Embed Size (px)

Citation preview

The importance of Energy Efficiency for Medium Enterprises

Mark Liptrot – Group Sustainability Manager, Afripack

PSEE Conference 11November 2015, Maharani Hotel, Durban, South Africa

INTRODUCTION

2

• Afripack was founded in 1933 in Cape Town as Paper Sacks (SA). Now spreading throughout Africa, it has two main product lines:

• Industrial Flexibles - the supply of paper- and plastic-based printed products for the industrial packaging and roof insulation markets, eg cement bags and Sisalation®;

• Consumer Flexibles - supplying flexible packaging and a variety of label types, including wraparound, shrink and stretch for the beverage, cosmetic , food and pharmaceutical markets.

• The SA plants are based in Pinetown (2), Mobeni and Brits

• This study concentrates on the Pinetown Flexibles site, which had the first PSEE-funded energy audit in July 2014

INTRODUCTION

3

6 Mahogany Rd Mahogany Ridge Pinetown

2014

THE ONLY WAY FORWARD… …BE SUSTAINABLE!

ENOUGH FOR ALL, FOREVER

AFRIPACK’S COMMITMENT TO SUSTAINABILITY

SUST

AIN

AB

LE S

OU

RC

ING

O

F R

AW

MA

TER

IALS

CA

RB

ON

FO

OTP

RIN

T R

EDU

CTI

ON

WA

STE

MIN

IMIS

ATI

ON

REC

YCLA

BIL

ITY

RESPONSIBLE PACKAGING INITIATIVES

RESPONSIBLE PACKAGING IS BASED ON 4 PRINCIPLES:

• We set up “green teams” at each of the Afripack sites to monitor and have reported on energy, water, waste and carbon footprint each month since 2011

• We have been working with the CSIR and NBI on ways to improve our productivity. Engineering interns from the CSIR started at 3 sites between June 2013 and Feb 2014.

• Energy audits were conducted between July 2014 and March 2015 at the 3 sites in KZN, arranged by the NBI

• They have outlined where we could make energy, water and material savings

AFRIPACK’S STRATEGY:

THE AUDIT METHODOLOGY

7

• One week on site

• Tariff Analysis

• Factory Electrical Usage by Area

• Energy Monitoring and Targeting

• Process analysis

From the above, the following were deduced:

