Embed Size (px)

Citation preview

© 2015 Research Academy of Social Sciences

http://www.rassweb.com 147

International Journal of Empirical Finance

Vol. 4, No. 3, 2015, 147-164

The Impact of Auditing in Controlling Fraud and Other Financial

Irregularities

Lawal Babatunde Akeem1

Abstract2

Fraud in the Nigerian Banking Industry before the recent merger, acquisition and recapitalization efforts was

at alarming rate. It has caused many banks to collapse, and many investors and depositors funds were trapped

in. Infact it has prevented many banks from achieving their goals and many businesses went into liquidation.

Honestly speaking it has become a cankerworm that has eating deep into the financial sector of the Nigerian

economy. That calls for the need for this study and the purpose of this study therefore is to identify the

causes of fraud, measure its impact and identify the means of controlling it. The study is a survey research

and questionnaire was used for the collection of primary data. Questionnaires were administered to staff of

First Bank of Nigeria PLC. Chi-square was used in analyzing data. The findings show that lack of adequate

training, communication gap, and poor leadership skills were the greatest causes of fraud in Nigerian banking

industry. It was concluded that adequate internal control system should be put in place and that workers

satisfaction and comfort should be taking care of.

Keywords: fraud, banking, merger, acquisition, recapitalization, investors.

1. Introduction

According to Gay, Schelluh and Reid 1997, an auditor has the responsibility for the prevention,

detection and reporting of fraud, other illegal acts and errors is one of the most controversial issues in

auditing, and has been one of the most frequently debated areas amongst auditors, politicians, media,

regulators and the public. This debate has been especially highlighted by the collapse of both small and big

corporations across the globe. The auditing profession in Nigeria has caught the media’s attention following

financial scandals in some of the Nigerian banks such as Intercontinental Bank, Oceanic Bank, Afri Bank,

and Bank PHB among others. There seems presently to be a misconception that auditors’ duties are largely

the preventing, detecting and reporting of fraud, for example, Idris (2009). The aim of this paper is to

identify financial report users’ perceptions of the extent of fraud and financial irregularities in first bank of

Nigeria plc, and to determine their perceptions of the auditor’s responsibilities in detecting fraud and other

financial irregularities and the performance of related audit procedures in first bank. The project also aims to

ascertain whether the report users’ perceptions of auditors’ responsibilities on fraud and other financial

irregularities are consistent with those of the auditing profession as expressed in auditing standards in

Nigeria.

Bank organizations in Nigeria perform a variety of tasks and responsibilities not only for transformation

agenda but also to enable it to function in an effective manner. These tasks and responsibilities are

distributed among teams, which are assigned to fulfil their duties in a specific organisation. All designated

tasks are equally important in Nigerian Banks, thus, making all employees and staff crucial to the operations

of the bank. One of the crucial functions in these organizations is the process of auditing especially in the

1MBA, BSc, Department of Economics, Accounting & Finance, Jomo Kenyatta University of Agriculture and

Technology, Juja, Nairobi, Kenya. 2 To cite this article: Lawal Babatunde Akeem (2015). The Impact of Auditing in Controlling Fraud and Other

Financial Irregularities. International Journal of Empirical Finance, 4(3), 147-164.

L. B. Akeem

148

cases of fraud and irregularities. It has been reported that an audit is an evaluation of an organization, system,

process, project or product, which involves the independent and fair assessment of the financial statements of

the organization. Knowledgeable, independent, and objective individual or group of individuals, known as

auditors or accountants, makes a report based on the results of the audit. In addition, this function is

performed to determine the reliability and validity of financial information, and to present an evaluation of a

specific company or an internal control of a particular business system, for these systems must comply with

the generally accepted standards laid down by national governing bodies for regulation (Power, Walsh, &

O’Meara, 2001). Because of such importance, this project seeks to consider the effect of fraud and

irregularities on first bank performance in Nigeria and its control.

In accordance to fraud and irregularities on banks performance in Nigeria, auditing and financial

evaluation are crucial since it reflect on how their respective administrators manage the flow of their income,

assets and transactions. For this reasons, banks in Nigeria should hire several experts to do the auditing and

financial evaluations. Aside from hiring accountants and auditors that will work for them internally, they

also need to seek help of other experts to avoid biasness and also in order reveal the genuine stability of the

entity being audited (Jones and Pendlebury, 2000). According to Arter, (2002), these people are called

independent auditors expert or sometimes called external auditors. Basically, external auditors/accountants

are audit experts who perform an audit on the financial statements of a government, company, individual, or

any other legal entity (Cameron, 1982). As stated previously, these people are working independently to

present an unbiased and independent evaluation on such entities. In comparison to internal auditors, external

auditors’ primary responsibility is assessing the risk management practices and strategy, management and

governance processes of an entity. These experts usually does not express any opinion on the entity's

financial statements, they just evaluate and never do such recommendations. Similar to internal auditors,

independent auditors are considered by the public service sector and other organisations to take a look at

financial statement to confirm they are free of errors and obvious misstatements (Arter, 2002).

The objectives of this paper are to:

Examine and report in writing of opinion on the truth and fairness of the financial statements so that

anybody reading and or using the financial statements can belief in them.

Attest to the fairness of the financial statements and compliance with laws, regulations and the

effectiveness of controls.

To gather sufficient evidence so as to be able to form an opinion on the accuracy and correctness of the

financial statement.

To provide credibility to financial information that can be relied upon by outsiders, such as

stockholders, creditors, government regulators, customers and other interested third parties.

To prevent errors and fraud by the deterrent and moral effect of the audit. .

The above objectives will be guided by the following questions:

What are the auditors’ duties towards fraud?

What should auditors’ do if he discovers an irregularity in the form of material error or fraud?

What options do auditors’ have if they detect a fraud by management?

What effect does lack of auditing have in the banking industry?

Basically, fraud and irregularities occurring among banks in Nigeria created significant effect. This

event may result to business failure or worst bankruptcy. Aside from this, fraud & irregularities could also

have significant effect to capital market, capital structure, Efficiency Market Hypothesis and credit ratings. In

accordance to the impact on control environment and internal controls within Banks in Nigeria, the

independent auditor has a number of affirmative responsibilities. According to the Jones and Pendlebury

(2000), firstly, the independent auditor must be precise in strategies to find out and report the bank's genuine

financial position. Secondly, as a representative for the public, the independent auditor must stay independent

of the management of the bank. The independent auditor owes the independence duty to the shareholders of

the bank, the public and the board of directors. Thirdly, the independent auditor must completely reveal all

material features of the financial condition of the bank. The independent auditor duty of disclosure requires

International Journal of Empirical Finance

149

them to reject an improper engagement, report cheating, and place a caution on statements pertaining to the

ability and liquidity of the company to continue as a going concern.

In independent auditor experts’ affirmative duty to discover irregularities and material errors, including

fraud, the independent auditor fulfils a function that the public considers the independent auditor's most

significant role (Monaghan 1989). According to Harvey, (1990), fraud does not become visible on the face

of bank's records, but frequently signs of it will likely in the form of irregularities, and, hence, the auditor can

only divulge fraud by closely examining irregularities. Whereas the Statements of Auditing Standards (SAS)

according to Arter, (2002) asserts the independent auditor's clear liability to identify management fraud, that

same SAS does not oblige the auditor to guarantee the accuracy of the firm's financial statements.

