Embed Size (px)

Citation preview

Market Research Report on

THE INDIAN METAL CUTTING MACHINE

TOOL INDUSTRY

Preface

2

Indian Machine Tool Manufacturers Association (IMTMA) is the apex body of machine tool industry in India . The

association aims to enhance the competitiveness of Indian industry through its various initiatives on productivity,

quality enhancement and technology exposures to Indian machine tool manufacturers and end-users.

As a part of various initiatives IMTMA has commissioned a market research to study the market and technology

adoption levels in cutting technology in Indian market.

In this regard, they have engaged BDB India Private Limited to carry out a Market Research Study to evaluate the

market and technology adoption levels in metal cutting technology in India for the products under the scope of the

study.

The Study has transformed to a detailed report on market dynamics and technology trends in short, medium and

long term for Indian market.

The market forecasting focused on market size estimation, product type wise demand assessment, end user

segment wise share and preference, need gaps and pain areas .

BDB India Private Limited was set up 2 decades ago with the objective of providing world class management inputs

to engineering businesses in India. Today, BDB offer business consulting including market research services to most

market savvy organizations worldwide.

BDB has offered market research inputs for setting up new businesses and in expanding existing ones. BDB has

assisted in identifying new opportunity areas and in evaluating their short, medium and long term commercial

potential. BDB has developed business analysis expertise in industrial products, systems & consumables, consumer

durables and medical equipment.

Continued...

3

BDB also has a division (BDB QSAMM) that assists our customers to analyze and establish customer satisfaction

indices.

BDB specializes in the following :

- Analysis for estimating the market size and potential

- Technology and emerging trends

- Competition analysis

- Distribution channel analysis

- Market entry strategies

- Partner identification

The study has been successfully completed and its output is being presented in the form of this report.

The findings of the study are presented in this report, and its contents are strictly confidential and meant for

the exclusive use of IMTMA.

The statements and analyses in this report are based on the information and opinion obtained during field

investigations and from various published sources.

Contents

4

Page No

Preface

CHAPTER 1 PROJECT BACKGROUND 5

Objectives of the study 6

Scope of the study 7

CHAPTER 2 EXECUTIVE SUMMARY 11

CHAPTER 3 CONCLUSIONS 42

CHAPTER 4 PRODUCT WISE ANALYSIS 48

Electric discharge machines 49

Turning centers 59

Machining centers 84

Milling machines 108

Grinding Machines 120

Tool grinding machines 131

SPMs 142

CHAPTER 5 TRENDS IN THE END USER SECTORS 150

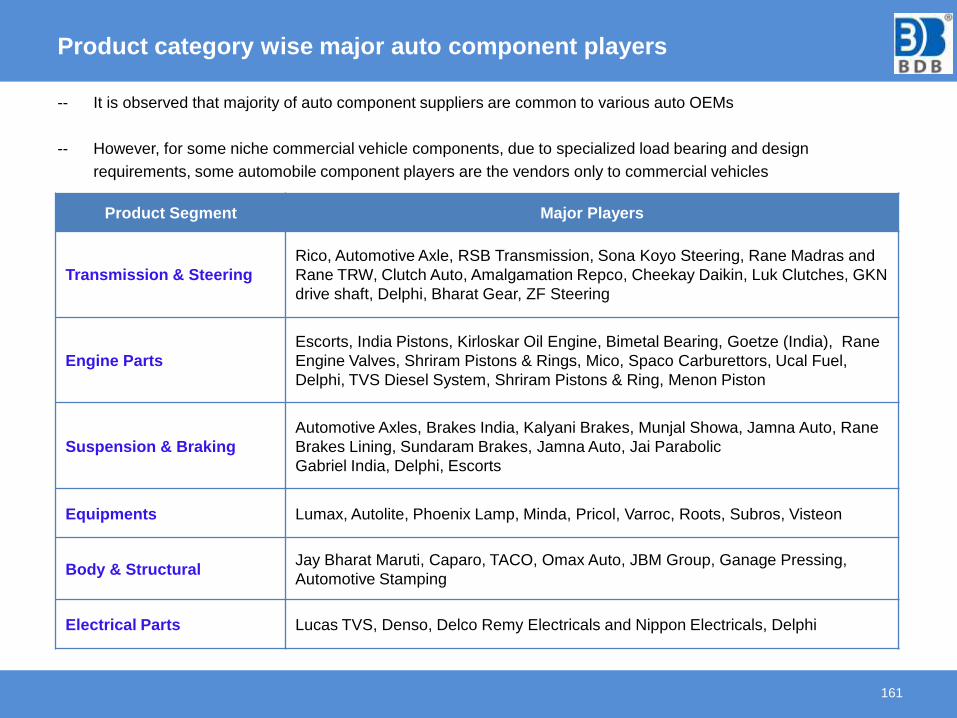

Automotive 151

Auto components 157

General Engineering 165

Heavy Engineering 170

Aerospace & Defence 176

Die & Mould 182

APPENDIX

1. PROJECT BACKGROUND

- OBJECTIVES OF THE STUDY

- SCOPE OF THE STUDY

Objectives of the study

6

aa Market size estimation for Metal cutting machines and category wise forecast

of demand on short, medium and long term basis.

bb To report on sector wise demand for metal cutting machines and trends related

to adoption of efficient technologies

cc To project the demand over the next 5 years based on the growth of the end

user sectors

dd To report on competitiveness of Indian Machine Tool Industry and recommend

key areas of improvement, end user perceptions on Indian suppliers and

technology gaps

ee To develop a detailed report to guide Indian machine tool manufacturers about

the road map of the industry and enable members to take informed decisions

Scope of the study

7

aa Product categories under focus

Metal Cutting Machines

- CNC Turning centers, Conventional Lathe Machines, Vertical Machining Centers,

Horizontal Machining Centers, Grinding Machines, EDMs, SPMs and Tool

Grinding Machines

bb Geographical regions under focus

India

- Prominent manufacturers, end users and institutions & manufacturing clusters

relevant to the study have been contacted to understand their views and

perception on market

Products Covered under metal cutting machines

Product Description Product Covered

Metal Cutting Machines

EDMs √

CNC Turning Centers √

Conventional Lathe Machines √

Vertical Turning Center √

Vertical Machining Centers √

Horizontal Machining Centers √

Milling Machines √

Grinding Machines √

Tool Grinding Machines √

Heavy Machineries √

SPMs √

8

Heavy machineries category has been considered under milling machines and SPMs

Study Methodology

9

The study was carried out with a multi pronged approach involving stakeholders like

end users, domestic manufacturers of machine tool, importers, component suppliers

key industry bodies and industry experts of the user industries.

Analysis regarding the total market potential and the product wise trends were sourced

from the domestic manufacturers, importers and import export data. Where as

discussions with end users were carried out to understand types of machinery used,

source, technology trends prevailing and the growth potential of the metal cutting

machinery based on their growth trends. The end users provided the vital inputs which

led to analyzing their buying behaviour.

A detailed analysis of the customs data on imports was carried out to understand the

extent of machine tool imports into the country and sources for such procurement;

information pertaining to imports of new and used machines were separately analyzed

to arrive at meaningful inputs for the industry.

A representative sample of stakeholders has been included in key demand and

manufacturing clusters covering companies from small, medium and large scale

categories.

Discussions with various stake holders were carried out through an intensive primary

research exercise involving personal meeting between BDB analysts and respondents.

Market Forecasting : Approach

10

Approach - Overview

Methodology :

Last 10 years historical data on metal cutting machinery

consumption, macro economic indicators and respective

user sector growth has been mapped

The forecast for the macro economic indicators and user

sector growth has been developed based on the economy

and industry reports and discussions with end users

Correlation between macro economic indicators, end user

sector growth and metal cutting machinery consumption

has been used to forecast the projected consumption of

metal cutting machinery

The results have been corroborated with manufacturers

and component suppliers based on their judgment and

experience

Important factors that could cause actual

results to differ from our expectations include,

among others:

-- Changes in political and social conditions in

India;

-- Extraordinary changes in monetary & fiscal

policies of the Government of India, inflations,

foreign exchange rates, unanticipated

turbulence in interest rates;

-- The performance of the financial markets in

India and globally;

-- Occurrence of natural disasters or calamities

affecting the economy

Assumptions :

Growth in metal cutting machinery is proportional to the user industry growth

Absence of any major technological change in machining amongst the user industry

No major change in the value of the metal cutting machinery currently used

2. EXECUTIVE SUMMARY

Overview of Indian Economy

12

8.6% 9.3%

6.2%5.0% 4.7%

11.3%9.7%

2.7%

1.0% 1.0%

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014

India GDP Growth (%) Manufacturing GDP Growth (%)

The performance of the Indian economy over

the past two years especially the

manufacturing output has been

disappointing.

The recessionary pressure of 2012-13 have

severely impacted the industrial activity within

India.

The Index of industrial production has seen a

negative growth predominantly due to the

slowdown in the manufacturing sectors

A large current account deficit, high domestic

inflation and a fiscal stance that was widening

compounded the problems facing the

economy

Low growth and weak business confidence

feed into each other in a negative feedback

loop

However the economy is expected to recover

and see a GDP growth of around 5.7% for the

year FY 2015 (2014 - 2015)

152.9

165.5

170.3172.2

166.55%

8%

3%

1%

-3%

-4%

-2%

0%

2%

4%

6%

8%

10%

140.0

145.0

150.0

155.0

160.0

165.0

170.0

175.0

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 (Apr - Nov)

Index of Industrial production (IIP) IIP Growth (%)

Source : Central Statistics Office, World Bank

Source : Department of Economic Affairs

FY 2010 indicates 2009-2010

Overview of Indian machine tool industry

13

India is the 16th largest manufacturer of machine tools in the world as per Gardner’s world consumption report 2013.

The Indian machine tool industry consists of around1000 manufacturing units covering large, medium and small

companies. Domestic manufacturers account for about 36% of consumption within the Indian machine tools market.

Since 2002, the Indian engineering sector especially the auto and auto ancillary sector has witnessed increased

investments as global engineering giants have started outsourcing from India and have started to establish their

manufacturing facilities based in India. This led to a spurt in demand for machine tools in India. Now the Indian machine

tool industry is in a position to export the general purpose and standard machine tools to even industrially advanced

countries.

The recessionary pressure of 2012-13 have severely impacted the industrial activity within India.

Decline in turnover is due to the slowdown of industrial activity in the country particularly in the

automotive, infrastructure, heavy engineering and construction industries as a result the growth of the Indian machine

tools industry was hampered. However the recent revival in the index of industrial production can be construed as a

harbinger of growth for the Indian machine tools industry.

