dana Alokasi Umum (DAU) secara parsial dan secara

simultan terhadap Belanja Pemerintah Daerah dan menganalisis yang flypaper

effect terjadi atau tidak di 10 Kabupaten / Kota di Provinsi Lampung pada 2008-

2010.

Penelitian ini menggunakan metode purposive sampling, yang ditujukan

oleh peneliti yang mungkin untuk mendapatkan informasi dari kelompok sasaran

tertentu, sampling di sini terbatas pada jenis tertentu orang / sampel yang dapat

memberikan informasi yang diinginkan, baik karena mereka adalah satu-satunya

yang memilikinya, atau sesuai dengan beberapa kriteria yang ditetapkan oleh

peneliti.Di antara jumlah kabupaten / kota mengirimkan realisasi, Laporan APBD

antara tahun 2008 dan 2010 ke situs www.djpk.depkeu.go.id dan www.bps.go.id

disebutkan sebanyak 10 kabupaten / kota di Provinsi Lampung.

Penelitian ini menemukan bahwa pendapatan asli daerah (PAD)

berpengaruh positif terhadap Belanja Pemerintah Daerah. Semakin tinggi PAD

Pendapatan Daerah dan Belanja (APBD), alokasi lebih besar dari pengeluaran

pemerintah daerah. Dana Alokasi Umum (DAU) berpengaruh positif signifikan

terhadap Belanja Daerah (BD). Pendapatan Pemerintah Daerah dan Belanja

(APBD) dengan DAU yang lebih tinggi akan memiliki pengeluaran pemerintah

daerah yang lebih tinggi. Penelitian ini telah menemukan bahwa Pendapatan Asli

Daerah Pemerintah (PAD) dan Dana Alokasi Umum (DAU) secara bersamaan

memiliki dampak pada Belanja Pemerintah Daerah (BD).

Para penulis menyimpulkan bahwa telah terjadi flypaper effect di 10

kabupaten / kota di Provinsi Lampung dengan menganalisis komposisi

Pendapatan Daerah Pemerintah dan Belanja (APBD) antara PAD, dan DAU jauh

berbeda.

Kata kunc i: Pendapatan Asli Daerah (PAD), Dana Alokasi Umum (DAU),

Belanja Daerah (BD), flypaper effect

ix

FOREWORD

Assalamu’alaikum Wr.Wb

All praise to Allah SWT and Shalawat always gives to our Prophet

Muhammad SAW.

With the strength, intelligence, patience, and passion from Allah SWT, I

can to finish this my thesis as one of requirements to achieve bachelor degree. I

believe there is an invisible hand (God) which have helped me going through this

proces.

My special thank for my Mom, Rohida Adi, who has been helping and

support to finish the thesis. You are my angels in human form. So, I want to make

you always smile and proud of me at any situations. Thank you mom for

everything, I love you so much. You are the best mother in this whole world, and

thanks to allah because i have chance became your son.

My Beloved Father, Hersyah, who always give me lot of spirits and

motivations when i felt hopeless to finish my thesis. You always belived that I can

do everything on my own. You are the first man that I want to say thanks in the

world when I finish this thesis. I love you so much and thanks for everything.

I believe I am nothing without each one of you who has helped me to

finish this thesis. Thus, in this very special moment, let me say thanks to all of

them who were helped me through the process of this thesis, including:

1. Prof. Dr. Abdul Hamid, MS as Dean of Economic Faculty of UIN Syarif

Hidayatullah Jakarta.

x

2. Ahmad Dumyathi Bashori, MA as Head of International Program.

3. Prof. Dr. H.Margareth Gfrerer as my supervisor I. You are my inspiring

woman, thanks for your time, motivations, and knowledge which you had

given to me. So, I able to finish this thesis and the last thanks for quote “

do not become a man with developed country mindset if you want to

become number one”.

4. Abdul Hamid Cebba, Drs, Mba, Ak as my supervisor II who has provided

guidance and thank you for your time that you gave to me, I can finish this

mini thesis.

5. All Lecturers who have taught me patiently, may what they have given to

me useful in future and all staff UIN Jakarta, special thanks to:

Mr. Sugih Waluyo “thanks you have taught me and given explanation

about the thesis and also for provided any information”.

Mr. agusman who had gave motivations and change my mindset “do

not ever say IMPOSSIBLE but say I’M POSSIBLE”.

Mr. chairul anwar and Mrs. Ari purwanti thanks for your experience

and knowledge which you had shared to me.

Mr.Herni Ali, HT,. MM thanks for your directions, suggestions and

help so I can finish my study at university.

6. All my friends in Accounting International Program 6th

Batch (2009), who

helped me in finishing this thesis. Bunch of love for you guys Nanda, ,

Pipit, angga, bimo, dea, arini and eca thanks for every support and

motivation that you have gave to finish my thesis. ucup jihan, angga,

xi

Evi,cici, Diah, Septian tami, Opi and Aul thanks for every foolish things

and jokes that you have done, and you made my day full of laugh. Adnan,

Osman thanks for the time we have been through together for three and

half years. Senior, Junior, and management class thanks all who couldn’t

mention one by one “Thanks for your pray”.

7. My family.. Special thanks to my brother sadarsyah, SH, slamet

riyadi,S.E, and adam syah for moral and material supports my sister

Wahyuni Herda .

Authors realize that this thesis is still far from perfection, the suggestions

and constructive criticism from all parties are expected to improve further.

Finally, only Allah SWT will return all and writer hope this skripsi will be useful

to all parties, especially for writers and readers in general, may Allah bless us.

Amin.

Wassalammualaikum Wr.Wb.

Author

Jakarta, September 2013

(Merdiansyah)

xii

CONTENTS OF TABLE

INFORMATION PAGE

Cover ................................................................................................................... i

Certifivation From Supervisor ............................................................................ ii

Certification of Comprehensive Exam Sheet ...................................................... iii

Certification of Thesis Exam Sheet .................................................................... iv

Sheet Statement Authenticity Scientific Work .................................................... v

Curriculum Vitae ................................................................................................ vi

Abstract ............................................................................................................... vii

Abstract ............................................................................................................... viii

Foreword .............................................................................................................. ix

Table of Content ................................................................................................. xii

List of Tables ...................................................................................................... xiii

List of Figures ..................................................................................................... xiv

List of Appendix .................................................................................................. xv