2. Literature Review

Introduction

From 1900, the financial statements became the basic mechanism by which the activities of company

managers were monitored, and, to some extent, this is still true today. Once the directors were required by

law to prepare annual financial statements shareholders then had access to financial information about the

company they owned. However, this access is limited and the shareholders may come to believe that they are

not getting all the information, or the right information to enable them to make investment decisions. Thus,

the role of auditor as agent for the shareholder becomes crucial and the costs of the audit are as nothing with

the comfort and reassurance the audit affords the shareholders. The independent audit is a crucial part of this

process to ensure that the financial statements faithfully represent the activities of the managers during the

financial period.

There is a difference, known as the ‘Perception Gap’ between the public and the auditing profession in

relation to an auditor’s duty regarding fraud and irregularities. The auditors see their duty as: the independent

examination of an expression of opinion on, the financial statement of an organization by an appointed

auditor in pursuance of that appointment and in compliance with any relevant statutory obligation. The

emphasis is on the financial statements. However, the public, including much of the business community,

tend to see an auditor’s duties primarily in terms of the detention, and possibly prevention, of fraud and

irregularities. There is an ISA 240, “the auditor’s duty to consider fraud in an audit of financial Statements”.

Also relevant are ISA 315 “Understanding the entity and its environment and assessing the risks of a material

misstatement”.

During the 1970s, new organization and expenses pressures caused a shift in the accounts payable

function in many companies. These changes combined with overload, overwork, reduced staffing, high

volume and a need to create low charges led to more errors in the transaction processing. During the late

1970s, the account payable recovery audit industry was developed to audit accounts payable transactions and

recover funds paid in error. The work was done on contingency, and audit recovery firms collected on

agreed-upon percentage of the recovery amount. Sometimes, senior managers are reluctant to approve

recovery audits; they think the result may make them look as though they are performing up to standard.

However, most CEOs understand the value of an increased bottom-line profit, especially when it has no cost.

In today’s organizational environment, there are two classes of audit;

Pre-Audit

Pre-audit is available as a result of technology advances which were not available few years ago. Pre-

audit eliminates errors associated with processing accounts payable transactions before the cheque is written.

This eliminates the loss of cash due to errors.

Post-Audit

Post-audit examines accounts payable transaction after the cheque has been processed. The auditor

reviews transaction after software exposes errors through the data mining function. These errors are

examined and validated with related documents. When a claim is presented to the client, the auditors have

L. B. Akeem

150

the responsibility to follow-up and answer any of the questions. The auditor collects his contingency fee after

the claim is settled. Many firms offer post audit services from one or two-person firms to large companies.

The key to a strong audit is software which has the ability to investigate and locate errors; and when the

errors are found, can track the collection process, once the clients approves collection. An audit firm does not

get paid until the collection is made. Post-audit software also can be purchased by clients to be used

internally by the accounts payable staff and eliminate the cost of external audits. Each major post audit

company has developed its own audit software to find and mine errors. Each company believes its software

is best. Many firms allow a second audit (post-audit) to confirm the completeness of the first that is (pre-

audit).

Audits are often viewed as falling into three major categories:

i. Financial audits

ii. Compliance audits

iii. Operational audits.

In addition, the Sarbanes-Oxley Act requires an integrated audit for public companies.

Financial Audits

A financial audit is an audit of the financial statements of an entity. An audit of financial statements

ordinarily covers the balance sheet and the related statements of income, retained earnings and cash flows.

The goal is to determine whether these statements have been prepared in conformity with the generally

accepted accounting principles. Financial statement audits are normally performed by firms of certified

public accountants; however, internal auditors often perform financial audits of departments or business

segments. Users of auditors’ reports include management, investors, bankers, creditors, financial analysts,

and government agencies.

Compliance Audits

The performance of a compliance audit is dependent upon the existence of verifiable data and of

recognized criteria or standards, such as established laws and regulations, or an organization’s policies and

procedures. Compliance auditing involves testing and reporting on whether an organization has complied

with the requirements of various laws, regulations and agreements. These audits measure compliance with

banking laws and regulations and with traditional standards of sound banking practice. Internal auditors

perform audits of compliance with internal controls, other company policies and procedure, and applicable

laws and regulations. Internal audits departments often are involved with documenting and testing internal

control for management’s reports required by the Sarbanes-Oxley Act. Finally, many state and local

governmental entities and nonprofit organizations that receive financial assistance from the federal

government must arrange for compliance audits under the Single Audit Act or OMB Circular A-133. Such

audits are designed to determine whether the financial assistance is spent in accordance with applicable laws

and regulations.

Operational Audit

An operational audit usually includes the intention to appraise the performance of a particular

organization, function or group of activities. An operational audit tends to require more subjective judgment

than do audits of financial statements or compliance audits. Before starting an operational audit, the auditor

must obtain a comprehensive knowledge of the objectives, organizational structure, and operating

characteristics of the unit been audited.

Fraud

Fraud according to Webster’s new world dictionary is the “intentional deception to cause a person to

give up property or some lawful right.” The Association of Fraud Examiners (1999) report to the nation on

occupational fraud and abuse as “the use of one’s occupation for personal enrichment through the deliberate

misuse or misapplication of employing an organizations resources or assets.” Fraud, according to Adeniji

International Journal of Empirical Finance

151

(2004) and ICAN (2006), is an intentional act by one or more individuals among management, employees or

third parties, which results in a misrepresentation of financial statements. Fraud can also be seen as the

intentional misrepresentation, concealment, or omission of the truth for the purpose of deception or

manipulation to the financial detriment of an individual or an organization which also includes

embezzlement, theft or any attempt to steal or unlawfully obtain, misuse or harm the asset of the

organization, (Adeduro, 1998 and, Bostley and Drover 1972). Fraud has increased considerably over the

recent years and professionals believe this trend is likely to continue. According to Brink and Witt (1982),

fraud is an ever present threat to the effective utilization of resources and it will always be an important

concern of management. ISA 240 ‘The Auditor’s Responsibilities to Consider Fraud in an Audit of Financial

Statement (Revised)’ refers to fraud as “an intentional act by one or more individuals among management,

those charged with governance, employees or third parties, involving the use of deception to obtain an unjust

or illegal advantage”. Aderibigbe and Dada (2007) define fraud as a deliberate deceit planned and executed

with the intent to deprive another person of his property or rights directly or indirectly, regardless of whether

the perpetrator benefits from his/her actions.

- Irregularity: is an intentional mistake or distortions of financial statement such as misrepresentation or

misappropriation of assets.

- Misappropriation: is any dishonest or fraudulent act which includes such things as:

Unauthorized use, taking, or destruction of banks property for personal gain, or to purposely deprive the

organization of its use,

Forgery or alteration of cheques, drafts, promissory notes, and securities,

Any taking or unauthorized use of bank’s funds, securities, or any other assets,

Forgery or alteration of policy-related items, such as loans, assignments, changes in beneficiaries, etc,

The Cost of Fraud to Banking Organizations

The cost of fraud in banking is difficult to estimate because not all fraud or abuse is discovered as a

result of lack of audit in the banking industry, not all uncovered fraud is reported, and civil or criminal

actions are not always pursued. Data show that the overall cost of fraud is over double the amount of missing

money or assets. As computerized systems become more complex, so is the expected cost of fraud.

