Embed Size (px)

Citation preview

The Influence of Formal and Informal Controls on Employee

Performance: Three Essays

Ruidi Shang

Department of Accounting

The University of Melbourne

ORCID identifier: 0000-0002-6671-0764

Doctor of Philosophy

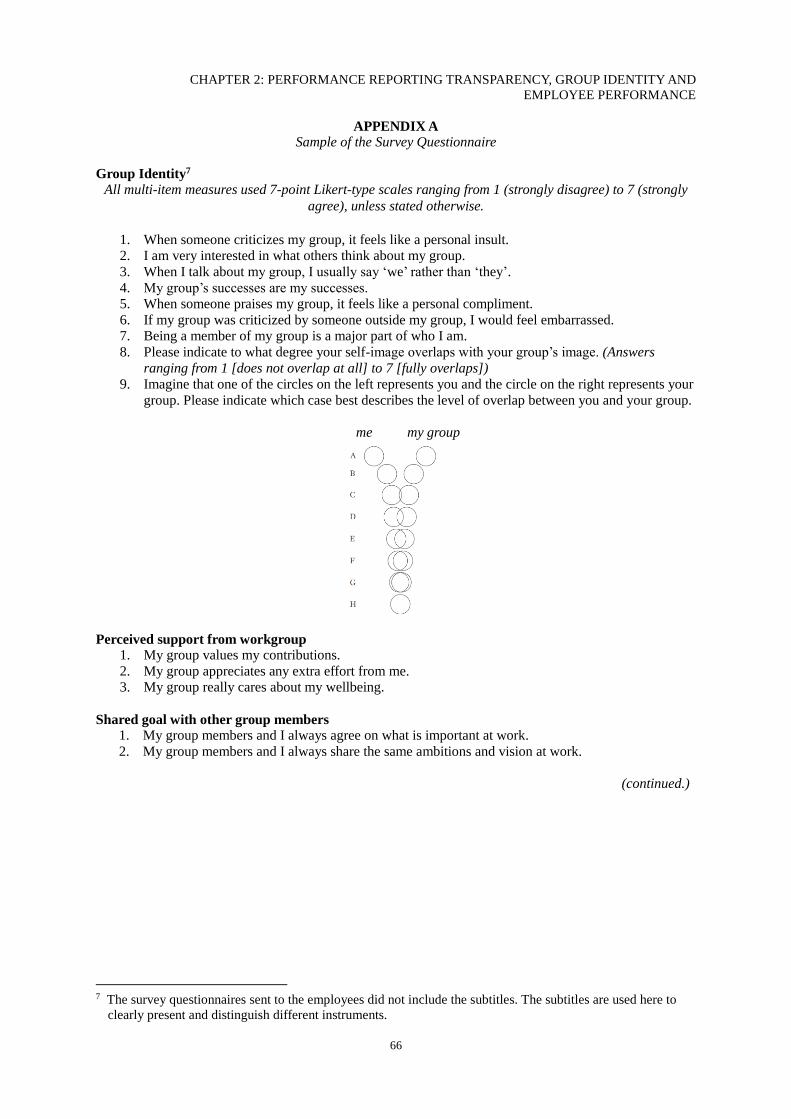

July 2017

Submitted in total fulfilment of the requirements of the degree of Doctor of

Philosophy

Produced on archival quality paper

ii

DECLARATION

This is to certify that:

(1) This thesis compromises only my original work;

(2) Due acknowledgment has been made to in the text to all other material used;

(3) This thesis is less than 100,000 words in length, exclusive of tables, figures,

bibliographic references and appendices.

Ruidi Shang

03 July 2017

iii

ACKNOWLEDGEMENTS

The past four years have been a wonderful journey for me. I could explore the area that I am

interested in, build up my ability and skills in doing research, and share ideas with wonderful

people from all over the world. None of these could happen without the support from my

supervisors, colleagues, friends, and family. I am glad to express my deep and sincere gratitude

to them.

First and most, I would like to thank my supervisor, Prof. Maggie Abernethy, for her enormous

help, great guidance, and critical evaluation of my work throughout the last four years. When I

joined the Ph.D. program in 2013, I was inexperienced, depressed, and not sure about what I

should do in the future. Maggie found me and kindly offered to be my supervisor. In the past

four years, she helped me find myself and grow up into a mature, responsible person and an

enthusiastic accounting researcher. I cannot remember how many times she read my thesis and

how many comments she has given me (all of which are fast and constructive)! Her kind and

sharp feedback not only helped me develop this thesis but also helped me find my interests in

management accounting research. I really appreciate the effort that she put into my thesis and

the Ph.D. program, and I really enjoy working with her. Maggie is the best role model that I

can even imagine. She works so efficiently and effectively, which changed my view about

lifestyle and helped me become an efficient worker. As an academic, she cares for people in

both academia and practice. Her attitude and vision amazed me and changed the way that I

think of my responsibility in the society. She has demonstrated what is an academic, a mentor,

and a real woman. I have learned a lot from her, and I will keep learning.

I would also like to thank Dr. Chung-Yu Hung, who has been my co-supervisor since 2015.

Chung-Yu gave me wonderful comments and suggestions in the last two years. When I was

frustrated about the framework of my thesis, Chung-Yu gave me enormous help so that I can

eventually develop the three papers in this thesis. Chung-Yu had numerous chats with me and

I really appreciate her effort, patience, and advice. I am thankful for having her as my co-

supervisor. I will remember all the fun we had together and look forward to having more in the

future!

I was fortunate to be part of the Department of Accounting at the University of Melbourne. It

is a wonderful department and I received tremendous support from its faculty members and

Ph.D. students. I would like to give my special thanks to Prof. Greg Clinch, who recruited me

into the Ph.D. program and opened the gate of a wonderful world for me. I give my sincere

thanks to Prof. Naomi Soderstrom and Prof. Anne Lillis, who gave me constant support,

extremely useful feedback, and wise advice in the last four years and in the job market. I thank

Prof. Floral Kuang and Bo Qin for their useful feedback and kind encouragement. I also

appreciate that they shared their life experiences in the Netherlands with me, which prepared

me for the next journey! I thank Dr. Gladys Lee for all the thoughts and experiences she shared

with me, and all the good time we spent together. I also thank Prof. Michael Davern, Prof.

iv

Jennifer Grafton, and Dr. Stephan Schantl for their support and feedback. I also thank the Ph.D.

fellows in the department. They provide me with constant help and make the last four years

more tasteful. I thank the Department for funding me and supporting me in attending various

conferences.

I am highly indebted to the faculty members in Harvard Business School (HBS) for their

support and feedback. They made my visit in HBS enjoyable, fruitful, and memorable. I

especially thank Prof. Dennis Campbell, who not only helped me improve my paper and

prepared me for the job market but also shared many inspiring ideas (and the best coffee in

Boston) with me. I truly appreciate his effort and the wonderful time we spent together. I would

like to thank Wei Cai (now a Ph.D. student at HBS). Without her, I would not be able to

overcome the pressure on the job market. We spent so much wonderful time working and eating

together. I also thank Carolyn, Jee Eun, Jihwon, Paul, and the other PhD fellows for their help

and feedback. I thank Ms. Ellen Willemin for helping arrange my visit.

I was fortunate enough to receive tremendous help from academics around the world. I would

like to thank the participants in the 2016 EAA Doctoral Symposium and the 2017 GMARS

conference, as well as the faculty members at Tilburg University, the University of Amsterdam,

and the University of New South Wales, for their kind and constructive comments on my papers.

I give my special thanks to Prof. Shannon Anderson, for her comments on my paper and her

wonderful classes. My sincere thanks also go to Prof. Michael Williamson, who has been

helping me since 2014. Michael gave me wonderful life and career suggestions, as well as sharp

and detailed feedback on my job market paper. I give great thanks to Prof. Stephan Hollander,

for his critical feedback, the opportunities he kindly offered me, and all the generous help I

received from him. I thank Prof. Eddy Cardinaels for his sharp and thorough comments. I also

thank Prof. Laurance ven Lent, Shane Dikolli, Eva Labro, Karen Sedatole, Jeroen Suijs, Jan

Bowens, Victor Maas, Henri Dekker, Frank Moers, and Gavin Cassar, for their help and

feedback. I also thank my colleagues and friends Lu Yang, Nan Jiang, Wenjiao Cao, Yusiyu

Wang, and Ties de Kok for their support and all the fun we had together.

Finally, I would like to thank my parents for their life-long support. I thank my father for his

unconditional love and support. My deepest thanks go to my mother, an incredible woman who

came from a small village but used all her effort and recourses to help her daughter explore the

big world. Without her vision, support, and hard work in the last 26 years, I would not be able

to have so many wonderful experiences. I hope this thesis makes her proud.

v

TABLE OF CONTENTS

Chapter 1 Thesis Outline…………………………………………………………………… 1

1.1 Overview……………………………………………………………………... 1

1.2 Outline of the Three Essays........…………………………………………...... 3

1.3 Conclusion...…………………………………………………………………. 6

Chapter 2 Performance Reporting Transparency, Group Identity, and Employee

Performance………………………………………………………………….... 10

2.1 Introduction...…………………………………………………………………. 11

2.2 Literature and Hypothesis Development…………………………………….... 16

2.3 Research Site…………………………………………………………….…..... 22

2.4 Method…………………………………….………………………………...... 27

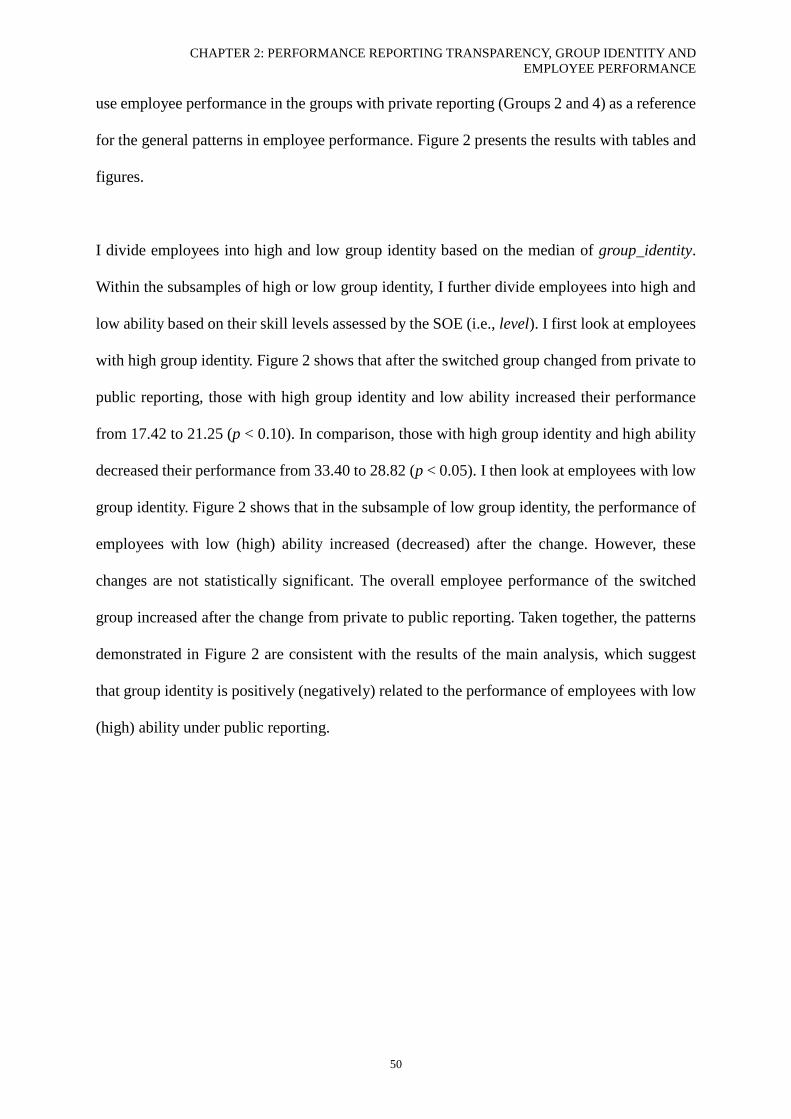

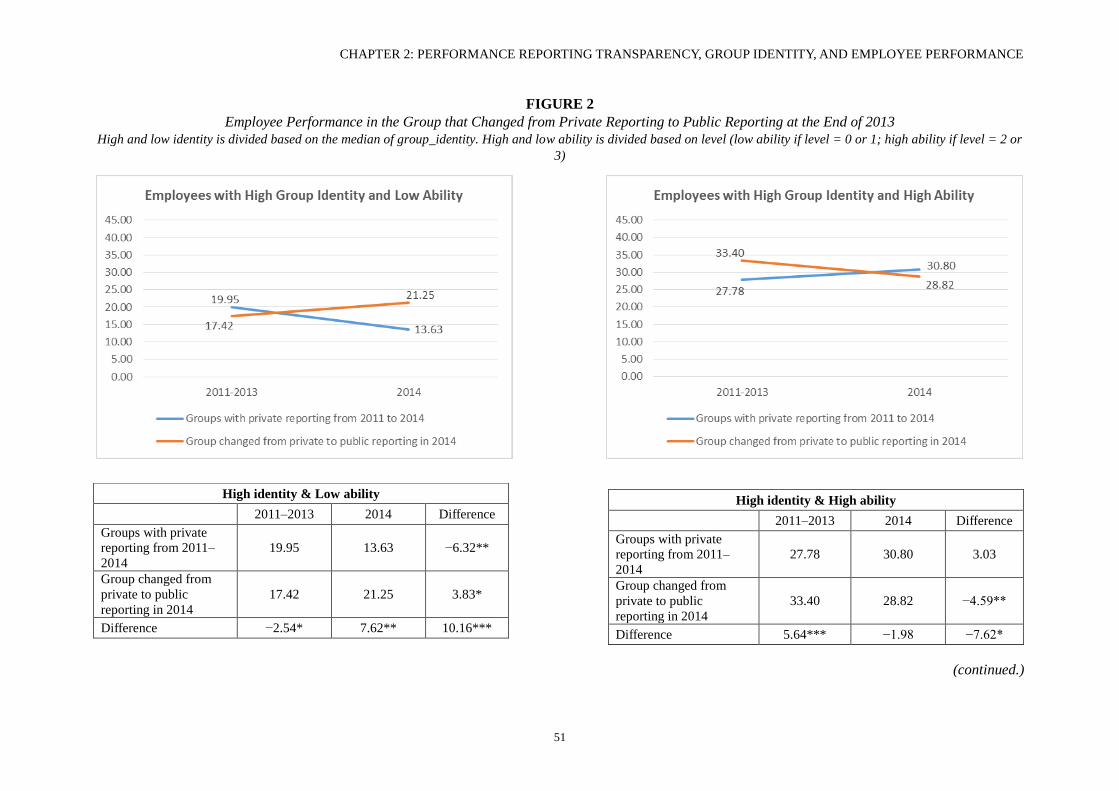

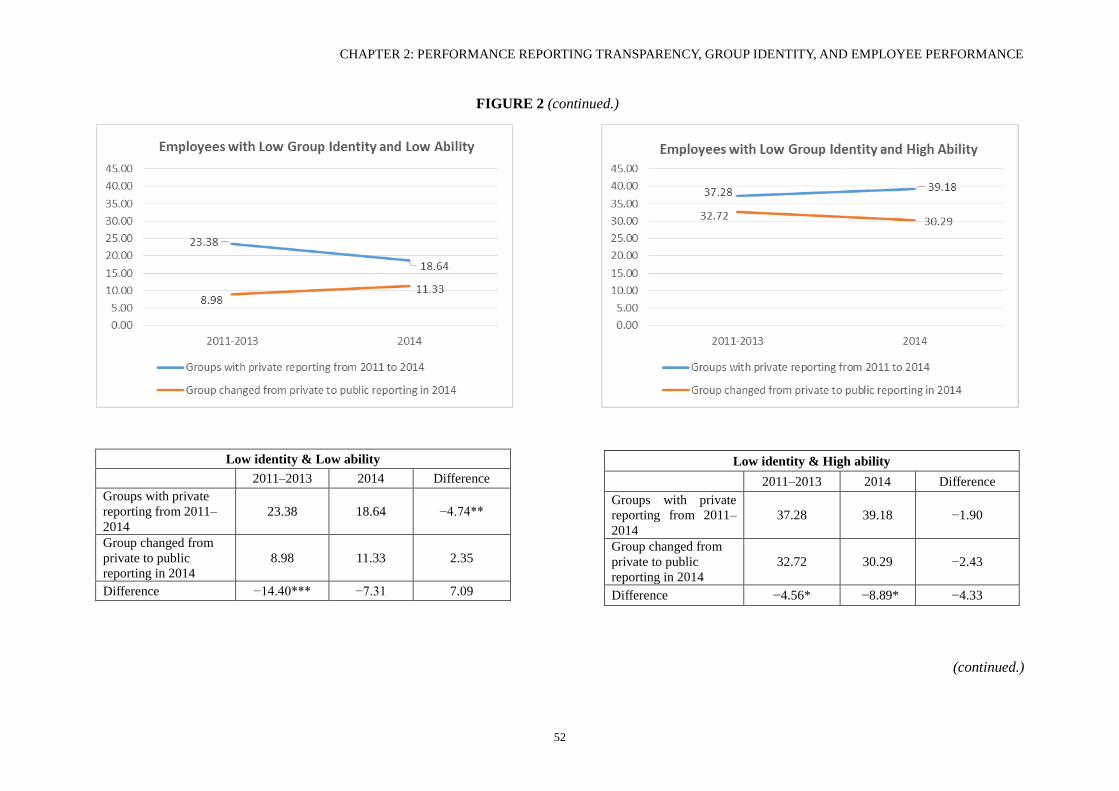

2.5 Results…………………………………..…………………………………….. 34

2.6 Concluding Remarks………………………………………………………….. 57

Chapter 3 Work Norms as a Control Mechanism: Implications for Employee

Performance…………………………………………………………………...… 67

3.1 Introduction...…………………………………………………………………. 68

3.2 Literature and Hypothesis Development…………………………………….... 72

3.3 Research Site…………………………………………………………….…..... 77

3.4 Method…………………………………….………………………………...... 80

3.5 Results…………………………………..…………………………………….. 89

3.6 Concluding Remarks………………………………………………………… 102

vi

Chapter 4 Internal Reporting, Personal Connections, and Employee Performance… 110