Indian Machine Tool Industry Journey

14

Post war to independence

Start of the ‘Planned Economy’

Cooper, Scottish India, ABMTM, Kirloskar etc

Louden, Ward, Herbert, Jones + Shipman Entry of First Wave of Foreign Technology

Share of Indian Machine Tool Industry ~ 51 %

1950s

1953, Birth of HMT. Oerlikon Tie up

Start of era of severe shortage of Foreign Exchange

Emphasis on Import Substitution

Share of Indian Machine Tool Industry ~ 17 %

1960s

Era of Collaborations – HMT-Peggard, PMT - Traub, Cooper – Pfanter

Horizontal Expansion in Product Range

Version Presses (HMT), Gear Cutting Machines (Premier + HMT) SPMs’ (XLO)

Birth of Ancillaries

Dominant public sector

Highly Protected. Tariff (>85%) and non Tariff barriers

Share of Indian Machine Tool Industry ~ 62 %

1970s

Start of Technology Denial Regime, Post Pokhran I

Era of Joint working arrangements – Defence Sector major buyer. Praga-Mitsubishi, LMW –

Mori Seiki, Cooper – Hitachi, PMT – Voumard, Mysore Kirloskar, Murata Warner & Swassey

Emergence of First OGL List (Only Machine Tool items). Start of declining Non Tariff Barriers

Era of Technocrats - Ace Designers, Parishudh Machines, Micromatic Grinding, Pragati,

Lokesh etc

Share of Indian Machine Tool Industry ~ 77 %

1980s

Over Diversification - Severe Technology Denial regime sets in, Post Pokhran II

Long tailed Industry structure (20% of companies produced 80% of Machine Tools)

No major investment by Machine Tool Manufacturers

Over Protected & uncompetitive - Peak Custom Duty rate mounts to 150% in 1991, Emergence

of new, adventurous Entrepreneurs: Galaxy, Jyoti, Askar Mikrons

Share of Indian Machine Tool Industry ~ 71 %

Indian Machine Tool Industry Journey

15

1990s

Advent of Open Market Economy, Era of high GDP Growth

Volume production of Standard CNC machine Tools. Rise of Auto Sector, Declining Custom

Duty Protection, Lowering of Entry Barriers

Fall of HMT from numero uno, demise of Public Sector dominance

Poor development of Sub Contract Structure

Technology Transfer route dries up, Demise of Joint Ventures

Indian Share falls dramatically to 34 % from 66 %

Post Y2K

Globalization – Jyoti / Huron, Batliboi / Quickmil, BFW / Matec, Ace / China

High Growth (20 -30%), Capacity Build up, scaling up, More of the same

Invasion of Foreign companies through – Sales & Service Centres, Tech Centres, Assembly

outfits

Indian share falls to 20%, recovers to ~ 30%.

Company 1993 – 94 (Rank) 2011 – 12

HMT 1 Ace Designers

Mysore Kirloskar * 2 BFW

BFW 3 PMT

Electronica 4 AMS

Telco (MTD) * 5 LMW

LMW 6 HMT

Batliboi 7 ISGEC

Premier 8 Prmier

Godrej * 9 MGTL

PMT 10 KENNAMETAL

Praga ** 11 Electropneumatics

Electropneumatics 12 Electronica Machine Tools

ISGEC 13 ITL

Ace Group 14 TAL

Ema India * 15 Batliboi

Start of second decade

of new millennium

In 2000, India was 18th in

Production and in

2012, India ranked 13th in

the world

In 2000 India was 11th in

consumption, In 2011 India

was ranked 7th

Indian Machine Tool

Industry’s impressive

growth in the new

millennium has not

allowed it to be among top

5 machine tool producers

in the world

* As on today these companies not in Machine Tools business

** Praga is merged with HMT

Overview of metal cutting machines in India

16

The current market size of the metal cutting industry stands at INR 6750 crores, off which the domestic

production makes for around 45% of the total consumption.

The Indian players have grown rapidly over the last ten years and now have their presence across all

product categories.

High value machines dominate the import market.

There are three major clusters of countries from which India imports machines:

-- Spain and Switzerland forming the high average value, low volume segment;

-- Japan, Germany, Italy and South Korea primarily operating in the high to medium

value, high volume segment;

-- China, Taiwan and USA forming the low value high volume segment.

India imports four critical components viz., CNC systems, ball screws, precision bearings and LM

guides which makes for around 40% of the total cost of a typical CNC Machine tool. India also imports

other major sub systems like , APC’s, Rotary indexing tables, motorized spindles etc.

Additionally, lack of development in high precision, multi-axes machines is currently hindering the rapid

growth in key strategic industries such as the nuclear and defense sectors. Due to India not being a

signatory to the NPT and CTBT, it cannot import these machines and hence it is imperative for the

country to develop these technologies at the earliest.

The consumption in this industry is primarily driven by the automobile sector which accounts for nearly

40% of the market, die and mould and industrial machinery are the other key user sectors in this

industry.

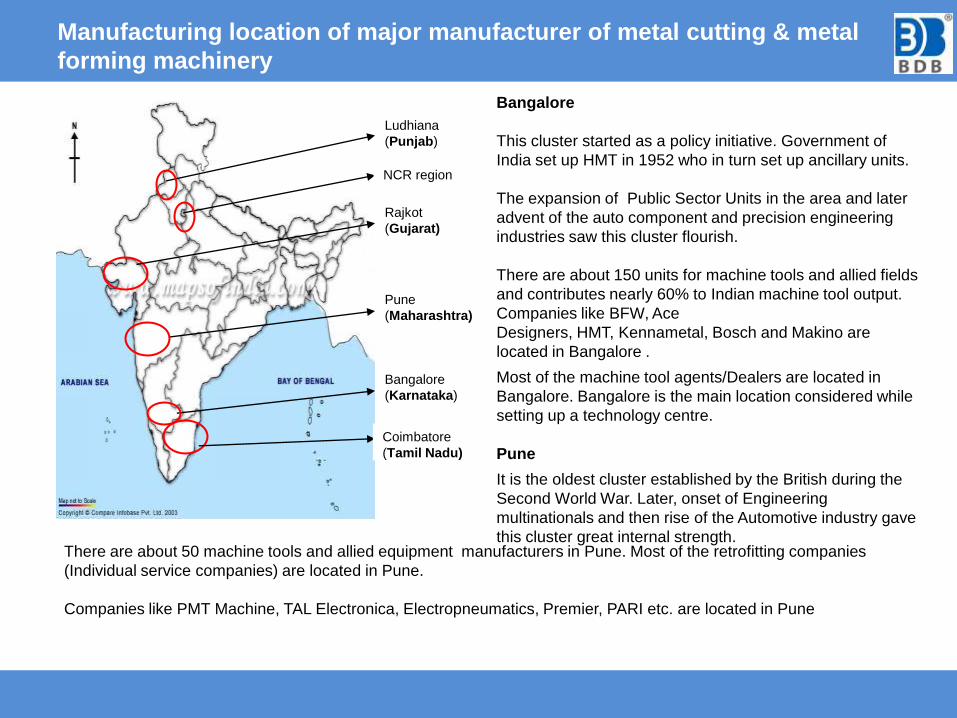

Manufacturing location of major manufacturer of metal cutting & metal

forming machinery

Ludhiana

(Punjab)

Rajkot

(Gujarat)

Pune

(Maharashtra)

Bangalore

(Karnataka)

Coimbatore

(Tamil Nadu)

Bangalore

This cluster started as a policy initiative. Government of

India set up HMT in 1952 who in turn set up ancillary units.

The expansion of Public Sector Units in the area and later

advent of the auto component and precision engineering

industries saw this cluster flourish.

There are about 150 units for machine tools and allied fields

and contributes nearly 60% to Indian machine tool output.

Companies like BFW, Ace

Designers, HMT, Kennametal, Bosch and Makino are

located in Bangalore .

Most of the machine tool agents/Dealers are located in

Bangalore. Bangalore is the main location considered while

setting up a technology centre.

Pune

It is the oldest cluster established by the British during the

Second World War. Later, onset of Engineering

multinationals and then rise of the Automotive industry gave

this cluster great internal strength. There are about 50 machine tools and allied equipment manufacturers in Pune. Most of the retrofitting companies

(Individual service companies) are located in Pune.

Companies like PMT Machine, TAL Electronica, Electropneumatics, Premier, PARI etc. are located in Pune

NCR region

Continue...

Rajkot

Traditionally a centre of turned parts, the cluster grew due to high demand from diesel engine industry. For long

languishing as craftsmen, Rajkot is at the nascent stage of the genuine engineering phase. Rajkot has emerged as the

second largest base for manufacture of CNC machine tools after Bangalore and overtaking Pune. Jyoti and

Manpower CNC Machines are the most prominent suppliers based in Rajkot.

NCR:

NCR is a cluster with a few large companies like ISGEC, Micromatic, Parishudh, SRB Hindustan Hydraulics etc.

Ludhiana

This cluster was developed as a natural cluster. Craftsmanship and reverse engineering capabilities coupled with

demand from a thriving bicycle and hand tool manufacturing segments, the cluster grew rapidly.

Dotted with tiny units, the cluster has around 400 units covering nearby areas such as Jalandhar and Batala producing

low end workshop machinery for small and tiny sectors and providing limited service (mechanical service, repair etc.)

Marshall machines and Rattan Hammers are the most prominent suppliers in this region.

Coimbatore

Essentially a domain of a few large companies, this is a modern cluster with high standards in Quality & Technology.

Around 20 companies represent this close knit cluster which caters to automotive sector mainly. LMW is located in

Coimbatore

Market demand of metal cutting machines in India for FY 2012 - 13

19

Total market demand of products under study for

FY 2012 - 13INR 6650 - 6870 Cr

Product NameTotal Market

(In Units)

Total Market

(In Rs Cr)

Turning Centers 7600 - 7800 1800 - 1825

Vertical Machining Centers 3750 - 3850 1360 - 1400

Horizontal Machining Centers 760 - 800 1125 - 1145

Grinding Machines 2700 - 2740 920 - 940

Milling Machines * 3210 - 3330 495 - 530

SPMs 320 - 340 360 - 400

Lathes* 2100 - 2150 365 - 385

EDMs 680 - 730 125 - 135

Tool Grinding machines 350 - 380 100 - 110

Total 21,470 - 22,120 6650 - 6870

Product wise estimated market for FY 2012 - 13 Product wise estimated market for FY 2012 - 13

21,470 - 22,120 6650 - 6870

Note : Market size indicates the total consumption in

India (Imports + Production – Exports)

Source : DGFT & BDB Analysis

Turning centers & Machining centers contribute to

60- 70% of the total market for metal cutting machines

35%27%

17%21%

4% 17%13%

14%15%

7%1%5%10%6%

In Units In Rs Cr

Turning Centers VMCs

HMCs Grinding Machines

Milling Machines SPMs

Lathes EDMs

Tool Grinding machines

3%5%

In the milling and lathes segment the study has only considered the organized

market and the light duty machines manufactured by the unorganized segment is

excluded from the analysis

5%

24%17%

22%18%

17%

10%

13%29%

12%16%

7%

In Units In Rs Cr

HMCs Turning Centers

Grinding Machines VMCs

Milling Machines Lathes

SPMs EDMs

Tool Grinding machines

52%

34%

25%

30%

8%

10%

2%9%

2% 9%5%3%

In Units In Rs Cr

Turning Centers VMCsGrinding Machines SPMs HMCs LathesEDMs Tool Grinding machines Milling Machines

