Embed Size (px)

Citation preview

1

THE IMPACT OF CLIENT INTIMIDATION ON AUDITOR INDEPENDENCE

IN AN AUDIT CONFLICT SITUATION

Damai Nasution*

* Corresponding author; email: [email protected]

, Ralf Östermark

School of Business & Economics

Åbo Akademi University

Finland

A DRAFT VERSION 18 OCTOBER 2012

Please Do Not Quote without Permission

2

Abstract

An audit conflict situation is argued may impair auditor independence; especially when a client exerts

pressures to an auditor in order to get favored results. Client pressures can manifest into several

forms, one of these is intimidation in which a client threatens to replace the auditor if the auditor

does not tend to the client’s position. This study aims to investigate the impact of client intimidation

on auditor independence in an audit conflict situation. It also attempts to investigate the impact of

auditor’s perceived pressure on auditor independence. Finally, this study also explores the

moderating roles of auditor’s professional commitment dimensions in the relationship between

auditor’s perceived pressure and auditor independence.

An instrument based case was administered to 119 auditors from mid-sized auditing firms in

Indonesia. The subjects were divided into two groups with the presence or absence of client

intimidation in an audit conflict situation. Auditor independence is measured through the net

equipment balance signed-off by auditors for equipment in question. The higher the net equipment

balanced signed by the auditor, the more likely the auditor compromised independence. ANOVA and

regression analyses were used to test the study’s hypotheses.

The results show that: (i) auditors who experience client intimidation in the audit conflict

situation will more likely to compromise independence than those who are in a similar situation but

do not experience the intimidation; (ii) auditors who experience the client intimidation perceive

higher pressure than those who do not experience it; (iii) auditors’ affective and continuance

professional commitment dimensions moderate the relationship between auditor’s perceived

pressure and auditor independence. The results indicate that the negative impact of client

intimidation on auditor independence; however, high auditors’ professional commitment can

hamper that negative impact.

Keywords: Auditing, auditor independence, audit conflict, client intimidation, perceived pressure,

professional commitment

3

INTRODUCTION

The public and regulators have expressed concerns regarding auditor independence for a long time.

However, these concerns culminated after a series of corporate failures that failed to be faulted by

auditors and restatements to audited accounts, e.g. the HIH Insurance (March, 2001) and One.Tel

(July, 2001) in Australia; Enron (October, 2001) and WorldCom (June, 2002) in the U.S.; Vivendi (July

2002) in France; Ahold (February, 2003) in the Netherlands; Parmalat (February, 2003) in Italy; and

Kanebo (2006) and Olympus (2011) in Japan. These corporate failures caused public to doubt the

independence of auditors and raise serious concerns to auditors’ ability to resist client management

pressures, especially in an audit conflict situation, and the overall value of auditing (Lin and Frazer,

2008; Ye, Carson, and Roger, 2011). The public places trust to auditor to conduct their duty in

independent ways. By benign the independence, auditor could increase the reliability and credibility

of financial statements. Thereby, the public can rely to the audited financial statements as a basis for

their decision; especially investment and loan decisions. Meanwhile, regulators concerns to auditor

independence are more likely to avoid any shock to the stability of capital markets caused by audit

failures.

An audit conflict situation is one of situations that may impair auditor independence. Accordingly,

Knapp (1985) stated that audit conflict is potentially a serious threat to auditor independence. It is a

situation in which there is disagreement between an auditor and a client over some accounting

issues. In the presence of audit conflict, the auditor commonly is in a weak position when dealing

with the client because of an imbalance of power between the auditor and the client; hence the

auditor is tending to be lenient to the client’s position. Moreover, the client, in order to get favored

results, can also exert pressures on the auditor. These pressures can be materialized into threats; one

of them is intimidation threat. The international Federation of Accountants (IFAC, 2012) also

categorizes this threat as one of five threats to auditor independence. Intimidation threat occurs

when a member of an auditing team may be deterred from acting objectively and exercising

professional skepticism by threats, actual or perceived from directors, officers or employees of an

audit client (IFAC, 2012). Accordingly, Bennett and Hatfield (2012) stated that client management

may use explicit or implicit intimidation tactics on auditors in order to achieve their goal. In the

survey that Bannet and Hatfield conducted, they found that auditors, especially staff-level auditors

often experience intimidation by audit clients. A common form of intimidation threat is the threat of

replacement of an auditor. For instance, as the Olympus scandal revealed in 2011, it also revealed

that Olympus replaced its auditor in 2009 as an outcome of a disagreement over accounting issues

(Layne and Ridley, 2011). In addition, Cheung and Hay (2004) found that shareholders believe that

4

intimidation threat affects auditor independence. Astonishingly, according to Fearnley, Beattie, and

Richard (2005), intimidation threat is the threat that has the least prohibition and safeguards in the

auditor independence frameworks.

Prior studies have examined the impact of audit conflict on auditor independence and found

important evidences. Yet, to our knowledge, there are no studies that directly examine the impact of

client pressures in the form of explicit client intimidation to replace the auditor on auditor

independence in an audit conflict situation. The lack of literature is motivating this study. Moreover,

DeZoort and Lord (1997) develop a pressures model described several variables that may affect how

auditors will behave in the presence of pressures. Hence, based on that model, this study includes

auditor’s perceived pressure and auditor’s professional commitment that might affect and moderate

auditor independence in the presence of client intimidation. Moreover, the present study advances

upon prior studies by using a multidimensional measure of professional commitment. Auditor

independence is measured through the value of the net equipment balance signed-off by the

auditor. The higher the net equipment balance signed-off by the auditor indicates the more likely the

auditor will compromise independence.

This study contributes to existing auditing literature in several ways. First, this study examines the

impact of explicit client intimidation on auditor independence in an audit conflict situation. Second,

this study provides empirical evidence of a pressure model that was developed by DeZoort and Lord

(1997) in two respects, by examining:

1. The impact of auditor’s perceived pressure in the presence of client intimidation on auditor

independence,

2. The moderating role of auditor’s multidimensional professional commitment on the relation

between auditor’s perceived pressure and auditor independence in the presence of client

intimidation.

Overall, the study contributes to our understanding of how explicit client intimidation may

deteriorate auditor independence and affect auditor’s perceived pressure. It also contributes to our

understanding about the moderating role of each auditor’s professional commitment on auditor

independence.