• Key Energy Savings Opportunities

• Other savings, eg waste control, water use

THE AUDIT FINDINGS

8

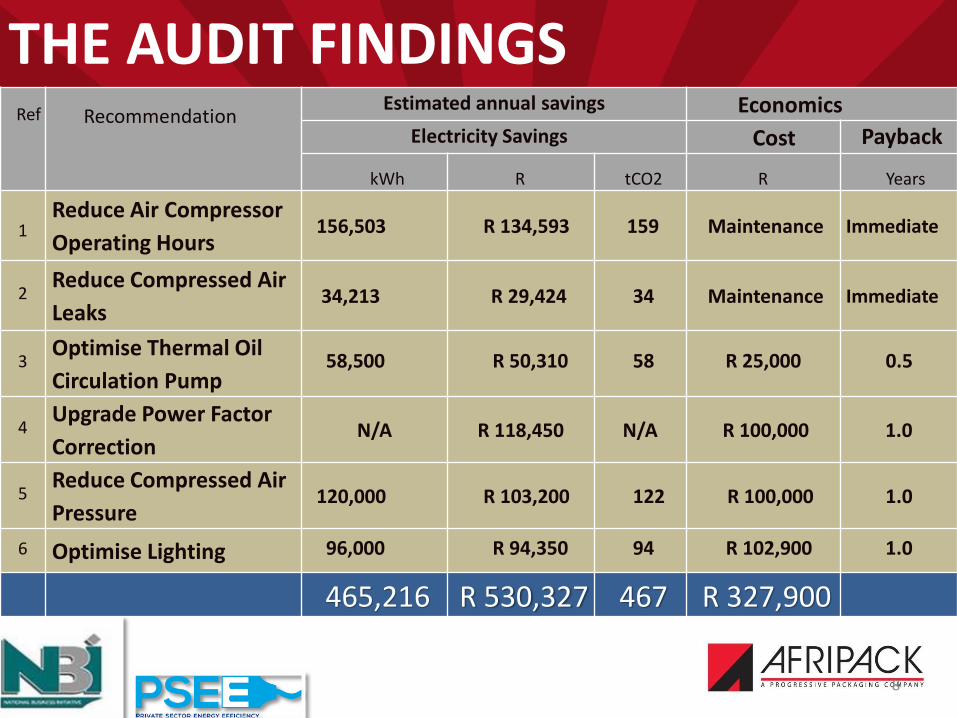

Ref

Recommendation Estimated annual savings Economics

Electricity Savings Cost

Payback

kWh

R

tCO2

R

Years

1

Reduce Air Compressor

Operating Hours 156,503 R 134,593 159 Maintenance Immediate

2 Reduce Compressed Air

Leaks 34,213 R 29,424 34 Maintenance Immediate

3 Optimise Thermal Oil

Circulation Pump 58,500 R 50,310 58 R 25,000 0.5

4 Upgrade Power Factor

Correction N/A R 118,450 N/A R 100,000 1.0

5 Reduce Compressed Air

Pressure 120,000 R 103,200 122 R 100,000 1.0

6 Optimise Lighting 96,000 R 94,350 94 R 102,900 1.0

465,216 R 530,327 467 R 327,900

THE AUDIT FINDINGS

9

Ref

Recommendation

Estimated annual savings Economics

Fuel Savings Cost Payback

kg

R

tCO2

R

Years

1 Heat Recovery 1,815,600 R 2,115,622 2,723 R 500,000 0.25

2 Fuel Swop from

LPG to Paraffin 0 R 1,765,262 N/A R 500,000 0.30

Total

1,815,600

R 3,880,884 2,723 R 1,000,000 0.50

THE AUDIT FINDINGS

10

11

The compressor findings

• We have reduced the operating hours of the compressor, it gets shut down weekends when not required, we also ensured that it is ramped down when the demand is low

• Programme began to trace and fix the compressor leaks

• A programme has started to replace all air-driven pumps with those that work on a lower bar rating – 26 out of 38 so far

• Once complete, we can reduce the air pressure

THE AFRIPACK RESPONSES

12

Lighting

• We have optimised all outdoor lighting to LED and done away with 400W sodium/metal halide lights

• Internally we have converted the majority of the lights to T5 fluorescent tubes, and we are over the required lux level at work stations and around machines, as this is an operational requirement

THE AFRIPACK RESPONSES

13

Power factor correction

• Power factor correction is a project also on the cards, we have removed some machinery and our power factor has improved to an acceptable 0.98

• We will relook PF correction after we have installed our new machines by 2017.

THE AFRIPACK RESPONSES

14

Fuel swop from LPG to paraffin

• We didn’t do the fuel swop – LPG is a cleaner burning fuel and the burners require less maintenance - what we did do is renegotiate our supply price (saving of R3.5/L)

• In December we will do efficiency tests on our burners and change our supplier for a bigger reduction in cost (by R6/L)

• After the tests and optimisation we expect to save somewhere in the region of R2mil/annum – this was not an audit recommendation, but the actions we did were sparked from this finding

•

THE AFRIPACK RESPONSES

15

Heat recovery

• We didn’t do the recommendation but because of it we looked at our ventilation system, we found flaws in the design and we are currently rectifying; this will stop us from dumping all the hot air thus requiring less heating due to circulation of used hot air. This will also result in reducing the burner temperature which is a further gas saving.

• We are doing a heat recovery exercise for our curing room so that we don’t use electric elements, and this is a project for implementation in 2017.