Market demand of metal cutting machines in India for FY 2012 - 13

20

Domestic Contribution for FY 2012-13 Import Contribution for FY 2012-13

Total market demand for metal cutting machines in India (in Units) : 21,470 - 22,120

Total market demand for metal cutting machines in India (in Rs Cr) : 6650 - 6870

11,710 - 11980 3020 - 3115 9760 - 10,140 3630 - 3755

Domestic manufacturers have a significant share in turning centers, vertical machining centers and Grinding Machines

Imports are dominated by horizontal machining centers, turning centers, grinding machines, vertical machining centers and

milling machines because of the more complex nature of the machines

6%9% 4%4.5%

Source : DGFT

Product wise domestic vis-à-vis import contribution for FY 2012-13

21

1800 - 1825 1360 - 1400 1125 - 1145 920 - 940 495 - 530 360 - 400 365 - 385 125 - 135 100 - 110

Total market for metal cutting machines in India (in Units) : 21,470 - 22,120

Total market for metal cutting machines in India (in Rs Cr) : 6650 - 6870

Source : DGFT & BDB Analysis

Indian Manufacturers have strong market presence in Turning Centers, VMCs, EDMs and SPMs;

however, product categories such as HMCs, Milling Machines and Grinding Machines are being imported in

high volumes

56%66%

23%32%

9%

78%

26%

63% 60%

44%34%

77%68%

91%

22%

74%

37% 40%

Turning Centers

VMCs HMCs Grinding Machines

Milling Machines

SPMs Lathes EDMs Tool Grinding machines

Domestic Import

Total Market

in

Rs Cr

52%

34%

25%

30%

8%

10%

2%9%

2% 9%5%3%

In Units In Rs Cr

Turning Centers VMCs

Grinding Machines SPMs

HMCs Lathes

EDMs Tool Grinding machines

Milling Machines

Domestic sale of metal cutting machines for FY 2012-13

22

Product

Domestic sales

In Units In Rs Cr

Turning Centers 5900 - 6000 1010 - 1020

VMCs 2800 - 2850 900 - 920

Grinding Machines 930 - 950 295 - 305

SPMs 270 - 280 280 - 300

HMCs 260 - 280 255 - 265

Lathes 510 - 530 95 - 105

EDMs 490 - 510 80 - 85

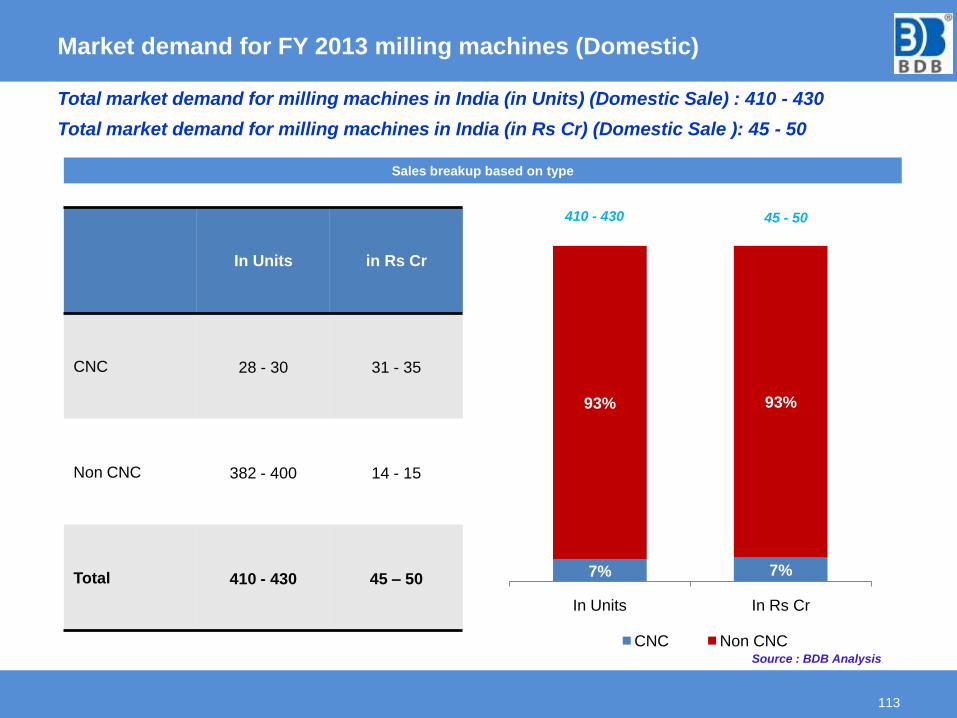

Milling Machines 410 - 430 45 - 50

Tool Grinding machines 140 - 150 60 - 65

Total 11,710 - 11,980 3020 - 3115

Total domestic sale of metal cutting machines (in Units) : 11,710 - 11,980

Total domestic sale of metal cutting machines (in Rs Cr) : 3020 - 3115

11,710 - 11,980 3020 - 3115

Source : BDB Analysis

6%9%

Major domestic manufacturers by product category

23

ProductProduction in Rs Cr

FY 2013Major Manufacturers

Turning Centers 1050 - 1070 Ace Designers, HMT, Jyoti CNC, LMW, Lokesh

VMCs 940 - 970Ace Manufacturing System, BFW, HMT, Jyoti CNC, Lokesh,

LMW, TAL

Grinding Machines 309 - 323Alex Machine Tools, HMT, Micromatic Grinding

Technologies, Parishudh Machine Tools, PMT Machine

Tools

SPMs 280 - 300Batliboi, BFW, Bosch, Esskay, HMT, Kennametal, Lokesh,

TAL

HMCs 269 - 283Ace Manufacturing System, BFW, HMT, Jyoti CNC, LMW,

Lokesh, TAL

Vertical Turning Centers 95 - 100 Ace Designers, BFW, Lokesh, TAL

Lathes 95 - 105 Askar, HMT, PMT

EDMs 82 - 89 Concord, Electronica

Tool Grinding Machines 60 - 65 HMT, Kennametal, TGT

Milling Machines 45 - 50 BFW, Batliboi, HMT

5%

24%17%

22%18%

17%

10%

13%29%

12%16%

7%

In Units In Rs Cr

HMCs Turning Centers

Grinding Machines VMCs

Milling Machines Lathes

SPMs EDMs

Tool Grinding machines

Import of metal cutting machines for FY 2012-13

24

Product

Import

In Units In Rs Cr

HMCs 500 - 520 870 - 880

Turning Centers 1700 - 1800 790 - 805

Grinding Machines 1770 - 1790 625 - 635

VMCs 950 - 1000 460 - 480

Milling Machines 2800 - 2900 450 - 480

Lathes 1590 - 1620 270 - 280

SPMs 50 - 60 80 - 100

EDMs 190 - 220 45 - 50

Tool Grinding machines 210 - 230 40 - 45

Total 9760 - 10,140 3630 - 3755

Total Import of metal cutting machines in India (in Units) : 9760 - 10,140

Total Import of metal cutting machines in India (in Rs Cr) : 3630 - 3755

5%5%

Source : DGFT

9760 - 10,140 3630 - 3755

Country wise import of metal cutting machines for FY 2012-13

25

CountryTotal Market

(In Rs Cr)

Japan 1165 - 1207

Germany 500 - 518

Korea 385 - 400

Taiwan 357 - 364

Italy 220 - 230

China 168 - 170

USA 175 - 185

UK 50 - 51

Others 610 - 630

Total 3630 - 3755

3330 - 3395 300 - 360

Others include countries like Singapore, Switzerland, Romania, Thailand, Poland, France, Sweden, Spain etc

Source : DGFT

33%

18%

13%

19%

11%

4%

10%

3%

5%

14%

5%

1%

5%

9%

1%

5%

16%26%

New Used

Japan Germany Korea Taiwan Italy

China USA UK Others

Total Import of metal cutting machines in India (in Units) : 9760 - 10,140

Total Import of metal cutting machines in India (in Rs Cr) : 3630 - 3755

Product wise - Country wise import of metal cutting machines for

FY 2012-13

26

Source : DGFT

Total import of metal cutting machines in India (in Units) : 9760 - 10,140

Total import of metal cutting machines in India (in Rs Cr) : 3630 - 3755

870 - 880 790 - 805 210 - 220 460 - 480 625 - 635 450 - 480 80 - 100 45 - 50 40 - 45Import in

Rs Cr

63%

19%

2%

40%

15% 15%

67%

10% 12%

19%

10%

8%

16%

10%15%

6%

5%

17%

8%

22%

25%

2%

14% 2%

1%

10%

20%

4%35%

3%

3%

14%

3%

1%

8%

8%

9%

1%

16%

1%

8%

6%

1%

5%

21%

25%

2%

5%

6%

3%7%

14%

1%

1%

14%

1% 6%

1%

3%

7%

17%25%

15% 17%

1%

45%49%

HMCs Turning

Centers

VTLs Grinding

Machines

VMCs Milling

Machines

SPMs EDMs Tool Grinding

Machines

Japan Germany Korea Taiwan Italy China USA UK Others

27

ProductMarket demand in

Rs Cr for FY 2013Major Manufacturers

HMCs 870 - 880Komastu NTC, Makino, Mazak, DMG, Mori seiki, MAG, Heller,

Doosan

Turning Centers 790 - 805 Mazak, Doosan, Hyundai, Takisawa, DMG

Grinding Machines 625 - 635 Cincinnati, Kent, Izumi, TOYODA, KOYO

VMCs 460 - 480 Makino, Mazak, FEELER, DMG, HAAS

Milling Machines 450 - 480 Manford, WMW, Saimp, Kent

Lathes 270 - 280Some of the brands observed are Tornos, Takisawa, WMW,

Daewoo, Esteem, Moriseiki

Vertical Turning Centers 210 - 220YOU Ji, Titan TMG Machine Tools, Hwachion, EMAG, Hyundai,

Komatsu

SPMs 80 - 100 Not Available

Tool Grinding Machines 40 - 45 Anca, Deckel, Walter, China Manufactures

EDMs 45 - 50 Sodick, Makino, AGIE CHARMILLES, MITSUBISHI, Chmer

Major imported brands by product category

Segment wise contribution for metal cutting machines for FY 2012-13

28

SegmentTotal Market

(In Rs Cr)

Auto Component 1645 - 1700

General Engineering 1150 - 1190

Auto OEM 970 - 999

Heavy Engineering 635 - 655

Defence & Aerospace 395 - 410

Die & Mould 365 - 375

Railway 105 - 110

Others 1385 - 1430

Total 6650 - 6870

Other segments include construction & mining, electronics, steel, forging, ship building and consumer durables

(Heavy Engineering - Turbines, Boiler, Power & energy, textile machinery, cement machinery, sugar machinery etc.