Approximately one in twenty banks failures are attributed to fraud (MacErlean 1998).

- The Offenders

It is the trusted and valued employees who generally commit fraud. When frauds are discovered, there is

often shock and disbelief that they could have committed such an act. The perpetrator of fraud could be “the

person next door.” (Russell 1995)The losses for men employees are four times greater than those of women

employees. Losses of employees over 60 years are 28 times greater than those of 25 years old or younger.

Approximately 58 percent of reported fraud is committed by non-managerial employees, 30 percent by

managers, and 12 percent by owner executives (Association of Fraud Examiners 1999). In most cases,

offenders do not view stealing from organizations as harmful; they may think that the crime is victimless;

and they do not view their theft as being devastating or costly to the organizations. Many frauds occur

because the opportunity exists and the perpetrator does not believe he or she will be caught. In many cases,

the offender has “little or no criminal self concept offenders view violation as part of their work “(Hagan

1997). Further, they usually minimize their crime since it results in minor losses for a large volume of

clients; no one client is usually targeted for the crime.

o Factors Involved in Preventing Fraud

The directors and management have the overall responsibility for the prevention of fraud. Prevention

they say is better than cure and although it may be impossible to completely eliminate fraud because of the

effect of collision between the staff and management’s ability to over-ride controls. It is however possible to

reduce the incidence of fraud to the barest minimum. The following factors should be taking into

consideration when trying to prevent the incidence of fraud;

L. B. Akeem

152

1. Fraud Policy- The organization should have a fraud policy which should be well circulated. Posters

explaining the evil effects of fraud should be pasted at strategic points within the company’s premises.

Employees should be well aware of the policy and the punitive measures that would be visited on any person

that violates the policy, management at all levels should also be ready to abide by the policy and lead by

examples.

2. Continuing Education and Training- Management and staff should continuously update their

knowledge about frauds and the latest risks. This can be achieved by attending fraud awareness seminars

offered by accountancy firms, the police and other consultancy outfits.

3. Employee Recruitment and Selection- The recruitment and selection of employee is a key initiative

in fraud prevention. The company should maintain a policy of employing honest, competent and reliable

people. It is also of important that the background and employment history of people to be recruited are

properly reviewed before employment offers are made. There should be rules regarding pre-employment

screening, promotion, performance evaluation and termination. Applicants should be told that offers will

only be made after appropriate responses have been received from referees and necessary follow-ups made.

4. Install Effective Accounting and Control Systems- The installation of an effective accounting system

with appropriate controls is a key to both the detection and prevention of fraud. The accounting system and

the related controls need to be adequate, appropriate and up to date..

Management fraud is possible where the management of an organization is dominated by one person or

a small group of people and there is no external supervisory body or committee. The audit committee, (or

other supervisory committee) if given adequate powers, will be in a position to check the ability of

management to override otherwise effective control so as to perpetrate fraud.

o Auditor’s Duty Regarding Fraud

The auditor’s duty is not to discover fraud. It is widely but erroneously believed that the auditor’s duty

is to discover fraud, error or irregularities. This view might be correct if the auditor is specially engaged to

investigate the incidence of fraud or other irregularities. The auditor is not therefore duty bound to discover

fraud or error while discharging his duties in pursuant to his appointment as auditor under the Companies Act

or other statue.

The following are the reasons why the public in general including the auditor’s client cannot hold the

auditor responsible for failing to discover fraud and other irregularities in the ordinary course of performing

an audit:

i. Audits are usually carried out on test basis: it is not practical to test the transactions one hundred

percent. In most cases, the auditor takes a small number of items or transactions for testing and he uses his

best judgment to determine the areas to be tested. As a result of this, there is a risk that some material

misstatements resulting from fraud in the financial statement might not be tested.

ii. Frauds are usually executed with great ingenuity: fraudsters believe they are smarter than any other

person because they usually take very great care to conceal their acts. Also, fraud always involves acts such

as collision, forgery, deliberate failure to record transactions or intentional misrepresentation. The auditor

ordinarily gets his evidence from the accounting records, documents (such as invoices) and representation by

management.

It should however be recognized, that the auditor has a duty to form an opinion and also report on the

truth and fairness of the financial statements. In forming his opinion, the auditor normally carry out

procedures and tests which are designed to obtain evidence that will provide reasonable assurance that the

financial statements are properly stated and free from fraud and error which may materially affect it. The

auditor should therefore plan his audit so that he can have a reasonable expectation of detecting material

misstatement resulting from fraud or error in the financial statements.

International Journal of Empirical Finance

153

Controls Auditors Have in Preventing Fraudulent Activities

Due in the part to the phenomenal losses in the banking industry, the controversy as existed concerning

the role of the external auditor and the public’s perception of that role SAS no 53, “ the auditors

responsibility to detect and report errors and irregularities”, issued by the Accounting Standards

Board(1988), was originally intended to address this problem. However, the public oversight board of the

AICPA SEC practice section concluded in 1993 that management believed that auditors’ had a greater

responsibility for the detection of fraud than was currently been met. Business owners, legislators, judges,

juries and the general public also share such beliefs. Most people do not realize what the responsibility of the

auditor is according to SAS no1, codification of auditing standards and procedures :” the auditor has the

responsibility to plan and perform the audit to obtain reasonable assurance about whether the financial

statement are free of material misstatement, whether caused by error or fraud. Because of the nature of audit

evidence and the characteristic of fraud, the auditor is able to obtain reasonable, but not absolute, assurance

that material misstatements are detected. The auditor has no responsibility to plan and perform the audit to

obtain reasonable assurance that misstatement whether caused error or fraud, that are not material to the

financial statement are detect”. In an attempt to stifle criticism and appropriately respond to the public’s

demand for improved auditors’ performance, the American institute of certified accountant issued SAS no

82. The new auditing standard details the auditors’ responsibility to detect and report material misstatement

in financial statement due to fraud. This is the first time the AICPA has used the word ‘fraud’ rather than the

more discreet word ‘irregularity’. The two types of misstatement relevant to the auditors’ consideration of

fraud in a financial statement audit are those arising from fraudulent financial reporting and misappropriation

of assets. The SAS is effective for financial statement audit periods ending on or after December 15, 1997.

Similarly, the private securities litigation reform Act of 1995 imposes some of the same requirement on

public company auditors. The requirements are as follows:

1. Audit must include procedures designed to provide reasonable assurance of detecting illegal acts that

would have a direct and material effects on financial statement amounts.

2. Each audit must include procedures to identify related-party transactions that are material.

3. Each audit must include an evaluation of the ability of the issuer of financial statement to continue as

going concern.

Communication about Fraud to Management and the Audit Committee

Whenever the auditor has determined there is evidence that fraud may exists, that matter should be

brought to the attention of an appropriate level of management. This is generally appropriate even if the

matter might be considered inconsequential, such as a minor defalcation by an employee at a low level in the

entity’s organization. Fraud involving senior management and fraud (whether caused by senior management

and employees) that causes a material misstatement of the financial statement should be reported directly to

the audit committee regarding the expected nature and extent of communications about misappropriations

perpetrated by lower level employees.

