Embed Size (px)

Citation preview

THE IMPACT OF FISCAL INCENTIVES IN THE PRE-SALT OIL BUSINESS

IN BRAZIL

Patrícia Pereira Pedra

Dissertação de Mestrado apresentada ao Programa de

Pós-graduação em Planejamento Energético, COPPE,

da Universidade Federal do Rio de Janeiro, como parte

dos requisitos necessários à obtenção do título de

Mestre em Planejamento Energético.

Orientador: Alexandre Salem Szklo

Rio de Janeiro

Março de 2020

THE IMPACT OF FISCAL INCENTIVES IN THE PRE-SALT OIL BUSINESS IN

BRAZIL

Patrícia Pereira Pedra

DISSERTAÇÃO SUBMETIDA AO CORPO DOCENTE DO INSTITUTO ALBERTO LUIZ

COIMBRA DE PÓS-GRADUAÇÃO E PESQUISA DE ENGENHARIA DA

UNIVERSIDADE FEDERAL DO RIO DE JANEIRO COMO PARTE DOS REQUISITOS

NECESSÁRIOS PARA A OBTENÇÃO DO GRAU DE MESTRE EM CIÊNCIAS EM

PLANEJAMENTO ENERGÉTICO.

Orientador: Alexandre Salem Szklo

Prof. Alexandre Salem Szklo

Prof. Roberto Schaeffer

Prof. Edmar Luiz Fagundes de Almeida

RIO DE JANEIRO, RJ - BRASIL

MARÇO DE 2020

iii

Pedra, Patrícia Pereira

The Impact of Fiscal Incentives in the Pre-Salt Oil

Business in Brazil / Patrícia Pereira Pedra. – Rio de Janeiro:

UFRJ/COPPE, 2020.

XIII, 98 p.: il.; 29,7 cm.

Orientador: Alexandre Salem Sklo

Dissertação (mestrado) – UFRJ/ COPPE/ Programa de

Planejamento Energético, 2020.

Referências Bibliográficas: p. 72-83.

1. Oil production 2. Pre-salt. 3. Fiscal Incentives 4.

Economic Analysis I. Szklo, Alexandre Salem. II.

Universidade Federal do Rio de Janeiro, COPPE, Programa

de Planejamento Energético. III. Título.

iv

AGRADECIMENTOS

Agradeço à minha família, especialmente ao meu marido Paulo Brandão, por seu amor

em todos os momentos.

Meus filhos, pela compreensão das horas deles retiradas para o estudo. Meus pais que

sempre me apoiaram e incentivaram a nunca parar de aprender.

Ao Prof. Alexandre Salem Szklo, pelas conversas e orientação e por ser um exemplo

de mestre.

Aos professores Roberto Schaeffer e Edmar Almeida pela participação na banca de

mestrado.

Aos meus amigos e colegas de turma do PPE, partilhamos muitas horas de estudo juntos

e foi maravilhosa a convivência. Especialmente à Fernanda que foi uma ótima experiência

reencontrar após mais de 20 anos!

Aos professores do PPE que partilharam seus conhecimentos e experiências.

Aos funcionários do PPE, especialmente à Sandrinha que está sempre à disposição para

nos ajudar.

E à Deus por me presentear com mais uma benção!

v

Resumo da Dissertação apresentada à COPPE/UFRJ como parte dos requisitos necessários

para a obtenção do grau de Mestre em Ciências (M.Sc.)

O IMPACTO DOS INCENTIVOS FISCAIS NO PRÉ-SAL BRASILEIRO

Patrícia Pereira Pedra

Março/2020

Orientador: Alexandre Salem Szklo

Programa: Planejamento Energético

Sob uma perspectiva econômica, social e ambiental, é válido avaliar se a renda

petrolífera do pré-sal brasileiro está sendo devidamente apropriada pelo Estado, dada a

existência de incentivos fiscais na indústria nacional por mais de vinte anos. O petróleo

representa uma parcela de 40% no consumo de energia primária do país e a produção e

exportação do mesmo é fundamental para a balança comercial do país (i.e., foi o terceiro item

com maior participação de valor nas exportações em 2017). Após a descoberta da província de

óleo chamada pré-sal, o governo brasileiro expandiu até 2040 os termos do regime especial

fiscal chamado Repetro, que, entre outras provisões, permite isenções fiscais, ainda que

temporárias, para a indústria. No entanto, no contexto de uma recessão econômica, crescente

problemas sociais e compromissos com baixas emissões de carbono, é importante verificar se

tais incentivos são mesmo necessários para fazer com que os campos de pré-sal sejam atrativos

economicamente. Após análise de alguns tipos diferentes de campos de pré-sal, para um

cenário de preços acima de $60/bbl, os incentivos não são necessários para fazer com que os

maiores campos sejam economicamente viáveis, se tornando então subsídios indiretos para a

indústria nesses casos. Verificou-se também que o ajuste dos termos fiscais do contrato de

partilha existente permite adequar a participação governamental na partilha a diferentes

cenários de preço de petróleo.

vi

vii

Abstract of Dissertation presented to COPPE/UFRJ as a partial fulfillment of the requirements

for the degree of Master of Science (M.Sc.)

THE IMPACT OF FISCAL INCENTIVES IN THE PRE-SALT OIL BUSINESS

IN BRAZIL

Patrícia Pereira Pedra

Março/2020

Advisor: Alexandre Salem Szklo

Department: Energy Planning

From an economic, social and environmental perspective, it is worthwhile to assess if

oil rents from petroleum production in the Brazilian pre-salt fields are being appropriately

perceived by the State, given the current long-lasting fiscal incentives to the industry in Brazil.

Crude oil accounts for 40% of the country´s primary energy consumption, and is key to its

trade balance (e.g., the third export good in value in 2017). After the discovery of the oil

province called pre-salt, the Brazilian government expanded to 2040 and deepened the terms

of the special tax regime called Repetro that provides tax exemptions to the oil industry.

However, in the light of an economic recession allied with increasing social problems and

commitments to a low carbon world, the question that arises is weather these fiscal incentives

are truly needed to make pre-salt projects economic attractive. By evaluating some pre-salt

fields, under an oil price scenario of $60/bbl, this study shows that, for some fields, fiscal

incentives are not necessary, being, then, hidden subsidies. Moreover, the adjustment of the

existing production sharing contract terms allows a better fit of the government take within

different oil prices scenarios.

viii

TABLE OF CONTENTS

1 INTRODUCTION ............................................................................................................. 1

1.1 Hypothesis and Objective............................................................................................ 4

1.2 Dissertation Structure .................................................................................................. 5

2 PETROLEUM FISCAL SYSTEMS .................................................................................. 6

2.1 Oil and gas exploration and production commercial models ...................................... 6

2.1.1 Fiscal terms premises ........................................................................................... 6

2.1.2 Concession Contracts ......................................................................................... 14

2.1.3 Production Sharing Agreements ........................................................................ 16

2.1.4 Service Contracts ............................................................................................... 17

2.1.5 Others ................................................................................................................. 19

2.2 Discounted Cashflow Analysis ................................................................................. 20

2.3 Application of petroleum fiscal systems .................................................................. 23

3 BRAZIL´S OIL AND GAS FISCAL REGIMES ............................................................ 23

3.1 Oil and gas history in Brazil ...................................................................................... 24

3.1.1 Legal Framework history of the industry in Brazil ............................................ 26

3.1.2 Terms of the Concession Contract in Brazil ...................................................... 31

3.1.3 Transfer of Rights in Brazil (Onerous Assignment) .......................................... 33

3.1.4 Production Sharing Agreement in Brazil ........................................................... 34

3.2 Brazilian tax system .................................................................................................. 34

3.2.1 Changes made by Law 13,586/17 ...................................................................... 36

4 METHODOLOGY .......................................................................................................... 38

4.1 Fiscal Incentives ........................................................................................................ 42

4.2 Economic Metrics and Assumptions ......................................................................... 43

4.2.1 Oil Prices ............................................................................................................ 43

4.2.2 Metrics ............................................................................................................... 44