THE AFRIPACK RESPONSES

16

There was an immediate response to

the changes in our energy

management – as can be seen

from the following slides…

THE AFRIPACK RESULTS

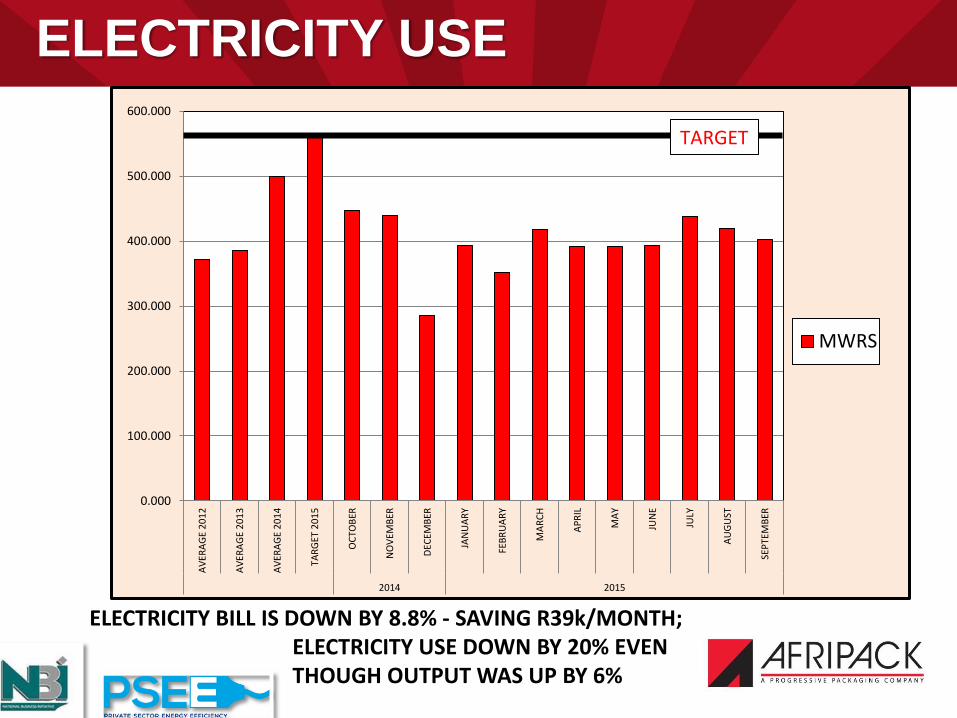

ELECTRICITY USE

0.000

100.000

200.000

300.000

400.000

500.000

600.000

AV

ERA

GE

20

12

AV

ERA

GE

20

13

AV

ERA

GE

20

14

TAR

GET

20

15

OC

TOB

ER

NO

VEM

BER

DEC

EMB

ER

JAN

UA

RY

FEB

RU

AR

Y

MA

RC

H

AP

RIL

MA

Y

JUN

E

JULY

AU

GU

ST

SEP

TEM

BER

2014 2015

MWRS

TARGET

ELECTRICITY BILL IS DOWN BY 8.8% - SAVING R39k/MONTH; ELECTRICITY USE DOWN BY 20% EVEN THOUGH OUTPUT WAS UP BY 6%

ELECTRICITY USE PER TONNE PRODUCT

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

AV

ERA

GE

20

12

AV

ERA

GE

20

13

AV

ERA

GE

20

14

TAR

GET

20

15

OC

TOB

ER

NO

VEM

BER

DEC

EMB

ER

JAN

UA

RY

FEB

RU

AR

Y

MA

RC

H

AP

RIL

MA

Y

JUN

E

JULY

AU

GU

ST

SEP

TEM

BER

2014 2015

MWHR/TONNEPRODUCT

TARGET

24% BELOW 2014 AVERAGE

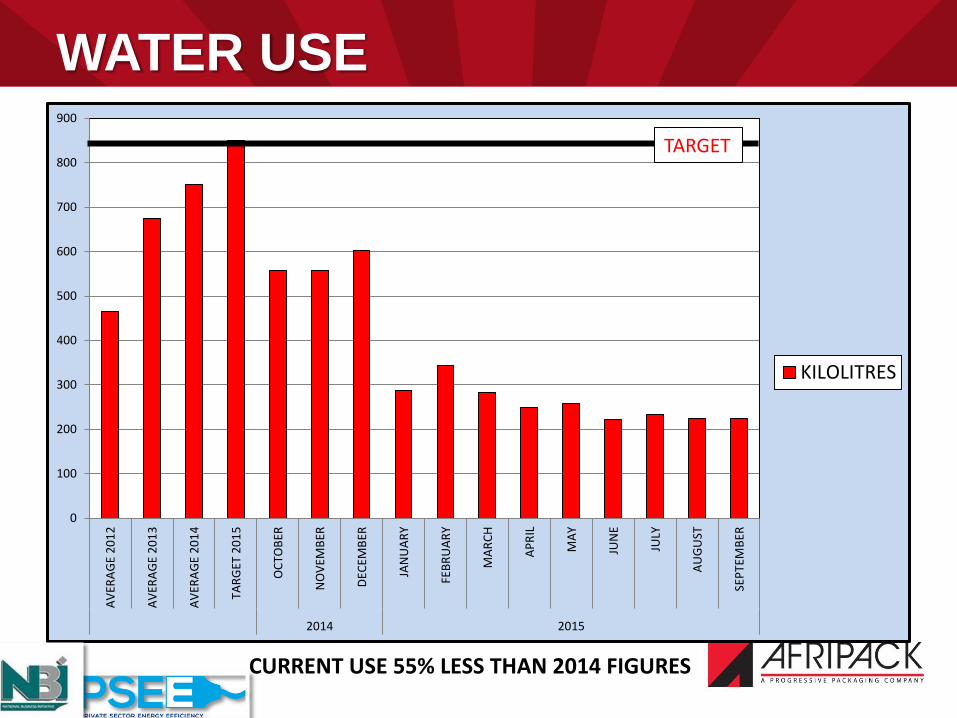

WATER USE

0

100