When the auditor, as a result of the assessment of the risk of material misstatement due to fraud, have

identified risk factors that have continuing control implications (whether or not transactions or adjustment

that could be the result of the fraud have been detected). The auditor should consider whether these risk

factors represent reportable conditions relating to the entity’s internal control that should be communicated to

senior management and the audit committee. (Section325, communication of internal control related matters

noted in an audit). The auditor also may wish to communicate their risk factors identified when actions can

be reasonably taken by the entity to address the risk. The disclosure of possible fraud to parties other than the

client’s senior management and its audit committee ordinarily is not part of the auditor’s responsibility and

ordinarily would be precluded by the auditor’s ethical or legal obligation of confidentiality unless the matter

is reflected in the auditor’s report.

L. B. Akeem

154

The Responsibilities of Management in Controlling Fraud

Given that the CPAs do not agree with the changed expectations of their role, and the limit on the

auditors possible role in controlling fraud, other consideration in the prevention and detection of corporate

fraud should be discussed. Which include managerial control, employee screening, forensic accounting, and

others.

Managerial Controls

Organizations with one hundred or fewer employees have the greatest median losses per capita. The

primary reason for this is because internal controls are not sophisticated and stringent in smaller

organizations. So what, if any, are management responsibilities when it comes to the prevention or detection

of fraud? Annual reports of management states clearly that management is responsible for the preparation

and integrity of the financial information presented, and the company and management maintain a system of

internal controls to provide for administrative and accounting controls.

Screening

Another element to combat fraud is adequate employee screening. Although, this statement might seem

obvious, a good rule to follow to minimize the risk of fraud is to hire honest employees. There are many

organizations specializing in pre-employment screening. These screening tests include lie detector and drug

tests and fingerprinting of employees. Through adequate background checks of information on resumes and

applications, an employer can elicit significantly more information and determine if the original information

is accurate.

Organizational Climate

A third component to deterring fraud is creating an organizational environment that reduces the

perceived need of a pressured employee to commit fraud. These environments include creating open and

consistent communications for hiring, evaluating employees’ performance, and assessing employees for

promotion. These factors, along with counseling programs and employees enrichment efforts, might curtail

the perceived need of an employee to commit fraud.

Forensic Accounting

Within the last ten years, alarming increase in the cost of fraud to organizations has brought attention to

a specialization called forensic accounting. Forensic accounting is the integration of accounting, auditing,

and special investigative skills. The goal of forensic accounting is to uncover the paper trail left by a fraud

and prepare the investigation prior to presenting it to a court of law. Forensic accountants are trained to

examine financial statements and related materials for wrongdoing and analyze the reality of organizational

situations. Many banks and brokerage firms are now adding this department to investigate possible frauds.

Although it is not yet the norm for all organizations to have forensic accounting department, the trend has

increased considerably.

Others

Finally, a few additional components to business fraud prevention include setting up a hotline whereby

fellow employees can report improper conduct, having a high level employee review unopened bank

statement monthly, establishing a written code of ethics, and making sure that management level employees

are role model. Although these additional practices may not seem important, they help establish the tone

within work environment and may help deter fraudulent activities.

o Auditors’ Responsibilities in Fraud Detection The role of auditors has not been well defined from inception (Alleyne and Howard 2005). Porter (1997)

reviews the historical development of the auditors’ duty to detect and report fraud over the centuries. Her

study shows that there is an evaluation of auditing practices and shift in auditing paradigm through a number

of stages.

International Journal of Empirical Finance

155

Porter study reveals that the primary objective of an audit in the pre-1920’s phase was to uncover fraud.

However, by the 1930’s, the primary objective of an audit had changed to verification of accounts. This is

most likely due to the increase in size and volume of organizations’ transactions which in turn made it

unlikely that auditors could examine all transactions. During this period, the auditing profession began to

claim that the responsibilities of fraud detection rested with the management. In addition, management

should also have implemented appropriate internal control systems to prevent fraud in their companies.

ISA 315 requires auditors to evaluate the effectiveness of an entity’s risk management framework in

preventing misstatements, whether through fraud or otherwise, in the course of an audit. Boynton, Johnson,

and Kell, (2005) stress that this requirement was not previously necessary. They further explain that such an

evaluation was only required previously when they chose to place reliance on that framework and to reduce

the extent of the audit investigation. In addition, all staff members engaged on an audit is now required to

communicate their findings with each other, to prevent situations where staff members, working

independently on their own sections of the audit, have failed to appreciate the significance of apparently

minor irregularities that, if combined, take on a more sinister meaning.

Internal Control

The primary responsibility for the prevention and detection of fraud rests with directors and

management. This is because fraud usually results in financial and other loss to the organization and the

directors and management have a responsibility of not only safeguarding the assets of the organization but o

increasing the wealth of their shareholders. Also, management and directors act in a stewardship capacity

with regard to the assets of the organization entrusted to them by the shareholders. Managers and directors

will be required to report to the shareholders on their stewardship.The tools with which directors and

management discharge this responsibility is through the institution and maintenance of an adequate system of

internal control. Internal controls, in most cases, are designed with the objective of preventing or detecting

fraud. As such, management has a duty to see to the continued operation and effectiveness of the controls

through regular reviews and updates. Internal control is a step taken by a business to prevent fraud- both

misappropriation of assets and fraudulent financial reporting. Others while acknowledging the importance of

internal control for fraud prevention, believed that internal control has an equal role in assuring control over

manufacturing and other processes. Committee of Sponsoring Organization (COSO) commissioned a study,

titled Internal Control-Integrated Framework, defines internal control as a process effected by the entity’s

board of directors, management and other personnel, designed to provide reasonable assurance regarding the

achievement of objectives in the following categories:

(a) Reliability of financial reporting

(b) Effectiveness and efficiency of operation

(c) Compliance with applicable laws and regulations.

o Effectiveness of Internal Control in Controlling Fraud

The effectiveness of internal control depends directly upon the communication and enforcement of

integrity and ethical values of the personnel who are responsible for creating, administering and monitoring

controls. Top management should develop a clearly articulated statement of ethical values. Also,

management should establish behavioral, ethical, and antifraud programs that discourage employees from

engaging in misappropriate acts and should provide proper recourse when they become aware of such acts.

- Employees should possess the skills and knowledge essential to the performance of their job. If

employees lack knowledge and skills, they may be ineffective in performing their assigned duties. Ideally,

management should be committed to hiring employees with appropriate levels of education and experience

and providing them with adequate supervision and training. It is especially important for individuals involved

in financial reporting to be competent in the selection and evaluation of accounting principles.

- The control environment of an organization is significantly influenced by the effectiveness of its

board of directors or its audit committee. The board of directors and the audit committee are responsible for

L. B. Akeem

156

overseeing the actions of management. Factor that bear on the effectiveness of the board or the audit

committee include the extent of its dependence from management, the experience and stature of its members,

the extent to which it raises and pursues difficult questions with management, and its interaction with the

internal and external auditors.

- Finance and accounting are the two departments most directly involved in the financial affairs of an

organization. The division of responsibilities between these departments illustrates the separation of the

accounting function from operations and also from custody of assets. Ultimately, the effectiveness of internal

control is affected by the characteristics of the organization’s personnel. Thus, management’s policies and

practices for hiring, providing orientation for, training, evaluating, counseling, promoting, and compensating

employees have s significant effect on the effectiveness of the control environment. Effective human

resources policies often can mitigate other weaknesses in the control environment.