ix

4.2.3 Signature Bonus, Profit Oil and Cost Oil Rates ................................................. 46

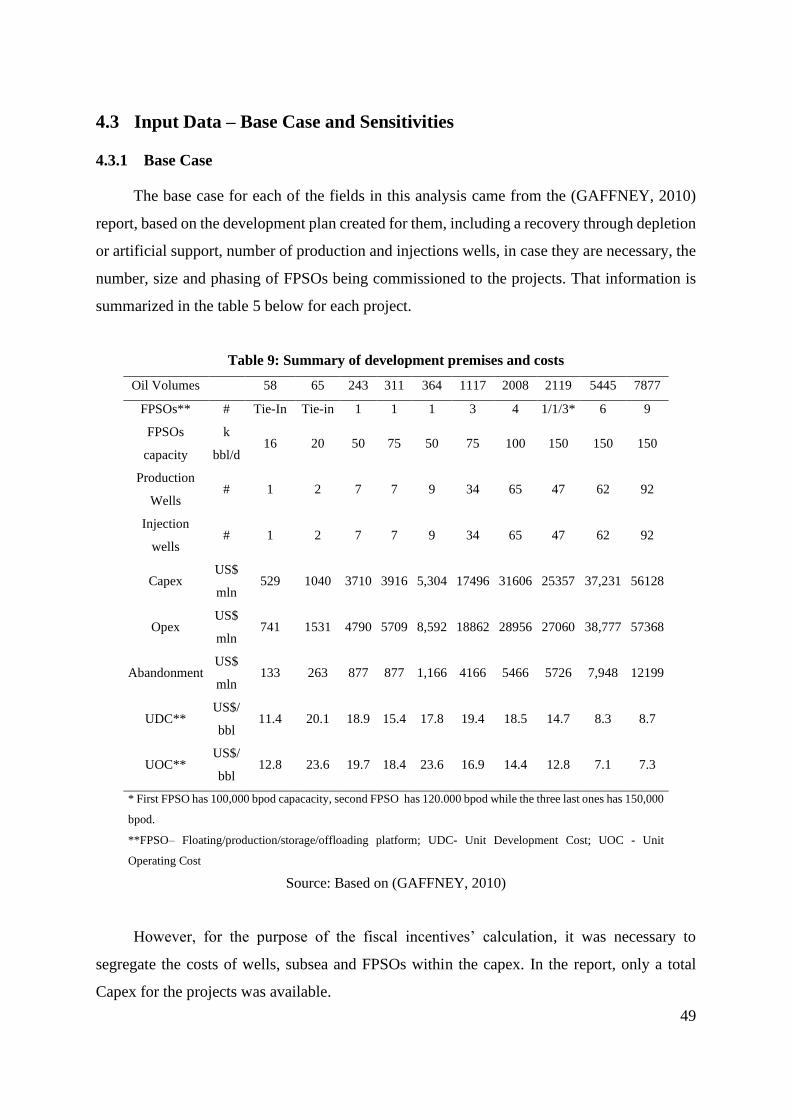

4.3 Input Data – Base Case and Sensitivities .................................................................. 49

4.3.1 Base Case ........................................................................................................... 49

4.3.2 Sensitivity Cases ................................................................................................ 56

4.4 Yet to Find Pre-Salt Volumes ................................................................................... 56

5 RESULTS ........................................................................................................................ 58

5.1.1 Base Case ........................................................................................................... 58

5.1.2 Sensitivities ........................................................................................................ 62

6 CONCLUSIONS.............................................................................................................. 70

7 REFERENCES ................................................................................................................ 72

Annex I – Special Participation Tax (SPT) .............................................................................. 84

Annex II – Petroleum Fiscal Regimes Examples .................................................................... 89

II.1 Indonesia ................................................................................................................... 89

II.2 Iran ............................................................................................................................ 91

II.3 Norway ...................................................................................................................... 94

II.4 United States of America .......................................................................................... 96

Annex III – Results from ANP Pre-Salt Bid Rounds until 2019 ............................................. 98

x

FIGURES

Figure 1: Typical oil and gas offshore, conventional reservoir cashflow .................................. 8

Figure 2: Typical oil and gas offshore, unconventional reservoir cashflow.………………………... 9

Figure 3: Concession contract structure…………………………………...……………………….. 15

Figure 4: General production sharing agreement structure………………..………………………... 17

Figure 5: General revenue-shared contract structure……………………...……………………….. 18

Figure 6: General risked-service contract structure……………………….………………………... 18

Figure 7: General pure-service contract structure………………………...………………………... 19

Figure 8: Straight Line Depreciation……………………………………………..………………………... 22

Figure 9: Unit of Production Depreciation………………………………..………………………... 22

Figure 10: Brazil’s historical oil production and consumption ……………….….……………... 26

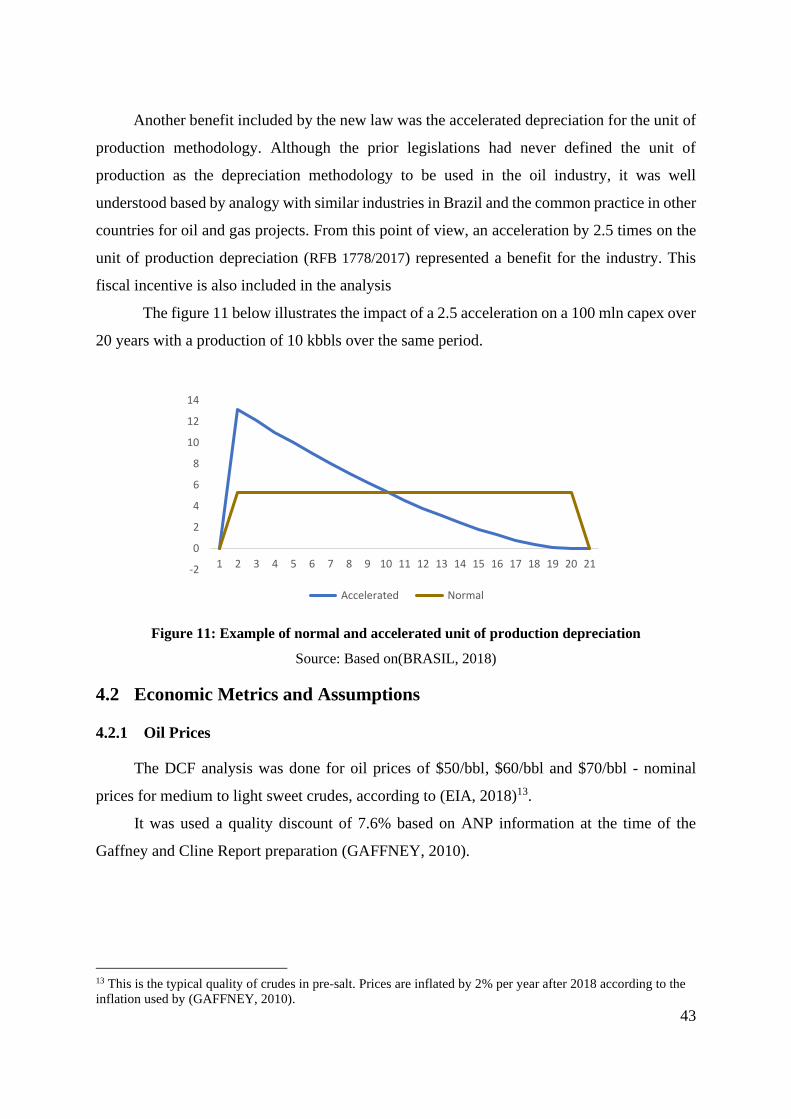

Figure 11: Example of normal and accelerated unit of production depreciation.………………... 43

Figure 12: Profit Oil Matrix…………………………………………………….………………... 48

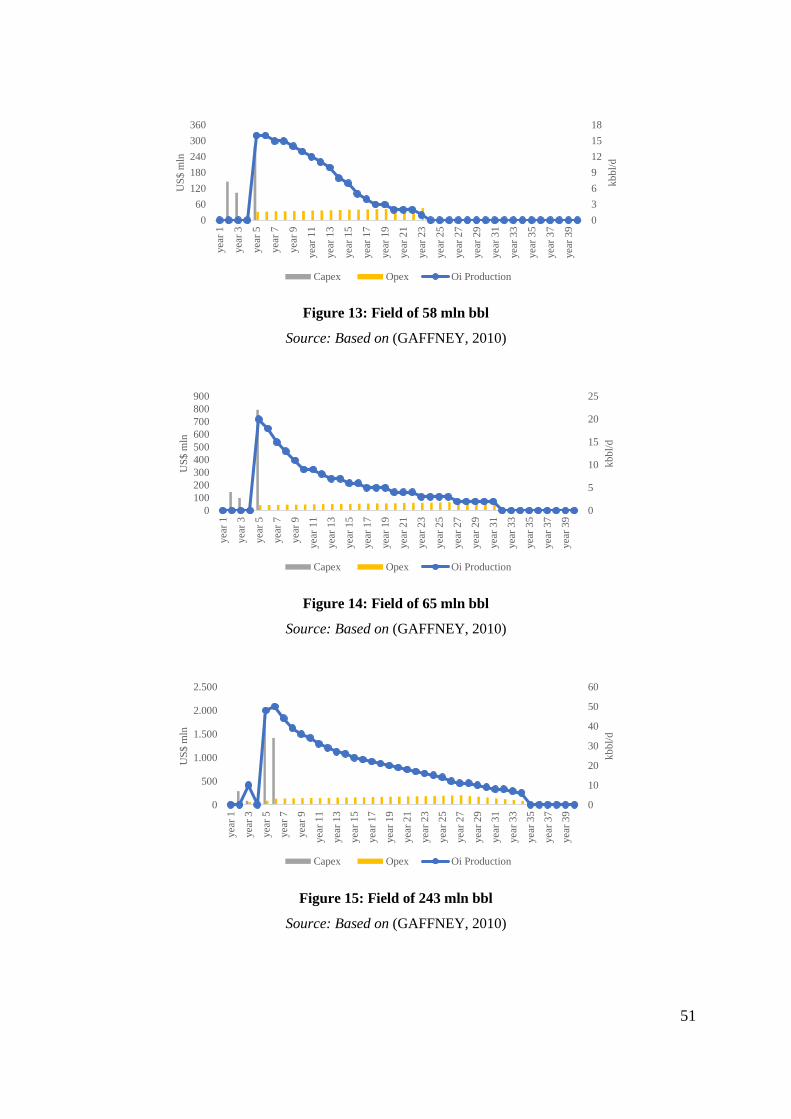

Figure 13: Field of 58 mln bbl…………………………………………………………………... 51

Figure 14: Field of 65 mln bbl…………………………………………………………………... 51

Figure 15: Field of 243 mln bbl ………………………………………………………………... 51

Figure 16: Field of 311 mln bbl………………………………………………………………... 52

Figure 17: Field of 364 mln bbl………………………………………………………………... 52

Figure 18: Field of 1117 mln bbl……………………………………………………….……... 52

Figure 19: Field of 2008 mln bbl…………………………………………………………..…... 53

Figure 20: Field of 2119 mln bbl……………………………………………………………… 53

Figure 21: Field of 5445 mln bbl………………………………………………………………... 53

Figure 22: Field of 7877 mln bbl …………………………………………………………….54

Figure 23: Average production per well after plateau…………………….………………………... 55

Figure 24: Impact of profit oil and signature bonus in IRR at $50/bbl…...………………………... 65

