Embed Size (px)

Citation preview

David E. Dismukes, Ph.D.

Center for Energy Studies

Louisiana State University

The Impact of Changing Natural Gas Prices on

Renewables and Energy Efficiency

NASUCA Gas Committee Conference Call/Webinar

June 12, 2012

Center for Energy Studies

Energy-Related

Carbon Dioxide

81.2%

Summary and Take Away

2

• New natural gas supply availability is having considerable

impacts on all energy markets today and on longer term,

forward-looking basis.

• Given the prevalence of natural gas at the margin, this impacts

not just retail gas usage, but also power, renewables and

environmental valuations.

• Lower gas commodity will also drive down gas as a share of total

bill and start to move base rate/commodity cost relationships to

longer-run averages.

• If avoided costs (future looking costs) are not re-calibrated to

reflect these market changes, it could result in higher-than-cost

effective energy efficiency and renewable energy being adopted.

Center for Energy Studies

© LSU Center for Energy Studies

Marginal cost – the change in total cost resulting from

an extremely small change in output. Typically

thought of in the short run, although long run marginal

costs can be important for planning purposes.

Avoided costs – the real world estimate of long run

marginal costs where all factors of production (or

inputs such as capital/capacity and other variable

costs) are variable.

Important in long run resource planning evaluation as

well as evaluation of renewable energy resources and

energy efficiency measures.

3

© LSU Center for Energy Studies

Marginal Costs/Avoided Costs

Center for Energy Studies

Energy-Related

Carbon Dioxide

81.2%

Avoided Cost Estimation

4

Avoided cost estimates are often a function of:

1. Future energy costs

2. Future capacity costs

3. Future natural gas commodity costs (LDC)

4. Future environmental costs

5. Future renewable costs

6. Zero dispatch benefits (use/application

varies by state)

Center for Energy Studies

© LSU Center for Energy Studies

Center for Energy Studies

Natural Gas Prices

5 © LSU Center for Energy Studies

$/M

cf

Source: Energy Information Administration, U.S. Department of Energy.

Natural Gas Price Variability

Center for Energy Studies

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11

average for period

2000-2001 heating season

through 2008: $6.24 (standard deviation: $2.39)

since 2009: $4.11 (standard deviation: $0.70)

6 © LSU Center for Energy Studies

The 2001 to 2009 market trend of higher average prices coupled with high

volatility is reversing itself and post 2009 prices are significantly lower.

Average 1997

through 2000: $2.79 (standard deviation: $1.28)

Pe

rce

nt o

f To

tal (%

)

Source: Energy Information Administration, U.S. Department of Energy

Estimated Gas and Non-Gas Costs in U.S. Distribution Rates

Center for Energy Studies

0%

10%

20%

30%

40%

50%

60%

70%

80%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Fuel

Non-Fuel

7 © LSU Center for Energy Studies

The commodity share of total bills are closer to percentages observed in

the 1990s rather than the early 2000s.

Source: Energy Information Administration, U.S. Department of Energy

Domestic Shale Gas Basins and Plays

Center for Energy Studies

8 © LSU Center for Energy Studies

Unlike

conventional

resources,

shale plays

(natural gas,

liquids, and

crudes) are

located

almost

ubiquitously

throughout

the U.S. and

are the

primary

reason for

the decrease

in overall and

regional

natural gas

prices.

Annual Production, Unconventional Resources

Center for Energy Studies

9 © LSU Center for Energy Studies

Bcf/d MMBBl/d

Source: Advanced Resource Intl; presentation to Cheniere Board, March 2011; Cheniere Research

0

1

2

3

4

5

6

7

8

2010 2011E 2012E 2013E 2014E 2015E 2020E

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Includes Eagle Ford, W. Barnett, Bakken Shales;

Granite Wash, Piceance & Uinta Tight Sands

Liquids

Gas

Liquids production from shale plays > 3 million barrels per day by 2020

Associated natural gas > 7 Bcf/d of “costless” supply (or about 2.3 Bcf/d per

every 1.0 MMBbls/d of shale-based liquids production).