5

THEORETICAL FRAMEWORK AND HYPOTHESES DEVELOPMENT

Audit Conflict and Client Intimidation

Independence is the most valuable asset of the auditing profession and has been discussed by

practitioners and academics for a long time. However, until nowadays the definition of auditor

independence is still inconclusive. According to prior studies, there are several definitions of auditor

independence. For example, Knapp (1985) define independence as “an auditor’s ability to resist

client pressure.” McKinley, Pany, and Reckners (1985) define independence as “the auditors’ ability

to act with integrity and objectivity.” Bartlett (1993) defines independence as “an unbiased mental

attitude in making decision about audit work and financial reporting.” Additionally, Nouri and

Lombardi (2009) define independence as “freedom from the control of those whose records are

being reviewed”.

From the perspective of aforementioned definitions indicate that there are some challenges that

may affect auditor independence. One of these is an audit conflict situation that occurs in the

auditing assignment between an auditor and a client. Audit conflict between the auditor and the

client usually emerges when there is a disagreement between the auditors and the client over some

accounting issues, including the need to make adjustments to the financial statements, the

appropriate of client’s applied accounting principles, or the adequacy of financial statements

disclosure (Knapp, 1985). The audit conflict situation has urged the interest of both regulators and

researchers because it is potentially a serious threat to auditor independence (Knapp, 1985).

Moreover, an audit conflict situation that occurs in the auditing process should be resolved before

the auditor can provide an opinion on the financial statements.

Goldman and Barlev (1974) argue that in an audit conflict situation, a client has a strong incentive

and power to get more favorable audited financial statements. This incentive aligns with

shareholders’ interests: both, although based on different motives, want the audited financial

statements to provide a good impression on third party. The good impression would assure potential

investors to invest in the firm as well as creditors to grant the loans. In the presence of audit conflict,

Auditors are commonly in a weak position because of an asymmetrical power relationship between

the auditor and the client in which the client selects the auditors, determine scope of auditing, and

terminate or replace auditors. The client also provides the auditor with the facilities and information

needed to perform the audit work; even when the auditor is selected by audit committee, there are

no specific enforcement mechanisms ensure that the client does not become involved, directly or

indirectly, in selecting the auditor or determining the audit fee and the scope of the audit (Windsor,

6

2005; Baker, 2005). Consequently, the auditor tends to favor to the client’s position (Kadaous,

Kennedy, and Peecher, 2003; Moore et al., 2006).

Furthermore, besides the asymmetrical power relationship between the auditor and the client, the

client may also exert pressures on the auditor in order to assure favored results. Accordingly, prior

studies reveal that there are at least two pressures that faced by auditors and can deteriorate

auditor independence (Knapp, 1985; Gul, 1991; Tsui and Gul, 1996; Lord and DeZoort, 2001; Lin and

Fraser, 2008; Nasution and Östermark, 2012). The first is pressures within the auditing firm, named

social influence pressures, consisting of obedience pressure that exerted by managers or partners

and conformity pressure that exerted by peers. The second is pressures exerted by a client. Lee

(1995) stresses the public doubt regarding the ability of an auditor to resist client pressures to

misreport. In addition, Lord (1992) states that even though auditors face several forms of pressures

in the audit assignment, research into auditor decisions or judgments has seldom incorporated these

pressures into their research design.

Pressures from a client can be directly or indirectly, explicitly or implicitly exerted by the client, and

can also manifest into several forms (Lord, 1992). Accordingly, Knapp (1985) examine how certain

contextual factors will affect of the audited financial statements users’ perception on auditor

independence. The contextual factors are: the nature of conflict issues, the client’s financial

condition, the provision of client management accounting system (hereafter MAS), and the degree of

competition in the external audit market. The findings supports that the contextual factors in

auditor-client conflicts affect users’ perception on auditor independence.

In line with Knapp’s study, Gul (1988) examines bankers’ perception on contextual factors that will

affect auditor independence. The contextual factors consist of audit committee, client’s financial

condition, provision of MAS, level of competition in the external audit market, and audit-firm size.

Using experimental method, this study finds that MAS, level of competition, and audit-firm size are

perceived to affect auditor independence. Furthermore, extending his prior study, Gul (1991)

examines the effect of audit fee size, MAS, audit firm size, and competition on audit independence.

Subjects, forty-nine bankers, were asked to make a subjective judgment regarding auditor

independence in the case of materially unrecorded liabilities. The results support the hypotheses

that audit fee size, MAS, audit firm size, and competition affect bankers’ perception of auditor

independence. Both Knapp (1985) and Gul (1988, 1991) focus only to the perception of financial

statements users and not to auditors directly. Felix et al. (2005) argue that focusing to users of

7

audited financial statements rather than on auditors might be due of difficulty in creating realistic

pressures or intimidation treatments in an experimental setting.

However, some further studies have tried to improve Knapp and Gul Studies through focusing on

auditors and treating pressure in their research designs. Felix, Gramling, and Maletta (2005) study

the influence of client pressure on auditor independence in term of auditor’s decisions to rely on

internal audit. They measure client pressure through auditors’ assessment on how intensively their

clients encourage them to use internal audit work. A survey was conducted to collect the data. The

finding shows that auditors appear to be less concerned with internal audit quality and coordination

in making internal audit reliance decisions when they face more intensive client pressure.

Hatfield, Jackson, and Vandervelde (2011) investigate auditor independence in term of auditor’s

proposed audit adjustment in the presence of a client pressure. A client pressure was materialized

into two components: client importance and client opposition to adopt the adjustment. They believe

that these two components together will create a strong manipulated treatment of the client

pressure. Using 149 auditors’ responses, they find that client pressure significantly affects auditor

independence. It indicates that auditors who face client pressure will propose audit adjustment to a

lower amount than those who do not face the client pressure.

Besides asymmetrical power relationship between the auditor and the client and also the possible

pressures exerted by the client, auditor independence may be impaired through an incitement to

ensure and retain consecutive audit assignments from the client. Chang and Hwang (2003) show

retention motivation or incentive will affect auditor independence; at the same time, the auditor will

also consider the client’s business risks. In addition, Blay (2005) argues that the fear of losing the

client will let auditors to compromise their independence. Moreover, Goodwin and Trotman (1995)

show that auditors will compromise their independence when the risk of losing the client is high. And

indeed, their study reveals that when the risk of losing the client is high then it appears to dominate

the risk of litigation. This means that auditors will weigh the risk of losing the client more than the

risk of litigations that may arise from audit failures.

Taken together, the literature suggests that when audit conflict occurs between the client and the

auditor, commonly, the auditor is in a weak position, especially in the presence of client pressures.

This is because of an asymmetrical power relationship between them. It also shows that the risk of

losing the client or reward for retaining the client will induce auditor’s consideration to favor the

client’s position. Indeed, the risk of losing the client will dominate other risks that possibly exist.

