Embed Size (px)

Citation preview

©2012

THE IMPORTANCE OF AUDITING IN AN ANTI-FRAUD WORLD

ACCOUNTS RECEIVABLE FRAUD

This session covers many aspects of accounts receivable fraud, which come directly from the

speaker’s life experiences investigating fraud cases in state and local government in the state of

Washington. Topics include segregation of employee duties and monitoring, off-book and on-

book accounts receivables, check-for-cash substitution and lapping schemes, other account

manipulations, eliminating customer accounts and fictitious account adjustments, and stealing

the statements.

JOSEPH R. DERVAES, CFE, ACFE FELLOW, CIA

President

Pacific Northwest Chapter/ACFE

Vaughn, WA

Joe retired after 42.5 years of audit service in 2006 as the Audit Manager for Special

Investigations for the Washington State Auditor’s Office. He was responsible for managing the

agency’s Fraud Program and participated in 730 fraud cases involving losses of $13 million

during his 20-year tenure in this position. In 2003, Joe received the ACFE’s coveted Donald R.

Cressey Award for his lifetime contributions to fraud detection and deterrence. He is the former

Chair of the Board of Regents and the ACFE Foundation’s Board of Directors, and the President

of the Pacific Northwest Chapter.

“Association of Certified Fraud Examiners,” “Certified Fraud Examiner,” “CFE,” “ACFE,” and the

ACFE Logo are trademarks owned by the Association of Certified Fraud Examiners, Inc. The contents of

this paper may not be transmitted, re-published, modified, reproduced, distributed, copied, or sold without

the prior consent of the author.

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 1

NOTES Introduction

Accounts receivable fraud schemes are quite common in

business today. Dishonest cashiers, accounting clerks, and

supervisors must continually manipulate the accounting and

financial records of the organization to conceal their

accounts receivable fraud schemes and the resulting

financial losses from everyone. Organizations often detect

the frauds when the employees cannot handle the

complexities of the charades they employ or do not pay

close attention to details when customers report

irregularities in their accounts. This fear of detection causes

employee stress. So, don’t be surprised if you observe the

accounts receivable staff under pressure but aren’t sure why

it’s happening.

The best way to detect accounts receivable fraud is to know

how the fraudsters conceal their schemes and then to focus

audit testing on at least these known methods. In this

session, the speaker discusses his life experiences dealing

with accounts receivable fraud in state agencies and local

governments in the state of Washington while managing his

agency’s statewide fraud program for more than two

decades. Accounts receivables exist in the public sector in a

wide variety of revenue streams including water, sewer,

garbage, and electricity utilities; personal and property

taxes; traffic fines and fees; printing services; catering

operations in food services; rentals of facilities and athletic

fields; and services among governments. The list is endless.

Small organizations might control one specific type of

revenue, such as a water utility district. But larger

organizations might operate one or more of these activities

as separate departments.

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 2

NOTES Class Outline

Part One: Internal Control Weaknesses

Deals with the system of internal controls and identifies

weaknesses that give employees the opportunity to

commit accounts receivable fraud and conceal it from

employers.

Part Two: Common Cash Receipt Fraud Schemes

Discusses two of the most common schemes fraudsters

use to conceal the misappropriation of revenue. The

employee most likely to succeed in committing these

frauds is a key supervisor who makes the daily bank

deposit without any monitoring or oversight by

managers. This individual manipulates the contents of

the daily bank deposit to commit this crime.

Part Three: Falsification of Accounting Records

Discusses how fraudsters manipulate the organization’s

accounting records to conceal fraud from their

employer. The same key employee identified above

falsifies accounting records to commit the crime.

Part Four: A Complex Accounts Receivable Fraud

Case Study

Concludes the session by reviewing a complex accounts

receivable fraud case study to bring everything together

and summarize what we’ve learned.

A key supervisor who makes the daily bank deposit is

the employee most likely to succeed in perpetrating a

fraud (in all of the above).

Part One: Internal Control Weaknesses

Every accounts receivable fraud report issued by my

organization reported on two major internal control issues.

They were:

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 3

NOTES Key employees do too much. An inadequate

segregation of duties is at the heart of their fraud

schemes. What amazed me the most was the number of

fraudsters who had access to and controlled all

revenue.

Managers do not monitor the work of these key

employees to determine if the organization’s

expectations were being met. These employees were

able to operate in secret while in plain view of everyone

within the organization.

Employees operate in secret while in plain sight of

everyone. Why?

Managers use “blind trust”:

Tell employees what to do.

Expect them to do it.

Never monitor their actions to see if

expectations are met.

Managers should use “trust but verify”:

Monitor employee actions.

Chinese saying: “It’s okay to trust employees,

just always keep one eye open!”

There are two types of employees—the doers and the

reviewers.

Every organization has “doers,” the first-line employees

who deal with customers on a daily basis. The organization

expects its “reviewers,” the supervisors, to monitor the

work of their subordinates to ensure they employ the

appropriate internal control procedures while processing

revenue from accounts receivable transactions. Most

internal controls focus on this relationship.