Figure 25: Impact of profit oil and signature bonus in IRR at $60/bbl…...………………………... 65

Figure 26: Impact of profit oil and signature bonus in IRR at $70/bbl.………….…………………... 66

xi

Figure 27: Impact of profit oil and oil price in IRR at US$2000 million Bonus …….………... 67

Figure 28: Impact of profit oil and oil price in IRR at US$4000 million Bonus …….………... 67

Figure 29: Impact of profit oil and oil price in IRR at US$8000 million Bonus …….………... 68

Figure 30: Impact of profit oil and oil price in IRR at US$2000 million Bonus with the fixed

case …………………………………………………………………………….…….………... 69

Figure 31: Indonesia’s historical oil production and consumption………….……………………... 90

Figure 32: Iran’s historical oil production and consumption….……………………………………... 93

Figure 33: Norway’s historical oil production and consumption.……………………….……………... 95

Figure 34: USA’s historical oil production and consumption …………………………………………...97

xii

TABLES

Table 1: Constitutional changes comparison. .......................................................................... 29

Table 2: Legal Framework for the Concession Contract in Brazil .......................................... 30

Table 3: Legal framework for the pre-salt and strategical areas in Brazil. .............................. 31

Table 4: Tax categories, average tax allocation - with Repetro. .............................................. 41

Table 5: Tax categories, average cost allocation and average tax rates - without Repetro ..... 41

Table 6: Summary of Fiscal Incentives of Repetro ................................................................ 42

Table 7: IOCs´ Selected Financial Information. ...................................................................... 45

Table 8: Bonus and Profit Oil estimation based on actual values. ........................................... 47

Table 9: Summary of development premises and costs. .......................................................... 49

Table 10: FPSO platforms costs according to production capacity – as of 2014 .................... 50

Table 11: Potential Evolution of E&P project costs in Brazil $/bbl ........................................ 54

Table 12: Well productivity in the world in 2015 (bbl/d) ........................................................ 55

Table 13: Number of Fields in each scenario. ......................................................................... 57

Table 14: Base Case results at $50/bbl, $60/bbl and $70/bbl without Incentive. .................... 58

Table 15: Base Case results at $50/bbl, $60/bbl and $70/bbl with Repetro. ........................... 59

Table 16: Base Case results at $50/bbl, $60/bbl and $70/bbl with Repetro and Depreciation

Incentive ................................................................................................................................... 59

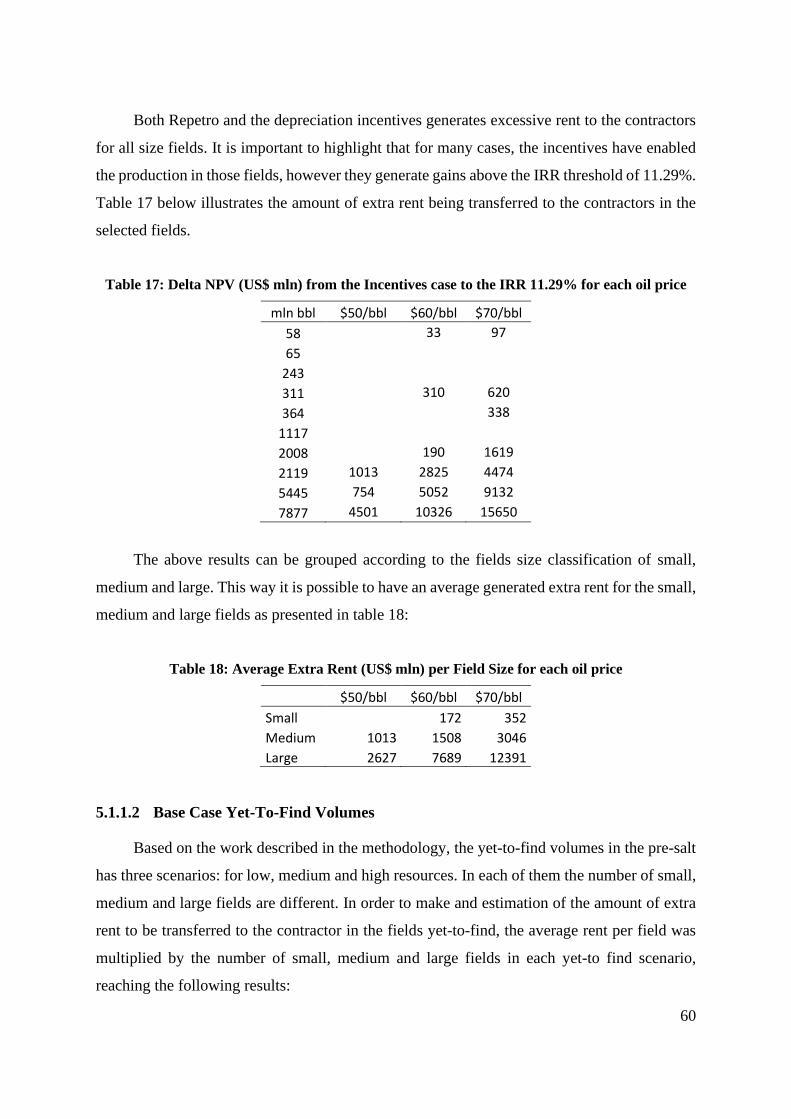

Table 17: Delta NPV (US$ mln) from the Incentives case to the IRR 11.29% for each oil price

.................................................................................................................................................. 60

Table 18: Average Extra Rent (US$ mln) per Field Size for each oil price ............................ 60

Table 19: Total Extra Rent Generated in the Low Yet-to-find Volumes scenario (US$ mln).61

Table 20: Total Extra Rent Generated in the Medium Yet-to-find Volumes scenario (US$ mln).

.................................................................................................................................................. 61

Table 21: Total Extra Rent Generated in the High Yet-to-find Volumes scenario (US$ mln).61

Table 22: Estimation for the Extra rent based on Yet-to-Find Pre-Salt Volumes (US$ mln) 61

xiii

Table 23: Sensitivities results at $50/bbl, $60/bbl and $70/bbl with no Incentive. ................. 63

Table 24: Sensitivities results at $50/bbl, $60/bbl and $70/bbl with Repetro

Incentive..……………………………………………………………………………...……..63

Table 25: Sensitivities results at $50/bbl, $60/bbl and $70/bbl with Repetro and Depreciation

Incentives……………………………………………………………………………...……..63

Table 26: Impact of geological risk on the base case with both incentives ...………...……..64

xiv

ACRONYMS

ANP Brazil Petroleum National Agency

Bbbl Billions of barrels

Bbp/d Billions of barrels per day

Boe Barrel of oil equivalent

BRL Brazilian Reais (currency)

IOC International oil company

IPCC Intergovernmental Panel of Climate Change

Mbbl Millions of barrels

Mbpd Millions of barrels per day

NOC National oil commpany

OPEC Organization of Petroleum Exporting Countries

PPSA Pre-Sal Petróleo S.A

SRF Secretaria da Receita Federal

UDC Unit development cost

UOC Unit operating cost

1

1 INTRODUCTION

In the last 150 years, the use of fossil fuels leaded to undeniable benefits to humankind

(SMIL, 2007; WILSON, 2012). However, negative externalities derive from the production

and use of fossil fuels, with a major threat being associated to global climate change (BRASIL,

2015). Subsidies (hidden or not) to fossil fuels are also relevant to explain their use (CHEON;

URPELAINEN; LACKNER, 2013; COADY et al., 2010).1

Governments dispose of subsidies (hidden or not) to generate impacts in the economy

that otherwise would not happen, or would take much more time than desired to occur. In the

oil industry, they can be used to produce different impacts, which can be, among others, to

increase overall production, to stimulate development of marginal fields, to benefit certain

segments like local industries or even to promote regional development of frontier areas that

cannot depend solely upon market conditions. Despite the benefits of the subsidies, if given

without discretion, they can generate distortions in the economy by transferring more benefits

to the industry than actually necessary, preventing a proper allocation of government resources.

Although oil discoveries had been present since the ancient times, the modern oil

industry as known today started with the Drake well discovery in USA. The “oil rush”

expanded worldwide and by 1910 significant oil fields had been discovered in the Dutch East

Indies (1885, in Sumatra), Persia (1908, in Masjed Soleiman), Peru (1863, in Zorritos District),

Venezuela (1914, in Maracaibo Basin), and Mexico, and were developed at an industrial level

(YERGIN, 1991). The prospection of oil required geological and technical knowledge that

most of the countries, where the initial discoveries were made, did not have, requiring

governments and companies to establish commercial terms to monetize the host countries’

natural resources and generating profit to the corporations. Under this scenario, the world

watched the establishment of different arrangements to regulate the activity of exploring and

producing petroleum.