Chapter I INTRODUCTION

A. Background Issues ................................................................ 1

B. Problem Formulation ............................................................. 7

C. Research Objectives .............................................................. 7

D. Research Benefits ................................................................. 8

Chapter II LITERATURE REVIEW

A. Theory Development ............................................................ 9

xiii

1. Local Government Budget (APBD) ............................... 10

2. Definition of Local Government Expenditures (BD) ..... 17

a. General Administration Expenditures ......................... 21

b. Operating Expenditures .............................................. 22

c. Capital Expenditures ................................................... 23

d. Transfer Expenditures ................................................. 23

e. Unexpected Expenditures ........................................... 23

3. Original Local Government Revenue (PAD) .................. 24

a. Local Taxes .............................................................. 26

b. Local Retribution ...................................................... 27

c. Results of Regional Owned-Enterprises and

Separated Local Wealth Management ...................... 28

d. Other Legal Revenue ............................................... 29

4. General Allocation Fund (DAU) ..................................... 30

B. Previous Research ................................................................. 32

C. Theoritical Framework ......................................................... 35

D. Hypothesis ............................................................................ 37

Chapter III RESEARCH METHODOLOGY

A. Scope of Research ................................................................. 38

B. Sampling Method .................................................................. 38

C. Data Collection Method ........................................................ 39

D. Data Analyze Method ............................................................ 39

1. Classical Assumption ...................................................... 40

xiv

a. Normality Test ........................................................... 40

b. Multicollinearity Test ................................................ 41

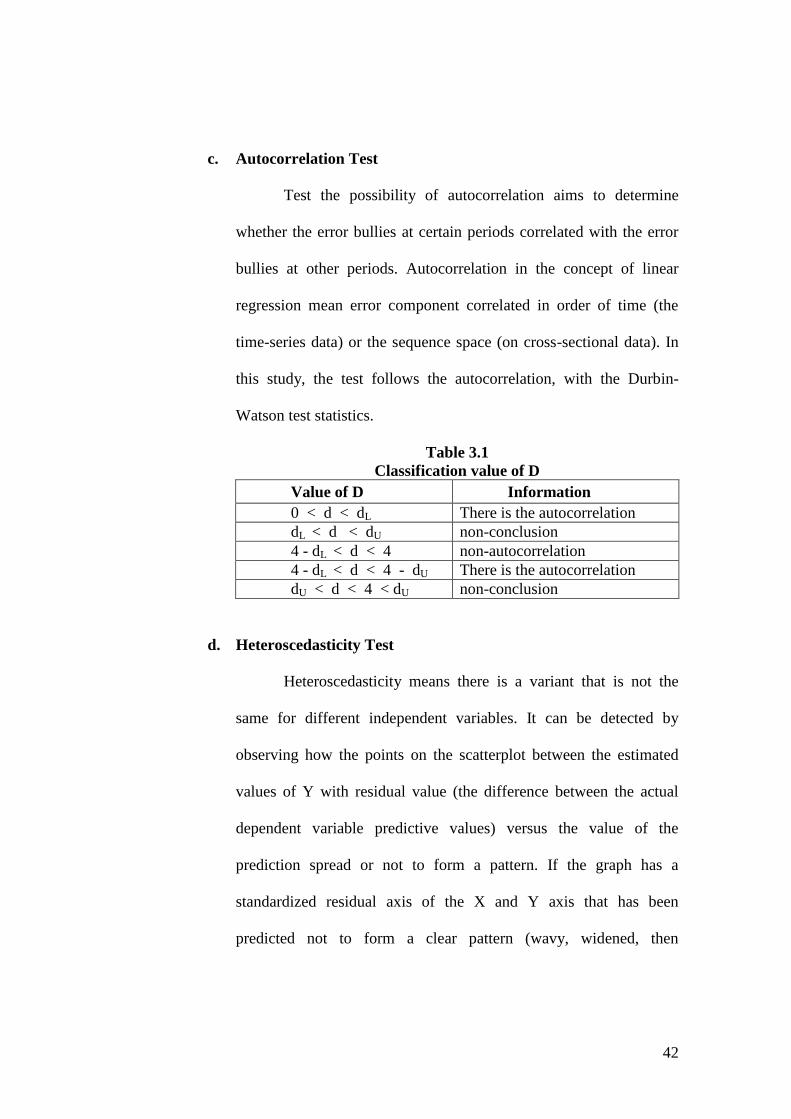

c. Autocorrelation Test .................................................. 42

d. Heteroscedasticity Test .............................................. 42

2. Hypothesis Testing .......................................................... 43

a. Multiple Regression .................................................. 43

b. Coefficient of Determination (R2) ........................... 44

c. Simultaneous Significance Test (F-Test) .................. 44

d. Partial Significance Test (t-Test) ............................... 45

E. Operational Variable ............................................................ 46

1. Original Local government revenue (variable X1) ........ 46

2. General Allocation Funds (Variable X2) ....................... 46

3. Local government Expenditures (Variable Y1) ............. 46

Chapter IV ANALYSIS AND DISCUSSION

A. General Description .............................................................. 48

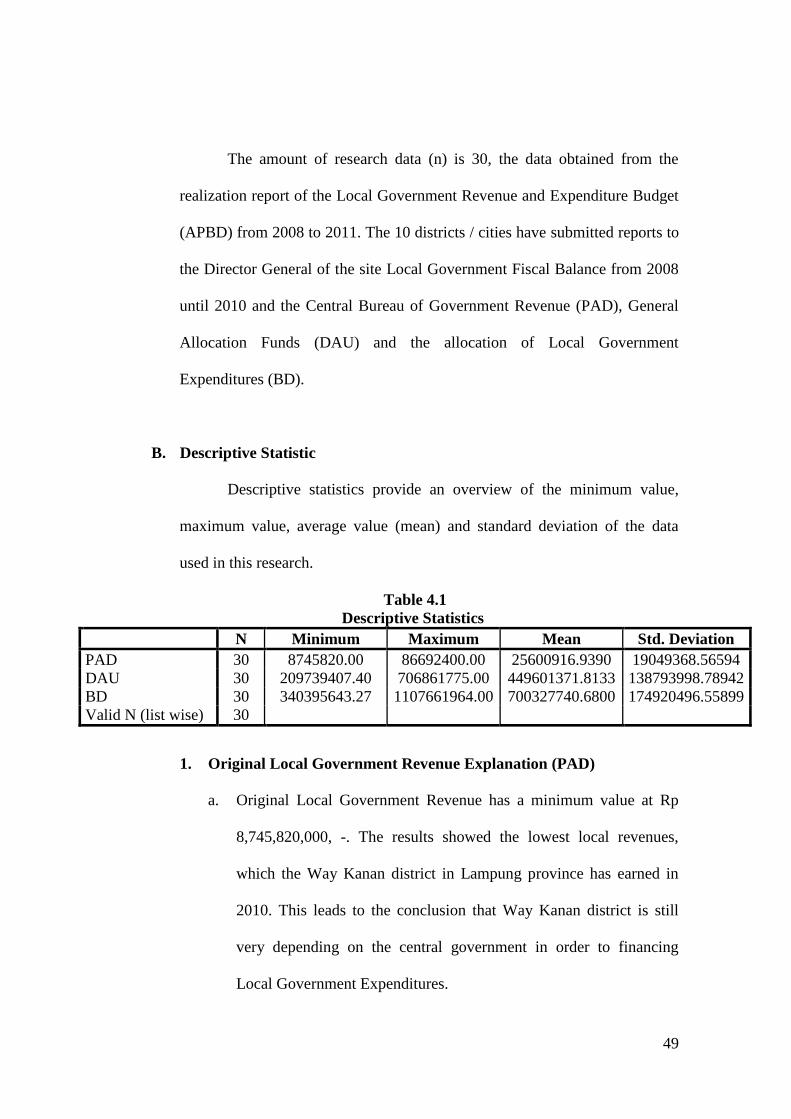

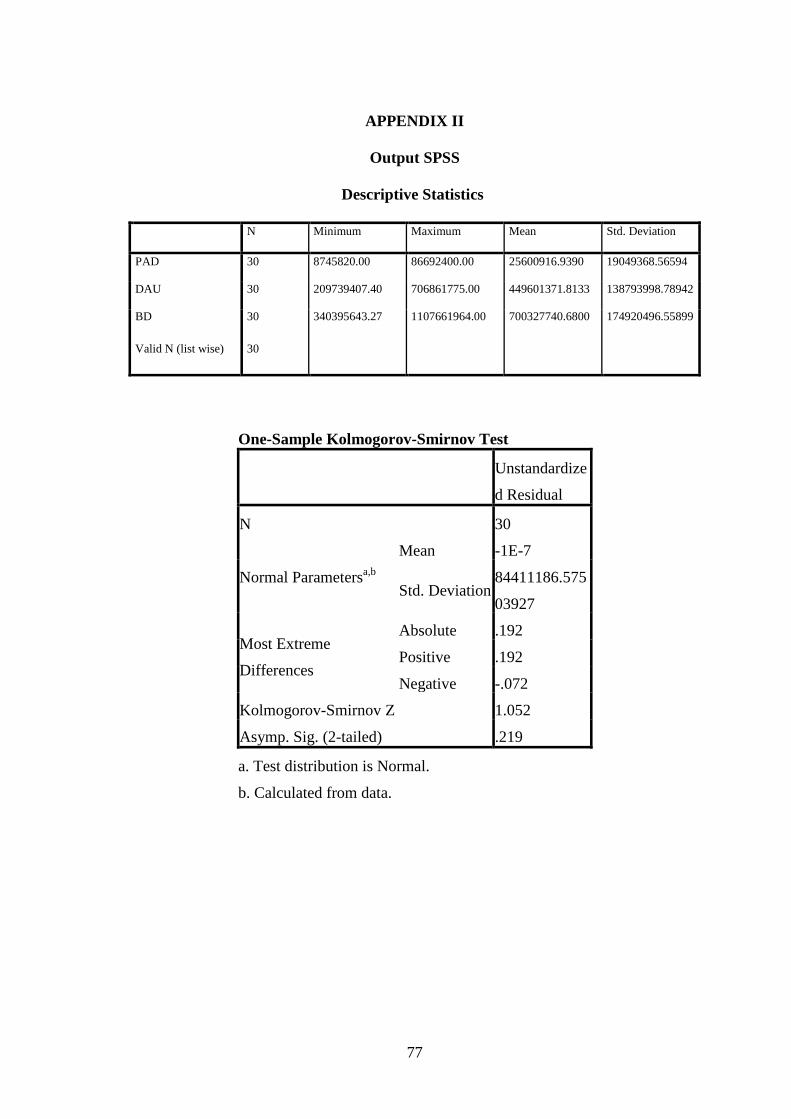

B. Descriptive Statistics ............................................................. 49

1. Original Local Government Revenue (PAD) ................. 49

2. General Allocation Funds (DAU) ................................... 50

3. Local Government Expenditures (BD) ........................... 51

C. Analysis and Discussion ....................................................... 52

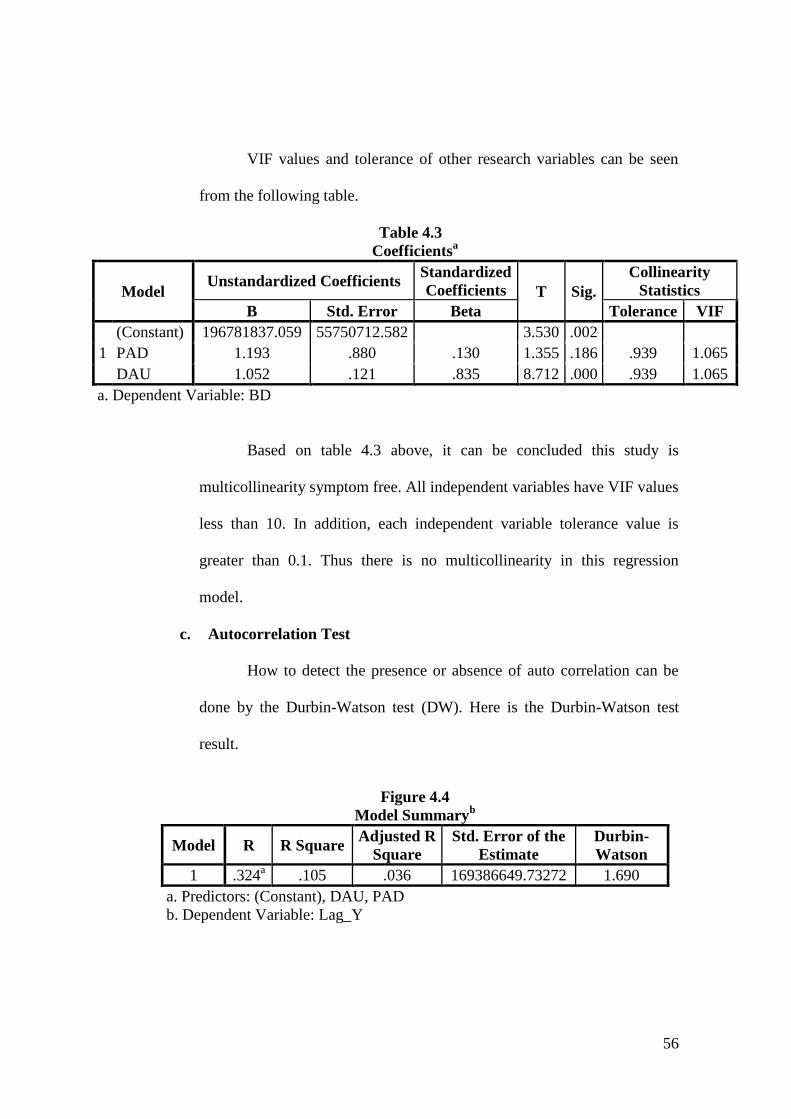

1. Classic Assumption Test ................................................. 52

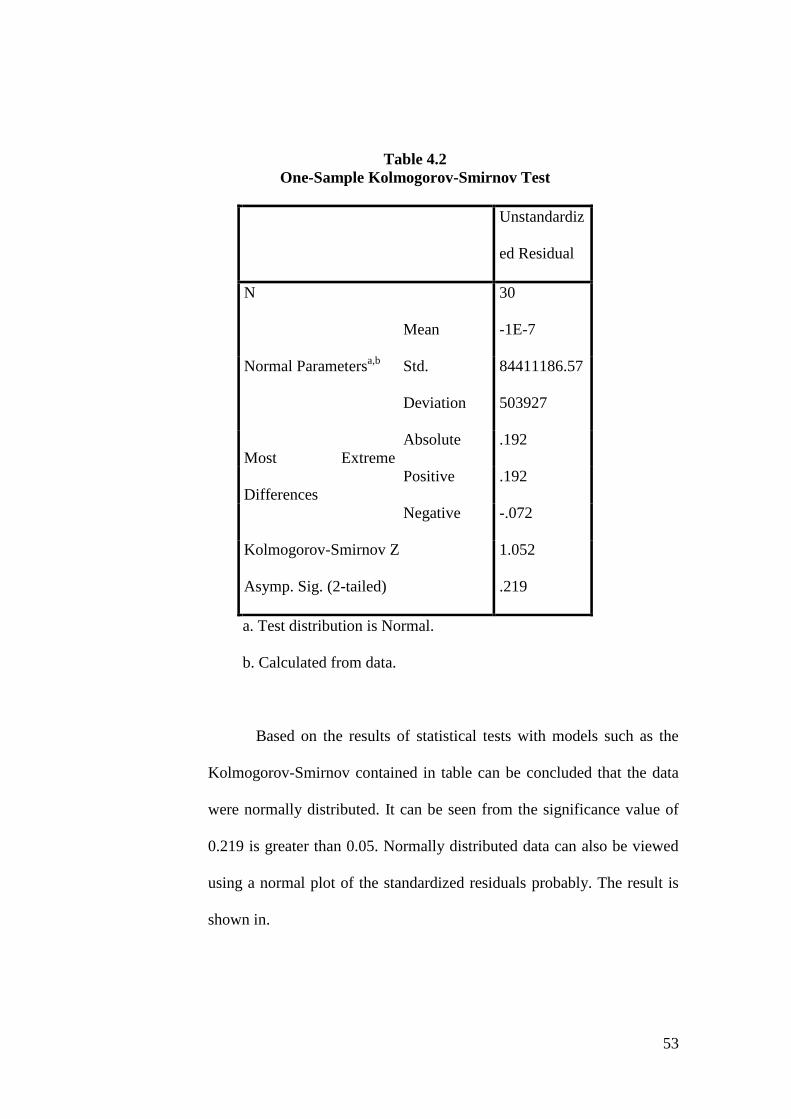

a. Normality Test ............................................................ 52