However, there are few internal controls designed for

managers to monitor the work of the reviewers in the same

way supervisors monitor the work of doers. To make things

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 4

NOTES worse, this key supervisor is usually in a position to make

the daily bank deposit without supervision by managers.

Some honest employees might never take advantage of this

internal control weakness, but others will eventually cross

the line from being honest employees to becoming

dishonest employees when they misappropriate revenue for

personal benefit. They manipulate the contents of the daily

bank deposit and falsify accounting records to conceal their

actions. Fraud perpetrators either ignore or compromise the

system of internal control. They simply don’t play by the

rules!

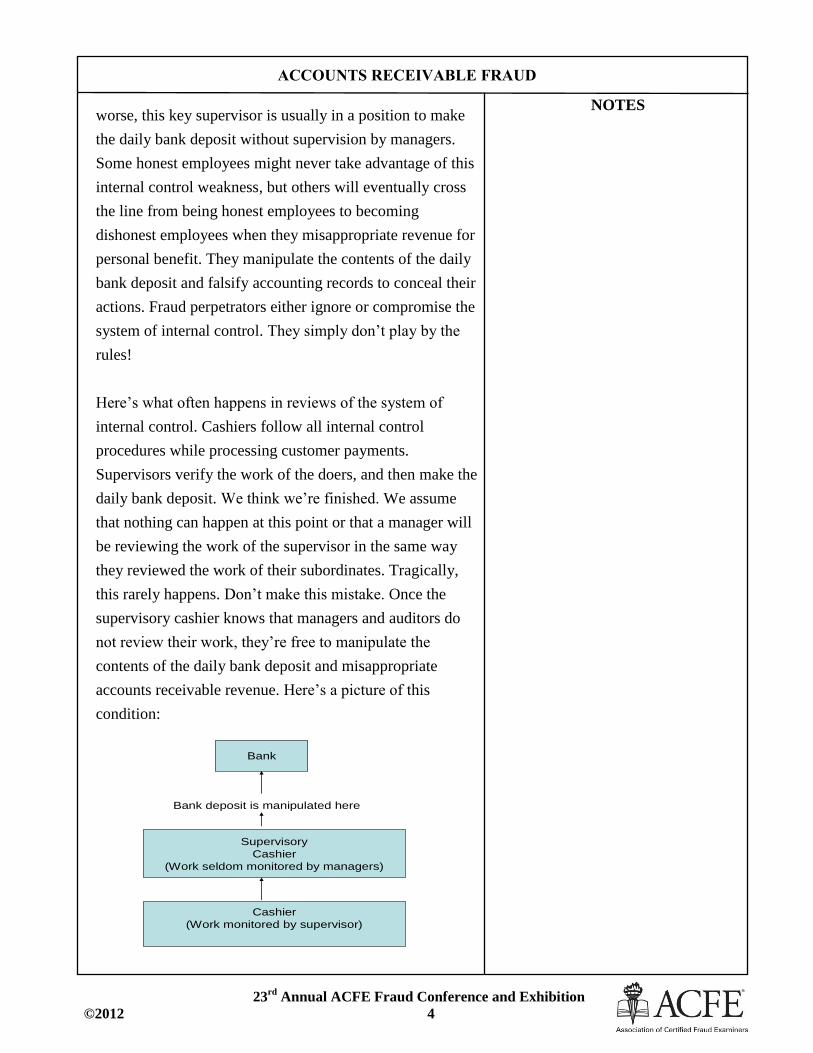

Here’s what often happens in reviews of the system of

internal control. Cashiers follow all internal control

procedures while processing customer payments.

Supervisors verify the work of the doers, and then make the

daily bank deposit. We think we’re finished. We assume

that nothing can happen at this point or that a manager will

be reviewing the work of the supervisor in the same way

they reviewed the work of their subordinates. Tragically,

this rarely happens. Don’t make this mistake. Once the

supervisory cashier knows that managers and auditors do

not review their work, they’re free to manipulate the

contents of the daily bank deposit and misappropriate

accounts receivable revenue. Here’s a picture of this

condition:

Bank deposit is manipulated here

Bank

Supervisory

Cashier

(Work seldom monitored by managers)

Cashier

(Work monitored by supervisor)

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 5

NOTES Every large revenue fraud that has occurred in the past,

every large revenue fraud that is currently ongoing that has

not yet been detected, and every large revenue fraud that

will ever occur in the future involves this internal control

failure. Therefore, the lack of monitoring the work of key

employees is the number one cause of revenue fraud

anywhere.

We must identify at-risk employees whose work habits

suggest they might commit fraud. They:

Come to work early or leave late.

Work nights and weekends.

Are seldom missing for leave or vacation.

Report to the office during brief absences.

Ask others to hold their work while they’re gone.

All of these elements demonstrate control of the work

environment. Fraud is hard work and requires concentration

and quiet. This is why most fraudulent accounts receivable

transactions are manipulated or recorded in the

organization’s accounting system before and after normal

work hours and on weekends.

Some small organizations maintain their financial records

on a personal computer. There are no internal controls in

the accounting system under these circumstances. If fraud

exists, you’ll find either missing or destroyed documents.