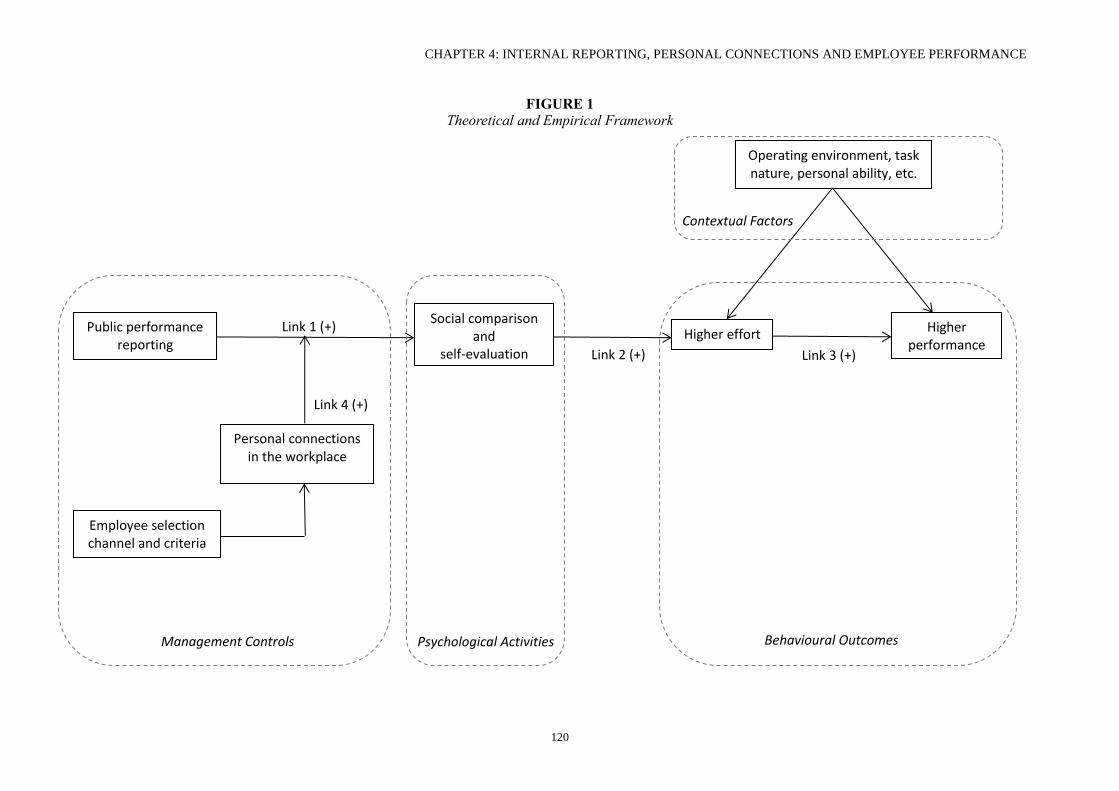

4.1 Introduction...……………………………………………………………….. 111

4.2 Literature and Hypothesis Development…………………………………….. 114

4.3 Research Site…………………………………………………………….…... 121

4.4 Method…………………………………….……………………………….... 127

4.5 Results…………………………………..…………………………………… 137

4.6 Concluding Remarks………………………………………………………… 149

Chapter 5 Conclusion…………………………………………………………………….. 156

5.1 Summary……………………………………………………………………. 156

5.2 Contributions……………….…………………………………..…………… 156

5.3 Limitations and Future Research…………………………………….……… 157

vii

LIST OF FIGURES

Chapter 2 Performance Reporting Transparency, Group Identity, and Employee

Performance

Figure 1 Performance Reporting at the Research Site ...……...…………………. 26

Figure 2 Employee Performance in the Group that Changed from Private Reporting

to Public Reporting at the End of 2013……………………………….... 50

Chapter 3 Work Norms as a Control Mechanism: Implications for Employee

Performance

Figure 1 Motivation and Research Question……………………………………… 76

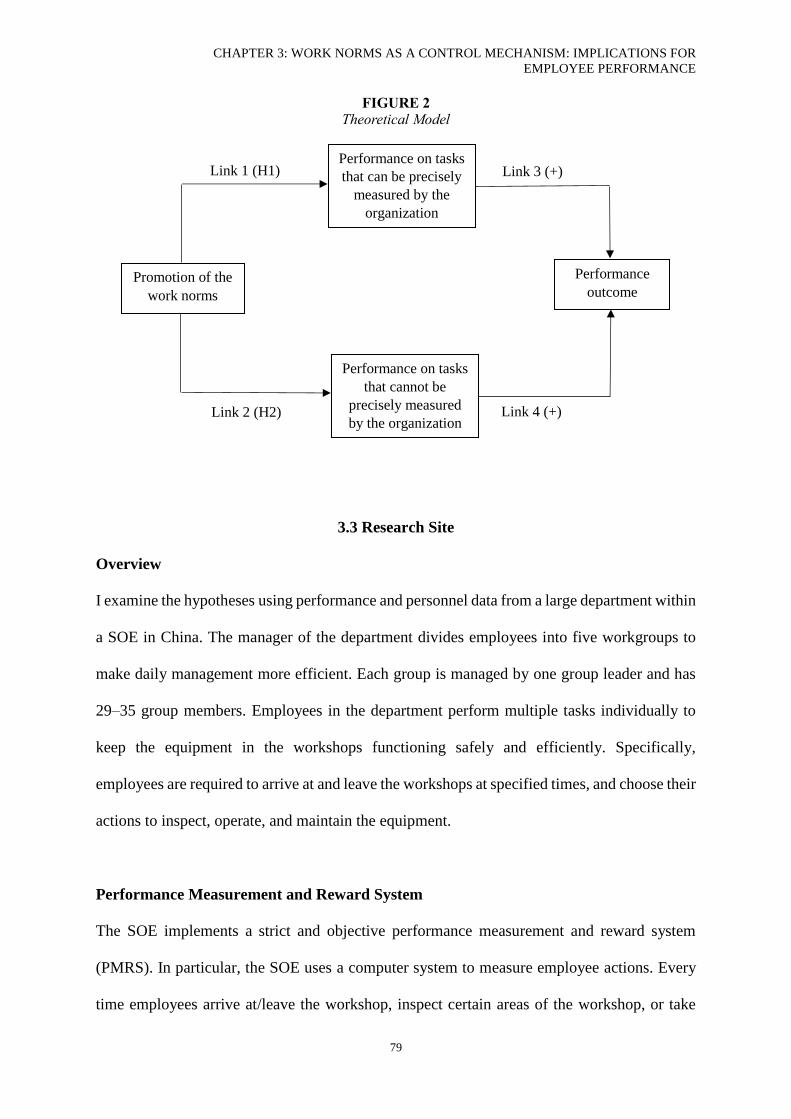

Figure 2 Theoretical Model……………….…………………………………….... 77

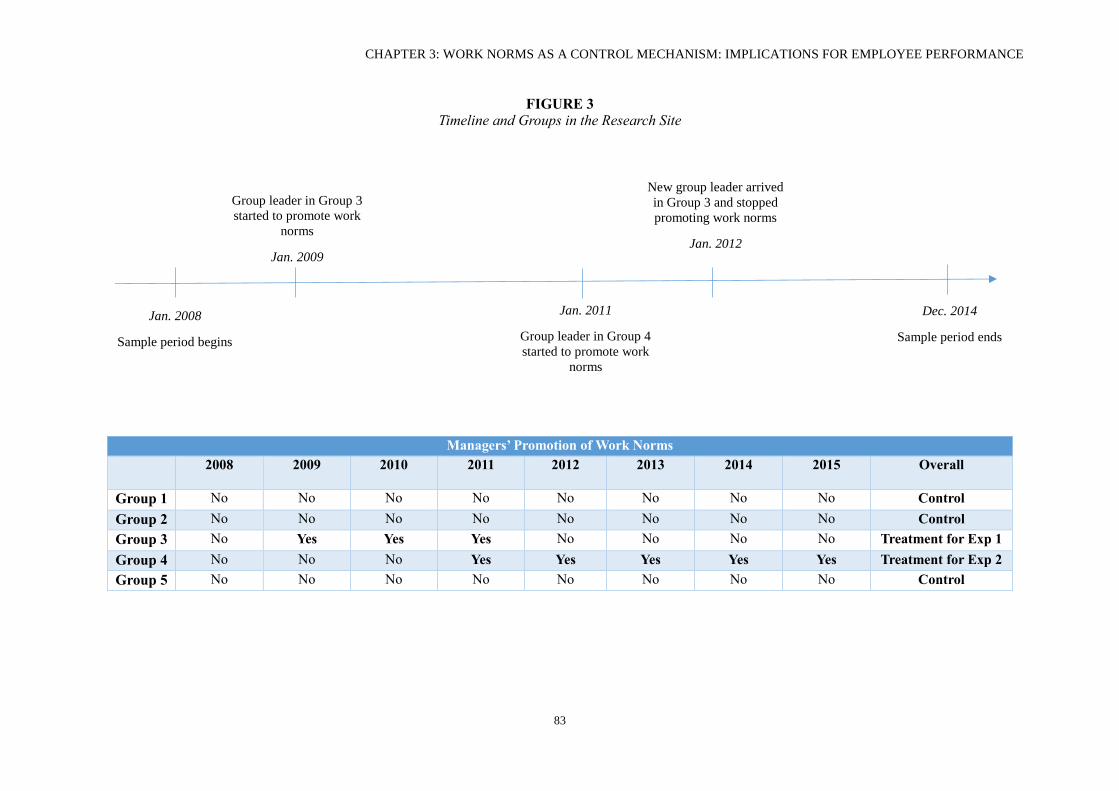

Figure 3 Timeline and Groups in the Research Site.………………….……........... 81

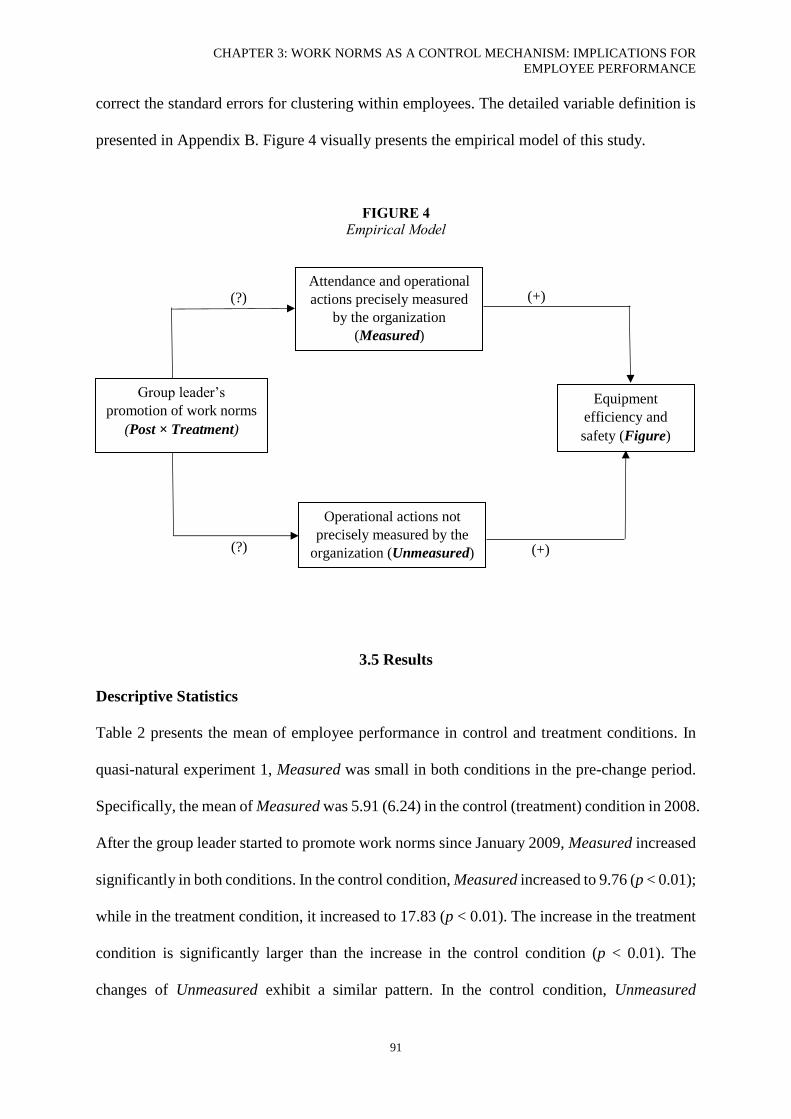

Figure 4 Empirical Model……………….………………………………...…….... 89

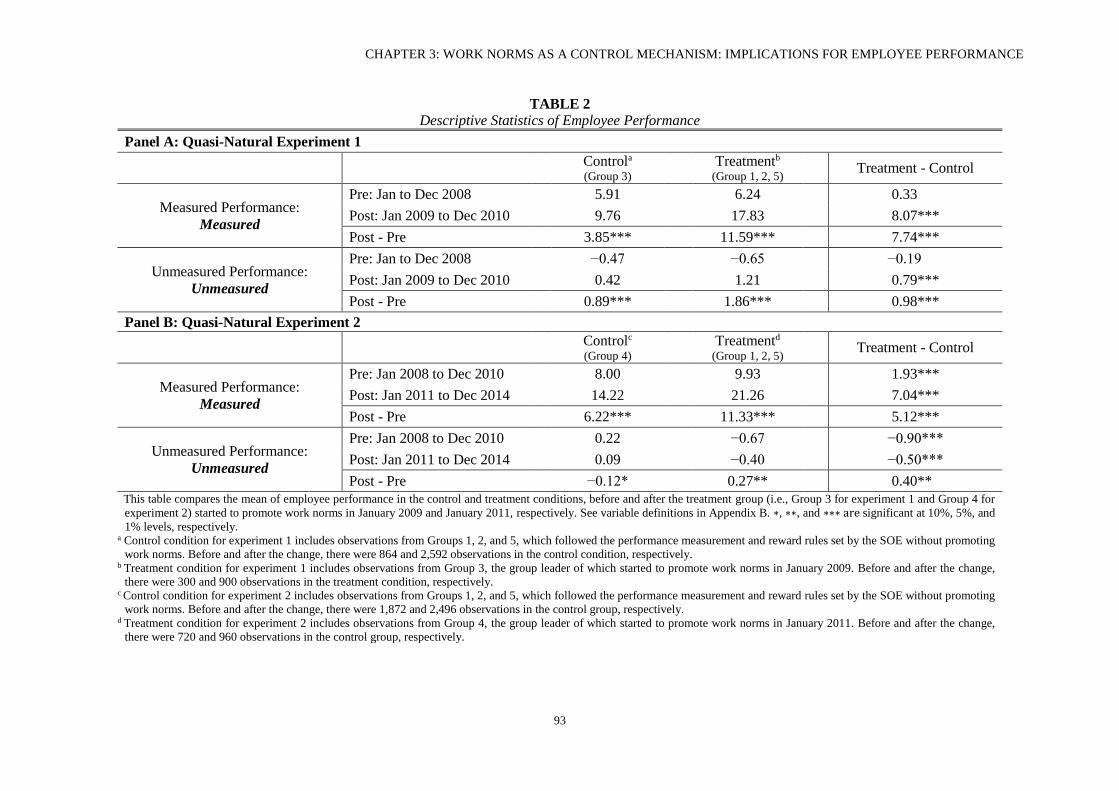

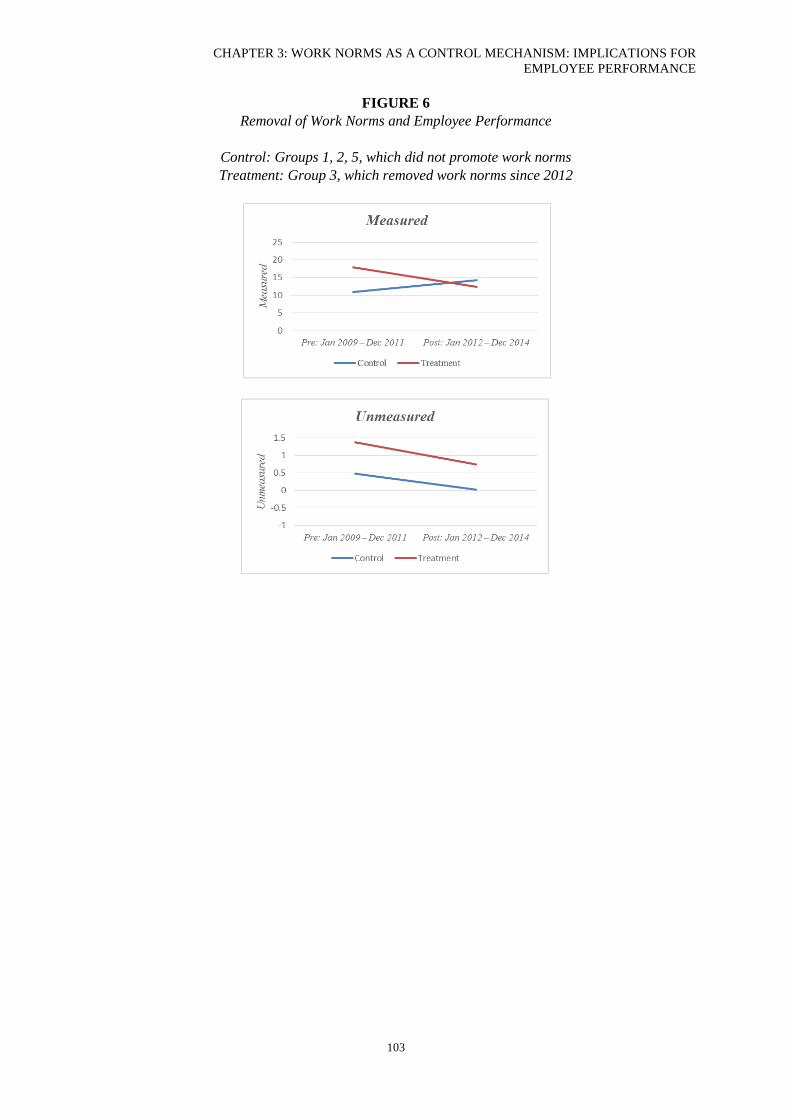

Figure 5 Promotion of Work Norms and Employee Performance …...………….. 92

Figure 6 Removal of Work Norms and Employee Performance………………… 101

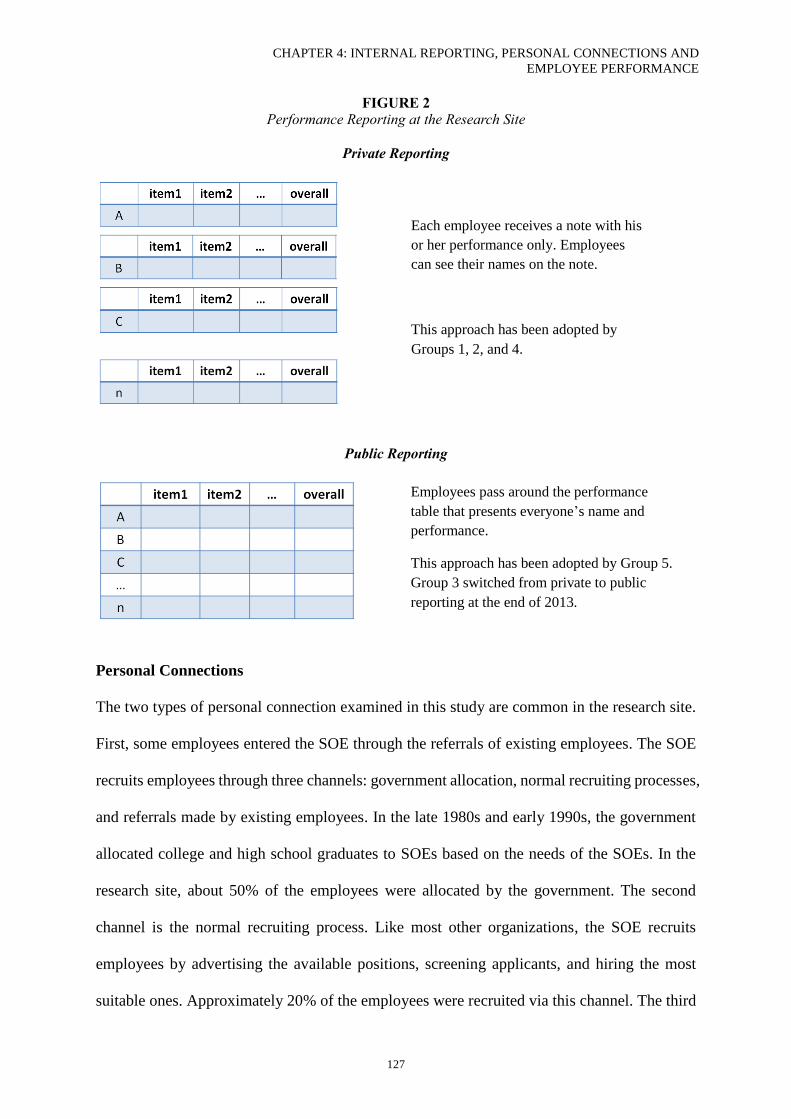

Chapter 4 Internal Reporting, Personal Connections, and Employee Performance

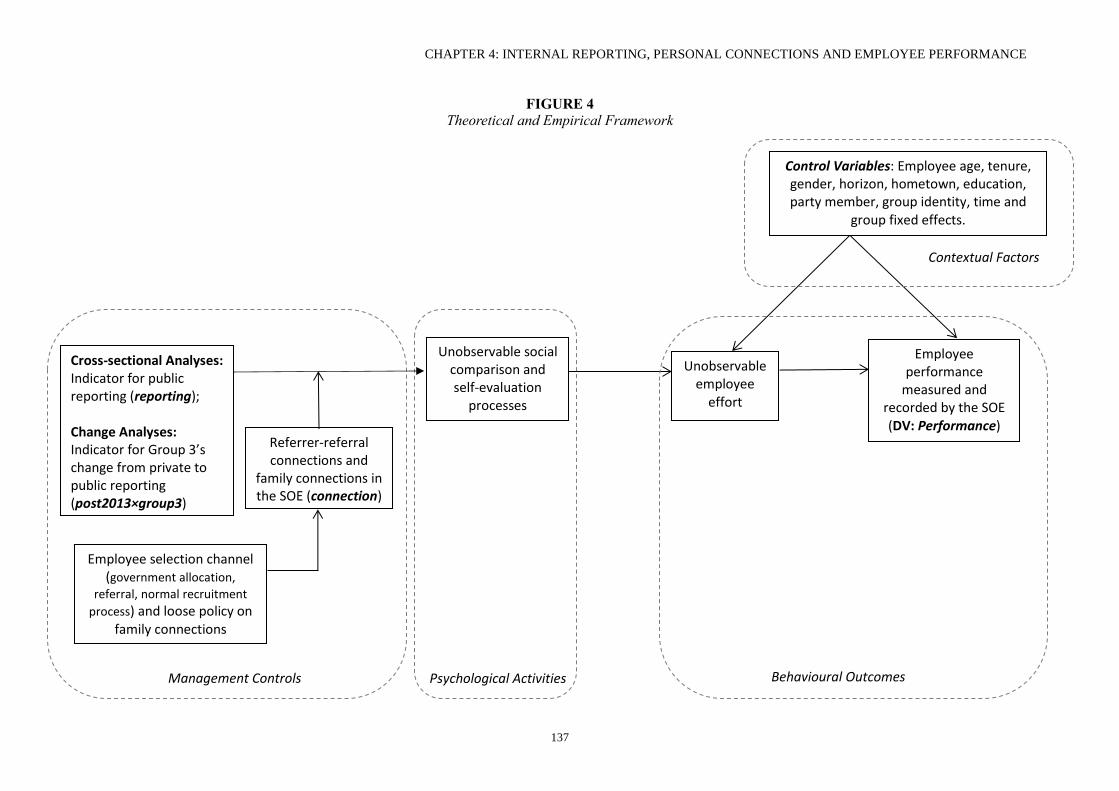