b. Multicollinearity Test .................................................. 55

xv

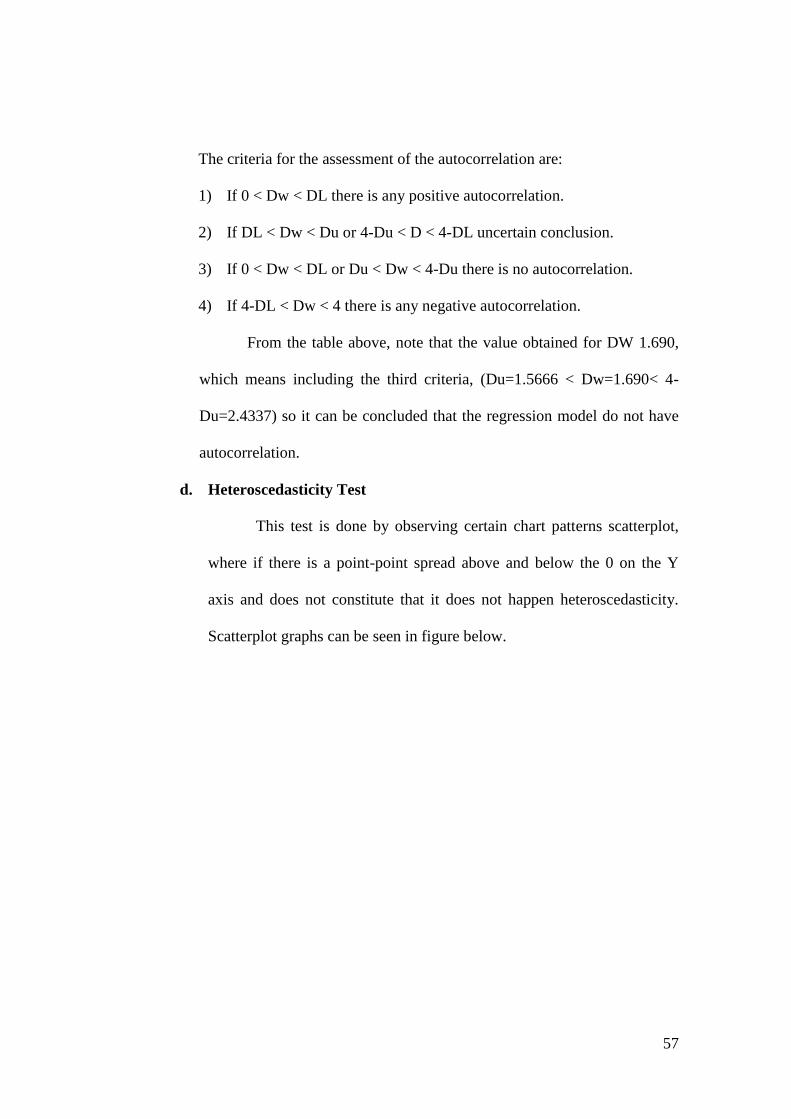

c. Autocorrelation Test ................................................... 56

d. Heterocedasticity Test ................................................ 57

2. Hypothesis Testing ......................................................... 58

a. Coefficient of Determination ..................................... 58

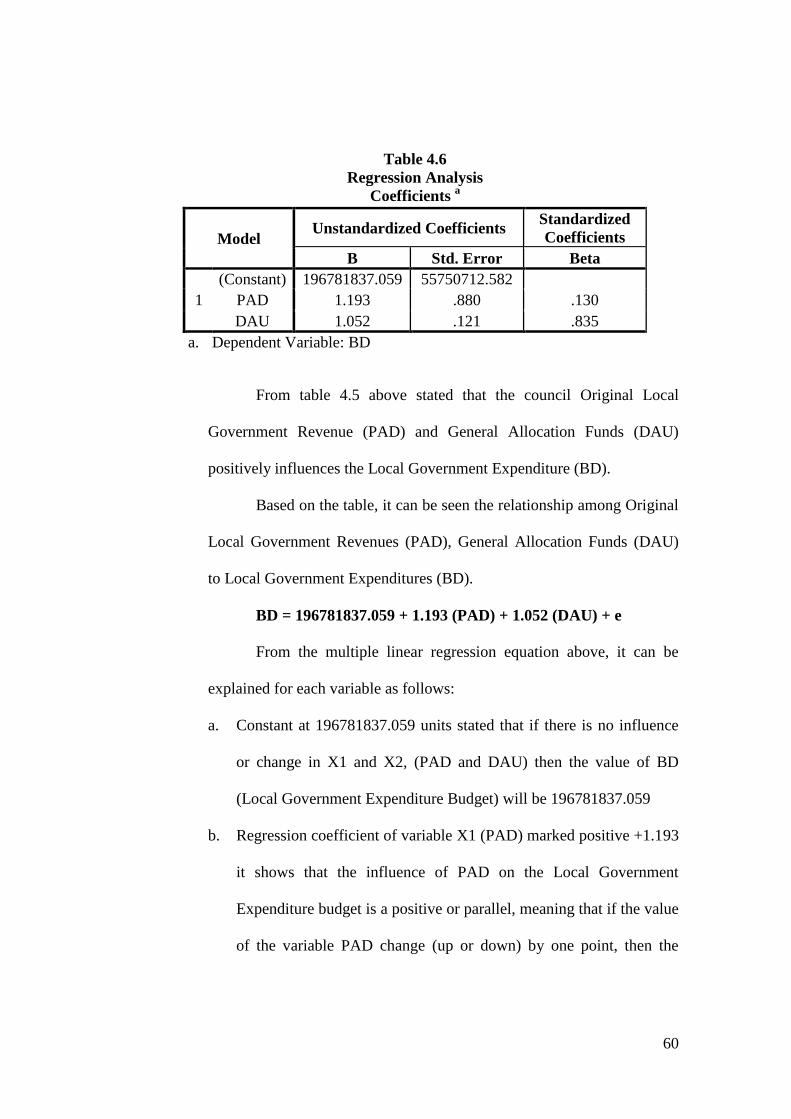

b. Multiple Linear Regression ........................................ 60

c. Simultaneous Significant Test (F-Test) ...................... 61

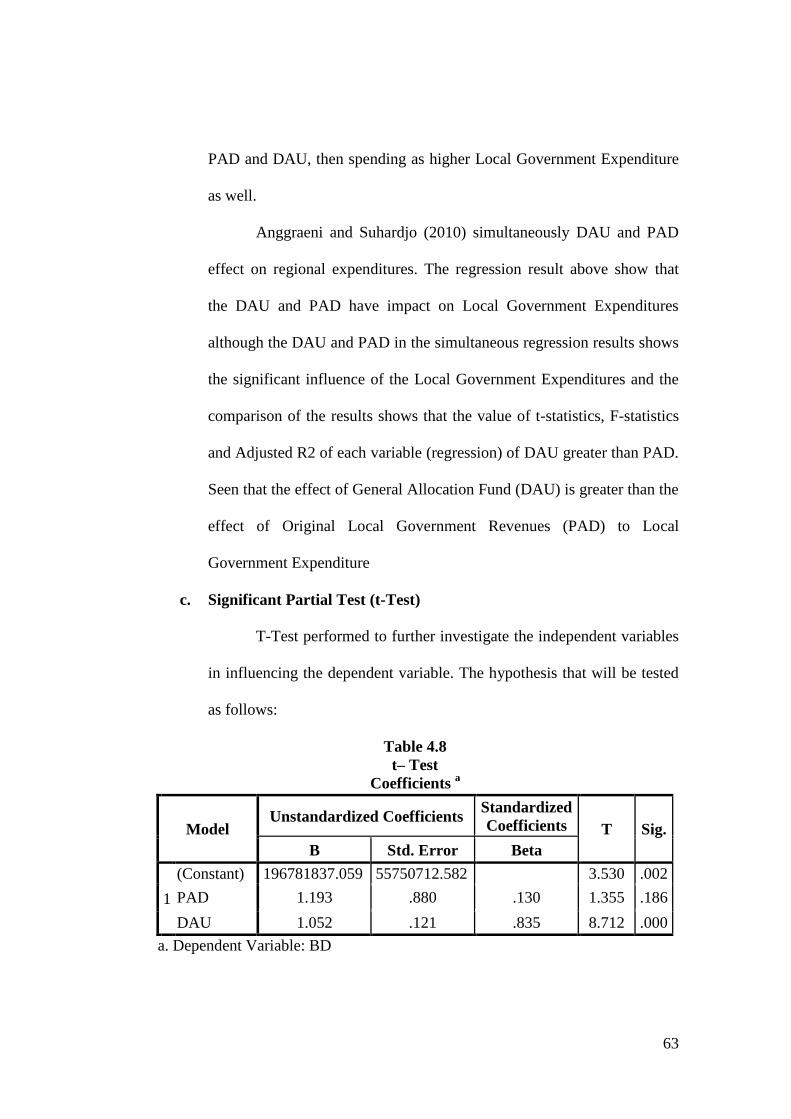

d. Significant Partial Test (t-Test) .................................. 63

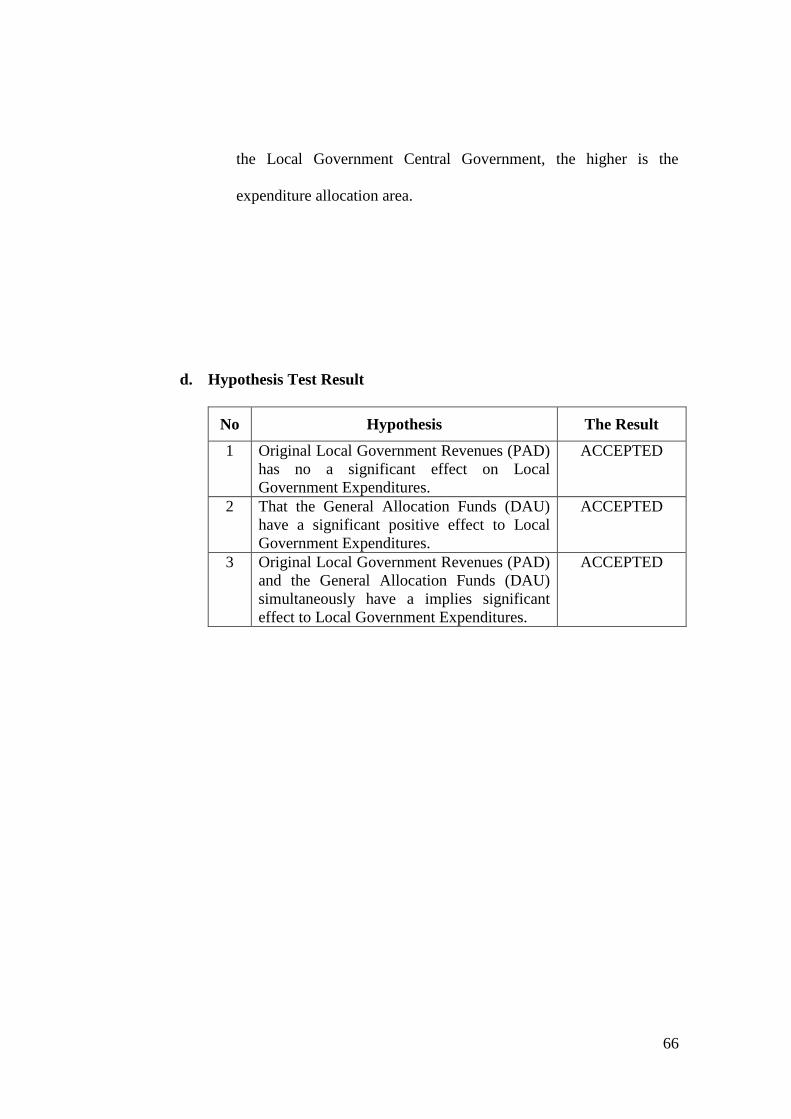

e. Hypothesis test result ................................................. 66

Chapter V CONCLUSIONS AND RECOMMENDATIONS

A. Conclusion ............................................................................ 67

B. Recomendation ..................................................................... 68

1. Local Government .......................................................... 68

a. Improving Strategy ................................................... 68

1). Local Tax ............................................................. 69

2). Regional Owned Enterprise (BUMD) ................. 70

3). Policy of side user ............................................... 71

2. Further Research ............................................................ 73

REFERENCE .................................................................................................... 74

APPENDIX I ..................................................................................................... 76

APPENDIX II .................................................................................................... 77

xvi

LIST OF TABLE

NO DESCRIPTIONS PAGE

2.1 Income and Expenditure Budget Chart ...................................................... 15

2.2 Previous Research Table ........................................................................... 34

3.1 Classification value of D ............................................................................ 42

4.1 Descriptive Statistics Test .......................................................................... 49

4.2 Kolmogorov-Smirnov Test ......................................................................... 53

4.3 Multicollinearity Test ................................................................................ 56

4.4 Autocorrelation Test ................................................................................... 56

4.5 Coefficient of Determination ...................................................................... 59

4.6 Multiple Regression ................................................................................... 60

4.7 Simultaneous Significant Test (F-Test) ..................................................... 62

4.8 Significant Partial Test (T-Test) ................................................................ 63

xvii

LIST OF FIGURE

NO DESCRIPTIONS PAGE

2.1 Theoritical Framework .............................................................................. 36

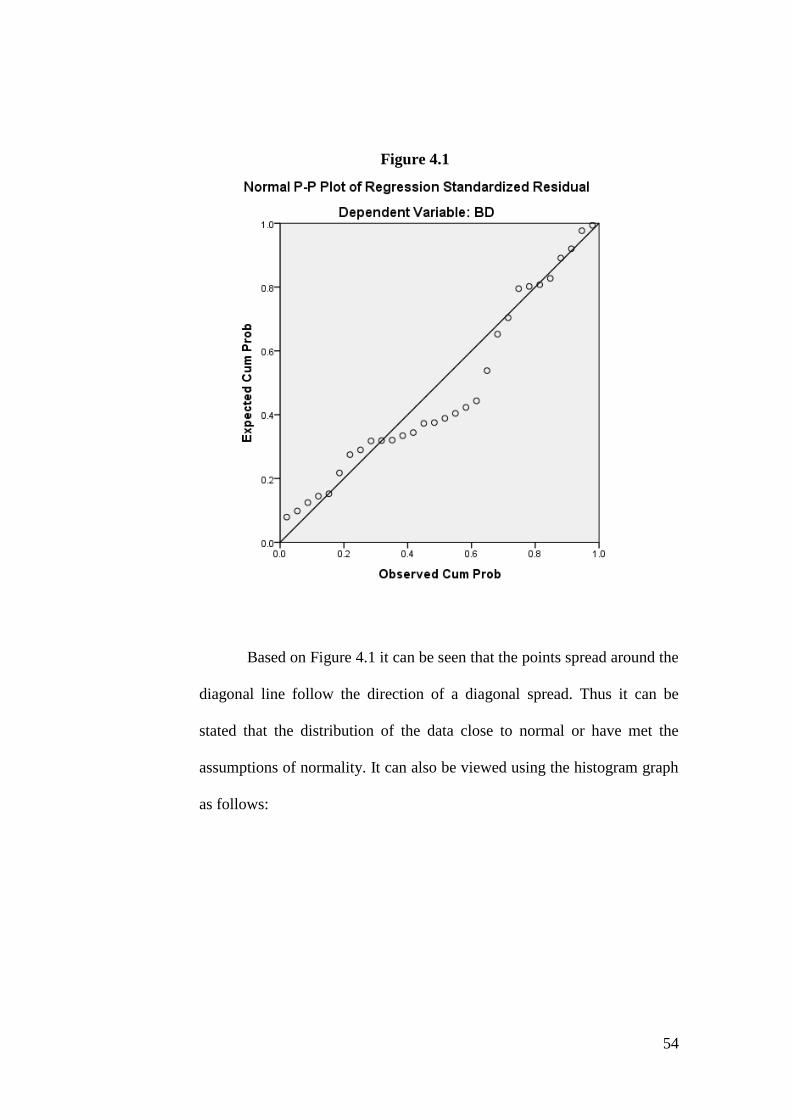

4.1 Normal P-Plot Graph ................................................................................. 54

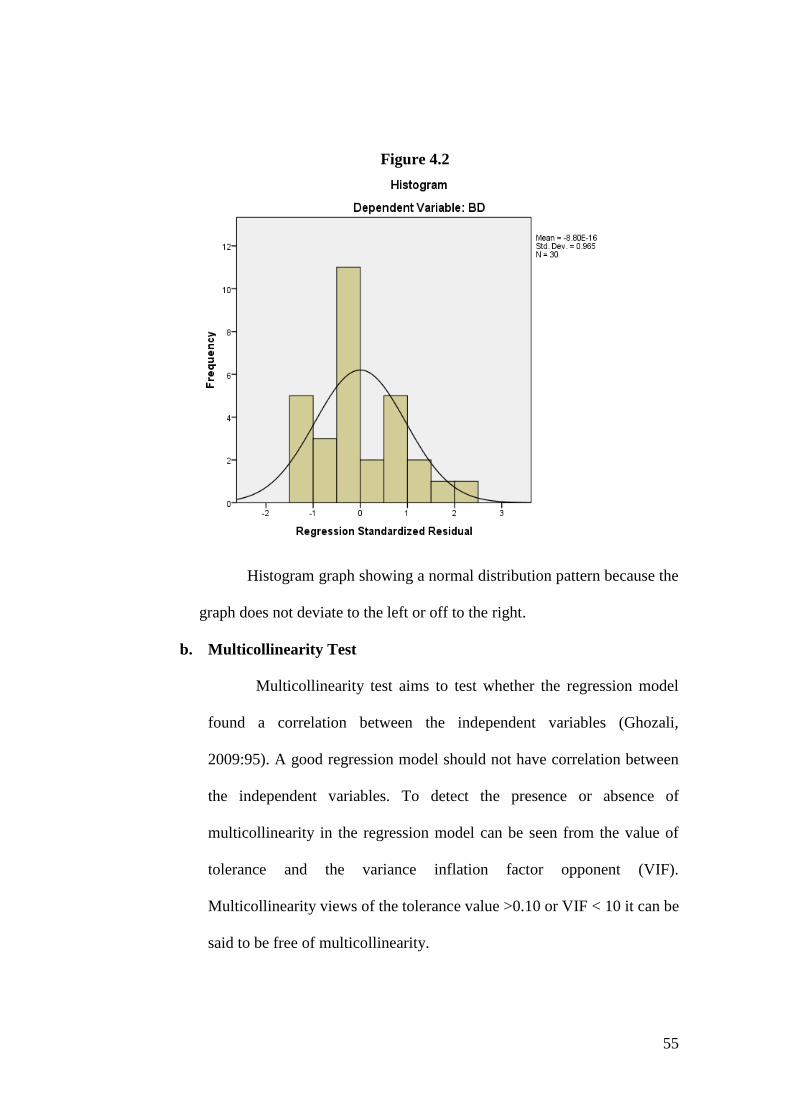

4.2 Histogram Graph ....................................................................................... 55

4.3 Heteroscedasticity Test .............................................................................. 58

xviii

LIST OF APPENDIXES

NO DESCRIPTIONS PAGE

Appendix 1 Research Data .............................................................................. 76

Appendix 2 Output SPSS That Used for the Result of the Research .............. 77

1

CHAPTER I

INTRODUCTION

A. Background Issues

In January 2001 in Indonesia began a new round of nation organizing

system on all government levels and is known as the regional autonomy.

Nearly all the authorities of the Central Government devolved on the area,