Other organizations only collect funds from customers with

current accounts receivable balances. They don’t have the

staff necessary to deal with delinquent accounts. So, they

send all delinquencies to a collection agency for further

processing. When funds have been collected from the

customer, the collection agency sends the money to the

organization. In most cases, these delinquent accounts

receivables are not recorded in the organization’s

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 6

NOTES accounting records or reported on its financial statements.

These off-book accounts receivable funds are a prime target

for fraudsters because managers do not pay an appropriate

level of attention to these potential revenue accounts.

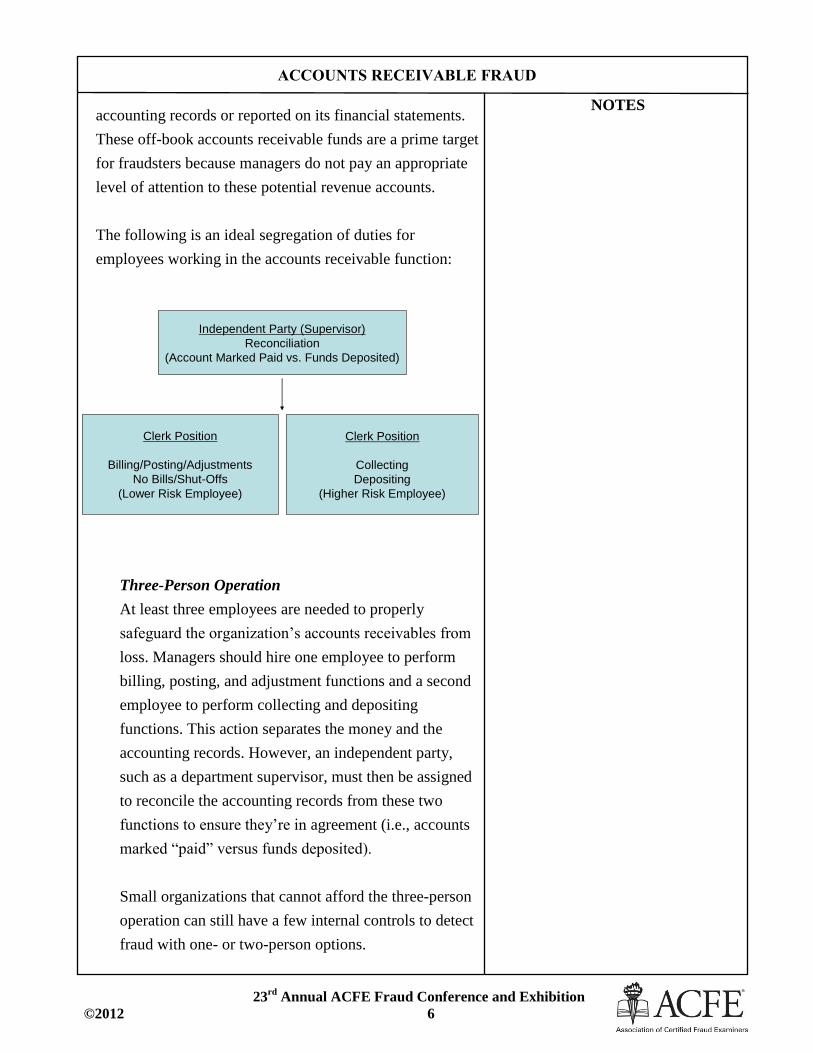

The following is an ideal segregation of duties for

employees working in the accounts receivable function:

Three-Person Operation

At least three employees are needed to properly

safeguard the organization’s accounts receivables from

loss. Managers should hire one employee to perform

billing, posting, and adjustment functions and a second

employee to perform collecting and depositing

functions. This action separates the money and the

accounting records. However, an independent party,

such as a department supervisor, must then be assigned

to reconcile the accounting records from these two

functions to ensure they’re in agreement (i.e., accounts

marked “paid” versus funds deposited).

Small organizations that cannot afford the three-person

operation can still have a few internal controls to detect

fraud with one- or two-person options.

Independent Party (Supervisor)

Reconciliation

(Account Marked Paid vs. Funds Deposited)

Clerk Position

Billing/Posting/Adjustments

No Bills/Shut-Offs

(Lower Risk Employee)

Clerk Position

Collecting

Depositing

(Higher Risk Employee)

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 7

NOTES One-Person Operation

Many small governments in my state employ only one

person to perform all cash receipting activities—

including accounts receivables—as well as all

disbursing functions. Yes, one person does everything.

The risk of fraud is tremendous. A manager must find

an independent party to monitor this employee’s work.

This person might be the mayor, a council member, or a

volunteer. It might also be a manager, executive

director, board member, or owner.

Two-Person Operation

A number of mid-size organizations are able to hire at

least two employees to work in the accounts receivable

function. Employee duties should be split between

billing, posting, and adjustment functions, and

collecting and depositing functions. But unlike a three-

person operation, no one is available to independently

reconcile the accounting records and determine if

accounts marked “paid” agree with funds deposited in

the bank. The challenge, as with a one-person

operation, is finding an independent party who can

monitor the operation. The next best alternative is to

have one of the accounts receivable employees

independently review the work of the other employee.

The question is: “How do you select the right

employee?”