Dry

Na

tura

l G

as P

rove

d R

ese

rve

s (

Tcf)

Source: Energy Information Administration, U.S. Department of Energy

Natural Gas Proved Reserves and Production

Center for Energy Studies

-

5

10

15

20

25

30

0

50

100

150

200

250

300

350

1970 1975 1980 1985 1990 1995 2000 2005 2010

Reserves

Production

Ma

rke

ted P

rod

uctio

n (T

cf)

1

0 © LSU Center for Energy Studies

Current U.S. natural gas reserves are approaching record levels not seen

since 1970. Natural gas production is at levels that surpass historic peaks.

Imp

ort

s -

Bcf

Source: Energy Information Administration, U.S. Department of Energy

Natural Gas Imports

Center for Energy Studies P

erc

en

t of T

ota

l U.S

. Su

pp

ly - %

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

LNG Imports Pipeline Imports Imports as a Percent of Total Supply

11 © LSU Center for Energy Studies

Natural gas imports, once thought the be the supply remedy for meeting

future gas needs are falling to levels also not seen since the 1990s.

Re

se

rve

s -

Tcf

Source: Energy Information Administration, U.S. Department of Energy

Annual Energy Outlook, Natural Gas Reserves

Center for Energy Studies

200

220

240

260

280

300

320

2010 2015 2020 2025 2030 2035

12 © LSU Center for Energy Studies

Unconventional resources are not a “flash in the pan” and are anticipated to

continue to increase over the next two decades or more.

Basin Competition

Center for Energy Studies

Source: MIT Energy Initiative. 13 © LSU Center for Energy Studies

Natural Gas Uses

China

1,275 Tcf

Australia

396 Tcf

South

Africa

485 Tcf

Argentina

774 Tcf

Brazil

226 Tcf

Mexico

681 Tcf

Canada

388 Tcf

U.S.

862 Tcf

France

180 Tcf

Poland

187 Tcf

Algeria

231 Tcf

Libya

290 Tcf

Close to 6,000 TCF of shale gas opportunities around the world. Coupled with 9,000 Tcf

in conventional suggest a potentially solid resource base for many decades.

(20

10

$/M

MB

TU

)

Source: Energy Information Administration, U.S. Department of Energy

Choosing Most Current Natural Gas Price Forecasts: AEO-2007 to AEO-2012

Center for Energy Studies

0

2

4

6

8

10

12

14

16

1997 2002 2007 2012 2017 2022 2027 2032

Actual Henry Hub AEO-2007 AEO-2008 AEO-2009

AEO-2010 AEO-2011 AEO-2012

14 © LSU Center for Energy Studies

Shale availability has significant impact on future price outlook.

Anticipated price outlook in 2009.

Anticipated price outlook today.

Raymond James

(long-term forecast

of $4.00)

Pritchard

Capital

($4.00)

Raymond

James ($3.25)

AESC 2011 Price

($5.91 in 2015)

Varying Industry Natural Gas Forecasts

Center for Energy Studies

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

Merrill Lynch

(<$2.00)

Deutsche

Bank

($3.50)

Current

Henry Hub

Price1 Pritchard

Capital

($3.30)

Barclay

Capital ($3.05)

Tudor

Pickering

Holt

($3.25)

Pritchard Capital

($5.00 from 2015

onward)

Raymond James

($2.50)

Bank of

America

Merrill

Lynch

($3.30)

AESC 2011

Price ($4.91)

AESC 2011

Price ($5.10)

Note: 1 As of May 31, 2012.