8

Moreover, pressures from the client can be manifested into a variety of forms; one of them is

intimidation threat. Intimidation threat is one of independence threats in the auditor independence

frameworks (e.g. IFAC, 2012) as well. There are no studies that directly and explicitly examine the

influence of intimidation threat on auditor independence. Intimidation threat erupts when a member

of auditing team may be deterred from acting objectively and exercising professional skepticism by

threats, actual or perceived from directors, officers or employees of an audit client (IFAC, 2012).

Regarding intimidation threat, Bennett and Hatfield (2012) state that clients may use explicit or

implicit intimidation tactics on auditors. Their survey also reveals that auditors, especially staff level

auditors, often experience this condition. Cheung and Hay (2004) find that shareholders believe that

intimidation threat affects auditor independence. Astonishingly, according to Fearnley, Beattie, and

Richard (2005), intimidation threat is the threat that has the least prohibition and safeguards in the

auditor independence frameworks. In addition, a common form of intimidation threat is the threat of

replacement of an auditor (IFAC, 2012). The present study argues that when the auditor experience

an audit conflict situation that is accompanied by client intimidation to replace the auditor then the

auditor will compromise their independence in order to avoid of losing the client; regardless of any

contingency factors. The level of compromise differs when auditors only experience auditor conflict

without any client intimidation. In the present study, auditor independence is measured in a

monetary response, in term of the auditor signs-off on the net equipment account balance for the

equipment in question. The higher the net equipment balance signed-off by the auditor, the more

likely the auditor will compromise independence. Based on the argument above, the first hypothesis

is stated as follows:

H1

: Auditors in an audit conflict situation that is accompanied by client intimidation will sign-off

higher on the net equipment account balance for the equipment in question than those who

experience a similar situation but without client intimidation.

Perceived Pressure

DeZoort and Lord (1997) generate a general model of pressure in the accounting and auditing field.

The model focuses on professional pressures that can be applied to a specific accounting situation

and potentially tested in an experimental setting. DeZoort and Lord develop this model grounded on

a general pressure model in the organizational stress literature.

There are three important constructs in this model. The first is job pressures (x), defined as an

objective stimulus constructs referring to individual characteristics or a combination of

9

characteristics and events that impose on the perceptual and cognitive processes of individual. The

second is a stress response (y), defined as how auditors perceive individual pressures at a specific

point in time as well as a cumulative effects of pressure over time . The last is strain outcomes,

defined as the behavioral or attitudinal consequences related to pressures stimuli (x) and stress

response (y). In the behavioral consequences, pressures that are experienced by auditors may affect

their judgment and decision.

Based on this model, the present study expects that client intimidation in an audit conflict situation

will have an impact on auditor’s stress outcome, namely perceived pressure. Subsequently, the level

of auditor’s perceived pressure will affect auditor independence (i.e. auditors sign-off on the net

equipment account balance for the equipment in question). The higher pressure perceived by the

auditor thus the higher the auditor will sign-off on the net equipment balance. Hence, the next

hypotheses are constructed as follows:

H2

H

: Auditors in an audit conflict situation that is accompanied by client intimidation will perceive

higher pressure than those who experience a similar situation but without client intimidation.

3

: Auditors’ perceived pressure will positively relate to the net equipment balance for equipment

in question signed-off by auditor in the presence of client intimidation.

Professional Commitment

The pressures model also shows that some individual variables could moderate the relationship

between pressures and stress-outcomes. Thereby, it is possible that a similar pressure that is

experienced by two or more auditors can produce different stress outcomes because of differences

in individual characteristics. The present study incorporates auditor’s professional commitment as an

individual variable that will moderate the relationship between pressures and stress-outcomes.

Professional commitment has been a concept of interest for researchers and practitioners in

accounting for more than 20 years (Hall, Smith, and Langfield-Smith, 2005). Professional commitment

refers to the attachment of individuals in the profession or, in other words, to the strength of an

individual’s identification with a profession. Individuals with high professional commitment are

characterized as having a strong belief in and acceptance of professional goals, a willingness to use

their efforts to advance the profession, and having a strong desire to maintain membership in the

profession. Prior studies showed that the strength of professional commitment has consequences on

performance improvement, turnover intentions, the level of satisfaction on the profession, and

ethical judgment (e.g. Jeffrey, Weatherholt, and Lo, 1996; Lord and DeZoort, 2001; and Hall et al.,

10

2005). However, thus far, prior studies usually used a single-dimensional construct to measure

professional commitment, namely affective professional commitment. Focusing on a single

dimension of professional commitment only provides a partial understanding of the auditors’

profession (Hall et al.,

2005). By examining professional commitment in multiple dimensions, a

complete understanding of individual commitment to the profession will be provided (Meyer, Allen,

and Smith, 1993).

Meyer et al. (1993) develop a multidimensional construct of professional commitment and it was

adapted to the accounting field by Hall et al. (2005). Hall et al. (2005) argue that because

multidimensional professional commitment has found support in every profession and occupation;

hence, the unique characteristics of the public accounting profession will have a significant impact on

all dimensions of professional commitment as well. However, to date, there are no empirical studies

that investigating the role of all dimension of professional commitment on auditor independence.

The multidimensional of professional commitment consists of affective professional commitment

(APC), continuance professional commitment (CPC), and normative professional commitment (NPC)

dimensions. APC is the extent to which individuals "want to stay" in the profession because they

identify themselves with the goals of the profession and want to help the profession to achieve those

goals. NPC refers to the extent to which individuals feel they "ought to stay" in the profession as an

obligation. Finally, CPC is the extent to which individuals feel they "have to stay" in the profession

because of the accumulated investment that they have made (e.g. in study effort, training, etc.) and

also because of the lack of other alternatives. According to Hall et al. (2005), auditors who have high

levels of APC and NPC may feel a moral obligation to engage in behaviors that are beneficial to the

profession in order to maintain the profession reputation. On the other hand, auditors who have

high levels of CPC tend to be pragmatic and engage in behaviors that are beneficial to themselves.

The present study predicts that auditor’s professional commitment dimensions will moderate the

relationship between auditor’s perceived pressure and auditor independence (i.e. auditors sign-off

on the net equipment balance for the equipment in question). High levels of APC and NPC will

moderate to enhance auditor independence in case of audit conflict accompanied by client

intimidation. Meanwhile, a high level of CPC will moderate to induce the auditor to compromise his

or her independence. Therefore, the hypothesis 4, 5, and 6 can be constructed as follow:

H4: The levels of auditor’s APC moderate the relationship between auditor’s perceived pressure

and auditor signs-off on the net equipment account balance for the equipment in question.