The employee performing the billing, posting, and

adjustment function is the best person to perform this

reconciliation (i.e., the least fraud risk) because that

individual does not normally handle money. The

employee performing the collecting and depositing

function is a poor selection to perform this task (i.e., the

highest fraud risk) because they do handle money and

thus have the ability to conceal irregularities. This

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 8

NOTES person will either not perform the task or will perform it

in a perfunctory manner when there is no independent

party to review their work.

But, always remember that internal controls self-

destruct at lunch and on breaks when the record keeper

becomes a relief cashier (i.e., incompatible duties).

Secrets to Detecting Fraud in Accounts Receivable

Study the system of internal controls. Focus on key

employees who have too many duties and responsibilities,

especially when those duties are incompatible, such as

when cashiering and recordkeeping are involved in the

accounts receivable function. Determine if managers are

monitoring the duties of all key employees to ensure their

expectations are being met.

In a personal computer environment, fraud examiners

should develop tests to search for missing transactions in

the accounting system by comparing manual accounting

records to computer accounting records for agreement.

Confirm the validity of missing transactions with customers

and obtain copies of redeemed checks that might show a

personal endorsement by an accounts receivable clerk

rather than a business endorsement by the organization.

This information establishes probable cause to subpoena

the individual’s personal bank records to help identify

additional misappropriated funds.

Fraud examiners should learn how to:

Observe client employee changes in behavior and

attitude toward other employees and recognize this as a

potential fraud indicator.

Observe client employees who have the ability to

access and control all accounts receivable revenue,

especially those who also make the daily bank deposit.

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 9

NOTES Listen and observe others to identify “at risk”

employees who might commit fraud based on their

work habits.

Develop Computer-Assisted Audit Techniques

(CAATs) to identify all transactions that fall outside of

normal work hours and determine validity.

Inquire of the staff about who performs relief cashier

duties to identify individuals with incompatible duties.

Determine if employees are required to take vacations,

and if the organization cross-trains employees by

periodically switching the duties of key employees.

Verify that the organization has implemented a “last

look” policy where managers analyze the contents of

the daily bank deposit after it has been prepared by a

key employee and before the deposit is actually made.

Search for off-book accounts receivable accounts, such

as delinquent traffic fines in municipal courts of small

cities, and verify that outstanding balances are reported

on the organization’s financial statements.

Part Two: Common Cash Receipt Fraud Schemes

Check-for-Cash Substitution Scheme

This is the most common fraud scheme in accounts

receivable. The scheme is perpetrated by a cashier or

accounting clerk who substitutes checks from

unrecorded payments for currency from payments that

have been receipted in the organization’s accounting

records. There is an immediate overage when the

cashier places the checks from these unrecorded

transactions in the cash register. To remedy this

situation, the cashier merely removes this same amount

of currency from the drawer and misappropriates it for

personal benefit. In my state, this scheme accounts for

about 10 percent of all fraud cases, but about 25 percent

of the dollar losses. This is the crime of choice for a

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 10

NOTES supervisory cashier, one who makes the daily bank

deposit without any supervision by a manager.

Perpetrators often begin misappropriating unrecorded

checks from non-accounts receivable revenue sources.

Miscellaneous revenue streams and other one-time

charges for services are prime targets of opportunity

because they’re not monitored by managers. The

critical attribute of this scheme is that the check and

cash composition of the daily bank deposit does not

agree with the mode of payment (e.g., check or cash)

shown on all cash receipts recorded each business day.

There will be more checks present in the daily bank

deposit and less currency.

The unrecorded checks used in this scheme are almost

always received through the mail because these

customers do not ever expect to receive a receipt for

their payment. Their canceled check is their receipt.

Cashiers also receive unrecorded checks directly from

customers by asking: “Do you need a receipt?” When

customers decline a receipt their payment becomes

“free” money because accountability has been

established for these funds.