except for five the field; Foreign policy, Security, Defense, Justice, Finance

and Religion. Since then the budget of the Local Government from year to

year had shown significant improvements, both in terms of coverage of the

types of funds allocated, as well as the quantity of allocation. Local

Government Expenditures are prioritized to execute government affairs, which

consist of the mandatory affairs and the option affairs that are set on the basis

statutory.

The Reformation brought many changes in the life of nation and the

state, one of the many reforms that led to a change is the reform of Central

Government relations with Local Governments better known as the "Regional

Autonomy." The term “Regional Autonomy” is not new, it is already

mentioned within the laws of the Constitution of 1945. The current Regional

Autonomy associated with the Law No. 32 of 2004, which concerns on local

governments and has been revised in the Law No. 22 of 1999 and Law No. 25.

In 1999 about of Local Government and Fiscal Balance between the Central

Government and Local Government. The enforcement of both statuary Laws

2

made an impact on changing patterns of regional accountability over funds

allocated. The pattern in use is the Horizontal Accountability pattern through

the House of Representatives (DPR).

Through the Regional Autonomy Act, the authority of regional

autonomy has been set up and is administrating the interests of the local

communities according to their own initiatives based on the aspirations of the

community. Bastian (2002:2) states that regional autonomy is a local

empowerment effort in regional decision making related to the management of

its resources consistence with the interests, priorities, and the regional

potency.

Regional Autonomy demanded local governments to be able to

providing excellent service as well as good news to the community, one of the

forms the service is to provide information that is transparent and accountable.

The concept of Regional Autonomy requires.

1. Community empowerment

2. Democratization in the sense of giving responsibility to all communities

3. Opportunities To accelerate the equally society welfare

4. The improvement quality of bureaucracy service.

5. Improved quality of supervision by the legislature.

Public sector reforms that accompanied the demands of

democratization become a global phenomenon, including in Indonesia. The

demands of democratization led to transparency and accountability aspect.

Both aspects are important parts in Governance, especially in the field of

3

financial management of the State or regions. Public accountability means the

obligation of authorities to explain publicly, fully and fairly, before and after

the fact, how they are carrying out responsibilities that affect the public in

important ways (McCandless, 2008). These explanations, whether publicly

and objectively validated for their fairness and completeness, will produce not

only useful information for citizens but also a beneficial self-regulating

influence on the decisions of authorities. The economy observers, political

observers, investors and the community members begin to pay attention to any

policies in financial management.

The execution of Government financing based on the principle of

decentralization is expended to Local Government Revenue and Expenditure

Budgets (APBD). In the framework of Government activities and services to

the community is based on the principles of decentralization, which has

transferred the tax/levy collection and the management of Natural resources to

the local authorities. The source of funds for the region is consisting of the

Original Local Government Revenues, the Balanced Budget (DAU, DBH, and

DAK) and the Local Government Loans. The first three sources of the fund

namely the Original Local Government Revenues (PAD), the Balanced

Budgets and the Local Government Loans are directly managed and set by the

local government in the Local Government Revenues and Expenditures

Budget (APBD), while the others (Grants Funds, Emergency Funds) are

managed by the Central Government through cooperation with local

governments (Halim, 2007:21).