General Engineering - Pumps, Compressors, Valves, Motors etc)

Source : BDB Analysis

Total market for metal cutting machines in India (in Units) : 21,470 - 22,120

Total market for metal cutting machines in India (in Rs Cr) : 6650 - 6870

25%

17%

15%

9%

6%

5%

2%

21%

Auto Component General Engineering Auto OEM

Heavy Engineering Defence & Aerospace Die & Mould

Railway Others

Segment wise contribution for metal cutting machines for FY 2012-13

(Domestic Manufacturers)

29

Domestic manufacturers : As a percentage of total market in Rs Cr

Source : BDB Analysis

42%

43%

41%

35%

35%

10%

30%

10%

18%

22%

22%

25%

25%

20%

25%

15%

20%

10%

19%

21%

21%

5%

10%

10%

3%

11%

7%

2%

2%

5%

12%

15%

6%

4%

2%

1%

1%

20%

10%

15%

11%

10%

9%

16%

16%

30%

13%

35%

Turning Centers

VMCs

HMCs

Grinding Machines

Tool Grinding Machines

EDMs

SPMs

Milling Machine

Auto OEM Auto Component General Engineering Heavy Engineering Defence & Aerospace Others

30

Segment wise contribution for metal cutting machines for FY 2012-13

(Import)

Import : As a percentage of total market in Rs Cr

Source : BDB Analysis

8%

8%

10%

35%

20%

10%

30%

10%

14%

12%

20%

25%

14%

20%

25%

15%

17%

12%

35%

21%

26%

5%

10%

10%

5%

15%

20%

2%

7%

5%

12%

15%

25%

25%

5%

1%

9%

20%

10%

15%

10%

16%

14%

30%

13%

35%

Turning Centers

VMCs

HMCs

Grinding Machines

Tool Grinding Machines

EDMs

SPMs

Milling Machine

Auto OEM Auto Component General Engineering Heavy Engineering Defence & Aerospace Others

38%

31%

28%

13%

-1%

-41%

42%

30%

-1%

-0.455

-0.45

-0.445

-0.44

-0.435

-0.43

-0.425

-0.42

-0.415

-0.41

-0.405

-0.4

-0.395

-0.39

-0.385

-0.38

-0.375

-0.37

-0.365

-0.36

-0.355

-0.35

-0.345

-0.34

-0.335

-0.33

-0.325

-0.32

-0.315

-0.31

-0.305

-0.3

-0.295

-0.29

-0.285

-0.28

-0.275

-0.27

-0.265

-0.26

-0.255

-0.25

-0.245

-0.24

-0.235

-0.23

-0.225

-0.22

-0.215

-0.21

-0.205

-0.2

-0.195

-0.19

-0.185

-0.18

-0.175

-0.17

-0.165

-0.16

-0.155

-0.15

-0.145

-0.14

-0.135

-0.13

-0.125

-0.12

-0.115

-0.11

-0.105

-0.1

-0.095

-0.09

-0.085

-0.08

-0.075

-0.07

-0.065

-0.06

-0.055

-0.05

-0.045

-0.04

-0.035

-0.03

-0.025

-0.02

-0.015

-0.01

-0.005

2E-17

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

0.045

0.05

0.055

0.06

0.065

0.07

0.075

0.08

0.085

0.09

0.095

0.1

0.105

0.11

0.115

0.12

0.125

0.13

0.135

0.14

0.145

0.15

0.155

0.16

0.165

0.17

0.175

0.18

0.185

0.19

0.195

0.2

0.205

0.21

0.215

0.22

0.225

0.23

0.235

0.24

0.245

0.25

0.255

0.26

0.265

0.27

0.275

0.28

0.285

0.29

0.295

0.3

0.305

0.31

0.315

0.32

0.325

0.33

0.335

0.34

0.345

0.35

0.355

0.36

0.365

0.37

0.375

0.38

0.385

0.39

0.395

0.4

0.405

0.41

0.415

0.42

0.425

0.43

0.435

0.44

0.445

0.45

0.455

0.46

0

1000

2000

3000

4000

5000

6000

7000

8000

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08 FY 08-09 FY 09-10 FY 10-11 FY 11-12 FY 12-13

INR

Cr

Market demand growth trend of metal cutting machines industry in India

31

1072

1734

2496

3468

3966

3932

2783

6788

4767

6738

The recessionary pressure of 2009-10 & 2012-13 have severely impacted the industrial activity within India.

Decline in turnover is due to the slowdown of industrial activity in the country particularly in the

automotive, infrastructure, heavy engineering and construction industries as a result the growth of the Indian

machine tools industry was hampered. However the recent revival in the index of industrial production can be

construed as a harbinger of growth for the Indian machine tools industry.

Source : IMTMA & BDB Analysis

Market demand growth trend in domestic vis-à-vis import of metal

cutting machines industry in India

32

1072 1734 2496 3468 3966 3932 2783 4767 6788 6737Market size in

Rs Cr

Source : IMTMA & BDB Analysis

46%53%

59% 62%68%

75%

60% 63%

53%

63%

54%47%

41% 38%32%

25%

40% 37%

47%

37%

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08 FY 08-09 FY 09-10 FY 10-11 FY 11-12 FY 12-13

Import Domestic

Market demand across product categories over the last decade

33

Most product categories have seen a healthy growth rate driven by the Indian engineering sector especially the

auto and auto ancillary sector which has witnessed increased investments

FY 2013 saw a contraction in demand across most product categories due to a broad based slowdown in the

Indian economy

Year

Growth across product categories (In Rs Cr)

Turning

CentersVMCs HMCs

Grinding

Machines

Milling

Machines Lathes SPMs

Tool

Grinding

machines

EDMs

2003-04 331 235 92 175 72 31 60 26 49

2004-05 477 428 251 232 122 45 97 27 57

2005-06 659 533 333 364 237 91 141 37 101

2006-07 850 740 617 520 217 116 195 66 146

2007-08 988 825 738 562 306 101 218 113 116

2008-09 960 641 857 569 354 136 215 109 92

2009-10 749 593 329 364 337 143 155 37 75

2010-11 1469 1034 806 459 434 145 264 59 96

2011-12 2115 1568 1055 842 313 233 376 116 170

2012-13 1814 1376 1127 929 514 374 372 100 132

CAGR 18.54% 19.33% 28.47% 18.17% 21.72% 28.28% 20.02% 14.42% 10.42%

Source : IMTMA & BDB Analysis

34

31%

27%

26%

25%

25%

24%

27%

31%

31%

27%

22%

25%

21%

21%

21%

16%

21%

22%

23%

20%

9%

14%

13%

18%

19%

22%

12%

17%

16%

17%

16%

13%

15%

15%

14%

14%

13%

10%

12%

14%

7%

7%

9%

6%

8%

9%

12%

9%

5%

8%

3%

3%

4%

3%

3%

3%

5%

3%

3%

6%

6%

6%

6%

6%

5%

5%

6%

6%

6%

6%

2%

2%

1%

2%

3%

3%

1%

1%

2%

1%

5%

3%

4%

4%

3%

2%

3%

2%

3%

2%

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

Turning Centers VMCs HMCs

Grinding Machines Milling Machines Lathes

SPMs Tool Grinding machines EDMs

Market demand across product categories over the last decade

117.1138.3

209.5243.4 251.9

293.1 275.7 269.9 269.9

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

IIP

Key factors impacting the growth of the metal cutting machinery

35

8.59.7

11.1 10.9 11.2

14.1

17.620.0

21.9

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

Automobile production (in Million Units)

Growth in Index of Industrial Production (Machinery, power equipment, Transport equipment)

Growth in the automobile production

522720

9001080 1104

13201560

2100 1980

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

Auto component industry size (INR Billion)

Growth in the auto component industry

510 589681

823 8901042

12141320 1400

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

Heavy engineering industry size (INR Billion)

Growth in the heavy engineering industry(Power, process equipment, cement,, sugar, mining equipment)

Source : SIAM

Source : SIAM, ACMA Source : Department of Heavy Industry

Source : Central Statistics Office, World Bank

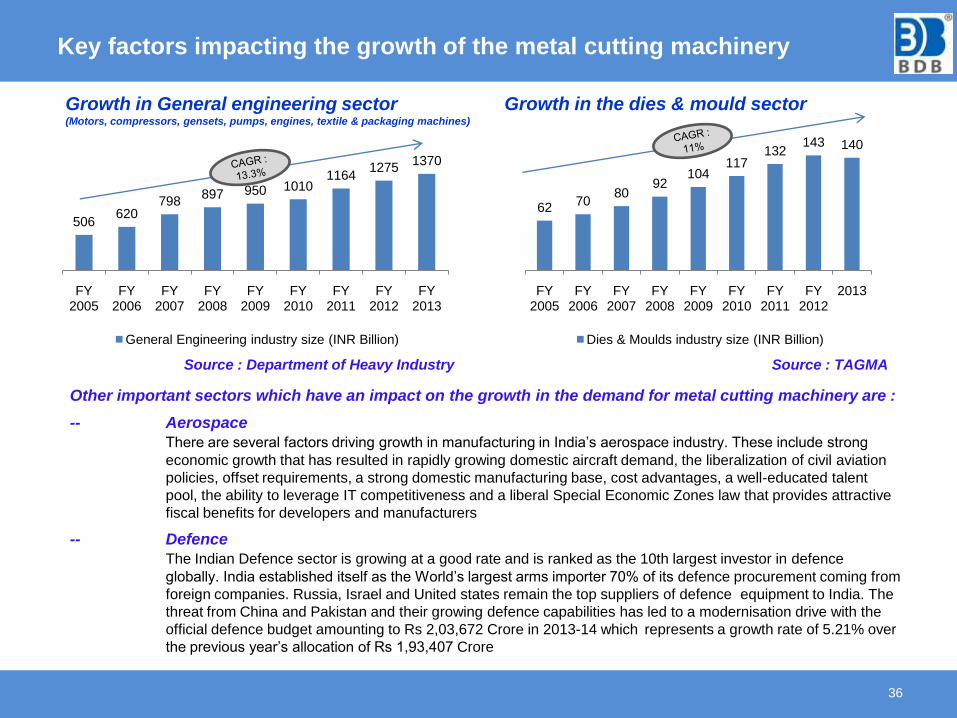

6270

8092

104117

132143 140

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

2013

Dies & Moulds industry size (INR Billion)

Key factors impacting the growth of the metal cutting machinery

36

Growth in General engineering sector (Motors, compressors, gensets, pumps, engines, textile & packaging machines)

Growth in the dies & mould sector

506620

798897 950 1010

11641275

1370

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

FY 2011

FY 2012

FY 2013

General Engineering industry size (INR Billion)

Other important sectors which have an impact on the growth in the demand for metal cutting machinery are :