- Effective human resource management is not a guarantee against losses from dishonest employees. It

is often the most trusted employees who engineer large embezzlements. Most organizations purchase fidelity

bonds to cover employees handling cash and other negotiable assets. Fidelity bonds are a form of insurance

in which a bonding company agrees to reimburse an employer, within limits, for losses attributable to theft or

embezzlement by bonded employees. This service offers added protection by preventing the employment of

persons with dubious records in position of trust.

3. Research Methodology

Research Design

According to Nworgu (1991), research design is a plan or blueprint which specifies how data relating to

a given problem should be collected and analyzed. Therefore, it provides the procedural outline for the

conduct of any given investigation. The objectives of this study are to attest to the fairness of the financial

statements and compliance with laws, regulations and the effectiveness of controls, prevent errors and fraud

by the deterrent and moral effect of the audit, gather sufficient evidence so as to be able to form an opinion

on the accuracy and correctness of the financial statement and provide credibility to financial information

that can be relied upon by outsiders, such as stockholders, creditors, government regulators, customers and

other interested third parties. Survey research design was adopted for this study where a sample of the

population is selected and used as respondents.

Population of the Study

The population of the study is made up of 100 staff of FIRST BANK OF NIGERIA, PLC which

consists of bankers, managers, and accountants.

Sample and Sampling Technique

The set questionnaires will be personally administered by the researcher; eighty (80) questionnaires will

be administered for the purpose of this study which is expected to give a result that would adequately

represent the population. This study will make use of random sampling technique in analyzing the data. The

population obtained from this sample is the basis on which deduction and conclusion will be made with

reference to this research.

Validation of the Research Instrument

Adedokun (2005) defined validity as the accuracy with which an instrument measures the characteristic

of interest, which it claims to measure. The contents and context of the questionnaire will determine the

validity of this study (Ali & Raza, 2015; Raza & Hanif, 2013).

International Journal of Empirical Finance

157

Administration of Instrument

The questionnaire will be self-administered to the sampled population of First Bank of Nigeria, Plc. The

respondents will be asked not to indicate their names on the questionnaires so as to make the responses

anonymous.

Sources of Data

The aim of data collection procedure is to get worthwhile data which would enable the researcher to get

the roots of the problem under investigation. Due to the time constraint of this research study, the researcher

will make use of only primary data collection method to collect relevant information to assess whether there

is a significant association between organizations with an internal and external audit function, the number

and value of their self-reported level of fraud and also organizations that does not in source part of their

internal audit function.

Method of Data Analysis

Because of the efficacy and authensity of this research, Chi-square test will be employed. The chi square

test is performed by defining the numbers categories and observing the number of case falling into each

category and knowing the expected number of cases fully in each category, the formulae for the Chi-square

is:

X2= (Oi-Ei)2

Ei

Where X2= chi square

Oi = number of observed case in category i

Ei = number of expected cases in category i

K = number of category, summation runs from 1=1 to 1=K

The researcher used 0.05 and 0.95 level of significance in testing the hypothesis.

The calculated chi-square (x2cal) and the tabulated chi-square (x2tab) are compared and a decision made

therefore.

Accept H1 if x2cal< x2 tab

Reject H0 if x2cal> x2 tab

4. Data Presentation, Interpretation and Analysis

Introduction

The primary data used for this study were obtained through the administration of well-designed

questionnaire to respondents. Using random sampling techniques, the questionnaire was handed to 80

respondents in First Bank of Nigeria, Plc. The respondents were bankers, managers, investors and

accountants. 58 questionnaires were returned, yielding a 72.5 percent response rate. Furthermore, more than

90 percent of the respondents claimed that they were aware of what auditors do. The high level of awareness

combined with their accounting qualifications and audit experience should add credibility to the findings of

the research.

Interpretation and Analysis of Data

This section interprets and analyzes the data gathered by the researcher.

L. B. Akeem

158

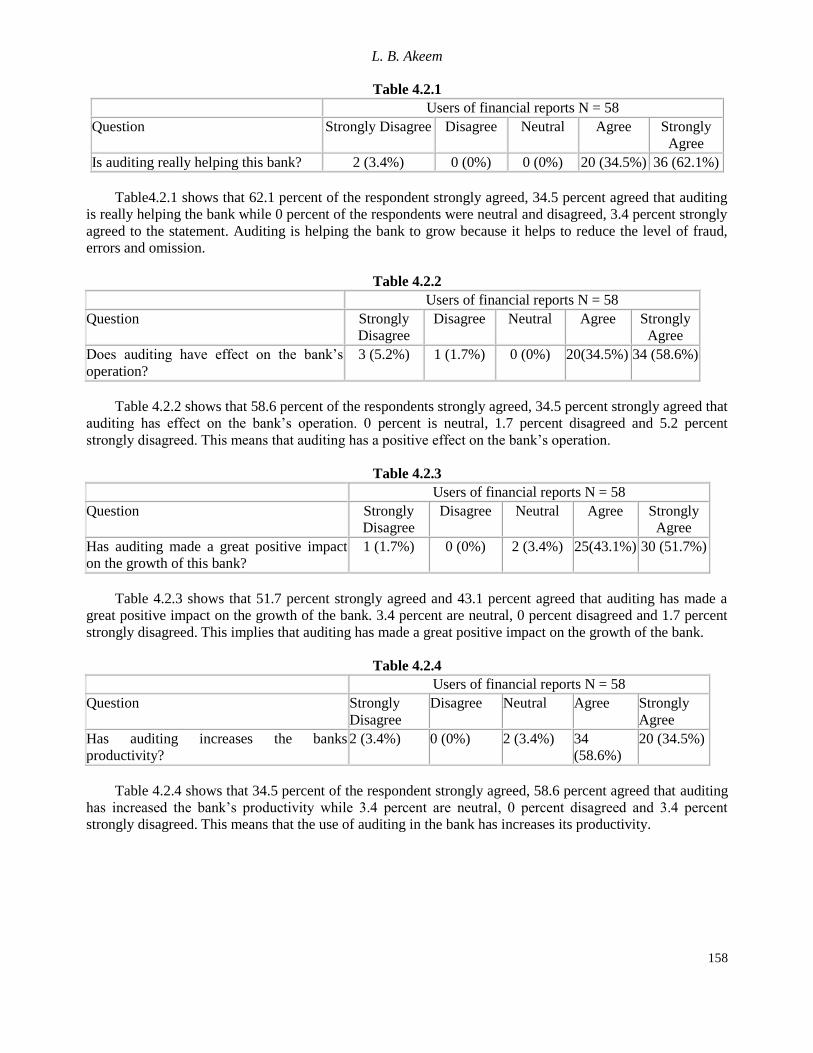

Table 4.2.1

Users of financial reports N = 58

Question Strongly Disagree Disagree Neutral Agree Strongly

Agree

Is auditing really helping this bank? 2 (3.4%) 0 (0%) 0 (0%) 20 (34.5%) 36 (62.1%)

Table4.2.1 shows that 62.1 percent of the respondent strongly agreed, 34.5 percent agreed that auditing

is really helping the bank while 0 percent of the respondents were neutral and disagreed, 3.4 percent strongly

agreed to the statement. Auditing is helping the bank to grow because it helps to reduce the level of fraud,

errors and omission.

Table 4.2.2

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Does auditing have effect on the bank’s

operation?