4

When local governments carry out their functions effectively and get

freedom in the public sector expenditure decision-making then their support

should be considered as a source of financial resources coming from the

Original Local Government Revenues (PAD), the Balanced Budgets (DAK,

DAU, DBH), the Local Government Financing, and others legal revenues

(Halim, 2007:22).

Original Local Government Revenues (PAD) are an area of earned

income withheld based on local regulations in accordance with legislation

(Act No. 33 of 2004). Optimization of the acceptance of the Original Local

Government Revenues should be supported by local government efforts to

improve the quality of public services (Mardiasmo, 2002). The Original Local

Government Revenues (PAD) per region are different. For regions, which

have advanced in the field of industry and have natural resources it is likely to

have greater Original Local Government Revenues (PAD) than the other

regions. Because of that an inequality of the Original Local Government

Revenues might occur. On one side, there are very rich regions with a high

PAD and on the other side, there are regions that are lagging behind with a

low PAD.

According to Halim (2009), the problems faced by the regions are seen

in the general deal with digging up the sources of taxes and local retribution. It

is one of the components of the Original Local Government Revenues (PAD),

Taxes and Retribution still do not give a contribution significantly to the

Original Local Government Revenues as a whole. Missing planning

5

capabilities and a weak financial supervision can result in leaks of the budget.

The role of the Original Local Government Revenues in financing Local

Government Expenditures is very small and varies among the regions.

Overall, the regional funding is somewhere between smaller than 10% and up

to 50% depending on the region.

The distribution of taxes between regions is unequal because the tax

bases among regions are different. The role of taxes and retribution in

financing regions is extremely low and this is due to the differences in terms

of population, geographical situation (impact on costs relatively expensive)

and the capability of the communities.

Many previous researchers have analyzed the influence of the General

Allocation Funds (DAU) and the Original Local Government Revenues

(PAD) to the Local Government Expenditures on the Java Island, Bali, even

Sumatra. The result of the analysis on the Sumatra Island about The Original

Local Government Revenues (PAD) showed no significance on the Local

Government Expenditures. A Flypaper Effect occurred. This is in accordance

with the hypotheses, which stated that the influence of General Allocation

Funds (DAU) against Local Government Expenditures is larger than the

influence of the Original Local Government Revenues (PAD) to Local

Government Expenditures. These results are consistent with the findings

before, such as Sukriy & Halim (2004) and Maemunah (2006). Noni Puspita

Sari (2009) examines in Riau results, i.e. DAU gives significant effects against

direct expenditures. While The PAD shows insignificant influence of direct

6

expenditures that PAD individually does not affect direct spending. From the

previous researches results, investigators had depth examination of the

influence of PAD and DAU to allocation of Local Government Expenditures,

particularly in Lampung province.

Indonesia is an archipelago consisting of 32 provinces and 434

districts/cities, each has its own characteristics and cultural customs, so the

effects of income or spending vary in each of the provinces/districts/cities

This research will focus on the different circumstances, which influence the

expenditure predictions of the DAU and the PAD in local governments in

Indonesia.

The Flypaper Effect is a financial condition of local governments,

which have spent more by using funds from the transfer of the Central

Government (DAU) than using own funds (PAD). This effect is the main topic

discussed in this study.

THE INFLUENCE OF THE ORIGINAL LOCAL GOVERNMENT

REVENUES (PAD) AND GENERAL ALLOCATION OF FUNDS (DAU)

TO LOCAL GOVERNMENT EXPENDITURES

(Case study in 10 districts/cities in Lampung province).

B. Problem Formulation

Based on the background described above, the subject is considered to

find answers on the following questions:

7

1. Does the General Allocation Funds (DAU) and Original Local

Government Revenues (PAD) effecting to the local government

expenditures (BD) partially and simultaneously in 10 Districts / cities in

Lampung province?

2. What is happening the Flypaper Effect ON the General Allocation Funds

(DAU) and the Original Local Government Revenues (PAD) against Local

Government Expenditure (BD) in 10 districts/cities in Lampung province?

C. Research Objective

The purposes of this research are:

1. To analyze the influences of Original Local Government Revenues (PAD)

and General Allocation Funds (DAU) partially and simultaneously the to

Local Government Expenditures in 10 Districts/ Cities in Lampung

province.

2. To analyze the Flypaper Effect occurred or not in 10 Districts/ Cities in

Lampung province.

D. Research Benefits

This research is expected to be beneficial for:

1. Local Government

Provide advises to the Central Government and the Regions in terms of

future policy formulation.

2. For Researchers

8

a. Add science and insights from the information gathered, as well as add

to the experience of researchers in the field of research.

b. Increase knowledge and understanding of the influence of the Original

Local Government Revenues (PAD) and General Allocation Funds

(DAU) towards the Local Government Expenditures.

3. For The World of Education.

a. Provide input for academics to develop science in the Government

Accounting field, in particular, on the effect of Original Local

Government Revenues (PAD) and the General Allocation Funds

(DAU) to Local Government Expenditures.

b. Open the research subject to similar studies.

9

CHAPTER II

LITERATURE REVIEW

A. Theory Development

The elements contained in the Local Government Revenue and

Expenditure Budgets (APBD) are the income and the expenditures, where the

income in question is the source of acceptance for the area known by the

Original Local Government Revenues (PAD). While expenditures are equal

to the expenditures incurred by local governments in carrying out the tasks

and functions. In accordance with Act No. 32 of 2004 concerning Local

Governments, local governments have the right to set up and take care of

their own Government Affairs according to the principles of the regional

autonomy of the region, geared to accelerate the achievement of well-being

communities through improving the services, empowerment and participation

of all communities, as well as the increase the competitiveness of the area

having regard to the principles of democracy, equity, justice and the

specificities of an area in a unitary state system of the Republic of Indonesia.

In order to fulfill the rights and obligations, the Government

elaborates a plan to achieve the purpose, which is aspired to. This plan is used

as a guide in each step of the execution of the duties of the State. (Ghozali,

1997:37).

10

1. Local Government Revenue and Expenditure Budgets (APBD)

Halim (2007:19) said APBD (Local Government Revenue and

Expenditure Budgets) is the operational plan of the local government,

which, on the one hand, illustrate the estimated expenditures as high as

possible in order to finance activities and projects of the specific budget

for one year, and on the other hand, described the estimates and the

acceptance of sources in order to cover the expenditures in question.

In the pre-Reformation characteristics of regional financial

budgeting in the pre-vaccine era of reform are as follows: (Henri Edison

2009: 23).

a. Input planning system.

b. Output planning System.

c. Views of the structure, APBD consists of revenue and expenditure,

where expenditure is divided into two, namely routine expenditure

and development expenditures.

d. Process of planning systems uses line-item budget and the

incremental approach, whereas the preparation that is applied is the

input-oriented and fragmental.

e. Preparation of Documents used in DUKDA/DUPDA

f. Loans and the rest of the budget calculations more last year as the

income of the region.

g. Transfer of Funds from the Center consists of donations. subsidies,

and rewards.

11

h. The establishment of a reserve fund is not allowed.

i. Unexpected expenditures consist of miscellaneous expenditures and

are executed by the head of area’s policy.

j. The Local Government Revenue and Expenditure Budgets (APBD)

of Districts/ Cities is ratified by the Governor for the province, while

endorsed by the Ministers in the Country.

k. To change Local Government Revenue and Expenditure Budgets

(APBD), Representative Members get informed.

In the new order, APBD is the financial work plan made for a period

of time when the legislature (DPRD) gives credit to the Executive

Board (region leaders) to finance the household needs in accordance

with the draft, which became the basis of the determination of the

budget and shows all earnings to cover expenses. The definition of

both concluded that the regional budget has elements as follows:

(Halim, 2007:19).

1) An Activity plan is presented along with the supporting details

2) An acceptance minimum target is set, which is to cover the costs

related to such activity, and any costs, which are the maximum

limit of expenditures, which will be implemented.

a) The types of activities and projects implemented are listed

in the form of numbers.

b) The budget is enforced for one fiscal year

12

Budgeting for future areas of reform refers to different

characteristics of financial management areas in pre-reformation that

differences in the characteristics of budgeting in the pre-vaccine era

reform with budgeting in the era of reform are as follows:

1. Understanding of the region's provinces and districts/ cities.

2. The sense of regional government is the head of the region along

with other devices.

3. The calculation of APBD has become one of the responsibilities of

the head of the area and provides direction for APBD general policy

in line with the agreement between the Executive and the legislative.

4. Output system Differences, planning over APBD use a system of

surplus/deficit budget.

5. The structure of the APBD consists of revenues, and expenditures.

6. System planning is a performance budget, standard output

orientation of service-learning outcomes, and integrated.

7. The documentation for the preparation of the budget through RASK

(budget plans a unit of work).

8. Loans and the rest of the more budget calculation (SILPA) is a type

of financing.

9. Transfer of Funds from the Central Government consists of the

Balanced Budget (Tax share (DBH), Income Tax (PPh), Tax on

Acquisition of Land & Buildings (BPHTB), Natural Resources

13

(SDA), General Allocation Funds (DAU), and Special Allocation

Funds (DAK)).

10. Record-keeping and reporting systems using accounting systems

cash base pairing and customizations.

11. From the accountability report end of year budget consists of:

a. Report of the realization budget.

b. Balance sheet

c. Cash flow statement

d. Notes to the financial statements.

12. Come with performance research based on a benchmark strategic

plan areas.

13. The loans APBD are no longer included in the post, but revenues

have been introduced in the post of receipts.

14. The community was involved in the preparation of the APBD in

addition to the Government and Parliament.

15. An indicator of the performance of local governments includes:

a. Comparison of budget and actual

b. A comparison between standard costs with its realization.

c. Physical percentage targets and projects.

d. Accountability the head area at the end of its APBD fiscal year

calculation reports is covered by the Local Home of

Representatives (DPRD) and contains the consequences to the

head region, when legislators rejected twice.

14

In the post-war period of reform, APBD a lot of the changes are

pretty basic. The first form of APBD is based on the decision of the

Minister of Home Affairs Number 29 in 2002 about the management,

accountability and financial control area, as well as the procedures for the

preparation of the calculation of the budget revenues and local

government expenditure. In Act No. 17 of 2003 about the finances of the

State mentioned that:

1. APBD is the financial management, which is determined annually by

the regional regulation.

2. APBD consists of revenues, expenditures, and financing. Regional.

3. Revenue from PAD.

4. Local Government expenditure divided according to the

organization, function and type of expenditure.

According to the regulation of the Minister of Home Affairs No.

13 of 2006 articles 1 paragraph (9) mentioned that the APBD is the

annual budget plan for local government, which is discussed and

approved jointly by local governments and local parliament (DPRD), and

set as local regulations.