Figure 1 Theoretical and Empirical Framework…………………………………….. 118

Figure 2 Performance Reporting at the Research Site....……...…….………..…. 125

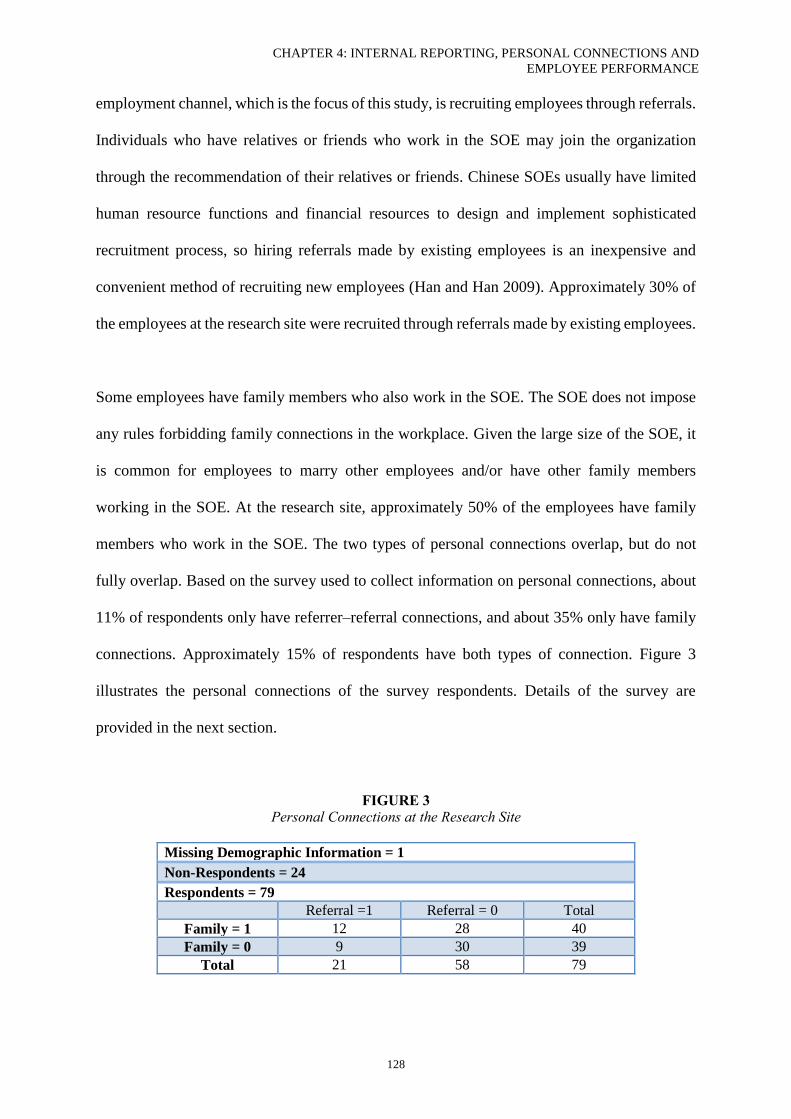

Figure 3 Personal Connections at the Research Site..……………………….…... 126

Figure 4 Theoretical and Empirical Framework………….…………………….... 135

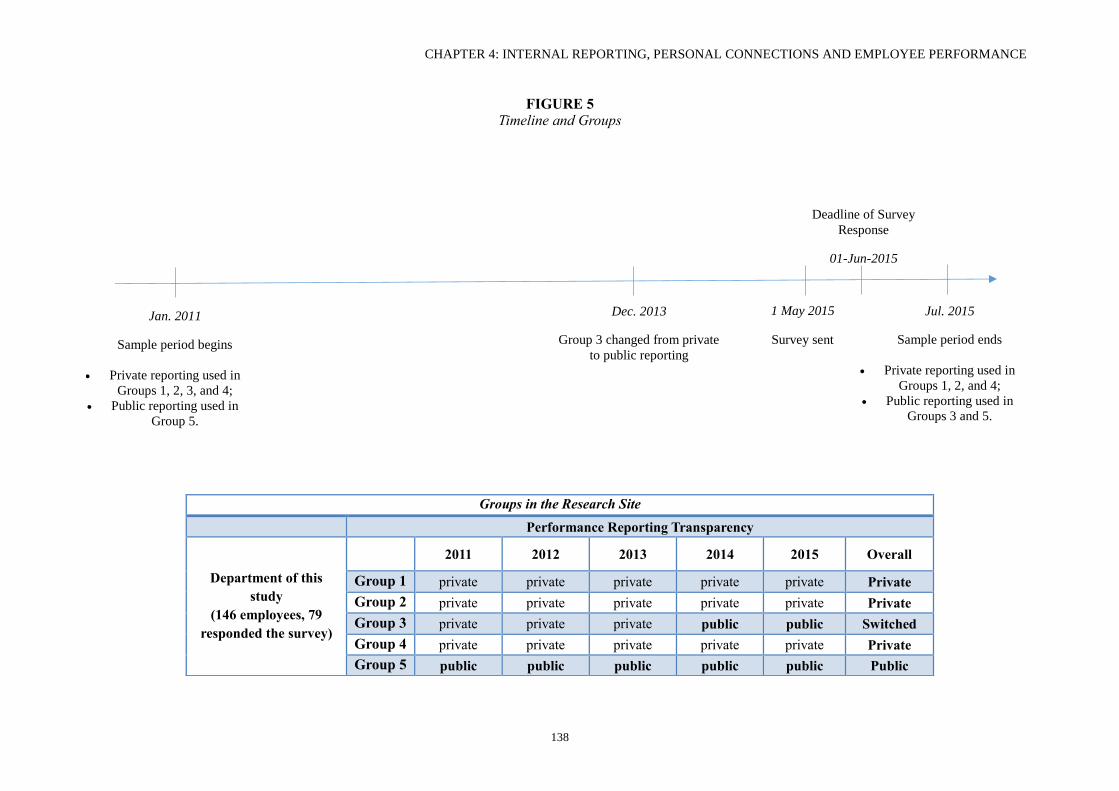

Figure 5 Timeline and Groups………………………..………………….……… 136

viii

LIST OF TABLES

Chapter 2 Performance Reporting Transparency, Group Identity, and Employee

Performance

Table 1 Sample Selection ...………………………………………………………. 29

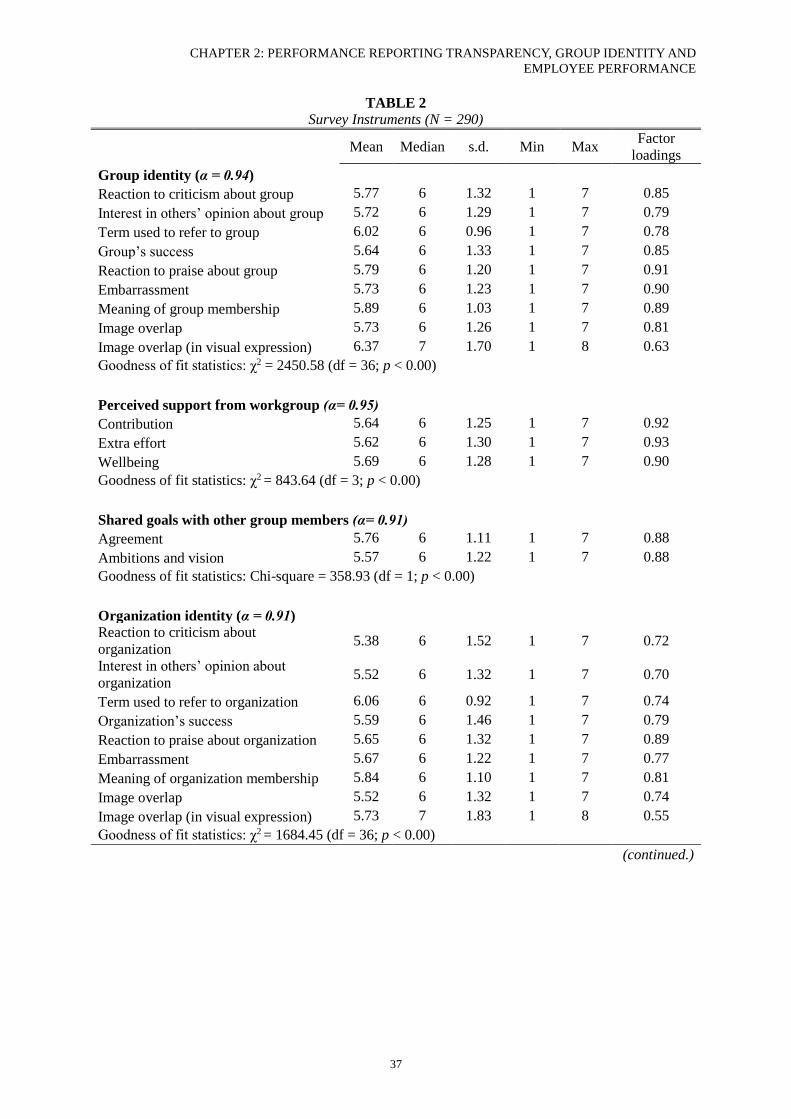

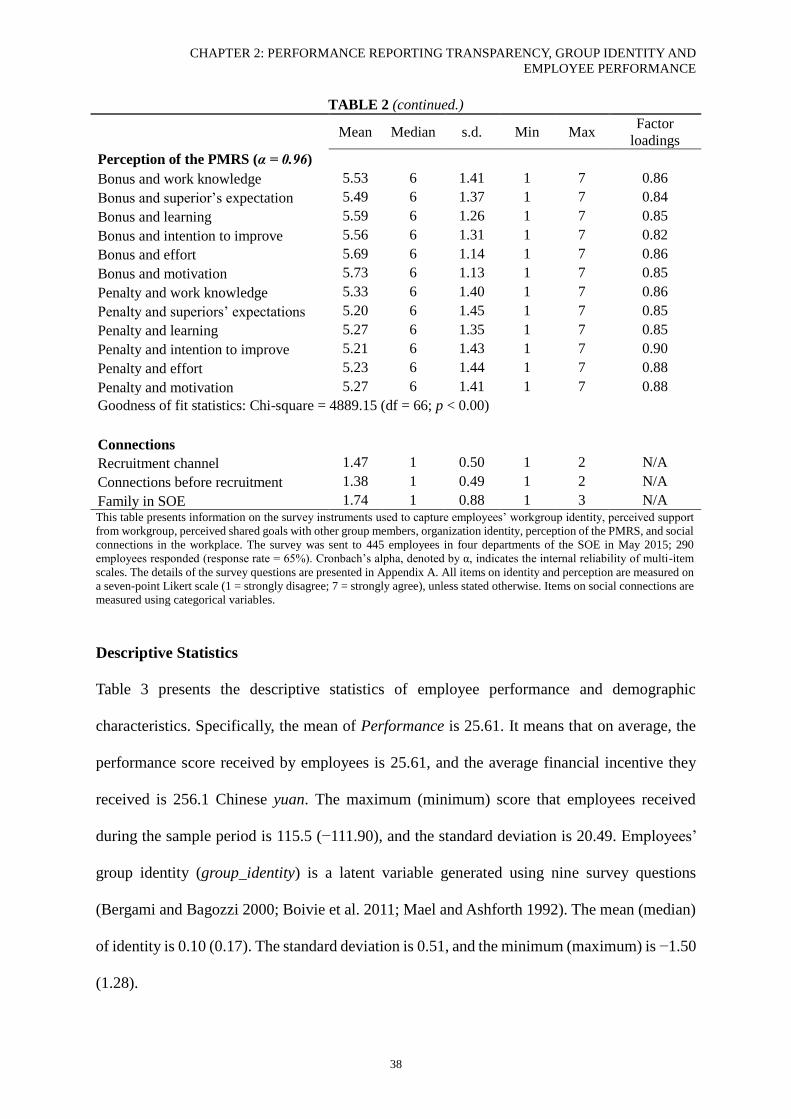

Table 2 Survey Instruments ...……………………………………………………. 36

Table 3 Descriptive Statistics ...……………………………………………..……. 39

Table 4 Pearson Correlations ...……………………………………………..……. 41

Table 5 Performance Reporting Transparency, Group Identity, and Employee

Performance …………..…………………………………….…………….. 44

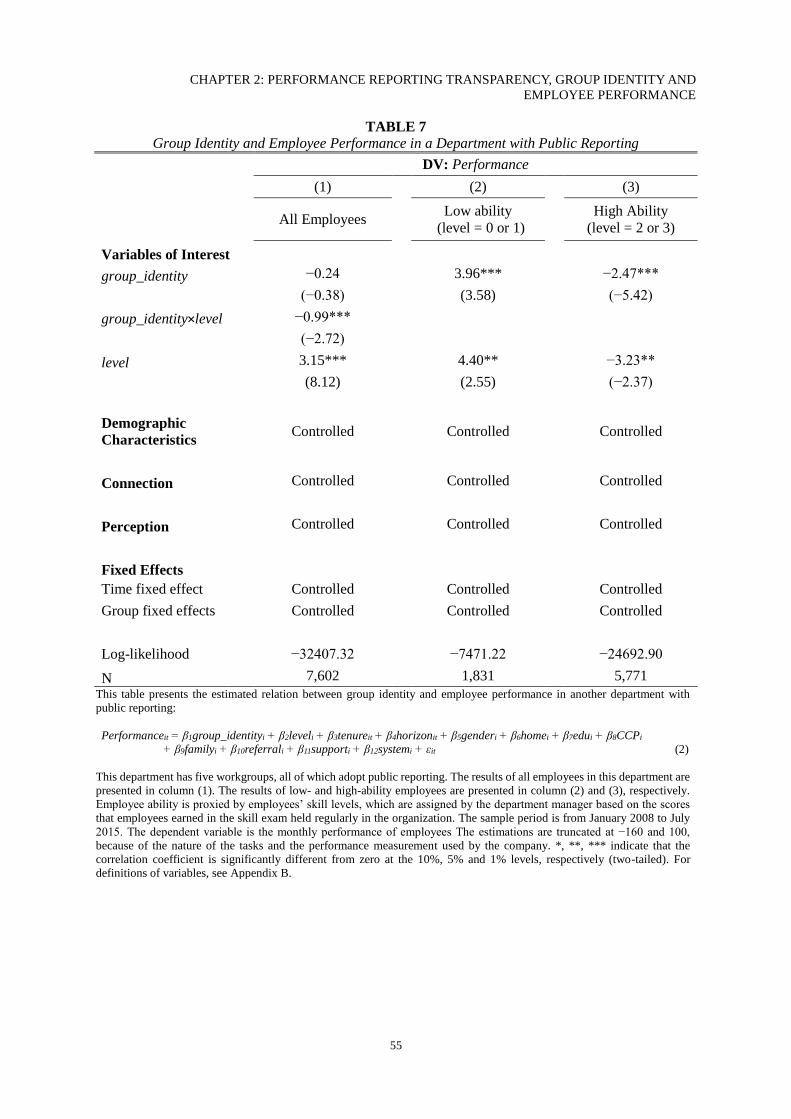

Table 6 Group Identity and Employee Performance under Public Reporting..….. 47

Table 7 Group Identity and Employee Performance in a Department with Public

Reporting………...…..…………………………………….…………….. 54

Table 8 Determinants of Group Identity…………………………………..…..…. 56

Chapter 3 Work Norms as a Control Mechanism: Implications for Employee

Performance

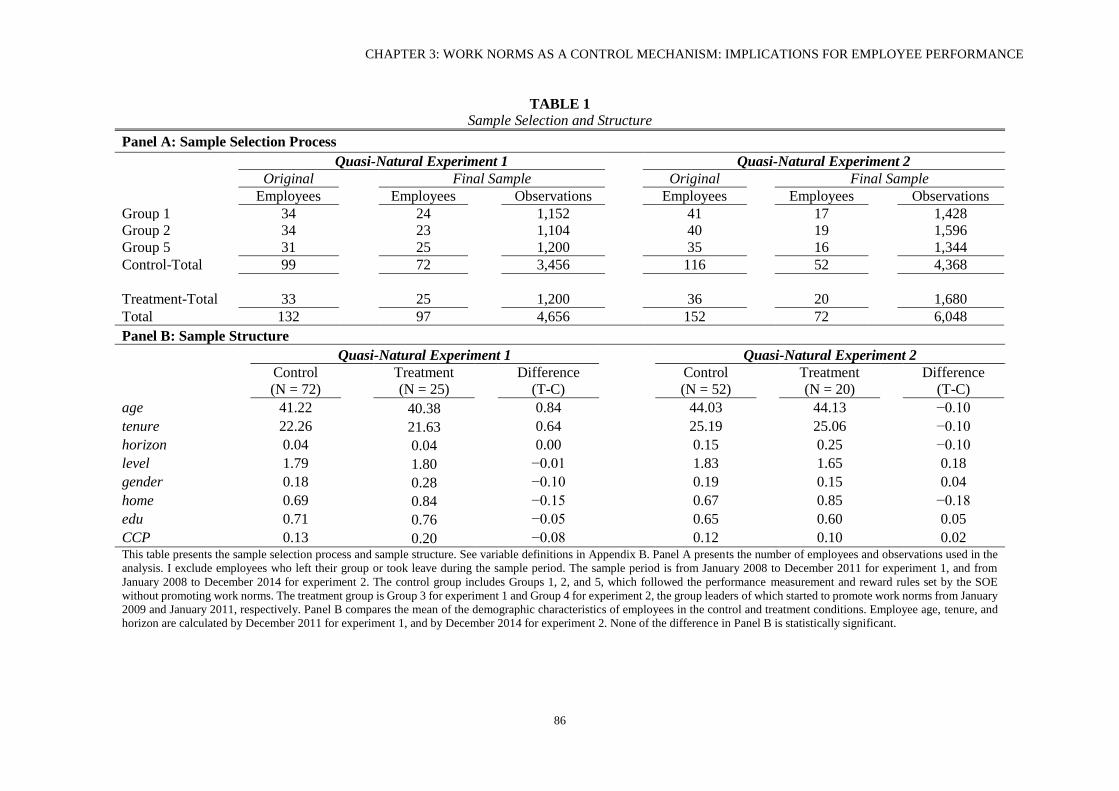

Table 1 Sample Selection and Structure ...………………………………………. 84

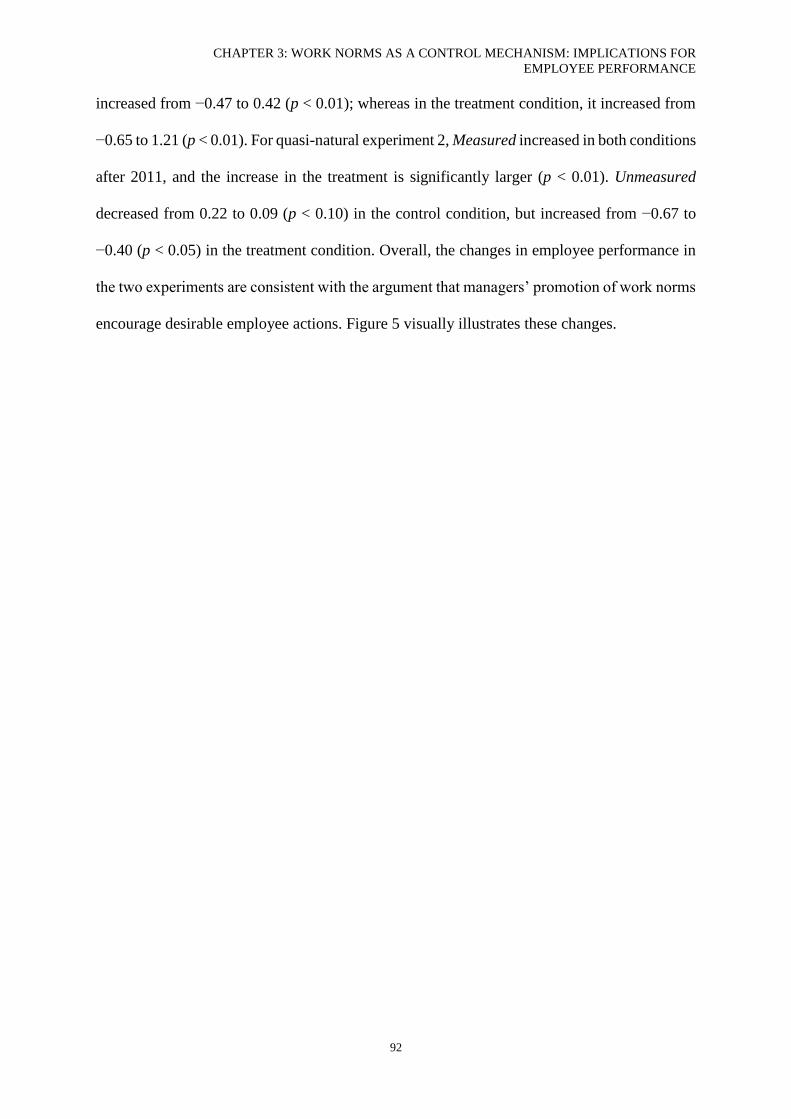

Table 2 Descriptive Statistics of Employee Performance...………………….……. 91

Table 3 Pearson Correlations ...……………………………………………..……. 94

Table 4 Managers’ Promotion of Work Norms and Employee Performance…..... 96

Table 5 Managers’ Promotion of Work Norms and Employee Performance:

Estimations by Demographic Groups ………………...………………….. 98

Table 6 Removal of Work Norms and Employee Performance ………………… 100

ix

Chapter 4 Internal Reporting, Personal Connections, and Employee Performance

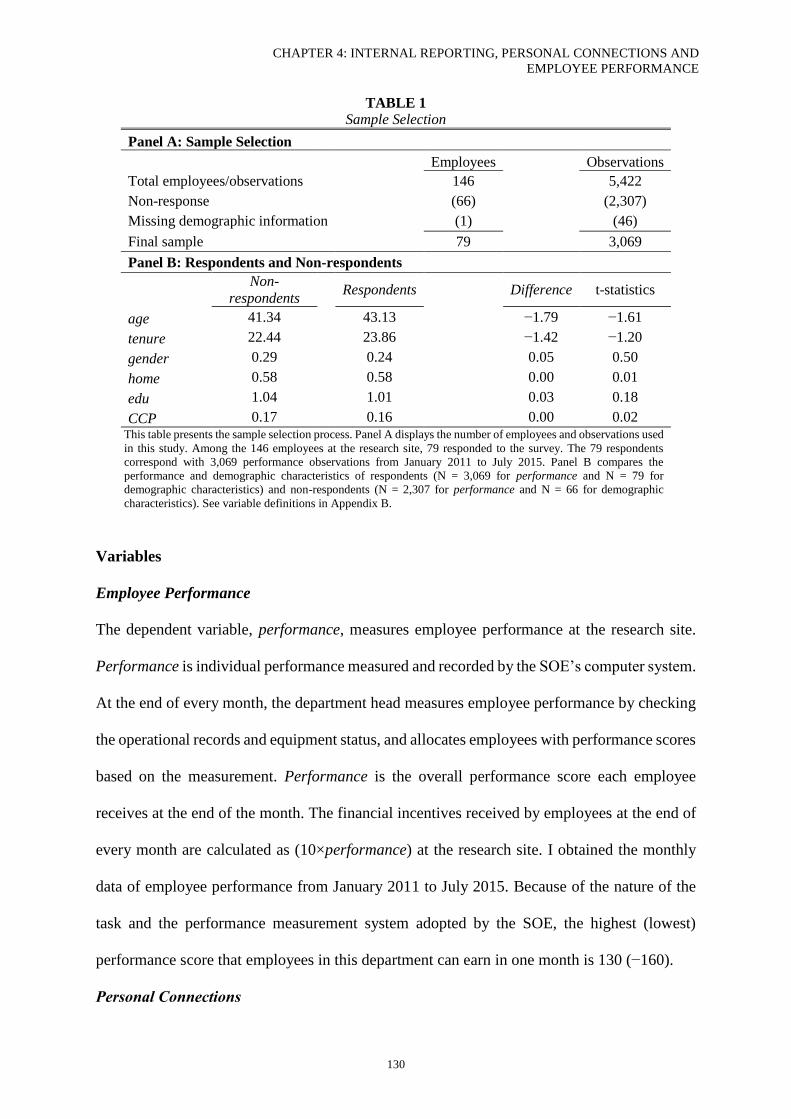

Table 1 Sample Selection ...………………………………………………..……. 128

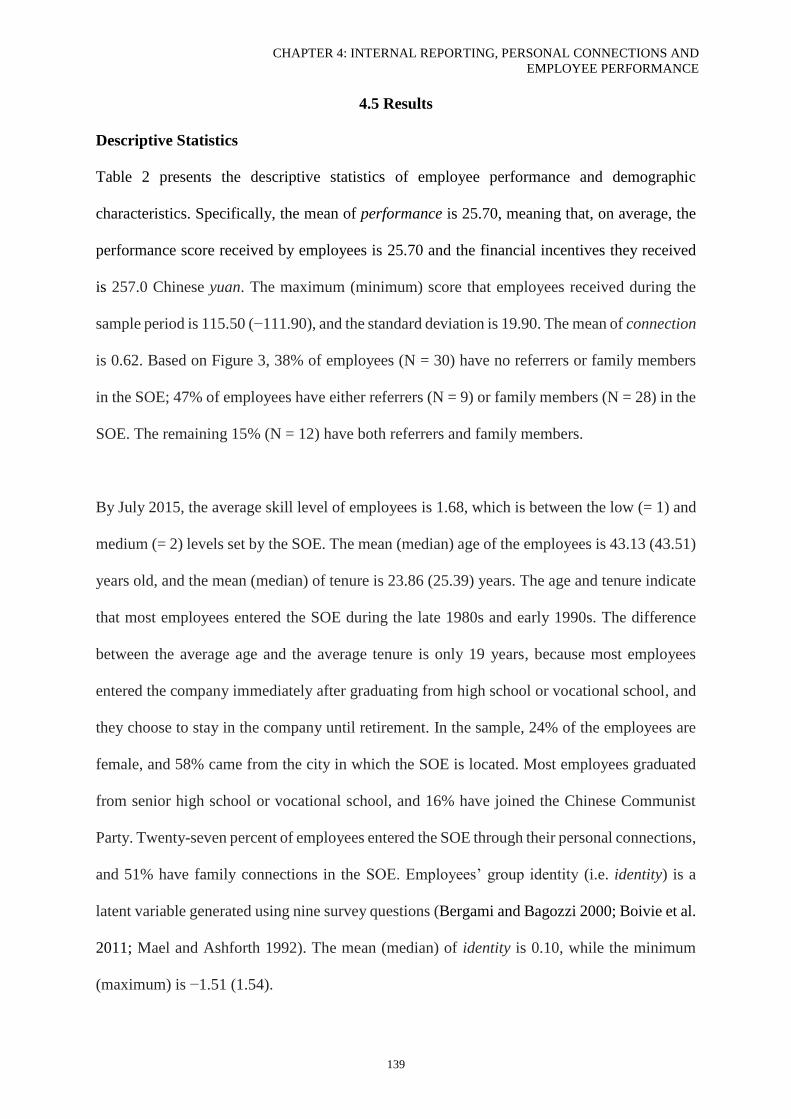

Table 2 Descriptive Statistics…………………………...………………………. 138

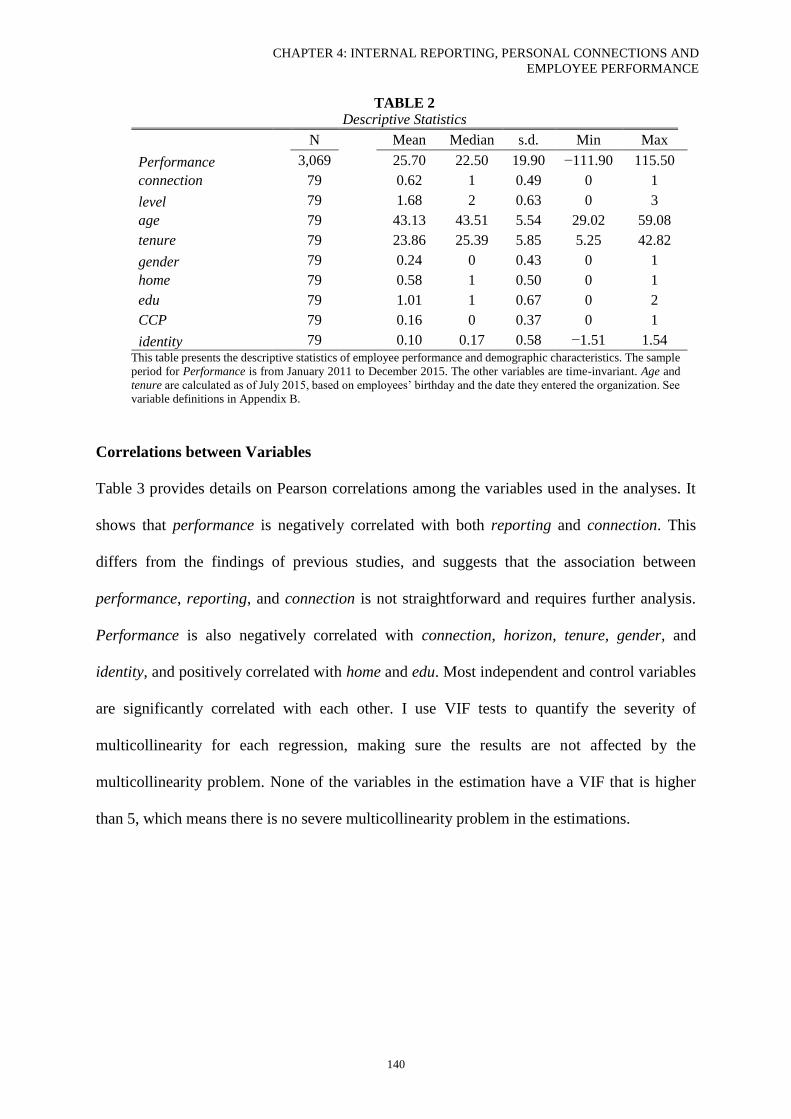

Table 3 Pearson Correlations ...…………………………………………………. 139

Table 4 Cross-Sectional Analysis……………………………………………….. 141

Table 5 Change Analysis………………………………………………………... 143

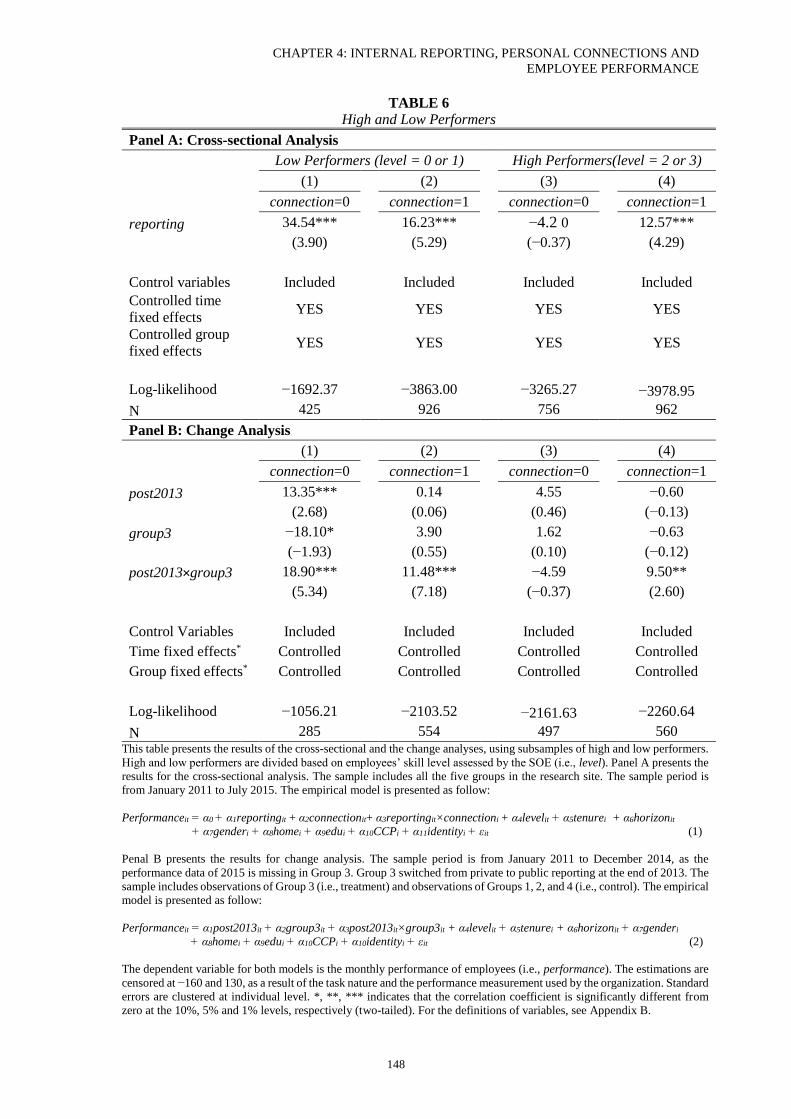

Table 6 High and Low Performers………………………………………………. 146

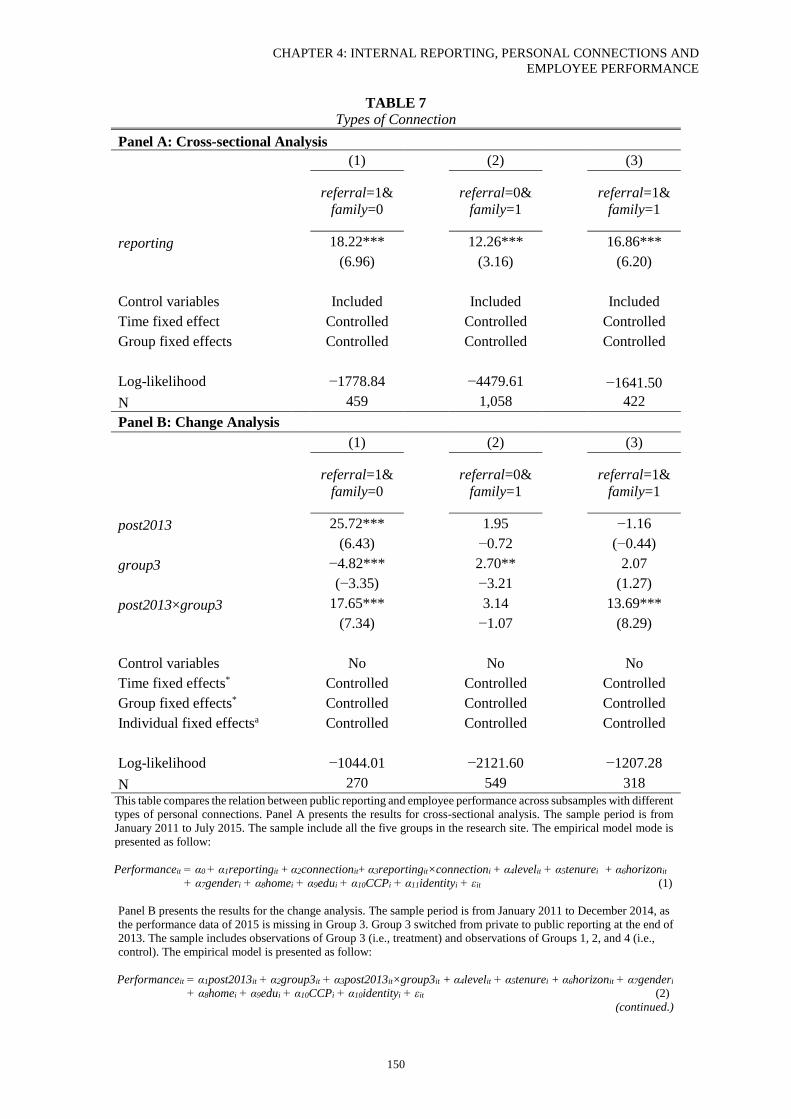

Table 7 Types of Connection…………………………………………………..... 148

CHAPTER 1: THESIS OUTLINE

1

CHAPTER I

THESIS OUTLINE

1.1 Overview

This thesis includes three essays that examine how management control systems (MCSs) affect

the behavior of lower-level employees. MCSs play an important role in directing the task

performance of lower-level employees. Managers can align employees’ interests with the

organization’s goals and strategic priorities, and motivate employee actions that contribute to

the desired organizational outcomes through the design of MCSs. Management controls

include both formal and informal controls (Gibbson and Kaplan 2015; Langfield-Smith 1997).

Formal controls—such as financial incentives, performance reporting, and employee

selection—are commonly used by organizations to motivate employee performance. However,

the effectiveness of these formal controls is conditional upon the informal controls, which work

through the cultures and norms that develop within organizations, or by encouraging employees’

identification with their organizations or workgroups. Little research has been conducted on

the role of informal controls, or whether they are effective in motivating employee performance.

The three essays in this thesis add to the existing literature by documenting how formal and

informal controls jointly affect employee performance.

I draw on psychology, management, and economic literature to inform my empirical models.

The development of social identity theory (Akerlof and Kranton 2000, 2003, 2010; Ashforth

and Mael 1989; Hogg 2006; Hogg and Terry 2000; Turner 1991), social comparison theory

(Festinger 1954; Suls and Wheeler 2000), and theories on social and work norms (Cialdini,

Kallgren, and Reno 1990, 1991; Cialdini and Goldstein 2004; Cialdini and Trost 1998) provide

CHAPTER 1: THESIS OUTLINE

2

theoretical foundations for the three studies relating to formal and informal controls. Drawing

on these theories, I examine how employee performance is affected by internal performance

reporting and group identity (essay 1), managers’ promotion of work norms (essay 2), and the

personal connections that employees have in the workplace (essay 3).

I conducted the three studies in a state-owned enterprise (SOE) in China. The SOE provides a

rich dataset of employee performance throughout multiple periods. A range of different formal

controls—including performance measurement and financial incentives, performance

reporting, and employee selection—are adopted in this organization. Additionally, employees’

group identity, work norms, and personal connections are salient in this setting, which allows

the informal norms and beliefs of employees to function as part of the organization’s control

system. These features make this organization an ideal setting for the studies in this thesis.

Specifically, I conduct the first and the third studies in a department with 146 employees. This

department has variation in performance reporting transparency. It allows me to examine how

employee performance is related employees’ group identity and personal connections, and

whether these relations are conditional upon the performance reporting choices made by

managers. I conduct the second study in a different department with 169 employees. Two out

of the five group leaders in this department have taken actions to promote work norms within

their groups. This allows me to examine whether managers’ promotion of work norms is

effective in motivating employee performance in a setting where weak financial incentives are

adopted.

CHAPTER 1: THESIS OUTLINE

3

1.2 Outline of the Three Essays

Essay 1: Performance Reporting Transparency, Group Identity and Employee

Performance

The first essay examines the relation between group identity and employee performance in

groups with private reporting (i.e., employees receive information on their own performance

only) and groups with public reporting (i.e., employees receive information on their own and

their peers’ performance). Using laboratory settings, previous studies find that compared with

private reporting, public reporting is more effective in motivating employee performance

(Hannan et al. 2013; Tafkov 2012). Public reporting makes employees concerned about their

self-image and motivates employees to demonstrate higher performance to “look good” in front

of their peers (Luft, 2016). However, in practice, how employees behave under private and

public reporting may depend on their group identity. “Group identity” is the extent to which

employees identify with their workgroups. Economics, management, and psychology theories

suggest that group identity plays an important role in directing individual behaviors (Akerlof

and Kranton 2000, 2003, 2010; Ashforth and Mael 1989; Hogg and Terry 2000; Terry, Hogg,

and White 1999; Turner 1991). In this study, I examine how group identity is related to

employee performance, and whether the relation between the two variables varies across

workgroups with private and public reporting.

I examine the research question in a department with 146 employees and five workgroups,

three of which adopt private reporting and the other two adopt public reporting. The results

indicate that the relation between group identity and employee performance is conditional upon

managers’ choice regarding performance reporting transparency. Under private reporting,

group identity motivates employees to improve their performance; while under public reporting,

group identity motivates employees with high (low) ability to suppress (improve) their

CHAPTER 1: THESIS OUTLINE

4

performance to look more similar to their peers. These findings add to the literature on internal

reporting (Azmat and Iriberri 2010; Frederickson 1992; Hannan, Krishnan, and Newman 2008;

Hannan McPhee, Newman, and Tafkov 2013; Maas and Van Rinsum 2013; Tafkov 2012), as

well as the growing literature on employees’ group identity (Abernethy, Bouwens, and Kroos

2017; Boivie, Lange, McDonald, and Westphal 2011; Towry 2003). This study also has

practical implications, as the findings suggest that when making decisions about performance

reporting transparency, managers need to consider employees’ group identity and ability, as

well as the performance distribution in the workplace.

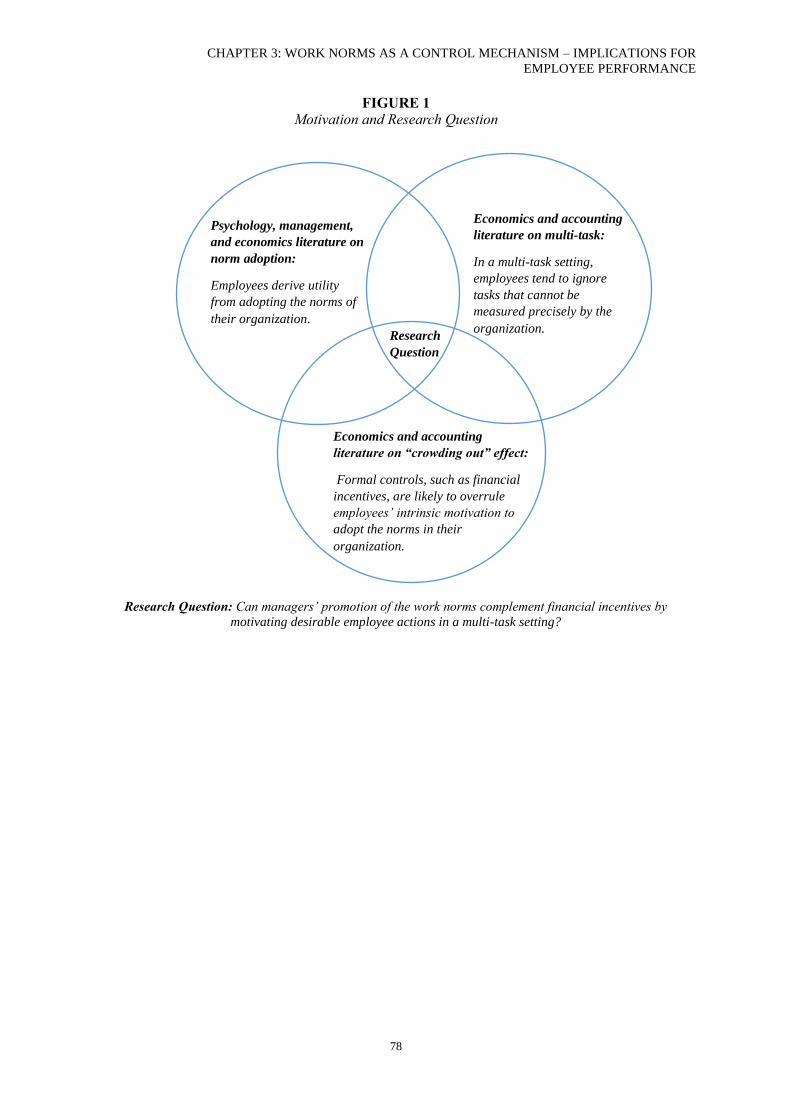

Essay 2: Work Norms as a Control Mechanism—Implications for Employee Performance

The second essay examines one mechanism that can be used as part of an organization’s

management control system: manager’s promotion of work norms. In laboratory settings,

psychology studies find that focusing individuals’ attention on a particular norm leads to

individuals’ adoption of the norm (Cialdini et al. 1990, 1991). In organizations, it is an

empirical question whether managers can motivate employee performance through deliberately