3 (5.2%) 1 (1.7%) 0 (0%) 20(34.5%) 34 (58.6%)

Table 4.2.2 shows that 58.6 percent of the respondents strongly agreed, 34.5 percent strongly agreed that

auditing has effect on the bank’s operation. 0 percent is neutral, 1.7 percent disagreed and 5.2 percent

strongly disagreed. This means that auditing has a positive effect on the bank’s operation.

Table 4.2.3

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Has auditing made a great positive impact

on the growth of this bank?

1 (1.7%) 0 (0%) 2 (3.4%) 25(43.1%) 30 (51.7%)

Table 4.2.3 shows that 51.7 percent strongly agreed and 43.1 percent agreed that auditing has made a

great positive impact on the growth of the bank. 3.4 percent are neutral, 0 percent disagreed and 1.7 percent

strongly disagreed. This implies that auditing has made a great positive impact on the growth of the bank.

Table 4.2.4

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Has auditing increases the banks

productivity?

2 (3.4%) 0 (0%) 2 (3.4%) 34

(58.6%)

20 (34.5%)

Table 4.2.4 shows that 34.5 percent of the respondent strongly agreed, 58.6 percent agreed that auditing

has increased the bank’s productivity while 3.4 percent are neutral, 0 percent disagreed and 3.4 percent

strongly disagreed. This means that the use of auditing in the bank has increases its productivity.

International Journal of Empirical Finance

159

Table 4.2.5

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Has auditing reduced the level of fraud? 2 (3.4%) 0 (0%) 2 (3.4%) 17(29.3%) 37 (63.8%)

Table 4.2.5shows that 63.8 percent of the respondents strongly agreed, 29.3 percent agreed that auditing

has reduced the level of fraud. However, 3.4 percent are neutral, 0 percent disagreed and 3.4 percent strongly

disagreed. Result shows that auditing has reduced the level of fraud in the bank.

Table 4.2.6

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Is fraud a major concern for banks in

Nigeria?

1 (1.7%) 3 (5.2%) 6 (10.3%) 19(32.8%) 29 (50%)

The results in Table 4.2.6 show that 50 percent of the respondents strongly agreed and 32.8 percent

agreed. However, 10.3 percent have a neutral opinion while 5.2 percent disagreed and 1.7 percent strongly

disagreed with this statement. Result shows that fraud is a major concern for banks in Nigeria and the

majority of responses agreed with the statements may be due to the high publicity of fraud cases in Nigeria.

Table 4.2.7

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Do you think that the discovery of

fraudulent activity would have a negative

impact on users?

2 (3.4%) 5 (8.6%) 6 (10.3%) 24 (41.4%) 21 (36.2%)

Table 4.2.7 shows that 36.2 percent strongly agreed and 41.4 percent agreed to this statement. 10.3

percent have a neutral opinion, 8.6 percent disagreed while 3.4 percent strongly disagreed. Fraud is an area of

concern in Nigeria; such responses reflect the common market reaction to negative publicity.

Table 4.2.8

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Do you feel that it is the responsibility of

the auditor to uncover fraud and to report

this to the appropriate authorities?

2 (3.4%) 1 (1.7%) 1 (1.7%) 27 (46.6%) 27 (46.6%)

Table 4.2.8 shows that 46.6 percent of the respondents strongly agreed and 46.6 percent agreed, in

comparison 1.7 percent is neutral, 1.7 percent disagreed and 3.4 percent strongly disagreed with this

statement. The results are in agreement with the requirements of the Approved Nigerian Standard on

Auditing. According to ISA 200 ‘Objective and general principles governing an audit of financial

statements’, the objective of an audit of financial statement is to enable the auditor to express an opinion

L. B. Akeem

160

whether the financial statements are prepared, in all material respects, in accordance with an applicable

financial reporting framework. However, ISA 200 also requires an audit to be designed so that it provides

reasonable assurance of detecting both material errors and fraud in the financial statements. To accomplish

this, the audit must be planned and performed with an attitude of professional skepticism in all aspects of the

engagement.

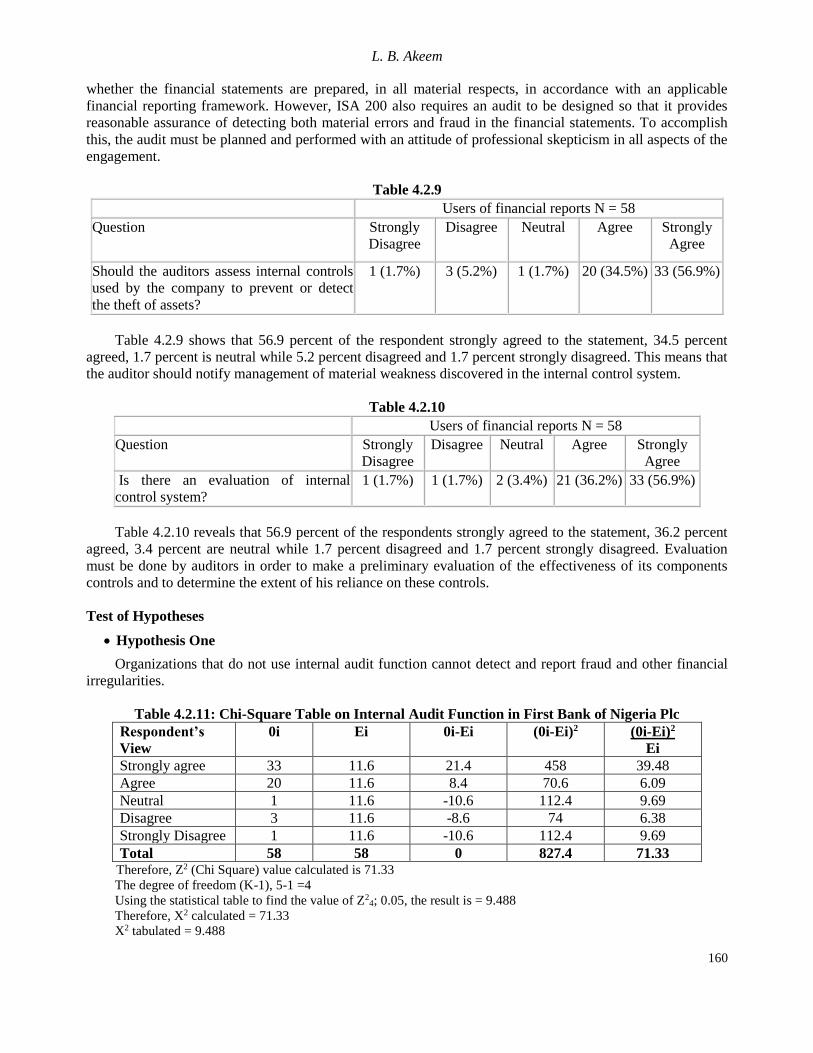

Table 4.2.9

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Should the auditors assess internal controls

used by the company to prevent or detect

the theft of assets?

1 (1.7%) 3 (5.2%) 1 (1.7%) 20 (34.5%) 33 (56.9%)

Table 4.2.9 shows that 56.9 percent of the respondent strongly agreed to the statement, 34.5 percent

agreed, 1.7 percent is neutral while 5.2 percent disagreed and 1.7 percent strongly disagreed. This means that

the auditor should notify management of material weakness discovered in the internal control system.