-- Aerospace

There are several factors driving growth in manufacturing in India’s aerospace industry. These include strong

economic growth that has resulted in rapidly growing domestic aircraft demand, the liberalization of civil aviation

policies, offset requirements, a strong domestic manufacturing base, cost advantages, a well-educated talent

pool, the ability to leverage IT competitiveness and a liberal Special Economic Zones law that provides attractive

fiscal benefits for developers and manufacturers

-- Defence

The Indian Defence sector is growing at a good rate and is ranked as the 10th largest investor in defence

globally. India established itself as the World’s largest arms importer 70% of its defence procurement coming from

foreign companies. Russia, Israel and United states remain the top suppliers of defence equipment to India. The

threat from China and Pakistan and their growing defence capabilities has led to a modernisation drive with the

official defence budget amounting to Rs 2,03,672 Crore in 2013-14 which represents a growth rate of 5.21% over

the previous year’s allocation of Rs 1,93,407 Crore

Source : TAGMASource : Department of Heavy Industry

Projected growth of the key sectors impacting the growth of the metal

cutting machinery

37

Growth in Index of Industrial Production (Machinery, power equipment, Transport equipment)

Growth in the automobile production

Growth in the auto component industry Growth in the heavy engineering industry(Power, process equipment, cement,, sugar, mining equipment)

269.0 271.0 278.4295.1

318.7344.2

0%1%

3%6%

8%

8%

-2%

0%

2%

4%

6%

8%

10%

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

IIP % Growth

21.92 21.92 23.0224.63

26.3528.46

10%

0%

5%

7% 7%8%

0%

2%

4%

6%

8%

10%

12%

0

5

10

15

20

25

30

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Automobile production (in Million Units) % Growth

1980 2089 22252425

26672987

-6%

6%7%

9%10%

12%

-8%-6%-4%-2%0%2%4%6%8%10%12%14%

0

500

1000

1500

2000

2500

3000

3500

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Auto component industry size (INR Billion) % Growth

1400 1428 1514

1650 1798

1996

6%2%

6%

9%9%

11%

0%

2%

4%

6%

8%

10%

12%

0

500

1000

1500

2000

2500

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Heavy engineering industry size (INR Billion) % Growth

Source : BDB Analysis

Projected growth of the key sectors impacting the growth of the metal

cutting machinery

38

Growth in General engineering sector (Motors, compressors, gensets, pumps, engines, textile & packaging machines)

Growth in the die & mould sector

1370 1439 1539

1678 1829

2030

7%

5%

7%

9% 9%

11%

0%

2%

4%

6%

8%

10%

12%

0

500

1000

1500

2000

2500

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

General Engineering industry size (INR Billion) % Growth

Source : BDB Analysis

140 147 162

181203

228

-2%

5%

10%

12% 12%

12%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

0

50

100

150

200

250

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Die & Mould industry size (INR Billion) % Growth

Other important sectors which have an impact on the growth in the demand for metal cutting machinery are :

-- Aerospace

There are several factors driving growth in manufacturing in India’s aerospace industry. These include strong

economic growth that has resulted in rapidly growing domestic aircraft demand, the liberalization of civil aviation

policies, offset requirements, a strong domestic manufacturing base, cost advantages, a well-educated talent

pool, the ability to leverage IT competitiveness and a liberal Special Economic Zones law that provides attractive

fiscal benefits for developers and manufacturers

-- Defence

The Indian Defence sector is growing at a good rate and is ranked as the 10th largest investor in defence

globally. India established itself as the World’s largest arms importer 70% of its defence procurement coming from

foreign companies. Russia, Israel and United states remain the top suppliers of defence equipment to India. The

threat from China and Pakistan and their growing defence capabilities has led to a modernisation drive with the

official defence budget amounting to Rs 2,03,672 Crore in 2013-14 which represents a growth rate of 5.21% over

the previous year’s allocation of Rs 1,93,407 Crore

The projected growth of key sectors have been considered for the machine-wise projections in the further slides

Projected consumption for metal cutting industry

39

6737 6854

73728195

9486

10962

-1% 2%

8%

11%

16% 16%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

2000

4000

6000

8000

10000

12000

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Consumption of metal cutting machinery (INR Cr) % Growth Source : BDB Analysis

The growth in the consumption of metal cutting machinery over the past two years has displayed a

downturn on the back of the poor investments in the manufacturing sectors

The Index of industrial production has seen a negative growth predominantly due to the slowdown in

the manufacturing sectors hence the weakness in the demand for metal cutting machines

Low growth and weak business confidence feed into each other in a negative feedback loop

However the consumption of metal cutting machines is expected to recover and see a growth of

around 11% for the year 2015 - 2016

Projected growth in consumption across product categories (Rs Cr)

40

The economy is expected to revive by the year FY 2015 and most user sectors will see an upturn in their volumes

FY 2014 is expected to see a marginal growth of around 2% growth mainly due to the slowdown in the

automotive sector

Due to the increasing application of VMC in aerospace & defence sector, VMCs are estimated to grow at a higher

rate compared to HMCs

Year

Projected growth across product categories (In Rs Cr)

Turning

CentersVMCs HMCs

Grinding

Machines

Milling

Machines Lathe SPMs

Tool Cutter

Grinding

machines

EDMs

Total metal

cutting

machinery

FY 2013 1814 1376 1127 929 514 374 372 100 132 6738

FY 2014 1874 1358 1197 948 509 385 361 97 125 6854

FY 2015 2019 1490 1319 995 544 408 368 102 127 7372

FY 2016 2261 1689 1471 1094 599 449 390 111 130 8195

FY 2017 2671 2047 1653 1237 677 512 425 125 138 9486

FY 2018 3129 2432 1883 1398 772 584 472 144 149 10962

CAGR 10% 11% 10% 9% 9% 9% 5% 8% 3% 10%

Factors considered for procurement of the products under study

41

Total number of Companies Covered - 120 Numbers

1 2 3 4 5 6 7 8 9

Graph indicates the average ranking by the companies covered as per their priority for the factors considered while procuring

Highest

Priority

Lowest

Priority

Source : BDB Analysis

7.9

7.45

7.23

7.1

4.71

4.52

3.05

2.52

1.91

0 1 2 3 4 5 6 7 8 9

Material Saving

Delivery Time

Electricity Consumption

Past Experience

Commercial

Brand Name

Afetr sale Service

Reliability

Technology

Average Ranking

3. CONCLUSIONS

Recommended key action areas to improve domestic manufacturers’

market participation

43

ProductsMarket Size

(In Rs Crore)

Share of Domestic

Supply

Share of

Imports

Major source of

importMarket Growth

Turning Centers 1800 - 1825 56% 44% Korea (22%)

Vertical Machining Centers 1360 - 1400 66% 34% Taiwan (35%)

Horizontal Machining Centers 1125 - 1145 23% 77% Japan (63%)

Grinding Machines 920 - 940 32% 68% Japan (40%)

Milling Machines 495 - 530 9% 91% Italy (16%)

SPMs 360 - 400 78% 22% Japan (67%)

EDMs 125 - 135 63% 27% China (25%)

Tool Grinding machines 100 - 110 60% 40% Germany (17%)

Turning CentersDemand for Turning Centers is on the higher side; The Indian machine tool manufacturers cover the popular range of turning

centers , but only in standard and basic designs

VMCs

This is a growing segment with high technology. Higher share of domestic manufacturers indicate that acceptability for Indian

brands is reasonably good for this product segment; however, the high imports from Taiwan makes this segment highly price

competitive

HMCs

Currently, this market is dominated by imports because of the demand for technologically advanced machineries; Majority of

import is from Japan; Indian manufacturers lack in manufacturing technologically high end machinerieswith multi axes movement

and high spindle speeds

Grinding MachinesDue to the incapability of Indian manufacturers to supply superior technology machines, most of the demand in this segment is

met through imports

Milling Machines Due to unavailability of required specifications, end users prefer to import used machineries from Europe or new machineries

from China at a very low price

SPMs SPMs built by Indian manufacturers are considered to be advanced technology machines which is accepted globally

EDMs Large quantity of imports of EDMs from China at low price levels is becoming a threat to the domestic manufacturers

Key action areas for major metal cutting machines

44

Products Market Opportunities & Constraints Strategy for domestic manufacturers

Turning Centers The Indian machine tool manufacturers cover the

popular range of turning centers , but only in standard

and basic designs

Focus on supplying multi function turning center machines like turn

mill centers

Supply turning centers with global standards having spindles with

integrated motors, speed of 6000 rpm and slide traverse rates above

60 meters per minute

Continue supplying turning center machines of sizes ranging from 100

to 250mm turning diameters with a more advanced designing

Vertical

Machining

Centers

The current trend in machining centers is to have

additional axes of movements to take on complex

machining requirements including turning and grinding

capabilities on the machining center.

Focus on supplying compact machines suitable for line integration for

mass production of auto components

Supply machining centers having axes of movements above 5,

traverse rates above 100 meters per minute and speed ranging from

10,000 to 50,000 rpm

Machining centers consisting of grinding and turning capabilities may

add value to the end user

Horizontal

Machining

Centers

Increasing demand for machining centers with more

axes of movements

Grinding

Machines

Machines lacking advanced technology features

Comparatively low performance of machines wrt to

parameters like accuracy and surface finish

Supply machines with creep-feed grinding capability which may add

value to the die & mould segment

Focus on developing machines with high accuracy and surface finish

qualities which will be at par with the import quality machines

Milling Machines High imports of used machineries from Europe and

new machineries from China at very low cost

Supply milling machines with technology features matching with that

of imported machines at a competitive price level

Supply machines capable of milling and boring

SPMs No market constraintMay focus on exports of SPMs as Indian built SPMs are considered to

be technologically advanced

EDMs High imports from China at a very low price Focus on supplying EDMs at a highly competitive price level

Technology gaps between domestic manufacturers and imports

45

Parts, peripherals and assemblies procured or manufactured in India::

Domestic manufacturers have the capability to build the machine body of similar quality as that of imported

machines; however, end users perceive that the difference is in the quality of parts, peripherals and

assemblies used within the machines as compared to machines from Europe and Japan.

Accuracy in positioning:

It is opined that domestically manufactured machines lack in precision and accuracy in positioning

compared to the import quality machines

Lack of installed base for new specification requirements:

End user segments opined that they are not willing to procure domestically manufactured machines in

case of upgraded specifications requirements though the Indian manufacturers have the capability to

supply the same; this is mainly due to lack of installed base or unproven technology due to which end

users feel that these machines would not be able to deliver the expected quality; hence they depend on

imports

Other areas where Indian manufacturers lack behind global manufacturers include:

Multi-functioning machines

Non reliability to achieve uptime above 98%

Lack in parameters like safety and eco-friendliness

Low performace rating compared to imported machines wrt parameters like tool change

time, chip to chip time, pallet change time, footprint, acceleration etc.