promoting the work norms that contribute to the desired organization outcomes. On the one

hand, the formal control mechanisms used in organizations, such as financial incentives, may

overrule the effect of the work norms (Ariely, Loewenstein, and Prelec 2006; Gneezy and

Rustichini 2000; Taylor and Bloomfield 2010). On the other hand, work norms may

complement financial incentives by guiding and motivating employees to demonstrate high

performance (Akerlof and Kranton 2000, 2003; Ashforth and Meal 1989; Hogg and Terry

2000). This study examines this question in a multi-task setting, where the control problem is

to motivate desirable employee actions that can be precisely measured and desirable employee

actions that cannot be precisely measured.

CHAPTER 1: THESIS OUTLINE

5

I conducted this study in a department with 169 employees and five workgroups, where the

leaders of two of the groups take procedures to promote work norms within their groups. The

promoted work norms require employees to engage in desirable actions that can be precisely

measured as well as desirable actions that cannot be precisely measured. The procedures that

the two group leaders take include directly communicating the work norms to employees, as

well as using feedback and recognition to focus employees’ attention on the work norms. The

performance measurement and reward system used by the SOE allowed me to not only measure

employee actions that can be precisely measured, but also construct a proxy for employee

actions that cannot be precisely measured. The results indicate that the group leaders’

promotion of work norms is related to an increase in both types of action. After removing the

work norms, employee performance on tasks that can be precisely measured declined, while

employee performance on tasks that cannot be precisely measured did not change significantly.

These findings contribute to the literature on management controls and employee performance.

The existing literature suggests that the use of financial incentives is subject to high monetary

costs and potential unintended consequences (e.g., employees will pay less attention to tasks

that cannot be measured precisely). This study finds that managers’ promotion of work norms

can complement financial incentives by motivating the desirable actions of employees,

especially for tasks that cannot be precisely measured. The findings also help managers to

better understand how their practices affect the way that employees perform their tasks.

Essay 3: Internal Reporting, Personal Connections and Employee Performance

The third essay examines how personal connections affect the relation between performance

reporting transparency and employee performance. Drawing on social comparison theory

(Festinger 1954; Suls and Wheeler 2000), existing studies experimentally find that reporting

CHAPTER 1: THESIS OUTLINE

6

employee performance publicly in the workplace increases employees’ concern for their self-

image, and motivates employees to demonstrate high performance to “look good” in front of

their peers (Hannan et al. 2013; Tafkov 2012). However, in real-world organizations, different

types of employees may have different image concerns and react differently toward public

reporting. This study examines whether the performance impact of public reporting varies

across employees with and without personal connections in the workplace.

This study focuses on two types of personal connection: the referrer–referral connection and

the family connection. Both types of connections are common in organizations, and can be

important to managers’ decision-making regarding employee selection. Based on social

psychology literature, both types of connection are likely to increase employees’ image concern

(Cupach and Metts 1994; Goffman 1979; Tedeschi 2013). The employee selection channels

and criteria of the SOE allow me to classify employees into two groups: those with and those

without personal connections in the SOE. By comparing the two types of employees, I find that

public reporting has a significant and positive performance effect on those with personal

connections. However, it has no significant effect on the performance of employees who have

no personal connections. These findings contribute to the literature on internal performance

reporting (Hannan et al. 2013; Luft 2016; Maas and Rinsum 2013; Tafkov 2013) and employee

selection (Abernethy, Dekker, and Schultz 2015; Campbell 2012), and suggest that managers

need to consider internal performance reporting and employee selection as integrated control

choices.

1.3 Conclusion

The three essays in this thesis examine how formal and informal controls jointly affect the task

performance of lower-level employees. Drawing on behavioral theories in the social

CHAPTER 1: THESIS OUTLINE

7

psychology, management, and economic literature, and using archival and survey data from a

field site, I find that formal and informal controls function as an integrated system. First, in

settings where group identity is salient, the relation between group identity and employee

performance is conditional on managers’ decisions regarding performance reporting

transparency. Second, in multi-tasking settings where employee performance in some tasks

cannot be precisely measured, managers can combine the use of financial incentives with the

promotion of work norms. Third, the relation between performance reporting transparency and

employee performance is conditional upon employees’ personal connections, which can be

controlled by employee selection channel and criteria. These findings not only add to the

management accounting literature, but also have important implications for the design and

implementation of management controls in organizations.

The remainder of this thesis is structured as follows. Each chapter describes one of the three

essays in detail. The structure of each chapter allows the three essays to be read separately and

in a different order than that presented here. Chapter 2 presents the study that examines the

relation between group identity and employee performance under private and public reporting.

Chapter 3 presents the study on managers’ promotion of work norms. Chapter 4 presents the

study on how personal connections in the workplace affect the performance impact of public

reporting. Chapter 5 concludes the thesis by summarizing the findings, contributions, and

limitations.

CHAPTER 1: THESIS OUTLINE

8

REFERENCES

Abernethy, M., J. Bouwens, and P. Kroos. 2017. Organization identity and earnings

manipulation. Accounting, Organizations and Society. Available at:

http://www.sciencedirect.com/science/article/pii/S0361368217300193 [Accessed 31

May 2017]

Abernethy, M. A., H. C. Dekker, and A. Schultz. 2015. Are employee selection and incentive

contracts complements or substitutes? Journal of Accounting Research 53(4): 633–668.

Akerlof, G. A., and R. E. Kranton. 2000. Economics and identity. Quarterly Journal of

Economics 115(3): 715–753.

Akerlof, G. A., and R. E. Kranton. 2003. Identity and the economics of organizations. The

Journal of Economic Perspectives 19(1): 9–32.

Akerlof, G. A., and R. E. Kranton. 2005. Identity and the Economics of Organizations. Journal

of Economic Perspectives 19(1): 9–32.

Akerlof, G. A., and R. E. Kranton. 2008. Identity, supervision, and work groups. The American

Economic Review 98(2): 212–217.

Akerlof, G. A., and R. E. Kranton. 2010. Identity Economics: How Our Identities Shape Our

Work, Wages, and Well-Being. Princeton, NJ: Princeton University Press.