11

H5: The levels of auditor’s NPC moderate the relationship between auditor’s perceived pressure

and auditor signs-off on the net equipment account balance for the equipment in question.

H6

: The levels of auditor’s CPC moderate the relationship between auditor’s perceived pressure

and auditor signs-off on the net equipment account balance for the equipment in question.

METHOD

Subjects

Subjects were practicing auditors from national public accounting firms in Indonesia. Contact persons

in the public accounting firms were approached and asked for their willingness to administer the

research instrument within their firm. After that, a research instrument was handed in to the contact

persons. They then distributed the instrument to the subjects of their choosing. Two weeks after

that, the contact persons collected the completed instruments.

We received responses from our contact persons for 126 auditors - providing a response rate of

approximately 60 percent, of which 119 (88 responses under audit conflict that is accompanied by

client intimidation and 31 without client intimidation) had the data necessary for testing our

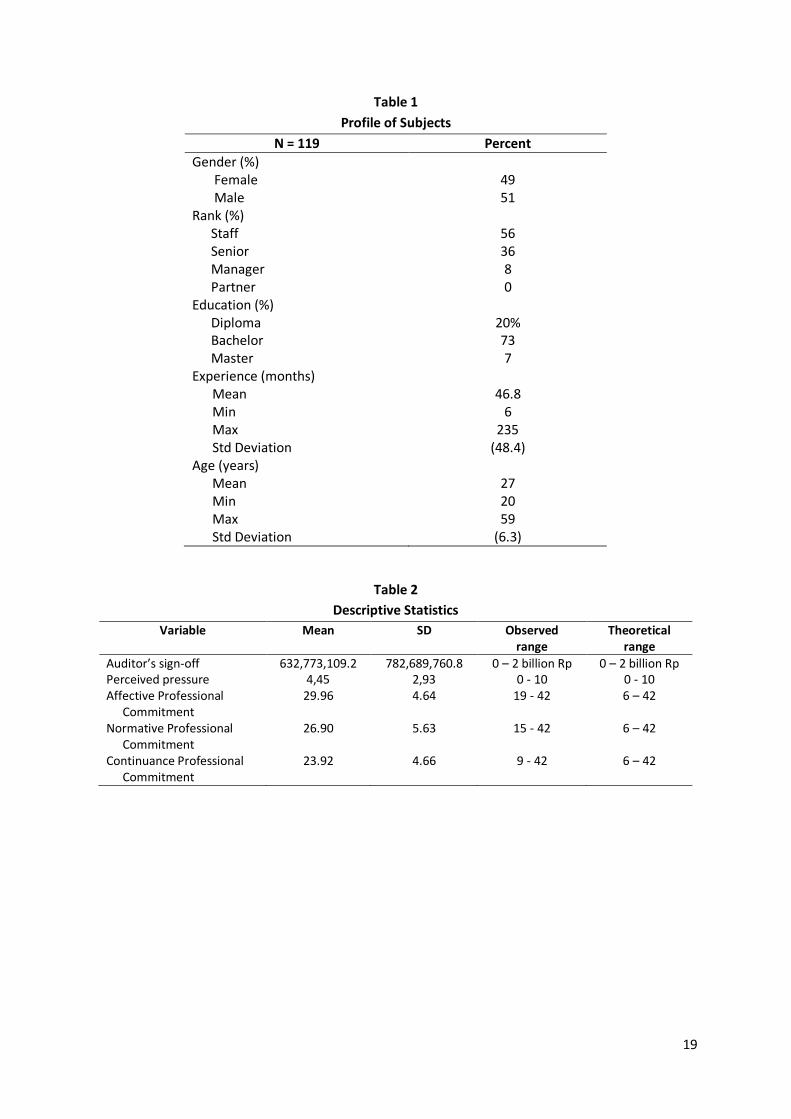

hypotheses. A demographic profile of subjects is provided in Table 1. The representative subjects

were staff and senior auditors with approximately 46.8 months experience on the average. Fifty-one

percent of the subjects were male and forty-nine percent were female; hence indicating a balanced

gender in the data. Seventy-three percent of the subjects had bachelor and 20 percent had diploma

education. The average age of the subjects was 27 years old.

Insert Table 1 about here

Procedure

Data used to test the hypotheses were collected using a research case instrument in which subjects

responded to one of two manipulated treatments, i.e. audit conflict accompanied by client

intimidation and that without client intimidation. The case was randomly assigned to the subjects.

The research instrument consists of four parts. In the beginning, a short introductory letter is

provided which introduced the researchers and assures subjects of their anonymity and right to

refuse to participate without any consequences. Next, subjects are asked to read the assigned case

regarding a hypothetical public accounting firm that was auditing a hypothetical firm. In the case

description, an audit conflict is included, as explained below. After reading the case, subjects are

asked to decide how much they will sign-off on the net equipment account balance for the

12

equipment in question based on information in the case. The second part relates to subjects’

perceived pressure. The third part relates to a multidimensional professional commitment. The

instrument ends with questions regarding subjects’ demographic data.

An auditor-client conflict case is applied as a research instrument.

Case

The case was adapted from Lord

and DeZoort (2001); however, the case has been adjusted and rephrased in order to make it fit-in

with the purpose of this study. In the case, subjects were asked

to hypothesize themselves as the

responsible auditor, whose the team has been assigned to a new client. In the auditing process, the

subject cannot verify the existence and valuation of 2.5 billion Rupiah of equipment (approximately

equal to 2.5 million USD). Based on this finding, the subject proposes the client’s CFO to write-off the

equipment. In the audit conflict situation that is accompanied by client intimidation (treatment A),

the client’s CFO strongly disagrees with the subject’s proposal. The CFO also attacks the competence

of the subject and the subject’s staff and threatens to replace the subject’s audit firm as the client

auditor. The CFO insists that the equipment is in the plant but cannot be separately identified. The

CFO also suggests keeping the equipment as recorded and begins depreciating the equipment from

2011 to 2015 using the straight line method. On the other hand, in the audit conflict situation

without client intimidation (treatment B), the client’s CFO only disagrees with the subject’s proposal.

The CFO said that the equipment is in the plant but cannot be separately identified. The CFO suggests

keeping the equipment as recorded and begins depreciating the equipment from this year using the

straight line method.