Just as in the land use, the oil industry also presents a differential rent based on the

“quality of the land”. Davi Ricardo´s Theory of Rent identified that depending on the

productivity of the land the costs to produce food could be reduced generating a differential

rent to its owner (RICARDO, 1817). The same way, the oil business generates rent depending

1 Hidden subsidies or indirect subsidies are those that do not involve direct payment of funds to an specific industry

(VICTOR, 2009)(STEFANSKI, 2017)(KOPLOW, 2012)(BENES et al., 2015)

2

on the location and quality of the resources. As rent is the surplus created after remuneration

of the cost of capital and all the production factors involved in this activity, many discussions

arise regarding who should benefit from the differential rent. It is the key concept for regulating

the oil industry when trying to balance attractiveness for the contractors with government take.

In the beginning of the twentieth century, the predominant commercial arrangement was

the concession contracts2, under which governments allowed international companies to

explore and produce their natural resources usually for a long period of time, over a large area

with limited or no intervention of the governments in the operations, against payment of a

signature bonus and royalties (JOHNSTON, 1994). It started with the signature of the Persian

contract in 1904 (SMITH, 2000a) considered therefore as the classical concession. However,

the unbalanced terms of the contracts in favor of the companies soon became noticeable

triggering attempts to revise them. Slowly, the host countries started to act towards exercising

more control over its natural resources. The chosen alternatives included renegotiation of the

terms, creation of new types of arrangements and even a complete banishment of the

international companies, as Mexico did in 1933 when it nationalized its petroleum industry

(YERGIN, 1991).

One of the new structures created to replace the concession contract was the production

sharing agreement (JOHNSTON, 1994). An attempt made by Indonesia, after its independence,

to increase control over its natural resources growing the Government´s profits

(TOLMASQUIM, 2011). As the ownership was being shifted to the Government, they would

now decide how the companies would take their share, part based on the investment made and

part built on the amount of profit the State would allow the companies to have. This model,

after its implementation in the early sixties, became very popular as an alternative for the

nations to restrict the dominance of the international oil companies in their territories and obtain

a higher take of the generated oil rent. and suffered several modifications accommodating

different needs each country had (JOHNSTON, 1994). On top of the classic concessions and,

productions sharing agreements, participation agreements and service agreements were also

used by host countries according to their discretion (DZIENLOWSKI, 2000; SMITH, 2000b).

In Brazil, the use of oil increased in the fifties with a late industrialization, creating an

oil-based economy (IBGE, 2018). Initially, the national oil industry was heavily dependent on

2 Concession contracts, production sharing agreements and service contracts are types of petroleum fiscal

models that will be described in more details in chapter 2.

3

imports but, as in many other countries, the increase of crude oil prices in the seventies,

generated, among other consequences, an intensification of efforts to increase national oil

production to reduce the dependency on the imported oil (NOGUEIRA HALLACK et al.,

2017).

Until 1997, the exploration and production of crude oil was a national monopoly

exercised by Petrobras. During that time, the first fields of 2 to 3 bln bbls were found,

inaugurating a cycle of giant field discoveries (MORAIS, 2013). In 2007, Petrobras announced

the existence of a major oil basin with estimated recoverable resources up to 176 bln bbl3

(JONES; CHAVES, 2016; LIMA; LIMA, 2017). This represented more than ten times the

country's reserves 4in 2007. Actually, 11 years after the first discovery, the pre-salt represents

more than 50% of the whole country's production reaching 1.8 mln boe/d in 2018, also

impacting other countries such as Portugal whose 43% of its oil comes from the Brazilian pre

salt (ANP, 2018a).

When the exploration and production segment was opened to foreign capital in 1997, the

government implemented several changes aiming to create a competitive scenario in the

industry. Particularly, an independent regulatory petroleum agency (ANP) was created and the

fiscal policy applied to petroleum production was reviewed. Brazil has several taxes at

different levels (national and subnationals) applied to goods and services for national and

imported materials. As oil and gas production depends on long-term projects, most of the

investment is made in the early years before receiving any revenues (UNITED NATIONS,

2017). This cash flow usually justifies fiscal incentives aiming at reducing taxes on costs at the

early years, but shifting their payment for when production had already started generating

revenue.

Moreover, at the end of the 1990s, Brent oil price was around $20/bbl (EIA, 2020a) and

Brazil wanted to attract investors. Therefore, a particular fiscal incentive was created in 1999,

the so-called Repetro (BRASIL, 1999), being established as a temporary special tax regime to

exempt taxes from imported and nationalized products associated with the country´s oil

industry. Twenty years later, despite a recently revision of the fiscal regime, this incentive

remains essentially the same, but now it was set to last until 2040 (LIMA, 2017).

3 Although these are not proved reserves, this resource value is for P90, showing a higher confidence to be

compared with Brazil proved reserves. 4 The proved oil reserves in 2007 were 12.6 bln bbl.(ANP, 2018c)

4

As mentioned before, this kind of incentives or hidden subsidies is commonly used in the

economy as a mechanism to stimulate specific segments of the business when they cannot,

under market conditions, provide return on investments and, consequently, would not happen

otherwise. As oil is still an energy source with strategical value to most economies,

governments want to increase their production and can make use of incentives or hidden

subsidies for this purpose (BHATTACHARYYA, 2011; CHEVALIER J.-M, 2004; SILVA,

2018; SOVACOOL, 2007) But they would have to balance the initiatives to increase

production with their revenues as taxes over oil activities compose a relevant fraction of

governments´ primary revenue (GERASIMCHUK et al., 2019; KOJIMA, 2009).

It is noted that oil business has many inefficient hidden subsidies, even with commitment

from countries such as US, China, India and European Union to remove them (ERICKSON et

al., 2017). Those subsidies are not needed to promote the production. Instead, they end up

enlarging producers’ profits. Actually, incentives are given to promote projects that would be

developed anyway (ERICKSON et al., 2017). Under the aegis of the theory of exhaustible

resources, Hartwick proposed that the scarcity rents from producing those resources should be

reinvested in reproducible capital (HARTWICK, 1977). Besides, from the perspective of an

energy transition from fossil fuels to renewable energy sources (WILSON, 2012), this rent

could be used to promote not yet competitive domestic low-carbon energy sources

(GOLDEMBERG et al., 2014), with the potential co-benefit of generating income and jobs

(COLLINS; HANSEN; HENDRYX, 2012; SANTOS et al., 2016; SORIA et al., 2015).

1.1 Hypothesis and Objective

There is a chance that the fiscal incentives given to the pre-salt oil industry in Brazil are

generating excessive petroleum rents to the oil companies in detriment of the Stat Therefore,

this dissertation aims to estimate the impact of the fiscal incentive Repetro and accelerate

depreciation on Brazilian petroleum fields in the oil frontier called “pre-salt”, which is ruled

by production sharing contracts (PSC). If the existence of unnecessary (hidden) fiscal

incentives is proved, these should be classified as extra rent (windfall profit) for the contractors

(or operators), which, at the same time, reduces the government take. Moreover, in the light

of climate change challenges and commitments assumed by the country in Paris (BRASIL,

2015), and Brazil´s urgent social needs, unnecessary fiscal incentives shall be reviewed

5

towards investments in innovative energy systems beyond the peak of oil supply and demand

in Brazil.

1.2 Dissertation Structure

In order to meet the objective, this dissertation is structured into 6 chapters including this

introductory one. Chapter 2 presents the main existing petroleum fiscal systems for oil and gas,

including the main concepts involving the fiscal terms and examples from countries with a

significant participation in the global oil industry history. That chapter also includes a brief

description of how the economic analysis is performed by the oil companies, highlighting the

drivers for an investment decision. In Chapter 3, Brazil’s petroleum fiscal system is described

including a brief history of how the country´s oil industry started and reached the level of

importance it has today, including the legal framework behind the different moments of oil

regulation in Brazil. In this part, the actual existing fiscal system and in place tax incentives for

the industry are presented. The methodology and the database used in this dissertation for both

the base and sensitivity cases are described in Chapter 4. Chapter 5 is where the results are

presented along with the discussion of findings. Finally, chapter 6 contains the conclusions and

suggestions for future work.

6

2 PETROLEUM FISCAL SYSTEMS

This chapter presents the commercial terms under which governments contract operators

to extract value from their hydrocarbon resources and how the contractors assess the value of

the areas, including:

• The discounted cashflow method applied to oil and gas industry;

• The fiscal terms used in the oil and gas industry to extract rent;

2.1 Oil and gas exploration and production commercial models

In the early years of the modern oil industry, oil exploration and production proceeded

from a reduced number of countries with a commercial model based on direct negotiations

between host countries and oil companies, the main actors of the industry at that time

(YERGIN, 1991). Classical concession contracts were the preferred instrument to regulate the

contract based on long term relationships and royalty payment, most of the time (BRAGA;

SZKLO, 2014; BRAZIL, 2015; MATHIAS, 2008; YERGIN, 1991; ). With time, the actors and

the roles they played changed based on the world conjunctural social, political, economic and

technological factors. It drove the creation of other types of contractual arrangements to

remunerate host countries and companies in oil and gas business such as production sharing

agreements and service contracts.

The drivers behind the contracting arrangements were a weight between risk and reward

for the governments and companies given the lifecycle and nature of oil and gas projects

(JOHNSTON, 1994).