Ariely, D., G. Loewenstein, and D. Prelec. 2006. Tom Sawyer and the construction of value.

Journal of Economic Behavior and Organization 60(1): 1–10.

Ashforth, B. E., and F. Mael. 1989. Social identity theory and the organization. Academy of

Management Review 14(1): 20–39.

Azmat, G., and N. Iriberri. 2010. The importance of relative performance feedback information:

Evidence from a natural experiment using high school students. Journal of Public

Economics 94(7): 435–452

Boivie, S., D. Lange, M. L McDonald, and J. D. Westphal. 2011. Me or we: The effects of CEO

organizational identification on agency costs. Academy of Management Journal 54(3):

551–576.

Bonner, S. E., R. Hastie, G. B. Sprinkle, and S. M. Young. 2000. A review of the effects of

financial incentives on performance in laboratory tasks: Implications for management

accounting. Journal of Management Accounting Research 12(1): 19–64.

Bonner, S. E., and G. B. Sprinkle. 2002. The effects of monetary incentives on effort and task

performance: Theories, evidence, and a framework for research. Accounting,

Organizations and Society 27(4): 303–345.

Campbell, D. 2012. Employee selection as a control system. Journal of Accounting Research

50(4): 931–966.

Cialdini, R. B., C. A. Kallgren, and R. R. Reno. 1990. A focus theory of normative conduct:

recycling the concept of norms to reduce littering in public places. Journal of Personality

and Social Psychology 58(6): 1015–1026.

Cialdini, R. B., C. A. Kallgren, and R. R. Reno. 1991. A focus theory of normative conduct: A

theoretical refinement and re-evaluation of the role of norms in human behavior.

Advances in Experimental Social Psychology 24: 201–234.

Cupach, W. R., and S. Metts. 1994. Facework. Thousand Oaks, CA: Sage Publications.

Festinger, L. 1954. A theory of social comparison processes. Human Relations 7(2): 117–140.

Frederickson, J. R. 1992. Relative performance information: The effects of common

uncertainty and contract type on agent effort. The Accounting Review 67(4): 647–669.

Gibbons, R., and R. S. Kaplan. 2015. Formal measures in informal management: Can a

balanced scorecard change a culture? American Economic Review: Papers and

Proceedings 105(5): 447–451.

Gneezy, U., and A. Rustichini. 2000. A fine is a price. Journal of Legal Studies 29: 1–17.

CHAPTER 1: THESIS OUTLINE

9

Goffman, E. 1979. The Presentation of Self in Everyday Life. England: Penguin.

Hannan, R. L., R. Krishnan, and A. H. Newman. 2008. The effects of disseminating relative

performance feedback in tournament and individual performance compensation plans.

The Accounting Review 83(4): 893–913.

Hannan, R. L., G. P. McPhee, A. H. Newman and I. D. Tafkov. 2013. The effect of relative

performance information on performance and effort allocation in a multi-task

environment. The Accounting Review 88(2): 553–575.

Hogg, M. A. 2006. Social identity theory. In Contemporary Social Psychological Theories,

edited by P. J. Burk, 111–136. Stanford, CA: Stanford University Press.

Hogg, M. A., and D. I. Terry. 2000. Social identity and self-categorization processes in

organizational contexts. Academy of Management Review 25(1): 121–140.

Luft, J. 2016. Cooperation and competition among employees: Experimental evidence on the

role of management control systems. Management Accounting Research.

doi:10.1016/j.mar.2016.02.00

Kachelmeier, S. J., B. E. Reichert, and M. G. Williamson. 2008. Measuring and motivating

quantity, creativity, or both. Journal of Accounting Research 46(2): 341–373.

Langfield-Smith, K. 1997. Management control systems and strategy: A critical review.

Accounting, Organizations and Society 22 (2): 202–232.

Maas, V. S., and M. Van Rinsum. 2013. How control system design influences performance

misreporting. Journal of Accounting Research 51(5): 1159–1186.

Sprinkle, G. B. 2000. The effect of incentive contracts on learning and performance. The

Accounting Review 75(3): 299–326.

Suls, J., and L. Wheeler. 2000. Handbook of Social Comparison: Theory and Research. New

York, NY: Kluwer Academic/Plenum Publishers.

Tafkov, I. D. 2012. Private and public relative performance information under different

compensation contracts. The Accounting Review 88(1): 327–350.

Tedeschi, J. T. (Ed.) 2013. Impression Management Theory and Social Psychological

Research. NY: Academic Press.

Terry, D. J., M. A. Hogg, and K. M. White. 1999. The theory of planned behavior: Self-identity,

social identity and group norms. British Journal of Social Psychology 38(3): 225–244.

Towry, K. L. 2003. Control in a teamwork environment—The impact of social ties on the

effectiveness of mutual monitoring contracts. The Accounting Review 78(4): 1069–1095.

Turner, J. C. 1991. Social Influence. Pacific Grove, CA: Brooks/Cole.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

CHAPTER II

PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY

AND EMPLOYEE PERFORMANCE

ABSTRACT

Experimental evidence indicates that compared with private reporting (i.e., employees receive

information on their own performance only), public reporting (i.e., employees receive

information on their own and their peers’ performance) is more effective in motivating

employee performance, as public reporting increases employees’ concern for their self-image.

However, in practice, employees’ image concern may depend on their group identity—the

extent to which employees identify with their workgroups. This study investigates the relation

between group identity and employee performance under private and public reporting. Using

archival and survey data from a Chinese organization, I find that in work groups with private

reporting, group identity is positively related to employee performance. However, in work

groups with public reporting, group identity is negatively related to employee performance. I

explore this further and find that, under public reporting, group identity is negatively (positively)

related to the performance of employees with high (low) ability. This study extends prior

research on the influence of performance reporting transparency on employee performance. It

also highlights the importance for managers to consider the group identity and ability of their

subordinates when making internal reporting choices.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

11

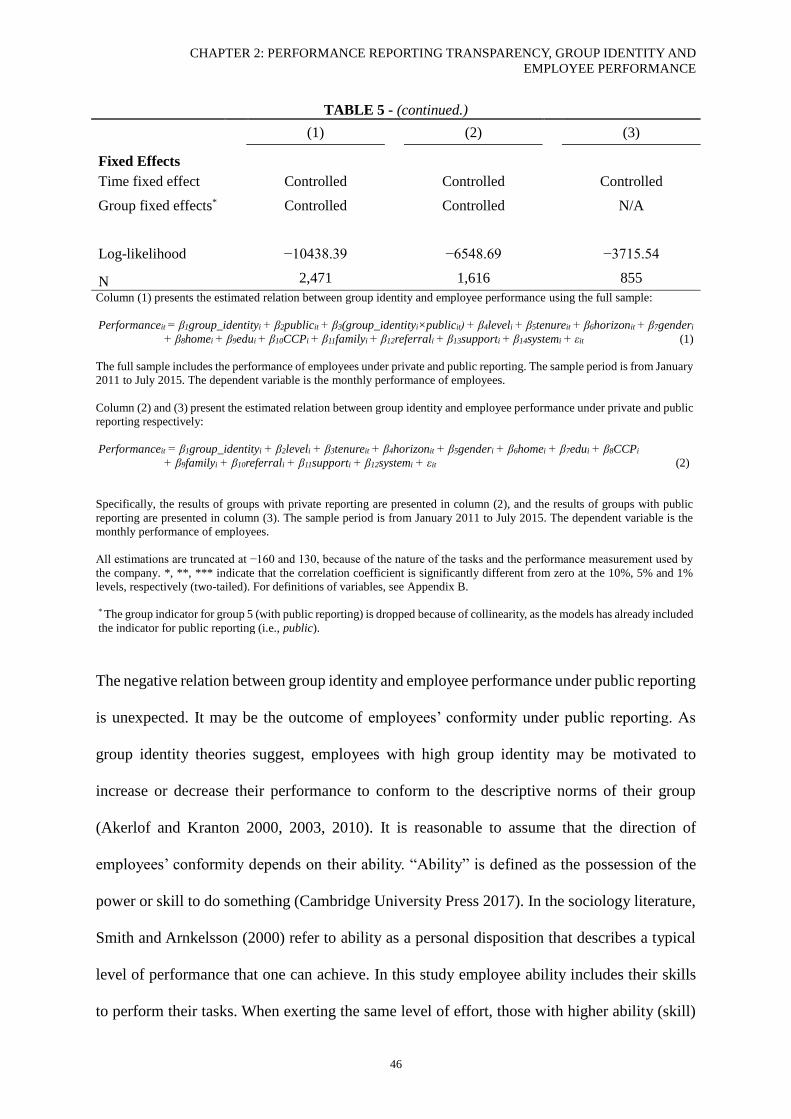

2.1 Introduction

Social comparison theories in psychology suggest that individuals tend to compare themselves

with others. Doing so allows individuals to evaluate their ability, and adjust their behaviors to

maintain a positive self-image in their social or work group (Festinger 1954; Suls and Wheeler

2000). In organizations, social comparisons make internal performance reporting an important

control mechanism. The way that employee performance is reported in organizations affects

the information that employees receive, the benchmark that they choose to evaluate themselves,

and their subsequent performance. Experimental evidence indicates that compared with private

reporting (i.e., employees receive information on their own performance only), public reporting

(i.e., employees receive information on their own and their peers’ performance) is more

effective in motivating employee performance, as public reporting increases employees’

concern for their self-image (Hannan, McPhee, Newman, and Tafkov 2013; Maas and Rinsum,

2013; Tafkov, 2012). However, in practice, employees’ concern for their self-image may

depend on the extent to which employees perceive themselves as a part of their work group, or

in other words, employees’ group identity.

“Group identity” refers to the extent to which employees identify with their work group

(Akerlof and Kranton 2000, 2003, 2010; Ashforth and Mael 1989). Employees with high group

identity have strong motivation to adjust their performance to enhance their self-image as

members of their group (Akerlof and Kranton 2000, 2003, 2010; Ashforth and Mael 1989;

Hogg and Terry 2000; Terry, Hogg, and White 1999; Turner 1991; Van Knippenberg 2000; Yun,

Takeuchi, and Liu 2007). Performance reporting transparency (private vs. public) affects the

information environment within work groups and the performance benchmark that employees

can choose to evaluate their performance. Therefore, managers’ choice of reporting

transparency is likely to affect the relation between group identity and employee performance.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

12

This study investigates the relation between group identity and employee performance in

groups with private reporting and groups with public reporting. Examining this question

extends prior research on the influence of performance reporting transparency on employee

performance. This study also highlights the importance for managers to consider the group

identity of their subordinates when making internal reporting choices.

Under private reporting, managers provide employees with information on their own

performance, but not the information on their peers’ performance. Employees do not receive

information on the descriptive norms (i.e., the performance of other employees) of their group.

Therefore, under private reporting, the performance requirements set by the organization tend

to be a more salient performance benchmark than the descriptive norms. Based on the existing

theories, group identity may motivate employees to increase their compliance with the

performance requirements, to reinforce their self-image as organizational participants and

members of their workgroups (Akerlof and Kranton 2000, 2003; Ashforth and Mael 1989;

Hoagg and Terry 2000). Increasing compliance with the performance requirements set by the

organization allows employees to demonstrate higher performance. Therefore, I expect that

group identity is positively related to employee performance in workgroups with private

reporting,

Under public reporting, employees not only can observe the descriptive norms of their groups,

but also are aware that their own performance can be observed by others in their group. It is

unclear how group identity is related to employee performance under public reporting. On the

one hand, employees with high group identity may still be motivated to demonstrate high

performance, as what they would do under private reporting. On the other hand, employees

with high group identity may be motivated to adjust their performance to look more similar to

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

13

others in their group (or in other words, conforming to the group descriptive norms).

Conforming to the group descriptive norms can reinforce employees’ self-image as group

members and prevent them from receiving social punishment from other group members (e.g.,

contempt for low performers, envy for high performers, or even social isolation) (Akerlof and

Kranton 2000, 2010; Charness, Masclet, and Villeval 2013; Smith 2000; Vecchio 2000).

Employees with high group identity may be motivated to increase or decrease their

performance to conform to the group descriptive norms. A potential downside of public

reporting is that some employees may decrease their performance to conform to look more

similar to others in their group. If this is the case, the relation between group identity and

employee performance under public reporting will not be as positive as under private reporting.

Therefore, I hypothesize that there is a positive relation between group identity and employee

performance; and this relation is more positive under private reporting than under public

reporting.

I examine the hypothesis using archival and survey data from a large department within a

Chinese state-owned enterprise (SOE). Employees in this department are responsible for

equipment inspection, operation and maintenance. The department head divides employees

into five workgroups to improve the efficiency of the management. Three features of this

department makes it an ideal setting for this study. First, three of the five workgroups in this

department adopt private reporting, and the other two adopt public reporting. In the three

groups with private reporting, the group leaders provide each group member with a note with

his or her own name and performance on it at the end of every month. In the two groups with

public reporting, the group leaders print the names and performance of all group members in a

table, and distribute this performance table within their groups at the end of every month. The

variation in the performance reporting practices provides an opportunity to examine the role of

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

14

performance reporting transparency with the contextual factors controlled. Second, employees’

group identity is salient in this setting, as employees usually work in the same workgroups for

years and engage various activities with the other members of their workgroups. This feature

provides an opportunity to examine the relation between group identity and employee

performance. Third, the operating environment of this setting is stable. Because of several

features of the SOE (explained in detail in the research site section), most employees work in

the organization and the same workgroups for many years. It allows the examination of

employee performance in multiple periods, which helps mitigate potential biases caused by

unobservable factors in certain time period(s).

I measure employee performance using the archival data of the monthly performance of

employees, and measure employees’ group identity using the survey instruments designed and

validated by prior research (Bartel 2001; Bergami and Bagozzi 2000; Boivie et al. 2011; Mael

and Ashforth 1992; Dukerich et al. 2002; Johnson et al. 2006; Shamir and Kark 2004). The

results indicate that group identity is positively related to employee performance in the groups

with private reporting. Surprisingly, in the groups with public reporting, group identity is

negatively related to employee performance. The unexpected findings for public reporting may

be the result of employees’ conformity. Under public reporting, it is possible that those with

high ability are motivated to suppress their performance and those with low ability are

motivated to improve their performance to conform to the group descriptive norms. To better

interpret the findings of public reporting, I divide employees under public reporting into high

and low ability. I find that, under public reporting, group identity is negatively (positively)

related to the performance of employees with high (low) ability. Additional analyses indicate

that the results are not driven by unobservable group feature(s), and employees’ group identity

is not significantly affected by performance reporting transparency. Overall, the results

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

15

demonstrate that the relation between group identity and employee performance is conditional

on the reporting choices made by the group leaders. Under private reporting, group identity

motivates employees to improve their performance; while under public reporting, group

identity motivates employees with high (low) ability to suppress (improve) their performance

to conform to the descriptive norms (i.e., the performance of others) of their group.

These findings contribute to the literature on internal performance reporting. Using

experimental settings, previous studies demonstrate that public reporting leads to higher

employee performance than private reporting does (Hannan et al. 2013; Tafkov 2012). This

study finds that performance reporting transparency affects employees’ choice of performance

benchmark and their task performance, and suggests that the performance effect of public

reporting is not always positive. Specifically, under private reporting, the salient performance

benchmark is the performance requirements set by the organization. Employees with high

group identity tend to exhibit high compliance toward the performance requirements, which

leads to high task performance. In comparison, the salient performance benchmark under

public reporting is the group descriptive norms. Employees with high group identity exhibit

high conformity toward the group descriptive norms, which means those with high (low) ability

tend to suppress (improve) their task performance.

This study also contributes to the growing literature on employees’ group identity. In recent

years, several studies examine the role of group identity in the accounting literature. Previous

studies find that group identity is negatively related to accounting manipulation (Abernethy et

al. 2017) and agency costs (Boivie et al. 2011). Additionally, experimental evidence indicates

that group identity increases the effectiveness of horizontal monitoring (i.e., employees control

the actions of each other), but decreases the effectiveness of vertical monitoring (i.e.,

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

16

employees report observations of their peers’ actions to managers) (Towry 2003). There is little

evidence on how group identity is related to employee performance, and how this relation is

affected by management control mechanisms such as internal performance reporting. This

study adds to the literature by documenting that the relation between group identity and

employee performance is conditional on the managers’ choice over performance reporting

transparency. When performance reporting transparency is low, group identity is positively

related to employee performance; when it is high, group identity is negatively (positively)

related to the performance of employees with high (low) ability.

This study also has practical implications. The findings suggest that when making decisions

about performance reporting, managers need to consider employees’ group identity and ability,

as well as descriptive norms (or performance distribution) in the workplace. If most employees

in a group demonstrate satisfactory performance, public reporting is likely to lead those with

high group identity and low ability to improve their performance. However, if most employees

fail to demonstrate satisfactory performance, public reporting may lead those with high group

identity and high ability to decrease their performance. Further, management theories posit that

group identity is determined by the in-group and out-group structure, the similarity between

employees and others in their group, as well as group outcome and prestige (Ashforth and Mael

1989; Hogg and Terry 2000). Therefore, managers may need to consider and design internal

performance reporting, employee selection, and group design as an integrated control system.

The remainder of this paper is organized as follows. The next section explains the theoretical

constructs and develops the hypotheses. I then describe the research site and the methodology

of the study, before presenting the results. The final section provides the concluding comments.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

17

2.2 Literature and Hypothesis Development

Performance Reporting Transparency

Social comparison theories in psychology suggest that individuals have an inherent desire to

compare themselves with others in order to evaluate themselves (Festinger 1954; Suls and

Wheeler 2000). The social comparison process motivates individuals to adjust their behavior

to maintain a positive self-image (i.e., how individuals believe others think of them) in their

social or work groups. Drawing on the social comparison theories, prior studies demonstrate

that internal performance reporting is an effective control mechanism in motivating employee

performance. Specifically, Frederickson (1992) experimentally find that providing employees

with information on their own performance relative to the performance of their peers (i.e.,

relative performance information, or RPI) motivates employees to exhibit high effort. This

finding is consistent with the findings obtained by Azmat and Iriberri (2010) using a natural

experiment in a high school. Further, Hannan et al. (2008) find that the performance effect of

RPI is conditional on the incentive contract (i.e., tournament or individual compensation) as

well as the precision of the RPI information. Later studies also find that providing employees

with RPI may motivate undesirable behaviors, such as sabotaging the work of peers (Charness,

Masclet, and Villeval 2013) or misreporting the budget (Brown, Fisher, Sooy, and Sprinkle

2014).