The case was reviewed by audit partners as well as pilot tested in the study by Lord and DeZoort

(2001). We applied similar procedures to revalidate it. First, after having been adjusted and

rephrased, the case was assessed by two auditor partners. In doing so, the realism of the case is

guaranteed. The partners suggested that the case is realistic enough. Second, the case was pilot

tested by ten auditors, in order to assess the instrument clarity. Some minor adjustments were made

based on the pilot test.

Dependent variable

Auditor independence is the dependent variable. Prior studies are usually asked the participants to

respond in the probability or likelihood estimation forms. Borrowing Solomon’s argument (1994),

using these response forms will produce a mixed response variable and it is not clear what reliably

can be discerned from such measures. The present study measures auditor independence through

subjects sign-off on the net equipment account balance for the equipment in question. The subjects

13

are asked to determine the value of net equipment account balance that they will sign-off within the

range from 0 to 2 million Rupiah. The higher the net equipment balance signed-off by the subjects

the more likely the subjects compromise independence.

Independent variables

We have both manipulated and measured independent variables. Our manipulated variable is client

intimidation that manipulated using a case. The case consists of two types of manipulated

treatments; the first is manipulated into audit conflict accompanied by client intimidation to the

auditor and the second is manipulated into audit conflict but without client intimidation.

The measured independent variables are perceived pressure and professional commitment. The

perceived pressure is measured by asking the subjects to indicate the extent to which they perceive

pressure from the client in the case. The eleven-point Likert scales anchored by 0 (does not perceive

pressure at all) and 10 (fully perceives pressure) are utilized.

The professional commitment is measured using a multidimensional instrument developed by Meyer

et al. (1993)

and adapted for the accounting profession by Hall et al. (2005). The instrument

separated among APC, CPC, and NPC dimensions in which each dimension is measured by six

question items. Subjects are asked to indicate the extent to which they disagree or agree with the

presented statements. For each item, seven-point Likert scales anchored by 1 (strongly disagree) to 7

(strongly agree) are utilized. Prior studies show that multidimensional of professional commitment

has good validity and reliability (Meyer et al., 1993; Smith and Hall, 2008; Somers, 2009). To test the

instrument’s validity this study correlated each item question score with the total score in each

dimension. The results show that each item question score is significantly correlated with the total

score. The score ranges from 0.681 to 0.774 for APC, 0.771 to 0.847 for NPC, and from 0.518 to 0.772

for CPC. Moreover, all correlations are statistically significant (ρ < 0.01). The alpha coefficients of

APC, NPC, and CPC are 0.807, 0.889, and 0.755, respectively. For hypotheses testing purpose, each

dimension of professional commitment is measured through single index by averaging the item

scores. Additionally, the subjects were asked whether they have had experience facing client

intimidation in the auditing assignments. The result showed that 48% of subjects responded that

they have had the experience and 52% have not.

14

RESULTS

Manipulation check and Descriptive Statistics

To test the effectiveness of

manipulated-treatment, we compare subjects’ perceived pressure both

the groups with and without client intimidation. Subjects were asked to respond how far they

perceive pressure when facing audit conflict based-on the assigned case. An eleven-point Likert-type

scale is used as a response scale, ranging from not perceiving any pressure at all (0) to fully

perceiving pressure (10). On average, the subjects under client intimidation perceive higher pressure

(4.77) than the others (3.52). The results indicate that the manipulated treatment was effective.

Second, subjects were asked to respond whether the case is realistic enough or not. A seven point

Likert-type scale is used as a response scale from completely realistic (1) to completely unrealistic (7).

In average, the subjects suggest that the case was realistic enough, with mean value 2.

Analysis of variance (ANOVA) and regression analyses are used to test whether demographic

variables have possible effects on subject responses. ANOVA analysis shows that neither gender,

rank, nor education affected subject responses. Regression analysis shows neither experience nor

age affected subject responses. Hence, demographic variables are excluded from further analysis.

The dependent variable is auditor independence, proxied by the subjects sign-off on the net balance

of the equipment in question. The higher the net equipment balance signed-off by the subjects, the

more likely the subjects compromise independence. The independent variables are manipulated

treatments (i.e. audit conflict with or without client intimidation), perceived pressure and

professional commitment (consisted of APC, NPC, and CPC). Table 2 presents the descriptive

statistics for both the dependent and independent variables.

Insert Table 2 about here

Tests of Hypotheses

The main focus in this study is to test whether auditors will compromise their independence when

facing the audit conflict situation that is accompanied by client intimidation. The H1 predicts that

auditors under client intimidation will sign-off higher on the net equipment account balance for the

equipment in question than those who are in similar situation but without client intimidation. The

higher the net equipment balance signed-off by the auditors, the more likely the auditors

compromise independence. The manipulated independent variable is divided into two treatments:

the presence and absence of client intimidation in the audit conflict situation. The mean responses of

15

the net equipment balance signed-off by the subjects under the audit conflict with and without the

client intimidation are 726,704,545.5 and 366,129,032.2 Rupiah, respectively. To test the H1, ANOVA

analysis is used and the results show that the manipulated variable is difference and statistically

significant (F = 5.032; p < 0.05). The result indicates that auditors under audit conflict that is

accompanied by client intimidation will compromise their independence compared to those who

experience the similar situation but without client intimidation. Thereby H1

is supported.

H2 predicts that auditors under audit conflict that is accompanied by client intimidation will perceive

a higher pressure than will those who face similar conflict but without client intimidation. The mean

values of perceived pressure of auditors in audit conflict with and without client intimidation are

4.77 and 3.52 on the eleven-point scale, respectively. To test this hypothesis, ANOVA is used and the

result showed that these two means are significantly different (F = 4.329; p < 0.05); hence H2

is

supported.