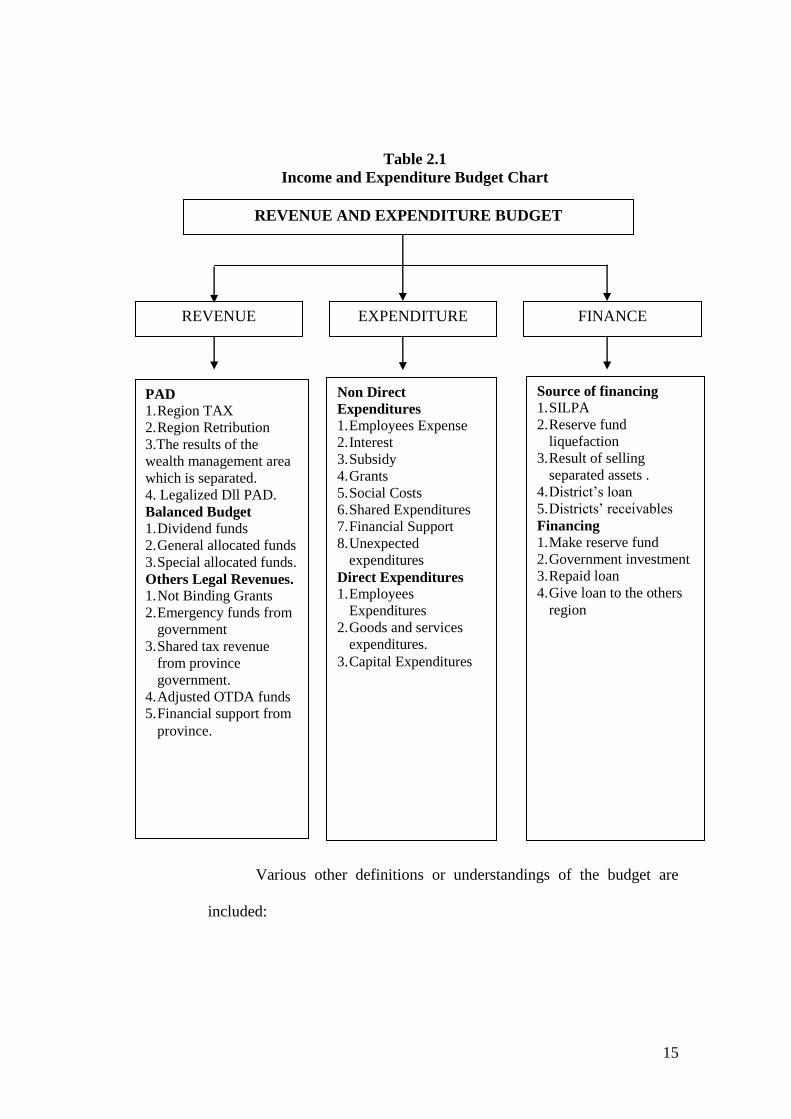

The budget income and expenditures can be presented - according

to the area of Ministry of Home Affairs No. 13 of 2006 in the image

below.

15

Table 2.1

Income and Expenditure Budget Chart

Various other definitions or understandings of the budget are

included:

PAD

1. Region TAX

2. Region Retribution

3.The results of the

wealth management area

which is separated.

4. Legalized Dll PAD.

Balanced Budget

1. Dividend funds

2. General allocated funds

3. Special allocated funds.

Others Legal Revenues.

1. Not Binding Grants

2. Emergency funds from

government

3. Shared tax revenue

from province

government.

4. Adjusted OTDA funds

5. Financial support from

province.

Non Direct

Expenditures

1. Employees Expense

2. Interest

3. Subsidy

4. Grants

5. Social Costs

6. Shared Expenditures

7. Financial Support

8. Unexpected

expenditures

Direct Expenditures

1. Employees

Expenditures

2. Goods and services

expenditures.

3. Capital Expenditures

Source of financing

1. SILPA

2. Reserve fund

liquefaction

3. Result of selling

separated assets .

4. District’s loan

5. Districts’ receivables

Financing

1. Make reserve fund

2. Government investment

3. Repaid loan

4. Give loan to the others

region

REVENUE AND EXPENDITURE BUDGET

REVENUE EXPENDITURE FINANCE

16

1. Budget describes any form of local government in look for sources

of revenue, and then how these funds are used to achieve

government objectives.

2. Budget estimates and expenditure describing areas expected to occur

within the next year based on the realization of the past.

3. Budget is a Government operational work plans to be carried out the

next year in units of numbers of dollars. This budget is a translation

monetarist of the existing regional planning documents and agreed to

be carried out during the year.

Budgeting needs to be a reference (BPKP, 2005 in Warsito, et al

2008) as follows:

1. Transparency and accountability of the budget

In order to achieve good governance, clean and respectable, budget

transparency is important, budget is one means of evaluating the

performance of government that provides information about the

goals, objectives, outcomes and community benefits of an activity or

project.

2. Budget discipline

The budget needs to be clarified clearly drafted to avoid overlap that

can lead to wastage and leakage of funds. Therefore, the budget must

be efficient, effective, timely and accountable.

17

3. Justice budget

Local government financing through taxes and retribution

mechanism imposed upon society. Therefore, they should be

allocated fairly and proportionately in order to be enjoyed by the

whole community.

4. The efficiency and effectiveness of budget

Funds collected and used for the development must be felt by most

people.

5. Compiled with the performance approach

Budgets are prepared with performance approach, which focus on

supporting the achievement of the performance results of the cost

allocation plan or the input set. This work should be equivalent or

greater than the cost or input set. In addition it must be able to foster

the professionalism of the work of any organization-related work.

2. Definition of Local Government Expenditures (BD)

The definition of expenditures by the Law 24 of 2005 is as follows:

“Expenditure is all expenditures from the account of the State / Regional

equity funds reduce smoothly in the corresponding period of the fiscal

year that will not be earned back by the government payment.”

Another definition of expenditure is as described in the

Regulation of the Minister of Home Affairs Decree. 59 of 2007 as

follows:

18

"Expenditures are the obligation of the local government which is

recognized as a deduction from net worth."

Both of these definitions make it clear that the deal will reduce

the equity fund expenditures of local governments. Both the rules, which

arrange the expenditures, classify expenditures by different

classifications. The difference is simply because there is anything else

you want covered by the Regulation of the Minister of Home Affairs

Decree. 59 of 2007. As it is defined by the Minister of Home Affairs

Decree 59 in 2007 as a local financial management guideline, which

includes the planning, budgeting, administration, accounting and

accountability. As the required budgetary instrument the information

control is indicated, which is considered the information associated with

the concept of performance-based budgeting.

Expenditures are measured and compared to the output achieved.

Direct expenditures are expenditures that are directly affected by the

program and planned activities. Government asked to focus more on

increasing expenditure (direct expenditure), either by increasing

consumer purchasing power and infrastructure development. Direct

expenditure is believed to have a more powerful multiplier effect in job

creation than just fiscal incentives enjoyed by some people only (Abdul

Halim, 2002) According to Law no.58 2005 the local government

expenditures are used in order to fund the implementation of government

affairs under the authority of the provinces or districts / cities consisting

19

of obligatory, choice affairs and the treatment affairs in certain sections

or areas that can be carried out jointly between the central government

and the local government or among local governments established by the

prevailing legislation.

Local Government expenditures are all local government

expenditures within a budget period. Revenues and expenditures consist

of three main components, namely the element of revenues, the routine

of expenditures and the expenditures’ development. The third component

is even prepared almost at same time, but the proceeding is within

different institutions. (Halim, 2002).

According to Law no 58 article 26.2005 Expenditure matters

concerning the implementation of priority referred to protect and

improving the quality of life of the community in an effort to meet local

obligations are realized in the form of increased basic services,

education, health, social facilities and public facilities and develop an

appropriate social security system.

The classification of expenditure by business shall include:

education, health, public works, housing, spatial planning, transport,

environment, land, population and civil, women's empowerment, family

planning and family welfare, social, labor, cooperative and small and

medium enterprises, investment, culture, youth and sports, national unity

and domestic politics, public administration, employment, community

development and rural, statistics, records and communications and

20

informatics. The classification of expenditures by business choices

includes: agriculture, forestry, energy and mineral resources, tourism,

marine and fisheries, trade, industry, and transmigration.

Expenditures in handling government affairs in a particular part

or midwife can be implemented jointly by the government and local

governments established by the statutory provisions set out in the form of

programs and activities that classified according to obligatory and

matters of choice.

The local government expenditures are all local government

expenditures in a budget period. (Abdul Halim, 2002). Revenues and

expenditures consist of three main components, namely the elements of

acceptance, routine and development expenditure. The three components

that though composed almost simultaneously, but the drafting process in

different institutions. The budget process as a whole is in the hands of the

Regional Secretaries responsibility for coordinating all activities of

budgeting. While the process of developing routines compiled by the

Government Finance Department, the process of preparing the reception

conducted by the Regional Revenue Service (DISPENDA) and the

preparation of development expenditures compiled by Regional Planning

Agency (Bapeda). (Pratiwi, 2007).

According to research of Pambudi (2007) expenditure can also be

categorized according to their characteristics into two parts, namely: (1)

in addition to Capital Expenditures (expenditures of public

21

administration; Expenditure of operation, maintenance of public

infrastructure; Expenditure transfers; Expenditure unexpected). (2) The

Capital expenditures. In general, expenditures in the budget are grouped

into five groups, namely:

a. General administration expenditure

Government expenditure is all that is not directly related to

the activity or public service. General administration expenditure

group consists of four types, namely:

1) Personnel expenditures are expenditures for the Local

Government/Personnel (salaries, honorarium, and overtime) that

is not directly related to the activities providing services to

citizens.

2) Expenditures for goods are local government expenditures on

goods and services not directly related to public services.

3) Expenditures for travel are expenditures on travel expenses and

council employees who are not directly related to the public

service.

4) Maintenance expenditures are expenditures for the maintenance

of the Local Government of goods that are not directly related to

the public service.

22

b. Operating Expenditures

Maintenance of public infrastructure is an all expenses

associated with the Local Government or public service activities.

Expenditure groups include:

1) Personnel expenditure (Operation and Maintenance Expenditure

Group facilities and public infrastructure) are expenditures for

the Local Government/Personal the effect directly to a specific

activity or in other words, an expenditure that is variable.

2) Goods expenditures (Group Operations and

Maintenance Expenditures infrastructure public) is local

government expenditure for the provision of goods and services

directly related to the public service.

3) Travel expenditures (Group Operations and

Maintenance Expenditures infrastructure public) are local

government expenditures for employee travel expenses directly

related to the public service.

4) Maintenance expenditures (Operation and Maintenance

Expenditure Group facilities and public infrastructure) are

government expenditures for the maintenance of assets from

current areas that have a direct impact on the public service.

23

c. Capital Expenditures

Government Capital Expenditures refer to government

spending on investment goods. This means spending on things that

last for a certain period of time. This may include investment in

hospitals, schools, equipment (furniture, IT-facilities, archive

facilities) and roads. Capital Expenditures are divided into:

1) Public expenditures, these are expenditures those benefits can be

enjoyed directly by the general public.

2) Apparatus expenditures, namely expenditures directly benefit

not enjoyed by the public, but it is felt directly by the apparatus.

d. Transfer expenditures

Transfer Expenditures are the expenditures for the transfer of

money from the government to third parties without expecting

reward or gain refunds of the money transferred. The group consists

of expenditures for:

1) Installment of loans.

2) Grants.

3) Reserve funds.

e. Unexpected Expenditures

Unexpected expenditures are the expenses incurred by local

governments to finance the activities of unexpected and

extraordinary events. According to Nurlan (2008) states that

unexpected expenditures are expenditures for activities are unusual

24

or not expected to recur like natural disasters and social disasters

unforeseen, including the refunds of excess revenues from previous

years that have been closed.