2.1.1 Fiscal terms premises

In order to describe the main modalities under which hydrocarbons were and still are

explored and produced, three main concepts that drive the fiscal systems commercial structures

need to be described. The first one is related to the lifecycle of the projects and how it impacts

the fiscal terms. The second one is the ownership of reserves, which is directly related to how

a company, either national or multinational, have access to the reserves and the third one is

related to the types of taxes the fiscal system are composed of, which are they and how they

7

have been used throughout the time by host countries as instruments to appropriate part of the

rent generated in the petroleum activity.

2.1.1.1 Oil and gas projects lifecycle

Oil and gas projects can be explored and produced in different ways, depending on the

location of the resources, the type of reservoir and available technology, among other factors.

For a large offshore conventional reservoir, the lifecycle of a typical oil and gas project includes

the phases of licensing, exploration, appraisal, development, production and abandonment (DA

HORA et al., 2019; TORDO, 2007). The first phase, licensing is when the government grants

a license to a company to execute activities of exploration, and production. It can be granted

through a competitive action or through direct negotiations and usually is for a limited period

of time. The exploration phase is associated with risk, despite the current available technologies

for prospecting hydrocarbons. Geophysical and geological methods to prospect hydrocarbons

are based on complex theories (THOMAS, 2001), but only after drilling wells there is certainty

about oil accumulations. Moreover, it takes dry holes, more or less, depending on the area, to

get to a successful well. The world offshore success exploration rate was around 32% in 2018

and since 1990, this value has never gone over 50%, with an average for the period just below

40% (KUNJAN, 2016; RIPED, 2019). Going forward, if oil and or gas are found, the appraisal

phase will start to delimitate the volumes and collect more information to select the best

development option for the field. The development phase is when all the necessary equipment

to produce oil/gas over the life of a field, which is on the range of 30 to 40 years5, is put in

place. It is the phase where the major investments are made. Profits, however, will only come

after oil or gas is produced in the production phase.

For the lifecycle of an oil and gas project, it is important to mention the difference

between conventional and unconventional resources. The first situation, that will be the basis

for this dissertation, includes the traditional reservoirs where permeability and porosity allow

the extraction of the resources through vertical wells with minimal stimulation and the

resources are trapped by rock formations. On the other hand, unconventional resources, due to

low porosity and permeability requires stimulation methods to extract them, such as hydraulic

fracturing.

5 This is not valid for unconventional fields, such as light tight oil in the United States.

8

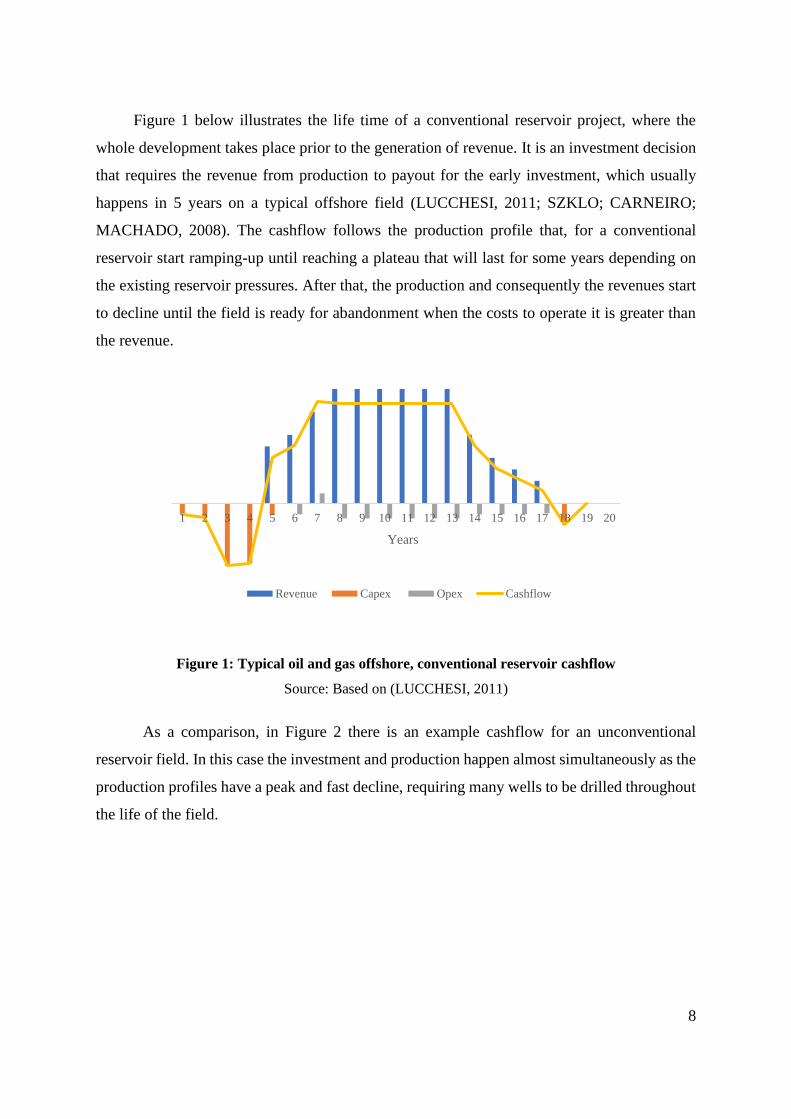

Figure 1 below illustrates the life time of a conventional reservoir project, where the

whole development takes place prior to the generation of revenue. It is an investment decision

that requires the revenue from production to payout for the early investment, which usually

happens in 5 years on a typical offshore field (LUCCHESI, 2011; SZKLO; CARNEIRO;

MACHADO, 2008). The cashflow follows the production profile that, for a conventional

reservoir start ramping-up until reaching a plateau that will last for some years depending on

the existing reservoir pressures. After that, the production and consequently the revenues start

to decline until the field is ready for abandonment when the costs to operate it is greater than

the revenue.

Figure 1: Typical oil and gas offshore, conventional reservoir cashflow

Source: Based on (LUCCHESI, 2011)

As a comparison, in Figure 2 there is an example cashflow for an unconventional

reservoir field. In this case the investment and production happen almost simultaneously as the

production profiles have a peak and fast decline, requiring many wells to be drilled throughout

the life of the field.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Years

Revenue Capex Opex Cashflow

9

Figure 2: Typical oil and gas offshore, unconventional reservoir cashflow

Source: Based on (KLEINBERG et al., 2016)

Therefore, given the nature of the typical offshore conventional reservoir cashflow, large

investments are required prior to monetizing the hydrocarbons. Usually, host countries do not

have the technical, human or financial resources to make investments that will take a long

period to mature.

For this reason, governments establish their petroleum law, or make direct negotiations

with the companies to allow them to make the required investment to generate profit in the

future for the companies but also to remunerate the governments. This balance between

government take and the companies return has been done under different types of contractual

arrangements over the time, being influenced by external factors, among others, such as price,

supply and demand for oil.

2.1.1.2 Ownership of reserves

To discuss ownership of reserves in fiscal terms, first it is necessary to determine how

the nations control their natural resources and what are the options they have to grant the private

companies the access to it.

Although today the sovereign of a nation signifies total control over a country resource,

in the past, the situation was that clear. There were situations when some countries faced

external pressure when deciding to unilaterally breaking existing oil and gas commercial

contracts, with even severe economic consequences. The main example was Mexico. In 1938,

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Years

Revenue Capex Opex Cashflow

10

they nationalized their oil industry expropriating all foreign oil companies´ assets. At the same

time, they created Pemex, their national oil company (SMITH, 2000a). The leaving companies

promoted an international boycott to Mexican oil and seek support for an official American

retaliation on international trade to the country (MAURER, 2011). Although the US

government did not engage in the call, it still took Mexico some time to find new markets for

its exported oil and new suppliers for the imported machinery (MAURER, 2011).

Mexico was the first, of a series of nations, that took actions towards increasing the

control over their mineral resources in detriment of private contractors. The next actions

included nor only nationalization but also revision of contractual terms in oil and gas

exploration and production. However, in the late events, the countries did not suffer the same

as Mexico. The main reason was the adoption, by the United Nations General Assembly (vote

of 87 to 2 with 12 abstentions), in 1963, of a Resolution on Permanent Sovereignty over Natural

Resources. By supporting this resolution, the countries, including the United States

“expressively sanctioned actions by foreign governments that unilaterally changed or revoke

long-term mineral development agreements” (SMITH, 2000a). This was the case for Iran in

1951 and lately the creation of OPEC in 1960, a collective act of sovereignty of oil exporters

(SMITH, 2000a).

Nowadays, according to the legal concept of ownership, “all mineral ownership regimes

are based on the jurisprudential theory of state sovereignty. The sovereign of a defined

geographical area has exclusive legal dominion over the area, including its natural resources.

Based on this concept, the petroleum law will define how property is assigned to mineral

resources. The sovereign can recognize private ownership of these resources or it can treat

them as State-owned. The sovereign can require all development of State-owned minerals to

be accomplished by a State agency, or it can authorize development by private companies,

including foreign corporations” (SMITH, 2000a).

Ownership of oil resources is important for companies as their value is directly associated

to the amount of reserves they have in their books. From a government perspective, maintaining

an oil stock can be strategical for economic and geopolitical purpose, as most economies are

based on oil products. Therefore, ownership is a key point taken into consideration when fiscal

terms are designed by host countries.

For a long time, governments allowed foreign companies to explore and produce their

mineral resources by conceding them areas where they could act by prospecting, extracting,

11

exporting and monetizing the oil against a tax payment, usually through royalties. By

conceding the companies a geographical area to work, the governments are giving them

ownership over the resources obtained in that area, it is a transfer of rights from the State to the

companies once they have permission to dispose the resources in their best interest.