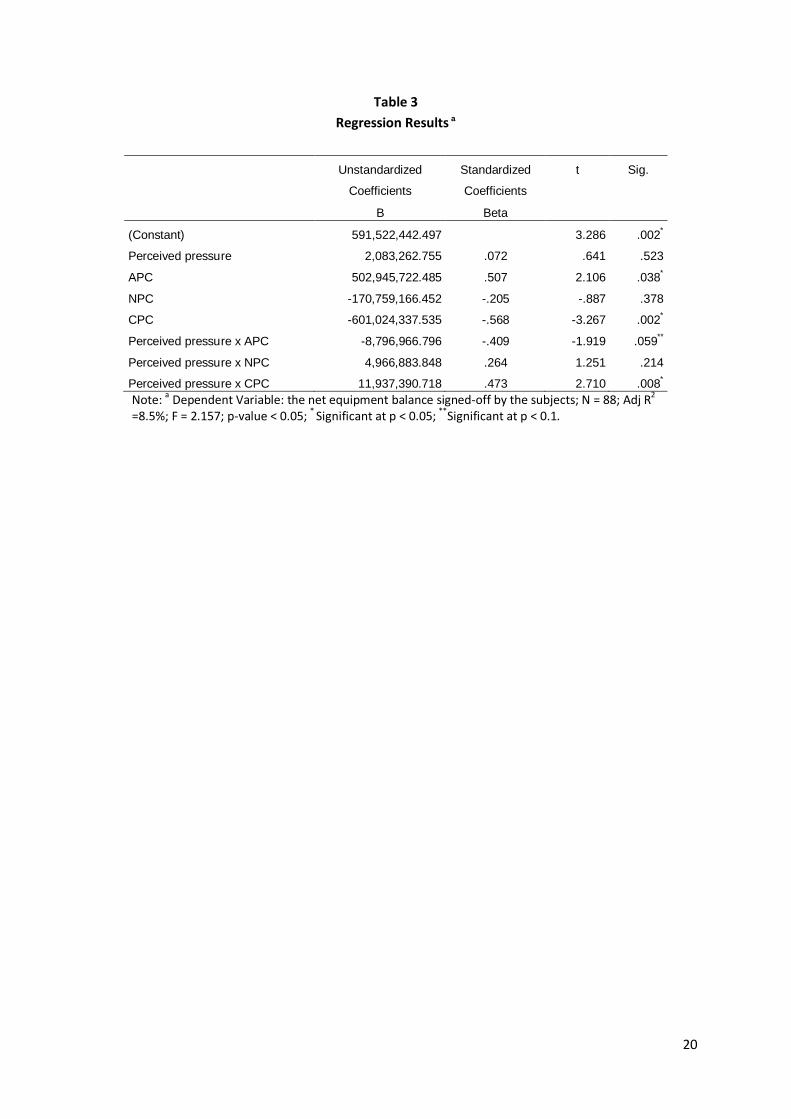

H3 to H6 relate to the impact of auditors’ perceived pressure on auditor independence and the

moderating role of multidimensional professional commitment on that relationship. To test such

hypotheses, including the interaction component, prior studies have usually utilized ANOVA analysis

using the median value of non-categorical variables to create a categorical proxy. The median

provides a cut-off point for dividing the data into two subgroups (e.g. high and low levels). However,

according to West, Aiken, and Krull (1996), this approach tends to reduce statistical power and yield

vague results. Therefore, a regression approach that is common in management accounting

literature (e.g. Dunk, 1991; Lau and Tan, 1998; Tsui, 2001; and Fellix, Gramling, and Maletta, 2005) is

used. To facilitate interpretation, in accordance to the suggestions of Jaccard and Turissi (2003) and

Aiken and West’s (1991), the data of multidimensional professional commitment is mean centered.

Mean centered reduces the multicollinearity between main effects and the interaction

𝑌𝑌 = 𝛽𝛽0 + 𝛽𝛽1𝑋𝑋1 + 𝛽𝛽2𝑋𝑋2 + 𝛽𝛽3𝑋𝑋3 + 𝛽𝛽4𝑋𝑋4 + 𝛽𝛽4𝑋𝑋1𝑋𝑋2 + 𝛽𝛽5𝑋𝑋1𝑋𝑋3 + 𝛽𝛽6𝑋𝑋1𝑋𝑋4

terms. The

regression model is run only for the data of the group under client intimidation. The regression

model is stated as follows:

where:

Y = the net equipment balance signed by the subjects;

X1 = perceived pressure;

X2 = affective professional commitment;

X3 = normative professional commitment;

16

X4

= continuance professional commitment.

Table 3 presents the regression results of the regression model.

Insert Table 3 about here

H3 predicts that the pressure perceived by the subjects is positively related to the net equipment

balance signed by them. Table 3 shows that the regression coefficient of perceived pressure (t =

0.41; p = 0.523) has a positive sign as predicted; however, it is not statistically significant. Hence, we

find no support for H3.

Finally, to consider H4 to H6, this study investigates whether the dimensions of professional

commitment moderate the forms of relationship between auditors’ perceived pressure and

auditors’ willingness to sign-off on the net equipment balance. As depicted in Table 3, the regression

results show that there are marginally significant interactions between auditor’s APC and perceived

pressure (t = -1.919; p-value < 0.1) and significant interaction between auditors’ CPC and auditor’s

perceived pressure (t = 2.710; p-value < 0.05). The interaction between auditor’s NPC and perceived

pressure are not statistically significant, however. Hence, we found support for H4 and H6, but not

for H5

.

To assist the interpretation of the moderation results, this study plots the high and low levels of

auditors’ APC and CPC respectively on the relationship between auditors’ perceived pressure and

auditors’ willingness to sign-off the net balance (figures 1 and 2). As showed in Figure 1, the

relationship between auditors’ perceived pressure and auditors’ willingness to sign-off on the net

balance is more negative when auditors’ APC is high and positive when auditors’ APC is low. On the

contrary, Figure 2 shows that there is a positive relationship between auditors’ perceived pressure

and auditors’ willingness to sign-off on the net equipment balance when auditors’ CPC is high.

Meanwhile, when auditor’s CPC is low, there is a negative relationship between auditor’s perceived

pressure and auditor’s willingness to sign-off on the net equipment balance.

Figure 1 about here

Figure 2 about here

17

CONCLUSIONS

The present study provides evidence on how auditors will compromise their independence in the

audit conflict that is accompanied by client intimidation. Client intimidation in this research is

materialized into a threat by the client to replace an auditor if the auditor does not adopt client’s

position in the questioned equipment. Moreover, auditor independence is proxied by the net

equipment balance signed-off by the auditors for the equipment in question. Specifically, this study

found that auditors will compromise their independence when the audit conflict is accompanied by

client intimidation. The finding indicates that an auditor has a weak bargaining position with a client,

especially in an audit conflict situation that is accompanied by client intimidation. It might also

indicate that motivation to retain the client is very important for auditors and the risk of losing the

client would deteriorate auditor independence, irrespective of any contingent factors.

The finding raises issues about mechanisms that can avoid an auditor from impairing his or her

independence caused by the risk of losing a client. One possible mechanism that can be considered

is a mandatory retention regime as discussed in the few accounting literature (Dopuch, King, and

Schwartz, 2001; and Comunale and Sexton, 2005). The mandatory retention requires a client to

retain an auditor at a specified number of years. This mechanism can possibly protect an auditor

from risk of losing the client and thereby avoiding the auditor from intimidation induced by the

client’s threat to replace the auditor. However, the possible negative side effects of this mechanism

should be taken into account before implementing it as well. Further study should address this issue

and combine it with the client intimidation issue.