200

300

400

500

600

700

800

900A

VER

AG

E 2

01

2

AV

ERA

GE

20

13

AV

ERA

GE

20

14

TAR

GET

20

15

OC

TOB

ER

NO

VEM

BER

DEC

EMB

ER

JAN

UA

RY

FEB

RU

AR

Y

MA

RC

H

AP

RIL

MA

Y

JUN

E

JULY

AU

GU

ST

SEP

TEM

BER

2014 2015

KILOLITRES

CURRENT USE 55% LESS THAN 2014 FIGURES

TARGET

WATER USE PER TONNE PRODUCT

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

AV

ERA

GE

20

12

AV

ERA

GE

20

13

AV

ERA

GE

20

14

TAR

GET

20

15

OC

TOB

ER

NO

VEM

BER

DEC

EMB

ER

JAN

UA

RY

FEB

RU

AR

Y

MA

RC

H

AP

RIL

MA

Y

JUN

E

JULY

AU

GU

ST

SEP

TEM

BER

2014 2015

56% LOWER THAN 2014 USAGE

TARGET

CARBON FOOTPRINT – TOTAL

83% OF TOTAL FOOTPRINT IS ESKOM ELECTRICITY

14%

83%

3%

TOTAL CARBON FOOTPRINT ACF KZN 2015

SCOPE 1

SCOPE 2

SCOPE 3

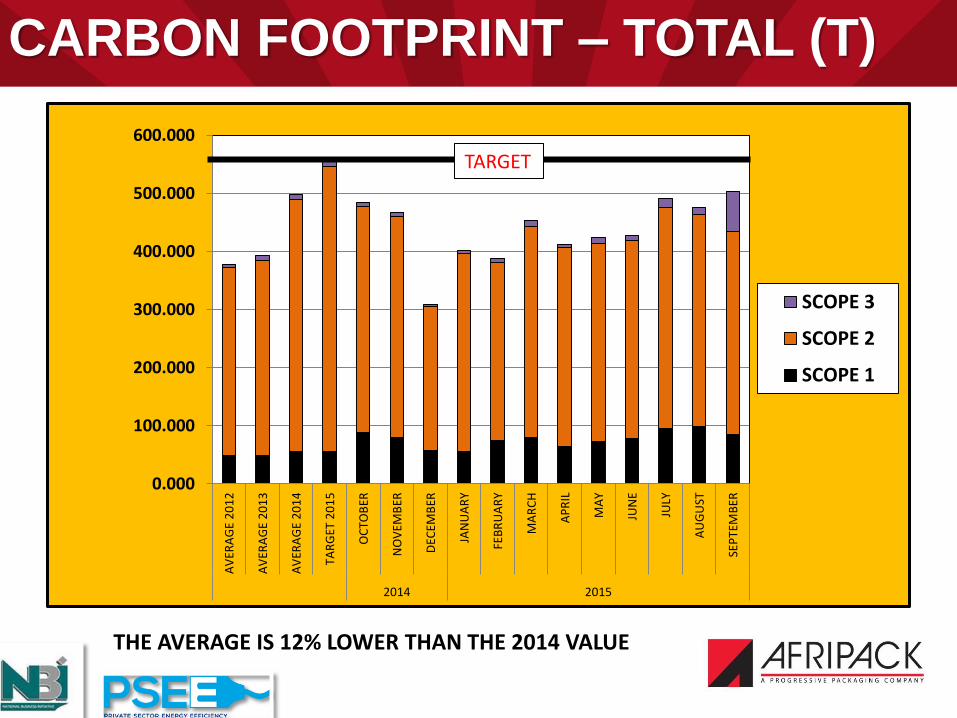

CARBON FOOTPRINT – TOTAL (T)

0.000

100.000

200.000

300.000

400.000

500.000

600.000

AV

ERA

GE

20

12

AV

ERA

GE

20

13

AV

ERA

GE

20

14

TAR

GET

20

15

OC

TOB

ER

NO

VEM

BER

DEC

EMB

ER