This is the case in most jurisdictions where petroleum law establishes State ownership

for mineral resources, but there are exceptions such as USA, Canada and possibly same other

small countries (SMITH, 2000a) The principles of English common law provide that the owner

of the soil owns the minerals beneath his land, with the except of gold and silver which are

traditionally owned by the sovereign. United Kingdom, however, have changed their law to

rule against the principles of common law declaring, in 1884, that ownership of oil and gas is

in the Crown. Other countries also changed their law the other way around. Mexico which

originally followed the civil law basis of mineral law ownership regime, have changed its

legislation providing that petroleum and natural gas were the property of the owner of the soil

in 1892, reverting back to its original principal in the Constitution of 1917 (SMITH, 2000a).

Even in common law countries where there is provision for ownership of mineral resources by

the owner of the land, the State still holds the majority of oil accounting for the offshore

reserves, which are owned exclusively by the state (SMITH, 2000a)

Although concession of a land and ownership is still used in many countries as a fiscal

model to explore and produce hydrocarbons, there are other ways to allow companies, State-

owned or private, to develop a country’s mineral resources. These modalities usually include

more restrictions to the resources, at different grades, which can vary from treating them strictly

as contractors to a more hybrid combination of benefiting from their services but also allowing

them some discretion on disposing of the oil. The contracts can be called service contracts or

production sharing agreements, which will be described in more details further in this chapter.

Based on their sovereignty, the countries define their mineral law according to how

ownership, if any, will be assignment to the companies, with the broad type of fiscal terms

included in concession, service contracts or production sharing agreements.

2.1.1.3 Taxes commonly used in fiscal systems

Taxes are the instrument governments use to fund their activity. The amount of

collected taxes will vary according to how each jurisdiction understands the State participation

(UNITED NATIONS, 2017). A tax system can be composed of different types of taxes at

12

different jurisdictional levels, but usually taxes are charged on individual and companies´

incomes. In economic terms, taxation transfers wealth from households or businesses to the

government. The same way, taxes applied to oil business aims to promote a balance distribution

of the petroleum rent between the State and companies (UNITED NATIONS, 2017).

The existence of a petroleum rent in the same sense of the land rent proposed by David

Ricardo in his work “On the Principles of Political Economy and Taxation” from 1817

(RICARDO, 1817), is based on the principle that petroleum fields, as lands, might have

different costs of production, with some being more productive than others, generating an

economic advantage and therefore a petroleum rent. The reason behind the existence of these

rents are based on the following factors (TOLMASQUIM, 2011):

• Rent of mines: this type of rent differentiates the oil fields according to the

accessibility of the resources, like onshore and deepwater offshore fields, high

permeability vs low permeability reservoirs; fields with high productivity wells

vs low productivity wells;

• Rent of position: the rent here is attribute to the fields located closer to the

consuming centers, reducing their transportation costs and therefore increasing

the rent for those fields with better position;

• Rent of quality: in this case the rent comes from the quality of the resources that

provides a high commercial value for it, like higher API grade and lower level of

contaminants;

• Rent of technology: technology can make production more efficient and therefore

create a rent in the oil industry (TOLMASQUIM, 2011).

The petroleum rent is related to the economic or supernormal profit (JOHNSTON, 1994),

a gain that exceeds the normal profit obtained after remunerating the costs and the invested

capital. Assessing the petroleum rents and creating a reasonable distribution between the States

6and Companies is not a straightforward task.

The regular national tax system is usually not sufficient to extract the petroleum rent, the

reason why petroleum fiscal systems are put in place. When building or selecting an oil and

6 For democratic regimes, the production period of a conventional resource is longer than their terms, making

this a State decision that will last through different governments.

13

gas fiscal model, governments are trying to optimize their government take from the oil

business. Although taxes can be created in many formats, historically oil and gas fiscal systems

have some traditional instruments described in the list below:

• Bonus: this tax can be used in different ways throughout the life of the oil field.

It is usually associated to an acquisition cost of an area to be explored (SZKLO;

CARNEIRO; MACHADO, 2008), but it is not limited to this use. It can also be

paid as a compensation for extra production, as a production bonus (TORDO,

2007). It can be a lump sum payment or paid at different moments of a field life

(TORDO, 2007). If associated with an acquisition it will be paid when the area is

obtained, either through a competitive bid or through a direct negotiation. A lump

sum payment at the beginning of a project shall have a balance value in

comparison with the gains that will come in the future, as the cashflow of such

projects present a long time of pure investments before making profit. A key

element for setting the acquisition bonuses’ values are the risks involved in a

project. A different perception of those risks from the government, setting the

bonus, and companies, aiming to acquire blocks, might create a situation of low

or high competition if bonus are set too high or too low, respectively, according

to the companies’ views. For sure, the attractivity of an area is not determined

only by a bonus payment, it is a combination of factors, but since it is usually an

early lump sum payment, it can have a significant impact in the cashflow.

• Royalties – the taxes paid to the landowners for the right to explore minerals in

their land. The origin of this word is related to royal family as they were the first

owners of the land. The world remains the same but the owners are now

represented by the State or the actual land owner according to the type of

jurisdiction. Royalties are usually applied on the gross revenue, making it a firm

return to governments independent of how profitable the project is. It can be a

fixed amount throughout the life of the field (TORDO, 2007) but it can also come

in tranches, according to production (TORDO, 2007). Royalties can be collected

in cash or in kind. Given the importance of oil for governments to maintain their

security reserves, if they do not have a national oil company from where they can

promptly obtain oil, they can choose to receive the royalties´ payment in oil, i.e.,

in kind, as is the case in USA (MCMICHAEL; SPENCER, 2001).

14

• R-Factor – this is a tool used to adapt taxes to be charged in a sliding scale manner

(JOHNSTON; JOHNSTON, 2015; TORDO, 2007). This way the R-factor can be

determined based on a variable parameter that can reflect the profitability of the

field and therefore adjust the taxes according to its size and productivity7

(JOHNSTON; JOHNSTON, 2015). It can be used as an incentive to small fields

development. Royalty, for example could be a sliding scale rate based on the net

profit of the field (JOHNSTON; JOHNSTON, 2015), making the net profit the

R-factor in this case.

• Taxes on profits – usually defined by regular national income taxes, but there can

also be surtaxes, extra taxes on profits if excessive (windfall) returns are achieved.

Income taxes are common in most countries as part of the standard economy, not

particular to an oil and gas industry. This is a way the companies share their gains

with governments. In oil and gas industry, profit takes some years to be achieved

and governments usually recognize the investment made in the early years of the

project by allowing a late recovery through depreciation or carrying losses for a

period of time. However, governments can also create restrictions to establish

what can be deducted or not from income tax purposes, like signature bonuses for

example (TORDO, 2007).

Depending on how a fiscal system is created it can be more progressive or regressive.

Both concepts are related to how the investment decisions impact the results A model is more

progressive if the taxes are collected based on the results of the project, the better the results

the higher the taxes. In this sense, the taxes will not distort the results when an investment

decision is made. On the other hand, taxes that are payed up front, like bonus, or that will be

charged independently of the results of the project, are considered regressive. Although they

create a firm revenue for the governments, they distort the impact of the investment decisions

once those taxes will be collected in case of good or bad results (TORDO, 2007).

2.1.2 Concession Contracts

“Historically, leases and concessions have been the most commonly used agreements

between oil companies and governments or mineral owners. In such agreements, the host

7 The Brazilian Special Participation Tax is a R-Factor as it is applicable in the profit based on the productivity

of the field.

15

government or mineral owner grants the producing company the right to explore for, develop,

produce, transport, and market hydrocarbons or minerals within a fixed area for a specific

amount of time. The concession and production and sale of hydrocarbons from the concession

is then subject to rentals, royalties, bonuses, and taxes. Under these types of agreements, the

company typically bears all risks and costs for exploration, development, and production and

generally would hold title to all resources that will be produced while the agreement is in effect.

Reserves consistent with the net working interest (after deduction of any royalties owned by

others) that can be recovered during the term of the agreement are typically reported by the

upstream contractor. Ownership of the reserves producible over the term of the agreement is

normally taken by the company; however, if the contract is voided for any reason, ownership

reverts back to the mineral owner or government (MCMICHAEL; YOUNG, 2001).”

The figure below illustrates how the revenue is divided with the between the contractor

and the government. In this case, the f is under the contractor´s control. He is the one

responsible to collect royalties and taxes to the government and also to make all the required

investment to the project. The project income is normally subjected to taxes. The middle

column indicates the project and the arrows indicate which part, either the government or the

contractor is responsible for what.

Figure 3: Concession contract structure

Source: Based on (JOHNSTON, 1994)

Revenue

Royalty

Costs

Profit

Taxes

Contractor Government

Total Profit

Received

16

2.1.3 Production Sharing Agreements

“In a production-sharing agreement between a contractor and a host government, the

contractor typically bears all risks and costs for exploration, development, and production. In

return, if exploration is successful, the contractor is given the opportunity to recover the

investment from production (cost hydrocarbons), subject to specific limits and terms. The

contractor also receives a stipulated share of the production remaining after cost recovery

(profit hydrocarbons). Ownership is retained by the host government; however, the contractor

normally receives title to the prescribed share of the volumes as they are produced. Reserves

consistent with the cost recovery plus profit hydrocarbons that are recoverable under the terms

of the contract are typically reported by the upstream contractor. ” (MCMICHAEL; YOUNG,

2001)

The production sharing agreement (PSA) started in Indonesia in an effort to exercise

more control over their resources, increase the participation of the State on the projects profits

and start a transfer of knowledge to the country (TOLMASQUIM, 2011) . Soon many countries

followed the example with the same intent.