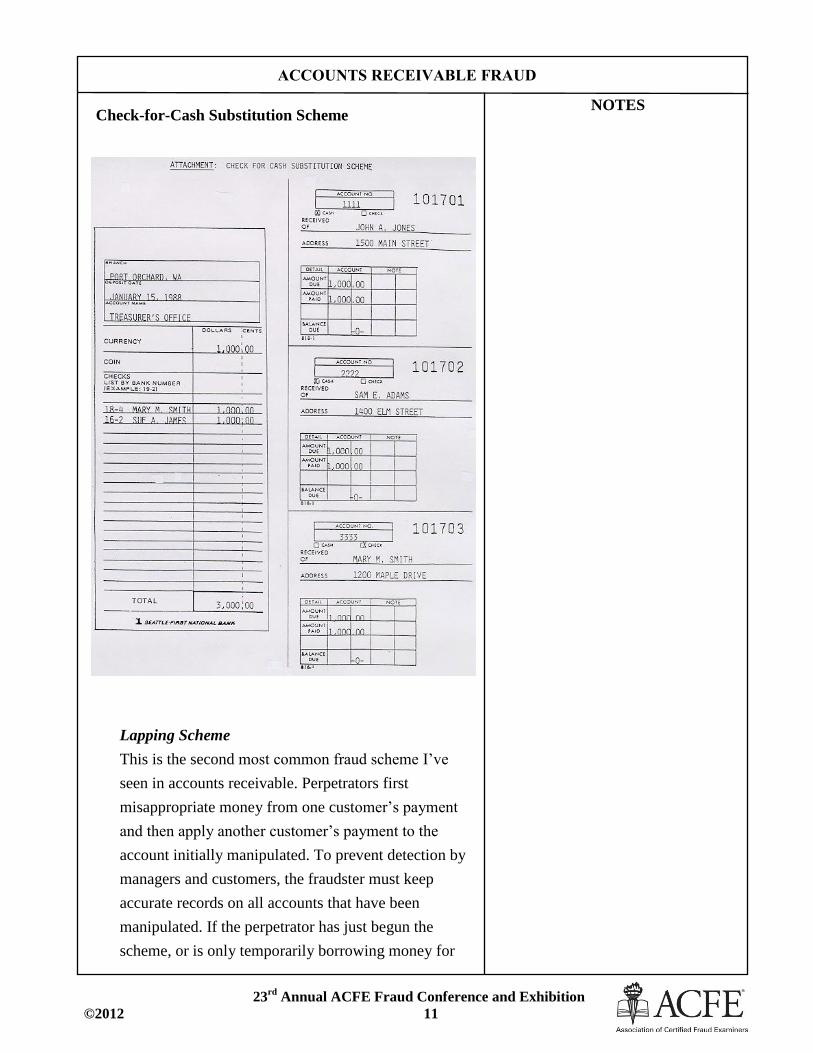

The following is an example of a check-for-cash

substitution scheme:

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 11

NOTES Check-for-Cash Substitution Scheme

Lapping Scheme

This is the second most common fraud scheme I’ve

seen in accounts receivable. Perpetrators first

misappropriate money from one customer’s payment

and then apply another customer’s payment to the

account initially manipulated. To prevent detection by

managers and customers, the fraudster must keep

accurate records on all accounts that have been

manipulated. If the perpetrator has just begun the

scheme, or is only temporarily borrowing money for

Check for Cash Substitution

Scheme -Training Example

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 12

NOTES personal use, they usually keep a copy of the applicable

utility stubs in their possession or somewhere in the

cashier area as a reminder that these customers must

receive credit for their payments sometime before the

end of the billing cycle.

The fraudsters rationalize that they’re only borrowing

the money and intend to make full restitution later. But,

as the size of the scheme increases over time, they soon

realize they can’t repay the money. The drama unfolds

as they try to properly credit all manipulated accounts

by the end of each billing cycle. This is a stressful

juggling act that often requires fraudsters to come to

work early and stay late to conceal the scheme from

managers and always be present in the workplace to

respond to any customer complaints. Eventually, the

perpetrator can’t control the scheme because of the

amount of the loss, the number of accounts involved,

and the amount of time required to manipulate the

accounting records. They make mistakes and the

scheme begins to unravel. These frauds are commonly

detected when the fraudster has a family emergency and

another employee performs the job temporarily.

Here’s what a lapping scheme looks like. Revenue is

collected from customer “A” and misappropriated

without recording the payment in the accounting

records. Revenue from customer “B” is then

misappropriated and used to make the payment for

customer “A.” As more funds are taken, the number of

customer accounts and the size of the loss rolling

through the accounting system increases over time

(progression). Eventually, fraud perpetrators lose

control and are detected.

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 13

NOTES When lapping schemes begin, fraudsters often start by

concealing losses in delinquent or “slow-pay” accounts.

If cash is involved, the switch might never be detected.

But if checks are involved, the check-for-cash

substitution attributes described above will be present

in the daily bank deposit. If these customer payment

habits were analyzed, they would be classified as “slow

pay” accounts because customer payments are always

recorded late in the billing cycle.

Many organizations record customer payments on the

current billing statement with a courteous statement,

such as “payment—thank you,” without indicating a

specific payment date. A small computer software

change will fix this weakness and allow customers to

become a part of the organization’s internal control

system. They will report account payment discrepancies

to an independent customer service function for

resolution.

Secrets to Detecting Fraud in Accounts Receivable

Fraud examiners should:

Obtain the detail of one or more daily deposits from the

bank’s microfilm records. Select a business day at or

near the end of a billing cycle to identify fraud schemes

that cannot be detected in other ways. Verify that the

check-and-cash composition of the bank deposit agrees

with the mode of payment for the cash receipts issued

each business day.

Use the lowest possible original source documents for

cash receipt testing and review the mathematical

accuracy of daily accounts receivable batches.

Conduct unannounced cash counts. Look carefully at

the supporting cash receipt documents to ensure that

they meet your expectations (e.g., utility stubs present

versus screen prints). Search the cash receipting area

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 14

NOTES for any extraordinary items, such as unauthorized cash

receipt books and batches of utility stubs with no

money attached.

Determine how managers monitor miscellaneous

revenue sources to ensure their expectations are being

met.

Review the work of key supervisors who make daily

bank deposits to ensure their work has been monitored

by managers in the same way these supervisors monitor

the work of their subordinates. For example:

On a periodic and unannounced basis, review the

daily bank deposit at the office after it has been

prepared. Complete the analysis of the check-and-

cash composition of the deposit, secure the funds,

and then accompany the staff to the bank when they

make the deposit.

