Embed Size (px)

Citation preview

the importance of field underwriting for Disability Income insuranceKeys to Quicker Issue and Better Placement Ratio

DI 1215 3/13

disclosures• In approved states, Disability Income insurance (forms 4501NC, 4502GR and 4503BOE) is issued

by Ameritas Life Insurance Corp. located at 5900 "O" Street, Lincoln, NE 68510. In New York, Disability Income insurance (forms 5501-NC, 5502-GR and 5503-BOE) is issued by Ameritas Life Insurance Corp. of New York located at 1350 Broadway, Suite 2201, New York, NY 10018. Policy and riders may vary and may not be available in all states.

• In approved states, DInamic FundamentalSM (form 4504LS) is issued by Ameritas Life Insurance Corp. located at 5900 "O" Street, Lincoln, NE 68510. Policy and riders may vary and may not be available in all states.

• This information is provided by Ameritas®, which is a marketing name for subsidiaries of Ameritas Mutual Holding Company, including: Ameritas Life Insurance Corp., Ameritas Life Insurance Corp. of New York, Acacia Life Insurance Company, The Union Central Life Insurance Company, and Ameritas Investment Corp., member FINRA/SIPC. Ameritas Life Insurance Corp. and Acacia Life Insurance Company are not licensed in New York. Each company is solely responsible for its own financial condition and contractual obligations. For more information about Ameritas®, visit ameritas.com.

• Ameritas® and the bison are registered service marks of Ameritas Life Insurance Corp. © 2013 Ameritas Mutual Holding Company

04/19/23 For Producer use only. Not for use with clients.

2

field underwriting

• Traditional Application

• Medical Requirements

• Financial Requirements

• How To Speed Up the Process

• DI EZ App Teleunderwriting

04/19/23 For Producer use only. Not for use with clients.

3

the DI application

• Legal document that becomes part of Disability Income insurance contract

• Contractual rights for insured and Ameritas® are governed by the application and state laws

• Proper completion is vital to the underwriting process

• Should be taken face-to-face with client

• Use correct version, based on state of full-time residence or full-time employment

• Complete electronically or using blue/black ink

04/19/23 For Producer use only. Not for use with clients.

4

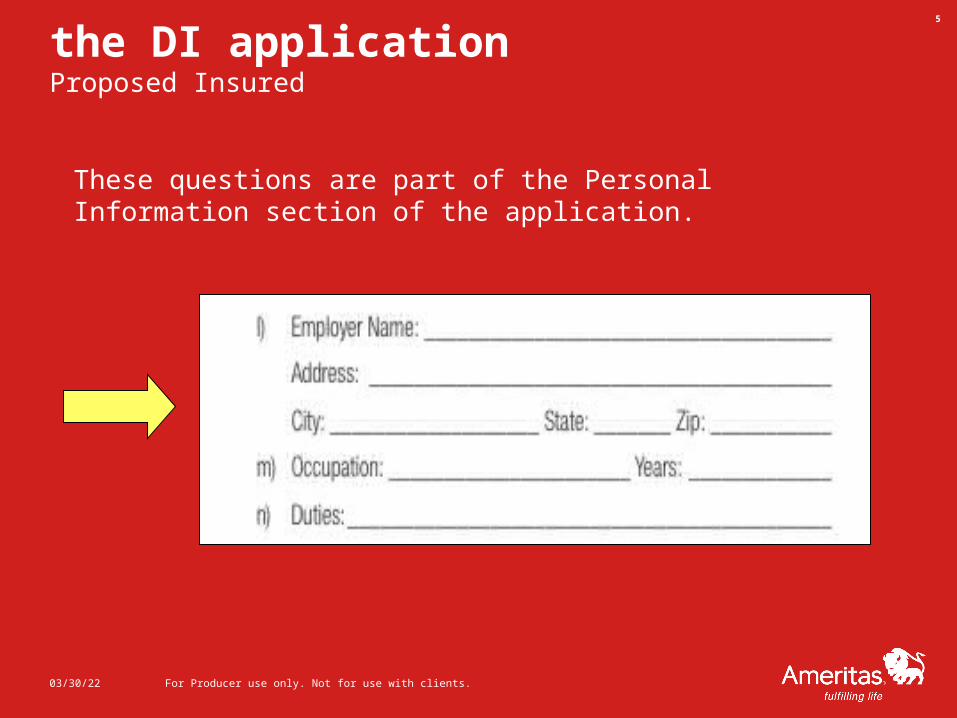

the DI applicationProposed Insured

04/19/23 For Producer use only. Not for use with clients.

5

These questions are part of the Personal Information section of the application.

the DI applicationCoverage

04/19/23 For Producer use only. Not for use with clients.

6

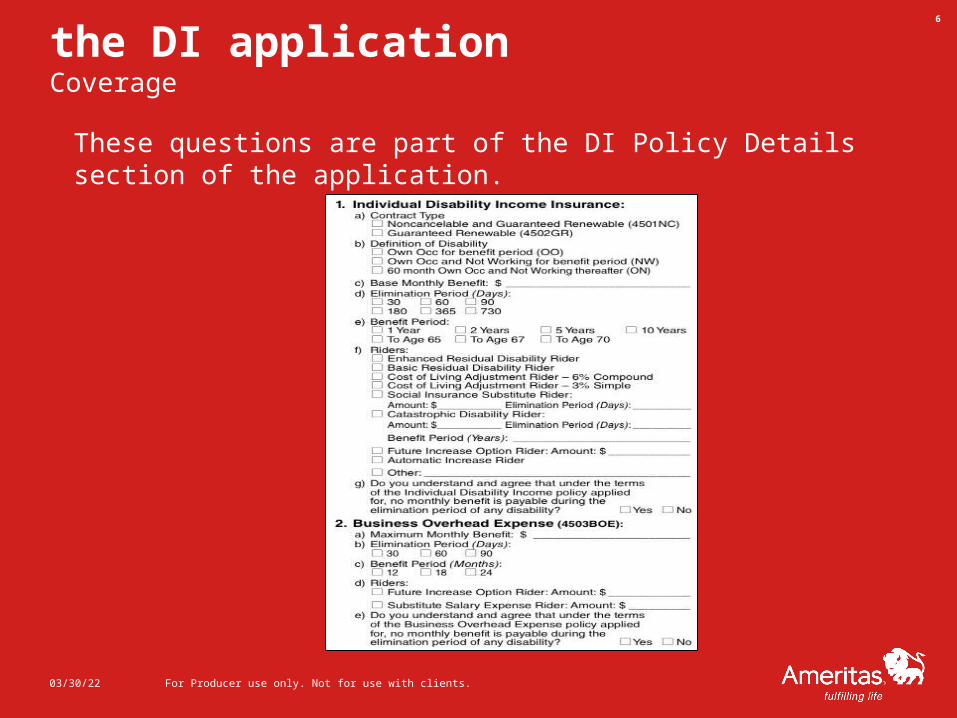

These questions are part of the DI Policy Details section of the application.

the DI applicationFinancials

04/19/23 For Producer use only. Not for use with clients.

7

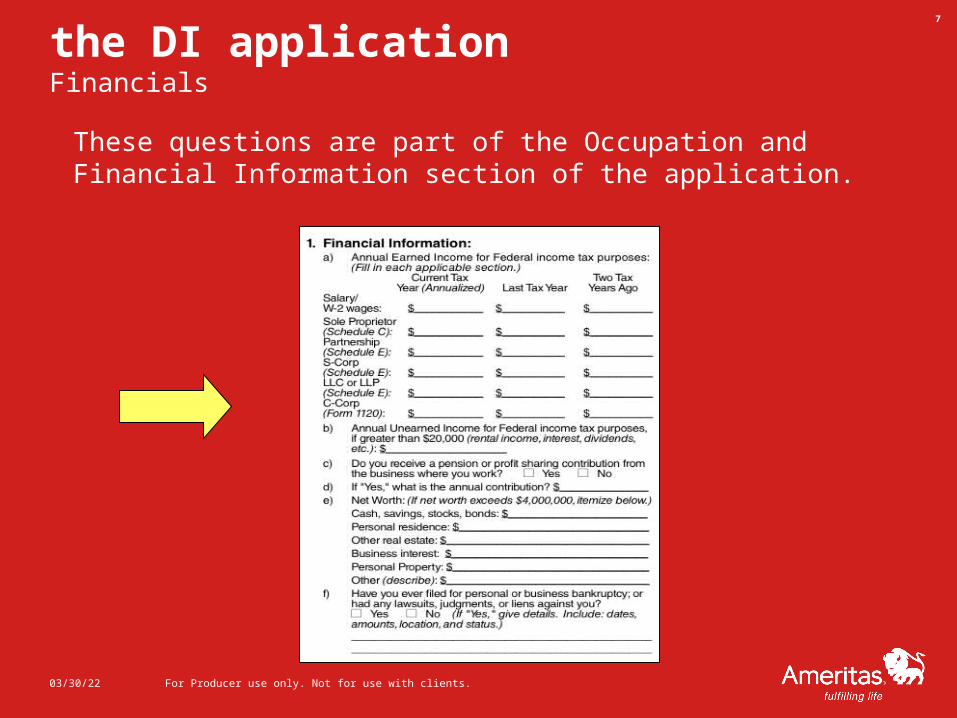

These questions are part of the Occupation and Financial Information section of the application.

the DI applicationFinancials

04/19/23 For Producer use only. Not for use with clients.