The traditional structure for a PSA assumes a cost recoverable rate and a profit oil rate.

The first one is the percentage under which the contractors will recover their costs. After the

recovery of the costs the remaining volume is shared between the government and the

contractor. The first PSC did not have royalties payment, nor taxes, but with the time, different

jurisdictions adapted this type of contract making modifications (TORDO, 2007; UNITED

NATIONS, 2017). The figure below describes a PSC with royalty and taxes. The middle

column representing the project and the contractor and government columns to illustrate the

flow of income, costs and taxes.

17

Figure 4: General production sharing agreement structure

Source: Based on (JOHNSTON, 1994)

2.1.4 Service Contracts

2.1.4.1 Revenue-Sharing/Risked-Service Contracts

“Revenue-sharing contracts are very similar to the production-sharing contracts

described before, with the exception of contractor payment. With a risked-service contract, the

contractor usually receives a defined share of revenue rather than a share of the production. As

in the production sharing contract, the contractor provides the capital and technical expertise

required for exploration and development. If exploration efforts are successful, the contractor

can recover those costs from the sale revenues.” (MCMICHAEL; YOUNG, 2001)

“A very similar type of agreement is commonly known as a risked-service contract. This

type of agreement is often used when the contracting party provides expertise and capital to

rehabilitate or implement improved recovery operations in an existing field. Provided that the

requirements for reserves recognition are satisfied, reported reserves are typically based on the

economic interest held or the financial benefit received.” (MCMICHAEL; YOUNG, 2001)

The same way, as in the prior petroleum fiscal models description, in figures 5 and 6 the

project and the flow views for contractors and government are described.

Revenue

Royalty

Cost Recovery

Profit Split

Taxes

Contractor Government

Cost Oil

Profit Oil % Profit Oil

(100 - %)

Total

Entiltlement Oil

18

Figure 5: General revenue-shared contract structure

Source: Based on (JOHNSTON, 1994)

Figure 6: General risked-service contract structure

Source: Based on (JOHNSTON, 1994)

2.1.4.2 Pure-Service Contracts

“A pure-service contract is an agreement between a contractor and a host government

that typically covers a defined technical service to be provided or completed during a specific

period of time. The service company investment is typically limited to the value of equipment,

tools, and personnel used to perform the service. In most cases, the service contractor’s

reimbursement is fixed by the terms of the contract with little exposure to either project

performance or market factors. Payment for services is normally based on daily or hourly rates,

a fixed turnkey rate, or some other specified amount.

Revenue

Royalty

Cost Recovery

Revenue Split

Taxes

Contractor Government

Cost Revenue

Profit

Revenue% Profit Revenue

(100 - Oil %

Total Revenue

received

Revenue

Investment

Expertise

Peformance

Taxes

Contractor Government

In-kind or

monetary

payment

Remainder after

contractor

payment

Total payment

received

Contractor payment

19

Payments may be made at specified intervals or at the completion of the service.

Payments, in some cases, may be tied to the field performance, operating cost reductions, or

other important metric.

Risks of the service company under this type of contract are usually limited to

nonrecoverable cost overruns, losses owing to client breach of contract, default, or contract

dispute. These agreements generally do not have exposure to production volume or market

price; consequently, reserves are not usually recognized under this type of agreement.”

(MCMICHAEL; YOUNG, 2001)

Figure 7 below illustrates the model.

Figure 7: General pure-service contract structure

Source: Based on (JOHNSTON, 1994)

2.1.5 Others

“There are other types of petroleum fiscal contracts that resume the ownership of the

resources on the financial resource holder. Under this category are the loan agreements, where

the contract is executed under a loan agreement that will be remunerated in case of success;

production loan, forward sales, carried interest, purchase contract, production payment and

conveyances. In all cases, there is a third party involved with the contract in a position of

financial investor, that have vested rights over the field, and will be remunerated through a

compensations scheme, production itself, a higher participation share in the future, buyers of

the contract itself or the buyers of the future revenue.” (MCMICHAEL; YOUNG, 2001)

Revenue

Investment

Expertise

Peformance

Taxes

Contractor Government

Monetary

payment Remainder after

contractor

payment

Total payment

received

Contractor payment

Taxes

20

2.2 Discounted Cashflow Analysis

When accessing the value of oil and gas assets, it is possible to use a market or an income

approach. The market approach consists on comparing the asset or company being assessed

with similar assets traded in the market. This method is based on external information, on how

investors see the value of that asset. The income approach relies on the income value the asset

will generate, based on intrinsic company data. The discounted cashflow is a type of income

methodology (KIBBEY; RASOR; BOSTWICK, 2017).

The discounted cashflow (DCF) is widely accepted in oil and gas business due to the

singular geology nature of the projects. In this method, the asset is evaluated based on the

cashflow it will generate in the future, throughout its lifetime. However, in this method it is

necessary to have a detailed information about the asset and reasonable assumptions for future

macroeconomic and commercial parameters on top of the good understanding for the location

tax system.

The results will be a projected annual free cash flow of the asset for its lifecycle that is

discounted to present using a discount rate. This rate is variable according to each company’s

Weighted Average Cost of Capital (“WACC”), that reflects the risk of the projected cash flows.

The limitation of a DCF analysis lie on the level data required and the uncertainties related to

future projections such as macroeconomic and commercial variables.

An economic analysis can be done at different levels of details and scope, especially if

aggregated with financial considerations. One important point is related to whether the cost of

financing the project is included or not in the analysis, meaning geared or ungeared assessment,

respectively. For asset economics in upstream projects usually ungeared analysis are made

based on the equity only. Therefore, a typical simplified cashflow structure considering only

income taxes will be as follows:

𝑅𝑒𝑣𝑒𝑛𝑢𝑒 = 𝑃𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛 𝑥 𝑃𝑟𝑖𝑐𝑒 (1)

𝑃𝑟𝑜𝑓𝑖𝑡 = 𝑅𝑒𝑣𝑒𝑛𝑢𝑒 − 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑎𝑙 𝐶𝑜𝑠𝑡𝑠 − 𝐷𝑒𝑝𝑟𝑒𝑐𝑖𝑎𝑡𝑖𝑜𝑛 (2)

𝑇𝑎𝑥 = 𝑃𝑟𝑜𝑓𝑖𝑡 𝑥 𝑇𝑎𝑥 𝑟𝑎𝑡𝑒 (3)

21

𝐶𝑎𝑠ℎ 𝑓𝑙𝑜𝑤 = 𝑅𝑒𝑣𝑒𝑛𝑢𝑒 − 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑎𝑙 𝐶𝑜𝑠𝑡𝑠 − 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 𝐶𝑜𝑠𝑡 − 𝑇𝑎𝑥

− 𝐷𝑒𝑐𝑜𝑚𝑖𝑠𝑠𝑖𝑜𝑛𝑖𝑛𝑔 𝐶𝑜𝑠𝑡𝑠 + 𝑆𝑎𝑙𝑣𝑎𝑔𝑒 𝑉𝑎𝑙𝑢𝑒

(4)

This operation will occur on an annual basis until the costs for operating the fields

exceeds the revenue generated by the production. Those yearly cashflows will then be

discounted to the present date according to the following formula:

𝑃𝑉 =𝐶𝑇

(1 + 𝑟)𝑇

(5)

Where:

PV is the present value

CT is the cashflow in the period T

T is the period

r is the discount rate.

At the end the sum of all the present values will the net present value (NPV) of the

cashflow. This is the metric used to demonstrate the absolute value of a project.

Another important metric that can be extracted from the cashflow is the internal rate of

return (IRR). This metric is related to the discount rate. It is the discount rate at which the NPV

will be zero. The value of this metric is to given indication of the discount rate, which can be

different according to the companies´ ability to finance their projects and assume risk.

Part of the costs to the deducted for taxes calculation is the depreciation. Depreciation is

an accounting instrument to consider the aging of the equipment used in a project. Profit

calculation considers the deduction of the operational costs from the revenue, once both of

them occur in the same counting period. Equipment is used throughout the life of the field or

for a long time, requiring a different methodology to be discounted from the revenue to generate

the profit. The depreciation is a way to account for the life of the asset and discount it from the

profit over a period.

The depreciation can be done in different ways, the straight-line basis and units of

production are two of them(TORDO, 2007) . The first one assumes the investment schedule

will be linear for a period of time. The second one assumes the asset will last throughout the

life of the field and will be depreciated on the same production profile. Figures 3 and 4 below

illustrates both depreciation methods for an example of a US$ 2000 mln investment:

22

Figure 8: Straight line depreciation

Source: Based on (MOTTA; CALÔBA, 2002)

Figure 9: Unit of production depreciation

Source: Based on (MOTTA; CALÔBA, 2002)

Depreciation can be used as a fiscal incentive as it impacts directly the taxable profit,

reducing it and consequently reducing the due income taxes. For this reason different

depreciation schedules that could anticipate the deduction would mean early benefits to a

project (TORDO, 2007) . One of the options to benefit the tax payer is through an accelerated

depreciation. In this modality, the method of depreciation is the same, but the distribution of

the depreciated costs over the time is different, with more value occurring earlier.