Table 4.2.10

Users of financial reports N = 58

Question Strongly

Disagree

Disagree Neutral Agree Strongly

Agree

Is there an evaluation of internal

control system?

1 (1.7%) 1 (1.7%) 2 (3.4%) 21 (36.2%) 33 (56.9%)

Table 4.2.10 reveals that 56.9 percent of the respondents strongly agreed to the statement, 36.2 percent

agreed, 3.4 percent are neutral while 1.7 percent disagreed and 1.7 percent strongly disagreed. Evaluation

must be done by auditors in order to make a preliminary evaluation of the effectiveness of its components

controls and to determine the extent of his reliance on these controls.

Test of Hypotheses

Hypothesis One

Organizations that do not use internal audit function cannot detect and report fraud and other financial

irregularities.

Table 4.2.11: Chi-Square Table on Internal Audit Function in First Bank of Nigeria Plc

Respondent’s

View

0i Ei 0i-Ei (0i-Ei)2 (0i-Ei)2

Ei

Strongly agree 33 11.6 21.4 458 39.48

Agree 20 11.6 8.4 70.6 6.09

Neutral 1 11.6 -10.6 112.4 9.69

Disagree 3 11.6 -8.6 74 6.38

Strongly Disagree 1 11.6 -10.6 112.4 9.69

Total 58 58 0 827.4 71.33 Therefore, Z2 (Chi Square) value calculated is 71.33

The degree of freedom (K-1), 5-1 =4

Using the statistical table to find the value of Z24; 0.05, the result is = 9.488

Therefore, X2 calculated = 71.33

X2 tabulated = 9.488

International Journal of Empirical Finance

161

Decision rule: X2 calculated is greater than X2 tabulated, (71.33 > 9.488) at 5% confidence level and 4

degree of freedom the null hypotheses is rejected and the alternative hypothesis which states that “ First

Bank use Internal Audit Function to detect and report Fraud and other Financial Irregularities” is accepted.

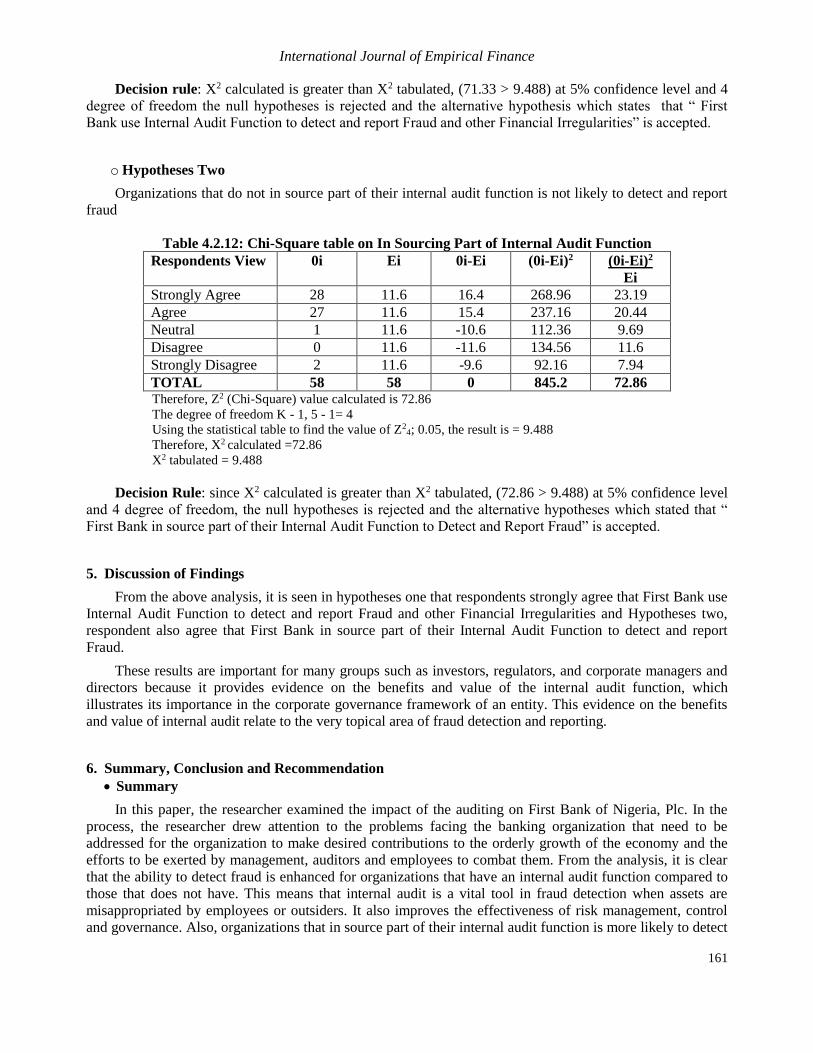

o Hypotheses Two

Organizations that do not in source part of their internal audit function is not likely to detect and report

fraud

Table 4.2.12: Chi-Square table on In Sourcing Part of Internal Audit Function

Respondents View 0i Ei 0i-Ei (0i-Ei)2 (0i-Ei)2

Ei

Strongly Agree 28 11.6 16.4 268.96 23.19

Agree 27 11.6 15.4 237.16 20.44

Neutral 1 11.6 -10.6 112.36 9.69

Disagree 0 11.6 -11.6 134.56 11.6

Strongly Disagree 2 11.6 -9.6 92.16 7.94

TOTAL 58 58 0 845.2 72.86 Therefore, Z2 (Chi-Square) value calculated is 72.86

The degree of freedom K - 1, 5 - 1= 4

Using the statistical table to find the value of Z24; 0.05, the result is = 9.488

Therefore, X2 calculated =72.86

X2 tabulated = 9.488

Decision Rule: since X2 calculated is greater than X2 tabulated, (72.86 > 9.488) at 5% confidence level

and 4 degree of freedom, the null hypotheses is rejected and the alternative hypotheses which stated that “

First Bank in source part of their Internal Audit Function to Detect and Report Fraud” is accepted.

5. Discussion of Findings

From the above analysis, it is seen in hypotheses one that respondents strongly agree that First Bank use

Internal Audit Function to detect and report Fraud and other Financial Irregularities and Hypotheses two,

respondent also agree that First Bank in source part of their Internal Audit Function to detect and report

Fraud.

These results are important for many groups such as investors, regulators, and corporate managers and

directors because it provides evidence on the benefits and value of the internal audit function, which

illustrates its importance in the corporate governance framework of an entity. This evidence on the benefits

and value of internal audit relate to the very topical area of fraud detection and reporting.

6. Summary, Conclusion and Recommendation

Summary

In this paper, the researcher examined the impact of the auditing on First Bank of Nigeria, Plc. In the

process, the researcher drew attention to the problems facing the banking organization that need to be

addressed for the organization to make desired contributions to the orderly growth of the economy and the

efforts to be exerted by management, auditors and employees to combat them. From the analysis, it is clear

that the ability to detect fraud is enhanced for organizations that have an internal audit function compared to

those that does not have. This means that internal audit is a vital tool in fraud detection when assets are

misappropriated by employees or outsiders. It also improves the effectiveness of risk management, control

and governance. Also, organizations that in source part of their internal audit function is more likely to detect

L. B. Akeem

162

and report fraud because more time is spent on in sourcing internal audit which will bring a high level of

entity specific knowledge to the internal audit function compared to outsourcing.