JAN

UA

RY

FEB

RU

AR

Y

MA

RC

H

AP

RIL

MA

Y

JUN

E

JULY

AU

GU

ST

SEP

TEM

BER

2014 2015

SCOPE 3

SCOPE 2

SCOPE 1

THE AVERAGE IS 12% LOWER THAN THE 2014 VALUE

TARGET

CARBON FOOTPRINT PER T product

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40A

VER

AG

E 2

012

AV

ERA

GE

20

13

AV

ERA

GE

20

14

TAR

GET

20

15

OC

TOB

ER

NO

VEM

BER

DEC

EMB

ER

JAN

UA

RY

FEB

RU

AR

Y

MA

RC

H

AP

RIL

MA

Y

JUN

E

JULY

AU

GU

ST

SEP

TEM

BER

2014 2015

23% LOWER THAN IN 2014

TARGET

SUMMARY OF RESULTS 2014

AVERAGE OVER

2014: ACF KZN ELECTRICITY

(MWhr/T)

WATER

(Kl/T)

WASTE

(DIVERSION

FROM LANDFILL)

CO2

FOOTPRINT (tCO2e/T product)

ON OR

ABOVE 2013

RESULT

-8%

UP TO 5%

WITHIN 2013

RESULT

+3%

MORE THAN

5% OFF 2013

RESULT

+6%

-11%

SUMMARY OF RESULTS 2015

AVERAGE OVER

2015: ACF KZN ELECTRICITY

(MWhr/T)

WATER

(Kl/T)

WASTE

(DIVERSION

FROM LANDFILL)

CO2

FOOTPRINT (tCO2e/T product)

ON OR

ABOVE 2014

RESULT

-24%

-56%

+4.9%

-23%

UP TO 5%

WITHIN 2014

RESULT

MORE THAN

5% OFF 2014

RESULT