8

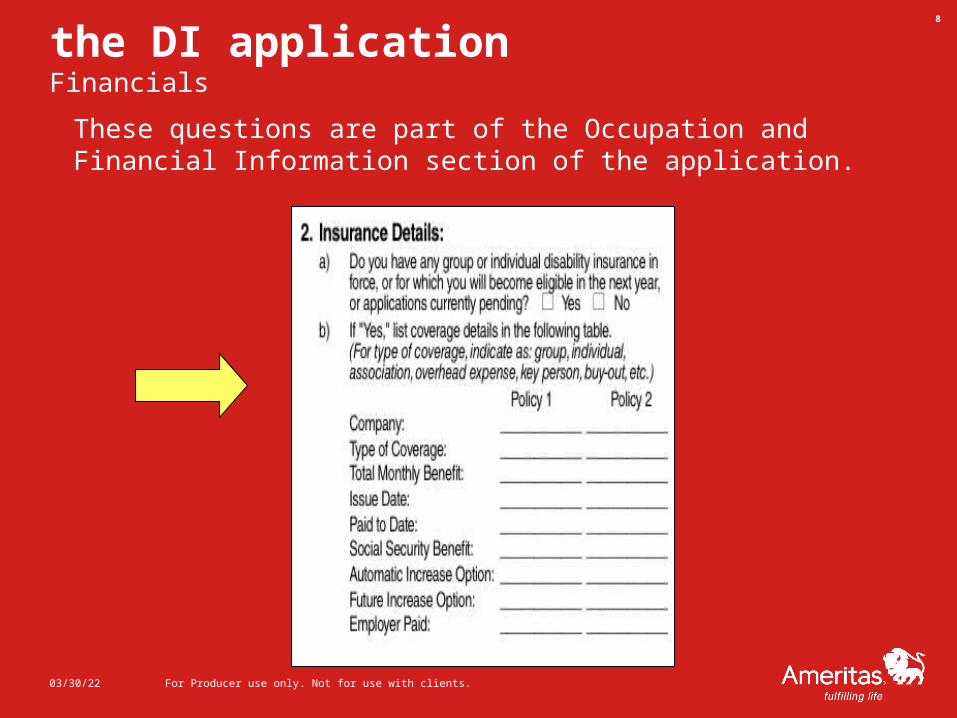

These questions are part of the Occupation and Financial Information section of the application.

the DI applicationOccupation & Financials

04/19/23 For Producer use only. Not for use with clients.

9

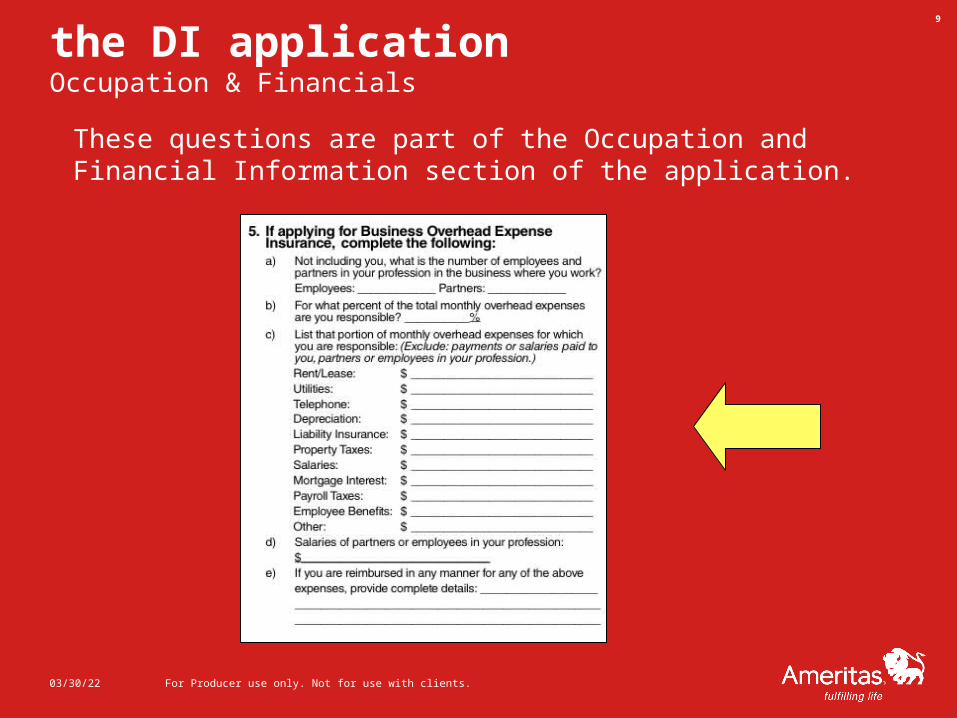

These questions are part of the Occupation and Financial Information section of the application.

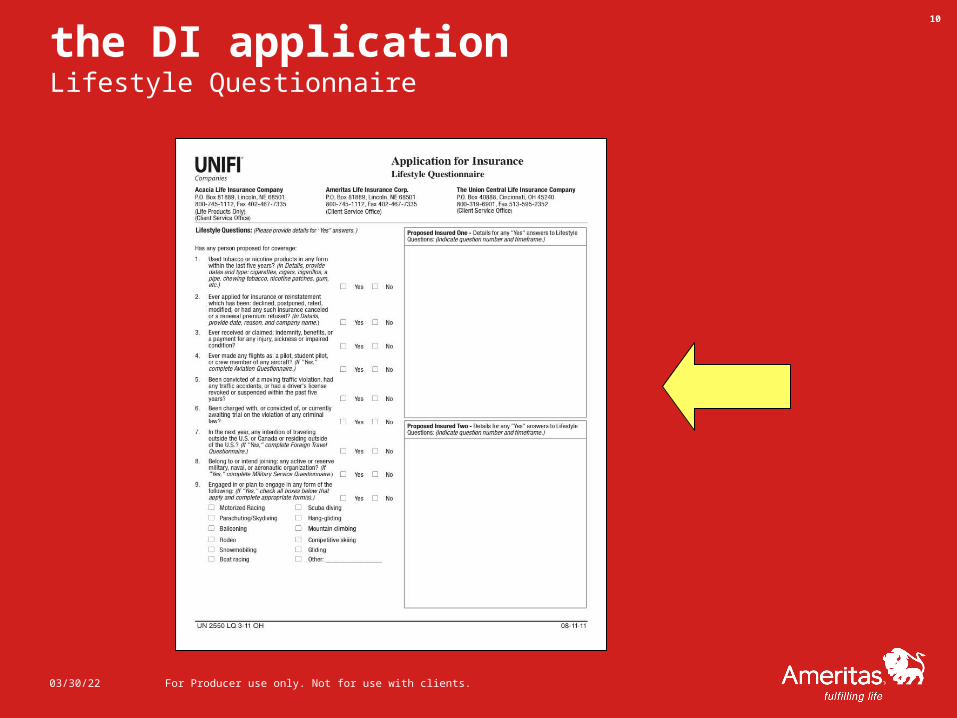

the DI applicationLifestyle Questionnaire

04/19/23 For Producer use only. Not for use with clients.