Conclusion

Bank can only reduce the occurrence of fraud by ensuring conclusive, satisfactory and comfortable

working conditions of staff and also, the importance of the auditors’ role in the detection of fraud is

continuously growing. Armed with combination of skills, these financial detectives are today important

assets to modern legal teams. In the backdrop of increasing levels of frauds, the demand for auditors is bound

to substantially increase in the future.

Recommendations

In order to reduce the growing trends of fraud and other financial irregularities, the following strategies

are recommended for further follow up:

1. Banks are to increase their requirements pertaining to qualifications and draw up more efficient

screening techniques.

2. They are to ensure that there is segregation of duties, efficient internal controls, jobs satisfactions and

job enrichment.

3. Awareness should also be created so as to ‘nip’ the situation in the ‘bud’ before anything serious

occurs. This requires more than just sound judgment and dynamic action; it calls for commitment that

can only be gained if the management has ensured that all the motivational incentives have been put

in place. A total alertness that takes nothing for granted and awareness that trust could be misplaced,

this being a diligent and painstaking approach.

4. Furthermore, training techniques should be upgraded to test honesty and integrity and not just

technical skills. This should entail extensive training programme regularly done, as well as

personality tests and Intelligent Quotient (IQ) tests so as to understand the personality and character

of the trainee. This would reduce negligence and carelessness in carrying out basic procedures that

could pose as loopholes for fraud.

References

Accounting Standards Board. 1988. “The Auditors Responsibility to Detect and Report Errors and

Irregularities.”

Adeduro, A.A. (1998): “An Investigation into Frauds in Banks”. An unpublished thesis of University of

Lagos

Adeniji, A. (2004): Auditing and Investigation. Lagos, Value Analysis Publishers

Aderibigbe, P. and Dada, S. O. (2007): Micro Auditing Principles. Lagos ICAN Journal, Vol 11 No 1,

Jan/March.

Akintoye, Ishola Rufus (2010) Quick Insight into Research Methodology, Unique press

Ali, M., & Raza, S. A. (2015). Measurement of Service Quality Perception and Customer Satisfaction in

Islamic Banks of Pakistan: Evidence from Modified SERVQUAL Model. MPRA Paper No. 64039,

University Library of Munich, Germany.

Alleyne, P. & Howard, M. (2005): An Exploratory Study of Auditors’ Responsibility for Fraud Detection in

Barbados.Managerial Auditing Journal. 20(3):284-303.

American Institute of Certified Public Accountants SAS 82

Arter, D. (2002) Quality Audits for Improved Performance. ASQ Quality Press; 3 edition Association of

Certified Fraud Examiners. 1999. “Report on the Nation Occupational Fraud and Abuse.”

International Journal of Empirical Finance

163

Bostley R.W.B. and Dover C.B. (1972): Sheldon’s Practice and Law of Banking, 10th edition, London,

Macdonald and Evans.

Brink, V.Z. & Witt, H. (1982), Internal Auditing. New York, John Wiley & Sons:

Boynton, W., Johnson, R. & Kell, W. (2005).Assurance and the Integrity of Financial Reporting.

8thedition. New York: John Wiley & Son, Inc.

Busari, Adekunle Alade (2005) Research Methodology, Zenith press and consult pg 60-74

Cameron, E.D. (1982) Report of the Independent Auditor on an Efficiency Audit of the Auditor General's

Office under the Audit Act 1901, 5 March, AGPS, Canberra.

Dixon, R. & Woodhead, A. (2006).An Investigation of the Expectation Gap in Egypt. Managerial

Auditing Journal. 21(3):293-302.

Epstein, M & Geiger, M. (1994). Investor Views of Audit Assurance: Recent Evidence of the Expectation

Gap. Journal of Accountancy. 177(1):60-66.

Fazdly, M. & Ahmad, Z. (2004). Audit Expectation Gap. Managerial Auditing Journal. 19:897-915.

First Bank of Nigeria Plc, (2013). Historical Background of First bank Plc.

Fullerton, R. and Durtschi, C. (2004), "The Effect of Professional Skepticism on the Fraud Detection Skills

of Internal Auditors"

Gay, G., Schelluch, P. & Reid, I. (1997): Users’ Perceptions of the Auditing Responsibilities for the

Prevention, Detection and Reporting of Fraud, other illegal acts and error.Accounting Review

Australian7(1):51-61.

Hagan, Frank E. 1997. Introduction To Criminology: Theories, Methods and Criminal Behavior,4th

edition.

Harvey, F. (1990) ‘Detecting and Investigating Fraud in the Public Sector’, AIC Public sector Auditing

Conference, September, Sydney.

Humphrey, C., Moizer, P. & Turley, W. (1993): The Audit Expectation Gap in Britain: an Empirical

Investigation. Accounting and Business Research. 23:395-411.

ICAN (2006): Financial Reporting and Audit Practice. Lagos, VI Publishing Ltd

Idris, J. (2009): Nigerian Auditors are Toothless Bulldogs. October 3

http://www.saharareporters.com/articles/external-contrib/3872

Jones R. &Pendlebury M. (2000) Public Sector Accounting, Financial Times/Division of Pearson Education.

ISBN: 0-273-64626-5. pp.288. 5th Edition.

Leung, P. &Chau, G. (2001). The Problematic Relationship between Audit Reporting and Audit

Expectations; Some Evidence from Hong Kong. Advance in International Accounting.14:181-206

Low, A.M. (1980). The Auditor’s Detection Responsibility: is there an ‘Expectation Gap’? Journal of

Accounting. Singapore.October: 65-70.

MacErlean, Neasa. (1993). Fraud Prevention and the Accountant.Accountancy 112: 42-44.

Moizer.and Turley, 1993 (Eds), Current Issues in Auditing, 3rd ed. Paul Chapman Publishing. London,

Ch. 2:31-54.

Monaghan, C.T. (1989) ‘Comprehensive Auditing for Efficiency’ in Selected Addresses on Public

Sector Auditing, No. 5, AAO, Canberra.

Monroe, G. & Wood liff, D. (1994): An empirical investigation of the audit expectation gap: Australian

Evidence. Australian Accounting Review. November, 42-53.

OremadeTunde (1988): Auditing and Investigation. Lagos, West African Book Publishers

L. B. Akeem

164

Pollick.M.Y. (2006).What is Fraud: http://www.wisegeek.com/what-is-fraud.htm Accessed: 15 February

2010.

Porter, B. (1997): Auditors’ Responsibilities with respect to Corporate Fraud: A Controversial issue, in

Sherer, M. and Turley, S. (Eds), 3rd ed., Current Issues in Auditing, Paul Chapman Publishing.

London, Ch. 2:31-54.

Power T. Walsh S. & O’Meara P. (2001) Financial Management: an Irish text, Gill and McMillan, Dublin.

Raza, S. A., & Hanif, N. (2013). Factors affecting internet banking adoption among internal and external

customers: a case of Pakistan. International Journal of Electronic Finance, 7(1), 82-96.

Russell, (1995).Understanding Fraud and Embezzlement.Ohio CPA Journal 54/1:37-39.

Zikmund P. (2008)."4 steps to a successful fraud risk assessment: internal auditing is in an excellent position

to identify fraud schemes and scenarios and evaluate the controls in a place to prevent them”.