Regarding auditors’ perceived pressure, this study finds that auditors under audit conflict that is

accompanied by client intimidation will perceive more pressure than those who under similar

conflict but without client intimidation. However, the relationship between the levels of auditors’

perceived pressure on auditor independence - though the regression coefficient shows a positive

sign - is not statistically significant. This study also finds that the relationship between auditors’

perceived pressure and the net equipment balance signed-off by the auditors is moderated by the

auditors’ APC and CPC levels. As predicted by the theory, the higher the levels of APC the more likely

auditors will engage in behaviors that are beneficial to the profession. Otherwise, the higher the

levels of CPC the more likely auditors tend to be pragmatic and engage in behaviors that are

beneficial to themselves. These findings are consistent with the predictions that the relationship

between auditors’ perceived pressure and the net equipment balance signed by the auditors is more

negative when the level of auditors’ APC is high and more positive when the levels of auditors’ APC

18

is low. Correspondingly, the relationship between auditors’ perceived pressure and the net

equipment balance signed by the auditors is more positive when the level of auditors’ CPC is high

and more negative when the level of auditors’ CPC is low.

The interpretations of these results are subject to several limitations; accordingly, the results should

be interpreted cautiously. First, our research instrument was completed by the subjects at their

convenient time. On the one hand, this may involve in some loss of control, but on the other hand, it

also stimulates the real conditions in which auditors commonly make decisions. Second, Bennet and

Hatfield (2012) stated that client management may use explicit or implicit intimidation tactics to

auditors in order to achieve their goal. This study focuses only to the explicit intimidation tactic,

materializing to a threat by the client to replace the auditor. It is possible that auditors will respond

to explicit and implicit intimidation differently. Third, subjects in this paper were Indonesian auditors

that work in national audit firms. Factors specific to these subjects may limit the extent to which the

results could be generalized to auditors from other countries and international audit firms.

19

Table 1 Profile of Subjects

N = 119 Percent Gender (%) Female Male

49 51

Rank (%) Staff Senior Manager Partner

56 36 8 0

Education (%) Diploma Bachelor Master

20% 73 7

Experience (months) Mean Min Max Std Deviation

46.8

6 235

(48.4) Age (years) Mean Min Max Std Deviation

27 20 59

(6.3)

Table 2 Descriptive Statistics

Variable Mean SD Observed range

Theoretical range

Auditor’s sign-off 632,773,109.2 782,689,760.8 0 – 2 billion Rp 0 – 2 billion Rp Perceived pressure 4,45 2,93 0 - 10 0 - 10 Affective Professional

Commitment 29.96 4.64 19 - 42 6 – 42

Normative Professional Commitment

26.90 5.63 15 - 42 6 – 42

Continuance Professional Commitment

23.92 4.66 9 - 42 6 – 42

20

Table 3 Regression Results

a

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.

B Beta

(Constant) 591,522,442.497 3.286 .002*

Perceived pressure 2,083,262.755 .072 .641 .523

APC 502,945,722.485 .507 2.106 .038

NPC

*

-170,759,166.452 -.205 -.887 .378

CPC -601,024,337.535 -.568 -3.267 .002

Perceived pressure x APC

*

-8,796,966.796 -.409 -1.919 .059

Perceived pressure x NPC

**

4,966,883.848 .264 1.251 .214

Perceived pressure x CPC 11,937,390.718 .473 2.710 .008* Note: a Dependent Variable: the net equipment balance signed-off by the subjects; N = 88; Adj R2 =8.5%; F = 2.157; p-value < 0.05; * Significant at p < 0.05; **

Significant at p < 0.1.

21

Figure 1 Interaction between Auditors’ Perceived Pressure

and Auditor’s APC

Figure 2 Interaction between Auditors’ Perceived Pressure

and Auditor’s CPC

22

REFERENCES

Aiken, L.S., and West, S.G. (1991) Multiple regression: Testing and interpreting interactions, Sage

Publication, London.

Baker, C.R. (2005) ‘The varying concept of auditors independence: Shifting with the prevailing

environment’, The CPA Journal, August, pp. 23-28.

Bartlett, R. W. (1991) ‘A Heretical challenge to incantations of audit independence’, Accounting

Horizon, Vol. 5 No. 1, pp. 11-16.

Barlett, R. W. (1993) ‘A scale of perceived independence: New evidence on an old concept’,

Accounting, Auditing and Accountability Journal, Vol. 6 No. 2, pp. 52-67.

Bennett, G.B. and Hatfield, R.C. (2012) ‘The Effect of the Social Mismatch between Staff Auditors and

Client Management on the

Collection of Audit Evidence’, Accounting Review In-Press, Available

at SSRN: http://ssrn.com/abstract=2137183 (accessed 12 September 2012).

Blay, A.D. (2005) ‘Independence threats, litigation risk, and the auditor’s decision process’,

Contemporary Accounting Research, Vol. 22 Iss. 4, pp. 759-89.

Chang, C.J., and Hwang, N.R. (2003) ‘The impact of retention incentives and client business risks on

auditors’ decision involving aggressive reporting practice’, Auditing: A Journal of Practice &

Theory, Vol. 22 Iss. 2, pp. 207-218.

Cheung, J, and Hay, D. (2004) ‘Auditor Independence: The voice of shareholders’, University Auckland

Business Review, Vol. 6 Iss. 2, pp. 67-75.

Comunale, C.L., and Sexton, T.R. (2005) ‘Mandatory auditor rotation and retention: impact on market

share’, Managerial Auditing Journal, Vol. 20 No. 3, pp. 235 – 248.

DeZoort, T. and Lord, A. (1997) ‘A Review and Synthesis of Pressure Effects Research in Accounting’,

Journal of Accounting Literature, Vol. 16, pp. 28-85.

23

Dopuch, N., King, R.R., and Schwartz, R. (2001) ‘An experimental investigation of retention and

rotation requirements’, Journal of Accounting Research Vol. 39 No. 1, pp. 93 – 117.

Dunk, A.S. (1991) ‘The effect of budget emphasis and information asymmetry on the relation

between budgetary participation and budget slack’, The Accounting Review, Vol. 68 No. 2, pp.

400-410.

Fearnley, S., Beattie V.A., Richard, B. (2005) ‘Auditor independence and audit risk: A

reconceptualization’, Journal of International Accounting Research, Vol. 4 Iss. 1, pp. 39-71.