Classification of expenditures by function for alignment and

integration of financial management consists of:

1) Public Service;

2) Order and Peace;

3) The Economy;

4) The Environment;

5) Housing and Public facilities;

6) Health;

7) Tourism and culture;

8) Education, and

9) Social protects.

3. Original Local Government Revenues (PAD)

One of the main objectives of fiscal decentralization is creating

local independence. In this perspective, the governments (local

governments) are expected to be able to explore the local financial

resources, particularly through revenues (Sidik, 2002). Dependence on

transfers from central government from year to year should be more

limited. (Oates, 1999) provide a fairly rational reason why the

government should reduce this dependency:

25

a. Central government transfers are usually accompanied by certain

conditions, so it is a compromise relative autonomy, especially if the

funds transfer is the dominant source of local revenues.

b. Rely on the central government transfer actually reduces the local

creativity to take a policy associated with an efficient local revenue

collection.

Original Local Government Revenues (PAD) ideally should be

the main source of local revenue. Another source of income is relatively

volatile and tend to out of control (authority) local government (Sidik,

2002; Bappenas 2003). The data indicate that the contribution of PAD

increased from 6.59% in 2001 to 7.33% in 2002 (Central Bureau of

Statistics, 2004), the main source of revenue from local taxes and

retribution. However, the contribution of PAD is still very small while

compared to the transfer from central government (DAU and DAK),

which reached 79.14%.

The Original Local Government Revenues are accumulated from

the Tax Revenues containing Local Tax and Local Retribution, Non Tax

Revenues, which contain the profit of Regional Owned Enterprise

(BUMD), Postal Receipts Investment and Management of Natural

Resources. (Bastian, 2002).

The Regional Original Revenues (PAD) are all local revenues

derived from the original local economy. The identification of revenue

source is : investigate, determine and establish where the real source of

26

revenues by way of researching and seeking and managing revenue

sources properly so as to provide maximum results. (Elita in Pratiwi,

2007).

In the Law, no.13 from 2006 the Ministry of Home Affairs

explains the revenues will be divided according to the type of income:

a. Local Taxes

According to Law no.28 2009, the local taxes are a

mandatory contribution to the region charged to individuals or

entities, which is not getting benefits directly. The purpose of the

local taxes is seen in a better citizen’s prosperity.

Mardiasmo et al, (2002) revealed that in order to reduce the

dependence on finance from the central government, local

governments should be given autonomy and flexibility in this area.

An important step that must be done to increase local tax revenues is

to calculate the potential tax revenues that the real area owned by the

area, so they can know region’s capacities (tax capacities). The

improvement of tax capacities is essential in order to optimize the

local revenue sources.

Law No. 34 of 2000 on the amendment of Law no. 18 Year

1997 on local Taxes broken down into:

1) Province taxes consist of: Motor vehicle tax and water vehicle,

transfer tax motor vehicles (BBNKB) and vehicles on the water,

27

motor vehicle fuels Tax, and Tax collection and utilization of

underground water and surface water.

2) Type of district / city tax consists of: Hotel Taxes, Restaurant

Tax, Entertainment Tax, Advertisement Tax, Tax of street

lighting, exploitation Minerals Group C Tax, Parking Tax.

b. Local Retribution

Collection of retribution paid directly by those who enjoy the

service, and are usually intended to cover all the costs or the

ministry. Retribution according to Law no. 28 of 2009 is taxation as

a payment for certain services or special permits provided and / or

administered by the local government for Personal or Entities. The

amount of retribution should be (more or less) equal to the value of

the services provided. In the new budget structure with performance

approach, the kind of income that comes from local tax and

retribution areas under Law 34 of 2000 on the Amendment Of Law

no. 18 Year 1997, Retribution broken down into:

Retribution is broken down into:

1) General Retribution

That is, a levy on services provided or provided by local

governments for general interest and can be enjoyed by private

persons or entities.

28

2) Business Retribution

i.e.: fees for services provided by the government to adhere to

commercial principles because basically provided by the private

sector.

c. Income of Local Government Corporate Management of

Regional Government Separated Wealth

As per Law no. 34 of 2004, the kind of results that separated

the area of wealth management can be broken down by revenue

object that covers the return on capital investment in locally-owned

companies / enterprises. Part return on capital investment in state-

owned enterprises / state and the return on equity investment in

privately-owned company or a group of business people.

1) Regional Company

In an effort to explore the sources of revenue can be done in

various ways, as long as not contrary to the Laws and

regulations. One source of revenue is very important and needs

special attention is the company area.

2) The company is a unit of production area that is:

(a) Providing services

(b) Conducting general use

(c) Cultivate revenue

3) The regional company's goal to participate in implementing

regional development, in particular, and the development needs

29

of the people with industrialization and peace and tranquility of

working towards a just and prosperous society.

4) Regional company engaged in the field according to household

affairs under the Laws governing local government subjects.

5) Branches of production which are important for the region and

to lord lives of many people in the area, the capital is entirely

separated regional assets.

d. Other Legal Revenues

Other types of PAD (Revenue) are constituted under Act No.

33 of 2004. Other legal revenues are revenues gained from outside

taxes, retribution, and income, which have been described above.

Other legal revenues include:

1) The sale of regional assets that are not separated by cash or

installment / mortgage, current account.

2) Interest income.

3) Receipt of compensation claims area.

4) Receipt of commissions.

5) Discounts or other forms achieved as a result of sales or

procurement of goods and services by a region.

6) Revenue gains from the differences in the exchange rate against

foreign currencies.

30

4. General Allocation Funds (DAU)

According to the Law No.33 2004, the General Allocation Funds

are sourced from the State Revenues and Expenditure Budget (APBN) to

be allocated for local government in balancing the financial capacities

among regions and to fulfill local government needs in terms of

decentralization.

The source of regional revenues in the context of autonomy and

decentralization are dominated by aid and transfer from the central

government in form of the General Allocation Funds (DAU), Special

Allocation Funds (DAK), and Tax shares (DBH), whereas the amount of

PAD is still relatively small (Mardiasmo, 2002).

Referring to Law 104, 2000 that the prime DAU objective is

horizontal equity and sufficiency. The objective of horizontal equity is in

the central government’s interest in order to distribute the income in a

fair and equitable way to avoid wide disparities among regions.

Meanwhile, the regional interest adequacy (sufficiency) is to close the

fiscal gap. The sufficiency is influenced by several factors, namely

Authority, Capacity, and Minimum Service Standards (MSS)

(Mardiasmo, 2002).

According to Halim (2009), economic disparities among the

provinces cannot be avoided by fiscal decentralization due to the lack of

tax sources and fewer natural resources, which can be explored by the

Regional Government. In order to tackle inequality, the Central

31

Government provides subsidies in the form of DAU to the local

government. For local government with a low level of Original Local

Government Revenues (PAD), the DAU is larger than for those with

sufficient income from local sources. In addition to reduce the disparities

in financial capacity among regions, the General Allocation Funds of

26% taken the national revenue. General Allocation Funds will provide

certainty for regions in obtaining financial means to cover the

expenditures.

General Allocation Funds (DAU) are funds coming from the state

budget (APBN) allocated to equal financial capacities among regions to

finance the Local Government Expenditures. The DAU provisions are as

follows (Halim, 2007):

a. General Allocation Funds (DAU) cover 26% at a minimum level of

the domestic revenues in the state budget.

b. General Allocation Funds (DAU) are set as 10% for the provinces

and 90% for districts / cities of the General Allocation funds as

defined above.

c. General Allocation Funds (DAU) for specific districts / cities are

determined by multiplying the number of general allocation funds

for districts / cities set by the state budget with a portion of

concerned districts / cities.

In Act, No.32/2004 mentions that for the implementation of the

local government authority, the central government will transfer the

32

Balanced Budget consisting of the General Allocation Funds (DAU),

Special Allocation Funds (DAK), and Tax Share (DBH) consisting of

taxes and income from natural resources. Besides the Balanced Budget

(DAU, DAK.etc), Local Governments have their own sources of funding

in the form of Original Local Government Revenues (PAD) and Local

Government Financing.

According to the Law No.33, 2004 about Central Balanced

Budget and local government stated that DAU in a Region (Provincial,

District and City) is determined by using a fiscal gap approach, which is

indicated by local needs and the potential of a region (Natural and

Human Resources). The General Allocation Funds (DAU) are used to

cover the fiscal gap. Fiscal gap happened when the Local Government

Expenditures exceed the Original Local Government Revenues (PAD).

B. Previous Research

Researchers had previously analyzed the effects of PAD, DAU and

local government expenditures in Java, Bali and Sumatra. The analysis of the

Sumatra case study shows that the PAD did not significantly affect the

local government expenditures. That means Flypaper Effect occurred. This

along with the hypothesis demonstrates that the influence of DAU on local

government expenditures is greater than the influence of PAD on

local government expenditures is accepted.

33

Previous researchers such as Abdullah & Halim (2004) stated DAU

and PAD had a significant effect on local government expenditure budget.

Maemunah (2006) analyzed the effect of General Allocation Funds (DAU)

and Original Local Government Revenues (PAD) on local government

expenditures on Sumatra with the objective to show:

1. The influence of General Allocation Funds (DAU) and regional original

revenues (PAD) to government expenditures districts / cities in Sumatra.

2. The possible Flypaper Effect on districts / cities expenditures on the

island of Sumatra.

3. The tendency of Flypaper Effect which led to an increasing number of

local government expenditures.

Another study conducted by Nur Indah Rahmawati (2010) who

investigated the districts / cities in Central Java province and concluded that

the PAD positively affects the allocation of expenditure budget. Local

Governments with high revenues show higher local government expenditure

allocations. If the General Allocation Fund (DAU) is higher, automatically

Local Government Expenditure (BD) higher too . It cannot be concluded

whether Flypaper Effect has occurred or not.

The research conducted by Puspita Sari (2009) tested the effect of the

DAU and PAD against direct expenditures in districts / cities in the Riau

Province. There are three conclusions:

34

1. The DAU has a positive and significant effect on direct expenditures.

2. The PAD has partially positive and significant effects on direct

expenditures.

3. The DAU and the PAD have simultaneously significant effects on direct

expenditures.

Table 2.2

Previous Research Table

No. Author (Year) Thesis Title Variables Conclusions

1 Syukriy

Abdullah &

Abdul Halim

(2004)

Effect of General

Allocation Funds

(DAU) and Original

Local Government

Revenues (PAD) On

Local government

expenditure Budget.

Case Study Districts

/ Cities on Java and

Bali island

1. General

Allocation Funds

(DAU)

2. Original Local

Government

Revenues (PAD)

3. Local

government

expenditure

Budget

Original Local

Government

Revenues (PAD)

and General

Allocation Funds

(DAU) have

significant

influence on the

local government

expenditure

budgets.

2 Mutiara

Maimunah

(2006)

Flypaper Effect on

General Allocation

Funds (DAU) and

Original Local

Government

Revenues (PAD) to

local government

expenditure budget

case study Sumatra

island

1. General

Allocation

Funds (DAU)

2. Original Local

Government

Revenues

(PAD)

3. Local

government

expenditure

Budget

Flypaper Effect

can used for

predicting Local

Government

Expenditures in

the future.There

are no differences

in the occurrence

of Flypaper Effect

on PAD.

