Embed Size (px)

Citation preview

The Impact of Audit Quality on Firm

Performance: Evidence from Malaysia

Hamed Sayyar

International Business School

Universiti Teknologi Malaysia

June 2015

Research model at a glance

Audit Fee

Audit Firm

Rotation

Firm

Performance

Background

• FP-> Stakeholders (Harrison and Wicks, 2013)

• FP-> Crisis and Scandals (Yap et al., 2014)

Crisis,

Scandals

Stakeholders,

Investors,

Users

Firm

Performance

Background

Audit

Quality

Crisis,

ScandalsInvestors,

Users

Firm

Performance

Audit Quality

� Audit Fees

� Audit Firm Rotation

Hypothesis Development

H1: There is a significant relationship between audit fees

and firm performance.

H2: There is a significant relationship between audit firm

rotation and firm performance.

Framework

Audit Fee

Audit Firm

Rotation

Firm Performance:

ROA

TQ

Methodology

Initial population (companies) 980

Financial industries (40)

uncompleted data (398)

Total sample 542

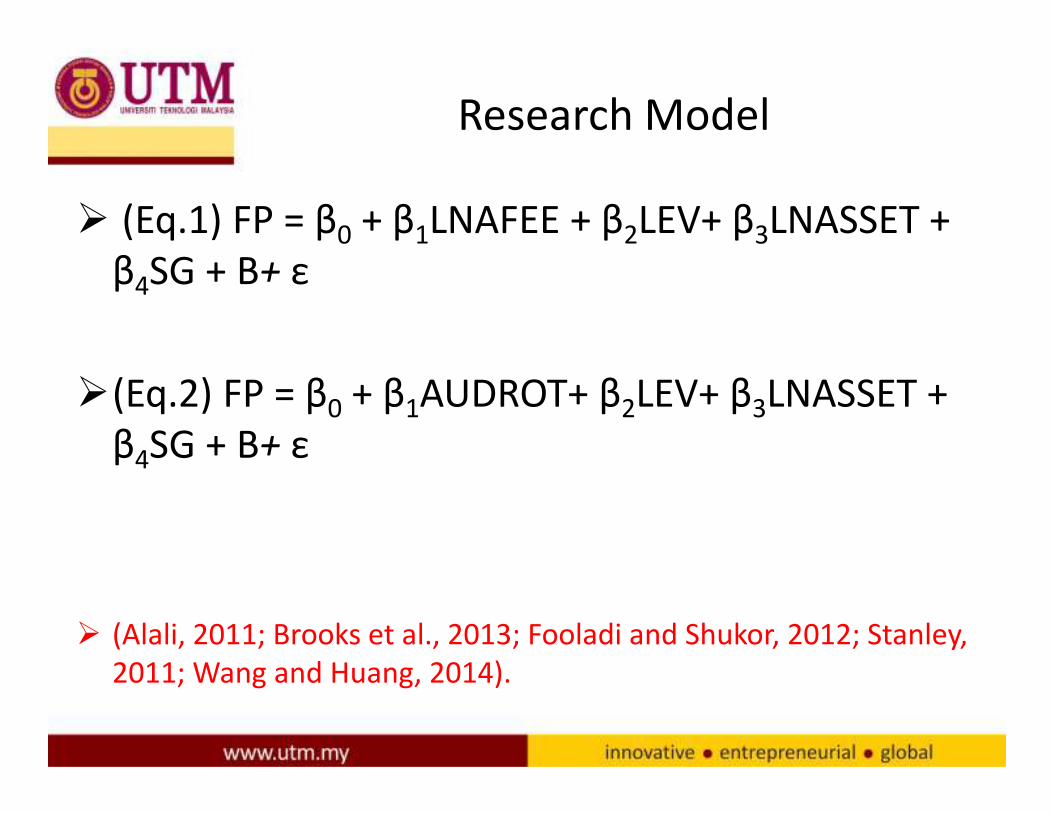

Research Model

� (Eq.1) FP = β0 + β1LNAFEE + β2LEV+ β3LNASSET +

β4SG + B+ ε

�(Eq.2) FP = β0 + β1AUDROT+ β2LEV+ β3LNASSET +

β4SG + B+ ε

� (Alali, 2011; Brooks et al., 2013; Fooladi and Shukor, 2012; Stanley,

2011; Wang and Huang, 2014).