10

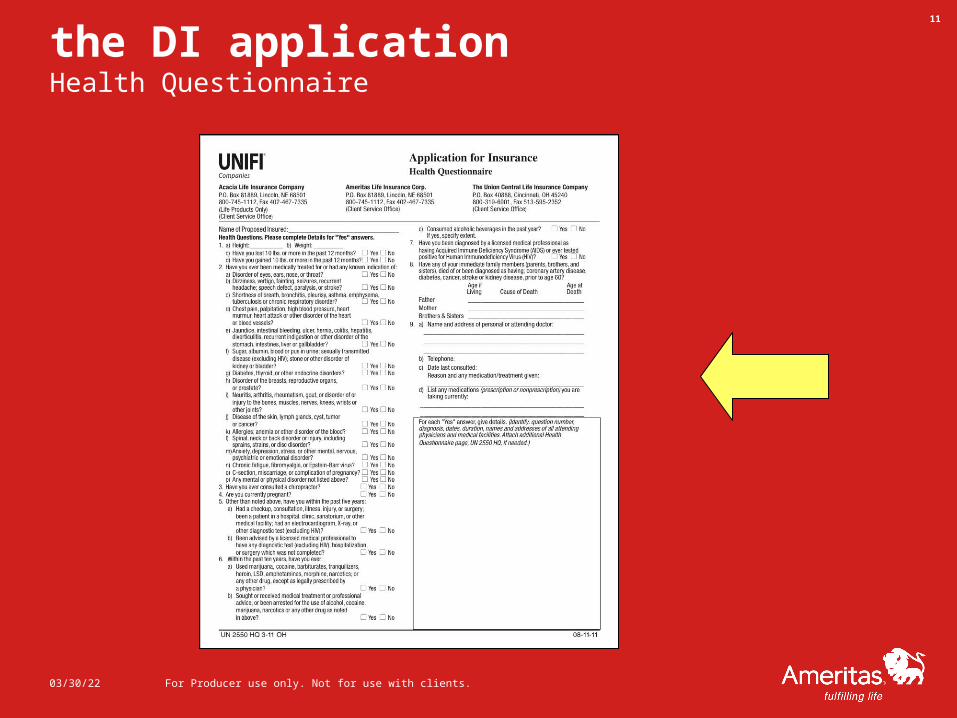

the DI applicationHealth Questionnaire

04/19/23 For Producer use only. Not for use with clients.

11

the DI applicationLifestyle & Health Questions

• For questions with a “yes” answer, get details:

• Dates, duration, resolution, residuals

• Doctor’s name, address, phone number

• Medication information

• Test results

• Questionnaires

• Driver’s license number

04/19/23 For Producer use only. Not for use with clients.

12

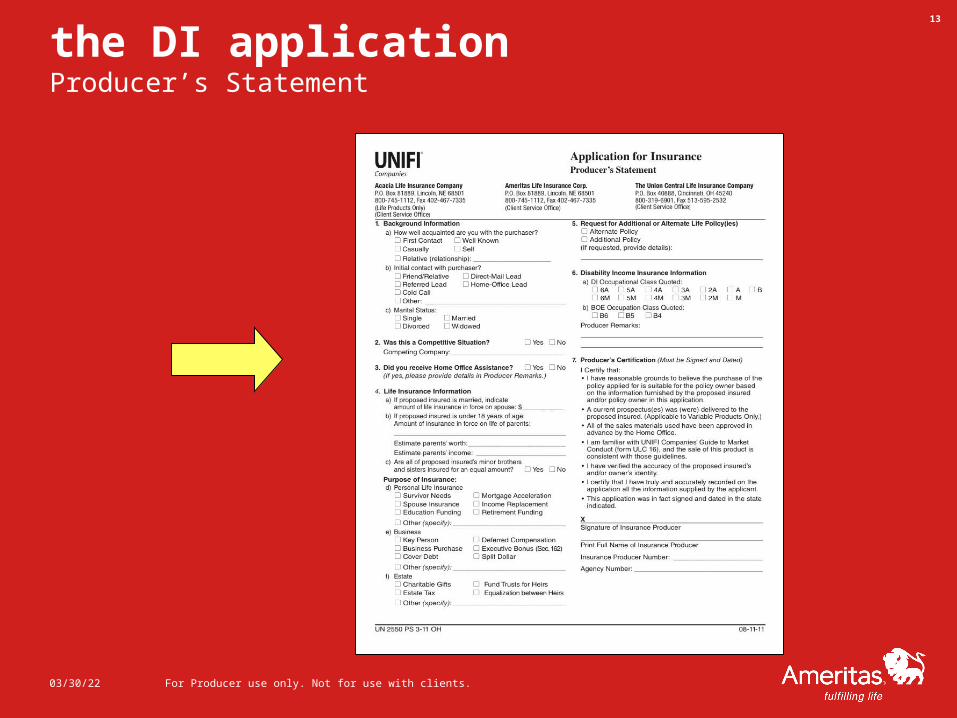

the DI applicationProducer’s Statement

04/19/23 For Producer use only. Not for use with clients.

13

the DI applicationProducer’s Statement

• Producer’s Statement

• Complete all areas

• Remarks section

• Sign and date

04/19/23 For Producer use only. Not for use with clients.

14

the DI applicationConditional Receipt

• Conditional Receipt

• Sign and give to applicant if money is collected

• Do not take money if medical history includes:

• Cancer

• Heart disease

• Diabetes

• Stroke

• Client being admitted to a medical facility in the past 90 days

04/19/23 For Producer use only. Not for use with clients.

15

the DI applicationConditional Receipt

• Conditional Receipt, continued

• Do not take money when benefit amount exceeds $8,000/month

• Do not take money if there is reason to believe the case may not be issued on a standard basis

• In all other cases, do collect money

• Can result in higher placement ratio

04/19/23 For Producer use only. Not for use with clients.

16

underwriting requirements

• Medical

• Financial

04/19/23 For Producer use only. Not for use with clients.

17

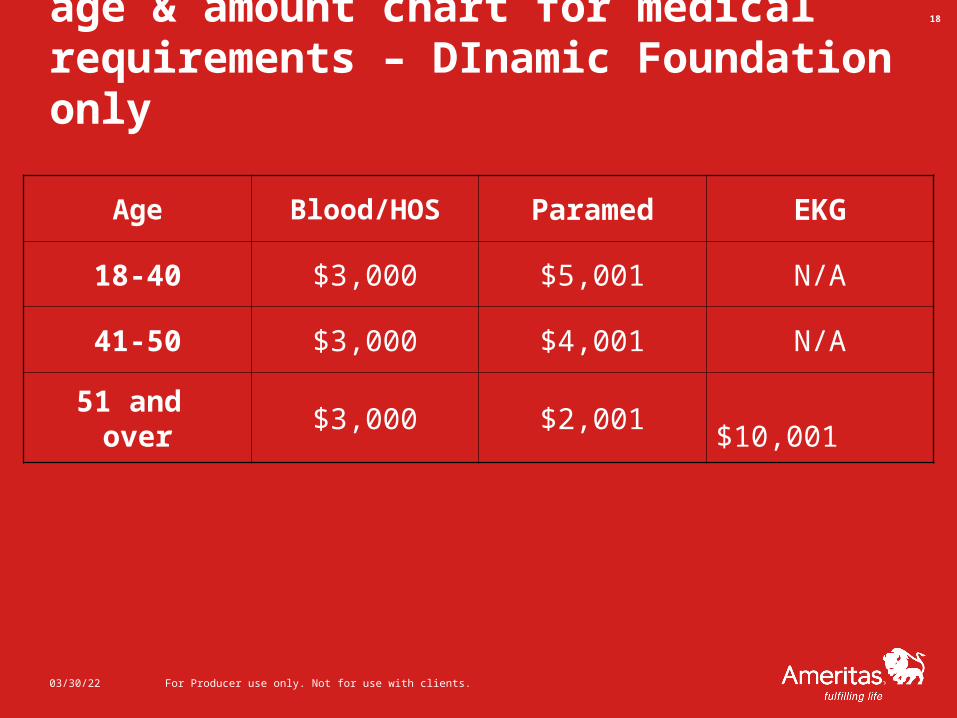

age & amount chart for medical requirements – DInamic Foundation only

Age Blood/HOS Paramed EKG

18-40 $3,000 $5,001 N/A

41-50 $3,000 $4,001 N/A

51 and over

$3,000 $2,001 $10,001

04/19/23 For Producer use only. Not for use with clients.