Source: Foster Natural Gas/Oil Report. Barclays Capital analysts: producer expectations of “very weak" gas prices in 2012, yet gas production will still manage

to grow. March 9, 2012; Hargreaves, S. 2012. Heating homes with gas gets cheaper. CNNMoney.com. January 12, 2012; Holland, B. 2012. Pritchard cuts

2012 gas price forecast 25%. Electric Power Daily. January 19, 2012; and Natural Gas Week. Treadmill: little hope seen for corralling burgeoning gas supply.

February 13, 2012 .

2012 2013 2014 and

beyond

15 © LSU Center for Energy Studies

Center for Energy Studies

Natural Gas & Energy Costs

1

6 © LSU Center for Energy Studies

Choosing Most Current Natural Gas Price Forecasts

Center for Energy Studies

• 2011 Avoided Energy Supply

Costs (“AESC”)

– Conducted on behalf of

energy efficiency program

administrators in New

England.

• Assumes that EIA’s AEO 2011

is “too optimistic” regarding

shale gas production and

utilizes “more conservative”

numbers from AEO 2010.

17 © LSU Center for Energy Studies

Source: Avoided Energy Supply Cost, 2011 Report

Effect of Changing Realities on Forecasted Natural Gas Prices

Center for Energy Studies

18 © LSU Center for Energy Studies

$0

$2

$4

$6

$8

$10

$12

2011 2016 2021 2026 2031 2036

AEO 2010 AEO 2012

Original Natural Gas Price Forecast Updated Natural Gas Price Forecast

(20

11

$/M

MB

tu)

AESC uses “high cost” shale outlook (original fcst) and even update

of this shows a wide near-term difference. 2016-2020 prices under

“original forecast’ are as much as 75 percent above AEO baseline.

Source: Avoided Energy Supply Cost, 2011 Report

Changing Forecasted Natural Gas Prices Impact on Electric Price

Center for Energy Studies

19 © LSU Center for Energy Studies

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2012 2017 2022 2027 2032 2037

Original On-Peak Electric Price

Updated On-Peak Electric Price (using new Natural Gas Price Forecast)

(20

11

$/M

MB

tu)

Updated forecasts can have a considerable impact on the forecasted avoided

cost. Energy costs often account for a sizable share of overall avoided cost.

Center for Energy Studies

Capacity Prices

2

0 © LSU Center for Energy Studies

Energy-Related

Carbon Dioxide

81.2%

Estimation of Capacity Costs

21

• Future capacity costs are a function of needed capacity.

• The tighter the (capacity) market, the more likely capacity

prices will rise to incent the development of new

capacity.

• Can be incentives to understate capacity requirements

that would/could arise from (1) load growth (2) EPA-

induced retirements (3) below-expected renewable

capacity development.

• Natural gas price decreases drive down an already lower-

capital cost investment, with higher operating

efficiencies and lower emissions. This creates a large

cost differential between natural gas based generation

and all other generation technologies (renewables AND

other fossil/nuclear).

Center for Energy Studies

© LSU Center for Energy Studies

Source: U.S. Department of Energy, Energy Information Administration.

Levelized Cost of Generation

Center for Energy Studies

0 50 100 150 200 250 300 350 400

Hydro

Biomass (Direct)

Offshore Wind

Onshore Wind

Solar PV

Advanced Nuclear

Coal IGCC

Conventional Coal

Combined Cycle (Today's gas ($2.40))

Combined Cycle ($8 gas)

Combined Cycle ($5 gas)

22 © LSU Center for Energy Studies

Lower gas prices move the levelized cost (and capacity cost) of the

development of new, incremental capacity even lower.

U.S. Power Generation – Fuel Mix

Center for Energy Studies

23 © LSU Center for Energy Studies

Coal 51%

Nuclear 20%

Natural Gas 16%

Petroleum 3%

Other 1%

Coal 45%

Natural Gas 24%

Nuclear 19%

Other 1%

Petroleum 1%

Renewables 9% Renewables 10%

2000 2010

Source: Energy Information Administration, U.S. Department of Energy

Over 250,000 MWs of natural gas power generation capacity has been added

over the past decade at the expense of coal and nuclear. Gas will continue to

be the marginal technology for a variety of reasons.