Results

variable mean median min max Skewness kurtosis

AFEE (RM) 43949.610 26000 500 1900000 10.731 176.195

LNAFEE 10.240 10.166 6.215 14.457 0.362 4.502

AUDROT 0.063 0.000 0.000 1.000 3.594 13.915

ROA 0.024 0.031 -1.758 1.272 -4.507 61.579

TQ 0.636 0.426 0.005 8.589 4.588 32.531

LEV 0.393 0.385 0.004 0.975 0.237 2.405

LNASSET 12.741 12.591 0.046 18.452 0.044 7.581

SG 0.106 0.070 -0.991 1.976 1.318 7.583

B 1.012 0.985 -2.585 3.987 0.371 4.401

DE 0.946 0.627 0.004 8.959 3.033 15.676

Descriptive statistics

Results

Variable LNAFEE AUDROT ROA TQ LEV LNASSET SG B

LNAFEE 1

AUDROT -0.035** 1

ROA 0.091*** -0.059*** 1

TQ 0.005 -0.007 0.276*** 1

LEV 0.17*** 0.0127 -0.097*** -0.212*** 1

LNASSET 0.578*** -0.082*** 0.218*** -0.021 0.239*** 1

SG -0.005 -0.007 0.161*** 0.059*** 0.057*** 0.072*** 1

B 0.090*** -0.003 -0.089*** -0.113*** 0.095*** 0.144*** 0.006 1

correlation matrix

Results

Variable

ROA TQ

Coefficient

(t-statistics)

Coefficient

(t-statistics)

Intercept-0.170 0.583

(-8.78)*** (4.78)***

LNAFEE-0.005 0.037

(-2.1)*** (2.57)***

LEV-0.094 -0.810

(-11.75)*** (-16.03)***

LNASSET0.023 0.009

(17.32)*** (1.01)

SG0.052 0.150

(11.68)*** (5.33)***

B-0.024 -0.131

(-8.61)*** (-7.41)***

N 5420 5420

Prob > F 0.000 0.000

R-squared 0.107 0.062

Adj R-squared 0.106 0.061

Multivariate regression for audit fee and ROA model

Results

Variable

ROA TQ

Coefficient

(t-statistics)

Coefficient

(t-statistics)

Intercept-0.194 0.802

(-13.9)*** (9.11)***

AUDROT-0.018 -0.002

(-2.71)*** (-0.05)

LEV-0.094 -0.804

(-11.75)*** (-15.91)***

LNASSET0.022 0.021

(19.19)*** (2.94)***

SG0.053 0.146

(11.82)*** (5.19)***

B-0.024 -0.131

(-8.61)*** (-7.39)***

N 5420 5420

Prob > F 0.000 0.000

R-squared 0.108 0.060

Adj R-squared 0.107 0.059

Multivariate regression for audit firm rotation and ROA model

Results

AFEE AUDROT

Variable VIF 1/VIF Variable VIF 1/VIF

LNASSET 1.58 0.634 LNASSET 1.09 0.917

LNAFEE 1.51 0.662 LEV 1.07 0.936

LEV 1.07 0.936 B 1.03 0.975

B 1.03 0.975 AUDROT 1.01 0.992

SG 1.01 0.99 SG 1.01 0.993

Mean VIF 1.24 Mean VIF 1.04

Multicollinearity test for firm performance model

Results

Breusch-Pagan or Cook-Weisberg test

Ho: Constant variance

Reject H0 if p-value is significant

ROA TQ

LNAFEE

chi2(1) 2247.65 27.74

Prob > chi2 0.000 0.000

AUDROT

chi2(1) 2258.93 19.22

Prob > chi3 0.000 0.000

Heteroskedasticity test

Results

Wooldridge test

Ho: no first-order autocorrelation

Reject H0 if p-value is significant

ROA TQ

LNAFEEF( 1, 541) 17.897 31.873

Prob > F 0.000 0.000

AUDROTF( 1, 541) 17.676 32.318

Prob > F 0.000 0.000

Serial correlation

Results

Variable LAGROA LAGTQ Variable LAGROA LAGTQ

Intercept-0.113 0.287

Intercept-0.106 0.618***

(-5.69)*** (2.34)** (-7.36)*** -6.96

LNAFEE0.001 0.0572

AUDROT0.002 0.038

-0.57 (3.97)*** -0.27 -0.91

LEV-0.0683 -0.679

LEV-0.0682 -0.672***

(-8.27)*** (-13.36)*** (-8.26)*** (-13.21)