18

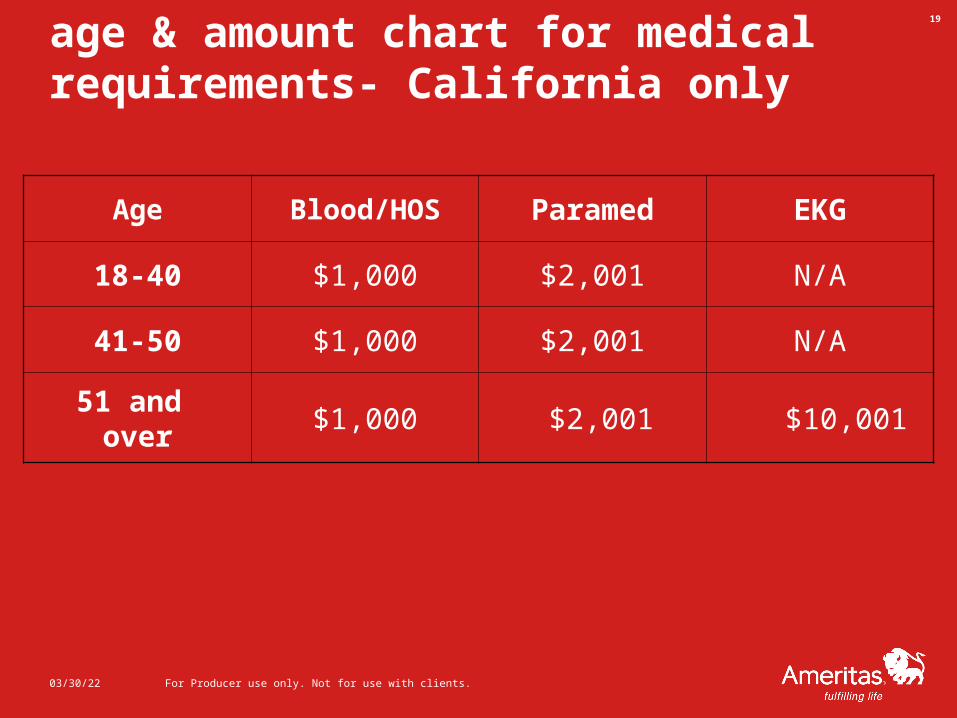

age & amount chart for medical requirements- California only

Age Blood/HOS Paramed EKG

18-40 $1,000 $2,001 N/A

41-50 $1,000 $2,001 N/A

51 and over

$1,000 $2,001 $10,001

04/19/23 For Producer use only. Not for use with clients.

19

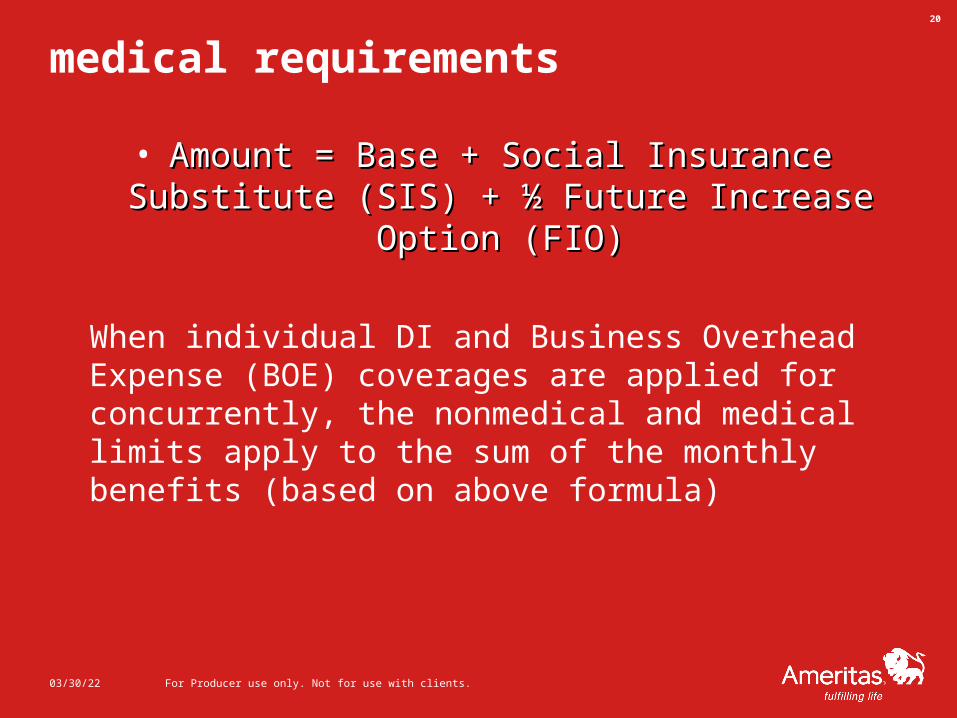

medical requirements

• Amount = Base + Social Insurance Substitute (SIS) + Amount = Base + Social Insurance Substitute (SIS) + ½ Future Increase Option (FIO)½ Future Increase Option (FIO)

04/19/23 For Producer use only. Not for use with clients.

20

When individual DI and Business Overhead Expense (BOE) coverages are applied for concurrently, the nonmedical and medical limits apply to the sum of the monthly benefits (based on above formula)

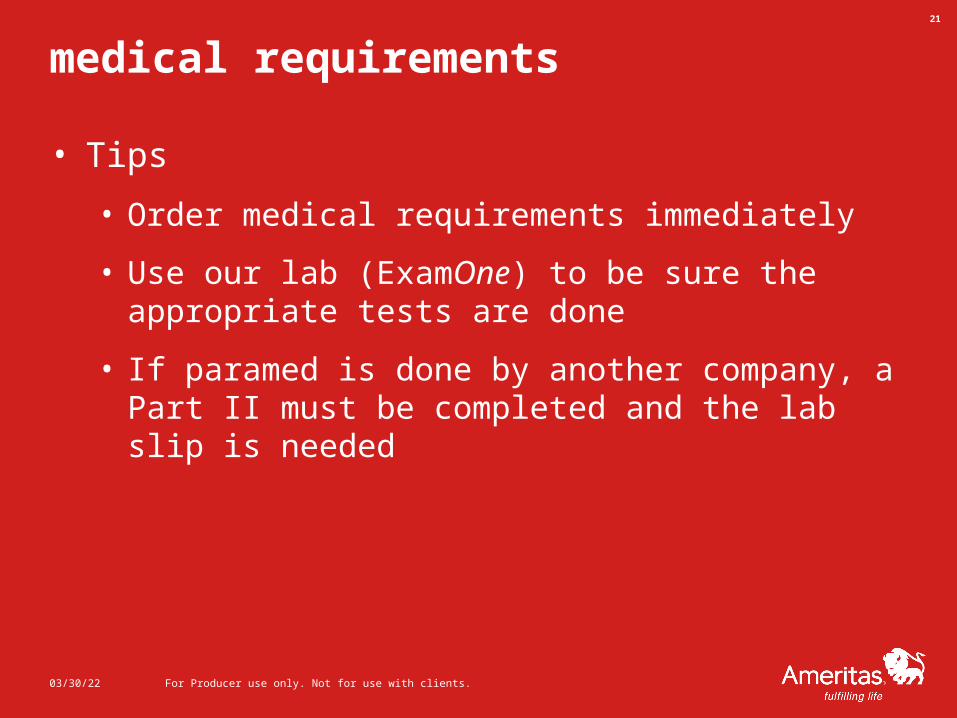

medical requirements

• Tips

• Order medical requirements immediately

• Use our lab (ExamOne) to be sure the appropriate tests are done

• If paramed is done by another company, a Part II must be completed and the lab slip is needed

04/19/23 For Producer use only. Not for use with clients.

21

medical requirements

• Tips, continued

• Use authorized providers for paramed exams

• Normally, an Attending Physician Statement (APS) is ordered to make an underwriting determination. These generally are ordered by the New Business Representative based on the recommendation from the underwriter

04/19/23 For Producer use only. Not for use with clients.