Center for Energy Studies

Electric Industry Environmental Regulations Create Uncertainty for Coal

National Ambient Air Quality Standards (NAAQS) • Sets acceptable levels for six criteria pollutants (carbon monoxide, lead, nitrogen dioxide, particulate matter, ozone, sulfur

dioxide).

• A network of 4,000 State and Local Air Monitoring Stations is used to determine if geographic areas are meeting or

exceeding the NAAQS.

Transport Rule (now CSAPR) [proposed] • Issued to replace the Clean Air Interstate Rule (CAIR) and its predecessor the Clean Air Transport Rule (“CATR”). Requires

31 states (and D.C.) to improve air quality by reducing power plant emissions (SO2 and NOX) that contribute to ozone and

fine particulate pollution in other states (some annual, some on ozone season only).

• By 2014, the rule and other state and EPA actions would reduce power plant SO2 emissions by 80% over 2005 levels.

Power plant NOx emissions would drop by 58%.

Utility Maximum Achievable Control Technology (MACT) [to be proposed] • EPA must set emission limits for hazardous air pollutants. The rule is expected to replace the Clean Air Mercury Rule

(CAMR) and add standards for lead, arsenic, acid gases, dioxins and furans.

Coal Combustion Residuals (CCR) [proposed] • Would establish, for the first time under the Resource Conservation and Recovery Act (RCRA) requirements for the proper

disposal of coal ash generated by coal combustion at electric power plants.

Power Plant Cooling Water Intake Structures Rule • Section 316(b) of the Clean Water Act is intended to address environmental impacts from cooling water intake to and

discharge from power plant cooling systems. Requires that the location, design, construction and capacity of cooling water

intake structures reflect the best technology available for minimizing adverse environmental impact.

24

Center for Energy Studies

Summary of Retirement Studies Related to EPA Rules

Source: Synapse Energy Economics, Inc., “Public Policy Impacts on Transmission Planning, Prepared for Earthjustice”, December 10, 2010; and “Miller, P. A Primer on Pending

Environmental Regulations and their Potential Impacts on Electric System Reliability. Working Draft, JD Northeast States for Coordinated Air Use Management. January 24, 2011.

Study Retired Capacity Regulation Requirements

Scenario 1 - Transport Rule

Scenario 2 - Transport Rule, MACT

Scenario 3 - Transport Rule, MACT,

316(b) Cooling Water, Coal Ash

Scenario 1 - Transport Rule, MACT

Scenario 2 - Transport Rule, MACT,

CWA 316(b)

Transport Rule, MACT, 316(b) Cooling

Water, Coal Ash

Size and existing controls

Transport Rule, MACT

Transport Rule, MACT

Switch to lower sulfur coal, install emission controls, or retire

Transport Rule, MACT

Transport Rule, MACT

In-house model (NEEMS) optimizing costs of existing capacity

and costs of potential new capacity.

Regulated Units - 15-year present value of costs >

replacement power from a CC or CT. Merchant unit -

15-year present value of cost > revenues from energy

and capacity markets.

Cost of retrofitting coal plant compared to cost of new

gas CC

Levelized costs (@2008 CF) after retrofitting each unit for the

environmental regulations compared to the cost of a new gas-

fired unit.

MJ Bradley

(August 2010)30 to 40 GW

FGS + emissions on all coal fired units by 2015Bernstein

Research (October

2010)

51 GW

Brattle Group

(December 2010)

50 to 65 GW by

2020

Credit Suisse

(September 2010)60 GW

Charles River

Associates

(December 2010)

39 GW by 2015

80

Estimated GW of Retired Coal

NERC (October

2010)

47 to 76 GW by

2018 (total fossil fuel

capacity, including oil

and gas)

10

ICF/IEE (May

2010)

25 to 60 GW by

2015

20 30 40 50 60 70

25

Source: NERC 2011 Long-Term Reliability Assessment

Anticipated Planning Reserve Margins

Center for Energy Studies

26 © LSU Center for Energy Studies

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2011 2013 2015 2017 2019 2021

ERCOT

FRCC

MISO

MRO-MAPP

NPCC-NE

NPCC-NY

PJM

SERC-E

SERC-N

SERC-SE

SERC-W

SPP

An

ticip

ate

d R

ese

rve

Ma

rgin

(%

)

Most areas of the country are anticipated future reserve

margins blow those typically utilized for planning purposes.