LNASSET0.0132 0.015

LNASSET0.0137 0.0344***

(9.48)*** (1.71)* (11.81)*** -4.8

SG0.0401 0.048

SG0.04 0.041

(8.7)*** (1.69)* (8.68)*** -1.46

B-0.0216 -0.161

B-0.0216 -0.161***

(-7.48)*** (-9.04)*** (-7.48)*** (-9.01)

Adj R2 0.0515 0.0497 Adj R2 0.0514 0.0471

*** are significant at p<0.01, ** are significant at p<0.05 and * are significant at p<0.10.

Endogeneity

Results

ROA TQ

Variable

OLS Robust GLS OLS Robust GLS

Coefficient

(t-statistics)

Coefficient

(t-statistics)

Coefficient

(z-statistics)

Coefficient

(t-statistics)

Coefficient

(t-statistics)

Coefficient

(z-statistics)

Intercept-0.170 -0.170 -0.170 0.583 0.583 0.583

(-8.78)*** (-7.720)*** (-8.78)*** (4.780)*** (4.210)*** (4.780)***

LNAFEE-0.005 -0.005 -0.005 0.037 0.037 0.037

(-2.100)** (-2.050)** (-2.10)** (2.570)*** (2.430)** (2.5700)**

LEV-0.094 -0.094 -0.094 -0.810 -0.810 -0.810

(-11.75)*** (-8.610)*** (-11.75)*** (-16.03)*** (-13.6)*** (-16.01)***

LNASSET0.023 0.023 0.023 0.009 0.009 0.009

(17.32)*** (9.260)*** (17.33)*** (1.010) (0.700) (1.010)

SG0.052 0.052 0.052 0.150 0.150 0.150

(11.68)*** (7.080)*** (11.69)*** (5.330)*** (5.070)*** (5.330)***

B-0.024 -0.024 -0.024 -0.131 -0.131 -0.131

(-8.61)*** (-6.370)*** (-8.62)*** (-7.410)*** (-5.71)*** (-7.41)***

Adj R2 0.106 0.11 - 0.061 0.062 -

*** are significant at p<0.01, ** are significant at p<0.05 and * are significant at p<0.10.

Additional regression estimators for Audit fees and firm performance model

Results

ROA TQ

Variable

OLS Robust GLS OLS Robust GLS

Coefficient

(t-statistics)

Coefficient

(t-statistics)

Coefficient

(z-statistics)

Coefficient

(t-statistics)

Coefficient

(t-statistics)

Coefficient

(z-statistics)

Intercept-0.194 -0.194 -0.194 0.802 0.802 0.802

(-13.90)*** (-7.71)*** (-13.91)*** (9.110)*** (6.750)*** (9.110)***

AUDROT-0.018 -0.018 -0.018 -0.002 -0.002 -0.002

(-2.710)*** (-1.72)* (-2.710)*** (-0.050) (-0.060) (-0.050)

LEV-0.094 -0.094 -0.094 -0.804 -0.804 -0.804

(-11.75)*** (-8.55)*** (-11.76)*** (-15.91)*** (-13.34)*** (-15.92)***

LNASSET0.022 0.022 0.022 0.021 0.021 0.021

(19.190)*** (10.47)*** (19.20)*** (2.940)*** (2.020)** (2.940)***

SG0.053 0.053 0.053 0.146 0.146 0.146

(11.820)*** (7.170)*** (11.830)*** (5.190)*** (4.950)*** (5.190)***

B-0.024 -0.024 -0.024 -0.131 -0.131 -0.131

(-8.610)*** (-6.35)*** (-8.620)*** (-7.390)*** (-5.690)*** (-7.390)***

N 5420 5420 5420 5420 5420 5420

Adj R2 0.107 0.11 - 0.059 0.060 -

*** are significant at p<0.01, ** are significant at p<0.05 and * are significant at p<0.10.

Additional regression estimators for audit firm rotation and firm performance

Implications�In a relation to audit quality the findings of

this study provide a guideline for companies

in terms of the extent to which the rotation

of audit firm can affect firm performance.

The result of this research also can be useful

for regulators to consider to issuing

mandatory audit firm rotation to enhance

auditors independence

Conclusion

Recommendation

�This research recommended for future

studies investigate other proxies of audit

quality and examine that how firm

performance can be influences by other

proxies of audit quality such as industry

specialist auditors and type of audit firm.

Conclusion

The EndThe EndThe EndThe End