22

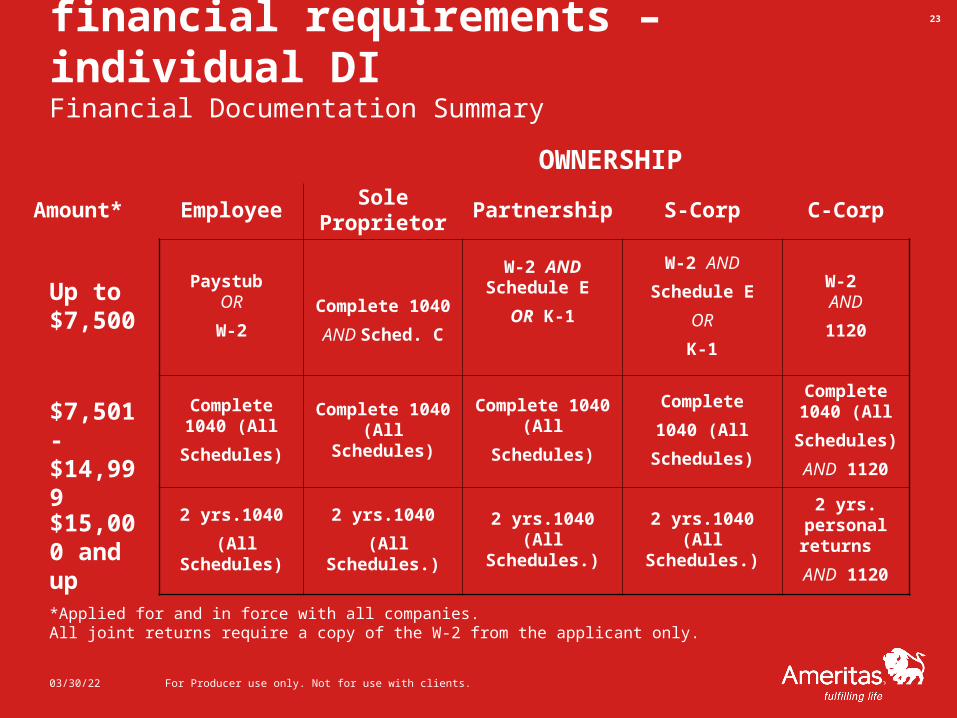

financial requirements – individual DIFinancial Documentation Summary

EmployeeSole

ProprietorPartnership S-Corp C-Corp

Paystub OR

W-2

Complete 1040

AND Sched. C

W-2 AND Schedule E

OR K-1

W-2 AND

Schedule E

OR

K-1

W-2 AND

1120

Complete 1040 (All

Schedules)

Complete 1040 (All Schedules)

Complete 1040 (All

Schedules)

Complete

1040 (All

Schedules)

Complete 1040 (All

Schedules)

AND 1120

2 yrs.1040

(All Schedules)

2 yrs.1040

(All Schedules.)

2 yrs.1040 (All Schedules.)

2 yrs.1040 (All Schedules.)

2 yrs. personal returns

AND 1120

04/19/23 For Producer use only. Not for use with clients.

23

OWNERSHIP

Amount*

Up to $7,500

$7,501-$14,999

$15,000 and up

*Applied for and in force with all companies.All joint returns require a copy of the W-2 from the applicant only.

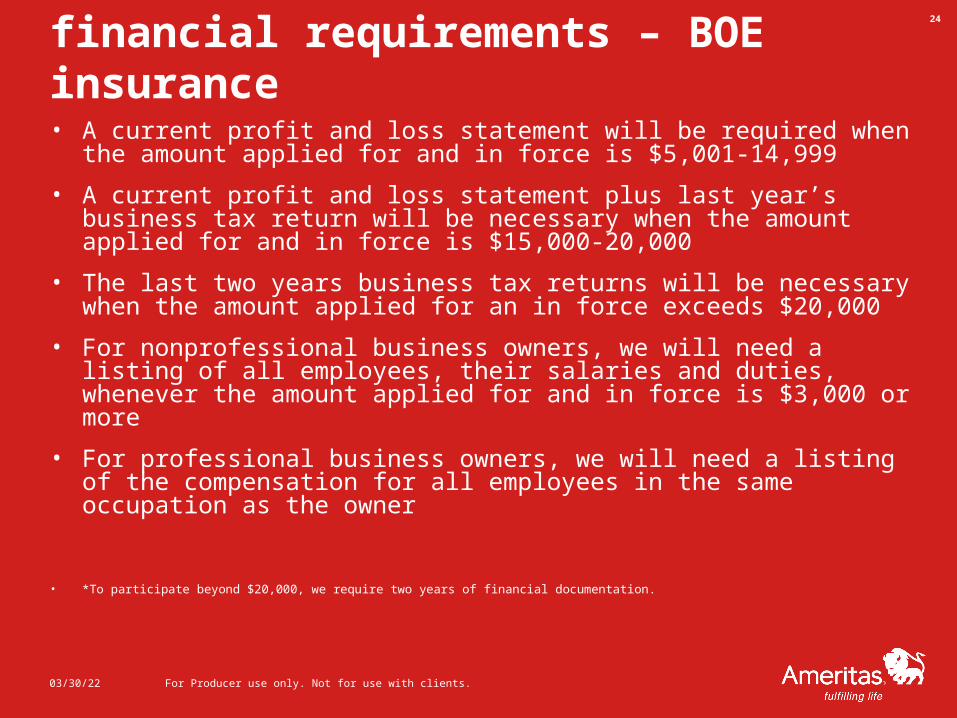

financial requirements – BOE insurance

• A current profit and loss statement will be required when the amount applied for and in force is $5,001-14,999

• A current profit and loss statement plus last year’s business tax return will be necessary when the amount applied for and in force is $15,000-20,000

• The last two years business tax returns will be necessary when the amount applied for an in force exceeds $20,000

• For nonprofessional business owners, we will need a listing of all employees, their salaries and duties, whenever the amount applied for and in force is $3,000 or more

• For professional business owners, we will need a listing of the compensation for all employees in the same occupation as the owner

• *To participate beyond $20,000, we require two years of financial documentation.

04/19/23 For Producer use only. Not for use with clients.

24

financial requirements – BOE insurance

04/19/23 For Producer use only. Not for use with clients.

25

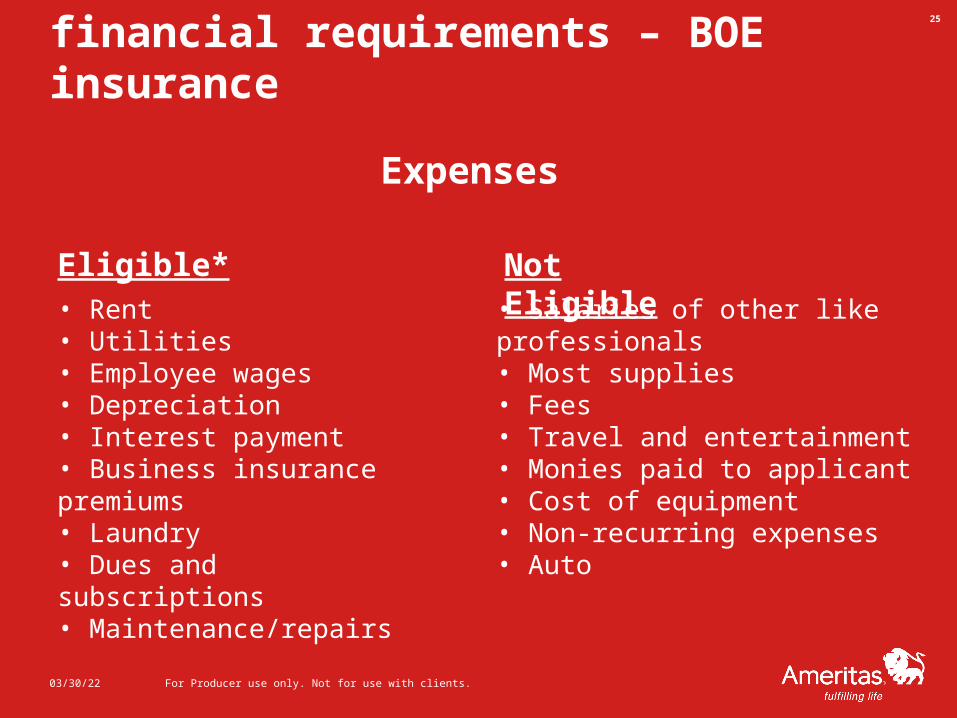

Expenses

Eligible* Not Eligible• Rent• Utilities• Employee wages• Depreciation• Interest payment• Business insurance premiums• Laundry• Dues and subscriptions• Maintenance/repairs

• Salaries of other like professionals• Most supplies• Fees• Travel and entertainment• Monies paid to applicant• Cost of equipment• Non-recurring expenses• Auto

how to speed up the underwriting process

• Applications

• Medical Requirements

• Financial Requirements

• Cover Letter

• DI EZ App Teleunderwriting Process

04/19/23 For Producer use only. Not for use with clients.

26

applications

• Complete the proper application in full

• Application and accompanying illustration should

match

• Complete Part II, even when paramed is required

• Inform applicant of Personal History Interview (PHI)

04/19/23 For Producer use only. Not for use with clients.

27

medical requirements

• Order medical requirements ASAP

• Amount = Base + SIS + ½ FIO

• Stay involved with and follow up on medical requirements

• Check Client Service System (CSS) for status

• Contact paramed service

04/19/23 For Producer use only. Not for use with clients.

28

financial requirements

• Consider contacting client’s accountant, if appropriate and with his/her permission

• Provide appropriate financial documentation with the application

04/19/23 For Producer use only. Not for use with clients.