Center for Energy Studies

Changes in Environmental and

Renewable Energy Costs

2

7 © LSU Center for Energy Studies

CO2 Emissions in RGGI States

Center for Energy Studies

28 © LSU Center for Energy Studies

Note: 1 New Jersey was also an original member state but withdrew from the RGGI program in 2011.

Source: RGGI.org

Regional Greenhouse Gas Initiative, Inc. (RGGI, Inc.) is a 501(c)(3) non-profit corporation

created to support development and implementation of the Regional Greenhouse Gas

Initiative (RGGI).

ME

NH

VT

NY MA

CT RI

MD DE

• A cooperative effort among nine states: Connecticut, Delaware, Maine, Maryland,

Massachusetts, New Hampshire, New York, Rhode Island and Vermont.1

• Started in 2008 and was the first market-based regulatory program to reduce GHG

emissions in the U.S.

• Establishes a regional cap on carbon dioxide (CO2) emissions from the

power sector and requires power plants to possess CO2 allowances equal

to their CO2 emissions over each three-year control period..

• The regional CO2 emission cap comprises the sum of each RGGI

participating state’s annual CO2 allowance budget. For the first six years

of the program (2009-2014) the emission cap is 188 million short tons of

CO2 per year. Beginning in 2015, the cap will decrease by 2.5% per year,

such that it will be 10% lower by the end of 2018.

• Recent reports have deemed the program a success and estimate that

the program has already created $1.6 billion in economic value, could

lead to $1.1 billion in ratepayer savings, and states participating in the

program have seen a 20 percent greater reduction in per-capita CO2

emissions than non-RGGI states.

How Does Cap & Trade Work?

29

Simply speaking, sources “long” on credits will trade with

those that are “short.”

20,000

25,000

30,000

35,000

40,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

em

issio

ns -

to

ns

Emissions

exceed

allowance –

Generator A

needs to buy

credits

Emissions are

lower than

allowance –

Generator B can

sell credits

Generator A

Generator B

Allowanc

e

Center for Energy Studies

How Does Cap & Trade Improve Overall Emissions?

30

20,000

25,000

30,000

35,000

40,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

em

issio

ns -

to

ns

Emissions

exceed

allowance –

Shortfall must be

made up from:

(1) credit

purchases

from those

facilities

individually

long ; and/or

(2) capital

investments to

lower emissions

profile.

Framework creates “scarcity” because the initial regulatory “design” is

intentionally “short” in the aggregate. More stringent caps result in more

expensive mitigation costs (higher marginal credit prices), other things

equal.

Center for Energy Studies

CO

2 E

mis

sio

ns (

tho

usa

nd to

ns/M

Wh)

Source: U.S. Environmental Protection Agency, Accessed at: http://camddataandmaps.epa.gov/gdm/.

CO2 Emissions in RGGI States

Center for Energy Studies

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

31 © LSU Center for Energy Studies

RGGI states have seen dramatic decreases in carbon emissions since

2000. Today, the CO2 emissions rate is about 29 percent lower than a

decade ago.

Nu

mb

er

of A

llow

an

ce

s

Source: Regional Greenhouse Gas Initiative, Inc., Accessed at: http://www.rggi.org/market/co2_auctions/results.