Major challenges faced by Indian Metal Cutting Industry

46

Lack of locally

developed technology

Indian manufacturers may invest in developing or improving the existing R&D facilities;

this will help to bridge the gap of lack of indigenously developed technology

Unavailability of locally

produced critical

components

Major critical components are currently being imported and contribute to approximately

30% - 40% of total costs. To improve cost competitiveness, Indian manufacturers may

focus on production of these critical components

Highly price competitive

market

With large quantities of machines being imported from countries like China and Turkey,

Indian manufacturers may focus on substituting this market with increased reach and

offering better service solutions

Highly dependent on

imports

Indian metal cutting industry is highly dependent on imports of machines and critical

components as well; Indian manufacturers may focus on developing high end

technologies locally and focus on price competitiveness

Low awareness / credibility

of Indian manufacturers

and their capabilities to

offer high technology

products

Perception exists among end user segments that domestic machine manufacturers are

not at par with imported machines with respect to the quality and life of the machine; this

may be changed by providing demonstrations of machines to end user segments and

increasing the brand awareness. End users are unaware about current capabilities of

Indian manufacturers; hence they may work on improving the awareness amongst end

users by displaying their technological capabilities in exhibitions

Challenges Strategic Recommendations

Most of the end users do not prefer Indian brands because of unproven

technology, Indian manufacturers have to prove their brands with respect to technologyUnproven Technology

Few areas to be focused by Indian metal cutting machine manufacturers

47

Linear Motor Drivers

Two Piece Construciton V/S Single Piece Construction (Monoblock)

Cast Iron V/S Alternate Materials

Single Purpose V/S Multi Tasking (Combi)

5 Axes Machining

Belt Driven Spindles V/S Direct Drive (In Line)

Wireless Connections From Control To Elements

High Speed Machining

High rpm spindles

Single hit machining

Machine tools for TPM, lean and cellular manufacturing

Rapid tool change

International alliances in design, development, manufacture and marketing

4. PRODUCT WISE ANALYSIS

MARKET SIZE ANALYSIS OF

ELECTRICAL DISCHARGE MACHINE

Overview of electrical discharge machines

50

Electro Discharge Machining (EDM) is an electro-thermal non-traditional machining process, where

electrical energy is used to generate electrical spark and material removal mainly occurs due to

thermal energy of the spark.

EDM is mainly used to machine difficult-to-machine materials and high strength temperature resistant

alloys. EDM can be used to machine difficult geometries in small batches or even on job-shop basis.

Work material to be machined by EDM has to be electrically conductive.

Among thermal removal methods, electrical

discharge machining or EDM is the oldest and

most widely used. Electron-beam (EBM) and

laser beam machining (LBM) are newer thermal

techniques also widely accepted in industry today.

Plasma-arc cutting using a plasma arc torch is

mostly used for cutting relatively thick materials

Type of EDM

Die-sinking (also known as ram) type EDM

machines require the electrode to be machined in

the exact opposite shape as the one in the work

piece.

Wire-cut EDM machines use a continuous wire as

the electrode. Sparking takes place from the

electrode wire-side surface to the work piece

Major Indian electrical discharge machine manufacturers & their

locations

51

Company Location Ownership

Electronica Machine Tools Pune Private

Concord United Products Bangalore Private

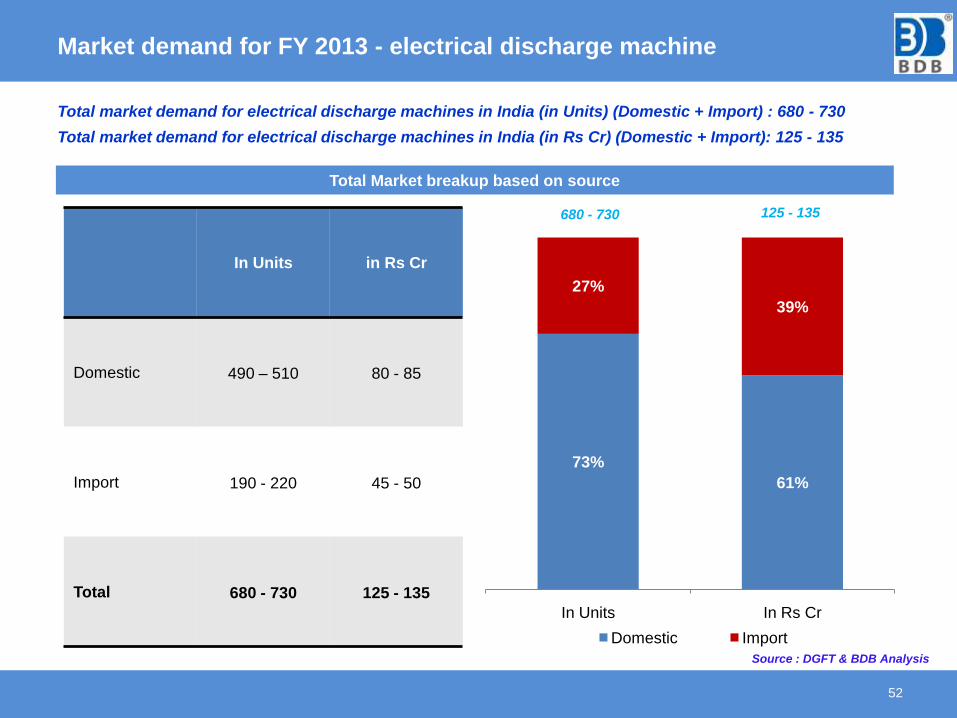

Market demand for FY 2013 - electrical discharge machine

52

73%

61%

27%

39%

In Units In Rs Cr

Domestic Import

Total market demand for electrical discharge machines in India (in Units) (Domestic + Import) : 680 - 730

Total market demand for electrical discharge machines in India (in Rs Cr) (Domestic + Import): 125 - 135

680 - 730 125 - 135

Total Market breakup based on source

In Units in Rs Cr

Domestic 490 – 510 80 - 85

Import 190 - 220 45 - 50

Total 680 - 730 125 - 135

Source : DGFT & BDB Analysis

Market demand for FY 2013 - electrical discharge machine (Domestic)

53

490 - 510 80 - 85

Sales breakup based Type of Machine

39% 40%

61% 60%

In Units In Rs Cr

Sinker Wire Cut

Among thermal removal methods, electrical discharge machining or EDM is the oldest and most widely used.

Electron-beam (EBM) and laser beam machining (LBM) are newer thermal techniques also widely accepted inindustry today.

EDM is not a fast method; some jobs can take days to produce holes, so its use is limited to jobs that cannoteasily be done in other ways (e.g. oblong slots or complex shapes, sometimes in very hard material).

Source : BDB Analysis

Total market demand for electrical discharge machines in India (in Units) (Domestic Sale) : 490 - 510

Total market demand for electrical discharge machines in India (in Rs Cr) (Domestic Sale ): 80 - 85

58% 58%

42% 42%

In Units In Rs Cr

CNC Non CNC

490 - 510 80 - 85

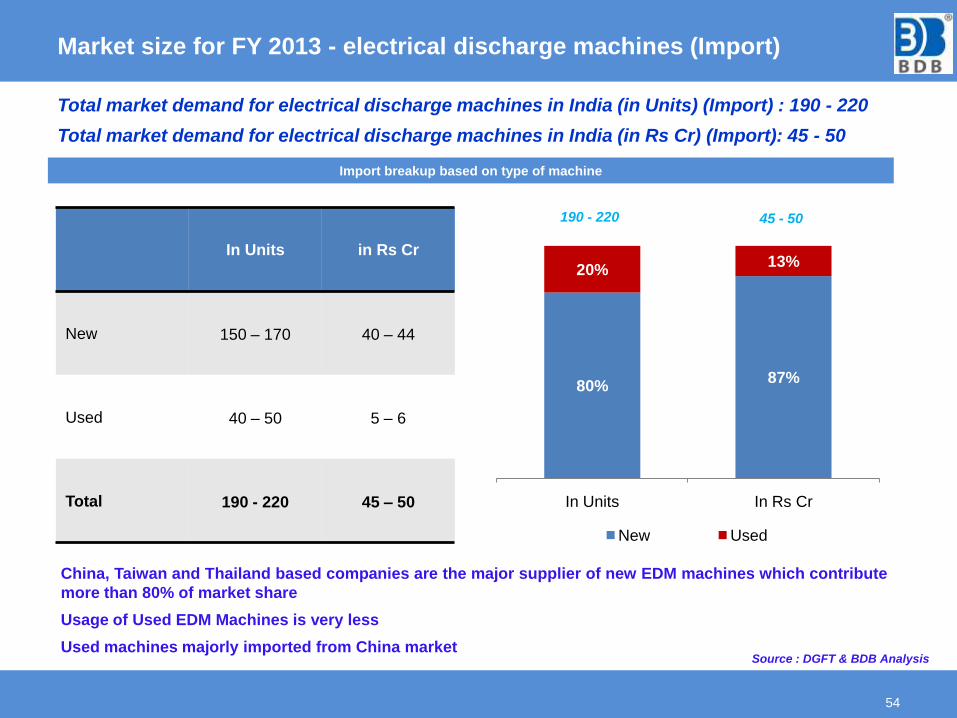

Market size for FY 2013 - electrical discharge machines (Import)

54

Total market demand for electrical discharge machines in India (in Units) (Import) : 190 - 220

Total market demand for electrical discharge machines in India (in Rs Cr) (Import): 45 - 50

80%87%

20%13%

In Units In Rs Cr

New Used

190 - 220 45 - 50

Import breakup based on type of machine

China, Taiwan and Thailand based companies are the major supplier of new EDM machines which contribute

more than 80% of market share

Usage of Used EDM Machines is very less

Used machines majorly imported from China market

In Units in Rs Cr

New 150 – 170 40 – 44

Used 40 – 50 5 – 6

Total 190 - 220 45 – 50

Source : DGFT & BDB Analysis

Market analysis for import of electrical discharge machines for FY 2013

- Country wise & Brand wise

55

Brand Name New Machinery Used Machinery Total

Market Share based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)New Used

SODICK 21 9.7 9 1.1 30 10.7 23% 18%

MAKINO 9 5.5 0 0.0 9 5.5 13% 0%

AGIE CHARMILLES 9 4.2 5 0.5 14 4.7 10% 8%

FANUC 7 4.2 0 0.0 7 4.2 10% 0%

MITSUBISHI 11 4.2 1 0.8 12 5.0 10% 14%

CHMER 18 2.9 0 0.0 18 2.9 7% 0%

YCM 6 1.3 0 0.0 6 1.3 3% 0%

JOEMARS 10 0.8 0 0.0 10 0.8 2% 0%

OSCAR 9 0.8 0 0.0 9 0.8 2% 0%

Suzhou Baoma 11 0.4 0 0.0 11 0.4 1% 0%

EXCELLENT 10 0.4 0 0.0 10 0.4 1% 0%

Zhongyuan 4 0.0 0 0.0 4 0.0 0% 0%

AGIE CHARMILLE 0 0.0 6 0.7 6 0.7 0% 11%

KINGRED 0 0.0 10 2.2 10 2.2 0% 36%

Others 34 7.6 10 0.8 44 8.3 20% 13%

Grand Total 159 42 41 6 200 48

Country Name New Machinery Used Machinery Total

Market Share based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)New Used

CHINA 66 8.8 12 3.2 78 12.1 21% 54%

THAILAND 18 8.0 3 0.4 21 8.3 19% 6%

TAIWAN 49 6.3 4 0.5 53 6.8 15% 8%

SINGAPORE 9 5.5 11 0.7 20 6.1 13% 11%

JAPAN 8 4.6 3 0.2 11 4.9 11% 4%

Others 9 8.8 8 1.0 17 9.8 20% 17%

Grand Total 159 42 41 6 200 48

Total market demand for electrical discharge machines in India (in Units) (Import) : 190 - 220