Make arrangements with the bank to have the

deposit returned to the organization (unopened).

Complete the verification above and then make the

bank deposit again.

Make arrangements with the bank to process the

daily bank deposit normally, but make copies of the

deposit slip, the checks, and any other documents

included in the deposit. These records should then

be used to complete the verification above.

Part Three: Falsification of Accounting Records

When the staff reconciles accounts receivable payment

records with bank deposit information in the absence of an

independent party supervisor, they falsify the

organization’s accounting records to conceal fraud.

When cashiers initially record accounts receivable

transactions, they:

Misappropriate funds from some transactions and

then dupe record keepers into posting all accounts

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 15

NOTES “paid” even when a lesser amount of funds have

been deposited in the bank.

Record all cash receipt transactions on a cash

register system and interface the accounting

information with another stand-alone computer that

marks all customer accounts “paid.” Cashiers then

eliminate entire batches of customer payments from

the cash register system. Check payments from

these batches are reentered in the cash register

system while cash payments are misappropriated.

These revised batches are never interfaced with the

accounts receivable computer. Numerical

sequencing discrepancies will exist in the bank

deposit batch information recorded in the cash

register system.

Misappropriate funds received from a record keeper

before making the daily bank deposit.

When record keepers initially record accounts

receivable transactions, they:

Record check payments in the accounting records

and turn in the funds to the cashier using a “sub-

total” accounting report. The cashier then includes

these funds in the daily bank deposit. The record

keeper then records cash payments in the

accounting records and prepares a “total”

accounting report which marks all accounts “paid.”

They then destroy the “total” accounting report and

misappropriate the funds from all cash payments.

The net result of these manipulations is an imbalance in the

accounting information—the number and amount of

customer accounts marked “paid” will be greater than the

number and amount of customer payments deposited in the

bank. When the staff performs the reconciliation of these

two records rather than an independent party, the

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 16

NOTES discrepancy is never reported to anyone. It rests in plain

sight awaiting discovery by a prudent fraud examiner.

Employees use two common methods to conceal fraud in

accounts receivable:

Write-off the customer’s account balance for any

manipulated payments. This is the fraudsters preferred

method. However, it can only be successful when

managers do not pay attention to the computer-

generated “exception” reports identifying the total

amount of account write-offs for specific periods of

time (preferably daily), or when the computer does not

create an “exception” report. All write-off transactions

should be properly authorized and approved, with

supporting documents retained on file for subsequent

review and audit.

Fictitious or unsupported account adjustments

simply eliminate the accountability for money.

Fraud perpetrators typically don’t prepare any

documents to support fictitious write-offs when they

know managers aren’t monitoring this information.

Managers often forget that employees who have the

ability to process account adjustments as a part of

their normal job responsibilities always have the

ability to do this, whether it’s authorized or not.

These employees have access to the computer

system at all times—24 hours a day, 7 days a week,

and 365 days a year—and can abuse their access at

will.

Allow the customer’s account balances to become

delinquent. This is risky business because the

delinquencies are clearly available for managers to

review. When this review function is not performed or

performed in a perfunctory manner, the employee must

only deal with customer complaints about irregularities

in their account. To preclude this from happening,

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 17

NOTES record keepers may employ schemes to “steal the

statements,” either inside or outside the organization, in

order to prevent customers from finding out about

delinquent account balances.

When employees manipulate prior account balance

information from inside the organization, they must

obtain the affected customer statement information,

prepare manual statements that reflect only the

current amount due, and then mail the revised

statement to customers.

When employees manipulate prior account balance

information from outside the organization, they first

must make address changes to the customer

accounts to ensure statements from manipulated

accounts are mailed to an address they control.

Once statements are received, the fraudsters prepare

manual statements that reflect only the current

amount due and mail them to the customer.

Customers will be unaware of any problem with

their account as long as the employee keeps

accurate records of all manipulated accounts and

makes no mistakes in the process. This is difficult

over time as the number of manipulated customer

accounts increases because all accounts must be

continually manipulated during every subsequent

billing cycle.

Organizations should have an independent customer service

function to process customer complaints about their

accounts or any other irregular accounts receivable

transactions. Accounts receivable staff should not be

permitted to investigate these types of transactions. In

addition, they should not be able to post notices on

customer billing statements advising them to contact any

accounts receivable staff member about questions on their

account. Finally, accounts receivable staff members should

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 18

NOTES not be able to password protect their telephone voice mail.

These procedures provide the opportunity for staff

members to conceal irregular activity from managers.

Accounts receivable staff often must falsify other

accounting records to conceal fraud from managers.

Computers create at least two reports related to delinquent

accounts receivable that can be useful to fraud examiners.

They are.

The “no-bill” report. The computer prepares a list of all

customers who are not currently being billed for

service. Reasons for this customer status are

unoccupied residences for long periods of time, such as

for lengthy hospital or convalescent hospital stays or

extended vacations. The accounts receivable function

should maintain a file for each residence listed on this

report that includes correspondence from the owner in

order to substantiate this status. The accounts receivable

staff can hide invalid delinquent balance accounts by

coding accounts with this status.