0

50

100

150

200

250

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

US

$ m

illi

on

tho

usa

nd

bar

rels

per

day

Production Depreciation Straigh line

0

50

100

150

200

250

0

20

40

60

80

100

120

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23U

S$

mil

lio

n

tho

usa

nd

bar

rels

per

day

Production Depreciation UOP

23

2.3 Application of petroleum fiscal systems

Worldwide, countries make use of the fiscal systems to balance incentives to private

investments in the oil business and the government take. This balance requires constant

revision to accommodate the global changes in politics, economics and technology that have

impact on oil and gas products supply and demand. Some examples of how these instruments

have been applied are described in Appendix III highlighting the variety of fiscal regimes and

also how they changed over the time, the countries regulatory history, their relevance on global

oil and gas production and reserves and their current fiscal system.

Other countries experiences serve as examples for new policies and adjustments of the

existing fiscal terms in Brazil. Although each country has its own singularities, it is still

possible to infer conclusions from the correlation of production changes in fiscal terms over

the time. In Annex II there is a description of the fiscal systems in Indonesia, Iran, Norway and

United States.

3 BRAZIL´S OIL AND GAS FISCAL REGIMES

The national oil and gas industry had gone through different phases all over the years.

Brazil started its history as a massive oil importer becoming a net oil exporter only in this

century (ANP, 2018a; LUCCHESI, 1998). At the same time, the regulatory model went

through moments of State monopoly period but also of openness to private investors. From

1953 to 1997, Petrobras was the only company allowed to invest in exploration and production.

After this period until the present data, the oil market in the country is opened to private

investors, which can make investments under concession contracts or production sharing

contacts, depending on the area (LUCCHESI, 2011). The general fiscal system of the country

includes the use of indirect taxes and special tax regimes created for the industry (COIMBRA;

ALMEIDA, 2012).

This chapter describes the oil and gas industry in Brazil and the legal framework that

permeated the changes over the time of the fiscal regimes established in the country. Also

included is a summary of the country´s general fiscal system applicable to the industry.

24

3.1 Oil and gas history in Brazil

Kerosene was first petroleum byproduct used commercially in Brazil replacing the

whales’ oil in the lightening system of the major cities in the country (ANP, 2019). Electricity

soon replaced the use of oil in the lightening system, but oil became even more necessary in

the incipient automobile industry at that time (SHELL, 2012). In 1910, Brazil's economy was

driven mostly by coffee exportation, but the society was already experiencing the use of cars.

The first models were imported, but from 1920, Ford and General Motors, started a line of

assembly in the country, all material were imported but the cars were assembly in Brazil

(NASCIMENTO, 2016). The major international oil companies, Shell, Standard Oil and

Texaco, were already in the country (ANP, 2019) first selling kerosene to latter participating

with gasoline and fuel oil (SHELL, 2012).

This initial period of the century was also marked by an intense search for oil. On the

global scenario, this period encompasses big discoveries in USA, Persia and Indonesia, driving

private efforts to find oil (YERGIN, 1991). Although, the first Brazilian discovery took place

in São Paulo between 1892-1897 (LUCCHESI, 1998), it was not until 1939 that the first

commercial discovery was made in the Lobato well in Bahia (LUCCHESI, 1998).

After both global wars, the use of oil had become strategical and have expanded, with

also the petrochemical industries (TORRES, 1997; YERGIN, 1991).

In the fifties, Brazil´s economy went through changes, with many investments in the

industrialization, moving from a predominantly rural based economy (FURTADO, 2005). The

restrictions imposed by World War II, impacted the availability of international goods,

stimulating the creation of a national industry to replace the items that were no longer available

(FURTADO, 2005).

The strategic value of the oil was reflected in Brazil as an internal movement to

nationalize the industry (DIAS; QUAGLINO, 1993). In 1953, the major international oil

companies were present in both the upstream and downstream segments and were severe

affected when Petrobras, the national oil company, was created in that year to hold the

monopoly of the activities of exploration, production, commercialization, refining and research

(DIAS; QUAGLINO, 1993). The only segment of the industry still opened for the private

companies was the distribution of fuels (DIAS; QUAGLINO, 1993).

Petrobras pace to make discoveries was slow at the beginning. While counting on the

revenues from the Bahia onshore production, the company invested in developing the

25

knowledge in geology and petroleum science, by training people mainly in the United States

to perform studies on the sedimentary basins all over the country. Many wells were drilled at

that time but fewer discoveries were made (LUCCHESI, 1998).

The oil shocks in 1973 and 1975, increased the cost of imported oil impacting the most

economies, including Brazil (EIA,2020; Yergin,1994). The country dependency on imported

oil aggravated the need to find reserves. At that time, based on the frustration about the

domestic exploration results, an international branch of Petrobras was created to look for oil

outside the country (LUCCHESI, 1998).

However, the increase in oil prices also enabled deeper offshore exploration, which

continued based on the initial drilling on the continental platform with the discoveries of the

Garoupa, Namorado and Enchova, among others (DE MENDONÇA; SQADINI; MILANI,

2003; LUCCHESI, 1998).

The deeper offshore proved to be prolific and in the eighties the first big discoveries were

made, first in 1979 with the Albacora field, than with Marlin, Barracuda and Roncador fields,

with oil in place estimated from 2.7 to 9 bln bbl (DE MENDONÇA; SQADINI; MILANI,

2003).

In 1997, changes were made in the regulatory system , opening the industry to private

investors and creating new players in the industry (LUCCHESI, 2011). The discoveries

continued to happen increasing the countries production and reserves (MENDONÇA;

SPADINI; MILANI, 2003). However, in 2007, a new oil province was found which changed

the country´s position for production and reserves, it was the pre-salt.

The discovery of the pre-salt province, a thick layer of rocks created before the salt and

located under this salt layer, created a new perspective in terms of reserves and production in

the Campos and Santos basins (PEDROSA JR; CORRÊA, 2014). According to (Jones and

Chaves, 2016) the area can aggregate 144 bln boe and in 2019, the proved reserves were around

13 bln boe (EIA, 2020b). If all the estimated volumes were to be included as reserves, that

would shift Brazil from the 15th position to the 5th, behind only Venezuela, Saudi Arabia,

Canada and Iran (EIA, 2020b). The graph below illustrates the increase of production in Brazil

after the discovery of the pre-salt.

26

Figure 10: Brazil’s historical oil production and consumption

Source: EIA, 2020a

3.1.1 Legal Framework history of the industry in Brazil

Brazil oil regulation history alternated moments with less and more State intervention,

with a long State monopoly period before opening the market to private investors in 1997 until

now (ALMADA; PARENTE, 2013; ANP, 2019). The current legal framework combines the

existence of concessions contacts, production sharing agreement and a third modality called

transfer of rights or onerous assignment contract (Transfer of Rights) (ALMADA; PARENTE,

2013).

Brazil oil industry remotes to the nineteenth century. At that time, there were not specific

regulations related to oil and gas industry. In this scenario, the first concession contract was

awarded to a British citizen to extract oil and other mineral for 90 years on Camamu and Ilhéus

counties in 1864 (LUCCHESI, 1998). Those areas never produced oil but it was a

demonstration of the participation of private entrepreneurs in the oil industry and the

application of a classical concession model in Brazil.

Below are described the key regulations related to oil and gas industry until 1953 (PPSA,

2018), when Petrobras, the national oil company (NOC) was created. They represent the

growing of petroleum participation in the political and economic life of the country at the same

time this source of energy was reaching a higher participation in the world economies.

• Constitution of 1824 – there was no clear provision in this law regarding the

mining rights, but doctrine understood that there was a separation of surface and

0

500

1000

1500

2000

2500

3000

3500

4000

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

20

17

tho

usa

nd

bar

rels

per

day

Production Consumption

27

subsurface rights, with the subsurface belonging to the State in the best interest

of the society. In this case, the State could authorize a private agent to explore

the subsurface through concessions. In this period, the Emperor Dom Pedro II,

gave 3 exploration concessions, one to explore petroleum in the Province of

Bahia and two in the Province of São Paulo (PPSA, 2018).

• Constitution of 1891 – this was the first constitution under the republican

government and it was influenced by the American model. Therefore, it included

expressively in its article 72 that the owner of the land was also the owner of the

subsurface and consequently would have control over the existing minerals in

the land (BRASIL, 1891).

• Federal Decree no 6323/1907 – created the Geological and Mineralogical Service

in Brazil to study and maintain geological data of the country (BRASIL, 1907).

• Federal Decree no 2933/1915 (Calógeras Law) – it was the first mining

legislation in Brazil to regulate its ownership. In its text it includes oil as a

possible as a mine product. It also had provision to separate the surface and

subsurface rights (BRASIL, 1915).

• Law no 4265/1921 – in this law there was a new regulation of the property but

it was also the first time the mining exploitation activity was regulated. In this

law the term fossil fuels were included as a mining product, expanding the

possibilities to also natural gas (BRASIL, 1921).

• Constitution of 1934 – this new constitution was done under the Mexican

influence and in recognition of the petroleum as a strategical resource. For this

reason, the article 118 brought an express separation of the surface and

subsurface rights, being the State responsible for the control, supervision and

concession of those areas (BRASIL, 1934a).

• Federal Decree no 23979/1934 – Creates the National Department of Mineral

Production (DNPM) (BRASIL, 1934b).

• Federal Decree no 24642/1934 – First Code of Mines including definitions of oil