Embed Size (px)

Citation preview

The impact of Fed’s balance sheet unwind on CEE

7th Annual NBP Conference on the Future of the European Economy (CoFEE)

20 October, 2017 Warsaw

Juliusz Jabłecki, Economic Analysis Department, NBP

*The views presented are mine, and not necessarily those of the NBP

0

1

2

3

4

5

0

1

2

3

4

5

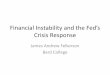

07m1 09m1 11m1 13m1 15m1 17m1 19m1 21m1

Treasuries

MBS

Other assets

USD trillion

Launchof QE1

Launch of QE2

Launch of QE3

The end of QE3

Beginning of balance sheet

reduction process

Effective in October 2017, the Fed is „taking away the punchbowl”

„…In October, the Committee

will initiate the balance sheet

normalization program…”

Yield to maturity

Time to maturity

Nominal yield = Expected short-term rate + term premium

Asset purchases lower yields by compressing „term premium”

3

Yield curve

Expected short-term rates

Term premium

-2,5

-2

-1,5

-1

-0,5

0

0,5

1

1,5

1 2 3 4 5 6 7 8 9 10

Time to maturity (years)

Change inexpected shortrates

Change interm premium

Change inyields

US yield curve changes 2009-2015 (percentage pts.)

4

US term premium developments spill over to emerging markets…

-1

0

1

2

3

4

5

-4

-2

0

2

4

6

8

08m1 10m1 12m1 14m1 16m1

Government bond yields in emerging market economies

Term premia in the United States (rhs)

per cent per cent

Bond yields in EM: 1st principal component of bond yields in CEE and Brazil, Columbia, Mexico, Korea, Turkey and South Africa.

5

US term premium developments spill over to emerging markets…

-1

0

1

2

3

4

5

-4

-2

0

2

4

6

8

08m1 10m1 12m1 14m1 16m1

Government bond yields in emerging market economies

Term premia in the United States (rhs)

per cent per cent

In good times…

6

US term premium developments spill over to emerging markets…

-1

0

1

2

3

4

5

-4

-2

0

2

4

6

8

08m1 10m1 12m1 14m1 16m1

Government bond yields in emerging market economies

Term premia in the United States (rhs)

per cent per cent

…and in bad (taper tantrum

sends yields up by +100bp)

Historically low inflation premium… unlikely to go up any time soon

7

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

93q4 96q4 99q4 02q4 05q4 08q4 11q4 14q4

percentage point

Inflation forecasts dispersion (4-quarter moving average)

Average level (1993-2017)

0

50

100

150

200

250

300

Ma

y-0

9

Ja

n-1

0

Se

p-1

0

Ma

y-1

1

Ja

n-1

2

Se

p-1

2

May-1

3

Ja

n-1

4

Se

p-1

4

May-1

5

Ja

n-1

6

Se

p-1

6

Ma

y-1

7

bps

3% cap 4% cap

The cost of hedging against US inflation

averaging above 3% and 4% in the next 5Y

Dispersion of forecasts of US inflation in the next 10Y

5Y zero-coupon CPI cap premiums. Source: BloombergDifference between 75-25 percentiles of SPF forecasts distribution.

Source: Philadelphia Fed

Historically low „expected” volatility of long-term yields

8

0

50

100

150

200

250

93q1 96q1 99q1 02q1 05q1 08q1 11q1 14q1 17q1

basis points

Merrill Lynch Option Volatility Estimate; weighted average of normalized implied volatility on 1-month Treasury

options; Source: Bloomberg

Regulatory pressure boosting banks’ demand for US treasuries

9

$100 reduction in Fed balance

sheet

$100 reduction in

bank reserves

$100 reduction in

HQLA

Reduction in LCR

The impact of ECB APP on CEE

10

Supplementary slides

11

CEE yields and DE term premium

-1

0

1

2

3

4

5

-4

-3

-2

-1

0

1

2

3

4

08m1 10m1 12m1 14m1 16m1

Government bond yields in CEE

10Y Bund term premium (rhs)

per cent percentage point

Are ECB asset purchases „destroying” fixed income markets?

12

Source: ECB survey on credit

terms and conditions in euro-

denominated securities

financing and over-the-

counter derivatives markets

Changes in liquidity and functioning of markets (net percentage of survey respondents)