The “shut-off” report. The computer prepares a list of

all customers who have been delinquent over a

specified period of time. The accounts receivable staff

uses this report to prepare “door-knocker” notices that

other utility staff use to notify the customer about the

impending shut-off of service unless a payment is made

within a specific due date. The utility staff hangs these

notices on the front door of these residences. If no

payment is received by the due date, the utility staff

shuts off service to the residence. If fraud is being

concealed in delinquent accounts receivables, an

accounts receivable staff member simply ignores the

accounts they have been manipulating (i.e.; invalid

delinquent balances), and does not prepare the required

shut-off notices. This fraud can be detected by

reviewing the “shut-off” report for validity.

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 19

NOTES Organizations should be able to estimate the amount of

currency deposited in the bank over time as a percentage of

total bank deposits made. Managers should periodically

review this information to ensure their expectations are

being met. The risk of fraud is high when there is little or

no currency shown in bank deposits.

Secrets to Detecting Fraud in Accounts Receivable

Fraud examiners should:

Compare the total amount of bank deposits with the

total accounts receivable payments posted to customer

accounts over time.

Scan bank deposits to determine the amount of currency

being deposited, and then determine if this percentage

meets manager’s expectations.

Know the difference between “sub-total” and “total”

accounting reports and review these documents

carefully.

Compare batch sequence numbers from the cash

register system to the accounts receivable accounting

system either manually or by using computers to

identify any unprocessed batches.

Obtain and review computer-generated “exception”

reports listing all write-off transactions. Review the

supporting documents on file and verify that all

transactions have been authorized and approved by

managers.

Confirm delinquent customer account balances by

sending account history statements to customers for

verification. Most customers will not know their

account balance, but can verify their recent payment

history. This procedure improves the response rate for

account confirmations.

Review the “no-bill” report for all accounts that aren’t

automatically billed for utility services to determine

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 20

NOTES whether this status has been authorized by managers

and is justified based on the circumstances of the case.

Review the “shut-off” report for all unpaid accounts to

ensure that utility services were terminated as required

by law.

Verify that all billing statements include the appropriate

account history information, including the prior account

balance, payment information (including the date of

payment instead of “payment—thank you”), new

billings for services, and amount due as of the statement

cut-off date.

Verify that the organization has established an

independent customer service function to properly

follow-up on customer complaints and other irregular

accounts receivable transactions.

Part Four: A Complex Accounts Receivable Fraud Case

Study

Case Summary

Perpetrator: Accounts receivable clerk

Loss amount: $357,237 (undetermined period of

time)

Manipulated 4,000 accounts (23%) from universe of

17,500 total customers

Inadequate segregation of duties for accounts

receivable clerk who:

Received all revenue, including checks that

came through the mail

Posted customer accounts “paid”

Prepared the daily bank deposit

Reconciled the monthly bank account

Established unauthorized “suspense” accounts

to conceal manipulated cash receipt transactions

Wrote-off customer account balances without

approval

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 21

NOTES Controlled customer feedback (telephone

password protected)

Placed a notice on utility bills for customers

to contact her about problems with their

accounts with the help of other staff

The district did not have an independent customer service

function to deal with customer complaints, the finance

director did not monitor her work to determine if the

organization’s expectations were being met, and there was

no computer “exception” report listing the total of all

accounts adjusted each day to compare to the approved file

of source documents. The clerk worked early and late, and

rarely took vacation. No one ever did her work when she

was gone.

Delinquent accounts receivables were not monitored by

managers, and there were no accounts receivable aging

reports.

No one noticed that there was very little cash in the

district’s bank deposits even though large cash payments

were routinely received in the cash receipting function.

In lieu of utility stubs, there were a wide variety of irregular

documents present in the supporting documents for daily

batches of cash receipt transactions.

Detection of the Fraud

During the annual audit of a water utility district, the

finance director informed the external auditor they had

discovered an irregular miscellaneous revenue

transaction. The district sold a vehicle for $1,500 cash.

However, an employee informed the finance director

that the bank deposit for miscellaneous revenue for that

transaction was short $1,000 in cash. The finance

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 22

NOTES director then obtained the detail of the deposit from the

bank’s microfilm records and performed the following

tests:

Test one: Determine if the amount of the deposit

agreed with the total amount of accountability from

the cash receipts issued. In this case, these records

agreed.

Test two: Compare the check-and-cash composition

of the deposit with the mode of payment (i.e., check

and cash) of the cash receipts issued. In this case,

these records didn’t agree.

The attributes of less cash and more checks are red flags for

a check-for-cash substitution fraud. The cashier substituted

an unrecorded revenue check for $1,000 in currency in the

bank deposit on this date to conceal the theft of currency

from the vehicle sale.

This event began one of the most complex accounts

receivable lapping schemes I’ve ever encountered in my

42.5-year audit career at federal, state, and local

government levels.

When notified about this deposit irregularity, the external

auditors were at the very end of their audit. They opted to

complete the current audit and include this irregular

transaction in a subsequent special investigation. They then

issued an audit report citing a host of internal control

weaknesses in the cash receipting and accounts receivable

functions.