3 Nur Indah

Rahmawati

(2010)

The Effect of

General Allocation

Funds (DAU) and

Original Local

Government

Revenues (PAD) On

Local government

expenditure Budget

1. General

Allocation Funds

(DAU)

2. Original Local

Government

Revenues (PAD)

3. Local

government

expenditure

Budget

Original Local

Government

Revenues (PAD)

and General

Allocation Fund

(DAU) have

significant

influence on local

government

expenditure

budgets

35

Table 2.2

Previous Research Table (Continued)

4 Puspita Sari

(2009)

Effect of General

Allocation Funds

(DAU) and Original

Local Government

Revenues (PAD) On

Local government

expenditure Budget

1. General

Allocation Funds

(DAU)

2. Original Local

Government

Revenues (PAD)

3. Local

government

expenditure

Budget

1. The DAU has a

positive and

significant effect

on direct

expenditures.

2. PAD has

partially a

positive and

significant effect

on direct

expenditures.

3. DAU and PAD

simultaneously

have a significant

effect on direct

expenditures

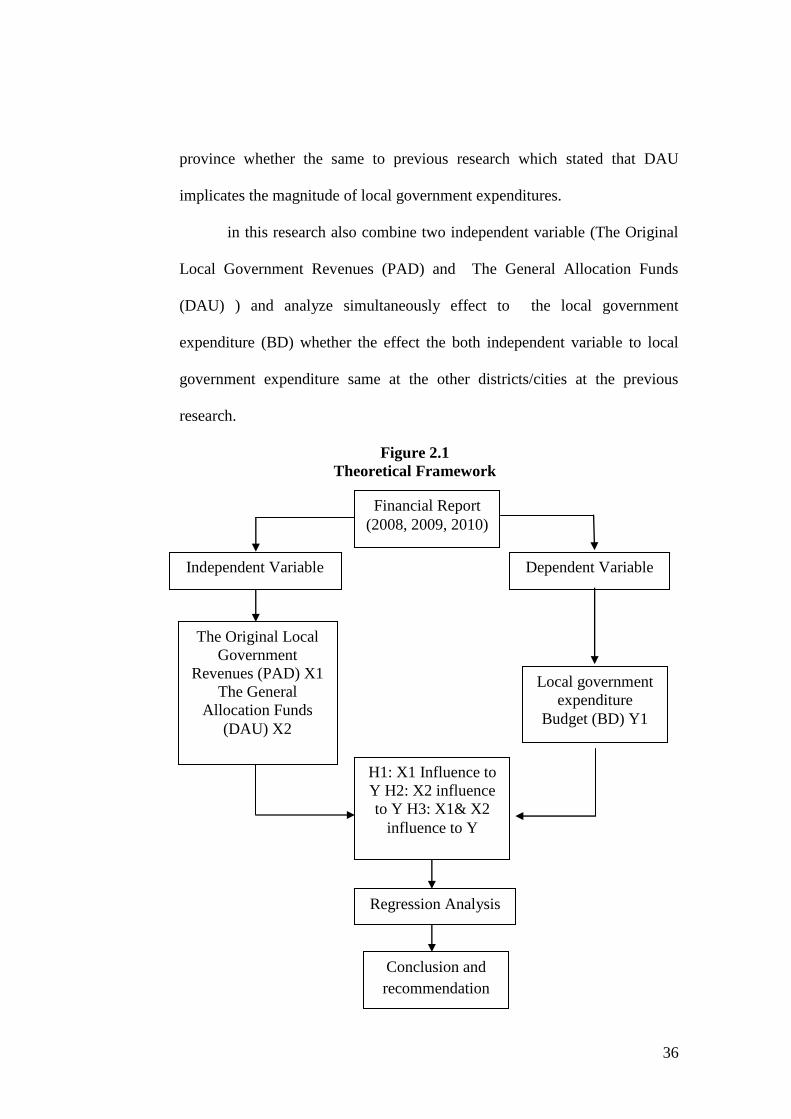

C. Theoritical Framework

The Original Local Government Revenues (PAD) is local revenues

consisting of the local taxes, Retribution, earnings from Regional Owned

Enterprises (BUMD) and other legitimate incomes. In this research try to

analyze the effect of The Original Local Government Revenues (PAD) to

local government expenditure (BD) in lampung province, whether the same

to the results of previous studies which can conclude that the larger PAD

increases the local government expenditure activities.

The General Allocation Funds (DAU) is the funding coming from the

state budget (APBN) allocated for the purpose of inter-regional fiscal

capacity equalization to finance the Expenditures in the context of

decentralization. In this research try to analyze the effect of The General

Allocation Funds (DAU) to local government expenditure (BD) in lampung

36

province whether the same to previous research which stated that DAU

implicates the magnitude of local government expenditures.

in this research also combine two independent variable (The Original

Local Government Revenues (PAD) and The General Allocation Funds

(DAU) ) and analyze simultaneously effect to the local government

expenditure (BD) whether the effect the both independent variable to local

government expenditure same at the other districts/cities at the previous

research.

Figure 2.1

Theoretical Framework

Financial Report

(2008, 2009, 2010)

The Original Local

Government

Revenues (PAD) X1

The General

Allocation Funds

(DAU) X2

Local government

expenditure

Budget (BD) Y1

Dependent Variable

H1: X1 Influence to

Y H2: X2 influence

to Y H3: X1& X2

influence to Y

Regression Analysis

Conclusion and

recommendation

Independent Variable

37

D. Research Hypothesis

Based on the theoretical framework above, can be formulated these

alternative hypotheses.

Ha1 : Original Local Government Revenues (PAD) no significantly

effecting Local Government Expenditures.

Ha2 : General Allocation Funds (DAU) significantly effecting Local

Government Expenditures

Ha3 : Original Local Government Revenues (PAD), the General

Allocation Funds (DAU), and simultaneously implies significant

impact on Local Government Expenditures.

38

CHAPTER III

RESEARCH METHODOLOGY

A. Scope of Research

Type of this research is association causality aimed to analyze the

relationship between variables to another variable (Sekaran, 2003: 30). In this

research, there are independent variables / variables that influence and

dependent variable / variable influenced. This research is conducted to

determine and prove the influence Original Local Government Revenue

(PAD), and the General Allocation Fund (DAU) as independent variables to

Local Government Expenditure (BD) as the dependent variable.

B. Sampling Method

The population is a collection of all possible people, objects, or the

size of the interest of the case to the attention (Sekaran, 2003: 31). The

population used in this research is the government of districts / cities in the

province of Lampung, amounting to 10 districts / cities in the year 2008 to

2010 for reasons of data availability.

The sample is a portion or part of a particular population of concern

(Mason and Douglas, 1996). This research is using purposive sampling

method, that is aimed by the researcher are likely to obtain information from

specific target groups, the sampling here is confined to specific types of

people/sample which can provide the desired information, either because they

39

are the only ones which have it, or conform to some criteria set by the

researcher.

Among the number of districts / cities submitting the realization,

APBD Report between 2008 and 2010 to the mentioned site are as many as

10 districts / cities in the Lampung Province. The 30 research data amounts

to, which is derived by the formula:

N= amount of districts / cities X research period

N= 10 X 3 years

N= 30

C. Data Collection Method

The secondary data collection method refers to the data collection

through recording and iterating data relating to the research objective. This

study uses the purposive sampling method by taking the sample of as many as

10 districts / cities in the Lampung Province from 2008 to 2010.

D. Data Analyze Method

The dependent variable in this study refers to the Local Government

Expenditures, while the independent variables refer to the DAU and the PAD.

The analytical tools used are the simple regression (simple regression) in

order to see the effect on each variable, on the separate expenditures and the

multiple regression (multiple regression) in order to see the effect on all these

40

variables simultaneously. Tests carried out by using the computer application

program SPSS 20.0 for Windows.

1. Classical Assumptions

a. Normality Test

Normality test is intended to determine whether the used data

is normally distributed or not. Normality test needs to be done to

determine the statistical tools, so that the conclusions drawn can be

accounted for. There are two ways to detect whether the residuals are

normally distributed or not, namely:

1) Graph Analysis

One of the easiest ways to see the normality of the

residuals is to see a histogram graph comparing the

observational data with the distribution which closes to normal

distribution. More reliable method is by looking the normal

probability plots comparing to the cumulative distribution of a

normal distribution. Normal distribution will form a straight

diagonal line and plot the data will be compared with the

residual diagonal lines. If the residual data distribution is

normal, then the line that describes the real data would follow

the diagonal line.

2) Statistical Analysis

Simple statistical test can be done by looking at the value

of the kurtosis and Z-values of skewness. Another statistical test

41

that can be used to test the normality of residuals is non-

parametric statistical test of Kolmogorov-Smirnov (KS), if the

significance level> 0.05, then the data is normally distributed

and can be performed multiple regression models. Guidelines

for decision-making about the data close to or a normal

distribution by Kolmogorov Smirnov can be seen from:

a) Sig. or significantly or probability <0.05, then the data

distribution is not normal.

b) Sig. Or significantly or probability> 0.05, then the data

distribution is normal.

b. Multicollinearity Test

Multicollinearity test means between the independent

variables included in the regression model has a linear relationship is

perfect or near-perfect (or even a high correlation coefficient of 1).

The Regression model should appear as neither perfect nor near-

perfect correlation between the independent variables. The

consequence is the correlation coefficient multicollinearity particular

variable, and the error becomes very large or infinite.

Multicollinearity can also be seen from (1) the value of

tolerance and the opponent (2) variation inflation factor (VIF). Cut-

off value commonly used to indicate the presence of

multicollinearity is tolerance value <0.10 or equal to the value of

VIF> 10

42

c. Autocorrelation Test

Test the possibility of autocorrelation aims to determine

whether the error bullies at certain periods correlated with the error

bullies at other periods. Autocorrelation in the concept of linear

regression mean error component correlated in order of time (the

time-series data) or the sequence space (on cross-sectional data). In

this study, the test follows the autocorrelation, with the Durbin-

Watson test statistics.

Table 3.1

Classification value of D

Value of D Information

0 < d < dL There is the autocorrelation

dL < d < dU non-conclusion

4 - dL < d < 4 non-autocorrelation

4 - dL < d < 4 - dU There is the autocorrelation

dU < d < 4 < dU non-conclusion

d. Heteroscedasticity Test

Heteroscedasticity means there is a variant that is not the

same for different independent variables. It can be detected by

observing how the points on the scatterplot between the estimated

values of Y with residual value (the difference between the actual

dependent variable predictive values) versus the value of the

prediction spread or not to form a pattern. If the graph has a

standardized residual axis of the X and Y axis that has been

predicted not to form a clear pattern (wavy, widened, then

43

narrowed), as well as scattered both above and below the 0 on the Y

axis Heteroscedasticity it did not happen.

Some ways to detect the presence or absence of

heteroscedasticity:

1) If there is a specific pattern, such that there are points that form

a regular pattern (wavy, widened and then narrowed), it has

been indicated heteroscedasticity.

2) If there is no clear pattern, and the points spread above and

below the 0 on the Y axis, then it does not happen

heteroscedasticity.

2. Hypothesis Testing

The analysis tools are the simple and the multiple regression.

Both are used in order to see the effects of income on government

expenditures. Simple regression is used to see the influence of each

variable to the prediction of expenditures separately, whereas multiple

regression is used to see the influence of all these variables

simultaneously.

a. Multiple Regression

To test the hypothesis (Ha), the method of analysis used is