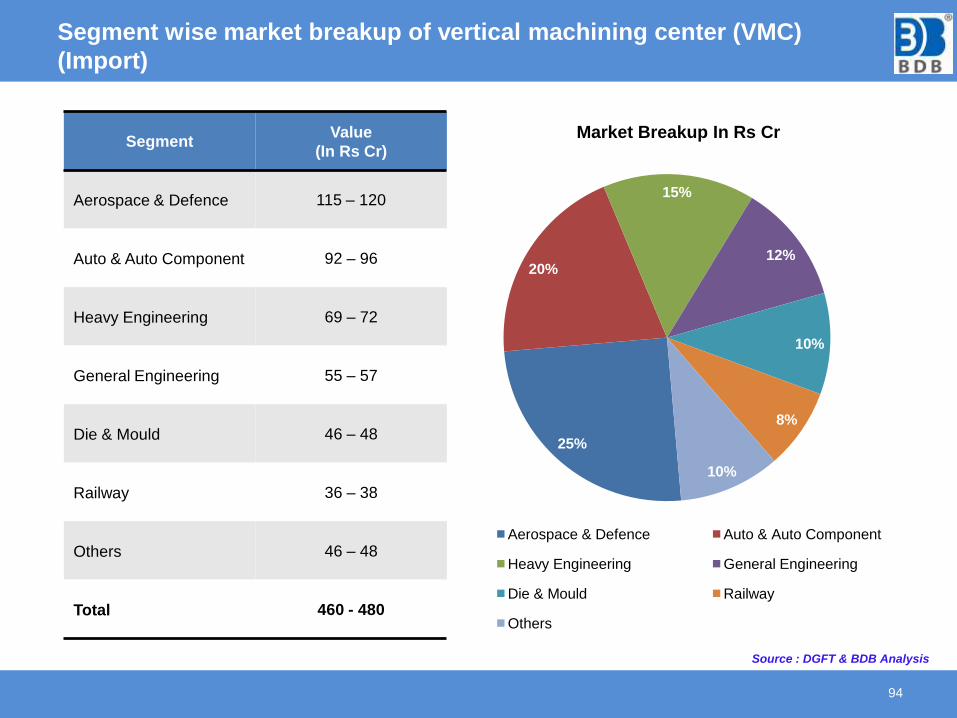

Total market demand for electrical discharge machines in India (in Rs Cr) (Import): 45 - 50

Segment wise market breakup of electrical discharge machine for FY

2012-13

56

Segment Market (in Rs Cr)

Auto& Auto Component 38 - 40

Aerospace & Defence 34 - 36

Electronic Industry 14 - 15

Die & Mould 18 - 20

Railway 5 - 6

Others 16 - 18

Total 125 - 135

30%

27% 11%

15%

4%

13%

Market Breakup In Rs Cr

Auto& Auto Component Aerospace & Defence

Electronic Industry Die & Mould

Railway Others

Source : BDB Analysis

Segment wise usage pattern of electrical discharge machine

57

Name SegmentMajor Brands

Indian Brands Foreign Brands

Auto OEM ElectronicaAGIE CHARMILLES, Suzhou

Baoma, Makino, Chmer

Auto Components Electronica, Concord Suzhou Baoma, Makino, Chmer

Aerospace - Makino, Mitsubishi, Chmer

Die & Mould Electronica Makino, Chmer

Electronic Industry Electronica Suzhou Baoma, King red

General Engineering Electronica Makino, Chmer, YCM

Market forecast of electric discharge machines for next 5 years

58

Year

Projected

market size

(In Rs Cr)

Growth in %

FY 2013 132

FY 2014 125 -5%

FY 2015 127 1%

FY 2016 130 3%

FY 2017 138 6%

FY 2018 149 8%

Source : BDB Analysis

132

125 127

130

138

149

-5%

1%

3%

6%

8%

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

110

115

120

125

130

135

140

145

150

155

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

Projected market size (In Rs Cr)

Projected market size(In Rs Cr) Growth in %

ANALYSIS OF CNC TURNING

CENTERS MARKET IN INDIA

Overview of CNC turning centers in India

60

The Indian machine tools industry produces a range of turning centers in all sizes, from the small to the

very large, and for special applications. However, the dominant market is for machines in the size range

from 100 mm to 250 mm turning diameters.

Indian machines are adequate to meet basic turning applications but have to be technologically

developed further to come abreast with international standards of multi function CNC turning machines.

Indian Manufacturer have good amount of

market share in turning centers, Indian

manufacturer majorly focus on popular

specification range which is majorly used in

Auto and Auto components segment

A Turning Center is simply a CNC lathe with a

multi-station turret and an enclosure

Turning is one of the most common of metal

cutting operations. In turning, a work piece is

rotated about its axis as single-point cutting

tools are fed into it, shearing away unwanted

material and creating the desired part.

Turning can occur on both external and internal

surfaces to produce an axially-symmetrical

contoured part.

Major Indian CNC turning center manufacturers & their locations

61

Company Location Ownership

Ace Designers Bangalore Private

HMT Bangalore Public limited

Jyothi CNC Automation Rajkot Private

Laxmi Machine Tools Coimbatore Private

Askar Microns Mysore Private

Miven Machine Tools Hubli Private

Galaxy machine tools Belgaum Private

Gedee Weiler Coimbatore Private

PMT machine tools Pune Private

Marshall Ludhiana Private

BFW Bangalore Private

Major foreign CNC turning center suppliers & their locations

62

Company Location Location in India

Mazak Japan Technical center, Pune

DMG Germany Bangalore

Takisawa Japan Bangalore

HAAS USA Technical center

Primero Taiwan --

Filler Taiwan --

Niles-Simmons Germany --

STOS Czechoslovakia --

FairFriend Taiwan --

EMCO Austria --

Tong Tai Taiwan --

WMW Germany --

Daewoo Korea --

Alextech Taiwan --

Hyundai-Kia Korea Chennai

Spinner Automation Germany Gurgaon ( Sales Office )

Goratu Spain Kolkata

Emag Germany Bangalore

Leadwell USA New Delhi (Dealer)

Takamaz Japan Bangalore

Pinacho Spain Bangalore

Lico Taiwan Bangalore

Hurco USA Chennai

Milltronics USA ( Sales Office )

63

Market demand for FY 2013 - CNC Turning center

Total market demand for turning centers in India (in Units) (Domestic + Import) : 7600 - 7800

Total market demand for turning centers in India (in Rs Cr) (Domestic + Import): 1800 - 1825

Total Market breakup based on source

77%

56%

23%

44%

In Units In Rs Cr

Domestic Import

1800 - 18257600 - 7800

In Units in Rs Cr

Domestic 5900 - 6000 1010 – 1020

Import 1700 - 1800 790 - 805

Total 7600 - 7800 1800 - 1825

Source : DGFT & BDB Analysis

Product TypeQuantity

(in units)

Value

(In Rs Cr)

Vertical Turning Centers 390 - 420 305 - 320

Horizontal Turning Centers 320 - 400 20 – 25

Other types 6890 - 6980 1475 - 1480

Total 7600 - 7800 1800 - 1825

Continue…

64

Market break up based on technology

All industries require turning centers up to 200 mm turning diameter

Industries like Aerospace, Heavy engineering, Die & mould segments use machineries of turning diameter

above 200 mm

Market In Rs Cr

85%

10%

5%

Upto 200 mm 200 - 600 mm 600 & Above

Source : BDB Analysis

Total market demand for turning centers in India (in Units) (Domestic Sales) : 5900 - 6000

Total market demand for turning centers in India (in Rs Cr) (Domestic Sales): 1010 - 1020

36%

24%

12%

10%

18%

upto 200 mm

Auto Components

Auto OEM

General Engineering

Aerospace & Defence

Others

20%

18%

15%

15%

12%

20%

above 200 mm

General Engineering

Aerospace & Defence

Heavy Engineering

Die & Mould

Auto & Auto Components

Others

Construction & Mining included in Heavy Engineering

Segment wise market breakup of CNC turning center for FY 2012-13

(Domestic)

65

Segment Market (in Rs Cr)

Auto Component 430 - 431

Auto OEM 180 - 181

General Engineering 200 - 201

Aerospace & Defence 60 - 62

Die & Mould 40 - 41

Construction & Mining 30 - 31

Railway 20 - 21

Others 50 - 51

Total 1010 - 1020

42%

18%

20%

6%

4%

3%2%

5%

Market Breakup In Rs Cr

Auto Component Auto OEM

General Engineering Aerospace & Defence

Die & Mould Construction & Mining

Railway Others

Source : BDB Analysis

Market demand for FY 2013 - CNC Turning center (Import)

66

Turning centers import market break up based on type

1700 - 1800 790 - 805

47%

92%

53%

8%

In Units In Rs Cr

New Used

Total market demand for turning centers in India (in Units) (Import Sales) : 1700 - 1800

Total market demand for turning centers in India (in Rs Cr) (Import Sales): 790 - 805

New turning centers are mostly imported from countries

like China, Japan, Korea and Taiwan

(Doosan, Hyundai, Mazak & Takisawa)

Used turning centers are mostly imported from countries

like Italy, Germany and France (Daewoo, Mori Seiki &

Tornos)

In Units In Rs Cr

New 1100 - 1160 730 - 740

Used 600 - 640 60 - 65

Total 1700 - 1800 790 - 805

Source : DGFT & BDB Analysis

Market analysis for import of CNC turning center for FY 2013 -

Country wise

67

Total market demand for turning centers in India (in Units) (Import Sales) : 1700 - 1800

Total market demand for turning centers in India (in Rs Cr) (Import Sales): 790 - 805