I was assigned to the special investigation and immediately

went undercover to begin work at one of our audit office

locations. We asked the district’s finance officer to obtain

copies of all of the district’s bank deposits for three months

as well as all of its accounts receivable accounting records

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 23

NOTES and reports for the same time period. The finance officer

sent these records to us and the investigation began.

Our subsequent audit tests proved that the check-and-cash

composition of the district’s daily bank deposits rarely

agreed with the mode of payment of the cash receipts

issued. The cashier had manipulated almost 23 percent of

all customer accounts—4,000 customers from a universe of

approximately 17,500. Our comparison of approximately

2,000 account postings in the accounting records with the

checks included in seven daily bank deposits proved that

only 1 percent of the records matched. Since there is

usually one check present in the deposit for each

customer’s account reflecting a payment, I normally would

expect just the opposite (i.e., a 99 percent match).

Sometimes two checks are submitted for one payment, such

as when two individuals share an apartment and expenses.

And sometimes only one check is present to pay for two or

more accounts such as a landlord making payments at

multiple locations. But these are exceptions to the rule.

The cashier had lost complete control over individual

transactions being manipulated and hadn’t retained a copy

of each customer’s utility stub to keep track of the scheme.

To compensate for this shortcoming, she accessed the

computer records and printed the page containing the

customer’s name, address, and account number. She then

used this document, a screen print, in lieu of the utility stub

as support for the payments for customer accounts that

were being manipulated. There were more pieces of paper

on file with the daily bank deposits than there were utility

stubs from customers.

Prior to our special investigation, the accounts receivable

clerk fell on the job and broke her leg. She went to the

hospital and returned to work the same day in a wheelchair.

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 24

NOTES She could not leave the work environment because of fear

that others might detect her scheme.

Prior to the detection of this fraud, the water district and a

nearby sewer district with the identical customer base were

trying to implement a new computer accounting system that

would send one combined bi-monthly bill to each water

and sewer customer. The bills would be bar-coded for ease

in processing bank deposits for each district, with the water

and sewer district staffs performing cash receipting duties

during alternating months. This new system would save

both districts a lot of money over time. However, the water

district accounts receivable clerk had done everything

possible to block this computer conversion for almost a

year because she had been unable to determine how to

continue the fraud scheme with the new computer.

After performing our initial audit tests, I visited the district

to observe the accounts receivable clerk’s work area when

she was not present. The executive director created a

computer training class for all employees so that I could do

this. While the work area was unoccupied, the accounts

receivable clerk’s workplace was littered with currency,

checks, and batches of utility stubs, some with funds and

some without funds. This environment could never protect

the district’s funds from loss.

As the executive director and I were viewing the

accounting clerk’s work area, all of the staff members

returned to work. The trainers had run out of material and

released the staff early. When the accounting clerk

returned, the executive director introduced me and said that

I was going to perform an unannounced cash count. The

clerk went to the safe and returned with two cash boxes—

one for the petty cash fund, and one for a change fund. My

count of these funds determined that both were short by

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 25

NOTES minor amounts. We then went to the front cashier function

and counted the other change fund. It was also short by a

minor amount. When this work was completed, the clerk

turned to me and said, “Now that you’ve counted the cash,

I need to get back to work. Please come back later when

I’m not so busy.” I informed her that I would not be leaving

until all funds in her workplace had been counted. She was

shocked.

Since all accounts receivable transactions were processed

in batches of 99 customer payments, each business day was

comprised of many batches of documents. I told the clerk

that I would be reviewing each batch of documents and

funds as she prepared them, and that I would begin with the

one batch that she had completed before she had attended

the training class. She was again shocked and stated, “I

wouldn’t begin there if I were you because that batch is

kind of messed up.” This is a technical accounting term for

fraud. We began our work. Every time I turned my back or

went to the copy machine to duplicate more cash count

sheets, the clerk threw money and stubs in drawers and

behind her desk hoping I wouldn’t see what she was doing.

She went home at the end of a very long day. After all other

staff departed, we cleared her work area and swept the

floor, gathering a lot of customer utility stubs, money, and

other paperwork in the process. I placed all of these

materials in a bag and then reassembled her work area for

her return the following morning.

When the clerk came to work the next day, the executive

director directed her to a conference room where I was

waiting to interview her. All of the materials I had collected

from her workplace the prior day were sitting in the middle

of the table in front of her. The interview went quickly.

During our discussion, she thanked me for making the

fraud scheme stop. She just couldn’t find a way to do it,

ACCOUNTS RECEIVABLE FRAUD

23rd

Annual ACFE Fraud Conference and Exhibition ©2012 26

NOTES short of making full restitution of the amount of the loss,

and she couldn’t do that. She did not know how long she

had perpetrated this lapping scheme, and her husband was

not aware of what she had done.

Sentencing

In a plea bargaining agreement with the county prosecutor,

she pleaded guilty to misappropriating $357,237 and was

sentenced to a term of 33 months in a state correctional

facility.

![[Webinar] Fraud in Accounts Payable](https://img.pdfslide.us/doc/110x75/55d521a5bb61eb627d8b4578/webinar-fraud-in-accounts-payable.jpg)