RGGI Auction Results, Quantities and Price

Center for Energy Studies

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

0

5

10

15

20

25

30

35

40

45

50

Quantity Offered Quantity Sold Clearing Price

Cle

arin

g P

rice

($)

32 © LSU Center for Energy Studies

The Regional Greenhouse Gas Initiative is the only existing cap and trade

market for CO2 in North America. Prices have been stable, but recent auctions

have seen falling volumes.

($/t

on

CO

2 E

mitte

d)

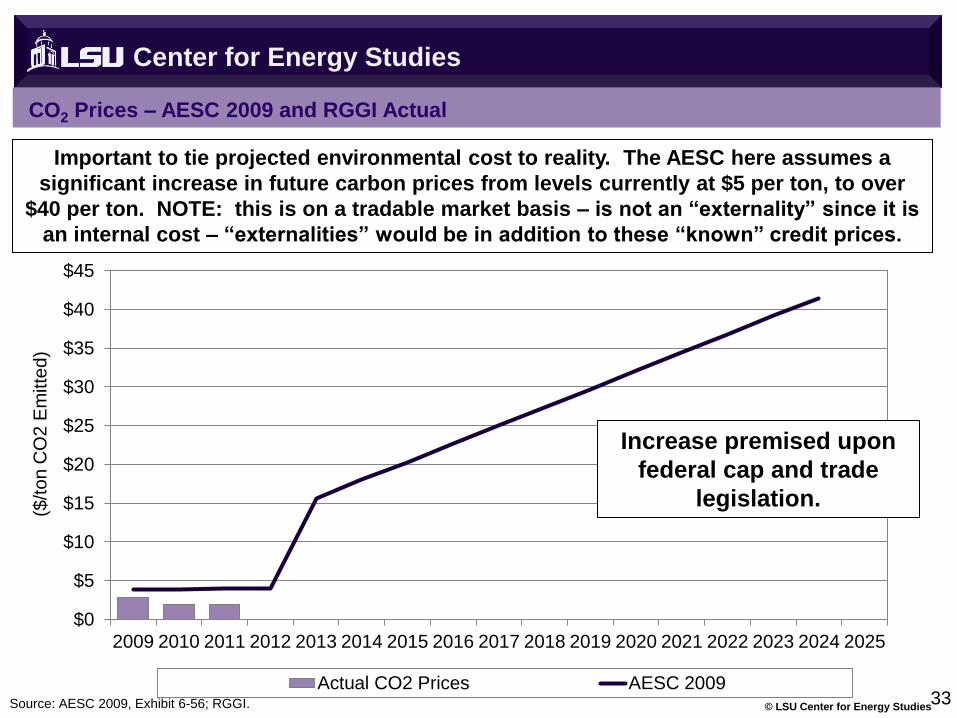

Source: AESC 2009, Exhibit 6-56; RGGI.

CO2 Prices – AESC 2009 and RGGI Actual

Center for Energy Studies

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Actual CO2 Prices AESC 200933

© LSU Center for Energy Studies

Important to tie projected environmental cost to reality. The AESC here assumes a

significant increase in future carbon prices from levels currently at $5 per ton, to over

$40 per ton. NOTE: this is on a tradable market basis – is not an “externality” since it is

an internal cost – “externalities” would be in addition to these “known” credit prices.

Increase premised upon

federal cap and trade

legislation.

($/t

on

CO

2 E

mitte

d)

Source: AESC 2009, Exhibit 6-56; AESC 2011, Exhibit 6-57.

CO2 Externality Value – AESC 2009 and AESC 2011

Center for Energy Studies

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

AESC 2009 AESC 2011

Assumes

emergence of

Federal cap and

trade program.

34 © LSU Center for Energy Studies

Comparing prior to current AESC shows impact and timing of federal carbon regulation

assumptions.