Previous studies have not only examined the content of internal performance reporting, but

also examined the transparency of internal performance reporting. Using laboratory settings,

recent studies have examined how making performance information public in the workplace

affects employee behaviors. Specifically, Tafkov (2012) find that public RPI (i.e., the

performance ranking of each employee in a group is provided to all group members) is more

effective in motivating employee performance than private RPI (i.e., each employee knows his

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

18

or her own rank only). Hannan et al. (2013) also find that compared to private RPI, public PRI

is more effective in motivating employees to exert high effort in a multi-task setting.

Additionally, Maas and Van Rinsum (2013) find that publicly disclosing managers’ self-

reported performance in the workplace motivates them to report their performance honestly, in

order to maintain a positive self-image in front of their peers. These studies suggest that public

reporting increases employees’ concern for their self-image. Demonstrating a positive (e.g.,

competent or honest) self-image enhances employees’ self-esteem and improves their feelings

about self (Beach and Tesser 2000). It also prevents employees from being looked down on by

their peers, and increases employees’ status in the workplace (Smith 2000). To create and/or

maintain a positive self-image, employees are motivated to adjust their behavior, such as

demonstrating higher performance (Hannan et al. 2013; Tafkov 2012) or reporting their

performance honestly (Maas and Van Rinsum 2013).

Group Identity

However, in practice, employees’ concern for their self-image may depend on the extent to

which they perceive themselves as a part of their work group, or in other words, their group

identity. The concept of “group identity” originates from the social identity theory developed

by Tajfel (1974, 1982) and Turner (1975, 1991). They define group identity as the extent to

which individuals identify with their social or work groups. That is, group identity refers to

individuals’ self-concept which derives from their group membership (Tajfel 1974, 1982;

Turner 1975, 1991). In management literature, Ashforth and Mael (1989) discuss employees’

group identity in organizations and how it differs from other related constructs. They suggest

that one’s group identity refers to the self in terms of one’s group (“I am”). It is a perceptual

cognitive construct that describes the extent to which an employee defines herself in terms of

the group she works for. Conceptually, group identity differs from any specific behaviors (e.g.,

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

19

effort), affective states (e.g., loyalty), or internalization of the goals or values of one’s group

(e.g., commitment). In practice, group identity may affect or be affected by these factors. It

may also be affected by group structure, the similarity and shared goal(s) between group

members, and other individual or group features (Ashforth and Mael 1989; Bergami and

Bagozzi 2000).

The psychology, management, and economics literatures on group identity suggest that group

identity plays an important role in directing individual behaviors. The psychology theories posit

that individuals with higher group identity are more likely to engage in actions that contribute

to group outcomes and the interests of other group members (Haslam and Ellemers 2005; Tajfel

1982; Turner 1975). The management theories posit that group identity motivates employees

to engage in actions that are aligned with the values and norms of their group (Ashforth and

Mael 1989; Hogg and Terry 2000). These propositions are supported by empirical evidence.

For example, psychology studies find that group identity motivates employees to exhibit high

job performance (Van Knippenberg 2000; Yun et al. 2007) and engage in organization

citizenship behaviors and cooperative behaviors (Bergami and Bagozzi 2000; Haslam and

Ellemers 2005; Van Dick, Van Knippenberg, Kerschreiter, Hertel, and Wieseke 2008).

Additionally, Terry et al. (1999) find that group identity leads individuals to conform to the

norms of their group. In the management literature, Boivie et al. (2011) find that chief executive

officers (CEOs) with higher organization identity tend to avoid pursuit of personal gains that

harm the value and image of their firms.

Akerlof and Kranton (2000, 2003, 2008, 2010) consider group identity from an economic

perspective. They suggest that employees with high group identity derive utility by adopting

the norms of their groups (Akerlof and Kranton 2000, 2003). Deviating from group norms not

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

20

only undermines one’s self-image as a group member, but also increases the risk of being

marginalized or isolated by other group members. Employees with high group identity have

strong motivation to adopt the norms of their groups to avoid such negative consequences

(Akerlof and Kranton 2000, 2003). In the accounting literature, Towry (2003) experimentally

finds that group identity increases the effectiveness of horizontal monitoring (i.e., employees

control the actions of each other), but decreases the effectiveness of vertical monitoring (i.e.,

employees report observations of their peers' efforts to managers). Abernethy et al. (2017) find

that managers with incentive-based compensation engage in less opportunistic earnings

manipulation if they identify with their organization. Overall, previous studies indicate that

group identity has an important behavioral effect in organizations.

In real-world organizations, employees may identify with their organizations as well as

subunits (such as divisions, departments, and workgroups) within their organizations.

(Ashforth and Mael 1989; Hogg and Terry 2000). Among units in different organizational

levels, workgroups are most relevant to lower-level employees in their daily work; and

employees’ workgroup identity is usually more salient than their identities derived from units

higher up in the organization (Van Dick et al. 2008). Therefore, this study focuses on employees’

workgroup identity (hereafter, “group” and “workgroup” are interchangeable).

In this study, I investigate the relation between group identity and employee performance under

private and public reporting. Performance reporting transparency (private vs. public) affects

the information environment in the workplace and the performance benchmark that employees

can choose to evaluate their performance. Therefore, the choice of reporting format is likely to

affect the relation between group identity and employee performance. I first consider groups

with private reporting. Under private reporting, managers provide employees with information

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

21

of their own performance, but not the information of their peers’ performance. That is,

employees do not receive information on the descriptive norms (i.e., the common practice of

other employees) of their group. Therefore, the performance requirements set by the

organization tend to be a more salient performance benchmark than the descriptive norms under

private reporting. Based on the existing theories, group identity may motivate employees to

increase their compliance with the performances requirements in order to reinforce their self-

image as organizational participants and members of their workgroups (Akerlof and Kranton

2000, 2003; Ashforth and Mael 1989; Hogg and Terry 2000). Following the performance

requirements allows employees to demonstrate high performance, as organizations usually

measure employee performance based on the extent to which employees meet the performances

requirements. Therefore, I expect that group identity is positively related to employee

performance under private reporting.

I then consider groups with public reporting. Under public reporting, managers provide

employees with the information on their own and their peers’ performance. That is, employees

can observe the descriptive norms (i.e., common practices of others) of their groups, and are

aware that their own performance can be observed by others in their group. It is unclear how

group identity is related to employee performance under public reporting. On the one hand,

employees with high group identity may still tend to demonstrate high performance, as what

they would do under private reporting. On the other hand, based on management and economic

theories, employees with high group identity may be motivated to conform to the descriptive

norms of their groups. Conforming to the descriptive norms of one’s group increases one’s

similarity with other group members, and reinforces one’s self-image as part of the group

(Akerlof and Kranton 2000, 2003, 2010; Ashforth and Mael 1989; Hogg and Terry 2000).

Further, individuals whose behaviors deviate from the group descriptive norms may receive

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

22

social punishment from other group members (e.g., contempt for low performers, envy for high

performers, social isolation), because such deviation threatens the self-image of other group

members (Akerlof and Kranton 2000; Ashforth and Mael 1989; Charness et al. 2013; Hogg

and Terry 2000; Smith 2000; Vecchio 2000). Employees with high group identity may have

strong motivation to reinforce their self-image as group members and avoid being punished by

others in their group. Therefore, employees with high group identity may choose the group

descriptive norms as the performance benchmark, and adjust their behaviors to become more

similar to others in their group. In other words, under public reporting, employees with high

group identity may increase or decrease their performance to conform to the group descriptive

norms.

Overall, based on group identity theories, I expect that group identity is positively related to

employee performance. However, under public reporting, group identity may motivate some

employees to decrease their performance to conform to the group descriptive norms. Because

of this potential downside of public reporting, I expect that relation between group identity and

employee is more positive under private reporting than under public reporting.

Hypothesis: There is a positive relation between group identity and employee performance;

and the relation is more positive under private reporting than under public

reporting.

2.3 Research Site

Overview

The research site of this study is a large department within a Chinese SOE. The SOE has been

the principal driver of the local economy, and has its own schools, hospitals, media, and

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

23

communities. It comprises 34 factories, plants, and institutions. This study focuses on one

department in a power plant in the SOE. Employees in the department are responsible for

equipment inspection, operation, and maintenance. Tasks include inspecting and operating

equipment, identifying and solving hidden issues, and keeping records of the conditions of the

equipment. The purpose of these tasks is to ensure that the equipment functions normally and

safely, prolonging the usable life of the equipment and reducing the risk of operational disasters.

Each employee’s task and responsibility is clearly specified by the SOE.

As the equipment functions 24/7, employees take shifts. The head of the department divides

employees into five workgroups to make the shifts more manageable. Employees in the same

group work on the same shifts. During each shift, employees work individually in different

areas of the workshops. Once allocated into a group, employees usually stay in the same group,

and a change of groups rarely happens. Each group is managed by a group leader and has 18–

25 group members.

Performance Measurement and Reward System

The SOE uses performance measures and financial incentives to motivate employee

performance. Specifically, employees receive performance scores based on the operational

actions they undertake and the operational outcomes they achieve. The operational actions refer

to the procedures and steps that employees take to inspect, operate, and maintain the equipment.

The operational outcomes include a range of parameters on the equipment, such as temperature

and pressure, which reflect the conditions of the equipment. The organization has specified a

series of performance requirements for operational actions and outcomes. It has also specified

rules about how to allocate performance scores to employees based on the extent to which their

operational actions and outcomes meet the performance requirements. Taking a certain set of

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

24

operational actions that can keep the equipment functioning normally allows employees to earn

a reasonable score. In comparison, inspecting the equipment more carefully, identifying and

solving more hidden issues, and choosing optimal operational actions based on the exact

conditions of the equipment helps employees earn higher scores.

The department manager measures employee performance objectively. In particular, the

department manager assesses employee performance by checking the operational records and

the conditions of the equipment. The operational records are kept by the machines and the

computer system employed by the organization. When taking actions to inspect, operate, and

maintain the equipment, employees must tap their ID cards on the machines in the workshops.

The system then records that the employees have taken certain actions in certain areas of the

workshop. The department manager measures employees’ operational actions by checking the

records kept by the system. Additionally, the department manager measures employees’

operational outcomes by checking the parameters on the equipment during each shift, which

are captured by specialized machines and kept in the system. By the end of every month, each

employee receives performance scores based on the extent to which their operational actions

and outcomes meet the performance requirements specified by the organization.

At the end of every month, employees receive a fixed payment and financial incentives. The

financial incentives are calculated based on the performance scores that employees received

for the month, and account for approximately 0–10% of the overall compensation that they

receive. The performance measurement, score allocation, and compensation structure are pre-

specified by the organization and require little judgment of the manager or group leaders.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

25

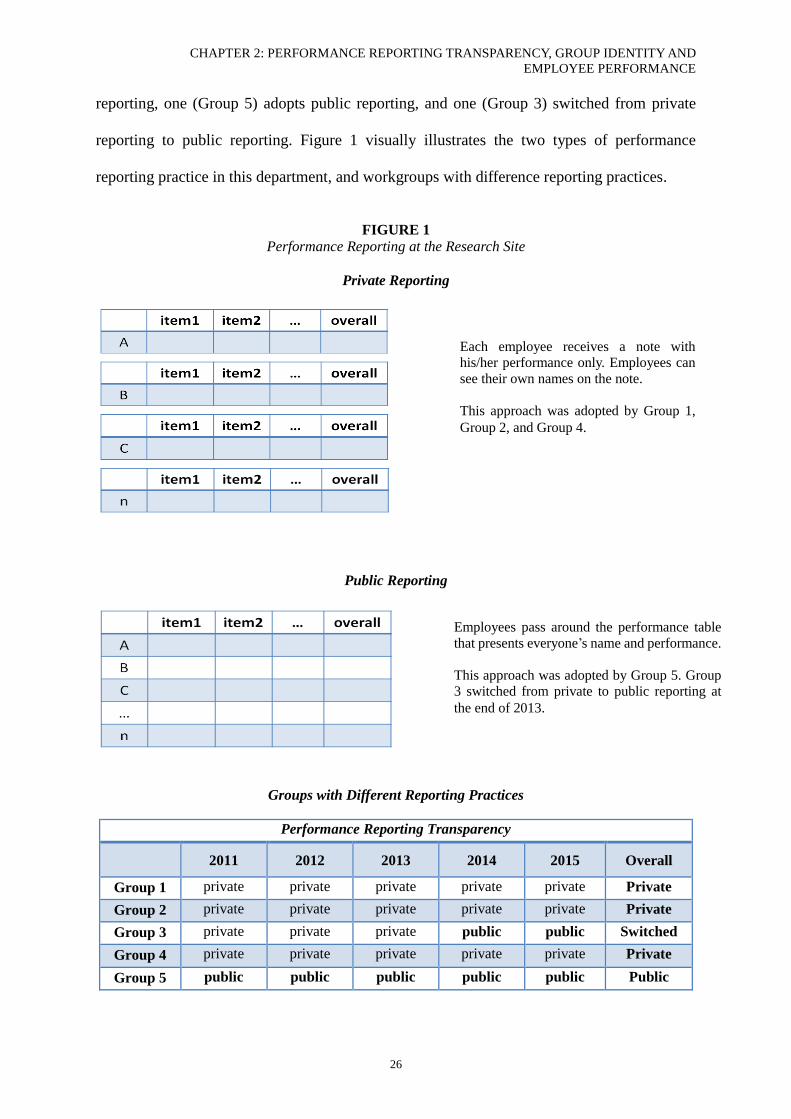

Performance Reporting Transparency

The SOE requires managers to report employee performance so that employees can access the

feedback on their own performance. However, the SOE does not impose strict rules on how

employee performance should be reported in each department or workgroup. In the department

of this study, two types of performance reporting practices have coexisted for years. In one of

the five workgroups (hereafter, Group 5), the group leader prints the names and performance

of all group members on a table, and distributes this performance table to the group members

at the end of every month. Each employee in the group can see their own performance as well

as the performance of their peers (i.e., public reporting). In the other four groups, the group

leaders prepare the same information but print the information on each employee’s

performance in a separate note and only provide each employee with the note that presents his

or her own performance. Employees can only see their own performance and not the

performance of their peers (i.e., private reporting).1

One of the groups (Group 3) switched from private reporting to public reporting at the end of

2013, because the group leader retired and the SOE appointed a new group leader.2 The old

group leader used to print employee performance on A4 paper, cut the paper into pieces, and

gave each employee the piece that contained his or her performance only. The new group leader

asks employees to pass the paper around the group without cutting it.

To sum up, three of the five groups (Groups 1, 2 and 4) in the department adopt private

1 In groups with private reporting, employees in the same group may exchange performance information privately.

When employees have questions or concerns about their performance, they may also request to see the

performance of their peers, in the office of their group leader. Although employees may obtain some information

on their peers’ performance through these channels, the performance transparency in these groups is still lower

than in the group that publicly discloses every employee’s performance. 2 The new group leader was one of the group members in Group 3. The SOE appointed him based on his seniority

(the length of time that he had worked in the SOE) and his leadership potential (subjectively assessed by the

SOE’s upper-level management).

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

26

reporting, one (Group 5) adopts public reporting, and one (Group 3) switched from private

reporting to public reporting. Figure 1 visually illustrates the two types of performance

reporting practice in this department, and workgroups with difference reporting practices.

FIGURE 1

Performance Reporting at the Research Site

Private Reporting

Public Reporting

Groups with Different Reporting Practices

Performance Reporting Transparency

2011 2012 2013 2014 2015 Overall

Group 1 private private private private private Private

Group 2 private private private private private Private

Group 3 private private private public public Switched

Group 4 private private private private private Private

Group 5 public public public public public Public

Each employee receives a note with

his/her performance only. Employees can

see their own names on the note.

This approach was adopted by Group 1,

Group 2, and Group 4.

Employees pass around the performance table

that presents everyone’s name and performance.

This approach was adopted by Group 5. Group

3 switched from private to public reporting at

the end of 2013.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

27

Rationale for the Choice of Research Site

This department is a suitable research site for the following reasons. First, the two types of

performance reporting in the department (public vs. private) provide an opportunity to examine

the research question with the contextual factors controlled. Second, once allocated into a group,

employees usually stay in the same group for years. Employees in the same group work during

the same shift and conduct various activities together (have lunch, take buses, and attend

group/department meetings, etc.). Therefore, employees’ group identity is likely to be salient.

As financial incentives are relatively weak in this setting, group identity is likely to play a

significant role in affecting employee performance. Third, the operating environment in the

department is stable. Because of the rules imposed by the government, the SOE cannot fire its

employees for poor performance. The compensation and other benefits of this SOE are better

than that of other organizations in the local area. Therefore, most employees choose to stay in

the organization and the same workgroup until retirement. The incentive of promotion is low,

as the operating environment is very stable and the group leaders and department managers are

usually appointed directly by the upper-level management team. The stable operating

environment provides an opportunity to examine the same employees’ performance over

multiple periods. It helps mitigate the effects of unobservable factors or other incentives (such

as career concern) that may affect employee performance in certain period(s).

2.4 Method

Data and Sample

In order to examine the research questions, I collected archival and survey data from the

research site. First, I extracted the archival performance data from the database of the SOE.

The SOE measures the individual performance of employees on a monthly basis. I obtained

the performance data from January 2011 to July 2015. The original dataset includes 146

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

28

employees and 5,422 performance observations. Second, I collected the demographic

information of the 146 employees from the personnel files of the SOE, including the employees’

gender, birthday, hometown, education, political affiliation, and recruitment date. Employees’

demographic characteristics are time-invariant. Third, I administered a survey on May 2015 to

measure employees’ perception on their group and the organization, as well as the personal

connections they have in the workplace. I sent the survey to 445 employees in four different

departments of the SOE, including the department of this study. There are 290 employees who

responded the survey (response rate = 65%). In the department of this study, 79 of the 146

employees responded (response rate = 54%).