Felix, W.L., Gramling, A.A., and Maletta, M.M. (2005) ‘The influence of nonaudit service revenues and

client pressure on external auditors’ decision to rely on internal audit’, Contemporary

Accounting Research, Vol. 22 No. 1, pp. 31-53.

Gul, F.A. (1988) ‘Bankers’ perception of factors affecting auditor independence’, Accounting, Auditing

& Accountability Journal, Vol. 2 Iss. 3, pp. 40-51.

Gul, F.A. (1991) ‘Size of audit fees and perception of auditors’ ability to resist management pressure

in audit conflict situations’, ABACUS, Vol. 27 Iss. 2, pp. 162-172.

Goodwin, J. and Trotman K., (1995) ‘Auditor Judgments of Revalued Assets - The Effect of Conflicting

Risks’, Accounting and Business Research, Vol 25, No. 2, pp. 177-185

Goldman, A, and Barlev, B. (1974) ‘The auditor-firm conflict of interests: Its implication for

independence’, The Accounting Review, Vol. 49 Iss. 4, p.707-718.

Hatfield, R.C., Jackson, S. B., and Vandervelde, S. D. (2011) ‘The effects of prior auditor involvement

and client pressure on proposed audit adjustments’, Behavioral Research in Accounting, Vol.

23 No. 2, pp. 117-130.

Hall, M. and Smith, D., and Langfield-Smith, K. (2005) ‘Accountants commitment to their profession:

Multiple dimensions of professional commitment and opportunities for future research’,

Behavioral Research in Accounting, Vol. 17 No. 1, p. 89-109.

24

International Federation of Accountants (2012) The 2012

Handbook of the Code of Ethics for

Professional Accountants, IFAC, New York.

Jaccard, J. and Turrisi, R. (2003) Interaction effects in multiple regression (2nd

ed.), Sage University

Papers Series on Quantitative Applications in Social Science, No. 07-072, Thousand Oaks, CA:

Sage.

Jeffrey, C., Weatherholt, N., and Lo, S. (1996) ‘Ethical Development, Professional Commitment and

Rule Observance Attitudes: A Study of Auditors in Taiwan’, International Journal of Accounting,

Vol. 31 No. 3, pp. 365-379.

Lau, C.M., and Tan, J.J. (1998) ‘The impact of budget emphasis, participation, and task difficulty on

managerial performance: a cross-cultural study of the financial services sector’, Management

Accounting Research, Vol. 9 No. 2, pp. 163-183.

Layne, N., and Ridley, K. (2011) ‘Exclusive: Olympus removed auditor after accounting’, Reuters, 4

November, available at: http://www.reuters.com/article/2011/11/04/us-olympus-auditor-

idUSTRE7A32VR20111104 (accessed 26 September 2012).

Lee, T. (1995) ‘The professionalization of accountancy’, Accounting, Auditing & Accountability

Journal, Vol. 8 No. 4, pp. 48-70.

Lin, K.Z., and Fraser, I.A. (2008) ‘Auditors' ability to resist client pressure and culture: perceptions in

China and the United Kingdom’, Journal of International Financial Management & Accounting,

Vol. 19 No. 2, pp. 161-183.

Lord, A. (1992) ‘Pressure: A methodological consideration for behavioural research in accounting’,

Auditing: A Journal of Practice & Theory, Vol. 11 No. 2, pp. 89-108.

Lord, A. & DeZoort, T. (2001) ‘The impact of commitment and moral reasoning on auditors’

responses to social influence pressure’, Accounting, Organizations and Society (April), pp. 215-

236.

Kadous

, K., Kennedy, S.J., and Peecher, M.E. (2003) ‘The effect of quality assessment and directional

goal commitment on auditors’ acceptance of client-preferred accounting methods’, The

Accounting Review, Vol. 78 Iss. 3, pp. 759-778.

25

Knapp, M.C. (1985) ‘Audit conflict: An empirical study of the perceived ability of auditors to resist

management pressure’, The Accounting Review, Vol. 60 Iss. 2, pp. 202-211.

McKinley, S., Pany, K. and Reckners, P.M. (1985) ‘An examination of the influence of CPA firm type,

size, and MAS provision on loan officer decision and perceptions’, Journal of Accounting

Research, Vol. 23 No. 2, pp. 887-896.

Meyer, J.P., Allen, N.J., and C.A. Smith. (1993) ‘Commitment to organization and occupations:

Extensions and test of a three-component conceptualization’, Journal of Applied Psychology,

Vol. 78 Iss. 4, pp. 538-551.

Moore, D.A., Tetlock, P.E., Tanlu, L., and Bazerman, M.H. (2006) ‘Conflict of interest and the case of

auditor independence: Moral seduction and strategic issue cycling’, Academy of Management

Review, Vol. 31 No. 1, pp. 10-29.

Nasution, D., and Östermark, R. (2012) ‘The impact of social pressures, locus of control, and

professional commitment on auditors’ judgment: Indonesian evidence’, Asian Review of

Accounting, Vol. 20 Iss: 2, pp. 163 – 178.

Nouri, H., and Lombardi, D. (2009) ‘Auditors’ Independence: An Analysis of the Montgomery’s

Auditing Textbooks in the 20th Century’, Accounting Historian Journal, Vol. 36 No. 1, pp. 81-

112

.

Solomon, I. (1994) ‘Commentary on: An investigation of obedience pressure effects on auditors’

judgment’, Behavioral Accounting Research, Vol. 6 (Supplement), pp. 31-34.

Somers, M.J. (2009) ‘The combined influence of affective, continuance, and normative commitment

on employee withdrawal’, Journal of Vocational Behavior, Vol. 74 No. 1, pp. 75-81.

Tsui, J.S., and Gul, F.A. (1996) ‘Auditors’ behavior in an audit conflict situation: A research note on the

role of locus of control and ethical reasoning’, Accounting, Organizations and Society, Vol. 21,

No. 1, p. 41-51.

26

Tsui, J.S. (2001) ‘The impact of culture on the relationship between budgetary participation,

management accounting systems, and managerial performance: An analysis of Chinese and

Western managers’, International Journal of Accounting, Vol. 36 No. 2, pp. 125-146.

Windsor, C.A. (2005). Management Economic Bargaining Power and Auditors’ Objectivity in Audit

and Ethics, eds Campbell, T. and Houghton, K., ANU E Press, Australian National University,

Canberra.

Ye, P., Carson E., and Roger S. (2011) ‘Threats to auditor independence: The impact of relationship

and economic bonds’, Auditing: A Journal of Practice & Theory, Vol. 30 Iss. 1, pp.121-48.