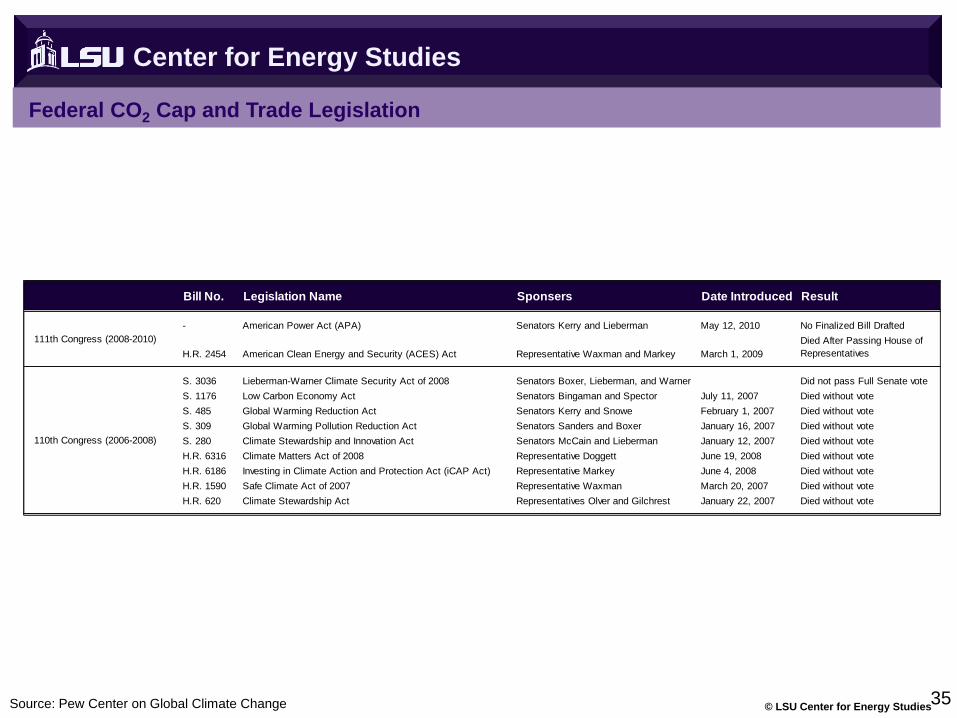

Source: Pew Center on Global Climate Change

Federal CO2 Cap and Trade Legislation

Center for Energy Studies

Bill No. Legislation Name Sponsers Date Introduced Result

- American Power Act (APA) Senators Kerry and Lieberman May 12, 2010 No Finalized Bill Drafted

H.R. 2454 American Clean Energy and Security (ACES) Act Representative Waxman and Markey March 1, 2009

Died After Passing House of

Representatives

S. 3036 Lieberman-Warner Climate Security Act of 2008 Senators Boxer, Lieberman, and Warner Did not pass Full Senate vote

S. 1176 Low Carbon Economy Act Senators Bingaman and Spector July 11, 2007 Died without vote

S. 485 Global Warming Reduction Act Senators Kerry and Snowe February 1, 2007 Died without vote

S. 309 Global Warming Pollution Reduction Act Senators Sanders and Boxer January 16, 2007 Died without vote

S. 280 Climate Stewardship and Innovation Act Senators McCain and Lieberman January 12, 2007 Died without vote

H.R. 6316 Climate Matters Act of 2008 Representative Doggett June 19, 2008 Died without vote

H.R. 6186 Investing in Climate Action and Protection Act (iCAP Act) Representative Markey June 4, 2008 Died without vote

H.R. 1590 Safe Climate Act of 2007 Representative Waxman March 20, 2007 Died without vote

H.R. 620 Climate Stewardship Act Representatives Olver and Gilchrest January 22, 2007 Died without vote

111th Congress (2008-2010)

110th Congress (2006-2008)

35 © LSU Center for Energy Studies

Source: Avoided Energy Supply Cost, 2011 Report

Changing Forecasted Environmental Costs Impact on Electric Price

Center for Energy Studies

36 © LSU Center for Energy Studies

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2012 2017 2022 2027 2032 2037

Original On-Peak Electric Price

Updated On-Peak Electric Price (using new Environmental Assumptions)

(20

11

$/M

MB

tu)

Below updates avoided cost estimate for changing outlook for natural gas

prices AND tradable environmental credits. Overall, the impact of tradable

allowances on total costs are not sizable, unless, some additional “externality”

value is added.