29

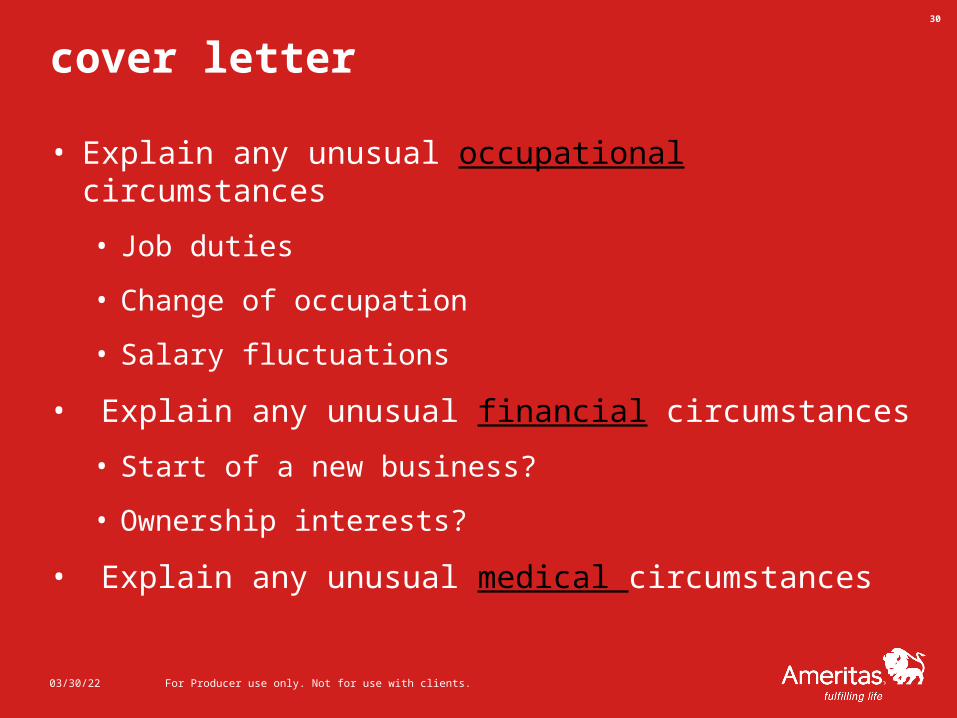

cover letter

• Explain any unusual occupational circumstances

• Job duties

• Change of occupation

• Salary fluctuations

• Explain any unusual financial circumstances

• Start of a new business?

• Ownership interests?

• Explain any unusual medical circumstances

04/19/23 For Producer use only. Not for use with clients.

30

cover letter

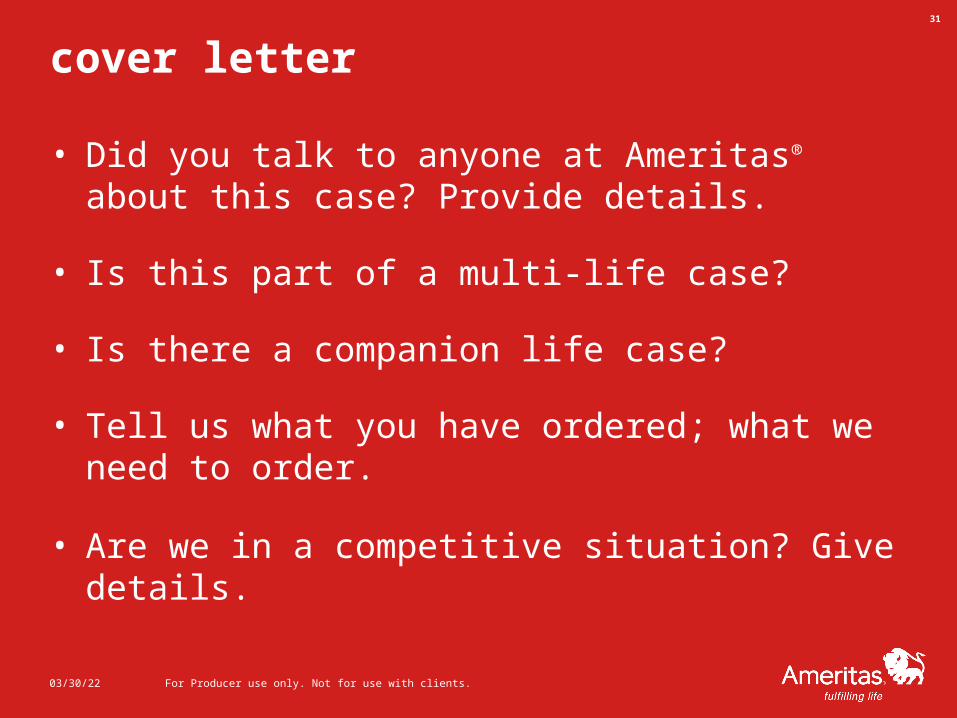

• Did you talk to anyone at Ameritas® about this case? Provide details.

• Is this part of a multi-life case?

• Is there a companion life case?

• Tell us what you have ordered; what we need to order.

• Are we in a competitive situation? Give details.

04/19/23 For Producer use only. Not for use with clients.

31

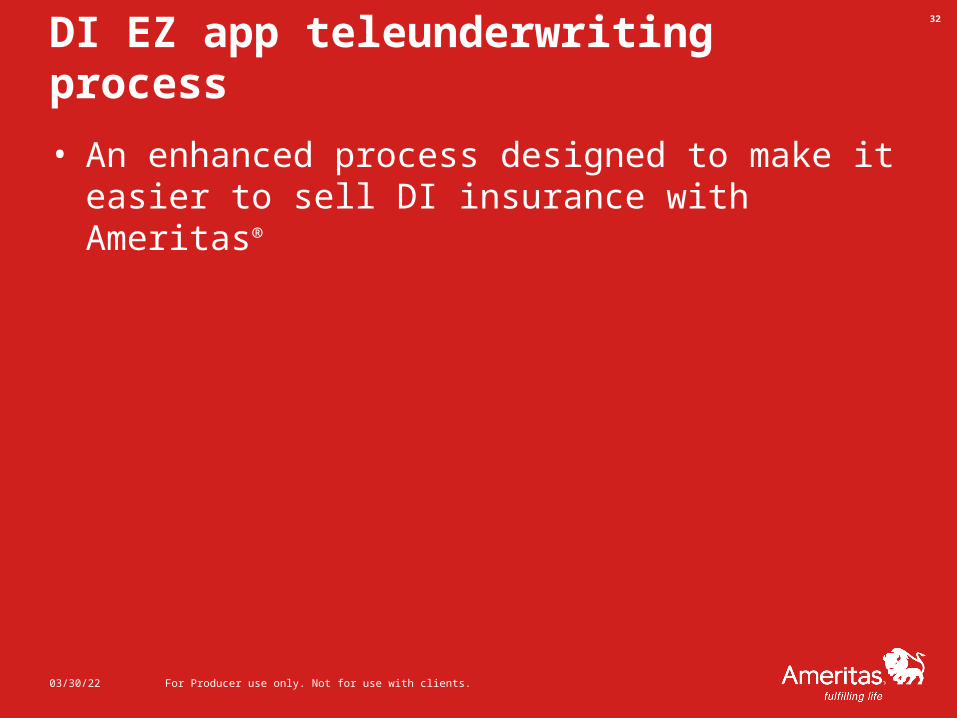

DI EZ app teleunderwriting process

• An enhanced process designed to make it easier to sell DI insurance with Ameritas®

04/19/23 For Producer use only. Not for use with clients.