In the sample selection process, only Group 5 consistently uses public reporting during the

sample period. Therefore, Group 5 is included in the sample to examine the relation between

group identity and performance under public reporting. It means that the groups chosen to

examine this relation under private reporting should be comparable to Group 5, in terms of data

availability and demographic characteristics. Because there was a breakdown in the computer

system of the SOE in early 2015, most observations in Group 1 and 3 are missing. Specifically,

most data for Group 1 (private reporting) is missing, except for that from January to August

2012 and July to October 2014. In Group 3 (switched reporting), the data from August to

December 2013 and the data from June to December 2014 are missing. To minimize any bias

introduced by unobservable factors in particular years or months and make sure data of private

reporting is comparable to the data of public reporting, I exclude these two groups in the

estimation. I include Group 2 and Group 4 in the sample of estimation, as these two groups

consistently use private reporting during the sample period and are not subject to the data

availability issue. The sample selection is described in Table 1.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

29

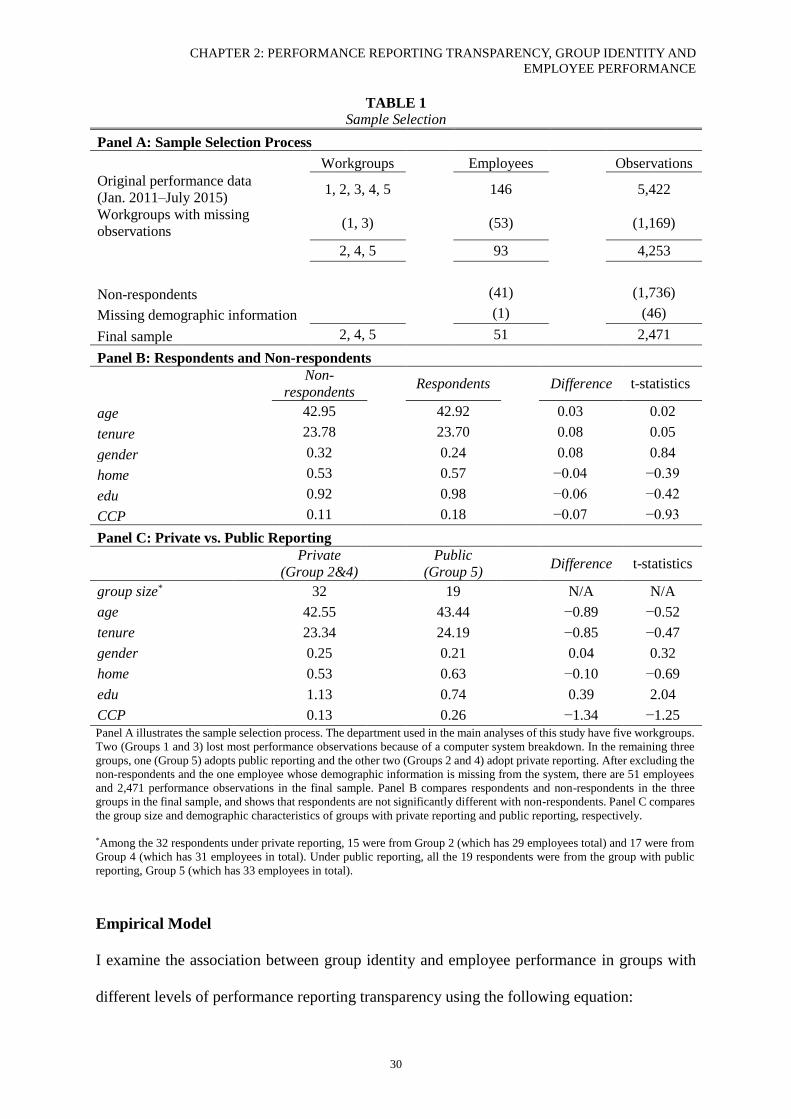

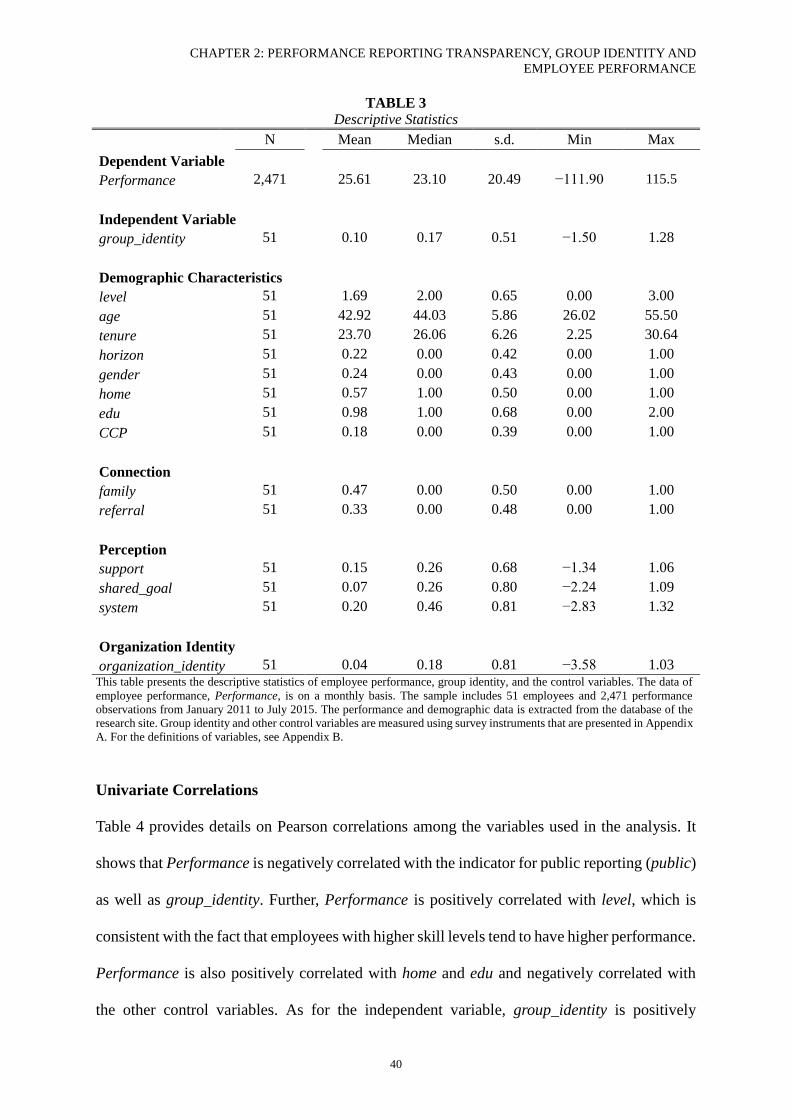

Panel A of Table 1 shows the number of employees and performance observations. The original

dataset on employee performance is from January 2011 to July 2015, and includes all five

workgroups in the department. There are 146 employees and 5,422 performance observations

in total. After excluding the groups with data availability issue, there are 93 employees and

4,253 performance observations left. In the remaining three groups, Group 2 and 4 adopt

private reporting while Group 5 adopt public reporting. After excluding the non-respondents

and one employee whose demographic information is missing in the personnel file, the final

sample includes 51 employees and 2,471 performance observations. Panel B compares

respondents and non-respondents. It shows that respondents are not significantly different with

non-respondents in terms of demographic characteristics. Panel C compares the groups with

private reporting and the group with public reporting. It shows that respondents under private

reporting are not significantly different from those under public reporting in terms of

demographic characteristics, except for the level of education (edu). Specifically, edu is slightly

higher under private reporting than under public reporting (difference = 0.39). This is because

there are five respondents who have master degree in Group 2 (private reporting). In

comparison, Group 4 (private reporting) and Group 5 (public reporting) each has three

respondents with master degree. Given the relatively small size of each group, this small

difference is statistically significant. However, I believe it is unlikely to affect the results

significantly, especially after controlling for employees’ demographic characteristics and the

group fixed effects in the estimation.

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

30

TABLE 1

Sample Selection

Panel A: Sample Selection Process

Workgroups Employees Observations

Original performance data

(Jan. 2011–July 2015) 1, 2, 3, 4, 5 146 5,422

Workgroups with missing

observations (1, 3) (53) (1,169)

2, 4, 5 93 4,253

Non-respondents (41) (1,736)

Missing demographic information (1) (46)

Final sample 2, 4, 5 51 2,471

Panel B: Respondents and Non-respondents

Non-

respondents Respondents Difference t-statistics

age 42.95 42.92 0.03*** 0.02

tenure 23.78 23.70 0.08*** 0.05

gender 0.32 0.24 0.08*** 0.84

home 0.53 0.57 −0.04*** −0.39

edu 0.92 0.98 −0.06*** −0.42

CCP 0.11 0.18 −0.07*** −0.93

Panel C: Private vs. Public Reporting

Private

(Group 2&4)

Public

(Group 5) Difference t-statistics

group size* 32 19 N/A N/A

age 42.55 43.44 −0.89 −0.52

tenure 23.34 24.19 −0.85 −0.47

gender 0.25 0.21 0.04 0.32

home 0.53 0.63 −0.10 −0.69

edu 1.13 0.74 0.39 2.04

CCP 0.13 0.26 −1.34 −1.25

Panel A illustrates the sample selection process. The department used in the main analyses of this study have five workgroups.

Two (Groups 1 and 3) lost most performance observations because of a computer system breakdown. In the remaining three

groups, one (Group 5) adopts public reporting and the other two (Groups 2 and 4) adopt private reporting. After excluding the

non-respondents and the one employee whose demographic information is missing from the system, there are 51 employees

and 2,471 performance observations in the final sample. Panel B compares respondents and non-respondents in the three

groups in the final sample, and shows that respondents are not significantly different with non-respondents. Panel C compares

the group size and demographic characteristics of groups with private reporting and public reporting, respectively.

*Among the 32 respondents under private reporting, 15 were from Group 2 (which has 29 employees total) and 17 were from

Group 4 (which has 31 employees in total). Under public reporting, all the 19 respondents were from the group with public

reporting, Group 5 (which has 33 employees in total).

Empirical Model

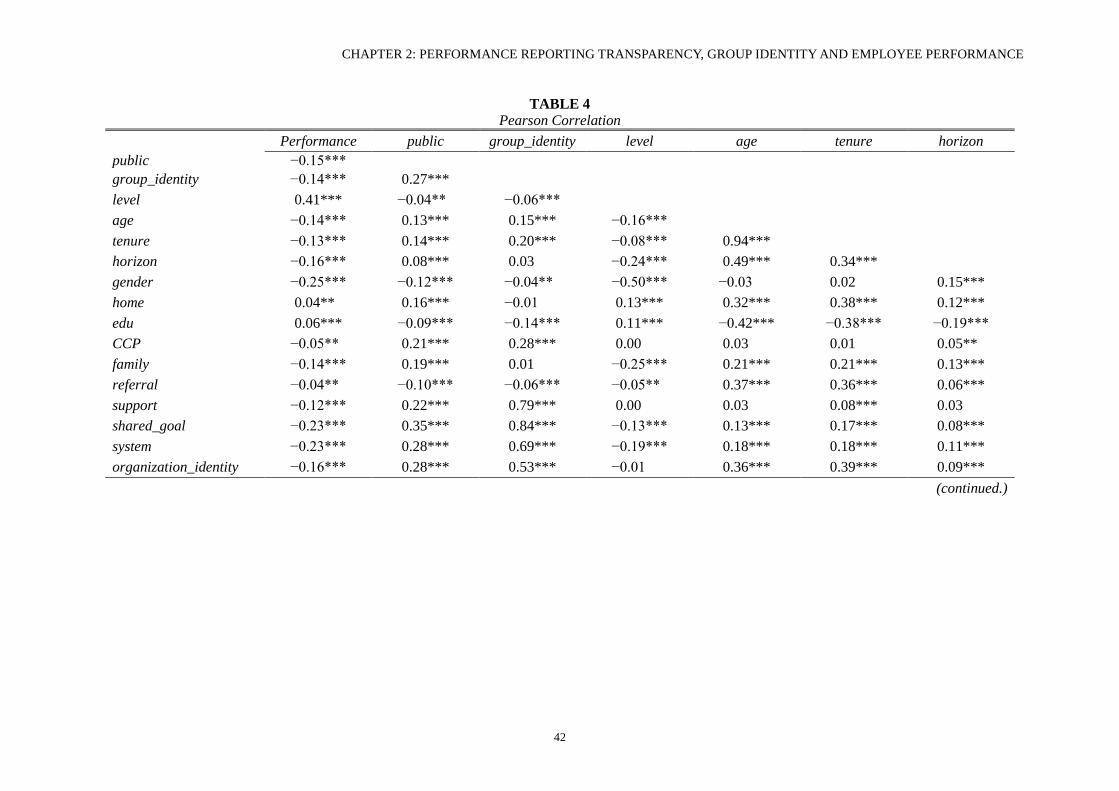

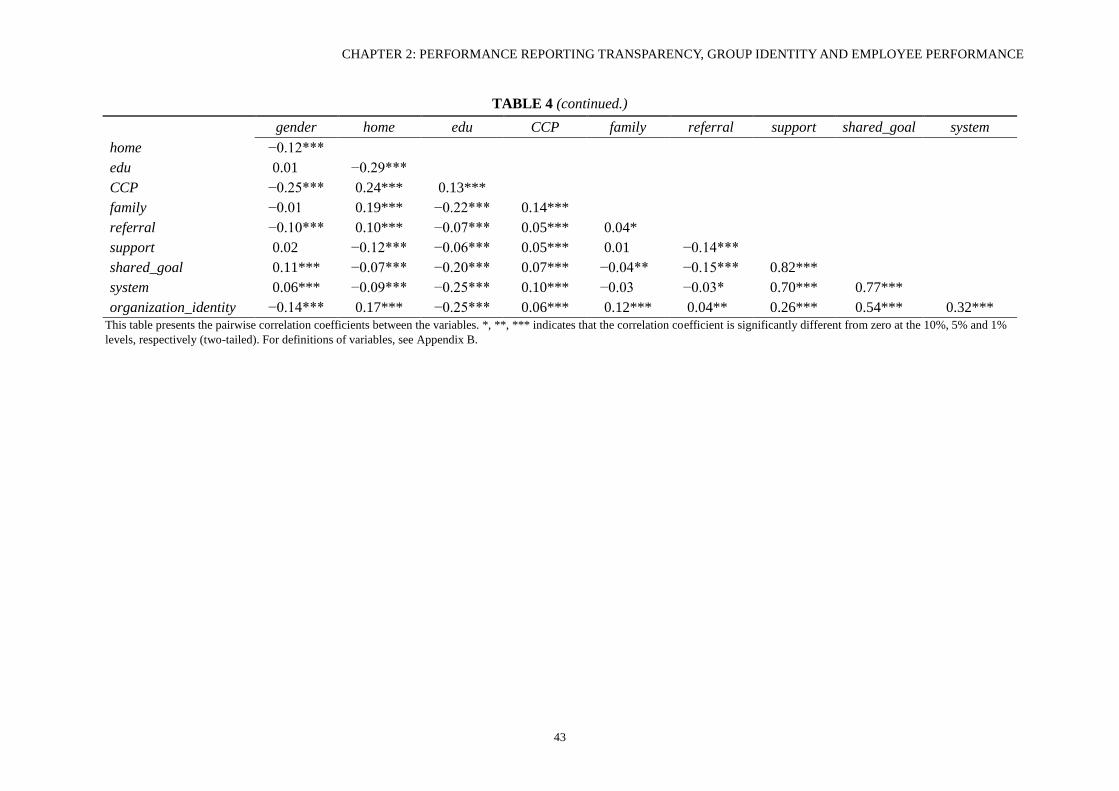

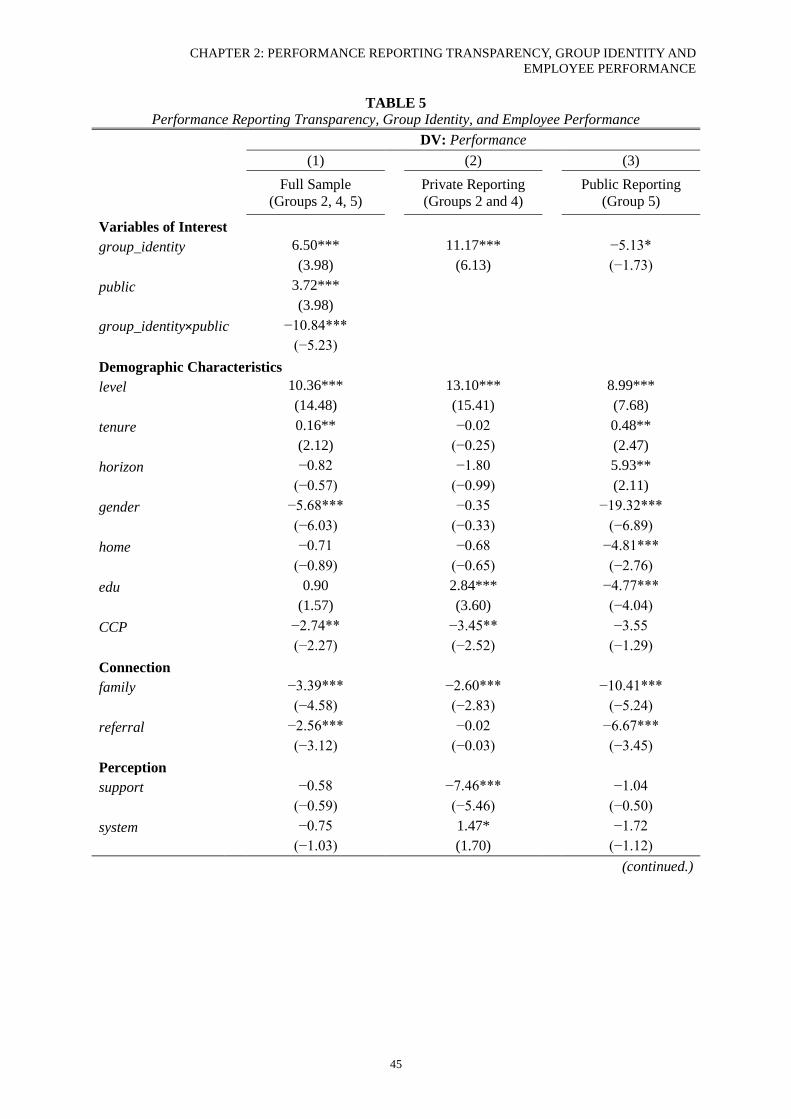

I examine the association between group identity and employee performance in groups with

different levels of performance reporting transparency using the following equation:

CHAPTER 2: PERFORMANCE REPORTING TRANSPARENCY, GROUP IDENTITY AND

EMPLOYEE PERFORMANCE

31

Performanceit = β1group_identityi + β2publicit + β3(group_identityi×publicit) + β4leveli

+ β5tenureit + β6horizonit + β7genderi + β8homei + β9edui + β10CCPi

+ β11familyi + β12referrali + β13supporti + β14systemi + εit (1)

Specifically, I examine the association between employees’ performance (Performance) and

group identity (group_identity) under private reporting and public reporting (public). The

coefficient on group identity (β1) captures the relation between group identity and employee