Center for Energy Studies

Renewables

3

7 © LSU Center for Energy Studies

Source: PJM-GATS

Cost of Solar Renewable Energy Credits through PJM-GATS

Center for Energy Studies

$0

$100

$200

$300

$400

$500

$600

$700

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12

Delaware District of Columbia Maryland

New Jersey Ohio Pennsylvania

Virgina

$ p

er

So

lar-

RE

C

38 © LSU Center for Energy Studies

Solar energy costs (SRECs) have decreased considerably over the

past year, even in high priced states such as New Jersey.

Cost of Non-Solar Renewable Energy Credits

Center for Energy Studies

39 © LSU Center for Energy Studies

Class 1 RECs have also seen considerable price decreases

although there has been some rebounding in the past year.

Source: Energy Efficiency & Renewable Energy Division, U.S. Department of Energy; Citing Spectron Group

Accessed at: http://apps3.eere.energy.gov/greenpower/markets/certificates.shtml?page=5

Source: Avoided Energy Supply Cost, 2011 Report

Changing Forecasted REC Prices Impact on Electric Price

Center for Energy Studies

40 © LSU Center for Energy Studies

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2012 2017 2022 2027 2032 2037

Original On-Peak Electric Price

Updated On-Peak Electric Price (using new REC Price Forecast)

(20

11

$/M

MB

tu)

REC prices are avoidable costs that can be credited to avoided cost

if used for energy efficiency cost effectiveness analysis.

Center for Energy Studies

Conclusion

4

1 © LSU Center for Energy Studies

Source: Avoided Energy Supply Cost, 2011 Report

Effect of Changing Realities on Estimates of Avoided Electrical Prices

Center for Energy Studies

42 © LSU Center for Energy Studies

Estimated Estimated Estimated Estimated

2040 2040 2040 2040

On-Peak Off-Peak On-Peak Off-Peak

Electric Price Electric Price Electric Price Electric Price

($2011/MWh) ($2011/MWh) ($2011/MWh) ($2011/MWh)

Original AESC 2011 Estimate (A) $141 $115 $155 $120

'A' with Natural Gas Price

Forecasts Updated to Reflect

More Recent AEO Projections

(B) $82 $69 $90 $71

'B' Modifided to Reflect Current

Environmental Policy

Understanding

(C) $66 $52 $73 $55

'C' Modifided to Reflect Current

REC Prices(D) $69 $56 $76 $58

Total Effect 'A' to 'D' -51.08% -51.67% -50.83% -51.55%

Winter Summer

Source: Avoided Energy Supply Cost, 2011 Report

Effect of Changing Realities on Estimates of Avoided Electrical Prices

Center for Energy Studies

43 © LSU Center for Energy Studies

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2012 2015 2018 2021 2024 2027 2030 2033 2036 2039

Original On-Peak Electric Price Updated On-Peak Electric Price

(20

11

$/M

Wh

)

Updated forecasts can result in differences of up to 50 percent.

Source: Avoided Energy Supply Cost, 2011 Report

Effect of Changing Realities on Estimates of Avoided Electrical Prices

Center for Energy Studies

44 © LSU Center for Energy Studies

$0

$20

$40

$60

$80

$100

$120

$140

2012 2015 2018 2021 2024 2027 2030 2033 2036 2039

Original Off-Peak Electric Price Updated Off-Peak Electric Price

(20

11

$/M

Wh

)

Updated forecasts can result in differences of up to 50 percent.

Center for Energy Studies

Questions, Comments and Discussion

45

www.enrg.lsu.edu