32

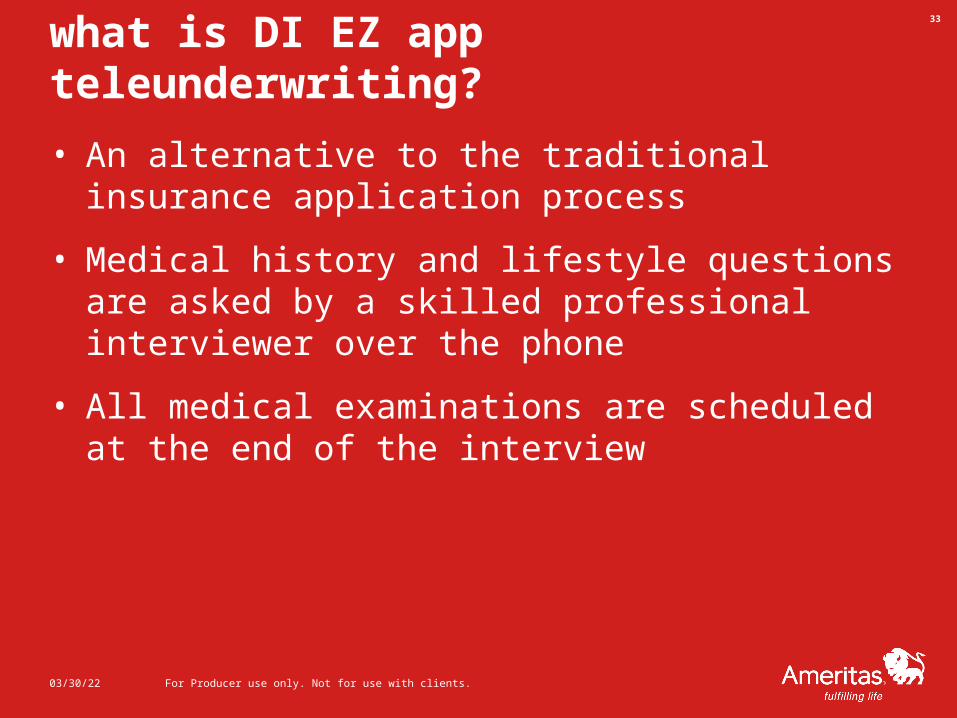

what is DI EZ app teleunderwriting?

• An alternative to the traditional insurance application process

• Medical history and lifestyle questions are asked by a skilled professional interviewer over the phone

• All medical examinations are scheduled at the end of the interview

04/19/23 For Producer use only. Not for use with clients.

33

what DI EZ app teleunderwriting offers

• EZ App speeds the processing of applications. It does this through:

• Better collection of necessary data to make the underwriting decision

• Use of other underwriting tools to validate the medical history

• Reduces the dependence on APSs

04/19/23 For Producer use only. Not for use with clients.

34

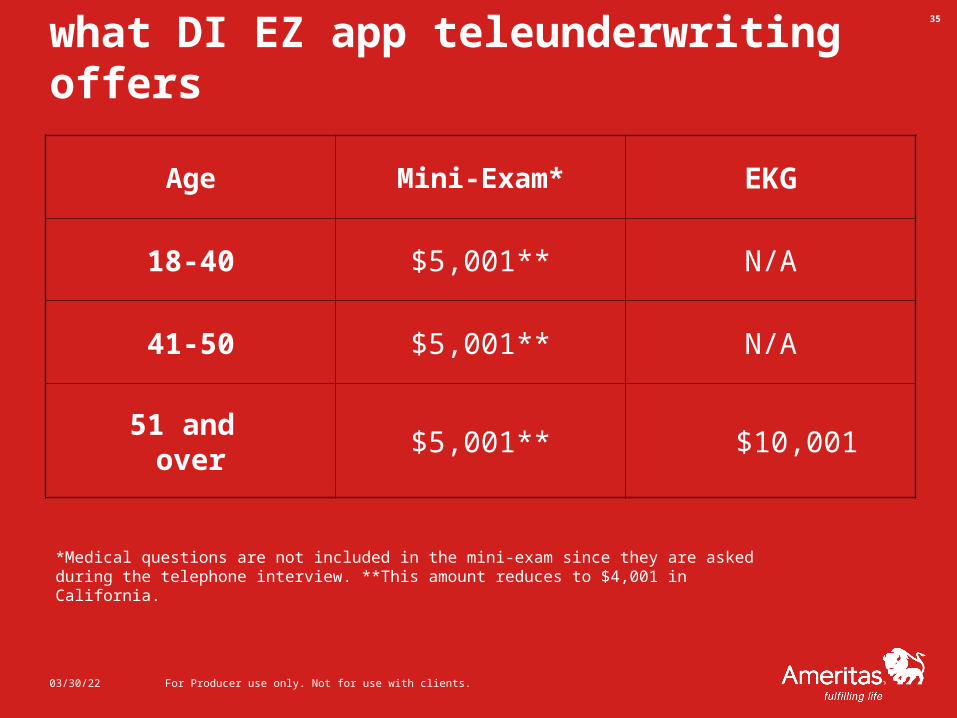

what DI EZ app teleunderwriting offers

Age Mini-Exam* EKG

18-40 $5,001** N/A

41-50 $5,001** N/A

51 and over

$5,001** $10,001

04/19/23 For Producer use only. Not for use with clients.

35

*Medical questions are not included in the mini-exam since they are asked during the telephone interview. **This amount reduces to $4,001 in California.

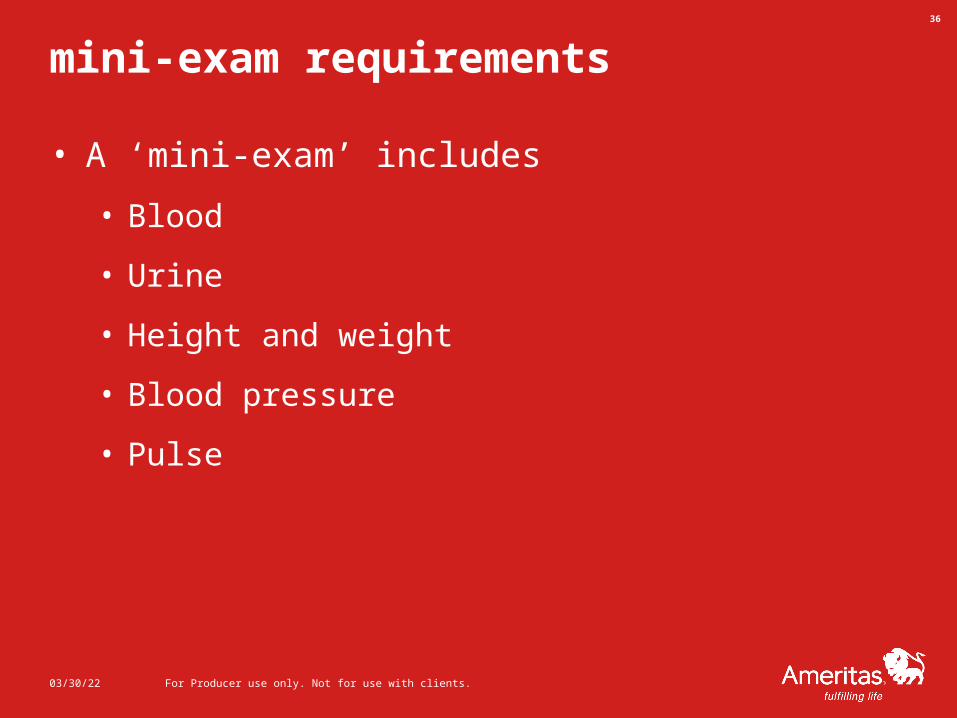

mini-exam requirements

• A ‘mini-exam’ includes

• Blood

• Urine

• Height and weight

• Blood pressure

• Pulse

04/19/23 For Producer use only. Not for use with clients.

36

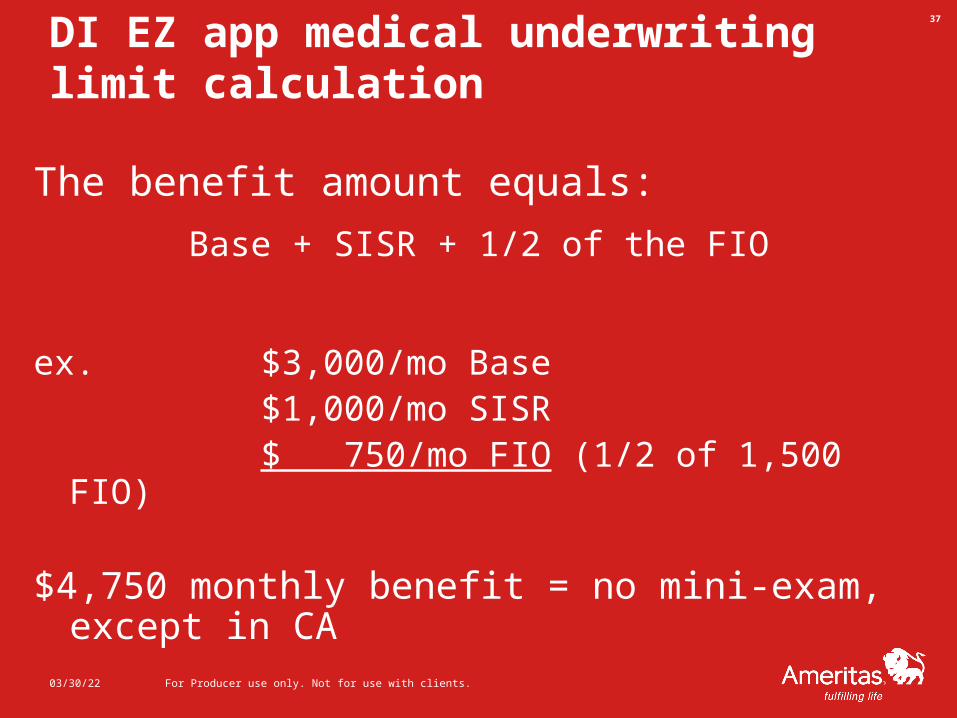

DI EZ app medical underwriting limit calculation

04/19/23 For Producer use only. Not for use with clients.