Country Name

Used Machinery

Market Share

based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)New

Germany 63 10 17%

Italy 76 6 10%

Japan 95 11 18%

Korea 56 7 11%

Taiwan 40 1 2%

USA 79 6 9%

Others 222 21 33%

Total 631 62

Country Name

New Machinery

Market Share

based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)New

China 279 66 9%

Germany 36 69 9%

Italy 24 59 8%

Japan 150 141 19%

Korea 286 168 23%

Taiwan 131 81 11%

USA 83 31 4%

Others 153 119 16%

Total 1142 735

Market analysis for import of CNC turning center for FY 2013 -

Brand wise

68

Total market demand for turning centers in India (in Units) (Import Sales) : 1700 - 1800

Total market demand for turning centers in India (in Rs Cr) (Import Sales): 790 - 805

Brand Name

New Machinery

Market Share

based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)New

DMG 36 39.4 5%

Doosan 100 50.6 7%

Hyundai 103 46.1 6%

HWACHEON 65 28.5 4%

Mazak 109 57.9 8%

TAKISAWA 53 33.0 4%

VICTOR 20 6.1 1%

OKUMA 24 15.2 2%

Zhejiang headman 95 5.1 1%

HAAS 72 25.7 3%

TAKANG 20 10.4 1%

You ji 22 20.7 3%

MORI SEIKI 12 12.6 2%

Others 411 383.9 52%

Total 1142 735

Brand Name

Used Machinery

Market Share

based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)Used

Daewoo 84 4.7 8%

HARDINGS 24 1.3 2%

Mazak 18 0.9 1%

WMW 11 3.4 6%

TAKISAWA 21 1.4 2%

LEADWELL 13 0.4 1%

TORNOS 30 0.2 0.3%

VICTOR 15 0.5 1%

OKUMA 14 1.6 3%

MORI SEIKI 32 1.3 2%

COLCHESTER 13 0.4 1%

STAR 9 1.3 2%

NAKAMURA 19 0.6 1%

Others 328 44.0 71%

Total 631 62

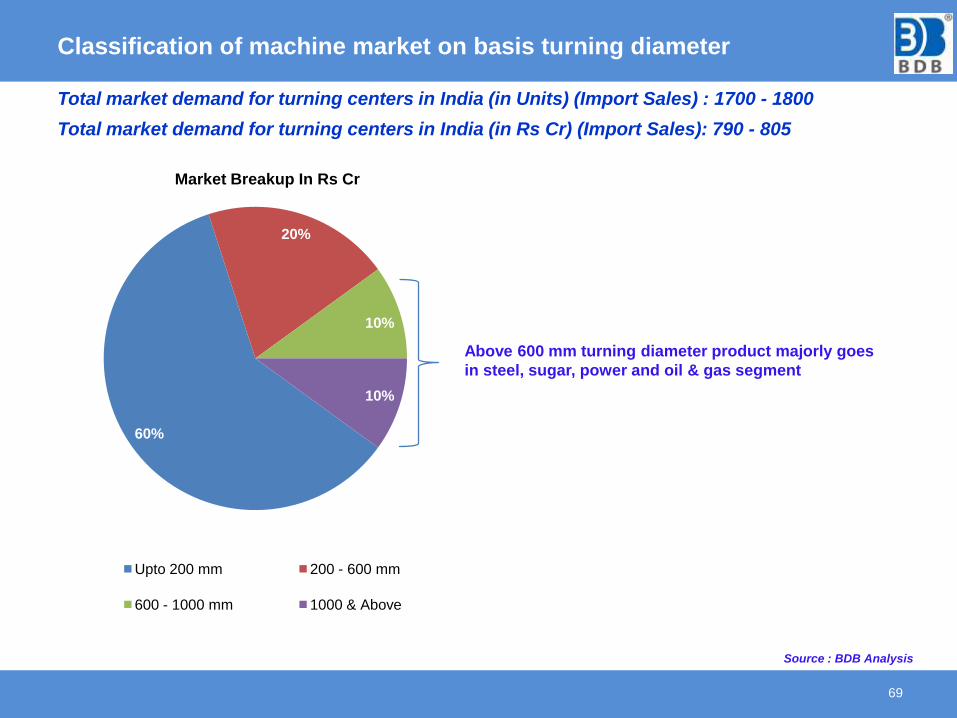

Classification of machine market on basis turning diameter

69

60%

20%

10%

10%

Market Breakup In Rs Cr

Upto 200 mm 200 - 600 mm

600 - 1000 mm 1000 & Above

Above 600 mm turning diameter product majorly goes

in steel, sugar, power and oil & gas segment

Total market demand for turning centers in India (in Units) (Import Sales) : 1700 - 1800

Total market demand for turning centers in India (in Rs Cr) (Import Sales): 790 - 805

Source : BDB Analysis

Segment wise market breakup of CNC turning center for FY 2012-13

(Import)

70

Segment Market (in Rs Cr)

Aerospace & Defence 198 – 201

Auto & Auto Component 174 – 177

Heavy Engineering 142 – 145

General Engineering 134 – 137

Others 142 – 145

Total 790 - 805

25%

22%

18%

17%

18%

Market Breakup In Rs Cr

Aerospace Auto & Auto Component

Heavy Engineering General Engineering

Others

Total market demand for turning centers in India (in Units) (Import Sales) : 1700 - 1800

Total market demand for turning centers in India (in Rs Cr) (Import Sales): 790 - 805

Source : BDB Analysis

ANALYSIS OF VERTICAL

TURNING CENTERS

MARKET IN INDIA

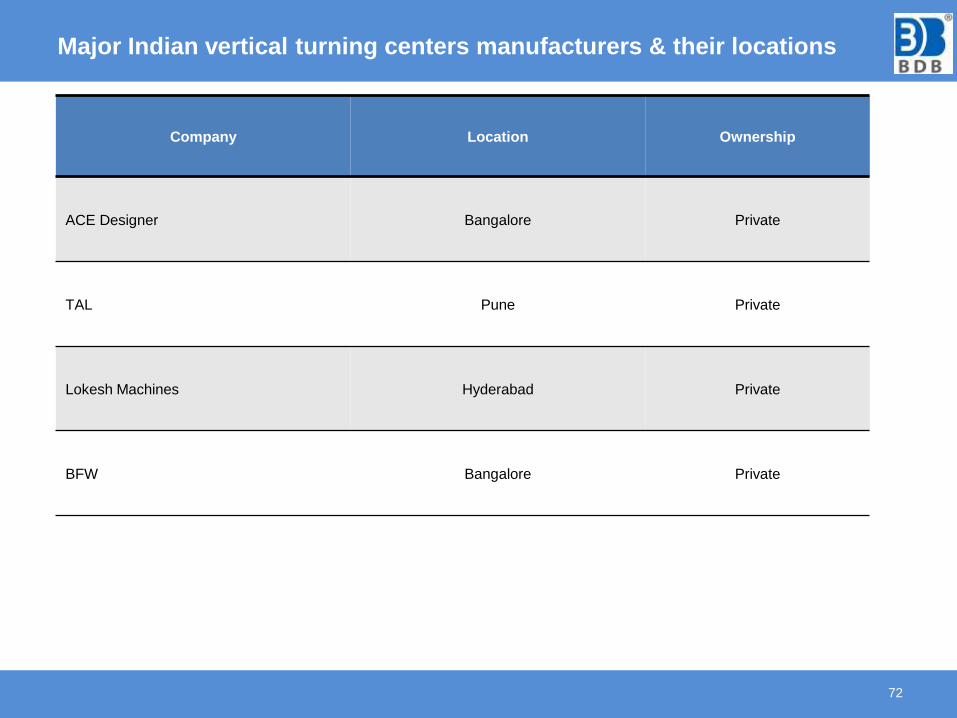

Major Indian vertical turning centers manufacturers & their locations

72

Company Location Ownership

ACE Designer Bangalore Private

TAL Pune Private

Lokesh Machines Hyderabad Private

BFW Bangalore Private

Market demand for FY 2013 - vertical turning centers

73

35%28%

65%72%

In Units In Rs Mn

Domestic Import

Total market demand for vertical turning centers in India (in Units) (Domestic + Import) : 390 - 420

Total market demand for vertical turning centers in India (in Rs Cr) (Domestic + Import): 305 -320

Total Market breakup based on source

390 - 420

In Units in Rs Mn

Domestic 140 - 150 95 – 100

Import 250 -270 210 - 220

Total 390 - 420 305 - 320

305 - 320

Source : DGFT & BDB Analysis

Segment wise market breakup of vertical turning centers for FY 2012-13

(Domestic manufactured)

74

Segment Market (in Rs Cr)

Auto & Auto Component 29 – 31

Heavy Engineering 20 – 21

General Engineering 11 – 12

Aerospace & Defence 9.5 – 10

Dies & Mould 7.5 – 8

Others 17 – 18

Total 95 - 100

31%

21%

12%

10%

8%

18%

Market Size in Rs Cr

Auto & Auto Component Heavy Engineering

General Engineering Aerospace & Defence

Dies & Mould Others

Source : BDB Analysis

Market demand for FY 2013 - vertical turning centers (Import)

75

Total market demand for vertical turning centers in India (in Units) (Import) : 250 - 270

Total market demand for vertical turning centers in India (in Rs Cr) (Import): 210 - 220

250 - 270 210 - 220

Import Breakup in terms of number and Value

50%

18%

50%

82%

In Units In Rs Cr

Used New

More than 50% of new machineries demand is catered by Korea and Taiwan based companies (You ji, Hyundai,

Doosan, Hwacheon etc)

Whereas used machineries demand is catered by Germany and Italy based companies

Emag is also one more popular brand in Vertical Turning center

In Units In Rs Cr

New 125 – 135 170 – 175

Used 125 – 135 40 – 45

Total 250 – 270 210 – 220

Market analysis for import of vertical turning center for FY 2013

- Country wise & Brand wise

76

Country Name New Machinery Used Machinery Total

Market Share based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)New Used

Korea 58 52.49 2 2.8 60 55.29 29% 7%

Taiwan 47 45.25 1 0 48 45.25 25% 0%

Germany 6 12.67 28 4 34 16.67 7% 10%

Italy 1 7.24 15 9.6 16 16.84 4% 24%

Japan 4 3.62 5 0.8 9 4.42 2% 2%

Others 14 59.73 78 22.4 92 82.13 33% 56%

Total 130 181 129 40 259 221

Brand Name New Machinery Used Machinery Total

Market Share based

on Rs Cr

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)

Quantity

(in units)

Value

(In Rs Cr)New Used

You Ji 19 18 0 0 19 18 10% 0%

TITAN 1 16 9 7.2 10 23 9% 18%

Hwachion 27 13 0 0 27 13 7% 0%

EMAG 4 11 0 0 4 11 6% 0%

Hyundai 14 11 0 0 14 11 6% 0%

Mori Sieki 11 7 2 0 13 7 4% 0%

Doosan 13 7 0 0 13 7 4% 0%

Others 41 98 118 32.8 159 131 54% 82%

Total 130 181 129 40 259 221

Total market demand for vertical turning centers in India (in Units) (Import) : 250 - 270

Total market demand for vertical turning centers in India (in Rs Cr) (Import): 210 - 220