37

The benefit amount equals:

Base + SISR + 1/2 of the FIO

ex. $3,000/mo Base $1,000/mo SISR

$ 750/mo FIO (1/2 of 1,500 FIO)

$4,750 monthly benefit = no mini-exam, except in CA

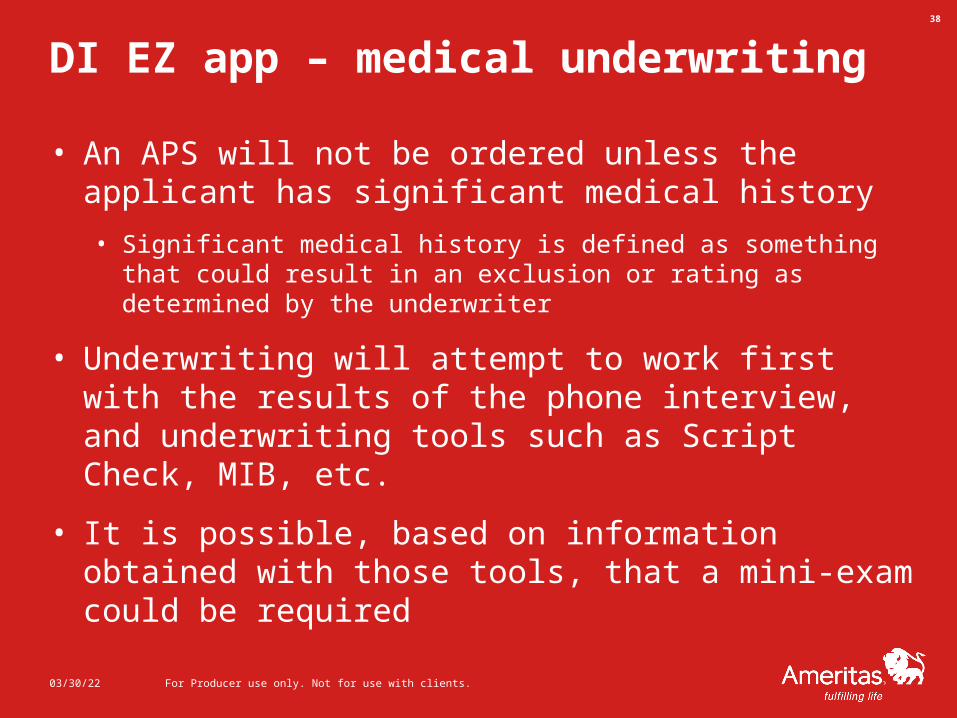

DI EZ app – medical underwriting

• An APS will not be ordered unless the applicant has significant medical history

• Significant medical history is defined as something that could result in an exclusion or rating as determined by the underwriter

• Underwriting will attempt to work first with the results of the phone interview, and underwriting tools such as Script Check, MIB, etc.

• It is possible, based on information obtained with those tools, that a mini-exam could be required

04/19/23 For Producer use only. Not for use with clients.

38

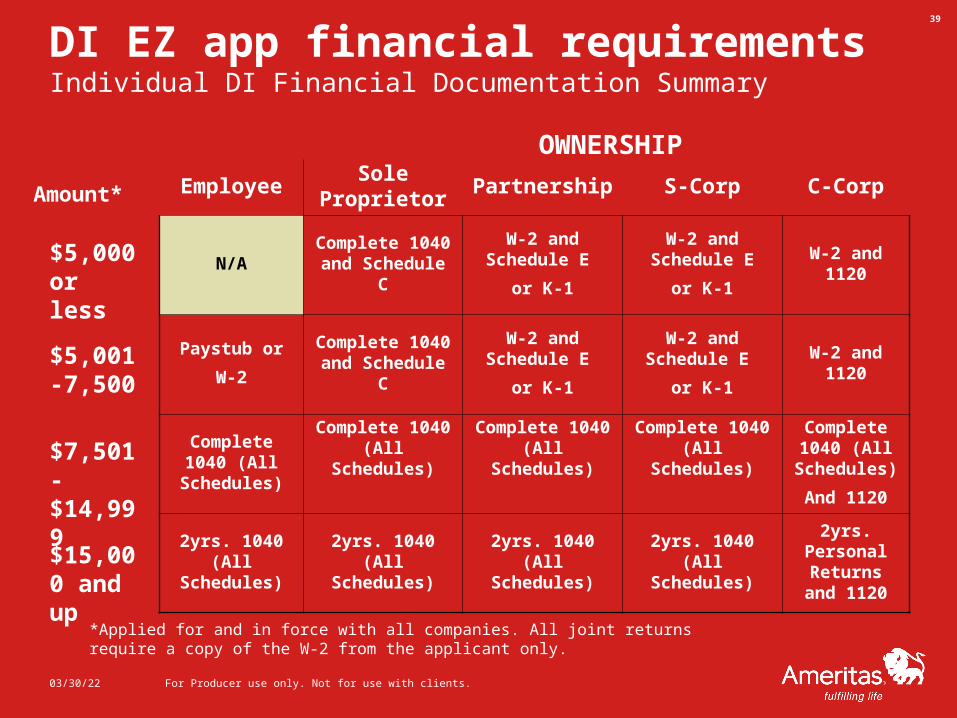

DI EZ app financial requirementsIndividual DI Financial Documentation Summary

EmployeeSole

ProprietorPartnership S-Corp C-Corp

N/AComplete 1040 and Schedule C

W-2 and Schedule E

or K-1

W-2 and Schedule E

or K-1

W-2 and 1120

Paystub or

W-2

Complete 1040 and Schedule C

W-2 and Schedule E

or K-1

W-2 and Schedule E

or K-1

W-2 and 1120

Complete 1040 (All Schedules)

Complete 1040 (All Schedules)

Complete 1040 (All Schedules)

Complete 1040 (All Schedules)

Complete 1040 (All

Schedules)

And 1120

2yrs. 1040 (All Schedules)

2yrs. 1040 (All Schedules)

2yrs. 1040 (All Schedules)

2yrs. 1040 (All Schedules)

2yrs. Personal

Returns and 1120

04/19/23 For Producer use only. Not for use with clients.

39

OWNERSHIP

Amount*

$5,000 or less

$5,001-7,500

$7,501 - $14,999

$15,000 and up

*Applied for and in force with all companies. All joint returns require a copy of the W-2 from the applicant only.

DI EZ app teleunderwriting

• Not to be used as a “dumping ground” for incomplete applications

• Not a way to avoid knowing about your client’s financial or health history

• “Field underwriting” is still important

04/19/23 For Producer use only. Not for use with clients.

40

expected results

• Reduce policy issue time

• Quicker turnaround time when scheduling and obtaining exam results

• Reduce the number of APSs required

• Reduce number of incomplete applications

• Improve customer satisfaction

• Medical & lifestyle questions are asked only once

• Greater comfort level providing medical and lifestyle information over the phone

• Improve placement rate

• Obtain more consistent and reliable information for underwriting decisions

• Less time for buyer’s remorse

• Increased sales

• Repeat business due to improvement in policy issue time

• Agents not selling DI might begin doing so if the process is easier

• Agents spend more time selling and less time underwriting

04/19/23 For Producer use only. Not for use with clients.

41

conclusions

• Underwriting is a partnership between the field and Ameritas®

• Full disclosure is a responsibility and the best way to expedite policy issue

• Proper authorization/confidentiality is of paramount importance

• Ameritas® is dedicated to helping you place every case possible.

04/19/23 For Producer use only. Not for use with clients.

42

questions?

04/19/23 For Producer use only. Not for use with clients.

43

key contacts

• Your Agency or Brokerage Manager

• Your Ameritas® Sales Development team

• Your GSI Regional Director

• The DI Product Management team

04/19/23 For Producer use only. Not for use with clients.

44